The rise of populism in recent years has stimulated interest in late nineteenth century American Populism and revealed conflicting interpretations of its nature and heritage.Footnote 1 Less controversial is the historical narrative stating that Populist policy proposals formed the basis of numerous Progressive Era reforms, which in turn influenced the political ideology underpinning the New Deal and the mid-century liberal state.Footnote 2 When the Great Depression hit, “a generation of Populist and Progressive policy proposals were already on the shelf, ready for [New Dealers] to pick them up.”Footnote 3 This article explores this narrative’s historical foundations through the prism of federal government support of cooperative business enterprise.

Cooperatives have a rich history in the US stretching back to the eighteenth century, but they became particularly salient around 1890 when the Southern Farmers’ Alliance, the forerunner of the People’s Party, championed the idea of a “cooperative commonwealth” in an attempt “to adapt the model of large-scale enterprise to their own needs of association and marketing.”Footnote 4 As Lawrence Goodwyn famously argued, under the leadership of Charles Macune the Alliance saw cooperatives as a means of increasing farmers’ market power and breaking the merchant-dominated crop-lien system that underpinned the South’s socioeconomic order. However, these grassroots efforts to develop new corporate forms encountered two major impediments: antitrust law and credit availability.Footnote 5 If, as Elizabeth Sanders has argued, farmers were the main driving force behind the federal state’s growth in the early twentieth century, then how did the federal government address these twin impediments in the decades preceding the New Deal?Footnote 6

Scholars have shown how farmers increasingly embraced the corporate model through a process of social accommodation and how changes to federal antitrust law favored that shift.Footnote 7 In the 1890s, antimonopoly provisions made it impossible for farmers to cooperate on a large scale across state boundaries, yet in the early 1920s, the Capper–Volstead Act—agriculture’s “Magna Carta”—gave farmers’ “benevolent trusts” a full exemption from federal antitrust law. Nevertheless, large-scale agricultural cooperatives experienced slow growth and failed to limit overproduction in the 1920s owing to collective action problems.Footnote 8 Farmers only effectively overcame these impediments thanks to the introduction of New Deal reforms such as the Agricultural Adjustment Act of 1933, which exhibited direct parallels “both in specific content and general orientation” with the Populist program of the 1890s.Footnote 9

A separate body of literature addresses how farmer cooperatives overcame the second impediment. Farmers’ struggles to access credit is of course very present in research on the “money question,” and generations of scholars have been fascinated by the Southern Farmers’ Alliance’s subtreasury plan—a state-based mechanism for monetizing crop inventories, allowing farmers to control the distribution of their produce rather than having to immediately sell their entire crop to the merchant.Footnote 10 By “remov[ing] merchant bankers from American agricultural production,” it would have provided a “workable system of democratic large-scale production” rather than “so-called ‘cooperation’ that was in reality a mode of bureaucratic collectivization hierarchically imposed by state planners.”Footnote 11 While the plan was never implemented, it has had a lasting influence on historical narratives of early twentieth century financial reforms. Scholars tell us that the Federal Reserve Act of 1913 and the Warehouse Act of 1916 together replicated the subtreasury plan’s “spirit” by increasing money supply elasticity thanks to a government backstop for loans made using commercial paper secured by agricultural commodities.Footnote 12 They claim the plan inspired the creation of a system of Federal Intermediate Credit Banks in 1923 (although others, such as Goodwyn, assert that because they mainly catered to middle-class farmers, “in no sense were the credit problems of the ‘whole class’ touched upon in ways that … Macune and other Populist Greenbackers would have respected”).Footnote 13 And they contend that the plan influenced New Deal-era debates about the macroeconomic advantages of agricultural credit reform, buffer stocks of key commodities, and commodity-based monetary systems.Footnote 14 Yet, the basis for these claims is unclear, and much is still to be learned about how Southern Populist credit proposals shaped institutional outcomes in a time of major changes in the architecture of money and credit. Admittedly, scholars note that the Federal Farm Loan Act of 1916—flagged as the federal government’s first active use of credit as a means of reaching policy goals—relied in part on cooperative credit and a democratization of farm credit decisions.Footnote 15 But because the act only addressed long-term financing of fixed capital and land, their studies shed no light on government involvement in facilitating farmer cooperatives’ access to working capital.

There are good reasons to believe that an examination of how cooperatives financed their operations, and the role of the state therein, might offer novel insights into the US political economy. Research on other countries has shown that governments have promoted cooperatives to redistribute market power, increase political and economic stability, and support economic development.Footnote 16 In addition, it offers an underexploited angle on the historical relationship between financial systems and business firms, which include cooperatives, since they face the same organizational challenges as other corporations.Footnote 17 Germany provides a concrete example illustrating this potential. As in the US South, the German cooperative movement sought to overcome the fragmented agricultural sector’s structural weaknesses vis-à-vis the merchant-creditor class.Footnote 18 The movement’s underlying ideology was “to stave off the twin forces of large-scale capitalism … and social democracy … by organizing farmers, small producers, and others in ways that allowed them to remain independent [while taking] advantage of the benefits of combination.”Footnote 19 State actors in Germany believed cooperatives could neutralize political extremism, and the creation of the Prussian State Central Cooperative Bank (Preussenkasse) in 1895 illustrated their desire to “shape and control the cooperative movement.”Footnote 20 While they could in theory obtain loans from the central bank, undercapitalized cooperatives did not possess the necessary collateral, so only a lender of last resort attuned to their needs could “offset the natural advantages big business enjoyed in their access to large banks.” As a Prussian parliamentarian noted: The Cooperative Central Bank’s creation signaled that the central bank was “unable to satisfy the credit needs of agriculture and the handicrafts” even though they had “the same right to have their credit needs met by the state as [did] heavy industry, large-scale trade, or the financial markets.”Footnote 21

This article explores the political economy of US federal state involvement in providing working capital to farmer cooperatives. To that end, it focuses on cooperative marketing associations (CMAs) in the raw cotton sector and seeks to identify how intermediate credit was established as a concept worthy of government attention in the 1910s and early 1920s—just a few decades after the initial calls for intervention. Of course, cotton was not the only sector that stood to benefit from government support of CMAs, but it makes sense to focus on this commodity for two main reasons. First, of all US agricultural products, cotton had unparalleled economic significance at the regional, national, and international level. Raw cotton production remained a systemically important sector across the South. It represented on average 48.5% of the aggregate value of all crops across the 10 biggest cotton-producing states, and in Mississippi and Texas (by far the largest producer by the 1920s) the figure was over 60%.Footnote 22 Just as the South was known as the “Cotton Kingdom” in the late nineteenth century when its farmers had cultivated the fiber “as though [it] were food and drink and wine and music,” cotton remained king through the interwar period, meaning “Southern economic fortunes were [still] closely tied to the fortunes of this monarch.”Footnote 23 In 1938—the year President Roosevelt famously referred to cotton as “the nation’s no. 1 economic problem”—it constituted the only source of income for half of Southern farmers.Footnote 24 Meanwhile, at the national level, cotton still represented the largest source of cash receipts of all US crops in the 1920s.Footnote 25 Finally, cotton remained a crucial component of US international trade. During the 1920–1927 period, between 43% and 78% of raw cotton production was exported; it remained the single largest export commodity until the late 1930s; and despite increased production by some foreign countries, the US still produced between 53% and 68% of the global raw cotton supply between 1920 and 1928.Footnote 26

The second reason to focus on cotton is that the fiber played a unique role in the US’s domestic banking system and its international financial relations. Agricultural commodities created profit-making opportunities for those able to provide the financial resources necessary to overcome the temporal disunity between production, harvest-time labor requirements, and distribution and storage.Footnote 27 However, these features also meant that cotton—which was subject to large price variations determined by elastic industrial demand, a particularly short harvest period, and huge storage needs—created a state of “systemic seasonality” in the US South where it dominated the economy and underlay much of the short-term commercial paper held on local banks’ balance sheets.Footnote 28 Owing to these banks’ reliance on correspondent banks to move the crop at harvest time, cotton constituted a destabilizing force in the entire banking and financial system. Furthermore, a substantial share of the foreign exchange used to pay for imports and service overseas debts came in the form of bills of exchange drawn by US exporters on European banks and merchants, so because cotton was such a crucial export, the fiber played a central role in the nation’s international financial and monetary relations and was a major determinant of the domestic money supply.Footnote 29 Given the profound financial and monetary reforms initiated with the Federal Reserve Act of 1913, focusing on cotton provides an effective lens for exploring how debates about government support of intermediate credit access fit into the broader institutional transformations that enabled the US to emerge as a global financial and monetary power after World War I (WWI).

This research weaves together primary sources from the Federal Reserve, the federal government, and key contemporary actors, illustrating how cotton and Southern Populist arguments about agricultural credit continued to shape institutional outcomes. It is inspired by the notion that finance is the “connective tissue” of capitalist systems and answers calls to “explore the ways that the financial system [binds] together elites and ordinary people” by focusing on “struggles over the means of payment as well as the means of production.”Footnote 30 The article argues that economic dynamics at the structural and conjunctural levels, as well as influential actors’ appropriation of Southern Populist claims about cooperatives’ macroeconomic benefits, are all essential to explain the federal government’s involvement in intermediate trade credit—a form of working capital used to purchase, transport, and distribute goods. If powerful actors—including the Fed, bankers, and industrialists—got behind “class legislation” favoring CMAs by liberalizing Fed rules and creating the Federal Intermediate Credit Banks, it was because they recognized the danger that commodity market volatility and agrarian politics posed to US capitalism itself. Yet despite top-down efforts to ensure the viability of corporate-style agricultural cooperatives, the focus on trade finance accommodated agriculture in a way that only addressed the distribution and storage phase of the production cycle. In so doing, central bankers, bureaucrats, and lawmakers betrayed the progressive impetus behind Populists’ original cooperative vision—to organize cotton farmers into collective bodies that could escape the merchant-dominated crop-lien system by controlling both the production and distribution of crops using cheap and reliable public credit.

These insights confirm that histories of public policies favoring cooperative enterprises reveal “deliberate state action […] even if it is not immediately visible.”Footnote 31 In this regard, they contribute to the literature on “alternative models of corporate liberalism” and stress the significance of private-order organizations, including “associative forms of enterprise” that transcend markets and hierarchies, in economic coordination.Footnote 32 The article also enriches histories of US capitalism. By highlighting federal involvement in “minting” new forms of marketable debt, the article provides an illustration of how government institutions actively contributed to capitalization and financialization processes, liquidity provision, and credit market discipline.Footnote 33 Thanks to its focus on cotton, it complements narratives of the structural importance of this commodity in US economic history, reminding us that it is key to understanding the country’s political economy in the late Progressive and New Eras.Footnote 34 Finally, the article offers insights into the institutions enabling the accommodation of agriculture in industrial capitalism and the ultimate resolution of the US economy’s contradictory status as “neither core nor periphery”—a history that has a direct bearing on debates about the role of agriculture in the Great Depression and the origins of New Deal-era efforts to achieve macroeconomic stabilization through commodity market intervention.Footnote 35

Unlikely Bedfellows

Late nineteenth century American Populism marked the culmination of a decades-old antimonopoly current in US political life in which the “money question” was central.Footnote 36 In the postbellum era, many Americans came to see money “as something that shaped the national political system” and advocated for government regulation of it to ensure equal economic opportunity and the democratic rights of all.Footnote 37

The “money question” manifested itself in particular ways in the Cotton South. Following the abolition of slavery and the end of the plantation system, general furnishing merchants provided farmers with foodstuffs and production inputs on credit secured by crop liens (a legal claim on the future crop) at exorbitant rates of interest. To liquidate their loans, farmers had to sell their harvested crops to the lien-holding merchant at the prevailing price.Footnote 38 Most small-scale cotton growers—including both Black and white sharecroppers and tenant farmers—were therefore subject to a system of debt peonage in which they were exploited “by the monopolistic financial structure dominated by the local merchant.”Footnote 39 These merchant-bankers funneled credit into the underbanked South and linked the region to global trading and credit networks.Footnote 40 The crop-lien system emerged as an institutional means for local credit merchants to funnel working capital from New York to farmers and became a powerful driver of land centralization since it reduced land-owning farmers to a state of permanent indebtedness, making them susceptible to seizure of their secondary assets.Footnote 41 Because of this danger and its structuring of social relations and imposition of labor discipline, the crop-lien system was widely considered by cotton growers as “a root ‘evil’ of the postbellum South.”Footnote 42

The rise of the Southern Farmers’ Alliance in the late 1870s embodied farmers’ resistance to this “evil.” Central to its vision was the creation of a “cooperative commonwealth” in which farmers would use cooperative enterprise to wrest control over the production and distribution of cotton from middlemen, turning themselves from price takers into price makers. However, cooperatives faced a major problem: The credit system’s local gatekeepers refused to provide them with the working and investment capital they needed to operate. Southern farmers concluded that their cooperative vision was doomed “unless fundamental changes were made in the American monetary system.”Footnote 43

Seeing the federal government as an alternative to private sources of credit, Alliance members led by Charles Macune developed the subtreasury plan. The plan consisted of a system of government warehouses in which farmers could store staple, nonperishable commodities such as cotton against which they could obtain certificates of deposit. They could then borrow up to 80% of the certificate’s face value for up to a year at 1% interest, or sell the certificates for cash when the price was right.Footnote 44 This mechanism would have established the US Treasury as the “preeminent capital institution in society” and “as such, it removed merchant bankers from American agricultural production.”Footnote 45 By providing medium-term working capital to farmers, it simultaneously addressed “the problems of financing cooperatives, the seasonal volatility of basic commodity prices, the scarcity of banking offices in rural areas, the lack of a ‘lender of last resort’ for agriculture, inefficient storage and cross-shipping, the downward stickiness of prices paid by farmers vis-à-vis prices received for crops, and the effects of the secular deflation on farmers’ debt burdens….”Footnote 46 Its advocates insisted that it would both “break the entire oppressive Southern system of credit and distribution” and benefit the economy as a whole.Footnote 47

The subtreasury plan was stillborn following in-fighting among Alliance members, but following the Panic of 1893, agrarians in favor of a more elastic money supply found unlikely bedfellows in the budding financial reform movement that eventually culminated in the Federal Reserve System’s creation. In the final report of the Indianapolis Monetary Conference of 1894, monetary economist J. Laurence Laughlin blamed the Panic on “the failure to provide the means for a gradual and sufficient increase in the volume of the currency to meet the needs of an increasing population and an enlarging commerce.”Footnote 48 Influential journalist Charles Conant “systematically related the glut of savings depressing investment and industry in the metropolitan Northeast to the scarcity of currency and credit sparking Populist protest in the rural South and West.” In so doing, financial reformers such as he were effectively “coopting agrarian calls for an elastic currency and low-interest loans for farmers” while rejecting “radical demands for public, democratic, [and] legislative control of currency and credit.”Footnote 49

Members of the National Monetary Commission formed after the Panic of 1907 established an influential narrative, still ubiquitous in the secondary literature, linking the vast agricultural sector’s huge seasonal demand for money to recurrent financial crises.Footnote 50 That demand, it alleged, prompted country banks to withdraw balances held with correspondent banks in major money centers such as New York, causing tremendous outflows that forced Wall Street banks to call in their loans to stockbrokers and triggering volatility in securities prices and wholesale interest rates. These banks were sometimes “so stressed, so drained of the lawful money needed to satisfy reserve requirements, that depositors with no agricultural interest but concerned about the solvency of the banks would convert their deposits to cash as a precautionary matter.”Footnote 51 The country’s inelastic money supply therefore constituted a threat to financial stability owing to the link that existed between the banking and financial systems through New York’s call loan market on stock exchange collateral, which served as the main outlet for the banking system’s liquid resources. Importantly, cotton had pride of place in this narrative. Given the South’s “‘colonial style’ dependence” on cotton production and the strong relationship between financial and commodity flows that prevailed there, the fiber was of systemic importance, “afflicting related segments of the cotton economy and its pivotal financial intermediaries”; as a result, banks in the region had a “disproportionate impact … on the seasonal liquidity strains in New York and national money markets prior to the founding of the Fed.”Footnote 52

On the one hand, Populists favored monetary reform on account of the “pattern of seasonal changes in interest rates,” which they considered as a creditor conspiracy designed to make them pay more for liquidity when they needed it most.Footnote 53 On the other hand, financial reformers believed the country’s inelastic currency posed a direct threat to banking and financial system stability. From 1907 onward, reformers increasingly saw their task as being as much about money market reform as it was about currency.Footnote 54 But disagreement remained about whether a central bank was desirable and how exactly the federal government should address farm credit demands.

Agricultural Credit in the Financial Reform Debate

In the first decade of the twentieth century, influential Wall Street banker Paul M. Warburg became the most prominent advocate of the creation of a “modern system of currency and finance” modeled on European precedents.Footnote 55 At the heart of this vision was the creation of a money market wherein standardized commercial paper in the form of bills of exchange (or “acceptances”) would serve as collateral instead of stock exchange securities. Creating a national acceptance market would increase financial stability and demonstrate to foreign investors that it was safe to keep liquid balances in the country.Footnote 56 Crucially, as Warburg argued, acceptances represented “a substitute for money” and an “auxiliary currency,” which would directly benefit farmers if widely adopted.Footnote 57 As the National Monetary Commission’s final report outlined:

The man who raises cotton in Mississippi or cattle in Texas, or the farmer who raises wheat in the Northwest, cannot readily find a market in Chicago, New York, or London, for the obligations arising out of the transactions connected with the growth and movement of his products, because the bankers of these cities have no knowledge of his character and responsibility.Footnote 58

However, if a liquid, impersonal market for standardized commercial paper emerged, farmers could access cheap liquidity anywhere in the country, thereby reducing regional interest rate differentials and effectively allowing them to circumvent the local gatekeepers of the credit system.

Despite the growing consensus that a new money market based on acceptances was an essential feature of financial reform, considerable discord remained about the need for a central bank. Financial reformers such as Laughlin espoused a specific version of the “real bills” doctrine according to which short-term commercial paper arising out of regular business transactions would constitute the main class of banking system liabilities. Issuing money and credit against such assets would, they claimed, create an elastic money supply that adjusted itself to economic demand without the need for active intervention by a central bank. This doctrinal framework ensured that “certain types of business credit could always be converted into bank reserves at a local reserve bank” such that “small bankers and their business clients would never again have to rely on the whim of some faraway Wall Street banker.”Footnote 59 In an alternative view, advocated by Warburg, a central bank and a national acceptance market were “absolutely interdependent” since the former relied on the latter to implement monetary policy, and the latter relied on the former to guarantee the liquidity of commercial paper by providing a mechanism to monetize it.Footnote 60 Only then could the acceptance market become a viable replacement for the call loan market and thus ensure increased banking and financial system stability. Furthermore, central banking advocates “roundly criticized and ridiculed” proponents of the “real bills” doctrine, not least because self-liquidating acceptances were almost nonexistent in the country.Footnote 61 While the first view embodied a vision of small-scale, competitive-entrepreneurial, market-based capitalism, the second view concretized a large-scale, corporate-industrial capitalism where the central bank played a key coordinating role (the tension between these views would last until the Great Depression).Footnote 62

An asset-backed currency and acceptance market had potential benefits for financial reformers and farmers, but the definition of what constituted “short-term commercial paper” remained contentious. In the lead-up to the Federal Reserve Act of 1913, former Populists drew attention to the distributional impact of policies governing the types of assets that the proposed reserve system would monetize, insisting it would “shift resources away from New York to rural communities.”Footnote 63 Agrarians wanted a decentralized public system guaranteeing independence from the so-called money trust, which many believed controlled the nation’s supply of credit—a claim vindicated, albeit mistakenly, by the Pujo Committee in early 1913—so they applauded the exclusion of long-term securities from Fed discount window eligibility.Footnote 64 However, they also opposed Rep. Carter Glass’s proposal to limit eligibility to commercial paper with maturities up to 45 days because this favored industrial and mercantile firms while disadvantaging farmers given their longer production and distribution cycle.Footnote 65 In the end, they successfully lobbied to extend the general eligibility limit to 90 days and secured special status for commercial paper with maturities up to 6 months drawn to finance agricultural activity.

The Federal Reserve Act of 1913 endowed the US monetary system with the elastic currency long demanded by farmers and made provisions to address their credit needs. As US cooperative history specialist Joseph Knapp observed: “Farmers overwhelmingly recognized the need for reform, and in their eyes the act constituted the first step in the right direction.”Footnote 66 Insofar as the Act ostensibly established the “real bills” doctrine as its guiding principle and ensured that the Fed could not monetize stock exchange securities, it offered solace to antimonopolist farmers.Footnote 67 As one economist noted: “At first glance, the sub-treasury…[appeared] to be consistent with the ‘real bills’ doctrine” insofar as “sub-treasury agents [would have stood] passively ready to store and make loans in legal tender notes on all new produce presented and to withdraw such notes when crops are redeemed.”Footnote 68 Nevertheless, the Act had limitations from the perspective of CMAs. It restricted agricultural paper holdings by reserve banks and provided no backstop for commercial paper beyond 90 days if drawn for the purpose of storage and distribution.Footnote 69 And although successive short-term credits could in theory be renewed to carry inventories over longer periods, CMAs might still have to offload their produce at prevailing market prices if their bankers refused to renew them. Furthermore, despite allowing member banks to accept bills of exchange on behalf of other firms, thereby creating “bankers’ acceptances,” the Act only authorized them to do so in international transactions, and the Fed itself could only buy bankers’ acceptances resulting from foreign trade. In this respect, it did not allow the creation of a broad, liquid, and impersonal market for domestic acceptances, so the Act fell short of empowering rural borrowers to escape the influence of local lenders in the ways that financial reformers had promised.

The Act’s broad support in Congress—including among representatives and senators from peripheral areas—was likely due to farmers’ success in “compelling the Wilson administration to commit to future action on long-term agricultural credit.”Footnote 70 This was made a reality when a system of Federal Land Banks was established under the Federal Farm Loan Act of 1916. Between the Federal Reserve and the Land Banks, federal credit machinery therefore provided a backstop for farmers’ short-term and long-term debt. However, as farmers increasingly embraced corporate organizational forms, and as WWI and its aftermath exacerbated commodity market instability and created a providential opportunity to build out the US acceptance market, both farmers and financiers came to appreciate the advantages of liberalizing Fed eligibility rules and introducing direct federal involvement in CMAs’ intermediate financing needs.

Early Federal Intermediate-Term Credit Support

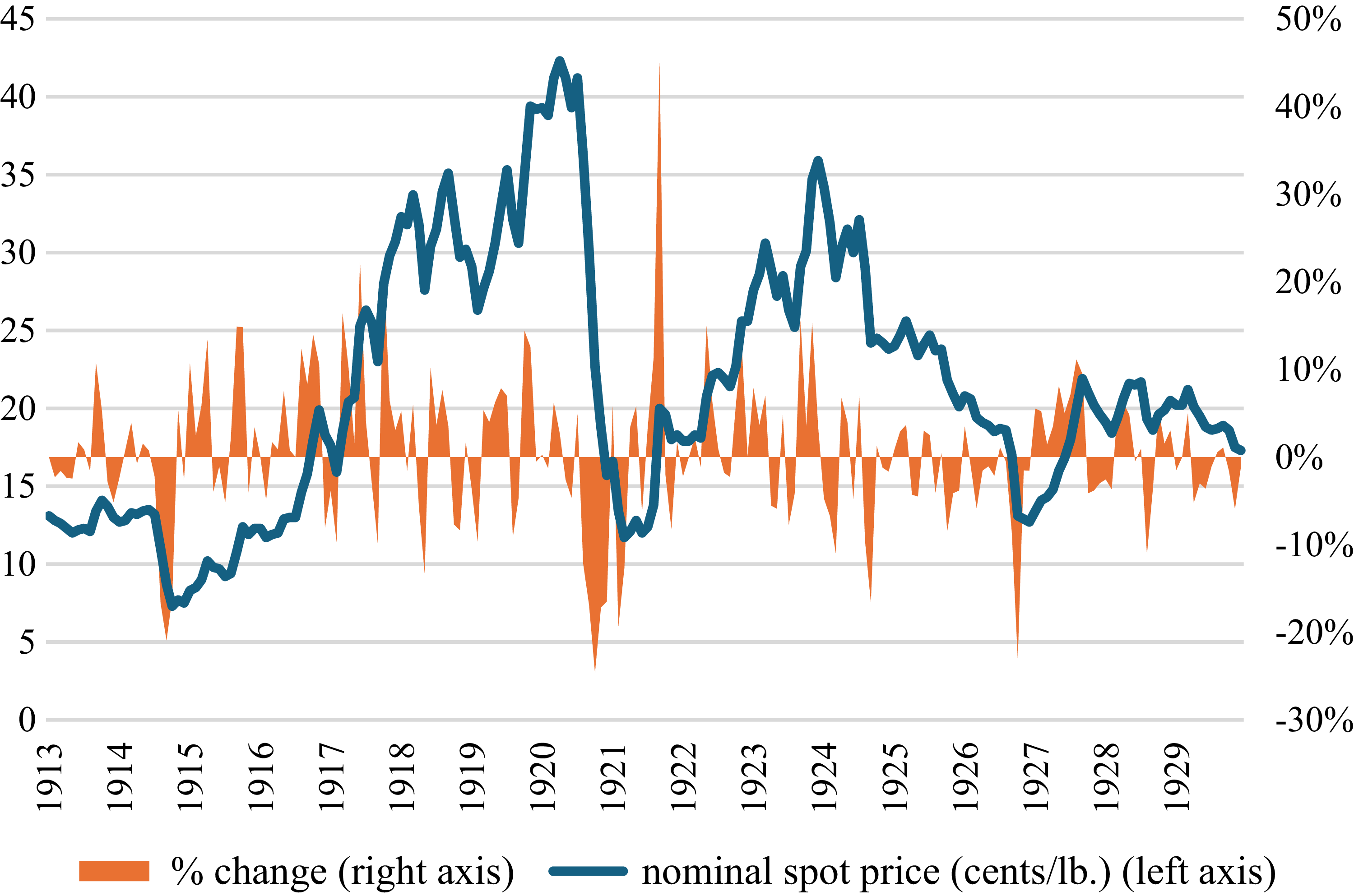

The eruption of WWI had a devastating effect on foreign demand for US cotton, underscoring both its economic importance and the threat it posed to banking system stability in the South. In the first 3 months of the 1914/1915 season, the value of cotton exports plummeted 76.4% compared with the previous year. Between July and November 1914, raw cotton prices in primary markets fell 45%.Footnote 71 The crop’s scale meant that even modest price changes greatly affected its total market value.Footnote 72 In 1914, the US cotton crop’s value dropped to $720 million, almost one-third less than the previous year’s $1.026 billion.Footnote 73 Demand for cotton later rebounded, but as Fig. 1 indicates, month-on-month fluctuations in wholesale prices were significant, both throughout the war and in subsequent years, posing a major threat to banks across the Cotton Belt and beyond.

Wholesale cotton prices (New York), monthly averages, 1913–1929.

(Source: Series 04006, National Bureau of Economic Research Macrohistory Database.)

The situation in cotton states led to a succession of early decisions liberalizing Fed eligibility regulations. In June 1915, the Fed created a special committee to study “the condition and needs of the cotton-growing districts.” In July, it introduced a preferential discount rate for commercial paper secured by staple commodities such as cotton that were fungible and commanded a ready market price, hoping to avoid “a repetition of the disastrous experiences of 1914” and to “[foster] a financial condition in which producers would not be obliged to sacrifice their cotton but would be assisted in the gradual and orderly marketing of the crop.”Footnote 74 In August, it made domestic trade acceptances eligible at the discount window.Footnote 75 Board Chairman Charles Hamlin expected this change would “aid materially in the marketing of the crops of the country during the coming autumn.” After all, “no staple commodity [was] subject to greater variations in price than is cotton” so it was “clearly in the common interest that credits based upon [cotton] be protected … from the danger of demoralization” because “sudden and violent fluctuations are clearly to the advantage of neither the loaning bank, the producer, the manufacturer nor the consumer.” The Fed trade acceptance backstop would be “a contributing factor in reducing these fluctuations” and “accomplished a great public good.”Footnote 76 The Board believed that extending the “acceptance system” to domestic trade would “tend to equalize interest rates the country over and help to broaden the [acceptance] market.”Footnote 77

Congress took two more decisive steps in this direction the following year. First, it passed the Warehouse Act of 1916 (essentially a broader version of the Cotton Warehouse Act of 1914, introduced to increase storage capacities in places such as Texas where they were lacking), creating a network of federally regulated private warehouses overseen by inspectors able to “sample, inspect, grade and weigh” warehoused products.Footnote 78 By giving warehouse receipts “real loan value,” this new legal framework ensured “a closer relation between the producers of commodities and the grantors of credit.”Footnote 79 Second, in a September 1916 amendment to the Federal Reserve Act, it formally authorized member banks to accept bills of exchange collateralized by shipping documents representing goods in transit or by warehouse receipts “conveying title covering readily marketable staples.”Footnote 80 This would “prove of especial value during crop-moving periods, when the lowest rates for bankers’ acceptances prevailing in any of the districts will become available for acceptances drawn against commodities in those districts where, owing to seasonal demands, rates naturally would have a tendency to be higher.”Footnote 81

The Federal Reserve Act supplied an institutional means of equalizing interest rates and providing an elastic source of currency and credit just as farmers and financial reformers had hoped. Considering the contentious nature of eligibility rules, justifying their liberalization in terms of the potential benefits for agriculture made it difficult to argue against them given the sector’s economic weight and agrarian political influence. Nevertheless, farmers were still at a disadvantage vis-à-vis merchants because their difficulties in accessing intermediate credit meant they still could not control the full production and distribution cycle. As the Progressive Farmer stated in 1915: “[We] must not continue to crucify labor on the merchants’ crop-lien crown of thorns.”Footnote 82

Demand for cotton increased in the latter part of WWI, driving up prices. But when cotton reemerged as a major concern after the conflict, the staple was central to the federal government’s decision to provide intermediate credit to farmer CMAs through the War Finance Corporation (WFC). The Treasury created the WFC in spring 1918 to stabilize securities markets strained by wartime borrowing.Footnote 83 By serving as a “rediscounting agency for banks holding long-term paper,” the WFC provided liquidity in ways that the Fed could not.Footnote 84 In its first 18 months, the WFC used its $500 million capital to advance hundreds of millions to public utility companies and railroads, while its securities operations successfully stabilized Liberty bond yields and influenced interest rates.Footnote 85 Then, in early 1919, WFC managing director Eugene Meyer—a former investment banker and War Industries Board veteran, later Fed governor, and architect and chairman of the Reconstruction Finance Corporation in the 1930s—suggested that the Corporation pivot to export financing.Footnote 86 Before the war, flows of securities offset trade imbalances, but Europe had sold much of its US securities holdings to pay for wartime imports, and a market for foreign securities had yet to emerge in New York.Footnote 87 As Meyer told the Senate: “We need at once, and on a large scale, an outlet for great quantities of our products. We cannot sell, if we demand payment now, because our customers [in Europe] have neither the gold nor the goods nor securities marketable in this country with which to make payment.”Footnote 88 Since private financial institutions struggled to set up adequate international dollar-based trade financing mechanisms, government support was needed. And so, in March 1919, Congress authorized the WFC to make up to $1 billion in export advances of up to 5 years provided that transactions could not be financed through normal banking channels.Footnote 89 Most of the advances in the following months financed food and cotton exports to Europe, sustaining demand for US staple commodities despite postwar political pressure to halt official lending. Although modest in quantitative terms, Meyer believed they were crucial because they reassured lenders and “[took] out of the hands of the professional price depressor a part of his power.”Footnote 90

On May 10, 1920, Treasury Secretary David F. Houston suspended WFC operations. For him, the corporation constituted an undesirable and superfluous relic of the war economy.Footnote 91 At the time, however, a crisis was looming. Between June and December 1920, as the wholesale price index plummeted 37%, livestock and staple commodity prices fell faster still.Footnote 92 Cotton prices fell 62% and, by spring 1921, they were down 80% in some primary markets.Footnote 93 Poverty in the South reached levels unseen since Reconstruction.Footnote 94 During the 1914 cotton crisis, Meyer had criticized the “regrettable exhibition of government paralysis” that had “cost the Southern Farmer tremendous and unnecessary losses”—a paralysis he attributed to US policymakers’ attachment to an “outworn laissez faire doctrine” despite the benefits of Europe’s “faire marcher” policies.Footnote 95 Meyer now vehemently criticized Houston’s decision and accused him of failing to recognize that economics “have to do with happiness and misery; solvency and insolvency; production and destruction; organization and disorganization; social and political stability or unrest and anarchy.”Footnote 96 He subsequently launched a national campaign to temporarily reactivate the WFC, lobbying bankers and businessmen to pressure Congress for support.Footnote 97 Opponents among Northeastern Republicans and financial and mercantile associations cast the WFC as “class legislation” designed by “politicking demagogues for the special benefit of farmers to the detriment of industrial interests,” or as “‘regional legislation’ in which prudent Northerners ‘were asked to pay for the financial embarrassment’ of improvident Southerners.”Footnote 98 However, despite considerable congressional wrangling, Meyer’s campaign succeeded, and the WFC resumed operations in early 1921.Footnote 99

In addition to mobilizing political support to revive the WFC, Meyer oversaw an August 1921 amendment to the WFC Act authorizing direct loans to CMAs. This outcome was not, however, a foregone conclusion. Congressional debates revealed deep divisions over whether the WFC should lend directly to farmers. Critics noted that the WFC financed commodity distributors, not producers. Initially, Meyer believed bank-mediated lending was more efficient; and some, such as Ellison DuRant “Cotton Ed” Smith, insisted bankers were a “necessary evil,” invoking “the absurdity of giving forty or fifty million men the right to come and apply for these loans.” But others criticized the disconnect between the WFC and farmers, intimating that corporation directors’ “only knowledge of agriculture has perhaps been acquired in their tedious trudging over the golf links” and decried the fact that it was only “after these farmers, who have viewed the crops from the twentieth story of a building in Wall Street, have decided that the farmer does not have good banking facilities or that he has a surplus of products […that] they can take some steps.”Footnote 100

Even those who supported direct government provision of trade finance to farmers disagreed about whether it should go to individuals or cooperatives. When an amendment explicitly naming “cooperative associations of producers” as eligible beneficiaries of WFC loans was proposed, one Mississippi Democrat clamored that this “presupposed that there is something sacred or valuable in an association of individuals which does not exist with an individual producer.” A Kentucky Democrat insisted there was “no reason why a producer with large holdings should be denied the right with sufficient collateral … to obtain aid from the government.” Nevertheless, the law passed on August 24, 1921 and authorized WFC advances of up to 1 year (3 years for livestock) “to any association composed of persons engaged in producing [staple agricultural products]” if members believed WWI’s effects caused “an abnormal surplus accumulation” or that “the ordinary banking facilities [were] inadequate to enable producers of or dealers in such products to carry them until they [could] be exported or sold for export in an orderly manner.”Footnote 101

Meyer himself subsequently emerged as a strong CMA advocate. In fact, when the amendment was passed, the WFC had already advanced funds to a Mississippi CMA to finance cotton inventories awaiting export, with more applications pending from cotton CMAs in Oklahoma and Texas, as well as fruit and grain CMAs in other states.Footnote 102 As Meyer later recounted, that first loan proved that CMAs “furnished a method by which the funds of the Corporation could be made available on a large scale to finance the orderly marketing of American agricultural products on a safe basis.” The spread of CMAs restored economic confidence across the cotton belt and “[did] more to facilitate recovery from the acute and extreme depression of last year than any other single factor.”Footnote 103 As he told the American Bankers Association in 1922: Because they had “grown up naturally in response to our own peculiar needs and economic conditions,” CMAs should occupy “a definite place in our economic structure.”Footnote 104

Underpinning Meyer’s advocacy of CMAs was a broader narrative about cotton’s central role in connecting the US economy to the world. While the cumulative US trade surplus amounted to $10.4 billion between 1865 and 1915, raw cotton exports reached $13.3 billion, so Meyer claimed it had been key to paying for imports and servicing foreign loans. Before WWI, US bankers borrowed in London and European money markets to meet peak agricultural credit demand in the summer, reimbursing lenders by remitting bills of exchange resulting from commodity exports in the fall. In the 6 months after the harvest, European merchants imported some 80% of the cotton crop, building up inventories that they then distributed to mills throughout the year. After WWI, cotton—the largest US export commodity—was still “king” and represented “white gold,” but the conflict had disrupted the fine-tuned distribution and financing machinery developed over decades. Owing to Europe’s financial and monetary instability, its merchants were buying cotton “hand-to-mouth” so just 50% of the crop was now exported during the first 6 months.Footnote 105 Between 1.2 and 2 million bales of cotton therefore had to be warehoused domestically until the second half of each year—an impossible task without improved storage mechanisms. In the prevailing economic uncertainty, the problem was exacerbated because US cotton jobbers, wholesalers, and manufacturers were “unwilling to carry their usual stocks in anticipation of demand,” preferring to shift this burden down the commodity chain to local merchants and producers. For Meyer, the inability of US firms to assume Europe’s former role in global cotton merchandising was the direct outcome of the “disorderly collapse” of the cotton market in 1920. This collapse threatened Southern banks’ stability and spread to the main money centers through the correspondent banking system, leading to reduced lending to other sectors.Footnote 106

In framing the domestic depression as a failure of US firms to assume the task of merchandising staple commodities such as cotton, Meyer was making an even more important point, namely that “the domestic consumption of American products was vitally dependent for … its buying power … on the smooth working of the whole machine of production and distribution, and that the breakdown in the foreign trade in American agricultural products and manufactured goods” was causing “a breakdown of the whole machine.”Footnote 107 Meyer liked to remind his interlocutors that farmers were the country’s biggest producers, borrowers, and consumers. In 1921, farm output topped $12 billion—about one-sixth of the gross domestic product and over two-thirds of world trade—down from an average of $18 billion in the prior 6 years. Outstanding loans to farmers in 1922 totaled $12 billion, about 25% of banking system resources. Farmers consumed one-tenth of US steel production, a quarter of coal and gasoline resources, almost half of all lumber, and three-fifths of all automobiles. Of the $500 million in farm machinery produced in 1920, 87% relied on domestic demand. When cotton and other primary commodity prices collapsed, “orders were cancelled, mills and factories shut down, and smokeless chimneys, idle cars, and jobless workers advertised … the dependence of business upon the farmers’ buying power.” The silver lining of the 1920–1921 Depression, Meyer quipped, was that it had “brought home to every businessman in every part of the nation a greater realization of the fact that agriculture furnishes the basis and the substance of American prosperity.”Footnote 108

The war’s effect on the raw cotton market drove early changes to Fed eligibility rules to boost banking stability and foster an acceptance market. Federal involvement in financing the cotton trade was driven by Meyer and the need to restore disrupted cotton distribution channels and counter the postwar downturn. Meyer not only initiated direct intermediate-term lending to CMAs but also legitimized such intervention by actively promoting a narrative echoing the Populist agrarian argument from the nineteenth century about the macroeconomic benefits of such a policy. As the next section shows, influential representatives from industry and finance concerned with economic, financial, and social stability, embraced this narrative. However, contention remained about how government-backed financial resources should be allocated to CMAs.

Friends in High Places

The Depression of 1920–1921 awakened the specter of a new agrarian revolt. Farmers blamed the crisis on the Fed and the Treasury’s deflationary policies—referred to as the “Crime of 1920”—which resulted in country banks calling in loans and forcing farmers “to dump their products on a demoralized market, adding greatly to the price panic.”Footnote 109 In early 1921, President Warren Harding “rode into office on the pleas of farmers oppressed by the panic,” but the Republican administration lacked a positive farm program.Footnote 110 This resulted in the formation of the influential “Farm Bloc,” whose primary goal was “to establish a proper balance between the agricultural and other industries.”Footnote 111 The Bloc was a cross-party group of senators instigated by Gray Silver, the director of the newly founded American Farm Bureau Federation, a conservative body that lobbied on behalf of large commercial farmers and played a major role in promoting CMAs in the 1920s.Footnote 112 Between 1921 and 1924, the Farm Bloc put forward a flurry of legislative proposals and enacted “the most advanced agricultural legislation to that date.”Footnote 113

The agricultural crisis of the early 1920s prompted Congress to create a Joint Commission of Agricultural Inquiry (JCAI) in 1921. It was tasked with investigating the crisis’ causes, the determinants of the differential between consumer prices and farmers’ income, the relationship between agricultural prices and the overall price level, and whether the banking and financial systems served the credit needs of agriculture.Footnote 114 The Commission condemned farmers’ reliance on profit-seeking middlemen for the merchandising of their produce and the management of marketing risks. Its final report endorsed cooperative marketing as a more efficient means of selling, sorting, grading, marketing, and processing farm goods, arguing that this would result in reduced consumer prices. It also concluded that “the banking machinery of the country [was] not adequately adapted to the farmer’s requirements.”Footnote 115

The cooperative movement experienced a flurry of activity in the post-depression years, and farmer associations and new government agencies supported their development.Footnote 116 The period was characterized by a push to create larger-scale marketing associations that would operate on a wider geographic scale than local cooperatives. These organizations took one of two forms: “commodity” (or centralized) and “federated” marketing associations. The differences between them can be described as follows:

The centralized organizations believe that it is absolutely necessary that all, or a large part of any one crop or commodity, shall be under the control of one organization, so that the movement of the crop to market can be absolutely regulated, and the price at which the crop is sold can be arranged by bargaining between this organization … and the buyers; whereas, in the federated organization, control more largely resides in the local cooperative unit, the central organization often merely acting as a selling agent for the locals, and ordinarily making little or no effort at collective bargaining.Footnote 117

Centralized marketing associations—referred to initially as the “California plan” and subsequently as the “Sapiro plan” after California lawyer Aaron Sapiro, who became their principal exponent—involved farmers signing multiyear sales contracts obliging them to sell their produce exclusively to such associations.Footnote 118 These were run by well-paid professional managers and operated on a noncapital, nonprofit basis and so were exempt from antitrust law under Section 6 of the Clayton Act.Footnote 119 In contrast to “federated” marketing associations, Sapiro-plan CMAs were top-down business organizations designed to overcome the fragmentation of individual producers by replicating the “group producer” model of large industrial firms.Footnote 120 Defenders of the federated model, meanwhile, thought cooperatives should remain “democratic organizations from the ‘ground up’” and considered Sapiro-plan CMAs as “autocratic.”Footnote 121 While these more “utopian” cooperatives tried to federate producers and consumers in a unified movement, Sapiro’s “militant” cooperatives “raised up a coöperative cult in America which cries down the Rochdale principles and exalts the new ‘coöperation American style,’ along lines of big business bargaining efficiency and ruthlessness. It is producer coöperation, legalistic in philosophy, monopolistic in spirit, and zealous for control of the market.”Footnote 122 Notwithstanding this fundamental difference of opinion, Sapiro was so successful that by 1923 he had helped found 66 centralized CMAs with annual revenues of $400 million, most of which involved fruit, grain, and dairy in the Northwest and the cotton, tobacco, and wheat sectors in the South and Midwest.Footnote 123

The idea that CMAs would support farmers, and that farmers faced unique economic problems requiring federal financial support, gained traction beyond agricultural circles. Increasingly, representatives from industry adopted a narrative similar to that advanced by Meyer, as illustrated by testimony at the National Agricultural Conference in January 1922. The National Vehicle and Implement Association bemoaned the 30% drop in its industry’s sales in 1921 and the 120,000 of its industry’s laborers unemployed in 1922. Faced with this situation, its members were “most earnestly in favor that to the greatest practicable extent … credit facilities to the farmers be extended.” The American Institute of Meat Packers agreed. Because its members were “expected to absorb all that is sent to market at whatever time or in whatever quantity [and] to pay cash on the spot” it was in their interest to avoid “violent fluctuations [in] labor, equipment, and financing.” Its representative insisted that “closer cooperation of the producers in stabilizing receipts at the market” was required to “stabilize values, prevent gluts and consequent wastes which will operate to the benefit of producer and consumer alike.”Footnote 124 Banking circles also acknowledged the benefits of organizing farmers through CMAs. Otto Kahn of investment bank Kuhn, Loeb & Co. was particularly wary of the dangers of agrarian radicalization.Footnote 125 If farmers could get “a larger percentage of the consumer’s dollar,” this would “prove of benefit to the financial, commercial and economic structure as a whole.” Although he “believe[d] in competition and [was] opposed to monopoly … [Kahn was] inclined to think that [they] had gone too far … in attempting to enforce competition under all circumstances and to prevent natural and legitimate cooperation” such as that envisaged by CMAs using sound business methods. To support their development, he therefore called on country bankers to buy CMAs’ commercial paper and on city banks to “carry such paper for their country correspondents for adequate periods.” This strategy, he believed, was the best way to discredit agrarian demagogues and their “quack remedies” and eliminate the danger “that the farming vote … succumb to the specious persuasiveness, the blandishments and false promises of those offering relief through unsound mercy and similar often-defeated and disproved but ever-resurging shame, illusions and heresies.”Footnote 126

Despite growing fears of social instability, there was also skepticism about CMAs’ ability to influence prices and resistance to the notion that they might try. Economist Wesley Clair Mitchell noted that understanding the relationship between financial policy and the price level required comprehensive price data that simply did not exist.Footnote 127 Cooperative specialists at the Department of Agriculture’s Bureau of Markets doubted that CMAs would become monopolies given their inability to control production.Footnote 128 Meanwhile, outright opposition to CMAs was led by merchant associations. Ostensibly in reaction to the proposed creation of a national grain sales cooperative for the purpose of eliminating middlemen and stabilizing prices, in June 1921 the National Grain Dealers’ Association formed a coalition of mercantile business groups that passed a resolution “holding ‘all class legislation to be vicious, indefensible and inimical to the general welfare.’”Footnote 129 The hostility of these business groups garnered sufficient attention for the US Senate to demand an inquiry into “the efforts of business, commercial, or other organizations to defeat the cooperative marketing movement which the farmers of the country have instituted.”Footnote 130 This resistance is hardly surprising given the words Sapiro used to describe them:

It is an essential of [the large speculative middlemen] that markets fluctuate as widely and as rapidly as possible, that there should be as many sales and resales of the product as possible, and there should be a surplus at the producing end from which he buys and a shortage at the consuming end to which he sells, as marked as possible. The speculators, as a class, have interests inimical to all other classes, and they are the only class that is hurt by co-operative marketing.Footnote 131

In addition to “middlemen,” the notorious articles on “The International Jew” in Henry Ford’s newspaper The Dearborn Independent formulated strong opposition. Through attacks on key CMA supporters, including Sapiro, Meyer, Khan, and Bernard Baruch, it mounted “a malignant assault … upon the fundamental principles and honest practices of cooperative marketing associations.”Footnote 132

Faced with this skepticism and outright hostility, CMA exponents needed to ensure their financial viability. Thankfully for them, they had a powerful ally: the Federal Reserve System. In the wake of WWI, Fed governor Harding was already endorsing “the creation of a cooperative sales organization to stimulate the exportation of cotton … [and give it] a more dependable market.” Noting that business organizations facilitated the coordination of production and distribution, a New York Fed memo stated that “it would be folly for any large manufacturer to devote his activities to production alone” since he “cannot afford to let his goods go on the market in a haphazard way nor does he wish to place himself at the mercy of a single buyer or group of buyers.” It asserted that “[cotton] is one of our great national industries, but of all our important industries it is the only one … which has no organized sales department.”Footnote 133

Following the postwar depression, in 1922, the Fed’s Advisory Council hailed “with great satisfaction” the JCAI’s suggestion of “strengthening the Federal Land Banks and extending their powers so as to permit them to discount agricultural or livestock paper with maturities running from six months to three years”; this would allow agriculture to access “vast sums in a sound and businesslike manner and would fill a serious gap in our present credit machinery.”Footnote 134 In early 1923, the American Acceptance Council—the body tasked with promoting the use of acceptances and the money market based on them—reported that the Fed was “greatly interested in the co-operative marketing movement and has used every opportunity to assist the organizers and managers of such associations to plan their financing so as to create ‘eligible paper.’”Footnote 135 This interest is confirmed by the Fed’s publication of a series of studies of the financing of cotton production and distribution in the spring of that same year.Footnote 136

Three policy changes introduced in 1922 illustrate the steps the Fed took to create eligible paper and facilitate CMAs’ access to cheap and flexible credit. The first one clarified whether bills of exchange drawn by farmers on, and accepted by, their CMA and discounted by farmers at their local bank would be counted as agricultural paper used for generic working capital purposes (maturities up to 6 months) or true commercial paper linked to distribution and marketing (maturities up to 90 days). As established in a separate 1921 decision in response to a query from Aaron Sapiro himself, such drafts were not bona fide trade acceptances because they “represented advancements made by the associations to the growers” and not irrevocable payments—in essence, they were not “real bills.”Footnote 137 The Fed assumed that “practically the only use which the growers are likely to make of the proceeds of such drafts when discounted is to pay debts previously incurred by them in growing and harvesting the crop,” and as such constituted a financial, and not an agricultural, operation.Footnote 138 Nevertheless, the Board reasoned that by considering such drafts as it did government securities, it could still intervene. Indeed, the Fed could not buy government debt directly, but since WWI, it had discounted member banks’ promissory notes when collateralized by US government bonds. This measure allowed investors to obtain liquidity to meet their obligations—be they commercial or financial—while still “carrying” the securities. “Similarly,” the Fed opined, “money borrowed by a grower to enable him to meet his obligations without selling his crop immediately enables him to ‘carry’ the crop.” On this basis, the Fed announced that drafts drawn by a grower on his CMA “may properly be considered to be drawn for an agricultural purpose.” It went on to justify that decision by stating that “the carrying of … agricultural products for such periods as are reasonably necessary in order to accomplish the orderly marketing thereof is a legitimate and necessary step incidental to normal distribution.” Indeed, the Fed found it “hard to imagine how a grower could use the proceeds of a loan to finance the carrying of a crop except by using them to meet obligations or make necessary expenditures which would necessitate the immediate sale of his crop if he did not obtain a loan.”Footnote 139

The second policy innovation had to do with the eligibility of promissory notes issued by CMAs and discounted at a bank to raise funds for the purpose of making payments to growers delivering their produce. Once again, whether such notes were eligible depended on whether the transaction was considered an outright sale (a commercial operation) or a cash advance (a financial operation). The Fed recognized that farmers handing over produce to their Sapiro-plan CMAs gave the latter full control over the goods and the power to decide when to sell them. However, farmers only knew what price they would receive when the warehoused commodities were effectively sold, suggesting that they were consignments, not outright sales. To overcome this contradiction, the Fed argued that “there is no material difference between these transactions and ordinary sales except that the sellers, the growers, have the ultimate hope of gain and risk of loss resulting from resale by the purchaser, the association.” Because “this difference exists by reason of the relation that necessarily exists between the association and its members,” the Fed intimated “that to conclude that the transactions are not sales … would be in effect to say that it is impossible for the association and its members to engage in purchase and sale transactions between themselves.”Footnote 140 On the basis of this logic, the Fed deemed CMA notes as eligible commercial paper if they had less than 90 days until maturity.

The third policy change affected the eligibility of bankers’ acceptances. In an official communiqué, the Fed announced that it could now purchase in the open market “bankers’ acceptances with maturities up to six months which are drawn by growers or by cooperative marketing associations to finance the orderly marketing of non-perishable, readily marketable, staple agricultural products when secured by warehouse receipts.” An additional change expected to be of “material assistance” to CMAs made the acceptances they drew on banks under acceptance credits eligible at the discount window. Although only bankers’ acceptances with up to 90 days until maturity had heretofore been eligible, “the new amendment…permits them to be purchased with maturities up to six months.” At the same time, the Fed eliminated the existing statutory limits on the amount of paper issued by any one borrower that Reserve banks could buy, a decision that “should be very beneficial to the farmers and their associations because it permits the rediscount of such paper in unlimited amounts.” According to the Fed, these changes signaled its desire to be “as liberal as possible under the terms of existing law” and reflected the fact that it was “greatly interested in the cooperative marketing movement and has sought every opportunity to assist the organizers and managers of such associations to work out the best means of arranging their financing so that it should not only be sound but should also enable them to obtain the lowest interest rates for necessary credit.”Footnote 141

These rulings on CMAs’ commercial paper eligibility aligned with the “aggressive policy action” that the Fed had pursued since 1917 to stimulate the supply of trade finance instruments essential for establishing a new money market.Footnote 142 They also resonated with growing calls—from well beyond the farming community—to support CMAs for the greater economic and financial good. This new liquidity backstop for agricultural trade debt was good news for CMAs. However, the Fed’s policies targeted “non-stock, non-profit corporation[s] composed exclusively of growers of the particular crop which the association was organized to market”—in other words, Sapiro’s centralized, top-down cooperatives—so they were not neutral. Creating a national market for intermediate-term farm debt could, in theory, free farmer cooperatives from their reliance on local bankers and merchants for the working capital they needed to operate as viable business enterprises.Footnote 143 Yet, as the final section shows, prevailing norms of good financial practice meant even a bespoke system of federal intermediate credit banks was insufficient to shake off the “crop-lien crown of thorns” that farmers still bore despite the Fed’s foundation, because it focused narrowly on trade finance rather than working capital in a broader sense.

Federal Intermediate Credit and Its Limits

CMAs had a powerful ally in the Fed, but debates persisted over whether a specialized institution was necessary to address their intermediate credit needs. Meyer himself opposed making the WFC permanent, arguing that only livestock producers required specialized credit machinery owing to their 1–3-year production cycle. Instead, he contended, the Fed-backed monetary system should be “Americanized.” Bankers had long discounted promissory notes on the basis of the general creditworthiness of their maker, making no distinction between short- and intermediate-term paper.Footnote 144 While the Fed’s focus on short-term paper had been imported from Europe where manufacturing dominated, the “basic business of America [remained] the production and distribution of agricultural commodities” so longer credit periods had to be accommodated. In fact, Meyer claimed that the Fed’s distinction between “good” and “bad” paper was arbitrary and challenged the notion that short-term paper was inherently more liquid than intermediate-term paper if secured by staple commodities (as the Depression of 1920–1921 had shown, even short-term commercial paper became illiquid during market disruption). Thus, agriculture should not settle for a “second-class rediscount facility” since it was entitled to the “best banking rediscount facility in the United States, and that facility is the Federal Reserve System.” As Meyer argued, “the full strength of the System should be made available for agricultural financing, as it now is for commercial and industrial financing.” Adjusting credit policy was essential to create “the elasticity that is needed to meet the changing conditions of our modern complex economic world.”Footnote 145

Congressional debates in 1923 about how best to ensure access to intermediate credit reveal agrarians’ preference for bespoke credit machinery. This was owing to fears that banks might still refuse to discount CMAs’ commercial paper. Some country bankers reportedly made vague invocations of the “real bills” doctrine to justify refusing CMA credit requests while others told CMAs that the Fed had explicitly told them to invest solely in short-term commercial paper. Others doubted the Fed’s commitment to farmers’ needs. As North Carolina Democratic Senator Furnifold McLendel Simmons noted: “Farmers do not want the board that they deal with to be subject to the temptation of directing their policy more in the interest of some other business than that of the farmers.”Footnote 146

Among a flurry of legislative proposals, two key bills stood out: the Capper–McFadden bill and the Lenroot–Anderson bill. The former—written with the help of Eugene Meyer—proposed extending Fed eligibility to agricultural paper with maturities up to 9 months, recognizing CMA commercial paper as agricultural paper per se, and loosening minimum capital requirements to encourage small country banks to join the Fed.Footnote 147 It would also create national agricultural credit corporations empowered to discount agricultural paper which would, in turn, rediscount this paper at “rediscount corporations” capitalized through public securities issues.Footnote 148 This approach, which focused on using a liberalized Fed backstop to accommodate agriculture within the existing banking system using minimal state intervention and was therefore “essentially a conservative one,” was backed by Sapiro and the centralized CMA movement as well as the livestock sector.Footnote 149 The latter bill, meanwhile, drew directly from the JCAI’s final report and was “based on the assumption that [the existing] banking system could not be changed to meet the credit requirements of agriculture without destroying its commercial nature.”Footnote 150 Rather than relying on the Fed, it suggested creating 12 government-based intermediate credit banks that would provide below-market interest rates on loans with extended maturities. This bill, which called for the creation of a parallel state-backed banking system for agriculture, received the support of Midwestern farmers and farmers’ associations such as the American Farm Bureau Federation, National Grange and the Farmers’ Union.Footnote 151 In January 1923, the Senate passed both bills, but in early March the House passed a composite of three different bills. After persistent disagreement, a Senate–House conference committee opted to replicate the parallel private–public model of the Federal Land Banks.Footnote 152 And on March 3rd, Congress passed the Agricultural Credits Act of 1923 (ACA).

The ACA created a secondary discount system composed of 12 Federal Intermediate Credit Banks (FICBs) overseen by the Federal Farm Loan Board. They covered the same geographical subdivisions as the Federal Land Banks, whose directors became ex officio board members of the new banks (six out of each bank’s nine directors were chosen by the borrowers themselves).Footnote 153 FICBs could discount agricultural paper from national and state banks, trust companies, cooperative agricultural credit corporations, CMAs, and other FICBs. Paper with maturities between 6 months and 3 years was eligible when secured by standardized warehouse receipts, shipping documents, or chattel mortgages, and loans could not exceed 75% of the underlying commodity’s market value. FICBs were capitalized with $5 million from the Treasury and could sell tax-exempt debentures up to 10 times their paid-in capital and surplus. However, in addition to the FICBs, the ACA also facilitated farmers’ access to the country’s primary discount system by loosening Fed eligibility rules, as Meyer had suggested.Footnote 154 Indeed, it authorized the Fed to discount agricultural paper with maturities of up to 9 months and issue Federal Reserve notes on this basis, rediscount agricultural bills held by FICBs, and buy and sell FICB debentures in the open market. It also relaxed capital requirements for prospective Fed members to coax more banks into joining the system in the hope that discount window access would make them more partial to buying CMA paper.

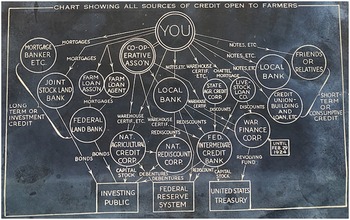

By early 1923, farmers had access to a comprehensive network of private and federal government-backed financial institutions that together addressed their long-term, short-term, and intermediate credit needs (Fig. 2). However, it’s worth examining whether the changes introduced since the 1890s satisfied the early calls of financial reformers for an elastic currency capable of reducing financial instability, and those of Southern farmers for the means to control production and distribution and eliminate the crop-lien system.

Private and public sources of farm credit, 1923.

(Source: “Viewpoints,” [Farm and Fireside?], May 1923, box 6, entry 105, RG 83, NACP.)

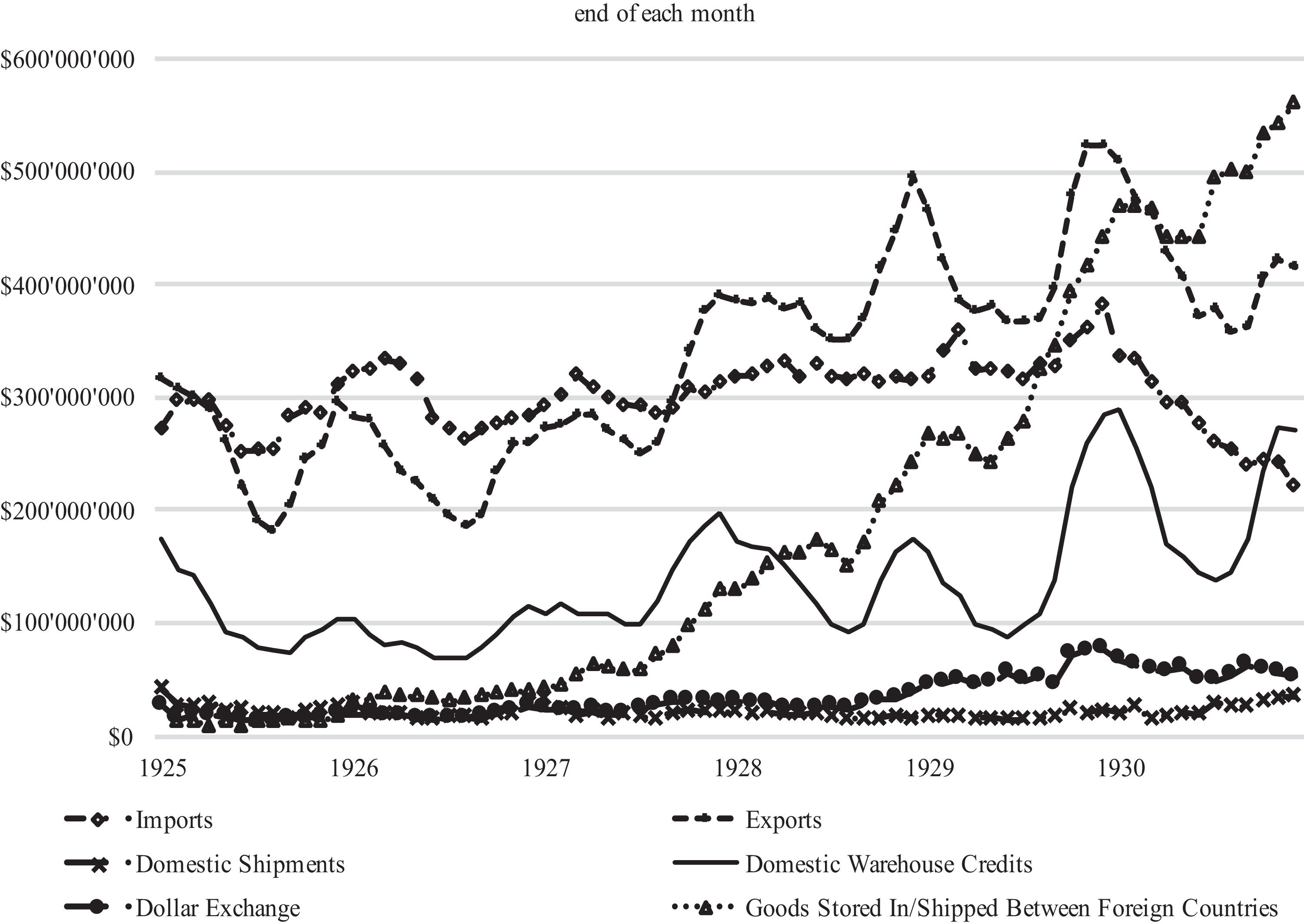

As previously explained, financial reformers viewed the creation of a new money market based on commercial paper as crucial to neutralizing agriculture’s destabilizing effects on the financial system. Bolstered by the Fed’s low discount rates in the decade following WWI, the US acceptance market competed on a par with London as the primary international money market, facilitating the dollar’s rise as an international currency.Footnote 155 Staple agricultural commodities—and cotton in particular—underpinned that success, generating the majority of acceptances in the market.Footnote 156 Figures from earlier years are lacking; however, from 1925 to 1929, cotton was the single largest commodity collateralizing bankers’ acceptances representing goods shipped and warehoused domestically—on average it constituted 36–50% of the total, followed by grain (13%) and tobacco (7%). Cotton generated an even higher proportion of acceptances resulting from exports, representing 55–68% of the total. The highly seasonal fluctuations in acceptances generated from domestic and foreign warehousing and exports reflect the importance of raw materials on the market’s supply side and exemplify the monetary elasticity for which financial reformers had advocated (Fig. 3).

Classification of US bankers’ acceptances outstanding, 1925–1930.

(Source: American Acceptance Council, Facts and Figures Relating to the American Money Market, 1931, 42–3, JAJM A51 1931, BLSC.)

It is difficult to ascertain the acceptance market’s significance for cotton CMAs relative to other financing methods. Nevertheless, in 1924 the American Acceptance Council asserted that acceptances were enabling Southern country banks “to make a more complete use of their credit and give them credit instruments which have a wide market and thereby enable a larger supply of capital to be reached.” Although small-scale distributors still mainly used promissory notes, large-scale cotton CMAs had reportedly come “[to rely] principally on bankers’ acceptances as a means of raising funds.”Footnote 157 In 1928, the Council noted that the acceptance market was relieving credit conditions in local cotton markets because country banks that reached their lending limit could solicit “other banks in sections far removed from the crop belt [that] stand ready to accept against warehouse receipts covering cotton awaiting shipment.”Footnote 158 A Federal Trade Commission report that year also noted that cotton CMAs used bankers’ acceptances “to a considerable extent.”Footnote 159 When Senator Carter Glass sought to limit the Fed’s involvement in domestic bankers’ acceptances owing to alleged abuses, the Fed’s vice governor warned that doing so “would destroy what is supposed to be one of the bulwarks of the cooperative marketing system.” Despite acknowledging that some CMAs had been “tempted to overstay the market because of the low rate of financing provided by acceptances,” the official insisted that there was no evidence of abuse.Footnote 160 Still, because bankers’ acceptances had to be based on existing collateral, they offered a means of financing commodity distribution but not production, so they did not allow cotton CMAs to coordinate both phases and effectively escape the crop-lien system.

What of the FICBs and their ability to give farmers agency over both the production and distribution of their crops? By 1929, the FICBs had a lending potential of $660 million and provided a total of $1.125 billion in loans between 1923 and 1930, offering CMAs a “practically unlimited source of commodity credit.”Footnote 161 In 1926, 32% of these loans were based on cotton and, by the end of 1928, two-thirds of the outstanding loans benefitted cotton CMAs.Footnote 162 But this was not enough to escape the crop lien. Because CMAs customarily only advanced up to 65% of the value of the cotton delivered to them, payments were insufficient to allow producers to reimburse local creditors and release the mortgage on the crop.Footnote 163 And although growers could in theory assign the proceeds of cotton sold through a CMA to the mortgage holder, even if the latter were to give his permission, this meant paying interest to the lien holder for a longer period.Footnote 164

Senate hearings before the ACA’s passage reveal that production credit had in fact been a major concern. Experts such as farm loan commissioner Charles E. Lobdell warned against conflating marketing and production credits. While the former were impersonal loans secured by warehouse receipts representing fungible commodities, the latter provided no “tangible basis” for credit. Aaron Sapiro agreed, noting that production credits were necessarily “localized in character” because they depended on the “character” of tenant farmers, the nature and location of the commodity in question, and “the color of the tenancy, which is important.”Footnote 165 Former assistant Treasury Secretary Russel C. Leffingwell concurred, stating that rural credits were “complicated by matters of history and matters of politics which are a little bit outside the strictly economic problem” and claiming that bankers could only safely lend if borrowers possessed a margin of equity in mortgaged land or capital goods—or, alternatively, an unimpeachable personal reputation. While landowners and merchants could safely lend to tenants and sharecroppers thanks to insider knowledge, distant banks and government agencies could not and should not because making credit too accessible would exacerbate overproduction. Furthermore, Sapiro also cautioned that “if the collateral for marketing credit [was] mixed up with production credit, it [would] reduce the salability and value of the bonds that are sold against such combined credits.” Despite acknowledging cotton growers’ production credit challenges, he therefore believed it would be best for each state to “pass the proper legislation depending on its local conditions and its type of commodities” to address them.Footnote 166

But were credit cooperatives up to the task of addressing production credit needs? Following the ACA’s passage, only one national agricultural credit corporation was organized, and no rediscount corporation was created, so state-level agricultural credit corporations (ACCs) had to pick up the slack. They made “considerable progress across the South,” usually as incorporated subsidiaries of non-stock CMAs.Footnote 167 And according to the Department of Agriculture, “by far the largest” class of their loans consisted of intermediate production loans for fertilizer, seeds, livestock, and tools, or advances to tenants for living expenses. In theory, therefore, ACCs could “provide [CMA] members with enough bargaining power to obtain permission from their creditors to market their cotton through the cooperative,” but in practice they fell short. They faced high fixed costs, management inefficiencies, and legal limits on the interest they could charge, and struggled to manage the risk resulting from their narrow focus on a single, highly seasonal, climate-sensitive crop. These challenges resulted in limited earnings and an inability to accumulate reserves, leaving them vulnerable to shifts in world markets. And, crucially, they could not cover the FICB’s 35% lending margin shortfall needed to reimburse crop-lien holders. Attempts to close this gap with supplementary loans on pooled cotton failed as these loans were ineligible for rediscount at the FICBs. As a result, ACCs financed less than a quarter of the cotton delivered to CMAs in the 1920s.Footnote 168

Despite major changes to the financial and monetary architecture since the 1890s, many cotton growers remained trapped by the crop-lien system. In 1926, Aaron Sapiro estimated that 80% of cotton was still grown under the system and reported that “little local bankers [were still stopping farmers] from joining cooperatives either for their own profit or for the profit of local buyers who are friends of bankers.”Footnote 169 As the Dallas Fed Governor noted, the South’s dire situation that year highlighted the enduring limitations of the credit system: