Introduction

Local government amalgamations are a globe-spanning reform megatrend (Blom-Hansen et al. Reference Blom-Hansen, Houlberg, Serritzlew and Treisman2016; Gendźwiłł et al. Reference Gendźwiłł, Kurniewicz and Swianiewicz2021; Askim, Gendźwiłł, and Klausen Reference Askim, Gendźwiłł and Klausen2025); they radically change the political, organizational, and economic landscape of the jurisdictions involved. One major change, which occurs in the interim period between when a merger has been decided and its implementation, is that the economic incentive structure of local governments becomes disrupted. A common-pool problem arises, i.e. a situation where the costs of an activity that benefits a small group are shared among a larger group (Ostrom Reference Ostrom1990). The common-pool resource created by a merger is the financial capacity of the merged entity, control of which is turned over to the new entity’s leaders before the merger is implemented. This incentivizes the old units to, for example, take up loans and increase their spending beyond what they would normally do – so-called freeriding or pre-merger overspending. The benefits derived from the increased spending, improvements in infrastructure for example, will accrue to the present political leadership’s constituency, while the costs of repaying loans and refilling coffers will (soon) be borne by the merged constituency (Hinnerich Reference Hinnerich2009; Blom-Hansen Reference Blom-Hansen2010).

The occurrence of pre-merger overspending is in fact the most consistently well-documented economic effect of local government amalgamations (Gendźwiłł et al. Reference Gendźwiłł, Kurniewicz and Swianiewicz2021; Tavares Reference Tavares2018). A significant body of research has provided compelling evidence of the extent of pre-merger overspending, how it is financed and used, how overspending varies during the reform period, and how it varies across classes of municipalities. However, rather than adding to these sorts of insights, the objective of this article is to investigate how pre-merger overspending can be prevented, by studying the effectiveness of reform-specific national regulations on pre-merger overspending in local government amalgamation reforms.

Given that national governments understand the tendency for pre-merger overspending to occur, it is not unexpected that amalgamation reforms are sometimes accompanied by loan- and spending restrictions and other regulations temporarily restricting the fiscal autonomy of local governments. What is perhaps more surprising is that these regulations are not more stringent and widespread, and, most notably, that national governments often choose not to implement any reform-specific fiscal regulations, giving free rein to the incentive to overspend.

Existing scholarship has struggled to provide a satisfactory answer regarding the effects of reform-specific regulations in preventing pre-merger overspending. The reason for this gap in the literature is to a large extent the absence of a control group, or, put differently, the lack of a proper basis for comparing regulation and non-regulation scenarios.

Making causal inferences about the impact of regulation is challenging (Capano et al. Reference Capano, Pritoni and Vicentini2020; Coglianese Reference Coglianese2012; Heinzel et al. Reference Heinzel, Reinsberg and Zaccaria2024). This study uses a Difference-in-Difference-in-Difference design (DDD) that allows us to quantitatively estimate the difference in pre-merger overspending in soon-to-merge municipalities in a non-regulation scenario (Norway) and a scenario with multiple reform-specific regulations (Denmark). No other comparative quantitative study of pre-merger overspending of this kind currently exists. The study utilizes the fact that Denmark and Norway, two countries with strikingly similar characteristics, adopted contrasting approaches to regulating pre-merger overspending in amalgamation reforms during the 2000s and 2010s. In the period leading up to the implementation of mergers in 2007, the Danish government introduced several measures that temporarily restricted local fiscal autonomy, including requiring ministerial approval for loans, mandatory saving and a tax freeze (Blom-Hansen Reference Blom-Hansen2010). Conversely, the Norwegian government chose to not implement any reform-specific regulations. Instead, it expressed the trust and hope that the municipalities would act responsibly and not follow the incentive to overspend prior to merging (Klausen et al. Reference Klausen, Askim and Christensen2021; Ministry of Local Government and Modernization 2014, 137–8).

Based on a comparison of these two cases, the article asks how divergence in reform-specific regulation of municipal fiscal behavior affects the level and form of pre-merger overspending. In each case, we compare fiscal policies among merging and non-merging municipalities before and after enactment of the reform (difference-in-difference) and subsequently estimate the difference in pre-merger overspending in the two countries (difference-in-difference-in-difference). The study thus contributes with new knowledge about the effects of regulation of opportunistic fiscal behavior in the context of mergers of local governments. The results show that pre-merger overspending in the soon-to-merge municipalities was significantly higher in the non-regulation scenario (Norway) than in the regulation scenario (Denmark), regarding current expenditure and capital investment.

The article is structured as follows. The next section presents the theoretical and methodological problem of regulating pre-merger overspending. We then outline the research context and design before presenting the results. The final section discusses theoretical and practical insights emerging from the study, including the case for not implementing effective regulations of opportunistic fiscal behavior.

The problem of regulating pre-merger overspending

As already stated, a significant body of research has provided compelling evidence of the extent of pre-merger overspending, how it is financed and used, how overspending varies during the reform period, and how it varies across classes of municipalities. For instance, municipalities finance last-minute spending sprees on both current- and capital expenditure by taking out loans, using savings and running down the operating balance (Askim et al. Reference Askim, Houlberg and Klausen2023). Furthermore, although overspending can begin several years earlier if local decision-makers anticipate future mergers, pre-merger overspending tends to peak in the year immediately before mergers are implemented (Hansen Reference Hansen2019). Additionally, certain municipalities are more prone to overspending than others: smaller municipalities, for example, have more to gain from overspending than larger ones (Hinnerich Reference Hinnerich2009; Hirota and Yunoue Reference Hirota and Yunoue2017; Nakazawa Reference Nakazawa2016; Saarimaa and Tukiainen Reference Saarimaa and Tukiainen2015).

In contrast to real-life reformers and common pool research in the tradition of Elinor Ostrom (Reference Ostrom1990), local government scholars have devoted limited attention to understanding how pre-merger overspending can be curtailed. Exceptions include Nakazawa’s (Reference Nakazawa2016) study of the effect of permanent debt accumulation regulations, Blom-Hansen’s (Reference Blom-Hansen2010) study of temporal limitations of local fiscal autonomy (see also Hansen Reference Hansen2014, Reference Hansen2019), and Askim and Houlberg’s (Reference Askim and Houlberg2023) and Askim et al.’s (Reference Askim, Gendźwiłł and Klausen2025) studies of the effect of informal institutions.

The fact that pre-merger overspending is perceived as a common pool problem means that preventing it is not likely to be a major preoccupation for individual local governments, for whom freeriding on the merged entity’s resources is simply rational behavior. As the costs can be shared with others, overspending by a soon-to-be-merged municipality allows the citizens within its jurisdiction to benefit “on the cheap” from enduring improvements, such as high-quality infrastructure and recreational facilities. The “tragedy” is in the aggregate, with new, amalgamated units struggling to develop a solid organization if they inherit depleted coffers and significant debts. Furthermore, the limited scope to enhance cost- and allocative efficiency is not only a challenge for amalgamated local units, but also a concern for the national government, which is often the initiator of amalgamation reforms.

With leaders of soon-to-merge municipalities incentivized to overspend on popular goods for their current citizenry, potential overspending may materialize in increased spending on current- and/or capital expenditure. Allocation of more resources for either current- and/or capital expenditure may thus be regarded as the most direct measurement of extraordinary pre-merger spending. Whether leaders of the old units choose to finance overspending by taking on debts, using savings or running down operating surpluses can be considered a secondary consequence of the incentive to overspend prior to the merger (Askim et al. Reference Askim, Houlberg and Klausen2023).

As already stated, national governments are typically aware of the incentive for pre-merger overspending, and therefore sometimes, but far from always, ensure that amalgamation reforms are accompanied by regulations that temporarily restrict local fiscal autonomy (Askim et al. Reference Askim, Houlberg and Klausen2023). Such regulations may be directed directly towards allocation of resources for current- and/or capital expenditure or may be directed towards the sources of finance for overspending in the form of restrictions on accruing debts, using savings, or running down operating surpluses. However, there are numerous examples of reforms that were not accompanied by temporary regulations aimed at preventing pre-merger overspending, including reforms implemented in Sweden in 1952 (Jordahl and Liang Reference Jordahl and Liang2010) and 1974 (Hinnerich Reference Hinnerich2009), Finland in 2008 (Saarimaa and Tukiainen Reference Saarimaa and Tukiainen2015), Japan in 2005 (Nakazawa Reference Nakazawa2016; Hirota and Yunoue Reference Hirota and Yunoue2017), and Norway in 2020 (Askim et al. Reference Askim, Houlberg and Klausen2023). To our knowledge, the only case of an amalgamation reform that was accompanied by a targeted limitation of local fiscal autonomy, and where pre-merger overspending has been analyzed in existing research, is Denmark’s reform implemented in 2007 (Blom-Hansen Reference Blom-Hansen2010; Hansen Reference Hansen2014, Reference Hansen2019). Other with-regulation examples from the same region are Denmark’s local government reform of the 1970s and Norway’s county government reform of the early 2000s.

But do these anti-freeriding regulations work, and if so, how effective are they? Wall-to-wall regulation of municipal fiscal policymaking is impractical, and local authorities have ways to circumvent and find loopholes in the regulations that the upper echelons of government decide to implement. Moreover, the absence of regulations does not imply that local authorities completely empty their coffers before merging; informal conventions also play their part (Askim and Houlberg Reference Askim and Houlberg2023, Askim, Houlberg and Serritzlew Reference Askim, Houlberg and Serritzlew2025).

The challenge in evaluating the performance of rules and regulations is a general one. It is not only in relation to the prevention of municipalities from fiscally exploiting amalgamations that studies of regulation tend to be limited to a single country and not have a control group. Moreover, policymakers are generally hesitant to adopt an experimental approach to regulation (Greenstone, Reference Greenstone, Moss and Cisternino2009). Implementing a new set of rules solely for a subset of the target population, whether individuals, businesses, or local governments, can invite criticism of unequal treatment. Regulatory experimentation is consequently usually limited to hypothetical scenarios. As presented in the next section, our aim is to fill that gap, based on a Difference-in-Difference-in-Difference design in relation to the cases of Denmark and Norway.

Overall, a lower level of pre-merger overspending can be expected in a regulation scenario than in a non-regulation scenario. In addition to testing this expectation, we estimate how effective pre-merger regulation is and examine if pre-merger overspending materializes as extra spending of current expenditure and/or capital investment.

Amalgamations will often involve merging smaller with larger units. There is strong support in the literature for the proposition that the smaller units have the strongest incentive to overspend before merging (e.g., Hinnerich Reference Hinnerich2009, Hirota and Yunoue Reference Hirota and Yunoue2017, Saarimaa and Tukiainen Reference Saarimaa and Tukiainen2015). This illustrates that ex-ante knowledge about the composition of their respective enlarged units can influence the initial units’ fiscal policy. Anti-overspending regulations should affect senior and junior amalgamation partners equally, though. Our expectation is therefore that the effect of regulation is the same irrespective of a unit’s size relative to its amalgamation partners.

As indicated above, based on theory and existing research, municipalities undergoing a merger within a regulatory framework cannot be expected to fully avoid pre-merger overspending. Nor can it be expected that municipalities merging within a non-regulatory framework uniformly run their operating balance down, empty their coffers and accrue maximum loans to fund a last-minute spending spree. It has been established that despite the national regulations to prevent pre-merger overspending, merging municipalities in Denmark did find ways to overspend prior to merging (Blom-Hansen Reference Blom-Hansen2010; Hansen Reference Hansen2014, Reference Hansen2019), and similarly, that merging municipalities in Norway displayed considerable divergence in pre-merger overspending despite the absence of anti-freeriding regulations (Askim et al. Reference Askim, Houlberg and Klausen2023). Possible explanations for municipalities overspending despite regulations include gaps in the regulationsFootnote 1 and a cost-benefit calculus suggesting that the benefits of overspending are greater than the penalties incurred for breaching the regulations. Possible explanations for municipalities choosing not to overspend despite the absence of regulations include fiscal responsibility, neighborliness, and other informal norms, municipalities voluntarily obeying government encouragements, and merging partners keeping each other in check (Askim et al. Reference Askim, Houlberg and Klausen2023, Askim and Houlberg Reference Askim and Houlberg2023; Klausen et al. Reference Klausen, Askim and Christensen2021).

While this study is designed to answer whether anti-freeriding regulation works and how effective it is, policymakers would surely also like to know which specific regulations that are most effective. For example, are regulations that limit the purposes to which resources can be allocated (e.g., external vetting procedures for capital investment projects) more or less effective than regulations that limit the availability of resources? And more specific yet, which is the most effective way to limit the availability of freeriding resources – a debt ceiling or a tax freeze? Unfortunately, our research context does not involve the regulatory experimentation necessary to answer these more detailed questions. As described next, the Danish municipalities were subjected to a uniform set of temporary fiscal regulations prior to merging, and the Norwegian ones uniformly to none.

Research context

The context for the research is the two Nordic countries of Denmark and Norway, with Norway representing a non-regulation merger scenario and Denmark representing a regulation scenario. The two countries have similar political-institutional systems and have long been recognized as good cases for comparative cross-country studies under a most similar systems design (Blom-Hansen et al. Reference Blom-Hansen, Christiansen, Fimreite and Selle2012; Vabo et al. Reference Vabo, Fimreite and Houlberg2023). Denmark and Norway are unitary, parliamentary, multi-party states with relatively similar welfare systems. Both countries have a three-tier government system with elected bodies at all levels: municipality, county/region, and state. The two countries represent the Nordic type of local government system, involving a high level of decentralization via multi-purpose entities that enjoy significant levels of local autonomy. Municipalities in both countries are responsible for a wide range of politically and economically important welfare services and are entitled to a high level of autonomy in securing financing and allocating resources (Ladner et al. Reference Ladner, Keuffer and Baldersheim2016). In both countries, the most important sources of financing are local taxes and central government grants. Municipalities in both countries can also obtain loans to finance capital expenditure and, if liquid assets are available, the locality can use them to finance activities. Accounting systems- and practices are also similar, which allows us to calculate the same outcome indicators for spending and financing in the two countries (see section on Design, methods, and data).

Both Denmark and Norway have implemented major amalgamation reforms since the turn of the century in order to establish larger and more sustainable municipalities (Vabo et al. Reference Vabo, Fimreite and Houlberg2023). The reform in Denmark was implemented in 2007, reducing the number of municipalities from 271 to 98. Norway’s reform was completed in January 2020, resulting in a reduction from 428 to 356 municipalities. Different reform tools were used, with Denmark’s reform more top down than Norway’s, which was largely voluntary. The Danish reform partners set up a minimum size requirement of 20,000 inhabitants and gave the municipalities six months (the latter half of 2004) to decide with whom to merge, and explicitly stated that if municipalities were not able to meet the minimum size requirement of 20,000 inhabitants, the reform partners in Parliament would decide on the amalgamation. In Norway, the reform partners gave the municipalities two years to discuss whether to merge without setting any size requirement, simply signaling a latent threat of enforced mergers (Vabo et al. Reference Vabo, Fimreite and Houlberg2023). Although the reduction in the number of municipalities was markedly higher in Denmark than in Norway, both reforms shared the same feature of amalgamating some municipalities and leaving others untouched. In other words, the reforms in both countries represent quasi-experiments that make it possible to compare the pre-treatment development in a “treatment group” of merging municipalities with a “control group” of municipalities that were not facing merger (Blom-Hansen et al. Reference Blom-Hansen, Houlberg, Serritzlew and Treisman2016).

What is most important for the purpose of this study is that the national governments in the two countries chose two very different strategies to regulate pre-merger overspending in the years leading up to the actual mergers. Prior to the amalgamations in Denmark in 2007, the national government implemented several regulations to prevent pre-merger overspending, whereas the national government in Norway chose not to implement any regulations in relation to municipal expenditure and finances ahead of the reform in 2020.

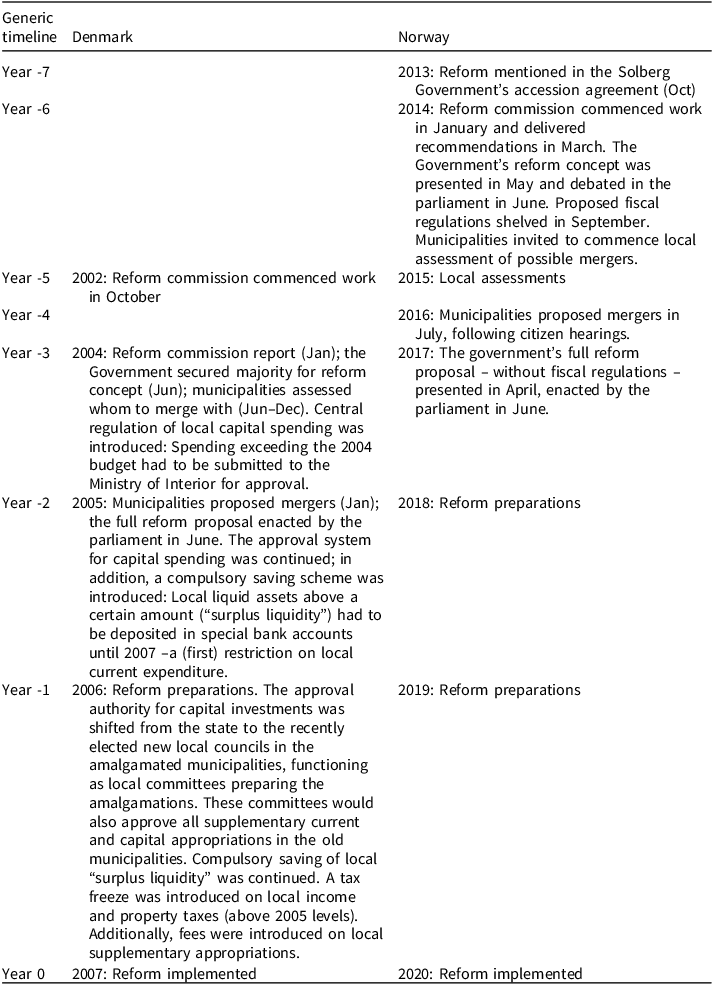

The national government in Denmark implemented a multitude of pre-merger regulations in the period between 2004, when the amalgamation reform was initiated by the national government, and 2007. The regulations included a ministerial loan approval, a compulsory saving scheme, a tax freeze, and fees on local supplementary appropriations (Blom-Hansen Reference Blom-Hansen2010). For example, in the final years before the amalgamations in 2007, the municipalities were not to allowed change local taxes and “excess liquidity” had to be deposited with the national government. In addition, all new capital investments in 2004 and 2005 had to be approved by the national government, as well as by the local amalgamation committees responsible for preparing the amalgamation in 2006 (see Table 1). Approval of capital investments and loans had the aim of limiting pre-merger overspending on capital expenditure (as only capital expenditure is allowed to be loan-financed), while restrictions on taxes, liquid assets and supplementary appropriations also had the aim of limiting overspending on current expenditure.

Key reform events

Sources: Blom-Hansen, Houlberg and Serritzlew (Reference Blom-Hansen, Houlberg, Serritzlew and Treisman2016), Blom-Hansen (Reference Blom-Hansen2010), Klausen et al. (Reference Klausen, Askim, Vabo, Klausen, Askim and Vabo2016, Reference Klausen, Askim and Christensen2021).

Despite being aware of potential pre-merger overspending, the national government in Norway chose a very different strategy to regulate local fiscal autonomy. In May 2014, the government proposed curtailing the freedom of municipalities to take out loans and enter into long-term lease agreements until implementation of the reform in 2020. The government cited fears that “debts may increase because the current municipal council can invest and roll the costs onto the new, larger municipality” (Ministry of Local Government and Modernization, 2014, p. 50). However, the government shelved the proposal in September 2014 after protests from the local government sector and opposition parties in parliament. The government judged that the reform would only result in a small number of voluntary local merger proposals unless it backtracked from placing any extraordinary regulations on the municipalities’ fiscal autonomy (Klausen et al. Reference Klausen, Askim and Christensen2021).

Design, methods, and data

We use a DDD design to estimate the difference between pre-merger overspending in a non-regulation scenario (Norway) and a scenario with multiple regulations (Denmark).

For each country, we use a difference-in-difference (DiD) logic to compare the pre-merger fiscal policies in a treatment group of municipalities that were amalgamated with a control group of municipalities that were not. On top of this, we estimate the difference between overspending in the treatment group of Danish municipalities that came under national pre-merger regulations and the control group of Norwegian municipalities that were not affected by specific pre-merger regulations. The overall design thus represents a DDD design comparing the difference between (1) the DiD of amalgamated and non-amalgamated Danish municipalities and (2) the DiD of amalgamated and non-amalgamated Norwegian municipalities. The DDD estimator is also known as the triple difference estimator (Olden and Møen Reference Olden and Møen2022). To illustrate the DDD-logic, we first use the DiD-logic to estimate overspending in Norway and Denmark, respectively, by comparing the fiscal development in amalgamating municipalities and non-amalgamating municipalities within each of the two countries. We then pool the data for the two countries and interact the DiD-estimators with a dummy for regulation (Denmark) vs. non-regulation (Norway) to achieve the DDD-estimator. The DDD estimator can thus be interpreted as the difference in overspending among the amalgamating units in a no-regulation scenario (Norway) and the amalgamating units in a regulation scenario (Denmark), compared to the concurrent spending development in the non-amalgamating units of the two countries, respectively.

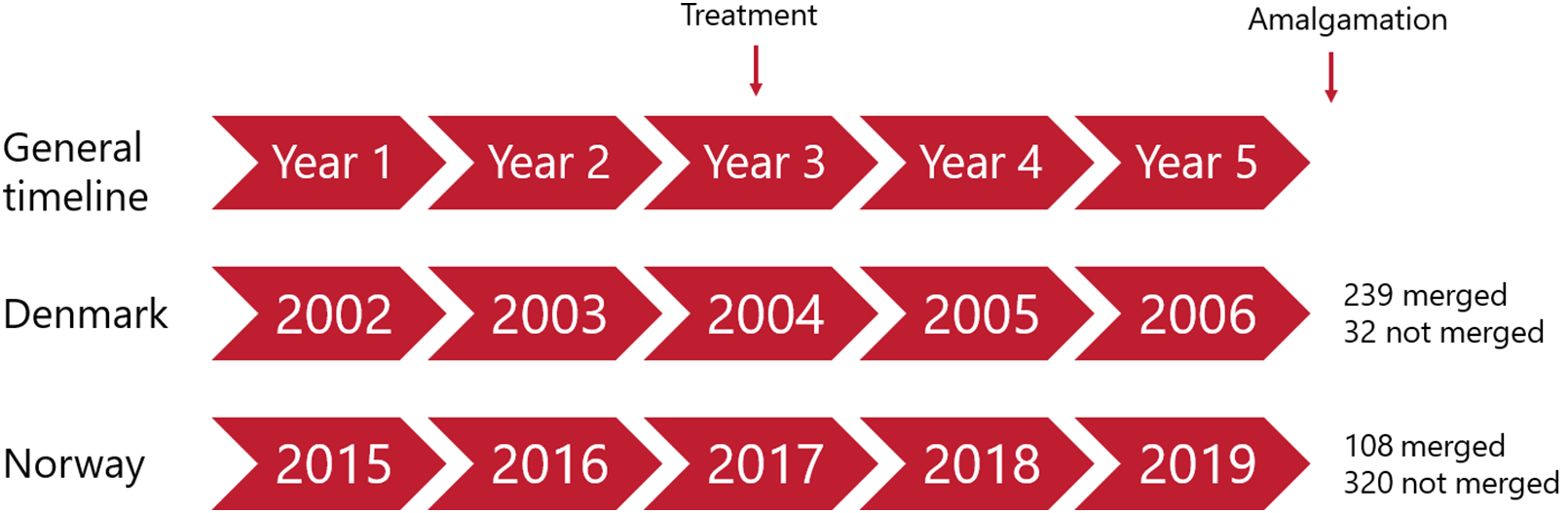

The design is illustrated in Figure 1 and explained in further detail below. The label “treatment” marks the year in which the municipalities in the two countries knew whether they were going to be merged two years later.

Illustration of the quasi-experimental design in each of the two countries with two pre- and two post-treatment years.

In Denmark, 239 municipalities were amalgamated into 66 municipalities by 1 January 2007, with 32 municipalities remaining unchanged. Our treatment group in the Danish reform context is the group of 239 municipalities that knew by the end of 2004 that 2005 and 2006 would be the final years they had authority over their financial policies. The remaining 32 municipalities constitute our control group of non-amalgamating municipalities. Our dataset for Denmark covers the 5 years from 2002 to 2006, with 2004 as the year when 239 municipalities were “treated” with the knowledge that they were going to be amalgamated by 2007. The years 2002–2003 can thus be considered pre-treatment years and the years 2005–2006 as treatment years.

In the Norwegian case, by the time the reform was enacted by parliament in June 2017, 108 municipalities were aware that they would be part of a merger and thus cease to exist in their current form in 2020. 2018 and 2019 would consequently be the final years in which they had full authority over their financial policies. This is our treatment group. The remaining municipalities knew they would not be part of a merger in 2020, and they constitute our control group. Our dataset for Norway covers the 5 years from 2015 to 2019, with 2017 the treatment year when 108 municipalities were “treated” with a parliamentary decision for them to be amalgamated in 2020. 2015 and 2016 constitute two pre-treatment years and 2018 and 2019 two post-treatment years. As already mentioned, the government did not set any specific regulations regarding fiscal policies for the soon-to-merge municipalities in 2018 and 2019.

To improve the potential for generalization we exclude certain municipalities due to incomparability. We exclude 5 of the 271 Danish municipalities: Copenhagen, Frederiksberg, and Bornholm whose task portfolio and fiscal situation are incomparable due to their two-tier status as both counties and municipalities and two municipalities that were amalgamated one year earlier than the rest. We thus end up with a dataset containing 266 Danish cases across 5 years, and a total of 1,330 observations. Of the 266 cases included, 234 municipalities were merged in 2007 and 32 were not. In Norway, we exclude 23 of the 428 municipalities: Oslo, due to its two-tier status as both county and municipality; Utsira, because it is extraordinarily small; and 10 municipalities because they are extraordinarily rich because of revenues from hydropower plants (Andersen and Sørensen, Reference Andersen and Sørensen2022). We also exclude 11 municipalities that were fast-tracked in the reform process and merged two or three years earlier than the rest. We thus end up with a dataset containing 405 Norwegian cases across 5 years, and a total of 2,025 observations. Of the 405 cases included, 107 municipalities were merged in 2020 and 298 were not.

The total merged dataset for the two countries contains a panel of 3,355 observations comprising data for 671 municipalities across 5 years. The 671 municipalities consist of 266 Danish municipalities “treated” with pre-merger regulation (234 merged municipalities and 32 non-merged), and a control group of 405 Norwegian municipalities not regulated by pre-merger regulations (107 merged municipalities and 298 non-merged).

Variables

Pre-merger overspending has previously been studied separately in the two countries (e.g. Blom-Hansen Reference Blom-Hansen2010; Hansen Reference Hansen2014; Hansen Reference Hansen2019; Askim et al. Reference Askim, Houlberg and Klausen2023). The indicators for overspending however vary across the studies. To be able to quantitatively compare pre-merger overspending in the two countries, we in this study apply the same set of variables in both countries. The outcome variables consist of a total of five indicators covering two aspects of pre-merger overspending: allocation of overspending and financing of overspending.

The two main dependent variables measure the allocation of pre-merger overspending to, respectively, current- and capital expenditure:

-

• Net current expenditure per capita

-

• Gross investments per capita

In addition, we include three dependent variables focusing on the sources of financing for pre-merger overspending:

-

• Net operating surplus per capita (current revenue less current expenditure and interest)

-

• Liquid assets per capita (savings)

-

• Long-term debt per capita

For the Norwegian case, all five dependent variables are based on final accounts data from KOSTRA, the official Norwegian database for local-to-central government reporting (Statistics Norway, 2025). For Denmark, all variables are based on final accounts data from Statistics Denmark (2025). In line with former DiD-studies of pre-merger overspending in the two countries, these dependent variables are per capita measures (e.g. Hansen Reference Hansen2014; Hansen Reference Hansen2019; Askim et al. Reference Askim, Houlberg and Klausen2023).

All economic figures are measured in EUR in fixed 2020 prices. To convert to EUR, we used the following conversion rates throughout the study period: 10.4956 NOK and 7.4542 DKK to 1 EUR.

Fiscal policy is influenced by factors other than mergers, and the sorting of municipalities into groups for merged and non-merged was not random in either country. We therefore include controls for two variables known to affect the fiscal policies of Norwegian and Danish municipalities: municipal wealth and population (Blom-Hansen et al. Reference Blom-Hansen, Houlberg, Serritzlew and Treisman2016; Askim et al. Reference Askim, Houlberg and Klausen2023). In addition, we include year dummies to control for the general time trend in the period. As fiscal policy can be conditioned by political preferences, we also include a control for the political leaning of the municipalities, specifically the share of seats for right-wing parties in the municipal council.

See Online Supplementary Tables A1a and b in the appendix for descriptive statistics and information about the measurement of all variables. Additional background information concerning the sample and the two groups of municipalities (merged and non-merged) for each country is included in Online Supplementary Table A2 in the appendix.

Results

The results of the DiD-based regression analyses are presented below, first for Norway and then for Denmark. We subsequently present the DDD analysis estimating the difference in pre-merger overspending between Norway’s no-regulation scenario and Denmark’s regulation scenario.

The results are displayed for our two main indicators of spending allocation, current expenditure and capital expenditure, as well as our three financing indicators for potential pre-merger overspending (running down operating surpluses, using liquid assets and increasing long term debt).

Pre-merger overspending in Norway and Denmark respectively (DiD)

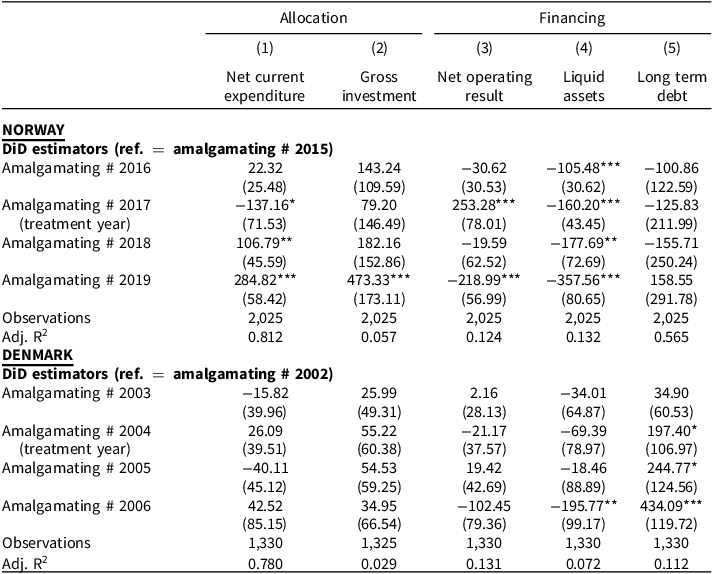

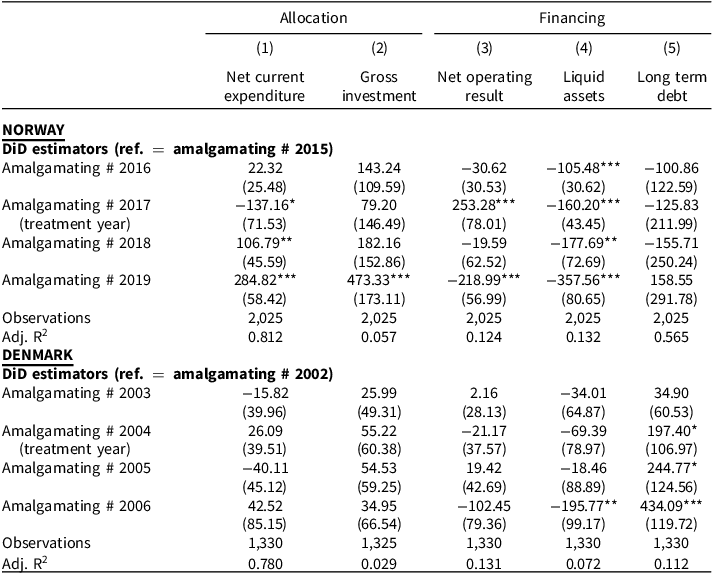

Table 2 presents the results of the DiD analysis of pre-merger overspending in Norway and Denmark respectively. The table show the regression models’ DiD estimators. For full models, see Online Supplementary Table A3a and Online Supplementary Table b in the appendix.

DiD analysis of pre-merger overspending in Norway and Denmark respectively, merging vs. non-merging municipalities. EUR per capita, 2020 prices

Control variables and year dummies included but not shown. Robust standard errors in parentheses (cluster-corrected at the level of each municipality), ***p < 0.01, **p < 0.05, *p < 0.1.

The results for Norway resemble the findings of Askim et al. (Reference Askim, Houlberg and Klausen2023). The interaction term “amalgamating # 2016” estimates the pre-treatment change in difference between the treatment and control groups between 2015 and 2016. Apart from model 4 (Liquid assets), these estimates are statistically insignificant. The estimates thus indicate that the pre-treatment trends for treatment and control groups are largely parallel.

We now address the DiD estimates for the 2018 and 2019 treatment years. The DiD estimates are terms that interact the group to which a municipality belongs with a treatment year. The reference group for all DiD estimates is the pre-treatment level of the dependent variable in 2015 for the control group of non-merging municipalities. We thus estimate whether the difference between the treatment group and the control group was larger or smaller than it was in 2015 for each treatment year.

The DiD estimates for 2018 show that the amalgamating Norwegian municipalities significantly increased spending allocated to current expenditure, but not to capital investments, relative to the non-merging municipalities in the penultimate year before the merger. In regard to financing options, it should be noted that the results for the liquid assets variable are indicative, as the pre-treatment trends for treatment and control groups were not parallel. Nevertheless, the 2018 estimate for liquid assets indicates that the increase in spending on current expenditure was financed by a decrease in liquid assets. There are no indications that overspending was financed by running down the operating surplus and taking out loans (long-term debt) in 2018.

The picture changes in the final year before amalgamation. The DiD estimates for 2019 are significant in four of the five models. In this final year before the merger, the merging municipalities significantly increased spending on both gross investment and current expenditure. In terms of financing, the merging municipalities reduced their operating surplus, and, indicatively, reduced liquid assets. The only indicator not affected by the forthcoming merger seems to be long-term debt.

For Denmark, the DiD estimators for 2003 are insignificant for all indicators, thus indicating that pre-reform trends for treatment and control groups are parallel.

The DiD estimators for the post-treatment years (2005 and 2006) are insignificant for both allocation indicators. In other words, the soon-to-merge Danish municipalities did not increase their spending in the last two years before the actual amalgamations on either current expenditure or capital investments relative to the non-merging municipalities. However, in 2006, the final year before amalgamation, the merging municipalities did reduce liquid assets and increase long-term debt more than the non-merging municipalities compared to the difference between the two groups in 2002. In other words, the merging Danish municipalities did not engage in pre-merger overspending as measured directly by increased spending before “closing time”. They did however change fiscal policies by draining the coffers and accruing additional loans.

Comparing pre-merger overspending in Norway and Denmark (DDD)

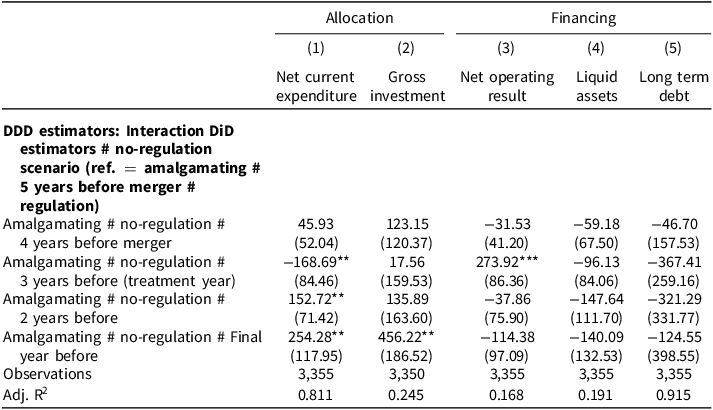

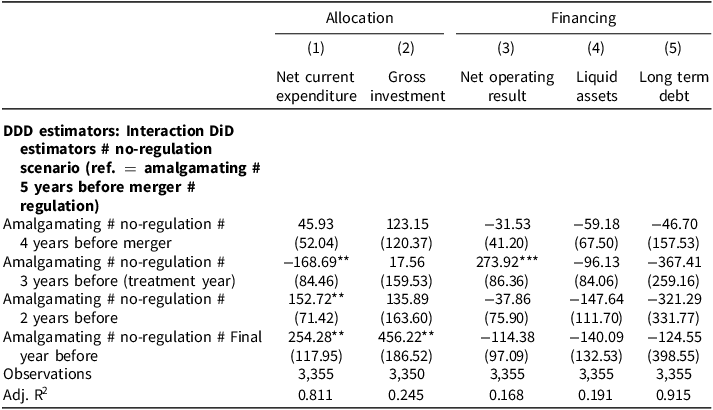

The two datasets for Norway and Denmark are combined in Table 3 to directly compare and estimate the difference in pre-merger overspending in the no-regulation scenario (Norway) with the regulation scenario (Denmark). As we use the same control variables for both countries, the combined dataset allows us to estimate the difference in the DiD estimators for Norway and Denmark (DDD), while controlling for differences in municipal size, wealth, and party composition of municipal councils in the two countries. Table 3 presents the DDD estimators, which interact the DiD-estimators for pre-merger overspending in Norway with the DiD-estimators for pre-merger overspending in Denmark. For full models, see appendix A.4.

DDD analysis of pre-merger overspending in a no-regulation scenario (Norway) vs. a regulation scenario (Denmark). EUR per capita, 2020 prices

Control variables and year dummies included but not shown. Robust standard errors in parentheses (cluster-corrected at the level of each municipality), ***p < 0.01, **p < 0.05, *p < 0.1.

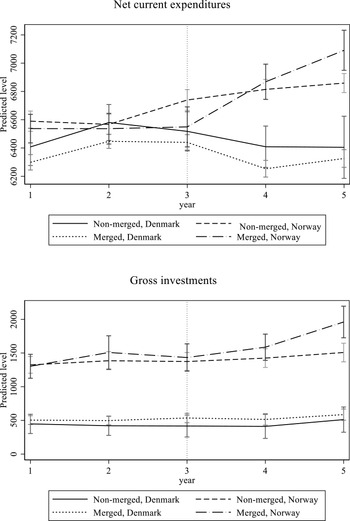

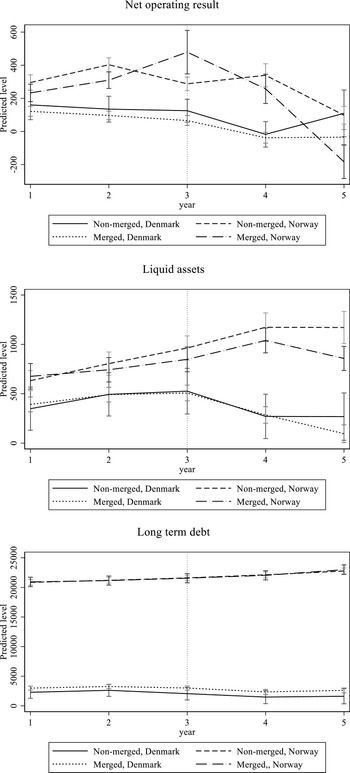

To support interpretation of the results, predictive margins for the five outcome variables are illustrated graphically in Figures 2 and 3.

Predictive margins for allocation of pre-merger overspending. EUR per capita, 2020 prices (with 95% CIs).

Note: Based on the models in Table 3. Dotted vertical line indicates treatment year.

Predictive margins for financing of pre-merger overspending. EUR per capita, 2020-prices (with 95% CIs).

Note: Based on the models in Table 3. Dotted vertical line indicates treatment year.

The DDD results for allocation of pre-merger overspending in models 1 and 2 in Table 3 show that pre-merger overspending in the final year before amalgamation was significantly higher in Norway than in Denmark in relation to both current expenditure and capital investment. In the final year before amalgamation, the soon-to-merge Norwegian municipalities increased current expenditure by 254 EUR per capita more than the soon-to-merge Danish municipalities (compared to the non-merging municipalities in the two respective countries). Overspending on capital investments was similarly 456 EUR per capita higher in the soon-to-merge Norwegian municipalities than in their Danish counterparts. Compared to average spending in Norway of 6,767 EUR current expenditure per capita and 1,454 EUR capital expenditure per capita, the additional overspending represents a substantial amount. In addition, overspending on current expenditure was 153 EUR per capita higher in Norway than in Denmark two years before the mergers. Figure 2 illustrates the results for current expenditure and capital investment. Bearing in mind that the DDD estimator is less sensitive to the parallel trend assumption than DiD estimators (Olden and Møen Reference Olden and Møen2022), we nevertheless note largely parallel trends for merging and non-merging municipalities for current- and capital expenditure in both Norway and Denmark in the years prior to merger-decision treatment in year 3. In Denmark, the parallel trends continue in the years after treatment, whereas in Norway the merging municipalities increase both current expenditure and gross investment significantly more than their non-merging fellow countrymen.

The DDD results for financing of pre-merger overspending in models 3–5 in Table 3 indicate that the higher level of pre-merger overspending in Norway in the final year before amalgamation was primarily financed by running down operating surpluses. In the year before amalgamation the soon-to-merge Norwegian municipalities reduced their net operating result by 104 EUR per capita more than the soon-to-merge Danish municipalities (compared to the non-merging municipalities in the two respective countries). However, the estimate is not statistically significant. For liquid assets (model 4), the results indicate that the merging municipalities in Norway over-reduced their liquid assets significantly more than the merging municipalities in Denmark in years 2–4 of the reform process, i.e. starting in year 2, one year before treatment with merger-decisions. This indicates that the municipalities may have anticipated a forthcoming merger before the actual merger decision was made. Regarding long term debt (model 5), the DDD estimators show no signs of higher pre-merger take up of loans in Norway than in Denmark. Figure 3 supports these interpretations by showing a higher drop in operating results in the soon-to-merge Norwegian municipalities than in their Danish peers in the final year before amalgamation. For liquid assets and debt, the trend in the difference between merging and non-merging municipalities is not significantly different in the two countries in the final year before amalgamation.

The effects of the regulations are not only statistically, but also substantively significant. In Norway’s non-regulation scenario, the additional overspending on current expenditure of 254 EUR per capita in the final year before merger equates to 3.8 per cent of average current expenditure per capita (6767 EUR) in the period studied. Similarly, the additional overspending on capital expenditure of 456 EUR per capita equates to 31 per cent of average capital expenditure per capita (1,454 EUR) in Norway. This is a substantial amount of additional freeriding on the common pool of the forthcoming amalgamated units in the soon-to-merge Norwegian municipalities compared to the soon-to-merge Danish municipalities. With 1.5 million citizens in the merged Norwegian municipalities, the additional overspending amounted to 380 million EUR on current expenditure and 680 million EUR on capital investment, approximately 1 billion EUR in total.

In a supplementary analysis, we test whether pre-merger overspending is more pronounced among junior partners to a merger than among senior partners. The analysis shows that the junior partners in both Norway (Online Supplementary Table A5a) and Denmark (Online Supplementary Table A5b) overspent relatively more than their senior partners prior to amalgamation. The effect of the relative size of the merging municipalities is, however, neither significantly larger nor smaller in the non-regulation context of Norway than in the regulation context of Denmark (Online Supplementary Table A6). In other words, the pre-merger regulations in Denmark seem to have affected all partners to the merger equally, independent of their relative share of the new merged municipality’s population.

Concluding discussion

The article contributes new knowledge about the effects of regulation of fiscal behavior in the context of mergers of local governments. Specifically, it contributes to the nascent scholarship on the possibility of counteracting the “iron law” of pre-merger overspending: As soon as a merger is certain or likely, the original local units are incentivized to overspend on local goods before the merger is implemented and they cede power to the new, amalgamated unit.

Our starting point was, firstly, the paradox that so few amalgamation reforms are accompanied by regulations that limit local fiscal autonomy during this interim period. Despite the infamous “iron law”, upper levels of government often choose to allow the overspending incentive to operate freely during amalgamation reforms. Secondly, there is a lack of knowledge concerning how well anti-overspending regulations work.

Our research question concerned how divergence in reform-specific regulation of municipal fiscal behavior affects the level and form of pre-merger overspending at the local level. Our expectation was that pre-merger overspending would be lower in a regulation scenario than in a non-regulation scenario.

To test this expectation, we needed to overcome a general problem in regulatory studies: i.e. that lack of a proper control group makes it difficult to tell how effective any regulation is (Coglianese, Reference Coglianese2012). Policymakers rarely experiment by only subjecting parts of a target group to unpopular regulations. To our knowledge, there has never been any regulatory experimentation in relation to prevention of pre-merger overspending. To overcome this research design problem, we utilized the fact that Denmark and Norway underwent local government amalgamation reforms since the turn of the millennium that were similar in most relevant respects, e.g. with some municipalities amalgamating and others not, but with one crucial difference in the reform design: i.e. that Denmark regulated pre-merger overspending while Norway did not. It was thus possible to use a comparative DiD design, i.e., a DDD design, to facilitate quantitative estimation of the difference in pre-merger overspending between a non-regulation scenario and a scenario with multiple regulations. No other comparative quantitative study of pre-merger overspending of this kind currently exists.

The results supported our expectation. Pre-merger overspending in the soon-to-merge municipalities was significantly higher in the non-regulation scenario (Norway) than in the regulation scenario (Denmark), regarding both current expenditure and capital investments. Compared to their fiscally regulated peers in Denmark, there was a substantial additional overspend both in the form of current expenditure and capital investments in the soon-to-merge Norwegian municipalities. The additional overspending is estimated to around 250 EUR per capita on current expenditure and 450 EUR per capita on capital expenditure in the final year before the merger. The results indicate that the additional overspending was primarily financed by running down operating surpluses.

The estimated effect should be considered conservative, implying that the true effect of regulation is likely to be even greater than we were able to document in this study. The reason to emphasize this is that divergence in regulation was not the only relevant difference between the amalgamation reforms in the two countries. Two important differences between the two reforms may potentially have affected the likelihood of pre-merger overspending. One is that the global macro-fiscal environments differed in the two time-periods, as the Danish reform was implemented prior to the global financial crises in 2008–2010 and the Norwegian reform a decade later. The macro-fiscal environment was however more different globally than between these two countries, as the average annual GDP-growth was 2.0% in Denmark in 2002–2006 and 1.5% in Norway in 2015–2019 (World Bank 2025). The time dummies in our analyses basically handle the general time-trends in the reform periods, including time differences in macro-fiscal environments. If these controls are imperfect and if overspending is affected by differences in macro-fiscal environments, the higher GDP growth in Denmark and accompanying higher purchasing power would indicate a higher potential for overspending in Denmark than in Norway. This suggests that the estimated effect of regulation should be considered conservative.

The other difference is that Norway’s reform was mainly bottom up, with most amalgamating municipalities having volunteered to do so, while Denmark’s reform was top-down (coercive), with far firmer central control. Existing research has demonstrated that pre-merger overspending is more prevalent among municipalities that are forced to amalgamate than those that do so voluntarily (Fritz and Feld Reference Fritz and Feld2015, Mughan Reference Mughan2019). This can be interpreted to reflect that those forced to amalgamate overspend to express dissent (Askim et al. Reference Askim, Blom-Hansen, Houlberg and Serritzlew2019). Any effect of reform coerciveness on pre-merger overspending thus points in the opposite direction compared to the effect of anti-overspending regulations. Stated differently, had Norway’s reform been less voluntary, it is likely that the estimated effects of divergent regulation would have been greater.

In extension of this study’s conclusion, we mention some questions that could be addressed in future research on the regulation of pre-merger overspending – questions that concern, respectively, regulation, regulatees, and regulators. First, which specific regulations are most effective in preventing pre-merger overspending? Answers could be obtained by comparing scenarios with different types of formal regulations, for example, regulations limiting the availability of- and regulations limiting the allocation of resources. This could be achieved in future research by studying comparable cases displaying this critical difference, or by conducting survey experiments.

Relatedly, given that regulations are intended to limit local units’ possibility of collecting a “war chest” for freeriding, what should be prioritized? Which local financing option that has the most detrimental long-term implications is likely context dependent. Given strong employment protection, running the operating surplus down to hire new staff is difficult to reverse by the new and merged polity; re-establishing a healthy fiscal balance would require the new polity letting people go. Accruing debts or depleting of savings to finance one-off capital investments is comparably easier to handle in the long term, e.g., by the new polity selling off or renting out infrastructure.

Second, a question concerning regulatees: Why do some municipalities adhere to anti-freeriding regulations while others evade them? Qualitative studies would be welcome to shed light on local decision-makers’ reasoning. Additionally, answering this question quantitatively would require making municipality-level variance in regulation adherence into the dependent variable and seek to explain this variance using municipality-level independents. A further question about regulatees is if knowledge about the composition of the enlarged units influence the initial units’ responsiveness to anti-freeriding regulations. This study suggests the answer is no, as municipalities were equally responsive to regulation irrespective of a variance known to affect the freeriding incentive itself, namely whether they would be a senior or a junior partner in the amalgamated unit. The generalizability of this conclusion could be tested by examining if responsiveness to regulation is affected by other sources of heterogeneity that could affect the initial units’ balancing of self-interest against motivations such as altruism and reciprocity.

Third, a question concerning regulators: Should all amalgamation reforms include anti-overspending regulation? We offer our assessment by way of returning to the paradox that so few amalgamation reforms are accompanied by extraordinary constraints on local fiscal autonomy just before mergers are implemented. Governments can have different reasons for not regulating pre-merger overspending, and this study has not shed any direct light on their reasoning. We can speculate, however, that amalgamation reforms present governments with dilemmas known from the politics of regulation more generally (Wilson, Reference Wilson, Fergusen and Rogers1984). Regulation can have unintended consequences opposite to their intent. The upper level of government can fear that the incentive to overspend before merging is strong enough to tempt local units to waste resources on identifying and exploiting loopholes in the regulations – loopholes that correspond to spending purposes that are inefficient compared to purposes the local units would have prioritized in the absence of anti-freeriding regulations.

Moreover, regulation can construct a barrier to “market entry”: Upper levels of government want to avoid incurring animosity towards the reform by signaling a lack of trust in responsible fiscal policymaking at the local level. In top-down reforms, local authorities are forced to amalgamate, but avoiding animosity might still be useful as the implementation of reforms is likely to be aided by willing participants. In bottom-up reforms, where, to have any real scope and effect, the upper level for political or constitutional reasons is dependent on local willingness to opt in to the reform (i.e., enter the “market”), avoiding local animosity can be crucial. The question becomes one of cost and benefit. What produces the greatest benefits in the short- and long-term? On the one hand, by choosing not to regulate (or even temporarily lift normal regulations), governments can ensure that many local authorities merge willingly. This incurs certain costs in the short-term in the form of pre-merger overspending (and obviously other transaction costs of merging) but can also produce aggregate benefits in the long run – far greater overall than if fewer local authorities had opted in to the reform. On the other hand, by choosing to regulate, the short-term costs are lower, and likewise the long-term benefits. The accuracy of such cost-benefit analysis will be aided by the cost estimates in this article and the knowledge that regulation substantially reduces pre-merger overspending.

Finally, regulations can be avoided due to oversight costs. Irrespective of the degree of voluntariness of a reform, governments may expect the overall benefits of preventing overspending to be less than the transaction costs incurred by designing and implementing effective anti-overspending regulations. We do not have any data on the cost of implementing regulations. However, this article’s estimation of the benefits of regulating (or inversely, the cost of non-regulation) might constitute useful input for policymakers, facilitating more precise cost-benefit analyses and providing an insight into what types of regulations might be necessary.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S0143814X26101160.

Data availability statement

Replication materials are available in the Journal of Public Policy Dataverse at: https://doi.org/10.7910/DVN/IYBJLV.

Acknowledgments

The authors are grateful for comments from participants in a research seminar at the Danish Center for Social Science Research (VIVE) in April 2024, and from participants in panels at the Nordic Political Science Congress (NOPSA), 25–28 June 2024 in Bergen, Norway and the ECPR General Conference, 12–15 August 2024 in Dublin, Ireland.

Funding statement

This work was supported by the Research Council of Norway under grant number 255111.

Competing interests

The authors declare none.

Open access

Open access