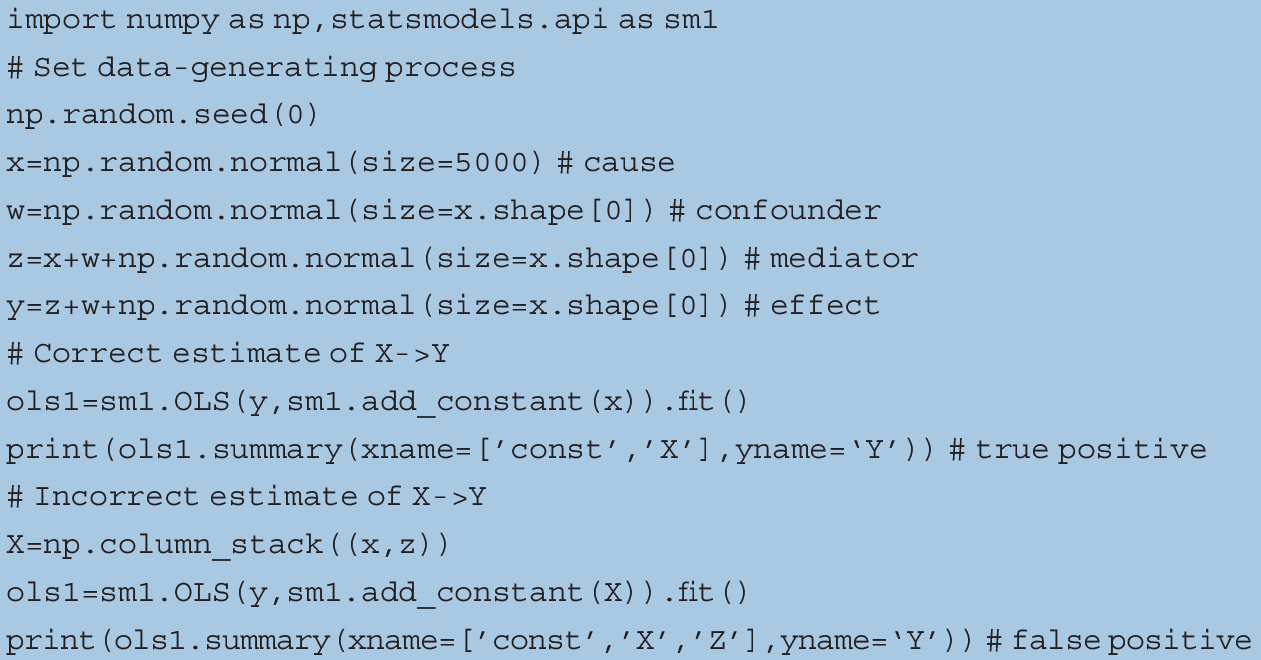

1 Introduction

Science is more than a collection of observed associations. While the description and cataloging of phenomena play a role in scientific discovery, the ultimate goal of science is the amalgamation of theories that have survived rigorous falsification (Reference Hassani, Huang and GhodsiHassani et al. 2018). For a theory to be scientific, it is generally expected to declare the falsifiable causal mechanism responsible for the observed phenomenon (for one definition of falsifiability, see Reference PopperPopper 1963).Footnote 1 Put simply, a scientific theory explains why an observed phenomenon takes place, where that explanation is consistent with all the empirical evidence (ideally, including experimental results). Economists subscribe to this view that a genuine science must produce refutable implications, and that those implications must be tested through solid statistical techniques (Reference LazearLazear 2000).

In the experimental sciences (physics, chemistry, biology, etc.), it is relatively straightforward to propose and falsify causal mechanisms through interventional studies (Reference FisherFisher 1971). This is not generally the case in financial economics. Researchers cannot reproduce the financial conditions of the Flash Crash of May 6, 2010, remove some traders, and observe whether stock market prices still collapse. This has placed the field of financial economics at a disadvantage when compared with experimental sciences. A direct consequence of this limitation is that, for the past fifty years, most factor investing researchers have focused on publishing associational claims, without theorizing and subjecting to falsification the causal mechanisms responsible for the observed associations. In the absence of plausible falsifiable theories, researchers must acknowledge that they do not understand why the reported anomalies (risk premia) occur, and investors are entitled to dismiss their claims as spurious. The implication is that the factor investing literature remains in an immature, phenomenological stage.

From the above, one may reach the bleak conclusion that there is no hope for factor investing (or financial economics) to produce and build upon scientific theories. This is not necessarily the case. Financial economics is not the only field of study afflicted by barriers to experimentation (e.g., astronomers produce scientific theories despite the unfeasibility of interventional studies). Recent progress in causal inference has opened a path, however difficult, for advancing factor investing beyond its current phenomenological stage. The goal of this Element is to help factor investing wake up from its associational slumber, and plant the seeds for the new field of “causal factor investing.”

In order to achieve this goal, I must first recite the fundamental differences between association and causation (Section 2), and why the study of association alone does not lead to scientific knowledge (Section 3). In fields of research with barriers to experimentation, like investing, it has become possible to estimate causal effects from observational studies, through natural experiments and simulated interventions (Section 4). After laying out this foundation, I turn the reader’s attention to the current state of causal confusion in econometrics (Section 5) and factor investing studies (Section 6). This state of confusion easily explains why factor investing remains in a phenomenological stage, and the proliferation of hundreds of spurious claims that Reference CochraneCochrane (2011) vividly described as the “factor zoo”Footnote 2 (Section 7). The good news is, once financial economists embrace the concepts described in this Element, I foresee the transformation of factor investing into a truly scientific discipline (Section 8).

This Element makes several contributions. First, I describe the logical inconsistency that afflicts the factor investing literature, whereby authors make associational claims in denial or ignorance of the causal content of their models. Second, I define the two different types of spurious claims in factor investing, type-A and type-B. These two types of spurious claims have different origins and consequences, hence it is important for factor researchers to distinguish between the two. In particular, type-B factor spuriosity is an important topic that has not been discussed in depth until now. Type-B spuriosity explains, among other literature findings, the time-varying nature of risk premia. Third, I apply this taxonomy to derive a hierarchy of empirical evidence used in financial research, based on the evidence’s susceptibility to being spurious. Fourth, I design Monte Carlo experiments that illustrate the dire consequences of type-B spurious claims in factor investing. Fifth, I propose an alternative explanation for the main findings of the factor investing literature, which is consistent with type-B spuriosity. In particular, the time-varying nature of risk premia reported in canonical journal articles is a likely consequence of under-controlling. Sixth, I propose specific actions that academic authors can take to rebuild factor investing on the more solid scientific foundations of causal inference.

2 Association vs Causation

Every student of statistics, and by extension econometrics, learns that association does not imply causation. This statement, while superficially true, does not explain why association exists, and its relation to causation. Two discrete random variables X and Y are statistically independent if and only if

, where

, where

is the probability of the event described inside the squared brackets. Conversely, two discrete random variables

is the probability of the event described inside the squared brackets. Conversely, two discrete random variables

and

and

are said to be statistically associated (or codependent) when, for some

are said to be statistically associated (or codependent) when, for some

, they satisfy that

, they satisfy that

. The conditional probability expression

. The conditional probability expression

represents the probability that

represents the probability that

among the subset of the population where

among the subset of the population where

. When two variables are associated, observing the value of one conveys information about the value of the other:

. When two variables are associated, observing the value of one conveys information about the value of the other:

, or equivalently,

, or equivalently,

. For example, monthly drownings (

. For example, monthly drownings (

) and ice cream sales (

) and ice cream sales (

) are strongly associated, because the probability that

) are strongly associated, because the probability that

people drown in a month conditional on observing

people drown in a month conditional on observing

ice cream sales in that same month does not equal the unconditional probability of

ice cream sales in that same month does not equal the unconditional probability of

drownings in a month for some

drownings in a month for some

. However, the expression

. However, the expression

does not tell us whether ice cream sales cause drownings. Answering that question requires the introduction of a more nuanced concept than conditional probability: an intervention.

does not tell us whether ice cream sales cause drownings. Answering that question requires the introduction of a more nuanced concept than conditional probability: an intervention.

A data-generating process is a physical process responsible for generating the observed data, where the process is characterized by a system of structural equations. Within that system, a variable

is said to cause a variable

is said to cause a variable

when

when

is a function of

is a function of

. The structural equation by which

. The structural equation by which

causes

causes

is called a causal mechanism. Unfortunately, the data-generating process responsible for observations is rarely known. Instead, researchers must rely on probabilities, estimated on a sample of observations, to deduce the causal structure of a system. Probabilistically, a variable

is called a causal mechanism. Unfortunately, the data-generating process responsible for observations is rarely known. Instead, researchers must rely on probabilities, estimated on a sample of observations, to deduce the causal structure of a system. Probabilistically, a variable

is said to cause a variable

is said to cause a variable

when setting the value of

when setting the value of

to

to

increases the likelihood that

increases the likelihood that

will take the value

will take the value

. Econometrics lacks the language to represent interventions, that is, setting the value of

. Econometrics lacks the language to represent interventions, that is, setting the value of

(Reference Chen and PearlChen and Pearl 2013). To avoid confusion between conditioning by

(Reference Chen and PearlChen and Pearl 2013). To avoid confusion between conditioning by

and setting the value of

and setting the value of

, Reference PearlPearl (1995) introduced the do-operator,

, Reference PearlPearl (1995) introduced the do-operator,

, which denotes the intervention that sets the value of

, which denotes the intervention that sets the value of

to

to

. With this new notation, causation can be formally defined as follows:

. With this new notation, causation can be formally defined as follows:

causes

causes

if and only if

if and only if

.Footnote 3 For example, setting ice cream sales to

.Footnote 3 For example, setting ice cream sales to

will not make

will not make

drownings more likely than its unconditional probability for any pair

drownings more likely than its unconditional probability for any pair

, hence ice cream sales are not a cause of drownings. In contrast, smoking tobacco is a cause of lung cancer, because the probability that

, hence ice cream sales are not a cause of drownings. In contrast, smoking tobacco is a cause of lung cancer, because the probability that

individuals develop lung cancer among a collective where the level of tobacco smoking is set to

individuals develop lung cancer among a collective where the level of tobacco smoking is set to

(through an intervention) is greater than the unconditional probability of

(through an intervention) is greater than the unconditional probability of

individuals developing lung cancer, for some pair

individuals developing lung cancer, for some pair

.Footnote 4

.Footnote 4

Variables

and

and

may be part of a more complex system, involving additional variables. The causal structure of a system can be represented through a directed acyclic graph, also denoted a causal graph.Footnote 5 While a causal graph does not fully characterize the data-generating process, it conveys topological information essential to estimate causal effects. Causal graphs declare the variables involved in a system, which variables influence each other, and the direction of causality (Reference PearlPearl 2009, p. 12). Causal graphs help visualize do-operations as the action of removing all arrows pointing toward

may be part of a more complex system, involving additional variables. The causal structure of a system can be represented through a directed acyclic graph, also denoted a causal graph.Footnote 5 While a causal graph does not fully characterize the data-generating process, it conveys topological information essential to estimate causal effects. Causal graphs declare the variables involved in a system, which variables influence each other, and the direction of causality (Reference PearlPearl 2009, p. 12). Causal graphs help visualize do-operations as the action of removing all arrows pointing toward

in the causal graph, so that the full effect on

in the causal graph, so that the full effect on

can be attributed to setting

can be attributed to setting

. This is the meaning of the ceteris paribus assumption, which is of critical importance to economists.

. This is the meaning of the ceteris paribus assumption, which is of critical importance to economists.

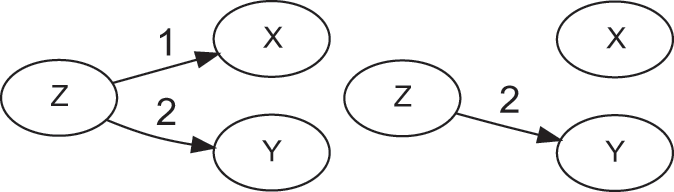

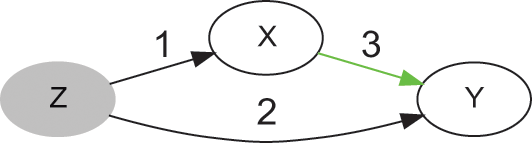

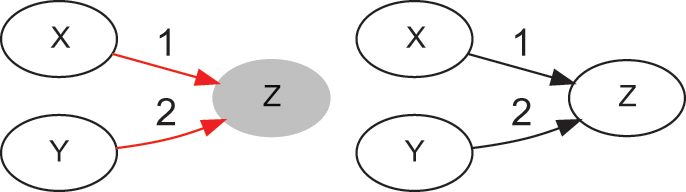

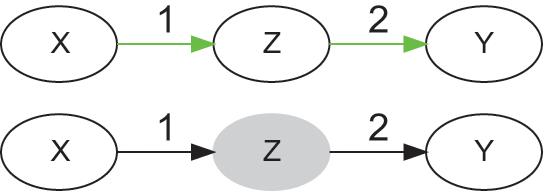

The causal graph in Figure 1 tells us that

causes

causes

, and

, and

causes

causes

. In the language of causal inference,

. In the language of causal inference,

is a confounder, because this variable introduces an association between

is a confounder, because this variable introduces an association between

and

and

, even though there is no arrow between

, even though there is no arrow between

and

and

. For this reason, this type of association is denoted noncausal. Following with the previous example, weather (

. For this reason, this type of association is denoted noncausal. Following with the previous example, weather (

) influences ice cream sales (

) influences ice cream sales (

) and the number of swimmers, hence drownings (

) and the number of swimmers, hence drownings (

). The intervention that sets ice cream sales removes arrow (1), because it gives full control of

). The intervention that sets ice cream sales removes arrow (1), because it gives full control of

to the researcher (

to the researcher (

is no longer a function of

is no longer a function of

), while keeping all other things equal (literally, ceteris paribus). And because

), while keeping all other things equal (literally, ceteris paribus). And because

does not cause

does not cause

, setting

, setting

(e.g., banning the sale of ice cream,

(e.g., banning the sale of ice cream,

) has no effect on the probability of

) has no effect on the probability of

. As shown later, noncausal association can occur for a variety of additional reasons that do not involve confounders.

. As shown later, noncausal association can occur for a variety of additional reasons that do not involve confounders.

Causal graph of a confounder (

), before (left) and after (right) a do-operation

), before (left) and after (right) a do-operation

Five conclusions can be derived from this exposition. First, causality is an extra-statistical (in the sense of beyond observational) concept, connected to mechanisms and interventions, and distinct from the concept of association. As a consequence, researchers cannot describe causal systems with the associational language of conditional probabilities. Failure to use the do-operator has led to confusion between associational and causal statements, in econometrics and elsewhere. Second, association does not imply causation, however causation does imply association because setting

through an intervention is associated with the outcome

through an intervention is associated with the outcome

.Footnote 6 Third, unlike association, causality is directional, as represented by the arrows of the causal graph. The statement “

.Footnote 6 Third, unlike association, causality is directional, as represented by the arrows of the causal graph. The statement “

causes

causes

” implies that

” implies that

, but not that

, but not that

. Fourth, unlike association, causality is sequential. “

. Fourth, unlike association, causality is sequential. “

causes

causes

” implies that the value of

” implies that the value of

is set first, and only after that

is set first, and only after that

adapts. Fifth, the ceteris paribus assumption simulates an intervention (do-operation), whose implications can only be understood with knowledge of the causal graph. The causal graph shows what “other things” are kept equal by the intervention.

adapts. Fifth, the ceteris paribus assumption simulates an intervention (do-operation), whose implications can only be understood with knowledge of the causal graph. The causal graph shows what “other things” are kept equal by the intervention.

3 The Three Steps of Scientific Discovery

Knowing the causes of effects has long been a human aspiration. In 29 BC, ancient Roman poet Virgil wrote “happy the man, who, studying Nature’s laws, / thro’ known effects can trace the secret cause” (Reference DrydenDryden 1697, p. 71). It was not until around the year 1011 that Arab mathematician Hasan Ibn al-Haytham proposed a scientific method for deducing the causes of effects (Reference ThieleThiele 2005; Reference SabraSabra 1989).

Science has been defined as the systematic organization of knowledge in the form of testable explanations of natural observations (Reference HeilbronHeilbron 2003). Mature scientific knowledge aims at identifying causal relations, and the mechanisms behind them, because causal relations are responsible for the regularities in observed data (Reference Glymour, Zhang and SpirtesGlymour et al. 2019).

The process of creating scientific knowledge can be organized around three critical steps: (1) the phenomenological step, where researchers observe a recurrent pattern of associated events, or an exception to such a pattern; (2) the theoretical step, where researchers propose a testable causal mechanism responsible for the observed pattern; and (3) the falsification step, where the research community designs experiments aimed at falsifying each component of the theorized causal mechanism.

3.1 The Phenomenological Step

In the phenomenological step, researchers observe associated events, without exploring the reason for that association. At this step, it suffices to discover that

. Further, a researcher may model the joint distribution

. Further, a researcher may model the joint distribution

, derive conditional probabilities

, derive conditional probabilities

, and make associational statements of the type

, and make associational statements of the type

(an associational prediction) with the help of machine learning tools. Exceptionally, a researcher may go as far as to produce empirical evidence of a causal effect, such as the result from an interventional study (e.g., Ohm’s law of current, Newton’s law of universal gravitation, or Coulomb’s law of electrical forces), but without providing an explanation for the relationship. The main goal of the phenomenological step is to state “a problem situation,” in the sense of describing the observed anomaly for which no scientific explanation exists (Reference PopperPopper 1994b, pp. 2–3). At this step, inference occurs by logical induction, because the problem situation rests on the conclusion that, for some unknown reason, the phenomenon will reoccur.Footnote 7

(an associational prediction) with the help of machine learning tools. Exceptionally, a researcher may go as far as to produce empirical evidence of a causal effect, such as the result from an interventional study (e.g., Ohm’s law of current, Newton’s law of universal gravitation, or Coulomb’s law of electrical forces), but without providing an explanation for the relationship. The main goal of the phenomenological step is to state “a problem situation,” in the sense of describing the observed anomaly for which no scientific explanation exists (Reference PopperPopper 1994b, pp. 2–3). At this step, inference occurs by logical induction, because the problem situation rests on the conclusion that, for some unknown reason, the phenomenon will reoccur.Footnote 7

For instance, a researcher may observe that the bid-ask spread of stocks widens in the presence of imbalanced orderflow (i.e., when the amount of shares exchanged in trades initiated by buyers does not equal the amount of shares exchanged in trades initiated by sellers over a period of time), and that the widening of bid-ask spreads often precedes a rise in intraday volatility. This is a surprising phenomenon because under the efficient market hypothesis asset prices are expected to reflect all available information at all times, making predictions futile (Reference FamaFama 1970). The existence of orderflow imbalance, the sequential nature of these events, and their predictability point to market inefficiencies, of unclear source. Such associational observations do not constitute a theory, and they do not explain why the phenomenon occurs.

3.2 The Theoretical Step

In the theoretical step, researchers advance a possible explanation for the observed associated events. This is an exercise in logical abduction (sometimes also called retroduction): Given the observed phenomenon, the most likely explanation is inferred by elimination among competing alternatives. Observations cannot be explained by a hypothesis more extraordinary than the observations themselves, and of various hypotheses the least extraordinary must be preferred (Reference Wieten, Bex, Prakken, Renooij, Prakken, Bistarelli, Santini and TaticchiWieten et al. 2020). At this step, a researcher states that

and

and

are associated because

are associated because

causes

causes

, in the sense that

, in the sense that

. For the explanation to be scientific, it must propose a causal mechanism that is falsifiable, that is, propose the system of structural equations along the causal path from

. For the explanation to be scientific, it must propose a causal mechanism that is falsifiable, that is, propose the system of structural equations along the causal path from

to

to

, where the validity of each causal link and causal path can be tested empirically.Footnote 8 Physics Nobel Prize laureate Wolfgang Pauli famously remarked that there are three types of explanations: correct, wrong, and not even wrong (Reference PeierlsPeierls 1992). With “not even wrong,” Pauli referred to explanations that appear to be scientific, but use unfalsifiable premises or reasoning, which can never be affirmed nor denied.

, where the validity of each causal link and causal path can be tested empirically.Footnote 8 Physics Nobel Prize laureate Wolfgang Pauli famously remarked that there are three types of explanations: correct, wrong, and not even wrong (Reference PeierlsPeierls 1992). With “not even wrong,” Pauli referred to explanations that appear to be scientific, but use unfalsifiable premises or reasoning, which can never be affirmed nor denied.

A scientist may propose a theory with the assistance of statistical tools (see Section 4.3.1), however data and statistical tools are not enough to produce a theory. The reason is, in the theoretical step the scientist injects extra-statistical information, in the form of a subjective framework of assumptions that give meaning to the observations. These assumptions are unavoidable, because the simple action of taking and interpreting measurements introduces subjective choices, making the process of discovery a creative endeavor. If theories could be deduced directly from observations, then there would be no need for experiments that test the validity of the assumptions.

Following on the previous example, the Probability of Informed Trading (PIN) theory explains liquidity provision as the result of a sequential strategic game between market makers and informed traders (Reference Easley, Kiefer, O’Hara and PapermanEasley et al. 1996). In the absence of informed traders, the orderflow is balanced, because uninformed traders initiate buys and sells in roughly equal amounts, hence market impact is mute and the mid-price barely changes. When market makers provide liquidity to uninformed traders, they profit from the bid-ask spread (they buy at the bid price and sell at the ask price). However, the presence of informed traders imbalances the orderflow, creating market impact that changes the mid-price. When market makers provide liquidity to an informed trader, the mid-price changes before market makers are able to profit from the bid-ask spread, and they are eventually forced to realize a loss. As a protection against losses, market makers react to orderflow imbalance by charging a greater premium for selling the option to be adversely selected (that premium is the bid-ask spread). In the presence of persistent orderflow imbalance, realized losses accumulate, and market makers are forced to reduce their provision of liquidity, which results in greater volatility. Two features make the PIN theory scientific: First, it describes a precise mechanism that explains the causal link: orderflow imbalance

market impact

market impact

mid-price change

mid-price change

realized losses

realized losses

bid-ask spread widening

bid-ask spread widening

reduced liquidity

reduced liquidity

greater volatility. Second, the mechanism involves measurable variables, with links that are individually testable. An unscientific explanation would not propose a mechanism, or it would propose a mechanism that is not testable.

greater volatility. Second, the mechanism involves measurable variables, with links that are individually testable. An unscientific explanation would not propose a mechanism, or it would propose a mechanism that is not testable.

Mathematicians use the term theory with a different meaning than scientists. A mathematical theory is an area of study derived from a set of axioms, such as number theory or group theory. Following Kant’s epistemological definitions, mathematical theories are synthetic a priori logical statements, whereas scientific theories are synthetic a posteriori logical statements. This means that mathematical theories do not admit empirical evidence to the contrary, whereas scientific theories must open themselves to falsification.

3.3 The Falsification Step

In the falsification step, researchers not involved in the formulation of the theory independently: (i) deduce key implications from the theory, such that it is impossible for the theory to be true and the implications to be false; and (ii) design and execute experiments with the purpose of proving that the implications are false. Step (i) is an exercise in logical deduction because given some theorized premises, a falsifiable conclusion is reached reductively (Reference GenslerGensler 2010, pp. 104–110). When properly done, performing step (i) demands substantial creativity and domain expertise, as it must balance the strength of the deduced implication with its testability (cost, measurement errors, reproducibility, etc.). Each experiment in step (ii) focuses on falsifying one particular link in the chain of events involved in the causal mechanism, applying the tools of mediation analysis. The conclusion that the theory is false follows the structure of a modus tollens syllogism (proof by contradiction): using standard sequent notation, if

, however

, however

is observed, then

is observed, then

, where

, where

stands for “the theory is true” and

stands for “the theory is true” and

stands for a falsifiable key implication of the theory.

stands for a falsifiable key implication of the theory.

One strategy of falsification is to show that

, in which case either the association is noncausal, or there is no association (i.e., the phenomenon originally observed in step (i) was a statistical fluke). A second strategy of falsification is to deduce a causal prediction from the proposed mechanism, and to show that

, in which case either the association is noncausal, or there is no association (i.e., the phenomenon originally observed in step (i) was a statistical fluke). A second strategy of falsification is to deduce a causal prediction from the proposed mechanism, and to show that

. When that is the case, there may be a causal mechanism, however, it does not work as theorized (e.g., when the actual causal graph is more complex than the one proposed). A third strategy of falsification is to deduce from the theorized causal mechanism the existence of associations, and then apply machine learning techniques to show that those associations do not exist. Unlike the first two falsification strategies, the third one does not involve a do-operation.

. When that is the case, there may be a causal mechanism, however, it does not work as theorized (e.g., when the actual causal graph is more complex than the one proposed). A third strategy of falsification is to deduce from the theorized causal mechanism the existence of associations, and then apply machine learning techniques to show that those associations do not exist. Unlike the first two falsification strategies, the third one does not involve a do-operation.

Following on the previous example, a researcher may split a list of stocks randomly into two groups, send buy orders that set the level of orderflow imbalance for the first group, and measure the difference in bid-ask spread, liquidity, and volatility between the two groups (an interventional study, see Section 4.1).Footnote 9 In response to random spikes in orderflow imbalance, a researcher may find evidence of quote cancellation, quote size reduction, and resending quotes further away from the mid-price (a natural experiment, see Section 4.2).Footnote 10 If the experimental evidence is consistent with the proposed PIN theory, the research community concludes that the theory has (temporarily) survived falsification. Furthermore, in some cases a researcher might be able to inspect the data-generating process directly, in what I call a “field study.” A researcher may approach profitable market makers and examine whether their liquidity provision algorithms are designed to widen the bid-ask spread at which they place quotes when they observe imbalanced order flow. The same researcher may approach less profitable market makers and examine whether their liquidity provision algorithms do not react to order flow imbalance. Service providers are willing to offer this level of disclosure to key clients and regulators. This field study may confirm that market makers who do not adjust their bid-ask spread in presence of orderflow imbalance succumb to Darwinian competition, leaving as survivors those whose behavior aligns with the PIN theory.

Popper gave special significance to falsification through “risky forecasts,” that is, forecasts of outcomes

under yet unobserved interventions

under yet unobserved interventions

(Reference Vignero and WenmackersVignero and Wenmackers 2021). Mathematically, this type of falsification is represented by the counterfactual expression

(Reference Vignero and WenmackersVignero and Wenmackers 2021). Mathematically, this type of falsification is represented by the counterfactual expression

, namely the expected value of

, namely the expected value of

in an alternative universe where

in an alternative universe where

is set to

is set to

(a do-operation) for the subset of observations where what actually happened is

(a do-operation) for the subset of observations where what actually happened is

and

and

.Footnote 11 Successful theories answer questions about previously observed events, as well as never-before observed events. To come up with risky forecasts, an experiment designer scrutinizes the theory, deducing its ultimate implications under hypothetical

.Footnote 11 Successful theories answer questions about previously observed events, as well as never-before observed events. To come up with risky forecasts, an experiment designer scrutinizes the theory, deducing its ultimate implications under hypothetical

, and then searches or waits for them. Because the theory was developed during the theoretical step without knowledge of

, and then searches or waits for them. Because the theory was developed during the theoretical step without knowledge of

, this type of analysis constitutes an instance of out-of-sample assessment. For example, the PIN theory implied the possibility of failures in the provision of liquidity approximately fourteen years before the flash crash of 2010 took place. Traders who had implemented liquidity provision models based on the PIN theory (or better, its high-frequency embodiment, VPIN) were prepared for that black-swan and profited from that event (Reference Easley, Prado and O’HaraEasley et al. 2010, Reference Easley, Prado and O’Hara2012, Reference López de PradoLópez de Prado 2018, pp. 281–300), at the expense of traders who relied on weaker microstructural theories.

, this type of analysis constitutes an instance of out-of-sample assessment. For example, the PIN theory implied the possibility of failures in the provision of liquidity approximately fourteen years before the flash crash of 2010 took place. Traders who had implemented liquidity provision models based on the PIN theory (or better, its high-frequency embodiment, VPIN) were prepared for that black-swan and profited from that event (Reference Easley, Prado and O’HaraEasley et al. 2010, Reference Easley, Prado and O’Hara2012, Reference López de PradoLópez de Prado 2018, pp. 281–300), at the expense of traders who relied on weaker microstructural theories.

3.4 Demarcation and Falsificationism in Statistics

Science is essential to human understanding in that it replaces unreliable inductive reasoning (such as “

will follow

will follow

because that is the association observed in the past”) with more reliable deductive reasoning (such as “

because that is the association observed in the past”) with more reliable deductive reasoning (such as “

will follow

will follow

because

because

causes

causes

through a tested mechanism

through a tested mechanism

”). Parsimonious theories are preferable, because they are easier to falsify, as they involve controlling for fewer variables (Occam’s razor). The most parsimonious surviving theory is not truer, however, it is better “fit” (in an evolutionary sense) to tackle more difficult problems posed by that theory. The most parsimonious surviving theory poses new problem situations, hence re-starting a new iteration of the three-step process, which will result in a better theory yet.

”). Parsimonious theories are preferable, because they are easier to falsify, as they involve controlling for fewer variables (Occam’s razor). The most parsimonious surviving theory is not truer, however, it is better “fit” (in an evolutionary sense) to tackle more difficult problems posed by that theory. The most parsimonious surviving theory poses new problem situations, hence re-starting a new iteration of the three-step process, which will result in a better theory yet.

To appreciate the unique characteristics of the scientific method, it helps to contrast it with a dialectical predecessor. For centuries prior to the scientific revolution of the seventeenth century, academics used the Socratic method to eliminate logically inconsistent hypotheses. Like the scientific method, the Socratic method relies on three steps: (1) problem statement; (2) hypothesis formulation; and (3) elenchus (refutation), see Reference VlastosVlastos (1983, pp. 27–58). However, both methods differ in three important aspects. First, a Socratic problem statement is a definiendum (“what is

?”), not an observed empirical phenomenon (“

?”), not an observed empirical phenomenon (“

and

and

are associated”). Second, a Socratic hypothesis is a definiens (“

are associated”). Second, a Socratic hypothesis is a definiens (“

is …”), not a falsifiable theory (“

is …”), not a falsifiable theory (“

causes

causes

through mechanism

through mechanism

”). Third, a Socratic refutation presents a counterexample that exposes implicit assumptions, where those assumptions contradict the original definition. In contrast, scientific falsification does not involve searching for contradictive implicit assumptions, since all assumptions were made explicit and coherent by a plausible causal mechanism. Instead, scientific falsification designs and executes an experiment aimed at debunking the theorized causal effect (“

”). Third, a Socratic refutation presents a counterexample that exposes implicit assumptions, where those assumptions contradict the original definition. In contrast, scientific falsification does not involve searching for contradictive implicit assumptions, since all assumptions were made explicit and coherent by a plausible causal mechanism. Instead, scientific falsification designs and executes an experiment aimed at debunking the theorized causal effect (“

does not cause

does not cause

”), or showing that the experiment’s results contradict the hypothesized mechanism (“experimental results contradict

”), or showing that the experiment’s results contradict the hypothesized mechanism (“experimental results contradict

”).Footnote 12

”).Footnote 12

The above explanation elucidates an important fact that is often ignored or misunderstood: not all academic debate is scientific, even in empirical or mathematical subjects. A claim does not become scientific by virtue of its use of complex mathematics, its reliance on measurements, or its submission to peer review.Footnote 13 Philosophers of science call the challenge of separating scientific claims from pseudoscientific claims the “demarcation problem.” Popper, Kuhn, Lakatos, Musgrave, Thagard, Laudan, Lutz, and many other authors have proposed different demarcation principles. While there is no consensus on what constitutes a definitive demarcation principle across all disciplines, modern philosophers of science generally agree that, for a theory to be scientific, it must be falsifiable in some wide or narrow sense.Footnote 14

The principle of falsification is deeply ingrained in statistics and econometrics (Reference Dickson, Baird, Bandyopadhyay and ForsterDickson and Baird 2011). Frequentist statisticians routinely use Fisher’s p-values and Neyman–Pearson’s framework for falsifying a proposed hypothesis (

), following a hypothetico-deductive argument of the form (using standard sequent notation):

), following a hypothetico-deductive argument of the form (using standard sequent notation):

(1)

(1)

where

denotes the observation made and

denotes the observation made and

denotes the targeted false positive rate (Reference PerezgonzalezPerezgonzalez 2017). The above proposition is analogous to a modus tollens syllogism, with the caveat that

denotes the targeted false positive rate (Reference PerezgonzalezPerezgonzalez 2017). The above proposition is analogous to a modus tollens syllogism, with the caveat that

is not rejected with certainty, as it would be the case in a mathematical proof. For this reason, this proposition is categorized as a stochastic proof by contradiction, where certainty is replaced by a preset confidence level (Reference ImaiImai 2013; Reference Balsubramani and RamdasBalsubramani and Ramdas 2016). Failure to reject

is not rejected with certainty, as it would be the case in a mathematical proof. For this reason, this proposition is categorized as a stochastic proof by contradiction, where certainty is replaced by a preset confidence level (Reference ImaiImai 2013; Reference Balsubramani and RamdasBalsubramani and Ramdas 2016). Failure to reject

does not validate

does not validate

, but rather attests that there is not sufficient empirical evidence to cast significant doubt on the truth of

, but rather attests that there is not sufficient empirical evidence to cast significant doubt on the truth of

(Reference Reeves and BrewerReeves and Brewer 1980).Footnote 15 Accordingly, the logical structure of statistical hypothesis testing enforces a Popperian view of science in quantitative disciplines, whereby a hypothesis can never be accepted, but it can be rejected (i.e., falsified), see Wilkinson (2013). Popper’s influence is also palpable in Bayesian statistics, see Reference Gelman and Rohilla-ShaliziGelman and Rohilla-Shalizi (2013).

(Reference Reeves and BrewerReeves and Brewer 1980).Footnote 15 Accordingly, the logical structure of statistical hypothesis testing enforces a Popperian view of science in quantitative disciplines, whereby a hypothesis can never be accepted, but it can be rejected (i.e., falsified), see Wilkinson (2013). Popper’s influence is also palpable in Bayesian statistics, see Reference Gelman and Rohilla-ShaliziGelman and Rohilla-Shalizi (2013).

Statistical falsification can be applied to different types of claims. For the purpose of this Element, it is helpful to differentiate between the statistical falsification of: (a) associational claims; and (b) causal claims. The statistical falsification of associational claims occurs during the phenomenological step of the scientific method (e.g., when a researcher finds that “

is correlated with

is correlated with

”), and it can be done on the sole basis of observational evidence. The statistical falsification of causal claims may also occur at the phenomenological step of the scientific method (e.g., when a laboratory finds that “

”), and it can be done on the sole basis of observational evidence. The statistical falsification of causal claims may also occur at the phenomenological step of the scientific method (e.g., when a laboratory finds that “

causes

causes

” in the absence of any theory to explain why), or at the falsification step of the scientific method (involving a theory, of the form “

” in the absence of any theory to explain why), or at the falsification step of the scientific method (involving a theory, of the form “

causes

causes

through a mechanism

through a mechanism

”), but either way the statistical falsification of a causal claim always requires an experiment.Footnote 16 Most statisticians and econometricians are trained in the statistical falsification of associational claims and have a limited understanding of the statistical falsification of causal claims in general, and the statistical falsification of causal theories in particular. The statistical falsification of causal claims requires the careful design of experiments, and the statistical falsification of causal theories requires testing the hypothesized causal mechanism, which in turn requires testing independent effects along the causal path. The next section delves into this important topic.

”), but either way the statistical falsification of a causal claim always requires an experiment.Footnote 16 Most statisticians and econometricians are trained in the statistical falsification of associational claims and have a limited understanding of the statistical falsification of causal claims in general, and the statistical falsification of causal theories in particular. The statistical falsification of causal claims requires the careful design of experiments, and the statistical falsification of causal theories requires testing the hypothesized causal mechanism, which in turn requires testing independent effects along the causal path. The next section delves into this important topic.

4 Causal Inference

The academic field of causal inference studies methods to determine the independent effect of a particular variable within a larger system. Assessing independent effects is far from trivial, as the fundamental problem of causal inference illustrates.

Consider two random variables

, where a researcher wishes to estimate the effect of

, where a researcher wishes to estimate the effect of

on

on

. Let

. Let

denote the expected outcome of

denote the expected outcome of

when

when

is set to

is set to

(control), and let

(control), and let

denote the expected outcome of

denote the expected outcome of

when

when

is set to

is set to

(treatment). The average treatment effect (ATE) of

(treatment). The average treatment effect (ATE) of

on

on

is defined as

is defined as

(2)

(2)

In general, ATE is not equal to the observed difference,

. The observed difference between two states of

. The observed difference between two states of

is

is

(3)

(3)

where

is a counterfactual expression, representing the expected value of

is a counterfactual expression, representing the expected value of

in an alternative universe where

in an alternative universe where

is set to

is set to

, given that what actually happened is

, given that what actually happened is

. Naturally,

. Naturally,

, for

, for

, because the counterfactual expression (the left-hand side) replicates what actually happened (right-hand side).

, because the counterfactual expression (the left-hand side) replicates what actually happened (right-hand side).

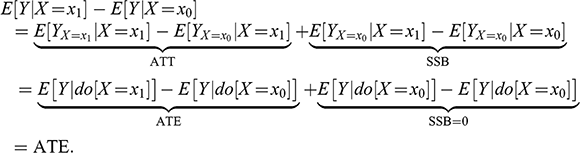

The above equation splits the observed difference into two components, the so-called average treatment effect on the treated (ATT) and self-selection bias (SSB). The fundamental problem of causal inference is that computing ATT requires estimating the counterfactual

, which is not directly observable. What is directly observable is the difference

, which is not directly observable. What is directly observable is the difference

, however that estimand of ATT is biased by SSB. The impact of SSB on

, however that estimand of ATT is biased by SSB. The impact of SSB on

can be significant, to the point of misleading the researcher. Following the earlier example, suppose that

can be significant, to the point of misleading the researcher. Following the earlier example, suppose that

is the number of drownings in a month,

is the number of drownings in a month,

represents low ice cream monthly sales, and

represents low ice cream monthly sales, and

represents high ice cream monthly sales. The value of

represents high ice cream monthly sales. The value of

is high, because of the confounding effect of warm weather, which encourages both, ice cream sales and swimming. While high ice cream sales are associated with more drownings, it would be incorrect to infer that the former is a cause of the latter. The counterfactual

is high, because of the confounding effect of warm weather, which encourages both, ice cream sales and swimming. While high ice cream sales are associated with more drownings, it would be incorrect to infer that the former is a cause of the latter. The counterfactual

represents the expected number of drownings in a month of high ice cream sales, should ice cream sales have been suppressed. The value of that unobserved counterfactual is arguably close to the observed

represents the expected number of drownings in a month of high ice cream sales, should ice cream sales have been suppressed. The value of that unobserved counterfactual is arguably close to the observed

, hence

, hence

, and the observed difference is largely due to SSB.

, and the observed difference is largely due to SSB.

Studies designed to establish causality propose methods to nullify SSB. These studies can be largely grouped into three types: interventional studies, natural experiments, and simulated interventions.

4.1 Interventional Studies

In a controlled experiment, scientists assess causality by observing the effect on

of changing the values of

of changing the values of

while keeping constant all other variables in the system (a do-operation). Hasan Ibn al-Haytham (965–1040) conducted the first recorded controlled experiment in history, in which he designed a camera obscura to manipulate variables involved in vision. Through various ingenious experiments, Ibn al-Haytham showed that light travels in a straight line, and that light reflects from the observed objects to the observer’s eyes, hence falsifying the extramission theories of light by Ptolemy, Galen, and Euclid (Reference ToomerToomer 1964). This example illustrates a strong prerequisite for conducting a controlled experiment: the researcher must have direct control of all the variables involved in the data-generating process. When that is the case, the ceteris paribus condition is satisfied, and the difference in

while keeping constant all other variables in the system (a do-operation). Hasan Ibn al-Haytham (965–1040) conducted the first recorded controlled experiment in history, in which he designed a camera obscura to manipulate variables involved in vision. Through various ingenious experiments, Ibn al-Haytham showed that light travels in a straight line, and that light reflects from the observed objects to the observer’s eyes, hence falsifying the extramission theories of light by Ptolemy, Galen, and Euclid (Reference ToomerToomer 1964). This example illustrates a strong prerequisite for conducting a controlled experiment: the researcher must have direct control of all the variables involved in the data-generating process. When that is the case, the ceteris paribus condition is satisfied, and the difference in

can be attributed to the change in

can be attributed to the change in

.

.

When some of the variables in the data-generating process are not under direct experimental control (e.g., the weather in the drownings example), the ceteris paribus condition cannot be guaranteed. In that case, scientists may execute a randomized controlled trial (RCT), whereby members of a population (called units or subjects) are randomly assigned either to a treatment or to a control group. Such random assignment aims to create two groups that are as comparable as possible, so that any difference in outcomes can be attributed to the treatment. In an RCT, the researcher carries out the do-operation on two random samples of units, rather than on a particular unit, hence enabling a ceteris paribus comparison. The randomization also allows the researcher to quantify the experiment’s uncertainty via Monte Carlo, by computing the standard deviation on ATEs from different subsamples. Scientists may keep secret from participants (single-blind) and researchers (double-blind) which units belong to each group, in order to further remove subject and experimenter biases. For additional information, see Reference Hernán and RobinsHernán and Robins (2020) and Reference Kohavi, Tang, Xu, Hemkens and IoannidisKohavi et al. (2020).

We can use the earlier characterization of the fundamental problem of causal inference to show how random assignment achieves its goal. Consider the situation where a researcher assigns units randomly to

(control group) and

(control group) and

(treatment group). Following with the earlier example, this is equivalent to tossing a coin at the beginning of every month, then setting

(treatment group). Following with the earlier example, this is equivalent to tossing a coin at the beginning of every month, then setting

(low ice cream sales) on heads and setting

(low ice cream sales) on heads and setting

(high ice cream sales) on tails. Because the intervention on

(high ice cream sales) on tails. Because the intervention on

was decided at random, units in the treatment group are expected to be undistinguishable from units in the control group, hence

was decided at random, units in the treatment group are expected to be undistinguishable from units in the control group, hence

(4)

(4)

(5)

(5)

Random assignment makes

and

and

independent of the observed

independent of the observed

. The implication from the first equation above is that

. The implication from the first equation above is that

. In the drownings example,

. In the drownings example,

, because suppressing ice cream sales would have had the same expected outcome (

, because suppressing ice cream sales would have had the same expected outcome (

) on both, high sales months and low sales months, since the monthly sales were set at random to begin with (irrespective of the weather).

) on both, high sales months and low sales months, since the monthly sales were set at random to begin with (irrespective of the weather).

In conclusion, under random assignment, the observed difference matches both ATT and ATE:

(6)

(6)

4.2 Natural Experiments

Sometimes interventional studies are not possible, because they are unfeasible, unethical, or prohibitively expensive. Under those circumstances, scientists may resort to natural experiments or simulated interventions. In a natural experiment (also known as a quasi-experiment), units are assigned to the treatment and control groups determined randomly by Nature or by other factors outside the influence of scientists (Reference DunningDunning 2012). Although natural experiments are observational (as opposed to interventional, like controlled experiments and RCT) studies, the fact that the assignment of units to groups is assumed random enables the attribution of the difference in outcomes to the treatment. Put differently, Nature performs the do-operation, and the researcher’s challenge is to identify the two random groups that enable a ceteris paribus comparison. Common examples of natural experiments include (1) regression discontinuity design (RDD); (2) crossover studies (COSs); and (3) difference-in-differences (DID) studies. Case–control studies,Footnote 17 cohort studies,Footnote 18 and synthetic control studiesFootnote 19 are not proper natural experiments because there is no random assignment of units to groups.

Regression discontinuity design studies compare the outcomes of: (a) units that received treatment because the value of an assignment variable fell barely above a threshold; and (b) units that escaped treatment because the value of an assignment variable fell barely below a threshold. The critical assumption behind RDD is that groups (a) and (b) are comparable in everything but the slight difference in the assignment variable, which can be attributed to noise, hence the difference in outcomes between (a) and (b) is the treatment effect. For further reading, see Reference Imbens and LemieuxImbens and Lemieux (2008).

A COS is a longitudinal study in which the exposure of units to a treatment is randomly removed for a time, and then returned. COS assumes that the effect of confounders does not change per unit over time. When that assumption holds, COSs have two advantages over standard longitudinal studies. First, in a COS the influence of confounding variables is reduced by each unit serving as its own control. Second, COS are statistically efficient, as they can identify causal effects in smaller samples than other studies. COS may not be appropriate when the order of treatments affects the outcome (order effects). Sufficiently long wash-out periods should be observed between treatments, to avoid that past treatments confound the estimated effects of new treatments (carryover effects). COS can also have an interventional counterpart, when the random assignment is under the control of the researcher. To learn more, see Reference Jones and KenwardJones and Kenward (2003).

When factors other than the treatment influence the outcome over time, researchers may apply a pre-post with-without comparison, called a DID study. In a DID study, researchers compare two differences: (i) the before-after difference in outcomes of the treatment group; and (ii) the before-after difference in outcomes of the control group (where the random assignment of units to groups is done by Nature). By computing the difference between (i) and (ii), DID attempts to remove from the treatment effect (i) all time-varying factors captured by (ii). DID relies on the “equal-trends assumption,” namely that no time-varying differences exist between treatment and control groups. The validity of the equal-trends assumption can be assessed in a number of ways. For example, researchers may compute changes in outcomes for the treatment and control groups repeatedly before the treatment is actually administered, so as to confirm that the outcome trends move in parallel. For additional information, see Reference Angrist and PischkeAngrist and Pischke (2008, pp. 227–243).

4.3 Simulated Interventions

The previous sections explained how interventional studies and natural experiments use randomization to achieve the ceteris paribus comparisons that result in

. Each approach demanded stronger assumptions than the previous one, with the corresponding cost in terms of generality of the conclusions. For instance, the conclusions from a controlled experiment are more general than the conclusions from an RCT, because in the former researchers control the variables involved in the data-generating process in such a way that ceteris paribus comparisons are clearer. Likewise, the conclusions from an RCT are more general than the conclusions from a natural experiment, because in an RCT the researcher is in control of the random assignment, and the researcher performs the do-operation.

. Each approach demanded stronger assumptions than the previous one, with the corresponding cost in terms of generality of the conclusions. For instance, the conclusions from a controlled experiment are more general than the conclusions from an RCT, because in the former researchers control the variables involved in the data-generating process in such a way that ceteris paribus comparisons are clearer. Likewise, the conclusions from an RCT are more general than the conclusions from a natural experiment, because in an RCT the researcher is in control of the random assignment, and the researcher performs the do-operation.

In recent decades, the field of causal inference has added one more tool to the scientific arsenal: when interventional studies and natural experiments are not possible, researchers may still conduct an observational study that simulates a do-operation, with the help of a hypothesized causal graph. The hypothesized causal graph encodes the information needed to remove from observations the SSB introduced by confounders, under the assumption that the causal graph is correct. The price to pay is, as one might have expected, accepting stronger assumptions that make the conclusions less general, but still useful.

Simulated interventions have two main applications: First, subject to a hypothesized causal graph, a simulated intervention allows researchers to estimate the strength of a causal effect from observational studies. Second, a simulated intervention may help falsify a hypothesized causal graph, when the strength of one of the effects posited by the graph is deemed statistically insignificant (once again, a modus tollens argument, see Section 3.4).

It is important to understand the difference between establishing a causal claim and falsifying a causal claim. Through interventional studies and natural experiments, subject to some assumptions, a researcher can establish or falsify a causal claim without knowledge of the causal graph. For this reason, they are the most powerful tools in causal inference. In simulated interventions, the causal graph is part of the assumptions, and one cannot prove what one is assuming. The most a simulated intervention can achieve is to disprove a hypothesized causal graph, by finding a contradiction between an effect claimed by a graph and the effect estimated with the help of that same graph. This power of simulated interventions to falsify causal claims can be very helpful in discovering through elimination the causal structure hidden in the data.

4.3.1 Causal Discovery

Causal discovery can be defined as the search for the structure of causal relationships, by analyzing the statistical properties of observational evidence (Reference Spirtes, Glymour and ScheinesSpirtes et al. 2001). While observational evidence almost never suffices to fully characterize a causal graph, it often contains information helpful in reducing the number of possible structures of interdependence among variables. At the very least, the extra-statistical information assumed by the causal graph should be compatible with the observations. Over the past three decades, statisticians have developed numerous computational methods and algorithms for the discovery of causal relations, represented as directed acyclic graphs (see Reference Glymour, Zhang and SpirtesGlymour et al. 2019). These methods can be divided into the following classes: (a) constraint-based algorithms; (b) score-based algorithms; and (c) functional causal models (FCMs).

Constraint-based methods exploit conditional independence relationships in the data to recover the underlying causal structure. Two of the most widely used methods are the PC algorithm (named after its authors, Peter Spirtes and Clark Glymour), and the fast causal inference (FCI) algorithm (Reference Spirtes, Glymour and ScheinesSpirtes et al. 2000). The PC algorithm assumes that there are no latent (unobservable) confounders, and under this assumption the discovered causal information is asymptotically correct. The FCI algorithm gives asymptotically correct results even in the presence of latent confounders.

Score-based methods can be used in the absence of latent confounders. These algorithms attempt to find the causal structure by optimizing a defined score function. An example of a score-based method is the greedy equivalence search (GES) algorithm. This heuristic algorithm searches over the space of Markov equivalence classes, that is, the set of causal structures satisfying the same conditional independences, evaluating the fitness of each structure based on a score calculated from the data (Reference ChickeringChickering 2003). The GES algorithm is known to be consistent under certain assumptions, which means that as the sample size increases, the algorithm will converge to the true causal structure with probability approaching 1. However, this does not necessarily mean that the algorithm will converge to the true causal structure in finite time or with a reasonable sample size. GES is also known to be sensitive to the initial ordering of variables.

FCMs distinguish between different directed-acyclic graphs in the same equivalence class. This comes at the cost of making additional assumptions on the data distribution than conditional independence relations. A FCM models the effect variable

as

as

, where

, where

is a function of the direct causes

is a function of the direct causes

and

and

is noise that is independent of

is noise that is independent of

. Subject to the aforementioned assumptions, the causal direction between

. Subject to the aforementioned assumptions, the causal direction between

and

and

is identifiable, because the independence condition between

is identifiable, because the independence condition between

and

and

holds only for the true causal direction (Reference Shimizu, Hoyer, Hyvärinen and KerminenShimizu et al. 2006; Reference Hoyer, Janzing, Mooji, Peters and SchölkopfHoyer et al. 2009; and Reference Zhang and HyvärinenZhang and Hyvaerinen 2009).

holds only for the true causal direction (Reference Shimizu, Hoyer, Hyvärinen and KerminenShimizu et al. 2006; Reference Hoyer, Janzing, Mooji, Peters and SchölkopfHoyer et al. 2009; and Reference Zhang and HyvärinenZhang and Hyvaerinen 2009).

Causal graphs can also be derived from nonnumerical data. For example, Reference Laudy, Denev and GinsbergLaudy et al. (2022) apply natural language processing techniques to news articles in which different authors express views of the form

. By aggregating those views, these researchers derive directed acyclic graphs that represent collective, forward-looking, point-in-time views of causal mechanisms.

. By aggregating those views, these researchers derive directed acyclic graphs that represent collective, forward-looking, point-in-time views of causal mechanisms.

Machine learning is a powerful tool for causal discovery. Various methods allow researchers to identify the important variables associated in a phenomenon, with minimal model specification assumptions. In doing so, these methods decouple the variable search from the specification search, in contrast with traditional statistical methods. Examples include mean-decrease accuracy, local surrogate models, and Shapley values (Reference López de PradoLópez de Prado 2020, pp. 3–4, Reference López de PradoLópez de Prado 2022a). Once the variables relevant to a phenomenon have been isolated, researchers can apply causal discovery methods to propose a causal structure (identify the links between variables, and the direction of the causal arrows).

4.3.2 Do-Calculus

Do-calculus is a complete axiomatic system that allows researchers to estimate do-operators by means of conditional probabilities, where the necessary and sufficient conditioning variables can be determined with the help of the causal graph (Reference Shpitser and PearlShpitser and Pearl 2006). The following sections review some notions of do-calculus needed to understand this Element. I encourage the reader to learn more about these important concepts in Reference PearlPearl (2009), Reference Pearl, Glymour and JewellPearl et al. (2016), and Reference NealNeal (2020).

4.3.2.1 Blocked Paths

In a graph with three variables

, a variable

, a variable

is a confounder with respect to

is a confounder with respect to

and

and

when the causal relationships include a structure X ← Z → Y. A variable

when the causal relationships include a structure X ← Z → Y. A variable

is a collider with respect to

is a collider with respect to

and

and

when the causal relationships are reversed, that is, X → Z ← Y. A variable

when the causal relationships are reversed, that is, X → Z ← Y. A variable

is a mediator with respect to

is a mediator with respect to

and

and

when the causal relationships include a structure X → Z → Y.Footnote 20

when the causal relationships include a structure X → Z → Y.Footnote 20

A path is a sequence of arrows and nodes that connect two variables

and

and

, regardless of the direction of causation. A directed path is a path where all arrows point in the same direction. In a directed path that starts in

, regardless of the direction of causation. A directed path is a path where all arrows point in the same direction. In a directed path that starts in

and ends in

and ends in

,

,

is an ancestor of

is an ancestor of

, and

, and

is a descendant of

is a descendant of

. A path between

. A path between

and

and

is blocked if either: (1) the path traverses a collider, and the researcher has not conditioned on that collider or its descendants; or (2) the researcher conditions on a variable in the path between

is blocked if either: (1) the path traverses a collider, and the researcher has not conditioned on that collider or its descendants; or (2) the researcher conditions on a variable in the path between

and

and

, where the conditioned variable is not a collider. Association flows along any paths between

, where the conditioned variable is not a collider. Association flows along any paths between

and

and

that are not blocked. Causal association flows along an unblocked directed path that starts in treatment

that are not blocked. Causal association flows along an unblocked directed path that starts in treatment

and ends in outcome

and ends in outcome

, denoted the causal path. Association implies causation only if all noncausal paths are blocked. This is the deeper explanation of why association does not imply causation, and why causal independence does not imply statistical independence.

, denoted the causal path. Association implies causation only if all noncausal paths are blocked. This is the deeper explanation of why association does not imply causation, and why causal independence does not imply statistical independence.

Two variables

and

and

are d-separated by a (possibly empty) set of variables

are d-separated by a (possibly empty) set of variables

if, upon conditioning on

if, upon conditioning on

, all paths between

, all paths between

and

and

are blocked. The set

are blocked. The set

d-separates

d-separates

and

and

if and only if

if and only if

and

and

are conditionally independent given

are conditionally independent given

. For a proof of this statement, see Reference Koller and FriedmanKoller and Friedman (2009, chapter 3). This important result, sometimes called the global Markov condition in Bayesian network theory,Footnote 21 allows researchers to assume that

. For a proof of this statement, see Reference Koller and FriedmanKoller and Friedman (2009, chapter 3). This important result, sometimes called the global Markov condition in Bayesian network theory,Footnote 21 allows researchers to assume that

, and estimate ATE as

, and estimate ATE as

(7)

(7)

The catch is, deciding which variables belong in

requires knowledge of the causal graph that comprises all the paths between

requires knowledge of the causal graph that comprises all the paths between

and

and

. Using the above concepts, it is possible to define various specific controls for confounding variables, including: (a) the backdoor adjustment; (b) the front-door adjustment; and (c) the method of instrumental variables (Reference PearlPearl 2009). This is not a comprehensive list of adjustments, and I have selected these three adjustments in particular because I will refer to them in the sections ahead.

. Using the above concepts, it is possible to define various specific controls for confounding variables, including: (a) the backdoor adjustment; (b) the front-door adjustment; and (c) the method of instrumental variables (Reference PearlPearl 2009). This is not a comprehensive list of adjustments, and I have selected these three adjustments in particular because I will refer to them in the sections ahead.

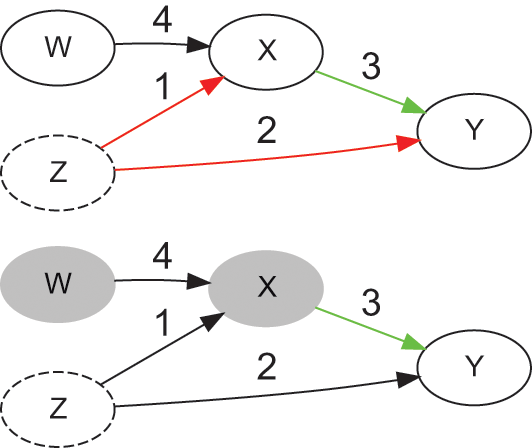

4.3.2.2 Backdoor Adjustment

A backdoor path between

and

and

is an unblocked noncausal path that connects those two variables. The term backdoor is inspired by the fact that this kind of paths have an arrow pointing into the treatment (

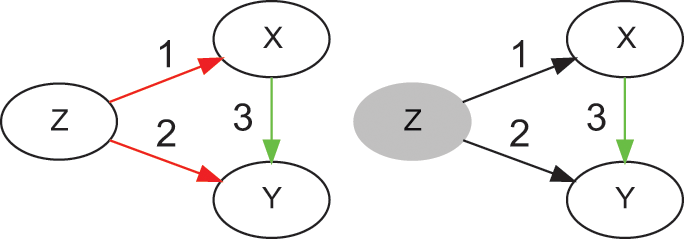

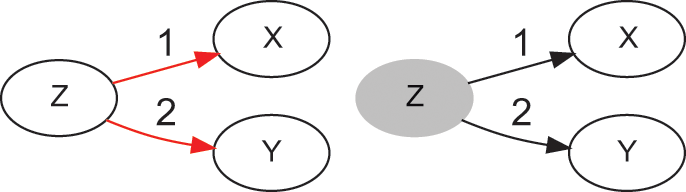

is an unblocked noncausal path that connects those two variables. The term backdoor is inspired by the fact that this kind of paths have an arrow pointing into the treatment (

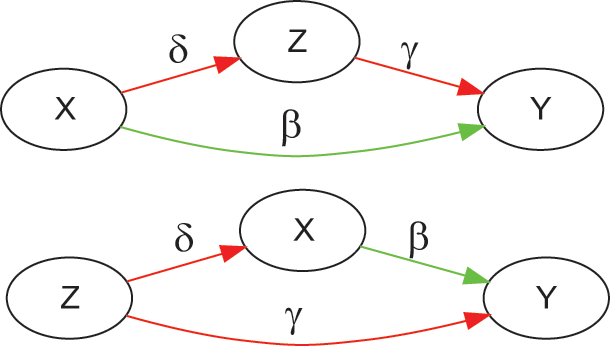

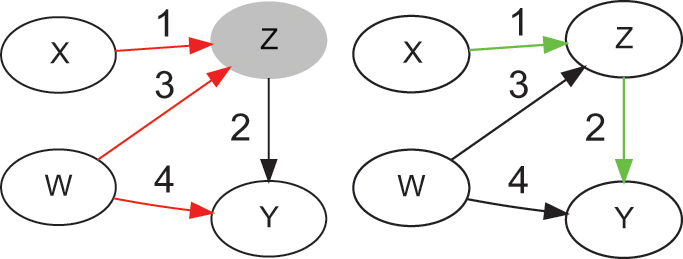

). For example, Figure 2 (left) contains a backdoor path (colored in red, Y ← Z → X), and a causal path (colored in green, Y → X). Backdoor paths can be blocked by conditioning on a set of variables

). For example, Figure 2 (left) contains a backdoor path (colored in red, Y ← Z → X), and a causal path (colored in green, Y → X). Backdoor paths can be blocked by conditioning on a set of variables

that satisfies the backdoor criterion. The backdoor criterion is useful when controlling for observable confounders.Footnote 22

that satisfies the backdoor criterion. The backdoor criterion is useful when controlling for observable confounders.Footnote 22

Example of a causal graph that satisfies the backdoor criterion, before (left) and after (right) conditioning on Z (shaded node)

A set of variables

satisfies the backdoor criterion with regards to treatment

satisfies the backdoor criterion with regards to treatment

and outcome

and outcome

if the following two conditions are true: (i) conditioning on

if the following two conditions are true: (i) conditioning on

blocks all backdoor paths between

blocks all backdoor paths between

and

and

; and (ii)

; and (ii)

does not contain any descendants of

does not contain any descendants of

. Then,

. Then,

is a sufficient adjustment set, and the causal effect of

is a sufficient adjustment set, and the causal effect of

on

on

can be estimated as:

can be estimated as:

(8)

(8)

Intuitively, condition (i) blocks all noncausal paths, while condition (ii) keeps open all causal paths. In Figure 2, the only sufficient adjustment set

is

is

. Set

. Set

is sufficient because conditioning on

is sufficient because conditioning on

blocks that backdoor path Y ← Z → X, and

blocks that backdoor path Y ← Z → X, and

is not a descendant of

is not a descendant of

. The result is that the only remaining association is the one flowing through the causal path, thus adjusting the observations in a way that simulates a do-operation on

. The result is that the only remaining association is the one flowing through the causal path, thus adjusting the observations in a way that simulates a do-operation on

. In general, there can be multiple sufficient adjustment sets that satisfy the backdoor criterion for any given graph.

. In general, there can be multiple sufficient adjustment sets that satisfy the backdoor criterion for any given graph.

4.3.2.3 Front-Door Adjustment

Sometimes researchers may not be able to condition on a variable that satisfies the backdoor criterion, for instance when that variable is latent (unobservable). In that case, under certain conditions, the front-door criterion allows researchers to estimate the causal effect with the help of a mediator.

A set of variables

satisfies the front-door criterion with regards to treatment

satisfies the front-door criterion with regards to treatment

and outcome

and outcome

if the following three conditions are true: (i) all causal paths from

if the following three conditions are true: (i) all causal paths from

to

to

go through

go through

; (ii) there is no backdoor path between

; (ii) there is no backdoor path between

and

and

; (iii) all backdoor paths between

; (iii) all backdoor paths between

and

and

are blocked by conditioning on

are blocked by conditioning on

. Then,

. Then,

is a sufficient adjustment set, and the causal effect of

is a sufficient adjustment set, and the causal effect of

on

on

can be estimated as:

can be estimated as:

(9)

(9)

Intuitively, condition (i) ensures that

completely mediates the effect of

completely mediates the effect of

on

on

, condition (ii) applies the backdoor criterion on X → S, and condition (iii) applies the backdoor criterion on S → Y.

, condition (ii) applies the backdoor criterion on X → S, and condition (iii) applies the backdoor criterion on S → Y.

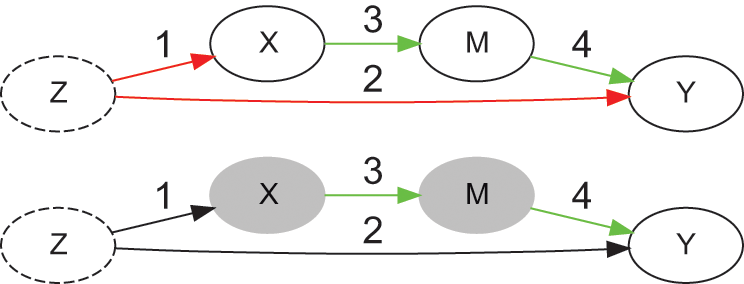

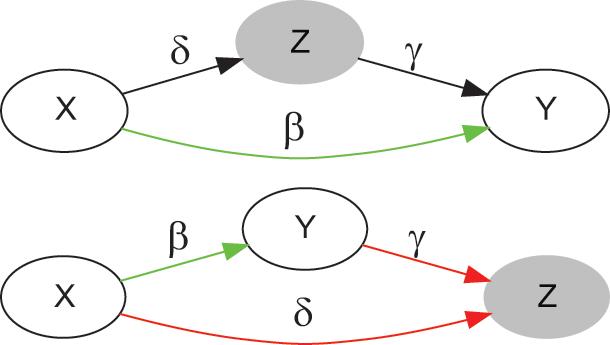

Figure 3 provides an example of a causal graph with a latent variable

(represented as a dashed oval) that confounds the effect of

(represented as a dashed oval) that confounds the effect of

on

on

. There is a backdoor path between

. There is a backdoor path between

and

and

(colored in red, Y ← Z → X), and a causal path (colored in green, X → M → Y). The first condition of the backdoor criterion is violated (it is not possible to condition on

(colored in red, Y ← Z → X), and a causal path (colored in green, X → M → Y). The first condition of the backdoor criterion is violated (it is not possible to condition on

), however

), however

satisfies the front-door criterion, because

satisfies the front-door criterion, because

mediates the only causal path (X → M → Y), the path between

mediates the only causal path (X → M → Y), the path between

and

and

is blocked by collider

is blocked by collider

(M → Y ← Z → X), and conditioning on

(M → Y ← Z → X), and conditioning on

blocks the backdoor path between

blocks the backdoor path between

and

and

(Y ← Z → X → M). The adjustment accomplishes that the only remaining association is the one flowing through the causal path.

(Y ← Z → X → M). The adjustment accomplishes that the only remaining association is the one flowing through the causal path.

Example of a causal graph that satisfies the front-door criterion, before (top) and after (bottom) adjustment

4.3.2.4 Instrumental Variables

The front-door adjustment controls for a latent confounder when a mediator exists. In the absence of a mediator, the instrumental variables method allows researchers to control for a latent confounder

, as long as researchers can find a variable

, as long as researchers can find a variable

that turns

that turns

into a collider, thus blocking the backdoor path through

into a collider, thus blocking the backdoor path through

.

.

A variable

satisfies the instrumental variable criterion relative to treatment

satisfies the instrumental variable criterion relative to treatment

and outcome

and outcome

if the following three conditions are true: (i) there is an arrow W → X; (ii) the causal effect of

if the following three conditions are true: (i) there is an arrow W → X; (ii) the causal effect of

on

on

is fully mediated by

is fully mediated by

; and (iii) there is no backdoor path between

; and (iii) there is no backdoor path between

and

and

.

.

Intuitively, conditions (i) and (ii) ensure that

can be used as a proxy for

can be used as a proxy for

, whereas condition (iii) prevents the need for an additional backdoor adjustment to de-confound the effect of

, whereas condition (iii) prevents the need for an additional backdoor adjustment to de-confound the effect of

on

on

. Figure 4 provides an example of a causal graph with a latent variable