1. Introduction

The valuation of pension fund liabilities requires the use of consistent, realistic, and up-to-date mortality rates and also the forecast of these mortality rates into the future for cash flow discount or asset-liability management. Such requirements are embedded in modern solvency assessment principles and financial reporting standards; see Sandström (Reference Sandström2016) and IASB (2017). The vast majority of studies in mortality rates forecasting make use of national population data when performing applications; see Cairns et al. (Reference Cairns, Blake, Dowd, Coughlan, Epstein, Ong and Balevich2009), Dowd et al. (Reference Dowd, Cairns, Blake, Coughlan and Khalaf-Allah2011), Lee and Carter (Reference Lee and Carter1992), Li and Lee (Reference Li and Lee2005), Li (Reference Li2013), and Renshaw and Haberman (Reference Renshaw and Haberman2006), among others.

Since the national population is inevitably different from the pension fund population, there is an inherent basis risk in substituting the former mortality rates for the purposes of analyzing the latter. This basis risk may not present a meaningful problem when the difference between the national population and the underlying sub (selected) population is reasonable. For instance, in developed countries in Europe, the population mortality tends to be more homogeneous. However, in countries with high social inequalities, the income differences and healthcare access make the mortality rates significantly different among the selected and the overall national populations.

Brazil is a country with high social inequalities (OECD, 2018). According to supervisory authorities, less than 8% of Brazil’s population has a pension plan,Footnote

1

and the fraction that does tends to be in the upper deciles of the national income distribution. As a result, national mortality rates are much higher than the ones for actuarial subpopulations, such as participants of pension funds or insurance customers. Our data indicates that, on average, the mortality rates of the pension fund subpopulation are half (49%) of the mortality of the national Brazilian population for ages

$60+$

.

$60+$

.

Mortality modeling for a pension fund must contend with two fundamental challenges. On the one hand, the population of interest is relatively small, so stand-alone models lack sufficient credibility: there are simply not enough death counts to reliably estimate mortality rates. On the other hand, the pensioners often have materially distinct mortality patterns, so that simple adjustments of the national trends are inadequate. In this paper, we aim to systematically explore and ultimately bridge this gap. To this end, we construct a spectrum of deflator-based stochastic models that relate the pension fund mortality to the reference population. As a starting point, we observe that the commonly used parametric deflators (such as deflators that are constant across ages) are too rigid and underfit. At the other extreme, allowing for independent age- (or year-) specific deflators leads to over-parametrization and overfitting. This motivates us to develop non-parametric deflators that are constrained to be smooth yet flexible enough. Specifically, we propose to employ Gaussian-process (GP)-based deflators, which naturally embed dependence while providing a fully probabilistic, data-driven, non-parametric framework.

Methodologically, we make three contributions. First, we provide a taxonomy of over half a dozen deflator models for small population mortality, systematically comparing them (including discussing multiple nesting relationships present) and offering a comprehensive “menu” for how to approach this problem. Second, we propose a new class of GP-driven deflators. Such models offer a valuable hybrid of leveraging the reference mortality table while building in sufficient flexibility. Third, with an emphasis on capturing model risk due to the small underlying population, we utilize Bayesian methods throughout our analysis, so that all our model hyperparameters come with priors. We employ the Stan package and underlying MCMC routines to provide uncertainty quantification, contributing to the literature on Bayesian mortality analysis.

Empirically, we are motivated by and illustrate our developments with two datasets of Brazilian pensioners. The pension fund in our primary case study (pension fund 1) consists of about 14,000 exposed lives with about 100 annual deaths. Compared to the national baseline, these pensioners have about half the mortality rate, with the respective longevity gap notably growing over time. We demonstrate that our proposed models outperform extant alternatives, including the two extremes of our modeling spectrum: a stand-alone GP model and a fully specified fixed-deflator model. Given that age-specific death counts in this fund are often 0 or 1, we moreover explore the observation likelihood, namely the overdispersion in death counts relative to the Poisson baseline. Our analysis provides insights into the mortality experience in Brazil and in developing countries more broadly, offering new takeaways on pension funds in highly heterogeneous settings. To confirm the above findings, we further explore a second Brazilian pension fund that is slightly smaller.

Our interest is on ages 60 and over (60

$+$

), ages that are most relevant for insurance and pension funds when paying annuities. This is another difference between our approach and the majority of papers in the mortality modeling literature. In this paper, Gaussian processes will be used in a subpopulation framework to forecast mortality at ages 60+ of small, specific pension funds’ populations, using as reference the annual Brazilian national mortality tables.

$+$

), ages that are most relevant for insurance and pension funds when paying annuities. This is another difference between our approach and the majority of papers in the mortality modeling literature. In this paper, Gaussian processes will be used in a subpopulation framework to forecast mortality at ages 60+ of small, specific pension funds’ populations, using as reference the annual Brazilian national mortality tables.

The rest of the paper is organized as follows. Section 2 reviews existing methods for subpopulation models, as well as the Gaussian Process paradigm. Section 3 summarizes our Brazil pension fund dataset and the IBGE reference mortality tables. Section 4 presents the list of the considered deflator models, both from existing approaches as well as new ones proposed here for the first time. Section 5 illustrates and discusses the respective fits for our motivating dataset, while Section 6 provides a statistical assessment across all the fitted models. Appendix summarizes the models fitted in this paper, additional plots for the primary pension fund, and, finally, discussions for pension fund 2.

2. Subpopulation models

Given the small size of the modeled population, we directly work with death and exposed counts, disaggregated by age and calendar year. We employ the following notation:

-

•

$d_{x,t}$

is the number of deaths at age

$x$

and calendar year

$t$

for the pension fund, where

$x = \{60,\ldots ,89 \}$

and

$t = \{2013,\ldots ,2019\}$

;

$d_{x,t}$

is the number of deaths at age

$x$

and calendar year

$t$

for the pension fund, where

$x = \{60,\ldots ,89 \}$

and

$t = \{2013,\ldots ,2019\}$

; -

•

$E_{x,t}$

is the risk exposure at age

$x$

and calendar year

$t$

for the pension fund; -

•

$m^{BRA}_{x,t}$

is the central mortality rate relative to age

$x$

and calendar year

$t$

of

$BRA$

– Brazilian national mortality rates.

To overcome the scarce data available about the pension fund experience, we adopt the solution of external reference tables. The idea of such relational models is to adjust the reference table to the experience of the pension fund. In our work, we consider as a benchmark the national Brazilian mortality tables (

$BRA$

), also known as the IBGE (Brazilian Institute of Geography and Statistics) tables. These tables, as well as the pension fund’s data, are described in detail in Section 3.

$BRA$

), also known as the IBGE (Brazilian Institute of Geography and Statistics) tables. These tables, as well as the pension fund’s data, are described in detail in Section 3.

Reflecting the limited number of deaths in the pension fund population, the common approach is to use a discrete (Poisson) likelihood where the reference mortality rate

$m^{BRA}_{x,t}$

is part of the intensity parameter:

$m^{BRA}_{x,t}$

is part of the intensity parameter:

\begin{align} d_{x,t} \sim \mathrm{Poi}\left(e^{\theta _{x,t}} m^{BRA}_{x,t} E_{x,t}\right), \end{align}

\begin{align} d_{x,t} \sim \mathrm{Poi}\left(e^{\theta _{x,t}} m^{BRA}_{x,t} E_{x,t}\right), \end{align}

and

$e^{\theta _{x,t}}$

is the deflator applied to the reference population. Model (1) implies the fund mortality rate

$e^{\theta _{x,t}}$

is the deflator applied to the reference population. Model (1) implies the fund mortality rate

$m_{x,t} \,:\!=\, \mathbb{E}[ d_{x,t}]/E_{x,t}$

is given by

$m_{x,t} \,:\!=\, \mathbb{E}[ d_{x,t}]/E_{x,t}$

is given by

$m_{x,t}= e^{\theta _{x,t}} m^{BRA}_{x,t}$

. Hence,

$m_{x,t}= e^{\theta _{x,t}} m^{BRA}_{x,t}$

. Hence,

\begin{equation*}\theta _{x,t} = \log m_{x,t} - \log m^{BRA}_{x,t}\end{equation*}

\begin{equation*}\theta _{x,t} = \log m_{x,t} - \log m^{BRA}_{x,t}\end{equation*}

is the difference on the log scale between the fund mortality and the reference mortality, or equivalently, the percent ratio between them. Since the funds’ mortality is lower than the reference population’s,

$\theta _{x,t} \lt 0$

.

$\theta _{x,t} \lt 0$

.

An important modeling premise underlying the deflator framework is that the reference mortality surface

$ m^{BRA}_{x,t}$

is treated as fixed and exogenous. Any preprocessing, smoothing, or extrapolation embedded in the reference table therefore only affects the baseline level against which the pension fund mortality is measured and does not alter the stochastic structure of the deflators themselves. Consequently, the deflator process

$ m^{BRA}_{x,t}$

is treated as fixed and exogenous. Any preprocessing, smoothing, or extrapolation embedded in the reference table therefore only affects the baseline level against which the pension fund mortality is measured and does not alter the stochastic structure of the deflators themselves. Consequently, the deflator process

$ \theta _{x,t}$

is interpreted as capturing relative deviations of the pension fund experience from a given reference trend, rather than as an attempt to recover an underlying “true” mortality surface.

$ \theta _{x,t}$

is interpreted as capturing relative deviations of the pension fund experience from a given reference trend, rather than as an attempt to recover an underlying “true” mortality surface.

Before describing our method in detail, we provide a review of existing deflator models. The deflator approach was introduced in Hardy and Panjer (Reference Hardy and Panjer1998), who started with a constant deflator

$d_{x,t} \sim \mathrm{Poi}(\Theta \cdot m^{BRA}_{x,t} \cdot E_{x,t})$

. Beyond directly fitting

$d_{x,t} \sim \mathrm{Poi}(\Theta \cdot m^{BRA}_{x,t} \cdot E_{x,t})$

. Beyond directly fitting

$\Theta$

as a static parameter, they consider a sequential Bayesian setup, where

$\Theta$

as a static parameter, they consider a sequential Bayesian setup, where

$\Theta$

is endowed with a prior, which is updated over time based on observed

$\Theta$

is endowed with a prior, which is updated over time based on observed

$(d_{x,t}, E_{x,t})$

. Specifically, they leverage Poisson-Gamma conjugacy to assign a Gamma prior

$(d_{x,t}, E_{x,t})$

. Specifically, they leverage Poisson-Gamma conjugacy to assign a Gamma prior

$\Theta \sim \mathrm{Gamma}(c,c)$

which has a mean of 1, and therefore, a priori, the portfolio is expected to have the same mortality as the reference population. Olivieri and Pitacco (Reference Olivieri and Pitacco2012) generalize to independent age-specific random effects, obtaining the posterior

$\Theta \sim \mathrm{Gamma}(c,c)$

which has a mean of 1, and therefore, a priori, the portfolio is expected to have the same mortality as the reference population. Olivieri and Pitacco (Reference Olivieri and Pitacco2012) generalize to independent age-specific random effects, obtaining the posterior

$\Theta _x | \mathcal{D} \sim \mathrm{Gamma}( c + \sum _t d_{x,t}, c+ \sum _t m^{BRA}_{x,t} E_{x,t})$

.

$\Theta _x | \mathcal{D} \sim \mathrm{Gamma}( c + \sum _t d_{x,t}, c+ \sum _t m^{BRA}_{x,t} E_{x,t})$

.

Olivieri (Reference Olivieri2011) takes

\begin{equation*}d_{x,t} \sim \mathrm{Poi}\left(\Theta _{x,t} \cdot m^{BRA}_{x,t} \cdot E_{x,t}\right) \qquad \text{ where } \quad \Theta _{x,t} \sim \mathrm{Gamma}( \alpha _{x,t}, \beta _{x,t})\end{equation*}

\begin{equation*}d_{x,t} \sim \mathrm{Poi}\left(\Theta _{x,t} \cdot m^{BRA}_{x,t} \cdot E_{x,t}\right) \qquad \text{ where } \quad \Theta _{x,t} \sim \mathrm{Gamma}( \alpha _{x,t}, \beta _{x,t})\end{equation*}

and the hyperparameters

$\alpha ,\beta$

are sequentially updated over the years based on realized

$\alpha ,\beta$

are sequentially updated over the years based on realized

$d_{x,t}$

. van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017) use age-specific Bayesian “random effects,”

$d_{x,t}$

. van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017) use age-specific Bayesian “random effects,”

$d_{x,t} \sim \mathrm{Poi}(\Theta _x \cdot m^{BRA}_{x,t} \cdot E_{x,t})$

, where

$d_{x,t} \sim \mathrm{Poi}(\Theta _x \cdot m^{BRA}_{x,t} \cdot E_{x,t})$

, where

$m^{BRA}$

is estimated using a Lee-Carter model, and the age-specific deflators

$m^{BRA}$

is estimated using a Lee-Carter model, and the age-specific deflators

$\Theta _x$

are given either independent

$\Theta _x$

are given either independent

$\mathrm{Gamma}( c_x, c_x)$

priors (forcing

$\mathrm{Gamma}( c_x, c_x)$

priors (forcing

$\mathbb{E}[\Theta _x ] =1$

) or a log-AR(1) structure,

$\mathbb{E}[\Theta _x ] =1$

) or a log-AR(1) structure,

$\log \Theta _x = \mu + \rho \log \Theta _{x-1} + \eta$

, with a log-normal prior on

$\log \Theta _x = \mu + \rho \log \Theta _{x-1} + \eta$

, with a log-normal prior on

$\log \Theta _{x_0}$

, a uniform prior on the variance of

$\log \Theta _{x_0}$

, a uniform prior on the variance of

$\eta$

, and a logit-normal prior on

$\eta$

, and a logit-normal prior on

$\rho$

.

$\rho$

.

Making the deflators

$\theta _x$

constant in time offers a coherent projection into the future. For instance, it is common to assume that the mortality trend of the small population (which is difficult to reliably estimate due to a paucity of data) matches that of the reference; see e.g. Olivieri and Pitacco (Reference Olivieri and Pitacco2012), Salhi et al. (Reference Salhi, Thérond and Tomas2015), van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017), Li and Lu (Reference Li and Lu2017), Hyndman et al. (Reference Hyndman, Booth and Yasmeen2013), Salhi and Loisel (Reference Salhi and Loisel2017). Salhi et al. (Reference Salhi, Thérond and Tomas2015) focuses on time-dependent “differential mortality law,” i.e.

$\theta _x$

constant in time offers a coherent projection into the future. For instance, it is common to assume that the mortality trend of the small population (which is difficult to reliably estimate due to a paucity of data) matches that of the reference; see e.g. Olivieri and Pitacco (Reference Olivieri and Pitacco2012), Salhi et al. (Reference Salhi, Thérond and Tomas2015), van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017), Li and Lu (Reference Li and Lu2017), Hyndman et al. (Reference Hyndman, Booth and Yasmeen2013), Salhi and Loisel (Reference Salhi and Loisel2017). Salhi et al. (Reference Salhi, Thérond and Tomas2015) focuses on time-dependent “differential mortality law,” i.e.

$\theta _t$

depending only on year.

$\theta _t$

depending only on year.

Closely related to our work is Tomas and Planchet (Reference Tomas and Planchet2015). They consider a sequence of models, starting with an endogenous nonparametric

$d_{x,t} \sim \mathrm{Poi}( E_{x,t} \cdot e^{f(x,t)})$

to the relational versions

$d_{x,t} \sim \mathrm{Poi}( E_{x,t} \cdot e^{f(x,t)})$

to the relational versions

$d_{x,t} \sim \mathrm{Poi}( E_{x,t} \cdot e^{\,f(\log m^{BRA}_{x,t} ) } )$

,

$d_{x,t} \sim \mathrm{Poi}( E_{x,t} \cdot e^{\,f(\log m^{BRA}_{x,t} ) } )$

,

$d_{x,t} \sim \mathrm{Poi}(E_{x,t} \cdot m^{BRA}_{x,t} \cdot e^{\,f(x,t)} )$

, where the smooth functions

$d_{x,t} \sim \mathrm{Poi}(E_{x,t} \cdot m^{BRA}_{x,t} \cdot e^{\,f(x,t)} )$

, where the smooth functions

$f(x,t)$

are estimated using local kernel weighted log-likelihood methods.

$f(x,t)$

are estimated using local kernel weighted log-likelihood methods.

A related strand of literature directly proposes a parametric functional relationship between the mortality surfaces of the small and benchmark populations. In the original Brass model of Brouhns et al. (Reference Brouhns, Denuit and Vermunt2002), the authors take

$m_{x,t}= \theta _1 (m^{BRA}_{x,t})^{\theta _2}$

for parameters

$m_{x,t}= \theta _1 (m^{BRA}_{x,t})^{\theta _2}$

for parameters

$\theta _1, \theta _2$

to be fitted by GLM. More generally, Brouhns et al. (Reference Brouhns, Denuit and Vermunt2002) consider

$\theta _1, \theta _2$

to be fitted by GLM. More generally, Brouhns et al. (Reference Brouhns, Denuit and Vermunt2002) consider

$m_{x,t} = \theta _0 f(m^{BRA}_{x,t}) + \theta _1$

, for a given link function

$m_{x,t} = \theta _0 f(m^{BRA}_{x,t}) + \theta _1$

, for a given link function

$f$

(such as the logit). Plat (Reference Plat2009) directly models the ratio

$f$

(such as the logit). Plat (Reference Plat2009) directly models the ratio

$P_{x,t} =(d_{x,t}/E_{x,t}) / (d^{ref}_{x,t}/E^{ref}_{x,t})$

of the observed portfolio and reference mortality rate, imposing a linear relationship,

$P_{x,t} =(d_{x,t}/E_{x,t}) / (d^{ref}_{x,t}/E^{ref}_{x,t})$

of the observed portfolio and reference mortality rate, imposing a linear relationship,

$P_{t,x} = a_t + b_t x + \epsilon _{x,t}$

. Bienvenüe and Rulliére (Reference Bienvenüe and Rulliére2012) use distortion of probability distributions to connect

$P_{t,x} = a_t + b_t x + \epsilon _{x,t}$

. Bienvenüe and Rulliére (Reference Bienvenüe and Rulliére2012) use distortion of probability distributions to connect

$m^{BRA}$

and

$m^{BRA}$

and

$m$

.

$m$

.

A different way to frame the small population problem is via a multi-population approach. Such joint modeling of the larger and smaller subpopulation is especially appropriate when the smaller subpopulation is sufficiently large and moreover, when starting with raw data for both pools. For example, van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017) consider the CMI subpopulation in the United Kingdom, which consists of assured male lives and is roughly 20% of the total population, weighted towards pre-retirement ages. Hyndman et al. (Reference Hyndman, Booth and Yasmeen2013) consider the joint modeling of female and male log-mortality by building functional time-series models for their sum and difference (the product-ratio method). This setup is, however, not applicable to our case, where the pension fund is much smaller, and moreover, we work with the fixed national mortality table. A related approach to sub-national populations is to first compute the principal age components of mortality and then estimate the respective time-dependent coefficients:

$m_{x,t} = \sum _i a_i(t) Y^{ref}_i(x) + \epsilon _{x,t}$

(Alexander et al., Reference Alexander, Zagheni and Barbieri2017). Gravity models (Dowd et al., Reference Dowd, Cairns, Blake, Coughlan and Khalaf-Allah2011) work in the Lee-Carter paradigm and introduce the dependence of the small population period effect on the larger population:

$m_{x,t} = \sum _i a_i(t) Y^{ref}_i(x) + \epsilon _{x,t}$

(Alexander et al., Reference Alexander, Zagheni and Barbieri2017). Gravity models (Dowd et al., Reference Dowd, Cairns, Blake, Coughlan and Khalaf-Allah2011) work in the Lee-Carter paradigm and introduce the dependence of the small population period effect on the larger population:

\begin{equation*} \kappa _t = \kappa _{t-1} + \phi (\kappa ^{ref}_{t-1}-\kappa _{t-1}) + \mu + \rho \epsilon ^{ref}_{t} + \sqrt {1-\rho ^2} \epsilon _t,\end{equation*}

\begin{equation*} \kappa _t = \kappa _{t-1} + \phi (\kappa ^{ref}_{t-1}-\kappa _{t-1}) + \mu + \rho \epsilon ^{ref}_{t} + \sqrt {1-\rho ^2} \epsilon _t,\end{equation*}

similarly for the cohort term

$\gamma _{x-t}$

.

$\gamma _{x-t}$

.

A nonparametric framework for capturing the co-dependence of mortality across multiple populations via multi-output Gaussian processes was proposed in Huynh and Ludkovski (Reference Huynh and Ludkovski2021). As an extension, Huynh and Ludkovski (Reference Huynh and Ludkovski2024) developed hierarchical multi-output GPs to capture multiple cause-of-death mortality rates across different countries and both genders. In these extensions, different populations (or causes of death) translate into distinct levels of a factor covariate, with the latter contributing a cross-population covariance term. In our context, the national mortality table is already calibrated or smoothed out through statistical procedures applied by the National Institute of Statistics (IBGE), so there is no reason to smooth it again through a (multi-output) GP. Therefore, we employ GP regression within a single-output approach, i.e. solely for the pension fund mortality rates, whether directly or through deflators.

2.1 GP modeling

GP models (Oakley & O’Hagan, Reference Oakley and O’Hagan2002) are one of the most popular regression methods thanks to the great flexibility they offer in the representation of complex non-linear input–output relationships. GPs define probabilistic models of functional behavior, offering high prediction power, interpretability, and the ability to provide both an interpolation of the data and an uncertainty quantification in the unexplored regions (Marrel et al., Reference Marrel, Iooss, Van Dorpe and Volkova2008). The GP model was first developed in spatial statistics under the name of kriging (Cressie, Reference Cressie1990) and rapidly gained attention in the machine learning community. The core idea is to assume the regression function is distributed according to a Gaussian process, which allows treating the regression function values as unknown quantities and estimating them from the training data. Over the years, the GP model has become popular in a wide range of applications, such as wind power generation (Mori & Kurata, Reference Mori and Kurata2008), vehicle design and navigation (Chen et al., Reference Chen, Dai, Wang and Liu2014), modeling and prediction of natural hazards (Liu & Guillas, Reference Liu and Guillas2017; Rohmer & Idier, Reference Rohmer and Idier2012), etc.

We call a stochastic process

$f$

a Gaussian process if for any finite collection of index points

$f$

a Gaussian process if for any finite collection of index points

$\textbf{y} = \{y_j, j=1,\ldots ,n\}$

, the

$\textbf{y} = \{y_j, j=1,\ldots ,n\}$

, the

$n$

-dimensional multivariate density function of the random vector

$n$

-dimensional multivariate density function of the random vector

$\textbf{f} = [f(y_1), \ldots , f(y_n)]^\top$

is multivariate Gaussian (Rasmussen & Williams, Reference Rasmussen and Williams2005). A GP is completely specified by its mean and covariance functions. The mean function

$\textbf{f} = [f(y_1), \ldots , f(y_n)]^\top$

is multivariate Gaussian (Rasmussen & Williams, Reference Rasmussen and Williams2005). A GP is completely specified by its mean and covariance functions. The mean function

$m(y) \,:\!=\, \mathbb{E}[{f(y)}]$

describes what the expected value of

$m(y) \,:\!=\, \mathbb{E}[{f(y)}]$

describes what the expected value of

$f(y)$

. The covariance or kernel function, denoted as

$f(y)$

. The covariance or kernel function, denoted as

$c(\cdot ,\cdot )$

, expresses the degree of dependence between two different function values as a function of two index points,

$c(\cdot ,\cdot )$

, expresses the degree of dependence between two different function values as a function of two index points,

$\mathrm{Cov}(f(y), f(y')) = c(y, y')$

. In compact notation, this is written as

$\mathrm{Cov}(f(y), f(y')) = c(y, y')$

. In compact notation, this is written as

\begin{align*} f\sim \mathrm{GP} \bigl (m(\!\cdot\! ), c(\cdot , \cdot ) \bigr ). \end{align*}

\begin{align*} f\sim \mathrm{GP} \bigl (m(\!\cdot\! ), c(\cdot , \cdot ) \bigr ). \end{align*}

In the GP regression framework, we usually work with a finite collection of index points, which is equivalent to working with a multivariate Gaussian distribution. The collection of index points

$y_j$

, for

$y_j$

, for

$j = 1,\ldots ,n$

, in the previous definition plays the role of covariates. In our case, these are age and/or calendar year. The vector of function values whose components are now associated with each of those covariates is then distributed according to a

$j = 1,\ldots ,n$

, in the previous definition plays the role of covariates. In our case, these are age and/or calendar year. The vector of function values whose components are now associated with each of those covariates is then distributed according to a

$n$

-dimensional multivariate Gaussian distribution,

$n$

-dimensional multivariate Gaussian distribution,

\begin{eqnarray*} \begin{bmatrix} f(y_1) \\ . \\ . \\ \,f(y_n) \end{bmatrix} \sim \mathcal{N}\left ( \begin{bmatrix} m(\,y_1) \\ . \\ . \\ m(\,y_n) \end{bmatrix}, \begin{bmatrix} c(\,y_1,y_1) & \quad\cdots &\quad c(\,y_1,y_n) \\ . & \quad\cdots &\quad .\\ . & \quad\ddots &\quad . \\ c(\,y_n,y_1) & \quad\ldots &\quad c(\,y_n,y_n) \end{bmatrix} \right ) = \mathcal{N}( m(\textbf{y}), \textbf{C}). \end{eqnarray*}

\begin{eqnarray*} \begin{bmatrix} f(y_1) \\ . \\ . \\ \,f(y_n) \end{bmatrix} \sim \mathcal{N}\left ( \begin{bmatrix} m(\,y_1) \\ . \\ . \\ m(\,y_n) \end{bmatrix}, \begin{bmatrix} c(\,y_1,y_1) & \quad\cdots &\quad c(\,y_1,y_n) \\ . & \quad\cdots &\quad .\\ . & \quad\ddots &\quad . \\ c(\,y_n,y_1) & \quad\ldots &\quad c(\,y_n,y_n) \end{bmatrix} \right ) = \mathcal{N}( m(\textbf{y}), \textbf{C}). \end{eqnarray*}

For mortality modeling, GPs were introduced in Ludkovski et al. (Reference Ludkovski, Risk and Zail2018) as a data-driven approach for determining age-time dependence in mortality rates and jointly smoothing raw rates across these dimensions. The kernel

$c(\cdot ,\cdot )$

above then captures the correlation between different covariate coordinates. For example, it is expected that the mortality for age 70 in 2018, or

$c(\cdot ,\cdot )$

above then captures the correlation between different covariate coordinates. For example, it is expected that the mortality for age 70 in 2018, or

$y_j = (70;\, 2018)$

, is more correlated with

$y_j = (70;\, 2018)$

, is more correlated with

$y_p = (69;\, 2017)$

than with

$y_p = (69;\, 2017)$

than with

$y_q = (60;\, 2015)$

. The GP model provides uncertainty quantification associated with smoothed historical experience and generates full stochastic trajectories for out-of-sample forecasts. In this paper we analyze univariate GP models that work either with age

$y_q = (60;\, 2015)$

. The GP model provides uncertainty quantification associated with smoothed historical experience and generates full stochastic trajectories for out-of-sample forecasts. In this paper we analyze univariate GP models that work either with age

$y_{ag}$

or with year

$y_{ag}$

or with year

$y_{yr}$

as the sole covariate, as well as a bivariate GP model that takes in both

$y_{yr}$

as the sole covariate, as well as a bivariate GP model that takes in both

$(y_{ag}, y_{yr})$

, see Sections 4.2-4.4.

$(y_{ag}, y_{yr})$

, see Sections 4.2-4.4.

3. Pension fund population and reference mortality tables

Our analysis is motivated by a dataset summarizing mortality experience of two medium-size pension funds in Brazil that manage pension plans for employees of two firms, which in turn sponsor the pension plan, matching contributions for each one of their workers. By Brazilian law, pension funds are not allowed to write business for non-employees. Our sample is from firms with mainly office workers, belonging to the medium–high income segment. The pension fund population data comprise exposure to risk and number of deaths from 2013 to 2021 (9 years) for male and female employees and pensioners. Approximately two-thirds of the pensioners are males for both samples. Some of the pensioners, especially among the females, are surviving spouses of deceased employees.

Remark. In our dataset, the number of observed female lives and deaths was a fraction of males, leading to highly sparse exposure and mortality observations, such as the majority of ages with zero female deaths. The resulting level of sparsity rendered the female data unsuitable for robust model estimation and validation. Therefore, in the analysis below, we focus exclusively on male data. We emphasize that while our methodology is tailored to accommodate small populations (exposures on the order of

$[10^3,10^5]$

), it nevertheless assumes a minimum data richness to enable smoothing and regularization techniques and capture meaningful patterns across ages and years.

$[10^3,10^5]$

), it nevertheless assumes a minimum data richness to enable smoothing and regularization techniques and capture meaningful patterns across ages and years.

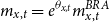

Figure 1 shows the annual time series of total exposure

$\sum _x E_{x,t}$

to risk (i.e. the number of male pensioners aggregated across ages 60–89) and the annual aggregate number of male deaths

$\sum _x E_{x,t}$

to risk (i.e. the number of male pensioners aggregated across ages 60–89) and the annual aggregate number of male deaths

$\sum _x d_{x,t}$

. There is a marked increase in the number of deaths in 2020 and 2021, probably linked to the COVID-19 pandemic. Although various extrapolation approaches could be used to smooth or impute post-COVID mortality and thus approximate a “normal” trajectory, our datasets end in 2021, and no post-pandemic observations are available. Implementing such corrections would therefore require strong assumptions about the unobserved recovery period, which could introduce more uncertainty than it resolves. For this reason, the analysis presented here relies on the observed data without attempting to reconstruct a counterfactual post-COVID path.

$\sum _x d_{x,t}$

. There is a marked increase in the number of deaths in 2020 and 2021, probably linked to the COVID-19 pandemic. Although various extrapolation approaches could be used to smooth or impute post-COVID mortality and thus approximate a “normal” trajectory, our datasets end in 2021, and no post-pandemic observations are available. Implementing such corrections would therefore require strong assumptions about the unobserved recovery period, which could introduce more uncertainty than it resolves. For this reason, the analysis presented here relies on the observed data without attempting to reconstruct a counterfactual post-COVID path.

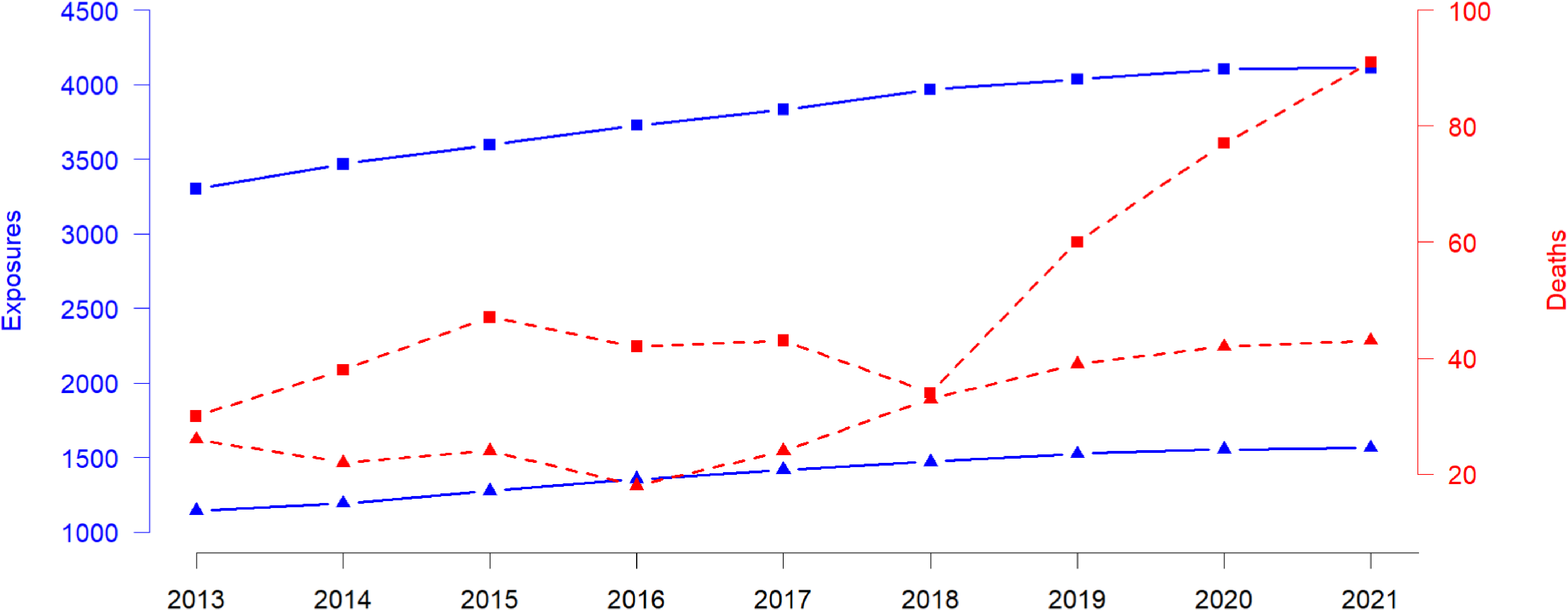

Figure 2 shows the age distribution of pensioners and deaths in the year 2018 for both pension funds when there were

$4,113$

and

$4,113$

and

$1,564$

male pensioners aged 60–89, respectively. For the primary sample, the exposure

$1,564$

male pensioners aged 60–89, respectively. For the primary sample, the exposure

$E_{x,t}$

varies from 5 (for ages close to 90) to 250 (for ages close to 70). The number of deaths

$E_{x,t}$

varies from 5 (for ages close to 90) to 250 (for ages close to 70). The number of deaths

$d_{x,t}$

in 2018 ranges from none to 7.

$d_{x,t}$

in 2018 ranges from none to 7.

Time series of total exposure

$E_{t} \,:\!=\, \sum _x E_{x,t}$

(blue solid lines) and number of deaths

$E_{t} \,:\!=\, \sum _x E_{x,t}$

(blue solid lines) and number of deaths

$d_{t} \,:\!=\, \sum _x d_{x,t}$

(red dashed lines) per year

$d_{t} \,:\!=\, \sum _x d_{x,t}$

(red dashed lines) per year

$t$

for both pension funds. Data from 2013 to 2021, males, ages 60–89, pension fund 1 (squares) and pension fund 2 (triangles).

$t$

for both pension funds. Data from 2013 to 2021, males, ages 60–89, pension fund 1 (squares) and pension fund 2 (triangles).

Age pyramids of exposures

$E_{x,t}$

(left) and number of deaths (right)

$E_{x,t}$

(left) and number of deaths (right)

$d_{x,t}$

per age

$d_{x,t}$

per age

$x$

for year

$x$

for year

$t=2018$

for the pension funds 1 and 2: ages 60–89.

$t=2018$

for the pension funds 1 and 2: ages 60–89.

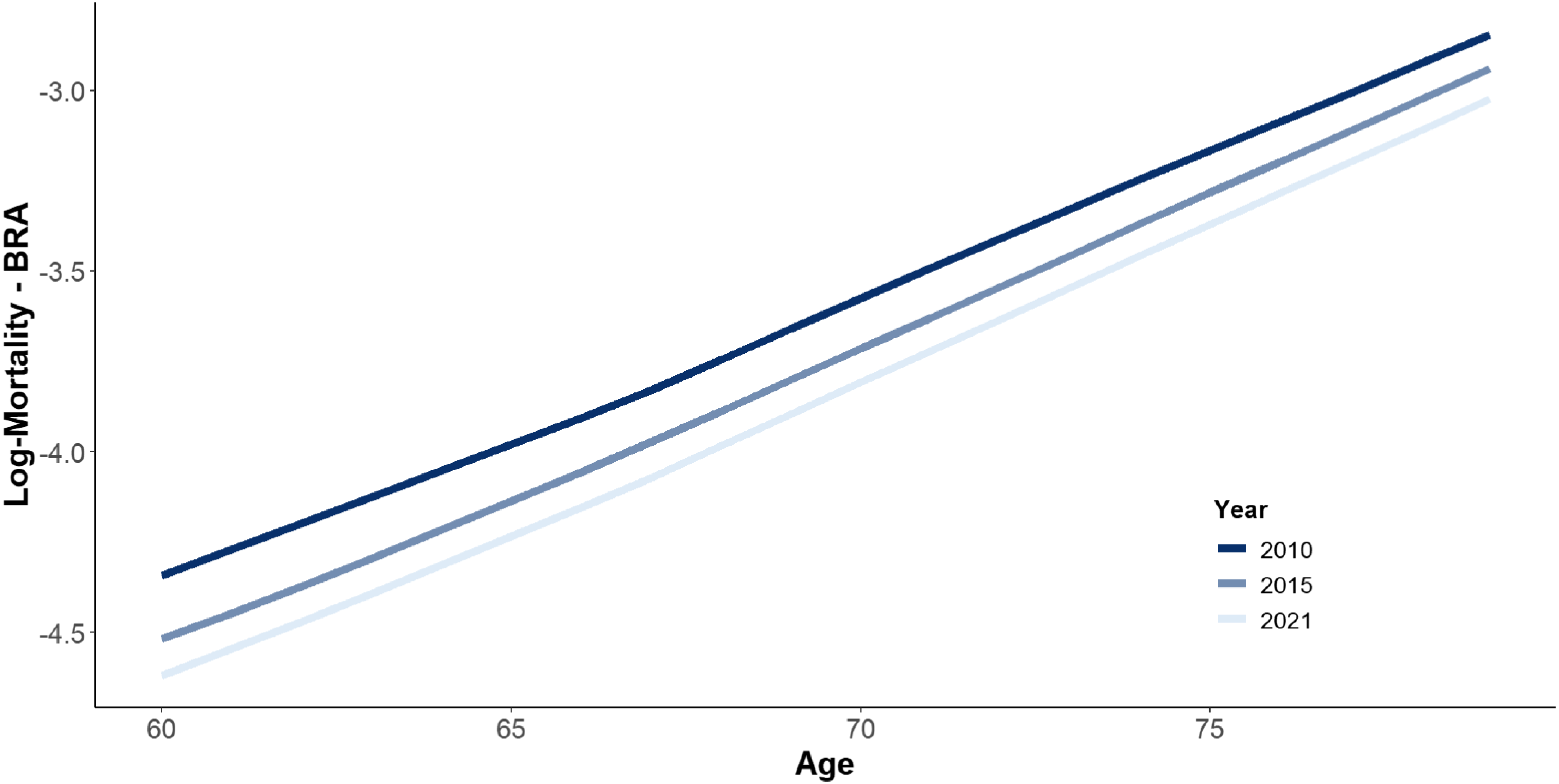

Figure 3 shows the reference Brazilian mortality tables (

$BRA$

) published by the Brazilian Institute of Geography and Statistics (IBGE, 2022).Footnote

2

Data is available from 1998 to 2021 for ages 0–80, male, female, and both genders. It is essential to keep in mind that these tables are heavily post-processed and do not represent raw data. According to IBGE (2016), the Gompertz law (mortality being exponential in age) is used to calibrate mortality rates for ages 60–80. As we are interested in older ages for the pension fund, we used the same IBGE estimated coefficients to extrapolate the mortality rates from age 81 to 89 for each year. In terms of time, the IBGE mortality tables are built based on the results of the Brazilian census, which is normally held every 10 years. The 2020 Brazilian Census was postponed to 2022 due to the COVID-19 pandemic. The BRA national mortality tables are available annually, according to an interpolation method described in IBGE (2024), which is based on a coherent Lee-Carter model; see United Nations (2015).

$BRA$

) published by the Brazilian Institute of Geography and Statistics (IBGE, 2022).Footnote

2

Data is available from 1998 to 2021 for ages 0–80, male, female, and both genders. It is essential to keep in mind that these tables are heavily post-processed and do not represent raw data. According to IBGE (2016), the Gompertz law (mortality being exponential in age) is used to calibrate mortality rates for ages 60–80. As we are interested in older ages for the pension fund, we used the same IBGE estimated coefficients to extrapolate the mortality rates from age 81 to 89 for each year. In terms of time, the IBGE mortality tables are built based on the results of the Brazilian census, which is normally held every 10 years. The 2020 Brazilian Census was postponed to 2022 due to the COVID-19 pandemic. The BRA national mortality tables are available annually, according to an interpolation method described in IBGE (2024), which is based on a coherent Lee-Carter model; see United Nations (2015).

Brazilian national population (BRA) log-mortality rates for males for years 2010/2015/2021, ages 60–80.

4. Mortality models

In this section, we introduce the approaches used to model the mortality of the pension funds’ populations that were described in Section 3. First, we introduce the simplest frameworks: the use of a predetermined mortality table with no deflator and the use of a constant deflator relative to a reference population. Then we discuss how one may add age or calendar year dependence to the deflators. We conclude the presentation of the models by introducing GP-based models. All stochastic models in this paper follow the Bayesian paradigm, implying that all parameters should be assigned prior distributions and inference should be made based on posterior distributions. Prior distributions are generally vaguely informative, but as all the hyperparameters are easily interpretable, it is expected for specialists to have some degree of expert opinion on the range of the hyperparameters.

4.1 Practitioners’ approach

The first two frameworks are common for practitioners in the insurance or pension fund industries: the use of known mortality tables with no deflator or deflated by a single fixed value for all ages. In the latter case, the fixed effect deflator model may be represented by a simple Generalized Linear Model (GLM) with a Poisson (or negative binomial) likelihood, where the offset variable is the product of the reference population mortality rates (IBGE) and the pension fund exposure. This approach is known in the industry as a loading deduction of a determined mortality/annuity table.

These two Fixed Deflator (FD) models are formally defined as:

Model FD-0 (no deflator). The number of deaths is deterministic given

$E_{x,t}$

:

$E_{x,t}$

:

\begin{align} d_{x,t} = m^{BRA}_{x,t} \cdot E_{x,t}. \end{align}

\begin{align} d_{x,t} = m^{BRA}_{x,t} \cdot E_{x,t}. \end{align}

Model FD-1 (constant deflator):

\begin{align} d_{x,t} \mid \theta , \omega &\sim \mathrm{NegBin}\left( e^{\theta } \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \,\omega \right) \nonumber\\ \theta &\sim \mathcal{N}(\!-0.5, 0.5^2) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )}, \end{align}

\begin{align} d_{x,t} \mid \theta , \omega &\sim \mathrm{NegBin}\left( e^{\theta } \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \,\omega \right) \nonumber\\ \theta &\sim \mathcal{N}(\!-0.5, 0.5^2) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )}, \end{align}

where

-

•

$\mathrm{NegBin}(\cdot , \omega )$

is a negative binomial distribution. The notation

$d \sim \mathrm{NegBin}(\mu , \omega )$

corresponds to

$\mathbb{E}[d]=\mu$

and

$\mathrm{Var}(d) = \mu (1 + \omega )$

. When

$\omega = 0$

, we recover the Poisson distribution

$d \sim \mathrm{Poi}(\mu )$

; otherwise,

$\omega$

captures the amount of variance overdispersion compared to the Poisson base case. -

•

$\theta$

is the constant deflator across all ages relative to the reference population. For example, if

$\theta = -0.5$

, then, on average, the mortality of the pension fund is

$\exp (\!-0.5) = 61\%$

of the mortality of the reference population. Above we take

$-0.5$

as the prior mean given a ballpark estimate of the deflators and the fact that the pensioners clearly have much lower mortality than the national population. See the end of Section 4.2 below for further discussion of this choice.

Note that the “model” FD-0 does not have any unknown parameters, and therefore, no prior distribution is needed. Moreover, it is not stochastic either, and it can be retrieved from the model FD-1 when

$\theta \equiv 0$

. For the bonified stochastic model FD-1, for a fixed reference population

$\theta \equiv 0$

. For the bonified stochastic model FD-1, for a fixed reference population

$i$

, both

$i$

, both

$\theta$

and

$\theta$

and

$\omega$

are unknown with priors given as above. The need to generalize from the Poisson to the negative binomial observation likelihood is driven by the well-known overdispersion of death counts, cf. Section 5.1 below.

$\omega$

are unknown with priors given as above. The need to generalize from the Poisson to the negative binomial observation likelihood is driven by the well-known overdispersion of death counts, cf. Section 5.1 below.

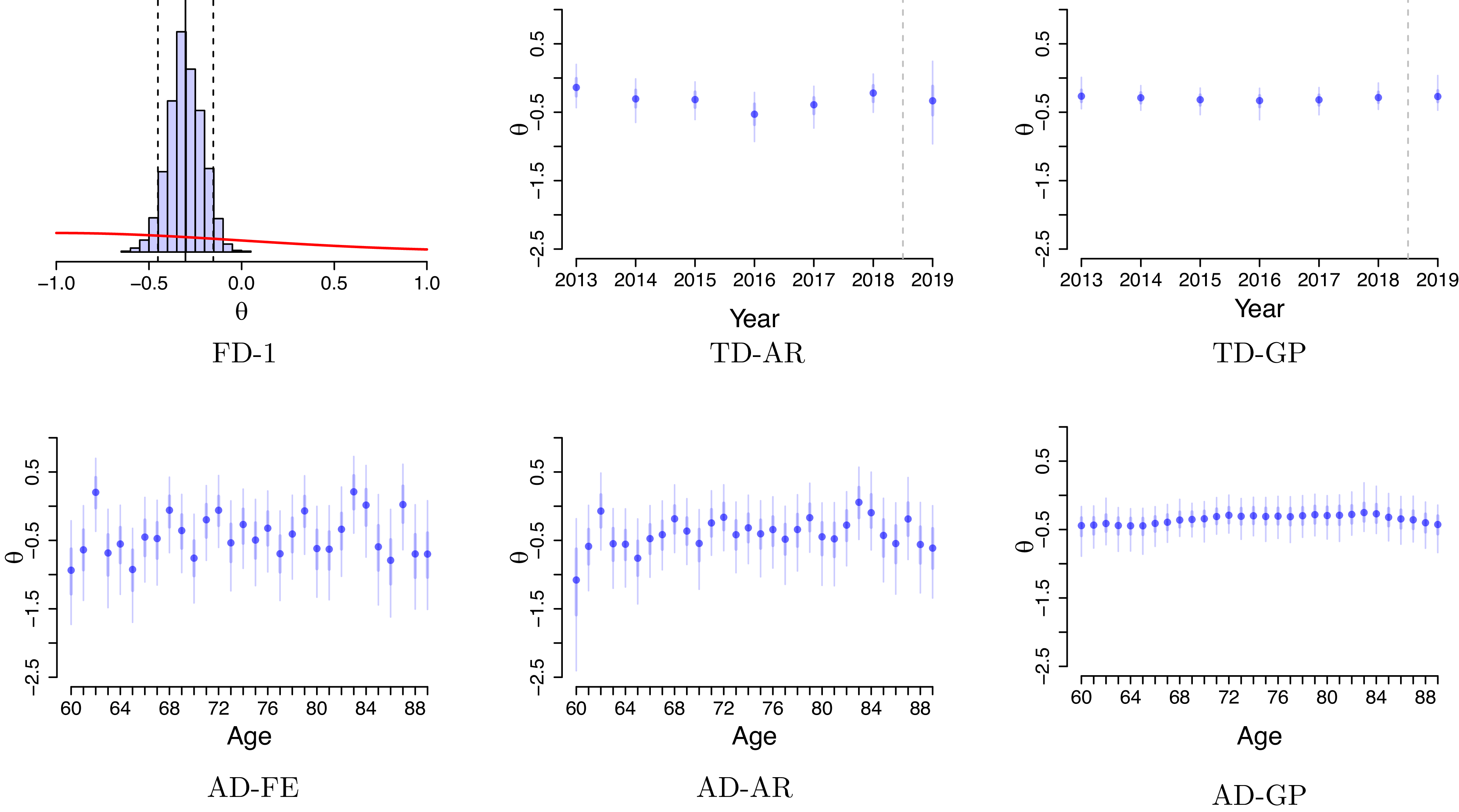

4.2 Age-dependent deflators

In this subsection, we present the age-dependent deflators’ models (AD). All three models presented share the same likelihood function, their difference being in the structure (or lack thereof) imposed on the deflators.

The age-dependent deflator fixed effects model (AD-FE) does not impose any structure on the deflators, allowing, in principle, completely unrelated deflators across ages. The model is formally defined as follows:

Model AD-FE (age-dependent deflators fixed effects):

\begin{align} d_{x,t} &\sim \mathrm{NegBin} \left ( e^{\theta _{x}} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right ) \nonumber\\ \theta _{x} &\sim \mathcal{N}(\!-0.5, 0.5^2) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )}, \end{align}

\begin{align} d_{x,t} &\sim \mathrm{NegBin} \left ( e^{\theta _{x}} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right ) \nonumber\\ \theta _{x} &\sim \mathcal{N}(\!-0.5, 0.5^2) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )}, \end{align}

where

$\theta _{x}$

is the deflator at age

$\theta _{x}$

is the deflator at age

$x$

relative to the reference population. The priors are assigned independently, see Table A.1, and are selected to maximally make the models comparable. For instance, we use the same prior mean

$x$

relative to the reference population. The priors are assigned independently, see Table A.1, and are selected to maximally make the models comparable. For instance, we use the same prior mean

$-0.5$

for

$-0.5$

for

$\theta _x$

as we did for FD-1. Note that FD-1 is a special case of AD-FE with constant

$\theta _x$

as we did for FD-1. Note that FD-1 is a special case of AD-FE with constant

$\theta _x$

across ages.

$\theta _x$

across ages.

In order to impose structure on age deflators, an autoregressive age dependence among

$\theta _{x}$

’s has been suggested. In existing literature, van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017) proposed an autoregressive structure on

$\theta _{x}$

’s has been suggested. In existing literature, van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017) proposed an autoregressive structure on

$\theta _{x}$

; Li and Lu (Reference Li and Lu2017) also use an autoregressive approach to the age-deflators, which is then applied to a reference population; Oliveira et al. (Reference Oliveira, Loschi and Assunção2021) use a random walk for

$\theta _{x}$

; Li and Lu (Reference Li and Lu2017) also use an autoregressive approach to the age-deflators, which is then applied to a reference population; Oliveira et al. (Reference Oliveira, Loschi and Assunção2021) use a random walk for

$\theta _{x}$

in terms of

$\theta _{x}$

in terms of

$x$

.

$x$

.

Model AD-AR (Age-dependent deflators with autoregressive predictor):

\begin{align} d_{x,t} \mid \theta _{x}, \omega &\sim \mathrm{NegBin} \left ( e^{\theta _{x}} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right ) \nonumber \\ \theta _{x} \mid \theta _{x-1}, \rho &\sim \mathcal{N} \left ( \mu + \rho \theta _{x-1}, 0.5^2(1-\rho ^2) \right ), \nonumber \\ \theta _{60} &\sim \mathcal{N}(\!-0.5, 0.5^2 ) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )} \nonumber \\ \rho &\sim \mathcal{N}(1, 1^2)I_{(0,1)} \nonumber \\ \mu &= -0.5 \times (1 - \rho ) . \end{align}

\begin{align} d_{x,t} \mid \theta _{x}, \omega &\sim \mathrm{NegBin} \left ( e^{\theta _{x}} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right ) \nonumber \\ \theta _{x} \mid \theta _{x-1}, \rho &\sim \mathcal{N} \left ( \mu + \rho \theta _{x-1}, 0.5^2(1-\rho ^2) \right ), \nonumber \\ \theta _{60} &\sim \mathcal{N}(\!-0.5, 0.5^2 ) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )} \nonumber \\ \rho &\sim \mathcal{N}(1, 1^2)I_{(0,1)} \nonumber \\ \mu &= -0.5 \times (1 - \rho ) . \end{align}

The structure of the AD-AR model is similar to the one used in van Berkum et al. (Reference van Berkum, Antonio and Vellekoop2017), where the prior choices ensure that the unconditional mean and variance of the deflators are the same for all ages. To see that, we first compute the mean and the variance of the deflators conditional on the autoregressive parameter

$\rho$

(which is itself random). As the prior for

$\rho$

(which is itself random). As the prior for

$\rho$

restricts its values to the interval

$\rho$

restricts its values to the interval

$(0,1)$

, the autoregressive process for

$(0,1)$

, the autoregressive process for

$\theta _{x}$

is stationary and therefore

$\theta _{x}$

is stationary and therefore

\begin{equation*}\mathbb{E}[ \theta _{x} \mid \rho ] = \frac {\mu }{1- \rho } = -0.5 \text{ and } \text{Var}(\theta _{x} \mid \rho ) = \frac {0.5^2(1-(\rho )^2)}{1-(\rho )^2} = 0.5^2.\end{equation*}

\begin{equation*}\mathbb{E}[ \theta _{x} \mid \rho ] = \frac {\mu }{1- \rho } = -0.5 \text{ and } \text{Var}(\theta _{x} \mid \rho ) = \frac {0.5^2(1-(\rho )^2)}{1-(\rho )^2} = 0.5^2.\end{equation*}

Then, using the Law of Total Expectation/Variance, we observe that

\begin{equation*}\mathbb{E}[ \theta _{x}] = \mathbb{E}[ \mathbb{E}[ \theta _{x} \mid \rho ] ] = -0.5 \end{equation*}

\begin{equation*}\mathbb{E}[ \theta _{x}] = \mathbb{E}[ \mathbb{E}[ \theta _{x} \mid \rho ] ] = -0.5 \end{equation*}

and

\begin{equation*} \mathrm{Var}(\theta _{x}) = \mathbb{E}[\mathrm{Var}(\theta _{x} \mid \rho )] + \mathrm{Var}(\mathbb{E}[\theta _{x} \mid \rho ]) = \mathbb{E}[0.5] + 0 = 0.5.\end{equation*}

\begin{equation*} \mathrm{Var}(\theta _{x}) = \mathbb{E}[\mathrm{Var}(\theta _{x} \mid \rho )] + \mathrm{Var}(\mathbb{E}[\theta _{x} \mid \rho ]) = \mathbb{E}[0.5] + 0 = 0.5.\end{equation*}

As

$\mathbb{E}[\theta _{60}] = -0.5$

and

$\mathbb{E}[\theta _{60}] = -0.5$

and

$\text{Var}(\theta _{60}) = 0.5$

, our prior assigned for the deflators in the AD-AR model is consistent with those from the AD-FE model.

$\text{Var}(\theta _{60}) = 0.5$

, our prior assigned for the deflators in the AD-AR model is consistent with those from the AD-FE model.

In both models, for a reference population, the deflators for one age depend (stochastically) on the deflator of the previous age. In the AD-AR model, the parameter

$\mu$

can be interpreted as the base level for all the deflators, regardless of age, while

$\mu$

can be interpreted as the base level for all the deflators, regardless of age, while

$\rho$

provides the strength of the dependence between any age and its preceding one. As the deflator of each age depends on the deflator of the immediately younger group, we also set a probability distribution for the first age group being analyzed, i.e. the 60-year-olds.

$\rho$

provides the strength of the dependence between any age and its preceding one. As the deflator of each age depends on the deflator of the immediately younger group, we also set a probability distribution for the first age group being analyzed, i.e. the 60-year-olds.

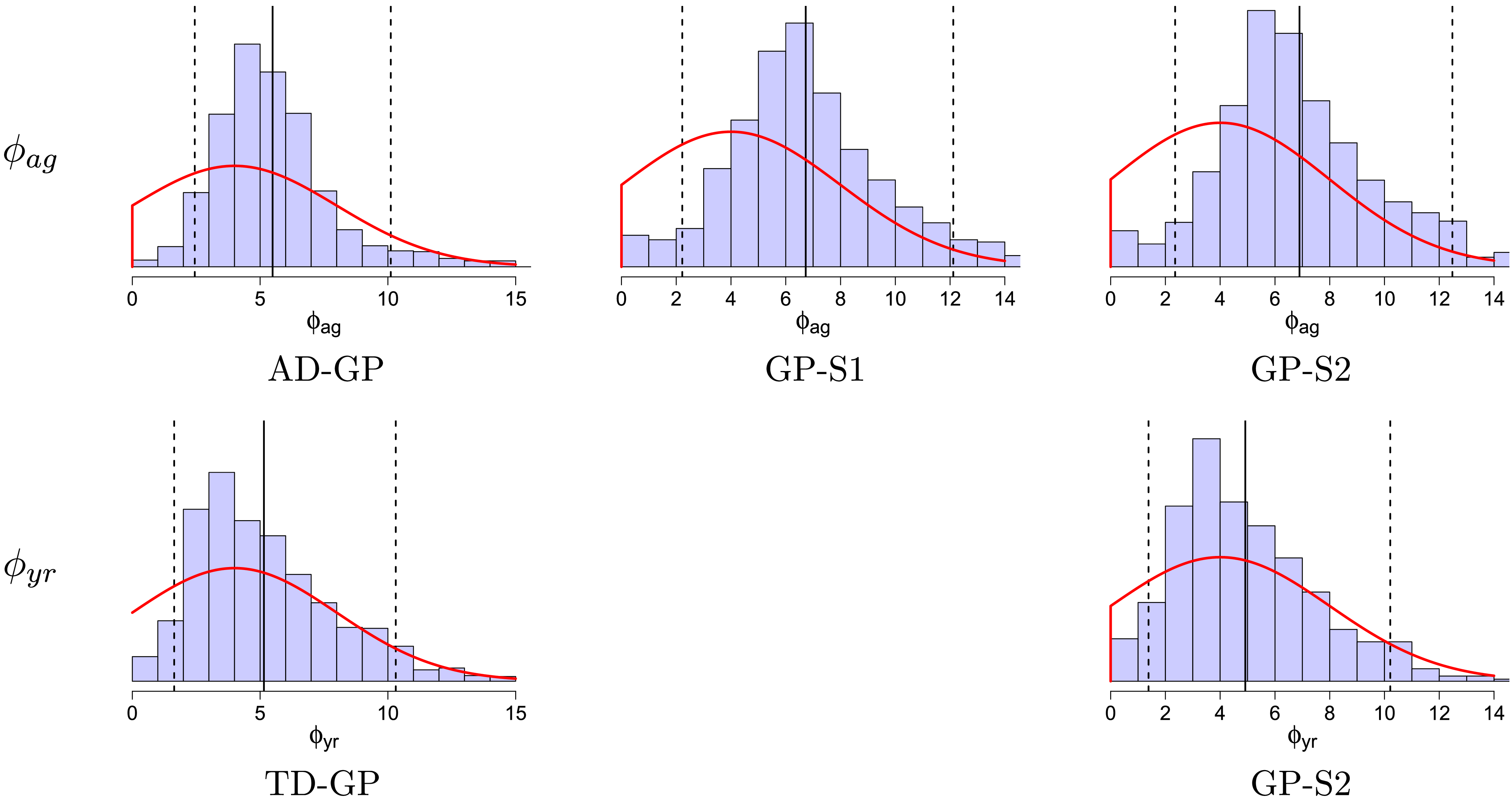

As a different generalization of AD-FE, we consider GP models for the age-dependent deflators (AD-GP) relative to the reference population. Instead of forcing an autoregressive structure across age groups, the AD-GP model postulates that the dependence between deflators for different ages is given by a Gaussian process driven by

$y_{ag}$

. We use the squared-exponential kernel that takes the form

$y_{ag}$

. We use the squared-exponential kernel that takes the form

\begin{eqnarray} c_{ag}(y_j,y_p) \,:\!=\, \sigma ^2 \exp \left (\!- \frac {\big(y_{ag}^{\,j} - y_{ag}^p \big)^2}{2\phi _{ag}^2} \right ). \end{eqnarray}

\begin{eqnarray} c_{ag}(y_j,y_p) \,:\!=\, \sigma ^2 \exp \left (\!- \frac {\big(y_{ag}^{\,j} - y_{ag}^p \big)^2}{2\phi _{ag}^2} \right ). \end{eqnarray}

This kernel has two hyperparameters: the process variance

$\sigma ^2$

and the length scale

$\sigma ^2$

and the length scale

$\phi _{ag}$

.

$\phi _{ag}$

.

For reference population

$i$

, let

$i$

, let

$x \mapsto \theta (x)$

denote now a function representing the deflator for age

$x \mapsto \theta (x)$

denote now a function representing the deflator for age

$x$

. To be consistent with the previous models, when

$x$

. To be consistent with the previous models, when

$x \in \{60, 61, \ldots , 89\}$

, we write

$x \in \{60, 61, \ldots , 89\}$

, we write

$\theta (x) = \theta _{x}$

, but the reader should note that

$\theta (x) = \theta _{x}$

, but the reader should note that

$\theta (\!\cdot\! )$

can be applied to any

$\theta (\!\cdot\! )$

can be applied to any

$x$

, even if it is not an integer value. In the AD-GP model this function is assumed a priori to follow a GP.

$x$

, even if it is not an integer value. In the AD-GP model this function is assumed a priori to follow a GP.

Model AD-GP (Age-dependent deflators with Gaussian process):

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}\left(e^{\theta ({x})} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right) \nonumber\\\theta (\!\cdot\! ) \mid \sigma , \phi _{ag} &\sim \mathrm{GP}(\!-0.5, c_{ag}(\cdot , \cdot )) \nonumber\\\omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \nonumber\\(\sigma )^2 &\sim \mathcal{N}(0.5, 0.5^2)I_{(0,\infty )} \nonumber\\ \phi _{ag} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}\left(e^{\theta ({x})} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right) \nonumber\\\theta (\!\cdot\! ) \mid \sigma , \phi _{ag} &\sim \mathrm{GP}(\!-0.5, c_{ag}(\cdot , \cdot )) \nonumber\\\omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \nonumber\\(\sigma )^2 &\sim \mathcal{N}(0.5, 0.5^2)I_{(0,\infty )} \nonumber\\ \phi _{ag} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

As an abuse of notation, the mean function in the second row above is denoted as a single number,

$-0.5$

, meaning the deflator for all ages has the same expected value a priori.

$-0.5$

, meaning the deflator for all ages has the same expected value a priori.

To interpret the structure of (2), note that the covariance reaches its maximum value

$c_{ag}(y_j,y_p) = (\sigma )^2$

when

$c_{ag}(y_j,y_p) = (\sigma )^2$

when

$y^j =y^p$

, and when the ages

$y^j =y^p$

, and when the ages

$y^j$

and

$y^j$

and

$y^p$

are far apart

$y^p$

are far apart

$c_{ag}(y^{\,j};\, y^p) \approx 0$

, so that

$c_{ag}(y^{\,j};\, y^p) \approx 0$

, so that

$\theta (y^j)$

and

$\theta (y^j)$

and

$\theta (y^p)$

are statistically independent. The length scale parameter

$\theta (y^p)$

are statistically independent. The length scale parameter

$\phi _{ag}$

controls how fast the dependence between two deflators decays in age. If

$\phi _{ag}$

controls how fast the dependence between two deflators decays in age. If

$\phi _{ag}$

is large, the dependency between two different values of the function decays very slowly, and the function

$\phi _{ag}$

is large, the dependency between two different values of the function decays very slowly, and the function

$\theta$

is expected to vary only a little, resembling almost a linear function. The process variance parameter

$\theta$

is expected to vary only a little, resembling almost a linear function. The process variance parameter

$\sigma ^2$

controls the magnitude of variation (i.e. the amplitude) of

$\sigma ^2$

controls the magnitude of variation (i.e. the amplitude) of

$\theta (\!\cdot\! )$

.

$\theta (\!\cdot\! )$

.

For a fixed age

$x$

, we have that, a priori,

$x$

, we have that, a priori,

\begin{equation*} \theta ({x}) \mid \sigma , \phi _{ag} \sim \mathcal{N} \left (\beta _{0}, (\sigma )^2 \right ). \end{equation*}

\begin{equation*} \theta ({x}) \mid \sigma , \phi _{ag} \sim \mathcal{N} \left (\beta _{0}, (\sigma )^2 \right ). \end{equation*}

Therefore,

\begin{equation*}\mathbb{E}[\theta (x)] = \mathbb{E}[ \mathbb{E}[\theta _{x} \mid \sigma , \phi _{ag} ]] = \mathbb{E}[-0.5 ] = -0.5 \end{equation*}

\begin{equation*}\mathbb{E}[\theta (x)] = \mathbb{E}[ \mathbb{E}[\theta _{x} \mid \sigma , \phi _{ag} ]] = \mathbb{E}[-0.5 ] = -0.5 \end{equation*}

and

\begin{align*} \text{Var}(\theta (x)) &= \text{Var}(\theta _{x}) = \mathbb{E}[ \text{Var}(\theta _{x} \mid \sigma , \phi _{ag} )] + \text{Var}(\mathbb{E}[\theta _{x} \mid \sigma , \phi _{ag} ]) \\ &= \mathbb{E}[ (\sigma )^2] + \text{Var}(\!-0.5) = 0.5 + 0. \end{align*}

\begin{align*} \text{Var}(\theta (x)) &= \text{Var}(\theta _{x}) = \mathbb{E}[ \text{Var}(\theta _{x} \mid \sigma , \phi _{ag} )] + \text{Var}(\mathbb{E}[\theta _{x} \mid \sigma , \phi _{ag} ]) \\ &= \mathbb{E}[ (\sigma )^2] + \text{Var}(\!-0.5) = 0.5 + 0. \end{align*}

Remark. In AD-GP, the deflator function

$\theta (\!\cdot\! )$

is taken to have the SE kernel

$\theta (\!\cdot\! )$

is taken to have the SE kernel

$c_{ag}$

(2) in age. In fact, the AD-AR model can also be viewed as a GP model with the exponential Matérn-1/2 kernel

$c_{ag}$

(2) in age. In fact, the AD-AR model can also be viewed as a GP model with the exponential Matérn-1/2 kernel

$\theta (\!\cdot\! ) \sim GP(\!-0.5, c_{M12,ag}(\cdot , \cdot ))$

, with

$\theta (\!\cdot\! ) \sim GP(\!-0.5, c_{M12,ag}(\cdot , \cdot ))$

, with

$c_{M12,ag}(y^j, y^p) = \exp (\! - \phi | y^j_{ag} - y^p_{ag})| )$

for a (distinct from

$c_{M12,ag}(y^j, y^p) = \exp (\! - \phi | y^j_{ag} - y^p_{ag})| )$

for a (distinct from

$\phi _{ag}$

) length scale hyperparameter

$\phi _{ag}$

) length scale hyperparameter

$\phi \in \mathbb{R}_+$

.

$\phi \in \mathbb{R}_+$

.

As is always the case in a Bayesian framework, it is important to revisit the prior assumptions about the model parameters. Throughout our analysis, our intent is for the priors to be mildly informative so that they are not strongly impacting the posteriors but still provide some guardrails on what is plausible. For the Brazilian pension funds in question, it is clear that the pensioners have vastly lower mortality than the IBGE reference. Consequently, we wish to start with a prior that leans towards

$\theta \lt 0$

, i.e. the deflators are negative. At the same time, we use a fairly wide prior standard deviation of 0.5. The upshot is that the precise prior mean (

$\theta \lt 0$

, i.e. the deflators are negative. At the same time, we use a fairly wide prior standard deviation of 0.5. The upshot is that the precise prior mean (

$-0.5$

everywhere above) is not so important. To illustrate this point, Figure 11 in the Online Appendix shows AD-GP results under the alternate choice of prior mean

$-0.5$

everywhere above) is not so important. To illustrate this point, Figure 11 in the Online Appendix shows AD-GP results under the alternate choice of prior mean

$\theta _i = -0.2$

. As can be observed, the resulting posterior is almost identical to the one with

$\theta _i = -0.2$

. As can be observed, the resulting posterior is almost identical to the one with

$\theta _i=-0.5$

, indicating that the data evidence strongly dominates the prior choice (as it should). Some minor upward shift in the posterior can be seen at the edges (ages less than 65 and over 85), where the influence of data is weaker. Moreover, the posterior variance is independent of the choice of the prior deflator mean, so the width of the band is invariant.

$\theta _i=-0.5$

, indicating that the data evidence strongly dominates the prior choice (as it should). Some minor upward shift in the posterior can be seen at the edges (ages less than 65 and over 85), where the influence of data is weaker. Moreover, the posterior variance is independent of the choice of the prior deflator mean, so the width of the band is invariant.

Further flexibility is provided by the opportunity to take non-constant prior means that depend on age. Indeed, expert knowledge suggests that deflators ought to be smaller for extreme old ages as the compensation law suggests convergence of respective mortality rates (see Gavrilov & Gavrilova, Reference Gavrilov and Gavrilova2005; Richards, Reference Richards2020). So far, we used a constant prior mean to make the priors of AD-GP, AD-AR, and FD-1 consistent with each other in order to facilitate their comparison. Figure 11 in the Online Appendix further demonstrates the results of AD-GP under the alternate age-dependent prior mean where

$\mathbb{E}[\theta _i] = -0.50 + (i-80)\times 0.04$

for

$\mathbb{E}[\theta _i] = -0.50 + (i-80)\times 0.04$

for

$i \gt 80$

. This represents a strong increase in the prior mean towards zero for higher ages. While the resulting posterior mean of

$i \gt 80$

. This represents a strong increase in the prior mean towards zero for higher ages. While the resulting posterior mean of

$\theta$

in Figure 11 in the Online Appendix is pulled upwards, the deflators are still declining for

$\theta$

in Figure 11 in the Online Appendix is pulled upwards, the deflators are still declining for

$x\gt 80$

, indicating that even with a strongly increasing prior trend, the evidence of the data pulls

$x\gt 80$

, indicating that even with a strongly increasing prior trend, the evidence of the data pulls

$\theta _i$

down. Also note that the width of the posterior band is almost identical to the original setting, showing that change in the prior mean has minimal influence on the posterior uncertainty.

$\theta _i$

down. Also note that the width of the posterior band is almost identical to the original setting, showing that change in the prior mean has minimal influence on the posterior uncertainty.

4.3 Time-dependent deflators

In this subsection, we present the time-dependent deflators’ models (TD), which follow the same structure as the age-dependent ones from Section 4.2. Instead of focusing on the role of age, our interest lies in introducing time-dependence for the deflators to capture the idea that the evolution of the pension funds’ mortality and of the national populations follow different trends.

When deflator-based models are used for forecasting, two distinct sources of uncertainty arise. The first is associated with projecting the reference mortality table itself (the reference trend), which in practice may be obtained using standard mortality forecasting techniques, such as Lee–Carter or its coherent extensions. The second source stems from the stochastic evolution of the deflators

$ \theta (t)$

(the deflator trend), which captures the relative divergence between the pension fund and the reference population. In our framework, these two components are conceptually distinct and assumed independent, so that their respective forecast uncertainties can be combined when constructing predictive distributions for future pension fund mortality.

$ \theta (t)$

(the deflator trend), which captures the relative divergence between the pension fund and the reference population. In our framework, these two components are conceptually distinct and assumed independent, so that their respective forecast uncertainties can be combined when constructing predictive distributions for future pension fund mortality.

Similar to the notation in Section 4.2, we denote by

$\theta (t)$

the function that returns the deflator for the year

$\theta (t)$

the function that returns the deflator for the year

$t$

when the reference population

$t$

when the reference population

$i$

is fixed. We first consider the autoregressive and the random walk specifications:

$i$

is fixed. We first consider the autoregressive and the random walk specifications:

Model TD-AR (time-dependent deflator with autoregressive predictor):

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}( e^{\theta (t)} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega ) \nonumber\\ \theta (t) \mid \theta (t-1), \rho &\sim \mathcal{N} \left ( \mu + \rho \theta (t-1), 0.5^2(1-(\rho )^2) \right ), \nonumber \\ \theta (2013) &\sim \mathcal{N}(\!-0.5, 0.5^2 ) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )} \nonumber \\ \rho &\sim \mathcal{N}(1, 1^2)I_{(0,1)} \nonumber \\ \mu &= -0.5 . (1 - \rho ). \end{align}

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}( e^{\theta (t)} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega ) \nonumber\\ \theta (t) \mid \theta (t-1), \rho &\sim \mathcal{N} \left ( \mu + \rho \theta (t-1), 0.5^2(1-(\rho )^2) \right ), \nonumber \\ \theta (2013) &\sim \mathcal{N}(\!-0.5, 0.5^2 ) \nonumber \\ \omega &\sim \mathcal{N}(0, 1^2)I_{(0,\infty )} \nonumber \\ \rho &\sim \mathcal{N}(1, 1^2)I_{(0,1)} \nonumber \\ \mu &= -0.5 . (1 - \rho ). \end{align}

Similarly to the AD-AR setup, the TD-AR model defines a parametric stochastic relationship between the mortality deflators of different calendar years. Due to its similarities, the interpretation of the parameters is the same too.

As it may be hard, a priori, to pinpoint how the deflators in different years relate to each other, we propose the TD-GP model – the equivalent of AD-GP in the time domain. The analogous calendar-year kernel is

\begin{eqnarray} c_{yr}(y_j,y_p) \,:\!=\, \sigma ^2 \exp \left (\!- \frac {(y_{yr}^{\,j} - y_{yr}^{\,p} )^2}{2\phi _{yr}^2} \right ). \end{eqnarray}

\begin{eqnarray} c_{yr}(y_j,y_p) \,:\!=\, \sigma ^2 \exp \left (\!- \frac {(y_{yr}^{\,j} - y_{yr}^{\,p} )^2}{2\phi _{yr}^2} \right ). \end{eqnarray}

Model TD-GP (time-dependent deflator with GP structure):

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}\left(e^{\theta (t)} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right) \\ \nonumber \theta (\!\cdot\! ) \mid \sigma , \phi _{yr} &\sim \mathrm{GP}(\!-0.5, c_{yr}(\cdot , \cdot )) \\ \nonumber \omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \\ \nonumber (\sigma )^2 &\sim \mathcal{N}(0.5, 0.5^2)I_{(0,\infty )} \\ \nonumber \phi _{yr} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

\begin{align} d_{x,t} \mid \theta (\!\cdot\! ), \omega &\sim \mathrm{NegBin}\left(e^{\theta (t)} \cdot m^{BRA}_{x,t} \cdot E_{x,t}, \, \omega \right) \\ \nonumber \theta (\!\cdot\! ) \mid \sigma , \phi _{yr} &\sim \mathrm{GP}(\!-0.5, c_{yr}(\cdot , \cdot )) \\ \nonumber \omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \\ \nonumber (\sigma )^2 &\sim \mathcal{N}(0.5, 0.5^2)I_{(0,\infty )} \\ \nonumber \phi _{yr} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

Once again, the GP kernel is chosen from the squared-exponential family (3), and the GP prior mean is constant across different years.

4.4 Direct modeling of the pension fund

The last set of models we consider employs Gaussian processes to model the pension fund population by itself, with no reference population. In lieu of having a baseline mortality, we de-trend the data using parametric prior means. Both a univariate GP that captures only age dependence and a bivariate age-year GP are considered. The respective prior means are (i) a Gompertz (Reference Gompertz1825) curve with no calendar year covariate (model GP-S1) and (ii) a Gompertz curve with a calendar year covariate (model GP-S2).

Model GP-S1 (S for single-population) directly captures the pension fund log-mortality

$\psi (x)$

, postulating it to be a function of age

$\psi (x)$

, postulating it to be a function of age

$x$

and employing the GP to map from

$x$

and employing the GP to map from

$x$

to

$x$

to

$\psi ({x})$

. GP-S1 assumes that the log-mortality is independent of time

$\psi ({x})$

. GP-S1 assumes that the log-mortality is independent of time

$t$

and uses a prior mean

$t$

and uses a prior mean

$\mu _{age}(x) = \beta _{0} + \beta _{ag} x$

. This linear trend in

$\mu _{age}(x) = \beta _{0} + \beta _{ag} x$

. This linear trend in

$x$

for

$x$

for

$\psi (\!\cdot\! )$

matches the Gompertz assumption of mortality growing exponentially in age. As with all GP models in this paper, the kernel is chosen as the squared-exponential family specified in (2).

$\psi (\!\cdot\! )$

matches the Gompertz assumption of mortality growing exponentially in age. As with all GP models in this paper, the kernel is chosen as the squared-exponential family specified in (2).

Model GP-S1 (single population GP with Gompertz prior):

\begin{align} d_{x,t} \mid \psi (\!\cdot\! ), \omega &\sim \mathrm{NegBin}(e^{\psi (x)} \cdot E_{x,t}, \, \omega ) \qquad \\ \nonumber \psi (\!\cdot\! ) \mid \beta _{0}, \beta _{ag}, \sigma ^2, \phi &\sim \mathrm{GP} \left ( \mu _{ag}(\!\cdot\! ), c_{ag}(\cdot , \cdot ) \right ) \\ \nonumber \mu _{ag}(x) &= \beta _{0} + \beta _{ag} (x-60) \\ \nonumber \omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \\ \nonumber \beta _{0} &\sim \mathcal{N}(\!-5, 1^2) \\ \nonumber \beta _{ag} &\sim \mathcal{N}(0.1, 0.1^2) \\ \nonumber \sigma ^2 &\sim \mathcal{N}(0.5, 0.5^2) I_{(0,\infty )} \\ \nonumber \phi _{ag} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

\begin{align} d_{x,t} \mid \psi (\!\cdot\! ), \omega &\sim \mathrm{NegBin}(e^{\psi (x)} \cdot E_{x,t}, \, \omega ) \qquad \\ \nonumber \psi (\!\cdot\! ) \mid \beta _{0}, \beta _{ag}, \sigma ^2, \phi &\sim \mathrm{GP} \left ( \mu _{ag}(\!\cdot\! ), c_{ag}(\cdot , \cdot ) \right ) \\ \nonumber \mu _{ag}(x) &= \beta _{0} + \beta _{ag} (x-60) \\ \nonumber \omega &\sim \mathcal{N}(0,1^2)I_{(0,\infty )} \\ \nonumber \beta _{0} &\sim \mathcal{N}(\!-5, 1^2) \\ \nonumber \beta _{ag} &\sim \mathcal{N}(0.1, 0.1^2) \\ \nonumber \sigma ^2 &\sim \mathcal{N}(0.5, 0.5^2) I_{(0,\infty )} \\ \nonumber \phi _{ag} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \end{align}

We emphasize that

$\psi (x)$

is now the log-mortality rate, so it is on a different scale compared to the deflators

$\psi (x)$

is now the log-mortality rate, so it is on a different scale compared to the deflators

$\theta _x$

considered in the previous section. To guarantee our prior views are consistent across all models, we compare model GP-S1 with AD-GP. Based on the likelihoods, both mortality rates should be the same, implying that

$\theta _x$

considered in the previous section. To guarantee our prior views are consistent across all models, we compare model GP-S1 with AD-GP. Based on the likelihoods, both mortality rates should be the same, implying that

\begin{equation*}e^{\psi (x)} E_{x,t} = e^{\theta _{x}} m^{BRA}_{x,t} E_{x,t} \Rightarrow \psi (x) = \theta _{x} + \log \left( m^{BRA}_{x,t}\right). \end{equation*}

\begin{equation*}e^{\psi (x)} E_{x,t} = e^{\theta _{x}} m^{BRA}_{x,t} E_{x,t} \Rightarrow \psi (x) = \theta _{x} + \log \left( m^{BRA}_{x,t}\right). \end{equation*}

Conditioning on the parameters of both models, on the one hand, we have that

\begin{align} \mathbb{E}[ \psi (x) \mid \ldots ] = \beta _{0} + \beta _{ag} (x-60) \end{align}

\begin{align} \mathbb{E}[ \psi (x) \mid \ldots ] = \beta _{0} + \beta _{ag} (x-60) \end{align}

and on the other, to have consistency with AD-GP,

\begin{align} \mathbb{E}[ \psi (x) \mid \ldots ] = \mathbb{E}[ \theta _{x} + \log ( m^{BRA}_{x,t}) \mid \ldots ]. \end{align}

\begin{align} \mathbb{E}[ \psi (x) \mid \ldots ] = \mathbb{E}[ \theta _{x} + \log ( m^{BRA}_{x,t}) \mid \ldots ]. \end{align}

Therefore, taking the expectation in (4) and (5), we would like to have

\begin{align} \mathbb{E}[\beta _{0}] + \mathbb{E}[\beta _{ag}] (x-60) = -0.5 + \log ( m^{BRA}_{x,t}), \end{align}

\begin{align} \mathbb{E}[\beta _{0}] + \mathbb{E}[\beta _{ag}] (x-60) = -0.5 + \log ( m^{BRA}_{x,t}), \end{align}

where we used the fact that under AD-GP model assumptions the unconditional mean of the deflators is set to

$-0.5$

for all ages. In order to define a reasonable prior mean for

$-0.5$

for all ages. In order to define a reasonable prior mean for

$\beta _0$

and

$\beta _0$

and

$\beta _{ag}$

we do a standard linear regression of

$\beta _{ag}$

we do a standard linear regression of

$m_{x,t}$

against

$m_{x,t}$

against

$(x-60)$

(note that

$(x-60)$

(note that

$g$

is fixed but

$g$

is fixed but

$t$

is not, so there are multiple observations for each age

$t$

is not, so there are multiple observations for each age

$x$

) and then set the prior mean of

$x$

) and then set the prior mean of

$\beta _0$

to the resulting

$\beta _0$

to the resulting

$y$

-intercept minus

$y$

-intercept minus

$0.5$

, and the prior mean of

$0.5$

, and the prior mean of

$\beta _{ag}$

to the resulting slope in

$\beta _{ag}$

to the resulting slope in

$(x-60)$

. For the population under analysis, the prior means for

$(x-60)$

. For the population under analysis, the prior means for

$\beta _0$

and

$\beta _0$

and

$\beta _{ag}$

are then chosen as, respectively,

$\beta _{ag}$

are then chosen as, respectively,

$-5.0$

and

$-5.0$

and

$0.1$

.

$0.1$

.

Remark. Placing a prior mean can be interpreted as parametrically de-trending the original data and then using the non-parametric GP to model the residuals. Because the globally imposed

$\beta$

’s in

$\beta$

’s in

$\mu _{ag}$

create a correlation between

$\mu _{ag}$

create a correlation between

$\psi (x)$

’s as

$\psi (x)$

’s as

$x$

varies, the latter residual GP should have a weaker dependence structure, i.e. a shorter length scale

$x$

varies, the latter residual GP should have a weaker dependence structure, i.e. a shorter length scale

$\phi _{ag}$

that decorrelates the above residuals relatively quickly across different ages.

$\phi _{ag}$

that decorrelates the above residuals relatively quickly across different ages.

Model GP-S2 generalizes GP-S1 by fitting a two-dimensional GP for the mortality surface in age-year. Accordingly, it also employs a bivariate prior mean that accounts for both the age

$x$

and the year

$x$

and the year

$t$

in the GP modeling the pension fund’s log-mortality. The GP kernel in this case is chosen as the separable bivariate squared exponential kernel

$t$

in the GP modeling the pension fund’s log-mortality. The GP kernel in this case is chosen as the separable bivariate squared exponential kernel

\begin{eqnarray} c(y_j,y_p) = \sigma ^2 \exp \left (\!- \frac {(y_{ag}^j - y_{ag}^p )^2}{2\phi _{ag}^2} - \frac {(y_{yr}^j - y_{yr}^p )^2}{2\phi _{yr}^2} \right ) \end{eqnarray}

\begin{eqnarray} c(y_j,y_p) = \sigma ^2 \exp \left (\!- \frac {(y_{ag}^j - y_{ag}^p )^2}{2\phi _{ag}^2} - \frac {(y_{yr}^j - y_{yr}^p )^2}{2\phi _{yr}^2} \right ) \end{eqnarray}

with three hyperparameters

$\sigma , \phi _{ag}, \phi _{yr}$

.

$\sigma , \phi _{ag}, \phi _{yr}$

.

Model GP-S2 (single population bivariate GP with linear prior mean):

\begin{align} d_{x,t} &\sim \mathrm{NegBin}(e^{\psi ({x,t})} \cdot E_{x,t}, \, \omega ) \qquad \nonumber \\ \psi (\cdot ,\cdot ) \mid \beta _{0}, \beta _{ag}, \beta _{yr}, \sigma ^2, \phi _{ag}, \phi _{yr} &\sim \mathrm{GP}( \mu _{ag,yr}(\cdot ,\cdot ), c(\cdot , \cdot )) \qquad \nonumber \\ \mu _{ag,yr}(x,t) &= \beta _{0} + \beta _{ag} (x-60) + \beta _{yr} (t-2013) \qquad \nonumber \\ \beta _{yr} &\sim \mathcal{N}(0,0.1^2) \qquad \nonumber \\ \phi _{yr} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \qquad \end{align}

\begin{align} d_{x,t} &\sim \mathrm{NegBin}(e^{\psi ({x,t})} \cdot E_{x,t}, \, \omega ) \qquad \nonumber \\ \psi (\cdot ,\cdot ) \mid \beta _{0}, \beta _{ag}, \beta _{yr}, \sigma ^2, \phi _{ag}, \phi _{yr} &\sim \mathrm{GP}( \mu _{ag,yr}(\cdot ,\cdot ), c(\cdot , \cdot )) \qquad \nonumber \\ \mu _{ag,yr}(x,t) &= \beta _{0} + \beta _{ag} (x-60) + \beta _{yr} (t-2013) \qquad \nonumber \\ \beta _{yr} &\sim \mathcal{N}(0,0.1^2) \qquad \nonumber \\ \phi _{yr} &\sim \mathcal{N}(4,4^2)I_{(0,\infty )}. \qquad \end{align}

Revisiting (6), we wish to have

\begin{equation*} \mathbb{E}[\beta _{0}] + \mathbb{E}[\beta _{ag}] x + \mathbb{E}[ \beta _{yr}] t = -0.5 + \log \left( m^{BRA}_{x,t}\right) \end{equation*}

\begin{equation*} \mathbb{E}[\beta _{0}] + \mathbb{E}[\beta _{ag}] x + \mathbb{E}[ \beta _{yr}] t = -0.5 + \log \left( m^{BRA}_{x,t}\right) \end{equation*}

which is implemented by doing a multiple linear regression of

$\log (m^{BRA}_{x,t})$

against age and calendar year

$\log (m^{BRA}_{x,t})$

against age and calendar year

$(x,t)$

(keeping reference population

$(x,t)$

(keeping reference population

$i$

fixed) and then matching the respective coefficients in age and year. and the constant term (minus the

$i$

fixed) and then matching the respective coefficients in age and year. and the constant term (minus the

$-0.5$

offset). After performing this exercise for

$-0.5$

offset). After performing this exercise for

$i=BRA$

, we choose the priors for

$i=BRA$

, we choose the priors for

$\beta _0$

,

$\beta _0$

,

$\beta _{ag}$

, and

$\beta _{ag}$

, and

$\beta _{yr}$

to be centered around

$\beta _{yr}$

to be centered around

$-5.0$

,

$-5.0$

,

$0.1$

, and

$0.1$

, and

$0$

, respectively.

$0$

, respectively.

Prior distributions for the hyper-parameters of all models are summarized in Table A.1 in Appendix A.

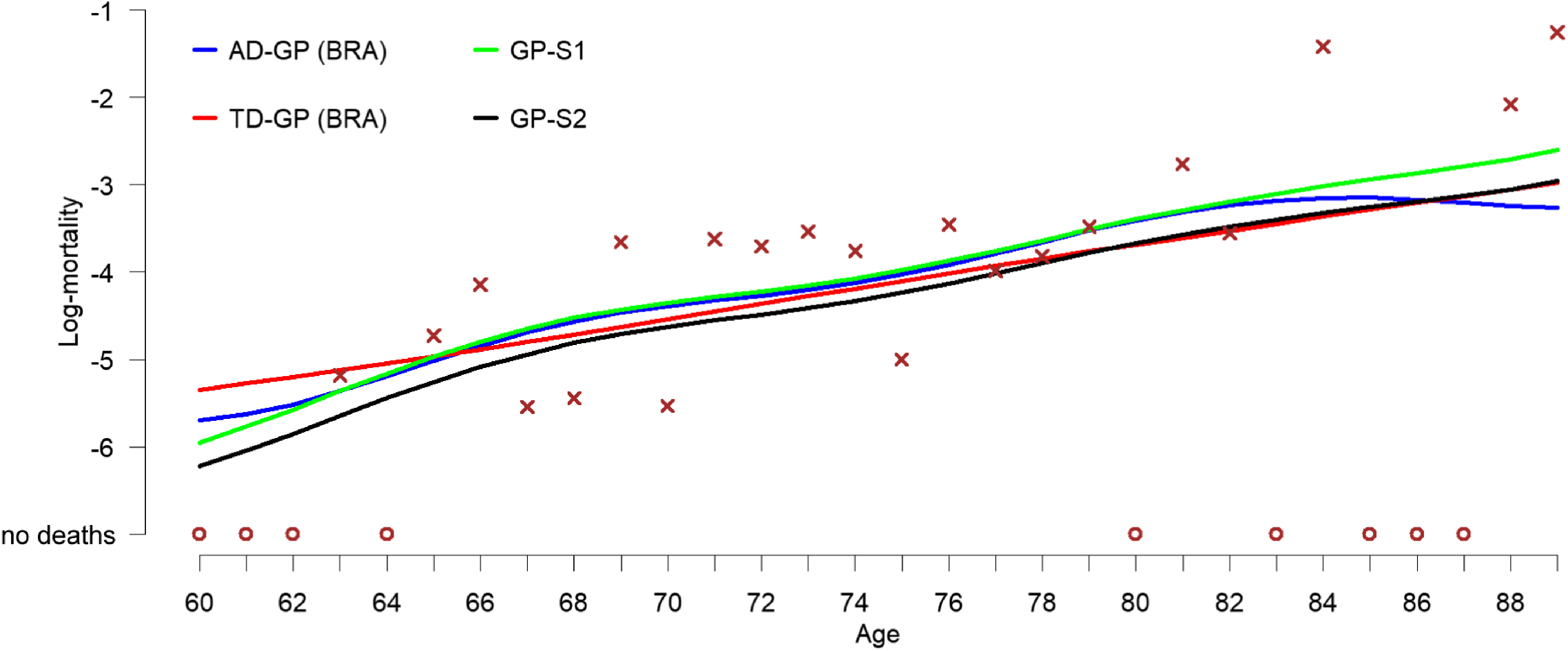

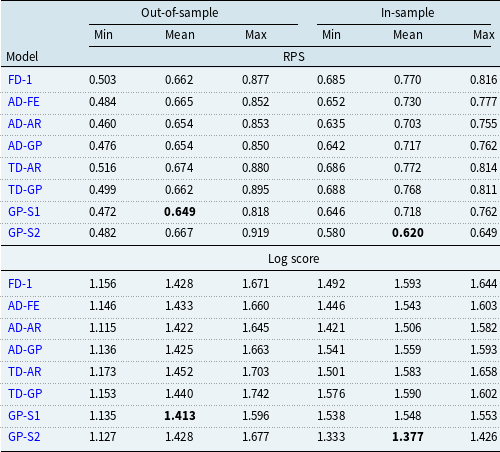

5. Fitted models

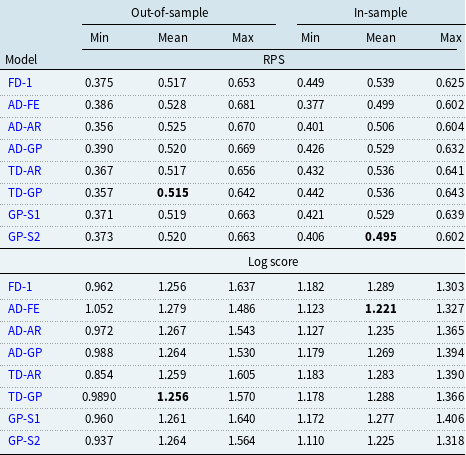

In this section, we present the results obtained from training the 8 models (FD-1, AD-AR, AD-FE, AD-GP, TD-AR, TD-GP, GP-S1, GP-S2) on pension fund 1 data from 2013 to 2018. Supplementary analysis for an alternative pension fund is presented in Appendix B.

Our models were implemented in a Bayesian framework using the Stan library in

$\texttt {R}$

(Carpenter et al., Reference Carpenter, Gelman, D.Hoffman, Lee, Goodrich, Betancourt, Brubaker, Guo, Li and Riddell2017; Stan Development Team, 2018). We implemented the GP models with a method for scaling inference of GPs with stationary kernels in Stan using the Fast Fourier Transform, as described in Hoffmann and Onnela (Reference Hoffmann and Onnela2025). We run 3 chains, each with

$\texttt {R}$

(Carpenter et al., Reference Carpenter, Gelman, D.Hoffman, Lee, Goodrich, Betancourt, Brubaker, Guo, Li and Riddell2017; Stan Development Team, 2018). We implemented the GP models with a method for scaling inference of GPs with stationary kernels in Stan using the Fast Fourier Transform, as described in Hoffmann and Onnela (Reference Hoffmann and Onnela2025). We run 3 chains, each with

$10,000$

samples, a burn-in of

$10,000$

samples, a burn-in of

$2,000$

, and a thinning factor of

$2,000$

, and a thinning factor of

$20$

. This provided

$20$

. This provided

$1,200$

samples for the posterior and predictive distributions for each model.Footnote

3

$1,200$

samples for the posterior and predictive distributions for each model.Footnote

3

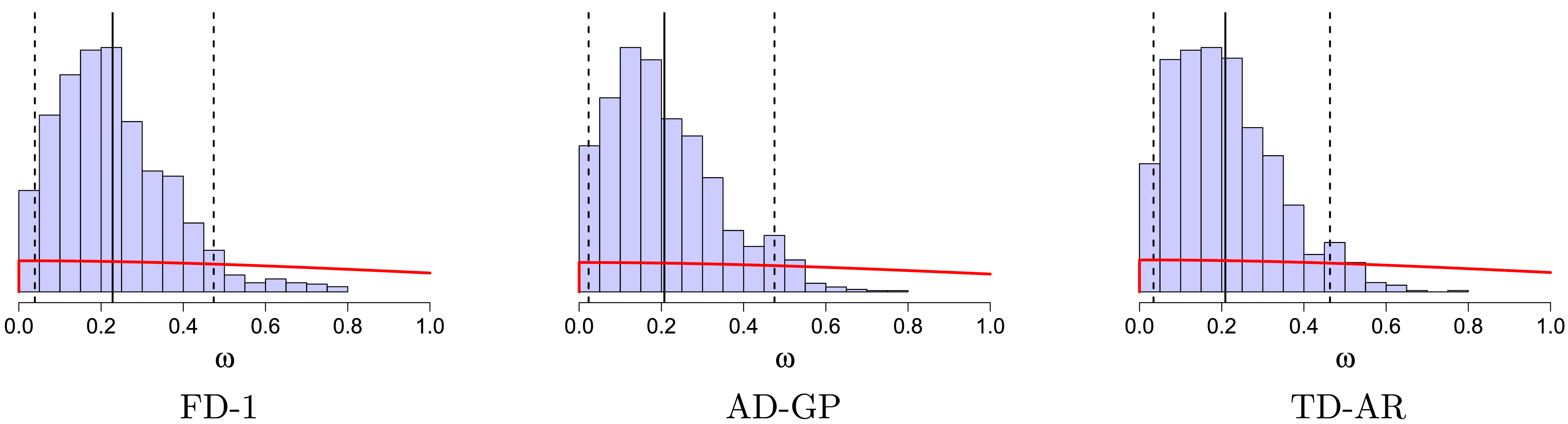

5.1 Overdispersion parameter

Since all the eight models presented are based on a negative binomial likelihood, the estimated overdispersion parameter

$\omega$

is comparable across models. The histograms of the posterior distributions of

$\omega$

is comparable across models. The histograms of the posterior distributions of

$\omega$

for several of the models are shown in Figure 4. The results are qualitatively similar: the mode of the posterior distribution of

$\omega$

for several of the models are shown in Figure 4. The results are qualitatively similar: the mode of the posterior distribution of

$\omega$

shifts to the right compared to the prior. For most models, the posterior mode is around

$\omega$

shifts to the right compared to the prior. For most models, the posterior mode is around

$0.2$

, implying that the conditioned variance of the observed number of deaths is

$0.2$

, implying that the conditioned variance of the observed number of deaths is

$20\%$

higher than its conditioned mean, confirming the expected overdispersion that has been repeatedly observed in small mortality samples. The fact that the posterior of

$20\%$

higher than its conditioned mean, confirming the expected overdispersion that has been repeatedly observed in small mortality samples. The fact that the posterior of