Introduction

The amount of public pension reflects, to a large extent, lifetime earnings (Betti et al., Reference Betti, Bettio, Georgiadis and Tinios2015), particularly in earnings-related pension systems such as those in Germany and Sweden. As the employment behaviour of women often overlaps with their family histories, women may be disadvantaged compared to men and accumulate only low pension entitlements of their own. Consequently, this puts women at higher risk of old-age poverty (Haitz, Reference Haitz2015; Klerby et al., Reference Klerby, Larsson, Palmer, Holzmann, Palmer, Palacios and Sacchi2020). Gender gaps in pensions illustrate these inequalities in biographies; although the gap has narrowed over the years, Germany still performed exceptionally poorly in 2019, with women's pensions being on average 36 per cent lower than men's pensions. Despite Sweden being considered a gender-equal society, women's pensions were also 28 per cent lower than men's in the same year (Eurostat, 2022a).

Differences in the pension entitlements of women and men have long been of less concern, as they were taken for granted as a result of the gendered division of work and family within couples in ‘male-breadwinner’ settings (Bonnet and Geraci, Reference Bonnet and Geraci2009). Hence, in most welfare states, marriage was considered an economically secure institution at retirement, as within a household, the wife's often lower pension income could be offset by the higher pension income of the ‘male-breadwinner’. Even in the case of the loss of a partner, women were usually protected from old-age poverty by the survivor's pension, calculated based on the deceased husband's previous pension income. Persistently high divorce rates during recent decades, however, have caused the rationale of that system to be called into question (Bonnet and Hourriez, Reference Bonnet and Hourriez2012). The loss of a partner through divorce is often not covered by social policy, although it entails similar economic consequences as the death of a partner. After divorce, neither being able to pool pension entitlements nor receiving a supplementary pension while solely depending on one's own pension entitlements puts women's economic wellbeing at risk.

This study analyses how divorce is related to the monthly public old-age pension income of women and men in two different welfare states, West Germany and Sweden. Research has shown that family biographies are related to income sources at retirement (McDonald and Robb, Reference McDonald and Robb2004) and associated poverty risks (Peeters and De Tavernier, Reference Peeters and De Tavernier2015), but most studies have been conducted for single countries. Only a few studies have investigated country differences (Evandrou et al., Reference Evandrou, Falkingham and Sefton2009; Fasang et al., Reference Fasang, Aisenbrey and Schomann2013; Kreyenfeld et al., Reference Kreyenfeld, Mika and Radenacker2018) and examined how welfare states impact the individual accumulation of pension entitlements (Uunk, Reference Uunk2004). By using public pension register data from Germany and Sweden for women and men who retired between 2013 and 2018, this study contributes to the literature on the economic security of divorcees in old age. The large sample sizes and precise longitudinal income information allow for comparisons of income histories across the lifecourse and robust estimates of monthly public old-age pension income by gender and family status.

In Sweden, the share of divorcees aged 65–69 increased from 16 to 22 per cent for women and from 14 to 19 per cent for men between 1999 and 2019 (SCB, 2000, 2020). In Germany, the share increased from 6 to 18 per cent and 4 to 12 per cent, respectively, from 1996 to 2018 (Mikrozensus, 1996, 2018). In both countries, therefore, a large proportion of individuals of retirement age have been divorced at least once in their lifetime. At the time of the emergence of ‘new social risks’ (Bonoli, Reference Bonoli2005), stemming from changes in the labour market and increasing family diversity, such as rising divorce rates, the Swedish and German welfare states started to follow different policy approaches (Lewis, Reference Lewis1992; Meyer, Reference Meyer2014). During the 1970s, Sweden adopted an approach of individual economic independence and has therefore long pursued policies that promote gender equality in the labour market, such as individual taxation and work–family reconciliation policies, thereby increasing individual employment irrespective of family status. In contrast, in West Germany, a family model characterised by a gender-specific division of labour for married couples was the norm and incentivised by tax and transfer policies (e.g. joint taxation, health insurance). This was accompanied by the introduction of the system of ‘divorce-splitting’ in 1977 to protect the economically ‘weaker part’ of a marriage in the event of divorce (Schmähl, Reference Schmähl2018). Under this system, the accumulated pension entitlements during marriage are divided equally between the ex-spouses upon divorce. Hence, while the Swedish welfare state combined different policies to enable women and men to achieve economic autonomy over the lifecourse, the West German welfare state took the imbalance between women's and men's incomes as given, and emphasis was placed on ‘equalisation payments’.

In this study, monthly public old-age pension income is defined as all entitlements that an individual receives as a result of previous employment, other pension qualifying periods, such as education, childcare or unemployment, and in the German case, the divorce-splitting mechanism. Drawing on large-scale pension register data, we address the question of how divorce is related to women's and men's economic wellbeing in old age in West Germany and Sweden. The main comparison groups are divorced and (re)married women and men, whereby family status is measured in the year of retirement (time constant). Comparatively analysing the pension incomes of divorced women and men in two different welfare states contributes to the discussion on the role of social policies throughout the lifecourse in shaping gender- and family status-dependent income histories and ensuring ‘pension adequacy’.

Lifecourse perspective, social policies and prior research

From a lifecourse perspective, pension entitlements can be seen as the late-life outcome of intersecting lifecourse developments within institutional settings (Elder et al., Reference Elder, Johnson, Crosnoe, Mortimer and Shanahan2003). A central assumption is that lifecourse transitions not only affect one domain of the lifecourse but can also impact other lifecourse domains. Divorce not only channels women and men into a different family trajectory (i.e. partnered to single) but can also shape their working trajectory, and vice versa. Welfare states, as institutional settings, further shape these trajectories as social policies structure the relationship between the labour market and the family (Lewis, Reference Lewis1992; DiPrete, Reference DiPrete2002). Therefore, social policies can play an important role throughout individual's working lives by shaping women's and men's accumulation of individual pension entitlements. Similarly, pension regulations can compensate for previous labour market or gender-related inequalities at retirement.

Interrelation between social policies and work–family trajectories

Lifetime earnings are strongly linked to labour market participation (Kail et al., Reference Kail, Quadagno, Keene, Bengtson, Silverstein, Putney and Gans2009). Women tend to have lower incomes than men, and they are also more often subject to interrupted careers due to family obligations, which impacts their career advancement and their total years in employment (Chłoń-Domińczak et al., Reference Chłoń-Domińczak, Góra, Kotowska, Magda, Ruzik-Sierdzińska, Strzelecki, Holzmann, Palmer, Palacios and Sacchi2020). Hence, gendered work–family lives are shown to be more detrimental for the pension income of women, as they often cannot build up adequate lifetime earnings (Sefton et al., Reference Sefton, Evandrou, Falkingham and Vlachantoni2011; Möhring and Weiland, Reference Möhring and Weiland2022), while men are usually less affected (Möhring, Reference Möhring2015). These path dependencies, following the intersection of work and family life, are stressed by the concept of cumulative (dis)advantage (Dannefer, Reference Dannefer2003). Negative events, such as periods outside employment (e.g. unemployment, care, illness), elevate the possibility of future disadvantages, e.g. re-entry into the labour market or lower earnings. This usually marks the onset of ‘ageing unequally’ (Organisation for Economic Co-operation and Development (OECD), 2017), as the inequality of such (dis)advantages often accumulates over time.

During working life, social policies that strengthen women's economic autonomy and help reconcile work–family life can mitigate the economic consequences of periods of absence from the labour market, such as during childrearing (McDonough et al., Reference McDonough, Worts, Booker, McMunn and Sacker2015). Individual taxation and childcare availability, for example, aim to support women in their roles as full-time workers. These policies are also believed to shelter women from the adverse effects of divorce, as women can then acquire their own income and not be solely dependent on their husbands (Lewis, Reference Lewis2001; DiPrete, Reference DiPrete2002). Policies to ensure gender equality within paid and unpaid work, however, vary by welfare regime (Möhring, Reference Möhring2016). In male-breadwinner settings, policies such as joint taxation schemes and other marriage benefits are in favour of supporting women as childcare providers, which can lower their time spent in paid work. As comparative studies have shown, the institutional context impacts the extent of gendered work–family lives and, thus, also the economic consequences following divorce (DiPrete, Reference DiPrete2002; Uunk, Reference Uunk2004; Andreß et al., Reference Andreß, Borgloh, Brockel, Giesselmann and Hummelsheim2006). Although social welfare and alimony can mitigate the economic consequences of divorce in the short term (Uunk, Reference Uunk2004), employment-related measures help women maintain their ties to the labour market, which increases their pension entitlements in the long term. Hence, institutional contexts shape the extent to which women and men are protected against negative consequences of lifecourse risks (DiPrete, Reference DiPrete2002).

Lifecourse events and transitions

A frequently overlooked event that can direct women and men into different working trajectories is divorce. As divorce mostly occurs at a time when women's and men's economic situation is already shaped by their previous work–family life arrangements (Statistisches Bundesamt, 2021; SCB, 2022), it often represents a turning point in an individual's lifecourse. In a cross-European study, Möhring (Reference Möhring2021) showed that each year of marriage decreased women's individual retirement income, whereas each year of divorce without repartnering increased it. For men, she found the reverse pattern. Similar results were shown for the US context, where being continuously married was found to increase the odds of receiving a private pension for men and lower the odds for women (Yabiku, Reference Yabiku2000). Family history therefore had opposite effects on women's and men's acquisition of pension entitlements. For women, gendered work–family lives during marriage are often assumed to be the underlying mechanism that increases the dependence on a male-breadwinner's pension in old age (Fasang et al., Reference Fasang, Aisenbrey and Schomann2013), while having to be self-reliant after divorce is associated with gains in women's individual pension income (Möhring, Reference Möhring2021). ‘Marriage premiums’ for men, however, are often discussed as being driven by selection (Killewald and Lundberg, Reference Killewald and Lundberg2017; Ludwig and Brüderl, Reference Ludwig and Brüderl2018).

Selection into marriage and divorce

Selection arguments state that it is not marriage itself that leads to higher pension incomes for men. Instead, the association is driven by the selection of individuals with different characteristics into specific family lifecourses. Men who have favourable traits (e.g. higher education, better earnings tracks) are also more likely to have so-called normative lifecourses, such as a stable marriage, which will be rewarded the most (e.g. higher pension incomes) (Jalovaara and Fasang, Reference Jalovaara and Fasang2020). Following the same argument, men who have unfavourable traits (e.g. lower education, unstable employment, illness) are more likely to ‘deviate’ from the normative lifecourse by becoming divorced or separated. This is supported by studies showing that men's wages were already falling prior to divorce (Killewald and Lundberg, Reference Killewald and Lundberg2017) and that unemployment (Solaz et al., Reference Solaz, Jalovaara, Kreyenfeld, Meggiolaro, Mortelmans and Pasteels2020), low education (Härkönen and Dronkers, Reference Härkönen and Dronkers2006) and poor health (Mortelmans, Reference Mortelmans, Schneider and Kreyenfeld2021) increase men's risk of becoming divorced. In this context, research on the intergenerational transmission of divorce must be mentioned (Diekmann and Schmidheiny, Reference Diekmann and Schmidheiny2013). This research also predicts unfavourable outcomes among children whose parents have divorced, e.g. on health and education (Devor et al., Reference Devor, Stewart and Dorius2018; Auersperg et al., Reference Auersperg, Vlasak, Ponocny and Barth2019), and a higher likelihood of such children eventually being divorced themselves (Bergvall and Stanfors, Reference Bergvall and Stanfors2022). Although selection arguments are commonly used for men, they also apply for women. Yet, the association is weaker and mixed, e.g. in the case of the link between unemployment and a higher risk of divorce (Solaz et al., Reference Solaz, Jalovaara, Kreyenfeld, Meggiolaro, Mortelmans and Pasteels2020). However, there are also studies showing that the event of divorce can lead to further penalties for men (Kalmijn, Reference Kalmijn2005), such as an increased risk of disability (Brüggmann, Reference Brüggmann, Kreyenfeld and Trappe2020), unemployment and/or downwards social mobility (Covizzi, Reference Covizzi2008). In the long run, both channels of work–family trajectories – a poorer earnings trajectory leading to divorce or divorce leading to an increased risk of adverse health effects and/or unemployment – can negatively impact the accumulation of lifetime earnings and thus the pension income for divorced men.

Work–family trajectories and pension regulations

Pension incomes are ‘lifecourse sensitive’ in terms of not only lifetime earnings but also pension regulations. In line with the welfare state context, pension regulations account for individual lifecourse developments by granting credits for (non)contribution periods and pension rights. Comparable to social policies during working life, pension regulations can therefore alleviate the risk of old-age poverty entailed by biographies deviating from the ‘standard full-time worker’ (Möhring, Reference Möhring2015).

Pension regulations that address gendered work–family lives are, for example, childcare credits, survivor's pensions and divorce-splitting mechanisms. Their existence or absence likely shapes how divorce is related to women's and men's pension incomes. Childcare credits, for example, aim to compensate parents, mostly mothers, for income loss due to childcare-related career interruptions (Jankowski, Reference Jankowski2011). Despite increasing women's pension entitlements, however, they do not fully compensate for these income losses (Möhring, Reference Möhring2018; Lis and Bonthuis, Reference Lis, Bonthuis, Holzmann, Palmer, Palacios and Sacchi2020).

Survivor's pensions are designed to mitigate the survivor's loss of income after a partner's death and are usually based on the deceased partner's pension (Bonnet et al., Reference Bonnet, Hourriez and Depledge2012). Especially for women who were dependent on their husbands' income before retirement, survivor's pensions play an important role in old-age security (Fasang et al., Reference Fasang, Aisenbrey and Schomann2013). Once a marriage is dissolved, the entitlement to such a derived right is often forfeited, at the latest after remarriage (for exceptions, see OECD, 2018). Compared to divorced women, widowed women usually have higher pension entitlements due to their survivor's pension (Sefton et al., Reference Sefton, Evandrou, Falkingham and Vlachantoni2011; Peeters and De Tavernier, Reference Peeters and De Tavernier2015).

The risk of losing a partner through divorce is not ameliorated in most welfare states (Bonnet and Hourriez, Reference Bonnet and Hourriez2012), although divorced women usually face similar low pension entitlements to married women (McDonald and Robb, Reference McDonald and Robb2004). This is further supported by the higher likelihood of divorced women who do not repartner continuing to work after retirement or postponing retirement to compensate for their insufficient pension entitlements, while this is not the case for divorced men (Finch, Reference Finch2014; Kridahl, Reference Kridahl2017a; Dingemans and Möhring, Reference Dingemans and Möhring2019). Only a few countries, such as the United Kingdom, Canada and Germany, explicitly account for divorce in their pension regulations with a pension-splitting mechanism (Choi, Reference Choi2006). Under this mechanism, the acquired pension entitlements during years of marriage are summed and split between the former spouses.

Institutional differences between Sweden and West Germany

Policies supporting the compatibility of work and family

Starting in the 1970s, Sweden turned away from the male-breadwinner model and steadily expanded its individual and gender egalitarian policies. These included broad access to education and targeted policies, such as a parental leave system, subsidised public childcare, and the active recruitment of women into employment. As a result, female employment rates increased to approximately 80 per cent until the mid-1980s, however, often on a long part-time basis (Gonäs and Tyrkkö, Reference Gonäs and Tyrkkö2015). Thus, while the older cohorts of women in this study were part of the transition phase of female employment rates, the younger cohorts had increasingly similar employment rates to those of men. The introduction of individual taxation in 1971 further promoted women's employment and the presence of ‘dual-earner households’, improving the accumulation of individual pension rights for women, albeit at a lower level than for men (Gunnarsson, Reference Gunnarsson2016; Swedish Pensions Agency, 2018). By 1995, the income gap between women and men was still approximately 35 per cent (Government Offices of Sweden, 2021). In line with the concept of ‘individualisation of rights’, marriage and divorce laws were reformed starting in 1973, leading to a decline in social, legal or economic benefits due to marriage (Hoem, Reference Hoem1991; Perelli-Harris and Gassen, Reference Perelli-Harris and Gassen2012). This also entailed that if ex-spousal alimony is provided, it can only be for a short ‘adaptation’ period, as individuals are expected to be self-reliant.

In West Germany, until reforms started in the 2000s, policies supported the male-breadwinner–female-carer model in the tax and transfer system (Trappe et al., Reference Trappe, Pollmann-Schult and Schmitt2015). Particularly, the system of joint taxation together with derived social security entitlements due to marriage (e.g. health insurance) and high marginal tax rates that penalise second earners encouraged a gendered division of labour (Sainsbury, Reference Sainsbury1999; Gottschall and Schröder, Reference Gottschall and Schröder2013). Although parental leave benefits were introduced in 1976, additional policies supporting the compatibility of work and family were scarce, especially childcare for children under the age of three (Aisenbrey et al., Reference Aisenbrey, Evertsson and Grunow2009). While the average labour force participation rate for women was comparatively high until women were in their mid-twenties, it dropped with the family formation phase and did not rebound significantly thereafter. This pattern slowly changed with the economic upswing of the 1960s and the educational expansion that mainly women gained from. Beginning with women born in the 1940s, employment rates started to increase after the family formation phase (Ziefle, Reference Ziefle2009), although pronounced part-time or marginal employment continued to limit women's possibilities of accumulating sufficient pension entitlements. However, acknowledging the gendered imbalance in income, women in the cohorts studied were covered in the event of divorce by generous maintenance payments from their former husbands. Until a reform in 2008, spousal maintenance was granted to the ‘resident parent’ under the assumption that mothers were unable to work full-time before the youngest child reached age 15 (Bröckel and Andreß, Reference Bröckel and Andreß2015). Nevertheless, compared to women in Sweden, women in Germany lose all their social security entitlements previously derived from their marriage, which leads them to a different ‘legal reality’ after divorce. This has been shown to have a positive effect on women's income as they start providing for themselves (Kreyenfeld et al., Reference Kreyenfeld, Mika and Radenacker2018).

Pension policies and gendered work–family lives

The Swedish and German pension systems are based on three pillars (public, occupational, private) and can both be described as strongly lifetime earnings-related pension systems. In Sweden, almost all residents are covered by the public pension and an occupational pension scheme (OECD, 2019). Although the public pension is the most important pension source for women and men, occupational pension income is often higher for men than women. In 2019, occupational pension income increased the gender pension gap by 13 per cent (Swedish Pensions Agency, 2022a). A guaranteed pension is provided for individuals who had no or only little pensionable income during life. Retirement age is flexible, and starting from age 61, individuals can decide what percentage of their income pension they want to withdraw while continuing to work until age 67 (there are also possibilities to work past age 67). In the German public pension system, the mandatory retirement age for any old-age pension is gradually increasing from age 65 to 67 until 2029. In addition to civil servants and certain professions (e.g. farmers), approximately 90 per cent of the residents in Germany have an account in the public pension insurance, and it is by far the most important income source in old age (Wagner et al., Reference Wagner, Klenner and Sopp2017).

Both pension systems include additional pension qualifying periods, such as schooling, care periods, unemployment, sick leave and childcare credits (Swedish Pensions Agency, 2018; DRV, 2021). In Sweden, for the first four years after childbirth, the parent with the lower income is credited with entitlements based on the most favourable option, i.e. either based on (a) earnings the year before childbirth, (b) 75 per cent of average earnings in Sweden, or (c) a fixed amount equivalent to a basic income amount (Jankowski, Reference Jankowski2011). In 2018, 4 per cent of women's allocated pension entitlements were due to childcare credits, while they accounted for only 0.8 per cent of men's (Swedish Pensions Agency, 2018).

In Germany, a parent (by default the mother) receives three pension points for each child born after 1 January 1992 and 2.5 pension points for each child born earlier. One ‘pension point’ is equivalent to the average earnings of all insured persons in a given year. Before a reform in 2019, only two pension points were granted for children born before 1992. If a woman is employed during the first three years after childbirth, pension points for childcare and from employment are summed (up to the contribution assessment ceiling). In 2016, childcare credits accounted on average for 14 per cent of women's public pension entitlements, showing their importance in relation to entitlements from employment. For the small fraction of men who claimed them, they accounted for 7 per cent (Wagner et al., Reference Wagner, Klenner and Sopp2017).

With respect to risks arising from the loss of a spouse, whether through death or divorce, there are major differences between Sweden and Germany in line with each country's welfare and gender regime. In Sweden, the survivor's pension applies to the surviving partner irrespective of whether the couple were married and is usually paid for 12 months (Swedish Pensions Agency, 2022b). Different from the Swedish pension system, the German system includes a ‘small’ survivor's pension (paid for two years prior to age 47) and a ‘large’ survivor's pension, which supports the surviving spouse until death (55% of the deceased spouse's pension) (DRV, 2020).

As one of few countries, the German public pension system attempts to ameliorate negative economic consequences following divorce for the economically ‘weaker spouse’. Since the grand divorce reform in 1977, the ‘divorce-splitting’ mechanism has been in place in West Germany (since 1992 East Germany). In the case of divorce, the accrued pension entitlements during the years of marriage, including childcare credits, are summed up and divided equally between the ex-spouses upon divorce. This mechanism is mandatory by law and results mostly in an increase in pension entitlements for divorced women – by approximately 20 per cent over those for married women (Kreyenfeld et al., Reference Kreyenfeld, Mika and Radenacker2018) – whereas it decreases divorced men's pension entitlements.Footnote 1

Expectations

In the following, we outline four expectations on how divorce is related to public pension entitlements in the two welfare states by comparing divorced and (re)married women's and men's public pension incomes in West Germany and Sweden (for a summary, see Table A1 in the online supplementary material). Depending on the welfare state context, women and men face different social policies that shape gendered work–family lives and, thus, the possibility of accumulating individual pension entitlements during working life. Similarly, different pension regulations function as a continuation of social policies by providing credits for previous lifecourse developments. Hence, the outlined mechanisms that link divorce to pension entitlements might vary by welfare state context.

In Germany, social policies and pension regulations are built upon the idea of the male-breadwinner–female-carer model, and emphasis is placed on ‘equalisation payments’ to account for the gendered division of labour during the years of marriage. After divorce, women in Germany not only face different work incentives but also benefit on average from the divorce-splitting mechanism, which aims to protect them from the ‘loss of the male-breadwinner’. Regarding the relationship between divorce and public pension income, we therefore expect divorced women to have higher public pension incomes than (re)married women in West Germany (Expectation 1). Regarding men, we expect divorced men to have lower public pension incomes than (re)married men, as they face, on average, a deduction by the divorce-splitting mechanism (Expectation 2).

In Sweden, social policies and pension regulations are built upon the idea of gender quality and economic independence throughout the lifecourse. Hence, divorce hardly entails any policy-related consequences, as it is assumed that women and men are both self-reliant and have accumulated sufficient individual pension incomes, regardless of family status. We therefore expect more comparable public pension incomes between divorced and (re)married women (Expectation 3) and between divorced and (re)married men (Expectation 4). Prior research has indicated a strong negative social gradient in separations and divorce in Sweden, which may entail stronger differences in working histories. These differences may be reflected in public pension incomes, especially in those of divorced men. Nonetheless, from a theoretical perspective, there is no distinction in how social policies impact divorced and married women's and men's public pension incomes in Sweden.

Data and methods

Swedish and German data

For Germany, we draw on the subsample ‘biographical data on completed insured lives (VVL)’ from the German public pension registers. For Sweden, we utilise data from a large collection of registers, covering the entire Swedish population registered in Sweden since 1960. Both data sources include individual-level data on public pension entitlements, demographic characteristics and earning histories.

For comparability, the samples are restricted to women and men who (a) retired between 2013 and 2018, (b) were aged between 60 and 67 in the year of retirement, and (c) received a public old-age pension. This age bracket was chosen based on each country's pension regulations together with the statistics on the effective labour market exit age (OECD, 2022) to cover the majority of the retired population in both countries.Footnote 2 For Sweden, drawing an old-age pension is defined as the first year in which an individual receives only the public pension entitlement (100%) and no longer income from employment (Kridahl, Reference Kridahl2017a).Footnote 3 For Germany, it is defined as receiving any kind of old-age pension, which in practice corresponds to the Swedish definition. The German sample is restricted to individuals living in West Germany. East Germans in the cohorts under scrutiny are not considered, as they were subject to a different policy context before unification. Our final datasets include 3,278,808 individuals (51% women, 49% men) for Germany and 446,145 individuals (52% women, 48% men) for Sweden, reflecting the population size in each country after restrictions. All analyses are conducted separately by country and gender.

Dependent variable

The dependent variable is the monthly public old-age pension income in euros (OA-pension). Hence, we do not consider occupational or private pensions and assets. All measures, particularly the occupational pension, usually increase gender pension gaps (Birman et al., Reference Birman, Gustafson, Korsell and Lindquist2017). This suggests that differences in economic security in old age should be larger if other measures are factored in. In the Swedish registers, pension entitlements are stored in Swedish kroner (SEK), while in the German registers, pension entitlements are stored as ‘pension points’. Swedish pension income is calculated using the consumer price index, and the pension incomes of both countries are analysed in euros, using 2018 as a reference year (SGB VI, Reference SGB VI2019; SCB, 2021). Public old-age pension income in both countries is mainly acquired through gainful employment but also consists of other pension qualifying periods. We further calculate the monthly public old-age pension income without childcare credits and, for the German sample, without the supplements/deductions for the ‘divorce-splitting’.

Independent variables

The main variable of interest is family status, measured in the year of retirement (implying that it is time constant). In the Swedish data, family status indicates whether women and men were married, remarried, divorced, widowed, cohabiting or never married/single. We do not distinguish between previously widowed and/or divorced individuals in the co-habiting group. Thus, this group may include a fraction of women and men who have been divorced and/or widowed before moving together with their new partner. In the German data, family status has four categories: married, remarried, divorced or widowed/never married. Unfortunately, widowed and never-married individuals cannot be distinguished. This is a rather small problem for widowed individuals, as we would expect them to have similar individual public old-age pension incomes as married individuals (Kreyenfeld et al., Reference Kreyenfeld, Schmauk and Mika2022). However, we do not know how never-married individuals' income histories develop and if they might have lower or higher pension incomes compared to the remaining sample. As the focus of this study is on the relationship between divorce and public pension incomes, it seems reasonable to focus on groups associated with divorce, such as (re)married individuals. Moreover, we are aware that other family forms, such as cohabiting and separated individuals, deserve attention. This is especially true in the Swedish case, where cohabitation is common and research has long shown a strong negative social gradient in separations (Härkönen and Dronkers, Reference Härkönen and Dronkers2006). However, separation is difficult to identify fully in the registers. Since Sweden first introduced a dwelling register in 2012 (Thomson and Eriksson, Reference Thomson and Eriksson2013), many separations may disappear ‘under the radar’ for the cohorts studied here.

For the descriptive part, we display annual income histories from pensionable income (reference year 2018) from age 20 until age 65 by family status (see SCB, 2016; FDZ-RV, 2020). Pensionable income also includes replacement payments, such as parental leave and times of unemployment. In the regression models, the year of retirement is included, as we use pooled data over the period 2013–2018. Further controls that were shown to have an effect on retirement income are the age at retirement and education (Möhring, Reference Möhring2015). For Germany, education can only be measured by whether an individual has completed more than the regular years of schooling after age 17, as no information is available on the individuals' obtained educational qualifications. For Sweden, education is categorised into up to nine years of education, 12 years or higher education. For the female samples, the number of children (childless, one, two, three or more) is also included. As the German pension registers mainly store this information for women, we cannot include this variable for men.

The sample statistics for women and men (Table A2 in the online supplementary material) show an even distribution across retirement years in both countries. While most individuals in the German sample were born between 1949 and 1953, the majority in the Swedish sample were born slightly earlier, between 1947 and 1952. In line with prevailing retirement regulations, this is reflected in the average age at retirement, which is approximately 65.2 years in Sweden and 64.4 years in Germany. With respect to family status, the large share of almost 15 per cent of divorcees in the year of retirement in Sweden stands out, as this group amounts to only 9 per cent in the German sample. Conversely, the German sample shows a large group of married individuals, with more men (69.3%) being married than women (63.1%), while in Sweden, this group is 48.4 per cent for both women and men. The share of remarried women and men is slightly higher in Sweden than in Germany. In both countries, men in the cohorts studied have slightly higher education levels than women. While there are no large differences in the descriptive statistics by family status for women in Germany, divorced men seem to be less educated than married men. In Sweden, this holds true for divorced women and men, who also tend to retire later than their married counterparts (Tables A3 and A4 in the online supplementary material).

Analytical strategy

For most of the analysis, we focus on divorced and (re)married women and men in the year of retirement. For the descriptive part, we construct annual income histories from age 20 until age 65, as they are the most relevant determinant of individual public pension income. To disentangle the impact of social policies and pension regulations, we calculate the monthly public OA-pension income across family status with respect to lifetime income and childcare credits, and divorce-splitting for Germany. The analytical part consists of bivariate and multiple ordinary least squares regression models in each country. The aim is to analyse how monthly public OA-pension income relates to family status without and with adjusting for socio-demographic covariates that have been shown in previous research to be related to pension incomes. The last step includes an interaction term of family status and the year of retirement to account for the pooled data structure and to rule out major variations in public pension incomes over the six retirement years.

Sensitivity analyses

Sensitivity analysis for Sweden showed that the results were stable when accounting for the time spent divorced. Compared to married individuals, those divorcing within five years prior to retirement seemed to be the most economically disadvantaged. Due to limitations in the German data, we can measure family status only as a time-constant variable in the year of retirement and do not have an equivalent analysis for the German sample. Moreover, to account for the positive skewedness of pension income, models with log-transformed pension income were conducted for both countries, showing comparable and robust results. Although we could not include further variables that might be correlated with the risk of getting divorced, we did adjust our models for the mentioned socio-demographic confounders. We also conducted sensitivity analysis controlling for months spent incapacitated (Germany) and on sick leave (Sweden) prior to age 60, as these variables are likely correlated with the risk of getting divorced and at the same time with expected pension income, showing comparable results. As the variable information was available only for ages 40–59 in Sweden, while it covered the whole working history in the German data, we did not include them in the main models due to comparability reasons.

Results

Descriptive results

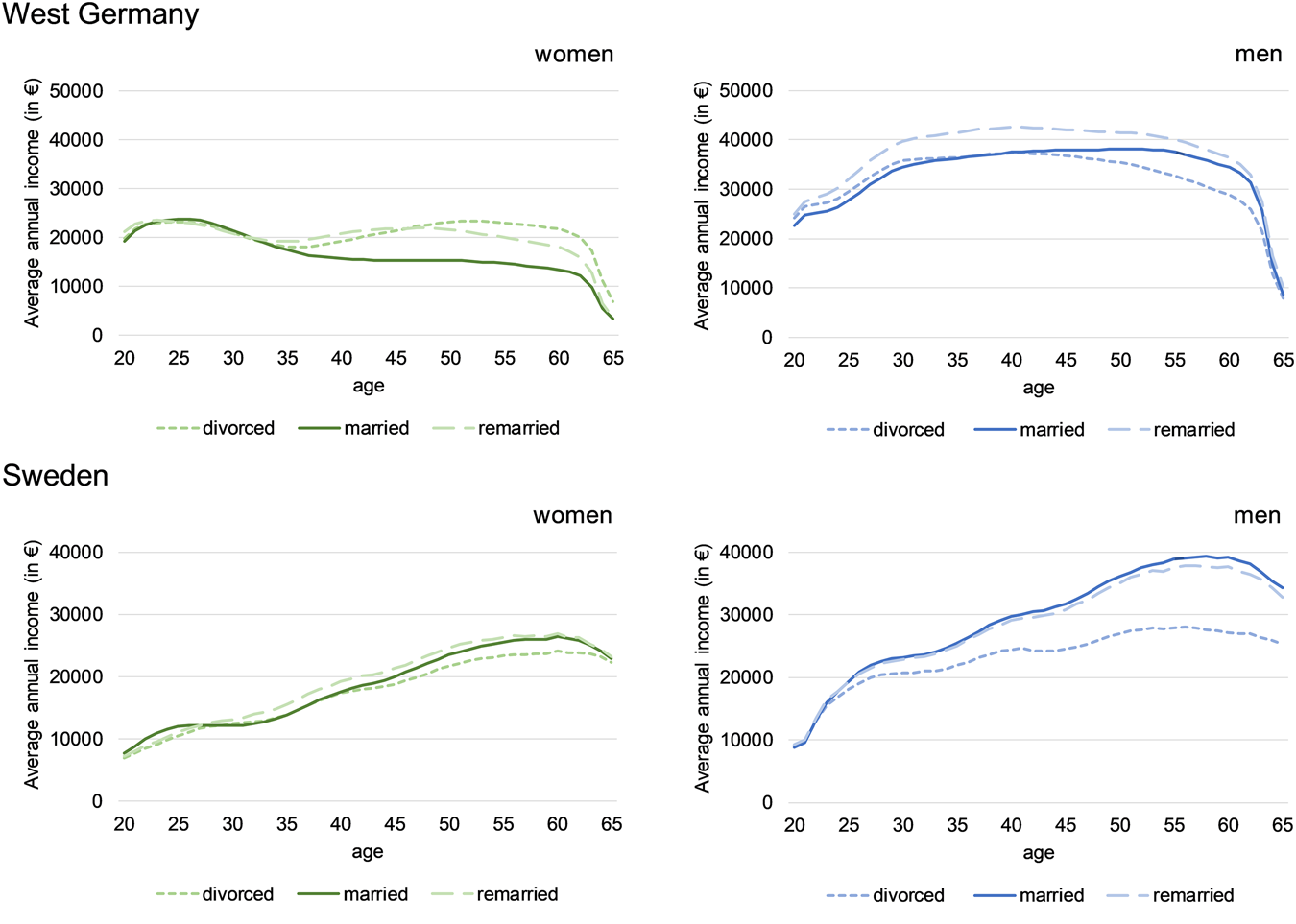

The descriptive analyses show large differences in women's and men's annual income histories in both countries (Figure 1). In Germany, women's annual income always remains below €25,000 and starts declining after the age of 25, most likely due to their family formation phase. While the average annual income of divorced and remarried women starts to rise again, married women's incomes stay at a low level. In contrast, (re)married men in Germany show stable annual incomes, averaging over €30,000 from the age of 25. Only the annual income of divorced men starts to decline from approximately age 40, suggesting that there might be gendered consequences following divorce for income histories in Germany.

Average annual income histories from pensionable income for married, remarried and divorced women and men in the year of retirement, West Germany and Sweden.

Notes: The scales differ, as income histories reflect the earning distribution in each country. Due to one pension point being equivalent to the average income in a given year, we do not observe the same upwards trend for Germany as for Sweden. Base year for earning deflation: 2018.

Source: RTZN-VVL2013–2018 and Swedish registers; authors' own calculations.

In Sweden, the annual incomes of women plateau around the family formation years but increase afterwards to approximately €25,000. There are almost no differences in women's annual income histories across family status. Only divorced women's annual incomes fall slightly behind after age 40 until retirement. Men in Sweden show continuously increasing incomes, but they differ across family status. While (re)married men's incomes reach a maximum of approximately €40,000, divorced men's annual incomes start lagging behind at approximately age 25 and continue to fall behind until retirement. While income histories seem to differ by women's family status only slightly, divorced men show very different income histories than (re)married men. However, it is difficult to disentangle the mechanisms that select women and men into being divorced or (re)married in the year of retirement. As in the case of divorced men, the more successful ones could have entered a new marriage and thus end up in the remarried group. Given that divorce is associated with other concurrent life events for men, such as invalidity or unemployment, the observed patterns could also be related to divorced men already being negatively selected in terms of their health and socio-economic status.

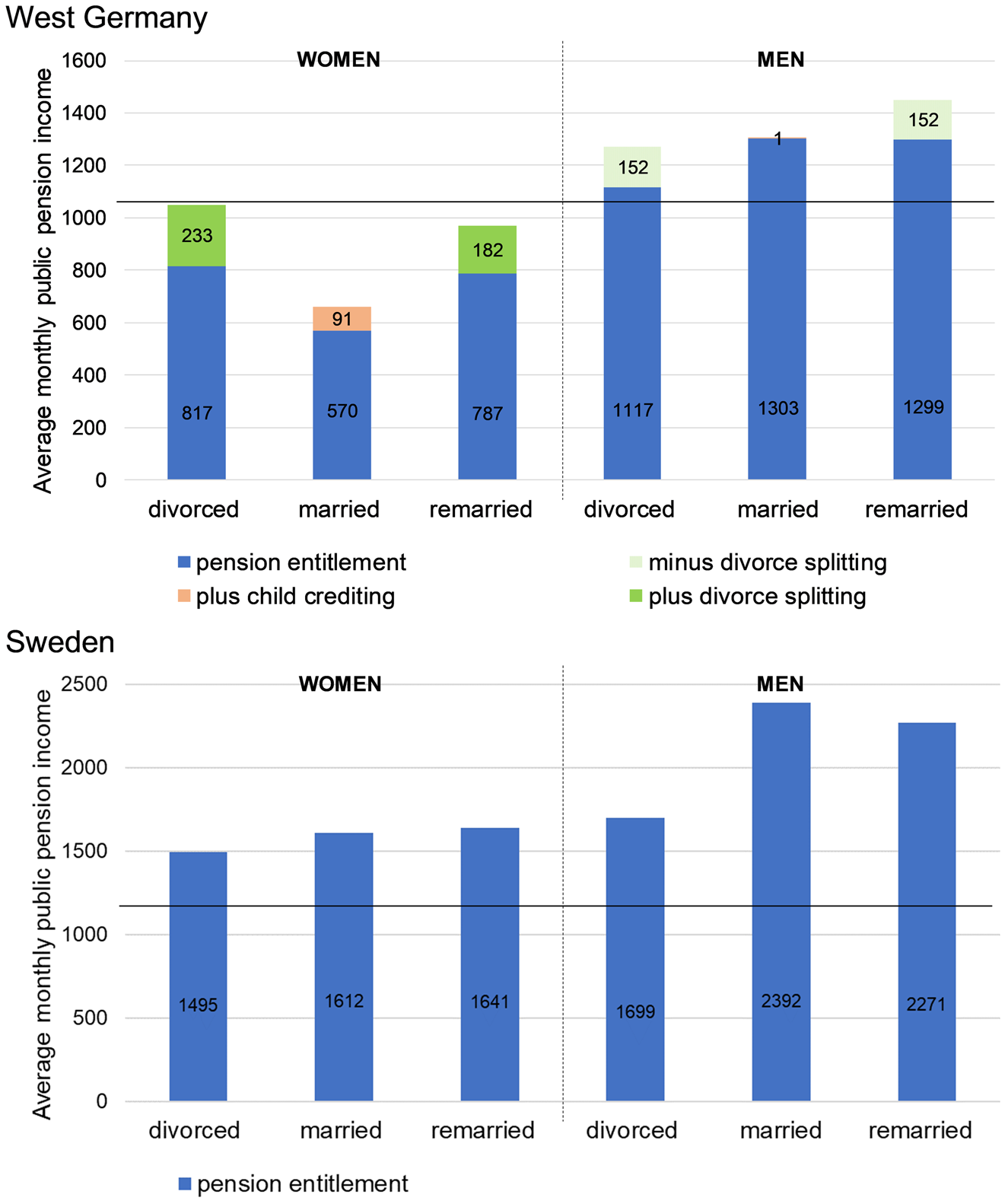

Figure 2 shows the average monthly public old-age pension income of women and men by family status and source of the pension entitlement (statistics across family status groups, Table A5 in the online supplementary material). In Germany, women have lower public OA-pension incomes than men. Divorced and remarried women have, on average, a public OA-pension income of approximately €1,000. This is largely due to the divorce-splitting mechanism, which increases their public pensions on average by €200, but also by their comparatively higher lifetime income, as expected from the annual income histories. Although married women's public pension incomes increased by €91 due to childcare credits, which correspond to 14 per cent, they still received the lowest public OA-pension of €661. Married men in Germany receive the highest public OA-pension income of €1,304, followed by remarried men, and divorced men receive the lowest public OA-pension income of €1,117. The divorce-splitting mechanism reduces the monthly public OA-pension income of divorced and remarried men by approximately €150. It seems that this mechanism aligns the public OA-pension incomes of divorced women and men, while married and remarried women show a greater gender public pension gap. In 2018, the poverty line for a single-person household in West Germany, calculated as 60 per cent of the median disposable household income, was €1,062 (WSI, 2019). If the public old-age pension income were the only source of income, both divorced women and men would, on average, have a household income close to this threshold.

Average monthly public old-age pension income for divorced, married and remarried women and men in the year of retirement, West Germany and Sweden.

Notes: The scales differ for both countries. Childcare credits are included in the divorce-splitting mechanism. The poverty line in West Germany (2018) was €1,062 and that in Sweden (2017) was €1,200.

Source: RTZN-VVL2013–2018 and Swedish registers; authors' own calculations.

In Sweden, (re)married women show comparable monthly public OA-pension incomes averaging €1,600. However, divorced women's public OA-pension income is €117 less on average than that of married women. Divorced women would thus, on average, still be above the poverty line for a single-person household in old age if this were their only source of income (EAPN, 2019). Compared to women's earnings, childcare credits play a minor role in women's public pension income (Figure A3 in the online supplementary material). Men in Sweden also have higher public OA-pension incomes than women, especially (re)married men, with an average public OA-pension income of approximately €2,300. Divorced men receive the lowest public OA-pension income, €1,699. This low value for men in Sweden is mainly related to their lower lifetime income. While differences in women's and men's public OA-pension incomes are also the smallest for divorcees in Sweden, it seems that this is mainly driven by divorced men doing worse during working life (see Figure 1).

Regression results

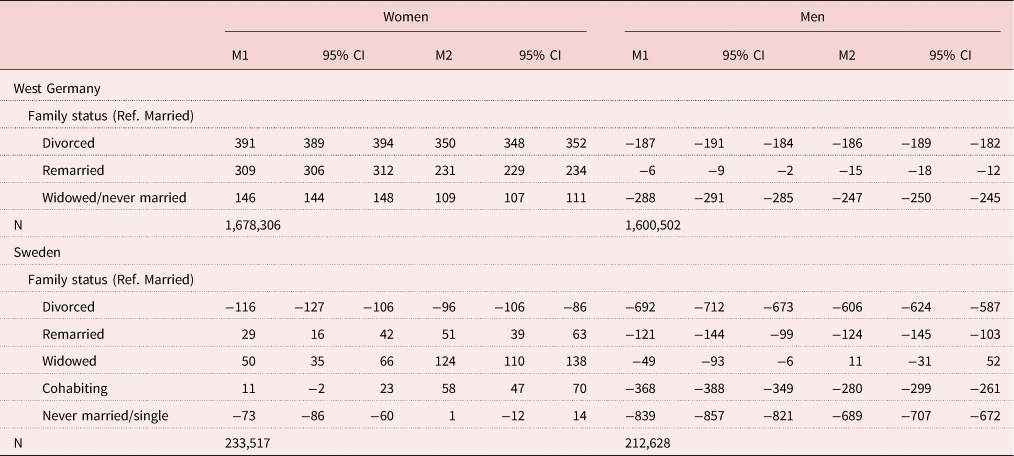

Table 1 shows the estimates of family status on monthly public old-age pension income obtained from the bivariate and multiple regression models separately for women and men by country (full models, Tables A6 and A7 in the online supplementary material). Even after adjusting for socio-demographic confounders, such as education and age at retirement, the results reveal that the monthly public OA-pension income varies by family status for women and men in both countries. For women in Germany, compared to being married, being divorced increases the public OA-pension income by €350, which is equal to 34 per cent (Table A8 in the online supplementary material). For men, an opposite pattern is observed, with divorced men receiving €186 (14%) less per month than married men.

Regression results with monthly public old-age pension income (in euros) as the dependent variable for West Germany and Sweden

Notes: Controlled for M1 = no controls; M2 = retirement year, education, age at retirement and female models for number of children. The results are rounded. CI: confidence interval. Ref.: reference group.

Source: RTZN-VVL2013–2018 and Swedish registers; authors' own calculations.

For women in Sweden, family status seems to play a minor role in differences in monthly public OA-pension income. Only divorced women are expected to have a public OA-pension income that is €96 (6%) less than that of married women. For men in Sweden, a similar pattern as in Germany is observed, with married men receiving the highest public OA-pension income. However, there is a clear divide between the comparison groups: while remarried men show only a comparatively small difference of €124 (5%) from married men, and cohabiting men a difference of €280 (12%), divorced and never-married men show a large difference in expected public OA-pension income: €606 (26%) and €689 (29%) less, respectively.

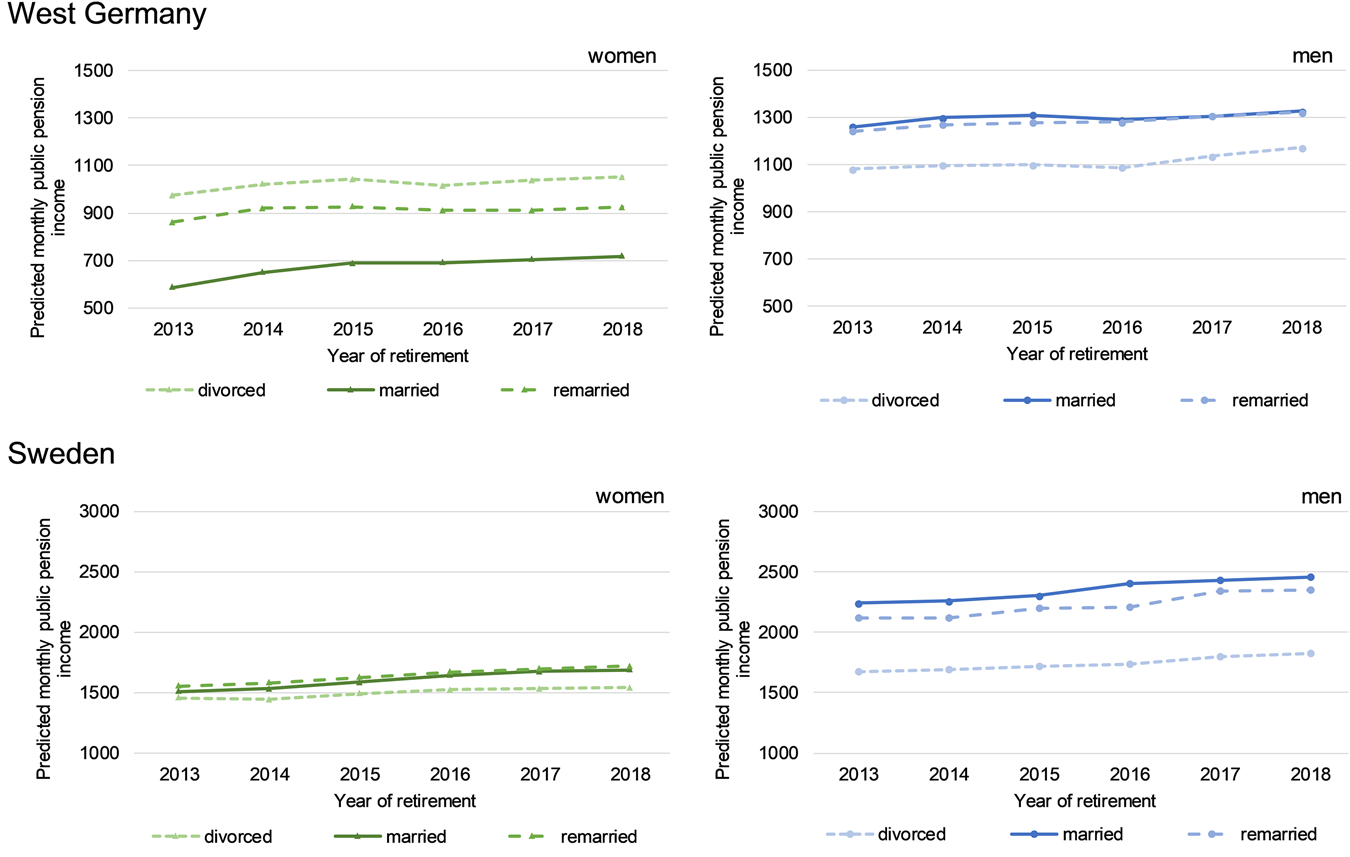

To account for the pooled data structure and examine whether estimates of monthly public old-age pension incomes are stable over time, interaction models of family status and retirement year are analysed (Tables A9 and A10 in the online supplementary material). The results are displayed as predicted values from these models for divorced, married and remarried women and men in both countries. As expected for women in Germany (Expectation 1), there are persistent differences in their public OA-pension income, as shown in Figure 3. Divorced women received a public OA-pension income of €1,050 by the end of the observation window (2018), while married women received a lower public OA-pension income of €719. For men, we observe an opposite result, with divorced men's public OA-pension incomes being significantly lower than those of married men, which is in line with our expectations (Expectation 2).

Predicted monthly public old-age pension income by gender and family status over 2013–2018, West Germany and Sweden.

Notes: The scales differ for the countries. Controlled for education, age at retirement and female models for number of children. The results are rounded.

Source: RTZN-VVL2013–2018 and Swedish registers; authors' own calculations.

For women in Sweden, pension incomes are more comparable by family status across retirement years. However, the difference between divorced and (re)married women's public OA-pension incomes increases slightly. Divorced women who retired in 2013 have, on average, public OA-pension incomes that are only €54 less than those of married women. For divorced women who retired in 2018, the difference increased to €149 less, on average. This difference translates into a pension gap of 9 per cent in 2018, which, together with its increasing pattern across retirement years, challenges the expectation of comparable retirement incomes among women with different family statuses (Expectation 3). For men in Sweden, patterns are similar to those of men in Germany, although we expected comparable public OA-pension incomes across family status. The persistently much lower public OA-pension incomes of divorced men thus force us to reject Expectation 4. In 2018, the public OA-pension of a divorced man was, on average, €633 lower, which is almost 26 per cent lower than that of a married man and far from comparable. However, divorced men still have higher public OA-pension incomes than women of any family status in Sweden. Although women generally seem to have a relatively stable income level until retirement (see e.g. Figure 1), their public OA-pension incomes still do not reach the same level as that of men.

Summary and discussion

By comparing the public old-age pension incomes for women and men who retired between 2013 and 2018 in West Germany and Sweden, this study has contributed to a better understanding of how divorce is related to economic wellbeing in old age in two different welfare states. The findings partly support the outlined theoretical assumptions about how each welfare state may mitigate the possible consequences following divorce. In Germany, the divorce-splitting mechanism ‘equalises’ pension entitlements by increasing women's and decreasing men's public pension incomes. In Sweden, social policies seem to enable women comparatively similar and independent of their family status to acquire individual pension entitlements, although not yet to the same extent as men.

The results reveal different income histories for women and men by family status in both countries, which are, together with the prevailing pension regulations, also reflected in their monthly public old-age pension incomes. In Germany, divorced women have pension incomes approximately €350 higher than those of married women, while divorced men's public OA-pension incomes lag behind those of married men by approximately €180. This is mainly due to the divorce-splitting mechanism but also due to the higher lifetime incomes of divorced women and lower incomes of divorced men. For Sweden, divorced women have, on average, slightly lower public OA-pension incomes than married women, particularly those who retired in 2017 and 2018. Divorced men, however, show a persistently large difference, with €600 less per month on average than married men.

In line with the recognition of the imbalance in women's and men's working lives, the divorce-splitting mechanism in Germany fulfils its aim by redistributing public pension entitlements between the ex-spouses. Nonetheless, compared to married men, both divorced women and men have lower public OA-pension entitlements of €1,100 on average. In 2018, this amount was slightly above the poverty line of a single household (WSI, 2019) if the public OA-pension income would be the only income source of a divorced individual. It can therefore be considered below adequate. Although this study did not take a couples' perspective, the results indicate that only splitting up the ‘male-breadwinner pension’ seems insufficient to sustain two separate households, especially if the ex-spouses practised a gendered division of labour during marriage. This gendered division of labour seems to be the root of the problem, as even cohabiting women still reduce their working hours after childbirth in Germany. In the case of separation, these women are at high risk of experiencing old-age poverty, as ‘divorce-splitting’ does not apply to them (Kreyenfeld et al., Reference Kreyenfeld, Schmauk and Mika2022).

Following the Swedish approach of individual economic independence over the lifecourse, we did not expect public pension income to vary strongly across family status, as social policies aim to enable everyone to be part of the labour market. This partly holds for women, as they display more comparable annual income trajectories and public OA-pension incomes across family status. In comparison to previous research (e.g. Möhring, Reference Möhring2021) and the findings for West Germany that show higher public pension incomes for divorced women than for married women, it seems that social policies in Sweden achieved a stronger labour market participation of women regardless of family status. However, women's public OA-pension entitlements are still lower than those of divorced men, which are the lowest among men in Sweden. Occupational segregation and the gender pay gap might explain parts of this difference (Hustad et al., Reference Hustad, Bandholtz, Herlitz and Dekhtyar2020). However, it appears that even the gender-equality policies in Sweden did not manage, at least for the cohorts studied, to eliminate gendered work–family lives completely, and the existing childcare credits do not compensate for these differences. The gap between women's and men's public OA-pension entitlements is especially concerning for divorced women, as they may have to be self-reliant in old age, especially if they do not repartner and share public pension entitlements. The significantly lower public OA-pension incomes of divorced men are also alarming. This pattern cannot be explained as easily as in the German case since there are no pension-related measures in place that would lower their pension income after divorce.

A limitation of this study is that family status in the German data is available only in the year of retirement, and thus, it is not possible to account for the time spent in each family status (e.g. years being divorced) or the timing and occurrence of other factors that may be related to that status (e.g. unemployment, illness, occupation). The study results also indicate that men face economic consequences following divorce (e.g. Andreß et al., Reference Andreß, Borgloh, Brockel, Giesselmann and Hummelsheim2006). However, as we cannot consider the lifecourse history and adequately account for the importance of possible selection effects, these consequences may already be caused by other factors that lead men to divorce in the first place and some men to repartner afterwards. Particularly in Sweden, divorced men's incomes lag behind early in the lifecourse, pointing to possible disadvantages that existed before the divorce, which then translate into lower pension incomes. Poorer health and lower education are related to a higher risk of divorce (Mortelmans, Reference Mortelmans, Schneider and Kreyenfeld2021) and, at the same time, negatively to earnings, as both increase the risk of unemployment and sick leave. Hence, treatment and selection effects are hard to disentangle (Jalovaara and Fasang, Reference Jalovaara and Fasang2020), and we can only speculate about mechanisms. As there are only small differences in pension incomes between married and remarried men, even in West Germany, where the divorce-splitting mechanism will on average decrease men's pensions, it seems that those men selecting into (re)marriage are on more advantageous tracks. This is further supported by the results for never-married men in Sweden, who receive even lower pension incomes than divorced men (Figure A6 in the online supplementary material). Future studies may investigate potential lifecourse differences during the adolescence and young adulthood of divorced and married men and the process of selection into marriage (and later divorce).

An important finding of this study is that neither welfare state seems able to shield women and men from the possible disadvantages related to divorce for economic wellbeing in old age. This finding is corroborated by other studies, which have shown that divorced women in Sweden (Kridahl, Reference Kridahl2017a) and Germany (Radl and Himmelreicher, Reference Radl and Himmelreicher2014) tend to postpone retirement, together with a general increase in the share of working pensioners over recent years (Eurostat, 2022b). Hence, ‘ageing unequally’ does not stop around retirement but possibly continues into older ages. As witnessed by the rise of late-life divorce, it is possible that family status will still change after retirement (Öberg, Reference Öberg, Bildtgård and Öberg2017), while at this point in the lifecourse, opportunities to adjust retirement income are limited.

Given these trends, the findings of this study indicate that there may be a large share of divorced pensioners at risk of being economically disadvantaged relative to married pensioners in the years to come. Although the analyses only included public old-age pension incomes, earlier research has shown that gender inequalities increase when adding occupational or private pension incomes (Birman et al., Reference Birman, Gustafson, Korsell and Lindquist2017). Furthermore, divorced women and men tend to have less wealth accumulated at retirement, as assets are often split upon divorce. Unstable careers and/or part-time employment further act as an obstacle for investments in occupational and private pension schemes. This is of concern in light of reforms strengthening the role of private and occupational pensions (Frericks et al., Reference Frericks, Knijn and Maier2009), as they contribute to ‘ageing unequally’ in a way that those in already advantageous positions can build up complementary entitlements more easily.

The results show that both welfare state approaches – preventing inequality from the onset (Sweden) and compensating for inequality afterwards (Germany) – have advantages and disadvantages. Given the growing diversity of family forms, policies should aim to address both issues: they should aim to mitigate the onset of ‘ageing unequally’ by reducing labour market and gender-related inequalities. Concurrently, they should aim to put in place measures that compensate for existing inequalities, such as childcare credits, and decouple policies from marital status and extend them to cohabiting unions to include individuals following ‘non-normative’ family lifecourses. Future studies could evaluate different pension types (public, occupational, private) by family status to examine who benefits and who loses with different pension regulations, thereby also considering (equivalised) household income. They could also compare similar family risk-related pension arrangements across countries to assess how effective they are in each welfare state, for instance, using harmonised survey data including information on pension income, benefits and other income compensations.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S0144686X23000703.

Financial support

This work was supported by the Deutsche Forschungsgemeinschaft – DFG, German Research Foundation (390285477/GRK 2458); and the Swedish Research Council for Health, Working Life and Welfare – Forte (DNR: 2020-00923).

Competing interests

The authors declare no competing interests.

Ethical standards

We confirm that the data used are anonymised by the respective research institution (Statistics Sweden; Research Data Center of the German Pension Insurance) and comply with ethical standards. The Swedish part of the project has been further approved by the Swedish Ethical Approval Board (DNR 2021-02981).

Open access

Open access

_AE2020.png){kind=link}