1. Introduction

In actuarial science, credibility theory plays a central role in premium estimation by integrating individual claims experience with information from the broader portfolio. Originating from early actuarial efforts to reconcile individual risk assessment with collective experience, it provides a statistically grounded approach for balancing sensitivity to recent data with the stability of estimates. Early contributions to limited fluctuation credibility, such as those by Mowbray (Reference Mowbray1914) and Whitney (Reference Whitney1918), laid the foundation for more advanced credibility methods by introducing techniques to account for risk heterogeneity while maintaining estimation stability.

A major advancement in credibility theory came with the development of greatest accuracy credibility, which minimizes the squared-error loss of linear estimators when estimating an insured’s pure risk premium and serves as the cornerstone of classical credibility models. Notable contributions include those of Keffer (Reference Keffer1929), Bailey (Reference Bailey1943, Reference Bailey1950), who pioneered early credibility models, and Bühlmann (Reference Bühlmann1967, Reference Bühlmann1970), Bühlmann & Straub (Reference Bühlmann and Straub1970), whose work led to the establishment of the Bühlmann and Bühlmann-Straub credibility models. These models assume an optimal linear structure, combining individual and collective experience. However, as noted by Yan & Song (Reference Yan and Song2022), Bühlmann’s linear Bayesian credibility estimators lack robustness and are highly sensitive to heavy-tailed excess claims, potentially leading to significant estimation errors when approximating a nonlinear Bayesian credibility estimator.

Building on the foundational work of Bühlmann (Reference Bühlmann1967) and Bühlmann & Straub (Reference Bühlmann and Straub1970), researchers have developed credibility methods from various perspectives. Künsch (Reference Künsch1992) introduced a linear credibility estimator in which claims are replaced by a robust

$M$

-estimator, while Gisler & Reinhard (Reference Gisler and Reinhard1993) examined the application of robust credibility within the general Bühlmann-Straub model. Pitselis (Reference Pitselis2008) applied robust statistical methods to regression credibility estimation using the influence function approach of

$M$

-estimator, while Gisler & Reinhard (Reference Gisler and Reinhard1993) examined the application of robust credibility within the general Bühlmann-Straub model. Pitselis (Reference Pitselis2008) applied robust statistical methods to regression credibility estimation using the influence function approach of

$M$

-estimators. The asymptotic optimality of pure robust credibility was later established in Pitselis (Reference Pitselis2013). Further, robust estimators have been extended naturally to credibility theory for generalized mixed linear models (see, e.g., Nelder & Verrall, Reference Nelder and Verrall1997; Garrido & Zhou, Reference Garrido and Zhou2006; Lai & Sun, Reference Lai and Sun2012; Erdemir & Sucu, Reference Erdemir and Sucu2016), strengthening their applicability in actuarial science.

$M$

-estimators. The asymptotic optimality of pure robust credibility was later established in Pitselis (Reference Pitselis2013). Further, robust estimators have been extended naturally to credibility theory for generalized mixed linear models (see, e.g., Nelder & Verrall, Reference Nelder and Verrall1997; Garrido & Zhou, Reference Garrido and Zhou2006; Lai & Sun, Reference Lai and Sun2012; Erdemir & Sucu, Reference Erdemir and Sucu2016), strengthening their applicability in actuarial science.

Overall, the credibility theory literature has mainly focused on estimating the hypothetical mean for each risk group and, in turn, the expected pure premium. That is, it has been centered on mean estimation. However, focusing only on the mean may place less importance on the variability of observed losses. For example, the role of variance is seen in the well-known variance premium principle, which satisfies several desirable properties (Dickson, Reference Dickson2017, Chapter 3), while Hong & Martin (Reference Hong and Martin2017) address this issue in a more general framework by modeling the entire predictive distribution using a Dirichlet process mixture of lognormal models, rather than focusing solely on moments such as the mean or variance. Chen et al. (Reference Chen, Cheung, Choi and Yam2020) provide empirical evidence that both mean and variance shape credibility risk premiums, with variance proving more volatile than traditionally assumed. From the perspective of premium principles, Yong et al. (Reference Yong, Zeng and Zhang2024) studied a credibility framework based on the variance premium principle, where the goal is to estimate both the mean and variance instead of only the mean.

The linear credibility model, referred to as semi-linear credibility, for transformed loss data was first studied by De Vylder (Reference De Vylder1976), with further discussion in Bühlmann & Gisler (Reference Bühlmann and Gisler2005). Credibility models incorporating data trimming (Kim & Jeon, Reference Kim and Jeon2013) and winsorization (Zhao & Poudyal, Reference Zhao and Poudyal2024) can also be classified as semi-linear credibility. Semi-linear credibility explicitly incorporates the relationship between original and transformed data, improving estimation robustness. However, this study focuses on pure robust linear credibility and derives an explicit formula for its asymptotic properties. In the context of data truncation techniques in credibility theory, Cheung et al. (Reference Cheung, Yam and Zhang2022) proposed a satisficing approach to develop semi-linear credibility for heterogeneous risks.

Building upon the transition from linear to more complex credibility models, Le Courtois (Reference Le Courtois2021), with further insights from Hong & Martin (Reference Hong and Martin2021), introduced the

$q$

-credibility estimator based on observed ground-up losses, rather than transformed data. The phrase “ground-up” loss refers to the individual loss amount that is assumed to be unaffected by policy modifications or data transformations; see, for example, Klugman et al. (Reference Klugman, Panjer and Willmot2019, p. 186, Section 9.7) and Poudyal & Brazauskas (Reference Poudyal and Brazauskas2022, Section 2). By incorporating quadratic term adjustments (hence the term

$q$

-credibility estimator based on observed ground-up losses, rather than transformed data. The phrase “ground-up” loss refers to the individual loss amount that is assumed to be unaffected by policy modifications or data transformations; see, for example, Klugman et al. (Reference Klugman, Panjer and Willmot2019, p. 186, Section 9.7) and Poudyal & Brazauskas (Reference Poudyal and Brazauskas2022, Section 2). By incorporating quadratic term adjustments (hence the term

$q$

), this approach enhances premium estimation accuracy by capturing nonlinear dependencies in claim data. This manuscript extends the

$q$

), this approach enhances premium estimation accuracy by capturing nonlinear dependencies in claim data. This manuscript extends the

$q$

-credibility framework to transformed data, addressing an important gap in credibility estimation and forming the core contribution of this work, whereas Le Courtois (Reference Le Courtois2021) considered

$q$

-credibility framework to transformed data, addressing an important gap in credibility estimation and forming the core contribution of this work, whereas Le Courtois (Reference Le Courtois2021) considered

$q$

-credibility only for ground-up loss data. Specifically, we propose a quadratic credibility model that integrates both ground-up and robustly transformed data, referred to as robust quadratic credibility (RQC). To our knowledge, this is the first study to develop a second-order credibility framework that systematically incorporates transformed data, enhancing robustness in quadratic credibility estimation. The RQC framework embeds robust winsorized moments within the quadratic credibility model. RQC stabilizes and improves premium estimation accuracy by transforming ground-up loss data and applying second-order polynomial adjustments, particularly under heterogeneous risks. This framework extends the semi-linear credibility methodology originally introduced by De Vylder (Reference De Vylder1976), while maintaining interpretability and statistical efficiency.

$q$

-credibility only for ground-up loss data. Specifically, we propose a quadratic credibility model that integrates both ground-up and robustly transformed data, referred to as robust quadratic credibility (RQC). To our knowledge, this is the first study to develop a second-order credibility framework that systematically incorporates transformed data, enhancing robustness in quadratic credibility estimation. The RQC framework embeds robust winsorized moments within the quadratic credibility model. RQC stabilizes and improves premium estimation accuracy by transforming ground-up loss data and applying second-order polynomial adjustments, particularly under heterogeneous risks. This framework extends the semi-linear credibility methodology originally introduced by De Vylder (Reference De Vylder1976), while maintaining interpretability and statistical efficiency.

We establish the asymptotic properties of the proposed RQC estimators, derive closed-form expressions for premium calculations, and compare their performance against classical and semi-linear credibility models. Our results show that RQC reduces mean squared error (MSE) relative to classical credibility,

$q$

-credibility, and semi-linear credibility, while capturing claim heterogeneity more effectively.

$q$

-credibility, and semi-linear credibility, while capturing claim heterogeneity more effectively.

The remainder of the paper is organized as follows. Section 2 introduces the RQC framework, outlining its motivation and theoretical foundation. The classical credibility models are revisited, followed by an extension that integrates robust estimators into quadratic credibility models. Section 3 presents two parametric examples – Exponential-Inverse Gamma and Lognormal-Normal models – demonstrating the applicability of RQC. The theoretical formulations are examined alongside estimation of credibility structural parameters, with explicit derivations of key quantities such as variance-covariance structures and credibility factors. Section 4 extends the analysis to nonparametric examples, reinforcing the robustness of RQC without assuming specific distributional forms. Section 5 evaluates RQC in practical actuarial contexts through analytical comparisons and applications to real-world insurance datasets, highlighting its advantages in achieving a more robust and equitable premium determination and performance of RQC taken against outlier. The empirical analysis assesses the practical implications of the proposed model and benchmarks its predictive performance against conventional credibility approaches. Finally, Section 6 summarizes the main findings, discusses their relevance to actuarial practice, and outlines potential directions for future research.

2. Robust q-credibility

Consider the risk class random variable

$\Theta$

(Bühlmann & Gisler, Reference Bühlmann and Gisler2005, p. 12) with prior probability density (or mass) function

$\Theta$

(Bühlmann & Gisler, Reference Bühlmann and Gisler2005, p. 12) with prior probability density (or mass) function

$\pi (\theta )$

. For a particular policyholder, that is, conditional on

$\pi (\theta )$

. For a particular policyholder, that is, conditional on

$\Theta =\theta$

, assume we have observed

$\Theta =\theta$

, assume we have observed

$n$

independent and identically distributed (i.i.d.) past-claim observations

$n$

independent and identically distributed (i.i.d.) past-claim observations

$ X_{1} \mid \theta , \, X_{2} \mid \theta , \, \ldots , \, X_{n} \mid \theta .$

Consequently, the marginal variables

$ X_{1} \mid \theta , \, X_{2} \mid \theta , \, \ldots , \, X_{n} \mid \theta .$

Consequently, the marginal variables

$X_{1},\ldots ,X_{n}$

are exchangeable and identically distributed, though not necessarily independent; see, e.g., Hong & Martin (Reference Hong and Martin2020) and Le Courtois (Reference Le Courtois2021). Then, an actuary is interested in setting a premium rate to cover

$X_{1},\ldots ,X_{n}$

are exchangeable and identically distributed, though not necessarily independent; see, e.g., Hong & Martin (Reference Hong and Martin2020) and Le Courtois (Reference Le Courtois2021). Then, an actuary is interested in setting a premium rate to cover

$X_{n+1}$

, for the next policy period for that particular policyholder. First, we note that the classical linear credibility problem is defined as:

$X_{n+1}$

, for the next policy period for that particular policyholder. First, we note that the classical linear credibility problem is defined as:

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 1: \quad & \min _{\alpha , \, \beta _{i} \, \in \,\mathbb{R}} \, P_{1}, \quad P_{1} \,:\!=\, \mathbb{E}_{X_{1:n+1}} \left \{ {\left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, X_{i} - X_{n+1} \right ]}^{2} \right \}, \end{align}

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 1: \quad & \min _{\alpha , \, \beta _{i} \, \in \,\mathbb{R}} \, P_{1}, \quad P_{1} \,:\!=\, \mathbb{E}_{X_{1:n+1}} \left \{ {\left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, X_{i} - X_{n+1} \right ]}^{2} \right \}, \end{align}

where

$ \mathbb{E}_{X_{1:n+1}}$

(the subscript

$ \mathbb{E}_{X_{1:n+1}}$

(the subscript

$X_{1:n+1}$

will be dropped when clear from the context) denotes expectation with respect to the joint distribution of

$X_{1:n+1}$

will be dropped when clear from the context) denotes expectation with respect to the joint distribution of

$X_1$

,

$X_1$

,

$\ldots$

,

$\ldots$

,

$X_n$

, and

$X_n$

, and

$X_{n+1}$

.

$X_{n+1}$

.

Building on this framework, the

$q$

-credibility model proposed by Le Courtois (Reference Le Courtois2021) introduces an additional term to capture quadratic information,

$q$

-credibility model proposed by Le Courtois (Reference Le Courtois2021) introduces an additional term to capture quadratic information,

$\{X_{i}^2\}_{i=1:n}$

, formulated as:

$\{X_{i}^2\}_{i=1:n}$

, formulated as:

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 2: \quad & \min _{\alpha , \ \beta _{i}, \, \gamma _{i} \, \in \, \mathbb{R}} \, P_{2}, \quad P_{2} \,:\!=\, \mathbb{E}_{X_{1:n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, X_{i} + \sum _{i=1}^{n} \gamma _{i} \, X_{i}^2 - X_{n+1} \right ]^{2} \right \}. \end{align}

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 2: \quad & \min _{\alpha , \ \beta _{i}, \, \gamma _{i} \, \in \, \mathbb{R}} \, P_{2}, \quad P_{2} \,:\!=\, \mathbb{E}_{X_{1:n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, X_{i} + \sum _{i=1}^{n} \gamma _{i} \, X_{i}^2 - X_{n+1} \right ]^{2} \right \}. \end{align}

The primary motivation behind the credibility model (2) is to incorporate quadratic terms into the credibility framework. This approach integrates both linear and quadratic information, enhancing credibility estimation. Hong & Martin (Reference Hong and Martin2021) further explored the relationship between this quadratic estimator and the classical Bühlmann methodology, emphasizing its potential to improve the estimation accuracy by accounting for nonlinear dependencies in the data.

2.1 General structure

Being a loss random variable, we assume that the support of

$X$

is

$X$

is

$[0, \infty )$

. Let

$[0, \infty )$

. Let

$Y = f(X)$

denote a robust transformation of the ground-up loss

$Y = f(X)$

denote a robust transformation of the ground-up loss

$X$

, where

$X$

, where

$ f \,:\, [0, \infty ) \to [0, \infty )$

is an arbitrary, nondegenerate function representing a general transformation of the loss variable

$ f \,:\, [0, \infty ) \to [0, \infty )$

is an arbitrary, nondegenerate function representing a general transformation of the loss variable

$X$

. Using this transformation, the optimization problem for estimating the robust credibility premium under the semi-linear credibility, see, e.g., Bühlmann & Gisler (Reference Bühlmann and Gisler2005, Definition 5.1, p. 126), framework is defined as

$X$

. Using this transformation, the optimization problem for estimating the robust credibility premium under the semi-linear credibility, see, e.g., Bühlmann & Gisler (Reference Bühlmann and Gisler2005, Definition 5.1, p. 126), framework is defined as

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 3: \quad & \min _{\alpha , \ \beta _{i} \, \in \, \mathbb{R}} \, P_{3}, \quad P_{3} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, Y_{i} - X_{n+1} \right ]^{2} \right \}. \end{align}

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 3: \quad & \min _{\alpha , \ \beta _{i} \, \in \, \mathbb{R}} \, P_{3}, \quad P_{3} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, Y_{i} - X_{n+1} \right ]^{2} \right \}. \end{align}

Robust credibility methods based on trimming (Kim & Jeon, Reference Kim and Jeon2013) and winsorizing (Zhao & Poudyal, Reference Zhao and Poudyal2024) can be viewed as special cases of Problem 3, where

$ X_{n+1}$

is replaced by its trimmed or winsorized counterpart,

$ X_{n+1}$

is replaced by its trimmed or winsorized counterpart,

$ Y_{n+1}$

.

$ Y_{n+1}$

.

The classical credibility model described in Problem 1 and the

$q$

-credibility model outlined in Problem 2 rely on the first and second moments of ground-up losses. These approaches are susceptible to contamination by outliers, potentially leading to sensitivity in the credibility premium. Semi-linear credibility, as formulated in Problem 3, aims to provide a more stable linear premium structure. However, to the best of our knowledge, the

$q$

-credibility model outlined in Problem 2 rely on the first and second moments of ground-up losses. These approaches are susceptible to contamination by outliers, potentially leading to sensitivity in the credibility premium. Semi-linear credibility, as formulated in Problem 3, aims to provide a more stable linear premium structure. However, to the best of our knowledge, the

$q$

-credibility model in Problem 2 has not yet been investigated with transformed data

$q$

-credibility model in Problem 2 has not yet been investigated with transformed data

$ Y = f(X)$

. Therefore, the primary motivation of this study is to address this gap by replacing the moments of ground-up losses with the corresponding moments of robustly transformed data,

$ Y = f(X)$

. Therefore, the primary motivation of this study is to address this gap by replacing the moments of ground-up losses with the corresponding moments of robustly transformed data,

$ Y = f(X)$

, and to extend the credibility framework by incorporating quadratic terms of the transformed losses into Problem 3. Accordingly, the desired optimization problem is defined as

$ Y = f(X)$

, and to extend the credibility framework by incorporating quadratic terms of the transformed losses into Problem 3. Accordingly, the desired optimization problem is defined as

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 4: \quad & \min _{\alpha , \, \beta _{i}, \, \gamma _{i} \, \in \, \mathbb{R}} \, P_{4}, \quad P_{4} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, Y_{i} + \sum _{i=1}^{n} \gamma _{i} \, Y_{i}^2 - X_{n+1} \right ]^{2} \right \}. \end{align}

\begin{align} \mathrm{P}\scriptstyle{\mathrm{ROBLEM}}\ 4: \quad & \min _{\alpha , \, \beta _{i}, \, \gamma _{i} \, \in \, \mathbb{R}} \, P_{4}, \quad P_{4} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \left \{ \left [ \alpha + \sum _{i=1}^{n} \beta _{i} \, Y_{i} + \sum _{i=1}^{n} \gamma _{i} \, Y_{i}^2 - X_{n+1} \right ]^{2} \right \}. \end{align}

As the transformed variables, we note that

$ Y_1 \mid \theta , \, Y_2 \mid \theta , \, \ldots , \, Y_n \mid \theta$

are i.i.d. The corresponding marginal variables

$ Y_1 \mid \theta , \, Y_2 \mid \theta , \, \ldots , \, Y_n \mid \theta$

are i.i.d. The corresponding marginal variables

$Y_i$

’s are also identically distributed as

$Y_i$

’s are also identically distributed as

$X_{i}$

’s. Consequently, under a symmetric quadratic loss function and equal exposure weights (i.e., no observation-specific weights), the optimal coefficients are index-invariant; that is,

$X_{i}$

’s. Consequently, under a symmetric quadratic loss function and equal exposure weights (i.e., no observation-specific weights), the optimal coefficients are index-invariant; that is,

\begin{equation*} \beta _{1} = \cdots = \beta _{n} \equiv \beta \quad \text{and} \quad \gamma _{1} = \cdots = \gamma _{n} \equiv \gamma . \end{equation*}

\begin{equation*} \beta _{1} = \cdots = \beta _{n} \equiv \beta \quad \text{and} \quad \gamma _{1} = \cdots = \gamma _{n} \equiv \gamma . \end{equation*}

Then, Problem 4 becomes

\begin{align} \quad & \min _{\alpha , \ \beta , \, \gamma \, \in \, \mathbb{R}} \, P_{5}, \quad P_{5} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \Big\{ \big[ \alpha + n\beta \widehat {Y} + n\gamma \widehat {Y^{2}} - X_{n+1} \big]^{2} \Big\}, \end{align}

\begin{align} \quad & \min _{\alpha , \ \beta , \, \gamma \, \in \, \mathbb{R}} \, P_{5}, \quad P_{5} \,:\!=\, \mathbb{E}_{Y_{1:n}, X_{n+1}} \Big\{ \big[ \alpha + n\beta \widehat {Y} + n\gamma \widehat {Y^{2}} - X_{n+1} \big]^{2} \Big\}, \end{align}

where

\begin{align} \widehat {Y^{k}} & \,:\!=\, \dfrac {1}{n} \sum _{i=1}^{n} Y_{i}^{k}, \quad k \ge 1, \quad \mbox{with} \quad \widehat {Y^{1}} \,:\!=\, \widehat {Y}. \end{align}

\begin{align} \widehat {Y^{k}} & \,:\!=\, \dfrac {1}{n} \sum _{i=1}^{n} Y_{i}^{k}, \quad k \ge 1, \quad \mbox{with} \quad \widehat {Y^{1}} \,:\!=\, \widehat {Y}. \end{align}

Then, the solution of this problem produces the estimator of

$X_{n+1}$

and is summarized in Theorem1.

$X_{n+1}$

and is summarized in Theorem1.

We now introduce the following notations for the ground-up loss random variable

$X$

and its corresponding transformed variable

$X$

and its corresponding transformed variable

$Y$

:

$Y$

:

\begin{align} \begin{array}{l@{\quad}l@{\quad}l}a=\mathbb{V}ar(\mathbb{E}[Y \mid \theta ]), & \quad b=\mathbb{C}ov(\mathbb{E}[Y^2 \mid \theta ],\mathbb{E}[Y \mid \theta ]), & \quad c=\mathbb{V}ar(\mathbb{E}[Y^2 \mid \theta ]), \\[3pt]d=\mathbb{V}ar(\mathbb{E}[X \mid \theta ]), & \quad e=\mathbb{C}ov(\mathbb{E}[Y \mid \theta ], \mathbb{E}[X \mid \theta ]), & \quad f=\mathbb{C}ov(\mathbb{E}[Y^{2} \mid \theta ],\mathbb{E}[X \mid \theta ]), \\[3pt] g=\mathbb{E}[\mathbb{C}ov(Y^2,Y \mid \theta )], & \quad h=\mathbb{E}[\mathbb{V}ar(Y^2 \mid \theta )], & \quad v= \mathbb{E}[\mathbb{V}ar(Y \mid \theta )], \\[3pt] l=\mathbb{E}[\mathbb{C}ov(Y^2,X \mid \theta )], & \quad k=\mathbb{E}[\mathbb{C}ov(Y,X \mid \theta )], & \quad u= \mathbb{E}[\mathbb{V}ar(X \mid \theta )], \\[3pt] \mu _{X}^{1}=\mathbb{E}[\mathbb{E}[X \mid \theta ]], & \quad \mu _{Y}^{1}=\mathbb{E} \left [ \mathbb{E} \left [ Y \mid \theta \right ]\right ] & \quad \mu _{Y}^{2}=\mathbb{E}[\mathbb{E}[Y^2 \mid \theta ]]. \end{array}\end{align}

\begin{align} \begin{array}{l@{\quad}l@{\quad}l}a=\mathbb{V}ar(\mathbb{E}[Y \mid \theta ]), & \quad b=\mathbb{C}ov(\mathbb{E}[Y^2 \mid \theta ],\mathbb{E}[Y \mid \theta ]), & \quad c=\mathbb{V}ar(\mathbb{E}[Y^2 \mid \theta ]), \\[3pt]d=\mathbb{V}ar(\mathbb{E}[X \mid \theta ]), & \quad e=\mathbb{C}ov(\mathbb{E}[Y \mid \theta ], \mathbb{E}[X \mid \theta ]), & \quad f=\mathbb{C}ov(\mathbb{E}[Y^{2} \mid \theta ],\mathbb{E}[X \mid \theta ]), \\[3pt] g=\mathbb{E}[\mathbb{C}ov(Y^2,Y \mid \theta )], & \quad h=\mathbb{E}[\mathbb{V}ar(Y^2 \mid \theta )], & \quad v= \mathbb{E}[\mathbb{V}ar(Y \mid \theta )], \\[3pt] l=\mathbb{E}[\mathbb{C}ov(Y^2,X \mid \theta )], & \quad k=\mathbb{E}[\mathbb{C}ov(Y,X \mid \theta )], & \quad u= \mathbb{E}[\mathbb{V}ar(X \mid \theta )], \\[3pt] \mu _{X}^{1}=\mathbb{E}[\mathbb{E}[X \mid \theta ]], & \quad \mu _{Y}^{1}=\mathbb{E} \left [ \mathbb{E} \left [ Y \mid \theta \right ]\right ] & \quad \mu _{Y}^{2}=\mathbb{E}[\mathbb{E}[Y^2 \mid \theta ]]. \end{array}\end{align}

Lemma 1.

With the notation introduced in Eq.

(7)

and for

$\widehat {Y^{k}}$

,

$\widehat {Y^{k}}$

,

$k \ge 1$

, defined in Eq.

(6)

, assume that

$k \ge 1$

, defined in Eq.

(6)

, assume that

$ Y^{2} \neq \beta _{0} + \beta _{1} Y$

almost surely (a.s.). Then, the following moment relations hold:

$ Y^{2} \neq \beta _{0} + \beta _{1} Y$

almost surely (a.s.). Then, the following moment relations hold:

-

(i)

$ \mathbb{V}ar ( \widehat {Y} ) = a+\dfrac {v}{n},$

$ \mathbb{V}ar ( \widehat {Y} ) = a+\dfrac {v}{n},$

-

(ii)

$ \mathbb{V}ar ( \widehat {Y^{2}} ) = c+\frac {h}{n}.$

-

(iii)

$\mathbb{C}ov ( \widehat {Y},\widehat {Y^{2}} ) = b+\frac {g}{n}$

, -

(iv) The covariance matrix,

$ \Sigma _n = \begin{bmatrix} \mathbb{V}ar (\widehat Y) & \mathbb{C}ov ( \widehat Y,\widehat {Y^2} ) \\[5pt] \mathbb{C}ov ( \widehat Y,\widehat {Y^2} ) & \mathbb{V}ar (\widehat {Y^2} ) \end{bmatrix}$

is positive definite.

Proof. See Appendix A.1.

Theorem 1.

The robust credibility premium that minimizes the expected quadratic loss function defined in Problem 4, based on the nondegenerate transformed data

$Y = f(X)$

satisfying

$Y = f(X)$

satisfying

$ Y^{2} \neq \beta _{0} + \beta _{1} Y$

a.s., is given by

$ Y^{2} \neq \beta _{0} + \beta _{1} Y$

a.s., is given by

\begin{align} \widehat {P}_{\mbox{rqc}} & = \mu _{X}^{1} + z_{1} \left ( \widehat {Y} - \mu _{Y}^{1} \right ) + z_{2} \big( \widehat {Y^2}-\mu _{Y}^{2} \big), \end{align}

\begin{align} \widehat {P}_{\mbox{rqc}} & = \mu _{X}^{1} + z_{1} \left ( \widehat {Y} - \mu _{Y}^{1} \right ) + z_{2} \big( \widehat {Y^2}-\mu _{Y}^{2} \big), \end{align}

where

\begin{align*} & \alpha = \mu _{X}^{1}-z_{1}\,\mu _{Y}^{1}-z_{2}\,\mu _{Y}^{2}, && \!\!\beta = \dfrac {e(nc+h)-f(nb+g)}{(na+v)(nc+h)-(nb+g)^{2}}, && \!\!\gamma = \dfrac {f(na+v)-e(nb+g)}{(na+v)(nc+h)-(nb+g)^{2}}, \\ & z_{1} = n \beta , && z_{2} = n \gamma , \end{align*}

\begin{align*} & \alpha = \mu _{X}^{1}-z_{1}\,\mu _{Y}^{1}-z_{2}\,\mu _{Y}^{2}, && \!\!\beta = \dfrac {e(nc+h)-f(nb+g)}{(na+v)(nc+h)-(nb+g)^{2}}, && \!\!\gamma = \dfrac {f(na+v)-e(nb+g)}{(na+v)(nc+h)-(nb+g)^{2}}, \\ & z_{1} = n \beta , && z_{2} = n \gamma , \end{align*}

where the common denominator in both

$\beta$

and

$\beta$

and

$\gamma$

is strictly positive by Lemma

1

.

$\gamma$

is strictly positive by Lemma

1

.

Proof. See Appendix A.2.

Note 1.

For the linear term only, the result of Theorem

1

reduces to the semi-linear credibility premium structure but with a different

$ z_{1}$

. This corresponds to Problem

3

and is presented in Theorem 5.2 of Bühlmann & Gisler (Reference Bühlmann and Gisler2005

, p. 126).

$ z_{1}$

. This corresponds to Problem

3

and is presented in Theorem 5.2 of Bühlmann & Gisler (Reference Bühlmann and Gisler2005

, p. 126).

When comparing the credibility models (2) and (4), it becomes evident that (4) represents a robust extension of (2), achieved by employing the robust transformation

$ Y=f(X)$

of the ground-up loss random variable

$ Y=f(X)$

of the ground-up loss random variable

$X$

. This transformation incorporates robustness directly into the credibility framework, making (4) better equipped to handle outliers and extreme values in the data. Consequently, the robust credibility premium derived from (4) is expected to exhibit greater stability and reduced sensitivity when compared to the credibility premium associated with Problem 2, ensuring improved reliability in premium estimations under varying data conditions.

$X$

. This transformation incorporates robustness directly into the credibility framework, making (4) better equipped to handle outliers and extreme values in the data. Consequently, the robust credibility premium derived from (4) is expected to exhibit greater stability and reduced sensitivity when compared to the credibility premium associated with Problem 2, ensuring improved reliability in premium estimations under varying data conditions.

With the robust

$ q$

-credibility premium structure given in Eq. (8), we also summarize other credibility premium structures here for completeness.

$ q$

-credibility premium structure given in Eq. (8), we also summarize other credibility premium structures here for completeness.

Solving Problem 1, the resulting classical credibility premium is then calculated as

\begin{align} \widehat {P}_{\mbox{cc}} & = \mu _{X}^{1} + z \left ( \widehat {X} - \mu _{X}^{1} \right ), \quad z = \dfrac {na}{na + v}. \end{align}

\begin{align} \widehat {P}_{\mbox{cc}} & = \mu _{X}^{1} + z \left ( \widehat {X} - \mu _{X}^{1} \right ), \quad z = \dfrac {na}{na + v}. \end{align}

Similarly, solving Problem 2, the corresponding

$q$

-credibility premium is then calculated as

$q$

-credibility premium is then calculated as

\begin{align} \widehat {P}_{\mbox {qc}} & = \mu _{X}^{1} + z_{1} \left ( \widehat {X} - \mu _{X}^{1} \right ) + z_{2} \big( \widehat {X^{2}}-\mu _{X}^{2} \big), \end{align}

\begin{align} \widehat {P}_{\mbox {qc}} & = \mu _{X}^{1} + z_{1} \left ( \widehat {X} - \mu _{X}^{1} \right ) + z_{2} \big( \widehat {X^{2}}-\mu _{X}^{2} \big), \end{align}

where for the right winsorizing proportion

$q = 0$

, Theorem1 yields

$q = 0$

, Theorem1 yields

\begin{equation*} \begin{cases} z_{1} = \dfrac {n\left [a(nc+h)-b(nb+g)\right ]} {(na+v)(nc+h)-(nb+g)^{2}}, \\[10pt] z_{2} = \dfrac {n\left (bv-ag\right )}{(na+v)(nc+h)-(nb+g)^{2}}. \end{cases} \end{equation*}

\begin{equation*} \begin{cases} z_{1} = \dfrac {n\left [a(nc+h)-b(nb+g)\right ]} {(na+v)(nc+h)-(nb+g)^{2}}, \\[10pt] z_{2} = \dfrac {n\left (bv-ag\right )}{(na+v)(nc+h)-(nb+g)^{2}}. \end{cases} \end{equation*}

This result coincides exactly with Proposition 1.1 of Le Courtois (Reference Le Courtois2021).

Finally, solving Problem 3, the corresponding semi-linear credibility premium is then calculated as

\begin{align} \widehat {P}_{\mbox{slc}} & = \mu _{X}^{1} + z \left ( \widehat {Y} - \mu _{Y}^{1} \right ), \quad z = \dfrac {ne}{na+v}. \end{align}

\begin{align} \widehat {P}_{\mbox{slc}} & = \mu _{X}^{1} + z \left ( \widehat {Y} - \mu _{Y}^{1} \right ), \quad z = \dfrac {ne}{na+v}. \end{align}

More discussion can be found in Bühlmann & Gisler (Reference Bühlmann and Gisler2005).

We now calculate the mean square error (MSE) of the RQC premium structure given in Eq. (8).

Proposition 1.

The MSE for a new observation,

$X_{n+1}$

, with RQC premium as given in Eq.

(8)

, is given by

$X_{n+1}$

, with RQC premium as given in Eq.

(8)

, is given by

\begin{align} MSE_{\mbox{rqc}} & \equiv MSE \left ( \widehat {P}_{\mbox{rqc}}, X_{n+1} \right ) = d+u-z_{1}e-z_{2}f. \end{align}

\begin{align} MSE_{\mbox{rqc}} & \equiv MSE \left ( \widehat {P}_{\mbox{rqc}}, X_{n+1} \right ) = d+u-z_{1}e-z_{2}f. \end{align}

Alternatively, the MSE can also be expressed in terms of the hypothetical mean

$\mu _{X}^{1}(\theta )=$

$\mu _{X}^{1}(\theta )=$

$\mathbb{E}[X_{n+1} \mid \theta ]$

as

$\mathbb{E}[X_{n+1} \mid \theta ]$

as

\begin{align} MSE_{\mbox{rqc}}^{'} & \equiv MSE^{'} \left ( \widehat {P}_{\mbox{rqc}}, \mu _{X}^{1}(\theta ) \right ) = d-z_{1}e-z_{2}f. \end{align}

\begin{align} MSE_{\mbox{rqc}}^{'} & \equiv MSE^{'} \left ( \widehat {P}_{\mbox{rqc}}, \mu _{X}^{1}(\theta ) \right ) = d-z_{1}e-z_{2}f. \end{align}

Proof. See Appendix A.3.

For the classical Buhlmann credibility whose premium structure is given in Eq. (9), the corresponding MSE is given by

\begin{align} MSE_{\mbox{cc}} & \equiv MSE \left ( \widehat {P}_{\mbox{cc}}, X_{n+1} \right ) = d+u-zd. \end{align}

\begin{align} MSE_{\mbox{cc}} & \equiv MSE \left ( \widehat {P}_{\mbox{cc}}, X_{n+1} \right ) = d+u-zd. \end{align}

For the

$q$

-credibility considered in Le Courtois (Reference Le Courtois2021) with the premium structure given in Eq. (10), the MSE is calculated as

$q$

-credibility considered in Le Courtois (Reference Le Courtois2021) with the premium structure given in Eq. (10), the MSE is calculated as

\begin{align} MSE_{\mbox{qc}} & \equiv MSE \left ( \widehat {P}_{\mbox{qc}}, X_{n+1} \right ) = d+u-z_{1}e-z_{2}f, \end{align}

\begin{align} MSE_{\mbox{qc}} & \equiv MSE \left ( \widehat {P}_{\mbox{qc}}, X_{n+1} \right ) = d+u-z_{1}e-z_{2}f, \end{align}

where

$z_{1}$

and

$z_{1}$

and

$z_{2}$

are defined in Theorem1 with

$z_{2}$

are defined in Theorem1 with

$(p,q) = (0,0)$

.

$(p,q) = (0,0)$

.

Similarly, for the semi-linear credibility with the premium structure given by Eq. (11), the corresponding MSE is given by

\begin{align} MSE_{\mbox{slc}} & \equiv MSE \big( \widehat {P}_{\mbox{slq}}, X_{n+1} \big) = d+u-ze. \end{align}

\begin{align} MSE_{\mbox{slc}} & \equiv MSE \big( \widehat {P}_{\mbox{slq}}, X_{n+1} \big) = d+u-ze. \end{align}

Proposition 2. As discussed in Remark 1.7 of Le Courtois (Reference Le Courtois2021) and Proposition 2 of Yong et al. (Reference Yong, Zeng and Zhang2024), it follows that

\begin{align} MSE_{\mbox{rqc}} & \leq MSE_{\mbox{slc}} \leq MSE_{\mbox{cc}} \quad \mbox{and} \quad MSE_{\mbox{rqc}} \leq MSE_{\mbox{qc}} \leq MSE_{\mbox{cc}}, \end{align}

\begin{align} MSE_{\mbox{rqc}} & \leq MSE_{\mbox{slc}} \leq MSE_{\mbox{cc}} \quad \mbox{and} \quad MSE_{\mbox{rqc}} \leq MSE_{\mbox{qc}} \leq MSE_{\mbox{cc}}, \end{align}

\begin{align} MSE_{\mbox{rqc}}^{'} & \leq MSE_{\mbox{slc}}^{'} \leq MSE_{\mbox{cc}}^{'} \quad \mbox{and} \quad MSE_{\mbox{rqc}}^{'} \leq MSE_{\mbox{qc}}^{'} \leq MSE_{\mbox{cc}}^{'}. \end{align}

\begin{align} MSE_{\mbox{rqc}}^{'} & \leq MSE_{\mbox{slc}}^{'} \leq MSE_{\mbox{cc}}^{'} \quad \mbox{and} \quad MSE_{\mbox{rqc}}^{'} \leq MSE_{\mbox{qc}}^{'} \leq MSE_{\mbox{cc}}^{'}. \end{align}

Proof. See Appendix A.4.

2.2 Data winsorization

The estimators derived from winsorized data exhibit greater robustness to outliers compared to their standard counterparts. They are extensively utilized in the analysis of both life and non-life insurance products; see, for example, Valdez et al. (Reference Valdez, Vadiveloo and and2014), Hwang et al. (Reference Hwang, Hu, Lee and Wang2017), and Lobo et al. (Reference Lobo, Fonseca and Alves2024).

In this paper, we consider the robust transformation

$ Y = f(X)$

of the underlying random variable

$ Y = f(X)$

of the underlying random variable

$ X$

. Specifically,

$ X$

. Specifically,

$ f(X)$

represents the winsorized transformation, where observations are adjusted based on left and right winsorizing proportions. For given proportions

$ f(X)$

represents the winsorized transformation, where observations are adjusted based on left and right winsorizing proportions. For given proportions

$ 0 \leq p, q \leq 1$

with

$ 0 \leq p, q \leq 1$

with

$ p \leq 1 - q$

, the transformed data are obtained by applying

$ p \leq 1 - q$

, the transformed data are obtained by applying

$ 100p\%$

left- and

$ 100p\%$

left- and

$ 100q\%$

right-winsorization, leading to the following representation:

$ 100q\%$

right-winsorization, leading to the following representation:

\begin{align} Y & = f(X) = \begin{cases} F^{-1}(p); & \mbox{for } X \lt F^{-1}(p), \\ X; & \mbox{for } F^{-1}(p) \le X \le F^{-1}(1-q), \\ F^{-1}(1-q); & \mbox{for } x\gt F^{-1}(1-q). \end{cases} \end{align}

\begin{align} Y & = f(X) = \begin{cases} F^{-1}(p); & \mbox{for } X \lt F^{-1}(p), \\ X; & \mbox{for } F^{-1}(p) \le X \le F^{-1}(1-q), \\ F^{-1}(1-q); & \mbox{for } x\gt F^{-1}(1-q). \end{cases} \end{align}

The proportions

$ p$

and

$ p$

and

$ q$

can be controlled by the researcher. That is, the winsorization proportions

$ q$

can be controlled by the researcher. That is, the winsorization proportions

$ p$

and

$ p$

and

$ q$

are selected subjectively, which can also be viewed as hyperparameter tuning, as discussed in Poudyal et al. (Reference Poudyal, Aryal and Pokhrel2025, Section 2.2) for a similar choice, and must be chosen in alignment with the modeling objectives. Since there is no universal rule for selecting

$ q$

are selected subjectively, which can also be viewed as hyperparameter tuning, as discussed in Poudyal et al. (Reference Poudyal, Aryal and Pokhrel2025, Section 2.2) for a similar choice, and must be chosen in alignment with the modeling objectives. Since there is no universal rule for selecting

$(p, q)$

, the choice is context-dependent and guided by the specific inferential or practical goals of the application. This approach is consistent with the broader

$(p, q)$

, the choice is context-dependent and guided by the specific inferential or practical goals of the application. This approach is consistent with the broader

$ L$

-estimation literature, where the weight function is typically chosen based on inferential goals rather than formal optimization; see Brazauskas et al. (Reference Brazauskas, Jones and Zitikis2009, Section 2.3) and Serfling (Reference Serfling1980, p. 263). The choice of

$ L$

-estimation literature, where the weight function is typically chosen based on inferential goals rather than formal optimization; see Brazauskas et al. (Reference Brazauskas, Jones and Zitikis2009, Section 2.3) and Serfling (Reference Serfling1980, p. 263). The choice of

$ p$

and

$ p$

and

$ q$

has a significant effect on risk control and the resulting credibility premium.

$ q$

has a significant effect on risk control and the resulting credibility premium.

For any positive integer

$k$

, the winsorized mean or moments are derived as the expectation of

$k$

, the winsorized mean or moments are derived as the expectation of

$ Y^k$

. That is,

$ Y^k$

. That is,

\begin{eqnarray} \mathbb{E} \big[ Y^{k} \mid \theta \big] & = & p^{k} \left [F^{-1}(p)\right ]^{k} + \int _{p}^{1-q} (F^{-1}(u))^{k} \,du + q^{k} \left [F^{-1}(1-q)\right ]^{k}. \end{eqnarray}

\begin{eqnarray} \mathbb{E} \big[ Y^{k} \mid \theta \big] & = & p^{k} \left [F^{-1}(p)\right ]^{k} + \int _{p}^{1-q} (F^{-1}(u))^{k} \,du + q^{k} \left [F^{-1}(1-q)\right ]^{k}. \end{eqnarray}

The corresponding empirical winsorized moments, which serves as an estimate of the population winsorized moments in Eq. (20) and is equivalent to Eq. (6), is now given by

where

$[\,]$

denotes the greatest integer part.

$[\,]$

denotes the greatest integer part.

2.3 Asymptotic properties

We now summarize the asymptotic distributional properties of

$ \widehat {Y^{k}}$

from Eq. (21). By Serfling (Reference Serfling1980, p. 264), the first sample winsorized moment in Eq. (21) can be written as

$ \widehat {Y^{k}}$

from Eq. (21). By Serfling (Reference Serfling1980, p. 264), the first sample winsorized moment in Eq. (21) can be written as

\begin{align*} \widehat {Y}=\frac {1}{n}\sum _{i=1}^{n}K \bigg (\frac {i}{n+1}\bigg )h(X_{i:n})+\sum _{m=1}^{2}c_{m}h\big(X_{[np_{m}],n}\big), \end{align*}

\begin{align*} \widehat {Y}=\frac {1}{n}\sum _{i=1}^{n}K \bigg (\frac {i}{n+1}\bigg )h(X_{i:n})+\sum _{m=1}^{2}c_{m}h\big(X_{[np_{m}],n}\big), \end{align*}

where

$c_{1}$

,

$c_{1}$

,

$c_{2}$

are nonzero constants, and

$c_{2}$

are nonzero constants, and

\begin{equation} K(x) = \begin{cases} 1; & \text{if } np_{1} \leq x \leq np_{2}, \\[4pt] 0;& \text{otherwise}, \\ \end{cases} \end{equation}

\begin{equation} K(x) = \begin{cases} 1; & \text{if } np_{1} \leq x \leq np_{2}, \\[4pt] 0;& \text{otherwise}, \\ \end{cases} \end{equation}

and

$np_{m}$

is the winsorized point. Chernoff et al. (Reference Chernoff and Gastwirth1967) prove that

$np_{m}$

is the winsorized point. Chernoff et al. (Reference Chernoff and Gastwirth1967) prove that

$\widehat {Y}$

is

$\widehat {Y}$

is

$\mathcal{AN} \big (\mu , \frac {\sigma ^{2}}{n} \big )$

, where the mean

$\mathcal{AN} \big (\mu , \frac {\sigma ^{2}}{n} \big )$

, where the mean

\begin{equation} \mu =\int _{0}^{1}K(u)H(u)du+\sum _{i=1}^{2}c_{i}h(p_{i}), \end{equation}

\begin{equation} \mu =\int _{0}^{1}K(u)H(u)du+\sum _{i=1}^{2}c_{i}h(p_{i}), \end{equation}

and the variance

\begin{align} \sigma ^{2}=\int _{0}^{1}\alpha ^{2}(u)du, \end{align}

\begin{align} \sigma ^{2}=\int _{0}^{1}\alpha ^{2}(u)du, \end{align}

where

\begin{align*} \alpha (u)=\frac {1}{1-u}\bigg [\int _{u}^{1} K(r)H^{'}(r)(1-r)dr+\sum _{p_{i}\geq u}c_{i}(1-p_{i})H^{'}(p_{i}), \quad H(u)=F^{-1}(u). \end{align*}

\begin{align*} \alpha (u)=\frac {1}{1-u}\bigg [\int _{u}^{1} K(r)H^{'}(r)(1-r)dr+\sum _{p_{i}\geq u}c_{i}(1-p_{i})H^{'}(p_{i}), \quad H(u)=F^{-1}(u). \end{align*}

For the winsorizing proportions

$ (p_{i}, q_{i})$

and

$ (p_{i}, q_{i})$

and

$ (p_{j}, q_{j})$

, there are six possible combinations. For further details, we refer the reader to Poudyal (Reference Poudyal2025), Zhao et al. (Reference Zhao, Brazauskas and Ghorai2018). Among the six possible scenarios, we consider the most natural combination of winsorizing proportions for the RQC structure, as formulated in Problem 4, which is given by

$ (p_{j}, q_{j})$

, there are six possible combinations. For further details, we refer the reader to Poudyal (Reference Poudyal2025), Zhao et al. (Reference Zhao, Brazauskas and Ghorai2018). Among the six possible scenarios, we consider the most natural combination of winsorizing proportions for the RQC structure, as formulated in Problem 4, which is given by

\begin{align} 0 \leq p_{j} \leq p_{i} \lt 1-q_{i} \leq 1-q_{j} \leq 1. \end{align}

\begin{align} 0 \leq p_{j} \leq p_{i} \lt 1-q_{i} \leq 1-q_{j} \leq 1. \end{align}

Theorem 2.

The

$k$

-variate vector

$k$

-variate vector

$ ( \sqrt {n} ( \widehat {Y^1} - \mu _{Y}^{1}(\theta ) ), \ldots , \sqrt {n} ( \widehat {Y^k} - \mu _{Y}^{k}(\theta ) ) )$

converges in distribution to the

$ ( \sqrt {n} ( \widehat {Y^1} - \mu _{Y}^{1}(\theta ) ), \ldots , \sqrt {n} ( \widehat {Y^k} - \mu _{Y}^{k}(\theta ) ) )$

converges in distribution to the

$k$

-variate normal random vector with the mean

$k$

-variate normal random vector with the mean

$\mathbf{0}=(0, \ldots , 0)$

and the variance-covariance matrix

$\mathbf{0}=(0, \ldots , 0)$

and the variance-covariance matrix

$\mathbf{\Sigma }$

:=

$\mathbf{\Sigma }$

:=

$[\sigma _{ij}^{2}]_{i,j=1}^{k}$

with the entries

$[\sigma _{ij}^{2}]_{i,j=1}^{k}$

with the entries

\begin{align} \sigma _{ij}^{2} & = \int _{p_{j}}^{1-q_{j}}\int _{p_{i}}^{1-q_{i}}H_{i}^{'}(r)H_{j}^{'}(s) \left [ \min \, \{r,s\}-rs \right ] \,dr\,ds \nonumber \\ & \quad + \left [ p_{j}^{2}H_{j}^{'}(p_{j})-q_{j}^{2}H_{j}^{'}(1-q_{j}) \right ] \Delta _{i} + q_{j}^{2}H_{i}(1-q_{i})H_{j}^{'}(1-q_{j}) - p_{j}^{2}H_{i}(p_{i})H_{j}^{'}(p_{j}) \nonumber \\ & \quad + p_{i}H_{i}^{'}(p_{i})\int _{p_{i}}^{1-q_{j}}H_{j}(s)\,ds + q_{i}H_{i}^{'}(1-q_{i})\int _{1-q_{i}}^{1-q_{j}}H_{j}(s)\,ds \nonumber \\ & \quad -\Big[p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\Big]\int _{p_{j}}^{1-q_{j}}H_{j}(s)\,ds \nonumber \\ & \quad + \Big[ p_{i}^{2}H_{i}^{'}(p_{i})+q_{i}(1-q_{i})H_{i}^{'}(1-q_{i}) \Big] q_{j}H_{j}(1-q_{j}) \nonumber \\ & \quad- \Big[ p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i}) \Big] p_{j}H_{j}(p_{j}) \nonumber \\ & \quad + p_{i}(1-p_{i})p_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(p_{j}) + p_{i}^{2}q_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(1-q_{j}) + p_{j}^{2}q_{i}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(p_{j}) \nonumber \\ & \quad + q_{i}(1-q_{i})q_{j}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(1-q_{j}), \end{align}

\begin{align} \sigma _{ij}^{2} & = \int _{p_{j}}^{1-q_{j}}\int _{p_{i}}^{1-q_{i}}H_{i}^{'}(r)H_{j}^{'}(s) \left [ \min \, \{r,s\}-rs \right ] \,dr\,ds \nonumber \\ & \quad + \left [ p_{j}^{2}H_{j}^{'}(p_{j})-q_{j}^{2}H_{j}^{'}(1-q_{j}) \right ] \Delta _{i} + q_{j}^{2}H_{i}(1-q_{i})H_{j}^{'}(1-q_{j}) - p_{j}^{2}H_{i}(p_{i})H_{j}^{'}(p_{j}) \nonumber \\ & \quad + p_{i}H_{i}^{'}(p_{i})\int _{p_{i}}^{1-q_{j}}H_{j}(s)\,ds + q_{i}H_{i}^{'}(1-q_{i})\int _{1-q_{i}}^{1-q_{j}}H_{j}(s)\,ds \nonumber \\ & \quad -\Big[p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\Big]\int _{p_{j}}^{1-q_{j}}H_{j}(s)\,ds \nonumber \\ & \quad + \Big[ p_{i}^{2}H_{i}^{'}(p_{i})+q_{i}(1-q_{i})H_{i}^{'}(1-q_{i}) \Big] q_{j}H_{j}(1-q_{j}) \nonumber \\ & \quad- \Big[ p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i}) \Big] p_{j}H_{j}(p_{j}) \nonumber \\ & \quad + p_{i}(1-p_{i})p_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(p_{j}) + p_{i}^{2}q_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(1-q_{j}) + p_{j}^{2}q_{i}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(p_{j}) \nonumber \\ & \quad + q_{i}(1-q_{i})q_{j}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(1-q_{j}), \end{align}

where

$ \Delta _{x} = p_{x}H_{x}(p_{x}) +\int _{p_{x}}^{1-q_{x}}H_{x}(s)\,ds +q_{x}H_{x}(1-q_{x}), \quad x \, \in \,\{ i, j \}.$

$ \Delta _{x} = p_{x}H_{x}(p_{x}) +\int _{p_{x}}^{1-q_{x}}H_{x}(s)\,ds +q_{x}H_{x}(1-q_{x}), \quad x \, \in \,\{ i, j \}.$

Proof.

Following Chernoff et al. (Reference Chernoff and Gastwirth1967, Remark 9) and using the variance formula from Eq. (24),

$\sigma _{ij}^{2}$

can be expressed as

$\sigma _{ij}^{2}$

can be expressed as

\begin{align*} \sigma _{ij}^{2} & = \int _{0}^{1}\alpha _{i}(u)\alpha _{j}(u)du \nonumber \\& = \int _{0}^{1} \bigg\{ \frac {1}{1-u} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr+\sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \bigg] \nonumber \\& \quad \times \frac {1}{1-u} \bigg[ \int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds+\sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] \bigg\} du \nonumber\end{align*}

\begin{align*} \sigma _{ij}^{2} & = \int _{0}^{1}\alpha _{i}(u)\alpha _{j}(u)du \nonumber \\& = \int _{0}^{1} \bigg\{ \frac {1}{1-u} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr+\sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \bigg] \nonumber \\& \quad \times \frac {1}{1-u} \bigg[ \int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds+\sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] \bigg\} du \nonumber\end{align*}

\begin{align}& = \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr\int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds \bigg] du \nonumber \\[5pt] & \quad + \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr \times \sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] du \nonumber \\[5pt] & \quad + \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds\times \sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \bigg] du \nonumber \\[5pt] & \quad +\int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \times \sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] du \nonumber \\ & = \Omega _{1} + \Omega _{2} + \Omega _{3} + \Omega _{4}, \end{align}

\begin{align}& = \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr\int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds \bigg] du \nonumber \\[5pt] & \quad + \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1} K_{i}(r)H_{i}^{'}(r)(1-r)dr \times \sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] du \nonumber \\[5pt] & \quad + \int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \int _{u}^{1}K_{j}(s)H_{j}^{'}(s)(1-s)ds\times \sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \bigg] du \nonumber \\[5pt] & \quad +\int _{0}^{1} \frac {1}{(1-u)^{2}} \bigg[ \sum _{p_{i}\geq u}c_{i}(1-p_{i})H_{i}^{'}(p_{i}) \times \sum _{p_{j}\geq u}c_{j}(1-p_{j})H_{j}^{'}(p_{j}) \bigg] du \nonumber \\ & = \Omega _{1} + \Omega _{2} + \Omega _{3} + \Omega _{4}, \end{align}

where

$ \Omega _{1}, \ \Omega _{2}, \, \Omega _{3}, \ \Omega _{4},$

represent the first, second, third, and fourth terms, respectively.

$ \Omega _{1}, \ \Omega _{2}, \, \Omega _{3}, \ \Omega _{4},$

represent the first, second, third, and fourth terms, respectively.

For the winsorizing proportions satisfying inequality (25), we consider the following notations:

\begin{align*} A_{i} & = p_{i}(1-p_{i})H_{i}^{'}(p_{i}), \quad B_{i}=q_{i}^{2}H_{i}^{'}(1-q_{i}), \quad A_{j}=p_{j}(1-p_{j})H_{j}^{'}(p_{j}), \quad B_{j}=q_{j}^{2}H_{j}^{'}(1-q_{j}), \\[6pt] R(r)&=H_{i}^{'}(r)(1-r),\quad S(s)=H_{j}^{'}(s)(1-s), \quad R_\ast (r)=\frac {R(r)}{(1-u)^2}, \quad S_\ast (s)=\frac {S(s)}{(1-u)^2}. \end{align*}

\begin{align*} A_{i} & = p_{i}(1-p_{i})H_{i}^{'}(p_{i}), \quad B_{i}=q_{i}^{2}H_{i}^{'}(1-q_{i}), \quad A_{j}=p_{j}(1-p_{j})H_{j}^{'}(p_{j}), \quad B_{j}=q_{j}^{2}H_{j}^{'}(1-q_{j}), \\[6pt] R(r)&=H_{i}^{'}(r)(1-r),\quad S(s)=H_{j}^{'}(s)(1-s), \quad R_\ast (r)=\frac {R(r)}{(1-u)^2}, \quad S_\ast (s)=\frac {S(s)}{(1-u)^2}. \end{align*}

Then, it follows that

\begin{align*} \Omega _{1} & = \int _{p_{j}}^{1-q_{j}}\int _{p_{i}}^{1-q_{i}}H_{i}^{'}(r)H_{j}^{'}(s)\,[\min \, \{r,s\}-rs]\,dr\,ds\\[6pt] & = p_{i}H_{i}(p_{i})H_{j}(p_{j})+q_{i}H_{i}(1-q_{i})H_{j}(1-q_{j})-\Delta _{i}\Delta _{j}+\int _{p_{j}}^{1-q_{j}}H_{i}(s)H_{j}(s)ds, \\[6pt] \Omega _{2}& = \int _{0}^{p_{j}} \frac {A_{j}+B_{j}}{(1-u)^{2}} \int _{p_{i}}^{1-q_{i}} R(r) \,dr \, du +\int _{p_{j}}^{p_{i}} \frac {B_{j}}{(1-u)^{2}} \int _{p_{i}}^{1-q_{i}} R(r) \,dr \, du \\[6pt] & \quad + \int _{p_{i}}^{1-q_{i}} \frac {B_{j}}{(1-u)^{2}} \int _{u}^{1-q_{i}} R(r) \,dr \, du \\[6pt] & = \bigg (\frac {p_{j}}{1-p_{j}}A_{j}+\frac {p_{i}}{1-p_{i}}B_{j}\bigg ) \int _{p_{i}}^{1-q_{i}}R(r) \,dr+B_{j}\int _{p_{i}}^{1-q_{i}} \int _{u}^{1-q_{i}}R_\ast (r)\,dr \, du. \\[6pt] & = \left [p_{j}^{2}H_{j}^{'}(p_{j})-q_{j}^{2}H_{j}^{'}(1-q_{j})\right ]\Delta _{i}+q_{j}^{2}H_{i}(1-q_{i})H_{j}^{'}(1-q_{j})-p_{j}^{2}H_{i}(p_{i})H_{j}^{'}(p_{j}), \\[6pt] \Omega _{3}& = \int _{0}^{p_{j}} \frac {A_{i}+B_{i}}{(1-u)^{2}} \int _{p_{j}}^{1-q_{j}}S(s)\,ds \, du + \int _{p_{j}}^{p_{i}} \frac {A_{i}+B_{i}}{(1-u)^{2}} \int _{u}^{1-q_{j}}S(s) \,dv \, du \\[6pt] & \quad + \int _{p_{i}}^{1-q_{i}} \frac {B_{i}}{(1-u)^{2}} \int _{u}^{1-q_{j}}S(s) \,ds \, du \end{align*}

\begin{align*} \Omega _{1} & = \int _{p_{j}}^{1-q_{j}}\int _{p_{i}}^{1-q_{i}}H_{i}^{'}(r)H_{j}^{'}(s)\,[\min \, \{r,s\}-rs]\,dr\,ds\\[6pt] & = p_{i}H_{i}(p_{i})H_{j}(p_{j})+q_{i}H_{i}(1-q_{i})H_{j}(1-q_{j})-\Delta _{i}\Delta _{j}+\int _{p_{j}}^{1-q_{j}}H_{i}(s)H_{j}(s)ds, \\[6pt] \Omega _{2}& = \int _{0}^{p_{j}} \frac {A_{j}+B_{j}}{(1-u)^{2}} \int _{p_{i}}^{1-q_{i}} R(r) \,dr \, du +\int _{p_{j}}^{p_{i}} \frac {B_{j}}{(1-u)^{2}} \int _{p_{i}}^{1-q_{i}} R(r) \,dr \, du \\[6pt] & \quad + \int _{p_{i}}^{1-q_{i}} \frac {B_{j}}{(1-u)^{2}} \int _{u}^{1-q_{i}} R(r) \,dr \, du \\[6pt] & = \bigg (\frac {p_{j}}{1-p_{j}}A_{j}+\frac {p_{i}}{1-p_{i}}B_{j}\bigg ) \int _{p_{i}}^{1-q_{i}}R(r) \,dr+B_{j}\int _{p_{i}}^{1-q_{i}} \int _{u}^{1-q_{i}}R_\ast (r)\,dr \, du. \\[6pt] & = \left [p_{j}^{2}H_{j}^{'}(p_{j})-q_{j}^{2}H_{j}^{'}(1-q_{j})\right ]\Delta _{i}+q_{j}^{2}H_{i}(1-q_{i})H_{j}^{'}(1-q_{j})-p_{j}^{2}H_{i}(p_{i})H_{j}^{'}(p_{j}), \\[6pt] \Omega _{3}& = \int _{0}^{p_{j}} \frac {A_{i}+B_{i}}{(1-u)^{2}} \int _{p_{j}}^{1-q_{j}}S(s)\,ds \, du + \int _{p_{j}}^{p_{i}} \frac {A_{i}+B_{i}}{(1-u)^{2}} \int _{u}^{1-q_{j}}S(s) \,dv \, du \\[6pt] & \quad + \int _{p_{i}}^{1-q_{i}} \frac {B_{i}}{(1-u)^{2}} \int _{u}^{1-q_{j}}S(s) \,ds \, du \end{align*}

\begin{align*} & = \frac {p_{j}}{1-p_{j}} \big (A_{i}+B_{i}\big )\int _{p_{j}}^{1-q_{j}}S(s) \,ds + \big (A_{i}+B_{i}\big )\int _{p_{j}}^{p_{i}} \int _{u}^{1-q_{j}}S_\ast (s)\,ds \, du \\[4pt] & \quad + B_{i}\,\int _{p_{i}}^{1-q_{i}} \int _{u}^{1-q_{j}}S_\ast (s)\,ds \, du. \\[4pt] & = \frac {p_{j}}{1-p_{j}} \big (A_{i}+B_{i}\big ) \int _{p_{j}}^{1-q_{j}}S(s) \,ds \\[4pt] & \quad + \big (A_{i}+B_{i}\big )\left [\int _{p_{j}}^{p_{i}} \int _{p_{j}}^{s}S_\ast (s)\,du \, ds +\int _{p_{j}}^{p_{i}} \int _{p_{i}}^{1-q_{j}}S_\ast (s)\,du \, ds \right ] \\[4pt] & \quad + B_{i}\,\left [\int _{p_{i}}^{1-q_{i}} \int _{p_{i}}^{s}S_\ast (s)\,du \, ds+\int _{1-q_{i}}^{1-q_{j}} \int _{p_{i}}^{1-q_{i}}S_\ast (s)\,du \, ds.\right ] \\[4pt] & = p_{i}H_{i}^{'}(p_{i})\int _{p_{i}}^{1-q_{j}}H_{j}(s)\,ds+ q_{i}H_{i}^{'}(1-q_{i})\int _{1-q_{i}}^{1-q_{j}}H_{j}(s)\,ds \\[4pt] & \quad -\left [p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\right ]\int _{p_{j}}^{1-q_{j}}H_{j}(s)\,ds \\[4pt] & \quad + \left [p_{i}^{2}H_{i}^{'}(p_{i})+q_{i}(1-q_{i})H_{i}^{'}(1-q_{i})\right ]q_{j}H_{j}(1-q_{j}) \\[4pt] & \quad -\left [p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\right ]p_{j}H_{j}(p_{j}), \\[4pt] \Omega _{4}& = \big (A_{i}+B_{i}\big )\big (A_{j}+B_{j}\big )\int _{0}^{p_{j}}\frac {1}{(1-u)^{2}} du \\[4pt] & \quad +\big (A_{i}+B_{i}\big )\,B_{j}\,\int _{p_{j}}^{p_{i}} \frac {1}{(1-u)^{2}} du +B_{i}\,B_{j}\,\int _{p_{i}}^{1-b_{i}} \frac {1}{(1-u)^{2}}du \\[4pt] & = \frac {p_{j}}{1-p_{j}}(A_{i}+B_{i})(A_{j}+B_{j})+\frac {p_{i}-p_{j}}{(1-p_{i})(1-p_{j})}(A_{i}+B_{i})\,B_{j}+\frac {1-p_{i}-q_{i}}{(1-p_{i})q_{i}}\,B_{i}\,B_{j} \\[4pt] & = p_{i}(1-p_{i})p_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(p_{j}) + p_{i}^{2}q_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(1-q_{j})+p_{j}^{2}q_{i}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(p_{j}) \\[4pt] & \quad +q_{i}(1-q_{i})q_{j}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(1-q_{j}). \end{align*}

\begin{align*} & = \frac {p_{j}}{1-p_{j}} \big (A_{i}+B_{i}\big )\int _{p_{j}}^{1-q_{j}}S(s) \,ds + \big (A_{i}+B_{i}\big )\int _{p_{j}}^{p_{i}} \int _{u}^{1-q_{j}}S_\ast (s)\,ds \, du \\[4pt] & \quad + B_{i}\,\int _{p_{i}}^{1-q_{i}} \int _{u}^{1-q_{j}}S_\ast (s)\,ds \, du. \\[4pt] & = \frac {p_{j}}{1-p_{j}} \big (A_{i}+B_{i}\big ) \int _{p_{j}}^{1-q_{j}}S(s) \,ds \\[4pt] & \quad + \big (A_{i}+B_{i}\big )\left [\int _{p_{j}}^{p_{i}} \int _{p_{j}}^{s}S_\ast (s)\,du \, ds +\int _{p_{j}}^{p_{i}} \int _{p_{i}}^{1-q_{j}}S_\ast (s)\,du \, ds \right ] \\[4pt] & \quad + B_{i}\,\left [\int _{p_{i}}^{1-q_{i}} \int _{p_{i}}^{s}S_\ast (s)\,du \, ds+\int _{1-q_{i}}^{1-q_{j}} \int _{p_{i}}^{1-q_{i}}S_\ast (s)\,du \, ds.\right ] \\[4pt] & = p_{i}H_{i}^{'}(p_{i})\int _{p_{i}}^{1-q_{j}}H_{j}(s)\,ds+ q_{i}H_{i}^{'}(1-q_{i})\int _{1-q_{i}}^{1-q_{j}}H_{j}(s)\,ds \\[4pt] & \quad -\left [p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\right ]\int _{p_{j}}^{1-q_{j}}H_{j}(s)\,ds \\[4pt] & \quad + \left [p_{i}^{2}H_{i}^{'}(p_{i})+q_{i}(1-q_{i})H_{i}^{'}(1-q_{i})\right ]q_{j}H_{j}(1-q_{j}) \\[4pt] & \quad -\left [p_{i}(1-p_{i})H_{i}^{'}(p_{i})+q_{i}^{2}H_{i}^{'}(1-q_{i})\right ]p_{j}H_{j}(p_{j}), \\[4pt] \Omega _{4}& = \big (A_{i}+B_{i}\big )\big (A_{j}+B_{j}\big )\int _{0}^{p_{j}}\frac {1}{(1-u)^{2}} du \\[4pt] & \quad +\big (A_{i}+B_{i}\big )\,B_{j}\,\int _{p_{j}}^{p_{i}} \frac {1}{(1-u)^{2}} du +B_{i}\,B_{j}\,\int _{p_{i}}^{1-b_{i}} \frac {1}{(1-u)^{2}}du \\[4pt] & = \frac {p_{j}}{1-p_{j}}(A_{i}+B_{i})(A_{j}+B_{j})+\frac {p_{i}-p_{j}}{(1-p_{i})(1-p_{j})}(A_{i}+B_{i})\,B_{j}+\frac {1-p_{i}-q_{i}}{(1-p_{i})q_{i}}\,B_{i}\,B_{j} \\[4pt] & = p_{i}(1-p_{i})p_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(p_{j}) + p_{i}^{2}q_{j}^{2}H_{i}^{'}(p_{i})H_{j}^{'}(1-q_{j})+p_{j}^{2}q_{i}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(p_{j}) \\[4pt] & \quad +q_{i}(1-q_{i})q_{j}^{2}H_{i}^{'}(1-q_{i})H_{j}^{'}(1-q_{j}). \end{align*}

Finally,

$ \sigma _{ij}^{2} = \Omega _{1} + \Omega _{2} + \Omega _{3} + \Omega _{4},$

provides the desired expression of Eq. (26).

$ \sigma _{ij}^{2} = \Omega _{1} + \Omega _{2} + \Omega _{3} + \Omega _{4},$

provides the desired expression of Eq. (26).

For each fixed

$ \theta \in \Theta$

, let the mean and variance of

$ \theta \in \Theta$

, let the mean and variance of

$ Y^{k}$

be denoted by

$ Y^{k}$

be denoted by

$ \mu _{Y}^{k}(\theta )$

and

$ \mu _{Y}^{k}(\theta )$

and

$ v^{k}(\theta )$

, respectively. Using these definitions and the result of Theorem2, we obtain

$ v^{k}(\theta )$

, respectively. Using these definitions and the result of Theorem2, we obtain

\begin{align} & \sqrt {n} \left ( \widehat {Y}-\mu _{Y}^{1}(\theta ) \right ) \, \sim \, \mathcal{AN} \left(0, v^{1}(\theta ) \right) \quad \mbox{and} \quad \sqrt {n} \big( \widehat {Y^{2}}-\mu _{Y}^2(\theta ) \big) \, \sim \, \mathcal{AN} \left(0, v^{2}(\theta )\right). \end{align}

\begin{align} & \sqrt {n} \left ( \widehat {Y}-\mu _{Y}^{1}(\theta ) \right ) \, \sim \, \mathcal{AN} \left(0, v^{1}(\theta ) \right) \quad \mbox{and} \quad \sqrt {n} \big( \widehat {Y^{2}}-\mu _{Y}^2(\theta ) \big) \, \sim \, \mathcal{AN} \left(0, v^{2}(\theta )\right). \end{align}

Further, using the asymptotic result from Theorem2 along with the inequality condition provided in (25), we can derive the conditional variance and covariance, in particular,

-

•

$\mathbb{C}ov(Y,Y^2 \mid \theta )$

is Eq. (26) with

$p_{i}=p_{j}=p,q_{i}=q_{j}=q, H_{i}=(F^{-1}),H_{j}=(F^{-1})^2,$

-

•

$\mathbb{V}ar(Y^2 \mid \theta )$

is Eq. (26) with

$p_{i}=p_{j}=p,q_{i}=q_{j}=q, H_{i}=(F^{-1})^{2},H_{j}=(F^{-1})^{2},$

-

•

$\mathbb{C}ov(X,Y \mid \theta )$

is Eq. (26) with

$ p_{i}=p,p_{j}=0,q_{i}=q,q_{j}=0, H_{i}=(F^{-1}),H_{j}=(F^{-1}),$

-

•

$ \mathbb{C}ov(X,Y^2 \mid \theta )$

is Eq. (26) with

$ p_{i}=p,p_{j}=0,q_{i}=q,q_{j}=0, H_{i}=(F^{-1})^2,H_{j}=(F^{-1})$

.

We conclude this section with the following lemma, which plays a crucial role in constructing the RQC premium for winsorized data.

Lemma 2.

Assume that

$ \mathbb{E} [ | X_{i} | ^{k} ] \lt \infty , k=1,2,3,4.$

Since

$ \mathbb{E} [ | X_{i} | ^{k} ] \lt \infty , k=1,2,3,4.$

Since

$Y$

is a winsorized version of

$Y$

is a winsorized version of

$X$

, Eq.

(19)

, then

$X$

, Eq.

(19)

, then

$ \mathbb{E} [ | Y_{i} |^k ] \lt \infty , k=1,2,3,4.$

And as

$ \mathbb{E} [ | Y_{i} |^k ] \lt \infty , k=1,2,3,4.$

And as

$n arrow \infty$

, we have

$n arrow \infty$

, we have

-

(i)

$\mathbb{E} [ \mathbb{E} [ \widehat {Y} ] ] \to \mu _{Y}^{1}$

, -

(ii)

$n\mathbb{E} [ \mathbb{V}ar [ \widehat {Y} ] ] \to v$

, -

(iii)

$\mathbb{V}ar [ \mathbb{E} [ \widehat {Y} ] ] \to a$

, -

(iv)

$\mathbb{C}ov ( \widehat {Y} ,\mu_{Y}^{1}(\theta) ) \to \mathbb{C}ov (\mu_{Y}^{1}(\theta) ,\mu_{Y}^{1}(\theta) ) = a$

, -

(v)

$\mathbb{C}ov ( \widehat {Y^2} ,\mu_{Y}^{1}(\theta) ) \to\mathbb{C}ov (\mu_{Y}^{2}(\theta) ,\mu_{Y}^{1}(\theta) ) = b$

, -

(vi)

$\mathbb{V}ar [ \mathbb{E} [ \widehat {Y}^2] ] \to c$

, -

(vii)

$\mathbb{C}ov (\mu_{X}^{1}(\theta), \widehat {Y} ) \to \mathbb{C}ov (\mu_{X}^{1}(\theta) ,\mu_{Y}^{1}(\theta) ) = e$

, -

(viii)

$\mathbb{C}ov (\mu_{X}^{1}(\theta), \widehat {Y^2} ) \to \mathbb{C}ov (\mu_{X}^{1}(\theta) ,\mu_{Y}^{2}(\theta) ) = f$

.

Proof. See Appendix A.5.

Note 3. The semi-linear credibility elements in Eqs. (11) and (16) can also be derived using the results of Lemma 2 .

Next, we will see how this robust credibility premium works on parametric models.

3. Parametric examples

This section examines the proposed RQC premium structure using two parametric models: Exponential-Inverse Gamma and Lognormal-Normal. The Exponential-Inverse Gamma combination is a conjugate prior pairing; thus, the classical credibility result aligns with the traditional Bayesian outcome. This makes it a suitable benchmark for comparing the results obtained through the RQC approach with those from the most widely used credibility method. While the normal-normal combination is another classical conjugate prior, the positive nature of the loss data necessitates modeling the loss component with a lognormal distribution instead of a normal one.

3.1 Exponential-inverse gamma model

Let

$X_{1} \mid \theta , \ldots , X_{n} \mid \theta$

be independent and identically distributed (i.i.d.) random variables, following an Exponential distribution with mean of

$X_{1} \mid \theta , \ldots , X_{n} \mid \theta$

be independent and identically distributed (i.i.d.) random variables, following an Exponential distribution with mean of

$\theta$

. And the parameter

$\theta$

. And the parameter

$\theta$

is Inverse Gamma

$\theta$

is Inverse Gamma

$(\alpha , \beta )$

distributed with mean of

$(\alpha , \beta )$

distributed with mean of

$\dfrac {\beta }{\alpha -1}$

. Now, the credibility premium for the Exponential-Inverse Gamma model is derived as follows.

$\dfrac {\beta }{\alpha -1}$

. Now, the credibility premium for the Exponential-Inverse Gamma model is derived as follows.

For loss random variable

$X \mid \theta \sim Exp(\theta )$

, we have

$X \mid \theta \sim Exp(\theta )$

, we have

$F(x \mid \theta )=1-e^{-x/\theta }=w$

and the quantile function

$F(x \mid \theta )=1-e^{-x/\theta }=w$

and the quantile function

$F^{-1}(w)=-\theta \log (1-w)$

. First, we note that for

$F^{-1}(w)=-\theta \log (1-w)$

. First, we note that for

$k=1,2,3,4$

;

$k=1,2,3,4$

;

\begin{eqnarray*} \int \big (\log u\big )^{k}\,du & = & u(\log u)^{k}-ku(\log u)^{k-1}+k(k-1)u(\log u)^{k-2} \\ & & -k(k-1)(k-2)u(\log u)^{k-3}+k(k-1)(k-2)(k-3) + \mbox{Constant}. \end{eqnarray*}

\begin{eqnarray*} \int \big (\log u\big )^{k}\,du & = & u(\log u)^{k}-ku(\log u)^{k-1}+k(k-1)u(\log u)^{k-2} \\ & & -k(k-1)(k-2)u(\log u)^{k-3}+k(k-1)(k-2)(k-3) + \mbox{Constant}. \end{eqnarray*}

Based on Eq. (20), we calculate the first four moments of the hypothetical mean

\begin{align*} \mu _{Y}^{1}(\theta ) & = -\theta \left\{p\,\text{log}(1-p)+\int _{p}^{1-q}\text{log}(1-w)dw+q\,\text{log}q\right\} \\& = -\theta \left\{p\,\text{log}(1-p)+q(1-\text{log}q)-(1-p)[1-\text{log}(1-p)]+q\,\text{log}q\right\}\end{align*}

\begin{align*} \mu _{Y}^{1}(\theta ) & = -\theta \left\{p\,\text{log}(1-p)+\int _{p}^{1-q}\text{log}(1-w)dw+q\,\text{log}q\right\} \\& = -\theta \left\{p\,\text{log}(1-p)+q(1-\text{log}q)-(1-p)[1-\text{log}(1-p)]+q\,\text{log}q\right\}\end{align*}

\begin{align*} & = -\theta \left\{\text{log}(1-p)+q-(1-p)\right\}\\[3pt] & = \theta \Bigg\{ \underbrace {1-p-q-\text{log}(1-p)}_{m_{1}(p,q)} \Bigg\} \\[3pt] & \,:\!=\, \theta \, m_{1}(p,q), \\[3pt] \mu _{Y}^{2}(\theta ) & = \theta ^{2} \left\{ p\,\big [\text{log}(1-p)\big ]^{2}+\int _{p}^{1-q}\big [\text{log}(1-w)\big ]^{2}\,dw+q\,\big (\text{log}\,q)^{2} \right\} \\[3pt] & = \theta ^{2} \Big\{ p\big [\text{log}(1-p)\big ]^{2}+(1-p)\big [\text{log}(1-p)\big ]^{2} \\[3pt] & \quad +2(1-p)[1-\text{log}(1-p)]-q(\text{log}\,q)^{2} -2q(1-\text{log}q)+q\big (\text{log}\,q)^{2} \Big\} \\[3pt] & = \theta ^{2} \left \{ \big [\text{log}(1-p)\big ]^{2}+2(1-p)\big [1-\text{log}(1-p)\big ]-2q (1-\log q) \right \} \\[3pt] & \,:\!=\, \theta ^{2}\,m_{2}(p,q), \\[3pt] \mu _{Y}^{3}(\theta )& = -\theta ^{3}\bigg \{p\,\big [\text{log}(1-p)\big ]^{3}+\int _{p}^{1-q}\big [\log (1-w)\big ]^{3}\,dw+q\,\big (\log \,q)^{3}\bigg \} \\[3pt] & = -\theta ^{3}\Big \{\big (\log (1-p)\big )^{3}-3(1-p)(\log (1-p))^{2}+6(1-p)\log (1-p) \\[3pt] & \quad -6(1-p)+3q(\log q)^{2} -6q\log q+6q\Big \} \\[3pt] & \,:\!=\, \theta ^{3}\, m_{3}(p,q), \\[3pt] \mu _{Y}^{4}(\theta ) & = \theta ^{4}\bigg \{p\,\big [\log (1-p)\big ]^{4}+\int _{p}^{1-q}\big [\log (1-w)\big ]^{4}\,dw+q\,\big (\log \,q)^{4}\bigg \} \\[1pt] & = \theta ^{4}\Big \{\big (\log (1-p)\big )^{4}-4(1-p)(\log (1-p))^{3}+12(1-p)(\log (1-p))^{2}\\[1pt] & \quad -24(1-p)\log (1-p) +24(1-p) +4q(\log q)^{3}-12q(\log q)^{2}+24q\log q-24q\Big \} \\[1pt] & \,:\!=\, \theta ^{4}\, m_{4}(p,q). \end{align*}

\begin{align*} & = -\theta \left\{\text{log}(1-p)+q-(1-p)\right\}\\[3pt] & = \theta \Bigg\{ \underbrace {1-p-q-\text{log}(1-p)}_{m_{1}(p,q)} \Bigg\} \\[3pt] & \,:\!=\, \theta \, m_{1}(p,q), \\[3pt] \mu _{Y}^{2}(\theta ) & = \theta ^{2} \left\{ p\,\big [\text{log}(1-p)\big ]^{2}+\int _{p}^{1-q}\big [\text{log}(1-w)\big ]^{2}\,dw+q\,\big (\text{log}\,q)^{2} \right\} \\[3pt] & = \theta ^{2} \Big\{ p\big [\text{log}(1-p)\big ]^{2}+(1-p)\big [\text{log}(1-p)\big ]^{2} \\[3pt] & \quad +2(1-p)[1-\text{log}(1-p)]-q(\text{log}\,q)^{2} -2q(1-\text{log}q)+q\big (\text{log}\,q)^{2} \Big\} \\[3pt] & = \theta ^{2} \left \{ \big [\text{log}(1-p)\big ]^{2}+2(1-p)\big [1-\text{log}(1-p)\big ]-2q (1-\log q) \right \} \\[3pt] & \,:\!=\, \theta ^{2}\,m_{2}(p,q), \\[3pt] \mu _{Y}^{3}(\theta )& = -\theta ^{3}\bigg \{p\,\big [\text{log}(1-p)\big ]^{3}+\int _{p}^{1-q}\big [\log (1-w)\big ]^{3}\,dw+q\,\big (\log \,q)^{3}\bigg \} \\[3pt] & = -\theta ^{3}\Big \{\big (\log (1-p)\big )^{3}-3(1-p)(\log (1-p))^{2}+6(1-p)\log (1-p) \\[3pt] & \quad -6(1-p)+3q(\log q)^{2} -6q\log q+6q\Big \} \\[3pt] & \,:\!=\, \theta ^{3}\, m_{3}(p,q), \\[3pt] \mu _{Y}^{4}(\theta ) & = \theta ^{4}\bigg \{p\,\big [\log (1-p)\big ]^{4}+\int _{p}^{1-q}\big [\log (1-w)\big ]^{4}\,dw+q\,\big (\log \,q)^{4}\bigg \} \\[1pt] & = \theta ^{4}\Big \{\big (\log (1-p)\big )^{4}-4(1-p)(\log (1-p))^{3}+12(1-p)(\log (1-p))^{2}\\[1pt] & \quad -24(1-p)\log (1-p) +24(1-p) +4q(\log q)^{3}-12q(\log q)^{2}+24q\log q-24q\Big \} \\[1pt] & \,:\!=\, \theta ^{4}\, m_{4}(p,q). \end{align*}

Besides, the derivatives of quantiles are

\begin{align*} H_{1}^{'}(w) & = \big [F^{-1}(w))\big ]^{'} = \dfrac {1}{F^{'}(F^{-1}(w))} = \dfrac {1}{F^{'} \left (-\theta \log (1-w) \right )} = \dfrac {1}{\frac {1}{\theta } e^{- \frac {-\theta \log (1-w)}{\theta }}}=\dfrac {\theta }{1-w}, \\ H_{2}^{'}(w) & = \big [\big (F^{-1}(w)\big )^2\big ]^{'} =\dfrac {2F^{-1}(w)}{F^{'}(F^{-1}(w))}= \dfrac {-2\theta \log (1-w)}{F^{'} \left ( \theta \log (1-w) \right )} = \dfrac {-2\theta \log (1-w)}{\frac {1}{\theta } e^{- \frac {-\theta \log (1-w)}{\theta }}}=-\dfrac {2\theta ^2\log (1-w)}{1-w}. \end{align*}

\begin{align*} H_{1}^{'}(w) & = \big [F^{-1}(w))\big ]^{'} = \dfrac {1}{F^{'}(F^{-1}(w))} = \dfrac {1}{F^{'} \left (-\theta \log (1-w) \right )} = \dfrac {1}{\frac {1}{\theta } e^{- \frac {-\theta \log (1-w)}{\theta }}}=\dfrac {\theta }{1-w}, \\ H_{2}^{'}(w) & = \big [\big (F^{-1}(w)\big )^2\big ]^{'} =\dfrac {2F^{-1}(w)}{F^{'}(F^{-1}(w))}= \dfrac {-2\theta \log (1-w)}{F^{'} \left ( \theta \log (1-w) \right )} = \dfrac {-2\theta \log (1-w)}{\frac {1}{\theta } e^{- \frac {-\theta \log (1-w)}{\theta }}}=-\dfrac {2\theta ^2\log (1-w)}{1-w}. \end{align*}

For the process variance and covariance, Zhao et al. (Reference Zhao, Brazauskas and Ghorai2018) have proved that for a location-scale or log-location-scale family distribution, and

$p_{i}=p_{j}=p,q_{i}=q_{j}=q$

, Eq. (26) leads to

$p_{i}=p_{j}=p,q_{i}=q_{j}=q$

, Eq. (26) leads to

\begin{align*} \mathbb{V}ar(Y \mid \theta ) & = \theta ^{2}\bigg\{m_{2}(p,q)-m_{1}^{2}(p,q)+2\left[m_{1}(p,q)\, (A-B) + B ({-}\log q) -A \big ({-}\log (1-p)\big )\right]\\ & \quad -(A-B)^2+\frac {A^{2}}{p}+\frac {B^{2}}{q}\bigg\}\\[-5pt] & \,:\!=\, \theta ^{2}v_{1}(p,q), \qquad \mbox{where} \quad A=p^2\,H_{1}^{'}(p)/\theta =\frac {p^2}{1-p},\,B=q^2\,H_{1}^{'}(1-q)/\theta =q. \end{align*}

\begin{align*} \mathbb{V}ar(Y \mid \theta ) & = \theta ^{2}\bigg\{m_{2}(p,q)-m_{1}^{2}(p,q)+2\left[m_{1}(p,q)\, (A-B) + B ({-}\log q) -A \big ({-}\log (1-p)\big )\right]\\ & \quad -(A-B)^2+\frac {A^{2}}{p}+\frac {B^{2}}{q}\bigg\}\\[-5pt] & \,:\!=\, \theta ^{2}v_{1}(p,q), \qquad \mbox{where} \quad A=p^2\,H_{1}^{'}(p)/\theta =\frac {p^2}{1-p},\,B=q^2\,H_{1}^{'}(1-q)/\theta =q. \end{align*}

\begin{align*} \mathbb{V}ar \left ( Y^2 \mid \theta \right ) & = \theta ^{4} \bigg \{m_{4}(p,q)-m_{2}(p,q)^{2}+2\big [m_{2}(p,q) (C-D)+D \log ^{2}(q)-C\log ^{2}(1-p)\big ] \\ & \quad -(C-D)^{2} +\frac {C^2}{p}+\frac {D^2}{q}\bigg \}\\ & \,:\!=\, \theta ^{4}v_{2}(p,q), \\ \mbox{where } C & = p^2\,H_{2}^{'}(p)/\theta ^2=-p^{2}\dfrac {2\log (1-p)}{1-p} \mbox{ and } D=q^2\,H_{2}^{'}(1-q)/\theta ^2=-q^{2}\dfrac {2\log (q)}{q}. \\ \mathbb{C}ov \left ( Y^2,Y \mid \theta \right ) & = \theta ^{3} \bigg\{ m_{3}(p,q)-m_{1}(p,q)m_{2}(p,q)+m_{1}(p,q)(C-D)+ D({-}\log (q))\\& \quad -C ({-}\log (1-p)) + m_{2}(p,q)(A-B) + B\log ^{2}(q)-A\log ^{2}(1-p)\\& \quad -(A-B)(C-D)+\frac {AC}{p}+\frac {BD}{q} \bigg\} \\ & \,:\!=\, \theta ^{3}v_{3}(p,q). \end{align*}

\begin{align*} \mathbb{V}ar \left ( Y^2 \mid \theta \right ) & = \theta ^{4} \bigg \{m_{4}(p,q)-m_{2}(p,q)^{2}+2\big [m_{2}(p,q) (C-D)+D \log ^{2}(q)-C\log ^{2}(1-p)\big ] \\ & \quad -(C-D)^{2} +\frac {C^2}{p}+\frac {D^2}{q}\bigg \}\\ & \,:\!=\, \theta ^{4}v_{2}(p,q), \\ \mbox{where } C & = p^2\,H_{2}^{'}(p)/\theta ^2=-p^{2}\dfrac {2\log (1-p)}{1-p} \mbox{ and } D=q^2\,H_{2}^{'}(1-q)/\theta ^2=-q^{2}\dfrac {2\log (q)}{q}. \\ \mathbb{C}ov \left ( Y^2,Y \mid \theta \right ) & = \theta ^{3} \bigg\{ m_{3}(p,q)-m_{1}(p,q)m_{2}(p,q)+m_{1}(p,q)(C-D)+ D({-}\log (q))\\& \quad -C ({-}\log (1-p)) + m_{2}(p,q)(A-B) + B\log ^{2}(q)-A\log ^{2}(1-p)\\& \quad -(A-B)(C-D)+\frac {AC}{p}+\frac {BD}{q} \bigg\} \\ & \,:\!=\, \theta ^{3}v_{3}(p,q). \end{align*}

When we consider the covariance of original value

$X$

and robust version

$X$

and robust version

$Y$

, we have

$Y$

, we have

\begin{align*} \mathbb{C}ov(Y,X \mid \theta ) & = pH_{i}^{'}(p)\int _{p}^{1}H_{j}(s)\,ds+ qH_{i}^{'}(1-q)\int _{1-q}^{1}H_{j}(s)\,ds \\[8pt]& \quad -\left [p(1-p)H_{i}^{'}(p)+q^{2}H_{i}^{'}(1-q)\right ]\int _{0}^{1}H_{j}(s)\,ds\\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}H_{i}^{'}(r)H_{j}^{'}(s)\,[\min \, \{r,s\}-rs]\,dr\,ds\\[8pt] & = \theta ^2\bigg \{\frac {-p}{(1-p)}\int _{p}^{1}\log (1-s)\,ds-\int _{1-q}^{1}\log (1-s)\,ds+(p+q)\,\int _{0}^{1}\log (1-s)\,ds\\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}\frac {1}{1-r}\frac {1}{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\bigg \}\\[8pt] & \,:\!=\, \theta ^2\,v_{4}(p,q),\quad \text{where}\, H_{i}(r)=F^{-1}(r)=-\theta \log (1-r), H_{j}(s) = -\theta \log (1-s). \\[12pt] \mathbb{C}ov \left ( Y^2,X \mid \theta \right ) & = p\frac {-2\theta ^2\log (1-p)}{1-p}\int _{p}^{1}-\theta \log (1-s)\,ds+ q\frac {-2\theta ^2\log (q)}{q}\int _{1-q}^{1}-\theta \log (1-s)\,ds \\[8pt] & \quad -\bigg [p(1-p)\frac {-2\theta ^2\log (1-p)}{1-p} +q^{2}\frac {-2\theta ^2\log (q)}{q} \bigg ]\,\int _{0}^{1}-\theta \log (1-s)\,ds \\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}\frac {-2\theta ^2\log (1-r)}{1-r}\frac {\theta }{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\\[8pt] & = \theta ^{3}\bigg \{\frac {2\log (1-p)}{1-p}\int _{p}^{1}\log (1-s)\,ds+2\log (q)\int _{1-q}^{1}\log (1-s)\,ds \end{align*}

\begin{align*} \mathbb{C}ov(Y,X \mid \theta ) & = pH_{i}^{'}(p)\int _{p}^{1}H_{j}(s)\,ds+ qH_{i}^{'}(1-q)\int _{1-q}^{1}H_{j}(s)\,ds \\[8pt]& \quad -\left [p(1-p)H_{i}^{'}(p)+q^{2}H_{i}^{'}(1-q)\right ]\int _{0}^{1}H_{j}(s)\,ds\\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}H_{i}^{'}(r)H_{j}^{'}(s)\,[\min \, \{r,s\}-rs]\,dr\,ds\\[8pt] & = \theta ^2\bigg \{\frac {-p}{(1-p)}\int _{p}^{1}\log (1-s)\,ds-\int _{1-q}^{1}\log (1-s)\,ds+(p+q)\,\int _{0}^{1}\log (1-s)\,ds\\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}\frac {1}{1-r}\frac {1}{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\bigg \}\\[8pt] & \,:\!=\, \theta ^2\,v_{4}(p,q),\quad \text{where}\, H_{i}(r)=F^{-1}(r)=-\theta \log (1-r), H_{j}(s) = -\theta \log (1-s). \\[12pt] \mathbb{C}ov \left ( Y^2,X \mid \theta \right ) & = p\frac {-2\theta ^2\log (1-p)}{1-p}\int _{p}^{1}-\theta \log (1-s)\,ds+ q\frac {-2\theta ^2\log (q)}{q}\int _{1-q}^{1}-\theta \log (1-s)\,ds \\[8pt] & \quad -\bigg [p(1-p)\frac {-2\theta ^2\log (1-p)}{1-p} +q^{2}\frac {-2\theta ^2\log (q)}{q} \bigg ]\,\int _{0}^{1}-\theta \log (1-s)\,ds \\[8pt] & \quad + \int _{0}^{1}\int _{p}^{1-q}\frac {-2\theta ^2\log (1-r)}{1-r}\frac {\theta }{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\\[8pt] & = \theta ^{3}\bigg \{\frac {2\log (1-p)}{1-p}\int _{p}^{1}\log (1-s)\,ds+2\log (q)\int _{1-q}^{1}\log (1-s)\,ds \end{align*}

\begin{align*} & \quad -\big [2p\log (1-p)+2q\log (q)\big ] \int _{0}^{1}\log (1-s)\,ds \\[4pt] & \quad - \int _{0}^{1}\int _{p}^{1-q}\frac {2\log (1-r)}{1-r}\frac {1}{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\bigg \}\\[4pt] & \,:\!=\, \theta ^{3}v_{5}(p,q), \text{ where } H_{i}(r)=[F^{-1}(r)]^2=\theta ^2\log ^2(1-r), H_{j}(s) = F^{-1}(s)\\ & =-\theta \log (1-s). \end{align*}

\begin{align*} & \quad -\big [2p\log (1-p)+2q\log (q)\big ] \int _{0}^{1}\log (1-s)\,ds \\[4pt] & \quad - \int _{0}^{1}\int _{p}^{1-q}\frac {2\log (1-r)}{1-r}\frac {1}{1-s}\,[\min \, \{r,s\}-rs]\,dr\,ds\bigg \}\\[4pt] & \,:\!=\, \theta ^{3}v_{5}(p,q), \text{ where } H_{i}(r)=[F^{-1}(r)]^2=\theta ^2\log ^2(1-r), H_{j}(s) = F^{-1}(s)\\ & =-\theta \log (1-s). \end{align*}

When

$\alpha \gt 4$

, using the moment formula of an Inverse Gamma distribution, we derived the collective premium, variance/covariance of hypothetical means, and the expectation of process variance/covariance for this Exponential-Inverse Gamma model. See details in Appendix B.1.

$\alpha \gt 4$

, using the moment formula of an Inverse Gamma distribution, we derived the collective premium, variance/covariance of hypothetical means, and the expectation of process variance/covariance for this Exponential-Inverse Gamma model. See details in Appendix B.1.

Exponential (

$\theta$

)-inverse gamma (

$\theta$

)-inverse gamma (

$5, 2$

) using winsorized data. Fix

$5, 2$

) using winsorized data. Fix

$p=0$

, as

$p=0$

, as

$q$

increases, left column shows the variance or covariance of mean under risk parameter

$q$

increases, left column shows the variance or covariance of mean under risk parameter

$\theta$

; middle column panel shows the expectation of variance or covariance under risk parameter

$\theta$

; middle column panel shows the expectation of variance or covariance under risk parameter

$\theta$

; right column panel shows the expectation of mean under risk parameter

$\theta$

; right column panel shows the expectation of mean under risk parameter

$\theta$

.

$\theta$

.

Speaking of the connection between non-robust parameters and robust parameters, when

$(p,q)\to (0,0)$

, the values

$(p,q)\to (0,0)$

, the values

$m_{1}(p,q)\to\! 1, m_{2}(p,q)\to\! 2, m_{3}(p,q)\to\! -6, m_{4}(p,q)\to\! 24, v_{1}(p,q)\to 1,$

$m_{1}(p,q)\to\! 1, m_{2}(p,q)\to\! 2, m_{3}(p,q)\to\! -6, m_{4}(p,q)\to\! 24, v_{1}(p,q)\to 1,$

$v_{2}(p,q)\to 20, v_{3}(p,q)\to -8, v_{4}(p,q)\to 1 , v_{5}(p,q)\to 4$

, and the winsorized mean

$v_{2}(p,q)\to 20, v_{3}(p,q)\to -8, v_{4}(p,q)\to 1 , v_{5}(p,q)\to 4$

, and the winsorized mean

$\widehat {Y}$

converges to the original sample mean

$\widehat {Y}$

converges to the original sample mean

$\widehat {X}$

. Then, the RQC factors

$\widehat {X}$

. Then, the RQC factors

$z_{1}$

and

$z_{1}$

and

$z_{2}$

become conventional

$z_{2}$

become conventional

$q$

-credibility factors.

$q$

-credibility factors.

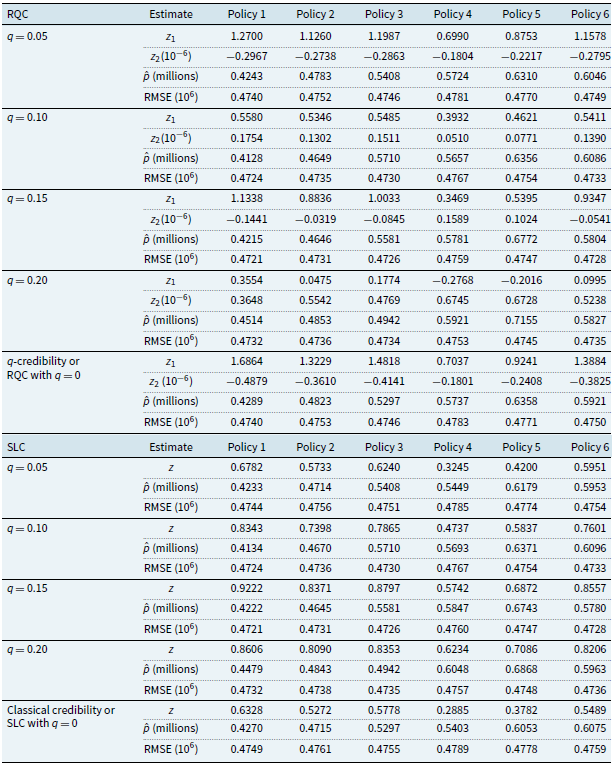

Fixed

$p=0$

, we demonstrate the impact of the right-winzorizing proportion

$p=0$

, we demonstrate the impact of the right-winzorizing proportion

$q$

(to take against extremely large loss) on the QRC estimation of this combination. As

$q$

(to take against extremely large loss) on the QRC estimation of this combination. As

$q$

increases from 0 to 1, the structural parameters discussed above are visualized in Figure 1. The prior distribution of the Inverse Gamma is set with parameters

$q$

increases from 0 to 1, the structural parameters discussed above are visualized in Figure 1. The prior distribution of the Inverse Gamma is set with parameters

$ \alpha = 5$

and

$ \alpha = 5$

and

$ \beta = 2$

. The similarity between

$ \beta = 2$

. The similarity between

$ v$

and

$ v$

and

$ k$

, as well as between

$ k$

, as well as between

$ g$

and

$ g$

and

$ l$

, raises the question of whether this behavior is influenced by the conjugate prior. As the right winsorizing proportion

$ l$

, raises the question of whether this behavior is influenced by the conjugate prior. As the right winsorizing proportion

$ q$

increases, all structural parameters exhibit a decreasing trend. When comparing the transformed variable

$ q$

increases, all structural parameters exhibit a decreasing trend. When comparing the transformed variable

$ Y$

with the original variable

$ Y$

with the original variable

$ X$

, the variance of the hypothetical mean (VHM) for

$ X$

, the variance of the hypothetical mean (VHM) for

$ Y$

declines more rapidly than that for

$ Y$

declines more rapidly than that for

$ X$

. For instance,

$ X$

. For instance,

$ b = \mathbb{E}[\mathbb{C}ov(Y^2,Y \mid \theta )]$