INTRODUCTION

‘How does an organization respond when influential stakeholders hold contradicting views about its appropriate course of action’? (Pache & Santos, Reference Pache and Santos2010: 455)

Corporate philanthropic giving[Footnote 1] is an institutionalized practice that a firm uses to acquire legitimacy conferred by stakeholder groups and respond to stakeholder claims (Jeong & Kim, Reference Jeong and Kim2018). For example, firms engage in charitable donations to respond to government claims and gain sociopolitical legitimacy (Wang & Qian, Reference Wang and Qian2011). This definition may not be used in the contexts of western environments, such as US, because corporate philanthropic giving is voluntary transfers of cash or other assets by firms (Gautier & Pache, Reference Gautier and Pache2015). Scholars largely deduce that firms can establish and maintain good relations with stakeholders through philanthropic giving under the assumption that all stakeholders form one uniform group (e.g., Cuypers, Koh, & Wang, Reference Cuypers, Koh and Wang2015; Godfrey, Reference Godfrey2005; Wang & Qian, Reference Wang and Qian2011).

However, various stakeholders may have divergent and conflicting demands, which creates tension for firms on how to engage in charitable donations (Wang, Tong, Takeuchi, & George, Reference Wang, Tong, Takeuchi and George2016). Thus, managing multiple stakeholders is increasingly important for firms (Pache & Santos, Reference Pache and Santos2010). As Wang et al. (Reference Wang, Tong, Takeuchi and George2016: 540) suggested, future research should ‘study the interaction of shareholders and other stakeholders and how firms resolve the conflict between them’.

Recent literature on decoupling suggests organizations can use a decoupling tactic to accommodate competing stakeholder pressures (Greenwood, Raynard, Kodeih, Micelotta, & Lounsbury, Reference Greenwood, Raynard, Kodeih, Micelotta and Lounsbury2011; Heese, Krishnan, & Moers, Reference Heese, Krishnan and Moers2016; Luo, Wang, & Zhang, Reference Luo, Wang and Zhang2017). Decoupling refers to the process through which organizations symbolically endorse or adopt policies, while separating these policies from actual implementation (Bromley & Powell, Reference Bromley and Powell2012; Meyer & Rowan, Reference Meyer and Rowan1977; Oliver, Reference Oliver1991). Such research has focused mostly on organizational external environments (e.g., stakeholder pressures) and failed to consider organizational interpretation towards stakeholder pressures or demands from an internal perspective (Durand, Hawn, & Ioannou, Reference Durand, Hawn and Ioannou2019). The demands of stakeholders are not perceived or interpreted as equally salient across firms. Faced with the conflicting demands, firms may not take the decoupling response because of their different interpretations of stakeholder demands. However, prior decoupling research has focused limited attention to when and why firms are less likely to use decoupling to cope with the conflicting demands.

To address these research gaps and based on stakeholder theory (e.g., Carroll, Reference Carroll1989; Freeman, Reference Freeman1984), we propose a stakeholder framework in which firms respond to the conflicting pressures that arise from governments and investors in the context of corporate philanthropic giving. Specifically, we argue that firms that experience increased government pressures (i.e., the salience of governments increases) are likely to engage in philanthropic giving. However, this notion creates conflict with investors who prioritize economic returns. Firms that experience such conflict may take a decoupling response in philanthropic giving, which refers to these firms still engaging in charitable donations but donating to a lesser extent.

More importantly, we identify the boundary conditions that weaken the relationship between the conflicting demands and decoupling of corporate giving. Drawing on stakeholder salience literature (e.g., Durand et al., Reference Durand, Hawn and Ioannou2019; Mitchell, Agle, & Wood, Reference Mitchell, Agle and Wood1997), we argue that different managers perceive the same stakeholder demands as more or less salient, and such perception of stakeholder salience influences their decoupling decisions. Hence, this relationship will be weaker when managers perceive government demands as more salient or when managers perceive investor claims as less salient. Specifically, we identify contingent factors that may affect managerial perceptions or interpretations of stakeholder demands. We argue that firms with CEOs who are more sensitive to government demands (such as those with a communist ideology) are less likely to take the decoupling response. In addition, we expect that firms with CEOs who have fewer career concerns are less sensitive to investor claims, and thus are less likely to take the decoupling response.

We test our theory by using Chinese firms listed on the Shanghai and Shenzhen Stock Exchanges from 2006 to 2015. The China context is ideal to test our theory for several reasons. First, Chinese listed firms are commonly trapped in a struggle between government demands for social performance and investor expectations on economic returns (Fligstein & Zhang, Reference Fligstein and Zhang2011; Tang & Tang, Reference Tang and Tang2018). Second, we can easily observe the impact of government pressures on corporate giving. In China where provincial governments’ need for public services is often unmet, they tend to transfer their fiscal pressures to local firms. Philanthropic giving is a common way for local firms to forge ties with the governments (e.g., Lin, Tan, Zhao, & Karim, Reference Lin, Tan, Zhao and Karim2015). Third, CEOs’ communist ideology and varying degrees of career concerns in Chinese firms allow us to test the boundary conditions for corporate decoupling response. Communist ideology has been the dominant ideology in China since the CP took power in 1949 (Wang, Du, & Marquis, Reference Wang, Du and Marquis2019). The CP often exerts impact on firms via injecting its communist ideology into the firms, for example, it appoints senior managers of state-owned enterprises and controls their job rotation, and it requires certain private firms to hire party members among their employees and establishes a party organization (Shi, Markóczy, & Stan, Reference Shi, Markóczy and Stan2014). In addition, CEOs’ career concerns vary with their age because of the stipulated retirement age set by the State Council (described in METHODS section). CEOs who are also the chairmen of the board have fewer worries about involuntary replacement in Chinese firms (Pi & Lowe, Reference Pi and Lowe2011).

We aim to make several contributions. First, our study adds novel insights into the stakeholder salience literature in terms of how the salience of a stakeholder changes.[Footnote 2] Generally, the study contributes to stakeholder management literature by examining how managerial perceptions of stakeholder salience influence corporate responses to conflicting stakeholder pressures. Second, this study advances decoupling literature (e.g., Luo et al., Reference Luo, Wang and Zhang2017; Wang, Wijen, & Heugens, Reference Wang, Wijen and Heugens2018) by identifying the boundary conditions of decoupling response to conflicting pressures. Hence, we can develop a more nuanced understanding of a firm's decision on when and how to respond to conflicting stakeholder demands. Third, this study contributes to the research on the antecedents of corporate philanthropy by examining the simultaneous influences of multiple stakeholders.

THEORETICAL BACKGROUND

Stakeholders can influence organizational practices by exerting expectations and pressures on their organizations. According to Freeman (Reference Freeman1984: 25), a stakeholder is ‘any group or individual who can affect or is affected by the achievement of the firm's objectives’. In turn, an organization is not ‘self-contained or self-sufficient’ and is dependent on its environment (i.e., stakeholders) for resources and legitimacy (Pfeffer & Salancik, Reference Pfeffer and Salancik1978: 43; Suchman, Reference Suchman1995). Thus, firms should comply with stakeholder expectations and pressures.

Firms may not respond to all stakeholder claims but stakeholders with high salience would. Prior research suggests that firms can divide stakeholders into primary and secondary stakeholder groups (Clarkson, Reference Clarkson1995). This division neglects stakeholder salience, which is defined as ‘the degree to which managers give priority to competing stakeholder claims’ (Mitchell et al., Reference Mitchell, Agle and Wood1997: 854). The literature on stakeholder salience suggests that managers perceive a stakeholder as salient depending on the stakeholder's three attributes, namely, the power to influence firms, the legitimacy of its claim on firms, and the urgency of the claim (Mitchell et al., Reference Mitchell, Agle and Wood1997). A stakeholder claim is urgent when it is important and calls for immediate attention. Stakeholder salience is thus positively related to the cumulative number of the three attributes (Agle, Mitchell, & Sonnenfeld, Reference Agle, Mitchell and Sonnenfeld1999).

Managerial perceptions of stakeholder salience largely determine whether and how firms respond to stakeholder claims or demands. The stakeholder attributes are not static but variable (Mitchell et al., Reference Mitchell, Agle and Wood1997). Different managers may perceive the same claims from primary stakeholders as more or less salient and then take different responses (Durand et al., Reference Durand, Hawn and Ioannou2019). Based on stakeholder salience literature, we introduce managerial perceptions of stakeholder salience to examine how firms respond to conflicting stakeholder claims. Specifically, we focus on conflicting stakeholder pressures that emanate from government and investor stakeholders as two key stakeholders in the context of corporate giving.[Footnote 3]

Conflicts from Government and Investor Stakeholders in Corporate Giving

As Zhang, Marquis, and Qiao (Reference Zhang, Marquis and Qiao2016: 2) infer, ‘the government is an important initiator, stakeholder, and audience of corporate charitable donations’. The government plays a dominant role in driving corporate giving, especially in China, because it can use guidelines or policies to ‘regulate business in the public interest’ (Freeman, Reference Freeman1984: 13) and ‘create norms and standards of legitimacy for firms’ (Jia & Zhang, Reference Jia and Zhang2013; Marquis & Qian, Reference Marquis and Qian2013: 127). Government bodies have the power to allocate resources (e.g., government subsidies), ratify public projects, determine taxation and market structures, and grant property protections (Li & Zhang, Reference Li and Zhang2007; Shaffer, Reference Shaffer1995; Shi et al., Reference Shi, Markóczy and Stan2014). To maintain or gain political legitimacy, firms take actions that are consistent with government guidelines and policies, which are sources of uncertainty and risk for firms (Hillman, Reference Hillman2005).

As a highly visible practice, corporate giving can be easily observed and measured by governments (Zhang et al., Reference Zhang, Marquis and Qiao2016). Governments might immediately appreciate corporate giving because it helps reduce their fiscal burdens (Dickson, Reference Dickson2003; Lin et al., Reference Lin, Tan, Zhao and Karim2015). As Wang and Qian (Reference Wang and Qian2011: 1165) note, ‘corporate philanthropy meets government needs for providing social services, it may substitute for other means of establishing links with a government’. In addition, corporate donation helps firms obtain sociopolitical legitimacy (Sánchez, Reference Sánchez2000; Wang & Qian, Reference Wang and Qian2011), which enables them to gain political access (e.g., political resource).

Investors, who prioritize economic returns over social performance (Carroll, Reference Carroll1991, Reference Carroll2016; Hubbard, Christensen, & Graffin, Reference Hubbard, Christensen and Graffin2017), will only evaluate corporate giving positively after firms satisfy their primary claims (Wang & Qian, Reference Wang and Qian2011). As Jeong and Kim (Reference Jeong and Kim2018) claim, ‘tensions between economic efficiency and social legitimacy are often inevitable in corporate giving’. Therefore, conflicts regarding corporate giving between government and investor stakeholders may exist.

HYPOTHESES DEVELOPMENT

Philanthropic Giving in China

Philanthropic giving comprises gifts or monetary contributions that firms often use to seek political access in China (e.g., Jia & Zhang, Reference Jia and Zhang2013). Business operations are largely intertwined with politics. Through significant control over rules and policies, the Chinese government largely shapes the regulatory environment for firms and thus constitutes a major source of risk or uncertainty on firms’ operation.

The Chinese government has issued a number of regulations and guidelines to alleviate poverty, such as ‘Outline of China's Rural Poverty Alleviation (2011–2020)’. Given that economic development is largely uneven across regions, fiscal difficulties and public service gaps exist in many places, and firms are often called on to provide public services (Zhang et al., Reference Zhang, Marquis and Qiao2016). Corporate charitable donations are an important form of helping governments provide public services. For instance, the Mianyang government in Sichuan forced local firms to fund the region's educational programs. The government published the ranking lists of firms who made donations and called them ‘caring corporations’ in its official website.[Footnote 4] Consequently, firms often make donations to cater to government claims and establish good firm – government relationships (Lin et al., Reference Lin, Tan, Zhao and Karim2015).

Public Budget Deficits and Corporate Giving

Many studies emphasize that a firm's location exposes it to its region's institutional environment. A region's government constitutes a pivotal source of the region's institutional pressure (Greenwood et al., Reference Greenwood, Díaz, Li and Lorente2010; Kassinis & Vafeas, Reference Kassinis and Vafeas2006). Although firms’ activities may refer to various regions, firms mainly respond to the pressure from the location of their headquarters. For example, Marquis and Qian (Reference Marquis and Qian2013) demonstrate how regional government institutional development affects CSR substance of local firms, whose headquarters are in corresponding provinces.

The salience of governments to firms increases when local governments encounter public budget deficits. Government demands on corporate giving becomes urgent because governments’ fiscal budgets may generate pressure on local firms (Carroll, Reference Carroll1989). For instance, Kassinis and Vafeas (Reference Kassinis and Vafeas2006) use state environmental budgets to capture the state governments’ pressures on firm environmental performance.

We expect that firms will use corporate giving to respond to local governments’ public budget deficits. On the one hand, the governments’ unmet needs for providing public services may generate pressures on local firms, particularly in countries with weak institutions (Hornstein & Zhao, Reference Hornstein and Zhao2018). For instance, a government may reach out to firms for charitable donations when it fails to fund public services (Friedman, Johnson, Kaufmann, & Zoido-Lobaton, Reference Friedman, Johnson, Kaufmann and Zoido-Lobaton2000) (see a case below). Such pressures constitute a key external source of uncertainty and risk on firms’ operations (Hillman, Reference Hillman2005). The governments may raise tax rates on local firms to eliminate such fiscal pressures. However, frequent changes in tax policy will be detrimental to the governments’ authority and prestige and likely harm social order and stability (Friedman et al., Reference Friedman, Johnson, Kaufmann and Zoido-Lobaton2000).

Case Illustration. Chinese local governments with budget deficits generally launch several projects (e.g., anti-poverty programs, hope projects, and infrastructure construction), which informally require firms in their jurisdictions to engage in charitable activities (Jia & Zhang, Reference Jia and Zhang2013). For instance, the Yangzhou government in Jiangsu province printed an official document that pressured local firms to give charitable donations to anti-poverty programs.[Footnote 5]

On the other hand, such deficits provide an important opportunity for local firms to establish good relationships with the governments. In this case, the governments should urgently provide social services to maintain their authority and social stability. Firms will lose this opportunity when delay in paying attention to the urgent demands.

Previous studies suggest that firms can take various political activities to manage the uncertainty and risk associated with government expectations and pressures, such as lobbying and donations (Lin et al., Reference Lin, Tan, Zhao and Karim2015; Sánchez, Reference Sánchez2000; Shaffer, Reference Shaffer1995). Particularly, corporate giving directly helps governments provide public services and reduce their fiscal burdens (Dickson, Reference Dickson2003). In return, governments are willing to provide key resources and confer sociopolitical legitimacy to firms with philanthropic activities. In this regard, firms may seize this opportunity to cater to the governments’ needs via corporate giving, which is frequently used to establish firm – government relationships (Lin et al., Reference Lin, Tan, Zhao and Karim2015; Sánchez, Reference Sánchez2000). Thus:

Hypothesis 1a: The greater the public budget deficit in a region, the more philanthropic giving firms in the region will provide.

Earnings Pressure and Corporate Giving

In this part, we explain when and why investor claims on economic returns create conflict with government demands when firms engage in philanthropic giving.

Investors will value corporate giving when the firm acquires pragmatic legitimacy, which refers to ‘the self-interested calculations of an organization's most immediate audiences’ (Schuman, Reference Suchman1995: 578). The primary responsibility or objective of a firm is to generate economic profits for shareholders or investors (Carroll, Reference Carroll1991, Reference Carroll2016). This idea is the base of the pyramid where other corporate responsibilities (i.e., legal, moral, and philanthropic) rest on (see Carroll, Reference Carroll1991, Reference Carroll2016). In this regard, when a firm has met investor expectations (i.e., primary responsibility) through achieving high profitability, it is likely to gain pragmatic legitimacy. With pragmatic legitimacy established, investors may value corporate giving as a response to other stakeholder pressures, such as government expectations, which further help firms acquire sociopolitical or moral legitimacy (Schuman, Reference Suchman1995).

However, when firms encounter earnings pressure, they may lack the motivation or the ability to engage in philanthropic giving. We expect that the salience of investors to a firm increases when the firm faces earnings pressure, which is defined as the difference between analysts’ earnings forecast and a firm's expected performance (Skinner & Sloan, Reference Skinner and Sloan2002; Zhang & Gimeno, Reference Zhang and Gimeno2010). Investor claims on economic return becomes more urgent for firms under earnings pressure. Delay in paying attention to earnings pressure may lead to investor penalties, for example, stock price declines, employment risk increases and investors withdraw their capital (Pfarrer, Pollock, & Rindova, Reference Pfarrer, Pollock and Rindova2010; Skinner & Sloan, Reference Skinner and Sloan2002; Zhang & Gimeno, Reference Zhang and Gimeno2010, Reference Zhang and Gimeno2016). In addition, as earnings pressure threatens a firm's pragmatic legitimacy, investors may devalue corporate giving, which directly diverts corporate current earnings, products, or human resources (Wang, Choi, & Li, Reference Wang, Choi and Li2008). Consequently, such firms are less likely to engage in philanthropic giving.

Hypothesis 1b: The greater earnings pressure firms encounter, the less likely these firms will engage in philanthropic giving.

Conflicting Stakeholder Pressures and the Decoupling of Corporate Giving

As argued above, in a region with large public budget deficits, firms are more likely to respond to government expectations of philanthropic giving (investor claims are likely latent to these firms). However, when these firms face earnings pressure (investors become salient), they may lack the motivation or ability to make charitable donations. How should firms that face such conflicting demands allocate resources to philanthropic giving? The literature on stakeholder salience suggests a stakeholder's claims or demands on corporate responses are largely determined by its salience (Mitchell et al., Reference Mitchell, Agle and Wood1997).

However, firms are trapped in a dilemma when firms face competing claims from different stakeholders who are all assessed as salient. On the one hand, these firms should engage in philanthropic giving in response to public budget deficits to obtain sociopolitical legitimacy and establish good relationships with governments. On the other hand, the primary responsibility of these firms from the investor perspective is generating current earnings and gaining pragmatic legitimacy. In such a dilemma, compliance with one salient stakeholder's demands may violate the other's claims. Therefore, firms should balance conflicting pressures from governments and investors without satisfying one at the expense of the other.

To resolve this dilemma, we argue that firms use a decoupling response in corporate giving that can balance the conflicting pressures. Although policy or practice adoption is a symbolic dimension of a firm's response to stakeholder demands (Luo et al., Reference Luo, Wang and Zhang2017), such practice can help firms maintain or obtain legitimacy in the eyes of stakeholders and deter further scrutiny from the stakeholders (Meyer & Rowan, Reference Meyer and Rowan1977; Shipilov, Greve, & Rowley, Reference Shipilov, Greve and Rowley2010). Practice implementation is a substantive dimension of the firm's response (Westphal & Zajac, Reference Westphal and Zajac1994). Policy adoption thus preserves and gives firms more discretion to decouple from actual implementation (e.g., Oliver, Reference Oliver1991).

In our context, decoupling of corporate giving refers to firms still making charitable donations but donating less to balance the conflicting pressures. As compliance with what one stakeholder claim may dissatisfy other stakeholders, firms may consider whether and to what extent to engage in philanthropic giving. Specifically, firms may still make donations in response to public budget deficits and donate monetary contributions to a lesser extent to meet earnings pressure. As mentioned, policy adoption helps the organization maintain legitimacy and delay further supervision (Luo et al., Reference Luo, Wang and Zhang2017). Thus, making donations implies that firms are compliant with government demands and are willing to help governments ease public budget deficits. This practice may restrain further government scrutiny and provide such firms more discretion (e.g., resources and attention) to meet earnings pressure. As a result, these firms may make fewer donations after deciding to donate.

Therefore, a decoupling response can reflect a firm's best effort to balance the competing demands (Luo et al., Reference Luo, Wang and Zhang2017). When the competing demands from governments and investors are all assessed as salient, the decoupling response in philanthropic giving may be the practical way for firms to find a balance. In turn:

Hypothesis 2: The greater public budget deficits of a region where the firms are headquartered and the greater earnings pressure the firms encounter, the more likely these firms will exhibit a decoupling response in philanthropic giving.

Perceived Salience of Stakeholder Claims and Boundary Conditions of Decoupling Response to Conflicting Pressures

As argued above, firms take a decoupling response in philanthropic giving when governments and investors raise competing demands. To extend literature on stakeholder salience and decoupling, we further identify the boundary conditions under which firms may not use decoupling in response to the conflicting demands. Studies have implicitly assumed that firm–stakeholder relationship is fixed or static (e.g., Freeman, Reference Freeman1984). This assumption is likely problematic because different managers may perceive or interpret certain stakeholders as more or less salient (Bundy, Shropshire, & Buchholtz, Reference Bundy, Shropshire and Buchholtz2013; Durand et al., Reference Durand, Hawn and Ioannou2019; Mitchell et al.,Reference Mitchell, Agle and Wood1997). Similar stakeholder demands are not interpreted as equally salient across firms (Durand et al., Reference Durand, Hawn and Ioannou2019). Accordingly, we argue that different managers perceive the same stakeholder demands as more or less salient, and such perception of stakeholder salience influences their decoupling decisions.

Consistent with this logic, firms are less likely to take the decoupling response to the conflicting demands when the CEOs perceive government demands as more salient or when the CEOs assess investor claims as less salient. Below, we expect that the relationship between the conflicting demands and the decoupling response is weaker for firms with CEOs who have a communist ideology and for firms with CEOs who have fewer career concerns.

CEO Communist Ideology and Perceived Salience of Government Claims

CEOs with a communist ideology are more sensitive to government demands.[Footnote 6] Communist ideology presents the CP's beliefs and values that advocate a Marxist–Leninist doctrine. Individuals who joined the CP tend to have a communist ideology (e.g., Marquis & Qiao, Reference Marquis and Qiao2019; Wang et al., Reference Wang, Du and Marquis2019). People who attained CP membership must undergo a rigorous socialization process of learning the CP's beliefs, tenets, and values (Higgins, Reference Higgins2005; Li, Meng, Wang, & Zhou, Reference Li, Meng, Wang and Zhou2008). Particularly in China, to promote communist ideology (‘dang xing’ or ‘party spirit’), the CP stipulates that becoming a CP member requires numerous training and selection processes, which take at least three years. For example, the candidates must regularly submit handwritten reports to show loyalty to the CP, pass a selection test that is mainly about the CP's communist doctrines, attend classes to foster communist beliefs, and engage in organized activities to extol communist principles (Bian, Shu, & Logan, Reference Bian, Shu and Logan2001; Li et al., Reference Li, Meng, Wang and Zhou2008; Marquis & Qiao, Reference Marquis and Qiao2019). Finally, after the CP leaders evaluate and examine the candidates’ loyalty to the CP and their communist beliefs, these candidates must take an oath to state they are ready to sacrifice everything for the CP and fight for the communist cause during their whole lives. To further improve the loyalty of party members, the CP stipulates that party organizations should regularly host collective training programs for their formal members. Consequently, CP members tend to have a communist ideology after the intensive socialization process mentioned above.

As an ideology advocates a specific set of assumptions, ideology functions as an important filter to shape how individuals process information and thus influence individuals’ decisions and behaviors (Wang et al., Reference Wang, Du and Marquis2019). An ideology can influence individuals to filter out information that is not consistent with what it justifies and to make choices that are consistent with its assumptions (Chin, Hambrick, & Treviño, Reference Chin, Hambrick and Treviño2013). For instance, US studies find that CEOs with liberal political ideology (e.g., Democrats) compared with the conservative political ideology (e.g., Republicans) can influence their firms to take strategies consistent with their liberal values, such as risk-taking strategy (Christensen, Dhaliwal, Boivie, & Graffin, Reference Christensen, Dhaliwal, Boivie and Graffin2015) and CSR initiatives (Chin et al., Reference Chin, Hambrick and Treviño2013).

Similarly, the communist ideology has a great influence on members’ decision making. Studies show that individuals with a communist ideology likely make decisions consistent with the CP's interests and values. For example, Dickson (Reference Dickson2007) find that entrepreneurs with a communist ideology tend to hire workers who are CP members. Chizema, Liu, Lu, and Gao, (Reference Chizema, Liu, Lu and Gao2015) reveal that the board of directors who share the CP's values promote the CP's interests when making decisions on CEO pay. Recently, Marquis and Qiao (Reference Marquis and Qiao2019) find that entrepreneurs with a communist ideology imprint are less likely to influence their firms to take internationalization strategies, which are not consistent with CP's anti-capitalism stand.

We thus expect that CEOs with a communist ideology may perceive government demands as more salient (Mitchell et al., Reference Mitchell, Agle and Wood1997), particularly in countries ruled by the CP, such as China, Vietnam, and Cuba. China is an authoritarian regime ruled by the CP, which has taken power since 1949 and entirely control the government's affairs and bureaucratic system. Hence, the claims from governments often mean the CP's claims. As mentioned, managers with a communist ideology tend to make decisions consistent with what the CP advocates. As a result, faced with the conflicting pressures from governments and investors, the more urgent task for CEOs with a communist ideology is to meet government demands through their firms’ philanthropic giving to demonstrate their loyalty to the CP and the state. Therefore, CEOs with a communist ideology are less likely to influence their firms to decouple from government demands when dealing with the conflicting demands.

Hypothesis 3: The positive interaction effect between public budget deficit and earnings pressure on firms’ decoupling of philanthropic giving will be weaker for firms with CEOs who have a communist ideology than firms with CEOs who do not have a communist ideology.

CEO Career Concern and Perceived Salience of Investor Claims

Previous studies suggest that CEOs who are close to retirement and who are also the chairmen of the board have fewer career concerns (Krause, Semadeni, & Cannella Jr, Reference Krause, Semadeni and Cannella2014; Yuan, Tian, Lu, & Yu, Reference Yuan, Tian, Lu and Yu2017).

CEOs who are close to retirement may perceive investor claims as less urgent for two reasons. First, such CEOs have less motivations to prove their high ability in the market because their current positions are likely to be the last positions (Yuan et al., Reference Yuan, Tian, Lu and Yu2017). Such CEOs are less likely to make major investments and pursue economic profits for firms (Ortiz-de-Mandojana, Bansal, & Aragón-Correa, Reference Ortiz-de-Mandojana, Bansal and Aragón-Correa2019). Second, they are less likely to be fired than younger CEOs following poor firm performance (Jensen & Murphy, Reference Jensen and Murphy1990; Parrino, Reference Parrino1997) given that they have an advantage from earlier performance and achievements (Lausten, Reference Lausten2002). Hence, they are less likely to be punished when they delay in paying attention to investor expectations.

As a result, the salience of investors likely decreases in the views of CEOs who are close to retirement (Mitchell et al., Reference Mitchell, Agle and Wood1997). Subsequently, firms with such CEOs may experience the conflicts from governments and investors to a less extent. That is, such CEOs perceive less disapproval from investors when their firms engage in philanthropic giving in response to government demands. Faced with the conflicting pressures, they may influence their firms to pay less attention to investor claims (i.e., earnings pressure) and then are less necessary to decouple from government demands.

Hypothesis 4a: The positive interaction effect between public budget deficit and earnings pressure on firms’ decoupling of philanthropic giving will be weaker for firms with CEOs who are close to retirement than firms with CEOs who are far from retirement.

Similarly, CEOs who also hold chair positions may perceive investor claims as less urgent. Board of directors is responsible for monitoring and evaluating CEOs (Fama & Jensen, Reference Fama and Jensen1983). CEOs are likely to be dismissed by the board following poor financial performance. CEOs who are also the chairmen of the board of directors are likely to hold strong power over the board (Finkelstein, Reference Finkelstein1992) and thus are better able to be insulated from replacement following poor performance (Krause et al., Reference Krause, Semadeni and Cannella2014). For example, Cannella and Lubatkin (Reference Cannella and Lubatkin1993) demonstrate that CEO duality prevents the selection of outside successors. Pi and Lowe (Reference Pi and Lowe2011) show that CEO duality increases CEO power and protects CEOs from involuntary replacement in Chinese firms. Hence, such CEOs are less likely to be punished by the board when they delay in paying attention to investor claims.

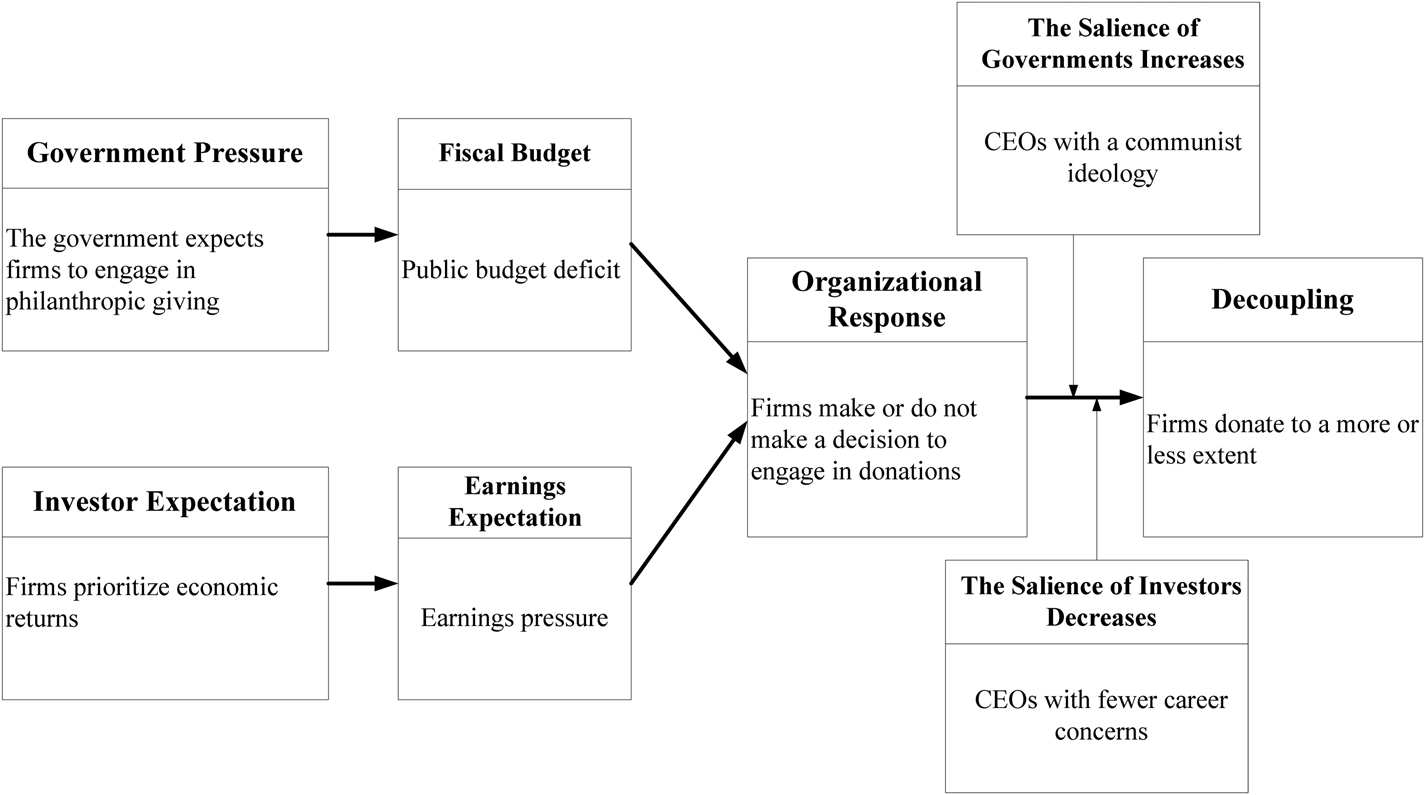

We thus expect that such CEOs experience the conflicts that arise from governments and investors in a less extent because the salience of investors decreases. Faced with such conflicting pressures, they may influence their firms to pay less attention to investor expectations (i.e., earnings pressure) and then the firms are less necessary to decouple from government demands. Figure 1 summarizes the stakeholder framework that we develop. We summarized the literature review for the development of our key theoretical concepts in Appendix I and II.

Hypothesis 4b: The positive interaction effect between public budget deficit and earnings pressure on firms’ decoupling of philanthropic giving will be weaker for firms with CEOs who are also the chairmen of the board than firms with CEOs who are not the chairmen.

Figure 1. A stakeholder framework that examines how firms engage in philanthropic giving to respond to conflicting stakeholder pressures

METHODS

Data and Sample

This article covers all Chinese firms (A shares) listed on the Shanghai or Shenzhen Stock Exchanges from 2006 to 2015. Data sources include the China Stock Market and Accounting Research (CSMAR) database, company annual reports, official websites of the government Finance Bureau (OWGFB), and the Chinese Statistics Bureau (CSB). CSMAR is widely used to study Chinese stock markets and listed firms (e.g., Sun, Hu, & Hillman, Reference Sun, Hu and Hillman2016; Zhang et al., Reference Zhang, Marquis and Qiao2016). Thus, we collected information on firms’ earnings pressure from CSMAR's Analyst Forecasts database and obtained information on the CEO's CP membership from CSMAR's Personal Characteristic database.

We manually collected the public budget on expenditure and revenue of all provinces from the OWGFB's government budget reports. A government's public budget expenditures include expenditure for public security and national defense, education, science, culture, health, sports, social security and employment, environmental protection, urban and rural communities, natural disasters, assistance to other regions, and other public programs. Public budget information dates back to 2006. At the beginning of every year (around February), all local governments in China disclose the financial budget reports of their provinces and cities through the Finance Bureau.

Similar to Zhang et al. (Reference Zhang, Marquis and Qiao2016), we collected philanthropy information from the notes in financial reports (termed as ‘corporate (charitable) donations’). The People's Republic of China Public Welfare Donation Law and Accounting Standards for Business Enterprises stipulate that corporate donations refer to public welfare and relief donations. Public welfare donations include donations for (a) poverty alleviation; (b) education, science, culture, health, and sports; (c) environmental protection and construction of social public facilities; and (d) other public programs that promote social development and progress. Relief donations include donations to natural disasters, vulnerable groups, and poor regions.[Footnote 7] Hence, corporate charitable donations assist provincial governments in providing public services or goods.

In addition, the provincial-level development information is obtained from the CSB. We manually collected information on firm celebrity from Fortune's official Chinese website by Baidu (Pfarrer et al., Reference Pfarrer, Pollock and Rindova2010). We obtained other firm-level information from the CSMAR. After merging these data and removing observations with unavailable data, we obtained a sample of 8,857 firm-year observations pertaining to 2,136 unique firms.[Footnote 8] Among these firms, 1,812 unique firms engage in charitable donations pertaining to 6,371 firm-year observations.

Dependent variables

Given that our theoretical framework is to examine whether and at what level a firm makes donations, we constructed two dependent variables. Following previous research (e.g., Wang et al., Reference Wang, Choi and Li2008; Zhang et al., Reference Zhang, Marquis and Qiao2016), we first employed likelihood of donation to predict the likelihood of a firm makes donations. Specifically, the variable equals 1 if a firm donates in a given year and 0 otherwise. Second, we gauged amount of donation by the logarithm of a firm's total donation in a specific year (e.g., Wang & Qian, Reference Wang and Qian2011).

In addition, we used a third dependent variable to directly test H2, H3, H4a, and H4b by constructing a decoupling response. The decoupling of a certain practice means the low extent of implementation (Westphal & Zajac, Reference Westphal and Zajac2001: 207). Marquis and Qian (Reference Marquis and Qian2013) show that decoupling occurs when a firm's extent of CSR implementation is lower than other firms that have issued CSR reports. Luo et al. (Reference Luo, Wang and Zhang2017) coded decoupling as 1 if firms issue CSR reports early and the extent of CSR implementation is lower than the average of all firms in a given year and 0 otherwise. Following these studies, we measured decoupling as 1 if (i) a firm makes charitable donations and (ii) the amount of donation is below the mean of all firms in a given year; otherwise it is 0.

Independent variables

Because firms located in provinces with large public budget deficits are vulnerable to government demands for philanthropy, public budget deficit is a continuous variable that equals the public expenditure budget minus the public revenue budget.

Based on Zhang and Gimeno (Reference Zhang and Gimeno2010), we measured earnings pressure as the difference between analysts’ earnings forecasts for year t and firms’ expectations from potential earnings for year t. Analysts’ earnings forecasts equals the average of earnings per share (EPS) among all analysts multiplied by the total number of shares and then divided by total assets. Different from US investors who can rely on EPS to estimate firm financial performance (Skinner & Sloan, Reference Skinner and Sloan2002; Zhang & Gimeno, Reference Zhang and Gimeno2010), China's managers have incentives to manipulate EPS and return on equity (Jiang & Wang, Reference Jiang and Wang2008). Return on assets (ROA) is widely used to help investors predict firm financial performance (e.g., Wang et al., Reference Wang, Choi and Li2008). Corporate performance expectations equal the average ROA from years t-1 to t-3. Specifically, earnings pressure is calculated using the following formula, where i refers to the firm, and t is time.

$${\rm Earnings\ pressur}{\rm e}_{{\rm it}}{\rm}={\rm } \displaystyle{{{\rm EP}{\rm S}_{{\rm it}}{\rm {^\ast}Total\ shar}{\rm e}_{{\rm it}}} \over {{\rm Total\ asset}{\rm s}_{{\rm it}}}}{\rm -}\displaystyle{{{\rm RO}{\rm A}_{{\rm i,t-1}}{\rm}+{\rm RO}{\rm A}_{{\rm i,t-2}}{\rm}+{\rm RO}{\rm A}_{{\rm i,t-3}}} \over {\rm 3}}$$

$${\rm Earnings\ pressur}{\rm e}_{{\rm it}}{\rm}={\rm } \displaystyle{{{\rm EP}{\rm S}_{{\rm it}}{\rm {^\ast}Total\ shar}{\rm e}_{{\rm it}}} \over {{\rm Total\ asset}{\rm s}_{{\rm it}}}}{\rm -}\displaystyle{{{\rm RO}{\rm A}_{{\rm i,t-1}}{\rm}+{\rm RO}{\rm A}_{{\rm i,t-2}}{\rm}+{\rm RO}{\rm A}_{{\rm i,t-3}}} \over {\rm 3}}$$Moderating variables

Chinese listed firms are required to disclose their executives’ biographical sketches (e.g., career history, education background, and CP membership) in their annual reports (Sun et al., Reference Sun, Hu and Hillman2016). To study the CEO's CP membership, we manually coded the membership of all the sample firms’ CEOs based on their biographical sketches. Based on previous studies (e.g., Marquis & Qiao, Reference Marquis and Qiao2019; Wang et al., Reference Wang, Du and Marquis2019), we measured communist ideology as a dummy variable that equals 1 if the CEO is a CP member and 0 otherwise.

Following Ortiz-de-Mandojana et al. (Reference Ortiz-de-Mandojana, Bansal and Aragón-Correa2019), we measured retirement as the number of years between the CEO's age and the stipulated retirement age. The smaller the value of this variable, the closer to retirement the CEO is. The State Council stipulates that the retirement age for males and females is 60 and 55, respectively. The State Council first issued the rules on retirement age in 1978,[Footnote 9] when private firms were completely banned (Wang et al., Reference Wang, Du and Marquis2019). Employees in state-owned firms and state organizations should retire upon reaching the stipulated age. Since Chairman Deng Xiaoping's Southern Tour of 1992, private firms have been playing an increasingly important role in China's economic growth. Legislative institutions and the State Council re-stated that the stipulated retirement age was applied for employees in all types of firms and state organizations in 2002 and 2008, respectively.[Footnote 10]CEO duality equals 1 if the CEO is also the chair of the board; otherwise, it equals 0.

Control variables

Considering firm attributes that may capture heightened scrutiny from the central government (Luo et al., Reference Luo, Wang and Zhang2017) and thus affect philanthropic giving, we controlled for several attributes. We first controlled for firms with political connections by CEOs’ political connection. A CEO is deemed to have political connections if s/he has prior or current political experiences (Sun et al., Reference Sun, Hu and Hillman2016). We coded the variable according to the political rank (national, provincial, city, county, and below county) in China, reflected as 5, 4, 3, 2, and 1, respectively; 0 represents that the CEO has no political connections. Second, private ownership equals 1 if the ultimate owner of the firm is a private shareholder and 0 otherwise. Third, firm size is the logarithm of total revenue.

In addition, we considered the pressure resulting from a firm's activities (e.g., its subsidiary) operating outside the province where the firm is located. Lee, Walker, and Zeng (Reference Lee, Walker and Zeng2017) indicate that firms receiving government subsidy may be exposed to the scrutiny of the governments that give subsidy to these firms and their subsidies. Thus, we controlled for government subsidy, measured as the total amount of government subsidy a firm receives divided by its total assets.

Moreover, we controlled for other firm-level characteristics that may influence a firm's decision to donate. Sales growth is defined as the ratio of annual increase in sales revenues. Because there is a complex relationship between corporate giving and firm financial performance (e.g., Wang et al., Reference Wang, Choi and Li2008), we controlled for a firm's ROA adjusted by industry. Slack is measured as firms’ cash flow over firms’ market capitalization. Firm age is the number of years since the firm was established. Certain research has argued that firms will use philanthropic giving to cover their previous wrongdoing (Godfrey, Reference Godfrey2005). Thus, we coded firm misconduct as 1 if CSMAR discloses firm misconduct such as misleading statements, material omissions, or manipulating stock price; it equals 0 otherwise. Further, we controlled for firm celebrity because celebrity firms tend to attract a huge amount of public attention (Pfarrer et al., Reference Pfarrer, Pollock and Rindova2010). Firm celebrity equals 1 if a firm (including its subsidiaries) is in Fortune Global 500 ranking list in a specified year and 0 otherwise. ST firm equals 1 if a firm's net income is below 0 for two consecutive years, and 0 otherwise. Control ownership measures the percentage of stocks held by the largest shareholder. Blockholders may perceive large charitable donations as excessive and unnecessary (Bartkus, Morris, & Seifert, Reference Bartkus, Morris and Seifert2002). Internationally active firms are considered less dependent on local governments and are less likely to make donations to establish firm–government relationships. We measured a firm's internationalization as the ratio of the firm's overseas sales to its total sales (Du & Luo, Reference Du and Luo2016).

Several studies demonstrate that CEOs and boards play a significant role in determining corporate giving (e.g., Gautier & Pache, Reference Gautier and Pache2015; Werbel & Carter, Reference Werbel and Carter2002). A CEO affiliated with other corporate givers is likely to imitate other firms’ giving activities (Werbel & Carter, Reference Werbel and Carter2002). Therefore, we controlled for CEO network, which equals 1 if the CEO is appointed to other firms and 0 otherwise. CEO share is calculated as the percentage of shares owned by the CEO. Board independence is calculated as the ratio of the number of independent directors to board size. Female directors have a stronger incentive to engage in corporate giving than male directors (Gautier & Pache, Reference Gautier and Pache2015); thus, we controlled for female director, which is defined as the ratio of the number of female directors to board size.

Moreover, we included province development, which reflects a province's institutional development (Marquis & Qian, Reference Marquis and Qian2013). It equals the logarithm of the provincial GDP divided by the total population size. Practice diffusion literature suggests that firms may imitate the social practice of other firms in the same industry (Byun & Kim, Reference Byun and Kim2013). We thus added additional controls: average likelihood of donation in industry (ALD) and average amount of donation in industry (AAD). Last, we included the year, industry, and province dummy variables.

Estimation Method

We first applied random-effects logit regression to predict the likelihood of donation because it is a binary variable. We adopted the random-effects regression because our study focuses on between-firm variance (Greene, Reference Greene, Fried and Schmidt1993). In addition, some variables may remain constant across time (e.g., private ownership).

Selection bias may exist because our second independent variable – amount of donation – is contingent on a firm's decision to donate (Zhang et al., Reference Zhang, Marquis and Qiao2016). Following Zhang et al. (Reference Zhang, Marquis and Qiao2016), we employed the two-step Heckman model to estimate the amount of donation. The first stage of Heckman model is likelihood of donation as mentioned above. In the second stage, we adopted random-effects linear regression to estimate the amount of donation by using the sample of 6,371 firms that made donations and controlled for inverse Mill's ratio calculated from the first stage.

For the third dependent variable, we used decoupling to directly test H2, H3, H4a, and H4b. We also performed random-effects logit regression to predict decoupling.

We created the interaction term between public budget deficit and earnings pressure to test H2. According to our argument, the interaction effect should not be significantly negative when predicting the likelihood of donation, as firms facing government and investor pressures should still make donations to please governments. The interaction effect should be significantly negative when estimating the amount of donation. Moreover, the interaction effect should be significantly positive when conducting a direct decoupling test.

Consistent with previous research (e.g., Qian, Wang, Geng, & Yu, Reference Qian, Wang, Geng and Yu2017), we employed a split-sample analysis to test H3, H4a, and H4b. Specifically, we divided the entire sample into two subsamples based on communist ideology (or retirement or CEO duality) and then assessed whether the coefficients of the interaction term on decoupling differed in the subsamples. We lagged all explanatory variables by one year to alleviate potential endogeneity, except for public budget deficit. We winsorized the top and bottom 1% of all continuous variables to avoid the undue effect of outliers.

RESULTS

Table 1a presents the descriptive statistics and a correlation matrix for analyzing the likelihood of donation. Table 1b presents those for the amount of donation and decoupling. The VIF in all regressions ranged from 1.02 to 1.77, which is below the rule-of-thumb cutoff of 10, suggesting that multicollinearity is not a concern.

Table 1a. Descriptive statistics and correlations

Notes: * denotes statistical significant at 5% level, N = 8,857

Table 1b. Descriptive statistics and correlations

Notes: * denotes statistical significant at 5% level, N = 6,371

In Table 2, Models 1 to 3 present the results of the random-effects logit regressions predicting the likelihood of donation, which are the first stage of the two-step Heckman model. Model 1 represents a baseline model which includes only control variables. We added earnings pressure and public budget deficit in Model 2. In Model 3, we added the interaction term between earnings pressure and public budget deficit. Models 4 to 6 present the results of the random-effects regressions of estimating the amount of donation, which are the second stage of the two stage Heckman model. Model 4 represents a baseline model. Model 5 presents the results of earnings pressure and public budget deficit. Model 6 shows the results of our interaction term. Models 7 and 8 present the results of the baseline model and our interaction term to predict decoupling, respectively.

Table 2. The effects of the conflicting pressures on corporate giving (H1a, H1b, and H2)

Notes: Standard errors in parentheses. + p < 0.10, * p < 0.05, ** p < 0.01, *** p < 0.001. Year, industry, and province dummies are included in all models.

H1a assumes that firms in a province with large public budget deficits will make large donations. Public budget deficit is positively and significantly associated with the likelihood of donation (p < 0.001) in Models 2 and 3 of Table 2. In Models 5 and 6 of Table 2, public budget deficit has a significant and positive effect on the amount of donation. Thus, H1a receives a strong support. In addition, we argue that firms under earnings pressure are less likely to make donations. In Table 2, Models 2 and 3 demonstrate that earnings pressure is negatively and significantly associated with the likelihood of donation. Hence, H1b is supported.

H2 argues that firms facing earnings pressure and government pressure exhibit a decoupling response in philanthropic giving. Consistent with our prediction, the coefficient on the interaction term between public budget deficit and earnings pressure on likelihood of donation is not significantly negative in Model 3 (b = 3.69, p < 0.05) of Table 2, and Model 6 reveals that the effect of the interaction term on the amount of donation is negative and significant (b = -2.79, p < 0.01). For a direct test of decoupling, the interaction term is positive and significant in Model 8 (b = 5.64, p < 0.01). Hence, H2 is supported.

To shed further light on the interaction effect, we plotted the results from Model 8 of Table 2 to depict the likelihood of decoupling when earnings pressure ranges from low to high. Figure 2 shows that firms in provinces with large public budget deficits are less likely to decouple than their counterparts when earnings pressure is low; however, these firms are more likely to decouple as earnings pressure gradually increases.

Figure 2. The interaction effect of public budget deficit and earnings pressure on the decoupling of corporate giving

Table 3 presents models utilizing a split-sample analysis to test H3, H4a, and H4b. To test H3, we divided the entire sample into two subsamples based on communist ideology. The results are presented in Models 1 and 2 of Table 3 (one sample is communist ideology and the other is non-communist ideology). H3 posits that the interaction term between public budget deficit and earnings pressure on decoupling is weak for firms with CEOs who have a communist ideology. The coefficient of the interaction term on the decoupling is positive and significant in Model 2 (b = 7.22, p < 0.001), but is not significant in Model 1 (b = 1.84, p > 0.1). Hence, H3 receives support.

Table 3. The moderating effects on the relationship between the conflicting pressures and decoupling of corporate giving (H3, H4a, and H4b)

Notes: Standard errors in parentheses. + p < 0.10, * p < 0.05, ** p < 0.01, *** p < 0.001. Year, industry, and province dummies are included in all models.

To test H4a, we divided the entire sample into two subsamples based on the median of retirement. The results are presented in Models 3 and 4 of Table 3 (one sample is close to retirement and the other is far from retirement). H4a posits that the interaction term between public budget deficit and earnings pressure on decoupling is weaker for CEOs near to retirement than their counterparts. The coefficient of the interaction term on the decoupling is positive and significant in Model 4 (b = 7.74, p < 0.01), but is not significant in Model 3 (b = 3.04, p > 0.1). Hence, H4a is supported.

Similarly, Models 5 and 6 present the results of two subsamples based on whether the CEO is also the chair of the board (one sample is CEO duality and the other is non-CEO duality). H4b posits that the interaction term between public budget deficit and earnings pressure on decoupling is weak for CEOs who are also the chairmen of the board. The effect of the interaction term on the decoupling is positive and significant in Model 6 (b = 5.89, p < 0.01), but is not significant in Model 5 (b = 2.19, p > 0.1). Thus, H4b is supported.

Robustness Checks

We also performed quantities of supplementary analyses to check the robustness of our results. All the relevant results are consistent with our main results (available from the authors). First, given that fiscally constrained provinces may be those which are economically underdeveloped and institutionally weak in China, local firms may have strong incentives to show their goodwill to governments in exchange for legitimacy and policy resources. Thus, this positive relationship may be driven by regional institutional development. As mentioned, we have controlled provincial institutional development. Further, we ruled out such an alternative explanation by excluding those underdeveloped provinces.[Footnote 11]

Second, given that managers may manipulate earnings to avoid actual penalties from investors or the capital market when firm financial performance is low (Jiang & Wang, Reference Jiang and Wang2008), earnings-based measures may not be a reliable proxy for the extent to which Chinese firms meet investor objectives. To rule out this issue, we excluded samples with ROA below or within the 10th percentile.

Third, we excluded samples that may drive our results. First, we excluded observations in 2008 and 2010 because the Wenchuan and Yushu earthquakes occurred during those years. Second, given that some CEOs may apply for re-employ after retirement, we dropped the sample wherein CEO age is over the stipulated retirement age.[Footnote 12] Third, we excluded the sample that a CEO turnover occurs because the new CEO may exhibit different sensitivities to the competing demands.

Fourth, considering similar characteristics among firms within the same province, the firms may not be independent or identically distributed. We ran our analyses using robust standard errors clustered by province (Primo, Jacobsmeier, & Milyo, Reference Primo, Jacobsmeier and Milyo2007). Furthermore, given our panel data, we conducted our regression with robust standard errors clustered by firm (Petersen, Reference Petersen2009).

Fifth, we conducted several tests by changing the proxy for our key variables. First, we recalculated decoupling that equals 1 if (i) a firm makes charitable donations and (ii) the amount of donation is below the mean of all firms in a given year and industry; it equals 0 otherwise. Second, we remeasured the extent of philanthropy implementation by the logarithm of amount of donation divided by total revenues. Third, we remeasured communist ideology as whether the CEO is a leader of the CP because the leader always has a stronger communist ideology than a common member.

Last, our results may be driven by a potential reverse causality concern that firms with large donations may increase earnings pressure. To mitigate this issue, we used the propensity score matching (PSM) method to generate a sample of treatment group (i.e., firms with earnings pressure) and control group (i.e., firms without earnings pressure). We performed a one-to-one matching based on the propensity score, resulting in 1,801 pairs of treatment and control group.

DISCUSSION

In this study, we proposed a stakeholder framework to examine the influence of conflicting stakeholder pressures on corporate giving. Our emerging market context provides evidence to support our framework. We found that firms in provinces with large public budget deficits are likely to engage in philanthropic giving, which creates tension among firms under earnings pressure. Firms that experience such conflict exhibit a decoupling response in philanthropic giving. Furthermore, we identified that this relationship is contingent upon CEOs’ perceptions of the salience of stakeholders, which is weaker for firms with CEOs who have a communist ideology and for firms with CEOs who have fewer career concerns.

However, our findings do not indicate that government demands invariably conflict with investor expectations. Our findings suggest that government and investor stakeholders are in conflict only when firms face earnings pressure because firms under earnings pressure likely lack the ability to make donations. Such firms should focus on managing immediate economic challenges rather than investing in philanthropic giving. However, when earnings pressure is assessed as low or has eased, firms have the ability and the motivation to engage in philanthropic giving in response to government demands.

Theoretical Contributions

Our findings may offer contributions to research on stakeholder theory, decoupling, and corporate philanthropy. First, our study contributes to the stakeholder salience literature in terms of how stakeholder salience changes. This study first reveals that stakeholder attributes determine how a stakeholder moves from being latent to becoming more salient (Mitchell et al., Reference Mitchell, Agle and Wood1997). Our findings suggest that a government becomes a more salient stakeholder for firms to accommodate when it encounters public budget deficits (H1a). Public budget deficit influences the governments’ transformation from a latent stakeholder to a definitive stakeholder (Mitchell et al., Reference Mitchell, Agle and Wood1997). Similarly, earnings pressure makes investors more salient (H1b). Instead of treating firm – stakeholder relationships as static (e.g., Freeman, Reference Freeman1984), our study further reveals that the salience of a certain stakeholder is contingent upon managerial perceptions (H3, H4a, and H4b).

By examining how managerial perceptions of stakeholder salience influence their firms’ responses to competing stakeholder demands, our study further advances stakeholder management literature (e.g., Li et al., Reference Li, Xia and Zajac2018; Wang et al., Reference Wang, Wijen and Heugens2018). This literature strives to understand corporate responses to competing stakeholder demands and recognizes that firms are most responsive to stakeholders with high salience. However, this literature does not explain managerial perceptions or interpretations of the competing stakeholder claims. Our work advances the understanding of the micro-foundation of corporate responses based on stakeholder salience literature (Durand et al., Reference Durand, Hawn and Ioannou2019; Mitchell et al., Reference Mitchell, Agle and Wood1997). Our findings show that firms exhibit a decoupling response when the competing demands are all assessed as salient (H2). Moreover, our findings suggest that different managers perceive a certain stakeholder demand as more or less salient, and such perceived salience influences the decoupling response (H3, H4a, and H4b).

Second, our study advances decoupling literature by identifying the boundary conditions of decoupling responses to conflicting pressures. Recently, certain scholars have begun to pay attention to the relationship between conflicting stakeholder pressures and corporate decoupling response (Luo et al., Reference Luo, Wang and Zhang2017; Wang et al., Reference Wang, Wijen and Heugens2018). This literature has largely focused on organizational external environments (e.g., stakeholder pressures) (Greenwood et al., Reference Greenwood, Raynard, Kodeih, Micelotta and Lounsbury2011) and failed to consider the organizational interpretation of stakeholder pressures from an internal perspective (Durand et al., Reference Durand, Hawn and Ioannou2019). As a result, the literature has ignored when and why firms are less likely to adopt the decoupling response to accommodate the conflicting pressures. To fill this gap, we identify the contingent factors that affect the managerial interpretations of stakeholder pressures and weaken this relationship (H3, H4a, and H4b). In so doing, this study develops a more nuanced understanding of a firm's decision on when and how to respond to conflicting stakeholder demands.

Third, this study contributes to the literature on the antecedents of corporate philanthropy. Most research has examined the influence of single stakeholders such as governments (Lin et al., Reference Lin, Tan, Zhao and Karim2015; Zhang et al., Reference Zhang, Marquis and Qiao2016), media (Jeong & Kim, Reference Jeong and Kim2018), and communities (Marquis & Tilcsik, Reference Marquis and Tilcsik2016). Although certain studies have referred to multiple stakeholders, they still ‘consider stakeholders as a whole’ (Tang & Tang, Reference Tang and Tang2018: 645) and fail to recognize the potential conflicts among different stakeholder groups. Our study suggests that investor expectations on current earnings create tension with government demands for corporate giving (H1a and H1b).

Practical Implications

This study offers practical implications. First, our findings remind managers that stakeholder demands on corporate giving are not consistent. Although corporate giving improves relations with governments (H1a), managers should consider whether firms possess the ‘ability’ to be philanthropic (H1b), which can be determined by investor expectations.

Second, our study has implications for shareholders and corporate governance mechanisms by finding that some CEOs may not use the decoupling response to cope with the conflicting pressures. Corporate paralysis (Pache & Santos, Reference Pache and Santos2010) or ‘the failure of that corporate system’ occurs (Clarkson, Reference Clarkson1995: 110) if firms fail to resolve the conflicts among stakeholders. As for shareholders who normally value political connections (Li et al., Reference Li, Meng, Wang and Zhou2008; Li & Zhang, Reference Li and Zhang2007), they should give attention to CEOs with a communist ideology, who may attach more importance to government demands than investor claims when dealing with the conflicts between governments and investors (H3). In addition, corporate governance mechanisms (e.g., board of directors) should pay attention to the CEOs with fewer career concerns because they are less sensitive to the conflicts and may respond in a way that goes against firm expectations (H4a and H4b).

Generalizability, Limitations, and Future Research

This study has some limitations. First, our findings (H1a, H1b, and H2) may be informative for countries with powerful governments and weak institutions (e.g., India, Vietnam, Malaysia, and Thailand) because firms in these countries may see government deficit as an opportunity to seek firm – government relationships (Hornstein & Zhao, Reference Hornstein and Zhao2018). The findings of H3 can be valuable to countries in Asia (e.g., China, Vietnam, and North Korea) and Eastern Europe (e.g., Lithuania, Ukraine, and Russia) that is or was ruled by the CP (Wang et al., Reference Wang, Du and Marquis2019).

However, the nature of our context (i.e., China) may limit the generalizability of the results to developed markets. We must exercise caution in generalizing our findings across national contexts. The wide range of regions in our sample partly overcomes this limitation. China's provinces vary significantly in market development (e.g., the development of Beijing and Shanghai are more market-oriented than Gansu and Ningxia), thus providing ‘a pseudo–cross-country test' of how public budget deficits affect corporate giving (Chen, Li, Luo, & Zhang, Reference Chen, Li, Luo and Zhang2017: 73). To extend our understanding, future research should examine our conclusions in developed markets.

Second, although we demonstrated the importance of governments and investors as stakeholders in China, we may have neglected the impact of other stakeholders. Future research should give attention to the influence of creditors, employees, consumers, local communities, and auditors on Chinese firms’ social practices.

Third, we did not examine the internal heterogeneity of regional governments or investors. Future research should consider that different regional governments (investors) may hold various or competing demands on organizational practices. Thus, a comprehensive stakeholder model should be developed to examine complex demands and claims among and within stakeholder groups. For instance, market development and legal environments across regions may moderate the relationship between public budget deficit and corporate philanthropy. In addition, dedicated and transient investors may exhibit different sensitivities to earnings pressure (Zhang & Gimeno, Reference Zhang and Gimeno2016), thus affecting the relationship between earnings pressure and corporate philanthropy.

Fourth, additional research is needed to investigate the relationship between conflicting stakeholder demands and other corporate social practices (e.g., CSR reports). Last, given that our study focuses on managerial perceptions of stakeholder claims, future research should consider firm-level contingent factors that affect how they experience conflicting stakeholder pressures and moderate the relationship between the conflicting pressures and the decoupling responses.

CONCLUSION

This study develops a stakeholder framework that examines the effect of conflicting demands from governments and investors on corporate giving. The results reveal that firms donate to respond to public budget deficits. This creates conflict with firms under earnings pressure. Firms exhibit a decoupling response in philanthropic giving when such conflicting demands are all perceived as salient. Moreover, we identify the boundary conditions of the relationship between the conflicting pressures and the decoupling response, which is largely ignored in previous decoupling literature. The results further indicate that the relationship is weak for CEOs who perceive government demands as more salient or assess investor claims as less salient. Our study thus contributes to a more nuanced understanding of firms’ responses to conflicting stakeholder pressures.

APPENDIX I

References for the Development of the Key Theoretical Concepts in Our Stakeholder Model

APPENDIX II

Empirical references for the Key Theoretical Concepts in Our Stakeholder Model