No CrossRef data available.

Article contents

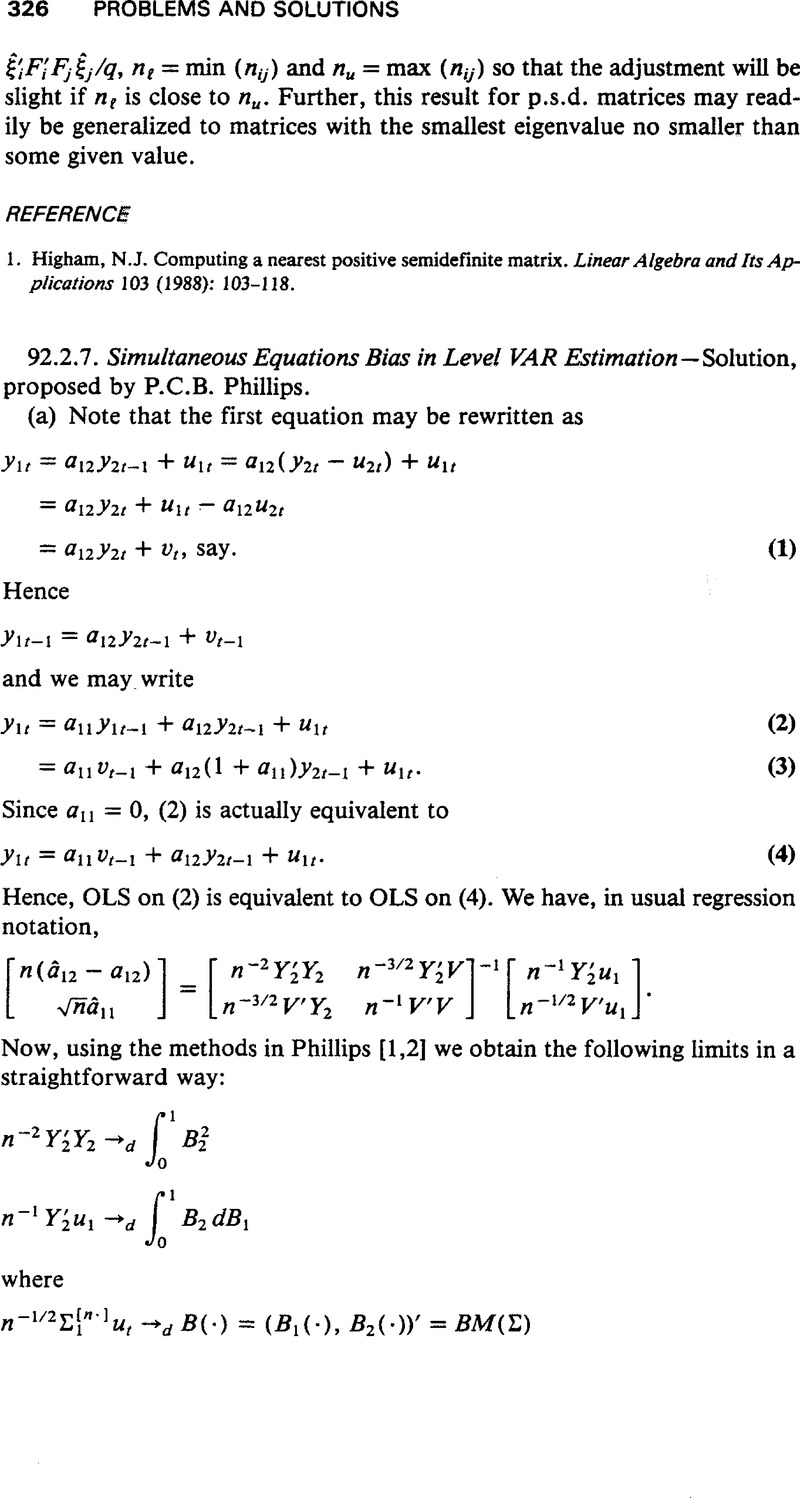

Simultaneous Equations Bias in Level VAR Estimation

Published online by Cambridge University Press: 11 February 2009

Abstract

An abstract is not available for this content so a preview has been provided. Please use the Get access link above for information on how to access this content.

Information

- Type

- Solutions

- Information

- Copyright

- Copyright © Cambridge University Press 1993

References

1.Phillips, P.C.B. Optimal inference in cointegrated systems. Cowles Foundation Discussion Paper No. 866, Econometrica (forthcoming), (1988/1991).Google Scholar

2.Phillips, P.C.B.Partially identified econometric models. Econometric Theory 5 (1989): 181–240.CrossRefGoogle Scholar

3.Phillips, P.C.B. & Durlauf, S.N.. Multiple time series with integrated variables. Review of Economic Studies 53 (1986): 473–496.CrossRefGoogle Scholar

4.Stock, J.H.Asymptotic properties of least squares estimators of cointegrating vectors. Econometrica 55 (1987): 1035–1056.CrossRefGoogle Scholar