Key messages

Chapter 2.2 investigates the design and implementation of health benefits packages (HBPs) in different contexts. A benefits package is the range of health care goods and services that people covered by a system or scheme are entitled to or should be able to access. Key learning includes that:

All health systems have budgetary constraints and set some limits to entitlement, and therefore have some kind of benefits package.

Benefits packages may be explicitly defined or implicit only, with the latter more common in high-income countries (HICs) and the former more common in low- and middle-income countries (LMICs).

What is included or excluded, and the ways these decisions are made, vary widely but well-designed benefits packages should address population health needs and ensure the efficient use of health system resources.

Defining a package of care is complex and often highly sensitive – using evidence and economic evaluation to determine what to include (or exclude) supports efficiency and equity and allows policy-makers to explain and defend their choices.

There are a range of evidence-led instruments that can support policy choices such as health technology assessment (HTA), which incorporates economic evaluation.

Any decision-making process should:

○ gain agreement and buy-in from key stakeholders on the ultimate goals of the benefits package and the level of explicitness;

○ take into account the specific characteristics of the setting where the benefits package will be implemented, including its cultural values, market configuration, political system and wealth.

Introduction

Every country’s health care system embodies some form of benefits package – the range of health care treatments or services that should be accessible to those individuals entitled to health services in the country concerned. In countries with a national health service or national health insurance, this would normally be the whole population. In countries with social security or private insurance health care, the entitled individuals would be the members of the insurance plan. Explicit HBPs can serve several purposes, including setting standards for health care, or specifying the basic services that should be made available to all eligible individuals. They also offer the possibility for using analysis, such as HTA, incorporating economic evaluation, to determine which services should be included or excluded. However, in many HICs the HBP may be implicit, or defined only in general terms (e.g. free access to primary and secondary care services). Therefore, the role of analysis in setting the benefits package tends to be limited to decisions on whether new health technologies should be reimbursed. Explicit benefits packages, with more definition of the services included, are more common in LMICs, often in the context of initiatives to implement universal health coverage (UHC) (Jehu-Appiah et al., Reference Jehu-Appiah2008; Youngkong et al., Reference Youngkong2012). However, in HICs, in the absence of explicit benefit catalogues, inpatient and outpatient remuneration schemes often have the character of implicit or less explicit benefit catalogues (Schreyögg et al., Reference Schreyögg2005).

When elaborating on population coverage and benefits packages it is important to define the terms used as well as the scope of this chapter. We follow the definition of the EU HealthBasket project (Schreyögg et al., Reference Schreyögg2005) and use the term “benefit basket” to be synonymous with “benefits package”; we differentiate these from “benefit catalogues”. Benefits package refers to the totality of services, activities and goods covered by publicly funded statutory/mandatory insurance schemes (i.e. social health insurance (SHI)) or by national health services. Benefit catalogues are defined as the documents (e.g. for inpatient and outpatient care or for pharmaceuticals) in which the different components of the benefits package are stated in detail. These benefit catalogues can either be defined rather generally (e.g. inpatient care after acute myocardial infarction (AMI)) or by enumerating services or procedures in a more detailed way (e.g. insertion of stents after AMI) (Schreyögg et al., Reference Schreyögg2005). Especially in LMICs, but also in HICs, there may be a disconnect between the aspirational health plans and the actual availability of funds and resources. It thus seems important to distinguish the benefits package offered in theory and the care actually received by patients (Glassman et al., Reference Glassman2016).

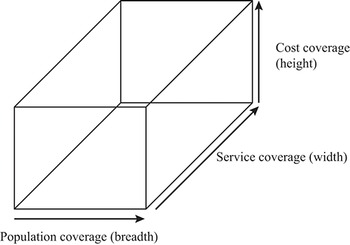

Further, a given benefits package can be characterized by different dimensions of coverage. “Breadth” can be defined as the extent of the covered population (e.g. certain parts of the population or full coverage). “Depth” is defined as the number and character of covered services (e.g. hip replacement for all persons up to the age of 80 years). The third dimension, “height”, specifies the extent to which costs of the defined services are covered by financial resources (e.g. full reimbursement of services versus cost-sharing requirements for certain services) (Busse, Schreyögg & Gericke, Reference Busse, Schreyögg and Gericke2007). Fig. 2.2.1 displays the three dimensions of a benefits package. An ideal HBP would fill this box as much as possible. In this chapter we mainly focus on the “depth” dimension (service coverage).

A benefits package involves consideration of coverage in terms of cost, service and population

In terms of service coverage, there are different ways of defining which services are included in the benefit catalogues forming a benefits package. Definition may be based on need, if enough financial resources are available to cover all the services required to address population needs. However, since most countries recognize the scarcity of resources, criteria such as effectiveness, cost–effectiveness or budgetary impact are often taken into consideration. An explicitly defined benefit catalogue, and more general benefits package, usually requires the formulation of evidence-based allocation criteria.

This chapter discusses the role of explicit benefits packages in achieving efficiency and equity in health care provision. It reviews the arguments for and against explicit benefits packages, provides examples from different health care contexts, and discusses the challenges in setting a benefits package. Although the chapter discusses a broad range of issues, one specific focus is on the use of evidence in determining the benefits package, in particular the use of HTA, incorporating economic evaluation.

The case for and against explicit benefits packages

The advantages of setting an explicit benefits package have been documented by Glassman et al. (Reference Glassman2016) (Box 2.2.1). The advantages, along with the potential limitations, have been further discussed by Smith and Chalkidou (Reference Smith and Chalkidou2017), using the English National Health Service as an example. They argue that an explicit package would: (i) encourage equitable access to health services, by reinforcing the principle of horizontal equity (i.e. equal access for equal need); (ii) ensure maximum benefit from the funds available, if appropriate cost–effectiveness criteria were used for coverage; (iii) improve transparency and clarity for the public, thereby empowering individuals in dealing with providers; (iv) provide clear signals to the market, by identifying which services will and will not be reimbursed; (v) protect politicians and clinicians from special pleading, reducing the risk of undue influence and corruption; and (vi) promote clarity for those involved in planning, funding and operating the health care system, by helping to identify where the highest priorities exist.

1. It creates explicit entitlements for patients, whose access to services might otherwise be largely determined by clinical professionals, with the consequent potential for arbitary variations in access.

2. It helps to identify whether funds are being spent wisely on services that create the maximum benefit for the society.

3. By specifying the services to be delivered, it facilitates important resource allocation decisions, such as regional funding allocations, and other planning functions, creating a precondition for reducing variations in care and outcomes.

4. It facilitates orderly adherence to budget limits, which might otherwise be attained only through arbitrary restrictions on access and services.

5. It reduces the risk that providers will require informal payments from patients to secure access to high-value services.

6. The entitlements created empower poor and marginalized groups, who cannot be made aware of any specific entitlement without an explicit health benefits package.

7. It create the preconditions for a market in complementary health insurance for services not covered, with a number of potential benefits for the health system as a whole.

Furthermore, Smith and Chalkidou (Reference Smith and Chalkidou2017) identify some of the potential challenges in setting an explicit benefits package: (i) the practical difficulties in specifying a package; (ii) the possible inhibition of innovation, if the package is not regularly updated; (iii) restrictions on legitimate variations in services, if local needs vary from place to place or among individuals; (iv) the creation of serious political and legal difficulties, if the package is perceived as giving priorities for some groups over others, or inappropriately rationing care; (v) the difficulties caused by existing rigidities in the health care system, making changes in care difficult or costly; and (vi) the creation of uncertain financial liabilities, by making it difficult to limit access to services even if there is no budget.

In addition, politicians may be reluctant to engage in discussions on allocation decisions being inevitably linked to setting explicit benefits packages. The openness of societies to discuss allocation decisions in health care is certainly also determined by the culture and history of a given country (Torbica, Tarricone & Drummond, Reference Torbica, Tarricone and Drummond2018). While, for instance, in the United Kingdom allocation decisions based on cost–effectiveness thresholds are commonly acceptable, historically, decision-makers in Germany have tended to avoid public allocation discussions as they may be too politically contentious. Moreover, since HICs use reimbursement schemes as benefit catalogues, they have to consider the incentives for providers and patients. Fee-for-service (FFS) schemes explicitly listing single items to be reimbursed may lead to an overprovision of services.

The fact that relatively few HICs have a detailed explicit benefits package, listing items to be reimbursed, suggests that these limitations are perceived to be more important than the potential advantages, at least by the decision-makers who would be responsible for setting an explicit package. Many of the practical difficulties, such as the information required to set and update a package, could be overcome, albeit with some effort. This will be discussed later. However, it may be more difficult to overcome decision-makers’ views about the political problems arising from setting a detailed explicit package, if it is perceived to make rationing more explicit or to reduce budgetary control. Nevertheless, it is important to recognize that failure to specify an explicit benefits package can cause similar political problems. The most obvious manifestation of this is the problem observed in many Latin American countries, where health is considered a basic right under the constitution. This has led to a situation where individuals often take legal action (known as “right-to-health litigation”) to secure access to expensive health technologies that are not routinely available in the country’s health care system (Reveiz et al., Reference 195Reveiz2013). This can pose a threat to the health care budget, and/or distort health care priorities.

Evidence in practice: examples of setting explicit HBPs

Despite the practical challenges of setting an explicit HBP, several examples of doing this exist. Five case studies are discussed in this section, reflecting different health care settings and challenges for the process of developing and implementing a benefits package. The first case study on Italy exemplifies the approach of a HIC, with a decentralized national health service, to update its existing benefit catalogues. The second case of German inpatient care illustrates the trend in several HICs to move from rather implicitly defined to more explicitly defined benefit catalogues, including the challenges involved with this. The third case discusses a value-based approach for determining access to medicines, in a private health insurance setting of the USA. The fourth case study describes how Chile, an upper-middle-income country (UMIC), used an HBP to improve the quality of, and access to, health care for all of its citizens.

The final case study considers the establishment of HBPs in a LIC, and shows how an analytic framework based on economic evaluation can be used to support the development of an explicit benefits package. It might be argued that this poses additional challenges, since the relevant data and skills, although not absent, may not be as available as in HICs. In addition, the criteria considered in setting the package may place a greater weight on improving the equality of access to services, particularly for vulnerable groups and family welfare more generally. For example, in their work considering the inclusion of health interventions in the benefits package in Thailand (a UMIC), Youngkong et al. (Reference Youngkong2012) applied the criteria of “economic impact on household expenditure” and “equity, ethical and social implication”, alongside criteria such as effectiveness, disease severity and size of the population affected.

Example 1: Evolving a benefits package over time in the Italian National Health Service

The Italian National Health Service (INHS), known as Servizio Sanitario Nazionale, is characterized by universal coverage, providing comprehensive health care services to all citizens and residents across national territory. The issue of an HBP in Italy is deeply embedded in the history of the INHS and its reforms over the past four and a half decades. One of the main features of these reforms has been a progressive decentralization of the health care system, with regional governments gaining greater decision autonomy in planning, organizing and delivering health care services to their residents. While decentralization aimed to allow regions to tailor health care services to meet the unique requirements of their populations, it inevitably led to shaping a complex relationship between the central state and the various regions over a series of issues. The definition of what should be included in the HBP has been much debated within Italy’s health care system. The benefits package, intended as the overall set of services guaranteed to citizens under public coverage across the whole country, has changed over the years in its form, contents and objectives to become increasingly explicit.

From 1978 to 2017

The principle of a benefits package available to all citizens irrespective of age, social condition or income was introduced when the INHS was established in 1978. Although the law introducing it listed the areas in which treatments were to be delivered directly by the INHS and used the expression “levels of care”, it was only in its health sector reforms of 1992/1993 that the national government explicitly defined the set of services to be provided under INHS coverage (“uniform levels of care”, livelli uniformi di assistenza, LUA). Since then, regions have been held accountable for providing the services included in the benefits package with the budgets allocated from the central government. In cases of overspending, the regions are financially responsible to cover the extra expenditure in order to guarantee the provision of the benefits package. They can also expand the services beyond what is set at the national level provided that they use their own resources. But there were demands for the benefits package to be made more explicit still. In the late 1990s, the National Health Plan produced guidelines as to what else was needed: a definition of principles (decision criteria), the amount of per capita funding required to provide guaranteed services, and a set of tools to monitor the implementation across regions. Subsequent reform, in 1999, specified guiding principles to determine the health care services to be included the benefits package – human dignity, effectiveness, appropriateness and efficiency. Underlining the importance of the equity principle in the access of care, the reform introduced a new expression – “essential level of care” (livelli essenziali di assistenza, LEA). Much debated during the years since, LEAs are considered key policy tools to regulate the relations (mainly financial) between the state and the regions and to ensure territorial equity within national borders. The services included at different levels of care, from community to hospital services, were defined at that time in a national law of 2001, and remained a pivotal element of the Italian HBP until its most recent redefinition in 2017.

Italy’s health benefits package today

The services included in the benefits package are now defined at three major levels: (i) collective prevention and public health; (ii) community health care services; and (iii) hospital/inpatient care. A Permanent Committee within the Ministry of Health has responsibility for verifying and monitoring the provision by the regions of all services in the benefits package in line with the principles of appropriateness and efficiency in the use of resources, as well as ensuring congruity between the services to be provided and the resources made available by the central government. In 2020, a National Commission responsible for updating the LEA was established with a three-year remit to ensure systematic and regular updating of the benefits package.Footnote 1

HTA, and more specifically economic evaluation, is also playing a role in shaping the benefits package in Italy, though so far it is largely limited to the evaluation of health care technologies for reimbursement decisions, namely pharmaceuticals and medical devices.

For pharmaceuticals, the Italian Medicines Agency (Agenzia Italiana del Farmaco, AIFA) undertakes the assessments. The decision-making power is concentrated in the Price and Reimbursement Commission (Comitato prezzi e rimborso, CPR), a technical body with 12 expert members that oversees the appraisal process. The criteria for appraisal include the degree of innovation, availability of existing products and extent of therapeutic benefit using clinical effectiveness, cost–effectiveness, risk-benefit ratio and budget impact studies, which constitute a support tool in the decision-making process. This type of assessment is used to support pricing and eligibility for reimbursement decisions and de facto determines which pharmaceuticals are included in the Italian benefits package and which are not.

The evaluation of medical devices is undertaken as part of the National Health Assessment Technology Programme for Medical Devices. The Programme was introduced by the Italian Stability Law of 2015, after a highly participatory, stakeholder-engaged, structured process of harmonization and centralization to address the hitherto fragmented system of appraisal and approval (Tarricone et al., Reference Tarricone2021). The main objective is to ensure effective stewardship and guarantee equal access to innovative technologies in all parts of the nation, notwithstanding the decentralized nature of the INHS. The Programme includes the most updated methods in assessing medical devices, coherent with those developed by EUnetHTA (www.eunethta.eu) and other international scientific consortia, such as, MedtecHTA (www.medtechta.eu), and links the recommendations of HTA with the most relevant policies in the health domain: coverage, reimbursement and procurement of medical devices. This initiative has the potential to break the traditionally “siloed” mentality and to foster a value-based approach in prioritizing, assessing, introducing and diffusing new technologies in the INHS.

Example 2: Germany: from an implicitly defined to an explicitly defined benefits package

A core principle of the German health care system is the sharing of decision-making powers between the governments of the federal states, the federal government and designated self-governmental institutions. Responsibilities are traditionally delegated to self-governing institutions of payers and providers that are involved in financing and delivering health care. Payers (sickness funds) and providers (physicians, dentists and hospitals) are represented by their associations, which are recognized as corporate bodies. These bodies constitute the structures of self-government that operate the financing and delivery of benefits covered by the Statutory Health Insurance scheme within the legal framework of the Social Code Book V. The most important body for the benefit negotiations between sickness funds and providers, concerning the scope of benefits, is the Federal Joint Committee (G-BA). Based on the legislative framework, the Committee issues directives relating to all sectors of care. The main body of the Committee consists of five representatives of the sickness funds, five representatives from provider groups, two neutral members and a neutral chairperson. The directives of the Committee are legally binding for all actors in the Statutory Health Insurance scheme. These directives primarily concern the coverage of benefits and ensure that Statutory Health Insurance services are adequate, appropriate and efficient. Beyond these general goals, the actual criteria for benefit definitions vary largely between sectors and types of catalogues (Blümel et al., Reference Blümel2020; Busse, Stargardt & Schreyögg, Reference Schreyögg2005).

In the outpatient sector, a service provided must be proven to fulfil the criteria “expedience, necessity and cost–effectiveness” to be included in the catalogue of services and benefits. In contrast, health care services in the inpatient sector will only be excluded from the benefit catalogue of the sickness funds if the criteria are proven to be unfulfilled (Busse, Stargardt & Schreyögg, Reference Schreyögg2005). For this reason, several health care services provided in the inpatient sector are not included in the benefit catalogue of the outpatient sector. In other words, any authorized new procedure or service in inpatient care can be provided by hospitals on behalf of the Statutory Health Insurance scheme. The ability of hospitals to provide a certain service is primarily regulated by prices via the diagnosis-related group (DRG) catalogue and its appendices for cost-intensive drugs and procedures (see Chapter 3.2). The rationale behind this practice of setting the benefits package is that new (experimental) services should first be incorporated and tested in inpatient care before they are allowed to diffuse into outpatient care. For pharmaceuticals, like the benefit regulation in inpatient care, the benefits package includes all authorized products launched on the German market. There is no positive list for pharmaceuticals. The availability of a given pharmaceutical on the German market, and therefore being part of the benefits package, is mainly determined by price regulation.

The decisions on benefits taken by the G-BA finally shape the benefit catalogues of the different health care sectors, which were originally introduced for reimbursement purposes. Thus, the level of explicitness varies between sectors. FFS-based catalogues in outpatient care, such as the Einheitlicher Bewertungsmaßstab for physician services or the Einheitlicher Bewertungsmaßstab für zahnärztliche Leistungen for dental care services, list most reimbursable services and procedures in detail. In contrast, the DRG catalogue for inpatient care started in 2003 with 664 DRGs, which were meant to reimburse all services unless excluded by the G-BA. Therefore, in 2003 the approach of defining the benefit catalogue in inpatient care could be characterized as quite implicit. However, Gibis, Koch and Bultman (Reference Gibis, Koch, Bultman, Saltman, Busse and Figueras2004) anticipated that the DRG catalogue would be extended over time to a more detailed benefit catalogue, where most approved interventions are listed and grouped around the relevant diagnoses.

Indeed, in the last 10 to 20 years, the German health care system has moved towards a more explicitly defined benefits basket. Since the inception of the G-BA in 2004, the number of issued directives on reimbursement of benefits has increased substantially compared with its predecessor committees. This has led to more inclusions and exclusions of benefits in inpatient and outpatient care, and has certainly contributed to a more explicit definition of benefits and in reimbursement catalogues. However, the most noteworthy change towards a more explicit definition of benefits took place in inpatient care.

In 2003, the DRG catalogue was introduced for inpatient care with the ambitious aim of reimbursing all inpatient services across all care structures, including academic medical centres with highly complex services. With 664 DRGs, the diagnoses-led catalogue acted as a rather implicitly defined benefit catalogue. It soon became clear that a given DRG did not sufficiently cover certain cost-extensive services and led to the threat of implicit rationing of certain services. This exerted a lot of pressure on the self-governing institutions to split DRGs and add reimbursement components. Thus, the DRG catalogue has been slowly transformed into a procedures-based catalogue with 1275 DRGs (50% of those is triggered by at least one procedure) and 275 fixed supplementary payments for explicitly mentioned high-cost drugs and procedures. On top of this, several other reimbursement components, such as separate payments for new technologies and negotiated supplementary payments for more established new technologies, were introduced (Ex & Henschke, Reference Ex and Henschke2019).

The case of the German DRG-catalogues reveals how what started out as an implicitly defined diagnoses-led catalogue can be transformed to an explicitly defined benefit catalogue without changing the rules for inclusion or exclusion of benefits. However, this development had certain side-effects. The more procedure-based catalogue led to incentives to increase treatment volume and treatment intensity (Bäuml & Kümpel, Reference Bäuml and Kümpel2021; Schreyögg et al., Reference Schreyögg2014). It also created incentives to favour operative procedures over conservative procedures, since operative procedures receive a higher reimbursement price (see Chapter 3.2 for more on methods for paying hospitals).

Example 3: HBPs under private health insurance – the Premera Blue Cross value-based formulary in the USA

The private health insurance sector of the USA’s health care system comprises more than 900 health plans. These plans offer individuals and their employers health care coverage for an annual premium, and also stipulate co-payments for some services. An important component of the HBP is the drug formulary, which determines the access to medicines for plan enrollees. Typically, health plan formularies contain most available drugs, organized in tiers, with the level of patient co-payment varying by tier, with inexpensive generic drugs being placed on a tier associated with a low co-payment. Branded drugs and expensive specialty drugs would be placed on tiers associated with higher levels of co-payment. In most health plans, formulary placement decisions are made by a Drug and Therapeutics Committee. Clinical evidence of drug effectiveness and safety is considered, but the use of economic evidence is sparse.

Premera Blue Cross is a large not-for-profit health plan in the Pacific Northwest which has used economic evaluation as part of its decision-making in the adoption of new health technologies. In 2010 it decided to implement a value-based drug formulary, in which drugs would be placed on tiers based on their value for money, rather than based on their acquisition cost. It was considered that aligning the individual drug’s co-payment to its specific value might yield greater clinical and economic benefits. However, in making this change, the health plan was also conscious of any impact it might have on enrollees’ costs or utilization of medicines, since health plans in the USA operate in a competitive environment. This is different from setting a benefits package in a publicly funded or social security system, where individuals cannot change their basic health insurance because of changes in the benefits package, although they do have the option of paying for supplementary private insurance.

The design, implementation and first-year outcomes of the value-based formulary were analysed and discussed in academic literature (Sullivan et al., Reference Sullivan2015). Value was assessed primarily by cost–effectiveness analysis, with the value for money of each drug assessed by the level of the incremental cost–effectiveness ratio (ICER) compared with the most relevant alternative (e.g. basic supportive care or an alternative drug). The value-based formulary was designed as a four-tier system, plus a “preventive” tier, for which the co-payment was set at zero. Higher rates of co-payment were set for the other four tiers based on commonly used cost–effectiveness thresholds identified from a literature review (Sullivan et al., Reference Sullivan2015). To allow for the fact that the ICER does not consider all the factors that might be relevant for formulary listing decisions, a “special case” category was created to allow for other aspects of social value, such as treatment for serious rare conditions for which there was no other acceptable treatment. The main difference between the value-based formulary and a standard formulary was that drugs with higher acquisition cost were not automatically assigned to a higher tier. They might be assigned to a lower tier if the benefits outweighed the costs. The tiers, ICER thresholds and co-payment levels are shown in Table 2.2.1.

| Tier | Typical case ICER threshold | Special case ICER threshold | Co-payment (US$)Footnote a |

|---|---|---|---|

| Preventive | Not applicable | Not applicable | 0 |

| Tier 1 | Cost saving or <US$ 10 000/QALY | Cost saving or <US$ 50 000/QALY | 20 |

| Tier 2 | US$ 10 000–<US$ 50 000/QALY | US$ 50 000–US$ 150 000/QALY | 40 |

| Tier 3 | US$ 50 000–US$ 150 000/QALY | >US$ 150 000/QALY | 65 |

| Tier 4 | >US$ 150 000/QALY or insufficient evidence to determine ICER | Insufficient evidence to determine ICER | 100 |

ICER: incremental cost–effectiveness ratio; QALY: quality-adjusted life-year.

a Amount of the retail co-payment for 30-day supply of medicine.

In constructing the formulary, the clinical safety and effectiveness assessment followed Premera’s normal practice. The value assessments were made by reviewing available ICER estimates from a variety of sources including: (i) economic models provided by manufacturers in their formulary submission; (ii) published economic studies; (iii) the Tufts Cost–Effectiveness Analysis registry (Tufts Medical Center, 2021); (iv) Cochrane Collaboration reviews; and (v) reviews by health technology agencies. In cases where no suitable evidence existed, Premera conducted its own economic analyses. Within the first year, value assessments were produced for drugs in each of the 25 highest volume drug classes used by Premera members in the previous year, accounting for approximately 75% of total drug utilization within the plan.

Since Premera was the first health plan to develop a value-based formulary, the level of acceptability to enrollees was unknown. Therefore, the new value-based formulary was initially only offered to Premera’s employees and dependents enrolled in the standard preferred provider organization (Premera Associates Plan). Sullivan and colleagues (Reference Sullivan2015) report the results of the first-year evaluation. The distribution of drugs across the tiers were markedly changed, with 39.9% being on the new “preventive” tier, 14% on Tier 1, 36% on Tier 2, 7.4% on Tier 3 and 2.7% on Tier 4. Pharmacy costs decreased by 3% compared with the previous 12 months and 11% compared with expected costs. There was no significant decline in medication use or adherence to treatments for patients with diabetes, hypertension or dyslipidaemia. Sullivan and colleagues (Reference Sullivan2015) argue that these results suggest that it is possible to implement a value-based formulary in a USA employer-based health plan and achieve efficiency and value gains.

A longer-term evaluation of the value-based formulary, using an interrupted time series of employer-sponsored plans from 2006 to 2013, was reported in another paper by Yeung and colleagues (Reference Yeung2017). They compared 5235 beneficiaries exposed to the value-based formulary with 11 171 beneficiaries in plans without any changes in pharmacy benefits. The primary outcome compared was medication expenditures from member, health plan and overall (member plus plan) perspectives. Secondary outcomes were medication utilization, emergency department visits, hospitalizations, office visits and nonmedication expenditures. It was found that member medication expenditures increased by US$ 2 per member per month (95% CI US$ 1–US$ 3), whereas plan medication expenditures decreased by US$ 0 (95% CI US$ 18– US$ 2), resulting in a net decrease of US$ 8 (95% CI US$ 15– US$ 2). This translated into net savings of US$ 1.1 million. Utilization of medicines moved into lower tiers increased by 17%, but total medication utilization, health services utilization and nonmedication expenditures did not change.

Example 4: Using the development of a health benefits package to improve the access and quality of services in a middle-income country – the Acceso Universal con Garantias Explicitas (AUGE) in Chile

Like several countries in Latin America, Chile relies on SHI to provide health care to a substantial proportion of its population. However, its insurance scheme has been criticized over the years for having two separate components. The first is a large public insurer (Fonasa), using mostly public providers, covering about 75% of the population including those on low and middle incomes and indigent citizens. The other component consisted of several private insurers (Isapres), using mostly private providers, covering a further 16% of higher income citizens.

This fragmentation led to differences in the content and quality of services, and the level of access to them. Prior to 2005, Fonasa did not have an explicit benefits package and there was rationing of care through queues, denial of services and provision of low-quality services. Also, different Isapres could offer different health plans, with a different range of services of different levels of quality. The lack of a benefits package was seen as a major weakness of the scheme overall, which allowed for divergences in coverage between Fonasa and Isapres and for risk selection and limited risk pooling in the Isapres (Bitran, Reference Bitran2013).

Therefore, in 2005, Chile’s government introduced the Universal Access with Explicit Guarantees (Acceso Universal con Garantias Explicitas – AUGE), which defined a basic HBP consisting of guaranteed and explicit treatments for 56 priority health problems. This was expanded to 69 priority problems in 2010 (see Table 2.2.2).

Priority health problems in tde AUGE benefits package

1. End-stage chronic renal failure

2. Operable congenital heart disease (under 15 years of age)

3. Cancer of the uterus or cervix

4. Cancer pain relief and palliative care

5. Acute myocardial infarction

6. Diabetes mellitus type I

7. Diabetes mellitus type II

8. Breast cancer (15 years of age or more)

9. Spinal dysraphia

10. Scoliosis surgery (under 25 years of age)

11. Cataract surgery

12. Total hip replacement in people with severe osteoarthritis of the hip (65 years of age or more)

13. Cleft palate

14. Cancer (under 15 years of age)

15. Schizophrenia

16. Testicular cancer (15 years of age or more)

17. Lymphoma (15 years of age or more)

18. HIV/AIDS

19. Ambulatory care lower acute respiratory illness (under 5 years of age)

20. Ambulatory pneumonia (65 years of age or more)

21. Primary or essential arterial hypertension

22. Epilepsy (non-refractory) (1 to 15 years of age)

23. Prevention and education for oral health (6 years old)

24. Prematurity – retinopathy of prematurity –deafness of prematurity

25. Conduction disturbance for those with pacemakers (15 years of age or more)

26. Bladder cancer preventive cholecystectomy

27. Gastric cancer

28. Prostate cancer

29. Adult leukaemia

30. Strabismus (under 9 years of age)

31. Diabetic retinopathy

32. Retinal detachment

33. Haemophilia

34. Depression (15 years of age or more)

35. Benign prostatic hyperplasia

36. Acute stroke

37. Chronic obstructive pulmonary disease

38. Bronchial asthma

39. Newborn respiratory distress syndrome

40. Orthesis and aids (65 years of age or more)

41. Deafness (65 years of age or more)

42. Ametropia (65 years of age or more)

43. Eye trauma

44. Cystic fibrosis

45. Severe burns

46. Alcohol and drug dependency (10 to 19 years of age)

47. Pregnancy and delivery integral care

48. Rheumatoid arthritis

49. Knee arthrosis (55 years of age or more) and hip arthrosis (60 years of age or more)

50. Intracranial aneurysm and venous malformation rupture

51. Central nervous system tumours

52. Herniated nucleus pulposus

53. Dental emergencies

54. Dental care (65 years of age or more)

55. Politrauma

56. Traumatic brain injury

57. Retinopathy of prematurity

58. Bronchopulmonary dysplasia of prematurity

59. Bilateral sensorineural hearing loss of prematurity

60. Epilepsy in patients over 15 years of age

61. Bronchial asthma in patients over 15 years of age

62. Parkinson disease

63. Juvenile idiopathic arthritis

64. Secondary prevention of chronic renal failure

65. Hip dysplasia

66. Integral oral health in pregnant women

67. Multiple sclerosis

68. Hepatitis B

69. Hepatitis C

The AUGE not only guaranteed access to treatments for these priority programmes, but it also guaranteed quality of care by explicit definition of the interventions to be provided and the treatment protocols to be used, the adoption of maximum waiting times for treatment and limits on out-of-pocket (OOP) spending for health care. The Ministry of Health and Ministry of Finance determine the content of the benefits package, taking into account the burden of disease, the share of the population suffering from the disease, the expected cost per beneficiary, the supply capacity of the health network and the effectiveness of the interventions. Since the AUGE reform, there has been a sizeable increase in total health spending from both public and private resources, but by 2013 it had stabilized at around 7.5% of gross domestic product (GDP) (Bitran, Reference Bitran2013). The financial management of the AUGE has mainly been at an aggregate level, by monitoring the average cost per beneficiary, rather than by cost–effectiveness assessments of the services provided.

As reported by Bitran (Reference Bitran2013), there have been several evaluations of the AUGE. Bitran, Escobar and Gassibe (Reference Bitrán, Escobar and Gassibe2010) assessed the impact of AUGE on access to care, treatment outcomes, hospitalization rates and medical (sick) leave rates for six chronic conditions, including hypertension, diabetes and depression. For most of these conditions the reform increased access to services, increased coverage and in some cases reduced hospital fatality rates. A study by Valdivieso and Montero (Reference Valdivieso and Montero2010) found that AUGE’s access guarantee has been a powerful instrument to improve equity in health care.

However, the consequences of AUGE for health system efficiency had not been measured by 2013, and there have been few assessments of the cost–effectiveness of individual health care interventions in Chile. Nonetheless, Bitran (Reference Bitran2013) suggested that allocative efficiency may have been improved by the selection of cost-effective treatments in AUGE’s benefits package, and that productive efficiency may have also improved through the adoption of explicit treatment protocols. However, an increased use of HTA including economic evaluation, particularly in the adoption of new treatments within AUGE, may generate further benefits. The opportunities and challenges of using economic evaluation in a LMIC are discussed in the next case study.

Example 5: Economic analysis in supporting the development of a health benefits package in Malawi

The constraints on the availability of public resources for health care in LMICs limits access to necessary services and shifts costs to patients and their households, inevitably resulting in financial hardship. Consequently, the development of HBPs is becoming increasingly frequent in these countries in relation to SDG 3.8 – UHC. Benefits packages have the potential to guide investment and strengthen weak health systems, while being mindful of budget constraints. However, the process of benefits package design in these contexts is often opaque and not informed by explicit analysis. In particular, one of the greatest limitations in the low-resource setting is that the health opportunity cost of decisions is rarely accounted for.

Ochalek and colleagues (Reference Ochalek2018) reported on the development of an analytic framework to guide resource allocation within the Malawi Health Sector Strategic Plan (HSSP) 2017–2022. The framework needed to inform the following key questions posed by the Ministry of Health.

What is the appropriate scale of the HBP?

Which interventions represent “best buys” for the health care system and should be prioritized?

Where should investments in scaling up interventions and health system strengthening be made?

Should the package be expanded to include additional interventions?

What are the costs of the conditionalities of donor funding?

How can objectives beyond improving population health be considered?

Since including an intervention in the HBP commits resources that could otherwise be used to fund alternative interventions that also improve health, it is important that the opportunity costs in foregone health care are considered. Therefore, an empirical estimate of the costs and effects of a range of health interventions was made using data from the Tufts Global Health Cost–Effectiveness Registry (Tufts Medical Center, 2021) and WHO-CHOICE analyses (Bertram et al., Reference Bertram2021). Budgetary analysis to determine the total cost of the package used drug and supply costs from a 2014 midterm review of the previous strategic plan. The size of the eligible patient populations for each intervention and an assessment of the extent to which interventions were implemented in Malawi in 2014 were obtained from data available locally.

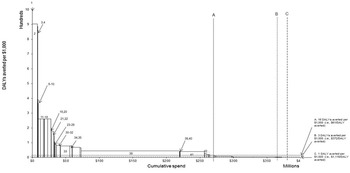

The estimates of the cost per disability-adjusted life-year (DALY) averted for interventions for which all required data were available are shown in Fig. 2.2.2, ordered from lowest to highest. The height of each bar represents the intervention’s effectiveness–cost ratio, and the width of each bar represents the intervention’s total cost. Previous research has indicated that US$ 61 spent on health care at the margin would be expected to avert one DALY (or 61 DALYs per US$ 1000). Bearing in mind a possible budgetary limit of US$ 265 million, this would imply that interventions 1–48 would be included in the benefits package (see vertical line A). Vertical lines B and C show the implication of higher budgets, representing higher willingness-to-pay thresholds per DALY-averted.

A framework can be used to help identify “best buys” and priorities for the health system given different budget thresholds

Ochalek et al. (Reference Ochalek2018) highlighted that while Fig. 2.2.2 provides a useful way to visualize the budgetary implications of using a higher or lower “threshold” value, cost per DALY-averted ratios are not useful for prioritizing interventions because they do not indicate the scale of the potential health impact. Therefore, Ochalek et al. (Reference Ochalek2018) also present data in their paper ranking interventions according to the net DALYs averted that they would achieve, assuming that they were fully implemented, or implemented to the extent they were in 2014.

These analyses were intended to provide an analytic framework for supporting the development of the benefits package, rather than prescribing decisions. Decision-makers in Malawi added other decision-making criteria (in addition to health maximization) such as equity (whether an intervention was for at risk or marginalized groups), continuum of care (where interventions are linked), complementarities (where interventions are a linked part of a given package of services), and exceptional donor-funded interventions that were expected to remain stable in the medium term.

Other issues emerged in the deliberative process. For example, some interventions that were good value for money were likely to be difficult to implement because of reluctance on the part of the population (e.g. male circumcision), or because some donors were rigid about the types of intervention they would and would not fund. There were other rigidities in the funding arrangements that made investment and disinvestment in various services difficult. Also, data limitations meant that complete evidence of cost–effectiveness and budgetary impact was not available for some services. However, the analyses performed showed that there were potentially substantial gains from investing in policies to reduce these constraints to implementation. The analytic framework developed provided a basis for conducting these debates and considering ways to improve the allocation of resources.

Policy relevance and conclusions

Key issues in setting a benefits package

The case studies presented above show that countries take very different approaches to drawing up a benefits package. Although it is acknowledged that benefits packages have the potential to strengthen health care systems and respond to population health need while controlling expenditure, the approach followed for each health care system strongly depends on cultural values, market configuration, political system, level of wealth and other determinants. Therefore, whatever system is used, it is important to gain agreement from key stakeholders (e.g. politicians and health professional groups) on the need for an explicit benefits package and on what the benefits package should seek to achieve (i.e. ensure equity, control costs).

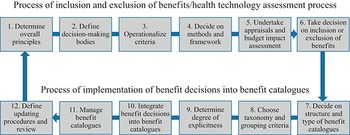

Given the various contexts, it is ambitious to draft a generic framework for setting a benefits package. Fig. 2.2.3 visualizes the core steps involved in doing so, inspired by the approach taken by Glassman et al. (Reference Glassman2016). We have extended their framework by the process of implementing benefit decisions into benefit catalogues. Thus, our framework essentially contains two processes that are linked to each other. In the first process, inclusion and exclusion of benefits are defined, while in the second process benefit decisions that result from the first process are implemented into benefit catalogues.

A generic framework for setting a benefits package will require context-specific interpretation

Figure 2.2.3 Long description

The flowchart represents a cyclic process (the last step feeds back into the first one), where steps 1 through 6 represent the Process of inclusion and exclusion of benefits or health technology assessment process, while steps 7 through 12 represent the Process of implementation of benefit decisions into benefit catalogues. The steps are as follows. 1. Determine overall principles. 2. Define decision-making bodies. 3. Operationalise criteria. 4. Decide on methods and framework. 5. Undertake appraisals and budget impact assessment. 6. Take a decision on the inclusion or exclusion of benefits. 7. Decide on structure and type of benefit catalogues. 8. Choose taxonomy and grouping criteria. 9. Determine degree of explicitness. 10. Integrate benefit decisions into benefit catalogues. 11. Manage benefit catalogues. 12. Define updating procedures and review.

The different steps of the two processes require more in-depth explanation.

1. Determine the overall principles: in the first step the guiding principles for setting a benefits package should be clearly stated by policy-makers and closely aligned with the general goals of the health care system. Typically, these principles are set by the parliament of a given country, in the context of national health service systems or SHI systems. The parliament of a given country will be held accountable to the general public for setting the package and monitoring its implementation. This may differ according to jurisdictions, but the overall principles should be rooted in broad support from the population.

2. Define decision-making bodies: responsibilities must be defined for the subsequent steps. In particular, the final decision-maker who determines the inclusion or exclusion of benefits, the structure and type of benefit catalogues, and the degree of explicitness of benefit catalogues must be defined. Decision-making bodies could either be ministries and parliaments or self-governmental institutions and committees. SHI countries have a long tradition of delegating responsibilities to self-governing institutions (e.g. in France, Germany and the Netherlands), while in national health service countries ministries and committees play an important role in this process (e.g. in Italy and United Kingdom). For example, in the case study on Italy, the Ministry designed the process and criteria for updating benefits which were then implemented by a commission.

3. Operationalize criteria: coherent with the overall principles, criteria for benefit decisions must be defined. Results of the EUHealthBasket project demonstrated that the criteria used for inclusion and exclusion of benefits varied considerably between European countries. While most countries used variations of effectiveness, cost and cost–effectiveness, Denmark used need as the central criterion and Spain used efficacy, efficiency and safety as the main criteria (Schreyögg et al., Reference Schreyögg2005). Criteria often also differ according to benefit catalogues of different sectors or different types of health technologies; for example, different criteria for pharmaceuticals than for medical devices.

4. Decide on methods and frameworks: most countries, especially HICs, use some kind of health technology framework including economic evaluation to determine the inclusion and exclusion of benefits. Although most countries in fact apply a framework with different criteria, as shown in the case studies above, not every country publishes the applied criteria in a transparent way, for example, the Netherlands (Stolk et al., Reference Stolk2009). Schreyögg et al. (Reference Schreyögg2005) found that in European countries, criteria for the inclusion in or exclusion from benefit catalogues are often fairly opaque.

5. Undertake appraisals and budget impact assessment: the formulated frameworks and criteria must be applied by a designated institution. Often, this institution is not the decision-making body, but it has the role to systematically collect evidence on (new) technologies and services as input to appraisals. This institution, often a HTA agency, may also perform a budget impact assessment to inform the decision-making body. One of the lessons from the Malawi case study above, and from attempts to use economic evaluation in the development of an HBP in the Netherlands (Stolk et al., Reference Stolk2009), is that assessments of clinical and cost–effectiveness may not be readily available for all the services or treatments in the benefit catalogue. Therefore, either substantial resources may be required, or priorities need to be set for which services to assess. Tackling this issue is likely to be the main practical challenge in setting a detailed explicit benefits package.

6. Take decisions on inclusion or exclusion of benefits: after evidence is available and synthesized for decision-makers, the defined decision-making body has to make the final decision on inclusion and exclusion of benefits. At this point, services or technologies may be included/excluded completely or partially (e.g. tied to specific conditions). For instance, in several European countries, positron emission tomography-computed tomography scans are not regularly reimbursed, but are reimbursed for specific conditions such as suspected bronchial carcinoma. Decisions in certain countries may also allow regional differentiation. For example, Spain and Italy allow regions to include additional services in their benefits packages, which are not included at national level (Torbica & Fattore, Reference Torbica and Fattore2005; Planas-Miret, Tur-Prats & Puig-Junoy, Reference Planas-Miret, Tur-Prats and Puig-Junoy2005).

A benefit catalogue may also be complemented by a negative list, explicitly listing services that are excluded from reimbursement (see Chapter 2.3). For instance, Germany uses a negative list for pharmaceuticals, clarifying that, among others, expectorants and laxatives are not reimbursable. Beyond this it may be a general principle to decide that all services can be reimbursed unless explicitly excluded; for example, in the German inpatient setting (see case study above). Finally, it is worth noting that inclusion/exclusion decisions can and should take account of considerations beyond the synthesized evidence (e.g. equity, continuity of care), consistent with the general criteria specified earlier (3. Operationalize criteria).

7. Decide on structure and type of benefit catalogues: benefit catalogues can be of very different structures and types. They may take the structure of aggregate and implicit definitions of certain service areas through reimbursement schemes (as one type of benefit catalogue); for example, the DRG system for inpatient care, often used by HICs. In contrast, LMICs often maintain detailed lists of services not indicated for reimbursement but give a guarantee that at least the listed benefits will be reimbursed if needed. For instance, in Chile, benefits are listed in the Plan AUGE as a minimum guaranteed health benefit catalogue, whereby prioritized services are made available to the entire population (Glassman et al., Reference Glassman2016; Bitran, Reference Bitran2013).

8. Choose taxonomy and grouping criteria: The decision on taxonomy and grouping criteria is relevant for further steps in the process, as it has a direct impact on the degree of explicitness and the ability to integrate new technologies at a later stage of updating. European countries use some kind of taxonomy structured along medical specialities such as DRG classifications for inpatient care, or some kind of procedure-based classification for outpatient care; for example, the Common Classification of Medical Procedures in France. Regarding grouping criteria within taxonomies, the situation is quite heterogeneous including criteria such as age, comorbidity, area of care product group and procedures (Schreyögg et al., Reference Schreyögg2005).

9. Determine degree of explicitness: the fact that HICs tend to rely on reimbursement catalogues as a substitute for benefit catalogues does not necessarily imply that benefits are defined implicitly only. The EU HealthBasket project revealed that the degree of explicitness varies substantially both between European countries and sectors of care (Schreyögg et al., Reference Schreyögg2005). While inpatient services tend to be defined rather implicitly, outpatient services are often defined with a high degree of explicitness through procedure-based reimbursement schemes. But even implicitly defined reimbursement schemes may undergo a certain evolution, as presented above in the case of inpatient care in Germany. When deciding on the degree of explicitness, decision-makers, especially in HICs, are faced with a trade-off between the advantages of an explicit definition of benefits; for example, through encouraging equitable access and the threats of explicitness; for example, through overprovision of services in FFS reimbursement schemes.

10. Integrate benefit decisions into benefit catalogues: benefit catalogues/reimbursement schemes often have a long tradition and the ways in which taxonomies and groupings are defined influence whether innovations may be more or less easily integrated into existing schemes. Therefore, countries frequently decide to add lists of explicit inclusions/exclusions of new technologies.

11. Manage benefit catalogues: once a benefit catalogue is established, the government or other decision-making units have to continuously maintain it and monitor provision or reimbursement of benefits. Among other issues, this includes communication with stakeholder groups on included and excluded services, resolving disputes, and informing price negotiations with manufacturers (Glassman et al., Reference Glassman2016).

12. Define updating procedures and review mechanisms: an often-neglected issue is the process of updating procedures. Even HICs struggle with defining terms and conditions or technologies to enter benefit catalogues. Manufacturers and providers typically demand innovation-friendly processes with low entry barriers, while governments and payers have to keep the balance between rapid access to new technologies and costs. Another important point to consider is the frequency of updates. While some countries continuously update their catalogues, others define fixed periods; for example, every year. Finally, whether the development of benefit catalogues is aligned with the overall principles and available resources of a given health care system should be regularly reviewed. This relates back to the first step of determining the overall principles. Changing those principles may require changes in both processes.

Conclusions

HBPs differ in their level of detail and explicitness. There are both advantages and disadvantages of setting an explicit package, and this is an important policy choice. For those considering setting an explicit HBP, we have outlined the key steps, illustrated by examples from high-, middle- and low-income countries with different types of health care systems. Our particular focus has been on the use of HTA and economic evaluation, as this is one of the main practical issues that must be resolved in setting an explicit HBP.Footnote 2

Open access

Open access