Introduction

Buy Now Pay Later (BNPL) has seen exponential growth in recent years, and its popularity has accelerated across borders.Footnote 1 As its popularity grows, concerns have been raised over the risks it poses. Described as a debt trap, BNPL often operates in a less regulated space than similar forms of consumer finance, even in countries with developed consumer credit regulatory frameworks.Footnote 2 Reports have highlighted debt problems among many consumers drawn by BNPL marketing as an interest-free ‘way to pay’.Footnote 3 Easy access to credit and an attractive digital interface have further precipitated the increasing uptake of BNPL.Footnote 4 This article investigates emerging evidence of detrimental consequences faced by BNPL users and considers regulatory reforms aimed at strengthening protection for vulnerable consumers. The analysis focuses on Malaysia, which is developing a regulatory framework for the protection of credit consumers.Footnote 5 The study’s insights are valuable for other emerging economies contemplating interventions to address similar issues.

The Malaysian BNPL industry has grown rapidly in line with international trends. In 2023, there were 77.3 million BNPL transactions worth RM6.2 billion, significantly higher than the RM1.49 billion value of non-bank BNPL providers in 2021.Footnote 6 At the same time, concerns have been raised in the media over consumers falling into unmanageable debt as a result of BNPL.Footnote 7 To alleviate such harm, Malaysian law reformers introduced the Consumer Credit Act 2025 [Act 873], drawing on the experience of other common law countries, such as the UK and Australia, which have established consumer credit regulatory frameworks.Footnote 8 The legislation received royal assent on 22 December 2025.Footnote 9 It empowers the Consumer Credit Commission to regulate and supervise the industry, and the Commission’s powers include issuing standards or guidelines for credit providers.Footnote 10

This article contributes to the development of consumer credit regulation in Malaysia by facilitating a more nuanced understanding of consumers’ experiences with BNPL. It investigates the intersection between financial stress, credit use, and harmful outcomes, drawing on original empirical data collected by the author. The study sheds light on strategies that the Consumer Credit Commission can implement, and regulatory guidance that it can issue, to increase the efficacy of current reform initiatives and strengthen safeguards for the most vulnerable consumers. Insights from the analysis are relevant for other emerging economies, particularly Member States of the ASEAN Economic Community, seeking to address consumer harm from BNPL and other forms of online credit. Problems with consumers falling into unmanageable debt after using BNPL have also been raised in other Member States.Footnote 11 Member States of the ASEAN Economic Community collectively comprise the fifth-largest economy in the world, with a nominal GDP of USD3.8 trillion in 2023.Footnote 12

The ASEAN Economic Blueprint envisages regional economic integration, emphasising the need for consumer credit protection frameworks in the region, and information sharing and exchange among Member States.Footnote 13 In ASEAN’s characteristic form of consensus-based cooperation, Malaysia’s burgeoning regulatory framework, the first by way of legislation in the region, provides a model for other Member States. Singapore has a voluntary code for BNPL that sets out best practices, including caution when using the word ‘free’ in advertising, processes to enable consumers to apply for financial hardship assistance, and internal dispute resolution.Footnote 14 However, concerns have been raised over its lack of enforceability, and consumer advocates argue that voluntary codes elsewhere have not been effective in curbing consumer harm from unaffordable BNPL.Footnote 15 Singaporean experts assert that further safeguards are necessary to protect vulnerable consumers.Footnote 16

This article examines the growing popularity of BNPL, its underlying drivers, and risks of harm. The discussion then turns to the methodology and insights from a survey of 400 Malaysian consumers, focus group interviews, an interview with consumer advocates, and an analysis of BNPL providers’ websites. Proposals for regulatory guidance and broader reforms to alleviate the risk of harm are considered.

BNPL: Growth and consumer harm

The Malaysian BNPL industry has grown rapidly in recent years.Footnote 17 In the first quarter of 2024 alone, 29 million transactions worth RM2.3 billion were recorded, more than double the transaction volume in the first quarter of 2023 (14 million).Footnote 18 BNPL is used primarily by adults aged 31-45 years (47%) and 21-30 years (44%). Concerns have been raised over the lack of transparency, the targeting of younger and low-income borrowers, and the risk of over-indebtedness.Footnote 19 While BNPL is often advertised as having ‘zero interest’, fees for late payments, processing charges and other opaque costs are often comparable to credit card rates.Footnote 20 The rapid growth of BNPL in Malaysia resonates with international trends, such as in the UK, where £2.7 billion worth of transactions were recorded in 2020.Footnote 21 In Australia, the transaction value was estimated at AUD2 billion, with almost a third of Australians using BNPL in 2023.Footnote 22 While there is some diversity in the business models adopted by BNPL providers, a number of common traits have given rise to observations of consumer harm, with remarkable similarity across countries.

Although BNPL has its benefits, financial counsellors have observed that ‘without adequate safeguards it can too easily cause harm to others.’Footnote 23 By incorporating specific features, such as zero interest, providers have circumvented consumer protection laws, even in countries with robust regulatory frameworks.Footnote 24 Reforms have been introduced in Australia to extend the scope of consumer credit regulatory frameworks to include BNPL, while several other countries are considering similar measures.Footnote 25 Various features of BNPL give rise to risks of harm, including marketing strategies and easy access to credit through digital platforms.

Digital disruption and the new ‘way to pay’

The widespread use of the digital interface is thought to promote the rising use of BNPL. Ease of access and its availability through merchants further encourage the perception of BNPL as a ‘casual way to consume’ with ‘just a few taps’ on the phone.Footnote 26 Strategies that appeal to consumers include apps that ‘replicate the experiences of a digital game’ and ‘offer rewards and positive reinforcements’ while ‘promoting themselves as helping customers to manage their finances.’Footnote 27 Gamification of debt encourages engagement, and BNPL providers’ digital interface is often similar to those of social platforms. By emulating the experience of interacting with social, informal platforms as opposed to formal, intimidating economic relationships with banks, digital platforms mask the risks of credit arrangements.Footnote 28

BNPL is often marketed as an interest-free way to pay by instalments. References to ‘zero cost’ and ‘new ways to pay’ have fostered perceptions that BNPL is similar to a debit card.Footnote 29 Consumers often fail to recognise that it is a form of debtFootnote 30 and, as a result, they ‘may not apply the same level of scrutiny to their decision-making as they would for other credit products,’ including considering the consequences of failing to repay.Footnote 31

Advertising strategies play into consumers’ behavioural biases, increasing the likelihood of impulsive decisions that are not in their best interest.Footnote 32 The benefits of BNPL are highlighted while risk disclosures are made to appear relatively inconspicuous. Further, splitting the total cost of an item into several smaller instalments creates the impression that the purchase is more affordable. Advertisements tap into people’s identities and aspirations, promoting BNPL as a means to ‘empower the life you want’,Footnote 33 emphasising the potential to achieve a lifestyle that might not otherwise be attainable.Footnote 34

As marketing strategies camouflage the risks of indebtedness, the lack of friction and affordability checks further facilitates impulse buying. Critics observe that ‘the overall consumer journey’ is ‘designed to drive sales without due consideration for the affordability of the commitment the consumer is taking on.’Footnote 35 Providers often market BNPL to retailers on the grounds that ‘consumers spend more when they use BNPL offers than they would when paying by traditional methods.’Footnote 36 The relatively seamless digital interface between merchants and BNPL providers bolsters perceptions of BNPL as a payment method rather than a form of credit or debt, which carries risks of harm.

Adverse consequences

Several Malaysian news articles have underscored the challenges faced by BNPL consumers who were drawn to it for its easy access without realising the risks.Footnote 37 Subsequently, they fell behind on instalment payments. As late charges accrued, their indebtedness increased, and they were pursued by debt collectors.Footnote 38 Regulators, consumer advocates and financial counsellors in other countries have raised similar concerns.Footnote 39 In the UK, two in five BNPL users struggled to meet BNPL repayments.Footnote 40 Late fees of £39 million were recorded in the UK over a 12-month period,Footnote 41 while Australians paid AUD43 million.Footnote 42 As BNPL repayments are often automatically deducted from credit or debit card accounts, consumers are at times left with insufficient funds for other expenses, incur interest on their credit card debt, take on additional BNPL debts, or are pursued by debt collectors.Footnote 43 More than two in five British BNPL consumers borrowed money to pay BNPL debt, often incurring interest as a result.Footnote 44 In Australia, 61% of financial counsellors surveyed report that vulnerable consumers struggle to pay living expenses such as rent, food, or utilities because of BNPL debt, often prioritising BNPL payments to keep their accounts open.Footnote 45

Malaysian law reformers have often drawn on developments in common law countries such as the UK and Australia, and the consultation papers reflect the perceived value of looking to innovations in other common law jurisdictions.Footnote 46 At the same time, scholars underscore the importance of considering differences in socioeconomic conditions and the specific challenges consumers face in a local context to ensure that borrowed laws achieve their underlying aims.Footnote 47

Financial stress

An estimated 53,000 young Malaysian adults aged below 30 years were described as ‘drowning in debt’ worth nearly RM1.9 billion in October 2024.Footnote 48 This is attributed in part to ‘growing reliance by young people on BNPL services as well as credit cards and personal loans’.Footnote 49 Further, the high cost of living, inadequate income, and housing unaffordability contribute to widespread financial stress.Footnote 50 According to the Gallup World Poll 2018, ‘nearly a third of Malaysians in the sample said they did not have enough money for food’, noting that this was ‘more than double the rate reported in 2012.’Footnote 51 Approximately 27% of households in Kuala Lumpur earned ‘less than the recommended living wage’,Footnote 52 and 28% of working adults needed to borrow to buy essential goods, resorting to personal loans, including non-bank credit.Footnote 53 Female-headed households, people with disabilities and the elderly are especially vulnerable, with about 60% struggling to provide adequate food for the family, and without savings for emergencies.Footnote 54

Malaysia offers the lowest level of social protection among upper-middle-income countries in Asia, and its inadequacy has been underscored in various reports.Footnote 55 Benefits are given to ‘a small share of an eligible population’, but many other vulnerable individuals receive no social security.Footnote 56 Even with government assistance, many low-income families are unable to pay their utility bills, rent, or mortgage on time.Footnote 57 In the words of one low-income earner, ‘We get groceries on credit. We get loans from friends and family if they have extra. It’s mostly to pay for food; most importantly for rice.’Footnote 58 For vulnerable consumers, credit is a double-edged sword. While it helps to make ends meet, the high cost of interest or fees in addition to repayments leads to a debt spiral, exacerbating financial stress. Bankruptcy statistics list personal loans as the highest cause of personal insolvency,Footnote 59 while the harmful effects of unmanageable debt include anxiety, depression, relationship problems, and even suicide ideation.Footnote 60

Even in Australia, where social security benefits are more readily available, Good Shepherd argues that ‘BNPL is taking the place of adequate social security payments’ and is used by low-income earners for essentials such as food and utilities.Footnote 61 Calls have been made for better income support for vulnerable Australians. The need is ostensibly greater in Malaysia, where the level of support is substantially lower, and many vulnerable individuals are ineligible for social security.Footnote 62 One media report describes BNPL as a ‘lifeline’ for consumers in financial difficulty.Footnote 63 In the absence of adequate social security, the potential for BNPL to serve as a temporary buffer against the rising cost of living is an important consideration that is absent from the current discourse on Malaysia’s emerging consumer credit laws.

Concerns about rising debt levels among young Malaysians have prompted regulators to introduce legislation to curb the risk of unaffordable BNPL debt.Footnote 64 This article contributes to the burgeoning Malaysian consumer credit framework through empirical research that fosters a more nuanced understanding of the experiences of Malaysian BNPL consumers and the challenges that shape their choices.

Methodology

Regulators in leading jurisdictions have sought to enhance the effectiveness of consumer protection by deepening their understanding of the interactions and processes that influence consumers’ decisions.Footnote 65 By drawing on insights from consumer behaviour, targeted strategies can reduce risks of harm and promote better outcomes for vulnerable individuals.Footnote 66 This study examines four sets of empirical data.

The first dataset examines the websites of BNPL providers to determine how they market their services and engage with consumers at the outset. BNPL providers were identified through searches using the terms ‘pay later Malaysia’ and ‘buy now pay later’ in February 2023. Banks were excluded because they are subject to more stringent regulations, including consumer protection measures.Footnote 67 Ten non-bank BNPL providers were randomly selected from the compiled list; the selection was not based on their representativeness of the industry. As the aim of the study was to analyse evidence of non-bank BNPL providers’ practices, their websites were examined with respect to variables such as their main marketing strategies, fee disclosures, ease of obtaining credit, and support for consumers in financial hardship.

The second dataset considered the impact of BNPL from consumers’ perspectives. To gain deeper insights into consumers’ experiences, an online survey of 400 consumers who have used non-bank BNPL was conducted with the assistance of Pureprofile, a company that specialises in internet-based consumer research. Approval to conduct the research was obtained from the Monash University Human Research Ethics Committee, and the survey was conducted in Bahasa Malaysia and translated by the author, who is bilingual. Respondents were asked about their motivations for using BNPL, whether they missed any payments or incurred fees, and whether they were aware of the fees before signing up. The questions also explored the impact of BNPL on consumers’ financial and overall well-being, and whether they could obtain support from BNPL providers if they experienced financial hardship. Pureprofile recruited participants from its panel of consumers who have signed up to receive surveys. The invitation to participate in the survey was circulated to Pureprofile’s consumer database across Malaysia from March to April 2023, and participants were offered a token payment of approximately RM 15 each. Within 11 days, 400 participants who had used non-bank BNPL within the past 3 years responded to the survey, and the survey was closed.

Several limitations should be noted regarding the datasets. By focusing on websites offering BNPL, the survey of advertising practices does not capture in-store BNPL offers. Nonetheless, reports indicate that BNPL providers rely predominantly on digital platforms to reach consumers.Footnote 68 The survey respondents drawn from Pureprofile’s panel of consumers cannot be said to be representative of Malaysian consumers more generally. In particular, an online survey is less likely to be representative of demographic groups that experience higher rates of digital exclusion, such as the elderly, those living in rural or remote parts of the country where internet coverage may be poorer, people with disabilities, and disadvantaged consumers for whom the cost of digital technology may not be affordable. At the same time, the challenges faced by consumers, as reflected in the survey, resonate with studies in the UK and Australia.

To provide further layering to the survey findings, the author conducted focus group interviews with university students who had used BNPL. Focus groups are a useful means of facilitating the joint construction of ideas, drawing on a variety of perspectives within the group to investigate specific issues, and eliciting diverse views on the discussion topic.Footnote 69 The focus group participants were recruited through a Malaysian university. Each person was offered a Grab RM50 voucher as an incentive to participate in the research. Semi-structured interviews were conducted via Zoom in November 2023, following ethics approval. To encourage participants to share their views freely, cameras were turned off, and participant anonymity was maintained during the Zoom meeting. The first focus group had four participants, and the second had two. In addition, each group had a discussion facilitator. The focus group interviews were recorded with participants’ consent and subsequently transcribed using AI-enabled software. Participants’ comments were tagged with descriptors to attribute them to de-identified individuals. Transcripts of the interviews were manually coded to identify themes, and similarities and differences in participants’ views.Footnote 70 These were synthesised, and the conclusions drawn in this article are supported by direct quotations.

The author also conducted an interview with the Consumer Association of Penang (CAP), the leading grassroots, non-profit organisation for consumers in Malaysia, in December 2023. The interview was guided by open-ended questions on caseworkers’ experiences of assisting consumers. The interview was recorded and transcribed. The author manually coded the transcript and identified themes. The four datasets illuminate Malaysian consumers’ experiences, the interaction between credit and hardship, and the challenges encountered by BNPL users. The findings inform regulatory reforms proposed in this article.

Empirical results

BNPL providers’ websites

To gain a better understanding of BNPL providers’ marketing strategies, websites were examined by reference to the variables described earlier. By way of background, the non-bank BNPL providers whose websites were examined also operate in several other Southeast Asian countries, in addition to Malaysia. Some have a presence in Hong Kong, and several appear to be headquartered or have origins in Singapore, a major financial hub for the region. One BNPL provider is a company that provides financial services in Australia and New Zealand as well.

A consistent theme across all of the ten of the BNPL providers’ websites in the study was the advertising of BNPL as having no interest or fees. Claims such as ‘Absolutely ZERO interest’ and ‘No interest, No hidden fees’ were prominently highlighted on their homepages, often in large bold font. Despite the ‘no fee’ claim appearing as a central tenet of their advertising, eight providers disclosed in a much less conspicuous manner that some fees would be charged. The fee disclosures were consistently overshadowed by colourful, prominent ‘no fee’ claims. To find these disclosures, consumers would need to scroll past brightly coloured, eye-catching advertising material promoting the benefits of BNPL and search through relatively insignificant small print. One provider did not disclose any information on fees, while another has a business model that genuinely does not charge fees even when payments are late.

Overall, the website layouts used by BNPL providers emphasised the interest-free, fee-free aspects. Information on the fees and interest that consumers would incur for various reasons such as late payments was relatively obscure. Of the eight providers who disclosed some form of fees payable, two did not give any details of the amounts payable. Four of the providers disclosed the amount of fees payable among a range of questions on various matters such as ‘troubleshooting help’ and ‘managing orders’. These were located on separate webpages, requiring users to click on other tabs on the homepage such as ‘support’ to find the information. Another two providers disclosed the amount of late fees further down the homepage in small font which appeared relatively inconspicuous beneath bright, bold claims emphasising that there were no hidden charges and ‘absolutely zero interest’. BNPL providers usually describe these as fees for overdue instalments, while a few providers described their fees as administrative charges for various matters such as to ‘reactivate suspended accounts’.

The second prominent theme was the emphasis on BNPL as a smart, convenient way to pay. This is reflected in statements which highlighted the ease with which consumers could register with BNPL providers. Two websites indicated that consumers could obtain ‘instant approval’ of RM1,000 in just a few steps if they linked a debit card, another offered $1,500 for debit cards, while credit cards enabled consumers to have a higher threshold such as RM4,000 or RM5,000. Several websites promoted BNPL as a way to manage expenses, track expenditure and pay ‘flexibly’, advertising automatic deductions as a ‘virtually impossible’ way to miss payments. Seven of the BNPL providers offered discounts, points or rewards, promoting ‘extra savings’.

The strategy of marketing BNPL as a means to achieving an aspirational lifestyle and empowerment was also reflected in eight of the Malaysian websites, in line with observations in UK and Australia.Footnote 71 Examples include statements such as ‘freedom like you’ve never experienced’ and ‘reward yourself with beautiful things in life’, and descriptions of BNPL as the way to ‘pay for life’s many pleasures’, ‘earn dreams when you shop’ and dress fashionably. BNPL websites were often linked to e-commerce sites, facilitating a relatively seamless interface between merchants and BNPL providers.

The majority of websites did not mention financial hardship or any support for payment difficulties. One BNPL expressly mentioned that it was not possible to postpone payments. Nonetheless, two providers suggested contacting them to ‘work out a solution’ if consumers had difficulty paying instalments, while another provider suggested contacting collections or live chat tools for assistance.

Consumer survey

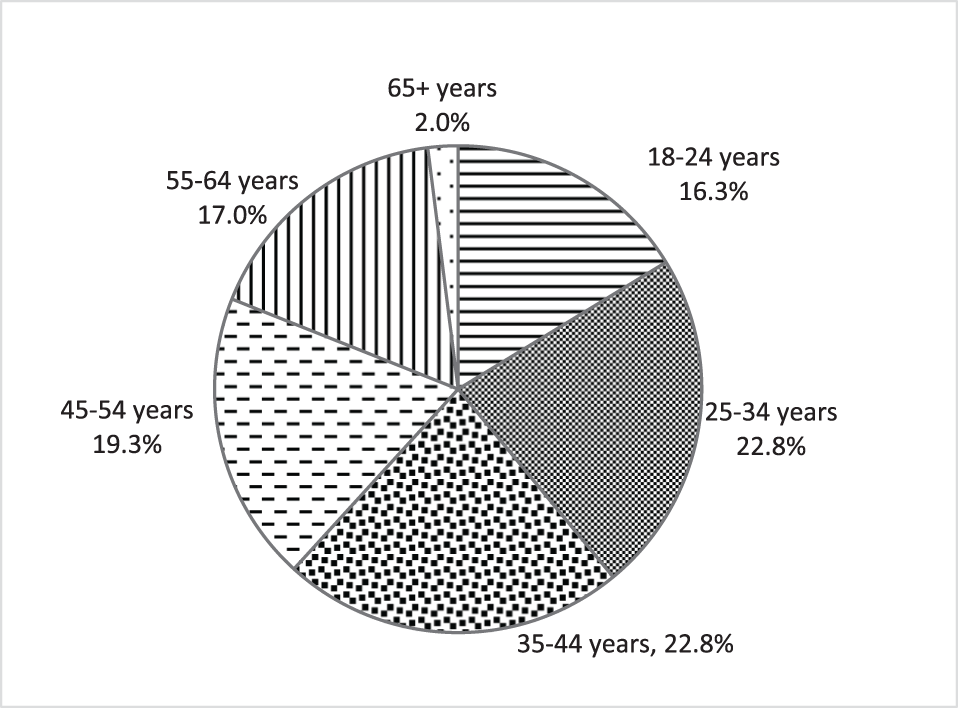

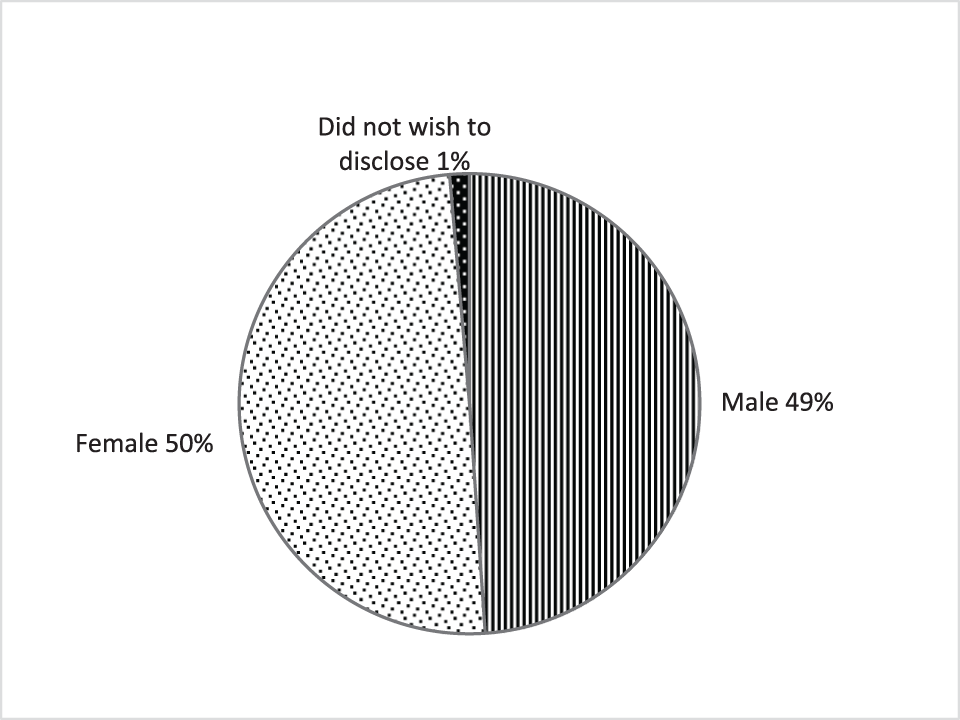

The survey asked approximately 30 questions of 400 consumers to gain a deeper understanding of their experiences with BNPL. The questions explored consumers’ interactions with BNPL providers, the effects of BNPL on their spending and financial situations, and their perspectives on fee transparency, payment difficulties, and suggestions for strengthening consumer protection. The survey sought the views of consumers across a range of age groups and genders in line with national representative quotas. Figure 1 sets out details of survey respondents’ age groups, while Figure 2 shows their gender.

Survey respondents by age.

Figure 1 Long description

The pie chart illustrates the age distribution of a surveyed group. The segments are labeled as follows: 18 to 24 years at 16.3 percent, 25 to 34 years at 22.8 percent, 35 to 44 years at 22.8 percent, 45 to 54 years at 19.3 percent, 55 to 64 years at 17.0 percent and 65 years and older at 2.0 percent. Each segment is visually distinguished by different patterns.

Survey respondents by gender.

Figure 2 Long description

The pie chart illustrates the gender distribution of survey respondents. The chart uses different patterns to represent each category.

Consumers’ use of BNPL

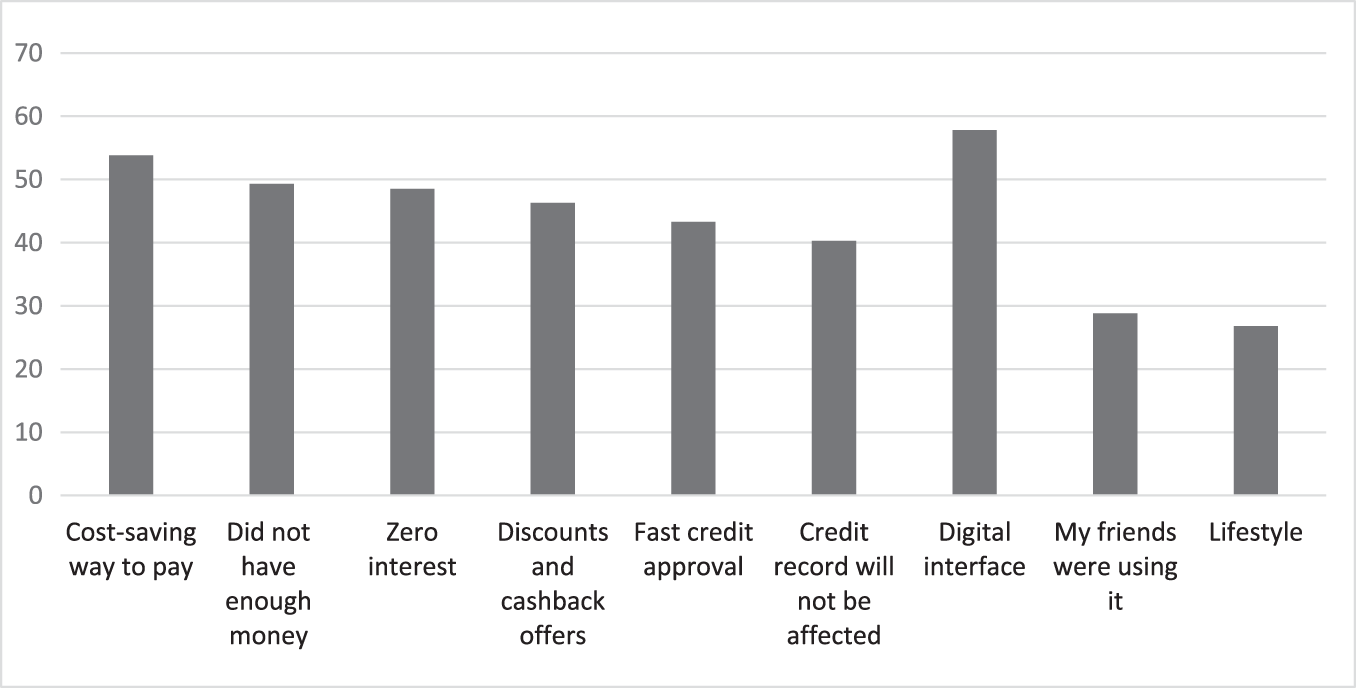

Respondents were asked why they signed up for BNPL and could choose multiple responses. Figure 3 reflects their reasons for using BNPL. Survey respondents indicated that they used BNPL because it was a cost-effective way to pay (53.8%). Common reasons for using BNPL included not having enough money (49.3%), providers’ claims that there was ‘zero interest’ (48.5%), discounts and cashback offers from providers (46.3%), fast credit approval (43.3%) and perceptions that their credit records would not be affected by BNPL (40.3%). More than half of respondents (57.8%) reported being drawn to the digital interface and apps, which they found appealing and convenient. Lifestyle and peer influence also motivated their use of BNPL to a lesser degree, with 28.8% noting that they were motivated to use BNPL as their friends were using it, and 26.8% citing aspirations towards a better lifestyle.

Reasons for using BNPL.

Figure 3 Long description

A bar graph illustrating reasons for using BNPL. The x-axis lists reasons: cost-saving way to pay, did not have enough money, zero interest, discounts and cashback offers, fast credit approval, credit record will not be affected, digital interface, my friends were using it and lifestyle. The y-axis ranges from 0 to 70. The bars show varying heights: cost-saving way to pay and digital interface are the highest, followed by did not have enough money, zero interest, discounts and cashback offers, fast credit approval, credit record will not be affected, my friends were using it and lifestyle.

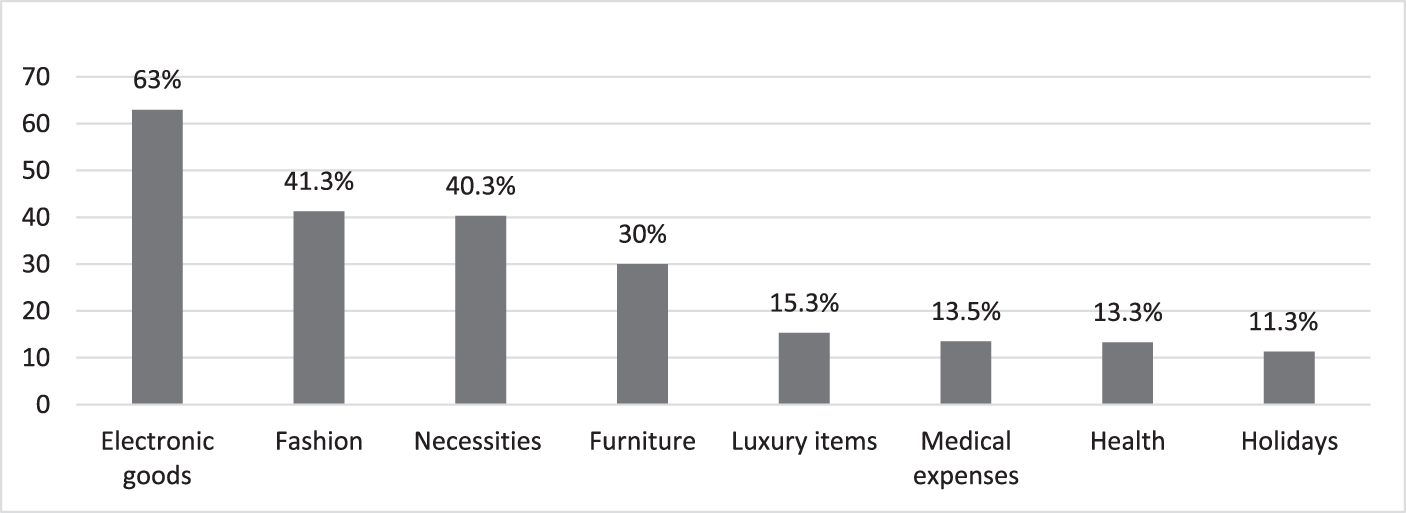

Sixty-two percent of consumers reported spending more as a result of their access to BNPL. A similar proportion (62.5%) used BNPL at least once a month, and 23.5% used BNPL about once a week. Most of the respondents used 1 to 3 BNPL providers,Footnote 72 although 11.4% used 4 or more providers, and 1.5% reported using 9 or more BNPL companies. Figure 4 shows the goods or services respondents purchased with BNPL. Respondents commonly purchased electronic goods and fashion. Notably, 40.3% used BNPL for necessities such as groceries, school uniforms and other school equipment, and telephone expenses. A smaller proportion of respondents used BNPL to pay for furniture, luxury items, medical expenses, health, and holidays.

Respondents’ use of BNPL.

Figure 4 Long description

The bar graph displays the percentages of goods and services purchased using Buy Now Pay Later (BNPL). The x-axis lists categories: electronic goods, fashion, necessities, furniture, luxury items, medical expenses, health and holidays. The y-axis represents percentage values from 0 to 70. Electronic goods are the highest at 63 percent, followed by fashion at 41.3 percent, necessities at 40.3 percent, furniture at 30 percent, luxury items at 15.3 percent, medical expenses at 13.5 percent, health at 13.3 percent and holidays at 11.3 percent.

Unexpected charges

Just under a third of respondents (32.5%) missed a scheduled payment, and 83.8% of those who did incurred fees. More than 1 in 5 (22%) consumers who missed scheduled payments said they did not know they would incur a charge for missed payments. As noted earlier, despite prominent claims that they do not charge interest, many BNPL providers state in less conspicuous parts of their websites that there are a range of fees. These vary across providers and include fees for administration, missed payment or account reactivation, and interest on unpaid amounts. 46.5% of consumers who incurred fees or interest said they were charged more than they expected. In addition, the majority of respondents (56.1%) also incurred interest on their credit cards, which they had used to make BNPL payments.

Financial difficulties

Overall, the majority (51.5%) reported that BNPL had a positive effect on their financial situation. However, using BNPL had a detrimental impact on more than 1 in 10 respondents (11.3%).Footnote 73 Concerningly, 35.5% of respondents had problems paying instalments. More than half of these respondents (57%) reported having insufficient funds due to expenses exceeding their income, health problems, job loss, or earning less than they had anticipated. Many cited fees or interest imposed by BNPL providers for late payments (43.7%) as a reason for their financial difficulties. 14.1% of those who had difficulties meeting BNPL instalments also reported incurring interest on their credit cards, which ostensibly exacerbated their financial hardship. A quarter of respondents (25.1%) reported being contacted by debt collectors after failing to pay BNPL instalments on time. When asked whether BNPL providers were willing to assist them with their payment difficulties, 60.6% were given more time to pay, 18.3% had their debts reduced. Nonetheless, nearly 1 in 5 (19.7%) were unable to obtain any assistance from providers, with 14.1% saying the provider refused to help them and 5.6% were unable to contact the provider.Footnote 74

Extended comments

In the extended comments, respondents highlighted the need for more transparency. In particular, clearer explanations of the charges were required upfront, with specific details of penalties or interest imposed for late payments. One respondent recounted that there were charges which they did not know about until they asked for clarification. Suggestions included reminding consumers of the potential cost of using BNPL before they entered into a transaction. They also emphasised the need for more user-friendly explanations that consumers can easily understand, such as explanatory videos.

Respondents further observed that it was ‘easy to fall into the trap of excessive spending’, suggesting the need for measures to ensure that repayments are affordable, such as credit limits and affordability checks. They noted that greater flexibility, more time to pay without interest, and lower charges or interest rates would also be advantageous for consumers. Better consumer education about the costs and risks of BNPL, and skills training in managing personal finances and avoiding debt traps and predatory business practices, would help foster resilience amid increasingly easy access to credit.

Several consumers called for stronger government regulation and oversight of the BNPL industry, while several respondents noted the need for stronger personal data protection. Calls to reduce the price of goods resonate with the significant levels of financial hardship reflected in the use of BNPL to purchase necessities: 49.3% of respondents indicated they used BNPL because they did not have enough money, and 35.5% of respondents reported difficulties paying instalments.

Focus groups

Focus group participants were asked about their experiences with BNPL; whether it was clear from the websites or apps that BNPL is a type of borrowing or loan; whether the fees for late payments or administration were clearly communicated upfront; the pros, cons and attractions of BNPL; and what changes they would recommend for better consumer protection. Participants observed that BNPL is useful as it allows people with budget constraints the flexibility to make larger purchases, reducing the financial burden of upfront payments.Footnote 75 The comments from the focus groups align with the survey findings. For instance, several participants said that they were drawn to use BNPL when providers offered ‘cash incentives’ and ‘savings’ for new users.Footnote 76 Like many survey respondents, the focus groups noted that the advertising of ‘zero interest’ is ‘very attractive’ but observed a lack of transparency around fees. They noted the obscurity around the amount of fees for late payments.Footnote 77 In the words of a participant, ‘you have to look it up … it’s not like … zero interest, [which is] very big.’Footnote 78 The amount of late payment fees is often on another webpage, among other terms and conditions. Participants described these terms as ‘lengthy’, ‘too wordy’, and ‘worded in a way that is very confusing’. They noted that ‘some people can be (sic) lost in the terms’ and ‘mostly we just want to check out really fast, so we don’t really click on the terms and conditions and read through all the late payment charges.’Footnote 79

Participants said that they only found out the amount of late payment fees when they were charged.Footnote 80 One participant recounted being charged RM20 for an instalment of RM50, remarking that the fee was disproportionately high and that this was ‘not communicated’ earlier.Footnote 81 Another participant said that ‘a lot of my friends ran into’ problems with ‘late penalty fees’ and ‘didn’t know how much the fees were’ before that.Footnote 82 A third participant added that they won’t ‘give you a warning about how much you will need to pay if you don’t manage to pay on time.’Footnote 83 The lack of transparency around administrative fees was also raised. According to one student, ‘they will tell you on their website, but if you don’t actively look for it, then it can come as a bit of a surprise’.Footnote 84 Another participant mentioned ‘hidden fees’, saying that when you ‘look at your account’ and find money missing ‘then you find out that actually there is an administrative fee.’Footnote 85

Several comments from the focus groups also resonate with the proposition that BNPL’s advertising and structure play into behavioural biases.Footnote 86 In relation to instalments, they noted that ‘visually it looks like you’re paying less’ and it’s like the TikTok trend, Girl Math – if an item costs RM1,000 ‘and I use it for 3 years, it’s just RM1 a day’.Footnote 87 Although some participants said that it was clear that they were borrowing money, one remarked, ‘I wouldn’t say it’s borrowing money, they’re instalments’, resonating with the perception of BNPL as a smart ‘way to pay’ rather than as debt or credit. The propensity towards impulse buying was also reflected in participants’ comments that they had shopaholic friends or family members who ‘very easily spend too much’ and ‘go into debt.’Footnote 88 Participants noted that it was difficult to keep track of payment obligations, especially when making multiple purchases across multiple BNPL providers. One participant said BNPL is popular among students and that ‘a lot of friends’ use it, while another said they had been cautioned by friends against using it.

Suggestions for improving consumer protection included displaying ‘fees and charges prominently’ and having a pop-up warning that ‘is very easy to understand, like a drawing or comics … that makes you understand that this is borrowing money … don’t spend more than you can afford. Spend wisely and responsibly.’Footnote 89 Another participant commented on the need for better customer service by some providers: ‘Instead of using a bot, maybe can we have a human.’

Interview with consumer advocates

The author interviewed two CAP staff members who assist consumers with complaints. The interview was held on Zoom in December 2023. CAP staff were asked about their views on BNPL, the cost of living and any concerns they may have had relating to consumers. They said they had not received any complaints about BNPL. They noted that BNPL is easily accessible with minimal eligibility requirements, such as only needing to ‘show that they have used Grab for 6 months’ and falling ‘within certain age group – above 21 years and below senior citizen.’ They cautioned against acting ‘on the spur of the moment’ and advised consumers to ensure they can pay on time before using BNPL, noting the potentially high late payment charges and the risk of increasing indebtedness.

CAP staff mentioned that they had received complaints about the rising cost of living. Food is too expensive, and consumers are under pressure to reduce their food intake and leave fruits, vegetables, and fish out of their diets to reduce their costs. Social security is insufficient and low-income earners (B40)Footnote 90 receive a token sum. They have to ‘weigh whether to fill their stomachs or eat nutritious food’ and ‘look for a second or even a third job’, leaving their children neglected at home, which, in turn, leads to social problems. Consumers are also ‘dipping into EPFFootnote 91 meant for retirement’, depleting ‘their meagre retirement funds.’

Consumer advocates also raised concerns about ruthless debt-collection practices. They received reports of debt collectors using ‘scare tactics’, ‘saying they are from a lawyer’s office’, ‘calling any phone number related to the debtor’, and making debtors fearful. They noted that the Consumer Credit Oversight Board Task Force is gathering feedback from interested parties and the public on the Consumer Credit Act to address these issues.

Analysis

Both the survey and focus groups emphasised the lack of transparency around fees. More than 1 in 5 survey respondents who missed a payment did not realise that they would be charged a fee, and 46.5% of respondents who incurred fees were charged more than expected. The survey of websites also indicated that fee disclosures were relatively inconspicuous and overshadowed by bright, bold advertising that emphasises ‘zero interest’. Focus group participants noted a tendency to act on conspicuous, readily available information, highlighting the challenges of accessing fee disclosures in small, dense print on separate webpages amid large amounts of information. Dense, relatively small text in long lines is visually unappealing and difficult to read.Footnote 92 When presented with large amounts of information perceived as boring or pointless, research suggests that information overload often leads consumers to ignore the fine print.Footnote 93 Such advertising is contrary to best practice for effective risk disclosure,Footnote 94 and judicial decisions have criticised practices that require consumers to find their way to the truth past misleading claims.Footnote 95

The need for effective disclosure of fees and risks to facilitate informed decisions is bolstered by findings from the focus groups, which reveal how marketing strategies play on behavioural biases. These include breaking down the cost into four instalments, creating the perception that items are more affordable, and the tendency to seek immediate gratification without thinking about potential future costs. Insights from behavioural economics reveal that consumers commonly find financial decisions difficult, and many ‘lack motivation to invest time and effort to make informed decisions.’Footnote 96

The survey responses also reflect a degree of financial hardship. Over a third (35.5%) of respondents experienced difficulties paying instalments on time, and 83.8% who missed a payment incurred fees. Fees or interest for late payments caused financial hardship for 43.7% of respondents. These findings resonate with the experiences of BNPL consumers in other countries who ended up paying fees or interest, at times on their credit cards, despite the promise of ‘zero fees.’Footnote 97 The risks of harm to vulnerable consumers from ‘falling into a debt spiral’ as a result of high-cost credit, as borrowers channel greater proportions of their income towards repayments, lead to entrenched disadvantage and adverse effects on consumers’ health and well-being.Footnote 98 These findings underscore the importance of regulatory intervention to facilitate informed decisions and to guard against risks of over-indebtedness. At the same time, there is an urgent need to address the problem of poverty, reflected in the finding that close to half (49.3%) used BNPL because they lacked sufficient money. More than 40% of respondents used BNPL to purchase essential items such as groceries, utilities, and school equipment, including uniforms.

Regulatory reforms

Malaysian law reformers have recently introduced the Consumer Credit Act 2025 to address gaps in the fragmented legal framework for consumers of non-bank credit,Footnote 99 drawing from the experience of countries such as the UK and Australia.Footnote 100 The reforms require businesses that provide consumer credit to be licensed, their senior management to be fit and proper persons, and they must undertake their activities in a fair, responsible and professional manner.Footnote 101 The legislation envisages the issuance of regulations or further guidelines relating to business conduct, including advertising practices; transparency and disclosure; ensuring that information provided to consumers is accurate, clear and timely; affordability assessments; complaints handling, and fair debt collection.Footnote 102 In addition, the new laws state that credit consumers may apply for hardship assistance from a credit provider.Footnote 103

A critical aspect of effective consumer credit regulatory frameworks which appears to have been sidelined relates to enforcement mechanisms.Footnote 104 Access to free external dispute resolution (EDR) provides consumers with an important avenue for redress when credit providers breach the rules.Footnote 105 Both the Australian and UK regulatory frameworks for consumer credit require firms to be members of free EDR providers.Footnote 106 This has not been adopted by the Malaysian reforms, which envisage that complaints may be lodged with the regulators.

The survey results indicate that a substantial proportion of respondents used BNPL because they did not have enough money. In such circumstances, free EDR plays a critical role in providing access to justice, particularly for low-income consumers for whom the cost of legal advice or litigation would be prohibitive.Footnote 107 The absence of free EDR for credit consumers leaves a significant gap in enforcement mechanisms. If the Financial Markets Ombudsman Service’s existing jurisdiction were extended to consumer credit, including BNPL, vulnerable consumers in financial difficulty would be able to have their disputes resolved quickly, alleviating their financial stress. Such accountability also incentivises credit providers to comply with their obligations to act in a fair, responsible and professional manner.

The protection of vulnerable credit consumers is one of the key objectives of the Malaysian reforms.Footnote 108 The effectiveness of consumer credit laws in improving industry standards is contingent on strong regulatory supervision and enforcement.Footnote 109 Avoidance strategies are a recurrent problem in the consumer credit industry,Footnote 110 and robust regulatory supervision is crucial.Footnote 111 The empirical findings of the present research suggest the need for specific measures, including user-friendly disclosure of costs and risks, to protect vulnerable Malaysian BNPL consumers from harm.

Transparency

The Consumer Credit Act 2025 seeks to promote informed consumer decisions by promoting transparent disclosure of information.Footnote 112 To facilitate informed decisions by vulnerable consumers, particularly those with limited financial knowledge, regulatory guidance should require the nature of risks to be disclosed as prominently as the benefits.Footnote 113 Merely disclosing percentages or fee formulas is inadequate. The need to calculate total costs using obscure mathematical formulas is a barrier to those who lack financial knowledge. Such disclosure has limited value for low-income, vulnerable consumers who struggle with the ‘humiliation of admitting an inability to understand’ and leads to poorly informed risk-taking.Footnote 114 With advances in technology, websites can and should incorporate cost calculators which automatically display the full cost of borrowing in Ringgit, including fees for late payment, before consumers enter transactions.

Research suggests that BNPL fees are often comparable to those of high-cost credit.Footnote 115 Repeated use of high-cost credit is known to be a debt trap that entrenches vulnerable consumers in financial disadvantage. In addition, the fees that consumers unwittingly incur on their credit cards, from which BNPL payments are automatically deducted, also heighten the risk of increasing indebtedness that exacerbates financial difficulties. Such adverse consequences from BNPL use are reflected in the consumer survey. The risks warrant warnings about potential detrimental consequences before entering into transactions.Footnote 116 A warning that missed payments will incur specified fees and affect their credit record, together with signposts directing consumers to financial hardship assistance, would be consistent with responsible advertising standards. Risk warnings are especially relevant given the marketing of BNPL as a cost-saving ‘way to pay’. Clear communication is essential, such as a ‘pop up’ warning using illustrations that vulnerable consumers will understand, making it clear that they are borrowing money, and cautioning against spending more than they can afford to repay.

Easy access to digital credit 24/7 with a few clicks of a mouse, frequently emerging on shopping websites as a ‘way to pay by instalments’ at the point of purchase, further warrant adequate warnings against the risk of over-indebtedness. Discounts or rewards create the impression of ‘savings’ that mask the risks, and artificial intelligence enables advertising to emerge when debtors are potentially vulnerable.Footnote 117 The majority of survey respondents indicated that they were drawn to BNPL providers’ digital interfaces or applications, which have been likened to social platforms, and focus group participants mentioned ‘shopaholic’ friends or family members who easily fell into debt.

To alleviate such harm, user-friendly cost disclosures, including an automatic cost calculator and risk warnings, should be mandated across the full range of digital interactions used by credit providers, including phone apps, social media advertising, and BNPL payments on merchants’ sites. Notably, one suggestion from the consumer survey was to include more videos explaining the costs and risks of BNPL. The use of multimedia, such as short videos that explain risks, is supported by FinCoNet, an international network of supervisory authorities for financial consumer protection.Footnote 118 Visual representations of how debt spirals occur in the context of BNPL are likely to be more effective in communicating risks to visual learners, including millennials and consumers with lower literacy levels.Footnote 119 Further, Malaysia has about 2.2 million documented migrant workers, an estimated 1.2 to 3.5 million undocumented migrants primarily from other Southeast Asian and South Asian countries, and approximately 182,820 refugees and asylum seekers.Footnote 120 Many migrants and refugees know little or no English or Bahasa Malaysia. Hence, it is critical that the Ringgit amount of late payment fees be disclosed prominently upfront, as are the advertisements of ‘zero interest’, and that risk warnings be clear and simple. As suggested by a focus group participant, illustrations could enhance the effectiveness of risk warnings.

Likewise, there is value in broader financial education for higher-risk groups, such as young adults, who are often considered a target demographic for BNPL and often lack financial experience. Proactive supervision by the regulator is crucial, given that financially stressed, vulnerable consumers often lack the requisite knowledge, time, and resources to seek redress for claims arising from misleading conduct.Footnote 121 These challenges are compounded by a sense of ‘shame, failure and a fear of being judged’ that individuals commonly experience when faced with debt problems.Footnote 122

Financial hardship

BNPL consumers are far from homogeneous, with varying income levels. Their BNPL use differs depending on individual circumstances. The focus group emphasised the utility of BNPL for ‘budget smoothing’, such as purchasing a laptop by instalments. At the same time, they observed risks inherent in easy access to credit, including impulse buying and losing track of multiple repayment obligations. Challenges arise particularly when consumers are in precarious financial situations. Although data collected by the Consumer Credit Oversight Board Task Force suggests that most (96%) of the consumers they surveyed paid on time, research has shown that timely payments can mask the extent of financial hardship as people tend to prioritise BNPL payments, cutting back on essentials or using other forms of credit to cover BNPL instalments.Footnote 123 The present survey indicates that some respondents incurred credit card fees when paying BNPL instalments.

Over a third (35.5%) of survey respondents reported having difficulties meeting payment obligations. Health problems, loss of employment or earning less than expected were cited as reasons for respondents’ challenges in making repayments. For some, their use of BNPL was driven by the inability to make ends meet. In such situations, they would have struggled to meet repayment schedules, incurring fees for missed payments, which exacerbated their financial problems.Footnote 124 A proportion of survey respondents who indicated that they used BNPL due to a lack of adequate funds bought essential items with BNPL, experienced hardship due to late fees, and had poorer long-term financial outcomes. Likewise, the interview with CAP highlighted the substantial challenges that lower-income consumers face with the rising cost of living.

At first blush, BNPL fees for missed payments may not seem high. However, studies that have calculated the equivalent interest rates have refuted this perception.Footnote 125 Malaysian law reformers have proposed prohibiting providers from imposing excessive or unreasonable fees, though it is unclear at this juncture how reasonableness will be determined.Footnote 126 To address high BNPL fees, one option is to introduce a fee cap.Footnote 127 Consumer advocates have also suggested prohibiting the use of credit cards to pay for BNPL debt to avoid incurring high interest charges.Footnote 128

The Consumer Credit Act 2025 introduces financial hardship provisions.Footnote 129 Credit providers must give due consideration to varying a credit agreement if consumers are unable to meet payment obligations due to financial hardship, and debt recovery is paused while the hardship application is assessed.Footnote 130 Nevertheless, credit providers have the discretion to determine the form and manner of assistance, if any.Footnote 131 The new laws state that the Consumer Credit Commission may issue guidelines on the circumstances that qualify as financial hardship, and the assistance it warrants.Footnote 132

In developing the guidelines for credit providers, Malaysian regulators could potentially draw lessons from Australia. While financial hardship provisions appear to be promising on paper, in practice, Australian experience indicates that financial hardship provisions, similar to those adopted in the Consumer Credit Act 2025, have offered limited respite.Footnote 133 The most common variation is to allow consumers more time to pay. However, studies have shown that this is inadequate for consumers facing chronic long-term financial hardship who simply cannot afford to pay, even with an extension of time.Footnote 134 Fewer providers are willing to allow reductions in amounts. Credit providers have also been criticised for being inconsistent, ‘difficult to contact and communicate with’, ‘not being responsive to the needs of clients,’ failing to understand financial hardship, ‘being judgmental’ and ‘not responding appropriately to family violence.’Footnote 135 The lack of appropriate support is especially detrimental to vulnerable consumers such as those with mental illness and victims of financial abuse or identity theft.Footnote 136 The challenges are ostensibly greater in Malaysia, where the stigma associated with mental illness is prevalent,Footnote 137 and there is less community awareness of family violence-related financial abuse against a backdrop of political and cultural distrust of women’s activists.Footnote 138

Experience suggests that access to free EDR is important for consumers aggrieved by their credit provider’s response to financial hardship.Footnote 139 Extending the Financial Markets Ombudsman Service to credit consumers will enable financially stressed consumers to seek fairer outcomes and avoid dealing with debt collectors and the escalation of debt. This is important in light of poor practices such as ‘scare tactics’ used in debt collection.Footnote 140 Broader reforms are also needed in debt collection, particularly because Malaysia still has archaic laws that allow debtors to be arrested and imprisoned.Footnote 141 These are unduly harsh and should be repealed.Footnote 142

As part of affordability assessments, consumers are usually required to provide evidence of their income and financial capacity to make repayments. Questions remain about how individuals with insecure work and those in the gig economy will fare under these assessments. Access to credit plays an important role in enabling consumers to improve their quality of life, subject to conditions such as the affordability of interest, fees and repayments. The positive impacts of access to credit are reflected in the consumer survey and focus groups, although these also emphasised the need for transparency. From a broader policy perspective, consumer credit regulation must balance between promoting financial inclusion and providing protection from the adverse impacts of misleading business practices and unmanageable debt.Footnote 143

Credit providers can help redirect financially stressed consumers to appropriate sources of debt help, such as free financial counselling.Footnote 144 Hence, it is essential that the free debt management services provided by the government-sponsored Agensi Kaunseling & Pengurusan Kredit (AKPK)Footnote 145 should be made available to credit consumers. This is essential as businesses that offer debt ‘help’ have often been criticised for predatory practices.Footnote 146 In countries where social security benefits are available for those experiencing financial hardship, credit providers are sometimes required by law to provide consumers with information on how to access social security and free debt help, while warning of the high cost of credit.Footnote 147 Social security benefits for Malaysians are far more limited than those of their counterparts in Western industrialised countries.Footnote 148 Consequently, signposting consumers to cheaper alternative sources of funding is more challenging due to the limitations in the social safety net.

Poverty & social protection

Affordability limits guard against individuals falling into debt spirals but may have unintended consequences of further excluding some of the most vulnerable consumers from access to funds necessary for their basic living expenses. In tandem with the introduction of the Consumer Credit Act, there is an urgent need for measures to alleviate the underlying problem of poverty that propels consumers to rely on BNPL to make ends meet. While UK and Australian laws have often served as a model for reforms in common law Asia, it is important to consider significant differences in the fabric of social protection, which forms an inextricable part of the affordability measures that underpin safeguards for credit consumers. Malaysia is a newly industrialised Southeast Asian country with a significantly lower gross domestic product (GDP) per capita.Footnote 149 In addition to the disparity in poverty levels, there are fewer social protection mechanisms in place for vulnerable individuals, increasing the risks of adverse consequences for the hard-core poor who rely on credit to survive.Footnote 150

An OECD cross-country comparison described the scope of Malaysia’s social protection as ‘very limited’, well below that of Australia, China, India, Japan, and neighbouring countries such as Singapore and Thailand.Footnote 151 Unlike the UK and Australia, common law countries whose laws continue to serve as a model for Malaysian law reformers, Malaysia does not have unemployment benefits, family or child allowances, or an old-age pension apart from the Employees Provident Fund.Footnote 152 Recent studies highlight the many gaps through which various segments of Malaysian society fall, including middle-income earners who struggle with the rising cost of living, people with disabilities, workers in the gig economy, the unemployed, the aged who do not have retirement savings, migrant workers, refugees and indigenous communities.Footnote 153 In the absence of adequate social security benefits, vulnerable individuals turn to credit, and the adverse consequences are reflected in personal loans being the main cause of bankruptcy in Malaysia.Footnote 154 Without access to alternative sources of sustenance, financial deprivation may drive some of the most vulnerable to destitution, insolvency or illegal moneylenders who are known to engage in far more predatory lending practices and abusive debt collection tactics.Footnote 155

Scholars and government reports emphasise the need for interest-free or other affordable credit for low-income earners, and for government support for vulnerable individuals to cover their basic needs and tide them through unforeseen, unaffordable financial shocks.Footnote 156 The urgent need for broader reforms to address the underlying problem of poverty is reflected in the consumer survey discussed earlier, in which many respondents cited a lack of funds as a reason for using BNPL. These resonate with concerns over the rising cost of living,Footnote 157 and a recent poll which found that 86.6% of the Malaysian adults surveyed were experiencing financial stress.Footnote 158

Even in countries where social security benefits are more readily available, insufficient income has resulted in vulnerable communities relying on BNPL for essentials.Footnote 159 One of the innovations that has helped to bridge the gap is the no-interest loan scheme run by not-for-profit organisations in partnership with banks.Footnote 160 These genuinely interest-free and fee-free loans, designed with vulnerable communities in mind, do not entail problems of debt spirals or harsh debt collection methods. Nascent initiatives by not-for-profit organisations to provide interest-free microcredit to low-income microentrepreneurs, in collaboration with companies through social responsibility programmes, are exemplars for further developing similar measures to alleviate poverty.Footnote 161 Recent changes to Bursa Malaysia’s sustainability reporting framework for listed companies, along with tax deductions for donations to approved organisations, provide further incentives towards such developments.Footnote 162 Likewise, as environmental and social governance has grown increasingly important to investors and employees,Footnote 163 there is potential for businesses to embed greater social responsibility in their core activities by offering concession prices to vulnerable communities to help counter the rising cost of living. Another innovation is the debt consolidation plan offered by Singaporean banks to over-indebted individuals at relatively low interest rates.Footnote 164 These allow debtors to escape debt spirals from high-cost credit and provide them with some breathing space to turn their financial situation around, without the stress of being pursued by debt collectors.

Conclusion

As BNPL continues to gain traction in many parts of the world, Malaysian law reformers are seeking to mitigate the risks to vulnerable consumers through the Consumer Credit Act 2025. The new legislation sets out protections that resonate with consumer credit laws from countries with established regulatory frameworks.Footnote 165 These protections would be more effective if consumers had access to free EDR to seek redress when credit providers breach their obligations. Likewise, financial hardship provisions are likely to yield better outcomes for consumers if credit providers’ discretion is subject to review by an EDR body such as the Financial Markets Ombudsman Service. In addition, there is a need for regulatory guidance which requires credit providers to clearly warn consumers of the costs and risks of BNPL across the range of digital platforms used. Warnings should be prominent and communicated in a way that is easily understood by consumers with lower levels of financial literacy, such as an automatic cost calculator and illustrations or explanatory videos.

At the same time, it is important to ensure that the consumer credit laws do not have the unintended consequence of further excluding marginalised consumers from credit, leaving them without the means to afford basic necessities. Social security benefits, which form an integral part of social protection mechanisms for the most vulnerable members of society in the more financially developed countries, are far more limited in Malaysia. Such social security is an integral aspect of the capacity to afford the basic cost of living in countries on which Malaysia’s consumer credit laws are modelled. Affordability checks in the UK and Australia, intended to protect vulnerable consumers from unmanageable debt, are often premised on the assumption that vulnerable individuals receive social security benefits. Without such social protection and the ability to make ends meet, vulnerable families could be driven to destitution, homelessness or insolvency, or turn to illegal moneylenders who are far more predatory and harmful. Consequently, there is an urgent need to increase the availability and amount of social security benefits, or to pursue collaborative initiatives with the private sector, to address poverty alongside the regulation of consumer credit. Interest-free loans for low-income or financially stressed consumers, and free debt help from AKPK, are also required to fulfil the underlying objective of promoting better outcomes for vulnerable consumers.

Open access

Open access