1. Introduction

Collective defined contribution (CDC) pension schemes have arrived in the UK after a long and fragile genesis (Wilkinson, Reference Wilkinson2024). These are pension schemes that share risks, such as longevity, investment, and inflation risk, collectively among the scheme members. This is different from individual defined contribution (DC) pension schemes, where members bear only their own risk. Unlike defined benefit (DB) pension schemes, the other main form of pension provision in the UK, benefit payments in CDC schemes are not guaranteed; indeed, they are expected to fluctuate. It is important to understand what risks are being borne by which members in CDC schemes and to quantify them, to reduce and mitigate against unfairness between different members.

We study two different whole-life CDC scheme designs. The first is a stylization of the Royal Mail Collective Pension Plan (RMCPP), a single-employer scheme that is the first CDC scheme in the UK. The second models the likely design of the multiemployer schemes that will launch in the next couple of years. Our aim is to compare these two scheme designs and evaluate the extent to which they succeed in their goals: providing an income for life, minimizing intergenerational unfairness, and smoothing pension outcomes. This is important to analyze because if they do not succeed in their goals, then the CDC industry will fail in the UK. The UK’s success or failure is likely to influence the development of CDC schemes in other countries too.

In each of these schemes, the collective risk-sharing is done through declaring the same increases on all members’ benefits, a UK regulatory requirement for CDC schemes. We refer to such schemes as shared-indexation schemes to highlight this common feature of their design.

The first shared-indexation scheme is a flat-accrual scheme, in which the contributions paid into the scheme are a fixed percentage of salaries. In exchange, they receive a deferred retirement income linked to their current salary. This scheme is closely modeled on that of the RMCPP, the first, and currently only, UK CDC scheme in existence. The design of RMCPP has strong similarities with the DB scheme it replaces. The desire to launch the RMCPP has been the driving force behind the introduction of the legislation enabling CDC schemes in the UK (Wilkinson, Reference Wilkinson2024). Combined with the scale of the scheme, which has over 100,000 members, the importance and significance of the RMCPP is clear. It is the prototype for CDC plan design in the UK, for UK regulations and regulators, for actuaries, employers, and workers’ unions.

The second shared-indexation scheme we consider is a dynamic-accrual CDC scheme, which is the anticipated design of the multiemployer whole-life CDC schemes that are due to be authorized in 2026 in the UK (Wilkinson, Reference Wilkinson2024; Upton, Reference Upton2024). Multiemployer decumulation-only CDC schemes, which have recently been consulted on by the UK’s Department of Work and Pensions, are also expected to follow a dynamic-accrual approach. In such a scheme, members can choose how much to contribute and, in return, receive a deferred retirement income that reflects financial market conditions at the time the contribution was paid.

Due to the novelty of UK CDC schemes, with the RMCPP launched in October 2024, there is little literature on their unique design. A 2023 report prepared for the Association of British Insurers (ABI) (Taylor & Ward, Reference Taylor and Ward2023) summarizes numerous industry studies of similar designs, The Government Actuary’s Department (2009); AON (2013); Popat et al. (Reference Popat, Curry, Pike and Ellis2015); Taylor & Ward (Reference Taylor and Ward2023); Blake (Reference Blake2016); Willis Towers Watson (2020), as well as providing its own additional analysis. However, there are important differences in details between the scheme designs in these studies and the RMCPP. Notable differences include the use of buffers and funding corridors. Of these studies, only two perform stochastic modeling (The Government Actuary’s Department, 2009; Popat et al., Reference Popat, Curry, Pike and Ellis2015). In the academic literature, Owadally et al. (Reference Owadally, Ram and Regis2022) discuss CDC plans in the UK with respect to policy, as well as their risks and the ensuing advantages and disadvantages, and model an earlier proposal stochastically. They also compare the outcomes for a single member of their CDC plan model against typical DC-based alternative pension schemes when the scheme is mature. They find that their CDC plan can pay higher and more stable pensions compared to the alternative schemes considered.

This paper contributes to the literature in several ways. First, in Section 2, we describe an explicit mathematical model for shared-indexation CDC schemes. This model describes the contract of such a scheme. Once the realized contributions and investments are known, this model describes what the resulting benefits will be. In the case of the dynamic-accrual CDC scheme, this gives a precise operationalization of the broad shared understanding among pension professionals of what a dynamic-accrual CDC scheme should entail.

In describing a flat-accrual scheme, we follow the key design features of the RMCPP, but there are differences that we now summarize. Only a single-life pension in retirement is valued in our model – spousal benefits, death benefits, and the UK’s tax-free cash lump sum payment made at the point of retirement are omitted. We include an upper bound on indexation, which is not present in the RMCPP, but is required for dynamic-accrual and so aids comparison between the two scheme types. We assume that benefit cuts and bonuses that must occur when the fund is significantly over- or under-funded take effect immediately, rather than over time, as is done for benefit cuts in the RMCPP. In our model, the relationship between contribution rate and level of benefits is determined by choosing a long-term target rate of indexation. In the RMCPP, these levels are fixed in the Trust Deed and Rules (Slaughter and May, 2024), but it is not specified how they are determined. Nevertheless, the member handbook does suggest that “The aim is to provide increases to help keep up with the cost of living” (Royal Mail Collective Pension Plan, 2024, p. 67).

We endeavor to make a clear separation between the contract of a CDC fund and our modeling assumptions. Section 2 describes the contract. Section 3 describes modeling assumptions, including demographic and economic factors.

Having established the contract of CDC funds, the second way our paper contributes to the literature is by studying the extent of intergenerational cross-subsidy in CDC funds. This is the topic of Section 4.

We find that flat-accrual schemes and dynamic-accrual schemes contain very different levels of cross-subsidies. A dominant source of cross-subsidy in the flat-accrual scheme results from the combination of a fixed contribution rate and a fixed-accrual rate. This favors participants who are close to retirement, as they receive the same benefit amount as younger members for the same contribution, despite there being less time for their investments to grow. This qualitatively mirrors the behavior of the DB scheme that the RMCPP flat-accrual scheme is designed to replace. However, when examined quantitatively, we find that the level of cross-subsidy is considerably higher in a flat-accrual scheme than in a DB scheme.

Since the earliest generations in a flat-accrual scheme receive an income that is worth more than the value of their lifetime contributions, subsequent generations must receive an income that is worth less than their contributions. We find that the flat-accrual scheme broadly tends to a long-term steady-state situation where typical generations receive a retirement income worth less than their contributions. One can think of this as later generations paying interest on the debt built up by overpaying the earliest generations. We refer to this effect as “drag.” It may appear counterintuitive that a scheme can enter a steady state that is not actuarially fair. This is possible because over an infinite time horizon, one cannot argue that the total money paid into the scheme must equal the total money paid out, so we will also refer to this as an “infinite-horizon effect.”

The dynamic-accrual scheme is designed to avoid the obvious cross-subsidies of a flat-accrual scheme. It is instead intended to be actuarially fair, in the sense that members’ contributions match their new benefit entitlements at the time of each contribution. However, the implicit pricing methodology that has been proposed in industry to do this is only approximate, and so cross-subsidies still appear. These cross-subsidies are stochastic in nature, meaning one cannot predict in advance that generations will lose out.

We briefly consider two ways to mitigate the cross-subsidies we have identified. If a flat-accrual scheme is designed to replace a DB scheme, one might wish to design a scheme that has similar levels of cross-subsidy to the DB scheme it seeks to replace. This could be done using an age-based accrual rather than a flat-accrual. In a dynamic-accrual scheme, we show how to statistically calibrate a pricing formula to obtain fairer prices for benefits than the formula proposed by the industry. These mitigations are able to manage the level of cross-subsidies without departing from a shared-indexation design, but do not eliminate them entirely.

We use two distinct methodologies to examine the cross-subsidies. The cross-subsidies in a flat-accrual scheme and the notion of drag can be studied using a constant economic model (by which we mean a deterministic model where inflation, wage inflation, interest rates, and stock growth over each period are all constant). This allows us to find analytic results. However, the cross-subsidies in a dynamic-accrual scheme require stochastic modeling. In this case, we use a Black–Scholes economic model in order to ensure that any pension income can be priced unambiguously using the theory of risk-neutral pricing. The cross-subsidies then emerge from the difference between the true risk-neutral price and the discounting formulae used to determine how much members are charged for their pension benefits. In the case of flat-accrual schemes, stochastic modeling confirms the results obtained using a constant economic model.

Cross-subsidies have been studied in other types of CDC schemes, and the high cross-subsidies and consequent drag are a specific consequence of the flat-accrual design. For example, Haan, Lekniute, and Ponds (Reference Haan, Lekniute and Ponds2015) study a Dutch-style CDC scheme and show a greater financial fairness of those pension schemes.

The third way we contribute to the literature is by simulating the behavior of these funds using a stochastic economic model and comparing the performance to other scheme designs. This is done in Section 5, using the model described by Alvares Maffra, et al. (Reference Alvares Maffra, Armstrong and Pennanen2021). We compare the performance with the alternatives of DC schemes and a pooled annuity fund. Similar stochastic models have been used to study CDC designs that have been proposed for use in the UK, e.g., Popat et al. (Reference Popat, Curry, Pike and Ellis2015); Owadally et al. (Reference Owadally, Ram and Regis2022), but not for the current shared-indexation design of the RMCPP.

In all our modeling in this paper, we assume there is no systematic longevity risk, and there are sufficient numbers of members so that individual longevity risk is eliminated through pooling. We do not allow for any heterogeneity in the schemes in our simulations. However, we do show how heterogeneity can be incorporated into the scheme design if desired; results from simulating heterogeneous funds are discussed in Upton (Reference Upton2024).

The fourth contribution to the literature is studying the extent to which shared-indexation schemes are able to smooth pension incomes. This is considered in Section 6.

The design of shared-indexation schemes is such that younger generations experience greater volatility in the value of their future benefits, while older generations experience a smoothing in this value. This allows the fund to invest in riskier assets while still providing a smooth income in retirement. Other CDC plans studied in the literature have the same feature, and they can also outperform alternative pension options by taking on more investment risk (Bonenkamp & Westerhout, Reference Bonenkamp and Westerhout2014; Cui et al., Reference Cui, De Jong and Ponds2011; Gollier, Reference Gollier2008).

We find that the shared-indexation designs do provide some smoothing of benefits after retirement, but they do not smooth projected benefits before retirement by as much as has been suggested (AON, 2013). The discrepancy between our results and the literature can be attributed to the fact that none of the studies we examined attempted to compute projected benefits using a stochastic model, and the deterministic approximations used to project benefits are not sufficiently accurate for this purpose.

Our fifth contribution is in Section 7, where we consider how a scheme designer might control the outcomes in a CDC fund. We find that it is quite easy in a flat-accrual scheme to target a particular growth rate for median incomes in retirement by adjusting the relationship between benefits and contributions. This flexibility is not available in a dynamic-accrual scheme, making it difficult to design a scheme so that it will produce a desired level of indexation.

Our final contribution, in Section 8, is to briefly consider model risk by evaluating the cross-subsidies that occur when actual investment returns differ from their predictions. Since the level of pensions paid out depends on future predictions of returns, poor predictions of those returns lead to pension payments that are, in hindsight, either too low or too high. Consequently, future generations have higher or lower pensions. This type of cross-subsidy can go either way: it may benefit earlier or later generations to join. However, it is also true that once the plan begins its life, the cost due to previous predictions deviating from their observed expected values could be calculated.

Our key findings are that:

-

• dynamic-accrual schemes are not able to target a given level of annual pension increases as effectively as flat-accrual schemes;

-

• dynamic-accrual schemes have substantially lower intergenerational cross-subsidies than flat-accrual schemes;

-

• dynamic-accrual schemes still feature some level of intergenerational cross-subsidy as a result of the use of approximate pricing formulae in the design of CDC funds;

-

• flat-accrual schemes do not necessarily have higher pension outcomes than DC followed by life annuity purchase at retirement;

-

• dynamic-accrual schemes can markedly outperform flat-accrual schemes because they do not experience drag effects;

-

• shared-indexation CDC schemes do not result in as much smoothing of projected pension benefits as has been suggested in the literature;

-

• nominal benefits are not an accurate means for estimating projected benefits.

2. The contract of shared-indexation CDC funds

In this section, we detail the contractual aspects of shared-indexation CDC funds. The aspects of their operation that are common to both flat- and dynamic-accrual funds, namely, the annual indexation of accrued pensions, are described first. We then explain the different approaches taken in the flat- and dynamic-accrual CDC funds to the accrual of benefits. In online Appendix D, we explain briefly how our description of CDC funds corresponds to the UK regulations.

2.1 Elements common to all shared-indexation CDC funds

2.1.1 Scheme membership and contributions

To describe the operation, we assume there are a total of

$M$

different types of individual investing in the fund over time, indexed by

$M$

different types of individual investing in the fund over time, indexed by

$\xi \in \{0, 1,2,\ldots ,M-1\}$

. All individuals of type

$\xi \in \{0, 1,2,\ldots ,M-1\}$

. All individuals of type

$\xi$

share the same demographic and financial characteristics. For the numerical examples in this paper,

$\xi$

share the same demographic and financial characteristics. For the numerical examples in this paper,

$\xi$

is simply a generation index (Upton (Reference Upton2024) studies the situation when individuals vary by both generation and sex). Each individual of type

$\xi$

is simply a generation index (Upton (Reference Upton2024) studies the situation when individuals vary by both generation and sex). Each individual of type

$\xi$

who is below the retirement age makes a contribution

$\xi$

who is below the retirement age makes a contribution

$C^\xi _t$

at time

$C^\xi _t$

at time

$t$

and receives, in exchange, an additional nominal benefit amount

$t$

and receives, in exchange, an additional nominal benefit amount

$B^\xi _t$

in retirement.

$B^\xi _t$

in retirement.

2.1.2 Cumulative benefit and new benefit accrual amounts

At any time

$t$

, each individual of type

$t$

, each individual of type

$\xi$

has accrued a cumulative nominal benefit of annual amount

$\xi$

has accrued a cumulative nominal benefit of annual amount

$B^{\xi ,\mathrm{cum}}_{t-}$

before new contributions. At time

$B^{\xi ,\mathrm{cum}}_{t-}$

before new contributions. At time

$0$

, this is equal to

$0$

, this is equal to

$0$

and we will describe inductively below how the value is computed at subsequent times. Assuming the value

$0$

and we will describe inductively below how the value is computed at subsequent times. Assuming the value

$B^{\xi ,\mathrm{cum}}_{t-}$

is known at time

$B^{\xi ,\mathrm{cum}}_{t-}$

is known at time

$t$

, after paying a contribution at time

$t$

, after paying a contribution at time

$t \in \mathbb{N}_{0}$

, the individual accrues an additional annual nominal benefit of amount

$t \in \mathbb{N}_{0}$

, the individual accrues an additional annual nominal benefit of amount

$B^\xi _t$

. This increases their cumulative nominal benefit to

$B^\xi _t$

. This increases their cumulative nominal benefit to

\begin{align*} B^{\xi ,\mathrm{cum}}_t \,:\!=\, B^{\xi ,\mathrm{cum}}_{t-}+B^\xi _t. \end{align*}

\begin{align*} B^{\xi ,\mathrm{cum}}_t \,:\!=\, B^{\xi ,\mathrm{cum}}_{t-}+B^\xi _t. \end{align*}

Members do not accrue benefits until they begin contributing to the scheme (which may be at times

$t\gt 1$

; the notation considers all members who are ever in the scheme, even those not currently in the scheme). Retired individuals are paid

$t\gt 1$

; the notation considers all members who are ever in the scheme, even those not currently in the scheme). Retired individuals are paid

$B^{\xi ,\mathrm{cum}}_t$

at time

$B^{\xi ,\mathrm{cum}}_t$

at time

$t$

. For individuals who have not yet retired,

$t$

. For individuals who have not yet retired,

$B^{\xi ,\mathrm{cum}}_t$

represents their currently accrued benefit entitlement before allowance for future pension increases and benefit adjustments.

$B^{\xi ,\mathrm{cum}}_t$

represents their currently accrued benefit entitlement before allowance for future pension increases and benefit adjustments.

2.1.3 Pension increase mechanism

Each year, all accrued pensions are increased by the same pension increase factor

$\theta _t (1 + h^{\mathrm{nom}}_{t})$

, in which

$\theta _t (1 + h^{\mathrm{nom}}_{t})$

, in which

$\theta _t$

is a bonus level and

$\theta _t$

is a bonus level and

$h^{\mathrm{nom}}_{t}$

is the nominal indexation rate. It is currently a UK regulatory requirement that scheme members must receive identical adjustments to their accrued benefits. This is the defining characteristic of a shared-indexation scheme.

$h^{\mathrm{nom}}_{t}$

is the nominal indexation rate. It is currently a UK regulatory requirement that scheme members must receive identical adjustments to their accrued benefits. This is the defining characteristic of a shared-indexation scheme.

The procedure for determining the pair

$(h^{\mathrm{nom}}_{t}, \theta _t)$

is described next. Denote by

$(h^{\mathrm{nom}}_{t}, \theta _t)$

is described next. Denote by

$q_t=\frac {\mathsf{CPI}_t}{\mathsf{CPI}_{t-1}}-1$

the annual effective rate of change in the Consumer Price Index,

$q_t=\frac {\mathsf{CPI}_t}{\mathsf{CPI}_{t-1}}-1$

the annual effective rate of change in the Consumer Price Index,

$\mathsf{CPI}_t$

, from time

$\mathsf{CPI}_t$

, from time

$t-1$

to time

$t-1$

to time

$t$

. Define the real indexation rate

$t$

. Define the real indexation rate

$h_t$

, at time

$h_t$

, at time

$t$

, as the solution to

$t$

, as the solution to

\begin{align*} 1 + h^{\mathrm{nom}}_{t} = (1 + h_t) \left ( 1 + q_t \right )\!. \end{align*}

\begin{align*} 1 + h^{\mathrm{nom}}_{t} = (1 + h_t) \left ( 1 + q_t \right )\!. \end{align*}

After the pension increase factor is determined at time

$t$

, the total benefit accrued by each individual of type

$t$

, the total benefit accrued by each individual of type

$\xi$

becomes

$\xi$

becomes

\begin{equation} B^{\xi ,\mathrm{cum}}_{t-} \,:\!=\, \theta _t \, (1 + q_t)(1 + h_t) \, B^{\xi ,\mathrm{cum}}_{t-1}, \quad \text{for }t\geq 1. \end{equation}

\begin{equation} B^{\xi ,\mathrm{cum}}_{t-} \,:\!=\, \theta _t \, (1 + q_t)(1 + h_t) \, B^{\xi ,\mathrm{cum}}_{t-1}, \quad \text{for }t\geq 1. \end{equation}

2.1.4 Calculation of pension increases

Broadly, to calculate the real indexation rate

$h_t$

at time

$h_t$

at time

$t$

, first, the accrued benefits are projected from time

$t$

, first, the accrued benefits are projected from time

$t$

onwards assuming that the future real indexation rate remains

$t$

onwards assuming that the future real indexation rate remains

$h_t$

at all future times

$h_t$

at all future times

$s \geq t$

. Discounting the projected pension payments back to time

$s \geq t$

. Discounting the projected pension payments back to time

$t$

, their total value is equated with the market value of the scheme’s assets. The resulting expression can be solved for

$t$

, their total value is equated with the market value of the scheme’s assets. The resulting expression can be solved for

$h_t$

.

$h_t$

.

The design spreads the impact of market shocks over time, through changes to long-term indexation. We explain in more detail below how this smooths pensions in retirement. The projection of accrued pensions using an annual pension increase rate reflects the approach taken in UK DB schemes, although DB schemes typically apply a predetermined rate, such as CPI. The design of the RMCPP was strongly influenced by DB scheme principles, embedding those features into its structure. As UK regulations were developed to authorize the RMCPP, this approach became embedded in the regulatory framework.

However, there are some critical elements necessary to complete the calculation. The real indexation rate

$h_t$

is constrained to lie in the range

$h_t$

is constrained to lie in the range

$[-q_t, h^{\mathrm{upper}}_t]$

, in which

$[-q_t, h^{\mathrm{upper}}_t]$

, in which

$h^{\mathrm{upper}}_t \geq -q_t$

is chosen by the scheme manager. Although in the RMCPP, a flat-accrual scheme,

$h^{\mathrm{upper}}_t \geq -q_t$

is chosen by the scheme manager. Although in the RMCPP, a flat-accrual scheme,

$h^{\mathrm{upper}}_t = \infty$

, we will assume a finite upper limit for our studied flat-accrual scheme. In the considered dynamic-accrual scheme,

$h^{\mathrm{upper}}_t = \infty$

, we will assume a finite upper limit for our studied flat-accrual scheme. In the considered dynamic-accrual scheme,

$h^{\mathrm{upper}}_t \lt \infty$

and the goal is to ensure that the nominal indexation rate awarded at time

$h^{\mathrm{upper}}_t \lt \infty$

and the goal is to ensure that the nominal indexation rate awarded at time

$t$

on accrued benefits is neither negative nor too high. The use of such constraints on the value of

$t$

on accrued benefits is neither negative nor too high. The use of such constraints on the value of

$h_t$

is embedded in regulation. It is viewed by practitioners as necessary to ensure that the scheme provides planned benefit increases that will be acceptable to members.

$h_t$

is embedded in regulation. It is viewed by practitioners as necessary to ensure that the scheme provides planned benefit increases that will be acceptable to members.

If the solution

$h_t$

to the expression involving the scheme’s asset value and discounted benefits would imply breaching either of these limits, then the real indexation level is set equal to the relevant limit and a bonus level

$h_t$

to the expression involving the scheme’s asset value and discounted benefits would imply breaching either of these limits, then the real indexation level is set equal to the relevant limit and a bonus level

$\theta _t$

is applied to the accrued benefit entitlements.

$\theta _t$

is applied to the accrued benefit entitlements.

The intention is that, when the limits on

$h_t$

are not breached, then

$h_t$

are not breached, then

$\theta _t=1$

and changes to benefits arise only from the indexation rates. If, for example, the solution implied

$\theta _t=1$

and changes to benefits arise only from the indexation rates. If, for example, the solution implied

$h_t \lt -q_t$

, then

$h_t \lt -q_t$

, then

$h_t\,:\!=\,-q_t$

and the bonus level falls below one, i.e.,

$h_t\,:\!=\,-q_t$

and the bonus level falls below one, i.e.,

$\theta _t \lt 1$

, corresponding to a nominal benefit cut. The calculation of the value of

$\theta _t \lt 1$

, corresponding to a nominal benefit cut. The calculation of the value of

$\theta _t$

is explained more fully below.

$\theta _t$

is explained more fully below.

Let:

-

•

$N^{\xi }_t$

be the number of surviving individuals of type

$\xi$

in the fund at time

$t$

.

$N^{\xi }_t$

be the number of surviving individuals of type

$\xi$

in the fund at time

$t$

. -

•

$p^{\xi }_{t,k}$

be the probability that an individual of type

$\xi$

survives from time

$t$

to time

$t+k$

, given that they are alive and age

$x$

at time

$t$

. It is assumed that future lifetimes are independent random variables. -

•

$\nu ^{\xi }_{t,k}$

be the cumulative discount factor for an individual of type

$\xi$

, that discounts 1 unit paid at time

$t+k$

back to time

$t$

. Let

$\hat {R}^{\xi }_{t,k}$

be the expected annual effective rate of return at time

$t$

of the assets invested, in the time period

$[\!\max \{t+k-1,t\}, t+k)$

, in line with the investment strategy associated with individuals of type

$\xi$

. Then, for

$k \in \mathbb{N}_0$

,

\begin{align*} \nu ^{\xi }_{t,k} = \prod _{n=0}^{k} \big(1+\hat {R}^{\xi }_{t,n}\big)^{-1}. \end{align*}

Note that

$\hat {R}^{\xi }_{t,0}=0$

. We will describe how the asset mix associated with an individual is determined in our models in Section 3.4. When the scheme operates in practice, the appropriate rates of return for different asset classes are determined by regulatory reporting standards, but in our simulations, they are determined by our models. The only asset classes used in our simulations are an equity market index and index-linked bonds. -

•

$\widehat {q}_{t,k}$

be the projection made at time

$t$

, of the annual change in CPI from time

$t+k-1$

to time

$t + k$

, for

$k=0,1,2,\ldots$

. Note that

$\widehat {q}_{t,0}=q_t$

, the actual change in CPI over the year to time

$t$

. -

•

$I_{t,k}(\mathsf{h})$

be the projection made at time

$t$

of the cumulative nominal indexation rate from time

$t$

to time

$t+k$

, using a constant real indexation rate

$\mathsf{h}$

, for

$k = 0,1,2,\ldots$

, which is calculated as

\begin{align*} I_{t,k}(\mathsf{h}) \,:\!=\, \prod _{n=0}^{k} (1 + \widehat {q}_{t,n})(1 + \mathsf{h}). \end{align*}

-

•

${\mathbf{1}}^{\xi , \mathrm{Ret}}_t$

be the deterministic indicator function taking the value

$1$

if individuals of type

$\xi$

have retired at time

$t$

, and

$0$

otherwise. -

•

$A_{t-}$

be the value of assets at time

$t$

, just before new contributions are added or benefit payments are made at time

$t$

.

We now define

$\mathcal{L}_{t-}(\mathsf{h}, \vartheta )$

to be the discounted value of the accrued benefits at time

$\mathcal{L}_{t-}(\mathsf{h}, \vartheta )$

to be the discounted value of the accrued benefits at time

$t$

, just before new contributions are added or benefit payments are made, where the real indexation rate used to project the accrued pensions from time

$t$

, just before new contributions are added or benefit payments are made, where the real indexation rate used to project the accrued pensions from time

$t-1$

is

$t-1$

is

$\mathsf{h}$

, and the bonus level applied at time

$\mathsf{h}$

, and the bonus level applied at time

$t$

is

$t$

is

$\vartheta$

. Thus,

$\vartheta$

. Thus,

\begin{equation} \mathcal{L}_{t-}(\mathsf{h}, \vartheta ) \,:\!=\, \vartheta \sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t-1} \, \sum _{k=0}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(\mathsf{h}) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

\begin{equation} \mathcal{L}_{t-}(\mathsf{h}, \vartheta ) \,:\!=\, \vartheta \sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t-1} \, \sum _{k=0}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(\mathsf{h}) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

Equating the asset value with the discounted benefits yields a function of the unknown real indexation rate

$\mathsf{h}$

and the unknown bonus level

$\mathsf{h}$

and the unknown bonus level

$\vartheta$

, i.e.,

$\vartheta$

, i.e.,

\begin{equation} A_{t-} = \mathcal{L}_{t-}(\mathsf{h}, \vartheta ) \end{equation}

\begin{equation} A_{t-} = \mathcal{L}_{t-}(\mathsf{h}, \vartheta ) \end{equation}

A solution for the pair

$(\mathsf{h},\vartheta )$

is first sought by setting

$(\mathsf{h},\vartheta )$

is first sought by setting

$\vartheta \,:\!=\,1$

in (2) and solving for the constant

$\vartheta \,:\!=\,1$

in (2) and solving for the constant

$\mathsf{h}$

. There are three possible outcomes at each time

$\mathsf{h}$

. There are three possible outcomes at each time

$t$

.

$t$

.

-

• If

$\mathsf{h} \in [\!-q_t, h^{\mathrm{upper}}_t]$

, then

$h_t \,:\!=\, \mathsf{h}$

is the real indexation rate declared at time

$t$

, and no bonus is awarded, i.e.,

$\theta _t\,:\!=\,1$

. -

• If

$\mathsf{h} \lt -q_t$

, then the real indexation rate declared at time

$t$

is

$h_t \,:\!=\, -q_t$

. The expression (2) is solved for

$\vartheta$

with the free variable

$\mathsf{h}\,:\!=\,-q_t$

. The solution is the declared bonus, i.e.,

$\theta _t \,:\!=\, \vartheta$

, and it corresponds to a nominal benefit cut, i.e.,

$\theta _t\lt 1$

. -

• Similarly, if

$\mathsf{h} \gt h^{\mathrm{upper}}$

, then

$h_t \,:\!=\, h^{\mathrm{upper}}$

and expression (2) is solved for

$\vartheta$

with the free variable

$\mathsf{h}\,:\!=\,h^{\mathrm{upper}}$

. The solution is the declared bonus, that is,

$\theta _t \,:\!=\, \vartheta$

, corresponding to a uniform increase in the accrued benefits, i.e.,

$\theta _t\gt 1$

.

The net effect is to ensure that assets match discounted liabilities at all times, that

$h$

is appropriately constrained, and that benefit cuts and bonuses only occur if the constraints would be violated.

$h$

is appropriately constrained, and that benefit cuts and bonuses only occur if the constraints would be violated.

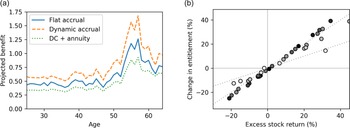

In Figure 1, we show a stylized picture of how the projected benefits change under two different pension increases. The dotted line depicts the projected benefits over time just before a shock occurs. In the example shown, markets have performed better than expected. Suppose that the concomitant increase to benefits can be distributed either as a uniform one-off increase by changing the one-off bonus level

$\vartheta$

, shown as a dashed line, or by changing the nominal indexation rate, shown as a solid line.

$\vartheta$

, shown as a dashed line, or by changing the nominal indexation rate, shown as a solid line.

A stylized diagram of how increased benefits might be distributed among different age groups when the market outperforms expectations.

The shaded regions illustrate the projected retirement benefits that are expected by two different generations. The left-hand colored block in Figure 1 shows the income received during retirement for a generation that has already retired. Its area represents the total income. The relative increase in their benefits when the nominal indexation rate

$h$

increases, depicted with lighter shading, is small.

$h$

increases, depicted with lighter shading, is small.

Similarly, the right-hand colored block indicates the retirement income for a generation that is yet to retire. The paler shaded area is much larger, showing that their retirement benefits are much more sensitive to changes in

$h$

. The increase in their annual pension in retirement is higher than that of the retired generation, compared to before the shock. If the shock results in a reduction in benefits, then the young would have a larger relative decrease in their pension at retirement, compared to the old.

$h$

. The increase in their annual pension in retirement is higher than that of the retired generation, compared to before the shock. If the shock results in a reduction in benefits, then the young would have a larger relative decrease in their pension at retirement, compared to the old.

Thus, using annual indexation rates results in lower volatility in the annual benefit amount paid to older generations. In exchange, there is a greater fluctuation in projected benefits for the younger generations. In other words, there is a risk transfer from the older to the younger generations. This argument is heuristic and should be seen as motivational; a more precise argument is made in Section 6.

In contrast, using only a one-off bonus level means that annual benefit amounts change by the same percentage. No pension smoothing would take place.

However, in our shared indexation schemes, the actual adjustment to benefits is a combination of an indexation rate (which is compounded annually to project future benefits) and a one-off bonus (which is applied only at its calculation time and is not reapplied in each projected year). The combination of using both indexation rates and one-off bonuses means that there are limits on the transfer of risk from the old to the young.

In RMCPP, nominal benefit cuts (corresponding to

$\theta _t \lt 0.95$

) are spread over two or three years with the goal of trying to keep reductions to at most 5% each year. Positive bonuses (i.e.

$\theta _t \lt 0.95$

) are spread over two or three years with the goal of trying to keep reductions to at most 5% each year. Positive bonuses (i.e.

$\theta _t \gt 1$

) can occur if they are used to mitigate against these multiyear reductions. In our flat-accrual scheme design, benefit cuts and bonuses are applied in full immediately, for simplicity.

$\theta _t \gt 1$

) can occur if they are used to mitigate against these multiyear reductions. In our flat-accrual scheme design, benefit cuts and bonuses are applied in full immediately, for simplicity.

The design does not allow individuals to customize their investment strategy in line with their risk preferences. The benefit increases received by different individuals are uniform across members and are not dependent on their chosen investment strategy. The purpose of associating an investment strategy with different individuals is to ensure that the asset mix of the fund will change if the demographics of the fund change significantly (as happens during start-up and shut-down of the scheme). When the scheme closes, the fund will invest more heavily in bonds. This is broadly intended to compensate for the reduced smoothing that will occur, but is only heuristically justified.

The inability to accommodate different risk preferences is a weakness of the shared-indexation design. However, proponents of the approach argue that most members want all decisions to be made for them, making a one-size-fits-all approach acceptable.

2.1.5 Asset and discounted benefit value dynamics

The scheme’s asset value evolves as

\begin{align*} A_{t-}=\begin{cases} 0 & \textrm {if $t = 0$}, \\ (1 + R_t) A_{t-1} & \textrm {if $t=1,2,\ldots $}. \end{cases} \end{align*}

\begin{align*} A_{t-}=\begin{cases} 0 & \textrm {if $t = 0$}, \\ (1 + R_t) A_{t-1} & \textrm {if $t=1,2,\ldots $}. \end{cases} \end{align*}

Here,

$R_t$

denotes the return realized by the fund on its investments over the time period

$R_t$

denotes the return realized by the fund on its investments over the time period

$(t-1,t]$

.

$(t-1,t]$

.

The assets of the fund at time

$t$

, after new payments have been received and annual pension payments have been made, are

$t$

, after new payments have been received and annual pension payments have been made, are

\begin{equation} A_{t} \,:\!=\, A_{t-} + \sum _{\xi =0}^{M-1} N^\xi _t \big(C^\xi _t - B^{\xi ,\mathrm{cum}}_t {\mathbf{1}}^{R,\xi }_t\big). \end{equation}

\begin{equation} A_{t} \,:\!=\, A_{t-} + \sum _{\xi =0}^{M-1} N^\xi _t \big(C^\xi _t - B^{\xi ,\mathrm{cum}}_t {\mathbf{1}}^{R,\xi }_t\big). \end{equation}

After new payments have been received and annual pension payments have been made at time

$t$

, the discounted benefit value is

$t$

, the discounted benefit value is

\begin{equation} \mathcal{L}_{t} \,:\!=\, \sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

\begin{equation} \mathcal{L}_{t} \,:\!=\, \sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

Note that the benefits paid out at time

$t$

are excluded from the calculation of

$t$

are excluded from the calculation of

$\mathcal{L}_{t}$

. Additionally, as

$\mathcal{L}_{t}$

. Additionally, as

$\theta _t$

is already incorporated into

$\theta _t$

is already incorporated into

$B^{\xi ,\mathrm{cum}}_{t}$

, the bonus level is neutral (i.e.,

$B^{\xi ,\mathrm{cum}}_{t}$

, the bonus level is neutral (i.e.,

$\theta _t=1$

) in this calculation. For brevity, we will sometimes call the quantity

$\theta _t=1$

) in this calculation. For brevity, we will sometimes call the quantity

${\mathcal L}_t$

the liability at time

${\mathcal L}_t$

the liability at time

$t$

, although, since the fund does not promise any particular pension payment, it is not strictly speaking a liability.

$t$

, although, since the fund does not promise any particular pension payment, it is not strictly speaking a liability.

It is straightforward to show that

\begin{align*} \begin{split} \mathcal{L}_{t} &= \mathcal{L}_{t-}(h_t,\theta _t)\\ &\hphantom {=:} - \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t} \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t}}_{\text{Benefits paid out at time $t$}} + \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi }_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}}_{\text{Discounted new benefits accrued at time $t$}}. \end{split} \end{align*}

\begin{align*} \begin{split} \mathcal{L}_{t} &= \mathcal{L}_{t-}(h_t,\theta _t)\\ &\hphantom {=:} - \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi ,\mathrm{cum}}_{t} \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t}}_{\text{Benefits paid out at time $t$}} + \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi }_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}}_{\text{Discounted new benefits accrued at time $t$}}. \end{split} \end{align*}

Since

$A_{t-} = \mathcal{L}_{t-}$

, substitution from (4) leads to

$A_{t-} = \mathcal{L}_{t-}$

, substitution from (4) leads to

\begin{align} \underbrace {A_t - \mathcal{L}_{t}}_{\substack {\text{Asset value less} \\ \text{discounted benefits} \\ \text{at time $t$}}} &= \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, C^\xi _t}_{\text{Contributions paid at time $t$}} \nonumber \\ &\hphantom {=:} - \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi }_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}}_{\text{Discounted new benefits accrued at time $t$}}. \end{align}

\begin{align} \underbrace {A_t - \mathcal{L}_{t}}_{\substack {\text{Asset value less} \\ \text{discounted benefits} \\ \text{at time $t$}}} &= \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, C^\xi _t}_{\text{Contributions paid at time $t$}} \nonumber \\ &\hphantom {=:} - \underbrace {\sum _{\xi =0}^{M-1} N^\xi _t \, B^{\xi }_{t} \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}}_{\text{Discounted new benefits accrued at time $t$}}. \end{align}

The last expression shows that if new contributions do not equal the value of the newly accrued benefits, then there will be an immediate scheme gain or loss at time

$t$

. This is in spite of the asset value equaling the discounted benefits immediately before the contributions are paid at time

$t$

. This is in spite of the asset value equaling the discounted benefits immediately before the contributions are paid at time

$t$

, i.e.,

$t$

, i.e.,

$A_{t-} = \mathcal{L}_{t-}(h_t,\theta _t)$

.

$A_{t-} = \mathcal{L}_{t-}(h_t,\theta _t)$

.

For this reason, the contribution rate is chosen so that, when a flat-accrual CDC scheme has a stable population, the right-hand side of equation (6) is zero. As the same contribution rate is used in the dynamic-accrual scheme for our numerical illustrations, there are different changes in the scheme’s funding position immediately after new contributions are made, depending on whether the scheme is a flat- or dynamic-accrual scheme, as discussed in Sections 2.2 and 2.3.

2.2 Flat-accrual scheme design

A flat-accrual CDC scheme has a design similar to a typical UK DB scheme. Like DB schemes, income benefits in flat-accrual CDC schemes are accrued at a constant proportion of salaries in exchange for a fixed rate of salaries being paid as contributions. This means that a member who is approaching retirement accrues the same amount of annual benefit as a member at the start of their career, assuming they pay the same contribution amount.

This leads to a difference in the value of the benefits accrued to the value of the contributions made in respect of those accrued benefits. Younger active members contribute more than the value of the benefits they are accruing, whereas older active members contribute less.

Let

$S^\xi _t$

denote the salary of individuals of type

$S^\xi _t$

denote the salary of individuals of type

$\xi$

, at time

$\xi$

, at time

$t$

. We write

$t$

. We write

$\mathbf{1}^{C,\xi }_t$

for the indicator function taking the value

$\mathbf{1}^{C,\xi }_t$

for the indicator function taking the value

$1$

if individuals of type

$1$

if individuals of type

$\xi$

make a contribution in year

$\xi$

make a contribution in year

$t$

, and 0 otherwise.

$t$

, and 0 otherwise.

Let the constant

$1/\beta$

be the accrual rate, that is, the proportion of salaries accrued as an annual benefit at time

$1/\beta$

be the accrual rate, that is, the proportion of salaries accrued as an annual benefit at time

$t$

by all currently contributing members. Then, the benefit amount accrued at time

$t$

by all currently contributing members. Then, the benefit amount accrued at time

$t$

, by each individual of type

$t$

, by each individual of type

$\xi$

, due to the contributions made at time

$\xi$

, due to the contributions made at time

$t$

in the flat-accrual model is

$t$

in the flat-accrual model is

\begin{equation} B^\xi _t=\frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t, \end{equation}

\begin{equation} B^\xi _t=\frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t, \end{equation}

which has a discounted value at time

$t$

of

$t$

of

\begin{equation} \frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

\begin{equation} \frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h_t) \, \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}. \end{equation}

Let the constant

$\alpha \gt 0$

be the proportion of salaries, which are paid at time

$\alpha \gt 0$

be the proportion of salaries, which are paid at time

$t$

in respect of all members who make a contribution at time

$t$

in respect of all members who make a contribution at time

$t$

. Then, the amount of contribution made at time

$t$

. Then, the amount of contribution made at time

$t$

, in respect of each individual of type

$t$

, in respect of each individual of type

$\xi$

, is

$\xi$

, is

\begin{equation} C^\xi _t = \alpha \, S^\xi _t \, \mathbf{1}^{C,\xi }_t. \end{equation}

\begin{equation} C^\xi _t = \alpha \, S^\xi _t \, \mathbf{1}^{C,\xi }_t. \end{equation}

It is assumed here that neither the contribution rate

$\alpha$

, nor the accrual rate

$\alpha$

, nor the accrual rate

$1/\beta$

, changes over time. In reality, both may change as a result of management decisions, but this is anticipated to happen infrequently.

$1/\beta$

, changes over time. In reality, both may change as a result of management decisions, but this is anticipated to happen infrequently.

The contribution rate

$\alpha$

is chosen so that the right-hand side of equation (6) is zero when the scheme has a stable population. This approach implies that there is collective financial fairness at the time of each contribution payment. However, there is no individual financial fairness at each time. The contribution

$\alpha$

is chosen so that the right-hand side of equation (6) is zero when the scheme has a stable population. This approach implies that there is collective financial fairness at the time of each contribution payment. However, there is no individual financial fairness at each time. The contribution

$C^\xi _t$

is, in general, not equal to the discounted value of the newly accrued benefit, which is seen by comparing (8) to (9). Moreover, the total contributions may not match the total additional discounted benefits. Consequently, new benefit accrual at time

$C^\xi _t$

is, in general, not equal to the discounted value of the newly accrued benefit, which is seen by comparing (8) to (9). Moreover, the total contributions may not match the total additional discounted benefits. Consequently, new benefit accrual at time

$t$

causes a sudden change in the scheme’s overall funding position, which can be calculated using (6). This movement away from a 100% funding position is only rectified at the next year’s valuation. The gain or loss due to the new contributions is then shared among all the scheme members through the pension increase factor. As a result, the level of indexation will typically vary from year to year, even if one assumes a constant economic model.

$t$

causes a sudden change in the scheme’s overall funding position, which can be calculated using (6). This movement away from a 100% funding position is only rectified at the next year’s valuation. The gain or loss due to the new contributions is then shared among all the scheme members through the pension increase factor. As a result, the level of indexation will typically vary from year to year, even if one assumes a constant economic model.

If we assume a deterministic model, then this gives rise to dynamical equations for

$h_t$

. Suppose we allow the number of types of individuals,

$h_t$

. Suppose we allow the number of types of individuals,

$M$

, and the time,

$M$

, and the time,

$t$

, to tend to infinity. Assume that the demographics of the fund and the economic factors all converge to long-term limits. In that event, we expect that

$t$

, to tend to infinity. Assume that the demographics of the fund and the economic factors all converge to long-term limits. In that event, we expect that

$h_t$

will also converge to a long-term limit

$h_t$

will also converge to a long-term limit

$h^\infty$

given by solving the equation

$h^\infty$

given by solving the equation

\begin{equation} \lim _{t\to \infty } \frac {\sum _{\xi =0}^{\infty } \frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h^\infty ) \, \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}} {\sum _{\xi =0}^{\infty } \alpha \, S^\xi _t \, \mathbf{1}^{C,\xi }_t} = 1. \end{equation}

\begin{equation} \lim _{t\to \infty } \frac {\sum _{\xi =0}^{\infty } \frac {1}{\beta } \, S^\xi _t \, \mathbf{1}^{C,\xi }_t \, \sum _{k=1}^\infty p^{\xi }_{t,k} \, \nu ^{\xi }_{t,k} \, I_{t,k}(h^\infty ) \, \, {\mathbf{1}}^{\xi , \mathrm{Ret}}_{t+k}} {\sum _{\xi =0}^{\infty } \alpha \, S^\xi _t \, \mathbf{1}^{C,\xi }_t} = 1. \end{equation}

The numerator in this equation is determined by equation (8) and represents the total discounted benefits at time

$t$

. The denominator is determined by equation (9) and represents the total contributions made at time

$t$

. The denominator is determined by equation (9) and represents the total contributions made at time

$t$

. If the demographics of the contributors to the scheme stabilize from some time

$t$

. If the demographics of the contributors to the scheme stabilize from some time

$\tau$

onwards, the fraction on the left-hand side will become constant for

$\tau$

onwards, the fraction on the left-hand side will become constant for

$t\geq \tau$

, so instead of the limit, one can simply work with values of

$t\geq \tau$

, so instead of the limit, one can simply work with values of

$t$

that are chosen to be sufficiently large. In the demographic model, we use in our simulations, one may take any

$t$

that are chosen to be sufficiently large. In the demographic model, we use in our simulations, one may take any

$t\geq 0$

.

$t\geq 0$

.

In a constant economic model, equation (10) can be used to determine the ratio between the contribution rate

$\alpha$

and the benefit accrual rate

$\alpha$

and the benefit accrual rate

$\frac {1}{\beta }$

, which gives a desired target level of indexation

$\frac {1}{\beta }$

, which gives a desired target level of indexation

$h^\infty =h^{\mathrm{target}}$

. More generally, in a stochastic, but stationary, economic model, one can compute median estimates for all terms and use equation (10) to roughly estimate the ratio of contributions to benefits that will achieve a target long-term median indexation. Conversely, however, one chooses the ratio of contributions and benefits, this will determine the long-term median indexation of the fund.

$h^\infty =h^{\mathrm{target}}$

. More generally, in a stochastic, but stationary, economic model, one can compute median estimates for all terms and use equation (10) to roughly estimate the ratio of contributions to benefits that will achieve a target long-term median indexation. Conversely, however, one chooses the ratio of contributions and benefits, this will determine the long-term median indexation of the fund.

In a flat-accrual scheme, the mismatch in a given year between a member’s discounted benefit and their contributions may be substantial. It is important to consider whether this is fair to members. In practice, the contribution calculated in equation (9) is really the sum of the member contribution and the sponsoring employer’s contribution made on behalf of a particular member (as is the case in (11), too). However, formally, the employer’s contribution is not allocated to any specific member, only to the fund as a whole. This enables money to be distributed unevenly across generations, which, as we discuss in detail later, is an essential feature of this type of “DB-lite” scheme.

If a member is in the scheme for their entire working life, one might imagine that lifetime benefits will match lifetime contributions. However, in general, this will not be the case. This is because the earliest generations receive disproportionately high benefits and later generations must, in effect, pay interest on the debt this creates. As a result, later generations receive less than they pay in, an effect we call drag. It is only in the long-term steady state that all scheme members are treated equally, and in this steady state, no member will receive as much benefit as they pay in. We quantify this effect in Theorem1 below.

The use of flat-accrual means that if a member leaves the scheme early, they can expect to have overpaid for the value of what they can transfer out of the scheme. This is considering the contributions paid by both member and employer. Similarly, it is not fair for existing members if someone close to retirement joins and their contributions are not sufficient to cover the value of their accrued benefits. This perception of unfairness may exist even if the employer’s contribution is not attributed to each individual member, but rather to the scheme as a whole. Existing members would suffer a decrease, albeit likely small, to make up for this individual deficit. Lastly, the calculation of the annual pension increases on accrued benefits can lead to significant changes in accrued pensions, depending on the scheme’s maturity and asset value. We discuss this further in Section 4.

2.3 Standard dynamic-accrual scheme design

The term dynamic-accrual is intended to suggest that accrual rates vary with market conditions. We define a standard dynamic-accrual CDC scheme to be one where the value of the new benefit accrued by a contribution matches the amount of that contribution.

A standard dynamic-accrual CDC scheme is intended as an alternative to a DC fund and could be well-suited to multiemployer schemes. In a multiemployer scheme, it is important to minimize intergenerational cross-subsidies as different employers may have different demographics of their workforce and would presumably not wish to provide an overall subsidy to another employer (see McInally (Reference McInally2023)).

In our studied dynamic-accrual scheme, the new benefit accrued at time

$t$

by the corresponding contribution

$t$

by the corresponding contribution

$C^\xi _t$

made at time

$C^\xi _t$

made at time

$t$

, is given by defining the price of a unit of nominal benefit by

$t$

, is given by defining the price of a unit of nominal benefit by

\begin{equation} \hat {V}^\xi _t \,:\!=\, \frac {1}{I_{t,0}(h_t)} \, \sum _{k=1}^\infty I_{t,k}(h_t) \, \nu ^\xi _{t,k} \, p^\xi _{t,k} \, {\mathbf{1}}^{R,\xi }_{t+k}, \end{equation}

\begin{equation} \hat {V}^\xi _t \,:\!=\, \frac {1}{I_{t,0}(h_t)} \, \sum _{k=1}^\infty I_{t,k}(h_t) \, \nu ^\xi _{t,k} \, p^\xi _{t,k} \, {\mathbf{1}}^{R,\xi }_{t+k}, \end{equation}

and then choosing

$B^{\xi }_t$

to solve

$B^{\xi }_t$

to solve

\begin{equation} C^\xi _t = B^{\xi }_t \hat {V}^{\xi }_t. \end{equation}

\begin{equation} C^\xi _t = B^{\xi }_t \hat {V}^{\xi }_t. \end{equation}

By equation (6), this ensures that

\begin{equation} A_t - \mathcal{L}_{t} = 0. \end{equation}

\begin{equation} A_t - \mathcal{L}_{t} = 0. \end{equation}

The basis used in (11) is the same as that used for the calculation of the pension increase awarded at time

$t$

. Assuming all interest rates are positive, the ratio of benefits to contributions will decrease with age, reflecting the time value of money.

$t$

. Assuming all interest rates are positive, the ratio of benefits to contributions will decrease with age, reflecting the time value of money.

Using the valuation basis to calculate the new accrued benefits means that there is no change in the scheme’s overall funding position due to new benefit accrual. Since the new contributions made at time

$t$

are equal to the value of the new accrued benefits, the right-hand side of (6) equals zero. Consequently, if the valuation basis is borne out in practice, then the asset value will automatically equal the discounted benefit value at the next and subsequent time periods, for the selection

$t$

are equal to the value of the new accrued benefits, the right-hand side of (6) equals zero. Consequently, if the valuation basis is borne out in practice, then the asset value will automatically equal the discounted benefit value at the next and subsequent time periods, for the selection

$(\mathsf{h}, \vartheta )\,:\!=\,(h_t,1)$

, i.e., equation (3) holds at the next time.

$(\mathsf{h}, \vartheta )\,:\!=\,(h_t,1)$

, i.e., equation (3) holds at the next time.

For the contributions paid into the scheme at time 0, an assumption is needed about the level of future pension increases in order to calculate the first benefits accrued. We assume that the real indexation rate is a constant,

$h^{\mathrm{target}}$

, at time 0 and hence set

$h^{\mathrm{target}}$

, at time 0 and hence set

$h_0 \,:\!=\, h^{\mathrm{target}}$

in (11). For contributions made at time

$h_0 \,:\!=\, h^{\mathrm{target}}$

in (11). For contributions made at time

$t=1,2,\ldots$

, the real indexation rate

$t=1,2,\ldots$

, the real indexation rate

$h_t$

calculated at time

$h_t$

calculated at time

$t_{-}$

is used in (11).

$t_{-}$

is used in (11).

We have seen that when designing a flat-accrual fund and in a mean-reverting economic model, it is possible to choose a target level of indexation

$h^{\mathrm{target}}$

and set the contribution and benefit accrual rates to ensure

$h^{\mathrm{target}}$

and set the contribution and benefit accrual rates to ensure

$h_t$

tends to revert to this level in the long term. There is no equivalent mechanism to set long-term indexation in a standard dynamic-accrual fund. Setting

$h_t$

tends to revert to this level in the long term. There is no equivalent mechanism to set long-term indexation in a standard dynamic-accrual fund. Setting

$h_0=h^{\mathrm{target}}$

will have a negligible influence on the values of

$h_0=h^{\mathrm{target}}$

will have a negligible influence on the values of

$h_t$

for large

$h_t$

for large

$t$

. Instead, if one wishes to target a long-term median level for

$t$

. Instead, if one wishes to target a long-term median level for

$h_t$

, one must choose the bounds on

$h_t$

, one must choose the bounds on

$h_t$

to limit its fluctuations and use benefit cuts and bonuses to constrain

$h_t$

to limit its fluctuations and use benefit cuts and bonuses to constrain

$h_t$

within reasonable limits. We will see a numerical example of this in Section 7.

$h_t$

within reasonable limits. We will see a numerical example of this in Section 7.

As nominal indexation rates, discount rates, and expectations of future lifetimes will vary over time, the amount of benefit calculated using (11) will also vary continuously for a fixed contribution amount. For occupational pension schemes in the UK, it is usual to have infrequently changing conversion factors for members. This is unlike life insurance companies, which may update their life annuity conversion rates daily. Although the trustees of a CDC pension scheme may prefer to have a rarely changing table of values for members, we do not explore the implications here, as we focus on dynamically changing benefit accrual only.

In a flat-accrual scheme,

$\nu ^\xi _{t,k}$

varies with

$\nu ^\xi _{t,k}$

varies with

$\xi$

and will ultimately be a function of a member’s age to give a lifestyle strategy (see Section 3.4). Some of the pension providers we spoke to were considering developing dynamic-accrual CDC funds where

$\xi$

and will ultimately be a function of a member’s age to give a lifestyle strategy (see Section 3.4). Some of the pension providers we spoke to were considering developing dynamic-accrual CDC funds where

$\nu$

depends upon

$\nu$

depends upon

$\xi$

in the same way. However, as all funds are pooled and subject to the same risks, if one allows

$\xi$

in the same way. However, as all funds are pooled and subject to the same risks, if one allows

$\nu$

to vary with

$\nu$

to vary with

$\xi$

, this will result in different generations being charged different amounts for the same future cashflows. This runs against the design goal of minimizing intergenerational cross-subsidies, as can be confirmed numerically using the techniques of Section 4, where we explore cross-subsidies in detail. To avoid this issue, we selected an overall strategy for the dynamic-accrual fund that was designed to reflect the cumulative effect of each generation’s lifestyle strategy and chose the discount rate

$\xi$

, this will result in different generations being charged different amounts for the same future cashflows. This runs against the design goal of minimizing intergenerational cross-subsidies, as can be confirmed numerically using the techniques of Section 4, where we explore cross-subsidies in detail. To avoid this issue, we selected an overall strategy for the dynamic-accrual fund that was designed to reflect the cumulative effect of each generation’s lifestyle strategy and chose the discount rate

$\nu ^\xi _{t,k}$

to match this overall strategy, and hence to be independent of

$\nu ^\xi _{t,k}$

to match this overall strategy, and hence to be independent of

$\xi$

. See Section 3.4.1.

$\xi$

. See Section 3.4.1.

3. Modeling details

3.1 Demographic assumptions

We will assume that the following modeling assumptions hold in all our simulations except where we explicitly state otherwise.

The earliest entry age to the scheme is age

$x_0 \,:\!=\, 25$

. An individual receives their first pension payment at age

$x_0 \,:\!=\, 25$

. An individual receives their first pension payment at age

$\mathsf{NRA} \,:\!=\, 65$

and pension payments are made annually in advance. Every individual is assumed to be dead at age

$\mathsf{NRA} \,:\!=\, 65$

and pension payments are made annually in advance. Every individual is assumed to be dead at age

$\omega \,:\!=\, 120$

, the limiting age. The fund is closed to new contributions after

$\omega \,:\!=\, 120$

, the limiting age. The fund is closed to new contributions after

$100$

years.

$100$

years.

In our simulations, the type

$\xi \in \{0,1,2,\ldots ,M-1\}$

represents the generation number of the individual. At time 0, there are

$\xi \in \{0,1,2,\ldots ,M-1\}$

represents the generation number of the individual. At time 0, there are

$\mathsf{NRA}-x_{0}+1 \leq M$

generations in the scheme, with generation

$\mathsf{NRA}-x_{0}+1 \leq M$

generations in the scheme, with generation

$\xi =0$

of age

$\xi =0$

of age

$\mathsf{NRA}-1$

, generation

$\mathsf{NRA}-1$

, generation

$\xi =1$

of age

$\xi =1$

of age

$\mathsf{NRA}-2$

, and so on, up to generation

$\mathsf{NRA}-2$

, and so on, up to generation

$\xi =\mathsf{NRA}-x_{0}+1$

who are age

$\xi =\mathsf{NRA}-x_{0}+1$

who are age

$x_0$

at time 0. At time 1, generation

$x_0$

at time 0. At time 1, generation

$\xi =\mathsf{NRA}-x_{0}+2$

joins the scheme at age

$\xi =\mathsf{NRA}-x_{0}+2$

joins the scheme at age

$x_0$

, and the new entrants continue to flow steadily into the scheme at each integer time. Thus, we have the following equations:

$x_0$

, and the new entrants continue to flow steadily into the scheme at each integer time. Thus, we have the following equations:

\begin{eqnarray} \mathsf{age}(\xi ,t) &\,:\!=\, \mathsf{NRA} - \xi + t - 1, \nonumber\\ \mathbf{1}^{R,\xi }_t &\,:\!=\, \mathbf{1}_{\mathsf{age} (\xi ,t) \geq \mathsf{NRA}}, \\ \mathbf{1}^{C,\xi }_t &\,:\!=\, \mathbf{1}_{\mathsf{age} (\xi ,t) \in [x_0,\mathsf{NRA})}.\nonumber \end{eqnarray}

\begin{eqnarray} \mathsf{age}(\xi ,t) &\,:\!=\, \mathsf{NRA} - \xi + t - 1, \nonumber\\ \mathbf{1}^{R,\xi }_t &\,:\!=\, \mathbf{1}_{\mathsf{age} (\xi ,t) \geq \mathsf{NRA}}, \\ \mathbf{1}^{C,\xi }_t &\,:\!=\, \mathbf{1}_{\mathsf{age} (\xi ,t) \in [x_0,\mathsf{NRA})}.\nonumber \end{eqnarray}

for

$\xi = 0,1,2,.\ldots , M-1$

.

$\xi = 0,1,2,.\ldots , M-1$

.

There is the same number of individuals in each generation when they join the scheme, so that the number of survivors satisfies

$N^0_0=N^1_0=\cdots =N^{\mathsf{NRA}-x_0+1}_0=N^{\mathsf{NRA}-x_0+2}_1=N^{\mathsf{NRA}-x_0+3}_2=\cdots$

. Additionally, before reaching age

$N^0_0=N^1_0=\cdots =N^{\mathsf{NRA}-x_0+1}_0=N^{\mathsf{NRA}-x_0+2}_1=N^{\mathsf{NRA}-x_0+3}_2=\cdots$

. Additionally, before reaching age

$\mathsf{NRA}$

, each individual in generation

$\mathsf{NRA}$

, each individual in generation

$\xi$

who makes a contribution at time

$\xi$

who makes a contribution at time

$t$

is paid the annual rate of salary

$t$

is paid the annual rate of salary

$S^{\xi }_t \,:\!=\, S_t$

at that time. Therefore, there are no promotional salary increases. Salaries increase annually at time

$S^{\xi }_t \,:\!=\, S_t$

at that time. Therefore, there are no promotional salary increases. Salaries increase annually at time

$t$

at the rate

$t$

at the rate

$g$

per annum, such that

$g$

per annum, such that

$S_t = S_0 (1+g)^t$

.

$S_t = S_0 (1+g)^t$

.

All scheme members survive to age

$\mathsf{NRA}$

. Thereafter, an individual who is alive at age

$\mathsf{NRA}$

. Thereafter, an individual who is alive at age

$x$

has the same probability of dying over the next year, regardless of their generation. In our simulations, the survival probabilities from age

$x$

has the same probability of dying over the next year, regardless of their generation. In our simulations, the survival probabilities from age

$\mathsf{NRA}$

are computed using the S1PMA tables produced by the Institute and Faculty of Actuaries’ Continuous Mortality Investigation.

$\mathsf{NRA}$

are computed using the S1PMA tables produced by the Institute and Faculty of Actuaries’ Continuous Mortality Investigation.

Let us write

$p(x,n)$

for the probability of an individual surviving

$p(x,n)$

for the probability of an individual surviving

$n \geq 0$

years from age

$n \geq 0$

years from age

$x$

, given that the individual is alive at age

$x$

, given that the individual is alive at age

$x$

. Then,

$x$

. Then,

\begin{equation} p^\xi _{t,n} \, =\!: \, p(\mathsf{age}(\xi ,t), n). \end{equation}

\begin{equation} p^\xi _{t,n} \, =\!: \, p(\mathsf{age}(\xi ,t), n). \end{equation}

We assume throughout that there are sufficient members so that individual longevity risk can be perfectly hedged at all ages. As a consequence, we use the proportion of survivors, rather than the number of survivors, in our calculations.

3.2 Economic assumptions

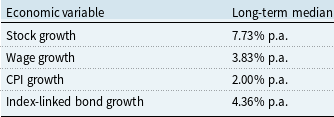

We use a number of economic models with varying levels of sophistication in this paper, but all the models share the same values for the long-term median of various risk factors, as shown in Table 1. Where applicable, values are chosen to match the figures of the UK Office for Budget Responsibility (2024). for September. The stock volatility in all stochastic models is

$15.3\%$

per annum to match the model of Alvares Maffra et al. (Reference Alvares Maffra, Armstrong and Pennanen2021).

$15.3\%$

per annum to match the model of Alvares Maffra et al. (Reference Alvares Maffra, Armstrong and Pennanen2021).

Long-term medians in our economic models

Table 1 Long description

A table comparing long-term medians of various economic variables. The table has two columns and four rows. The columns are labeled 'Economic variable' and 'Long-term median'. The rows are labeled with different economic variables and their corresponding long-term median values. Row 1: Stock growth, 7.73 percent per annum. Row 2: Wage growth, 3.83 percent per annum. Row 3: CPI growth, 2.00 percent per annum. Row 4: Index-linked bond growth, 4.36 percent per annum.

3.3 Scheme design assumptions

3.3.1 Bounds on the nominal indexation rate

For both CDC schemes, the real indexation rate at time

$t \in \mathbb{N}_0$

is constrained to lie in the range

$t \in \mathbb{N}_0$

is constrained to lie in the range

$h_{t} \in [-q_t, 0.05]$

, so that

$h_{t} \in [-q_t, 0.05]$

, so that

$h^{\mathrm{upper}}_t\,:\!=\,0.05$

. Any further adjustments to benefits required to equate the discounted benefits with the asset value are dealt with by changing the bonus level

$h^{\mathrm{upper}}_t\,:\!=\,0.05$

. Any further adjustments to benefits required to equate the discounted benefits with the asset value are dealt with by changing the bonus level

$\theta _t$

to a value other than one.

$\theta _t$

to a value other than one.

Consequently, real indexation rates granted on benefits are capped at

$5\%$

for both types of CDC fund, so nominal rates are capped at approximately

$5\%$

for both types of CDC fund, so nominal rates are capped at approximately

$q_t + 5\%$

. The floor for nominal rates is set at

$q_t + 5\%$

. The floor for nominal rates is set at

$0\%$

. Our industry consultation suggested that a benefit cap of

$0\%$

. Our industry consultation suggested that a benefit cap of

$q_t+2\%$

would be considered a more reasonable level for a standard dynamic-accrual scheme, but as we explain in more detail later, choosing the lower cap results in a decreasing median pension in retirement. The RMCPP does not have an upper bound on

$q_t+2\%$

would be considered a more reasonable level for a standard dynamic-accrual scheme, but as we explain in more detail later, choosing the lower cap results in a decreasing median pension in retirement. The RMCPP does not have an upper bound on

$h_t$

, but we have included one to aid comparison between the fund types.

$h_t$

, but we have included one to aid comparison between the fund types.

3.3.2 Benefit accrual rate

For the flat-accrual CDC scheme, the benefit accrual rate is set to

$1/\beta =1/80$

. This matches the value for the RMCPP. For the dynamic-accrual scheme, the benefit accrued depends on the amount of contribution and is determined using equation (11).

$1/\beta =1/80$

. This matches the value for the RMCPP. For the dynamic-accrual scheme, the benefit accrued depends on the amount of contribution and is determined using equation (11).

3.3.3 Setting the contribution rate

To aid comparability between scheme types, the same contribution rate

$\alpha$

is used for both the flat-accrual and dynamic-accrual CDC schemes.

$\alpha$

is used for both the flat-accrual and dynamic-accrual CDC schemes.

Within the flat-accrual CDC scheme,

$\alpha$

is computed as the rate required to deliver the desired benefits. To do this, it is assumed that the membership is a stable population and that, within the chosen economic model, the economic variables have attained their long-term medians, which are displayed in Table 1. We refer to these central estimates as steady-state rates.

$\alpha$

is computed as the rate required to deliver the desired benefits. To do this, it is assumed that the membership is a stable population and that, within the chosen economic model, the economic variables have attained their long-term medians, which are displayed in Table 1. We refer to these central estimates as steady-state rates.

We now assume the fund is targeting a long-term indexation rate

$h^\infty$

that matches the long-term CPI growth. Regulations require schemes to target at least CPI growth, and according to our industry consultation, schemes are expected to target this, as otherwise the cost of nominal benefits would be higher, potentially making the scheme appears less attractive. Using equation (10) for the resulting constant economic model, we may compute

$h^\infty$

that matches the long-term CPI growth. Regulations require schemes to target at least CPI growth, and according to our industry consultation, schemes are expected to target this, as otherwise the cost of nominal benefits would be higher, potentially making the scheme appears less attractive. Using equation (10) for the resulting constant economic model, we may compute

$\alpha$

. The resulting contribution rate is

$\alpha$

. The resulting contribution rate is

$\alpha =4.84\%$

. This is then used as the contribution rate for all the other fund types we simulate. Sensitivity testing shows that the contribution rate is most sensitive to the CPI and stock growth rate assumptions. For example, jointly increasing CPI by 1% per annum and lowering the stock growth rate by 1% per annum gives a contribution rate of just over 8%. Further lowering the stock growth rate by another 1% results in a contribution rate of around 11%.

$\alpha =4.84\%$

. This is then used as the contribution rate for all the other fund types we simulate. Sensitivity testing shows that the contribution rate is most sensitive to the CPI and stock growth rate assumptions. For example, jointly increasing CPI by 1% per annum and lowering the stock growth rate by 1% per annum gives a contribution rate of just over 8%. Further lowering the stock growth rate by another 1% results in a contribution rate of around 11%.

Since the argument used to derive the contribution rate assumes a deterministic model and does not take into account benefit cuts or bonuses, one cannot expect that a future nominal indexation rate of CPI is in any precise sense the “average” rate of increase that will occur in simulations.