Δ

Δ

1. Introduction

The theory of backward stochastic differential equations (BSDEs), initiated by Bismut [Reference Bismut7] and Pardoux and Peng [Reference Pardoux and Peng32], has been extensively studied over the past three decades, particularly in relation to stochastic control, finance, and insurance (see e.g. [Reference Delong17, Reference Zhang39]). Important applications include dynamic risk measures [Reference Barrieu and El Karoui4] and g-expectations [Reference Coquet, Hu, Memin and Peng16, Reference Peng33], which generalize classical expectations and martingales to nonlinear settings. Recent applications to financial economics include [Reference Beissner, Lin and Riedel6], [Reference Bouchard, Fukasawa, Herdegen and Muhle-Karbe8], [Reference Gonon, Muhle-Karbe and Shi20], [Reference Herdegen, Muhle-Karbe and Possamaï24], [Reference Kardaras, Xing and Žitkovi28], and [Reference Muhle-Karbe, Nutz and Tan30].

While BSDEs are powerful theoretical tools, their solutions are typically implicit and require discretization for numerical implementation. As discrete analogs, backward stochastic difference equations (BS

$\Delta$

Es) have been widely studied, falling into two main categories. The first focuses on BS

$\Delta$

Es) have been widely studied, falling into two main categories. The first focuses on BS

$\Delta$

Es as weak approximations of BSDEs [Reference Briand, Delyon and Mémin9, Reference Briand, Delyon and Mémin10, Reference Briand, Geiss, Geiss and Labart11, Reference Cheridito and Stadje12, Reference Ma, Protter, Martín and Torres29, Reference Nakayama31, Reference Stadje35, Reference Tanaka37]. The second explores the structure of BS

$\Delta$

Es as weak approximations of BSDEs [Reference Briand, Delyon and Mémin9, Reference Briand, Delyon and Mémin10, Reference Briand, Geiss, Geiss and Labart11, Reference Cheridito and Stadje12, Reference Ma, Protter, Martín and Torres29, Reference Nakayama31, Reference Stadje35, Reference Tanaka37]. The second explores the structure of BS

$\Delta$

Es themselves. A general framework is provided in [Reference Cohen and Elliot15], while specific cases involving driving martingales with the predictable representation property are studied in [Reference Cohen and Elliott14] and [Reference Elliott, Siu and Cohen19].

$\Delta$

Es themselves. A general framework is provided in [Reference Cohen and Elliot15], while specific cases involving driving martingales with the predictable representation property are studied in [Reference Cohen and Elliott14] and [Reference Elliott, Siu and Cohen19].

This paper falls into the second category and studies a class of BS

$\Delta$

Es including the one introduced in [Reference Nakayama31] and [Reference Tanaka37], where a d-dimensional scaled random walk – whose increments take only

$\Delta$

Es including the one introduced in [Reference Nakayama31] and [Reference Tanaka37], where a d-dimensional scaled random walk – whose increments take only

$d+1$

values – is used to approximate Brownian motion in BSDEs. Such a random walk is minimal among discrete-time processes that converge to d-dimensional Brownian motions. The weak convergence of this BS

$d+1$

values – is used to approximate Brownian motion in BSDEs. Such a random walk is minimal among discrete-time processes that converge to d-dimensional Brownian motions. The weak convergence of this BS

$\Delta$

E to the BSDE was proved in [Reference Nakayama31], and the convergence rate in a Markovian setting was given in [Reference Tanaka37], generalizing the one-dimensional case in [Reference Briand, Geiss, Geiss and Labart11].

$\Delta$

E to the BSDE was proved in [Reference Nakayama31], and the convergence rate in a Markovian setting was given in [Reference Tanaka37], generalizing the one-dimensional case in [Reference Briand, Geiss, Geiss and Labart11].

This minimal BS

$\Delta$

E is computationally efficient, as it involves only a

$\Delta$

E is computationally efficient, as it involves only a

$(d + 1)$

-dimensional problem, in contrast to a

$(d + 1)$

-dimensional problem, in contrast to a

$2^d$

-dimensional problem required when using d-dimensional Bernoulli random walks [Reference Cheridito and Stadje12]. Although Cohen and Elliott [Reference Cohen and Elliot15] have developed a general BS

$2^d$

-dimensional problem required when using d-dimensional Bernoulli random walks [Reference Cheridito and Stadje12]. Although Cohen and Elliott [Reference Cohen and Elliot15] have developed a general BS

$\Delta$

E theory, we focus on the specific structure of this minimal BS

$\Delta$

E theory, we focus on the specific structure of this minimal BS

$\Delta$

E, which exhibits properties not covered in their general framework. In the one-dimensional case, it reduces to a BS

$\Delta$

E, which exhibits properties not covered in their general framework. In the one-dimensional case, it reduces to a BS

$\Delta$

E on a binomial tree, studied in [Reference Elliott, Siu and Cohen19] in the context of dynamic risk measures. We treat the general multi-dimensional setting here.

$\Delta$

E on a binomial tree, studied in [Reference Elliott, Siu and Cohen19] in the context of dynamic risk measures. We treat the general multi-dimensional setting here.

Our key contribution is to identify a gradient constraint on the BS

$\Delta$

E driver, which endows the solution with certain properties as a generalized conditional expectation. This allows us to link the driver to a measure change for the driving random walk, and apply these insights to market equilibrium analysis.

$\Delta$

E driver, which endows the solution with certain properties as a generalized conditional expectation. This allows us to link the driver to a measure change for the driving random walk, and apply these insights to market equilibrium analysis.

The g-expectation is part of the solution of a BSDE or BS

$\Delta$

E, and generalizes the expectation and the certainty equivalent of an expected utility. A subclass of them with concavity and translation invariance has been employed as the utility functional for market equilibrium analyses in [Reference Antar and Dempster3], [Reference Cheridito, Horst, Kupper and Pirvu13], [Reference Horst, Pirvu and Dos Reis25], and [Reference Kardaras, Xing and Žitkovi28]. In this paper, we also apply our BS

$\Delta$

E, and generalizes the expectation and the certainty equivalent of an expected utility. A subclass of them with concavity and translation invariance has been employed as the utility functional for market equilibrium analyses in [Reference Antar and Dempster3], [Reference Cheridito, Horst, Kupper and Pirvu13], [Reference Horst, Pirvu and Dos Reis25], and [Reference Kardaras, Xing and Žitkovi28]. In this paper, we also apply our BS

$\Delta$

E to a market equilibrium analysis. In contrast to the preceding studies, which place an emphasis on incomplete markets, we are interested in explicit computations in a dynamically complete market.

$\Delta$

E to a market equilibrium analysis. In contrast to the preceding studies, which place an emphasis on incomplete markets, we are interested in explicit computations in a dynamically complete market.

Anderson and Raimondo [Reference Anderson and Raimondo2] proved the existence of equilibrium in a continuous-time dynamically complete market by means of non-standard analysis, where an approximation to a Brownian motion by a minimal random walk played a key role. We consider a simpler dynamically complete market to derive explicit conditions for market equilibrium.

Under a unique equivalent martingale measure, our asset price model is a multi-dimensional extension of the recombining binomial tree. In our approach, an asset price process is given as a stochastic process taking values on a lattice. We do not argue the existence of an equilibrium price but characterize the agents’ utilities under which the given discrete (in both time and space) price process is to be in general equilibrium. This feature is in contrast to the preceding studies [Reference Antar and Dempster3], [Reference Cheridito, Horst, Kupper and Pirvu13], and [Reference Horst, Pirvu and Dos Reis25] and similar to [Reference Bouchard, Fukasawa, Herdegen and Muhle-Karbe8], [Reference He and Leland23], [Reference Kardaras, Xing and Žitkovi28], and [Reference Sekine34] in continuous time.

Our framework includes heterogeneous agents with exponential utilities under heterogeneous beliefs. Their risk-aversion coefficients may be stochastic and time-varying. We observe in particular that under equilibrium with heterogeneous beliefs, agents trade with each other, even in the absence of random endowments to hedge, complementing earlier studies of heterogeneous beliefs [Reference Basak5, Reference Hara21, Reference Harris and Raviv22, Reference Jouini and Napp26, Reference Muhle-Karbe, Nutz and Tan30, Reference Varian38].

In Section 2.1 we describe a lattice in

$\mathbb{R}^d$

where a stochastic process

$\mathbb{R}^d$

where a stochastic process

$\{X_n\}$

takes values, and give some elementary linear algebraic lemmas as a preliminary. In Section 2.2 we introduce the process

$\{X_n\}$

takes values, and give some elementary linear algebraic lemmas as a preliminary. In Section 2.2 we introduce the process

$\{X_n\}$

that is the source of randomness in this paper and generates a filtration. It is minimal in the sense that the increment

$\{X_n\}$

that is the source of randomness in this paper and generates a filtration. It is minimal in the sense that the increment

$\Delta X_n$

takes values in a set

$\Delta X_n$

takes values in a set

$\{v_0,\ldots,v_d\}$

of

$\{v_0,\ldots,v_d\}$

of

$d+1$

points in

$d+1$

points in

$\mathbb{R}^d$

. Some elementary measure change formulas are also given as a preliminary.

$\mathbb{R}^d$

. Some elementary measure change formulas are also given as a preliminary.

In Section 2.3 our BS

$\Delta$

E

$\Delta$

E

\begin{equation*} \Delta Y_n = -g_n(Z_n) + Z_n^\top \Delta X_n,\quad Y_N = Y,\end{equation*}

\begin{equation*} \Delta Y_n = -g_n(Z_n) + Z_n^\top \Delta X_n,\quad Y_N = Y,\end{equation*}

is formulated. Due to the minimality of

$\{X_n\}$

, there exists a unique solution

$\{X_n\}$

, there exists a unique solution

$\{(Y_n,Z_n)\}$

to the above equation, without orthogonal martingale terms needed in [Reference Briand, Delyon and Mémin10] and [Reference Cheridito and Stadje12]. The process

$\{(Y_n,Z_n)\}$

to the above equation, without orthogonal martingale terms needed in [Reference Briand, Delyon and Mémin10] and [Reference Cheridito and Stadje12]. The process

$\{X_n\}$

itself takes more than

$\{X_n\}$

itself takes more than

$d+1$

points, so this BS

$d+1$

points, so this BS

$\Delta$

E is different from the one studied in [Reference Cohen and Elliott14]. The g-expectation

$\Delta$

E is different from the one studied in [Reference Cohen and Elliott14]. The g-expectation

$\mathcal{E}^g_n$

for

$\mathcal{E}^g_n$

for

$g = \{g_n\}$

is defined by

$g = \{g_n\}$

is defined by

$\mathcal{E}^g_n(Y) = Y_n$

. Proposition 2.1 concerns the case

$\mathcal{E}^g_n(Y) = Y_n$

. Proposition 2.1 concerns the case

$g_n(z) = f_n(X_{n-1},z)$

and

$g_n(z) = f_n(X_{n-1},z)$

and

$Y_N = h(X_N)$

for deterministic functions

$Y_N = h(X_N)$

for deterministic functions

$f_n$

and h to provide a nonlinear Feynman–Kac-type formula, which is a computationally efficient recurrence equation on the lattice for a deterministic function

$f_n$

and h to provide a nonlinear Feynman–Kac-type formula, which is a computationally efficient recurrence equation on the lattice for a deterministic function

$u_n$

such that

$u_n$

such that

$Y_n = u_n(X_n)$

.

$Y_n = u_n(X_n)$

.

Section 2.4 is about the aforementioned gradient constraint. First we observe that the g-expectation is a conditional expectation when

$g_n$

are linear with slope coefficients included in the convex hull

$g_n$

are linear with slope coefficients included in the convex hull

$\Theta$

of the set

$\Theta$

of the set

$\{v_0,\ldots,v_d\}$

. The importance of this constraint on the slope is a special feature of our BS

$\{v_0,\ldots,v_d\}$

. The importance of this constraint on the slope is a special feature of our BS

$\Delta$

E, and to the best of our knowledge has not been recognized in the preceding studies of multi-dimensional BS

$\Delta$

E, and to the best of our knowledge has not been recognized in the preceding studies of multi-dimensional BS

$\Delta$

Es. A balance condition introduced by Cohen and Elliot [Reference Cohen and Elliot15] for a comparison theorem to hold is translated in terms of

$\Delta$

Es. A balance condition introduced by Cohen and Elliot [Reference Cohen and Elliot15] for a comparison theorem to hold is translated in terms of

$\Theta$

for our BS

$\Theta$

for our BS

$\Delta$

E. We also prove a robust representation when

$\Delta$

E. We also prove a robust representation when

$g_n$

are concave, where the set

$g_n$

are concave, where the set

$\Theta$

again plays an important role. In Section 2.5 we show that a translation-invariant filtration-consistent nonlinear expectation is a g-expectation.

$\Theta$

again plays an important role. In Section 2.5 we show that a translation-invariant filtration-consistent nonlinear expectation is a g-expectation.

In Section 3 we regard

$\{X_n\}$

as a d-dimensional asset price process. In Section 3.1 we consider an optimal investment strategy which maximizes the g-expectation of terminal wealth. By the minimality, the market is complete, extending the well-known binomial tree model for a one-dimensional asset. Our asset price model can be seen as a discrete approximation of the multi-dimensional Bachelier model with constant covariance and general stochastic drift. An advantage of our use of the minimal process as an approximation is that the completeness of the Bachelier model is preserved. Further, the minimality property naturally arises in a variance swap pricing model as illustrated in Example 3.2. In Sections 3.2–3.4 we give a market equilibrium analysis. We consider agents whose utility functionals are g expectations and seek conditions on those g expectations under which

$\{X_n\}$

as a d-dimensional asset price process. In Section 3.1 we consider an optimal investment strategy which maximizes the g-expectation of terminal wealth. By the minimality, the market is complete, extending the well-known binomial tree model for a one-dimensional asset. Our asset price model can be seen as a discrete approximation of the multi-dimensional Bachelier model with constant covariance and general stochastic drift. An advantage of our use of the minimal process as an approximation is that the completeness of the Bachelier model is preserved. Further, the minimality property naturally arises in a variance swap pricing model as illustrated in Example 3.2. In Sections 3.2–3.4 we give a market equilibrium analysis. We consider agents whose utility functionals are g expectations and seek conditions on those g expectations under which

$\{X_n\}$

is an equilibrium price process.

$\{X_n\}$

is an equilibrium price process.

Throughout our financial application, we have short maturity problems in mind, and so, for brevity, assume interest rates, dividend rates, and consumption rates to be zero as in [Reference Antar and Dempster3], [Reference Cheridito, Horst, Kupper and Pirvu13], [Reference Horst, Pirvu and Dos Reis25], and [Reference Kardaras, Xing and Žitkovi28].

We use the convention that

\begin{equation*} \sum_{i=m}^n a_i= 0\end{equation*}

\begin{equation*} \sum_{i=m}^n a_i= 0\end{equation*}

for any sequence

$\{a_i\}$

if

$\{a_i\}$

if

$m \gt n$

.

$m \gt n$

.

2. BS

$\Delta$

E on a lattice

$\Delta$

E on a lattice

2.1. Lattice

We start by describing a lattice. Let

$\{v_1,\ldots, v_d\}$

be a basis of

$\{v_1,\ldots, v_d\}$

be a basis of

$\mathbb{R}^d$

. The subset

$\mathbb{R}^d$

. The subset

\begin{equation*} L = \Biggl\{\sum_{i=1}^d z_i v_i, \ ; \ z_i \in \mathbb{Z}, i=1,\ldots, d\Biggr\}\end{equation*}

\begin{equation*} L = \Biggl\{\sum_{i=1}^d z_i v_i, \ ; \ z_i \in \mathbb{Z}, i=1,\ldots, d\Biggr\}\end{equation*}

of

$\mathbb{R}^d$

is a d-dimensional lattice generated by the basis. Notice that L admits an alternative expression

$\mathbb{R}^d$

is a d-dimensional lattice generated by the basis. Notice that L admits an alternative expression

\begin{equation} L = \Biggl\{\sum_{i=0}^d n_i v_i, \ ; \ n_i \in \mathbb{N}, i=0,1,\ldots, d\Biggr\},\end{equation}

\begin{equation} L = \Biggl\{\sum_{i=0}^d n_i v_i, \ ; \ n_i \in \mathbb{N}, i=0,1,\ldots, d\Biggr\},\end{equation}

where

$v_0 = -v_1 - \cdots - v_d$

and

$v_0 = -v_1 - \cdots - v_d$

and

$\mathbb{N}$

is the set of the non-negative integers. Let

$\mathbb{N}$

is the set of the non-negative integers. Let

\begin{equation*} \mathbf{v} = [v_0,v_1,\ldots,v_d]\end{equation*}

\begin{equation*} \mathbf{v} = [v_0,v_1,\ldots,v_d]\end{equation*}

be the

$d \times (d+1)$

matrix with

$d \times (d+1)$

matrix with

$v_i$

,

$v_i$

,

$i=0,\ldots, d$

as its column vectors. Put

$i=0,\ldots, d$

as its column vectors. Put

\begin{equation*} \mathbf{1} = (1,\ldots,1)^\top \in \mathbb{R}^{d+1}.\end{equation*}

\begin{equation*} \mathbf{1} = (1,\ldots,1)^\top \in \mathbb{R}^{d+1}.\end{equation*}

The following lemmas will be of repeated use in this paper.

Lemma 2.1. The

$(d+1)\times (d+1)$

matrix

$(d+1)\times (d+1)$

matrix

$(\mathbf{1},\mathbf{v}^\top)$

is invertible.

$(\mathbf{1},\mathbf{v}^\top)$

is invertible.

Proof. We show that the row vectors of

$(\mathbf{1},\mathbf{v}^\top)$

are linearly independent. Suppose

$(\mathbf{1},\mathbf{v}^\top)$

are linearly independent. Suppose

\begin{equation*} (\alpha_0,\ldots,\alpha_d)(\mathbf{1},\mathbf{v}^\top) = 0,\end{equation*}

\begin{equation*} (\alpha_0,\ldots,\alpha_d)(\mathbf{1},\mathbf{v}^\top) = 0,\end{equation*}

or equivalently

\begin{equation*} \sum_{j=0}^d \alpha_j = 0,\quad \sum_{j=0}^d \alpha_j v_j = 0\end{equation*}

\begin{equation*} \sum_{j=0}^d \alpha_j = 0,\quad \sum_{j=0}^d \alpha_j v_j = 0\end{equation*}

for scalars

$\alpha_j$

. By the second equation and the definition of

$\alpha_j$

. By the second equation and the definition of

$v_0$

, we have

$v_0$

, we have

\begin{equation*} \sum_{j=1}^d (\alpha_j -\alpha_0) v_j = 0,\end{equation*}

\begin{equation*} \sum_{j=1}^d (\alpha_j -\alpha_0) v_j = 0,\end{equation*}

from which we can conclude

$\alpha_j = \alpha_0 $

for all j because

$\alpha_j = \alpha_0 $

for all j because

$\{v_1,\ldots,v_d\}$

is a basis. Together with the first equation, we then conclude

$\{v_1,\ldots,v_d\}$

is a basis. Together with the first equation, we then conclude

$\alpha_j = 0$

for all j.

$\alpha_j = 0$

for all j.

Lemma 2.2. Let

$y \in \mathbb{R}^{d+1}$

. The unique solution to the equation

$y \in \mathbb{R}^{d+1}$

. The unique solution to the equation

\begin{equation} y = (\mathbf{1}, \mathbf{v}^\top) z, \quad z = (z_0,z_1,\ldots,z_d)^\top \in \mathbb{R}^{d+1}\end{equation}

\begin{equation} y = (\mathbf{1}, \mathbf{v}^\top) z, \quad z = (z_0,z_1,\ldots,z_d)^\top \in \mathbb{R}^{d+1}\end{equation}

is given by

\begin{equation} z_0 = a(y) \,:\!=\, \frac{1}{d+1} \mathbf{1}^\top y, \quad (z_1,\ldots,z_d)^\top = b(y) \,:\!=\, (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}y. \end{equation}

\begin{equation} z_0 = a(y) \,:\!=\, \frac{1}{d+1} \mathbf{1}^\top y, \quad (z_1,\ldots,z_d)^\top = b(y) \,:\!=\, (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}y. \end{equation}

Proof. By Lemma 2.1, there exists a unique

$z \in \mathbb{R}^{d+1}$

such that (2.2) holds. Since

$z \in \mathbb{R}^{d+1}$

such that (2.2) holds. Since

$\mathbf{v}\mathbf{1} = 0$

, multiplying both sides of (2.2) by

$\mathbf{v}\mathbf{1} = 0$

, multiplying both sides of (2.2) by

$\mathbf{1}^\top$

, we obtain the first equation of (2.3). Also, multiplying both sides of (2.2) by

$\mathbf{1}^\top$

, we obtain the first equation of (2.3). Also, multiplying both sides of (2.2) by

$\mathbf{v}$

and again using

$\mathbf{v}$

and again using

$\mathbf{v}\mathbf{1} = 0$

, we have

$\mathbf{v}\mathbf{1} = 0$

, we have

$\mathbf{v}y = \mathbf{v}\mathbf{v}^\top (z_1,\ldots,z_d)^\top$

. Since

$\mathbf{v}y = \mathbf{v}\mathbf{v}^\top (z_1,\ldots,z_d)^\top$

. Since

$\{v_1,\ldots,v_d\}$

is a basis,

$\{v_1,\ldots,v_d\}$

is a basis,

$\mathbf{v}$

has rank d. Therefore

$\mathbf{v}$

has rank d. Therefore

$\mathbf{v}^\top$

has rank d and so, for any

$\mathbf{v}^\top$

has rank d and so, for any

$x \in \mathbb{R}^d\setminus\{0\}$

,

$x \in \mathbb{R}^d\setminus\{0\}$

,

$x^\top \mathbf{v}\mathbf{v}^\top x = | \mathbf{v}^\top x|^2 \neq 0$

. This implies that the

$x^\top \mathbf{v}\mathbf{v}^\top x = | \mathbf{v}^\top x|^2 \neq 0$

. This implies that the

$d\times d$

matrix

$d\times d$

matrix

$\mathbf{v}\mathbf{v}^\top$

is invertible and, in turn, the second equation of (2.3) is valid.

$\mathbf{v}\mathbf{v}^\top$

is invertible and, in turn, the second equation of (2.3) is valid.

2.2. Probability space

Let

$(\Omega,\mathscr{F},\mathbb{P})$

be a probability space. For a stochastic process

$(\Omega,\mathscr{F},\mathbb{P})$

be a probability space. For a stochastic process

$\{X_n\}_{n \in \mathbb{N}}$

, we put

$\{X_n\}_{n \in \mathbb{N}}$

, we put

$\Delta X_n = X_n - X_{n-1}$

. Let

$\Delta X_n = X_n - X_{n-1}$

. Let

$\{X_n\}$

be a d-dimensional stochastic process with

$\{X_n\}$

be a d-dimensional stochastic process with

$\Delta X_n$

taking values in

$\Delta X_n$

taking values in

$\{v_0,v_1,\ldots,v_d\}$

for all

$\{v_0,v_1,\ldots,v_d\}$

for all

$n \geq 1$

and

$n \geq 1$

and

$X_0 = 0$

. By (2.1),

$X_0 = 0$

. By (2.1),

$X_n$

takes values in L for all

$X_n$

takes values in L for all

$n \in \mathbb{N}$

. Let

$n \in \mathbb{N}$

. Let

$\mathscr{F}_n = \sigma(X_0,\ldots,X_n)$

,

$\mathscr{F}_n = \sigma(X_0,\ldots,X_n)$

,

$ n\in \mathbb{N}$

, be the natural filtration generated by

$ n\in \mathbb{N}$

, be the natural filtration generated by

$\{X_n\}$

, and put

$\{X_n\}$

, and put

$P_n = (P_{n,0},\ldots, P_{n,d})^\top$

for

$P_n = (P_{n,0},\ldots, P_{n,d})^\top$

for

$n\geq 1$

, where

$n\geq 1$

, where

\begin{equation*} P_{n,j} = \mathbb{P}(\Delta X_n = v_j \mid \mathscr{F}_{n-1}), \quad j=0,\ldots, d.\end{equation*}

\begin{equation*} P_{n,j} = \mathbb{P}(\Delta X_n = v_j \mid \mathscr{F}_{n-1}), \quad j=0,\ldots, d.\end{equation*}

Note that

$\{P_n\}$

is a

$\{P_n\}$

is a

$\Delta_d$

-valued predictable process, where

$\Delta_d$

-valued predictable process, where

\begin{equation*} \Delta_d = \bigl\{p \in \mathbb{R}^{d+1}\ ; \ \mathbf{1}^\top p = 1, \ p \geq 0\bigr\}.\end{equation*}

\begin{equation*} \Delta_d = \bigl\{p \in \mathbb{R}^{d+1}\ ; \ \mathbf{1}^\top p = 1, \ p \geq 0\bigr\}.\end{equation*}

We assume

$P_{n,j}$

is positive for all

$P_{n,j}$

is positive for all

$n \geq 1$

and

$n \geq 1$

and

$j = 0,\ldots, d$

. Let

$j = 0,\ldots, d$

. Let

$N \in \mathbb{N}\setminus\{0\}$

. The following lemma will be of repeated use in this paper.

$N \in \mathbb{N}\setminus\{0\}$

. The following lemma will be of repeated use in this paper.

Lemma 2.3. For any

$\Delta_d$

-valued predictable process

$\Delta_d$

-valued predictable process

$\{\hat{P}_n\}$

, there exists a probability measure

$\{\hat{P}_n\}$

, there exists a probability measure

$\hat{\mathbb{P}}$

on

$\hat{\mathbb{P}}$

on

$(\Omega,\mathscr{F}_N)$

such that

$(\Omega,\mathscr{F}_N)$

such that

$\hat{P}_n = (\hat{P}_{n,0},\ldots, \hat{P}_{n,d})^\top$

, where

$\hat{P}_n = (\hat{P}_{n,0},\ldots, \hat{P}_{n,d})^\top$

, where

\begin{equation} \hat{P}_{n,j} = \hat{\mathbb{P}}(\Delta X_n = v_j \mid \mathscr{F}_{n-1}), \quad j=0,\ldots, d, \ n=1,\ldots, N.\end{equation}

\begin{equation} \hat{P}_{n,j} = \hat{\mathbb{P}}(\Delta X_n = v_j \mid \mathscr{F}_{n-1}), \quad j=0,\ldots, d, \ n=1,\ldots, N.\end{equation}

Proof. Define

$\hat{\mathbb{P}}$

by

$\hat{\mathbb{P}}$

by

\begin{equation} \hat{\mathbb{P}}(A) = \mathbb{E}[L_N1_A],\quad L_n = \prod_{k=1}^n \Biggl(\sum_{j=0}^d\frac{\hat{P}_{k,j}}{P_{k,j}}1_{\{\Delta X_k = v_j \}} \Biggr) \end{equation}

\begin{equation} \hat{\mathbb{P}}(A) = \mathbb{E}[L_N1_A],\quad L_n = \prod_{k=1}^n \Biggl(\sum_{j=0}^d\frac{\hat{P}_{k,j}}{P_{k,j}}1_{\{\Delta X_k = v_j \}} \Biggr) \end{equation}

for

$A \in \mathscr{F}_N$

. The measure

$A \in \mathscr{F}_N$

. The measure

$\hat{\mathbb{P}}$

is a probability measure because

$\hat{\mathbb{P}}$

is a probability measure because

\begin{equation*} \mathbb{E}\Biggl[ \sum_{j=0}^d\frac{\hat{P}_{n,j}}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \bigg| \mathscr{F}_{n-1}\Biggr] = \sum_{j=0}^d\frac{\hat{P}_{n,j}}{P_{n,j}} P_{n,j} = 1\end{equation*}

\begin{equation*} \mathbb{E}\Biggl[ \sum_{j=0}^d\frac{\hat{P}_{n,j}}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \bigg| \mathscr{F}_{n-1}\Biggr] = \sum_{j=0}^d\frac{\hat{P}_{n,j}}{P_{n,j}} P_{n,j} = 1\end{equation*}

and so

$L_n$

is a martingale with

$L_n$

is a martingale with

$L_0 = 1$

. Using Bayes’ formula, we derive

$L_0 = 1$

. Using Bayes’ formula, we derive

\begin{equation*} \hat{\mathbb{P}}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = \frac{\mathbb{E}[L_N1_{\{\Delta X_n = v_j\}}\mid \mathscr{F}_{n-1}]}{\mathbb{E}[L_N \mid \mathscr{F}_{n-1}]} = \mathbb{E}\biggl[ \frac{\hat{P}_{n,j}}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \bigg| \mathscr{F}_{n-1}\biggr] = \hat{P}_{n,j},\end{equation*}

\begin{equation*} \hat{\mathbb{P}}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = \frac{\mathbb{E}[L_N1_{\{\Delta X_n = v_j\}}\mid \mathscr{F}_{n-1}]}{\mathbb{E}[L_N \mid \mathscr{F}_{n-1}]} = \mathbb{E}\biggl[ \frac{\hat{P}_{n,j}}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \bigg| \mathscr{F}_{n-1}\biggr] = \hat{P}_{n,j},\end{equation*}

by the martingale property of

$L_n$

.

$L_n$

.

Define a measure

$\mathbb{Q}$

on

$\mathbb{Q}$

on

$\mathscr{F}_N$

by

$\mathscr{F}_N$

by

\begin{equation*} \mathbb{Q}(A) = \mathbb{E}[L_N1_A],\quad L_N = \prod_{n=1}^N \Biggl( \frac{1}{d+1} \sum_{j=0}^d\frac{1}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \Biggr). \end{equation*}

\begin{equation*} \mathbb{Q}(A) = \mathbb{E}[L_N1_A],\quad L_N = \prod_{n=1}^N \Biggl( \frac{1}{d+1} \sum_{j=0}^d\frac{1}{P_{n,j}}1_{\{\Delta X_n = v_j \}} \Biggr). \end{equation*}

Let

$\mathbb{E}_\mathbb{Q}$

denote the integration under

$\mathbb{E}_\mathbb{Q}$

denote the integration under

$\mathbb{Q}$

.

$\mathbb{Q}$

.

Lemma 2.4. The measure

$\mathbb{Q}$

is the unique probability measure on

$\mathbb{Q}$

is the unique probability measure on

$\mathscr{F}_N$

under which

$\mathscr{F}_N$

under which

$\{X_n\}$

is a martingale. Under

$\{X_n\}$

is a martingale. Under

$\mathbb{Q}$

,

$\mathbb{Q}$

,

$\{\Delta X_n\}$

is i.i.d. with

$\{\Delta X_n\}$

is i.i.d. with

\begin{equation*} \mathbb{Q}(\Delta X_n = v_j ) = \mathbb{Q}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = \frac{1}{d+1}\end{equation*}

\begin{equation*} \mathbb{Q}(\Delta X_n = v_j ) = \mathbb{Q}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = \frac{1}{d+1}\end{equation*}

for all

$n =1,\ldots, N$

and

$n =1,\ldots, N$

and

$j=0,\ldots, d$

. We also have

$j=0,\ldots, d$

. We also have

\begin{equation}\mathbb{E}_\mathbb{Q}[\Delta X_n \mid\mathscr{F}_{n-1}] = 0,\quad \mathbb{E}_\mathbb{Q}[\Delta X_n (\Delta X_n)^\top \mid\mathscr{F}_{n-1}] = \frac{1}{d+1} \mathbf{v}\mathbf{v}^\top.\end{equation}

\begin{equation}\mathbb{E}_\mathbb{Q}[\Delta X_n \mid\mathscr{F}_{n-1}] = 0,\quad \mathbb{E}_\mathbb{Q}[\Delta X_n (\Delta X_n)^\top \mid\mathscr{F}_{n-1}] = \frac{1}{d+1} \mathbf{v}\mathbf{v}^\top.\end{equation}

Proof. By Lemma 2.3,

$\mathbb{Q}$

is a probability measure with

$\mathbb{Q}$

is a probability measure with

$ \mathbb{Q}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = 1/(d+1)$

, which implies

$ \mathbb{Q}(\Delta X_n =v_j \mid \mathscr{F}_{n-1}) = 1/(d+1)$

, which implies

\begin{equation*} \mathbb{E}_\mathbb{Q}[\Delta X_n \mid\mathscr{F}_{n-1}] = \frac{1}{d+1} \mathbf{v}\mathbf{1} = 0.\end{equation*}

\begin{equation*} \mathbb{E}_\mathbb{Q}[\Delta X_n \mid\mathscr{F}_{n-1}] = \frac{1}{d+1} \mathbf{v}\mathbf{1} = 0.\end{equation*}

Therefore

$\{X_n\}$

is a martingale with (2.6). There is no other such measure because

$\{X_n\}$

is a martingale with (2.6). There is no other such measure because

\begin{equation*} \sum_{j=0}^d \alpha_j = 1, \quad \sum_{j=0}^d \alpha_j v_j = 0\end{equation*}

\begin{equation*} \sum_{j=0}^d \alpha_j = 1, \quad \sum_{j=0}^d \alpha_j v_j = 0\end{equation*}

implies

$\alpha_j = 1/(d+1)$

as in the proof of Lemma 2.1. Since the conditional law of

$\alpha_j = 1/(d+1)$

as in the proof of Lemma 2.1. Since the conditional law of

$\Delta X_n$

given

$\Delta X_n$

given

$\mathscr{F}_{n-1}$

is deterministic for every n,

$\mathscr{F}_{n-1}$

is deterministic for every n,

$\{\Delta X_n\}$

is i.i.d.

$\{\Delta X_n\}$

is i.i.d.

Remark 2.1. For any positive definite

$d\times d$

matrix

$d\times d$

matrix

$\Sigma$

, we can construct such a lattice L that

$\Sigma$

, we can construct such a lattice L that

$\mathbf{v}\mathbf{v}^\top = \Sigma$

. Indeed, starting with an arbitrary basis, say,

$\mathbf{v}\mathbf{v}^\top = \Sigma$

. Indeed, starting with an arbitrary basis, say,

$\bar{v}_j = e_j$

(the standard basis of

$\bar{v}_j = e_j$

(the standard basis of

$\mathbb{R}^d)$

with

$\mathbb{R}^d)$

with

$\bar{v}_0 = -\bar{v}_1 - \cdots - \bar{v}_d$

and

$\bar{v}_0 = -\bar{v}_1 - \cdots - \bar{v}_d$

and

$\bar{\mathbf{v}} = [\bar{v}_0, \ldots, \bar{v}_d]$

, using the Cholesky decomposition

$\bar{\mathbf{v}} = [\bar{v}_0, \ldots, \bar{v}_d]$

, using the Cholesky decomposition

$\Sigma = CC^\top$

and

$\Sigma = CC^\top$

and

$\bar{\mathbf{v}}\bar{\mathbf{v}}^\top= \bar{C}\bar{C}^\top$

, if we take

$\bar{\mathbf{v}}\bar{\mathbf{v}}^\top= \bar{C}\bar{C}^\top$

, if we take

$v_j = C\bar{C}^{-1}\bar{v}_j$

,

$v_j = C\bar{C}^{-1}\bar{v}_j$

,

$j=0,\ldots, d$

, then

$j=0,\ldots, d$

, then

$\mathbf{v} = C\bar{C}^{-1}\bar{\mathbf{v}}$

and so we get

$\mathbf{v} = C\bar{C}^{-1}\bar{\mathbf{v}}$

and so we get

$\mathbf{vv}^\top = C\bar{C}^{-1}\bar{\mathbf{v}}\bar{\mathbf{v}}^\top (\bar{C}^\top)^{-1}C^\top = \Sigma$

. In particular, we can construct such

$\mathbf{vv}^\top = C\bar{C}^{-1}\bar{\mathbf{v}}\bar{\mathbf{v}}^\top (\bar{C}^\top)^{-1}C^\top = \Sigma$

. In particular, we can construct such

$v_j$

that

$v_j$

that

$\mathbf{vv}^\top$

is the identity matrix. In this case a scaling limit of

$\mathbf{vv}^\top$

is the identity matrix. In this case a scaling limit of

$\{X_n\}$

under

$\{X_n\}$

under

$\mathbb{Q}$

is the d-dimensional standard Brownian motion. Such a set of vectors played an essential role in proving the existence of continuous-time market equilibrium in Anderson and Raimondo [Reference Anderson and Raimondo2] by means of non-standard analysis, where the existence of the vectors was proved in a recursive manner. It is also the building block of a d-dimensional diamond in topological crystallography [Reference Sunada36].

$\mathbb{Q}$

is the d-dimensional standard Brownian motion. Such a set of vectors played an essential role in proving the existence of continuous-time market equilibrium in Anderson and Raimondo [Reference Anderson and Raimondo2] by means of non-standard analysis, where the existence of the vectors was proved in a recursive manner. It is also the building block of a d-dimensional diamond in topological crystallography [Reference Sunada36].

2.3. Existence, uniqueness and representation

Here we introduce our BS

$\Delta$

E. Let

$\Delta$

E. Let

$\mathcal{A}$

denote the set of the sequences

$\mathcal{A}$

denote the set of the sequences

$g = \{g_n\}_{n=1}^N$

of

$g = \{g_n\}_{n=1}^N$

of

$\mathscr{F}_{n-1}\otimes \mathscr{B}(\mathbb{R}^d)$

measurable functions

$\mathscr{F}_{n-1}\otimes \mathscr{B}(\mathbb{R}^d)$

measurable functions

$g_n\colon \Omega \times \mathbb{R}^d \to \mathbb{R}$

. Now we state an elementary but fundamental result.

$g_n\colon \Omega \times \mathbb{R}^d \to \mathbb{R}$

. Now we state an elementary but fundamental result.

Theorem 2.1. Let

$Y_N$

be an

$Y_N$

be an

$\mathscr{F}_N$

-measurable random variable, and let

$\mathscr{F}_N$

-measurable random variable, and let

$g = \{g_n\} \in \mathcal{A}$

. Then there exist uniquely an adapted process

$g = \{g_n\} \in \mathcal{A}$

. Then there exist uniquely an adapted process

$\{Y_n\}_{n=0,\ldots,N-1}$

and an

$\{Y_n\}_{n=0,\ldots,N-1}$

and an

$\mathbb{R}^d$

-valued predictable process

$\mathbb{R}^d$

-valued predictable process

$\{Z_n\}_{n=1,\ldots,N}$

such that

$\{Z_n\}_{n=1,\ldots,N}$

such that

\begin{equation} \Delta Y_n = -g_n(Z_n) + Z_n^\top \Delta X_n,\quad n=1,\ldots, N.\end{equation}

\begin{equation} \Delta Y_n = -g_n(Z_n) + Z_n^\top \Delta X_n,\quad n=1,\ldots, N.\end{equation}

Further, they admit the following representation:

\begin{align*}Y_{n-1}& = \mathbb{E}_\mathbb{Q}[Y_n\mid\mathscr{F}_{n-1}] + g_n(Z_n),\\*Z_n& = (d+1) (\mathbf{v}\mathbf{v}^\top)^{-1} \mathbb{E}_\mathbb{Q}[Y_n \Delta X_n\mid \mathscr{F}_{n-1}]= (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}\bar{Y}_n,\end{align*}

\begin{align*}Y_{n-1}& = \mathbb{E}_\mathbb{Q}[Y_n\mid\mathscr{F}_{n-1}] + g_n(Z_n),\\*Z_n& = (d+1) (\mathbf{v}\mathbf{v}^\top)^{-1} \mathbb{E}_\mathbb{Q}[Y_n \Delta X_n\mid \mathscr{F}_{n-1}]= (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}\bar{Y}_n,\end{align*}

where

$\bar{Y}_n = (\bar{Y}_{n,0}, \ldots, \bar{Y}_{n,d})^\top$

and

$\bar{Y}_n = (\bar{Y}_{n,0}, \ldots, \bar{Y}_{n,d})^\top$

and

\begin{equation*} \bar{Y}_{n,j} = \mathbb{E}_\mathbb{Q}[Y_n\mid\mathscr{F}_{n-1}, \Delta X_n = v_j] = (d+1) \mathbb{E}_\mathbb{Q}[Y_n1_{\{\Delta X_n = v_j\}}\mid \mathscr{F}_{n-1}].\end{equation*}

\begin{equation*} \bar{Y}_{n,j} = \mathbb{E}_\mathbb{Q}[Y_n\mid\mathscr{F}_{n-1}, \Delta X_n = v_j] = (d+1) \mathbb{E}_\mathbb{Q}[Y_n1_{\{\Delta X_n = v_j\}}\mid \mathscr{F}_{n-1}].\end{equation*}

Proof. Since

$Y_N$

is

$Y_N$

is

$\mathscr{F}_N$

-measurable, there exists a function

$\mathscr{F}_N$

-measurable, there exists a function

$f\colon L^N \to \mathbb{R}$

such that

$f\colon L^N \to \mathbb{R}$

such that

$Y_N = f(X_1,\ldots,X_N)$

. Since

$Y_N = f(X_1,\ldots,X_N)$

. Since

$\mathbb{P}_{N,j}$

are positive by the assumption, (2.7) for

$\mathbb{P}_{N,j}$

are positive by the assumption, (2.7) for

$n=N$

is equivalent to the system of equations for

$n=N$

is equivalent to the system of equations for

$\mathscr{F}_{N-1}$

-measurable random variables

$\mathscr{F}_{N-1}$

-measurable random variables

\begin{equation*}Y\,:\!=\,\begin{bmatrix}f(X_1,\ldots,X_{N-1},X_{N-1} + v_0) \\ \vdots\\f(X_1,\ldots,X_{N-1},X_{N-1} + v_d)\end{bmatrix}= (\mathbf{1},\mathbf{v}^\top)\begin{bmatrix} Y_{N-1} - g_N(Z_N) \\ Z_N\end{bmatrix}\!.\end{equation*}

\begin{equation*}Y\,:\!=\,\begin{bmatrix}f(X_1,\ldots,X_{N-1},X_{N-1} + v_0) \\ \vdots\\f(X_1,\ldots,X_{N-1},X_{N-1} + v_d)\end{bmatrix}= (\mathbf{1},\mathbf{v}^\top)\begin{bmatrix} Y_{N-1} - g_N(Z_N) \\ Z_N\end{bmatrix}\!.\end{equation*}

Applying Lemma 2.2, we obtain (2.7) for

$n=N$

with

$n=N$

with

\begin{equation*} Z_N = b(Y), \quad Y_{N-1} = a(Y)+g_N(Z_N),\end{equation*}

\begin{equation*} Z_N = b(Y), \quad Y_{N-1} = a(Y)+g_N(Z_N),\end{equation*}

where a(y) and b(y) are defined by (2.3). It is clear that both

$Z_N$

and

$Z_N$

and

$Y_{N-1}$

are

$Y_{N-1}$

are

$\mathscr{F}_{N-1}$

-measurable. By backward induction, we obtain

$\mathscr{F}_{N-1}$

-measurable. By backward induction, we obtain

$\{Y_n\}$

and

$\{Y_n\}$

and

$\{Z_n\}$

. The representation follows from (2.7) and (2.6) by taking the conditional expectation under

$\{Z_n\}$

. The representation follows from (2.7) and (2.6) by taking the conditional expectation under

$\mathbb{Q}$

.

$\mathbb{Q}$

.

For

$g = \{g_n\} \in \mathcal{A}$

fixed, the

$g = \{g_n\} \in \mathcal{A}$

fixed, the

$\mathscr{F}_n$

-measurable random variable

$\mathscr{F}_n$

-measurable random variable

$Y_n$

given by Theorem 2.1 is uniquely determined by the

$Y_n$

given by Theorem 2.1 is uniquely determined by the

$\mathscr{F}_N$

-measurable random variable

$\mathscr{F}_N$

-measurable random variable

$Y_N$

. We write this mapping as

$Y_N$

. We write this mapping as

$Y_n = \mathcal{E}^g_n(Y_N)$

and call it the g-expectation of

$Y_n = \mathcal{E}^g_n(Y_N)$

and call it the g-expectation of

$Y_N$

(with respect to

$Y_N$

(with respect to

$\mathscr{F}_n$

). The stochastic process

$\mathscr{F}_n$

). The stochastic process

$\{(Y_n,Z_n)\}$

given by Theorem 2.1 is called the solution of the BS

$\{(Y_n,Z_n)\}$

given by Theorem 2.1 is called the solution of the BS

$\Delta$

E (2.7).

$\Delta$

E (2.7).

Remark 2.2. In the literature, say, in [Reference Cohen and Elliot15], BS

$\Delta$

E is formulated by decomposing

$\Delta$

E is formulated by decomposing

$\Delta Y_n$

into a predictable part and a martingale difference part. In our formulation (2.7),

$\Delta Y_n$

into a predictable part and a martingale difference part. In our formulation (2.7),

$\Delta X_n$

is not necessarily a martingale difference. It is a minor reparametrization because (2.7) can be rewritten as

$\Delta X_n$

is not necessarily a martingale difference. It is a minor reparametrization because (2.7) can be rewritten as

\begin{equation*} \Delta Y_n = - \hat{g}_n(Z_n) + Z_n^\top(\Delta X_n - A_n)\end{equation*}

\begin{equation*} \Delta Y_n = - \hat{g}_n(Z_n) + Z_n^\top(\Delta X_n - A_n)\end{equation*}

with

$\hat{g}_n(z) = g_n(z) - z^\top A_n$

,

$\hat{g}_n(z) = g_n(z) - z^\top A_n$

,

$A_n = \mathbb{E}[\Delta X_n \mid \mathscr{F}_{n-1}]$

.

$A_n = \mathbb{E}[\Delta X_n \mid \mathscr{F}_{n-1}]$

.

Example 2.1. Let

$\gamma \gt 0$

,

$\gamma \gt 0$

,

$\{(\hat{P}_{n,0},\ldots,\hat{P}_{n,d})^\top\}$

be a

$\{(\hat{P}_{n,0},\ldots,\hat{P}_{n,d})^\top\}$

be a

$\Delta_d$

-valued predictable process, and

$\Delta_d$

-valued predictable process, and

\begin{equation} g_n(z) = -\frac{1}{\gamma} \log \Biggl(\sum_{j=0}^{d} \,{\mathrm{e}}^{-\gamma z^\top v_j} {\hat{P}}_{n,j}\Biggr).\end{equation}

\begin{equation} g_n(z) = -\frac{1}{\gamma} \log \Biggl(\sum_{j=0}^{d} \,{\mathrm{e}}^{-\gamma z^\top v_j} {\hat{P}}_{n,j}\Biggr).\end{equation}

Then

\begin{equation} \mathcal{E}^g_n(Y) = -\frac{1}{\gamma} \log \hat{\mathbb{E}}\big[{\mathrm{e}}^{-\gamma Y}\mid \mathscr{F}_n\big], \quad n=0,1,\ldots, N ,\end{equation}

\begin{equation} \mathcal{E}^g_n(Y) = -\frac{1}{\gamma} \log \hat{\mathbb{E}}\big[{\mathrm{e}}^{-\gamma Y}\mid \mathscr{F}_n\big], \quad n=0,1,\ldots, N ,\end{equation}

for any

$\mathscr{F}_N$

-measurable random variable Y, where

$\mathscr{F}_N$

-measurable random variable Y, where

$\hat{\mathbb{E}}$

is the expectation under the measure

$\hat{\mathbb{E}}$

is the expectation under the measure

$\hat{\mathbb{P}}$

on

$\hat{\mathbb{P}}$

on

$\mathscr{F}_N$

defined by (2.5). To see this, note that by Lemma 2.3,

$\mathscr{F}_N$

defined by (2.5). To see this, note that by Lemma 2.3,

\begin{equation*}g_n(z) = -\frac{1}{\gamma} \log \hat{\mathbb{E}}\bigl[{\mathrm{e}}^{-\gamma z^\top \Delta X_n}\mid \mathscr{F}_{n-1}\bigr]. \end{equation*}

\begin{equation*}g_n(z) = -\frac{1}{\gamma} \log \hat{\mathbb{E}}\bigl[{\mathrm{e}}^{-\gamma z^\top \Delta X_n}\mid \mathscr{F}_{n-1}\bigr]. \end{equation*}

Substituting

$Y_n= Y_{n-1}- g_n (Z_n) + Z_n ^\top \Delta X_n $

, we have

$Y_n= Y_{n-1}- g_n (Z_n) + Z_n ^\top \Delta X_n $

, we have

\begin{equation*} -\frac{1}{\gamma} \log \hat{\mathbb{E}}\big[{\mathrm{e}}^{-\gamma Y_n}\mid \mathscr{F}_{n-1}\big]= Y_{n-1} - g_n(Z_n)-\frac{1}{\gamma} \log \hat{\mathbb{E}}\bigl[{\mathrm{e}}^{-\gamma Z_n^\top \Delta X_n }\mid \mathscr{F}_{n-1}\bigr] =Y_{n-1}\end{equation*}

\begin{equation*} -\frac{1}{\gamma} \log \hat{\mathbb{E}}\big[{\mathrm{e}}^{-\gamma Y_n}\mid \mathscr{F}_{n-1}\big]= Y_{n-1} - g_n(Z_n)-\frac{1}{\gamma} \log \hat{\mathbb{E}}\bigl[{\mathrm{e}}^{-\gamma Z_n^\top \Delta X_n }\mid \mathscr{F}_{n-1}\bigr] =Y_{n-1}\end{equation*}

which implies (2.9) for

$n=N-1$

. The general case follows by backward induction.

$n=N-1$

. The general case follows by backward induction.

Next we give a discrete analog of the nonlinear Feynman–Kac formula, which is computationally efficient when dealing with large N.

Proposition 2.1. Let

$f_n \colon L \times \mathbb{R}^d \to \mathbb{R}$

,

$f_n \colon L \times \mathbb{R}^d \to \mathbb{R}$

,

$n=1,\ldots, N$

and

$n=1,\ldots, N$

and

$h \colon L \to \mathbb{R}$

. Define

$h \colon L \to \mathbb{R}$

. Define

$u_n \colon L \to \mathbb{R}$

,

$u_n \colon L \to \mathbb{R}$

,

$n=0,1,\ldots, N$

backward inductively by

$n=0,1,\ldots, N$

backward inductively by

\begin{equation*} u_{n-1}(x) = u_n(x) + \mathcal{L} u_n(x) + f_n(x, (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_n(x))\end{equation*}

\begin{equation*} u_{n-1}(x) = u_n(x) + \mathcal{L} u_n(x) + f_n(x, (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_n(x))\end{equation*}

with

$u_N = h$

, where

$u_N = h$

, where

\begin{align*} \mathcal{L} u_n(x) & = \frac{1}{d+1} \sum_{j=0}^d (u_n(x+v_j)-u_n(x)), \\* \mathcal{N} u_n(x) & = (u_n(x+v_0)-u_n(x), \ldots, u_n(x+v_d)-u_n(x))^\top.\end{align*}

\begin{align*} \mathcal{L} u_n(x) & = \frac{1}{d+1} \sum_{j=0}^d (u_n(x+v_j)-u_n(x)), \\* \mathcal{N} u_n(x) & = (u_n(x+v_0)-u_n(x), \ldots, u_n(x+v_d)-u_n(x))^\top.\end{align*}

Then the unique solution to (2.7) with

$g_n = f_n(X_{n-1},\cdot)$

and

$g_n = f_n(X_{n-1},\cdot)$

and

$Y_N = h(X_N)$

is given by

$Y_N = h(X_N)$

is given by

\begin{equation*} Y_{n-1} = u_{n-1}(X_{n-1}), \quad Z_{n} = (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_{n}(X_{n-1}), \quad n= 1,\ldots, N. \end{equation*}

\begin{equation*} Y_{n-1} = u_{n-1}(X_{n-1}), \quad Z_{n} = (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_{n}(X_{n-1}), \quad n= 1,\ldots, N. \end{equation*}

Proof. By definition,

$Y_N = h(X_N) = u_N(X_N)$

. Suppose

$Y_N = h(X_N) = u_N(X_N)$

. Suppose

$Y_n = u_n(X_n)$

. Then, by Theorem 2.1,

$Y_n = u_n(X_n)$

. Then, by Theorem 2.1,

$Z_n = (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}\bar{Y}_n$

, where

$Z_n = (\mathbf{v}\mathbf{v}^\top)^{-1}\mathbf{v}\bar{Y}_n$

, where

\begin{equation*}\bar{Y}_{n,j} = \mathbb{E}_\mathbb{Q}[Y_n\mid \mathscr{F}_{n-1}, \Delta X_n = v_j] = u_n(X_{n-1} + v_j).\end{equation*}

\begin{equation*}\bar{Y}_{n,j} = \mathbb{E}_\mathbb{Q}[Y_n\mid \mathscr{F}_{n-1}, \Delta X_n = v_j] = u_n(X_{n-1} + v_j).\end{equation*}

Using

$\mathbf{v1} = 0$

, we conclude

$\mathbf{v1} = 0$

, we conclude

$Z_n = (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_n(X_{n-1})$

. Further, again by Theorem 2.1,

$Z_n = (\mathbf{vv}^\top)^{-1}\mathbf{v}\mathcal{N} u_n(X_{n-1})$

. Further, again by Theorem 2.1,

\begin{equation*} Y_{n-1} =\mathbb{E}_\mathbb{Q}[Y_n\mid \mathscr{F}_{n-1}] + g_n(Z_n)= u_n(X_{n-1}) + \mathcal{L} u_n(X_{n-1})+ g_n(Z_n) = u_{n-1}(X_{n-1}),\end{equation*}

\begin{equation*} Y_{n-1} =\mathbb{E}_\mathbb{Q}[Y_n\mid \mathscr{F}_{n-1}] + g_n(Z_n)= u_n(X_{n-1}) + \mathcal{L} u_n(X_{n-1})+ g_n(Z_n) = u_{n-1}(X_{n-1}),\end{equation*}

which concludes the proof.

2.4. A gradient constraint

Let

$\Theta$

be the closed convex hull spanned by

$\Theta$

be the closed convex hull spanned by

$\{v_0,v_1,\ldots,v_d\}$

, or equivalently

$\{v_0,v_1,\ldots,v_d\}$

, or equivalently

\begin{equation*} \Theta = \{\mathbf{v}p \ ; \ p \in \Delta_d\}.\end{equation*}

\begin{equation*} \Theta = \{\mathbf{v}p \ ; \ p \in \Delta_d\}.\end{equation*}

In this section we study BS

$\Delta$

Es with the gradient of g being constrained in

$\Delta$

Es with the gradient of g being constrained in

$\Theta$

.

$\Theta$

.

Example 2.2. The triangular lattice of

$\mathbb{R}^2$

is generated by

$\mathbb{R}^2$

is generated by

\begin{equation*} v_1 =\frac{1}{\sqrt{6}} \begin{pmatrix} 0\\-2 \end{pmatrix}\!, \quad v_2 = \frac{1}{\sqrt{6}} \begin{pmatrix} \sqrt{3} \\ 1 \end{pmatrix}\!.\end{equation*}

\begin{equation*} v_1 =\frac{1}{\sqrt{6}} \begin{pmatrix} 0\\-2 \end{pmatrix}\!, \quad v_2 = \frac{1}{\sqrt{6}} \begin{pmatrix} \sqrt{3} \\ 1 \end{pmatrix}\!.\end{equation*}

In this case,

$\mathbf{v}\mathbf{v}^\top = I$

and

$\mathbf{v}\mathbf{v}^\top = I$

and

$\Theta$

is an equilateral triangle.

$\Theta$

is an equilateral triangle.

Proposition 2.2. Let

$g_n(z) = A_n^\top z + B_n$

for a

$g_n(z) = A_n^\top z + B_n$

for a

$\Theta$

-valued predictable process

$\Theta$

-valued predictable process

$\{A_n\}$

and a predictable process

$\{A_n\}$

and a predictable process

$\{B_n\}$

,

$\{B_n\}$

,

$n=1,\ldots,N$

. Then

$n=1,\ldots,N$

. Then

\begin{equation*} \mathcal{E}^g_n (Y) = \hat{\mathbb{E}}\Biggl[Y +\sum_{i=n+1}^N B_i \bigg|\mathscr{F}_n\Biggr], \quad n=0,1,\ldots,N, \end{equation*}

\begin{equation*} \mathcal{E}^g_n (Y) = \hat{\mathbb{E}}\Biggl[Y +\sum_{i=n+1}^N B_i \bigg|\mathscr{F}_n\Biggr], \quad n=0,1,\ldots,N, \end{equation*}

for any

$\mathcal{F}_N$

-measurable random variable Y, where

$\mathcal{F}_N$

-measurable random variable Y, where

$\hat{\mathbb{E}}$

is the expectation under the measure

$\hat{\mathbb{E}}$

is the expectation under the measure

$\hat{\mathbb{P}}$

on

$\hat{\mathbb{P}}$

on

$\mathscr{F}_N$

defined by (2.5) with

$\mathscr{F}_N$

defined by (2.5) with

$\hat{P}_n = (\hat{P}_{n,0},\ldots, \hat{P}_{n,d})^\top$

such that

$\hat{P}_n = (\hat{P}_{n,0},\ldots, \hat{P}_{n,d})^\top$

such that

$A_n = \mathbf{v}\hat{P}_n$

.

$A_n = \mathbf{v}\hat{P}_n$

.

Proof. By Lemma 2.3,

\begin{equation*} \hat{\mathbb{E}}[\Delta X_n \mid \mathcal{F}_{n-1}] = \frac{\mathbb{E}[L_N \Delta X_n \mid \mathcal{F}_{n-1}]}{\mathbb{E}[L_N \mid \mathcal{F}_{n-1}]}= \sum_{j=0}^d v_j \hat{P}_{n,j}= \mathbf{v}\hat{P}_n = A_n\end{equation*}

\begin{equation*} \hat{\mathbb{E}}[\Delta X_n \mid \mathcal{F}_{n-1}] = \frac{\mathbb{E}[L_N \Delta X_n \mid \mathcal{F}_{n-1}]}{\mathbb{E}[L_N \mid \mathcal{F}_{n-1}]}= \sum_{j=0}^d v_j \hat{P}_{n,j}= \mathbf{v}\hat{P}_n = A_n\end{equation*}

for all n. On the other hand, from (2.7), we have

\begin{equation*} Y= Y_N = Y_n + \sum_{i=n+1}^N \big({-}g_i(Z_i) + Z_i^\top \Delta X_i\big) = Y_n + \sum_{i=n+1}^N \big({-}B_i + Z_i^{\top}(\Delta X_i - A_i)\big).\end{equation*}

\begin{equation*} Y= Y_N = Y_n + \sum_{i=n+1}^N \big({-}g_i(Z_i) + Z_i^\top \Delta X_i\big) = Y_n + \sum_{i=n+1}^N \big({-}B_i + Z_i^{\top}(\Delta X_i - A_i)\big).\end{equation*}

Taking the conditional expectation under

$\hat{\mathbb{P}}$

, we get the conclusion.

$\hat{\mathbb{P}}$

, we get the conclusion.

Example 2.3. Let

$N=1$

,

$N=1$

,

$d=1$

,

$d=1$

,

$\Omega = \{+,-\}$

,

$\Omega = \{+,-\}$

,

$v_0 = -1, v_1 = 1$

, and

$v_0 = -1, v_1 = 1$

, and

$\Delta X_1(\pm) = \pm 1$

. Then

$\Delta X_1(\pm) = \pm 1$

. Then

$L = \mathbb{Z}$

,

$L = \mathbb{Z}$

,

$\mathbf{v} = ({-}1,1)$

,

$\mathbf{v} = ({-}1,1)$

,

$\Theta = [-1,1]$

and

$\Theta = [-1,1]$

and

$\mathbf{vv}^\top = 2$

. Following the proof of Theorem 2.1, the solution of the linear BS

$\mathbf{vv}^\top = 2$

. Following the proof of Theorem 2.1, the solution of the linear BS

$\Delta$

E

$\Delta$

E

$\Delta Y_1 = -AZ_1 + Z_1\Delta X_1$

can be constructed as

$\Delta Y_1 = -AZ_1 + Z_1\Delta X_1$

can be constructed as

\begin{equation*} Y_0 = \frac{Y_1(+) + Y_1({-})}{2} + A \frac{Y_1(+)-Y_1({-})}{2} = \frac{1+A}{2} Y_1(+) + \frac{1-A}{2} Y_1({-})\end{equation*}

\begin{equation*} Y_0 = \frac{Y_1(+) + Y_1({-})}{2} + A \frac{Y_1(+)-Y_1({-})}{2} = \frac{1+A}{2} Y_1(+) + \frac{1-A}{2} Y_1({-})\end{equation*}

for any

$A \in \mathbb{R}$

. The expression given by Proposition 2.2 is

$A \in \mathbb{R}$

. The expression given by Proposition 2.2 is

$Y_0 = \hat{E}[Y_1]$

, which can be directly seen with

$Y_0 = \hat{E}[Y_1]$

, which can be directly seen with

$\hat{P}_1 = ((1-A)/2, (1+A)/2)^\top$

for

$\hat{P}_1 = ((1-A)/2, (1+A)/2)^\top$

for

$A \in \Theta = [-1,1]$

. For

$A \in \Theta = [-1,1]$

. For

$A \notin \Theta$

, we observe that

$A \notin \Theta$

, we observe that

$Y_0$

is not increasing in either

$Y_0$

is not increasing in either

$Y_1(+)$

or

$Y_1(+)$

or

$Y_1({-})$

. In particular,

$Y_1({-})$

. In particular,

$Y_0$

cannot be represented as an expectation in this case.

$Y_0$

cannot be represented as an expectation in this case.

The set

$\Theta$

plays a key role also for a comparison theorem. Let

$\Theta$

plays a key role also for a comparison theorem. Let

$\mathcal{B}$

denote the set of the sequence

$\mathcal{B}$

denote the set of the sequence

$g = \{g_n\}_{n=1}^N \in \mathcal{A}$

with

$g = \{g_n\}_{n=1}^N \in \mathcal{A}$

with

\begin{equation} g_n(z_2) - g_n(z_1) \geq \min_{\theta\in\Theta}\theta^\top(z_2-z_1) \end{equation}

\begin{equation} g_n(z_2) - g_n(z_1) \geq \min_{\theta\in\Theta}\theta^\top(z_2-z_1) \end{equation}

for all

$z_1, z_2 \in \mathbb{R}^d$

.

$z_1, z_2 \in \mathbb{R}^d$

.

Proposition 2.3. (Comparison theorem.) For

$i=1,2$

, let

$i=1,2$

, let

$Y^{(i)}$

be

$Y^{(i)}$

be

$\mathscr{F}_N$

-measurable random variables with

$\mathscr{F}_N$

-measurable random variables with

$Y^{(1)} \geq Y^{(2)}$

, and

$Y^{(1)} \geq Y^{(2)}$

, and

$g^{(i)} = \{g^{(i)}_n\} \in \mathcal{A}$

with

$g^{(i)} = \{g^{(i)}_n\} \in \mathcal{A}$

with

$g^{(1)}_n \geq g^{(2)}_n$

. Let

$g^{(1)}_n \geq g^{(2)}_n$

. Let

$\mathcal{E}^{(i)}_n(Y^{(i)})$

denote

$\mathcal{E}^{(i)}_n(Y^{(i)})$

denote

$\mathcal{E}^g_n(Y^{(i)})$

for

$\mathcal{E}^g_n(Y^{(i)})$

for

$g = g^{(i)}$

,

$g = g^{(i)}$

,

$i=1,2$

respectively. Assume also

$i=1,2$

respectively. Assume also

$g^{(i)} \in \mathcal{B}$

for either

$g^{(i)} \in \mathcal{B}$

for either

$i=1$

or

$i=1$

or

$i=2$

. Then

$i=2$

. Then

\begin{equation*} \mathcal{E}^{(1)}_n(Y^{(1)}) \geq \mathcal{E}^{(2)}_n(Y^{(2)}), \quad n=0,1,\ldots, N.\end{equation*}

\begin{equation*} \mathcal{E}^{(1)}_n(Y^{(1)}) \geq \mathcal{E}^{(2)}_n(Y^{(2)}), \quad n=0,1,\ldots, N.\end{equation*}

Proof. Note first that

\begin{equation} \min_{\omega \in \Omega} z^\top \Delta X_n(\omega) = \min_{p \in \Delta_d} z^\top \mathbf{v}p = \min_{\theta \in \Theta}z^\top \theta\end{equation}

\begin{equation} \min_{\omega \in \Omega} z^\top \Delta X_n(\omega) = \min_{p \in \Delta_d} z^\top \mathbf{v}p = \min_{\theta \in \Theta}z^\top \theta\end{equation}

for any

$z \in \mathbb{R}^d$

and n. Therefore, under (2.10) for

$z \in \mathbb{R}^d$

and n. Therefore, under (2.10) for

$g= g^{(i)}$

,

$g= g^{(i)}$

,

$g^{(i)}$

is balanced in the terminology of [Reference Cohen and Elliot15], so the result follows from Theorem 3.2 of [Reference Cohen and Elliot15]. Here we repeat essentially the same proof for the readers’ convenience. Let

$g^{(i)}$

is balanced in the terminology of [Reference Cohen and Elliot15], so the result follows from Theorem 3.2 of [Reference Cohen and Elliot15]. Here we repeat essentially the same proof for the readers’ convenience. Let

$\bigl\{\bigl(Y^{(i)}_n,Z^{(i)}_n\bigr)\bigr\}$

be the solution of (2.7) with

$\bigl\{\bigl(Y^{(i)}_n,Z^{(i)}_n\bigr)\bigr\}$

be the solution of (2.7) with

$g = g^{(i)}$

and

$g = g^{(i)}$

and

$Y_N = Y^{(i)}$

. We have

$Y_N = Y^{(i)}$

. We have

$Y^{(1)}_N \geq Y^{(2)}_N$

by assumption. Suppose

$Y^{(1)}_N \geq Y^{(2)}_N$

by assumption. Suppose

$Y^{(1)}_k \geq Y^{(2)}_k$

for some k. Then

$Y^{(1)}_k \geq Y^{(2)}_k$

for some k. Then

\begin{equation*}0 \leq Y^{(1)}_k - Y^{(2)}_k = Y^{(1)}_{k-1} - Y^{(2)}_{k-1}- g^{(1)}_k\bigl(Z^{(1)}_k\bigr) + g^{(2)}_k\bigl(Z^{(2)}_k\bigr) + \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr)^\top \Delta X_k\end{equation*}

\begin{equation*}0 \leq Y^{(1)}_k - Y^{(2)}_k = Y^{(1)}_{k-1} - Y^{(2)}_{k-1}- g^{(1)}_k\bigl(Z^{(1)}_k\bigr) + g^{(2)}_k\bigl(Z^{(2)}_k\bigr) + \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr)^\top \Delta X_k\end{equation*}

and so

\begin{equation*} \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr)^\top \Delta X_k \geq - Y^{(1)}_{k-1} + Y^{(2)}_{k-1} + g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr).\end{equation*}

\begin{equation*} \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr)^\top \Delta X_k \geq - Y^{(1)}_{k-1} + Y^{(2)}_{k-1} + g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr).\end{equation*}

Since the right-hand side is

$\mathscr{F}_{k-1}$

-measurable, this implies further

$\mathscr{F}_{k-1}$

-measurable, this implies further

\begin{equation*} \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \geq - Y^{(1)}_{k-1} + Y^{(2)}_{k-1} + g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr)\end{equation*}

\begin{equation*} \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \geq - Y^{(1)}_{k-1} + Y^{(2)}_{k-1} + g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr)\end{equation*}

by (2.11). Therefore

\begin{align*} Y^{(1)}_{k-1} - Y^{(2)}_{k-1} & \geq g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & = g^{(1)}_k\bigl(Z^{(2)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) +g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(1)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & \geq 0 \end{align*}

\begin{align*} Y^{(1)}_{k-1} - Y^{(2)}_{k-1} & \geq g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & = g^{(1)}_k\bigl(Z^{(2)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) +g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(1)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & \geq 0 \end{align*}

under (2.10) for

$g_n = g^{(1)}_n$

, and also

$g_n = g^{(1)}_n$

, and also

\begin{align*} Y^{(1)}_{k-1} - Y^{(2)}_{k-1} & \geq g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & = g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(1)}_k\bigr) +g^{(2)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & \geq 0 \end{align*}

\begin{align*} Y^{(1)}_{k-1} - Y^{(2)}_{k-1} & \geq g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & = g^{(1)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(1)}_k\bigr) +g^{(2)}_k\bigl(Z^{(1)}_k\bigr) - g^{(2)}_k\bigl(Z^{(2)}_k\bigr) - \min_{\theta \in \Theta} \theta^\top \bigl(Z^{(1)}_k- Z^{(2)}_k\bigr) \\* & \geq 0 \end{align*}

under (2.10) for

$g_n = g^{(2)}_n$

. The result then follows by induction.

$g_n = g^{(2)}_n$

. The result then follows by induction.

Remark 2.3. A sufficient condition for

$g_n$

to meet (2.10) is that

$g_n$

to meet (2.10) is that

$g_n(z)$

is continuously differentiable in z with

$g_n(z)$

is continuously differentiable in z with

$\nabla g_n(z)$

taking values in

$\nabla g_n(z)$

taking values in

$\Theta$

. Indeed, by Taylor’s theorem,

$\Theta$

. Indeed, by Taylor’s theorem,

\begin{equation*} g_n(z_1) - g_n(z_2) = A_n^\top (z_1-z_2),\quad A_n = \int_0^1 \nabla g_n(z_2 + t(z_1 -z_2))\,\mathrm{d}t,\end{equation*}

\begin{equation*} g_n(z_1) - g_n(z_2) = A_n^\top (z_1-z_2),\quad A_n = \int_0^1 \nabla g_n(z_2 + t(z_1 -z_2))\,\mathrm{d}t,\end{equation*}

and then notice that

$A_n$

is

$A_n$

is

$\Theta$

-valued because

$\Theta$

-valued because

$\Theta$

is a convex set.

$\Theta$

is a convex set.

Example 2.4.

(

Locally entropic monetary utility.) Let

$\{(\hat{P}_{n,0},\ldots,\hat{P}_{n,d})^\top\}$

be a

$\{(\hat{P}_{n,0},\ldots,\hat{P}_{n,d})^\top\}$

be a

$\Delta_d$

-valued predictable process, let

$\Delta_d$

-valued predictable process, let

$\{B_n\}$

and

$\{B_n\}$

and

$\{\Gamma_n\}$

be positive predictable processes, and

$\{\Gamma_n\}$

be positive predictable processes, and

\begin{equation} g_n(z) = -\frac{1}{\Gamma_n} \log \Biggl(\sum_{j=0}^{d} \,{\mathrm{e}}^{-\Gamma_n z^\top v_j} \hat{P}_{n,j}\Biggr) - \frac{1}{\Gamma_n}\log B_n.\end{equation}

\begin{equation} g_n(z) = -\frac{1}{\Gamma_n} \log \Biggl(\sum_{j=0}^{d} \,{\mathrm{e}}^{-\Gamma_n z^\top v_j} \hat{P}_{n,j}\Biggr) - \frac{1}{\Gamma_n}\log B_n.\end{equation}

Using a similar calculation to Example 2.1, we deduce the relation

\[Y_{n-1}=-\frac{1}{\Gamma_n}\{\log \hat{\mathbb{E}}[ {\mathrm{e}}^{-\Gamma_n Y_n} \mid {\mathcal F}_{n-1}]+\log B_n\}, \quad n=N,\ldots, 1.\]

\[Y_{n-1}=-\frac{1}{\Gamma_n}\{\log \hat{\mathbb{E}}[ {\mathrm{e}}^{-\Gamma_n Y_n} \mid {\mathcal F}_{n-1}]+\log B_n\}, \quad n=N,\ldots, 1.\]

In particular, when

$B_n=1$

,

$B_n=1$

,

${\mathcal E}_{n-1}^g$

is locally the minus of the entropic risk measure with risk-aversion parameter

${\mathcal E}_{n-1}^g$

is locally the minus of the entropic risk measure with risk-aversion parameter

$\Gamma_n$

extending (2.9). In contrast to the dynamic entropic risk measure studied in [Reference Acciaio and Penner1], we have the time-consistency property

$\Gamma_n$

extending (2.9). In contrast to the dynamic entropic risk measure studied in [Reference Acciaio and Penner1], we have the time-consistency property

$\mathcal{E}_m^g(\mathcal{E}_n^g(Y))=\mathcal{E}_m^g(Y)$

for any

$\mathcal{E}_m^g(\mathcal{E}_n^g(Y))=\mathcal{E}_m^g(Y)$

for any

$m \leq n$

when

$m \leq n$

when

$B_n = 1$

for all n even if the process

$B_n = 1$

for all n even if the process

$\{\Gamma_n\}$

is not constant. We allow

$\{\Gamma_n\}$

is not constant. We allow

$B_n \neq 1$

in order to include an example in Section 3. We call

$B_n \neq 1$

in order to include an example in Section 3. We call

$\mathcal{E}^g_n$

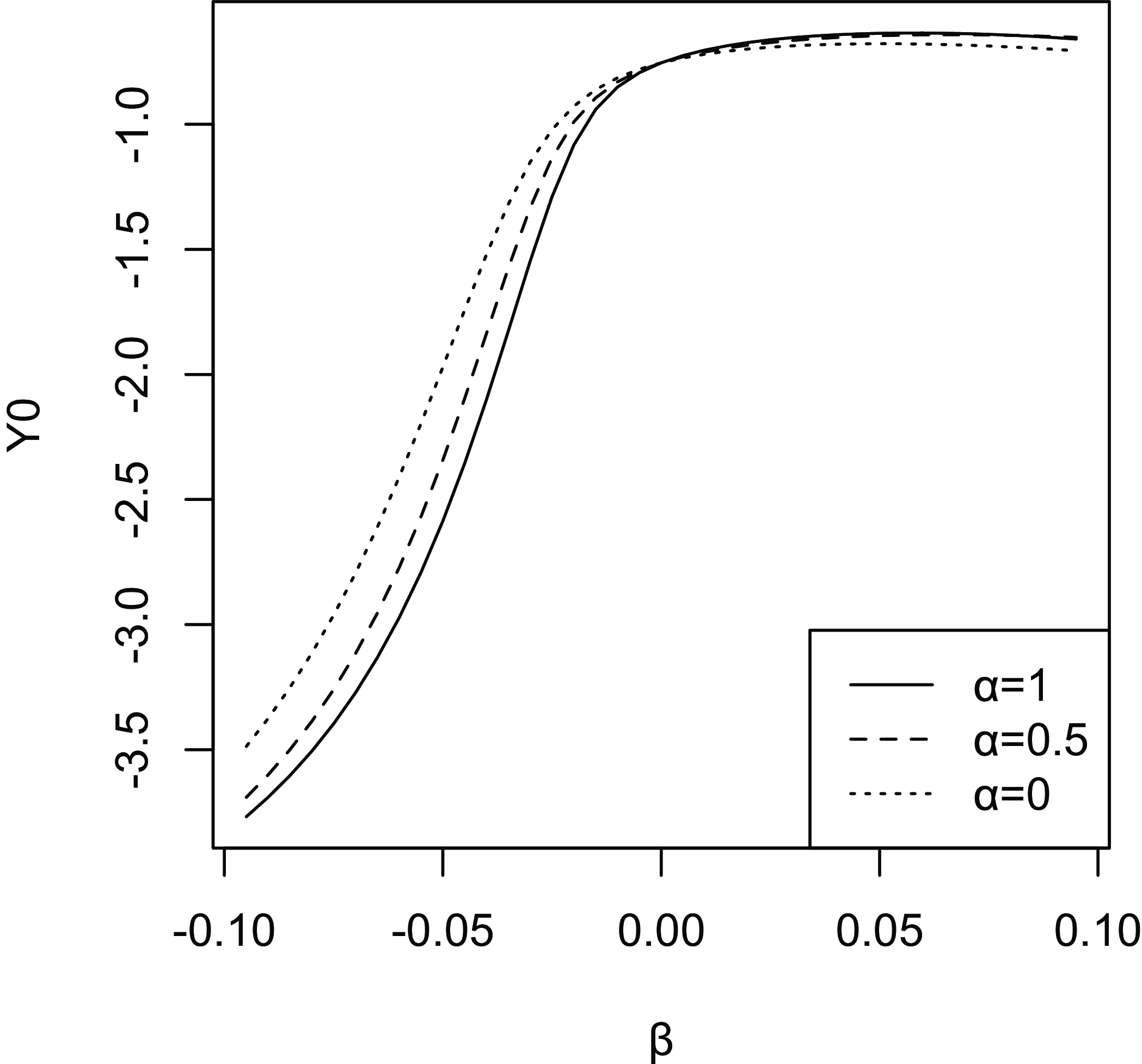

a locally entropic monetary utility. A brief numerical study for this utility is provided in Appendix B. We have

$\mathcal{E}^g_n$

a locally entropic monetary utility. A brief numerical study for this utility is provided in Appendix B. We have

\begin{equation*} \nabla g_n(z) = \frac{\hat{\mathbb{E}}[\Delta X_n \,{\mathrm{e}}^{-\Gamma_n z^\top \Delta X_n}\mid \mathscr{F}_{n-1}]}{\hat{\mathbb{E}}[{\mathrm{e}}^{-\Gamma_n z^\top \Delta X_n}\mid \mathscr{F}_{n-1}]} = \mathbf{v}\hat{P}_n(z), \end{equation*}

\begin{equation*} \nabla g_n(z) = \frac{\hat{\mathbb{E}}[\Delta X_n \,{\mathrm{e}}^{-\Gamma_n z^\top \Delta X_n}\mid \mathscr{F}_{n-1}]}{\hat{\mathbb{E}}[{\mathrm{e}}^{-\Gamma_n z^\top \Delta X_n}\mid \mathscr{F}_{n-1}]} = \mathbf{v}\hat{P}_n(z), \end{equation*}

where

$\hat{P}_n(z) = (\hat{P}_{n,0}(z),\ldots,\hat{P}_{n,d}(z))^\top$

and

$\hat{P}_n(z) = (\hat{P}_{n,0}(z),\ldots,\hat{P}_{n,d}(z))^\top$

and

\begin{equation*} \hat{P}_{n,j}(z)= \frac{{\mathrm{e}}^{-\Gamma_n z^\top v_j} \hat{P}_{n,j}}{\sum_{k=0}^d \,{\mathrm{e}}^{-\Gamma_n z^\top v_k} \hat{P}_{n,k}}. \end{equation*}

\begin{equation*} \hat{P}_{n,j}(z)= \frac{{\mathrm{e}}^{-\Gamma_n z^\top v_j} \hat{P}_{n,j}}{\sum_{k=0}^d \,{\mathrm{e}}^{-\Gamma_n z^\top v_k} \hat{P}_{n,k}}. \end{equation*}

Since

$\hat{P}_n(z)$

is continuous in z and

$\hat{P}_n(z)$

is continuous in z and

$\Delta_d$

-valued for all n, by Remark 2.3, the assumptions of Proposition 2.3 on

$\Delta_d$

-valued for all n, by Remark 2.3, the assumptions of Proposition 2.3 on

$g^{(i)}_n$

are satisfied.

$g^{(i)}_n$

are satisfied.

Next, we seek a robust representation of

$\mathcal{E}^g$

when g is concave. Let

$\mathcal{E}^g$

when g is concave. Let

$\mathcal{C}$

denote the set of

$\mathcal{C}$

denote the set of

$g = \{g_n\} \in \mathcal{B}$

with

$g = \{g_n\} \in \mathcal{B}$

with

$g_n(z)$

being concave in z for all n.

$g_n(z)$

being concave in z for all n.

Lemma 2.5. Let

$g = \{g_n\} \in \mathcal{A}$

. Then

$g = \{g_n\} \in \mathcal{A}$

. Then

$g \in \mathcal{C}$

if and only if

$g \in \mathcal{C}$

if and only if

\begin{equation} g_n(z) = \min_{\theta \in \Theta} \{z^\top \theta + b_n(\theta)\}, \end{equation}

\begin{equation} g_n(z) = \min_{\theta \in \Theta} \{z^\top \theta + b_n(\theta)\}, \end{equation}

where

\begin{equation*} b_n(\theta) = \sup_{z \in \mathbb{R}^d} \{g_n(z)-z^\top \theta\}. \end{equation*}

\begin{equation*} b_n(\theta) = \sup_{z \in \mathbb{R}^d} \{g_n(z)-z^\top \theta\}. \end{equation*}

Proof. If

$g_n$

is concave, then it is continuous on the interior of its domain that is

$g_n$

is concave, then it is continuous on the interior of its domain that is

$\mathbb{R}^d$

. Therefore by a well-known fact on the Legendre transform, we have

$\mathbb{R}^d$

. Therefore by a well-known fact on the Legendre transform, we have

\begin{equation*} g_n(z) = \inf_{x \in \mathbb{R}^d} \{z^\top x + b_n(x)\}. \end{equation*}

\begin{equation*} g_n(z) = \inf_{x \in \mathbb{R}^d} \{z^\top x + b_n(x)\}. \end{equation*}

Let

$x \notin \Theta$

. Since

$x \notin \Theta$

. Since

$\Theta$

is a closed convex set of

$\Theta$

is a closed convex set of

$\mathbb{R}^d$

, by the Hahn–Banach theorem (or the separating hyperplane theorem), there exists

$\mathbb{R}^d$

, by the Hahn–Banach theorem (or the separating hyperplane theorem), there exists

$z_0 \in \mathbb{R}^d$

such that

$z_0 \in \mathbb{R}^d$

such that

\begin{equation*} \min_{\theta \in \Theta}z_0^\top \theta > z_0^\top x.\end{equation*}

\begin{equation*} \min_{\theta \in \Theta}z_0^\top \theta > z_0^\top x.\end{equation*}

Using (2.10), for

$z = \alpha z_0$

,

$z = \alpha z_0$

,

$\alpha \gt 0$

,

$\alpha \gt 0$

,

\begin{equation*} g_n(z) - z^\top x \geq g_n(0) + \min_{\theta \in \Theta} \theta^\top z -z^\top x = g_n(0)+ \alpha \min_{\theta \in \Theta} z_0^\top(\theta -x).\end{equation*}

\begin{equation*} g_n(z) - z^\top x \geq g_n(0) + \min_{\theta \in \Theta} \theta^\top z -z^\top x = g_n(0)+ \alpha \min_{\theta \in \Theta} z_0^\top(\theta -x).\end{equation*}

Since the last term is positive, letting

$\alpha \to \infty$

, we conclude

$\alpha \to \infty$

, we conclude

$b_n(x)=\infty$

. This implies

$b_n(x)=\infty$

. This implies

\begin{equation*} g_n(z) = \inf_{\theta \in \Theta} \{z^\top \theta + b_n(\theta)\} = \inf_{(\theta,b) \in A_n} \{z^\top \theta + b\}, \end{equation*}

\begin{equation*} g_n(z) = \inf_{\theta \in \Theta} \{z^\top \theta + b_n(\theta)\} = \inf_{(\theta,b) \in A_n} \{z^\top \theta + b\}, \end{equation*}

where

$A_n = \{(\theta,b) \in \Theta \times \mathbb{R} \, ; \, g_n(w) \leq w^\top \theta + b \text{ for all } w \in \mathbb{R}^d\}$

. Fix n and z and then take a sequence

$A_n = \{(\theta,b) \in \Theta \times \mathbb{R} \, ; \, g_n(w) \leq w^\top \theta + b \text{ for all } w \in \mathbb{R}^d\}$

. Fix n and z and then take a sequence

$\{(\theta_k,b_k)\} \subset A_n$

such that

$\{(\theta_k,b_k)\} \subset A_n$

such that

$z^\top \theta_k + b_k \to g_n(z)$

. Since

$z^\top \theta_k + b_k \to g_n(z)$

. Since

$\Theta$

is compact, there exists a converging subsequence

$\Theta$

is compact, there exists a converging subsequence

$\{\theta_{k_j}\}$

with limit

$\{\theta_{k_j}\}$

with limit

$\theta_\ast \in \Theta$

. We have

$\theta_\ast \in \Theta$

. We have

$b_{k_j} = z^\top\theta_{k_j} + b_{k_j} - z^\top \theta_{k_j} \to g_n(z) - z^\top \theta_\ast = \! : \, b_\ast$

. Also,

$b_{k_j} = z^\top\theta_{k_j} + b_{k_j} - z^\top \theta_{k_j} \to g_n(z) - z^\top \theta_\ast = \! : \, b_\ast$

. Also,

$w^\top \theta_{k_j} + b_{k_j} \geq g_n(w)$

for all w implies

$w^\top \theta_{k_j} + b_{k_j} \geq g_n(w)$

for all w implies

$w^\top \theta_\ast + b_\ast \geq g_n(w)$

for all w, hence

$w^\top \theta_\ast + b_\ast \geq g_n(w)$

for all w, hence

$(\theta_\ast,b_\ast) \in A_n$

. Thus we obtain (2.13). Conversely, if (2.13) is true, then

$(\theta_\ast,b_\ast) \in A_n$

. Thus we obtain (2.13). Conversely, if (2.13) is true, then

$g_n(z)$

is concave, being the minimum of concave (affine) functions. Since

$g_n(z)$

is concave, being the minimum of concave (affine) functions. Since

\begin{equation*} z_1^\top \theta + b_n(\theta) = z_2^\top \theta + b_n(\theta) + \theta^\top(z_1-z_2) \geq z_2^\top \theta + b_n(\theta) + \min_{\theta \in \Theta} \theta^\top(z_1-z_2), \end{equation*}

\begin{equation*} z_1^\top \theta + b_n(\theta) = z_2^\top \theta + b_n(\theta) + \theta^\top(z_1-z_2) \geq z_2^\top \theta + b_n(\theta) + \min_{\theta \in \Theta} \theta^\top(z_1-z_2), \end{equation*}

Let

$\mathcal{P}_N$

denote the set of the probability measures on

$\mathcal{P}_N$

denote the set of the probability measures on

$(\Omega,\mathscr{F}_N)$

absolutely continuous with respect to

$(\Omega,\mathscr{F}_N)$

absolutely continuous with respect to

$\mathbb{P}$

. For

$\mathbb{P}$

. For

$\hat{\mathbb{P}} \in \mathcal{P}_N$

, there corresponds a

$\hat{\mathbb{P}} \in \mathcal{P}_N$

, there corresponds a

$\Delta_d$

-valued predictable process

$\Delta_d$

-valued predictable process

$\{\hat{P}_n\}$

by (2.4). The measure

$\{\hat{P}_n\}$

by (2.4). The measure

$\hat{\mathbb{P}}$

is recovered from

$\hat{\mathbb{P}}$

is recovered from

$\{\hat{P}_n\}$

by (2.5). Let

$\{\hat{P}_n\}$

by (2.5). Let

$\hat{\mathbb{E}}$

denote the expectation under

$\hat{\mathbb{E}}$

denote the expectation under

$\hat{\mathbb{P}}$

and define

$\hat{\mathbb{P}}$

and define

\begin{equation*} c^g_n(\hat{\mathbb{P}}) = \hat{\mathbb{E}}\Biggl[\sum_{i=n+1}^N b_i(\mathbf{v}\hat{P}_i)\bigg|\mathscr{F}_n\Biggr],\end{equation*}

\begin{equation*} c^g_n(\hat{\mathbb{P}}) = \hat{\mathbb{E}}\Biggl[\sum_{i=n+1}^N b_i(\mathbf{v}\hat{P}_i)\bigg|\mathscr{F}_n\Biggr],\end{equation*}

where

$b_i$

is associated with

$b_i$

is associated with

$g = \{g_n\} \in \mathcal{C}$

via (2.13). The following theorem shows the nature of the g-expectation with the gradient constraint as a nonlinear expectation, taking care of Knightian uncertainty, refining a general convex duality result in [Reference Detlefsen and Scandolo18] for an explicit representation of a penalty function.

$g = \{g_n\} \in \mathcal{C}$

via (2.13). The following theorem shows the nature of the g-expectation with the gradient constraint as a nonlinear expectation, taking care of Knightian uncertainty, refining a general convex duality result in [Reference Detlefsen and Scandolo18] for an explicit representation of a penalty function.

Theorem 2.2. Let

$g \in \mathcal{C}$

. Then, for any

$g \in \mathcal{C}$

. Then, for any

$\mathscr{F}_N$

-measurable random variable Y,

$\mathscr{F}_N$

-measurable random variable Y,

\begin{equation} \mathcal{E}^g_n(Y) = \min_{\hat{\mathbb{P}}\in \mathcal{P}_N} \big\{ \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}}) \big\}, \quad n=0,1,\ldots, N.\end{equation}

\begin{equation} \mathcal{E}^g_n(Y) = \min_{\hat{\mathbb{P}}\in \mathcal{P}_N} \big\{ \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}}) \big\}, \quad n=0,1,\ldots, N.\end{equation}

Proof. By (2.13), we have

\begin{equation*} g_n(z) \leq z^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)\end{equation*}

\begin{equation*} g_n(z) \leq z^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)\end{equation*}

for any

$\hat{\mathbb{P}} \in \mathcal{P}_N$

. Therefore, by Propositions 2.2 and 2.3, we have

$\hat{\mathbb{P}} \in \mathcal{P}_N$

. Therefore, by Propositions 2.2 and 2.3, we have

\begin{equation*} \mathcal{E}^g_n(Y) \leq \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}})\end{equation*}

\begin{equation*} \mathcal{E}^g_n(Y) \leq \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}})\end{equation*}

for any

$\hat{\mathbb{P}} \in \mathcal{P}_N$

. On the other hand, for any

$\hat{\mathbb{P}} \in \mathcal{P}_N$

. On the other hand, for any

$Y \in \mathscr{F}_N$

, there exists the solution

$Y \in \mathscr{F}_N$

, there exists the solution

$\{(Y_n,Z_n)\}$

of (2.7) with

$\{(Y_n,Z_n)\}$

of (2.7) with

$Y_N= Y$

. By (2.13), there exists

$Y_N= Y$

. By (2.13), there exists

$\hat{P}_n$

such that

$\hat{P}_n$

such that

\begin{equation*} g_n(Z_n) = Z_n^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)\end{equation*}

\begin{equation*} g_n(Z_n) = Z_n^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)\end{equation*}

for each n. Since

$\{g_n\}$

and

$\{g_n\}$

and

$\{Z_n\}$

are predictable,

$\{Z_n\}$

are predictable,

$\{\hat{P}_n\}$

is a

$\{\hat{P}_n\}$

is a

$\Delta_d$

-valued predictable process. Let

$\Delta_d$

-valued predictable process. Let

$\hat{\mathbb{P}} \in \mathcal{P}_N$

be associated with

$\hat{\mathbb{P}} \in \mathcal{P}_N$

be associated with

$\{\hat{P}_n\}$

. Then

$\{\hat{P}_n\}$

. Then

$\{(Y_n,Z_n)\}$

solves the BSDE with

$\{(Y_n,Z_n)\}$

solves the BSDE with

$\hat{g}_n(z) = z^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)$

as well, and so by Proposition 2.2,

$\hat{g}_n(z) = z^\top \mathbf{v}\hat{P}_n + b_n(\mathbf{v}\hat{P}_n)$

as well, and so by Proposition 2.2,

\begin{equation*} \mathcal{E}^g_n(Y) = Y_n= \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}}),\end{equation*}

\begin{equation*} \mathcal{E}^g_n(Y) = Y_n= \hat{\mathbb{E}}[Y\mid \mathscr{F}_n] + c^g_n(\hat{\mathbb{P}}),\end{equation*}

which implies (2.14).

Corollary 2.1. Let

$g \in \mathcal{C}$

. Let Y and

$g \in \mathcal{C}$

. Let Y and

$Y^\prime$

be

$Y^\prime$

be

$\mathscr{F}_N$

-measurable random variables.

$\mathscr{F}_N$

-measurable random variables.

-

(i) If

$Y \geq Y^\prime$

, then

$\mathcal{E}^g_n(Y) \geq \mathcal{E}^g_n(Y^\prime)$

,

$n=0,1,\ldots, N$

. -

(ii) For any

$\mathscr{F}_n$

-measurable [0,1]-valued random variable

$\lambda$

,

\begin{equation*} \mathcal{E}^g_n(\lambda Y + (1-\lambda)Y^\prime) \geq \lambda\mathcal{E}^g_n(Y) + (1-\lambda) \mathcal{E}^g_n(Y^\prime), \quad n=0,1,\ldots, N. \end{equation*}

Example 2.5. Let

$\Theta_n \subset \Theta$

and

$\Theta_n \subset \Theta$

and

\begin{equation*} g_n(z) = \inf_{\theta \in \Theta_n} z^\top \theta, \quad n= 1,\ldots, N.\end{equation*}

\begin{equation*} g_n(z) = \inf_{\theta \in \Theta_n} z^\top \theta, \quad n= 1,\ldots, N.\end{equation*}

Here, the set

$\Theta_n$

can be random in such a way that

$\Theta_n$

can be random in such a way that

$g_n$

is

$g_n$

is

$\mathscr{F}_{n-1}\otimes \mathscr{B}(\mathbb{R}^d)$

-measurable. Then we have (2.13) with

$\mathscr{F}_{n-1}\otimes \mathscr{B}(\mathbb{R}^d)$

-measurable. Then we have (2.13) with

$b_n$

such that

$b_n$

such that

$b_n(\theta) = 0$

if

$b_n(\theta) = 0$

if

$\theta \in \bar{\Theta}_n$

while