Introduction

Debt financing plays a critical yet underexplored role in nonprofit capital structures and financial sustainability (Tuckman & Chang, Reference Tuckman and Chang1993; Yetman, Reference Yetman and Young2007). Debt refers to borrowed funds that organizations must repay with interest. Although often associated with for-profit firms, nonprofits increasingly use debt to bridge cash flow gaps, finance capital projects, and expand services (e.g., Calabrese & Ely, Reference Calabrese and Ely2016; Elvira-Lorilla et al., Reference Elvira-Lorilla, Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2024; Jegers & Verschueren, Reference Jegers and Verschueren2006; Lancksweerdt et al., Reference Lancksweerdt, Van Caneghem and Reheul2023). When managed responsibly, borrowing can enhance financial flexibility and support mission-critical investments, but it can also introduce risk if repayment obligations strain operating capacity. Understanding when and why nonprofits use debt is therefore central to nonprofit capital structure decisions (Bowman, Reference Bowman2002), especially in resource-constrained environments where funding is volatile and information is limited.

Despite the importance of debt financing, scholarly attention remains limited, and the literature is still emerging. Existing studies examine how extensively nonprofits rely on debt, what drives borrowing, and how leverage relates to organizational performance (e.g., Calabrese, Reference Calabrese2011; Charles et al., Reference Charles, Sloan and Butler2021; Garcia-Rodriguez et al., Reference Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2022; Yan et al., Reference Yan, Denison and Butler2009). Yet our understanding remains less developed than research on debt in the government and business sectors. Moreover, much of the nonprofit literature implicitly treats debt and equity financing as interchangeable, assuming nonprofits can readily choose between them. In practice, many nonprofits face substantial barriers to borrowing (e.g., Calabrese & Grizzle, Reference Calabrese and Grizzle2012; von Schnurbein, Reference von Schnurbein2017), leaving the determinants of nonprofit creditworthiness an underexplored question in the study of nonprofit debt.

This study addresses this understudied question in the context of Chinese nonprofits, a setting largely overlooked in the nonprofit debt literature. Over the past few decades, the Chinese nonprofit sector has grown substantially, making important contributions to education, healthcare, poverty alleviation, and environmental protection (Lu & Dong, Reference Lu and Dong2018). However, this expansion has unfolded within a restrictive regulatory environment characterized by tight government oversight, a limited philanthropic culture, and heavy reliance on government funding and priorities (Hsu et al., Reference Hsu, Hsu and Hasmath2017; Ni & Zhan, Reference Ni and Zhan2017; Spires, Reference Spires2020; Zhang & Guo, Reference Zhang and Guo2021). As a result, many Chinese nonprofits operate with constrained financial resources and face persistent challenges in sustaining their activities. Examining their access to debt provides valuable insight into the financial strategies nonprofits use under resource constraints and into how they balance mission-driven goals with financial sustainability.

In this study, grounded in signaling theory, we hypothesize that political connections, revenue diversification, and organizational size are positively associated with creditworthiness. To test these hypotheses, we analyze survey data from Chinese social service nonprofits (i.e., private non-enterprise organizations). The findings reveal a widespread and heavy reliance on debt as a financial strategy, which appears to exceed that of nonprofits in some other countries. Further analysis confirms that political connections and organizational size significantly influence creditworthiness, whereas revenue diversification does not.

This study contributes to the literature in several ways. Empirically, it represents the first investigation into debt financing by Chinese nonprofits. The evidence shows how nonprofits navigate debt in an environment where lender expectations operate alongside political oversight, which helps assess whether factors identified in studies of nonprofit debt in Western contexts also hold in an authoritarian setting. Theoretically, this study is one of the first systematic attempts to examine the factors influencing nonprofits’ creditworthiness through the lens of signaling theory. The findings suggest that signals of credibility to external lenders can include not only organizational capacity but also political embeddedness, which may be especially important where financial information is opaque and resources are constrained.

Literature review

Nonprofits typically fund their operations and growth through either equity or borrowed funds. Equity financing encompasses both internal resources accumulated through surpluses and external contributions such as donations or grants (Calabrese, Reference Calabrese2020). Together, these funds constitute a nonprofit’s equity, or net assets, which can be used to finance operations or capital projects without repayment obligations. Debt financing, by contrast, involves obtaining funds through borrowing, such as lines of credit, bank loans, mortgages, tax-exempt bonds, and leases (Yetman, Reference Yetman and Young2007). While equity financing has the advantage of not tying future revenues to debt service requirements, it demands substantial upfront cash outlays, which can strain an organization’s finances and impede growth (Denison, Reference Denison2009). Unlike for-profits, nonprofits cannot access equity markets (e.g., issuing stock), making debt an especially important tool for raising funds (Yetman, Reference Yetman and Young2007). Debt financing spreads the cost of capital assets over their useful lifespan, allowing organizations to align annual costs with benefits. It can also support day-to-day operations, serving as a financial buffer during unexpected events or as a reserve to pursue emerging opportunities (Mitchell & Calabrese, Reference Mitchell and Calabrese2019).

The existing scholarship on nonprofits’ capital structures has predominantly examined two competing theories: pecking order theory and static trade-off theory. Pecking order theory suggests that nonprofits prefer internal funds over debt financing due to higher financing costs associated with information asymmetry (Myers & Majluf, Reference Myers and Majluf1984). Conversely, static trade-off theory posits that nonprofits seek an optimal capital structure by balancing the costs and benefits of debt (Modigliani & Miller, Reference Modigliani and Miller1958). Empirical findings have been mixed. Some studies support the trade-off perspective, showing that nonprofits aim for an optimal level of debt (e.g., Bowman, Reference Bowman2002). Others suggest that nonprofits prioritize minimizing debt, consistent with pecking order theory (Calabrese, Reference Calabrese2011; Garcia-Rodriguez et al., Reference Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2022; Su et al., Reference Su, Yan and Harvey2022). Some research finds evidence consistent with both theories, with neither fully dominating (Charles et al., Reference Charles, Sloan and Butler2021).

An emerging strand of literature proposes a broader theoretical framework to explain nonprofits’ capital structures (Jegers, Reference Jegers2011; Jegers & Verschueren, Reference Jegers and Verschueren2006; Szymańska et al., Reference Szymańska, Van Puyvelde and Jegers2015). Jegers and Verschueren (Reference Jegers and Verschueren2006) argued that nonprofits’ indebtedness is influenced by three factors: equity constraints, agency conflicts, and borrowing constraints. Equity constraints, consistent with pecking order theory, suggest that nonprofits avoid debt unless internal funds are insufficient to minimize capital costs. The agency perspective holds that nonprofits may rely on debt to limit managerial discretion when managerial-board conflicts are more pronounced. Borrowing constraints recognize that even when nonprofits seek external financing, their access to credit may be limited by lenders’ perceptions of their credibility.

Despite these contributions, systematic investigations into the factors influencing nonprofits’ creditworthiness remain scarce, even though creditworthiness is a prerequisite for borrowing. Some of the existing research assumes that nonprofits have equal access to both equity and debt financing, overlooking the significant barriers many organizations face in securing debt (e.g., Calabrese & Grizzle, Reference Calabrese and Grizzle2012; von Schnurbein, Reference von Schnurbein2017). While Jegers and Verschueren (Reference Jegers and Verschueren2006) acknowledged borrowing constraints, their empirical analysis is limited, using only organizational independence as a proxy for this concept. Consequently, there remains a critical gap in understanding the determinants of nonprofits’ access to debt and the factors shaping their creditworthiness.

Hypothesis development

A significant barrier to debt financing is agency conflict, which arises when lenders lack sufficient information about a borrower’s true creditworthiness (Elvira-Lorilla et al., Reference Elvira-Lorilla, Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2024; Mitchell & Calabrese, Reference Mitchell and Calabrese2020; Petersen & Rajan, Reference Petersen and Rajan1994). In this context, information plays a critical role, as decision-making depends on acquiring accurate information, both publicly available and privately held (Connelly et al., Reference Connelly, Certo, Ireland and Reutzel2011). Information asymmetry becomes especially problematic when certain private information is inaccessible to lenders, limiting their ability to assess a borrower’s repayment capacity. Signaling theory addresses this challenge by focusing on reducing information asymmetry between two parties (Connelly et al., Reference Connelly, Certo, Ireland and Reutzel2011; Spence, Reference Spence2002). At its core, the theory posits that one party can send signals to convey otherwise unobservable qualities to another. Spence’s (Reference Spence1973) seminal work illustrates this concept by showing how job applicants can pursue higher education to signal their unobservable quality to potential employers, thereby distinguishing themselves from lower-quality candidates.

Scholars have since extended signaling theory to various fields, including management and finance. A central focus of this research is on signals of quality, which communicate unobservable attributes of organizations and, in doing so, enhance organizational legitimacy (Connelly et al., Reference Connelly, Certo, Ireland and Reutzel2011). Legitimate organizations are more likely to outperform their peers and less likely to fail (Certo, Reference Certo2003). In the nonprofit sector, legitimacy is particularly important as it strengthens trustworthiness, improves access to resources, and fosters public support (Dart, Reference Dart2004; Lecy et al., Reference Lecy, Schmitz and Swedlund2012). For example, Lancksweerdt et al. (Reference Lancksweerdt, Van Caneghem and Reheul2023) found that financial information disclosure in the nonprofit sector, a key signal of transparency and accountability, improves access to long-term credit and financial resources. Building on these insights, this study examines three key signals of creditworthiness that may enhance nonprofits’ access to debt: political connections, revenue diversification, and organizational size. These signals are theorized to reduce information asymmetry, enhance legitimacy, and provide lenders with credible indicators of a nonprofit’s ability to repay debt, thereby facilitating greater access to debt financing.

Political connections

One way organizations can build and signal creditworthiness is through their political connections, which refer to the ties they maintain with political actors (Wei et al., Reference Wei, Jia and Bonardi2023). In organizational studies, particularly within the Chinese context, these political ties often manifest as individuals with government backgrounds or experience in the party-state apparatus serving on governing boards (Tihanyi et al., Reference Tihanyi, Aguilera, Heugens, Van Essen, Sauerwald, Duran and Turturea2019; Wang, Reference Wang2022). As Pfeffer and Salancik (Reference Pfeffer and Salancik1978, p. 145) observed, “prestigious or legitimate persons or organizations represented on the focal organization’s board provide confirmation to the rest of the world of the value and worth of the organization.” Similarly, research in corporate finance has demonstrated that the reputation of board members signals governance quality, thereby enhancing a firm’s market value (e.g., Certo et al., Reference Certo, Daily and Dalton2001).

Organizations with political connections are frequently associated with stronger financial performance and improved access to external financing and resources (Faccio, Reference Faccio2006; Fisman, Reference Fisman2001). For example, studies show that political connections help nonprofits secure additional resources (Dong & Lu, Reference Dong and Lu2021; Ni & Zhan, Reference Ni and Zhan2017). These connections can also increase organizational leverage, as “implicit government guarantees” enhance creditworthiness (Tihanyi et al., Reference Tihanyi, Aguilera, Heugens, Van Essen, Sauerwald, Duran and Turturea2019). This effect is especially pronounced in highly regulated and state-influenced contexts like China, where, although the government no longer directly controls loan allocation, its support helps organizations reduce information asymmetry with lenders. This, in turn, facilitates access to external funding, particularly from state-owned banks (Brandt & Zhu, Reference Brandt, Zhu and Calomiris2007). Therefore, we hypothesize that:

H1: Nonprofits with stronger political connections have better access to debt than otherwise similar organizations.

Revenue diversification

Revenue diversification, the strategy of drawing income from a broader range of sources, is often viewed as a signal of financial stability (Froelich, Reference Froelich1999). By reducing reliance on a single or highly concentrated funding stream, nonprofits can mitigate the risks associated with the potential loss of any one source of income. Diversified revenue portfolios may enhance creditworthiness by minimizing financial vulnerability and demonstrating adaptability to funding uncertainty (Chang & Tuckman, Reference Chang and Tuckman1994; Yan et al., Reference Yan, Denison and Butler2009). These benefits are particularly strong when revenue sources are independent rather than correlated, allowing declines in one stream to be offset by others and stabilizing overall financial health. Prior research has found that diversified nonprofits experience lower revenue volatility, reduced resource dependence, and lower risk of financial distress (e.g., Carroll & Stater, Reference Carroll and Stater2009; Hung & Hager, Reference Hung and Hager2019; Lu et al., Reference Lu, Shon and Zhang2020; Trussel & Parsons, Reference Trussel and Parsons2007).

At the same time, other studies suggest that concentrated revenue structures can promote organizational efficiency and growth: concentration allows nonprofits to deepen funder relationships, reduce transaction costs, and focus managerial attention on high-yield funding opportunities (Chikoto & Neely, Reference Chikoto and Neely2014; Frumkin & Keating, Reference Frumkin and Keating2011; Lu et al., Reference Lu, Lin and Wang2019). Thus, revenue strategies involve a trade-off between stability and efficiency: diversification spreads financial risks and supports stability, while concentration strengthens focus and growth potential (Chikoto-Schultz & Neely, Reference Chikoto-Schultz and Neely2016). From a signaling perspective, however, diversification remains a more favorable indicator to creditors. A broad revenue base signals stability, financial prudence, and the ability to manage uncertainty, which are qualities lenders tend to value when assessing nonprofit borrowing capacity (Calabrese, Reference Calabrese2011; Calabrese & Ely, Reference Calabrese and Ely2016). Therefore, we hypothesize that:

H2: Nonprofits with greater revenue diversification have better access to debt than otherwise similar organizations.

Organizational size

Organizational size plays a role in nonprofits’ access to credit, primarily due to the greater information availability associated with size. Larger nonprofits often have more transparent financial and managerial disclosures, and increased public visibility, all of which reduce information asymmetry between capital markets and internal management (Harris & Neely, Reference Harris and Neely2021). For example, in the United States, the Internal Revenue Service (IRS) mandates tiered financial disclosure requirements for nonprofits, with larger organizations subject to more stringent reporting standards. While Chinese nonprofits are not legally obligated to disclose financial information to the public, research has shown that larger organizations are more likely to voluntarily make such information available (Hu et al., Reference Hu, Zhu and Kong2020). Moreover, larger organizations are often subject to external audits and regulatory scrutiny, further reinforcing their reliability in the eyes of lenders (Waymire & Mechanick, Reference Waymire and Mechanick2023).

In addition to greater transparency, organizational size signals a stronger reputation and greater certainty about an organization’s future (Garcia-Rodriguez et al., Reference Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2022; Trussel & Parsons, Reference Trussel and Parsons2007), enhancing its creditworthiness (Lancksweerdt et al., Reference Lancksweerdt, Van Caneghem and Reheul2023). In turn, larger nonprofits are more likely to possess tangible assets that can serve as collateral, strengthening their ability to secure debt (Smith, Reference Smith2012). These organizations also benefit from a track record of stability and operational capacity, providing lenders with greater assurance of repayment. By contrast, smaller nonprofits often face challenges such as limited expertise in financial management (Nitterhouse, Reference Nitterhouse1997) and insufficient infrastructure to meet reporting and compliance requirements (Hager et al., Reference Hager, Pollak, Wing and Rooney2004). As a result, smaller nonprofits may struggle to meet the demands associated with debt financing, including managing repayment schedules (Calabrese, Reference Calabrese2011). Therefore, we hypothesize that:

H3: Larger nonprofits have better access to debt than otherwise similar organizations.

Empirical context

We explore the hypotheses within the context of the Chinese nonprofit sector, specifically focusing on service delivery nonprofits—private, non-enterprise organizations.Footnote 1 Over recent decades, the Chinese nonprofit sector has expanded significantly, reflecting the country’s rapid economic and social development (Teets, Reference Teets2014). Nonprofits now play active roles across diverse fields, including education, healthcare, environmental protection, poverty alleviation, and community services. This growth has been driven by both government initiatives and the escalating needs of Chinese society, as gaps in public services and social welfare have emerged due to challenges such as urbanization, an aging population, and income inequality (Lu & Dong, Reference Lu and Dong2018; Zhou, Reference Zhou2016). Consequently, nonprofits have become important contributors to social innovation and service delivery, complementing government efforts to address complex societal challenges.

A defining feature of the Chinese nonprofit sector is the government’s pivotal role in shaping its development and operations through regulatory frameworks and financial support (Ho, Reference Ho2007; Hsu & Hasmath, Reference Hsu and Hasmath2014). While authorities encourage nonprofits to leverage their service functions to tackle social challenges, this support is often accompanied by strict oversight, particularly of their expressive functions (Spires, Reference Spires2020). For example, organizations are required to register with government agencies to gain legal status, and those that fail to comply encounter significant operational constraints (Hildebrandt, Reference Hildebrandt2011). Even legally registered nonprofits must navigate political sensitivities to maintain good standing and secure government ties (Zhan & Tang, Reference Zhan and Tang2016). Additionally, many nonprofits rely heavily on government funding through grants and contracts, creating financial dependencies that influence their priorities and limit their autonomy (Ni & Zhan, Reference Ni and Zhan2017; Wang, Reference Wang2022). In some instances, the state’s influence extends to nonprofit governance, as government-affiliated personnel may serve on boards or hold other leadership roles (Hsu & Jiang, Reference Hsu and Jiang2015).

Beyond regulatory challenges, Chinese nonprofits face significant resource constraints (Guan et al., Reference Guan, Dong and Lu2025; Hsu et al., Reference Hsu, Hsu and Hasmath2017; Zhu et al., Reference Zhu, Ye and Liu2018). For example, the philanthropic culture in China remains underdeveloped, characterized by limited private donations and a relatively small base of individual and corporate donors. Applying for government grants and contracts is highly competitive, and such funding is typically project-specific, often failing to cover full operational costs in a timely manner. As a result, many nonprofits struggle to secure sufficient financial resources or build reserves, restricting their ability to pursue long-term projects or invest in organizational development. In this resource-constrained environment, nonprofits must strategically manage their limited resources, making financial tools, such as debt financing, particularly relevant.

Debt financing is an emerging yet underexplored strategy for Chinese nonprofits, offering both opportunities and risks. Legally, there are no explicit restrictions preventing Chinese nonprofits from taking on debt, providing them with the flexibility to explore diverse financial avenues (Ministry of Finance of China, 2024). In the face of limited philanthropic support and unpredictable government funding, nonprofits may turn to debt to bridge cash flow gaps or finance capital-intensive projects, such as building facilities, upgrading medical equipment, or expanding service offerings. By leveraging debt, these organizations can secure the resources needed to undertake substantial initiatives that might otherwise be delayed or deemed unfeasible due to funding constraints. Furthermore, responsible use of debt can support strategic growth and enable nonprofits to respond more effectively to urgent community needs. For example, a healthcare nonprofit might use debt to quickly expand its facilities during a public health crisis, thereby enhancing its capacity to serve more patients and increasing its overall impact.

However, the sector encounters substantial challenges in accessing loans from financial institutions, which can limit the widespread adoption of debt financing among nonprofits. Banks and other lenders often perceive nonprofits as high-risk borrowers due to their uncertain revenue streams, limited assets, and lack of collateral, making it difficult for these organizations to secure favorable loan terms. The absence of a robust credit history and standardized financial reporting within the nonprofit sector further exacerbates this issue, as lenders may find it challenging to assess the true creditworthiness of these organizations (Du, Reference Du2022; Wang et al., Reference Wang, Huang and Arner2023). Additionally, the political sensitivities surrounding nonprofit operations in China may further complicate the borrowing process and deter lenders from extending credit.

In sum, despite the promise and challenges associated with debt financing, the use of debt by Chinese nonprofits remains largely unknown. Therefore, it is important to examine the extent to which Chinese nonprofits engage in debt financing and the factors that influence their access to debt.

Methods

Data collection

We gathered our research data through a self-administered nationwide survey targeting social service nonprofits in mainland China. To address the lack of a comprehensive nationwide database or public registry accessible for research use, we relied on the Non-Governmental Organization (NGO) Directory maintained by China Development Brief (CDB) (http://www.chinadevelopmentbrief.cn/directory). Since its inception in 2005, the CDB Directory has been continuously updated and now includes nearly 7,000 active Chinese nonprofits across various service areas. Participation in the directory is voluntary, with organizations either self-registering or responding to invitations from CDB. As a result, the Directory tends to capture nonprofits that are active, outward-facing, and organizationally stable. This may introduce selection bias and limit the representativeness of the sample. Despite these limits, prior studies have used the CDB Directory to study Chinese nonprofits and treat it as a credible source for research on nonprofit activities and financial behavior (e.g., Dong & Lu, Reference Dong and Lu2021; Zhan & Tang, Reference Zhan and Tang2016).

In June 2020, we extracted a list of 7,077 organizations from the CDB Directory. To ensure the accuracy and relevance of our sample, we cleaned the list by excluding several categories: (1) duplicate entries, (2) organizations based outside mainland China, (3) entities operating as for-profit businesses, and (4) organizations whose primary purpose diverged from service provision, such as associations and foundations. These exclusion criteria refined our sampling frame to 2,003 eligible organizations. From this refined pool, we randomly selected a sample of 700 organizations for the survey, representing approximately one-third of the sampling frame. This proportion was determined based on practical considerations related to the feasibility of contacting and maintaining communication with each organization throughout the survey process.

Prior to launching the full survey, we conducted a pilot test in July 2020 with three nonprofits based in Beijing. This pilot phase was instrumental in refining the questionnaire and optimizing survey logistics. Following the pilot, the final questionnaire was integrated into an online survey platform. In August 2020, we initiated the survey by sending invitations via email and social media to the executive directors or equivalent leaders of the selected organizations. The survey aimed to collect comprehensive information on the operations and attributes of these nonprofits during 2019. To enhance participation rates, we implemented a multi-channel engagement strategy that included landline and mobile phone outreach, email follow-ups, and three rounds of reminders over a six-week period. By mid-September 2020, we had collected 336 valid responses, achieving a response rate of 48%. After excluding responses with missing data for the analysis, our final sample comprised data from 329 organizations.

Variable measurements

To measure the dependent variable, a nonprofit’s access to debt, we used two commonly employed metrics in the nonprofit finance literature (e.g., Jegers & Verschueren, Reference Jegers and Verschueren2006; Yan et al., Reference Yan, Denison and Butler2009): a binary measure and a continuous measure. First, we constructed a debt dummy coded as 1 if a nonprofit reported any liabilities and 0 otherwise. Second, we calculated a debt ratio as total liabilities divided by total assets. This ratio reflects the extent of liabilities relative to an organization’s asset base and provides a normalized indicator of financial leverage.

These debt data were self-reported by survey respondents. Because detailed, itemized financial statements for Chinese nonprofits are generally not publicly available and organizations are often reluctant to disclose sensitive internal financial information, the survey requested summary balance sheet figures rather than disaggregated liability categories. We adopted this approach to balance data quality and response rates, since requiring itemized debt information would have made the survey more difficult to answer and reduced completion. As a result, total liabilities may include different types of obligations (for example, short-term and long-term liabilities, as well as custodial liabilities) and may capture some obligations that do not arise directly from formal borrowing decisions.Footnote 2

For independent variables, we first measured a nonprofit’s political connections by calculating the proportion of governing board members with past or present experience in the party-state apparatus, following prior research (e.g., Dong & Lu, Reference Dong and Lu2021; Haveman et al., Reference Haveman, Jia, Shi and Wang2017). A higher proportion indicates stronger political connections and deeper integration into the political framework. Second, revenue diversification was assessed using the Hirschman–Herfindahl Index (HHI), a well-established measure of concentration and diversification in revenue streams. This study examines five primary revenue sources: government funding, charitable donations, earned income, investment income, and other sources. The HHI is calculated as:

where Ri represents the proportion of each of the five revenue sources relative to the nonprofit’s total revenue. The resulting HHI value ranges from 0 to 1, with higher values indicating greater revenue diversification (Yan et al., Reference Yan, Denison and Butler2009). Third, organizational size was measured by the nonprofit’s total assets (log-transformed) to reflect its capacity and operational scale. Larger organizations benefit from greater information availability, stronger reputations, and increased certainty, all of which enhance their credibility and attractiveness to lenders compared to smaller counterparts.

In addition, we included several control variables in our analysis. Organizational age was calculated based on each nonprofit’s founding year, with older organizations potentially benefiting from established reputations and longer operational histories, which may enhance their credibility. Board size was measured by the total number of board members within each nonprofit. A larger board size may indicate greater governance capacity, a broader range of expertise, and more extensive social networks, all of which could influence financial decision-making processes (Callen et al., Reference Callen, Klein and Tinkelman2010).

Service change was assessed by evaluating changes in the scale of a nonprofit’s programs and services between 2018 and 2019. Respondents rated this change on a 5-point scale, where 1 represented a “significant decrease,” 2 a “slight decrease,” 3 “no change,” 4 a “slight increase,” and 5 a “significant increase.” Controlling for service change is important as fluctuations in program and service delivery may influence financial behaviors, including decisions related to debt financing. To account for the broader resource environment in which nonprofits operate, we also controlled for the per capita Gross Domestic Product (GDP) (log-transformed) of the prefectural city where each nonprofit is based.Footnote 3 GDP data were obtained by asking nonprofits to report the prefectural city of their operations, followed by extracting the corresponding GDP and population size from the provincial Statistical Yearbook of each city.

Finally, we controlled for the service areas of nonprofits, recognizing that organizations in different sectors may operate within distinct task environments. Due to the absence of a standardized categorization system for nonprofit service areas in China, we asked each survey respondent to identify their primary service area. Using this information, we classified each nonprofit’s service area according to the International Classification of Non-profit and Third Sector Organizations (ICNP/TSO). Table 1 details the distribution of service areas among the nonprofits in our sample.

Descriptive statistics (N = 329)

Table 1. Long description

The table consists of five columns: Variable, Mean, S D (Standard Deviation), Min, and Max.

Section 1: Descriptive Statistics

* Debt dummy: Mean 0.659, S D 0.475, Min 0, Max 1.

* Debt ratio: Mean 0.508, S D 0.851, Min 0, Max 8.

* Political connections: Mean 0.039, S D 0.121, Min 0, Max 1.

* Revenue diversification: Mean 0.296, S D 0.292, Min 0, Max 0.963.

* Organizational size: Mean 3.502, S D 1.865, Min 0, Max 9.705.

* Organizational age: Mean 7.637, S D 4.414, Min 1, Max 29.

* Board size: Mean 5.779, S D 3.295, Min 0, Max 33.

* Service change: Mean 3.459, S D 1.209, Min 1, Max 5.

* Resource environment: Mean 11.471, S D 0.549, Min 8.745, Max 12.595.

Section 2: Service area percentages

* Culture, communication, and recreation activities: 0.91.

* Education services: 6.34.

* Human health services: 1.81.

* Social services: 31.72.

* Environmental protection and animal welfare activities: 8.16.

* Community and economic development, and housing activities: 31.72.

* Professional, scientific, accounting, and administrative services: 2.11.

* Others: 17.22.

Note: The numbers for service areas refer to the percentages service areas represented in our final sample. Service area classification is based on the ICNP/TSO.

Results

Table 1 reports descriptive statistics of the variables under study. The data reveal key insights into the overall debt profile of the nonprofits under study. Of the 329 nonprofits analyzed, 66% (mean = 0.659) reported holding debt, underscoring the significant adoption of borrowing as a financial strategy. The debt ratio, which measures the proportion of total assets financed through debt, had an average value of 0.51, with considerable dispersion (standard deviation = 0.85) and a maximum ratio of 8.0. These findings highlight both the prevalence of debt as a financial strategy and the significant variability in debt levels within the Chinese nonprofit sector.

It is useful to compare the debt information of Chinese nonprofits with patterns reported in other countries. The literature on nonprofit debt remains limited, which constrains systematic cross-country comparisons. However, existing evidence provides some reference points. Elvira-Lorilla et al. (Reference Elvira-Lorilla, Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2024) found that charities in England and Wales have an average debt ratio of 0.26. Jegers and Verschueren (Reference Jegers and Verschueren2006) observed that Californian nonprofits have an average debt ratio of 0.22, with 43% of organizations holding no debt, while Charles (Reference Charles2018) reported that U.S. arts and culture nonprofits have an average debt ratio of 0.22. Across U.S. nonprofits and subsectors, Calabrese (Reference Calabrese2011) found an average debt ratio of 0.40. While these figures are not directly comparable due to institutional, economic, and regulatory differences, the available evidence suggests that Chinese nonprofits in our sample appear to carry higher levels of debt. This indicates that debt may function as a more central financial tool for Chinese nonprofits than for nonprofits in many Western contexts.

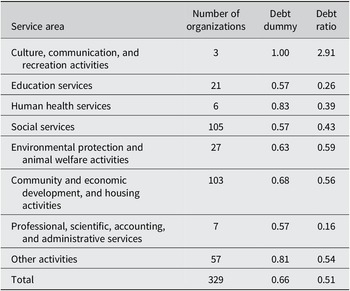

Table 2 presents debt information for nonprofits across various service areas. Culture, communication, and recreation nonprofits reported the highest debt prevalence, with 100% of organizations holding debt and the highest average debt ratio of 2.91. In contrast, nonprofits in education services, social services, and professional, scientific, accounting, and administrative services exhibited lower debt prevalence, with only 57% of organizations in each category holding debt. Among these, professional, scientific, accounting, and administrative services, as well as education services, reported the lowest average debt ratios (0.16 and 0.26, respectively). Nonprofits in community and economic development and housing activities demonstrated a higher debt prevalence (68%) and a moderate debt ratio of 0.56. Organizations engaged in environmental protection and animal welfare, as well as human health services, also exhibited relatively high debt prevalence at 63% and 83%, respectively, with average debt ratios of 0.59 and 0.39. Lastly, nonprofits categorized under other activities reported high debt prevalence (81%) and an average debt ratio of 0.54. These findings highlight the significant prevalence of debt financing among nonprofits and the notable variations in debt levels and ratios across different service areas.

Nonprofits’ debt levels by service area

Table 2. Long description

The table contains four columns and nine rows of data.

* Culture, communication, and recreation activities: 3 organizations, 1.00 debt dummy, 2.91 debt ratio.

* Education services: 21 organizations, 0.57 debt dummy, 0.26 debt ratio.

* Human health services: 6 organizations, 0.83 debt dummy, 0.39 debt ratio.

* Social services: 105 organizations, 0.57 debt dummy, 0.43 debt ratio.

* Environmental protection and animal welfare activities: 27 organizations, 0.63 debt dummy, 0.59 debt ratio.

* Community and economic development, and housing activities: 103 organizations, 0.68 debt dummy, 0.56 debt ratio.

* Professional, scientific, accounting, and administrative services: 7 organizations, 0.57 debt dummy, 0.16 debt ratio.

* Other activities: 57 organizations, 0.81 debt dummy, 0.54 debt ratio.

* Total: 329 organizations, 0.66 debt dummy, 0.51 debt ratio.

To further examine factors underlying variation in nonprofits’ access to debt, we estimated two models aligned with our dependent variables. We applied logistic regression to the debt dummy and ordinary least squares (OLS) regression to the continuous debt ratio. For the OLS regression, the debt ratio was winsorized at the 5th/95th percentiles to limit the influence of extreme values and then log-transformed to reduce right skew and improve linear fit. Both the logistic and OLS models use robust standard errors to address potential heteroscedasticity. Results are reported in Table 3 and show broadly consistent patterns for the key explanatory variables.

Regression results

Table 3. Long description

The table contains three columns: Variable, Debt dummy, and L n debt ratio.

* Political connections: Debt dummy 2.766 (standard error 1.403, p < 0.05); L n debt ratio 0.197 (standard error 0.113, p < 0.1).

* Revenue diversification: Debt dummy 0.064 (standard error 0.435); L n debt ratio 0.080 (standard error 0.062).

* Organizational size: Debt dummy 0.392 (standard error 0.075, p < 0.01); L n debt ratio 0.023 (standard error 0.010, p < 0.05).

* Organizational age: Debt dummy minus 0.043 (standard error 0.029); L n debt ratio minus 0.003 (standard error 0.004).

* Board size: Debt dummy minus 0.044 (standard error 0.039); L n debt ratio minus 0.003 (standard error 0.006).

* Service change: Debt dummy minus 0.211 (standard error 0.106, p < 0.05); L n debt ratio 0.002 (standard error 0.035).

* Resource environment: Debt dummy 0.226 (standard error 0.233); L n debt ratio minus 0.012 (standard error 0.015).

* Service area: Yes for both models.

* Constant: Debt dummy minus 1.982 (standard error 2.693); L n debt ratio 0.476 (standard error 0.473).

* Observations: 329 for both models.

* Chi-squared: 52.69 (p < 0.01) for Debt dummy.

* F-statistic: 2.45 (p < 0.01) for L n debt ratio.

* Pseudo R-squared: 0.123 for Debt dummy.

* R-squared: 0.109 for L n debt ratio.

Note: Robust standard errors in parentheses; *** p < 0.01, ** p < 0.05, * p < 0.1.

Political connections emerged as a significant predictor of both debt dummy and debt ratio. Nonprofits with a higher proportion of governing board members with party-state experience were more likely to hold debt (p < 0.05) and exhibited higher debt ratios (p < 0.1). These findings support H1, suggesting that political ties may enhance a nonprofit’s creditworthiness by reducing information asymmetry and signaling stability and trustworthiness to lenders. This aligns with prior research highlighting the role of political connections in improving access to financial resources in the Chinese context.

Organizational size also showed a significant positive association with both debt dummy and debt ratio. Larger nonprofits, as measured by total assets, were more likely to hold debt (p < 0.01) and had slightly higher debt ratios (p < 0.05). This finding supports H3, underscoring the role of organizational size in enhancing transparency, reputation, and operational stability, making larger nonprofits more attractive to creditors.

In contrast, revenue diversification was not a significant predictor in either model (p > 0.1). Although diversification is often viewed as a stabilizing financial strategy, its lack of significance in this study may suggest that Chinese lenders prioritize more observable signals, such as organizational size and political connections, when evaluating a nonprofit’s creditworthiness. Therefore, H2 is not supported.

Beyond the key variables, some control variables warrant attention. Specifically, service change was negatively and significantly associated with the debt dummy (p < 0.05), suggesting that nonprofits experiencing growth in programs and services are less likely to access debt. Other control variables did not show significant effects on either the debt dummy or debt ratio.

Discussion and conclusion

The use of debt has become increasingly common among nonprofit organizations as a legitimate and cost-effective means of financing (Calabrese & Ely, Reference Calabrese and Ely2016; Garcia-Rodriguez et al., Reference Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2022). While a growing body of literature has begun to examine nonprofit debt, existing studies have predominantly focused on Western contexts, leaving a gap in understanding how nonprofits in non-Western settings engage with borrowing. This study addresses this gap by providing the first empirical investigation into debt use among Chinese nonprofits. The findings offer preliminary evidence on the prevalence and antecedents of debt financing in Chinese nonprofits and point to mechanisms that may matter beyond China, such as the role of political ties and organizational scale in shaping access to credit in environments with constrained resources and limited transparency. By expanding the literature on nonprofit debt, this study provides new insight into the financial strategies of nonprofits operating under distinct institutional conditions and contributes to a broader understanding of borrowing behavior and its drivers.

This study provides preliminary evidence on the extent of debt use among Chinese nonprofits, addressing an area previously unexplored in the literature. Our findings reveal that nearly two-thirds (66%) of Chinese nonprofits report holding debt, with an average debt ratio of 51%, meaning that about half of their total assets are financed through debt. This level of debt use appears higher than what has been reported among nonprofits in Western contexts, where studies have generally found debt ratios in the range of 20%–40% (e.g., Calabrese, Reference Calabrese2011; Garcia-Rodriguez et al., Reference Garcia-Rodriguez, Romero-Merino and Santamaria-Mariscal2022; Lancksweerdt et al., Reference Lancksweerdt, Van Caneghem and Reheul2023; Su et al., Reference Su, Yan and Harvey2022). The more widespread and heavier reliance on debt in China likely reflects its role as a critical financing strategy in an environment characterized by constrained philanthropic support, unpredictable government funding, and regulatory uncertainty (Hsu et al., Reference Hsu, Hsu and Hasmath2017; Ni & Zhan, Reference Ni and Zhan2017; Zhang & Guo, Reference Zhang and Guo2021). At the same time, this reliance carries risk. Debt can provide short-term stability and allow nonprofits to sustain services, but high leverage may increase financial vulnerability if repayment capacity is weak. To balance debt use with long-term financial sustainability, nonprofits should monitor leverage, align borrowing with reliable revenue, maintain buffers such as cash reserves, and avoid excessive dependence on debt.

This study advances the nonprofit debt literature by providing preliminary insights into the factors shaping nonprofits’ access to debt, using signaling theory to explain how organizations mitigate information asymmetries in credit markets. The findings identify two key signals that enhance creditworthiness: stronger political connections and larger organizational size. These results underscore the role of credible signals in reducing lender uncertainty and improving debt access. In an authoritarian setting, political connections function not only as a channel to resources but also as a visible certification of legitimacy under government oversight. This differs from most applications of signaling theory in market settings, where lenders rely more heavily on audited financial indicators and asset strength. Here, signals tied to political embeddedness appear to substitute for formal disclosure and serve as assurances of stability and reliability. By demonstrating how nonprofits leverage political ties and organizational scale to strengthen their financial standing, this study extends signaling theory to the nonprofit sector. It shows that what counts as a credible signal depends on the institutional environment in which nonprofits operate, particularly the level of state involvement and the transparency of financial information. In doing so, this research contributes to the broader literature on nonprofit capital structure and financial strategy.

Beyond its theoretical contributions, this study offers practical insights for nonprofits and lenders. Nonprofits can improve their access to debt by making credible signals more visible to lenders. Recruiting respected individuals, including former officials or recognized experts, to serve on governing boards can function as a public endorsement of legitimacy and capacity. Such ties are costly to imitate because high-status individuals are unlikely to affiliate with weak or poorly managed organizations (Certo et al., Reference Certo, Daily and Dalton2001; Ho, Reference Ho2007). Building ongoing working relationships with government agencies and documenting program performance can also help signal stability and competence. These steps allow nonprofits to present themselves as lower-risk borrowers in settings where lenders may have limited access to reliable financial information. By contrast, easily imitable signals provide little credible information and do not materially reduce lender uncertainty (Connelly et al., Reference Connelly, Certo, Ireland and Reutzel2011).

Effective signals must also be easy for lenders to observe and interpret, especially in credit decisions where lenders face time and capacity constraints (Goranova et al., Reference Goranova, Alessandri, Brandes and Dharwadkar2007; Janney & Folta, Reference Janney and Folta2003). Signals that are hard to observe may fail to influence borrowing even if they reflect real strengths. This may help explain why revenue diversification does not show a significant effect in our analysis. Prior work suggests that diversification should enhance financial stability, yet lenders may not reward it because it is not a readily visible signal. Revenue diversification is a financial characteristic that is rarely highlighted in loan applications, and assessing it requires detailed review of multiple revenue streams across time. That type of review is costly and may be unrealistic in practice. In contrast, more visible indicators such as board composition, evidence of government ties, and organizational size are easy for lenders to identify and interpret, and therefore function as more effective signals of creditworthiness. This suggests that nonprofits seeking to strengthen their position with lenders should not only manage finances responsibly, but also increase transparency around capacity, oversight, and reliability in ways that are immediately legible to external audiences.

This study has several limitations that present avenues for future research. First, the findings are based on cross-sectional data, which cannot establish causality. Future research could take advantage of longitudinal data to investigate the causal relationships between the variables. For example, examining how gaining or losing political ties affects subsequent borrowing could provide stronger evidence of causality and deepen understanding of how political dynamics shape nonprofit financial decisions. Second, our measures of debt are based on total reported liabilities rather than liabilities disaggregated by type, which means they may capture obligations beyond formal borrowing. Future research should collect more granular liability information that distinguishes short-term and long-term borrowing from custodial or pass-through obligations, so that analyses can focus more specifically on debt financing decisions. Third, while the study examines some key explanatory variables informed by signaling theory, other factors not included in the analysis may also influence nonprofits’ access to debt, such as financial health, governance quality, and the presence of endowments. Incorporating these variables in future studies could provide a more comprehensive understanding of nonprofits’ creditworthiness.

Fourth, several key measures, including political connections, are based on self-reported survey data. Although we reviewed responses and followed up with organizations to clarify missing or unclear information, self-reporting may still introduce bias. Fifth, the sample consists of a relatively small group of Chinese nonprofits that are active and outward-facing. This may limit representativeness, so caution is needed in generalizing the findings. Finally, future work could complement this quantitative analysis with qualitative evidence, such as interviews with nonprofit executives and lenders, to provide deeper insight into how debt decisions are made in practice.

Despite these limitations, this study provides preliminary evidence from a non-Western context and helps explain the factors that shape Chinese nonprofits’ access to debt. The results suggest practical implications for both nonprofits and lenders. For nonprofits, visible signals such as credible board members, managerial capacity, and working relationships with public agencies can help reduce lender uncertainty and improve access to credit. For lenders, these same observable features can serve as indicators of reliability when financial disclosure is limited. By highlighting these dynamics, the study lays a foundation for future comparative and theoretical work on nonprofit debt financing across diverse institutional environments.

Funding statement

This research receives no funding.

Competing interests

The authors report there are no competing interests to declare.

Open access

Open access