1. Foreword by the Diabetes Steering Group on behalf of the Institute and Faculty of Actuaries

The Diabetes Steering Group (DSG), on behalf of the Institute and Faculty of Actuaries (IFoA), are delighted to introduce this paper, which, to our knowledge, is the first study that provides a comprehensive analysis of various mortality risk factors for individuals diagnosed with both Type 1 and Type 2 diabetes (Reid et al., Reference Reid, Oliver, Bagnall, Catchpole, Chadwick, Lambert, Li, Schneider, Tajapra, Yan and Zhou2023). This paper includes a model that provides the user with a mortality risk prediction for individuals living with and without diabetes.

This research is considered important to the primary audience, the UK insurance industry, as it furthers the DSG’s key research aim as set out in our initial paper (Reid et al., Reference Reid, Oliver, Bagnall, Catchpole, Chadwick, Lambert, Li, Schneider, Tajapra, Yan and Zhou2023); that is, to widen access to insurance products for customers living with diabetes by improving the insurance industry’s access to information on the specific mortality risk for those living with diabetes. The primary intended audience for this research is the actuarial community and insurance industry, specifically those insurers and reinsurers that write protection and longevity risk products in the UK. However, the IFoA has a Royal Charter under which the DSG also seeks to provide information for the wider public interest.

The Diabetes Working Party produced a sessional paper (Reid et al., Reference Reid, Oliver, Bagnall, Catchpole, Chadwick, Lambert, Li, Schneider, Tajapra, Yan and Zhou2023), published on 18th May 2023, which provided insights to diabetes mortality risk via a comprehensive literature review and a global underwriting survey. Following this, the working party sought to further the research aim by commissioning a research project. That research project is detailed herein and was commissioned by the IFoA Actuarial Research Centre (ARC) and a group of industry participants, specifically Pacific Life Re, Partner Re, Swiss Re, Legal & General and Zurich Insurance Group. The research was carried out by world-leading experts in risk analysis, risk modelling and risk evaluation at the University of Leicester, namely Dr Bogdan GrechukFootnote 1 , Dr Evgeny Mirkes and Prof Alexander Gorban. These academic researchers are supported by the Real World Evidence Centre and the Leicester Diabetes Centre, a unique, collaborative partnership between the NHS and the University of Leicester.

Individuals with diabetes, both Type 1 and Type 2, run a greater risk of developing one or more severe health complications, including cardiovascular and cerebrovascular disease. Diabetes is also a leading cause of blindness in working-aged individuals and a common cause of kidney failure. Life expectancy following a diagnosis of diabetes has historically been lower than in those without diabetes, given that inadequate glycaemic control gives rise to several complications that cause premature death, along with increased risks of long-term disability.

In recent years, early detection and management of diabetes, both from a personal as well as a physician-led perspective, has improved such that survival with diabetes has increased. New pharmaceuticals, coupled with enhanced monitoring and modern insulin dosage systems, have transformed the lives of individuals living with diabetes. Life expectancy with optimal glycaemic management has been extended in those with diabetes, but the long-term impact of new pharmaceuticals has yet to be fully appreciated.

The overarching aim of the research project is to develop a deeper understanding of the mortality risk associated with a diagnosis of Type 1 and Type 2 diabetes and the impact of recent improved medical treatments. More specifically, the DSG’s objectives are to:

-

• Gain insights from recent data by considering advanced data analytic techniques to understand relative mortality risk factors and interactions.

-

• Produce a model that can predict mortality across a wide age range at a granular level for lives living with and without both Type 1 and Type 2 diabetes. The model should include co-morbidities such that the impact on mortality of living with and without diabetes in the presence of a wide range of co-morbidities can be understood.

The work carried out by the University of Leicester is detailed within this paper: background on the data sources used, for example, Clinical Practice Research Datalink (CPRD) and linked data; the process of data ingestion and cleaning; the data analysis; and the fitting of a Cox proportional hazards model. The DSG sought a transparent model where inferences can be drawn, and therefore a regression model was selected, namely the Cox proportional hazards model. The DSG built an accompanying Shiny applicationFootnote 2 so that the insurance industry and any interested wider stakeholders, for example, Diabetes associations and general practitioners (GPs), can interact with the model output.

The DSG is satisfied that the research outputs have been carried out to a high quality and in line with expectations to produce findings that are relevant to the primary intended audience (e.g., the actuarial community and insurance industry).

The interactive Shiny application will enable the user to consider the impact of different attributes on a general sample population, as well as a population of diabetes Type 1 and Type 2. The DSG would like to draw the reader’s attention to the benefits and limitations in Section 6.6 and to advise that care be exercised when interpreting results and utilising the Shiny application. Section 7 includes a general industry discussion followed by an applied industry discussion. The modelling was appreciated in the general discussion but there are many complications such as the quality of the data and how to handle co-morbidities correctly. Building a general model that covers Type 1 and Type 2 for all the different co-morbidities was ambitious and we understand this is the first time that has been done. The general feedback was that creating a model based on CPRD data was worthwhile as an initial approach that can be improved in future based on the feedback from practitioners.

1.1 Data Used

This study is based in part on data from the CPRD obtained under licence from the UK Medicines and Healthcare products Regulatory Agency. The data is provided by patients and collected by the NHS as part of their care and support. The interpretation and conclusions contained in this study are those of the author(s) alone.Footnote 3 We also used linked Hospital Episode Statistics (HES) data and Office for National Statistics (ONS) mortality data.

2. Introduction

2.1 Background

Both Type 1 and Type 2 diabetes are serious diseases and there has been a dramatic increase in prevalence over the last few decades. The number of worldwide cases has quadrupled between 1980 and 2014 (NCD Risk Factor Collaboration (NCD-RisC), 2016) and has increased for both Type 1 and Type 2 diabetes (Patterson et al., Reference Patterson, Karuranga, Salpea, Saeedi, Dahlquist, Soltesz and Ogle2019). More than half a billion individuals are living with diabetes worldwide as of 2021, and this number is predicted to grow to 1.3 billion in the year 2050 (GBD 2021 Diabetes Collaborators, 2023). Over 300 million individuals have prediabetes (International Diabetes Federation, 2015) and it is estimated that almost half of all individuals (

$49.7{\rm{\% }}$

) living with diabetes are undiagnosed (Cho et al., Reference Cho, Shaw, Karuranga, Huang, da Rocha Fernandes, Ohlrogge and Malanda2018).

$49.7{\rm{\% }}$

) living with diabetes are undiagnosed (Cho et al., Reference Cho, Shaw, Karuranga, Huang, da Rocha Fernandes, Ohlrogge and Malanda2018).

In the UK, the number of individuals living with diabetes in all its forms is approaching 5 million, and this number is predicted to rise to 5.5 million by 2030 (Cho et al., Reference Cho, Shaw, Karuranga, Huang, da Rocha Fernandes, Ohlrogge and Malanda2018). The expected lifetime of an individual with diabetes is significantly lower than for non-diabetic individuals of similar age and other conditions (Bertoni et al., Reference Bertoni, Krop, Anderson and Brancati2002; Tancredi et al., Reference Tancredi, Rosengren, Svensson, Kosiborod, Pivodic, Gudbjörnsdottir, Wedel, Clements, Dahlqvist and Lind2015). The analysis of diabetes-related mortality is complicated by the fact that individuals rarely die from diabetes directly. Instead, individuals with diabetes have increased risk of death from other diseases (DeFronzo, Reference DeFronzo2009). In the last decade, significant advances in medical treatments for Type 1 (Boscari & Avogaro, Reference Boscari and Avogaro2021) and Type 2 (Chee & Dalan, Reference Chee and Dalan2024) diabetes seem to have reduced the mortality risk for many individuals. However, the effect of these treatments on mortality risk is not yet fully understood. Studies to date that provide information on mortality risk for individuals with diabetes are derived from data ten or more years old that do not reflect those more recent treatments.

2.2 Overview of this Research Project

This research project develops models for mortality prediction for individuals with Type 1 and Type 2 diabetes. These models are based on recent data (namely the years 2010–2019) and as such include the impact of recent treatments. The model output is mortality predictions for an individual based on risk factors including age, gender, body mass index (BMI), blood pressure (BP), cholesterol level (CL), smoking status, index of multiple deprivation (IMD), blood glucose (sugar) level (HbA1c), duration since diabetes diagnosis and existence of various co-morbidities. With this information on each risk factor as an input, the models provide an output of a probability of death for the individual within the next t years for any given

$t \gt 0$

. To compute this probability, the models allow for the effect of the risk factors, listed above, both separately and for some of the factors in combination. For example, coronary heart disease significantly increases the mortality risk for all individuals with diabetes, but the increase is particularly strong for individuals with high BMI.

$t \gt 0$

. To compute this probability, the models allow for the effect of the risk factors, listed above, both separately and for some of the factors in combination. For example, coronary heart disease significantly increases the mortality risk for all individuals with diabetes, but the increase is particularly strong for individuals with high BMI.

It is important to note that this analysis does not attempt to draw causal epidemiological conclusions. Instead, it seeks to pinpoint risk factors that are reliably correlated with mortality in the diabetic population. Such an approach reflects the requirements of underwriting practice, which relies on consistent and interpretable risk differentiators to support equitable, evidence-driven decisions.

The analysis of data in this research project, alongside the existing literature (Huxley et al., Reference Huxley, Peters, Mishra and Woodward2015; Kautzky-Willer et al., Reference Kautzky-Willer, Leutner and Harreiter2023) reveals many risk factors that correlate with mortality differently depending on whether the diagnosis is of Type 1 or Type 2 diabetes, and with gender. Therefore, separate mortality models were developed by gender for (i) the general population, (ii) individuals living with Type 1 diabetes and (iii) individuals living with Type 2 diabetes. There are therefore six models produced in total.

All of the models are Cox proportional hazards models (Cox, Reference Cox1972). A major advantage of this model is that the computed Cox coefficients explicitly show the effect of each factor on the mortality risk. The primary audience, the insurance industry, is required by regulation to have transparency in pricing terms and as such a transparent model where inferences can be drawn was preferred.

These models can be used to inform the insurance industry on the specific mortality risk posed by individuals with diabetes with the aim of achieving availability of insurance products for those living with diabetes and also more appropriate pricing and reserving for life and health insurance products. These models provide a better understanding of the mortality risk factors for individuals with diabetes which may also be of interest to wider stakeholders.

2.3 Comparison with the Existing Literature

The literature on diabetes is very rich. However, many studies investigate the effect of only one or at most several risk factors. Indeed, each risk factor considered herein can be found in the existing research as it affects the prevalence of diabetes or the associated health outcomes including: age (de Miguel-Yanes et al., Reference de Miguel-Yanes, Shrader, Pencina, Fox, Manning, Grant, Dupuis, Florez, D’Agostino, Cupples and Meigs2011; Constantino et al., Reference Constantino, Molyneaux, Limacher-Gisler, Al-Saeed, Luo, Wu, Twigg, Yue and Wong2013), gender (Ohkuma et al., Reference Ohkuma, Komorita, Peters and Woodward2019; Mauvais-Jarvis, Reference Mauvais-Jarvis2018), ethnicity (Goff, Reference Goff2019), physical activity (Wahid et al., Reference Wahid, Manek, Nichols, Kelly, Foster, Webster, Kaur, Friedemann Smith, Wilkins, Rayner, Roberts and Scarborough2016), BMI (Chatterjee et al., Reference Chatterjee, Khunti and Davies2017), alcohol consumption (Baliunas et al., Reference Baliunas, Taylor, Irving, Roerecke, Patra, Mohapatra and Rehm2009), socio-economic status (SES) (Evans et al., Reference Evans, Newton, Ruta, MacDonald and Morris2000) and co-morbidities such as cardiovascular disease (Leung et al., Reference Leung, Eurich, Lamb, Majumdar, Johnson, Blackburn and McAlister2009; Wilmot et al., Reference Wilmot, Edwardson, Achana, Davies, Gorely, Gray, Khunti, Yates and Biddle2012; Riley & Cowan, Reference Riley and Cowan2014; Stamler et al., Reference Stamler, Vaccaro, Neaton and Wentworth1993), heart failure (Ohkuma et al., Reference Ohkuma, Komorita, Peters and Woodward2019), coronary heart disease (Peters et al., Reference Peters, Huxley and Woodward2014), stroke (Emerging Risk Factors Collaboration, 2010), hypoglycaemia (Elwen et al., Reference Elwen, Huskinson, Clapham, Bottomley, Heller, James, Abbas, Baxter and Ajjan2015), high BP (Chiriacò et al., Reference Chiriacò, Pateras, Virdis, Charakida, Kyriakopoulou, Nannipieri, Emdin, Tsioufis, Taddei, Masi and Georgiopoulos2019), depression (Ali et al., Reference Ali, Stone, Peters, Davies and Khunti2006), dementia (Bello-Chavolla et al., Reference Bello-Chavolla, Antonio-Villa, Vargas-Vázquez, Ávila-Funes and Aguilar-Salinas2019), fatty liver disease (Song et al., Reference Song, Jia, Li, Wang, Ren and Chen2021) and Covid-19 (Hussain et al., Reference Hussain, Bhowmik and do Vale Moreira2020; Pal & Bhadada, Reference Pal and Bhadada2020) (non-exhaustive list).

In contrast, this project builds a model that allows for many risk factors, separately and, for some of the factors, in combination. Such studies are far less common in literature. Jensen et al. (Reference Jensen, Moseley, Oprea, Ellesøe, Eriksson, Schmock, Jensen, Jensen and Brunak2014) developed a clustering methodology that can be used to identify new risk factors related to diabetes. Golovenkin et al. (Reference Golovenkin, Bac, Chervov, Mirkes, Orlova, Barillot, Gorban and Zinovyev2020) studied a selection of more than 100,000 hospitalisation cases with individuals suffering from diabetes characterised by 55 attributes. The outcome of interest was hospital readmission, rather than mortality.

To the best of our knowledge, none of the existing recent literature provides a comprehensive analysis of the impact of various risk factors on the mortality of individuals living with diabetes. In addition, the literature does not provide a general model for mortality prediction for individuals with and without diabetes based on a large variety of risk factors. Herein, this is the focus of this research.

3. Data Structure

3.1 Data Collection

This research requires information regarding the outcome of interest - death. It also requires information regarding possible risk factors for that outcome of interest, such as diabetes diagnosis type and date, age, gender, etc. The first was sourced using the ONS Death Registration Data, which enables a status of alive or deceased to be mapped to an anonymised individual record, and, in the latter case, the date of death. The second was sourced using the CPRD database (Herrett et al., Reference Herrett, Gallagher, Bhaskaran, Forbes, Mathur, Van Staa and Smeeth2015), which contains anonymised individual data records from a network of general practices (GP) across the UK. In addition, information from the HES database was utilised to gain further information on co-morbidity diagnosis from the National Health Service (NHS) hospitals’ admissions and outpatient appointments data. Deprivation is considered a significant risk factor for mortality (Evans et al., Reference Evans, Newton, Ruta, MacDonald and Morris2000). To allow for this, an IMD score was mapped at a GP and at an individual level.

These data sets and the linkage of these data sets were necessary to enable the influence of various risk factors on the mortality of those living with diabetes to be understood. Samples of the full database were taken over a restricted time and geographical scope in order to work with the least amount of data to achieve the research aim. This approach aligns with the principle of data minimisation, ensuring that only the minimum amount of data necessary to adequately address the research question was used, thereby reducing computational burden and safeguarding data privacy. These data sets are fully anonymised, intended for use by researchers and their use in this project was approved by CPRD in 2021.

The time period for this research spans from 1 January 2010 (the “study start date”) to 31 December 2019 (the “study end date”). This was the most recent 10-year period that was not impacted by the Covid-19 pandemic. Although some of the data sets are UK wide, the HES data is restricted to England and as such, the geographical scope of the research was narrowed to England as this linkage was necessary to understand the influence of co-morbidities on the mortality of diabetes patients. Data from the private healthcare system is not included; this is not considered material because the vast majority of diabetes care and associated hospital admissions in England occur within the NHS, making NHS HES a comprehensive and representative source for the population under study.

The following samples were requested from the CPRD database:

-

• A diabetes sample: anonymised individual records from the database who have at least one record related to diabetes (Type 1 or Type 2), were alive at the study start date and were at least 18 years of age by that date (i.e., a year of birth is 1991 or earlier). This sample resulted in 621,115 individual records. Given that approximately 4 million adults in England were living with diabetes (diagnosed and undiagnosed) in 2019, about 15% of them were included in this sample.

-

• A general sample: a random sample of 250,000 anonymised individual records, regardless of diabetes status (i.e., general) who were alive and were at least 18 years of age at the study start date. This sample is about

$0.5{\rm{\% }}$

of the relevant population.

$0.5{\rm{\% }}$

of the relevant population. -

• An additional sample: a random sample of 25,000 anonymised individual records, regardless of diabetes status, with any of the following diseases: heart failure, coronary heart disease, angina, heart attack, stroke, amputation, macrovascular disease, asthma, atrial fibrillation, cancer, chronic kidney disease (CKD), chronic obstructive pulmonary disease (COPD), dementia and epilepsy.

These samples are not mutually exclusive and as such, some records appear in several samples. In total,

$1,205,657$

unique records were selected across the three samples. This is referred to herein as the “total data set”.

$1,205,657$

unique records were selected across the three samples. This is referred to herein as the “total data set”.

For each individual record in the total data set, the following were sought:

-

• The entire medical record available in CPRD.

-

• The HES data for that record linked.

-

• The ONS Death registration data for that record linked.

-

• The IMD mapped at an individual and GP level.

3.2 CPRD Data

The CPRD data arrived in the following tables: Patients, Practice, Staff, Consultation, Clinical, Additional Clinical Details, Referral, Immunisation, Test and Therapy (9 tables in total referred to herein as the “main tables”), plus additional tables without necessary information (referred to herein as “ignored tables”). The list of ignored tables is presented in Table 12.

Each table has its own set of columns of various lengths. The first column is Patient Identifier (“patid”), which is an encrypted unique identifier given to an individual record in the CPRD data set. All tables and figures can be found in the separate “Tables and Figures” document. Table 1 provides a list of columns and their description. The field patid is used to find records in all tables that correspond to a given individual record. Other forms of linkage are provided. Tables 1–10 describe all columns in the main tables, together with all forms of linkage. For convenience, links between fields are also summarised in Table 11 and Figure 1.

There are also two additional dictionary tables, “Medical dictionary” and “Product dictionary”. The diseases in CPRD tables are encoded using Read version (v) 2 codes also known as “Medcodes”, for example, Heart failure has Medcode “G58.00”. A list of Medcodes with descriptions of the corresponding medical terms is presented in the Table “Medical dictionary” and products (e.g., prescribed drugs) are encoded using “prodcodes”. Table “Product dictionary” lists all such drugs and their descriptions. Refer to Tables 13 and 14 for column descriptions in the dictionary tables.

3.3 Data from Linked Sources

The linked data from HES are organised into 11 tables: patients, hospitalisations, episodes, diagnoses by episode, diagnoses by hospitalisation, primary diagnoses across a hospitalisation, procedures, augmented care periods, critical care, maternity and health resource group. See Tables 15–25 for the descriptions of all table columns. For this research, only the first 6 tables were necessary as these contain information about diagnoses. All tables contain the column “patid” to assist in linkage. Individual patients may contribute data to more than one GP practice. In this case, multiple patid’s may represent the same individual. However, a column “gen hesid” within the table “Patients” in the HES data provides a CPRD generated unique key which allows information in CPRD tables and in HES tables to be identified where it refers to the same individual. Within the total data set, there were 15,107 cases that had multiple patid’s.

The information about diagnosis in HES is recorded using the International Classification of Diseases version 10 (ICD-10) coding frame. This differs from the CPRD’s medcodes, for example, Heart failure has Medcode “G58.00” while the corresponding ICD-10 code is “I50.9”. For this reason, a mapping between ICD-10 codes and medcodes was required (NHS Digital, 2018).

The linked ONS Death registration data consists of only one table. It contains the required information of patid, date and cause of death. A full list of columns is shown in Table 26.

The IMD data consists of two files: one contains a dictionary to identify the GP county, and another the deprivation score at the individual and GP level. A description of the columns is shown in Table 27.

Not all individuals in the total data set are “eligible” for the linked data: HES, ONS and IMD. There is a text document linkage eligibility named “new patids.txt” that specifies which individuals are “eligible” for linked data. Individuals eligible for HES linked data have the attribute “hes e” equal to 1. Similarly, individuals eligible for ONS linking have “death e” equal to 1, while individuals eligible for IMD linking have “lsoa e” equal to 1.

4. Data Treatment and Missing Data Analysis

4.1 Information Required for Mortality Risk Analysis

The selection of variables for this study was informed by a combination of evidence from the academic literature (as discussed in Section 2) and established actuarial practice within the insurance industry. Many of the included factors, such as age, gender, smoking status, BMI and indicators of co-morbid conditions, have consistently been associated with variations in mortality risk among individuals with diabetes. These are widely recognised both in clinical studies and in underwriting guidelines as relevant indicators of long-term health outcomes. Additionally, variables such as BP, CLs and HbA1c were included based on their routine use in risk stratification and premium setting by insurers, where actuarial judgement and historical claims experience inform expectations of mortality risk, even in the absence of strong causal evidence. As mentioned in Section 2.2, the objective of this analysis is not to establish epidemiological causation, but rather to identify variables that show meaningful correlations with mortality outcomes within the diabetes population. This distinction aligns with the practical needs of insurance underwriting, where the goal is to detect consistent, interpretable differentiators in mortality risk that can support fair and evidence-based decision-making.

The following data items are available across the linked data. The aim of data treatment was therefore to produce a data table, where each individual (patid) has the following information, which is appropriately cleaned and suitable for analysis:

-

• Outcome of interest:

-

• Individual’s status as alive or deceased as at study end date 31/12/2019.

-

• Date of death, where applicable.

-

-

• Mortality risk factors of interest:

-

• Static data items.

-

• Age at the start date.

-

• Gender.

-

• IMD.

-

• Smoking status.

-

-

-

• Regularly recorded data items.

-

• Body mass index (BMI).

-

• Blood pressure (BP).

-

• Cholesterol level (CL).

-

• Blood glucose (sugar) level (HbA1c).

-

• Indicator for diagnosed diseases which are considered “potentially significant” (see Table A). We emphasise that this is the original list of “potentially significant” diseases for the mortality of individuals with diabetes. This list was formed based on the literature review (Section 2) and consultations with specialists from Leicester Diabetes Research Centre. We do not claim that all these diseases are indeed significant. In fact, identification of a subset of significant diseases is a major part of this research project.

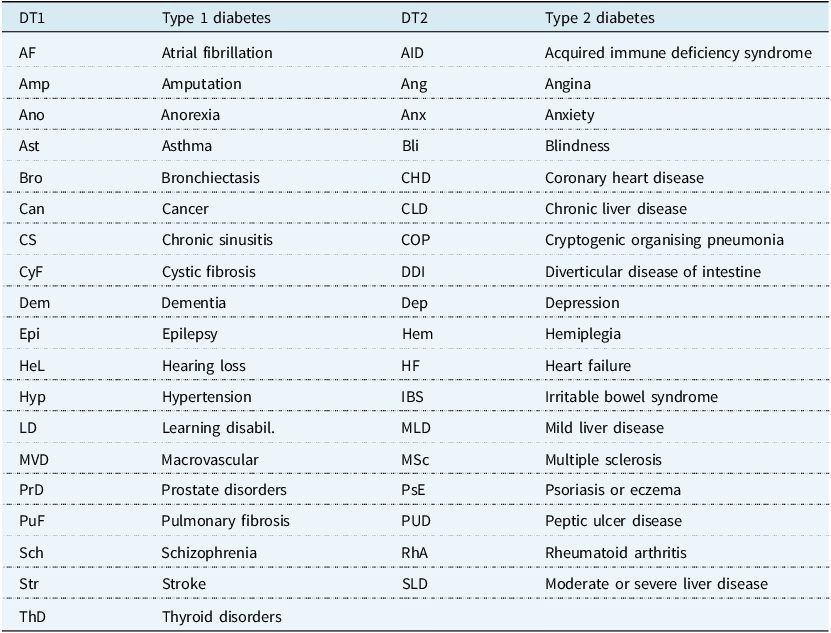

Table A.List of abbreviations used for medical conditions

Table A Long description

A table listing abbreviations for medical conditions related to Type 1 and Type 2 diabetes. The table has two columns: one for Type 1 diabetes abbreviations and one for Type 2 diabetes abbreviations. Each row lists a condition and its corresponding abbreviation. For Type 1 diabetes, conditions include atrial fibrillation (AF), amputation (Amp), anorexia (Ano), asthma (Ast), bronchiectasis (Bro), cancer (Can), chronic sinusitis (CS), cystic fibrosis (CyF), dementia (Dem), epilepsy (Epi), hearing loss (HeL), hypertension (Hyp), learning disabilities (LD), macrovascular disease (MVD), prostate disorders (PrD), pulmonary fibrosis (PuF), schizophrenia (Sch), stroke (Str), and thyroid disorders (ThD). For Type 2 diabetes, conditions include acquired immune deficiency syndrome (AID), angina (Ang), anxiety (Anx), blindness (Bli), coronary heart disease (CHD), chronic liver disease (CLD), cryptogenic organizing pneumonia (COP), diverticular disease of intestine (DDI), depression (Dep), hemiplegia (Hem), heart failure (HF), irritable bowel syndrome (IBS), mild liver disease (MLD), multiple sclerosis (MSc), psoriasis or eczema (PsE), peptic ulcer disease (PUD), rheumatoid arthritis (RhA), moderate or severe liver disease (SLD).

-

• Date of diagnosis, where applicable.

-

The following data items, although available across the linked data and considered potential risk factors of interest, were not included for analysis for the reasons shown below.

-

• Marital status – high level of missing data.

-

• Ethnicity – high level of missing data and not used by the UK insurance industry.

Sections 4.2 and 4.3 provide insights for each item of data used including commentary on missing data analysis where relevant and data treatment. Further commentary can be found alongside the relevant tables within the “Tables and Figures” document.

4.2 Data for Outcome of Interest

There are two potential sources of date of death: “deathdate” field in the original CPRD data and “ONSDeath” field in the linked ONS data. For some individuals there are discrepancies in these fields. Some individuals have different dates of death (see Table 46) and there are

$86,{\rm{\;}}825$

records with an ONS date of death without a “deathdate” in the CPRD data (this is 16% out of the total of

$86,{\rm{\;}}825$

records with an ONS date of death without a “deathdate” in the CPRD data (this is 16% out of the total of

$543,{\rm{\;}}668$

individuals in the total sample linked in ONS). The lack of any recorded activities (such as GP visits, hospitalisations, etc.) after the ONS date of death is considered adequate evidence that the ONS date of death is correct. Within the insurance industry, the ONS data is considered the “gold standard” for death records and this is supported in the literature (Gallagher et al., Reference Gallagher, Dedman, Padmanabhan, Leufkens and de Vries2019).

$543,{\rm{\;}}668$

individuals in the total sample linked in ONS). The lack of any recorded activities (such as GP visits, hospitalisations, etc.) after the ONS date of death is considered adequate evidence that the ONS date of death is correct. Within the insurance industry, the ONS data is considered the “gold standard” for death records and this is supported in the literature (Gallagher et al., Reference Gallagher, Dedman, Padmanabhan, Leufkens and de Vries2019).

All individuals who died before the study start date are removed. To ensure that individuals with deaths pre-dating the ONS death register’s creation in 1998 are not included within the study period, the CPRD date of death is used if it is before 1998. For deaths after 1998 the ONS death data is used.

The CPRD date of death is considered fit for the filtering purpose above but is not considered fit for the purpose of mortality analysis. Therefore, where a link between the ONS and CPRD data cannot be established, these cases are removed from the study. That is, only individuals with ONS linked data are used. Although, this reduces all sample sizes it is considered appropriate because the CPRD date of death information is considered to be unreliable for mortality analysis. In the diabetes sample, there were 621,115 individuals initially. A link can be established to the ONS for 283,057 (45%). Excluding those individuals who died before the study start date, the sample contains 242,461 individuals (85%). In the general sample, there were 250,000 individuals initially. A link can be established to the ONS for 103,597 (41%). Excluding those individuals who died before the study start date, the sample contains 95,786 individuals (92%). These data are summarised in Table B.

-

• The effect of excluding non-ONS linked individuals is compared between the initial sample (all individuals) and the linked sample (only individuals linked with ONS). Standard tests for statistical significance such as the Kolmogorov–Smirnov test (KS test) are not useful for large data sets.Footnote 4 Therefore, a manual threshold is introduced. A 1% difference in fractions for linked and non-linked subsamples is considered a sufficient effective size. The impact of filtering needs to be considered by the main variables of interest for mortality analysis including gender, age and co-morbidities.

-

• Table 47 shows the contingency of gender from the initial to the linked sample. Female individuals comprise

$47.8{\rm{\% }}$

of the initial sample and

$47.6{\rm{\% }}$

of the linked sample. The change in the composition of the samples, that is, the effect size is

$0.2{\rm{\% }}$

. Because this is less than 1%, it can be assumed that linking and gender are independent. -

• Figure 3 presents the contingency of age from the initial to the linked sample. The age distributions are similar and the mean age is

$59.79$

for the initial sample and

$60.82$

for the linked sample. The difference in mean age is nearly 1 year, which is considered negligible alongside the similar age distribution. -

• Table 48 presents a comparison of various diseases associated with the individuals in the initial and the linked sample. Most of the diseases (28 out of 41) show statistically significant differences in prevalence between the initial and the linked samples, indicating that linkage to the ONS is not independent of disease status for these conditions. This suggests that certain co-morbidities may affect the likelihood of successful linkage, potentially due to systematic differences in healthcare usage or death registration practices associated with specific conditions. As a result, this introduces the possibility of selection bias in analyses relying solely on the linked sample. While the effective sizes for many of these conditions remain modest, this dependency needs to be acknowledged in any inference about disease-related mortality risks to avoid over- or underestimating effects due to differential linkage rates.

Sample sizes before and after ONS linkage

Table B Long description

The table presents data on sample sizes before and after linkage to the Office for National Statistics (ONS) for diabetes and general samples. It consists of two rows and four columns. The columns are labeled Sample type, Initial individuals, Linked to ONS (percentage), and Alive at study start (percentage). The diabetes sample initially had 621,115 individuals, with 283,057 (45 percentage) linked to ONS, and 242,461 (85 percentage) alive at the study start. The general sample initially had 250,000 individuals, with 103,597 (41 percentage) linked to ONS, and 95,786 (92 percentage) alive at the study start. The table highlights the reduction in sample sizes due to the linkage process and the proportion of individuals alive at the study start.

A careful investigation of the database reveals the existence of some individuals of old age that are linked to ONS, have no death date records, but also have no recorded GP activity after the study start date. We suspect that these individuals are in fact deceased or emigrated and no longer residing within the UK,Footnote 5 and performed a more careful investigation.

Of the

$1,205,657$

records within the total sample:

$1,205,657$

records within the total sample:

-

• 53,045 records have an age at the study start date of at least 80.

-

• According to CPRD data, 33,079 were alive at the study start date.

-

• According to the ONS linked data, 8,566 of the above were linked to ONS and alive at the study end date.

-

• The overlapping cases from the above two data sets indicated as “alive” are 8,347.

For those 8,347 “alive” individuals, we then search for test dates and diagnosis dates, and we have discovered that

-

• 1,353 individuals have the last date of diagnosis before the study start date.

-

• 1,884 individuals have the last date of test before the study start date.

-

• In total, there are 1,251 individuals without any recorded GP activity after the study start date.

Table 49 shows the age distribution for the samples before and after removing those individuals. In particular, there are 5 individuals older than 120 with no death date records, and all 5 cases have no GP recorded activity after the study start date. It is unlikely that individuals alive at these ages are no longer interacting with the registered GP. It was considered likely that these individuals were deceased, but the death was not recorded. This may occur where an individual emigrated from the UK some time ago. On this basis, all records with an age greater or equal to 80 at the study start date, which do not have any GP recorded activity after the study start date, are removed from the analysis.

The removal of the above 1,251 individuals, who we call “fake” individuals, has a crucial effect on the research objective, especially in insurance context. While the proportion of these individuals in the entire database is negligible (1,251 out of

$1,205,657$

, which is about

$1,205,657$

, which is about

$0.1{\rm{\% }}$

), their proportion among 8,347 individuals of age 80+ linked to ONS is 15%. This percentage increases when we increase age threshold and reaches 100% for the individuals aged 110+. Therefore, if “fake” individuals were not excluded, they would lead to a severe underestimation of the mortality rate at old ages.

$0.1{\rm{\% }}$

), their proportion among 8,347 individuals of age 80+ linked to ONS is 15%. This percentage increases when we increase age threshold and reaches 100% for the individuals aged 110+. Therefore, if “fake” individuals were not excluded, they would lead to a severe underestimation of the mortality rate at old ages.

After removing these individuals, the number of individuals left in the total sample who are linked to ONS is 656,410. All the statistics for the total sample described below are based on this set of individuals.

4.3 Data for Mortality Risk Factors of Interest

The following data were processed as either static or regularly monitored.

4.3.1 Static Data Items

The following data items are considered static and therefore extracted from the data as at the study start date. Although some items may vary through the study period, such changes are not considered materially significant for the purposes of mortality modelling. For instance, occasional corrections to recorded date of birth or gender are rare and typically reflect data quality improvements rather than actual changes in the individual’s characteristics. In the context of this study, where the objective is to evaluate broad mortality risk patterns across a large population, treating these variables as fixed at the study start date simplifies the analysis without introducing meaningful bias. This assumption aligns with industry practice in insurance risk modelling, where underwriting is typically based on characteristics known at a specific point in time.

4.3.1.1 Age and Gender

Age is defined as the number of full years of age at the start of the study. It has been computed as 2009 minus the year of birth. In Cox proportional hazards model, we will also have a parameter t that represents time from the study start. The age at any moment can then be computed as

$A + t$

, where A is the age at the study start. Having A as a constant simplifies the analysis.

$A + t$

, where A is the age at the study start. Having A as a constant simplifies the analysis.

Gender is recorded as a binary value: 1 – for Male, 2 – for Female, as recorded at birth.

4.3.1.2 IMD

IMD takes an integer value from 1 to 10 and is computed based on the postcode recorded at the study start. For individual records, the data item “IMD decile” is missing for nearly 58% of the total sample and nearly 61% of the general sample. In these cases, the missing value is imputed with the IMD for the individual’s registered GP. The remaining missing values (291 cases – 171 of which have the IMD recorded as 0 and 120 for which it is recorded as NaN) are allocated a value 5, which is a middle value for the index.

We acknowledge that the proportion of missing individual-level IMD data is substantial and that GP catchment areas are geographically broader than individual postcodes. However, excluding these records would result in a loss of over half the study population, drastically reducing statistical power and likely introducing significant selection bias, as data missingness is rarely random. Consequently, we utilised the GP-level IMD as a pragmatic proxy, operating on the reasonable assumption that patients generally register with a GP practice in close proximity to their residence, thereby sharing similar socio-economic characteristics.

4.3.1.3 Smoking Status

Files Smoke_ent_*.txt contain information about smoker status (1 – Yes, 2 – No, 3 – Ex smoker). From Smoke_ent_*.txt we received

$12,511,090$

records. After removing records with value 0 “Data Not Entered” we have

$12,511,090$

records. After removing records with value 0 “Data Not Entered” we have

$12,509,309$

records. After removing duplicate records, we have

$12,509,309$

records. After removing duplicate records, we have

$11,068,831$

records.

$11,068,831$

records.

These files should be accompanied by Smoke_Clin_*.txt to identify dates. There were 10,714 records with missing event dates. These dates were substituted by system date, which is the date the record was made in the database.

In addition, files Smoke_Int_*.txt and Smoke_test_*.txt present smoking information using medcodes. ICD-10 codes and medcodes for smoker status are presented in Table 35. The total number of records from files Smoke_Int_*.txt, Smoke_test_*.txt and Smoke_diag.txt is 16,248. After removing all of records with medcodes unrelated to smoking status we have 4,107 records.

In the total data set we have 75,727 individuals, or

$6.7{\rm{\% }}$

, without smoker status recorded. In the general sample, this applies to 50,080 individuals, or

$6.7{\rm{\% }}$

, without smoker status recorded. In the general sample, this applies to 50,080 individuals, or

$21.6{\rm{\% }}$

. The results of the analysis of the randomness of missingness are presented in Table 36. They show that values are not missing completely at random. This means that we cannot remove records with missing values, and so we should impute the data. The imputation method we used was to set the value “Non-smoker” for records without smoker status. This approach is based on the heuristic of clinical coding practices, where positive risk factors (such as smoking) are actively recorded by clinicians, whereas the absence of a record is frequently used to implicitly denote a negative (non-smoking) status.

$21.6{\rm{\% }}$

. The results of the analysis of the randomness of missingness are presented in Table 36. They show that values are not missing completely at random. This means that we cannot remove records with missing values, and so we should impute the data. The imputation method we used was to set the value “Non-smoker” for records without smoker status. This approach is based on the heuristic of clinical coding practices, where positive risk factors (such as smoking) are actively recorded by clinicians, whereas the absence of a record is frequently used to implicitly denote a negative (non-smoking) status.

4.3.2 Regularly Recorded Data Items

The following data items are considered to be regularly recorded and therefore extracted from the data on an ongoing basis between the start date and end date of study.

It is a known issue in health data analysis that observational data can be recorded and missing in a biased way. This is because it is more likely for health metrics to be recorded where health is poor or there is a diagnosis that requires more frequent interaction with the health system or management of that metric (Rusanov et al., Reference Rusanov, Weiskopf, Wang and Weng2014). Therefore, missing data analysis and treatment is carefully considered and the impacts discussed within the results and conclusions.

4.3.2.1 Body Mass Index (BMI)

There are two sources of BMI observation data. Information was extracted from both sources, merged, cleaned and then analysed for missing data bias.

The first source is any table containing data with medcodes specified in Tables 28 and 29. In total, there are 489,756 records with medcodes from Tables 28 to 29, which represent 4% of all BMI measurements. For the 277 observations with an interval code and no corresponding event date (

$0.05{\rm{\% }}$

), the system date is substituted. That is, the date the information was entered into CPRD, which is, for those cases where both dates are known, within a few days of the event date.

$0.05{\rm{\% }}$

), the system date is substituted. That is, the date the information was entered into CPRD, which is, for those cases where both dates are known, within a few days of the event date.

The second source of BMI measurement observations is within the “Additional Clinical details” table of the CPRD data alongside the date of the observation as found in the clinical information file. There are

$14,317,076$

records in this table, which is 96% of all BMI measurements. Each record contains patid (ID of individual), adid (ID of measurement) and the value of the measurement. These records were filtered to remove a) those with no measurement value (308,392 measurements,

$14,317,076$

records in this table, which is 96% of all BMI measurements. Each record contains patid (ID of individual), adid (ID of measurement) and the value of the measurement. These records were filtered to remove a) those with no measurement value (308,392 measurements,

$2.5{\rm{\% }}$

) and b) any duplicate with the same combination of (patid, adid) (

$2.5{\rm{\% }}$

) and b) any duplicate with the same combination of (patid, adid) (

$1,824,379$

duplicates, 15%).

$1,824,379$

duplicates, 15%).

Joining the two sources provides a file with a time series of BMI measurement observations. Individuals have from 1 to a maximum of 1,508 observations within the study period. Records with obvious data input errors such as negative, nil, very small/large values (16,221 records,

$0.13{\rm{\% }}$

) are removed. After this, there are

$0.13{\rm{\% }}$

) are removed. After this, there are

$12,193,099$

BMI measurement observations for 978,380 individuals. We call this the “BMI total sample”.

$12,193,099$

BMI measurement observations for 978,380 individuals. We call this the “BMI total sample”.

BMI is known to be recorded and missing in a biased way. This is because it is more likely for BMI to be recorded where health is poor or there is a diagnosis that requires more frequent interaction with the health system or management of weight (Nicholson et al., Reference Nicholson, Aveyard, Bankhead, Hamilton, Hobbs and Lay-Flurrie2019). For the analysis of missing data, a given individual is considered to have a known value where there is at least one BMI measurement, otherwise it is missing. This disregards the lack of recording frequency that is expected for healthier lives. While this approach does not distinguish between the clinical context of individuals with differing health needs, it offers a pragmatic framework for handling large-scale, routinely collected data. It is important to acknowledge that the presence of a single BMI measurement may reflect varying levels of data quality: for instance, in individuals with chronic conditions such as diabetes, infrequent BMI recording may indicate incomplete data, whereas in healthier individuals, infrequent contact with healthcare services may reasonably result in fewer recordings. Although this introduces some bias, treating the presence of at least one BMI value as a known measurement provides a consistent and transparent definition of observed versus missing data.

Table 30 presents the results of the relationship between missingness of BMI and diagnosed diseases of interest in the BMI total sample. For most diseases of interest, the missingness of BMI is not random, as would be expected based on clinical practices. This aligns with prior expectations, since conditions such as diabetes, cardiovascular disease and obesity are known to prompt more regular weight and BMI monitoring as part of ongoing management and risk assessment. Conversely, there are only three diseases – Epilepsy, AIDS and Multiple Sclerosis – for which the association with BMI missingness is statistically insignificant. This also seems reasonable, as these conditions may not routinely require weight monitoring as part of standard care pathways. One further condition, Learning Disability, shows a small p-value suggestive of statistical dependence but a very small effect size, indicating minimal practical impact. This may reflect heterogeneous care patterns in this group, or variability in healthcare engagement and data recording practices. Overall, the observed pattern of associations largely corresponds with clinical expectations and known drivers of BMI measurement in routine care.

For the general sample of 250,000 individuals, there are 769,757 BMI measurements for 162,238 individuals (65%). Therefore, only 65% of the samples have at least one BMI measurement observation. Table 31 shows the results of missing data analysis where the

${\chi ^2}$

independence test shows that there are only 4 attributes for which we do not have enough evidence to reject hypothesis about independence with confidence level 99%. There is only one attribute (diagnosed stroke) which has significant p-value (

${\chi ^2}$

independence test shows that there are only 4 attributes for which we do not have enough evidence to reject hypothesis about independence with confidence level 99%. There is only one attribute (diagnosed stroke) which has significant p-value (

$0.758$

).

$0.758$

).

In conclusion, the missingness of BMI is highly correlated with age, sex and co-morbidities. This means that removing records with missing values is not appropriate and therefore imputing the missing data would be preferable. For this analysis, missing BMI measurements are imputed, based on the “nearest-neighbour” approach with regard to characteristics age, gender and co-morbidities. Specifically, we used the 1NN method, in which the imputed value corresponds to the actual BMI of the nearest neighbour, rather than an average or moving average of several nearest neighbours. This preserves the granularity of real observations while ensuring that imputations reflect biologically and clinically plausible values from similar individuals. This method is considered suitable in this context because these characteristics are strong predictors of BMI and are consistently recorded with high completeness in the data set.

4.3.2.2 Blood Pressure (BP)

Blood pressure measurements are found within the additional file named BP_medval_*.txt, which contains over 32 million observations. These records were filtered to remove those with a) no measurement value (544,923 records,

$1.7{\rm{\% }}$

) and b) any duplicate with the same patient ID (

$1.7{\rm{\% }}$

) and b) any duplicate with the same patient ID (

$3,875,362$

records, 12%). Where the diastolic field was greater than the systolic field (61,286 records,

$3,875,362$

records, 12%). Where the diastolic field was greater than the systolic field (61,286 records,

$0.2{\rm{\% }}$

), the values were reversed as this is a typical input error. The systolic and diastolic fields were reviewed for reasonableness (systolic range [50,300], diastolic range [30,120]). Where a record had values outside reasonable range, the record was removed (

$0.2{\rm{\% }}$

), the values were reversed as this is a typical input error. The systolic and diastolic fields were reviewed for reasonableness (systolic range [50,300], diastolic range [30,120]). Where a record had values outside reasonable range, the record was removed (

$281,831 + 201,426$

records,

$281,831 + 201,426$

records,

$1.5{\rm{\% }}$

). For the 475 cases with a missing event date, the date was substituted by system date with the same logic as per BMI.

$1.5{\rm{\% }}$

). For the 475 cases with a missing event date, the date was substituted by system date with the same logic as per BMI.

After the above data treatment, there are over 27 million BP measurement observations that correspond to individuals in the data, hence leaving the remaining observations without BP observations:

$7.6{\rm{\% }}$

(85,651) individuals in the total data set and 26% (65,286) individuals in the general sample. Table 31a shows that the analysis of the randomness of the missing data is not completely at random, as expected. Therefore, it is not appropriate to remove records with missing values and the preferred treatment is to impute the data. The imputation method adopted was to take the mean value from individuals with the same gender and the same (or similar, i.e., closest in the Hamming distance) set of co-morbidities.

$7.6{\rm{\% }}$

(85,651) individuals in the total data set and 26% (65,286) individuals in the general sample. Table 31a shows that the analysis of the randomness of the missing data is not completely at random, as expected. Therefore, it is not appropriate to remove records with missing values and the preferred treatment is to impute the data. The imputation method adopted was to take the mean value from individuals with the same gender and the same (or similar, i.e., closest in the Hamming distance) set of co-morbidities.

4.3.2.3 Cholesterol Level (CL)

The majority of cholesterol measurement observation data is found in the “Test” tables and some results are also found in the “Referral” tables. The data can be filtered specifically for cholesterol tests using readcodes and medcodes for cholesterol tests that are presented in Table 33.

The following values are measured during a CL test with the normal levels presented in Table 32.

-

• HDL (high-density lipoprotein) – the higher the better.

-

• Non-HDL (which includes LDL) – the lower the better. This group includes IDL, VLDL and lipoprotein.

-

• Total cholesterol (TC) or serum cholesterol – this is the total amount of cholesterol in the blood and includes both HDL and non-HDL cholesterol.

-

• Triglycerides – the lower the better.

-

• The TC to HDL ratio (TC:HDL) – the lower the better.

Under extreme conditions (e.g., homozygote with defective genes), TC can be above 1,000 mg/dL which corresponds to 26 mmol/L (Kattah et al., Reference Kattah, Gómez, Gutiérrez, Puerto, Moreno-Pallares, Jaramillo and Mendivil2019). Therefore, any case where the observation is above 40 mmol/L within the data is assumed to be an incorrect coding of units. That is, the true unit is mg/dL and as such, it is converted to mmol/L.Footnote 6

For the 256 cases with a missing event date, the date was substituted by system date with the same logic as for BMI. In total there are over 12 million CL measurement observations. After removing duplicates, there are over 10 million observations of 903,041 individuals, about 75% of all individuals in the total data set. For the general sample, cholesterol measurements are observed for about 33% individuals. Therefore, 67% of individuals do not have any CL measurements observations. Results of analysis of randomness of missingness (see Table 34) show that values are missed not completely at random. Therefore, it is not appropriate to remove records with missing values and the preferred treatment is to impute the data. The imputation method used is 1NN in space of age, gender and co-morbidities - this is the same method as we used for BMI.

4.3.2.4 Blood Glucose (Sugar) Level (HbA1c)

HbA1c information can be found mainly in table “Test” within the HES data. The result of HbA1c measurements can be presented either as interval or as scalar data. To extract measurements of HbA1c, the medcodes presented in Table 38 are used. There are 100,064 measurement observations with interval data among

$13,930,560$

observations from the “Test” table.

$13,930,560$

observations from the “Test” table.

For those records with a missing event date, the date of data registration is taken. This is considered appropriate because, based on available records with both values present, the date of measurement and the registration date typically occur within a few days of each other. Therefore, using the registration date provides a reasonable approximation of the measurement time with minimal impact on the temporal alignment of the data.

The units of measurements for all individuals and for the general sample individuals are presented in Tables 39 and 40, respectively. As we can see from these Tables, there are many units of measurements used, and the intervals of reasonable values in these units have non-empty intersections. Therefore, if the unit of measurement is not given, it is impossible to guess it based on the value. For this reason, measurements with some units such as “No Data Entered”, “No unit”, etc., were removed. When the unit is given, we convert the measurements to

${\rm{\% }}$

(A1c), which is one of the standard representations.Footnote

7

${\rm{\% }}$

(A1c), which is one of the standard representations.Footnote

7

Extreme value observations were treated as incorrect data inputs and the observations removed. The sample data contains 10 records with HbA1c less than 2%, and 190 records with values greater than 20%. These values fall outside the ranges for reasonableness, because a HbA1c value of

$3.2{\rm{\% }}$

is considered as pathologically low (Joob & Wiwanitkit, Reference Joob and Wiwanitkit2018); while, on the other hand, at values greater than 10% an individual “needs injectable therapy” (American Diabetes Association, 2017); and values exceeding 17% have been observed by medics only in rare cases (Petznick, Reference Petznick2011). The removal of these 200 outlier records (

$3.2{\rm{\% }}$

is considered as pathologically low (Joob & Wiwanitkit, Reference Joob and Wiwanitkit2018); while, on the other hand, at values greater than 10% an individual “needs injectable therapy” (American Diabetes Association, 2017); and values exceeding 17% have been observed by medics only in rare cases (Petznick, Reference Petznick2011). The removal of these 200 outlier records (

$0.0014{\rm{\% }}$

of the

$0.0014{\rm{\% }}$

of the

$13.9$

million total observations) is not considered to materially affect the results, given the minimal proportion and their likely erroneous nature. These exclusions help to preserve the overall quality and reliability of the data set without introducing meaningful bias.

$13.9$

million total observations) is not considered to materially affect the results, given the minimal proportion and their likely erroneous nature. These exclusions help to preserve the overall quality and reliability of the data set without introducing meaningful bias.

There are 1,522,020 measurement observations with a date recorded but a measurement value missing. In these cases, the observations are removed.

In total, HbA1c has been measured for about 61% of individuals in the total sample. That is, 39% of individuals do not have any HbA1c measurement observation data. This varies significantly across samples. In the diabetes sample, about 10% of individuals have missing HbA1c value. In the general sample, the missingness of HbA1c is 85%.

It is anticipated that this measure is missing for those without a diabetes diagnosis because HbA1c is not measured where medics do not consider an individual at risk of or showing signs of diabetes. Therefore the analysis of missing data is approached separately for the two groups.

Results of analysis of randomness of missingness show that, for some variables, missingness is not completely at random (see Table 41). Therefore, it is not appropriate to remove records with missing values and the preferred treatment is to impute the data. For individuals without a diabetes diagnosis for whom HbA1c has never been measured, a value within the “normal” range is imputed (say, 5%).Footnote 8

For individuals with a diabetes diagnosis, it is anticipated that HbA1c is missing without a significant bias by age (at least for adults) and gender (Weykamp, Reference Weykamp2013). This prior expectation is supported by our data. Hence, we focus the analysis on the dependence on co-morbidities. For every individual P with an unknown HbA1c value, a search is performed across all individuals

${P_t}$

in the diabetes sample such that (i) HbA1c is known and (ii) the Hamming distance between the co-morbidities of P and

${P_t}$

in the diabetes sample such that (i) HbA1c is known and (ii) the Hamming distance between the co-morbidities of P and

${P_t}$

is less than k, where k is the minimal value such that the number of nearest neighbours is at least 10. The imputed HbA1c value for P is then taken as the average HbA1c of its nearest neighbours. While we acknowledge that this method has some limitations, for example, it does not incorporate the temporal sequence of HbA1c observations, this approach allows us to preserve co-morbidity-related structure in the data, which is particularly relevant given the strong clinical association between certain conditions (e.g., cardiovascular disease, renal impairment) and glycaemic control.

${P_t}$

is less than k, where k is the minimal value such that the number of nearest neighbours is at least 10. The imputed HbA1c value for P is then taken as the average HbA1c of its nearest neighbours. While we acknowledge that this method has some limitations, for example, it does not incorporate the temporal sequence of HbA1c observations, this approach allows us to preserve co-morbidity-related structure in the data, which is particularly relevant given the strong clinical association between certain conditions (e.g., cardiovascular disease, renal impairment) and glycaemic control.

4.3.2.5 Diagnosed Diseases of Interest

Information is required regarding diseases (co-morbidities) that are expected to have a significant effect on the mortality risk. The list of diseases has been constructed by analysing the literature and in consultation with DSG and colleagues from Leicester Diabetes Research Centre. The resulting list of diseases is presented in Section 4.1.

The objective of the research is to differentiate mortality risk for individuals with diabetes. For example, those with coronary heart disease may have a higher mortality risk when there is also a diabetes diagnosis present compared to absence. Therefore, variables are coded to flag diabetes status and if any other disease is present.

Diagnosed diseases can be found in the CPRD data and in the HES linked data.

In the CPRD data, diagnosed diseases are encoded in the form of “medcodes” and “readcodes”; the codes relevant to diseases listed in Section 4.1 are summarised in Table 45. If any of the non-diabetes codes are present in the CPRD data for an individual, a corresponding disease status variable is set equal to 1.

A diabetes status variable is coded based on a list of diabetes-related medcodes/readcodes as described by Tate et al. (Reference Tate, Dungey, Glew, Beloff, Williams and Williams2017). This list is used here because it was freely available, and using it as a starting point significantly sped up the analysis.

The codes are split into three groups to define diabetes diagnosis status:

-

• 127 codes that are clearly related to Type 1 diabetes (D1T) – see Table 42.

-

• 124 codes that are clearly related to Type 2 diabetes (D2T) – see Table 43.

-

• 106 “unspecified” codes from which it is not possible to identify the Type of diabetes – see Table 44.

For each individual (patID) within the data, two variables are defined for modelling purposes based on whether items from the diabetes specific list of medcodes/readcodes are present or not before the end of the study period:

-

•

${d_1} = 1$

if Type 1 diabetes has ever been diagnosed,

${d_1} = 0$

otherwise. -

•

${d_2} = 1$

if Type 2 diabetes has ever been diagnosed,

${d_2} = 0$

otherwise. -

• For individuals with unspecified codes, these are classified as follows:

-

• If

${d_1} = {d_2} = 1$

, unspecified codes are disregarded. -

• If

${d_1} = 1$

and

${d_2} = 0$

, unspecified codes are classified as Type 1. -

• If

${d_1} = 0$

and

${d_2} = 1$

, unspecified codes are classified as Type 2. -

• If

${d_1} = {d_2} = 0$

, the classification is age dependent. If the first code is below age 28, set

${d_1} = 1$

and

${d_2} = 0$

, otherwise set

${d_1} = 0$

and

${d_2} = 1$

.

-

Classification of the unspecified codes by age is considered appropriate because Type 1 Diabetes is usually diagnosed earlier in life compared to Type 2 (Thomas et al., Reference Thomas, Jones, Weedon, Shields, Oram and Hattersley2018). The distribution of first diagnosis within the total sample by Type of Diabetes is presented in Figure 2. It can be seen that this also holds within the diabetes sample; for individuals with age of first diagnosis of diabetes less than 28 it is more likely to be Type 1 diabetes and for first diagnosis of diabetes at age 28 or more it is more likely to be Type 2 diabetes.

In the HES data, diagnosed diseases are encoded using ICD codes instead of medcodes/readcodes. At the time of the research, it was not possible to find a clear list of ICD codes corresponding to each disease as in Tables 42–45. To utilise the HES data, the ICD codes have been converted to medcodes/readcodes. Then we identify the diagnosis as per the process outlined above and summarised in Tables 42–45.

For the conversion, a dictionary from file ICD10.DBF from the “Clinical Terminology Browser” was used (the only version released on 19.03.2018) available online at https://isd.digital.nhs.uk/trud3/user/guest/group/0/pack/9/subpack/8/releases. It was developed to translate readcodes to ICD10 and there may be several readcodes for one ICD10 code. There are 14,702 different ICD10 codes covering 116,374 readcodes in the file. Unfortunately, there are 458 ICD10 codes used in the HES data within the sample that are not defined in this dictionary. In these cases, a nearest match is used to identify the diagnosis. For any given code, the ICD code with the same four symbols that could be found in the dictionary ICD code is used and then the corresponding row is used for decoding; otherwise the ICD code with the same three-symbol code is used.

For every disease, the date of the first record with the corresponding ICD, readcode, or medcode is used as the date of diagnosis. In effect, all records with the same disease at a later date are ignored. Some records are missing a date of diagnosis. However, all these cases contain a date of inclusion of information into the system (known as “system date”). Therefore, where the diagnosis date is missing the system date is used. Adopting this approach reduces the

$0.6{\rm{\% }}$

of records in the total sample with missing date of diagnosis to nil.

$0.6{\rm{\% }}$

of records in the total sample with missing date of diagnosis to nil.

5. Direct Data Analysis

To undertake reasonableness checks and better appreciate the morbidity and mortality risk within the samples, data analysis was undertaken. We computed various quantities of interest, such as mortality rates or disease probabilities, directly from data without the use of any models. This preliminary step aimed to ensure that the underlying data was consistent with expected trends and to offer initial insight into the proximity of observed outcomes, such as mortality and morbidity, to key rating factors. These analyses form a critical bridge between raw data and the structured modelling process, helping to distinguish correlation from causation and identifying patterns that may justify the inclusion or exclusion of certain variables in later stages.

The analysis in each subsection below is performed based on one of the following samples:

-

• General sample (GS).

-

• Diabetes sample (DIB).

The distribution of age for GS and DIB is presented in Table 51 and Figure 4.

5.1 Mortality Rates

To check the quality of data, a direct mortality estimation was performed by age bands on the GS and compared to the National Life Tables (NLT) (Office for National Statistics, 2025). These tables are appropriate for several reasons: they provide official, high-quality mortality benchmarks derived from comprehensive national data; they cover a similar geographical region as the study sample (the UK for NLT versus England for the study sample); and data for various time periods are available. Furthermore, the ONS methodology is transparent, statistically robust and widely accepted in actuarial and demographic research, making the NLT a reliable external reference point for validating age-specific mortality rates.

Mortality is estimated in age bands because, by any separate age, the direct estimate would produce inaccurate results due to small sample sizes. The age bands employed are in 10-year increments, except for the youngest group (e.g., 16–20, 20–30, 30–40, and so on).

For each age band A, the probability of death (e.g., the mortality rate) is calculated using the formula:

$${\mu _A} = {{{N_{DA}}} \over {{N_A}}}$$

$${\mu _A} = {{{N_{DA}}} \over {{N_A}}}$$

where

${N_A}$

is the number of individuals in age band A at the start of the study and

${N_A}$

is the number of individuals in age band A at the start of the study and

${N_{DA}}$

is the number of observed deaths within the study period from those individuals in age band A. The resulting mortality rates are presented in Table 68.

${N_{DA}}$

is the number of observed deaths within the study period from those individuals in age band A. The resulting mortality rates are presented in Table 68.

The NLT (“Tables”) present, for each age x, the probability

${q_x}$

that an individual aged x will die before reaching age

${q_x}$

that an individual aged x will die before reaching age

$x + 1$

. The notation

$x + 1$

. The notation

$q\left( {x,t} \right)$

therefore denotes the probability, for an individual aged x, of death during the year t. The Tables present mortality rates in three-year periods, for example,

$q\left( {x,t} \right)$

therefore denotes the probability, for an individual aged x, of death during the year t. The Tables present mortality rates in three-year periods, for example,

$q\left( {x,2011} \right)$

is the central estimate for the period

$q\left( {x,2011} \right)$

is the central estimate for the period

$2010-2012$

. A mortality rate by 10 year age bands over the study period is computed from the Tables in order to make a comparison to the

$2010-2012$

. A mortality rate by 10 year age bands over the study period is computed from the Tables in order to make a comparison to the

${\mu _A}$

values calculated from GS. To achieve this, the number of NLT expected deaths for each year t is calculated for a given population

${\mu _A}$

values calculated from GS. To achieve this, the number of NLT expected deaths for each year t is calculated for a given population

${N_x}$

for each age x, for example,

${N_x}$

for each age x, for example,

$$M\left( {x,t} \right) = {N_x} \cdot q\left( {x,t} \right).$$

$$M\left( {x,t} \right) = {N_x} \cdot q\left( {x,t} \right).$$

The number of deaths in the following year,

$t + 1$

, is calculated after reducing the population at age x for the deaths in the year t and by accounting for the change in the probability of death for the cohort now 1 year older:

$t + 1$

, is calculated after reducing the population at age x for the deaths in the year t and by accounting for the change in the probability of death for the cohort now 1 year older:

$$M\left( {x + 1,t + 1} \right) = \left( {{N_x} - M\left( {x,t} \right)} \right) \cdot q\left( {x + 1,t + 1} \right).$$

$$M\left( {x + 1,t + 1} \right) = \left( {{N_x} - M\left( {x,t} \right)} \right) \cdot q\left( {x + 1,t + 1} \right).$$

Therefore, the number of deaths during the year

$t + k$

, for the cohort aged in year t, can be calculated as

$t + k$

, for the cohort aged in year t, can be calculated as

$$M\left( {x + k,t + k} \right) = \left( {{N_x} - \mathop \sum \limits_{p = 0}^{k - 1} M\left( {x + p,t + p} \right)} \right) \cdot q\left( {x + k,t + k} \right).$$

$$M\left( {x + k,t + k} \right) = \left( {{N_x} - \mathop \sum \limits_{p = 0}^{k - 1} M\left( {x + p,t + p} \right)} \right) \cdot q\left( {x + k,t + k} \right).$$

This can also be rewritten as:

$$M\left( {x + k,t + k} \right) = {N_x} \cdot \mathop \prod \limits_{p = 0}^{k - 1} \left( {1 - q\left( {x + p,t + p} \right)} \right) \cdot q\left( {x + k,t + k} \right).$$

$$M\left( {x + k,t + k} \right) = {N_x} \cdot \mathop \prod \limits_{p = 0}^{k - 1} \left( {1 - q\left( {x + p,t + p} \right)} \right) \cdot q\left( {x + k,t + k} \right).$$

The total number of deaths, for the cohort aged x at the study start, over the study period of 2010–2019 is therefore:

$${M_x} = \mathop \sum \limits_{k = 0}^9 M\left( {x + k,2010 + k} \right).$$

$${M_x} = \mathop \sum \limits_{k = 0}^9 M\left( {x + k,2010 + k} \right).$$

The total number of deaths within an age band A is the summation of the total deaths for each age x within A:

$${M_A} = \mathop \sum \limits_{x \in A} {M_x}.$$

$${M_A} = \mathop \sum \limits_{x \in A} {M_x}.$$

To arrive at an estimation of mortality from NLT, the total deaths by age band,

${M_A}$

, are taken as a proportion of the population at the start of the period,

${M_A}$

, are taken as a proportion of the population at the start of the period,

${N_A} = \mathop \sum \nolimits_{x \in A} {N_x}$

,

${N_A} = \mathop \sum \nolimits_{x \in A} {N_x}$

,

$${\mu _A} = {{{M_A}} \over {{N_A}}}$$

$${\mu _A} = {{{M_A}} \over {{N_A}}}$$

Using the

${N_x}$

values from the GS, the implied mortality rate

${N_x}$

values from the GS, the implied mortality rate

${\mu _A}$

based on the NLT estimated rates are presented in Table 69. Figure 10 compares these to the GS mortality and the observed difference is negligible, which provides confidence that, at least in the aspect of general mortality, our data are consistent with the general UK population.

${\mu _A}$

based on the NLT estimated rates are presented in Table 69. Figure 10 compares these to the GS mortality and the observed difference is negligible, which provides confidence that, at least in the aspect of general mortality, our data are consistent with the general UK population.

5.2 Disease Probabilities

Before building the model for mortality prediction, we performed some direct estimates for disease probabilities that may be of independent interest. The objective of this exercise is to assess the plausibility and internal consistency of the morbidity information before incorporating it in a multivariate modelling framework. This step is of particular interest to the actuarial audience because the presence and prevalence of certain diseases, such as cardiovascular conditions or cancer, are known to be strong predictors of increased mortality risk of the individuals with diabetes and are frequently used as underwriting factors. By estimating these probabilities directly from the data (i.e., without modelling assumptions), we aimed to uncover potential patterns, anomalies, or data quality issues that might impact downstream risk assessment.

First, the probabilities of various diseases for individuals in the general (GS) and in diabetes (DIB) samples are computed as the ratio:

$$P\left( A \right) = {{{N_A}} \over {{N_T}}},$$

$$P\left( A \right) = {{{N_A}} \over {{N_T}}},$$

where

${N_T}$

is the total number of individuals in the sample and

${N_T}$

is the total number of individuals in the sample and

${N_A}$

is the number of individuals in this sample for which disease A has ever been diagnosed. The resulting disease probabilities are presented in Table 50. Some of the findings are highlighted in green: for example, the most frequent disease in GS is dementia and the most frequent in DIB (i.e., given a diabetes diagnosis) is hypertension. Care should be taken when interpreting such direct estimates. For example, it cannot be concluded that diabetes increases the risk of hypertension as other factors are not accounted for in such an analysis, such as the difference in the weighted average age of the samples. DIB is on average older than GS – see Table 51 and Figure 4 – and older individuals have higher risk of hypertension.

${N_A}$