1. Introduction

Correlation among assets plays an important role in the financial market. Empirical evidence shows that market returns are lower when correlations among assets are increasing, since higher correlations reduce the diversification effect and increase the market volatility. Roughly stated, the correlation risk premium (CRP) is the difference between the realized and the option-implied, i.e., risk-neutral correlation.Footnote 1 The CRP can be interpreted as an insurance premium paid for assets that hedge against unanticipated rises in correlation. Academic research has provided more empirical evidence to show that the CRP in equity markets is economically and statistically significant and long-term market returns can be predicted using the option-implied correlation; see, e.g., Driessen et al. (Reference Driessen, Maenhout and Vilkov2009), Faria & Kosowski (Reference Faria and Kosowski2014), Buss et al. (Reference Buss, Schönleber and Vilkov2017), and Faria et al. (Reference Faria, Kosowski and Wang2022). In this paper, we will provide a theoretical framework that allows to better understand the CRP.

Stocks and market indices are modeled as random variables on the probability space

$\left ( \Omega, \left ( \mathcal{F}_t\right ) _{t\geq 0},\mathbb{P}\right )$

. Under the assumption of no-arbitrage, the prices of traded derivatives can be expressed as discounted expected payoffs under a risk-neutral probability measure

$\left ( \Omega, \left ( \mathcal{F}_t\right ) _{t\geq 0},\mathbb{P}\right )$

. Under the assumption of no-arbitrage, the prices of traded derivatives can be expressed as discounted expected payoffs under a risk-neutral probability measure

$\mathbb{Q}$

. Implied correlations (i.e., the correlation between assets under the risk neutral measure) can be determined from traded derivative prices, as was shown in Skintzi & Refenes (Reference Skintzi and Refenes2004). Indeed, implied correlation provides a measure of the relative cheapness/richness of index options in relation to the index components, see, e.g., Chicago Board Options Exchange (2022). It reveals in the first place information about the degree of the comovement under the probability measure

$\mathbb{Q}$

. Implied correlations (i.e., the correlation between assets under the risk neutral measure) can be determined from traded derivative prices, as was shown in Skintzi & Refenes (Reference Skintzi and Refenes2004). Indeed, implied correlation provides a measure of the relative cheapness/richness of index options in relation to the index components, see, e.g., Chicago Board Options Exchange (2022). It reveals in the first place information about the degree of the comovement under the probability measure

$\mathbb{Q}$

, see also Dhaene et al. (Reference Dhaene, Linders, Schoutens and Vyncke2012), Linders et al. (Reference Linders, Dhaene and Schoutens2015), and Madan & Schoutens (Reference Madan and Schoutens2013) for alternative implied dependence measures. The discrepancy between the realized correlation (i.e., the correlation between assets under the real-world measure

$\mathbb{Q}$

, see also Dhaene et al. (Reference Dhaene, Linders, Schoutens and Vyncke2012), Linders et al. (Reference Linders, Dhaene and Schoutens2015), and Madan & Schoutens (Reference Madan and Schoutens2013) for alternative implied dependence measures. The discrepancy between the realized correlation (i.e., the correlation between assets under the real-world measure

$\mathbb{P}$

) and the implied correlation gives rise to the existence of the CRP.

$\mathbb{P}$

) and the implied correlation gives rise to the existence of the CRP.

The increasing complexity of insurance products has introduced the need to understand the difference between implied and real-world correlation when dealing with insurance problems. Indeed, modern insurance products combine actuarial and financial risks. Therefore, their valuation and risk management rely on real-world and risk-neutral probabilities. For example, Solvency II requires that insurance companies value their liabilities in a “fair’” way, which implies that risk-neutral valuation has to be used for financial risks and real-world valuation for the actuarial risks. See, for example, Pelsser & Stadje (Reference Pelsser and Stadje2014), Ghalehjooghi & Pelsser (Reference Ghalehjooghi and Pelsser2020), Dhaene et al. (Reference Dhaene, Stassen, Barigou and Chen2017), Barigou et al. (Reference Barigou, Chen and Dhaene2019), and Linders (Reference Linders2023) for various methodologies for pricing insurance products based on combinations of real-world and risk-neutral information. Examples of complex insurance products combining financial and actuarial risks are variable annuities. In Bauer et al. (Reference Bauer, Kling and Russ2008) and Bacinello et al. (Reference Bacinello, Millossovich, Olivieri and Pitacco2011), a valuation framework for a general class of variable annuities based on risk-neutral and real-world expectations was introduced. Concrete examples are then provided in Coleman et al. (Reference Coleman, Kim, Li and Patron2007), Feng & Jing (Reference Feng and Jing2017), and MacKay et al. (Reference MacKay, Vachon and Cui2023). Therefore, understanding the difference between risk-neutral and real-world information is important when considering variable annuities.

In this paper, we consider a discrete market setting. For stochastic finance in discrete time, one can refer to Föllmer & Schied (Reference Föllmer and Schied2004). We investigate to what extent the implied correlation reveals information about the degree of the comovement under the probability measure

$\mathbb{P}$

. We illustrate how statements which hold true in the risk-neutral world do not necessarily hold in the real world. For example, stock prices can be strongly negative dependent in the risk-neutral world (under

$\mathbb{P}$

. We illustrate how statements which hold true in the risk-neutral world do not necessarily hold in the real world. For example, stock prices can be strongly negative dependent in the risk-neutral world (under

$\mathbb{Q}$

) while being positive dependent in the real world (under

$\mathbb{Q}$

) while being positive dependent in the real world (under

$\mathbb{P}$

), this leads to a large difference between the real-world and the risk-neutral correlation, which is quantified by the correlation gap. Moreover, we introduce a new derivative called dispersion swap to trade the correlation gap and demonstrate that the correlation gap does not converge to zero for market equilibrium, i.e., the realized correlation can be different with the implied correlation in the case of market equilibrium.

$\mathbb{P}$

), this leads to a large difference between the real-world and the risk-neutral correlation, which is quantified by the correlation gap. Moreover, we introduce a new derivative called dispersion swap to trade the correlation gap and demonstrate that the correlation gap does not converge to zero for market equilibrium, i.e., the realized correlation can be different with the implied correlation in the case of market equilibrium.

In Section 2, we introduce a simple discrete financial market with two traded stocks. We apply the multivariate binomial tree model for the underlying stock prices. At time

$t,$

$t,$

$t=0, 1, 2\dots, $

the price of the stock at the next valuation moment

$t=0, 1, 2\dots, $

the price of the stock at the next valuation moment

$t+1$

can only take two possible outcomes. This financial market is arbitrage-free and incomplete, we characterize the set of feasible risk-neutral probability measures and demonstrate that it is feasible to determine a risk-neutral measure

$t+1$

can only take two possible outcomes. This financial market is arbitrage-free and incomplete, we characterize the set of feasible risk-neutral probability measures and demonstrate that it is feasible to determine a risk-neutral measure

$\mathbb{Q}$

by explicitly specifying the implied correlation. Note that we limit our analysis to two stocks in the financial market. This choice is motivated by the fact that a market with two assets offers an intuitive setting for both theoretical and numerical exploration of the correlation gap.Footnote

2

$\mathbb{Q}$

by explicitly specifying the implied correlation. Note that we limit our analysis to two stocks in the financial market. This choice is motivated by the fact that a market with two assets offers an intuitive setting for both theoretical and numerical exploration of the correlation gap.Footnote

2

In Section 3, we consider the situation where a pricing measure is chosen by the market from the set of feasible risk-neutral probability measures, see Section 3.1. We show that the pricing measure chosen by the market can differ substantially from the real-world probability measure without introducing arbitrage opportunities. We give an example where the dependence structure used to price multivariate derivatives is different from the real-world dependence structure. In such a situation there can be a significantly large correlation gap in the financial market, i.e., the difference between risk-neutral and real-world correlations is substantial.

In Section 4, we consider the sale of a unit-linked insurance product to a group of

$N$

policyholders. The payoff of this unit-linked contract is contingent upon the performance of a stock market fund comprising two stocks within the financial market. We demonstrate how disparities between real-world dependence and risk-neutral dependence contribute to determining the expected excess return above the risk-free return for each policyholder. To be more specific, an example is presented in Section 4.1 to illustrate that the expected excess return for the purchase of the unit-linked insurance is determined by the correlation gap. A nonzero correlation gap leads to a nonzero expected excess return for buying the unit-linked insurance product. Therefore, policyholders of the unit-linked insurance product are also facing the correlation risk in the financial market.

$N$

policyholders. The payoff of this unit-linked contract is contingent upon the performance of a stock market fund comprising two stocks within the financial market. We demonstrate how disparities between real-world dependence and risk-neutral dependence contribute to determining the expected excess return above the risk-free return for each policyholder. To be more specific, an example is presented in Section 4.1 to illustrate that the expected excess return for the purchase of the unit-linked insurance is determined by the correlation gap. A nonzero correlation gap leads to a nonzero expected excess return for buying the unit-linked insurance product. Therefore, policyholders of the unit-linked insurance product are also facing the correlation risk in the financial market.

At first, a large correlation gap may look like a dysfunction of the financial market. However, we propose in Section 5 that, in our simple market model, one can use a new derivative, the dispersion swap, to exploit the correlation gap. This strategy is not an arbitrage strategy, but as dependence under

$\mathbb{Q}$

is moving further and further away from its

$\mathbb{Q}$

is moving further and further away from its

$\mathbb{P}$

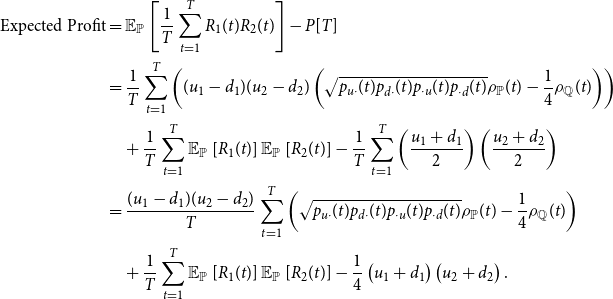

counterpart, buying the dispersion swap becomes more attractive in terms of larger expected profit. To be more precise, a large positive correlation gap, corresponding to the situation that the realized correlation is expected to exceed the implied correlation, results in a significant positive expected profit for longing the dispersion swap. Furthermore, we show how one can combine the floating leg of individual variance swaps and the floating leg of the index variance swap to approximate the floating leg of the dispersion swap, which is called the realized dispersion. The expected profit for a buyer of the dispersion swap is directly related to the correlation gap, the higher this gap, the higher the expected profit. The idea of setting up trading strategies to exploit the difference between realized and implied dependence was also discussed in Laurence (Reference Laurence2008), Laurence & Wang (Reference Laurence and Wang2008), Bossu (Reference Bossu2014), and Meissner (Reference Meissner2015).

$\mathbb{P}$

counterpart, buying the dispersion swap becomes more attractive in terms of larger expected profit. To be more precise, a large positive correlation gap, corresponding to the situation that the realized correlation is expected to exceed the implied correlation, results in a significant positive expected profit for longing the dispersion swap. Furthermore, we show how one can combine the floating leg of individual variance swaps and the floating leg of the index variance swap to approximate the floating leg of the dispersion swap, which is called the realized dispersion. The expected profit for a buyer of the dispersion swap is directly related to the correlation gap, the higher this gap, the higher the expected profit. The idea of setting up trading strategies to exploit the difference between realized and implied dependence was also discussed in Laurence (Reference Laurence2008), Laurence & Wang (Reference Laurence and Wang2008), Bossu (Reference Bossu2014), and Meissner (Reference Meissner2015).

Apart from trading the dispersion swap to make a profit, investors can also long the dispersion swap to hedge against unanticipated correlation spikes in the financial market. Because the investors may have a high degree of risk aversion towards the correlation risk, they are willing to buy the dispersion swap, even with a negative expected profit. The expected profit of a dispersion swap is also called the CRP, as it represents the price that market participants are willing to pay to sell correlation risk. On the other hand, we show that the dispersion swap with a strictly negative (or positive) expected return is not an arbitrage strategy. Therefore, we conclude in Section 6 that a market in equilibrium can accommodate a negative CRP.

2. The financial market

2.1 A discrete financial market

We consider a discrete financial market with two nondividend paying stocks over a finite time horizon. Today is time

$0$

, the price of stock

$0$

, the price of stock

$i$

$i$

$(i = 1 \text{ or } 2)$

, at the future time

$(i = 1 \text{ or } 2)$

, at the future time

$t$

(

$t$

(

$t=1,2,\ldots, n$

), is denoted by

$t=1,2,\ldots, n$

), is denoted by

$S_i(t)$

.Footnote

3

Given the price of stock

$S_i(t)$

.Footnote

3

Given the price of stock

$i$

at time

$i$

at time

$t-1$

, the future stock price at time

$t-1$

, the future stock price at time

$t$

can only increase to

$t$

can only increase to

$e^{u_{i}}S_{i}(t-1)$

or decrease to

$e^{u_{i}}S_{i}(t-1)$

or decrease to

$e^{d_{i}}S_{i}(t-1)$

. The forward return of stock

$e^{d_{i}}S_{i}(t-1)$

. The forward return of stock

$i$

at time

$i$

at time

$t$

is denoted by

$t$

is denoted by

$R_{i}(t)$

and defined as:

$R_{i}(t)$

and defined as:

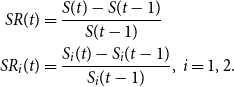

\begin{equation} R_{i}(t)=\log \frac{S_i(t)}{S_i(t-1)},\ i=1\text{ or }2\text{ and }t=1,2,\ldots, n. \end{equation}

\begin{equation} R_{i}(t)=\log \frac{S_i(t)}{S_i(t-1)},\ i=1\text{ or }2\text{ and }t=1,2,\ldots, n. \end{equation}

The financial market is also home to a bank account, which allows borrowing and lending at a constant, risk-free interest rate

$r$

. The time

$r$

. The time

$0$

value of the risk-free asset is

$0$

value of the risk-free asset is

$B(0)$

, and its time

$B(0)$

, and its time

$t$

value is given by

$t$

value is given by

$B(t) = e^{rt}B(0)$

. We assume that

$B(t) = e^{rt}B(0)$

. We assume that

$e^{u_{i}}$

and

$e^{u_{i}}$

and

$e^{d_{i}}$

are symmetric with respect to the forward rate

$e^{d_{i}}$

are symmetric with respect to the forward rate

$e^r$

:

$e^r$

:

\begin{equation} e^{u_i} - e^r = -(e^{d_i}-e^r),\text{ for }i=1,2. \end{equation}

\begin{equation} e^{u_i} - e^r = -(e^{d_i}-e^r),\text{ for }i=1,2. \end{equation}

Under the real-world probability measure

$\mathbb{P}$

, we denote the joint probabilities of the random vector

$\mathbb{P}$

, we denote the joint probabilities of the random vector

$\left ( R_{1}(t),R_{2}(t)\right )$

as follows:

$\left ( R_{1}(t),R_{2}(t)\right )$

as follows:

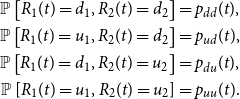

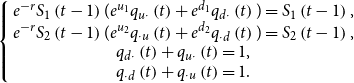

\begin{align} \mathbb{P}\left [ R_{1}(t)=d_1,R_{2}(t)=d_2 \right ] & =p_{d d}(t),\nonumber\\ \mathbb{P}\left [ R_{1}(t)=u_1,R_{2}(t)=d_2\right ] & =p_{u d}(t),\nonumber \\ \mathbb{P}\left [ R_{1}(t)=d_1,R_{2}(t)=u_2\right ] & =p_{d u}(t),\nonumber \\ \mathbb{P}\left [ R_{1}(t)=u_1,R_{2}(t)=u_2 \right ] & =p_{u u}(t). \end{align}

\begin{align} \mathbb{P}\left [ R_{1}(t)=d_1,R_{2}(t)=d_2 \right ] & =p_{d d}(t),\nonumber\\ \mathbb{P}\left [ R_{1}(t)=u_1,R_{2}(t)=d_2\right ] & =p_{u d}(t),\nonumber \\ \mathbb{P}\left [ R_{1}(t)=d_1,R_{2}(t)=u_2\right ] & =p_{d u}(t),\nonumber \\ \mathbb{P}\left [ R_{1}(t)=u_1,R_{2}(t)=u_2 \right ] & =p_{u u}(t). \end{align}

We assume that the joint probabilities under real-world measure

$\mathbb{P}$

are strictly positive. The distribution of the random vector

$\mathbb{P}$

are strictly positive. The distribution of the random vector

$\left ( R_{1}(t),R_{2}(t)\right )$

is determined by the marginal distributions of

$\left ( R_{1}(t),R_{2}(t)\right )$

is determined by the marginal distributions of

$R_{i}(t),$

and the dependence structure connecting

$R_{i}(t),$

and the dependence structure connecting

$R_{1}(t)$

and

$R_{1}(t)$

and

$R_{2}(t).$

We assume that for

$R_{2}(t).$

We assume that for

$i=1,2,$

the random variables

$i=1,2,$

the random variables

$R_{i}(1), R_{i}(2), \ldots, R_{i}\left ( n\right )$

are independent of each other. The probability of stock 1 moving up and down from

$R_{i}(1), R_{i}(2), \ldots, R_{i}\left ( n\right )$

are independent of each other. The probability of stock 1 moving up and down from

$t-1$

to

$t-1$

to

$t$

is denoted by

$t$

is denoted by

$p_{u \cdot }(t)$

and

$p_{u \cdot }(t)$

and

$p_{d \cdot }(t)$

, respectively. For stock 2, these probabilities are denoted by

$p_{d \cdot }(t)$

, respectively. For stock 2, these probabilities are denoted by

$p_{\cdot u}(t)$

and

$p_{\cdot u}(t)$

and

$p_{\cdot d}(t)$

.

$p_{\cdot d}(t)$

.

Assume the financial market is arbitrage free, hence, there exists at least one probability measure

$\mathbb{Q},$

called a risk-neutral probability measure, satisfying the following conditions:

$\mathbb{Q},$

called a risk-neutral probability measure, satisfying the following conditions:

-

1.

$\mathbb{Q}$

and

$\mathbb{P}$

are equivalent probability measures;

$\mathbb{Q}$

and

$\mathbb{P}$

are equivalent probability measures; -

2. For any traded asset, its future payoff discounted at the risk-free rate

$r$

is a martingale with respect to

$\mathbb{Q}$

:(4)

\begin{equation} \text{e}^{-r}\mathbb{E}_{\mathbb{Q}}\left [ S_{i}(t) |\mathcal{F}_{t-1}\right ] =S_{i}\left ( t-1\right ), \text{ for }i=1,2,\text{and }t=1,2,..,n. \end{equation}

If

$\mathbb{Q}$

is a probability measure satisfying the above-stated conditions, we say that it is a feasible risk-neutral probability measure. Under

$\mathbb{Q}$

is a probability measure satisfying the above-stated conditions, we say that it is a feasible risk-neutral probability measure. Under

$\mathbb{Q}$

, the joint probabilities of the random vector

$\mathbb{Q}$

, the joint probabilities of the random vector

$(R_1(t), R_2(t))$

are denoted by

$(R_1(t), R_2(t))$

are denoted by

$q_{u u}(t)$

,

$q_{u u}(t)$

,

$q_{u d}(t)$

,

$q_{u d}(t)$

,

$q_{d u}(t)$

, and

$q_{d u}(t)$

, and

$q_{d d}(t)$

. Additionally, the risk-neutral marginal probabilities in

$q_{d d}(t)$

. Additionally, the risk-neutral marginal probabilities in

$\left [t-1,t\right ]$

are denoted by

$\left [t-1,t\right ]$

are denoted by

$q_{u \cdot }\left (t \right ),q_{d \cdot }\left (t \right ),q_{\cdot u}\left (t \right )$

, and

$q_{u \cdot }\left (t \right ),q_{d \cdot }\left (t \right ),q_{\cdot u}\left (t \right )$

, and

$q_{\cdot d}\left (t \right ).$

We show in the next subsection that this simple market model is incomplete by characterizing the set of feasible risk-neutral probability measures.

$q_{\cdot d}\left (t \right ).$

We show in the next subsection that this simple market model is incomplete by characterizing the set of feasible risk-neutral probability measures.

2.2 The set of equivalent martingale measures

Let us now characterize the set of all feasible risk-neutral probability measures. This set is denoted by

$\mathcal{M}$

. Each

$\mathcal{M}$

. Each

$\mathbb{Q\in }$

$\mathbb{Q\in }$

$\mathcal{M}$

is characterized by the joint probabilities

$\mathcal{M}$

is characterized by the joint probabilities

$ q_{d d}(t)$

,

$ q_{d d}(t)$

,

$q_{u d}(t),$

$q_{u d}(t),$

$q_{d u}(t),$

$q_{d u}(t),$

$q_{u u}(t), t=1,2,\ldots, n$

. In Theorem1, we characterize the risk-neutral pricing measure

$q_{u u}(t), t=1,2,\ldots, n$

. In Theorem1, we characterize the risk-neutral pricing measure

$\mathbb{Q}$

by the correlation coefficients

$\mathbb{Q}$

by the correlation coefficients

$\rho _{\mathbb{Q}}(t)= \text{Corr}_{\mathbb{Q}}\left [ R_{1}(t), R_{2}(t) \right ]$

,

$\rho _{\mathbb{Q}}(t)= \text{Corr}_{\mathbb{Q}}\left [ R_{1}(t), R_{2}(t) \right ]$

,

$t=1,2,\dots, n$

. A proof of this Theorem can be found in Appendix A.1.

$t=1,2,\dots, n$

. A proof of this Theorem can be found in Appendix A.1.

Theorem 1.

Consider the stock price model (

3

) satisfying the conditions (

2

). The set

$\mathcal{M}$

of risk-neutral probability measures can be characterized as follows:

$\mathcal{M}$

of risk-neutral probability measures can be characterized as follows:

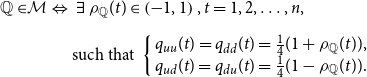

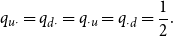

\begin{align} \mathbb{Q\in }\mathcal{M\Leftrightarrow }\text{ } & \text{ }\exists \text{ }\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right ), t=1,2,\ldots, n,\nonumber \\[5pt] & \text{such that }\left \{ \begin{array} [l]{l}q_{u u}(t)=q_{d d}(t) =\frac{1}{4}(1+\rho _{\mathbb{Q}}(t)),\\ q_{u d}(t)=q_{d u}(t) =\frac{1}{4}(1-\rho _{\mathbb{Q}}(t)). \end{array} \right . \end{align}

\begin{align} \mathbb{Q\in }\mathcal{M\Leftrightarrow }\text{ } & \text{ }\exists \text{ }\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right ), t=1,2,\ldots, n,\nonumber \\[5pt] & \text{such that }\left \{ \begin{array} [l]{l}q_{u u}(t)=q_{d d}(t) =\frac{1}{4}(1+\rho _{\mathbb{Q}}(t)),\\ q_{u d}(t)=q_{d u}(t) =\frac{1}{4}(1-\rho _{\mathbb{Q}}(t)). \end{array} \right . \end{align}

The risk-neutral measure

$\mathbb{Q}$

is not unique and the market is incomplete. It is clear to see from Theorem1 that the risk-neutral marginal probabilities are all equal to

$\mathbb{Q}$

is not unique and the market is incomplete. It is clear to see from Theorem1 that the risk-neutral marginal probabilities are all equal to

$\frac{1}{2}$

. Note, however, that our model can be generalized to situations where the marginal risk neutral probabilities are different from

$\frac{1}{2}$

. Note, however, that our model can be generalized to situations where the marginal risk neutral probabilities are different from

$\frac{1}{2}$

. Specifying a feasible risk-neutral measure

$\frac{1}{2}$

. Specifying a feasible risk-neutral measure

$\mathbb{Q}$

under the stock price model (3), requires specifying the correlation efficient

$\mathbb{Q}$

under the stock price model (3), requires specifying the correlation efficient

$\rho _{\mathbb{Q}}(t),t=1,2,\ldots, n.$

Each risk-neutral probability measure

$\rho _{\mathbb{Q}}(t),t=1,2,\ldots, n.$

Each risk-neutral probability measure

$\mathbb{Q}$

in

$\mathbb{Q}$

in

$\mathcal{M}$

has the same marginal distributions but different dependence structures. For instance, take

$\mathcal{M}$

has the same marginal distributions but different dependence structures. For instance, take

$\rho _{\mathbb{Q}}(t)\equiv 0$

, then we find the risk-neutral measure

$\rho _{\mathbb{Q}}(t)\equiv 0$

, then we find the risk-neutral measure

$\mathbb{Q}^{\perp }\in \mathcal{M}$

where the marginals are independent.

$\mathbb{Q}^{\perp }\in \mathcal{M}$

where the marginals are independent.

The situations characterized by the minimal correlation coefficient

$\rho _{\mathbb{Q}^{\min }}(t)\equiv -1$

and the maximal correlation coefficient

$\rho _{\mathbb{Q}^{\min }}(t)\equiv -1$

and the maximal correlation coefficient

$\rho _{\mathbb{Q}^{\max }}(t)\equiv 1$

correspond with the probability measure

$\rho _{\mathbb{Q}^{\max }}(t)\equiv 1$

correspond with the probability measure

$\mathbb{Q}^{\min }$

and the probability measure

$\mathbb{Q}^{\min }$

and the probability measure

$\mathbb{Q}^{\max },$

respectively. The random vector

$\mathbb{Q}^{\max },$

respectively. The random vector

$\left (R_1(t), R_2(t)\right )$

under the probability measure

$\left (R_1(t), R_2(t)\right )$

under the probability measure

$\mathbb{Q}^{\min }$

is counter-monotonic. In this situation, the components of the random vectors are maximum negative dependent. Inversely, the random vector

$\mathbb{Q}^{\min }$

is counter-monotonic. In this situation, the components of the random vectors are maximum negative dependent. Inversely, the random vector

$\left (R_1(t), R_2(t)\right )$

under the probability measure

$\left (R_1(t), R_2(t)\right )$

under the probability measure

$\mathbb{Q}^{\max }$

is comonotonic and the components of the random vector are maximum positive dependent.

$\mathbb{Q}^{\max }$

is comonotonic and the components of the random vector are maximum positive dependent.

The real-world joint probabilities are assumed to be strictly positive, hence all the risk-neutral probabilities specified by (5) are strictly positive. Using (5), we can directly find that for each

$\mathbb{Q} \in \mathcal{M},$

$\mathbb{Q} \in \mathcal{M},$

$\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right )$

, which means that the comonotonic and the counter-monotonic cases are not reachable in

$\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right )$

, which means that the comonotonic and the counter-monotonic cases are not reachable in

$\mathcal{M}$

. The larger

$\mathcal{M}$

. The larger

$\rho _{\mathbb{Q}}(t)$

, the “closer” the risk-neutral probability measure

$\rho _{\mathbb{Q}}(t)$

, the “closer” the risk-neutral probability measure

$\mathbb{Q}$

is to the maximum measure

$\mathbb{Q}$

is to the maximum measure

$\mathbb{Q}^{\max }$

.

$\mathbb{Q}^{\max }$

.

The set

$\mathcal{M}$

contains a wide range of dependence structures. Each element

$\mathcal{M}$

contains a wide range of dependence structures. Each element

$\mathbb{Q}$

in the set

$\mathbb{Q}$

in the set

$\mathcal{M}$

of risk-neutral probability measures can be expressed as a linear combination of

$\mathcal{M}$

of risk-neutral probability measures can be expressed as a linear combination of

$\mathbb{Q}^{\min }$

and

$\mathbb{Q}^{\min }$

and

$\mathbb{Q}^{\max }$

:

$\mathbb{Q}^{\max }$

:

\begin{equation} \mathbb{Q\in }\mathcal{M\Leftrightarrow }\text{ }\text{ }\exists \text{ }\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right ) \text{ such that }\mathbb{Q=}\text{ }\frac{\left ({ 1\mathbb{-}\rho _{\mathbb{Q}}(t)}\right )}{2} \mathbb{Q}^{\min }+\frac{\left ({ 1\mathbb{+}\rho _{\mathbb{Q}}(t)}\right )}{2}\mathbb{Q}^{\max }. \end{equation}

\begin{equation} \mathbb{Q\in }\mathcal{M\Leftrightarrow }\text{ }\text{ }\exists \text{ }\rho _{\mathbb{Q}}(t)\in \left ( -1,1\right ) \text{ such that }\mathbb{Q=}\text{ }\frac{\left ({ 1\mathbb{-}\rho _{\mathbb{Q}}(t)}\right )}{2} \mathbb{Q}^{\min }+\frac{\left ({ 1\mathbb{+}\rho _{\mathbb{Q}}(t)}\right )}{2}\mathbb{Q}^{\max }. \end{equation}

By increasing the correlation coefficient

$\rho _{\mathbb{Q}}(t),$

we can gradually increase the dependence of the components

$\rho _{\mathbb{Q}}(t),$

we can gradually increase the dependence of the components

$R_{1}(t)$

and

$R_{1}(t)$

and

$R_{2}\left (t\right ).$

$R_{2}\left (t\right ).$

It directly follows from (5) that the joint risk-neutral cdf

$F_t^{\mathbb{Q}}$

of the forward return vector

$F_t^{\mathbb{Q}}$

of the forward return vector

$(R_1(t),R_2(t))$

can be given by:

$(R_1(t),R_2(t))$

can be given by:

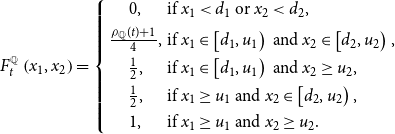

\begin{equation} F_{t}^{_{\mathbb{Q}}}\left ( x_{1},x_{2}\right ) =\left \{ \begin{array}[c]{cl} 0, & \text{if }x_{1}\lt d_1\text{ or }x_{2}\lt d_2,\\[4pt] \frac{\rho _{\mathbb{Q}}(t)+1}{4}, & \text{if }x_{1}\in \left [ d_1,u_1\right ) \text{ and }x_{2}\in \left [d_2,u_2\right ), \\[4pt] \frac{1}{2}, & \text{if }x_{1}\in \left [ d_1,u_1\right ) \text{ and }x_{2}\geq u_2,\\[4pt] \frac{1}{2}, & \text{if }x_{1}\geq u_1\text{ and }x_{2}\in \left [ d_2,u_2\right ), \\[4pt] 1, & \text{if }x_{1}\geq u_1\text{ and }x_{2}\geq u_2.\end{array} \right . \end{equation}

\begin{equation} F_{t}^{_{\mathbb{Q}}}\left ( x_{1},x_{2}\right ) =\left \{ \begin{array}[c]{cl} 0, & \text{if }x_{1}\lt d_1\text{ or }x_{2}\lt d_2,\\[4pt] \frac{\rho _{\mathbb{Q}}(t)+1}{4}, & \text{if }x_{1}\in \left [ d_1,u_1\right ) \text{ and }x_{2}\in \left [d_2,u_2\right ), \\[4pt] \frac{1}{2}, & \text{if }x_{1}\in \left [ d_1,u_1\right ) \text{ and }x_{2}\geq u_2,\\[4pt] \frac{1}{2}, & \text{if }x_{1}\geq u_1\text{ and }x_{2}\in \left [ d_2,u_2\right ), \\[4pt] 1, & \text{if }x_{1}\geq u_1\text{ and }x_{2}\geq u_2.\end{array} \right . \end{equation}

It follows from (7) that the joint risk-neutral cdf of forward return

$F_t^{\mathbb{Q}}(x_1, x_2)$

can be unambiguously determined by the correlation coefficient

$F_t^{\mathbb{Q}}(x_1, x_2)$

can be unambiguously determined by the correlation coefficient

$\rho _{\mathbb{Q}}(t)$

.

$\rho _{\mathbb{Q}}(t)$

.

2.3 Comparing different risk-neutral measures

The set

$\mathcal{M}$

contains different risk-neutral measures such that the marginals

$\mathcal{M}$

contains different risk-neutral measures such that the marginals

$R_1$

and

$R_1$

and

$R_2$

are always the same. Therefore, the difference between multivariate risk-neutral measures is in dependence structure. To compare different probability measures in

$R_2$

are always the same. Therefore, the difference between multivariate risk-neutral measures is in dependence structure. To compare different probability measures in

$\mathcal{M}$

and identify under which one the dependence is stronger or weaker, we can use multivariate stochastic orders. The notion of multivariate stochastic orders in actuarial science goes back to Yanagimoto & Okamoto (Reference Yanagimoto and Okamoto1969).

$\mathcal{M}$

and identify under which one the dependence is stronger or weaker, we can use multivariate stochastic orders. The notion of multivariate stochastic orders in actuarial science goes back to Yanagimoto & Okamoto (Reference Yanagimoto and Okamoto1969).

We first introduce the Positive Quadrant Dependence and the Negative Quadrant Dependence. The notions of PQD and NQD were introduced in Lehmann (Reference Lehmann1966).

Definition 2 (Quadrant Dependence). The random vector

$\left ( R_{1}(t),R_{2}(t)\right )$

is said to be Positive Quadrant Dependent under the probability measure

$\left ( R_{1}(t),R_{2}(t)\right )$

is said to be Positive Quadrant Dependent under the probability measure

$\mathbb{Q},$

notation

$\mathbb{Q},$

notation

$(R_1(t), R_2(t))\sim \mathbb{Q}$

-PQD, in case the vector

$(R_1(t), R_2(t))\sim \mathbb{Q}$

-PQD, in case the vector

$\left ( R_{1}(t),R_{2}(t)\right )$

satisfies:

$\left ( R_{1}(t),R_{2}(t)\right )$

satisfies:

\begin{equation*} \mathbb {Q}\left [ R_{1}(t)\leq x_{1}\right ] \mathbb {Q}\left [ R_{2}(t)\leq x_{2}\right ] \leq F_{t}^{_{\mathbb {Q}}}\left ( x_{1},x_{2}\right ), \,\text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb {R}^{2}. \end{equation*}

\begin{equation*} \mathbb {Q}\left [ R_{1}(t)\leq x_{1}\right ] \mathbb {Q}\left [ R_{2}(t)\leq x_{2}\right ] \leq F_{t}^{_{\mathbb {Q}}}\left ( x_{1},x_{2}\right ), \,\text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb {R}^{2}. \end{equation*}

The vector

$\left ( R_{1}(t),R_{2}(t)\right )$

is said to be Negative Quadrant Dependent under the probability measure

$\left ( R_{1}(t),R_{2}(t)\right )$

is said to be Negative Quadrant Dependent under the probability measure

$\mathbb{Q},$

notation

$\mathbb{Q},$

notation

$\mathbb{Q}$

-NQD, in case the vector satisfies:

$\mathbb{Q}$

-NQD, in case the vector satisfies:

\begin{equation*} \mathbb {Q}\left [ R_{1}(t)\leq x_{1}\right ] \mathbb {Q}\left [ R_{2}(t)\leq x_{2}\right ] \geq F_{t}^{_{\mathbb {Q}}}\left ( x_{1},x_{2}\right ), \,\text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb {R}^{2}, \end{equation*}

\begin{equation*} \mathbb {Q}\left [ R_{1}(t)\leq x_{1}\right ] \mathbb {Q}\left [ R_{2}(t)\leq x_{2}\right ] \geq F_{t}^{_{\mathbb {Q}}}\left ( x_{1},x_{2}\right ), \,\text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb {R}^{2}, \end{equation*}

where

$F_{t}^{_{\mathbb{Q}}}$

is the joint cdf of

$F_{t}^{_{\mathbb{Q}}}$

is the joint cdf of

$\left ( R_{1}(t),R_{2}(t)\right )$

under the probability measure

$\left ( R_{1}(t),R_{2}(t)\right )$

under the probability measure

$\mathbb{Q}$

.

$\mathbb{Q}$

.

Using Expression (7) for

$F_{t}^{_{\mathbb{Q}}}$

results in the following implications:

$F_{t}^{_{\mathbb{Q}}}$

results in the following implications:

\begin{align} \rho _{\mathbb{Q}}(t) & \geq 0\Longleftrightarrow \rho _{\mathbb{Q}}(t)\geq \rho _{\mathbb{Q}^{\perp }}(t)\Longleftrightarrow \left ( R_{1}(t),R_{2}(t)\right ) \text{ is }\mathbb{Q}\text{-PQD,} \\ \rho _{\mathbb{Q}}(t) & \leq 0\Longleftrightarrow \rho _{\mathbb{Q}}(t)\leq \rho _{\mathbb{Q}^{\perp }}(t)\Longleftrightarrow \left ( R_{1}(t),R_{2}(t)\right ) \text{ is }\mathbb{Q}\text{-NQD,}\nonumber \end{align}

\begin{align} \rho _{\mathbb{Q}}(t) & \geq 0\Longleftrightarrow \rho _{\mathbb{Q}}(t)\geq \rho _{\mathbb{Q}^{\perp }}(t)\Longleftrightarrow \left ( R_{1}(t),R_{2}(t)\right ) \text{ is }\mathbb{Q}\text{-PQD,} \\ \rho _{\mathbb{Q}}(t) & \leq 0\Longleftrightarrow \rho _{\mathbb{Q}}(t)\leq \rho _{\mathbb{Q}^{\perp }}(t)\Longleftrightarrow \left ( R_{1}(t),R_{2}(t)\right ) \text{ is }\mathbb{Q}\text{-NQD,}\nonumber \end{align}

where

$\rho _{\mathbb{Q}^{\perp }}(t)$

is the correlation of the independent copy of the random vector

$\rho _{\mathbb{Q}^{\perp }}(t)$

is the correlation of the independent copy of the random vector

$\left ( R_{1}(t),R_{2}(t) \right )$

, it is straightforward to show that

$\left ( R_{1}(t),R_{2}(t) \right )$

, it is straightforward to show that

$\rho _{\mathbb{Q}^{\perp }}(t)$

equals

$\rho _{\mathbb{Q}^{\perp }}(t)$

equals

$0$

. Using the notion of quadrant dependence, we can measure the joint behavior of two random variables. If the risk-neutral correlation

$0$

. Using the notion of quadrant dependence, we can measure the joint behavior of two random variables. If the risk-neutral correlation

$\rho _{\mathbb{Q}}(t)$

is larger than

$\rho _{\mathbb{Q}}(t)$

is larger than

$0$

, then the random vector

$0$

, then the random vector

$\left (R_{1}(t),R_{2}(t)\right )$

is

$\left (R_{1}(t),R_{2}(t)\right )$

is

$\mathbb{Q}\text{-PQD,}$

which means that the two random variables

$\mathbb{Q}\text{-PQD,}$

which means that the two random variables

$R_{1}(t)$

and

$R_{1}(t)$

and

$R_{2}(t)$

are likely to assume small or large values simultaneously. Conversely, if

$R_{2}(t)$

are likely to assume small or large values simultaneously. Conversely, if

$\rho _{\mathbb{Q}}(t)$

is less than

$\rho _{\mathbb{Q}}(t)$

is less than

$0$

, the random vector is

$0$

, the random vector is

$\mathbb{Q}\text{-NQD,}$

implying an inverse relationship where

$\mathbb{Q}\text{-NQD,}$

implying an inverse relationship where

$R_{1}(t)$

and

$R_{1}(t)$

and

$R_{2}(t)$

may move in different directions.

$R_{2}(t)$

may move in different directions.

The concept of quadrant dependence measures the association between two random variables. However, under different risk-neutral measures

$\mathbb{Q}^{(1)}$

and

$\mathbb{Q}^{(1)}$

and

$\mathbb{Q}^{(2)}$

, the marginals and quadrant dependence of the random vector

$\mathbb{Q}^{(2)}$

, the marginals and quadrant dependence of the random vector

$(R_1(t), R_2(t))$

may be identical. To distinguish the difference under such two different risk-neutral measures, we can use the correlation order introduced in Dhaene & Goovaerts (Reference Dhaene and Goovaerts1996), since the joint distribution of

$(R_1(t), R_2(t))$

may be identical. To distinguish the difference under such two different risk-neutral measures, we can use the correlation order introduced in Dhaene & Goovaerts (Reference Dhaene and Goovaerts1996), since the joint distribution of

$(R_1(t), R_2(t))$

is different when using two different risk-neutral measures.

$(R_1(t), R_2(t))$

is different when using two different risk-neutral measures.

Definition 3 (Correlation order). Consider the risk-neutral probability measures

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(2) }$

with correlation parameters

$\mathbb{Q}^{(2) }$

with correlation parameters

$\rho _{\mathbb{Q}^{(1) }}(t)$

and

$\rho _{\mathbb{Q}^{(1) }}(t)$

and

$\rho _{\mathbb{Q}^{(2) }}(t)$

, respectively. We say that the cdf’s

$\rho _{\mathbb{Q}^{(2) }}(t)$

, respectively. We say that the cdf’s

$F_{t}^{_{\mathbb{Q}^{(1) }}}$

and

$F_{t}^{_{\mathbb{Q}^{(1) }}}$

and

$F_{t}^{_{\mathbb{Q}^{(2) }}}$

are ordered in the correlation order, notation

$F_{t}^{_{\mathbb{Q}^{(2) }}}$

are ordered in the correlation order, notation

$F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}$

if the following holds:

$F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}$

if the following holds:

\begin{equation} F_{t}^{_{\mathbb{Q}^{(1) }}}\left ( x_{1},x_{2}\right ) \leq F_{t}^{_{\mathbb{Q}^{(2) }}}\left ( x_{1},x_{2}\right ), \text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb{R}^{2}. \end{equation}

\begin{equation} F_{t}^{_{\mathbb{Q}^{(1) }}}\left ( x_{1},x_{2}\right ) \leq F_{t}^{_{\mathbb{Q}^{(2) }}}\left ( x_{1},x_{2}\right ), \text{ for all }\left ( x_{1},x_{2}\right ) \in \mathbb{R}^{2}. \end{equation}

Intuitively, the inequality

$F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}$

implies that the two stock prices in

$F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}$

implies that the two stock prices in

$[t-1,t]$

move stronger together under the probability measure

$[t-1,t]$

move stronger together under the probability measure

$\mathbb{Q}^{(2) }$

than under the probability measure

$\mathbb{Q}^{(2) }$

than under the probability measure

$\mathbb{Q}^{(1) }$

, i.e., the probability of having simultaneously large/small realizations in

$\mathbb{Q}^{(1) }$

, i.e., the probability of having simultaneously large/small realizations in

$[t-1,t]$

is larger under

$[t-1,t]$

is larger under

$\mathbb{Q}^{\left ( 2\right ) }$

, compared to

$\mathbb{Q}^{\left ( 2\right ) }$

, compared to

$\mathbb{Q}^{(1) }$

. Moreover, comparing the correlations

$\mathbb{Q}^{(1) }$

. Moreover, comparing the correlations

$\rho _{{\mathbb{Q}^{(1) }}}(t)$

and

$\rho _{{\mathbb{Q}^{(1) }}}(t)$

and

$\rho _{{\mathbb{Q}^{(2)}}} (t)$

gives information about the correlation order between the probability measures

$\rho _{{\mathbb{Q}^{(2)}}} (t)$

gives information about the correlation order between the probability measures

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(2) }.$

Indeed, it follows directly from Expression (7) that the following equivalence relation holds:

$\mathbb{Q}^{(2) }.$

Indeed, it follows directly from Expression (7) that the following equivalence relation holds:

\begin{equation} \rho _{_{\mathbb{Q}^{(1) }}}(t)\leq \rho _{_{\mathbb{Q}^{(2) }}}(t)\iff F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}. \end{equation}

\begin{equation} \rho _{_{\mathbb{Q}^{(1) }}}(t)\leq \rho _{_{\mathbb{Q}^{(2) }}}(t)\iff F_{t}^{_{\mathbb{Q}^{(1) }}}\preceq _{\text{Corr}}F_{t}^{_{\mathbb{Q}^{(2) }}}. \end{equation}

There are infinitely many risk-neutral probability measures and each risk-neutral measure models the stock prices using a different dependence structure. If a contingent claim has to be priced, the market will pick a suitable pricing measure.

3. Real world vs risk-neutral measures

Section 2 shows that the market is incomplete and a whole set of risk-neutral measures exists. Market prices are determined by supply and demand, and we assume they do not allow for arbitrage. We also assume that sufficiently many derivatives are traded and these prices are publicly available. All market participants can observe these prices. Having these prices at our disposal allows to back out the choice of the market concerning the risk-neutral measure.

If we can obtain the risk-neutral pricing measure used to price traded derivatives, we can back out the view of the market about future dependencies between the stock prices. However, the market can choose from a wide range of possibilities for

$\rho _{\mathbb{Q}}(t)$

and our results show that there is, mathematically, no reason why the market should take

$\rho _{\mathbb{Q}}(t)$

and our results show that there is, mathematically, no reason why the market should take

$\mathbb{Q}$

such that

$\mathbb{Q}$

such that

$\rho _{\mathbb{Q}}(t)$

is close to the real-world correlation

$\rho _{\mathbb{Q}}(t)$

is close to the real-world correlation

$\rho _{\mathbb{P}}(t)$

for all

$\rho _{\mathbb{P}}(t)$

for all

$t$

.

$t$

.

3.1 A market with a combined asset

From Theorem1, the spot price of stock

$i$

and its potential outcomes

$i$

and its potential outcomes

$d_{i}$

and

$d_{i}$

and

$u_{i}$

, fully specify the distribution of

$u_{i}$

, fully specify the distribution of

$R_i$

. However, individual derivatives written on each stock do not give additional information about the joint distributions. To determine the multivariate distribution, a combined asset and derivative prices on this combined asset are necessary.

$R_i$

. However, individual derivatives written on each stock do not give additional information about the joint distributions. To determine the multivariate distribution, a combined asset and derivative prices on this combined asset are necessary.

Consider the market described above, but now also assume that a stock market index is traded. Its price at time

$0$

is denoted by

$0$

is denoted by

$S(0)$

and its price at time

$S(0)$

and its price at time

$t$

is denoted by

$t$

is denoted by

$S(t)$

:

$S(t)$

:

\begin{equation} S(t)=S_{1}(t)+S_{2}(t),\text{ for }t=0,1,2,\ldots, n. \end{equation}

\begin{equation} S(t)=S_{1}(t)+S_{2}(t),\text{ for }t=0,1,2,\ldots, n. \end{equation}

We have that

$\mathbb{E}_{\mathbb{Q}}\left [ S(t)\right ] =\mathbb{E}_{\mathbb{Q}}\left [ S_{1}(t)+S_{2}(t)\right ] =$

e

$\mathbb{E}_{\mathbb{Q}}\left [ S(t)\right ] =\mathbb{E}_{\mathbb{Q}}\left [ S_{1}(t)+S_{2}(t)\right ] =$

e

$^{rt}S\left ( 0\right ).$

The forward return of the stock market index at time

$^{rt}S\left ( 0\right ).$

The forward return of the stock market index at time

$t$

is denoted by

$t$

is denoted by

$R(t)$

and defined as follows:

$R(t)$

and defined as follows:

\begin{equation} R(t) = \log \frac{S(t)}{S(t-1)},\text{ for }t=1,2,\ldots, n. \end{equation}

\begin{equation} R(t) = \log \frac{S(t)}{S(t-1)},\text{ for }t=1,2,\ldots, n. \end{equation}

Call options on the index with maturity

$T=1,2,\ldots, n$

are also traded. The payoff of an index call option is given by

$T=1,2,\ldots, n$

are also traded. The payoff of an index call option is given by

$\left ( S\left ( T\right ) -K\right ) _{+}\,$

where

$\left ( S\left ( T\right ) -K\right ) _{+}\,$

where

$\left (x\right ) _{+}=\max \left \{x,0\right \}$

. The price of an index call with maturity

$\left (x\right ) _{+}=\max \left \{x,0\right \}$

. The price of an index call with maturity

$T$

and strike

$T$

and strike

$K$

is then denoted by

$K$

is then denoted by

$C_{\mathbb{Q}}\left [ K,T\right ]$

and can be expressed as follows:

$C_{\mathbb{Q}}\left [ K,T\right ]$

and can be expressed as follows:

\begin{equation*} C_{\mathbb {Q}}\left [ K,T\right ] =\text {e}^{-rT}\mathbb {E}_{\mathbb {Q}}\left [ \left ( S(T)-K\right ) _{+}\right ] . \end{equation*}

\begin{equation*} C_{\mathbb {Q}}\left [ K,T\right ] =\text {e}^{-rT}\mathbb {E}_{\mathbb {Q}}\left [ \left ( S(T)-K\right ) _{+}\right ] . \end{equation*}

The cumulative distribution function of the random variable

$S\left ( T\right )$

under the risk-neutral measure

$S\left ( T\right )$

under the risk-neutral measure

$\mathbb{Q}$

is denoted by

$\mathbb{Q}$

is denoted by

$F_{S\left ( T\right ) }^{\mathbb{Q}}$

. We introduce the stop-loss order between two risk-neutral probability measures in terms of their call option curves.

$F_{S\left ( T\right ) }^{\mathbb{Q}}$

. We introduce the stop-loss order between two risk-neutral probability measures in terms of their call option curves.

Definition 4 (Stop-loss order). Consider the stock price model described in (

3

) satisfying the conditions (

2

) and the stock market index defined in (

11

). Consider the risk-neutral probability measures

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(1) }$

and

$\mathbb{Q}^{(2) }$

. We say that

$\mathbb{Q}^{(2) }$

. We say that

$F_{S\left ( T\right ) }^{\mathbb{Q}^{(1) }}$

and

$F_{S\left ( T\right ) }^{\mathbb{Q}^{(1) }}$

and

$F_{S\left ( T\right ) }^{\mathbb{Q}^{(2) }}$

are ordered in the stop-loss order, notation

$F_{S\left ( T\right ) }^{\mathbb{Q}^{(2) }}$

are ordered in the stop-loss order, notation

$F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 1\right ) }}\preceq _{\text{sl}}F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 2\right ) }}$

if:

$F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 1\right ) }}\preceq _{\text{sl}}F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 2\right ) }}$

if:

\begin{equation} C_{\mathbb{Q}^{(1) }}\left [ K,T\right ] \leq C_{\mathbb{Q}^{(2) }}\left [ K,T\right ] \text{ for all }K\geq 0. \end{equation}

\begin{equation} C_{\mathbb{Q}^{(1) }}\left [ K,T\right ] \leq C_{\mathbb{Q}^{(2) }}\left [ K,T\right ] \text{ for all }K\geq 0. \end{equation}

Intuitively, the stop-loss order relation

$F_{S\left ( T\right )}^{\mathbb{Q}^{\left ( 1\right ) }}\preceq _{\text{sl}}F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 2\right ) }}$

implies that the stock market index

$F_{S\left ( T\right )}^{\mathbb{Q}^{\left ( 1\right ) }}\preceq _{\text{sl}}F_{S\left ( T\right ) }^{\mathbb{Q}^{\left ( 2\right ) }}$

implies that the stock market index

$S\left ( T\right )$

is more volatile under the pricing measure

$S\left ( T\right )$

is more volatile under the pricing measure

$\mathbb{Q}^{(2) }$

than under the pricing measure

$\mathbb{Q}^{(2) }$

than under the pricing measure

$\mathbb{Q}^{(1) }.$

Indeed, one can prove the following implication:

$\mathbb{Q}^{(1) }.$

Indeed, one can prove the following implication:

\begin{equation*} F_{S\left ( T\right ) }^{\mathbb {Q}^{(1) }}\preceq _{\text {sl}}F_{S\left ( T\right ) }^{\mathbb {Q}^{(2) }}\Longrightarrow \text {Var}_{\mathbb {Q}^{(1) }}\left [ S\left ( T\right ) \right ] \leq \text {Var}_{\mathbb {Q}^{(2) }}\left [ S\left ( T\right ) \right ] . \end{equation*}

\begin{equation*} F_{S\left ( T\right ) }^{\mathbb {Q}^{(1) }}\preceq _{\text {sl}}F_{S\left ( T\right ) }^{\mathbb {Q}^{(2) }}\Longrightarrow \text {Var}_{\mathbb {Q}^{(1) }}\left [ S\left ( T\right ) \right ] \leq \text {Var}_{\mathbb {Q}^{(2) }}\left [ S\left ( T\right ) \right ] . \end{equation*}

Therefore, call options are more expensive under the measure

$\mathbb{Q}^{\left ( 2\right ) }$

than under

$\mathbb{Q}^{\left ( 2\right ) }$

than under

$\mathbb{Q}^{\left ( 1\right ) }.$

The following theorem shows that the correlation

$\mathbb{Q}^{\left ( 1\right ) }.$

The following theorem shows that the correlation

$\rho _{\mathbb{Q}}\left ( 1\right )$

determines the variability of the stock market index

$\rho _{\mathbb{Q}}\left ( 1\right )$

determines the variability of the stock market index

$S\left ( 1\right ) .$

$S\left ( 1\right ) .$

Theorem 5. Consider the stock price model described in ( 3 ) satisfying the conditions ( 2 ) and the stock market index defined in ( 11 ). Then, the following equivalence relation holds:

\begin{equation*} \rho _{_{\mathbb {Q}^{(1) }}}(1)\leq \rho _{_{\mathbb {Q}^{(2) }}}(1)\iff F_1^{\mathbb {Q}^{(1)}} \preceq _{\text {Corr}} F_1^{\mathbb {Q}^{(2)}}\iff F_{S(1) }^{\mathbb {Q}^{\left ( 1\right ) }}\preceq _{\text {sl}}F_{S(1) }^{\mathbb {Q}^{\left ( 2\right ) }}. \end{equation*}

\begin{equation*} \rho _{_{\mathbb {Q}^{(1) }}}(1)\leq \rho _{_{\mathbb {Q}^{(2) }}}(1)\iff F_1^{\mathbb {Q}^{(1)}} \preceq _{\text {Corr}} F_1^{\mathbb {Q}^{(2)}}\iff F_{S(1) }^{\mathbb {Q}^{\left ( 1\right ) }}\preceq _{\text {sl}}F_{S(1) }^{\mathbb {Q}^{\left ( 2\right ) }}. \end{equation*}

Proof.

From (10), we find that

$\rho _{_{\mathbb{Q}^{(1) }}}(1)\leq \rho _{_{\mathbb{Q}^{(2) }}}(1)\iff F_1^{\mathbb{Q}^{(1)}} \preceq _{\text{Corr}} F_1^{\mathbb{Q}^{(2)}}$

. The call option price

$\rho _{_{\mathbb{Q}^{(1) }}}(1)\leq \rho _{_{\mathbb{Q}^{(2) }}}(1)\iff F_1^{\mathbb{Q}^{(1)}} \preceq _{\text{Corr}} F_1^{\mathbb{Q}^{(2)}}$

. The call option price

$C_{\mathbb{Q}}\left [ K,1\right ]$

can be expressed as follows:

$C_{\mathbb{Q}}\left [ K,1\right ]$

can be expressed as follows:

\begin{equation} C_{\mathbb{Q}}\left [ K,1\right ] =\text{e}^{-r}\left ( \frac{1}{4}\left ( P_{1}+P_{2}+P_{3}+P_{4}\right ) +\left ( P_{1}-P_{2}-P_{3}+P_{4}\right ) \frac{\rho _{\mathbb{Q}} \left ( 1 \right )}{4}\right ), \end{equation}

\begin{equation} C_{\mathbb{Q}}\left [ K,1\right ] =\text{e}^{-r}\left ( \frac{1}{4}\left ( P_{1}+P_{2}+P_{3}+P_{4}\right ) +\left ( P_{1}-P_{2}-P_{3}+P_{4}\right ) \frac{\rho _{\mathbb{Q}} \left ( 1 \right )}{4}\right ), \end{equation}

where,

\begin{align*} P_{1} & =\left ( S_{1}\left ( 0\right ) e^{u_{1}}+S_{2}\left ( 0\right ) e^{u_{2}}-K\right ) _{+};\, P_{2}=\left ( S_{1}\left ( 0\right ) e^{u_{1}}+S_{2}\left ( 0\right ) e^{d_{2}}-K\right ) _{+};\\ P_{3} & =\left ( S_{1}\left ( 0\right ) e^{d_{1}}+S_{2}\left ( 0\right ) e^{u_{2}}-K\right ) _{+};\, P_{4}=\left ( S_{1}\left ( 0\right ) e^{d_{1}}+S_{2}\left ( 0\right ) e^{d_{2}}-K\right ) _{+}. \end{align*}

\begin{align*} P_{1} & =\left ( S_{1}\left ( 0\right ) e^{u_{1}}+S_{2}\left ( 0\right ) e^{u_{2}}-K\right ) _{+};\, P_{2}=\left ( S_{1}\left ( 0\right ) e^{u_{1}}+S_{2}\left ( 0\right ) e^{d_{2}}-K\right ) _{+};\\ P_{3} & =\left ( S_{1}\left ( 0\right ) e^{d_{1}}+S_{2}\left ( 0\right ) e^{u_{2}}-K\right ) _{+};\, P_{4}=\left ( S_{1}\left ( 0\right ) e^{d_{1}}+S_{2}\left ( 0\right ) e^{d_{2}}-K\right ) _{+}. \end{align*}

It follows from Expression (14) that

$C_{\mathbb{Q}}\left [ K,1\right ]$

is an increasing linear function of

$C_{\mathbb{Q}}\left [ K,1\right ]$

is an increasing linear function of

$\rho _{\mathbb{Q}}(1), $

since

$\rho _{\mathbb{Q}}(1), $

since

$(P_{1}-P_{2}-P_{3}+P_{4})\geq 0.$

$(P_{1}-P_{2}-P_{3}+P_{4})\geq 0.$

The time

$0$

market price of a call option with strike

$0$

market price of a call option with strike

$K$

and maturity

$K$

and maturity

$1$

year, denoted by

$1$

year, denoted by

$C_{\mathbb{Q}}\left [ K,1\right ]$

, can then be used to extract the correlation

$C_{\mathbb{Q}}\left [ K,1\right ]$

, can then be used to extract the correlation

$\rho _{\mathbb{Q}}\left ( 1\right )$

associated with the risk-neutral measure

$\rho _{\mathbb{Q}}\left ( 1\right )$

associated with the risk-neutral measure

$\mathbb{Q}$

, as demonstrated in (14). Indeed, we have that:

$\mathbb{Q}$

, as demonstrated in (14). Indeed, we have that:

\begin{equation} \rho _{\mathbb{Q}} \left ( 1\right )=\frac{4 \text{e}^{r}C_{\mathbb{Q}}\left [ K,1\right ] - \left ( P_{1}+P_{2}+P_{3}+P_{4}\right ) }{\left ( P_{1}-P_{2}-P_{3}+P_{4}\right ) }. \end{equation}

\begin{equation} \rho _{\mathbb{Q}} \left ( 1\right )=\frac{4 \text{e}^{r}C_{\mathbb{Q}}\left [ K,1\right ] - \left ( P_{1}+P_{2}+P_{3}+P_{4}\right ) }{\left ( P_{1}-P_{2}-P_{3}+P_{4}\right ) }. \end{equation}

From Theorem1, the joint probabilities

$q_{d d}(1), q_{d u}(1), q_{u d}(1), q_{u u}(1)$

in this case are fully specified. For the single period case, Theorem 5 also indicates the equivalence relation between the correlation of two stocks and the volatility of the stock index. Moreover, we provide the following Theorem6 to show that having available the option prices

$q_{d d}(1), q_{d u}(1), q_{u d}(1), q_{u u}(1)$

in this case are fully specified. For the single period case, Theorem 5 also indicates the equivalence relation between the correlation of two stocks and the volatility of the stock index. Moreover, we provide the following Theorem6 to show that having available the option prices

$C_{\mathbb{Q}}\left [ K,T\right ], $

for

$C_{\mathbb{Q}}\left [ K,T\right ], $

for

$T=1,2,\ldots, n,$

one can back out the pricing measure

$T=1,2,\ldots, n,$

one can back out the pricing measure

$\mathbb{Q}$

.

$\mathbb{Q}$

.

Theorem 6.

Assume the index call option prices

$C_{\mathbb{Q}}\left [ K,T\right ], T = 1,2,\ldots, n$

are all available, then the correlation coefficient

$C_{\mathbb{Q}}\left [ K,T\right ], T = 1,2,\ldots, n$

are all available, then the correlation coefficient

$\rho _{\mathbb{Q}}(t), t =1,2,\ldots, n$

can unambiguously be determined.

$\rho _{\mathbb{Q}}(t), t =1,2,\ldots, n$

can unambiguously be determined.

Proof.

First, we already determined

$\rho _{\mathbb{Q}}(1)$

from expression (15). Next, knowledge about the price

$\rho _{\mathbb{Q}}(1)$

from expression (15). Next, knowledge about the price

$C_{\mathbb{Q}}[K,2]$

enables us to back out the correlation

$C_{\mathbb{Q}}[K,2]$

enables us to back out the correlation

$\rho _{\mathbb{Q}}(2)$

. Indeed, we can write:

$\rho _{\mathbb{Q}}(2)$

. Indeed, we can write:

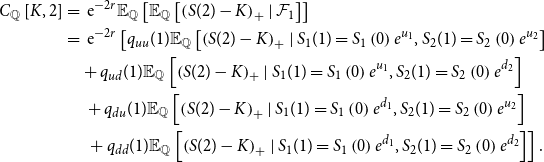

\begin{align} C_{\mathbb{Q}}\left [ K,2\right ] &=\text{ } \text{e}^{-2r}\mathbb{E}_{\mathbb{Q}}\left [ \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid \mathcal{F}_{1}\right ] \right ] \nonumber \\ &=\text{ } \text{e}^{-2r}\left [ q_{u u}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{u_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{u_{2}}\right ] \right . \nonumber \\ \text{ } &\quad +q_{u d}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{u_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{d_{2}}\right ] \nonumber \\ &\quad \text{ }+q_{d u}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{d_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{u_{2}}\right ] \nonumber \\ &\quad \text{ }\left . +\text{ }q_{d d}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{d_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{d_{2}}\right ] \right ] . \end{align}

\begin{align} C_{\mathbb{Q}}\left [ K,2\right ] &=\text{ } \text{e}^{-2r}\mathbb{E}_{\mathbb{Q}}\left [ \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid \mathcal{F}_{1}\right ] \right ] \nonumber \\ &=\text{ } \text{e}^{-2r}\left [ q_{u u}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{u_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{u_{2}}\right ] \right . \nonumber \\ \text{ } &\quad +q_{u d}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{u_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{d_{2}}\right ] \nonumber \\ &\quad \text{ }+q_{d u}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{d_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{u_{2}}\right ] \nonumber \\ &\quad \text{ }\left . +\text{ }q_{d d}(1) \mathbb{E}_{\mathbb{Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =S_{1}\left ( 0\right ) e^{d_{1}},S_{2}(1) =S_{2}\left ( 0\right ) e^{d_{2}}\right ] \right ] . \end{align}

From Expression (14), we find that the conditional expectations are given by:

\begin{equation*} \mathbb {E}_{\mathbb {Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =s_{1},S_{2}(1) =s_{2}\right ]=\frac { (P_{1}+P_{2}+P_{3}+P_{4}) + \left ( P_{1}-P_{2}-P_{3}+P_{4}\right )\rho _{\mathbb {Q}\left ( 2\right )}}{4}, \end{equation*}

\begin{equation*} \mathbb {E}_{\mathbb {Q}}\left [ \left ( S(2) -K\right ) _{+}\mid S_{1}(1) =s_{1},S_{2}(1) =s_{2}\right ]=\frac { (P_{1}+P_{2}+P_{3}+P_{4}) + \left ( P_{1}-P_{2}-P_{3}+P_{4}\right )\rho _{\mathbb {Q}\left ( 2\right )}}{4}, \end{equation*}

where the constants

$P_{j}$

,

$P_{j}$

,

$j=1,2,3,4,$

are now defined as follows:

$j=1,2,3,4,$

are now defined as follows:

\begin{align*} P_{1} & =\left ( s_{1}e^{u_{1}}+s_{2}e^{u_{2}}-K\right ) _{+};\,P_{2}=\left ( s_{1}e^{u_{1}}+s_{2}e^{d_{2}}-K\right ) _{+};\\ P_{3} & =\left ( s_{1}e^{d_{1}}+s_{2}e^{u_{2}}-K\right ) _{+};\,P_{4}=\left ( s_{1}e^{d_{1}}+s_{2}e^{d_{2}}-K\right ) _{+}. \end{align*}

\begin{align*} P_{1} & =\left ( s_{1}e^{u_{1}}+s_{2}e^{u_{2}}-K\right ) _{+};\,P_{2}=\left ( s_{1}e^{u_{1}}+s_{2}e^{d_{2}}-K\right ) _{+};\\ P_{3} & =\left ( s_{1}e^{d_{1}}+s_{2}e^{u_{2}}-K\right ) _{+};\,P_{4}=\left ( s_{1}e^{d_{1}}+s_{2}e^{d_{2}}-K\right ) _{+}. \end{align*}

The probabilities

$q_{u u}(1), q_{u d}(1), q_{d u}(1), q_{d d}(1)$

are already determined from the call option price

$q_{u u}(1), q_{u d}(1), q_{d u}(1), q_{d d}(1)$

are already determined from the call option price

$C_{\mathbb{Q}}[K,1]$

. As a result, the only unknown parameter in the Expression (16) is

$C_{\mathbb{Q}}[K,1]$

. As a result, the only unknown parameter in the Expression (16) is

$\rho _{\mathbb{Q}}(2)$

and observing the option price

$\rho _{\mathbb{Q}}(2)$

and observing the option price

$C_{\mathbb{Q}}\left [ K,2\right ]$

allows to solve for

$C_{\mathbb{Q}}\left [ K,2\right ]$

allows to solve for

$\rho _{\mathbb{Q}}(2).$

Suppose we have derived the correlations

$\rho _{\mathbb{Q}}(2).$

Suppose we have derived the correlations

$\rho _{\mathbb{Q}}(t), t=1,2,\ldots, i$

, where

$\rho _{\mathbb{Q}}(t), t=1,2,\ldots, i$

, where

$i\lt n$

, we can then apply the same approach to acquire the correlation

$i\lt n$

, we can then apply the same approach to acquire the correlation

$\rho _{\mathbb{Q}}\left ( i+1\right )$

from the correlations

$\rho _{\mathbb{Q}}\left ( i+1\right )$

from the correlations

$\rho _{\mathbb{Q}}(1)$

,

$\rho _{\mathbb{Q}}(1)$

,

$\rho _{\mathbb{Q}}(2)$

,

$\rho _{\mathbb{Q}}(2)$

,

$\dots, \rho _{\mathbb{Q}}\left ( i\right )$

and the index option price

$\dots, \rho _{\mathbb{Q}}\left ( i\right )$

and the index option price

$C_{\mathbb{Q}}\left [ K,i+1\right ]$

. The probability distributions of

$C_{\mathbb{Q}}\left [ K,i+1\right ]$

. The probability distributions of

$S_1(i)$

and

$S_1(i)$

and

$S_2(i)$

can be specified using

$S_2(i)$

can be specified using

$\rho _{\mathbb{Q}}\left ( 1\right )$

,

$\rho _{\mathbb{Q}}\left ( 1\right )$

,

$\rho _{\mathbb{Q}}\left ( 2\right ), \dots, \rho _{\mathbb{Q}}\left ( i\right )$

. Hence, by using the option price

$\rho _{\mathbb{Q}}\left ( 2\right ), \dots, \rho _{\mathbb{Q}}\left ( i\right )$

. Hence, by using the option price

$C_{\mathbb{Q}}\left [ K,i+1\right ]$

, we can solve for

$C_{\mathbb{Q}}\left [ K,i+1\right ]$

, we can solve for

$\rho _{\mathbb{Q}}\left ( i+1\right )$

. Therefore, we conclude that having available the option prices

$\rho _{\mathbb{Q}}\left ( i+1\right )$

. Therefore, we conclude that having available the option prices

$C_{\mathbb{Q}}\left [ K,T\right ], $

for

$C_{\mathbb{Q}}\left [ K,T\right ], $

for

$T=1,2,\ldots, n$

, one can back out the pricing measure

$T=1,2,\ldots, n$

, one can back out the pricing measure

$\mathbb{Q}$

.

$\mathbb{Q}$

.

Theorem6 showed that adding index call options with maturities

$t=1,2,\ldots, T,$

completes the market described in (3). Indeed, one can back out the risk-neutral correlation using index call options, and therefore the risk-neutral probability measure is unique in this market setting. The idea of extracting the implied correlation from available multivariate option prices is widely discussed in the literature. For example, Linders & Schoutens (Reference Linders and Schoutens2014) used basket option prices, Ballotta et al. (Reference Ballotta, Deelstra and Rayée2017) used quanto options, and Garcia et al. (Reference Garcia, Goossens, Masol and Schoutens2009) derived implied correlations using CDO spreads.

$t=1,2,\ldots, T,$

completes the market described in (3). Indeed, one can back out the risk-neutral correlation using index call options, and therefore the risk-neutral probability measure is unique in this market setting. The idea of extracting the implied correlation from available multivariate option prices is widely discussed in the literature. For example, Linders & Schoutens (Reference Linders and Schoutens2014) used basket option prices, Ballotta et al. (Reference Ballotta, Deelstra and Rayée2017) used quanto options, and Garcia et al. (Reference Garcia, Goossens, Masol and Schoutens2009) derived implied correlations using CDO spreads.

Prices of traded stocks and options can be used to back out the corresponding risk-neutral pricing measure, the correlation of the stock returns and the volatility of the stock market index. We refer to these quantities as implied measures, implied correlation, implied volatility. Note that market prices are expectations under the pricing measure

$\mathbb{Q}$

and therefore the implied correlation and the implied volatility have to be understood as correlation and volatility levels with respect to the risk-neutral probability measure

$\mathbb{Q}$

and therefore the implied correlation and the implied volatility have to be understood as correlation and volatility levels with respect to the risk-neutral probability measure

$\mathbb{Q}$

. Correlation and volatility under the probability

$\mathbb{Q}$

. Correlation and volatility under the probability

$\mathbb{P}$

are referred to as real-world correlation and volatility, respectively.

$\mathbb{P}$

are referred to as real-world correlation and volatility, respectively.

3.2 Example: A single period model

We consider a one-period financial market as described in Section 2. The risk-free rate

$r$

is assumed to be

$r$

is assumed to be

$0$

and consider

$0$

and consider

$e^{u_1}=1.4$

,

$e^{u_1}=1.4$

,

$e^{u_2}=1.7$

. The time

$e^{u_2}=1.7$

. The time

$0$

spot prices of the traded assets are given by

$0$

spot prices of the traded assets are given by

$S_{1}\left ( 0\right ) =100$

and

$S_{1}\left ( 0\right ) =100$

and

$S_{2}\left ( 0\right ) =200$

. The dynamics of the financial market under the real-world measure

$S_{2}\left ( 0\right ) =200$

. The dynamics of the financial market under the real-world measure

$\mathbb{P}$

are described by the following equations:

$\mathbb{P}$

are described by the following equations:

\begin{align} p_{d d}(1) & =0.3, p_{u d}(1)=0.2,\\ p_{d u}(1) & =0.2, p_{u u}(1) =0.3.\nonumber \end{align}

\begin{align} p_{d d}(1) & =0.3, p_{u d}(1)=0.2,\\ p_{d u}(1) & =0.2, p_{u u}(1) =0.3.\nonumber \end{align}

Notice that we choose the marginals such that the

$\mathbb{P}$

-marginals are the same as the

$\mathbb{P}$

-marginals are the same as the

$\mathbb{Q}$

-marginals, this is to make the example simpler and is not required in general case.

$\mathbb{Q}$

-marginals, this is to make the example simpler and is not required in general case.

Consider the stock market index

$S(t)=S_{1}(t) +S_{2}(t), $

$S(t)=S_{1}(t) +S_{2}(t), $

$t=0,1.$

We find that the real-world correlation

$t=0,1.$

We find that the real-world correlation

$\rho _{\mathbb{P}}(1) = \text{Corr}[R_1(1), R_2(1)] = 0.2,$

and the real-world volatility

$\rho _{\mathbb{P}}(1) = \text{Corr}[R_1(1), R_2(1)] = 0.2,$

and the real-world volatility

$\sigma _{\mathbb{P}}(1) =\sqrt{\text{Var}_{\mathbb{P}}\left [ R(1) \right ]} = 0.585.$

Since

$\sigma _{\mathbb{P}}(1) =\sqrt{\text{Var}_{\mathbb{P}}\left [ R(1) \right ]} = 0.585.$

Since

$\rho _{\mathbb{P}}(1) =0.2\gt 0$

, the return vector

$\rho _{\mathbb{P}}(1) =0.2\gt 0$

, the return vector

$\left ( R_{1}(1), R_{2}(1) \right )$

is Positive Quadrant Dependent under the real-world probability measure

$\left ( R_{1}(1), R_{2}(1) \right )$

is Positive Quadrant Dependent under the real-world probability measure

$\mathbb{P}$

:

$\mathbb{P}$

:

\begin{equation} \left ( R_{1}(1), R_{2}(1) \right ) \text{ is }\mathbb{P}-\text{PQD.} \end{equation}

\begin{equation} \left ( R_{1}(1), R_{2}(1) \right ) \text{ is }\mathbb{P}-\text{PQD.} \end{equation}

We conclude from (18) that stocks are positively dependent under the real-world measure

$\mathbb{P}$

specified by (17). However, the dependence structure under the risk-neutral measure

$\mathbb{P}$

specified by (17). However, the dependence structure under the risk-neutral measure

$\mathbb{Q}$

can be different, even opposite from the dependence under

$\mathbb{Q}$

can be different, even opposite from the dependence under

$\mathbb{P}$

. The following Proposition1 is presented to show that the stock prices can be negatively dependent under the risk-neutral measure.

$\mathbb{P}$

. The following Proposition1 is presented to show that the stock prices can be negatively dependent under the risk-neutral measure.

Proposition 1.

A call option written on the stock market index

$S(1)$

, with strike

$S(1)$

, with strike

$K = 300$

, is traded and its time

$K = 300$

, is traded and its time

$0$

price

$0$

price

$\hat{C}_{\mathbb{Q}}$

can be observed in the market. Then we have the following equivalence relations:

$\hat{C}_{\mathbb{Q}}$

can be observed in the market. Then we have the following equivalence relations:

\begin{align} \hat{C}_{\mathbb{Q}} \geq 70 & \Longleftrightarrow \mathbb{Q}-\text{PQD},\\ \hat{C}_{\mathbb{Q}} \leq 70 & \Longleftrightarrow \mathbb{Q}-\text{NQD} \nonumber \end{align}

\begin{align} \hat{C}_{\mathbb{Q}} \geq 70 & \Longleftrightarrow \mathbb{Q}-\text{PQD},\\ \hat{C}_{\mathbb{Q}} \leq 70 & \Longleftrightarrow \mathbb{Q}-\text{NQD} \nonumber \end{align}

Proof.

From (14), we have

$\hat{C}_{\mathbb{Q}} = 70 + 20\rho _{\mathbb{Q}}(1).$

Hence, it follows from (8) directly to derive (19).

$\hat{C}_{\mathbb{Q}} = 70 + 20\rho _{\mathbb{Q}}(1).$

Hence, it follows from (8) directly to derive (19).

Proposition1 shows that the market decides if the stocks are positive or negative dependent under the risk-neutral measure. Indeed, different market situations result in different risk-neutral measures, which can be different with the real-world measure

$\mathbb{P}$

. Here we provide three different market situations in Table 1.

$\mathbb{P}$

. Here we provide three different market situations in Table 1.

From Table 1, we can also conclude that the risk-neutral pricing measures

$\mathbb{Q}^{(1) }$

,

$\mathbb{Q}^{(1) }$

,

$\mathbb{Q}^{(2) }$

, and

$\mathbb{Q}^{(2) }$

, and

$\mathbb{Q}^{\left ( 3\right ) }$

are ordered in the correlation order:

$\mathbb{Q}^{\left ( 3\right ) }$

are ordered in the correlation order:

\begin{equation*} F_{t}^{\mathbb {Q}^{(1)}}{\preceq }_{\text {Corr}}F_{t}^{\mathbb {Q}^{(2)}}{\preceq }_{\text {Corr}}F_{t}^{\mathbb {Q}^{\left ( 3\right )}}. \end{equation*}

\begin{equation*} F_{t}^{\mathbb {Q}^{(1)}}{\preceq }_{\text {Corr}}F_{t}^{\mathbb {Q}^{(2)}}{\preceq }_{\text {Corr}}F_{t}^{\mathbb {Q}^{\left ( 3\right )}}. \end{equation*}

This example shows that deriving the implied correlation and volatility to learn about the future dynamics of the stock prices is only part of the story. Implied measures are giving information about the risk-neutral dynamics and these statements cannot be directly translated to statements under the real-world probability measure. If the risk-neutral measure

$\mathbb{Q}^{(1)}$

is chosen by the market, then implied volatility and correlation are substantially different with the real-world volatility and correlation. It might feel counter-intuitive to use a negative dependence structure to price the index option while under the real-world probability measure, the stocks are positive dependent. Notice that, however, the corresponding index option price does not lead to arbitrage and is consistent with other derivative prices.

$\mathbb{Q}^{(1)}$

is chosen by the market, then implied volatility and correlation are substantially different with the real-world volatility and correlation. It might feel counter-intuitive to use a negative dependence structure to price the index option while under the real-world probability measure, the stocks are positive dependent. Notice that, however, the corresponding index option price does not lead to arbitrage and is consistent with other derivative prices.

Three different market situations given that

$\rho _{\mathbb{P}} = 0.2$

and

$\rho _{\mathbb{P}} = 0.2$

and

$\sigma _{\mathbb{P}} = 0.585$

$\sigma _{\mathbb{P}} = 0.585$

3.3 Example: A multiperiod model

Consider the financial market described above, but now we consider the future times

$t=1,2,\ldots, 10.$

Assume that the real-world correlation

$t=1,2,\ldots, 10.$

Assume that the real-world correlation

$\rho _{\mathbb{P}}(t)$

is given by

$\rho _{\mathbb{P}}(t)$

is given by

$\rho _{\mathbb{P}}(t) = 0.92 - 0.08t, \text{ for } t=1,2,\ldots 10.$

Similar to the one-period case, we still assume the real-world marginals are the same as the risk-neutral marginals, then the real-world dynamics can be expressed as:

$\rho _{\mathbb{P}}(t) = 0.92 - 0.08t, \text{ for } t=1,2,\ldots 10.$

Similar to the one-period case, we still assume the real-world marginals are the same as the risk-neutral marginals, then the real-world dynamics can be expressed as:

\begin{align} p_{d d}(t) =\frac{1}{4}(1+\rho _{\mathbb{P}}(t))&, p_{u d}(t) =\frac{1}{4}(1-\rho _{\mathbb{P}}(t)), \\ p_{d u}(t) =\frac{1}{4}(1-\rho _{\mathbb{P}}(t))&, \nonumber p_{u u}(t) =\frac{1}{4}(1+\rho _{\mathbb{P}}(t)).\nonumber \end{align}

\begin{align} p_{d d}(t) =\frac{1}{4}(1+\rho _{\mathbb{P}}(t))&, p_{u d}(t) =\frac{1}{4}(1-\rho _{\mathbb{P}}(t)), \\ p_{d u}(t) =\frac{1}{4}(1-\rho _{\mathbb{P}}(t))&, \nonumber p_{u u}(t) =\frac{1}{4}(1+\rho _{\mathbb{P}}(t)).\nonumber \end{align}

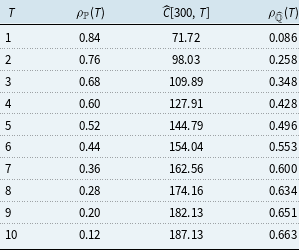

We show real-world correlations in the second column of Table 2.

Real-world and risk-neutral correlations

Assume at time 0, at-the-money call options with maturities

$T=1,2,\ldots, 10$

are traded. The market prices are denoted by

$T=1,2,\ldots, 10$

are traded. The market prices are denoted by

$\widehat{C}\left [ 300,T\right ], \text{ where }T=1,2,\ldots, 10,$

and are given in the third column of Table 2. The market prices can be used to determine the unique risk-neutral measure

$\widehat{C}\left [ 300,T\right ], \text{ where }T=1,2,\ldots, 10,$

and are given in the third column of Table 2. The market prices can be used to determine the unique risk-neutral measure

$\widehat{\mathbb{Q}}$

. Indeed, Theorem6 shows that implied correlations

$\widehat{\mathbb{Q}}$

. Indeed, Theorem6 shows that implied correlations

$\rho _{\widehat{\mathbb{Q}}}(t)$

can be uniquely determined by index call option prices

$\rho _{\widehat{\mathbb{Q}}}(t)$

can be uniquely determined by index call option prices

$\widehat{C}[300,t]$

for

$\widehat{C}[300,t]$

for

$t=1,2,\dots, n$

. We present implied correlations

$t=1,2,\dots, n$

. We present implied correlations

$\rho _{\widehat{\mathbb{Q}}}(t)$

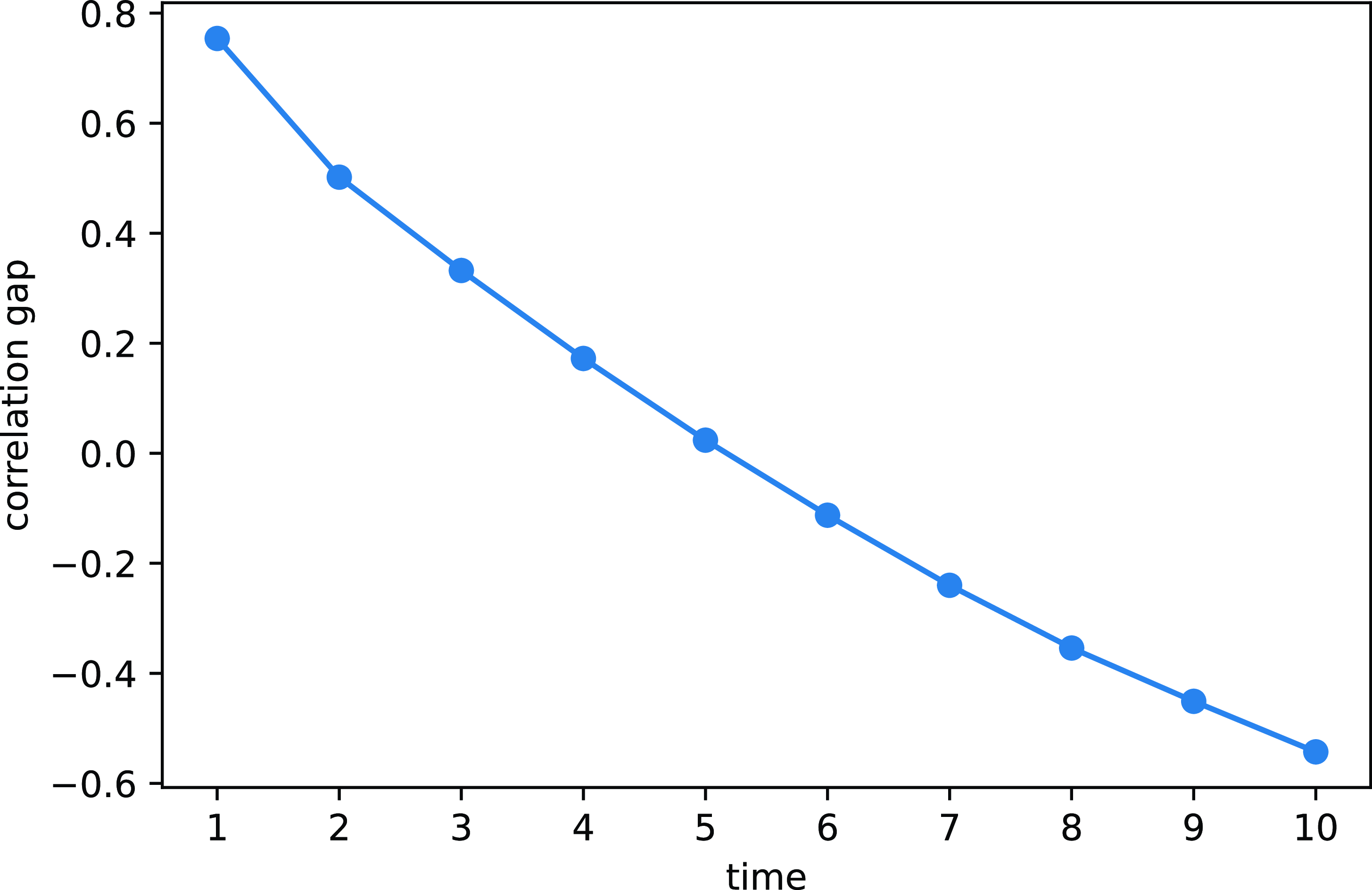

in the fourth column of Table 2. We can find from Table 2 that there always exists a gap between real-world and implied correlations. We call this gap the correlation gap. The following Fig. 1 shows the plot of the correlation gap,

$\rho _{\widehat{\mathbb{Q}}}(t)$

in the fourth column of Table 2. We can find from Table 2 that there always exists a gap between real-world and implied correlations. We call this gap the correlation gap. The following Fig. 1 shows the plot of the correlation gap,

$\rho _{\mathbb{P}}(t) - \rho _{\widehat{\mathbb{Q}}}(t)$

for time

$\rho _{\mathbb{P}}(t) - \rho _{\widehat{\mathbb{Q}}}(t)$

for time

$t = 1, 2, \dots, 10.$

$t = 1, 2, \dots, 10.$

The correlation gap

$\rho _{\mathbb{P}}(t) - \rho _{\widehat{\mathbb{Q}}}(t)$

with respect to time

$\rho _{\mathbb{P}}(t) - \rho _{\widehat{\mathbb{Q}}}(t)$

with respect to time

$t$

.

$t$

.