1. Introduction

The economic analysis of health insurance markets focuses on voluntary private health insurance and its potential market failure due to asymmetric information, in particular the problems of moral hazard and adverse selection. The dominant analytical framework for the problem of adverse selection in insurance markets with asymmetric information has been developed by Einav and Finkelstein (Reference Einav and Finkelstein2011) based on the theoretical model by Akerlof (Reference Akerlof1971). In their seminal paper Einav and Finkelstein (hereafter: EF) state that their framework ‘provides a unified approach for understanding both the conceptual welfare issues posed by selection in insurance markets and potential government intervention, as well as the existing empirical efforts to detect selection and measure its welfare consequences’ (p. 136). The focus of the welfare analysis is typically on the negative welfare effects of underinsurance for low-risk individuals.

In this paper we show that incorporating the extreme skewness of predictable individual health care expenses in the EF-framework may well shift the focus to the presumably much larger negative welfare effects of unaffordable health insurance for high-risk individuals: If the key assumption of the EF-framework holds that the demand and marginal cost curves for health insurance are tightly linked, the highly skewed distribution of predictable health care expenses across individuals will push the zero-profit equilibrium towards prices that are unaffordable for most individuals, which may even result in a total unravelling of the health insurance market. For most high-risk individuals their expected health care costs far exceed their individual ability-to-pay, irrespective of their income level and the magnitude of the risk premium they would be willing to pay. These conceptual considerations are supported by observations in real health care systems: Despite the theoretical focus on the welfare loss for low-risk individuals in the EF framework, in practice, most countries primarily focused on addressing the access problem for high-risk individuals. We argue that introducing mandatory insurance with mandatory cross subsidies is the most effective approach to tackle this problem.

This paper is organised as follows. Section 2 briefly discusses the EF framework. In Section 3 we discuss how we apply this framework to real-world health insurance markets using German data on individual predicted health care cost. Section 4 presents the results and implications of our analysis. In Section 5 we discuss practical solutions to the access problem of high-risk individuals that have been applied in health insurance markets in various countries. Section 6 concludes.

2. Einav-Finkelstein framework

Einav and Finkelstein argue that the most important distinguishing feature of insurance (or selection) markets is that demand and cost curves are tightly linked. According to EF the ‘market demand curve simply reflects the cumulative distribution of individuals’ willingness-to-pay for the contract’, whereas the ‘individual’s willingness-to-pay for insurance is the sum of the expected cost and the risk premium’. If the individual expected cost indeed reflects the marginal cost of each individual for the insurer (i.e., the expected claims experienced by the insurer), both the demand and marginal cost (MC) curve are downward sloping, as illustrated in Figure 1.

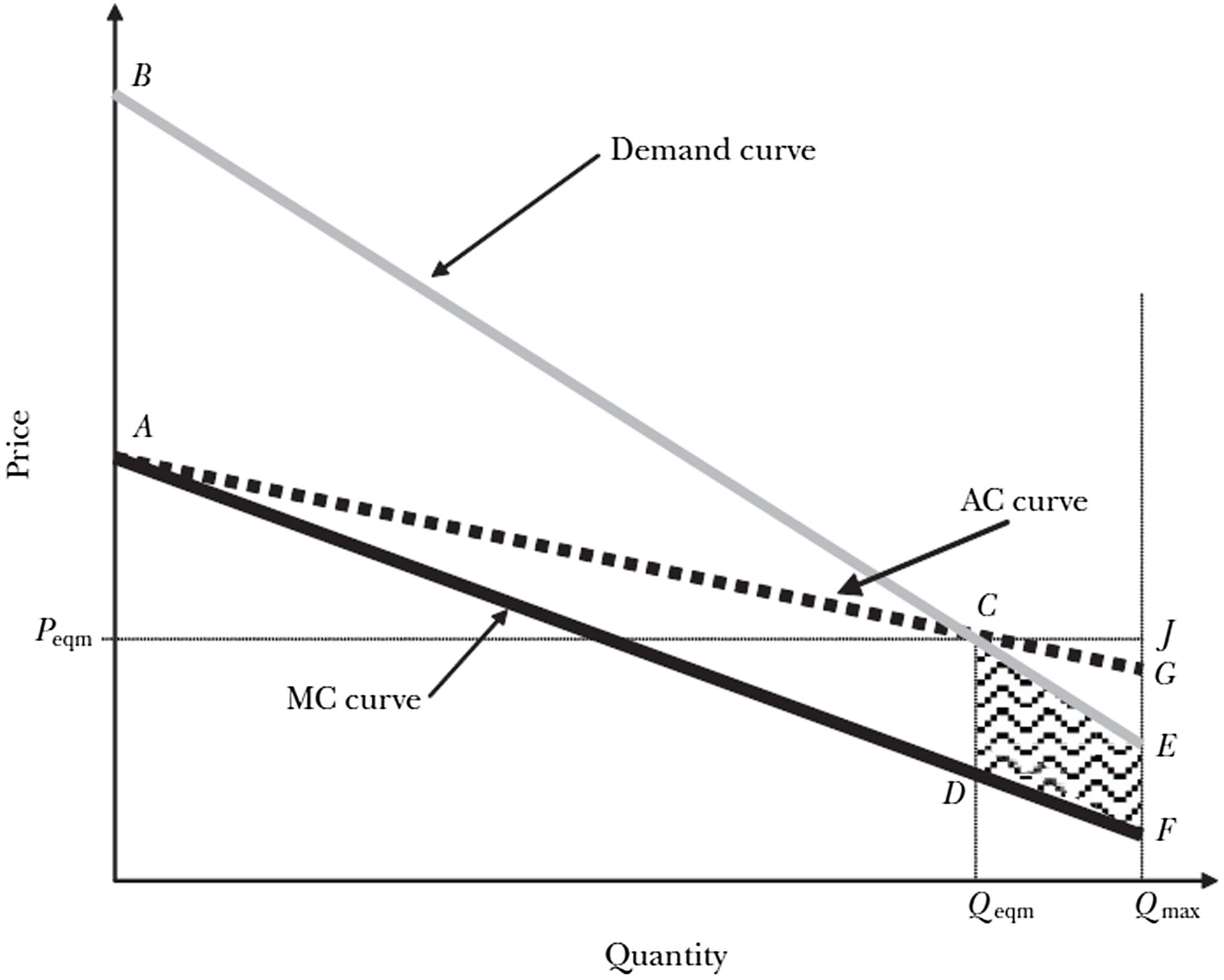

Einav and Finkelstein framework of an insurance market with a pooled premium and adverse selection.

Source: Einav and Finkelstein (Reference Einav and Finkelstein2011), Figure 1.

In Figure 1 the demand curve is always above the MC curve because all individuals are risk averse, and therefore the risk premium is always positive. As shown in Figure 1, EF assume that the risk premium increases in risk. In this textbook case, consumers have private information about their risk type respectively their expected cost and are treated identically by the insurer (i.e., extreme information asymmetry). Furthermore, it is assumed that insurers are risk neutral and compete only on price. This results in an average cost curve from an insurer’s perspective which represents the average cost of all individuals with the respective or higher expected cost (i.e., all individuals left of the respective point on the horizontal axis). The insurance contract is uniform for all individuals, who face a binary choice whether or not to buy this contract. The quantity of insurance on the horizontal axis is equal to the fraction of insured individuals.

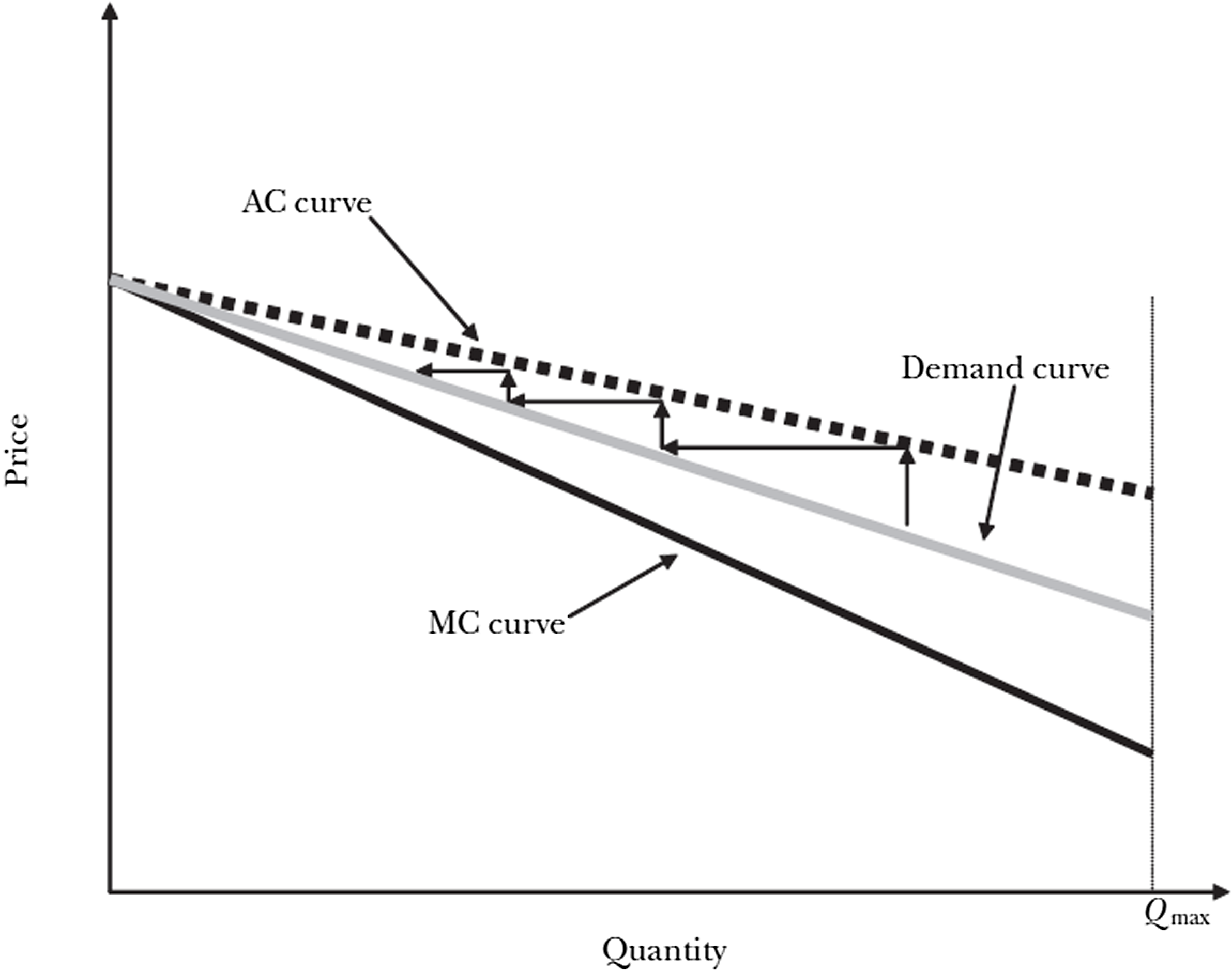

Under these textbook assumptions, there is a competitive zero-profit equilibrium in point C (at Qeqm and Peqm) where the demand curve intersects the average cost (AC) curve. At the pooled premium (Peqm) a certain fraction of population, consisting of the lowest-risk individuals (i.e., Qmax – Qeqm), is not willing to buy insurance, resulting in a welfare loss CDFE. The extent of welfare loss depends on people’s willingness-to-pay (demand), which in turn depends on the individual variation in risk and the level of risk aversion, reflected by the risk premium. EF show that depending on the specific assumptions, their framework may result in a continuum of equilibria, ranging from the extreme case of full coverage to the opposite extreme case of complete unravelling. In the extreme case of full coverage, the demand curve lies completely above the AC curve, which may occur if the variation in risk is small – implying a relatively flat MC and AC curve – and risk aversion is high – implying that people are willing to pay a high risk-premium (illustrated by Figure 2A in EF, not shown here). In the opposite extreme case of complete unravelling the demand curve completely lies below the AC curve, which may occur if the risk premium is sufficiently high and decreasing in risk, approaching zero for the highest risk individuals (illustrated by Figure 2 below or Figure 2B in EF). EF argue that this Figure may also illustrate the potential death spiral dynamics observed in health insurance markets (i.e., this dynamic adjustment process is depicted by the arrows in Figure 2).

Einav and Finkelstein framework of an insurance market with adverse selection and complete unravelling.

Source: Einav and Finkelstein (Reference Einav and Finkelstein2011), Figure 2B.

2.1 Public interventions

In addition, EF show that under these textbook assumptions, public interventions such as an insurance mandate and a lump sum subsidy towards the price of coverage are unambiguously welfare improving. However, they argue that these results may well be reversed in actual insurance markets due to the presence of insurance loads (i.e., the administrative costs of providing insurance) and preference heterogeneity. If insurance loads are greater than the risk premium for certain individuals, it would not be socially efficient to mandate these individuals to buy insurance.

2.2 Symmetric instead of asymmetric information

Obviously, in actual insurance markets, the assumption that insurers have no information about people’s health risk is unrealistic. Therefore, EF discuss the possibility that insurers can predict health care expenses by gender as an example of using information about predictable differences in individual risk to differentiate premiums. If consumers do not have residual private information (i.e., no information asymmetry), EF argue that risk rating premiums by gender is welfare increasing and pooled premiums (i.e., charging the same premium irrespective of gender) is unambiguously welfare decreasing because this will result in adverse selection. When insurers apply gender-rating this will split the market into two distinct insurance markets, i.e. two distinct variants of Figure 1. If this line of reasoning is extended by assuming insurers can distinguish many risk factors to risk rate premiums and consumers do not have residual private information, many distinct markets will emerge, that is: for each risk group a separate market with a risk-rated premium. Following the argument by EF, any restriction on risk rating would be unambiguously welfare decreasing because this would result in adverse selection.

3. Method and data

If the demand curve for health insurance would indeed reflect the expected individual health care costs plus risk premium, we show by means of data of a German sickness fund,Footnote 1 that the demand curve in health insurance markets would be highly convex. We then show that the application of this highly convex demand curve within the standard EF framework would almost certainly result in a complete unravelling of the market. Hence, the outcome of our analysis is similar to the outcome of one of the extreme cases described by EF, which is illustrated by Figure 2. However, the underlying reason is quite different. Whereas the unravelling in the EF-case is the result of a risk premium that is decreasing in risk, the unravelling in our case is due to the fact that the marginal cost curve is very steep for the 15–20 percent of the population with the highest expected health care cost.

3.1 Data on individual expected cost

The data on individual expected healthcare expenses are obtained from a large nationwide operating German health insurer (sickness fund) and consists of a sample of about 0.8 million insureds from 2017. For simulating the expected costs of an individual person, we use the risk-adjusted capitation payments of the German risk adjustment system of 2017.Footnote 2 Risk adjustment models in general are used to predict or model the individual cost of health care for insureds based on their characteristics as age, gender, and diagnostic information. The goal of adjustment systems is to destroy any incentives for risk selection and to create a level playing field for competition between health insurers. The German model used is a fully prospective model in which the costs for one year are estimated using individual data on a large set of predictors of the previous year. More specifically, the 2017 German risk adjustment model uses diagnostic information based on ICD10 codes as well as prescription drug codes of the previous year (2016), besides age, gender, and reduced earning capacity to calculate individuals’ expected cost of the next year (2017).Footnote 3 In the German risk adjustment system, the results of these calculations are used to determine risk-adjusted subsidies from the sponsor (in Germany the Central Health Fund) to the sickness funds.

The expenses predicted by the German risk adjustment model may serve to estimate the health care costs expected by individuals. Although individuals are not able to use the same information as used in the risk adjustment formula, they may instead base their expectations on their health expenditure of the previous year, which is also a very good predictor of next year’s costs.Footnote 4 So, this prospective risk adjustment approach seems to be a good way to model expected expenditure on an individual basis. For ease of explanation and illustration, we have clustered the individually expected costs predicted by the German risk adjustment formula into percentiles (i.e., average predicted cost per percentile) instead of using individual data.

4. Results

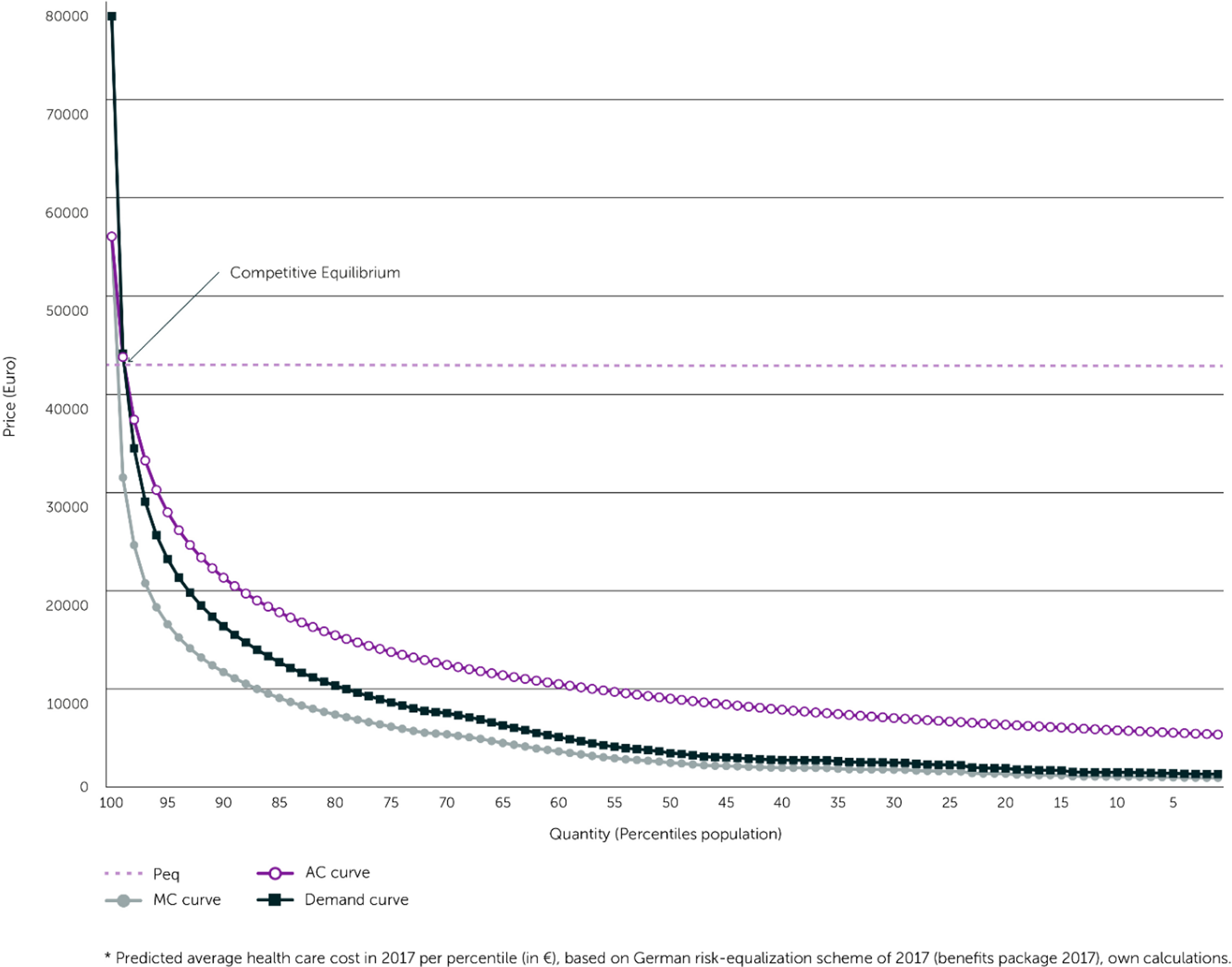

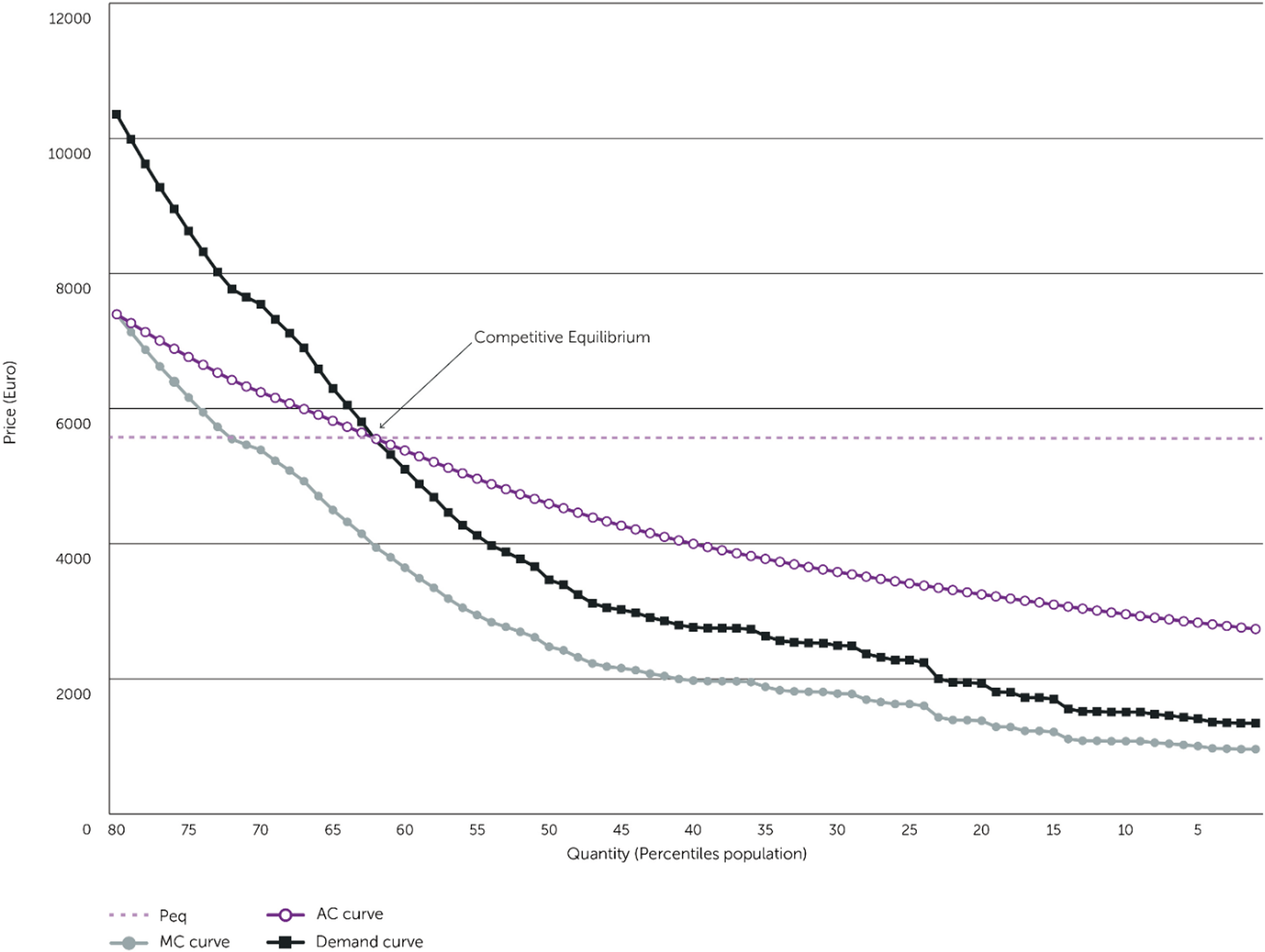

Using German data as predictable individual health care expenses results in a modification of the EF-framework, illustrated by Figure 3, in which both MC and AC curves are highly convex.

Einav and Finkelstein framework with convex cost curves based on German health insurance data*.

To construct these curves, average annualised individual predicted health care expenditures were calculated for each percentile of predicted health care expenditure. The predicted cost distribution represents the expected marginal cost for the health insurer of each individual in the same percentile. According to the key assumption of the EF framework people’s willingness to pay for insurance is increasing in their risk type – that is, their probability of loss or expected cost.

Assuming, in line with EF, that all people are risk averse and therefore willing to pay a certain risk premium and at the same time are able to pay this premium, the resulting demand curve will be highly convex too.Footnote 5 For sake of simplicity, in line with Figure 1 of EF we assumed that the risk premium (proportionally) increases in risk. However, for the analysis, this assumption is neither necessary nor important, since any credible risk premium structure will not have a major impact on the highly convex shape of the demand curve.

4.1 Competitive equilibrium: willingness and ability-to-pay

As shown in Figure 3, the use of convex predictable cost curves based on German risk adjustment data results in a competitive (zero-profit) equilibrium in which hardly anybody (about 2% of the population) would be willing to pay the equilibrium premium (Peq) of more than €40,000. However, even if this small fraction would be willing to pay this premium, it is highly unlikely that most of them would be able to pay this amount, given that the average annual wage in Germany was about €40,000 in 2017. Hence, if people have perfect private information about their risk type and insurers have no information at all, the market almost certainly unravels, resulting in a maximum welfare loss.

4.2 Symmetric instead of asymmetric information

As pointed out in Section 2, in actual private health insurance markets the assumption that insurers have no information about people’s health risk, and therefore must charge a pooled premium, is unrealistic. If we assume, in line with EF, that health insurers can predict individual health care expenses equally well as consumers (i.e., consumers do not have residual private information), then for each risk group distinguished by the German risk-equalisation scheme a separate market with a risk-rated premium will emerge. According to EF, any restriction on risk rating would be unambiguously welfare decreasing because this would result in adverse selection. However, this line of reasoning ignores the fact that unrestricted risk rating may render health insurance unaffordable for a substantial part of the population. In the German market, for instance, about 13 per cent of the population would have to pay a premium of at least €10,000. Even if these people would be willing to pay this premium for health insurance, most of them may not be able to do so. Clearly, if these individuals would not have access to health insurance, this would result in a major welfare loss because of losing access to care that would be unaffordable without health insurance. So, the underprovision of health insurance for these people would result in an underprovision of health care (Nyman, Reference Nyman1999). Light (Reference Light1992) shows that ‘risk rating makes insurance less affordable to those who need it most and thereby decreases both access to medical services and their quality if obtained’.

Hence, while the EF framework focuses on the welfare loss due to low-risk individuals not willing to buy insurance, the huge potential welfare loss due to high-risk individuals not being able to buy health insurance is the elephant in the room.Footnote 6

5. Discussion: how to tame the elephant in the room?

As shown, taking into account the highly convex shape of the individual expected health care cost curve when applying the standard EF framework both in case of asymmetric and symmetric information, reveals that the key welfare problem of health insurance markets is to provide high-risk individuals access to health insurance and affordable health care. Consequently, the key question in organising health insurance markets is how to prevent welfare loss due to unaffordable high premiums for high-risk individuals.Footnote 7 In practice, roughly three policy approaches – or a combination of them – can be distinguished that have been followed by different countries to address this problem.Footnote 8 The first two policy approaches aim to maintain a voluntary health insurance market by enforcing cross subsidies from low-risk individuals to high-risk ones. The third policy approach, which is followed by most countries, is to establish a mandatory health insurance system with mandatory cross-subsidies.

5.1 Maintaining a voluntary market by excluding or subsidising high-risk individuals

A first policy approach to maintain a voluntary health insurance market is to exclude people with predictable high health care expenses (and low incomes) from the market, by constituting subsidised high-risk pools or separate insurance schemes, which are partly financed by external resources.

The impact of this approach on the competitive equilibrium in the EF framework can be illustrated by Figure 4 in which 20% of the individuals with the highest expected cost (based on data from the German risk adjustment scheme) are excluded from the market.

Einav and Finkelstein framework with convex cost curves based on German health insurance data, excluding 20% per cent of the population with the highest predicted cost.

Figure 4 shows that under the assumptions of the EF framework in the competitive (zero-profit) equilibrium, only 17% of the residual population (Qeq) is willing to pay the pooled premium of more than €5,000.Footnote 9 Hence, even if all these people would be able to pay this premium, 63% of the population would not be willing to pay the pooled premium (at a risk premium of 40%). Hence, only excluding the highest-risk groups from the market may not be sufficient to make voluntary health insurance market an effective vehicle to cover the majority of the population. To realise this, more cross subsidies are likely to be required.

In a second policy approach, instead of excluding people with predictable high health care expenses (and low incomes) from the market and externally funding their cost by general tax money and/or employer contributions, (part of) their cost may be levied on the premium to those who buy voluntary health insurance, as a mandatory high-risk surcharge. Clearly, as this would require substantial surcharges, this may deter people from buying health insurance and may result in decreasing enrolment and upward spiralling surcharges.

Below we discuss two prominent examples of countries that pursued these approaches to provide affordable health insurance for high-risk individuals while maintaining a substantial part of a voluntary health insurance market.

5.1.1 Health insurance marketplaces in the US

A prominent example of a mixture of the first two policy approaches is the US health care system, where large categories of high-risk and/or low-income people are separated from the market through Medicare (providing coverage for disabled Americans and those of 65 years and older) and Medicaid (providing coverage for low-income households), together covering about 35% of US population in 2021 (KFF, 2023). In addition, about 50% of the population is covered by employment-based group insurance in which employers offer a limited menu of health plans at community-rated premiums. Participation of relatively low-risk individuals is strongly encouraged by substantial employer contributions, accounting for on average about 80% of total premiums for single coverage in 2022 (US Bureau of Labor Statistics, 2021). Clearly, at an employer contribution of about 80% of a community-rated premium most if not all employees would be willing to pay this pooled premium. Looking at Figure 4, a reduction of the pooled premium by 80% would increase Qeq from 17% to the entire residual population. Without this huge employer contribution, however, a large share of the US population might not be willing to pay a community-rated premium and the high-risk individuals within this population would probably be left without health insurance, even though many of the highest risks are already separated from the voluntary market via Medicare or Medicaid.

Still, employer-sponsored health insurance and Medicare and Medicaid do not provide health insurance coverage to a substantial part of the US population, which have to rely on the individual voluntary health insurance market. Without premium subsidies and regulation to prevent risk rating and risk selection (e.g. through medical underwriting and pre-existing condition clauses) this voluntary market clearly could not provide adequate health insurance coverage to high-risk individuals (Light, Reference Light1992), and by 2010 still about 16% of the US population was uninsured (ASPE, 2024). To reduce the number of uninsured and provide access to affordable health insurance for high-risk individuals in 2010 the Affordable Care Act (ACA) was passed to establish Health Insurance Marketplaces (which became in operation in 2014). The experience with the ACA Health Insurance Marketplaces shows that substantial regulation and cross subsidies are necessary (but still not enough) to guarantee access to individual voluntary health insurance for high-risk individuals.Footnote 10 By a combination of sophisticated risk-adjustment, cost-sharing reduction payments, premium tax credits for lower income groups and mandatory reinsurance,Footnote 11 access to affordable health insurance was substantially improved for previously uninsured high-risk individuals. As a result, the US uninsurance rate dropped from 16.0% in 2010 to 7.7% by the end of 2023 (ASPE, 2024). After four years of stagnation during the first Trump administration (2017–2021), from 2021 to 2025 enrollment in the Health Insurance Marketplaces doubled from 12 to 24 million (Choi, Reference Choi2025). This record-breaking growth has been credited to enhanced subsidies by the American Rescue Plan Act in 2021, which were extended by the Inflation Reduction Act through the end of 2025.Footnote 12 This shows that even in absence of a strong insurance mandate, a combination of premium subsidies, risk adjustment and extensive regulation can considerably reduce the problem for high-risk individuals to obtain affordable health insurance. Still, about 7% of the US population does not have health insurance, while the overall rates of cost sharing for Marketplace enrollees have increased over time due to the increased prevalence of health plans with low actuarial value (known as ‘bronze’ plans) (Treasure et al., Reference Treasure, Anderson, Hatcher, Makhoul, Johnson, Stefan and Griffith2023).

At the same time, the ACA experience clearly demonstrates the consequences of cancelling (part of) the external subsidies. Jacobs and Hill (Reference Jacobs and Hill2021) investigated the financial burden of health insurance in ACA Marketplaces on families with income between four and six times the federal poverty level which were excluded from premium tax credits before 2021. The financial burden was calculated as median percentage of potential Marketplace premium of family income. This burden increases from 2015 to 2019 independent of the coverage level (distinguished by the metal layers bronze, silver, gold and platinum) and independent of age group (insurers are allowed to differentiate premiums by age but not by health status). The strongest increase of financial burden was observed within the highest age group (the near-elderly of 55–64 years) showing an increase from 12.2% (2015) to 18.9% of family income (2019) for bronze-level coverage or from 18.2% to 28.6% for gold level coverage. These figures do not include the payments for deductibles which can make up another considerable part of the family income. The authors conclude that ‘an increasing number of middle-class families with incomes of 401–600 per cent of poverty [level] likely perceive these amounts to be unaffordable or unsustainable’. This is especially valid for the high-risk individuals which in this context are the near-elderly, which have to face increasingly difficult access to health insurance and health care. The disproportionate increase of premiums in comparison to incomes is in part the consequence of cancelling the federal reinsurance and corridor regulation in 2017, which were valid from 2014 until 2016, even though some states continued with publicly financed reinsurance regulations. In sum, the US experience shows that despite excluding a considerable part of the high-cost individuals from the market, and organising employer-sponsored group insurance for large parts of the population, still a substantial marketplace is left in which it seems necessary to take over a considerable part of the cost of high-risk individuals in order to organise sufficient access to health insurance. This is exactly in line with the results of our analysis.

Another relevant issue is the publicly regulated vertical differentiation of the ACA Health Insurance Marketplaces into the various metal tiers. This may have encouraged the uptake of health insurance by low-risk individuals since they have the option to choose a lower-priced bronze plan – and could in this way be an answer to the problem identified by EF: low-risks who do not find adequate health insurance. On the other hand, this differentiation has also resulted in low-risks concentrating in low-value plans whereas high-risks concentrate in the high-value plans. Indeed, Treasure et al. (Reference Treasure, Anderson, Hatcher, Makhoul, Johnson, Stefan and Griffith2023) find that individuals who select higher-value plans had greater mean HHS-HCC risk scores and higher mean health expenditure, while those who select lower-value plans had lower mean HHS-HCC risk scores. This can even exacerbate the problem of financing the (high-risks in the) high-value plans. Ultimately, with high probability this approach would drive the high-value plans out of the market due to adverse selection premium spirals and would cause the market to end up in a one-value plan system or even to unravel – at least in a system without accompanying regulation and resources from the state (like risk adjustment or tax credits). Hence, vertical differentiation is no solution to the problem of providing affordable health insurance coverage to high-risk individuals.

5.1.2 Voluntary private health insurance in the Netherlands

An interesting historical example of the second policy approach (i.e. enforcing mandatory cross-subsidies) is the former Dutch voluntary private health insurance market between 1986 to 2006. Until 2006 about one third of the Dutch population – consisting of high-income people exceeding the income threshold of eligibility for social health insurance – were covered by private health insurance. However, over time access to affordable private health insurance became problematic even for high-risk individuals with a relatively high income due to a combination of increasing risk rating and rising health care costs (Vonk and Schut, Reference Vonk and Schut2019). To keep private health insurance affordable for high-risk individuals since 1986 private health insurers were obliged to offer a legally standardized policy at a maximum premium to elderly (65 years and older) and other high-risk individuals (those whose premium exceeded the maximum premium). About 15% of the privately insured population were entitled to these standardized policies, accounting for about 35% of total expenses covered by private insurance (Vonk and Schut, Reference Vonk and Schut2019). As the legally determined maximum premium was far below the expected costs of these high-risk individuals, all privately insured had to pay a substantial surcharge to cover the additional costs for people in the high-risk pool.Footnote 13 Contrary to what might be expected, the mandatory cross subsidies did not affect the almost 100% uptake of private health insurance. Hence, the market clearly did not tend to unravel due to an upward spiralling surcharge (that would have occurred if an increasing number of relatively low-risk individuals would have left the market). Plausible explanations for the fact that the substantial mandatory cross subsidies did not reduce uptake of insurance are that the privately insured were those with a relatively high income and were facing a dichotomous choice between either buying private health insurance including a mandatory surcharge or having no health insurance at all. Another potential explanation is that the reclassification risk was included in the covered risk because all private health insurance contracts had a guaranteed renewability clause (Herring and Pauly, Reference Herring and Pauly2006; Vonk and Schut, Reference Vonk and Schut2019). Presumably, the Dutch privately insured were willing and able to pay a substantial cross subsidy to keep their health insurance coverage to reduce this risk.Footnote 14 However, since private health insurers were fully retrospectively compensated for the health care expenses of the high-risk individuals with a standardized policy, they did no longer have any incentive to contain cost of the most expensive enrollees. Hence, for this and other reasons, maintaining the voluntary private health insurance market was not considered viable and effective in the long run. Eventually, in 2006 the voluntary private health insurance was abolished and merged with the former sickness fund insurance scheme for lower and middle-income groups into a new universal mandatory health insurance scheme carried out by competing private health insurers (Vonk and Schut, Reference Vonk and Schut2019).

5.2 Mandatory universal health insuranceFootnote 15

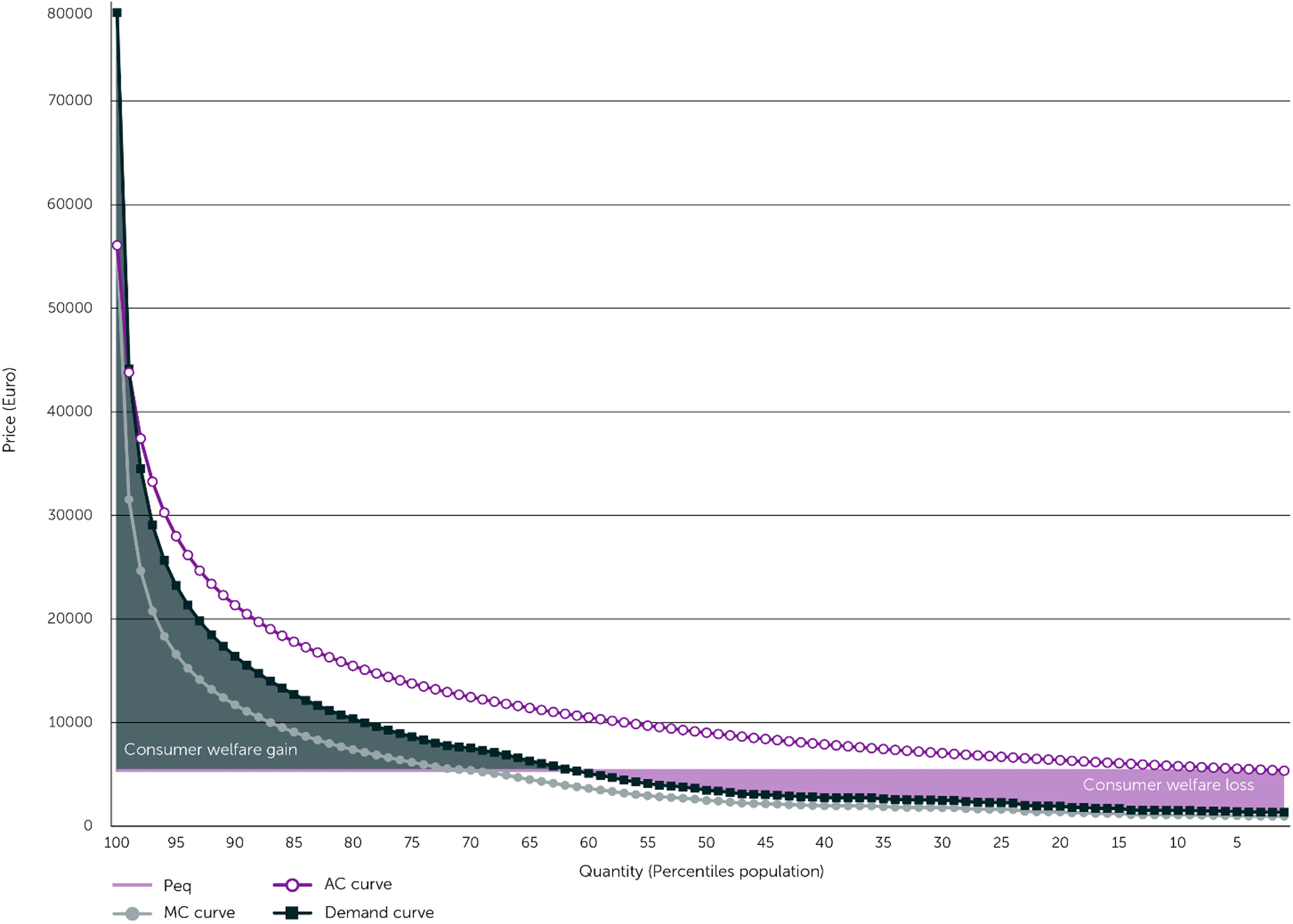

Establishing mandatory universal health insurance is by far the most popular policy approach in high-income countries to prevent welfare loss due to unaffordable health insurance for high-risk individuals.Footnote 16 As argued by EF, in the textbook case mandatory insurance is the canonical solution to solve the inefficiency created by adverse selection because it is always (weakly) welfare-improving.Footnote 17 Nevertheless, EF also point out that in the presence of insurance loads and preference heterogeneity, the textbook result of an unambiguous welfare gain from mandatory coverage no longer obtains. However, in the presence of highly convex marginal cost curves, the negative welfare effects of insurance loads and not accommodating preference heterogeneity are likely to be relatively small compared to the welfare loss of not being able to provide coverage to a substantial part of the population. Douven et al. (Reference Douven, Kauer, Demme, Paolucci, van de Ven, Wasem and Zhao2022) show that depending on the characteristics of the health insurance market in various countries, the share of the loading fee varies from about 5% of total premium payments in Germany and the Netherlands to about 20% in the US. At the average cost in Germany of 5,366 euro in 2017 this would mean a loading fee of about 270 euro (based on German loading percentage), which is likely to be well below the average risk premium people would be willing to pay. Moreover, as illustrated in Figure 5 the introduction of mandatory health insurance with a community-rated premium will result in a substantial welfare gain for the 40% higher-risk individuals (the grey-shaded area) which may outweigh the welfare loss for the 60% lower-risk individuals (the purple shaded area) if the risk premium is sufficiently high to compensate for the loading fee.Footnote 18

Einav and Finkelstein framework with consumer welfare gains and losses of mandatory insurance with community rating.

However, the welfare gains for high-risk individuals in Figure 5 are likely to be considerably underestimated because it presupposes that high-risk individuals are not only willing but also able to pay risk-rated premiums. This supposition may not be correct because, as argued before, risk-rated premiums will likely be unaffordable for most high-risk individuals, which would imply that they will not be able to buy health insurance at all. Hence, the introduction of mandatory insurance would result in providing high-risk people access to ‘otherwise unaffordable health insurance’ and presumably also access to ‘otherwise unaffordable health care’. As explained by Nyman (Reference Nyman1999) this is likely to result in a huge additional welfare gain.

A potential drawback of mandatory health insurance is that it may also result in welfare loss because insurers may be less incentivized to increase efficiency and to accommodate heterogeneous consumer preferences. However, in a growing number of countries these potential drawbacks have been reduced by combining mandatory health insurance with competition and consumer choice in the presence of an increasingly sophisticated system of risk adjustment (van de Ven et al., Reference van de Ven, Beck, Buchner, Schokkaert, Schut, Shmueli and Wasem2013; McGuire and van Kleef, Reference McGuire and van Kleef2018). Even apart from this, the welfare gains for high-risk individuals, including the gain of access to ‘otherwise unaffordable health insurance’ and presumably also ‘otherwise unaffordable health care’, is likely to be much higher than the welfare loss for low-risk individuals.

6. Conclusion

In this paper, we have shown that incorporating the extreme skewness of predictable individual health care expenses in the standard EF-framework for analysing the performance of voluntary (health) insurance markets with asymmetric information, shifts the focus from the negative welfare consequences of underinsurance of low-risk individuals to the presumably much larger negative welfare effects of unaffordable health insurance for high-risk individuals.Footnote 19 Moreover, since the skewness of the distribution of health care costs has become increasingly pronounced (i.e., steeper) over time (Buchner and Wasem, Reference Buchner and Wasem2006; Vonk and Schut, Reference Vonk and Schut2019), the access problem and negative welfare effects for high-risk individuals in a voluntary health insurance market have increased over time too.

Despite the theoretical focus on the welfare loss for low-risk individuals, in practice, many countries primarily focused on addressing the welfare loss for high-risk individuals by adopting various approaches. Some countries rely on external and internal mandatory cross-subsidies in voluntary health insurance markets. A first approach excludes high-risk individuals from the market and subsidises them by external funds. This may reduce the problem but may still leave a substantial part of the population without health insurance and would transfer the problem of funding the expenditure of high-risk individuals to anywhere else. The US health insurance system makes clear that external funding and pooling mechanisms, mandatory premium subsidies (e.g., by employers or by the government) and regulation (e.g., community rating, prohibiting pre-existing conditions clauses) are necessary to further reduce this problem. However, to date, this incremental approach has not been successful in realising universal access or even in coming close to it (Baicker et al., Reference Baicker, Chandra and Shepard2023).

A second approach, which was used in the former Dutch voluntary private health insurance market, is to impose mandatory internal cross-subsidies. However, whether this approach can be successful in ensuring access for high-risk individuals, critically depends on the willingness of low-risk individuals to buy this private health insurance since the mandatory cross-subsidy is likely to be high. Hence, this approach is vulnerable to an adverse selection spiral of increasing mandatory cross-subsidies and low-risk individuals leaving the market.

By far the most popular and effective way to solve the access problem for high-risk individuals is the establishment of universal mandatory health insurance with mandatory cross-subsidies. Apparently, in most societies following this approach the resulting welfare loss for low-risk individuals is outweighed by the huge welfare gains for high-risk individuals, including the gain of providing access to ‘otherwise unaffordable health insurance’ and presumably also ‘otherwise unaffordable health care’. Interestingly, Baicker et al. (Reference Baicker, Chandra and Shepard2023) argue that rather than the US approach of beginning with the presumption that the main need is addressing market failures to expand coverage, a more fruitful approach, which is followed by almost all other high-income countries, is to begin with the explicit presumption that covering everyone with some form of insurance is a social goal.Footnote 20 This presumption perfectly aligns with our finding that by taking into account the extreme skewness of predictable health care cost, the main problem of voluntary health insurance markets is to address the huge negative welfare consequences for high-risk individuals of having no access to affordable health insurance.

Acknowledgements

We thank two anonymous reviewers and Jacob Glazer, Tom McGuire, Richard van Kleef, Wynand van de Ven, Jürgen Wasem, and the participants of the conference of the Risk Adjustment Network in Weggis, Switzerland, September 2021, for their helpful comments. In addition, we thank Theresa Hüer for her support in making calculations based on the German data.

Financial support

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Competing interests

Both authors do not have any competing interests to disclose.

Open access

Open access