1. Introduction

Asymmetric information between parties is a common issue in economic exchange (Arrow, Reference Arrow1969). Trust and reciprocity are therefore essential for initiating and maintaining economic interactions (Falk & Fischbacher, Reference Falk and Fischbacher2006; Fehr et al., Reference Fehr, Kirchsteiger and Riedl1993; Fehr et al., Reference Fehr, Kirchsteiger and Riedl1998; Sapienza & Zingales, Reference Sapienza and Zingales2011). Research in behavioral economics documents that many individuals exhibit trustworthy behavior in bilateral interactions, even if behavior is anonymous and interactions are one-off (see, e.g., Berg et al. (Reference Berg, Dickhaut and McCabe1995) for empirical evidence; see also Bolton and Ockenfels (Reference Bolton and Ockenfels2000) for theory and Johnson and Mislin (Reference Johnson and Mislin2011) for a meta-analysis). However, in many agency problems (Jensen & Meckling, Reference Jensen and Meckling1976), trust and trustworthiness are not limited to relationships between two parties. Instead, agents may interact with multiple principals simultaneously, and their actions may impact the income and utility of all involved parties (see, e.g., Iossa & Martimort, Reference Iossa and Martimort2012; Iossa & Martimort, Reference Iossa and Martimort2015; Khalil et al., Reference Khalil, Martimort and Parigi2007; Rud et al., Reference Rud, Rabanal and Horowitz2018; Voorn et al., Reference Voorn, van Genugten and van Thiel2019; Ward & Filatotchev, Reference Ward and Filatotchev2010).

A prime example of such a setting is crowdlending, where trust and reciprocity are crucial not only in bilateral principal-agent (PA) relationships but also in interactions involving multiple principals (MPA). In crowdlending – also known as peer-to-peer (P2P) lending – borrowers (agents) often receive funds from multiple lenders (principals) and must repay them collectively, since selective default on individual lenders is usually not possible. For instance, some borrowers may receive a $1,000 loan from a single lender, while others may receive the same amount from 100 different lenders. In both cases, borrowers face the same fundamental decision: whether to act trustworthily and repay the loan or to default and act in their monetary self-interest. However, the consequences of default differ: a single lender bears the full $1,000 loss, whereas in the case of 100 lenders, each lender loses only $10.

Despite the prevalence of MPA settings, little is known about how reciprocity is affected when multiple principals trust. Theories of outcome-based inequality aversion (Bolton & Ockenfels, Reference Bolton and Ockenfels2000; Fehr & Schmidt, Reference Fehr and Schmidt1999) suggest that reciprocity may weaken as the number of principals increases, since the impact of an agent’s opportunistic behavior becomes diluted – each principal bears only a small portion of the total loss.Footnote 1 Alternatively, behavior may differ when prosocial preferences are at play and individuals interact with multiple others, as highlighted in the literature on congestible altruism (Andreoni, Reference Andreoni2007; Schank, Reference Schank2021; Schumacher et al., Reference Schumacher, Kesternich, Kosfeld and Winter2017; Soyer & Hogarth, Reference Soyer and Hogarth2011) and studies of donation behavior toward multiple charitable recipients (Barneron et al., Reference Barneron, Choshen-Hillel and Yaniv2021; Eckel et al., Reference Eckel, Guney and Uler2020; Filiz-Ozbay & Uler, Reference Filiz-Ozbay and Uler2019; Schmitz, Reference Schmitz2021).Footnote 2 However, empirical evidence on reciprocity in MPA relationships is lacking.

In this paper, I provide evidence from laboratory and online experiments on differences in reciprocity between PA and MPA interactions. The experiments demonstrate that interactions where multiple principals trust one agent are considerably riskier than bilateral PA interactions. The experiments indicate that the lower marginal financial damage to principals appears to be a primary factor for reduced reciprocity in MPA interactions. The negative effect on reciprocity remains significant, however, even after controlling for the impact of untrustworthy agent behavior on principals’ payoffs. This suggests that agents are not only responding to payoff structures but also exhibit a broader insensitivity to the number of principals affected, making them less likely to fully internalize the consequences of untrustworthy behavior in MPA contexts. Treatments designed to appeal to agents’ trustworthiness, which explicitly highlighted the number of principals they would disappoint through untrustworthy behavior demonstrate the robustness of this effect. While reciprocity increased across all conditions, the effect was not disproportionately stronger in MPA interactions, even when the number of affected principals was made highly salient.

The experiments consisted of a series of modified one-shot investment (trust) games (Berg et al., Reference Berg, Dickhaut and McCabe1995), in which participants took on the roles of lenders (principals) or borrowers (agents) within either a bilateral principal-agent or a multi-principal-agent interaction. The games were framed in a credit market context, ensuring that all participants made decisions within a setting closely resembling real-world scenarios such as crowdlending. Principals decided whether to extend credit to a paired agent, while agents chose whether to repay or default in both the PA and MPA conditions. The loan amount, repayment obligation, and monetary incentives for reciprocating (repayment) or acting selfishly (default) were held constant across both interaction types. However, the consequences of the agent’s decisions for principals’ payoffs differed. In the bilateral PA interaction, each principal was the sole lender and bore the full risk of default. In the MPA interaction, five principals jointly provided credit. Each principal contributed one-fifth of the total loan and, since selective default was not possible, the principals shared the risk of default equally.

Trust game behavior is considered externally valid, as it aligns with repayment patterns observed in real-world credit markets, where reciprocity plays a critical role (Karlan, Reference Karlan2005). Moreover, extending the bilateral trust game to settings involving multiple principals closely mirrors real-world scenarios such as crowdlending. Nonetheless, it is challenging to determine whether behavioral differences between PA and MPA interactions stem from reduced monetary damage to each principal or from the dynamics of interacting with multiple principals. To address this issue, two sets of additional control treatments were conducted in further online experiments. The first set of control treatments equalized the relative monetary loss or the final payoffs for principals in case of agent default between the PA and MPA treatments. The second set of control treatments introduced trustworthiness appeals explicitly appealing to behave trustworthily and mentioning the number of trusting principals. This allows to identify whether differences in reciprocity between the PA and MPA interactions persist when marginal and relative monetary payoff consequences from untrustworthy agent behavior are comparable and when the consequences on the number of affected principals are very salient.

The results indicate that interactions involving multiple principals are significantly riskier than bilateral principal-agent (PA) interactions. When the consequences of credit default are shared among multiple principals, reciprocity – as measured by the percentage of credit repaid – declines notably: from an average of 62% in the PA treatments of the online experiments (63% in the laboratory) to 46% in the MPA treatments online (37% in the laboratory).

Importantly, this negative effect on reciprocity persists – even if somewhat reduced – in additional treatments that control for principals’ payoffs. When the relative monetary consequences of opportunistic behavior are held constant across PA and MPA interactions, reciprocity remains lower in the MPA treatment (54%). A similar decline is observed when absolute payoffs for principals are equalized (57% in the MPA treatment), and even in conditions where the number of principals is unspecified (56%).

Treatments that included trustworthiness appeals led to increased reciprocity across all conditions. However, consistent with the baseline findings, the effect was not significantly stronger in MPA interactions. This suggests that while differences in payoff structure are a key explanation for lower levels of trustworthy behavior in MPA settings, agents also appear less responsive to the impact of their actions on each individual principal when multiple principals are involved – even when the consequences of their behavior are made highly salient.

These findings contribute to the literature on reciprocity, which has primarily focused on bilateral interactions (see, e.g., Johnson & Mislin, Reference Johnson and Mislin2011) and tends to emphasize personal or relational contexts over market-based exchanges (see, e.g., Smith, Reference Smith2003, for discussion). Some exceptions exist, such as the network trust games studied by Cassar and Rigdon (Reference Cassar and Rigdon2011), which examine how trustworthiness responds to the total amount sent by principals.Footnote 3 The literature on MPA problems has primarily focused on theoretical models examining conflicts between principals with misaligned interests (Khalil et al., Reference Khalil, Martimort and Parigi2007; Voorn et al., Reference Voorn, van Genugten and van Thiel2019; Ward & Filatotchev, Reference Ward and Filatotchev2010) or strategic competition among agents (Rud et al., Reference Rud, Rabanal and Horowitz2018). Empirical work on how the number of principals affects reciprocal behavior is limited.

Models of outcome-based reciprocity (Bolton & Ockenfels, Reference Bolton and Ockenfels2000; Fehr & Schmidt, Reference Fehr and Schmidt1999) directly relate to principal-agent setups involving trust and reciprocity. These models predict behavior based on relative payoff differences but do not explicitly account for variations in the number of principals involved. To my knowledge, these models have not been empirically tested in MPA contexts.Footnote 4

This paper provides direct empirical evidence on reciprocity in bilateral versus multi-principal-agent settings, holding constant both principals’ intentions and the stakes involved. The findings support predictions from outcome-based reciprocity theory: when monetary harm to each individual principal is reduced – because it is distributed across multiple principals – reciprocal behavior declines.

The findings from the trustworthiness treatments complement the treatments varying the payoff consequences for the principals in two ways. First, they contribute to the literature on nudging and reminders (see, e.g., Benartzi et al., Reference Benartzi, Beshears, Milkman, Sunstein, Thaler, Shankar, Tucker-Ray, Congdon and Galing2017; Bursztyn et al., Reference Bursztyn, Fiorin, Gottlieb and Kanz2019; Karlan, Reference Karlan2005; Thaler & Sunstein, Reference Thaler and Sunstein2009). Reminding agents of others’ trust and appealing to make a repayment can be an effective tool to increase reciprocity in all treatments. Second, since the effect of the trustworthiness appeals was not more pronounced in the MPA treatments – where multiple principals were harmed by untrustworthy behavior – the results provide additional support for the initial finding: that agents’ insensitivity to the number of affected principals, combined with the lower marginal damage imposed on each, reduces reciprocity in MPA interactions.

These results also complement those of Alós-Ferrer et al. (Reference Alós-Ferrer, García-Segarra and Ritschel2022), who compare prosocial behavior toward individuals with antisocial behavior toward groups. However, their design varies both the behavioral domain (prosocial vs. antisocial) and the stakes involved (e.g., giving small vs. taking large amounts), making the findings not directly comparable to the reciprocity-based interactions studied here (see also Cappelen et al., Reference Cappelen, Nielsen, Sorensen, Tungodden and Tyran2013; Korenok et al., Reference Korenok, Millner and Razzolini2014; List, Reference List2007).

Finally, this paper also contributes to the broader literatures on altruism and decision-making involving multiple recipients. In particular, it connects to research on congestible altruism and charitable giving (Andreoni, Reference Andreoni2007; Eckel et al., Reference Eckel, Guney and Uler2020; Filiz-Ozbay & Uler, Reference Filiz-Ozbay and Uler2019; Schank, Reference Schank2021; Schmitz, Reference Schmitz2021; Schumacher et al., Reference Schumacher, Kesternich, Kosfeld and Winter2017; Soyer & Hogarth, Reference Soyer and Hogarth2011), which shows that generosity per recipient often declines as the number of recipients increases. It also resonates with findings from social psychology on the identifiable victim effect (see, e.g., Dickert et al., Reference Dickert, Västfjäll, Kleber and Slovic2012; Genevsky et al., Reference Genevsky, Västfjäll, Slovic and Knutson2013; Lee & Feeley, Reference Lee and Feeley2016), which suggest that people respond less emotionally when helping or harming groups rather than identifiable individuals (Barneron et al., Reference Barneron, Choshen-Hillel and Yaniv2021).

The findings are particularly relevant for understanding principal-agent relationships in environments where multiple principals interact with a single agent – most notably in the rapidly growing crowdlending and crowdfunding market (Berg et al., Reference Berg, Burg, Gombović and Puri2020; Deb et al., Reference Deb, Oery and Williams2024; De Roure et al., Reference De Roure, Pelizzon and Tasca2016; Di Maggio & Yao, Reference Di Maggio and Yao2021; Fuster et al., Reference Fuster, Plosser, Schnabl and Vickery2018; Käfer, Reference Käfer2018; Miglo, Reference Miglo2024; Strausz, Reference Strausz2017).Footnote 5

The remainder of the paper is organized as follows: Section 2 describes the experimental design. Section 3 presents the results. Section 4 concludes.

2. Experimental design and procedure

2.1. Experimental design

To study whether reciprocity is influenced by the number of trusting principals, the standard one-shot trust game (Berg et al., Reference Berg, Dickhaut and McCabe1995) was modified and framed as a credit market interaction. This ensured a consistent and relevant decision-making environment for all participants within a principal-agent context.

Participants were assigned the role of either principal or agent. Principals acted as lenders, offering credit, while agents (borrowers) decided whether to repay (reciprocate) or default (behave untrustworthily). The agent’s potential payoffs remained constant across conditions, while the number of principals varied. Agents either interacted with a single principal in the bilateral PA setup or with multiple (five) principals in the MPA setup.

To maintain consistency in the total credit amount – and thus the financial consequences for the agent – credit provided by multiple principals was divided equally among them in the MPA condition. However, this design necessarily altered the financial risk borne by each principal. It is not feasible to hold all factors constant (e.g., agent and principal payoffs and credit size) while varying only the number of principals.

For example, in the trust game, principals decide to provide a credit of  $x$ to the agent. The credit is multiplied by a factor

$x$ to the agent. The credit is multiplied by a factor  $m \gt 1$ and the agent decides whether to repay (a fixed amount) of

$m \gt 1$ and the agent decides whether to repay (a fixed amount) of  $\frac{mx}{2}$ or to default and keep the full amount

$\frac{mx}{2}$ or to default and keep the full amount  $mx$ (see Brown et al., Reference Brown, Schmitz and Zehnder2024, for a similar credit-market trust game with one agent and one principal). To keep the agent’s incentives constant across conditions, the total credit of

$mx$ (see Brown et al., Reference Brown, Schmitz and Zehnder2024, for a similar credit-market trust game with one agent and one principal). To keep the agent’s incentives constant across conditions, the total credit of  $x$ must remain the same in both the PA and MPA setups. In the PA, this credit is provided entirely by one principal. In the MPA, it is split equally among

$x$ must remain the same in both the PA and MPA setups. In the PA, this credit is provided entirely by one principal. In the MPA, it is split equally among  $n$ principals (five in this experiment), so that each principal provides

$n$ principals (five in this experiment), so that each principal provides  $\frac{x}{n}$. Accordingly, if the agent defaults, the financial loss for each principal is reduced to

$\frac{x}{n}$. Accordingly, if the agent defaults, the financial loss for each principal is reduced to  $\frac{x}{n}$.

$\frac{x}{n}$.

It is not possible to hold this loss constant across conditions without changing the agent’s incentives. For example, if each principal in the MPA were to risk losing  $x$ – as in the PA – the total credit extended to the agent would need to increase to

$x$ – as in the PA – the total credit extended to the agent would need to increase to  $nx$. This would raise the agent’s payoff from defaulting to

$nx$. This would raise the agent’s payoff from defaulting to  $nmx$, substantially increasing the benefits of untrustworthy behavior. Achieving comparability would then require increasing both the credit size and the principal’s endowment in the PA to

$nmx$, substantially increasing the benefits of untrustworthy behavior. Achieving comparability would then require increasing both the credit size and the principal’s endowment in the PA to  $nx$, which would again alter the strategic environment.

$nx$, which would again alter the strategic environment.

This trade-off highlights a key challenge: differences in reciprocity between PA and MPA conditions may reflect either the lower financial exposure of individual principals in the MPA, or the presence of multiple trusting principals. To disentangle these effects, additional MPA conditions were introduced. These either equalized the monetary impact of default on principals – in relative terms (MPA-ED) or absolute terms (MPA-EP) – or emphasized trustworthiness through explicit appeals (Trust treatments). These modifications aimed to isolate whether reciprocity is shaped more by financial exposure or by the interaction with multiple trusting parties.

Principals were assigned either to the PA or to one of the MPA conditions (between-subjects design). Agents made repayment decisions in both the PA and one MPA condition (within-subjects design), contingent on receiving credit. To minimize order effects, the sequence of repayment decisions was randomized.

All treatments were conducted online (on Prolific), with the bilateral principal-agent treatment (PA) and the main multiple-principals one agent treatment (MPA-MD) also run at the Decision Science Laboratory at ETH Zürich in Switzerland. Tables 1 and 2 provide an overview of treatments and associated payoffs for each environment. Full experimental instructions are available in Appendix D (laboratory experiment) and Appendix E (online experiment).

Treatment overview and parameters: laboratory experiment

Table 1 Long description

The table presents payoffs and participant numbers for agents and principals in a laboratory experiment under PA and MPA-MD conditions. Agents receive 7.5 CHF for repayment and 12.5 CHF for default in both conditions, with 134 agents participating in each. Principals earn 7.5 CHF for repayment and 2.5 CHF for default in PA, compared to 5.5 CHF for repayment and 4.5 CHF for default in MPA-MD. There are 66 principals in PA and 340 in MPA-MD, forming 66 PA groups and 68 MPA groups. Data was collected over 19 sessions, with variations in the MPA treatment across sessions.

Notes: Treatment overview in the laboratory experiment. Panel A: Agent payoffs and number of agents in the laboratory experiment. Panel B: Principal payoffs and number of principals in the laboratory experiment. N (# Agents): The number of agents per treatment. N (# Principals): The number of principals per treatment. N (# PA/MPA Groups): The number of PA and MPA groups formed out of the number of agents and principals. Sessions: The data was collected in 19 sessions (between session variation in the MPA treatment). Because agents made decisions in the PA and the MPA conditions, agent’s decisions were collected in all 19 sessions. In 15 sessions, principals were in the MPA condition and in four sessions principals were in the PA condition.

Treatment overview and parameters: online experiment

Table 2 Long description

The table compares agent and principal payoffs across various treatments in an online experiment, with and without trustworthiness appeals. Agent payoffs remain constant at 1.5 USD for repayment and 2.5 USD for default across all treatments. Principal payoffs differ significantly, with MPA-MD offering 1.1 USD for repayment and MPA-ED offering only 0.3 USD. The number of agents and principals varies by treatment, with the highest number of agents in PA and the highest number of principals in MPA-MD. The number of principal-agent groups formed also varies, with more groups in trustworthiness treatments. Sessions for data collection differ between agents and principals, indicating potential variation in behavior across sessions.

Notes: Treatment overview in the online experiment. Panel A: Agent payoffs and number of agents in the standard treatments without trustworthiness appeals. Panel B: Agent payoffs and number of agents in the treatments with trustworthiness appeals. Panel C: Principal payoffs and number of principals in all treatments. Principals were ex-post assigned to treatments with and without trustworthiness appeals. The decisions were similar for principals in both treatments. N (# Agents): The number of agents per treatment. N (# Principals): The number of principals per treatment. N (# PA/MPA Groups): describes how many PA and MPA groups formed out of the number of agents and principals. Principals were proportionally distributed between treatments with and without trustworthiness appeals. N (# PA/MPA): The number of principal-agent groups in the standard treatments. N (# PA/MPA Trust): The number of principal-agent groups in the trustworthiness treatments. Sessions (agents/principals): The data on agent behavior was collected in six online sessions/on six different dates (between session variation in the MPA treatments). Data on principals were collected in seven sessions/on seven different dates. Because agents made decisions in the PA and one of the MPA conditions, observations in PA were collected in all sessions. All payoffs are in USD.

2.1.1. Bilateral principal – agent treatment (PA)

The PA condition serves as the baseline in the experiment, closely mirroring the classical bilateral trust game commonly found in the literature. In this condition, a principal, acting as a lender, received an endowment of $1 in the online experiment (CHF 5 in the laboratory sessions) and had to decide whether to extend a fixed credit of $0.5 (CHF 2.5) to a paired agent in the role of a borrower. The credit was quadrupled, and agents were required to repay a fixed debt of $1 (CHF 5), equivalent to twice the credit size. The principal’s payoff was contingent on the decision to extend credit and the agent’s repayment choice. If the principal chose not to extend credit, they retained their endowment of $1 (CHF 5). If credit was extended, the principal would receive $1.50 (CHF 7.5) if the agent repaid (their endowment minus the credit plus repayment, i.e., $1-$0.5+$1=$1.5; CHF 5- CHF 2.5+CHF 5= CHF 7.5), and $0.5 (CHF 2.5) if the agent defaulted (their endowment minus the credit, i.e., $1-$0.5=$0.5; CHF 5 - CHF 2.5= CHF 2.5).

Agents received an endowment of $0.5 (CHF 2.5) and had to decide whether to reciprocate the principal’s trust by repaying the credit. If the agent chose to repay, their profit would be $1.5 (their endowment plus four times the credit minus the repayment of the fixed credit debt, i.e., $0.5+4 $\times$$0.5-$1=$1.5; CHF 2.5+4

$\times$$0.5-$1=$1.5; CHF 2.5+4 $\times$ CHF 2.5 - CHF 5= CHF 7.5). If the agent defaulted, their profit would be $2.5 (their endowment plus four times the credit, i.e., $0.5+4

$\times$ CHF 2.5 - CHF 5= CHF 7.5). If the agent defaulted, their profit would be $2.5 (their endowment plus four times the credit, i.e., $0.5+4 $\times$$0.5=$2.5; CHF 2.5+4

$\times$$0.5=$2.5; CHF 2.5+4 $\times$ CHF 2.5= CHF 12.5). If the principal chose not to extend credit, the agent retained their endowment. Both principals and agents were fully informed about the payoff consequences of each other’s decisions (in all experimental conditions).

$\times$ CHF 2.5= CHF 12.5). If the principal chose not to extend credit, the agent retained their endowment. Both principals and agents were fully informed about the payoff consequences of each other’s decisions (in all experimental conditions).

2.1.2. Multiple principals – agent treatments (MPA)

MPA – marginal damage (MPA-MD)

In the MPA-MD condition, the PA interaction is extended to a scenario where an agent engages with multiple principals. Specifically, the MPA-MD condition maintained identical credit sizes, benefits from credit, and endowments as in the PA interaction. Agents’ payoffs from repayment or default were therefore identical to the PA. However, unlike the PA condition, where a single principal provided the credit, in the MPA-MD condition, the decision to extend credit was made collectively by a group of five principals. Each principal contributed $0.10 (CHF 0.5), corresponding to one-fifth of the total credit size of $0.5 (CHF 2.5) to the credit given to the agent.Footnote 6 Consequently, credit was granted to the agent only if all five principals agreed to extend it. Agents thus faced the decision of whether to repay or default on the same credit size as in the PA condition but when provided by five principals. In the event of repayment, each principal therefore received $1.10 (the endowment minus the share of the credit plus the share of the repayment, i.e., $1-$0.1+$0.2=$1.1; CHF 5 - CHF 0.5+ CHF 1= CHF 5.5). Conversely, in the event of default, each principals marginal monetary damage was lower than in the PA condition, and a principal’s income was $0.90 (the endowment minus the share of the credit, i.e., $1-$0.1=$0.9; CHF 5 - CHF 0.5 = CHF 4.5). If credit was not extended, both principals and agents retained their endowments.

MPA – ambiguous number of principals (MPA-A)

In the MPA-A treatment, the setup for principals was identical to that in the MPA-MD treatment. Principals received the same endowment and five principals collectively decided on a total credit of $0.5. Agents, however, were only informed that they were interacting with multiple (more than one) principals who provided the credit, without knowing the exact number of principals involved. Consequently, agents had to make their repayment decisions without explicit knowledge of the number of trusting principals, although they were aware that more than one principal was involved. They were also informed that each principal had an endowment of $1 and that the credit was provided jointly by all principals.

MPA – equal proportional damage (MPA-ED)

In the MPA-ED condition, similar to the MPA-MD, principals had to jointly decide whether to trust and extend credit. The total credit amount (of  \$0.5) was the same as in the PA condition. However, each principal received only one-fifth of the endowment (i.e.,

\$0.5) was the same as in the PA condition. However, each principal received only one-fifth of the endowment (i.e.,  \$0.2), compared to the solo principal in the PA condition (who received

\$0.2), compared to the solo principal in the PA condition (who received  \$1). As a result, the individual credit contribution of each principal amounted to 50% of their endowment ($0.5 of $1 in the PA and $0.1 of $0.2 in the MPA-ED). The agents’ payoffs from defaulting or repaying were identical to those in the PA condition. However, the monetary loss (as a percentage of endowment) suffered by each principal due to untrustworthy agent behavior was similar to that in the PA condition. If agents defaulted, principals lost 50% of their endowment. In this case, each principal received a default payoff of $0.1. If the credit was repaid, a principal’s payoff was $0.3. In case of no credit, principals received their endowment.

\$1). As a result, the individual credit contribution of each principal amounted to 50% of their endowment ($0.5 of $1 in the PA and $0.1 of $0.2 in the MPA-ED). The agents’ payoffs from defaulting or repaying were identical to those in the PA condition. However, the monetary loss (as a percentage of endowment) suffered by each principal due to untrustworthy agent behavior was similar to that in the PA condition. If agents defaulted, principals lost 50% of their endowment. In this case, each principal received a default payoff of $0.1. If the credit was repaid, a principal’s payoff was $0.3. In case of no credit, principals received their endowment.

MPA – equal payoff (MPA-EP)

In the MPA-EP condition principals payoffs from agents’ default were identical to that in the PA interaction. Each of the five principals in the MPA interaction still contributed $0.1 to the total credit of $1 but received an endowment of $0.6. As a result, a principal’s payoff in the event of default was $0.5. In case of repayment, each principal’s payoff was $0.7. The agents’ payoffs from defaulting or repaying remained unchanged compared to the PA and the other MPA conditions.

2.1.3. Trustworthiness treatments (PA Trust, MPA-MD Trust, MPA-A Trust, and MPA-ED Trust)

The Trust treatments included “trustworthiness appeals” addressed at the agents. Specifically, when making repayment decisions, agents were explicitly reminded to behave trustworthily and, in addition, the number of principals who had trusted them and provided credit was highlighted. Agents received the following message, which varied depending on the number of principals (one in the PA Trust, five in the MPA-MD/MPA-ED Trust, or multiple in the MPA-A Trust) who provided the credit: “Remember, your decision affects one/five/multiple lender(s) who extended credit and trusted in you to repay the total credit debt. Act trustworthily and don’t let the one/five/multiple lender(s) down by making the repayment!” All other parameters were kept constant between the PA Trust, MPA-MD Trust, and MPA-A Trust treatments and the respective treatments without such appeals (PA, MPA-MD, MPA-A, and MPA-ED). For principals, there was no difference between the treatments with and without trustworthiness appeal.

2.2. Discussion of the experimental design and predictions

To test whether reciprocity differs between bilateral principal-agent (PA) and multiple-principal-agent (MPA) interactions, several experimental treatments were implemented. These treatments aimed to isolate whether differences in reciprocity are driven by the reduced monetary loss that agents impose on principals in MPA settings, or by a potential insensitivity to the number of principals involved.

The PA condition serves as the baseline. Comparing the PA to the MPA-MD treatment allows us to examine whether agents reciprocate differently when receiving credit from a single principal versus multiple principals. This setup reflects common real-world scenarios, particularly in crowdlending, where borrowers often receive funds from multiple lenders.

Outcome-based models of reciprocity (Bolton & Ockenfels, Reference Bolton and Ockenfels2000; Fehr & Schmidt, Reference Fehr and Schmidt1999),Footnote 7 as well as research on congestible altruism (Andreoni, Reference Andreoni2007) suggest that reciprocity should decline in the MPA-MD condition relative to the PA. The MPA-A treatment, in which agents are not informed of the exact number of principals, complements the MPA-MD treatment and serves as a robustness check. It explores whether reciprocity is undermined when agents are uncertain about how many principals have extended trust – a situation that mirrors real-world crowdlending, where borrowers may not know the exact number of lenders.

In the MPA-A treatment, agents were told that multiple principals provided credit, but the exact number remains ambiguous. Since the perceived monetary damage from default decreases as the number of principals increases, reciprocity is expected to decline with agents’ beliefs about the number of principals involved. This leads to the first prediction:

Prediction 1 (Reciprocity in the PA, MPA-MD and MPA-A). Compared to the PA condition, reciprocity is reduced in both the MPA-MD and MPA-A conditions.

In both the MPA-MD and the MPA-A conditions, the financial ramifications for principals may affect reciprocity. Given the challenge of fully equalizing payoff consequences between the PA and MPA conditions, treatments were designed to equalize principals’ default payoffs. In the MPA-ED treatment, the marginal loss to principals from agent defaults was equalized across conditions: principals lost 50% of their endowment in case of default ($0.5 of $1 in PA, and $0.1 of $0.2 in MPA-ED). In the MPA-EP treatment, final default payoffs were made identical ($0.5 in both PA and MPA). Only focusing on default payoffs, Fehr and Schmidt (Reference Fehr and Schmidt1999) or Bolton and Ockenfels (Reference Bolton and Ockenfels2000) suggest that reciprocity may vary between PA and MPA treatments. Reciprocity is expected to be lower in the MPA-MD treatment, higher in the MPA-ED condition, and similar between PA and MPA-EP treatment (see Appendix C for further details). Prediction 2 follows:

Prediction 2 (Reciprocity in the PA compared with the MPA-ED and MPA-EP). If reciprocity is driven solely by the monetary damage inflicted on principals, it should be similar in PA and MPA-EP, and higher in MPA-ED. However, if the number of principals also negatively affects reciprocity, then reciprocity will be higher in PA than in both MPA-ED and MPA-EP.

The treatment variations thus far have focused on equalizing principals’ payoffs from agent defaults between the PA and the MPA conditions. The trustworthiness treatments were introduced to examine potential difference between the PA and MPA conditions from a different perspective and highlighted the number of trusting principals while keeping payoffs and procedures consistent with the PA, MPA-MD, MPA-A, and MPA-ED treatments.Footnote 8

Emphasizing the number of affected principals may enhance the psychological salience of the consequences of default. Consequently, if individuals struggle to relate the consequences of their actions to multiple people compared to a single individual (see, e.g., Andreoni, Reference Andreoni2007; Barneron et al., Reference Barneron, Choshen-Hillel and Yaniv2021), making the number of affected principals salient may lead to higher reciprocity in the MPA compared with the PA. An alternative way to describe this is that without the trustworthiness appeals, agents may not realize how many people trusted them and that defaulting would actually hurt multiple principals. Making this relationship salient in the trustworthiness treatments may therefore increase the psychological cost of default and highlight that this behavior betrays the trust of multiple others. Any differences between the PA and MPA observed in the treatments without trustworthiness appeals may then be explained by a lack of salience of the actions.

By contrast, if reciprocity is mostly driven by relative payoff differences between principals in the PA and MPA conditions, agents might focus on the relatively small harm imposed on each individual principal. In this case, salience should not matter. It is even possible that if reciprocity is only driven by marginal payoff harm, then salience could weaken the moral weight of default and potentially widen the reciprocity gap, especially in the MPA-MD and MPA-A conditions, where the financial damage to each principal is also relatively smaller in the MPA compared with the PA condition. This effect should be limited in the MPA-ED condition, where relative payoff consequences between PA and MPA-ED are aligned.

Additionally, the trustworthiness treatments appealed directly to agents’ sense of responsibility. Thus, while the trustworthiness appeals should increase reciprocity overall (see, e.g., Benartzi et al., Reference Benartzi, Beshears, Milkman, Sunstein, Thaler, Shankar, Tucker-Ray, Congdon and Galing2017; Bursztyn et al., Reference Bursztyn, Fiorin, Gottlieb and Kanz2019; Karlan, Reference Karlan2005; Thaler & Sunstein, Reference Thaler and Sunstein2009, for literature on the efficacy nudging in other domains), the relative size of the effects between the PA and MPA conditions is ex-ante ambiguous. Comparing differential effects between the PA and MPA treatments with and without trust allows to identify whether differences may be predominantly driven by a lack of salience about the number of affected principals or whether differences may be driven by the lower monetary damage imposed on principals. Prediction 3 summarizes the possible effects.

Prediction 3 (Reciprocity in the PA Trust compared with the MPA-MD Trust, MPA-A Trust, and MPA-ED Trust treatments). Trustworthiness appeals increase reciprocity across all treatments. If reciprocity is mainly driven by lower financial consequences in MPA, the increase will be stronger in PA Trust than in MPA Trust. If agents are simply unaware of the number of affected principals, the increase will be larger in the MPA Trust treatments, where this number is made salient.

2.3. Experimental procedure

The study was conducted using both online and laboratory experiments. This was done because running the experiment in both settings can be considered a replication (List & Rasul, Reference List, Rasul, Ashenfelter and Card2011) allowing to cross-validate findings. Besides the general importance of replications in economics (see, e.g., Berry et al., Reference Berry, Coffman, Hanley, Gihleb and Wilson2017), adding additional evidence from a different population increases the reliability and validity of the findings.Footnote 9 Budget limitations required prioritizing the robustness checks for the main experimental conditions (PA and MPA-MD) across both settings.

The online experiment was programmed in Qualtrics and recruited residents of the US through Prolific. This experiment included all treatment conditions and was conducted between August and November 2019. The sample size was designed to meet or exceed those used in prior studies on trust and trustworthiness using crowdworking platforms such as MTurk or Prolific (Chan & Wolk, Reference Chan and Wolk2023; Chen et al., Reference Chen, Foster and Putterman2019; Evans & Krueger, Reference Evans and Krueger2014; Klingbeil et al., Reference Klingbeil, Grützner and Schreck2024).Footnote 10

A total of 4438 participants (1113 agents and 3325 principals) took part in the online experiments, with an average age of 34 years and 54.5% of participants identifying as female.Footnote 11 Data on agent behavior was collected across six sessions (on six different dates), with between-session variation in the MPA treatments. Data on principal behavior was collected across seven sessions (on seven different dates). Because agents made decisions in both the PA and one MPA condition, observations for the PA condition were collected in all sessions.Footnote 12

The majority of participants reported an average household income between $48’001 and $60’000. Among the subjects figuring as agents, 70% were currently indebted at the time of the study, while 83% had been in debt previously, which included study loans, credit card debt, debt from family and friends, bank credits, or mortgage debt.

The main conditions of the experiment, the PA and the MPA-MD treatments were also conducted in the laboratory. The laboratory experiment was programmed in zTree (Fischbacher, Reference Fischbacher2007) and carried out at the Decision Science Laboratory of the ETH Zürich in September 2019, with 18 to 36 participants taking part in 19 sessions. A total of 540 participants (134 agents and 406 principals) were recruited, with an average age of 23 years and 61% identifying as female. Of the agents, 20% were currently in debt, while 42% had experienced debt in the past, including study loans, credit card debt, and debt from family and friends.

These figures suggest that both subject pools were well-suited for studying reciprocity in a PA and MPA setup framed as a credit market.

Participants in both the online and laboratory experiments made independent decisions as either agents or principals. Those assigned as agents made decisions contingent on receiving credit from either one principal or five/multiple principals (strategy method). The literature presents mixed findings on the influence of the strategy method on behavior (see Brandts & Charness, Reference Brandts and Charness2011, for a review), with some studies reporting no systematic differences (Fong et al., Reference Fong, Huang and Offerman2007; Reuben & Suetens, Reference Reuben and Suetens2008; Solnick, Reference Solnick2007), while others, such as Meidinger et al. (Reference Meidinger, Robin and Ruffieux2001), suggest that direct response elicitation may lead to lower levels of reciprocity. It is thus possible that reciprocity could be lower if a direct response method were used. However, in this experiment, the strategy method was applied uniformly across all treatments. Therefore, there is no reason to expect this would influence comparisons between treatments.

To mitigate any potential order effects arising from within-subjects design and the sequence of decisions – whether agents faced repayment decisions after receiving credit from one or multiple principals – both the order of decisions and the order in which these scenarios were introduced were randomized. Specifically, it was randomly determined whether agents first encountered the scenario of receiving credit from one or five/multiple principals.

After making their decisions, participants provided socio-demographic information such as age and gender. The experiments took approximately 10-15 minutes to complete. Following the experiment, decisions were implemented.

In the laboratory, grouping and matching of principals with agents was done within zTree. In the online experiment, this was done ex-post. In the PA, random principal-agent pairs were created and subsequently, decisions were implemented. In the MPA conditions, principals were first grouped with four other principals. Each group of five principals was then randomly matched with one agent. Subsequently, decisions were implemented, and payments were administered.

Payoffs were adjusted for the laboratory or online setting (see Table 1 for the laboratory experiment and Table 2 for the online experiment). In the laboratory payoffs were denoted in points. Principals were endowed with CHF 5 (approximately $5.50), while agents received an endowment of CHF 2.5, and the credit was CHF 2.5. All participants received a show-up fee of CHF 5. In the online experiment, all participants received a fixed income of $1 for participating. In addition, agents received an endowment of $0.5 and credit of $0.5, while principals in the PA condition received an endowment of $1. The endowment for principals in the MPA conditions varied depending on the treatment, as detailed in Section 2.1.

3. Results

3.1. Behavior of agents and reciprocity

Figure 1 presents the experimental results on reciprocity. Panel A shows data from the laboratory experiments, while Panel B displays results from the online experiment (without trustworthiness treatments). Reciprocity is measured as the average rate at which agents repaid the credit in the PA and MPA treatments.

Number of principals and reciprocity: laboratory experiment and online experiment (treatments without trustworthiness appeals)

Fig. 1 Long description

Panel A shows a bar graph comparing reciprocity rates in a laboratory experiment. The x-axis lists treatments PA and MPA-MD, while the y-axis shows reciprocity in percent. PA has a reciprocity rate of 63.43 percent and MPA-MD has 37.31 percent. Panel B displays a bar graph for an online experiment without trustworthiness appeals. The x-axis lists treatments PA, MPA-MD, MPA-A, MPA-ED and MPA-EP. The y-axis shows reciprocity in percent. PA has a rate of 61.65 percent, MPA-MD is 45.57 percent, MPA-A is 55.84 percent, MPA-ED is 53.94 percent and MPA-EP is 56.74 percent.

The figure demonstrates that reciprocity is significantly lower when agents’ opportunistic behavior imposes a smaller marginal cost on each principal in the MPA-MD treatment compared to the PA treatment. In the laboratory, 63.43% of agents reciprocated and repaid in the PA treatment, while only 37.31% did so in the MPA-MD treatment.

The online experiment replicates this result: 61.65% of agents repaid in the PA treatment compared to 45.57% in the MPA-MD treatment.Footnote 13 The results remain robust even when agents were unaware of the exact number of principals involved in the MPA-A treatment, with a reciprocity rate of 55.84%. Figure A.5 and Table A.12 (Appendix A.3) demonstrate that the negative effect on reciprocity in the MPA-A treatment correlates with agents’ beliefs about the number of principals providing credit. Reciprocity declines from 60% when agents believe 2-4 principals provided credit to 51.7% when they think that 5-9 principals were involved. Reciprocity is still lower at 54.2% when agents believe more than 10 principals provided credit, compared to when they believe 2-4 principals were involved. However, the difference is not statistically significant, and few agents held this belief. Result 1 emerges.

Result 1 (Reciprocity in the PA, MPA-MD and MPA-A). Reciprocity is significantly lower in the MP-A-MD and the MPA-A treatments, where agents’ opportunistic behavior imposes less monetary harm on each principal compared to the PA treatment.

The results from the online experiments (Panel B of Fig. 1) indicate that the negative effect on reciprocity persists across the MPA treatments, even when agents’ selfish behavior affects principals’ payoffs equally in percentage terms and when principals’ default payoffs are equalized between the PA and MPA conditions. Although the negative effect on reciprocity is reduced in the MPA-ED treatment (53.94%) and the MPA-EP treatment (56.74%) compared to the MPA-MD treatment, reciprocity remains substantially and significantly lower in both treatments relative to the PA treatment. This finding is summarized in Result 2.

Result 2 (Reciprocity in the PA compared with the MPA-ED and MPA-EP). Compared to the PA treatment, reciprocity remains significantly lower in the MPA-ED and MPA-EP treatments, even when agents’ selfish behavior affects principals’ payoffs equally in percentage or absolute terms.

Table 3 provides statistical evidence supporting the findings. The table presents regression results from linear probability models, with cluster-robust standard errors (in parentheses). The dependent variable is the binary decision to repay. The MPA treatment is the main explanatory variable, and standard errors are clustered at the individual agent level. The PA treatment in the respective PA and MPA conditions acts as the benchmark, i.e., because of the within-subjects design agents made two decisions in each MPA treatment (one for the PA and one for the respective MPA treatment, e.g., in the MPA-MD they decided upon repayment in the PA and the MPA-MD) only the PA decision from the respective MPA treatment is considered in the regression. Column (1) reports the differences between the PA and MPA-MD treatments in the laboratory. Columns (2)–(5) present results from the online experiments: Column (2) shows the comparison between the PA and MPA-MD treatments; Column (3) presents results for the PA and MPA-A treatments; Column (4) compares the PA and MPA-ED treatments, and Column (5) reports the regression results for the PA and MPA-EP treatments. The results confirm a significant decline in reciprocity across all MPA treatments, with the strongest effect in MPA-MD.

Treatment effects – linear probability models

Table 3 Long description

The table measures the impact of different treatments on the likelihood of reciprocation when credit is provided by multiple principals. In the lab experiment, the PA vs. MPA-MD treatment shows a significant negative effect of -0.261 on reciprocation, with a robust standard error of 0.0449. Online experiments show varying negative effects: MPA-MD (-0.101), MPA-A (-0.0909), MPA-ED (-0.0848), and MPA-EP (-0.0709), all significant at different levels. Constants range from 0.557 to 0.649, indicating baseline reciprocation rates. Observations and clusters vary across experiments, affecting the robustness of results. The F-statistics and R-squared values suggest varying model fit, with the lab experiment showing the strongest explanatory power.

Notes: Results from linear probability regressions with cluster robust standard errors in parentheses. Standard errors clustered at the individual agent level.

*  $p \lt 0.1$, **

$p \lt 0.1$, **  $p \lt 0.05$, ***

$p \lt 0.05$, ***  $p \lt 0.01$. The dependent variable in all regressions is the binary decision to reciprocate in case of receiving a credit. The main explanatory variable is the situation in which credit is provided by five/multiple principals. Column (1) shows differences between the PA and the MPA-MD in the laboratory. Column (2)–(5) presents results for the online experiments. Column (2) shows differences between the PA and the MPA-MD treatment. Column (3) presents results for the PA and the MPA-A treatment. Column (4) shows regressions for the PA and the MPA-ED treatment, and Column (5) displays regression results in the PA and MPA-EP treatment. MPA represents the multiple principals treatment (MPA-MD, MPA-A, MPA-ED, MPA-EP).

$p \lt 0.01$. The dependent variable in all regressions is the binary decision to reciprocate in case of receiving a credit. The main explanatory variable is the situation in which credit is provided by five/multiple principals. Column (1) shows differences between the PA and the MPA-MD in the laboratory. Column (2)–(5) presents results for the online experiments. Column (2) shows differences between the PA and the MPA-MD treatment. Column (3) presents results for the PA and the MPA-A treatment. Column (4) shows regressions for the PA and the MPA-ED treatment, and Column (5) displays regression results in the PA and MPA-EP treatment. MPA represents the multiple principals treatment (MPA-MD, MPA-A, MPA-ED, MPA-EP).

Importantly, Appendix A.1 (for the laboratory results) and Appendix A.2 (for the online experiments) show that these results are robust to session timing, demographic controls, order effects, and alternative model specifications (e.g., probit). In addition, agents’ beliefs about the likelihood of receiving credit were similar across treatments (53.79% in PA and 53% in MPA), suggesting that differences in reciprocity are not driven by expectations of credit allocation.Footnote 14

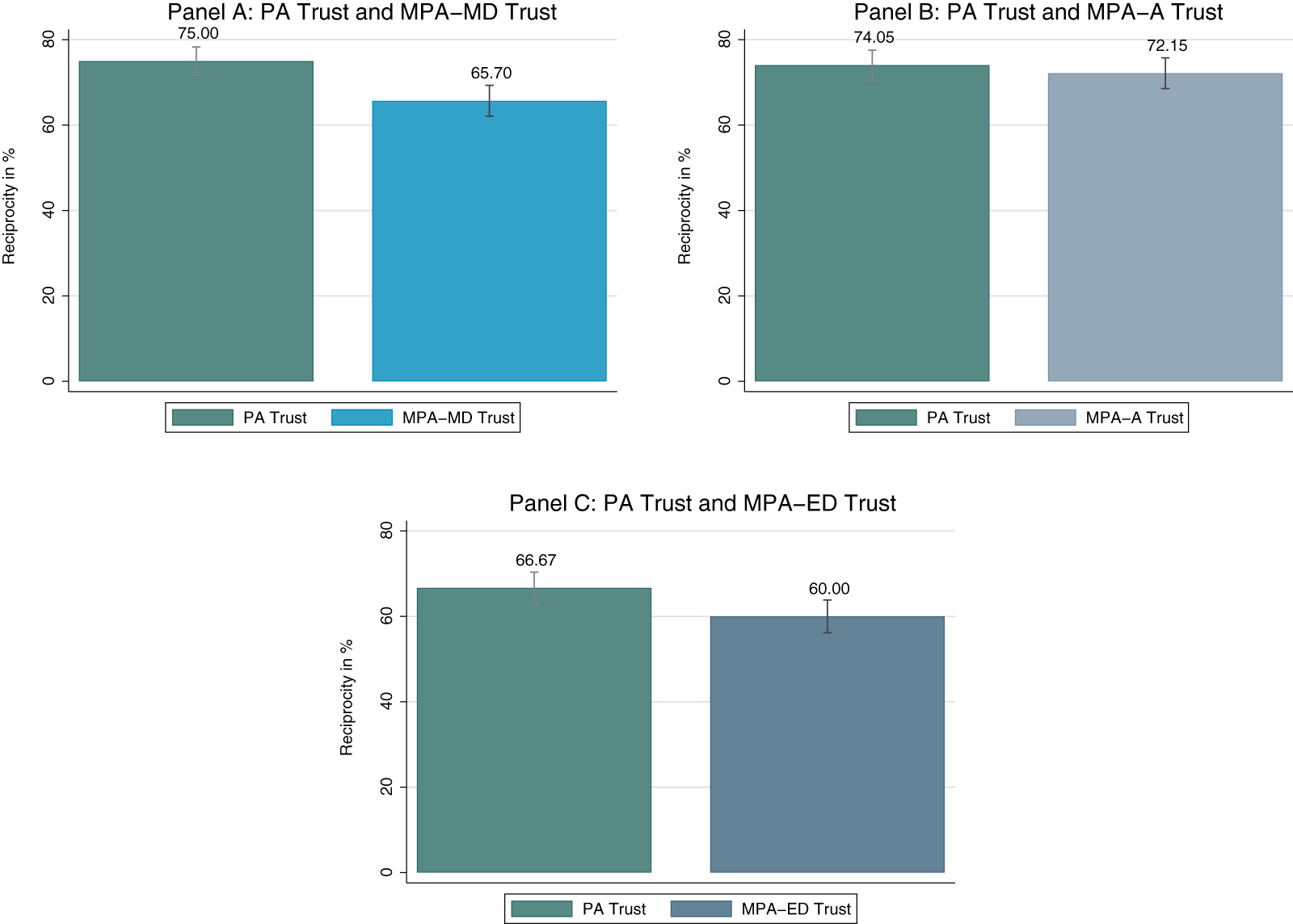

Figure. 2 shows the effects of the treatments including trustworthiness appeals. These appeals increased reciprocity across all treatments. However, the increase was not significantly greater in the MPA treatments.

Online experiment: trustworthiness treatments

Fig. 2 Long description

Panel A shows two bars representing PA Trust and MPA-MD Trust. The PA Trust bar reaches 75.00 percent, while the MPA-MD Trust bar is at 65.70 percent. Panel B displays PA Trust and MPA-A Trust, with PA Trust at 74.05 percent and MPA-A Trust at 72.15 percent. Panel C illustrates PA Trust and MPA-ED Trust, with PA Trust at 66.67 percent and MPA-ED Trust at 60.00 percent. Each panel includes error bars and labels for clarity. The x-axis is labeled with treatment types and the y-axis is labeled 'Reciprocity in percent'.

Moreover, reinforcing the results from the treatments without trustworthiness appeals, correlational evidence linking beliefs about the number of principals providing credit to reciprocity shows that the tendency to reciprocate declines as agents perceive more principals to be involved. Specifically, the reciprocity rate drops from 76.8% when agents believe 2–4 principals provided credit, to 72.9% when they think 5–9 principals provided credit, and to 60% when they believe more than ten principals trusted them (see Figure A.8 in Appendix A.4).

Table 4 provides statistical evidence for the effects of the trustworthiness treatments. Columns (1)–(3) present results from between-treatment comparisons: Column (1) compares PA Trust with MPA-MD Trust, Column (2) compares PA Trust with MPA-A Trust, and Column (3) compares PA Trust with MPA-ED Trust. These regressions use linear probability models with cluster-robust standard errors (clustered at the individual agent level), and the decision to reciprocate serves as the dependent variable. In these regressions, the PA Trust treatment is the benchmark condition. Columns (4)–(6) present difference-in-differences regressions (with cluster-robust standard errors at the individual agent level), comparing the PA and PA Trust treatments with the MPA-MD/A/ED and MPA-MD/A/ED Trust treatments. Again, the decision to reciprocate is the dependent variable, with the PA treatment as the benchmark. The results indicate that the trustworthiness treatments reduce the difference in reciprocity between the PA Trust and the MPA-A Trust and MPA-ED Trust treatments. However, while the effect of the trustworthiness treatments is positive, the differential effect is not statistically significant. This indicates that while making the number of affected principals salient increases reciprocity, the results from the treatments without trustworthiness appeals remain robust. Further robustness checks for these results are presented in Appendix A.4. Result 3 summarizes the key findings from the trust treatments.

Result 3 (Reciprocity in the PA Trust compared with the MPA-MD Trust, MPA-A Trust and MPA-ED Trust treatments). Trustworthiness appeals increase reciprocity in all treatments. The effect of the trustworthiness appeals on reciprocity is not significantly different between the PA and MPA treatments.

Trust treatments: linear probability models

Table 4 Long description

The table analyzes the impact of trust treatments on reciprocity using linear probability models. It compares PA Trust with various MPA Trust treatments and examines difference-in-difference effects. MPA treatments generally show negative effects on reciprocity, notably MPA-MD Trust at -0.0930** and MPA-ED Trust at -0.0667. Trust significantly increases reciprocity in difference-in-difference models, with coefficients of 0.193*** for MPA-MD and 0.0912* for MPA-A. The interaction term MPA × Trust shows minor effects, indicating limited differential impact of trust treatments across MPA conditions. Constants are consistently high, suggesting a strong baseline probability of reciprocity. Observations and clusters vary across models, affecting the robustness of findings.

Notes: Results from linear probability regressions with cluster robust standard errors in parentheses (clustered at the individual agent level).

*  $p \lt 0.1$, **

$p \lt 0.1$, **  $p \lt 0.05$, ***

$p \lt 0.05$, ***  $p \lt 0.01$. The dependent variable in all regressions is the binary decision to reciprocate in case of receiving a credit. The main explanatory variable is the situation in which credit is provided by five/multiple principals. Column (1) shows differences between the PA Trust and the MPA-MD Trust treatment. Column (2) presents results between the PA Trust and the MPA-A Trust treatment. Column (3) presents results between the PA Trust and the MPA-ED Trust treatment. Column (4)–(6) present results from difference-in-difference regressions between the PA, the PA Trust and the respective MPA and MPA Trust treatments. MPA represents condition with multiple principals in the treatments without trust appeal (MPA-MD/MPA-A/MPA-ED). Trust captures the effect of the trustworthiness treatments on reciprocity. MPA

$p \lt 0.01$. The dependent variable in all regressions is the binary decision to reciprocate in case of receiving a credit. The main explanatory variable is the situation in which credit is provided by five/multiple principals. Column (1) shows differences between the PA Trust and the MPA-MD Trust treatment. Column (2) presents results between the PA Trust and the MPA-A Trust treatment. Column (3) presents results between the PA Trust and the MPA-ED Trust treatment. Column (4)–(6) present results from difference-in-difference regressions between the PA, the PA Trust and the respective MPA and MPA Trust treatments. MPA represents condition with multiple principals in the treatments without trust appeal (MPA-MD/MPA-A/MPA-ED). Trust captures the effect of the trustworthiness treatments on reciprocity. MPA  $\times$ Trust captures the differential effect of trustworthiness treatments on reciprocity in the MPA treatments (MPA-MD Trust/MPA-A Trust/MPA-ED Trust).

$\times$ Trust captures the differential effect of trustworthiness treatments on reciprocity in the MPA treatments (MPA-MD Trust/MPA-A Trust/MPA-ED Trust).

3.2. Behavior of principals and trust

Although the primary focus of this paper is on how the number of principals affects agents’ reciprocity, it is also informative to examine whether principals anticipate that agents are less likely to reciprocate when multiple principals are involved.

Figure. 3 illustrates principals’ behavior in the laboratory experiment. Panel A shows the individual likelihood of extending credit (intended credit), while Panel B displays the actual rate at which credit was realized (realized credit). In the PA treatment, each principal’s decision directly determined whether credit was extended. In contrast, in the MPA-MD treatment, credit was only extended if all five principals agreed to lend.

Intended and realized credit in the laboratory experiment

Fig. 3 Long description

Panel A shows a bar graph with the x-axis labeled 'Intended credit in percent' and the y-axis labeled 'Intended credit in percent'. Two bars represent P-A and MPA-MD treatments, with values 83.3 and 82.6 respectively. Panel B shows a bar graph with the x-axis labeled 'Realized credit in percent' and the y-axis labeled 'Realized credit in percent'. Two bars represent P-A and MPA-MD treatments, with values 83.3 and 10.3 respectively.

The data show that while the individual likelihood of trusting was similar in both treatments (83.3% in PA vs. 82.6% in MPA-MD), the realized credit rate was significantly lower in the MPA-MD treatment (10.3%) due to the unanimity requirement.

Figure 4 presents similar results from the online experiment. Panel A shows the intended credit rates across all treatments, and Panel B shows the realized credit rates (pooled for treatments with and without trust appeals). Principals’ willingness to trust was comparable across treatments: 77.5% in PA, 79.4% in MPA-MD, 79.9% in MPA-A, 83.2% in MPA-ED, and 85.6% in MPA-EP. However, realized credit rates were substantially lower in the MPA treatments, ranging from 28.5% in MPA-MD to 45.6% in MPA-EP.

Intended and realized credit online experiments

Fig. 4 Long description

Panel A displays a bar graph of intended credit rates for five treatments: PA at 77.5, MPA-MD at 79.4, MPA-A at 79.9, MPA-ED at 83.0 and MPA-EP at 85.3. The x-axis lists the treatments and the y-axis shows intended credit rates from 0 to 100. Panel B shows a bar graph of realized credit rates for the same treatments: PA at 77.5, MPA-MD at 30.9, MPA-A at 35.5, MPA-ED at 40.0 and MPA-EP at 48.5. The x-axis lists the treatments and the y-axis shows realized credit rates from 0 to 100.

Table 5 provides statistical evidence supporting the findings illustrated in the figures. The table is structured similarly to the regressions in Table 3, but here, the dependent variables are the decision to provide credit (Panel A) and the likelihood of credit being realized (Panel B). The MPA treatments serve as the primary explanatory variables, with the PA treatment in the corresponding PA and MPA conditions used as the benchmark. Since the trustworthiness appeal and no trustworthiness appeal treatments were identical for principals, these were pooled.

Principal’s behavior – linear probability models

Table 5 Long description

The table compares the effects of multiple principal agent (MPA) treatments on credit decisions in lab and online experiments. Panel A indicates that the MPA treatment generally increases the likelihood of intended credit provision in online settings, with coefficients ranging from 0.0153 to 0.0606. Panel B reveals a significant negative impact of MPA treatments on realized credit, with coefficients between -0.309 and -0.730, all statistically significant at the 0.01 level. The constant values in both panels are consistently high and significant, suggesting a strong baseline probability of credit provision and realization. Observations and clusters are consistent across both panels, ensuring robust standard errors. The R-squared values indicate a better fit for realized credit models compared to intended credit models, especially in the lab experiment.

Notes: Results from linear probability regressions with cluster robust standard errors in parentheses. Standard errors clustered at the individual agent level.

*  $p \lt 0.1$, **

$p \lt 0.1$, **  $p \lt 0.05$, ***

$p \lt 0.05$, ***  $p \lt 0.01$. Panel A: Dependent variable in all regressions is the binary decision to provide credit. The main explanatory variable is the MPA treatment. Panel B: Dependent variable in all regressions is the binary realization of credit. The main explanatory variable is the MPA treatment. Column (1) shows differences between the PA and the MPA-MD in the laboratory. Column (2)–(5) presents results for the online experiments. Column (2) shows differences between the PA and the MPA-MD treatment. Column (3) presents results for the PA and the MPA-A treatment. Column (4) shows regressions for the PA and the MPA-ED treatment, and Column (5) displays regression results in the PA and MPA-EP treatment. MPA represents the multiple principals treatment (MPA-MD, MPA-A, MPA-ED, MPA-EP).

$p \lt 0.01$. Panel A: Dependent variable in all regressions is the binary decision to provide credit. The main explanatory variable is the MPA treatment. Panel B: Dependent variable in all regressions is the binary realization of credit. The main explanatory variable is the MPA treatment. Column (1) shows differences between the PA and the MPA-MD in the laboratory. Column (2)–(5) presents results for the online experiments. Column (2) shows differences between the PA and the MPA-MD treatment. Column (3) presents results for the PA and the MPA-A treatment. Column (4) shows regressions for the PA and the MPA-ED treatment, and Column (5) displays regression results in the PA and MPA-EP treatment. MPA represents the multiple principals treatment (MPA-MD, MPA-A, MPA-ED, MPA-EP).

These results suggest that principals do not fully anticipate the increased behavioral risk associated with MPA interactions. Despite lower reciprocity rates in MPA settings, principals’ trust levels remain high. This is further supported by incentivized belief elicitation: 50.08% of principals in the PA treatment believed that agents would repay, compared to 52.5% in the MPA treatments – a statistically significant difference (two-sided t-test: N = 3325; p = 0.051).

The lower realized credit rates in MPA treatments are primarily due to the coordination requirement among multiple principals. Even if individual trust levels are high, the probability of unanimous agreement decreases with group size, leading to fewer loans being extended.Footnote 15

Robustness checks for the results presented in Table 5 are available in Appendix B.Footnote 16

4. Discussion and conclusion

Trust and trustworthiness are fundamental for initiating and sustaining economic interactions. While agency problems often involve multiple principals interacting with a single agent – such as in crowdlending or gig work – most existing research on trust and reciprocity focuses on bilateral relationships (see, e.g., Johnson & Mislin, Reference Johnson and Mislin2011, for a review).

This paper takes a first step toward empirically comparing reciprocity in bilateral principal-agent (PA) versus multi-principal-agent (MPA) interactions using a stylized experimental design. Consistent with theories of outcome-based inequality aversion (Bolton & Ockenfels, Reference Bolton and Ockenfels2000; Fehr & Schmidt, Reference Fehr and Schmidt1999), the results show that the marginal damage imposed on each principal plays a significant role in agents’ repayment decisions. When multiple principals extend trust, each individual principal suffers less from selfish behavior, which reduces the agent’s incentive to reciprocate.

This effect persists even in treatments that control for the financial consequences of untrustworthy behavior on principals’ payoffs. Treatments that appealed to agents’ trustworthiness and made the number of affected principals salient increased reciprocity across all conditions. However, the increase was not more pronounced in the MPA treatments. This suggests that even when the consequences of default are made explicit, agents remain relatively insensitive to the number of principals affected and are less likely to reciprocate in MPA settings.

As a result, interactions in which multiple principals trust a single agent appear to be considerably riskier from a behavioral perspective than bilateral interactions. In the experiment, principals could only choose whether or not to extend credit, holding intentions constant across PA and MPA conditions. This design supports an interpretation based on outcome-based inequality aversion, which can largely explain the observed behavioral differences.

Nevertheless, in the MPA treatments, each principal’s individual credit contribution was smaller in absolute terms than in the PA condition. If agents interpret these smaller amounts as weaker signals of trust, intention-based reciprocity theories (see, e.g., Charness & Rabin, Reference Charness and Rabin2002; Dufwenberg & Kirchsteiger, Reference Dufwenberg and Kirchsteiger2004; Rabin, Reference Rabin1993; Toussaert, Reference Toussaert2017; Von Siemens, Reference Von Siemens2013) may also offer an alternative explanation.

The findings have implications for the design of incomplete contracts. Principals should recognize that MPA interactions carry a higher risk of untrustworthy agent behavior and adjust their expectations and strategies accordingly. These insights are also relevant for policymakers regulating technologies that facilitate MPA interactions – such as crowdlending platforms.

This paper provides the first empirical evidence on reciprocity in anonymous, one-shot PA versus MPA interactions. While many real-world MPA relationships are repeated and non-anonymous (e.g., employment), this study isolates the behavioral risks associated with MPA structures in a controlled setting. Future research could explore how factors such as reputation, enforcement mechanisms, or misaligned incentives among principals affect reciprocity in MPA contexts. Additionally, experiments with exogenously assigned credit (see Cox, Reference Cox2004) could further test the role of intention-based reciprocity in MPA interactions.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/eec.2025.10039.

Acknowledgements

I thank Rob Bauer, Philipp Doerrenberg, Manuel Grieder, Steve Heinke, Peiran Jiao, Deborah Kistler, Anita Kopányi-Peuker, Thomas Niederkofler, Paul Smeets, Utz Weitzel, and Yilong Xu for their input. I am grateful to Franziska Issler for excellent research assistance and Renate Schubert for her support during the research process. I further thank seminar participants in Basel, Nijmegen, and Maastricht, as well as participants at the 2021 Experimental Finance Conference and the 2021 ESA Global Conference, for valuable input. Financial support from the ETH Zürich is acknowledged (grant number: SEED-05 18-2). The replication material for the experiments is available at https://doi.org/10.34973/rdc4-tz38.

Open access

Open access