In an exceptional phenomenon in world history, eleven European countries, among the richest in the world, freely decided to create a monetary union in 1992, doing so during a powerful neoliberal shift. How should we explain this, and what connection is there between European monetary integration and neoliberalism? This chapter argues that monetary union cannot be reduced exclusively to its neoliberal dimension, as forging such a union was devised by European leaders before the neoliberal turn, and had numerous justifications including ones more consistent with the solidarity and the community governance of capitalism.

While the literature on the history of the European Monetary Union is extensive and convincing,1 additional archival research conducted for this book has shed new light on two neglected factors: the importance of projects for monetary cooperation devised in the 1950s and 1960s within the framework of the EEC (before the neoliberal turn); and the crucial importance of concerted stimulus in 1978, followed by German balance of payment difficulties in 1980–81, which explain the convergence towards stability-oriented policy.

This chapter will first present the theoretical argument supporting European monetary integration, in order to explain why such an original choice was made. It will then proceed chronologically, starting with the first plans devised in the 1950s and working up through the Maastricht Treaty in 1992, which created what became the eurozone.

7.1 Justifying European Monetary Union

The European Monetary Union is a surprising phenomenon. Usually, monetary unification has occurred after military conquest or national unification. For instance, the Zollverein, a customs union launched by Prussia in 1833, was supplemented by near-complete monetary union, and later by national union after the victory against France in 1871. To understand this striking phenomenon, it is important to return to the theoretical justifications for such unions (see Box 7.1). Politically, the aim was to foster European integration. Economically, the creation of a monetary union was in keeping with a market-oriented logic, according to which reducing barriers to trade boosts growth. Advocates of a solidarity approach can support a monetary union if it includes elements of redistribution (through market interventions in the event of attacks on the currency, budgetary transfers, or lower interest rates). Creating a monetary union is also consistent with the community approach, especially for the French, for whom it was important to assert a European monetary identity in the face of international competitors, the dollar in particular. The latter was the source of many problems, symbolised by the famous words of John Connally, the Treasury Secretary under US President Richard Nixon, who told Europeans worried about the fluctuations of the greenback in 1971 that ‘the dollar is our currency, but it is your problem’. The ‘exorbitant privilege’ of the dollar denounced by French Minister of Finance Valéry Giscard d’Estaing in 1964, was rooted in US geopolitical dominance. A common monetary identity would allow Europeans to influence the international monetary system, and to be more independent from the US.

Eliminates the time and costs associated with foreign exchange transactions. Removes the uncertainty linked to the exchange rate. Avoids non-cooperative monetary policies such as devaluation. Ensures a minimum convergence of economic policies. Facilitates transactions and travel, especially for the most mobile populations (tourists, students, cross-border workers, residents abroad). Ensures effective solidarity if transfer mechanisms exist. Provides lower interest rates for weaker countries. Asserts European interests in relation to other important currency areas, notably the dollar. Liberty

Solidarity

Community

The main economic disadvantage of a monetary union is the impossibility of conducting an independent exchange rate or interest rate policy suitable to every country. Central bank rules on financing government expenditure are also harmonised. This discrepancy is evident in the European Community, which includes strong-currency countries generally located in Northern Europe (except for the UK), and weak-currency countries in Southern Europe. Similar differences also exist within the same country, between highly competitive Northern Italy and less productive Southern Italy, for example. Another issue was that the Community was not an ‘optimal currency area’ as defined by Robert Mundell in 1961, because the mobility of labour and capital was too low. Such mobility is important to compensating for geographical differences in economic dynamism in the event of asymmetric shocks; for instance, Americans can easily emigrate to another state in the US in case of economic hardship. However, in this oft-quoted article, Mundell did not deny that the Community was an optimal currency area, he was merely citing arguments in both directions.2

7.2 An Old Debate on Monetary Cooperation

After 1945, the dollar’s domination pulled monetary issues into the Atlantic framework, which explains the quasi-absence of these matters in treaties involving the European communities (ECSC, EDC, EEC). In 1950, monetary exchanges were managed by the European Payments Union (EPU) associated with the Marshall Plan and the OEEC. The resumption of convertibility for European currencies in 1959 also took place within this Atlantic framework.

Monetary projects were nevertheless devised within the EEC as early as 1958.3 The Commissioner Robert Marjolin of France wanted to take advantage of the French financial crisis to strengthen the mechanisms of European solidarity, which were practically absent from the Treaty of Rome.4 His plan failed because member states were reluctant, and because the French financial recovery rendered the plan redundant. Marjolin continued to work on this project throughout the 1960s, combining his thinking with that of the Belgian-American economist Robert Triffin and Jean Monnet. Marjolin, Triffin, and Monnet developed several projects to set up a European Monetary Fund, with a view to reinforcing the mechanisms of monetary solidarity. A more intergovernmental project based on community capitalism was launched in 1966 by French Minister of the Economy and Finance Michel Debré.5 He asked the Six to form a common front against the US in connection with reforms to the international monetary system, which he accused of unduly favouring the US and facilitating money creation. He defended a purely intergovernmental vision sidelining the Commission, but his Gaullist offensive eventually lost momentum. Several Western European countries experienced monetary and financial crisis throughout the 1960s, both inside (Italy) and outside (UK) the EEC. These crises were resolved within the framework of the IMF and the Bretton Woods system, with no role for European authorities.6

The French crisis of May 1968 transformed the French franc into a weak currency again. From that point onward, France, like other weak-currency countries (Italy), demanded monetary solidarity from strong-currency countries, primarily West Germany. In the event of a crisis, Paris wanted the Bundesbank to have to buy French francs and grant credit to the Banque de France. Conversely, Bonn wanted to avoid any obligations to provide assistance to neighbours that it considered poorly managed, unless they made efforts to respect the rules of good management.7 In the 1970s, this opposition was referred to as a debate between the ‘economists’ (the Germans, who insisted on the convergence of economic policies) and the ‘monetarists’ (the French, who favoured monetary solidarity above all). The latter term was specific to this debate on monetary union, and has nothing to do with the heirs of Milton Friedman.

The debate between ‘economists’ and ‘monetarists’ started in 1969, when the Six officially began discussions on European monetary cooperation, notably at the initiative of the new German Social Democrat Chancellor, Willy Brandt.8 In early 1970, the Council asked Pierre Werner, the prime minister of Luxembourg, to draft a report on deepening monetary cooperation.9 The Werner Report, presented in October 1970, was the first to call for creating an economic and monetary union in several stages, leading to a monetary union within ten years. It reconciled the standpoints of weak-currency countries (France and Italy) that prioritised solidarity with those of strong-currency countries (Germany and the Netherlands) focused on convergence towards stability-oriented policies.

Beginning in 1971, the crisis in the international monetary system triggered two opposing effects. The monetary instability generated by the transition from fixed exchange rates to floating ones (between 1971 and 1973) made European monetary cooperation even more attractive. However, it further increased divergence among the Six, with Paris arguing for maintaining fixed exchange rates, and Bonn accepting floating rates. The latter created problems for the CAP, which was based on the same prices for all European countries. Consequently, monetary instability jeopardised a flagship European policy. To address this issue, a first monetary agreement emerged in 1972, the European Monetary Snake. It was based on a commitment to limit fluctuation margins between European currencies, and on very short-term credit agreements between central banks to implement this agreement. All member states were opposed to significant delegations of sovereignty.10 The currency turbulence following the 1973 oil crisis forced two weak currencies (the French franc and Italian lira) to leave the Snake, which was transformed into a small mark zone, resulting in the failure of European cooperation in this field.

7.3 The Impossible Concerted Recovery of 1978

In 1975–78, international monetary cooperation among Western countries was once again on the agenda. Since the oil crisis increased unemployment and lowered growth, the governments of countries in financial difficulty (the UK and Italy) and the European Trade Union Confederation (ETUC) called for a ‘concerted recovery’ among the richest Western countries. The aim was to convince the wealthiest countries to reflate (by spending more) in order to pull the weakest countries out of the crisis.11 Failing that, isolated stimulus by a single country would only result in more imports, and hence in a widened trade deficit rather than more growth. The idea was an old one: Keynes himself had visited the US in the spring of 1931 to promote concerted international action in order to combat the Great Crash.12

In 1975–77, British prime ministers, Wilson and Callaghan, pressured West Germany to revive this idea, because its balance of payments was in surplus, whereas London and Rome were at the IMF begging for financial help (the IMF rescued the UK in 1976 and Italy in 1977). Chancellor Schmidt nonetheless remained hostile to any European financial solidarity. He believed that the way out of the crisis was not to ‘print money’, since that would only encourage inflation, but to adopt stability-oriented national policies.13 The British note on the exchange between Schmidt and Callaghan ended with this ironic comment: ‘Mr Crosland [the British Foreign Secretary] commented that Chancellor Schmidt was apocalyptic in tone, bordering on bullying, and advocating a far more right-wing view than that of [opposition leader] Mrs Thatcher.’14 Schmidt presented the German example as a model in the field.

Even the French president suffered from Schmidt’s intransigence. While the French–German ‘couple’ of Valéry Giscard d’Estaing and Helmut Schmidt is often celebrated, their rapprochement on monetary issues only emerged in 1978, with profound differences prior to that. At the Luxembourg European Council in April 1976, when the weak French franc had just left the Snake, the French president asked for an expression of European solidarity in the form of a declaration.15 Schmidt refused. In early 1977, Giscard d’Estaing supported the project of concerted recovery, in which West Germany would have to make the greatest effort, although he was more moderate than Callaghan.16

In 1977, international pressure on West Germany increased as the new US President, Jimmy Carter, favoured better coordination between the three poles of North America, Western Europe, and Japan.17 He advocated the ‘locomotive’ theory, according to which West Germany and Japan should stimulate consumption to boost growth in developed countries. At the same time, the British Chancellor of the Exchequer, Denis Healey, pointed out to Schmidt that the IMF had also criticised West Germany for having too large a trade surplus, which was causing international disturbances.18 In the summer of 1978, documents from the OECD and the Commission recommended concerted economic action.

Finally, an agreement on macroeconomic policy coordination was reached at the G7 summit in Bonn on 16–17 July 1978.19 The US agreed to fight inflation and reduce its oil consumption, an important issue for Schmidt. In return, Japan and West Germany would stimulate demand (up to 1 per cent of GDP for West Germany). France had to contribute somewhat less to this stimulus, and the UK and Italy much less. Bonn accepted these concessions to ensure the success of the Bonn G7, and to support the international free trade system.

Initially the concerted recovery seemed to work, as German growth was strong in the first half of 1979. The 1979 oil shock, however, broke the momentum. It is often forgotten that West Germany ran a current account deficit for a couple of quarters around 1980. Its budget deficit widened, and became larger than that of France, while its debt was much higher.20 At the European Council, and again at the G7 meeting in Venice in June 1980, Schmidt complained that this deficit was due not only to the oil crisis, but also to the concerted recovery.21 The Bundesbank even had to resort to emergency measures to stabilise the Deutschmark on 19 February 1981.22 The bank’s archives provide a pessimistic report from its Board of Directors, which noted at its meeting on the same day that there was a ‘crisis of confidence’ in the Deutschmark because ‘Federal Germany had become a deficit country’.23 Finance Minister Hans Matthöfer attended the next meeting of the Bundesbank’s Governing Board a month later, and noted that its high interest rate policy was hampering economic expansion. However, he could not criticise it directly, due to the Bundesbank’s independence.24 The German situation was not dramatic, because its deficits were linked to cyclical causes (the oil crisis and spending by German tourists abroad), but this crisis convinced the German leader that concerted stimulus was too risky. These evolutions took place against the background of a profound cultural shift to market mechanisms.

7.4 A Cultural Shift to Market Mechanisms

In the 1970s and 1980s, norms based on free competition and private enterprise gradually took precedence over those focusing on public general interest and collective organisations. The ideological movement that structured this transformation is familiar. It originated in the growing influence, from the 1970s onwards, of neoliberal ideas, which is to say those of Hayek, Friedman, the second Chicago school, and the Virginia school. The influence of these economic thinkers was channelled through long-standing transnational networks, from the Mont Pelerin Society to transatlantic think tanks circulating ideas between Reaganites and Thatcherites.25 These networks used various intermediaries such as international institutions (like the OECD) and national leaders, with the pioneer being the dictator Augusto Pinochet of Chile and his ‘Chicago Boys’ (economists who had spent time at the University of Chicago). In 1979 Thatcher followed suit with policies that reduced taxes on companies and the highest incomes, and retrenched the welfare state, with Reagan embarking on the same path in 1981.26

This change was accentuated by the discrediting of the Marxist system. The Soviet model had already been criticised because of the violent repressions that occurred in Eastern Europe even after Stalin’s death (Berlin 1953, Budapest 1956, Berlin Wall 1961–89, Prague 1968, and Poland 1980–81). Criticism grew in the 1970s with the dissident movement, embodied by Alexander Solzhenitsyn. In the 1980s, the Soviet economy looked more inefficient than before, while in China the death of Mao in 1976 led to a successful experiment in economic liberalisation beginning in 1979. In many southern countries, the economic failure of socialist experiments also had a negative impact on Marxism.27

In the West, criticism of state inefficiency acquired a popular dimension. Antitax agitation gained a wider audience, as witnessed by the troubles with tax authorities experienced by French musicians in the 1970s, such as Michel Polnareff, Charles Aznavour, and Johnny Halliday, in addition to the Swedish actress Ingrid Bergman, who left her country in 1976 after a humiliating police investigation for tax evasion, for which she was finally acquitted.28 The actress Astrid Lingren warned of the risk of Sweden drifting towards a ‘bureaucratic dictatorship’. The Social Democrats, who had been in power since 1932, lost the elections in 1976. During those same years, the Progress Party – Mogens Gilstrup’s antitax movement in Denmark – became the second-largest political force in the country for a time, before its leader was finally sent to prison, ironically for tax evasion.29 In countries with the highest income tax brackets such as Sweden, the UK, and the US (where the top rates in 1975 were 85 per cent, 83 per cent, and 70 per cent respectively compared with 60 per cent in France), tax protests increased in the 1970s.30

Long-standing class divisions declined. In 1985, the left-wing intellectual Stuart Hall explained the success of Thatcherism by the fact that part of the working class had been severed from the left by a discourse emphasising the traditional values of order and security through ‘authoritarian populism’.31 Conversely, the traditional working class and trade union culture, sometimes driven by a masculine ethos, was less appealing to left-wing voters, who were more drawn by rising post-materialist values such as the defence of women, ethnic minorities, the environment, and human rights.32 There was also the persuasive power of neoliberal discourse. The British political economist Mark Blyth said as much when he explained how his father, a butcher by profession, told him that he would not vote Labour in 1987, because their policies were creating inflation, whereas the Conservatives’ tax cuts were going to boost growth.33

7.5 Growing Economic and Financial Constraints

The adoption of stability policies (based on low inflation and deficit targets) in the 1980s was also a response to two objective constraints: the ineffectiveness of uncoordinated Keynesian policies in the face of inflation, and financial crises. During the ‘Golden Age’ (1945–74), decision-makers could arbitrate between employment and inflation: in the event of a price spike, spending was tightened, which limited inflation but slightly increased unemployment. If unemployment rose too high, all that was needed was stimulus, which slightly increased inflation. However, after the 1973 crisis, stimulus policies often led to much higher inflation, with only a very modest rise in growth. This phenomenon of low growth and high inflation was known as ‘stagflation’. Inflation was persistent due to a fourfold rise in the price of oil in 1973, in addition to US deficits.34 Conversely, stimulus plans were hampered by the liberalisation of trade, as they tended to increase imports rather than national production. Western decision-makers gradually came to see the fight against inflation as an essential prerequisite for recovery, and therefore for reducing unemployment.

In theory, inflation is negative because it leads to uncertainty among economic agents (thereby discouraging investment and savings), poverty traps (for those whose income is not indexed), and decreased competitiveness (if trading partners have lower inflation). The only way to compensate for this deterioration in competitiveness is to devalue the currency, but that renders external financing more complicated. Money creation, or ‘money printing’, can be a way to compensate for this, but that may also revive inflation. The ultimate fear is runaway inflation, as witnessed by the hyperinflation in Germany in 1923. The German’s anti-inflationary mentality even spread to groups on the political left, including the Social Democratic Party of Germany (SPD) and the German Trade Union Confederation (DGB). In 1979, a note from the French trade union CFDT emphasised this culture of anti-inflationary ‘stability’ in the DGB.35

This concern regarding inflation went beyond elites in the 1970s. Surveys showed that it affected many segments of the Western population, which was worried about the erosion of their income and savings.36 On the left, the ETUC regularly called for intensifying the fight against inflation after 1973.37 Left-wing politicians often accused employers of creating inflation in order to increase profits.38 As a result, in the 1970s the fight against inflation was not just the prerogative of the most conservative, but also concerned a growing number of Europeans.

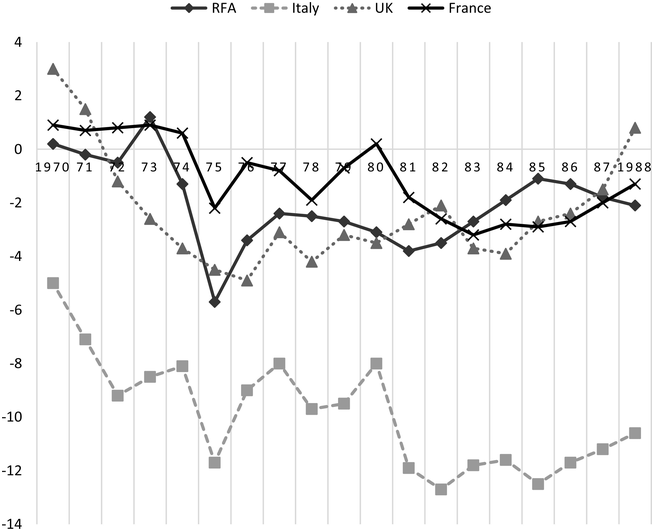

Financial crises played a major role in the turn towards a macroeconomic approach rejecting Keynesian stimulus. Financial difficulties were caused by several factors: the rising cost of energy (the price of oil increased tenfold due to the two oil shocks) and low growth led to reduced tax revenues and increased spending; the ageing population created additional burdens on the health and pension systems (even if the phenomenon remained measured at the time); and finally, the welfare state extended its prerogatives. The four major countries of Western Europe all experienced a marked deterioration in their public finances following the 1973 and 1979 oil crises (Figure 7.1).

Government account balance, 1970–87 (four countries) France, UK, FRG, Italy. Deficit or surplus as % of GNP/GDP.39

Figure 7.1 Long description

Four lines plot the evolution of public budget deficit in France, the U K, Germany, and Italy. Deficit or surplus is presented as a percentage of G N P or G D P. Overall, all deficit widened after the two oil shocks and diminished after 1983. Germany's situation became better than France's in the 1980s. The Italian situation was the worse.

These external financing problems were not unique to Western Europe in the 1970s. Dependence on external financing had already manifested itself there during post-war reconstruction, and again in France during the financial crisis of 1957–58, which prompted French negotiators to secure credit from the US and France’s European partners.40 Other countries also experienced monetary and financial difficulties in roughly the same period, such as Italy in 1964 and the UK in 1967.

This financial constraint was also visible in communist countries in the East, whose elites could hardly be accused of complacency with liberalism. In Poland and East Germany, the governments chose to take advantage of the abundant international financing made possible by the recycling of petrodollars after 1973. They borrowed massively in order to finance industrial development (exports would be used to repay the loans) and to support domestic consumption via subsidies. However, the low productivity of their industry condemned this strategy to failure.41 Faced with repayment difficulties and rising interest rates, Warsaw was forced to cut back on spending, which played a role in the massive protest movements of 1980.42 In East Berlin, Erich Honecker was determined to avoid this situation. To stem inflation, the East German state subsidised prices at exorbitant cost to state finance, accounting for up to 25 per cent of national expenditure in 1987, precipitating the system’s bankruptcy.43

The chronology of the turn towards stability policies varied geographically. It occurred first in West Germany, a country traumatised by inflation and possessing a limited Keynesian tradition. Chancellor Schmidt (1974–82) pursued a macroeconomic policy that combined the imperative of stability with targeted stimulus packages.44 This policy caused a stir within his Social Democratic Party. While on vacation in Marbella in January 1977, Schmidt explained to SPD leaders Brandt and Wehner in his Marbella Paper that the 1974 crisis differed from that of 1930. While the latter was a deflationary crisis calling for a Keynesian stimulus response, the former was an inflationary crisis. This ‘inflationary mentality’ therefore had to be destroyed in order for the recovery to proceed.45 In September 1982, the Minister of Economics Otto von Lambsdorff published a memorandum, the Lambsdorff paper, calling for the liberalisation of economic policy through deregulation, reduced government intervention, and the ‘adaptation of the social welfare system to the new conditions of growth’. These tensions led to the collapse of the SPD/FDP government and the rise to power of the Kohl government, which led a new CDU/CSU-FPD coalition. Lambsdorff once again was appointed Minister of Economics and pursued a gradual neoliberal policy (with a reduction in social benefits and civil servant salaries in real terms, corporate tax cuts, labour market flexibility, and privatisation).46 In 1983, Oskar Vetter, the former leader of the DGB, called it ‘sado-monetarism’.47

In France, the evolution was more uneven, marked by alternation between an austerity approach (1974, 1976–81) and vigorous stimulus packages (1975–76 under Jacques Chirac’s right-wing government, 1981–83 under Pierre Mauroy’s left-wing government). The Mauroy stimulus one was predicated on permanent spending increases, including a reduction in working time and a vast nationalisation programme for companies facing difficulty, which required massive injections of capital. The prospect of a financial crisis in 1983 prompted the French government to more fully convert to stability policies.

In the UK, inflation rose to an annualised rate of 24 per cent in early 1975, far higher than in continental Europe, while deficits grew. The country was named the sick man of Europe in the famous 1975 Trilateral Commission report.48 The ultimate humiliation came in 1976, when London had to turn to the IMF, which granted a loan in December of that year.49 The Callaghan government then tried to pursue a policy combining fiscal discipline, inflation control, and dialogue with unions. This high-wire act finally came crashing down when unions abandoned the government, with massive strikes during the Winter of Discontent in 1978–79.

Margaret Thatcher’s rise to power in 1979 brought a massive change in macroeconomic policy. The priority given to fighting inflation led to drastic budget cuts and credit restrictions. This policy resulted in massive protests, especially from employers who complained about high interest rates, in addition to 364 economists who signed a manifesto in 1981.50 Even within the Conservative Party, serious doubts emerged, thus explaining Thatcher’s defiant statement at the 1980 Conservative Party conference: ‘The lady’s not for turning.’ With regard to housing, the government granted long-time tenants the right to buy social housing at reduced prices and with loan facilities. This policy popularised neoliberalism while depriving the welfare state of one of its essential levers of action. In the areas of industrial and trade union policy, the change was more gradual, taking place over several years (see Chapter 5).

The evolution was similar elsewhere in the West. In the US, the turning point came with the Volcker Shock in 1979, when the new governor of the central bank, Paul Volcker, sharply raised interest rates. Ronald Reagan assumed power in 1981 and implemented a full-fledged neoliberal policy with massive tax cuts (especially for the rich) and reductions in social spending. Reagan combined this with community capitalism through increased military spending and a more aggressive trade policy. In Italy, the financial crisis of 1977, combined with the IMF intervention, led to a neoliberal shift between 1978 and 1981.51 In Northern Europe, two conservative leaders came to power in 1982 – Rudd Lubbers in the Netherlands and Poul Schlüter in Denmark – with both replacing social democratic governments and pursuing more free market policies. In the Netherlands, the Wassenar Compromise of 1982 between unions and employers established the principle of wage moderation, especially in exchange for working time arrangements. In Japan, Yakuhiro Nakasone became prime minister in 1982, and adopted Reagan’s rhetoric of government withdrawal through tax cuts and privatisation. In Canada, the neoliberal turn was prepared by the 1985 Macdonald Commission. Economic conditions improved after 1983, but growth and employment were still far below the Golden Age. This convergence towards stability-oriented policy facilitated the conclusion of the European Monetary System.

7.6 The Voluntary Constraint of the European Monetary System

In the absence of a concerted international recovery, macroeconomic policy coordination was provided by the European Monetary System (EMS), created in 1979 within the European Community. It marked a break with the past, not so much on the institutional level, since the EMS was an intergovernmental agreement (like the Snake), but on the political level, by demonstrating a desire for convergence in economic policy.

Both French President Giscard d’Estaing and Commission President Roy Jenkins had been eagerly awaiting a revival of monetary cooperation since 1977, but Chancellor Schmidt remained reluctant.52 The creation of the EMS was decided in late 1978 thanks to French–German convergence arising from three factors. The first was the good relationship between the two leaders, although their frequent clashes on numerous economic issues (see Chapter 6) shows that their good rapport was not enough on its own. Two other factors were needed to convince Schmidt and especially the (independent) Bundesbank to engage in extensive monetary cooperation in Europe: distrust in President Carter, who allowed the dollar to devalue, and Schmidt’s confidence in the anti-inflationary policies of the new French prime minister appointed in 1976, the austere Raymond Barre.53

Like the European Monetary Snake created in 1972, the EMS was a monetary stability area based on a voluntary commitment by each of its eight members (the UK refused to participate). Each country retained its currency, but had to maintain that currency’s value within a limited band of divergence from other currencies. Under the Snake, the pressure to remain within the fluctuation band fell primarily on weak currencies. Paris tried to establish a more symmetrical system by placing the adjustment burden on both countries whose currency was too weak (France and Italy) and those whose currency was too strong (West Germany).54 The French wanted to benefit from automatic German solidarity in the event of crisis, and sought assurances that the powerful Bundesbank would rescue the French franc if it was attacked on the markets.

German opposition, particularly from the Bundesbank, prevented any major institutional change. The adoption of a new unit of account, the ECU (an acronym for European Currency Unit, as well as a nod to ‘the ecu’, a medieval French currency), to serve as a reference for the exchange rate divergence indicator did not entail any obligation to intervene, nor did it prevent the Deutschmark from remaining at the centre of the system.55 If the German currency appreciated, weak-currency countries (France and Italy) bore the burden of adjustment: they had to converge with Germany’s economic policy, or their currency would risk leaving the EMS. As Chancellor Schmidt said to the Bundesbank on 30 November 1978, the EMS was a ‘bathing suit’ or ‘make-up’ used to hide the fact that France was returning to the Snake; it did not force the Bundesbank to intervene indefinitely in support of the franc.56 The EMS nevertheless created political pressure on Germany to cooperate more closely with its European partners (as the 1983 French financial crisis would eventually prove).

Similarly, for French and Italian leaders, joining the EMS would serve as a voluntary constraint, forcing them to intensify their fight against inflation in exchange for the promise of German solidarity in the event of monetary crisis. President Giscard d’Estaing’s advisor for international economic affairs was emphatically clear on the matter: ‘Our entry into the EMS is tantamount to a return to a fixed exchange rate system … It is therefore necessary to ensure, through internal money creation (treasury and credits to the economy), the adjustment needed to respect the growth objectives of the money supply. In particular, control over changes to public finances is absolutely essential.’57

The approach remained one based on liberty rather than solidarity. A solidarity mechanism was not included in the EMS due to German opposition and French reluctance. In late 1978, when the Italian Prime Minister Giulio Andreotti called for imposing rules on countries with problematic surpluses and not just those with deficits, Giscard d’Estaing did not support him.58 Similarly, the agreement creating the EMS provided for creating the European Monetary Fund (EMF) after two years (Article 1.4), but this provision remains unimplemented. Giscard d’Estaing opposed any major delegations of sovereignty, and Prime Minister Barre was not particularly interested, especially since the French franc was strong in 1979–81.59 Furthermore, Paris doubted that Italy, with its permanent financial difficulties, could join the EMS, which shows the absence of a common policy between France and Italy.60 After the change of majority in May 1981, the new socialist government in France was not interested in creating this fund either.61 The reference to ‘strengthening the instruments of European monetary solidarity’, in the draft version of the 1981 French memorandum on Europe did not appear in the final version.62

In Germany, opposition to creating the fund was even stronger, since it would have been the main contributor. A conversation between Chancellor Schmidt and Bundesbank President Pöhl in July 1980 is revelatory in this regard.63 Pöhl believed that the creation of a ‘European IMF’ would pose serious sovereignty issues. Schmidt recognised that it would be very difficult to envisage such an institution with the high inflation rates in France and Italy.64 The EMF was dead on arrival.

7.7 The 1983 French Financial Crisis: A European Turning Point

The problem of European solidarity was not theoretical, as demonstrated by the French financial crisis narrowly averted in the spring of 1983.65 The economic stimulus provided by the socialist government in 1981–82 was massive and isolated (all of France’s neighbours were still reeling from the 1979 oil shock). It soon led to a sharp increase in the trade deficit. In 1977 and 1980, the ETUC considered any attempt at a unilateral Keynesian revival in an open world to be illusory, except for targeted measures (especially for low-paid jobs).66

The French stimulus increased the budget deficit and debt, in a context in which high interest rates made borrowing expensive. The French government was one of the world’s largest borrowers on the international capital market in 1982 and 1983.67 The fall of the franc made borrowing foreign currency more expensive. Paris had to borrow from Saudi Arabia, and risked having to call on IMF assistance, as the UK had done in 1976, and Italy in 1977. Robert Lion, the Chief of Staff to Prime Minister Pierre Mauroy, summed up the general impression after a cabinet meeting in March 1982: ‘It is important that we do not give the French, or the outside world, the impression that we are going down the “British road”: that of complacency and the least effort.’68

In early 1983, the situation deteriorated with the depletion of reserves. Mitterrand was having difficulty deciding between two possible responses. The first, defended by the ‘Albanians’ (in reference to the autarchic and communist European country of Albania) and multiple ministers – including Bérégovoy (Social Affairs), Jean-Pierre Chevènement (Industry), and Laurent Fabius (Budget) – was to devalue the franc by leaving the EMS.69 It would have made French exports cheaper, but would also have increased inflation, potentially offsetting any advantage from the more favourable exchange rate. The drop in the franc’s value would likely have resulted in higher interest rates, thereby making industrial expansion more difficult.

The alternative was to pursue a policy of stability and to negotiate a measured devaluation within the framework of the EMS, with a view to gaining support from European partners in defending the parity of the franc. The main objective was to obtain Germany’s commitment (from both the government and the central bank) to defend the franc. This solution was advocated by Prime Minister Mauroy – who in 1981 had already expressed his desire to pursue a policy combining social justice and budgetary ‘rigour’70 – and by the Minister of Economy and Finance, Jacques Delors.

Mitterrand chose the second option, but the negotiations were tense, as he was asking for German solidarity in the form of a German stimulus package, monetary support, and the revaluation of the mark.71 On 18 March 1983, the German cabinet met in Bonn. The participants included: Helmut Kohl (Chancellor), Hans-Dietrich Genscher (Foreign Affairs), Jens Stoltenberg (Finance), and Karl-Otto Pöhl (Bundesbank). Stoltenberg, who had recently returned from a secret trip to Paris to meet with French officials, insisted that Germany pledge its support for France, because he was afraid that the French threat to leave the EMS was genuine.72 Delors confirmed that, for political reasons, there was a risk of protectionist measures by France if German support measures did not materialise. However, Stoltenberg ruled out the Deutschmark bearing the cost of monetary realignment alone. Kohl and Lambsdorff agreed, and supported keeping the franc in the EMS. Pöhl, the head of the Bundesbank, was more hesitant: he believed a French exit from the EMS would not be especially tragic, and in any event it was hardly in Paris’s interest to pursue a protectionist policy. Kohl finally imposed German support for the French devaluation. On 21 March 1983, the Chancellor sent a letter of support to Mitterrand.73 Kohl emphasised the link between German solidarity and French measures combatting inflation and protectionism.

The monetary operation that was finally decided upon on 21 March 1983 was a European one, since all EMS currencies were involved.74 The Bundesbank lowered rates slightly and sold Deutschmarks to limit the revaluation of the German currency. In addition, the European Community granted a loan of 4 billion ecus to France in May 1983.

France could very well have ended up before the IMF. The decisions of 1983 were not really neoliberal, since most of the welfare state reforms of 1981–82 were preserved. The Delors Plan of 1983 also included tax increases for the rich. The Communists even remained in government until 1984. The primary neoliberal measure was the end of wage indexing, but according to Thomas Piketty, the minimum wage (and the share of wages in GDP) rose much faster than productivity between 1968 and 1983.75 The policy of austerity and financial market liberalisation, which aimed to lower interest rates, was implemented by the new Prime Minister Laurent Fabius and the Minister of Economy and Finance Pierre Bérégovoy (1984–86), both of whom had been in favour of leaving the EMS in 1983. The conversion of French leaders to a stability-oriented policy also involved the opposition: when he met Chancellor of the Exchequer Nigel Lawson in November 1983, the centre-right leader Jacques Chirac praised Thatcherite policies, but criticised them for not going far enough in cutting taxes.76 London was now a model for some French leaders.

Overall, for France the choice made in 1983 was one of European and international influence rather than national withdrawal, because this policy of stability meant that the humiliation of an IMF intervention in France would be avoided.

7.8 Convergence towards a Federal Monetary Union

Despite this conversion to stability policies, the transition from an intergovernmental agreement on monetary cooperation (the EMS of 1979) to a federal monetary union at Maastricht in 1992 represented a considerable leap. It resulted from convergence among three actors: the Delors Commission, weak-currency countries (especially France), and the most powerful and reluctant actor, Germany.

In Brussels, Commission President Delors wanted to strengthen monetary cooperation right from the start, probably because he was a former Banque de France official, and as he served as the French Minister of Finance during the 1983 financial crisis.77 In early 1985, he asked Kohl and Genscher to deepen European monetary cooperation, but had no success.78 In his request Delors underscored three central ideas: reinforcing the EMS (with an obligation for strong-currency countries to intervene, and a convergence towards mixed policy combining stability and solidarity); the creation of a reserve fund to implement European solidarity and show unity in negotiations with the US; and lastly harmonisation of financial market regulation in order to facilitate the free movement of capital all while avoiding speculation. He was already thinking of giving central banks a major role. Delors therefore combined all three approaches of liberty, solidarity, and community.

During the 1985 negotiations for the Single European Act, Delors proposed creating a monetary fund, once again unsuccessfully.79 The Commission then entered the intellectual fray in order to justify monetary union as the necessary crowning achievement of the Single Market: it published several reports between 1987 and 1990, including one by the Italian economist Tommaso Padoa-Schioppa.80 The Commission had to convince Europeans that reinforcing the EMS was not sufficient (even if it involved creating a parallel currency instead of a common currency, as the British envisaged in the late 1980s). Only a fully federal monetary union would provide growth and solidarity.

In Paris, the French government felt that it had lost all monetary independence despite its stability-oriented economic policy. In Frankfurt, the Bundesbank maintained interest rates that were too high for France, but the Banque de France had to increase its rates each time its German counterpart did, otherwise devaluation would have been inevitable (creating additional challenges to funding the French economy). In September 1987, Paris and Bonn struck a compromise in the Basel–Nyborg Agreement: the French accepted the liberalisation of capital movements (leading to a European directive adopted in 1988), in exchange for an agreement in principle by the Germans to intervene in the foreign exchange market to assist weak currencies. But doubt remained in Paris over the extent of German solidarity. At the time, in 1990, Jacques de Larosière, the Governor of the Banque de France, remarked: ‘Today I am the governor of a central bank that has decided, along with his nation, to fully follow German monetary policy without voting on it. At least as part of a European central bank, I’ll have a vote.’81 Multiple French Ministers of the Economy and Finance (Balladur in 1987, Bérégovoy in 1988) had asked the Germans to consult with them more systematically over monetary matters, but the sacrosanct independence of the Bundesbank prevented any coordination. The loss of the French franc was not seen as a major loss of sovereignty by pro-Europeans. Similarly, the ban on monetary financing of the national debt, which was included in the Maastricht Treaty, was only a small concession, since this method of debt financing represented only 3 per cent of French debt in 1993.82

A major step was taken in December 1987 when the French Minister of Economy and Finance, Édouard Balladur, argued in a memorandum that the freedom of movement for capital put the prospect of a common currency managed by a common central bank back on the agenda.83 This perspective was echoed in memoranda issued the following year by the Italian Finance Minister Giuliano Amato and by the German Minister Hans-Dietrich Genscher (who spoke in his own name and not that of the German government).

Across the Rhine, the conversion was more difficult. West Germans did not want to abandon the Deutschmark, a currency that was created in 1948 even before the Federal Republic (1949), and a symbol of the new democratic Germany’s success. Nor did they wish to waste their resources by supporting countries accused of mismanagement. In 1985, Helmut Kohl justified his reluctance to strengthen monetary cooperation to the prime minister of Luxembourg, Jacques Santer. He cited past experiences of currency manipulation, especially by Hjalmar Schacht, the president of the Reichsbank during the first half of the Nazi period (1933–39).84

The key change came when Bonn secured the 1988 directive on the liberalisation of capital movements (strongly supported by the UK and the Netherlands).85 This measure was intended to both lower the cost of capital within the Community (by creating a larger market) and create indirect pressure for economic policy convergence towards the most virtuous country, otherwise capital flight would ensue. It was this agreement that convinced Kohl, during the Hanover European Council in 1988, to accept establishing a committee chaired by Delors to reflect on a future economic and monetary union. The result was the Delors Report of April 1989. It largely prefigured the economic and monetary union that was eventually adopted in the Maastricht Treaty, and implemented ten years later in the eurozone. The president of the Commission obtained the agreement of the Bundesbank president, Karl-Otto Pöhl, by accepting some of the German’s ordoliberal demands, such as the independence of the future central bank, in exchange for the single currency. Delors wanted to go even further by developing the idea of a common intervention budget, but it was shelved.86 He believed that in the long run, the European budget would reach 3 per cent of GDP (it has never exceeded 1.2 per cent) through expanded structural policies to help the poorest regions adapt to monetary union. Delors also included in his report the need to ‘coordinate the banking oversight policies of supervisory authorities’. In the end, it took the eurozone crisis (2010–12) to make this a reality.

The pressure of German reunification in 1989–90 facilitated the adoption of these ideas, especially in Bonn, where Kohl enjoyed a commanding stature that allowed him to marginalise internal opposition, and in Paris, where there was looming fear that Germany could reunify and turn away from Europe.87 The German cabinet accepted monetary union provided that it would adopt certain ordoliberal features. While this latter term was not used, German leaders consistently referred to Ordnungspolitisch, a concept denoting stability-oriented policy (low deficits, fiscal discipline, central bank independence, and free competition).88 The German cabinet’s official position on European monetary matters in 1989 also referred to the objective of a ‘high level of employment’.

At the European Council in Strasbourg held on 8–9 December 1989, Kohl agreed to initiate negotiations on a monetary union. This agreement came immediately after a meeting between Tyll Necker, the president of the employers’ association (the BDI) and Foreign Minister Genscher. Necker asked the minister to refuse monetary union, while Genscher insisted on Germany’s political duty to accept such a prospect, especially at a time of upheaval in the East.89 Once Kohl gave his own agreement and overcame internal opposition, the road to the federal monetary union was open.

7.9 Monetary Union at the Maastricht Treaty

The Maastricht Treaty, concluded in early 1992 by eleven countries (all EU members save the UK), created an economic and monetary union (known as the EMU) based on a fundamental asymmetry: while the monetary union was federal, the economic union remained intergovernmental. Member states remained free to determine their own economic policies. The Union was to be implemented in three stages between 1992 and 1999, culminating with the introduction of a single currency managed by a European Central Bank (ECB) independent of the states. To join the EMU, states had to meet stability criteria (low inflation, contained deficits and debts) as well as convergence criteria (with an inflation level and interest rates close to the eurozone average). The Treaty established multilateral monitoring, but the sanction procedure was difficult to apply because it required a two-thirds majority in the Council (not counting the votes of the state involved). The central bank was independent, and guided primarily by a ‘stability’ objective of low inflation.

An ordoliberal shift therefore occurred between the Delors Report (1989) and the Maastricht Treaty (1991). Two elements present in the former – solidarity and banking oversight – disappeared from the latter, despite appearing in the initial draft treaty presented by the Commission in 1990.90 These drafts were rejected by most European states out of opposition to the delegation of sovereignty. Moreover, for the Germans it would have been more difficult for the ECB to concentrate on price stability if it also had to take financial stability into account. This would run the risk of recapitalising weak banks.

Maastricht was the result of a compromise. Weak-currency countries such as France and Italy obtained a monetary union with the powerful Deutschmark, which allowed them to lower interest rates.91 French archives show that the negotiation was considered a success at the time, particularly because it was the Council that defined the ‘broad economic policy guidelines’: France could then benefit from more favourable financing conditions, while retaining full budgetary autonomy. What is more, while the ECB’s mandate focused primarily on inflation, Article 2 of the Protocol on the ECB also referred to the EU’s general objectives, which include ‘a high level of employment and of social protection, the raising of the standard of living and quality of life, economic and social cohesion and solidarity among Member States’. Most importantly for some French negotiators, monetary union warded off the spectre of the Community being replaced by an unregulated free trade area, a daunting but realistic prospect with the end of the Cold War.92

Germany had to abandon the Deutschmark, but in return obtained a monetary union designed to create a strong currency: the central bank was independent and oriented primarily towards the objective of low inflation, no common solidarity fund was created, no common responsibility for national debt existed, and financial assistance to a state in crisis required unanimity.

The features of the Maastricht Treaty should not be seen as an expression of German ordoliberalism alone, but rather as a consensus among governments on various ideas, such as the refusal to strengthen EU institutions beyond a certain degree (by increasing their budget), and the independence of central banks (an idea that had been gaining ground in the West throughout the 1980s). Member states opposed expanding the EU’s role in times of financial crisis.93 Incidentally, the prospect of providing financial assistance to Greece had already arisen in 1989.94

However, there was a debate regarding how to put the independence of the Central Bank into practice. In April 1989, just after the Delors Report, the socialist group at the European Parliament believed that while the future ECB should be independent in its choice of instruments, it should also be subject to the general objectives defined by the Council of Ministers in conjunction with the European Parliament. In addition to monetary stability, the group also felt that the ECB’s mandate should promote convergence in economic development.95 Similarly, during the negotiations on the Maastricht Treaty, Delors tried unsuccessfully to include provisions for some form of political control by European institutions over the ECB, while preserving its independence.96

As we have seen, the Maastricht Treaty provided for a transition towards a federal monetary union with a distinctly ordoliberal tinge, combined with an intergovernmental economic union. Solidarity was present thanks to the very existence of a monetary union that would allow the most fragile countries to benefit from low interest rates and avoid monetary crises. Community was inherently present, as a European monetary identity could be asserted vis-à-vis the dollar if the Europeans so wished. Delors used this argument in 1985, during a period of intense monetary discussions with Washington.97 The most neoliberal, such as Thatcher in London and certain North American economists, were very critical of this project, which they considered utopian. Such a surprising outcome – a federal monetary union among such powerful and differing nation states – was a bold political choice on the part of European leaders. For them, the fall of the Berlin Wall represented both an opportunity and a threat: the EU was in danger of being replaced if not consolidated. Pressure from structural economic forces, such as the internationalisation of financial movements or the Single Market programme, also played a role, but could not explain how a federal monetary union emerged as the solution, because other solutions (such as the strengthening of the EMS) could have been pursued.

7.10 Conclusion

The birth of the European Monetary Union largely based on liberty capitalism can be explained by three factors (in addition to long-term dynamics such as Europeanism). First, the conversion to more market-oriented and even neoliberal ideas was deep and influential across large segments of the population. However, these ideas were not dominant until the 1979 oil shock, and so the situation could have been different with Carter’s re-election in the US, combined with a successful concerted recovery in 1978, or even a European campaign by trade unions for shorter working hours (see Chapter 4).

Second, major economic and financial constraints resulted from the oil crises. Many European states found it more difficult to finance themselves and export goods. They came to see the lowering of inflation as a priority, so that they could later reduce unemployment. Inflation and budgetary constraints also began to affect the countries of Eastern Europe under communist rule. Even the communist government of China at the time was very sensitive to inflation, since it was aware of the role that hyperinflation played in the demise of Guomindang China in the 1940s.98 These examples from communist countries demonstrate that post-1973 financial and inflationary constraints were real, and not just the result of an ideological choice.

Third, the choice for a federal monetary union came late, since it emerged only after other avenues had failed. For a long time, ideas for monetary cooperation focused on creating a European fund that would reinforce solidarity. Such proposals were therefore not linked to a neoliberal dynamic. In the end, this idea was adopted by European leaders in the 1970s, notably with the EMS’s European Monetary Fund, but it was never fully implemented.

European solutions became more interesting after the failure of purely national approaches during financial crises or near-crises (UK in 1976, Italy and Portugal in 1977, France in 1983), as well as the limitations of the international approach, with the failure of the concerted recovery in 1978 (due to the 1979 oil shock, and to a German balance of payment crisis in 1980 that was largely ignored). In the 1980s, intergovernmental solutions such as the EMS were considered insufficient by weak-currency countries such as France and Italy, which were suffering from the Bundesbank’s high interest rate policy. Federal monetary union was paradoxically seen as a way of regaining lost international influence. Its predominantly ordoliberal features were accepted as a condition for a recovery that could include elements of solidarity. The fall of the Berlin Wall in 1989 helped to overcome opponents of this bold solution, because a federal monetary union was seen as a way to keep Germany firmly anchored in the peaceful project of European integration. There is consequently no automatic link between monetary union and neoliberalism. The surprising birth of the euro can ultimately be explained by a combination between an old pro-European project of monetary cooperation (which had existed since at least the 1960s), rising monetary and financial constraints beginning in the 1970s (which had reinforced the West German model), the limited success of alternatives (the Snake and later the EMS), and geopolitical upheavals (in 1989–92).

More generally, the Maastricht Treaty was dominated by the principle of liberty. Social Europe was present in the form of the Social Charter, social dialogue, and the broadening of competence to include environmental protection, whereas the community form of capitalism was only present in language mentioning large trans-European networks. Neoliberal Europe was expressed in certain ordoliberal clauses of the Economic and Monetary Union. For weak-currency countries, the single economic and monetary union also represented solidarity: a promise that Germany would assist them in the event of financial crisis, and an assurance of lower interest rates. Above all, many clauses of the Maastricht Treaty remained open to different interpretations, as confirmed by the ensuing decades.

Open access

Open access