I Introduction

There has been a long-standing debate whether China will assimilate into the global economic governance system built and shaped by Western countries, or whether it will challenge the system and impose its own rules on other countries. However, despite China’s phenomenal economic and political rise, it is still an open question as to whether and how China will reshape the current global economic governance system. In this respect, G. John Ikenberry pointedly asked already more than ten years ago: “Will China overthrow the existing order or become part of it?” (Ikenberry, Reference Ikenberry2008). This question refers to the debate between realists and liberal institutionalists about the effects of the power transition from Organization for Economic Co-operation and Development (OECD) member countries to emerging economies. From a realist perspective, one would expect that China will try to establish its own rules and organizations to better pursue its interests, thus challenging the current order set up by OECD countries. In contrast, Ikenberry argues from a liberal institutionalist perspective that it is more likely that China and other emerging economies will remain part of the current order, which he describes as “hard to overturn and easy to join” (Ikenberry, Reference Ikenberry2008). According to this perspective, China’s policies and approaches will converge with the established rules of the game.

Another useful conceptualization of China’s role in global economic governance in general and the international investment system in particular distinguished three possible roles it can pursue: rule-taker, rule-maker, or rule-breaker (Chin, Reference Chin, Eric and Jonathan2014; Wang, Reference Wang2017). While the two first categories would be in line with liberal institutionalist perspectives, the third one would be in line with the view that China challenges the existing status quo. Broadly speaking, we can observe all three positions being adopted in the ongoing transformation of the international investment regime (Bonnitcha et al., Reference Bonnitcha, Poulsen and Waibel2017). Some countries, in particular capital-exporting countries such as the US and the EU, are developing new model international investment agreements (IIAs) to better balance investor protection and host state regulatory space. Brazil, on the other hand, developed its own distinctive model of Cooperation and Facilitation Investment Agreements (CFIA) (Badin and Morosini, Reference Badin, Morosini, Badin and Morosini2017). They clearly assume the role of a rule-maker. Other countries follow these new rules and templates and assume the role of rule-takers. And then there are countries such as Venezuela, South Africa, or India that exit important segments of the international investment regime through the termination of IIAs or the exit from the World Bank’s International Centre for Settlement of Investment Disputes (ICSID).

This contribution will investigate whether China assumes the role of a rule-taker, acts as a rule-maker, or even breaks with the system. This question has been investigated in other realms of global economic governance, such as world trade or international monetary relations (Chin, Reference Chin, Eric and Jonathan2014; Gao, Reference Gao and Deere-Birkbeck2011), but investigations in the area of global investment governance are scarce. This lack of research is especially worrying in light of the upheavals of the global investment governance system that is facing a deep legitimacy crisis (Waibel, Reference Waibel2010). Given its significant FDI flows and economic as well as political clout, a better understanding of China’s ideas for and potential role in the reform of global investment governance is important.

The next section will divide China’s international investment policy into four distinct generations of IIA arguing that China has not made attempts to break up the existing system. Rather China acted as a rule-taker by broadly accepting the templates of its treaty partners while sticking to a number of defensive lines. The next two sections will investigate China’s current international investment policy-making. Section III analyses the outcomes of the China-EU Comprehensive Agreement on Investment (CAI). I will argue that China accepted the template proposed by its negotiation partner although not to the full extent. Section IV shows that China is one of the key drivers of the development of an alternative set of multilateral rules on investment facilitation under negotiation at the WTO. In this section, I will argue that China has been a key promoter lending diplomatic support to move the investment facilitation agenda forward but did not appear as the main rule-maker. Section V will conclude.

II Four Generations of Chinese Investment Treaties

China started to embrace IIAs as a tool of economic diplomacy and the promotion of foreign direct investment (FDI) right after its decision to open up in the late 1970s and early 1980s. This section will distinguish between four generations of Chinese IIAs.Footnote 1

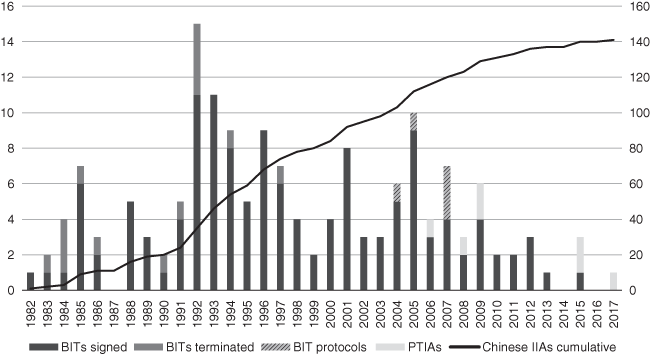

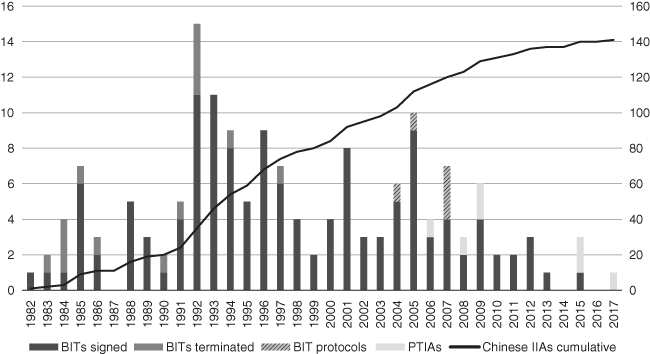

Since the early 1980s, China had signed a total of 150 bilateral investment treaties (BITs), of which 13 have been terminated upon the entry into force of a newly negotiated treaty. Only the treaty signed in 1994 with Indonesia has been unilaterally terminated in 2015. Five BITs negotiated in the 1980s and 1990s have been amended by a protocol in order to update their provisions. With a total of 114 treaties that are legally in force, China has the second-largest BIT network in the world, behind Germany with 129 BITs.Footnote 2 China also includes BIT-like investment chapters in its preferential trade agreements (Berger, Reference Berger, Broude, Busch and Porges2013). Since 2006, China has negotiated several preferential trade and investment agreements (PTIAs) with substantive investment provisions.

Figure 19.1 shows the development of Chinese IIAs signed since the early 1980s. During the 1980s, the growth of Chinese IIAs was rather slow with only a few treaties signed per year on average. Most of these treaties have been signed with European and Asian capital exporters. From the early 1990s onwards, China entered into an almost two-decade-long period of heightened treaty-making activity. In contrast to the 1980s, China signed most of its IIAs with developing countries during the 1990s. This trend to sign IIAs mainly with developing countries continued in the 2000s. During these years, China updated or amended a number of older treaties that it had signed with West European countries in the 1980s. Since the late 2000s, the number of newly negotiated treaties has declined substantially and China started to include more comprehensive investment rules in its PTIAs. Both trends are in line with the overall trends in the global investment regime.

Figure 19.1 Chinese IIAs signed per year and cumulatively, 1982–2017

To understand China’s motivations and preferences, it is important to focus both on the design of China’s IIAs and the characteristics of the partner countries. Based on these two characteristics it is possible to distinguish four phases of Chinese IIA policy-making (Berger, Reference Berger2015).

In the first two phases during the 1980s and 1990s, China negotiated IIAs that included the standard provisions of the so-called “European” investment treaty template such as fair and equitable treatment (FET), most-favored-nation (MFN), and clauses on expropriation. The notable feature of these early Chinese treaties was the restriction of the scope of investor-state dispute settlement (ISDS) provisions to claims regarding the amount of compensation in the case of expropriation. With regard to substantive provisions, China permitted the transfer of funds only in accordance with national law and was reluctant to include national treatment clauses. China’s approach in the 1980s can be interpreted as cautious learning from the investment treaty templates proposed by developed countries. As a result, the design of the IIAs China signed in the 1980s was specific to the partner country. While most of the key provisions remained largely unchanged, it is apparent that China’s treaty practice became much more coherent in the 1990s, which is a sign that it has started to use its own treaty template during negotiations.

Despite these slight differences in design, Chinese IIA negotiations in the 1980s and 1990s can best be distinguished according to the respective partner countries. The first generation of Chinese investment treaties was negotiated in the 1980s mainly with capital-exporting countries from Europe and Asia. The focus of China’s second-generation IIAs during the 1990s shifted to developing countries. This marked difference indicates that different political economy motivations explain the negotiation of Chinese treaties in the 1980s and the 1990s, respectively.

From the late 1990s onwards, China changed its legal practice by including comprehensive ISDS provisions and, depending on the partner country, broader national treatment provisions (Berger, Reference Berger and Zeng2011). The first treaty of this third generation was the BIT signed in 1997 with South Africa, which included for the first time a comprehensive ISDS provision. This shift in China’s treaty-making practice received high attention among legal scholars (e.g., Cai, Reference Cai2006; Gallagher and Shan, Reference Gallagher and Shan2009; Schill, Reference Schill2007; Shen, Reference Shen2010). While comprehensive ISDS provisions were included in almost all subsequent Chinese IIAs,Footnote 3 China’s approach towards granting national treatment to foreign investors was a more tailored one (Berger, Reference Berger and Zeng2011). Although China included national treatment provisions in almost all treaties signed in the third phase of its international investment policy, the exact wording of the national treatment clauses depended on the partner country: Chinese treaties signed with developing countries granted national treatment only subject to national law, limiting national treatment to a best-effort clause. In contrast, Chinese IIAs with developed countries featured national treatment clauses that were only restricted by the inclusion of an exemption for existing non-conforming measures and included a standstill commitment with regard to the adoption of new discriminatory measures. Interestingly, while the national law restriction in Chinese treaties signed with developing countries was a reciprocal provision, meaning that both contracting parties are allowed to discriminate against foreign investors in line with their respective national laws, the exemption of non-conforming measures in treaties with developed countries only applied to China. As a result, China was able to discriminate against foreign investors from the respective partner country in line with the legal framework in place at the entry into force of the treaty while Chinese investors enjoy full national treatment offered by the partner country (Berger, Reference Berger and Zeng2011).

In the fourth-generation IIAs that were signed in the late 2000s, China limited the scope of a number of treaty provisions in line with the global trend to rebalance investment treaties. This rebalancing was the result of a learning process about the effects of the increasing number of ISDS proceedings and at times the extensive interpretations of core substantive provisions like FET and indirect expropriation clauses by arbitration tribunals (Berger, Reference Berger2013). Because of this international trend of rebalancing, China started to negotiate treaties with countries that base their IIAs on the more extensive and nuanced North American model.

It is, however, puzzling to observe that while China was introducing balanced provisions in a number of treaties signed in the previous years, it was at the same time continuing to negotiate investment treaties that completely lacked balanced provisions. These treaties that were in line with the traditional European model were signed not only with European countries like Switzerland and Malta but also with many developing countries. Given the fact that MFN clauses can be used by investors to import more extensive treatment standards from other treaties their host state has signed with third countries (Schill, Reference Schill2009), the continuation of the signing of traditional IIAs contradicts the attempts to limit the scope of similar provisions in more balanced treaties signed with other countries. It has therefore become clear that China did not follow a coherent approach with regard to the rebalancing of investment treaties.

The notable aspect of the shift towards more balanced IIAs was that China followed a step-by-step approach towards the rebalancing of core IIA provisions and that this process is interlinked with the negotiation of investment rules in the context of preferential trade agreements in contrast to standalone investment treaties (Berger, Reference Berger2013). The PTIA signed in 2008 with New Zealand was the first Chinese treaty that included a broader range of balanced provisions such as an FET clause subject to customary international law and general exception clauses. China’s adoption of these novel features, however, varied from treaty to treaty. Later treaties, such as the investment treaty with Canada, include a broad range of more balanced substantive and procedural provisions.

The analysis of this section makes clear that throughout the 1980s, 1990s, and 2000s, China negotiated on the basis of the European model. The evolution of the contents of China’s IIAs during this time – and especially the policy shift towards more legalized and liberalized investment rules at the turn of the millennium – indicates that China’s IIA policy has been converging towards the IIA policies adopted by most capital exporters, in particular from Western Europe. Since the late 2000s, China’s IIA policy has become (at least partially) “NAFTA-ized,” as China has adopted a number of provisions that were invented by North American Free Trade Agreement (NAFTA) countries as a response to a number of ISDS cases. Besides concluding IIAs with the NAFTA countries Mexico (in 2008) and Canada (in 2012), China has negotiated with a number of countries that have been influenced by the NAFTA approach. In other words, innovative IIA policy models have diffused to China and to a large extent – although not completely, as argued above – substituted the European model as China’s main treaty template. This assessment is supported by the most recent decision of China to accept the model IIA text of the US and the EU as the basis for investment treaty negotiations (see next chapter).

Thus, despite the large number of IIAs and the growing role as an FDI host and source country, China has not used its new important role as a global economic powerhouse and major source and destination of FDI flows to redefine the rules of the game in the international investment regime. In fact, China has been swimming with the tide of international investment rule-making, aligning its policies with the approaches of OECD countries.

III Towards a Fifth Generation? The China-EU Comprehensive Agreement on Investment

A fifth generation of Chinese IIAs appeared on the horizon when Beijing entered into investment treaty negotiations with the US in 2008 and with Europe in 2013. It seemed that China was willing to give up on the last line of defense in comparison to US and EU-style IIAs and to commit to investment liberalization. In July 2013, China agreed to negotiate with the US on the basis of the US model treaty which includes the general commitment to open up its markets and schedule exceptions according to a negative list approach, that is only those sectors or measures are exempted that are explicitly recorded. As a result, China changed its regulatory system for foreign investments from a catalog approach, which divides sectors into encouraged, permitted, restricted, and prohibited categories, to a negative list approach that was first tested in a limited number of special free trade zones. In January 2020 a new Foreign Investment Law, which was in the making since 2015, entered into force and applies the negative list approach to the Chinese economy as a whole. Despite these changes to China’s regulatory system for inward FDI, the China-US investment treaty negotiations have petered out during the Trump administration. Instead, the Trump administration focused on the Phase One Trade Deal with China that covered investment to a limited extent only, for example by liberalizing market access for US financial services or by regulating forced technology transfers.

The commitment to adopt the US model as a template for a China-US investment agreement is also of high relevance for the negotiations between China and the EU. The CAI should not only update the existing 25 investment protection agreements between individual EU member states and China but also extend their coverage to the market access of European investors in China. The decision to negotiate a so-called “Comprehensive Agreement on Investment” between China and the EU dates back to the 15th China-EU Summit in February 2012. The 16th China-EU Summit in November 2013 agreed on the official launch of the negotiations that started with a first round of talks in January 2014. After a staggering 35 rounds of negotiations, China and the EU agreed in principle on the CAI on December 30, 2020. The fate of the CAI, however, is uncertain in light of the recent worsening of diplomatic relations between China and the EU. As a result of the EU’s decision to impose sanctions on four Chinese officials over human rights abuses against the Muslim Uyghur minority in the Xinjiang region, China imposed sanctions on several European politicians and individuals. In turn, the European Parliament decided to freeze the ratification process of the CAI. These recent developments make it unlikely that the CAI will enter into force in the near future.

A key milestone in the negotiations was the agreement between China and the EU in January 2016 that the CAI should be ambitious and comprehensive, meaning that the envisaged treaty should go beyond the scope of the existing BITs between China and the member states.Footnote 4 This important decision shows that the EU aimed at an agreement with China that should at least be on par with the BIT under negotiation between China and the US that intended to cover both pre-establishment and post-establishment investment protection. In addition to post-establishment protection provisions that should be updated in order to create a better balance between investor protection and host states’ right to regulate, the CAI would also address issues of market access and the right of establishment. Furthermore, the CAI should improve the regulatory environment such as transparency, licensing, and authorization procedures. In addition, the agreement should include environmental and labor provisions.Footnote 5 Last but not the least, the ISDS provisions of the old 25 BITs signed between China and EU member states, from the perspective of the EU, should be replaced by the EU’s new investment court system. In sum, the negotiating agenda between China and the EU was highly complex and comprehensive and in a number of key issues, such as market access, sustainability issues, and dispute settlement, China’s interests diverge substantially from those of the EU (Li et al., Reference Li, Qi and Bian2019).

From an EU perspective, the main objective of a China-EU CAI was to improve and guarantee access of European investors to the Chinese market thus achieving reciprocity in light of the market access European countries already grant to Chinese investors. Technically speaking, the CAI should include national and most-favored-nation treatment provisions that apply to the pre-establishment and post-establishment phases. The actual liberalization should take place on the basis of a negative list approach. Apart from these modalities, there is the important question of how extensive the negative list should be. While China implemented a negative list approach domestically, it appears to be in favor of a cautious and circumscribed approach in contrast to the EU that favors an ambitious opening up of the Chinese market for foreign investors (Bickenbach and Liu, Reference Bickenbach and Liu2015). The CAI should, in addition, include restrictions on the use of performance requirements and include transparency obligations with regard to the operation of SOEs.

The difficult ratification process of the CAI notwithstanding, the agreement text provides insight into the current negotiation strategies and substantive preferences of China. The CAI is a peculiar investment agreement, one that mainly seems to address those issues that are of importance to the EU. In view of the fact that Europe is already open to Chinese investors – additional market opening is thus expected from China – EU preferences are mostly centered around issues of market access, the regulatory environment, and sustainable development. These are the issues that are at the core of the CAI text that includes three main chapters.Footnote 6 The first substantive section focuses on investment liberalization where both parties commit to national and most-favored-nation treatment in the pre-establishment phase subject to reservations on non-conforming measures. China commits to opening up its markets in some sectors, including electric cars, private hospitals in Tier-1 cities, cloud services, and computer reservation systems.Footnote 7 Despite this rather limited additional market access, it seems that most market access commitments of China in the CAI merely lock in those reforms that China has already undertaken unilaterally (Poulsen, Reference Poulsen2021). Arguably, preventing the revocation of economic reforms in China is an important achievement in and by itself. Securing market access and locking-in reforms may be important outcomes, but they are unlikely to substantially increase two-way investment flows.

The second substantive section deals with the regulatory environment for foreign investments. This section of the CAI includes provisions that prohibit forced technology transfers and joint venture requirements. These provisions of the CAI appear more comprehensive than what China agreed to in its WTO accession protocol or in the Phase One Trade Deal with the US.Footnote 8 In addition to technology transfer requirements imposed by the state, China and the EU also commit not to “directly or indirectly require, force, pressure or otherwise interfere with the transfer or licensing of technology between natural persons and enterprises”. Furthermore, the CAI includes a number of level-playing-field provisions that may improve the transparency of subsidies, enhance procedural transparency, predictability, and fairness of regulatory and administrative procedures, and regulate the operations of state-owned enterprises.

The third main section of the CAI includes provisions on sustainable development. While sustainable development sections are a common feature of EU trade agreements, the CAI is China’s first agreement with such a comprehensive section. As the CAI offers the EU much less leverage compared to a fully fledged free trade agreement (FTA), the inclusion of such a comprehensive section on sustainable development is a success. But the obligations under this section are mainly based on the parties’ existing commitments under other international environmental and labor treaties. Moreover, the wording of several key provisions characterizes such obligations as “best-effort” in nature (Berger and Chi, Reference Berger and Chi2021).

The outcomes of the CAI do not address all the initial negotiation objectives of the EU. The CAI does not include sections on investment protection and investment dispute settlement. The EU’s insistence to replace ISDS with an Investment Court System, as well as the ongoing multilateral discussions on reform of ISDS, could explain this omission. While the parties will continue negotiating the sections on investment protection and ISDS and “endeavour” to conclude them within two years after the signature of the CAI, the 25 BITs with outdated ISDS rules between EU members and China remain in force and could possibly lead to unwanted ISDS claims for the time being. The CAI is thus stuck halfway in the development of China-EU bilateral investment relations. While it addresses important issues of market access, regulatory cooperation, and sustainable development, it does not replace the old BITs, nor contribute to the overall reform of the international investment regime. Both parties agreed to use the next two years to remedy this omission (Berger and Chi, Reference Berger and Chi2021).

The CAI negotiation process reveals that China is willing to negotiate on the basis of treaty templates put forward by its partner countries. The key sections on market access, regulatory frameworks, and sustainable development are clearly revealing the preferences of the EU rather than China. In the case of the CAI, the section on market access offers the best insight into China’s negotiation strategy. China agreed to negotiate on the basis of the negative list approach favored by the US and Europe and initiated a domestic reform program that introduced this new regulatory approach first in a handful of pilot free trade zones before scaling it up to the entire economy and enshrining the principle in a new foreign investment law. The question, however, remains how extensive China’s commitment to opening up its markets is. The outcomes of the CAI suggest that China is mainly agreeing to lock in existing unilateral reforms and only to a limited extent to additional market access. While China can still be described as a rule-taker, adopting the templates of its treaty partners, this assessment needs to be marked with an Asterix as China accepts only those treaty commitments that are clearly in line with its domestic preferences.

IV Thinking Outside the Box: From Investment Protection to Facilitation

Traditional models of international investment governance, in particular rules on investment protection, liberalization, and ISDS enshrined in IIAs, are increasingly criticized as one-sided, illegitimate, and ineffective. One important alternative avenue countries, and in particular developing countries, have pursued in recent years is the negotiation of investment facilitation agreements. Investment facilitation can be understood as a set of practical measures concerned with improving the transparency and predictability of investment frameworks, streamlining procedures related to foreign investors, and enhancing coordination and cooperation between stakeholders, such as the host- and home-country governments, foreign investors, domestic corporations, and societal actors. The main forum for negotiations on investment facilitation is the WTO where over 100 Members are negotiating an Investment Facilitation for Development (IFD) Agreement.Footnote 9 Furthermore, investment facilitation is becoming an integral part of regional as well as bilateral agreements or non-binding protocols (Schacherer, Reference Schacherer2021).

China played an influential role in advancing the international agenda on investment facilitation. The concept was proposed by a group of experts in 2015 (Sauvant and Hamdani, Reference Sauvant and Hamdani2015) and practiced by Brazil since 2015 in the so-called Cooperation and Facilitation Investment Agreements (CFIA) (Badin and Morosini, Reference Badin, Morosini, Badin and Morosini2017). China played a critical role in placing the idea of investment facilitation at the center of the reform debate on international investment governance during the Chinese G20 presidency in 2016 (Sauvant, Reference Sauvant and Chaisse2019). Discussions on investment facilitation were initiated during the Chinese G20 presidency and trade ministers welcomed “efforts to promote and facilitate international investment to boost economic growth and sustainable development”.Footnote 10 Furthermore, the G20 encouraged international organizations such as “UNCTAD, the World Bank, the OECD and the WTO to advance this work within their respective mandates and work programmes, which could be useful for future consideration by the G20”.Footnote 11 Discussions within the G20 were continued during the German G20 presidency within the Trade and Investment Working Group. The German chair put forward a non-binding investment facilitation package which reaffirmed the Guiding Principles for Global Investment Policymaking adopted at the G20 Hangzhou Summit in 2016 and which stated that investment policy frameworks should be transparent, efficient, predictable, and consistent (Berger and Evenett, Reference Berger and Evenett2018). China was one of the G20 Members that promoted the package to lay the foundation for the initiation of talks on investment facilitation under the auspices of the WTO. While the investment facilitation packages were blocked by the US, South Africa, and India, a group of developing countries, led by China and Brazil nevertheless succeeded in launching so-called structured discussions on investment facilitation for development at the WTO 11th Ministerial conference in December 2017.

China is a key promoter of investment facilitation negotiations in the WTO. China submitted a proposal that suggests three elements of a framework for investment facilitation including measures to increase transparency, and enhance the efficiency of administrative procedures and options for responding to developing and least-developed members’ needs.Footnote 12 At the same time, China joined a group of emerging and developing country members, the so-called “Friends of Investment Facilitation for Development” (FIFD), to propose an informal WTO dialogue on investment facilitation for development.Footnote 13 As the coordinator, China is the leading member of the FIFD group. At the 11th Ministerial Conference of the WTO in Buenos Aires, Argentina, China was among a group of 70 WTO members that signed a Joint Ministerial Statement calling for the start of Structured Discussions with the aim of developing a multilateral framework on investment facilitation. A second Ministerial Statement on investment facilitation was submitted by 98 WTO members during a trade ministers’ conference hosted by China in Shanghai.Footnote 14

China participated actively in the structured discussions and negotiations on investment facilitation in the WTO. It submitted another proposal on the entry and temporary stay of business persons for investment purposes. Its role, however, should be characterized more as a facilitator of the negotiation process rather than as a rule-maker similar to the role Brazil played which not only invented the model for bilateral CFIAs but also submitted the first comprehensive agreement text in the WTO negotiationsFootnote 15 and influenced its regional partners’ position on investment facilitation (Perez-Aznar and Choer Moraes, Reference Perez-Aznar and Choer Moraes2017). China’s role was nevertheless important to help the concept of investment facilitation, as an alternative to traditional approaches of investment protection and ISDS, achieve a breakthrough at the multilateral level given its role as a G20 chair, as a host of important trade ministers’ meetings or the coordinator of the FIFD group.

V Conclusion

This article assesses China’s role in the global investment regime asking whether it can be characterized as a rule-taker, a rule-maker, or rather as a rule-breaker. China has signed a total of 150 BITs since the early 1980s and is an active participant in multilateral fora such as the negotiations towards an IFD Agreement in the WTO. Despite this active involvement in the global investment regime and its significant economic and political clout, China seems to continue to pursue the role of a rule-taker. This passive role is visible in the contents of Chinese IIAs negotiated over four decades and does not seem to be contingent on the partner countries. The most recent and significant agreement negotiated by China, the CAI signed in principle with the EU, seems to be following a template that largely reflects the preferences of its partner. China, however, does not adopt the templates of its treaty partners unchecked. On the contrary, China seems to have a number of defensive positions, for example, comprehensive liberalization commitments, that characterize its treaty-making practice.

In addition to the negotiation of IIAs, China is also an active negotiation party in multilateral fora such as the WTO negotiations on investment facilitation. China did submit a limited number of proposals, which, however, are less comprehensive than those of other negotiating parties such as Brazil or the EU. Despite these proposals, China’s role in the IFD Agreement negotiations should be characterized not as a thought leader but as a key promoter of dialogue and negotiations. China used its chairmanship of the G20 in 2016 and hosted a trade ministers meeting in 2019 to promote discussions on investment facilitation. China, furthermore, is part of an informal group of WTO Members, the so-called Friends of Investment Facilitation for Development that assumes an important role to move the investment facilitation agenda in the WTO forward.

What are the implications of this assessment of China as being (still) a rule-taker? First, given its active participation in global investment policy-making, it is not acting as a rule-breaker and pursues its interest within the existing global investment governance system. To paraphrase the words of Ikenberry quoted in the introduction, China gradually becomes a part of the existing system and is not likely to attempt to overthrow it. Second, if an international agenda aligns with its interests, such as in the area of investment facilitation, China can be a very powerful promoter of international dialogue and negotiations. Thirdly, although China is willing to negotiate on its partner countries’ treaty templates, it does not indiscriminately accept all provisions and commitments put on the negotiation table by its partners. On the contrary, the changes in the design of Chinese IIAs seem to be conditioned by policy developments within China, as underlined by the CAI. While China seems to be comfortable with lock-in unilateral reforms, it does not seem to accept treaty provisions that would imply additional economic policy reforms at home. At least in this sense, China’s investment policy-making is not that different from that of other economic powers such as the US and the EU.

Open access

Open access