1 Introduction

Most analyses of Japan since the beginning of the twenty-first century portray a scenario of doom and gloom. As the world prepares for the digital transformation (DX), it is often assumed that leadership in future industries such as big data analysis, the cloud, and artificial intelligence will belong to the United States and China.Footnote 1 Japanese companies are generally seen as too slow or too weak to compete, and Japan’s economic structures are considered too ossified, stagnant, and unproductive.Footnote 2 What is more, Japan is the first country in the world to face rapid demographic change, with the population predicted to shrink by 25 percent in the next three decades, from 126 million to fewer than 100 million people by 2050. By 2040, 36 percent of Japan’s population will be older than sixty-five years (Cabinet Office 2020a). This has not only made labor shortage a certainty but has also raised grave concerns about the future fabric of Japanese society and economy, as well as its sustainable prosperity and social security.

To many observers, these two trends’ co-occurrence means Japan is destined for obsolescence. However, if one looks beyond the macroeconomic indicators and demographic prognostications, the story is not so simple. Together, the digital transformation and demographic change create a window of opportunity for Japan, where the changing needs of labor are creating space for companies to explore and shift to new strategies, which in turn are facilitating a rewriting of the mutual rights and obligations between government, business, and labor that defined Japan’s twentieth-century political economy.

The term “digital transformation” refers to the great advances in computing powers and analytical techniques, as well as communication and vision/sensing technologies that combine to create a new world of 5G-enabled constant connectivity, autonomous systems and robotics, blockchain, artificial intelligence and machine learning (AI/ML), data mining, and governance through “the cloud.” For industry, these advances coalesce into what has been termed “industry 4.0,” that is, the arrival of digital manufacturing, which will upend what we know about operations management. For humans, they bring the next step of our evolution, into “society 5.0,” namely, a constantly connected society based on autonomous systems for most service needs.Footnote 3 The digital transformation will be borderless, ubiquitous, and inescapable, and it has already begun. It is about to affect all industries, societies, and continents in similar ways. The nature of competition, the meaning of production, the demarcation of industrial sectors, and the identity and assignments of workers will all evolve. In many countries, the realization of these impending changes has brought fears of a world taken over by robots, riddled by social displacement and distress, governed by algorithms, and regulated in ways that favor machines over humans (e.g., Reference Brynjolfsson and AndrewBrynjolfsson and McAfee 2016; Reference FordFord 2016; Reference Acemoglu and RestrepoAcemoglu and Restrepo 2020).

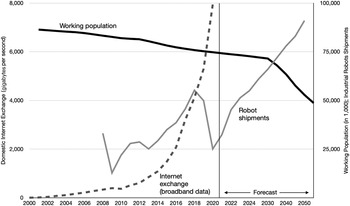

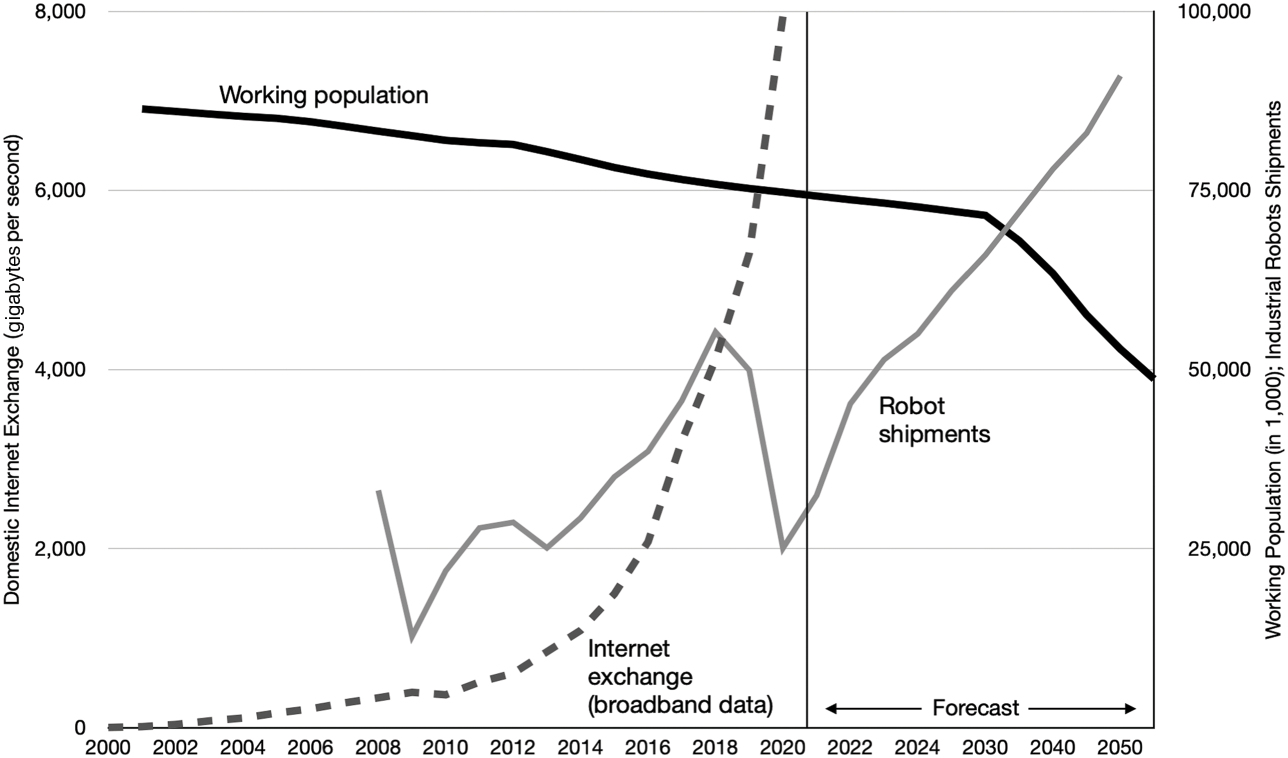

Japan is certainly not the only country to face the digital disruption, nor is it the only country facing demographic change. But what is special about Japan’s situation is the timing: Because Japan’s society is ageing and shrinking earlier and faster than any other advanced nation, the demographic shock and the digital transformation are arriving at exactly the same time. To visualize this coincidence, Figure 1 shows Japan’s working population in the top solid line (see Section 2 for comparative demographics), as well as two indicators of technological change. The first is the rapid increase in fixed-line broadband data exchange (dashed line). This began to rise in the 2010s and increased exponentially with the 2019–20 COVID-19 pandemic and the shift to telework. The gray line represents a second indicator, the number of shipments of multiuse industrial robots. While it declined during COVID-19, it is now conservatively estimated to grow at least at 5 percent year-over-year.

Figure 1 Demographic change and indicators of the digital transformation in Japan

Note: Decline in working population (in 1,000 people, right axis, top line), industrial robot shipments (right axis), and broadband-based data use, peak traffic in December of each year, left axisFootnote 4

This coincidence presents a window of opportunity, a “lucky moment,” for Japan. The simultaneous arrival of the two disruptions – ageing society and shrinking workforce cum digitization of industry and society – brings not so much a threat, but rather, the solution. Far from throwing Japan into obsolescence, they offer an opportunity to combine two negatives into one positive. Japan may emerge a stronger economy and society for it, as each disruption can solve the problems caused by the other. The arrival of automated systems at a time when many traditional industries are suffering from decline and labor shortage means that workers need not be displaced, and automated production, blockchain logistics, and stores without cashiers can proliferate without the societal upheaval and friction that is so often feared. At the same time, the digital transformation is opening new avenues for Japanese industry to compete. Globally, new technologies create new markets that allow for business growth and productivity gains. Domestically, as companies pivot and reinvent, they have new demand for specific labor skills. This is happening just at a time when the looming labor shortage is increasing the bargaining power of labor, in particular the highest skilled segment. The new power relations are allowing employees to renegotiate the time-honored institutions of Japanese labor relations.

When hearing about the ageing society and the digital disruption, most people conjure up images of a cute-looking robot helping an elderly person with a daily chore. Indeed, Japan is often said to be a leading innovator around robotic applications for nursing and “silver” entertainment.Footnote 5 However, in this Element we look at something much broader and deeper. The digital transformation is much more than just an increase in robots, or even the interaction between robots and society. It is about a fundamental shift of economic activity, a deep-seated transformation of what sectors of the economy perform what types of business, how production is governed, how productivity is measured, and how goods and services are presented and consumed.

For business, this necessitates a complete “model change,” as Toyota CEO Akio Toyoda labelled it.Footnote 6 For society, this means a redefinition of self, privacy, and lifestyle, as well as a shift from owning things to consuming subscription services, and to working in fully automated settings and moving in automated systems, with constant connectivity and information updating. For government, the digital disruption requires a redesign of regulation and policymaking in a world governed by ubiquitous connectivity, immediate information sharing, and borderless competition. Japan’s social contract – the tacit agreements of the rights and responsibilities of business, people, and the state – is also being rewritten. This means, Japan’s entire political economy is in the process of being updated for the “society 5.0” version. The twin disruptions are occurring with certainty; they cannot be avoided. This leaves the government with no choice but to adjust to the shifting industrial and societal architecture.

Japan’s rapid economic growth after WWII was characterized by proactive “industrial policies” that consisted of the rank-ordering of industries and anointing of champions to streamline growth through within-industry coordination. The digital transformation is now shifting the global technology frontier to places that the state can no longer organize or coordinate. For companies, the need to compete in the global race for deep-technology advances necessitates new business strategy. For the state, industrial policy needs to be redesigned to support corporate strategies that transcend industries and even economic sectors, as the overall governance of Japan’s markets evolves. In 2020, Japan was the first country to appoint a “Minister of Digital Transformation” (Dijitaru kaikaku tantō daijin), to design a Digital Agency (Dijitaru-chō) within the government tasked with bringing about a reorganization of ministries, responsibilities, and policymaking processes.

As of 2022, hardly a day goes by where the “digital transformation” is not front-page news in Japan. As this term is unwieldy, especially in Japanese katakana, it has been abbreviated as the “DX.” We will adopt Japan’s term of “DX” here, to refer to this coming technology–society–strategy shift in its entirety. In the United States, even though the “digital transformation” is still spelled out, new vocabulary has emerged to describe the coming industry-specific disruptions, often as a portmanteau ending with “-tech,” such as fintech (financial services), insurtech (insurance), agrotech (agriculture), proptech (real estate), matech (marketing), or medtech (health sciences and medical devices).

The goal of this Element is to lay out how the combination of the DX and demographic change are changing the underlying logic of Japan’s political economy, through the upheaval of the country’s industrial architecture and employment patterns. We show how industries such as agriculture and the manufacturing sector are evolving, and how the DX is affecting employment, skill formation, and education. Existing assumptions and definitions regarding how to divide economic activity into sectors, or how to assess policy successes, are no longer meaningful as the evolving business models straddle sectors and the technology race is global. The DX reduces corporate resource dependence on the state and empowers businesses with deep technology expertise. The COVID-19 pandemic has only accelerated these shifts, by pushing forward work style changes, shifting career ambitions, and the phasing out of legacy business sectors. In the new political economy, neither business nor people nor the state will work as they used to.

As the first country to face the onset of demographic change, Japan becomes a trailblazer. Its experience may shape how other countries utilize the DX for domestic social policies, and its mistakes may prove relevant for others. As the third-largest economy in the world and a leader in advanced production technologies, materials, mechatronics, and system solutions, Japan has the resources to be a strong global competitor at the technology frontier that is the manifestation of the DX. In what role and with what capacities the Japanese state will emerge, and how Japan’s political economy is preparing to compete is likely to be once again an important case study.

We focus on the opportunities that the twin disruptions are opening up for Japan. Of course, the DX will create similar opportunities for Japan’s global competitors, and it is unknown who will win in the jockeying for position at the technology frontier, or who will dominate the global supply chains of the future. Within Japan, too, there will be losers. These will include large firms that fail to adapt, and small firms and other parts of society that are left behind in low-productivity parts of the economy. To what extent these are stuck will depend on how the state will be able to compensate them, and how companies will adapt and reskill. The “lucky moment” may create new opportunities for the state to minimize some of these costs, as we allude to in Sections 5 and 6. That said, we will focus on the DX change process and the new constellations that are emerging. A study of the social costs as well as the role of small firms in Japan’s DX is beyond the scope of this Element and left for future research.

Our discussion will be structured as follows. We understand “political economy” to mean the interplay between business, people, and the government. We will analyze their relationships in three main sections in this Element.

For business, we are interested in how companies are adjusting corporate strategies for deep-technology innovation and business models that embrace servitization. The DX will require new skills, new specialization, and new approaches to innovation and measures of profitability. Japan’s leading companies are redefining their core businesses and identities to become providers of deep-technology solutions.

We use the label of people to refer to demographic change and the labor shortage, as well as changes in Japanese employment practices.Footnote 7 The DX will require new designs and processes in education as well as the reskilling of the current workforce. Further, the newly emerging job mobility has begun to alter the rights and responsibilities of employers and employees, just as the DX is removing old jobs and creating new ones.

The role of the state is also changing as the government no longer has the answers in a VUCA (volatile, uncertain, complex, ambiguous) world. Power relations between politicians and bureaucrats have changed, old industrial policies no longer apply, and fewer young people are applying to government jobs. But the DX is also bringing new tasks for the state, from geo-economic strategies to protect Japan’s global production networks, to education, retraining, and intellectual property protection.

We begin, in Section 2, with an introduction of definitions, examples, and basic data on the DX and demographic change. Section 3 offers context with a succinct summary of Japan’s post-WWII political economy, as needed to appreciate the transformations analyzed in this Element. Sections 4, 5, and 6 look into the actual DX that is underway, by presenting detailed case studies on evolving business strategies, employment patterns, and state policies. Each section presents examples of how the DX has already impacted Japan. Section 7 concludes that the “lucky moment” gives each of the three pillars of Japan’s political economy a push toward finding a new identity. Whether Japan will be successful is unknown at the time of this writing. Most likely, mistakes will be made, strategies will get thwarted, and losers will suffer. But good or bad, Japan’s experience will soon repeat across parts of Asia, followed by Europe. How Japan prepares, and how we can best analyze and assess Japan’s progress, will be meaningful for many other countries.

2 Definitions: The Digital Transformation (DX) and Demographic Change

This section introduces the core concepts we will discuss, to set up the case studies of ongoing change and transformation. To illustrate the ground-shifting impact of the DX, we begin with a glimpse into the future of the automobile industry, which is morphing from a manufacturing into a “mobility-as-a-service” (MaaS) business. We then present our argument for why the DX is inescapable, an analysis of what the DX means for Japanese business, and data on demographic change in Japan.

2.1 Vignette: The Automobile Industry of the Future

Imagine it is the year 2030. Like most other people, you no longer own a car. Instead, your transportation needs are filled through a monthly subscription service, similar to how Spotify or Netflix answers your audio-visual entertainment needs today. For a monthly fee, you are assured the provision of just-in-time mobility services. When you need to go somewhere, your phone presents you with a menu of transportation modes. Your choices may include a self-flying automobile for a short hopper, or a car that is parked in your immediate vicinity and will arrive promptly. This could be either electric, solar, or hydrogen-powered. It will be self-driving, and quietly and expeditiously take you to your destination.

If you think that 2030 is too soon for this utopian scenario to materialize, note that some of these options already exist, such as the German corporate car-sharing company fleetster, or Zipcar in the United States. In fact, the Toyota Motor Corporation – the world’s largest auto maker in 2022 – expects all of this to materialize much sooner. In 2019, Toyota launched “KINTO,” a subscription service car company, as well as “Toyota Share,” a car-sharing service.Footnote 8 In April 2021, Toyota acquired Lyft’s self-driving unit, to enhance its existing “e-Palette,” a self-driving, battery-powered electric small bus that was launched to transport athletes and visitors to and from venues during the 2020–1 Tokyo Olympics.Footnote 9 Earlier, in 2017, Toyota had invested $400 million in a group of Tokyo-based Japanese engineers who were moonlighting on a flying car project. In August 2020, their company, SkyDrive, Inc. made its first safe “test fly” in Aichi Prefecture with a three-wheeled drone that can carry one person. Of over 100 global flying car projects at the time, SkyDrive was one of only a few to take off and land safely.Footnote 10 To double down on its bets on the flying car, in 2020 Toyota invested another $400 million in Joby Aviation, a California-based startup company. Its eVTOL (electric, vertical take-off and landing) machine looks like a small helicopter but with six horizonal rotators.

These efforts are all in pursuit of a new corporate vision for Toyota to become the world’s leading MaaS provider. Toyota aims to dominate an industry that will morph automobile manufacturers into transportation operators of electric, self-driving vehicles and drones. This will represent a complete identity change for Toyota as a company. In the 2010s, Toyota earned annual revenues of about $250 billion by selling roughly nine million cars globally. Now, Toyota envisions a future where it no longer sells cars at all.Footnote 11 It may still make cars, flying and otherwise, but they will constitute the Toyota rental fleet that offers on-demand transportation and other services.

Traditionally, car companies have been designers and assemblers that oversee a large supply chain of part makers. The assembly process is complicated and characterized by significant economies of scale (Reference Womack, Jones and RoosWomack et al. 1990). As we will see in more detail in Section 4, “industry 4.0” now brings a shift to digital manufacturing that dramatically alters the logic and economics of production. In addition, in this shift to MaaS the design and product characteristics of a “car” are also turned upside down. Traditionally, car companies have competed with style, design, and engineering, all on a spectrum ranging from high-quality workmanship to low-price affordability. But in a future with no personal ownership, markers such as status, brand, looks, or engine (or motor) size will soon be irrelevant. Instead, going forward, the vehicle itself will become standardized and commoditized. This will be necessary in order to strip it of any idiosyncratic complications and make it as user-friendly and interchangeable as possible for the shared economy.

Add to this “servitization,” that is, the creation of business models based on revenue generation from subscriptions and other platform offerings. Until now, car maker services have consisted of leasing and repair services offered through dealerships. These were often seen as a necessary by-product of the core business of manufacturing.Footnote 12 Going forward, transportation services will be the new core business, and add-on service offerings will provide differentiation from competitors. Such offerings may include in-vehicle entertainment options, well-being programs, concierge and shopping services, and of course, user data collection.Footnote 13 Winners in the MaaS business competition will be those that offer the most immediate, reliable, and comfortable mobility solutions, at the best price. They will grow revenues with larger market share, which increases user data collection, which can be used or sold to marketing firms. That is, success will depend on how much traffic – literally and figuratively – the MaaS provider can attract to their platform.

Servitization will also bring a new meaning to the profession of the “car worker,” which is shifting from a factory to a desk job. Employees of MaaS companies will have assignments ranging from IT and advanced operations management to logistics, mapping and data solutions, and designing and managing third-party offerings and alliances. Japan’s shrinking workforce helps in this transition, as the labor shortage is already causing factory work problems. We will see in Section 5 how large companies are rolling out programs to “reskill” their existing office and shopfloor workforce. For younger workers, the government has launched an education reform, including the redesign of high school curricula as well as university course offerings to prepare the next generation of car workers for platform services jobs. For companies, the shrinking workforce leaves no choice but to retrain existing workers, and this affords Japan as a nation a chance to upgrade the skill level of its entire labor force. It also presents an opportunity to funnel the top talent into new and innovative assignments with fast-track promotions in ways that do not necessarily undermine the existing lifetime employment system.

The tectonic shifts in business models in Japan’s car industry are but one example. They repeat across industries, as we will see in Sections 4 and 5. Automobiles have long been one of Japan’s largest and most successful industries. Their pivot into a completely new business realm with different profit and employment logics is a harbinger of the changes that are to arrive for Japan’s entire industrial architecture, which is being disrupted at the core.

2.2 What Is the DX?

The DX is much more than a replacement of people with machines. It brings tectonic shifts in economic activity, industrial organization, revenue generation, connectivity, and access to information. This shift is coming about thanks to recent rapid advances in technology, especially in data collection through connectivity, storage capacity, and computing powers. DX technologies are divided into hardware and software. The hardware infrastructure consists of advanced communication (5G), sensors and vision technologies, embedded communication tools in all buildings, systems, parts, and machines (the IoT, “internet-of-things”), edge computing devices (on-site data governance), and “the cloud” (data center governance). These new hardware capabilities in turn have triggered great advances on the software side, namely in the collection and analysis of data, including unstructured data such as video. The tools developed for “mining” (deciphering, sorting, analyzing) these scrambled data are labelled artificial intelligence and machine learning (AI/ML). In combination, these technologies disrupt how economies are structured, industries organized, companies compete, governments rule, and people work and communicate (METI 2017, 2018b, 2020b; Reference Kimura and NumataKimura and Numata 2018).

Despite the constant news coverage on these developments, as of 2022, many still wondered how soon the DX would truly arrive, and to what extent people would resist the intrusions into privacy that these shifts will mandate. Indeed, there were still few use cases to prove the superiority, or even basic utility, of some of these advances, such as bitcoin, blockchain, or flying cars. Some even claimed that AI did not yet exist beyond some basic levels of visual pattern recognition, or that as a matter of personal daily-life experience, infrastructure was not nearly advanced enough to even allow ubiquitous access to the internet. Inadequate cybersecurity was also becoming a major concern.

Yet, from the perspective of policymakers and strategy planners, in the public and private sectors, the DX is already a force to be reckoned with. It will arrive with certainty, sooner rather than later. Nearly all policymakers, around the world, have realized that they cannot afford to postpone preparations for a future that is sure to arrive and needs to be shaped to serve the national, societal, economic, and human interest. The DX has three salient features that make it a critical juncture for all countries, and will touch all actors and institutions of a political economy:

1) Speed and volume of information exchange. Whereas it used to take several weeks, days, hours, or minutes to transfer a few words across the world, information is now shared instantaneously. The volume of information transmittals is growing rapidly. Inventions spread faster and are adopted more rapidly. This can be exploited for good and sinister purposes, with potential for huge advances or conflict. For any domestic political economy, the arrival of the DX means that policy decisions can no longer rely on using “time” either as a competitive advantage or a regulatory delay to allow slow adjustments.

2) Ubiquity. The “internet-of-things” (IoT) means that every single thing, every machine, every input part, every household item, and every person – and even every pet – is constantly connected to everything else, generating volumes of data along the way. What seemed to be a science fiction movie just a few years ago is now reality; in this new world, a smart watch can talk to a refrigerator to learn the expiration of the milk. There is no escaping this new interconnectivity, and no policy or strategy can be meaningfully upheld outside IoT.

3) Borderless reach. Breakthrough innovation used to be clustered in innovation ecosystems, such as California’s Silicon Valley, where colocation of inventors, universities, and financiers facilitated the cross-fertilization of ideas. The DX means that access to latest advances and collaboration are shifting to the digital and transcend country borders easily. The COVID-19 pandemic has shown that geographic barriers to knowledge access can be overcome. Meanwhile, the globalization of value chains and the expansion of corporate global production networks, with complicated paths of transfer pricing, knowledge sharing, and supply chain management, all mean that the nature of competition is turning truly transnational. There will be winners and losers to the DX in all countries, and no state or business can withdraw from this new reality. For the state, this means that the benefits of domestic policy measures are easily diluted, and the nature of industrial policy needs to change if it is to support companies in this new global competition.

To remain relevant in this new fast, ubiquitous, borderless connectivity, businesses need new competitive strategies and skill formation processes, people must negotiate and adjust to new paradigms of work and private life, and governments need new policy designs. The COVID-19 pandemic accelerated these processes by forcing telework and related new technologies onto society. Fresh possibilities of interactions have been introduced, and existing patterns of communications challenged. In Japan, the high reliance on fax machines and personal signature stamps (the hanko) caused significant consternation and necessitated lockdown violations, while the United States rolled out vaccinations without the ability to track them in an online registry. Both caused chaos in different ways and highlighted the real implications of the VUCA world when practices and policies remain stagnant.

2.3 The DX and Business: Industry 4.0

For business, “industry 4.0” brings the advent of digital manufacturing, which will change not only the conceptualization of the shopfloor and operations management, but also the economics of efficiency. Digitization enables single-unit production and undermines the concept of economies of scale, and robotics will change the skill requirements for factory workers, as the future shopfloor foremen will mostly oversee the execution of computer programs. At the company level, the DX requires adjusting to the evolving global competition with a new vision and compelling strategy, as well as business models that exploit the emergence of new markets and forms of consumption. Many of Japan’s leading companies stand to benefit from the DX, given their long-standing strengths in manufacturing technologies as well as “deep-tech.” This term was coined in the 2010s in venture capital circles, to distinguish “shallow-tech” inventions such as mobile apps, websites, and e-commerce services from more deep-seated, radical, and disruptive innovations. Deep-tech breakthroughs require more time, and often address big societal and environmental challenges.Footnote 14

2.3.1 Deep-Tech Japan

The most prominent deep-tech fields in the DX include advanced materials, advanced manufacturing, artificial intelligence, biotechnology, robotics, photonics, electronics, and quantum computing. Global private investment in young companies working in those fields increased more than 20 percent a year from 2015 and reached almost $18 billion in the year 2018 alone. Large companies, including in Japan, are investing magnitudes more in R&D and acquisitions of cutting-edge technologies (BCG 2019).

To assess Japan’s global competitiveness, Japan’s Ministry of Economy, Trade and Industry (METI) has tracked market shares by Japanese companies in global deep-tech markets. A first study, in 2003, showed that many Japanese companies had relinquished market shares in global consumer end products, such as in electronics or household goods. But rather than a defeat, this can be viewed as a successful strategic pivot into deep tech. Reference SchaedeSchaede (2020) argues that this shift has enabled leading Japanese companies to focus on difficult-to-make, difficult-to-imitate technologies and thus compete against rising competitors in East Asia, in particular South Korea and China. It works because profit margins are much higher in upstream deep-tech areas: As long as the Japanese companies do not stand still, they can sustain the high costs of technological innovation needed to stay ahead in the global competition. What is more, this specialized focus on innovating in upstream deep-tech segments makes Japan a key technology player in the DX just as the DX is redefining the logic of production.

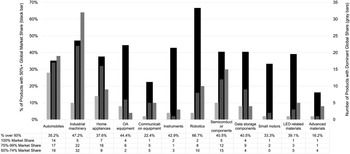

METI has since continued to collect market share data for a growing set of Japanese industries, from sensors needed for robotics, fine chemicals for electronics, and advanced materials to AI technologies and flying cars (NEDO 2018). These survey data underscore that some of Japan’s largest companies are global technology leaders in many important input materials and components. Figure 2 offers a snapshot of the breadth and depth of Japan’s competitiveness, from car parts and medicine to advanced materials and components for electronics. The black bars (left-hand scale) show the estimated combined market share of Japanese companies in that product category or industry, in percent. The gray bars (right-hand scale) are a visual presentation of the bottom legend rows. Overall, in this assessment of 1,217 product categories in 2017, Japanese companies combined to global market shares of over 50 percent in 309 categories (medium gray bars), and they held over 75 percent (dark gray) in another 112 products, and 100 percent in 57 products (light gray). In total, this added up to 478 products with dominant Japanese technology positions. Specifically, in 2017, Japanese companies dominated 66.7 percent of the input technologies needed for robotics, 47.2 percent for industrial machinery, 44.4 percent for office automation equipment, and 40.5 percent for semiconductors. Even though the end product may no longer carry a Japanese brand name, Japanese companies are important suppliers of the technologies that power these products.

Figure 2 Examples of combined world market shares by Japanese companies in 2017

The METI data are based on surveys and do not cover all industries, nor were those industry segments randomly selected. Thus, they represent just a snapshot and a lower boundary of the new shape and impact of Japan’s competitiveness. The impression created here is supported by other studies. For example, a 2019 US study of industrial robotics and machine vision technologies confirmed that Japan’s world market share exceeded 50 percent (compared to 30 percent in 2016). Competitors in this space included large firms (e.g., Denso, Epson, FANUC, and Kawasaki) as well as Japanese startup companies, such as Tokyo-based Connected Robotics, AI-company Preferred Networks, Paro Theropeutics, and Mujin, an industrial picking and sorting robotics company.Footnote 15 Overall, the message is becoming increasingly clear that a focus on end product market shares or brand names leads to a great underestimation of Japan’s economic and deep-technology contribution to the world economy (Reference SolísSolís 2020).

2.3.2 The 2025 “Digital Cliff”

The fortuitous timing of the DX for Japan’s political economy is also forcing change in an area where Japanese companies have come to be seen as pathetic laggards, namely: in software and the IT systems that run corporate Japan (e.g., Reference Cole and NakataCole and Nakata 2014). In the early 2020s, most Japanese companies were facing a “digital cliff,” that is, a tremendous challenge in their utterly obsolete corporate IT systems, both hardware and software that run operations ranging from supply chain and sales management to human resource management, finance, and corporate e-mail. In 2018, METI published a first report on this cliff, which estimated that by the year 2025, 60 percent of mission-critical IT systems in corporate Japan will be so outdated as to be useless. The report also assessed that by 2025 Japan will need 430,000 additional IT specialists, and if no action is taken, this digital dilemma will cause economic losses of ¥12 trillion (roughly $120 billion) annually, or 2 percent of Japan’s total GDP (METI 2018a, 2020b).

These deficiencies may come as a surprise: after all, were Japanese companies not at the forefront of IT in the 1980s? This is in fact the answer to the “digital cliff” puzzle: corporate Japan’s IT infrastructure is now so outdated precisely because it was cutting-edge four decades ago. In the 1980s and 1990s, Japan was celebrated as the world leader in communication equipment, ICT/ IT, and a numerical controls and mechatronics powerhouse (e.g., Reference Prahalad and HamelPrahalad and Hamel 1990). This leadership was deployed within Japan’s traditional industry architecture of long-term vendor relations anchored on business groups. Almost all companies (as well as the government) outsourced their IT systems to one exclusive external vendor who built a highly tailored, customized system for each of their large clients. These company-specific software systems were installed on-premises, on customized mainframe computers. Over time, hardware and software were occasionally updated, becoming progressively more bloated, complicated, and outdated. Running on Windows 7 or even older, they were tied to ageing mainframes for which semiconductor firms no longer produced legacy chips. Due to the customized design, these systems could not be scaled or updated. And since the client companies typically did not view IT as strategically important, and managers were rotated through the IT division on regular intervals, companies eventually no longer understood their own systems. IT had turned into a “black box” (METI 2018a).

This situation poses a huge challenge for companies. Maintaining their idiosyncratic legacy systems eats up most of the IT budget, leaving little room for innovation. Nor can they attract young IT specialists, as no capable programmer would want to work on such antiquated systems. And, due to their ancient code, the legacy systems cannot be transferred or transposed to a current mainframe or into the cloud. METI blew the whistle in 2018, over growing concerns that even the country’s largest banks and manufacturing firms were about to fall off this digital cliff as early as 2025 (Reference NishiyamaNishiyama 2021).

Perhaps ironically, the digital cliff offers yet another fortuitous window of opportunity for corporate Japan. Japanese companies must rebuild their entire IT infrastructure from scratch, just at a time when the DX is bringing new capabilities and cloud-based systems. New open-source and scalable IT infrastructures are likely to present corporate Japan with a new advantage, as it can leapfrog competitors who installed their systems a decade ago. It also provides an opportunity for Japanese vendors – including industry leaders NTT Data, Hitachi, Fujitsu, and NEC but also a fast-growing corps of smaller independent providers – to revise their own business models. Instead of being confined by long-standing business group obligations that dictated customized solutions, these vendors now have an opportunity for more aggressive globally competitive positioning in the AI/ML era. As with other aspects of the DX, not all Japanese companies will survive the digital cliff. But those that do will then operate on a spick-and-span, up-to-date IT infrastructure.

2.4 The DX and People: Society 5.0

For the changes the DX is bringing for people, Japan’s government has coined the phrase “society 5.0,” defined as “a human-centered society that balances economic advancement with the resolution of social problems by a system that highly integrates cyberspace and physical space.”Footnote 16 This refers to a new governance of society through constant connectivity and a revised definition of space and activity, from transportation modes to work styles (telework), health services (intelligent houses equipped with medical devices that send constant data to doctors for telemedicine), and fintech and blockchain (basing financial decisions on automated algorithms and enabling even large transactions in milliseconds). Of course, these innovations also raise major concerns, including privacy, personal record-keeping, and personalized medicine, as well as the future of jobs, learning, and skill formation.Footnote 17

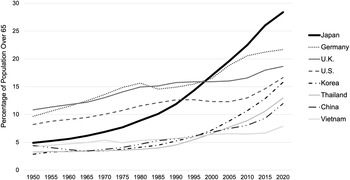

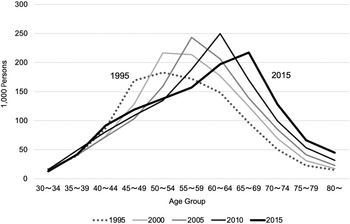

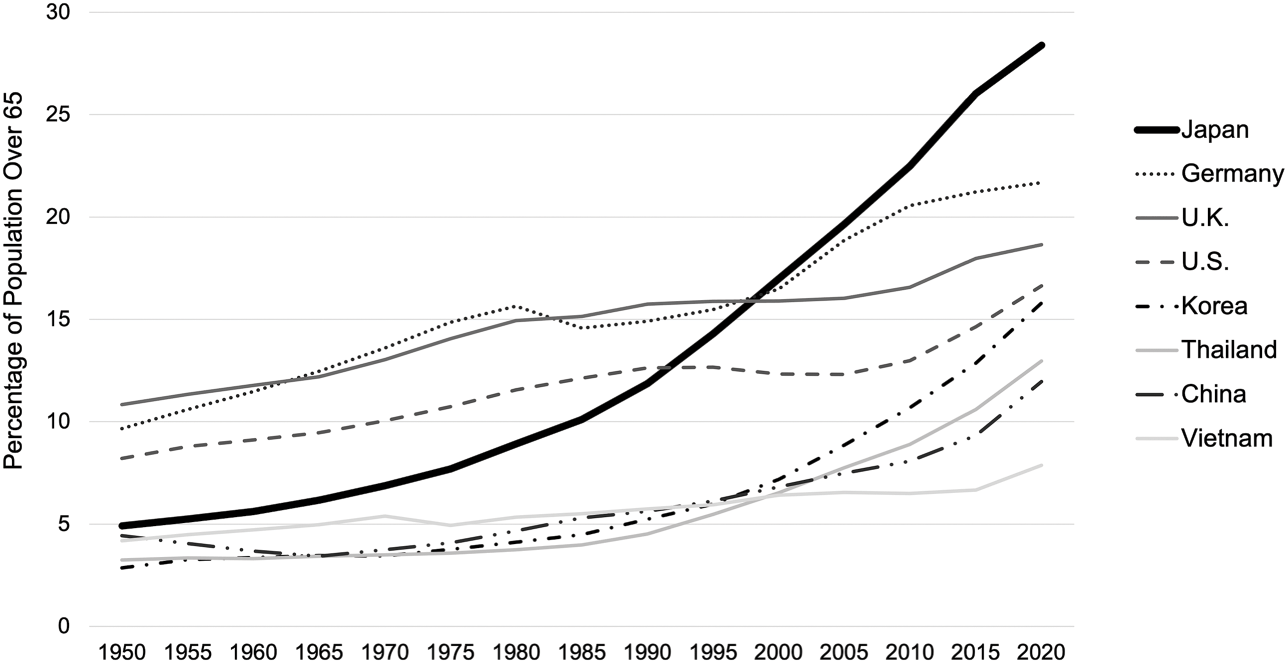

Society 5.0 is being rolled out before the rapidly changing demographic composition of Japan. Japan is the first industrialized country to experience both a rapidly ageing and shrinking society. Figure 3 shows that in 2020, 29 percent of Japan’s population was over sixty-five years old, and this ratio is projected to reach 33 percent by 2035. This far exceeds any other country, as Japan ranks ahead of Germany, the United Kingdom, the United States, and South Korea, not only in the absolute level but also in the slope of the trajectory (Cabinet Office 2020a).

Figure 3 Ratio of population over sixty-five years old, various countries

Note: Legend is arranged in order of country ranking in 2020.

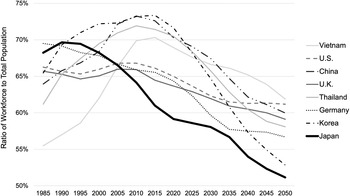

In addition to getting older, Japan’s population is shrinking, due to a rising death rate and a fertility rate that has hovered at around 1.4 since 2005.Footnote 18 Assuming no drastic changes in fertility rates or immigration policies, Japan will remain a leader also in the shrinking workforce category, ahead of South Korea, Germany, and Thailand. Figure 4 shows a projection through 2050, visualizing that Japan’s workforce is predicted to shrink by at least 20 percent over the next two decades, from the current sixty-five million people in 2017 to fifty-two million by 2040.

Together, these trends mean that Japan’s “old-age dependency ratio,” which measures the number of people aged sixty-five and older per 100 people of working age, is higher than in any other OECD country. Just thirty years ago, in 1990, Japan ranked below OECD average with about 15 percent; in 2020, Japan topped the OECD with 50 percent, and is forecast to reach 80 percent by 2050 (OECD 2021). Within Japan, research on the future of society prepares for 2050, when the population is forecast to dip below 100 million (e.g., MRI 2021). This watershed is seen to exacerbate current trends of increased social dependency, falling productive potential, and an unsustainable domestic economy.

However, demographic change also brings novel opportunities, especially in combination with the tectonic shifts of the DX. Certainly, the DX is about to wipe out many traditional industries and jobs. For example, blockchain, logistics advances, and e-commerce are bringing a disruption that makes Japan’s outmoded, multilayered wholesaling system superfluous. Fintech will eventually replace the physical bank, and with it the position of the bank teller. Agrotech is beginning to encroach on the old-fashioned tilling of farmland. But in Japan all of this is happening as wholesalers and farmers are, on average, sixty-eight years old and face difficulties finding successors, while local banks struggle to find business, and are about to be phased out (see Sections 4 and 5 for in-depth case studies). Thus, these sectors are poised for disruption just when the DX offers new solutions to provide and upgrade their economic functions and services.

The quantitative shift is only one aspect of Japan’s demographic change. Qualitatively, too, Japan’s workforce is undergoing a transformation, in terms of workstyle change, employment expectations, and skill specialization. A growing portion of Japan’s next-gen workforce, and in particular the highly trained top talent, are displaying a different attitude in regard to work–life balance, the meaning of work, and the rights of employees vis-à-vis employers and coworkers, as well as meritocracy, individualized career planning, and upward mobility. To them, the lockstep promotions of the lifetime employment system (see Section 3) no longer seem attractive, and the looming shortage of such talent is increasing their bargaining power. They demand meaningful work content, and if unsatisfied, they are likely to explore new opportunities elsewhere.Footnote 19 In 2019, the government passed an encompassing “Workstyle Reform” law (hatarakikata-kaikaku hō) that specifically facilitates mid-career job-changing and greater employment flexibility.

The DX also brings the need to reskill the existing workforce. With a shrinking workforce and continuing limitations on immigration, most companies will have to retrain their own employees to adjust to the technology shifts of the DX. As we will show in Section 5, Japan’s youth score very highly in global math and science comparisons (OECD 2021), but education lags in workforce preparation. As such, the government has launched education reforms that address concerns that the country’s education system is behind in basic computer skills, to prepare the future workforce for the DX.

These undercurrents for qualitative change in society gained high velocity with the 2020 onset of the COVID-19 pandemic. The sudden need to switch to distance learning as well as working-from-home not only boosted communication technologies and human acceptance of new modes of interaction. It also highlighted the deficiencies in Japan’s education and office technology systems, forcing companies to make adjustments for at-home use of a work computer, the availability of VPN networks, and the role of printed documents and in-person deliveries in daily business. Perhaps most importantly, it further reframed the next-gen employee’s mindset of what it means to work effectively and efficiently, and how they would like to structure their relationship with their employer.

These changes in business and demographics coalesce into a demand for a new role of the state. For example, rising labor mobility makes it uneconomical for companies to carry the responsibility for training the young, increasing the role of government to redesign, provide, and coordinate that service. Because the DX is fast, ubiquitous, and borderless, returns to capital are rising, as may inequalities. As the speed of change increases, the government needs to emphasize its role as a social protector. As we will recap in the next section, Japan’s post-WWII political economy represented a canonical framework where employees got lifetime employment, companies got loyal employees and government protection, and the government got to coordinate and pick winners to maximize economic growth. The DX and demographic change have destabilized this quid pro quo. While it is not yet clear what the future may bring, the rights and responsibilities of business, people, and the state – that is to say, Japan’s political economy – are evolving.

3 Context: Japan’s Political Economy in the Post-WWII Era

To place our argument into context, we review here the main institutions of Japan’s political economy of the post-WWII era. Our focus is on the quid pro quo between government, business, and people (in their role as workers), and the goals and coordination mechanisms of the government in spurring economic growth. In what was called the “developmental state” (Reference JohnsonJohnson 1982), the state designed a variety of mechanisms to coordinate industrial activity, guide technology imports, and streamline innovation. The state maintained this power by ensuring that almost all were compensated, including would-be losers. This worked as long as the pie was growing rapidly; as such, we also review the system’s collapse in the 1990s, as the collapse after the bubble economy combined with the impact of deregulation to destabilize the postwar deal. The DX now brings an inflection point for the entire political economy as the core logic of the former quid pro quo no longer works for either state, business, or employees.Footnote 20

3.1 Fast Economic Growth, 1950–1980s

After the severe losses in WWII, Japan as a nation sought to rebuild. The postwar economic recovery began with the export of basic supplies such as blankets to US troops during the Korean War (1950–1953). This brought the insight that the path to economic prosperity would depend on the successful commercialization of cutting-edge technologies. Japan’s process of “catching up” could be accelerated if Japan could import foreign technologies, use them to design and manufacture new commercialized uses and consumer products, and then export these products into world markets. The higher Japan’s value added in the design and manufacturing stages, the more foreign reserves were earned, with which more technologies could be imported, thus creating a virtuous cycle.

The critical elements in the upgrading cycle were the design of attractive commercial applications, continuous learning and improvement of manufacturing skills, and steep increases in product quality. Over time, this resulted in a core competence in monozukuri, “the art of making things,” that is, the ability to manufacture large quantities of complicated products and materials with consistently high quality at high yields. Manufacturing companies extended their knowhow upstream to their suppliers, thus nurturing entire industry value chains domestically.

The government saw its role in accelerating this process through “industrial policy” (sangyō seisaku). This referred to the streamlining of development by way of coordinating industries and investments, fostering innovation and learning, and reducing duplicative effort and even competition, which were seen as potentially wasteful. The government rank-ordered industries and companies by relevance for the country’s growth, and the cognizant ministries then designed roadmaps, including in terms of access to foreign technologies, subsidies and tax incentives, and export promotion schemes. In charge of manufacturing and therefore the most prominent ministry in this growth guidance was METI, the Ministry of Economy Trade and Industry (until 2001 named MITI, Ministry of International Trade and Industry).

The main purpose of industrial policy was to protect domestic infant industries to help them grow, and to promote exports in order to earn the foreign reserves needed for industrial upgrading. Domestically, companies were expected to grow in lockstep through “competitive convergence,” that is, the large companies in most industries were incentivized to diversify in very similar ways, and over time very stable corporate hierarchies emerged (Porter, Takeuchi, and Sakakibara 1991). This stability facilitated the government’s coordination efforts. For example, when Hitachi entered the nuclear power business, Toshiba followed suit. When Nikon developed a new camera technology, so did Canon. Corporate success was measured in terms of size and market share, and the largest companies had priority access to government promotions.

Export expansion was supported by allowing companies to adopt a “sanctuary strategy,” whereby domestic price agreements allowed for higher profit margins that could then be used for aggressive pricing in foreign markets. The government allowed price coordination by exempting many industries from antitrust statutes, as well as enforcing rules fairly leniently (Reference SchaedeSchaede 2000, Reference Schaede2004). This oriented companies to compete in domestic markets through fast product improvements and customer relations, to justify high prices. Over time, Japan came to be known for super-high product quality, fast product life cycles, and excellent service. This was helpful in foreign markets as well, but there, competition was also based on price. Thus, companies used the domestic markets as a profit sanctuary, through retail price maintenance and other restrictive agreements such as exclusive retail chains. These profits were then used to sell at razor-thin margins into foreign markets, with the goal to capture global market share.Footnote 21

The government’s powers in coordinating industry rested on a large number of special laws. Some of these were industry-specific (e.g., steel industry law, communications industry law, large-scale retail law), while others were encompassing, such as the “Foreign exchange and foreign trade law” (FEFTL, Gaitamehō, in short) of 1949. This law imposed restrictions on cross-border financial flows, which empowered METI (MITI at that time) to limit foreign investments into Japan and monitor the outflow of foreign reserves. The ministries used these laws to protect, incentivize, and guide industry leaders through a “carrot-and-stick” mechanism.

A second coordination lever was extensive financial regulation. A restriction on the use of bond and stock markets channeled most of corporate finance through bank loans. The 1949 “Temporary interest rate adjustment law” (TIRAL) tied most interest rates to the central bank’s base rate, which enabled the government to guide the price for bank loans. Most of the time, this was used to keep the cost of borrowing low, in order to encourage private investment. This created excess demand for bank loans. The Bank of Japan, Japan’s central bank, then employed tools of “window guidance,” which referred to regular conversations with the largest banks, to nudge bankers to extend loans to the desired growth sectors and leading companies.

The champion industries evolved over time. Initially, great successes were scored in establishing fast-growing steel and shipbuilding industries, as well as chemicals and processing (e.g., refineries, rubber, ceramics, and pharmaceuticals) and heavy electric machinery (such as turbines, generators, and power plants). The 1973 “oil shocks” (OPEC price cartel), subsequent sharp increases in energy prices, and an environmental crisis required a pivot toward less energy-intensive, less polluting, high-technology sectors, including automobiles, electronics, precision machinery, and semiconductors.

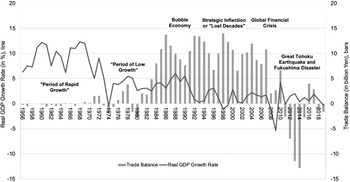

Figure 5 shows the annual GDP growth rate (solid line, left-hand scale, in percent) and Japan’s growing trade surplus (in bars, right-hand scale) from 1956 to 2019. The two decades of the early 1950s to 1973 were labeled the “period of rapid growth,” when Japan recorded an average annual GDP growth rate of 10 percent, similar to China fifty years later. This growth rate halved after the “oil shocks,” to an average of 5 percent. These successes also made Japan a trading nation: Beginning in the 1980s, the export push led to fast-growing trade surplus (vertical bars), and more than half of that trade was directed to the United States (Reference SolísSolís 2017).

Figure 5 Japan’s GDP growth and trade balance, 1956–2019

Note: Constructed with data from Cabinet Office of Japan (GDP) and Japan Ministry of Finance (trade)Footnote 22

By the 1980s, Japan’s successes had resulted in a growing trade imbalance with the United States. This led the US government to launch a trade war to gain concessions for market access, deregulation, and voluntary export restraints. Trade negotiations lasted over a decade and turned increasingly acrimonious. By the mid-1990s, Japan had agreed to remove import barriers and trade controls; abolish restrictive financial regulation; remove most of the special industry laws; open the retail markets; and introduce more transparency into its policymaking processes. But over time, these measures also eroded the government’s levers in choreographing companies and industries (see Section 6). Overall, Japan’s postwar system is generally seen as successful in ensuring fast economic growth, before the country lost its bearing in the 1990s, after the collapse of the bubble economy and the arrival of competition, especially from within Northeast Asia.

3.2 The Quid Pro Quo of Postwar Industrial Policy

Japan’s postwar political economy was anchored on a social contract that is now under siege for having become too inflexible and too constraining. This tacit quid pro quo laid out the expected roles, rights, and responsibilities of the state, companies, and workers. The state’s role was to enable speedy development by offering support to companies, ranging from low costs of borrowing to tax policies, subsidies, investment insurance schemes, and rescues in times of trouble. In turn, the state delegated a large portion of worker welfare to the large companies, in particular through offering stable, lifetime employment and benefits such as pensions. Corporate welfare was also extended to the many subcontractor hierarchies of these large firms. While expensive, companies could afford this assignment because corporate success was assessed by size, not profits (Reference SchaedeSchaede 2008). Over time, society came to expect that employment was a main component of corporate social responsibility (CSR) in Japan. Employees, for their part, were assured of stable jobs, steadily rising income, and stability. In turn, however, they had to trade in their rights to individual career planning as well as location and content of work, as the company could assign them to new rotations at will.

This setup allowed the government to greatly economize on social security, and those savings could be funneled not only into growth policies and infrastructure investments, but also into redistribution and the support of small firms outside the corporate network hierarchies, such as the services sectors and farmers (Reference CalderCalder 1988; Reference Estevez-AbeEstevez-Abe 2008; Reference MiuraMiura 2012). To this day, a large portion of Japan’s social welfare is predicated on keeping companies in business, by offering tax breaks, subsidized bank loans, and other disbursements to small firms.

3.2.1 Business: Stability through Networks

This system created incentives and constraints for senior managers of large Japanese companies (for brevity, referred to here as “CEO,” by which is meant the top managerial team) that were quite different from other countries. The key success metrics, in the eyes of the government and society, were growing sales and employment. Responsibility for lifetime employment and pensions meant that CEOs always kept an eye on stability and the company’s longevity. Falling into distress or having to dismiss workers were considered the most egregious failures. In contrast, not being very profitable or having a low stock price were not considered nearly as problematic as long as the company was stable.

The “go-go years” of fast growth in the 1960s and 1970s offered many opportunities for growth, but the wide swings in the business cycle (as seen in Figure 5) also brought instability. And, because financial regulation strictly curtailed the issue of equity or bonds, companies depended on bank loans to finance corporate growth. In the 1970s, the average debt-to-equity ratio for large firms exceeded five, meaning their bank loans were five times the company’s value. Failure to pay interest on these loans could easily topple the entire enterprise.

To reduce the risk of failure, many CEOs adopted a three-pronged approach. First, they continuously diversified into new businesses, including increasingly unrelated segments. At the time, corporate strategy advisers viewed diversification as stabilizing: having businesses with “uncorrelated income streams” under one roof was seen as safe, given that these business units were unlikely to all be hit by a demand shock at the same time. For example, Hitachi Co., Ltd., ended up as a manufacturer of trains, power plants, elevators, semiconductors, hard disk drives, refrigerators, chemicals, metals, and medical devices, among others. Nippon Steel ventured into amusement parks and semiconductors. Of course, adding more businesses also helped growing sales and employment. It also made the company “too big to fail”; that is, should it fall into distress it would need to be rescued to avoid large-scale unemployment and huge loan write-offs. Over time, however, this created huge conglomerates that became increasingly difficult to manage.

The second risk-reduction strategy was to join a business group (keiretsu) with stable, long-term trade relations cemented by cross-shareholdings. Many of these groups were vertical and included all core contributors to a product’s supply chain. Lying on top of those vertical groups were six large, horizontal groups, which included roughly 200 of the largest Japanese firms as core members, and indirectly all their subsidiaries and suppliers. These groups formed mutual insurance schemes, by way of a tacit agreement that they all would be stable shareholders of each other, as well as trading partners that offered mutual support through purchases or trade credit during downswings. The cross-shareholdings also insulated companies from hostile takeovers, and corporate governance was left in the hands of internal executive managers and the main bank, while the shareholders were mostly group companies who were typically loyal and did not interfere with management (Reference Lincoln and GerlachLincoln and Gerlach 2004).

The third system stabilizer was the “main bank.” Each of the six horizontal groups included a lead bank, which was the main provider of banking services and loans to all business group members and their affiliates. The main bank was also the “lender of last resort,” in charge of rescuing group firms that fell into distress (Reference Aoki and PatrickAoki and Patrick 1994; Reference Hoshi and KashyapHoshi and Kashyap 2001; Reference Ito and HoshiIto and Hoshi 2021). These tight intercorporate relationships helped spread the risk of bankruptcy across the horizontal business group. It also incentivized CEOs to heed long-term planning and collaboration in the domestic market. This system worked remarkably well: in the period between 1960 and 1990, fewer than 100 large, listed Japanese companies failed.

The biggest growth engine was to sell into foreign markets, and by far the largest and most attractive was the United States. Initially, the dominant strategy was to export made-in-Japan products through global sales offices, which were run as satellites with highly ethnocentric hiring practices, that is, all senior managers were Japanese, assigned to uphold headquarter culture around the globe. This focus on exports meant that domestic industrial policies were effective in also choreographing Japan’s global business expansion beginning in the 1960s. It was only in response to the US–Japan trade war of the 1980s that Japanese companies began to build production plants around the world, to comply with local content rules.

Over time, US business executives and trade negotiators used the term “Japan Inc.” to describe the thicket of intercorporate networks. The stable industry hierarchies facilitated industry policy, as it enabled repeated interaction and long-term reciprocal relations. But the system was still a market economy, and it allowed for mavericks and entrepreneurs. Even if not part of the master plan, underdogs could win and were often celebrated. Honda, Sony, Sharp, Nidec, Orix, all found ways to move up the ladder, and many suppliers managed to outgrow their roles, such as FANUC, Bridgestone, Denso, Nidec, and Hoya. An important route was their foreign successes. For example, Honda grew through motorbikes in Europe, while Sony captured the world with its transistor radio even before it earned respect within Japan. Thus, the domestic policy coordination was neither binding nor airtight, and it was counterbalanced by fierce competition abroad.

3.2.2 People: Lifetime Employment and Corporate Skill Formation

The Japanese people participated in the political economy quid pro quo in their roles as households, consumers and, of special interest here, workers. In post-WWII Japan, an estimated 75 percent of employees were in open-ended (“lifetime”) positions, meaning they enjoyed job security, predictable promotions, and steady salary raises based on seniority, as well as on-the-job training and skill formation.Footnote 23 In return for this stability, they relinquished the right to determine their use of time, career path, and work location. This was necessary in a no-layoff system, so that the company had the flexibility to assign employees wherever needed. Regular employees were trained as generalists, promoted through the various corporate divisions, and assigned to divisions as needed. This resulted in job rotations abroad and overtime demands without regard to a worker’s family situation or preferences, in ways that would have caused resistance in other countries. In the early decades, the trade-off was good for employees who valued stability above everything else (Reference Abegglen and George JrAbegglen and Stalk 1985). Over time, however, the system ossified, and when growth slowed in the 1990s, many employees were caught in a long-term struggle to find meaning in their jobs. The image of the “salaryman” as a hard-working, sometimes soulless soldier without agency became the fodder of movies and novels.

In the postwar system, companies assumed responsibility for employee training. While universities provided general education, corporate training provided applied skill formation and two-year, on-the-job training rotations. This resulted in a workforce deeply steeped in the operations of the company, but with few transferrable skills. Except for specialized engineers, the job market for mid-career employees was almost nonexistent. Society came to view job-changing as a failure, and there were few chances for upward mobility.

To this day, Japanese CEOs are usually promoted from within, working their way up through the rotations. A study of the late 1990s showed that 82 percent of senior managers in Japan had never worked for another company, compared with 28 percent in Germany and 19 percent in the United States; moreover, in the early 2000s, only 4 percent of Japanese CEOs were hired from the outside, compared to 20 percent in the United States and 25 percent in Europe and Asia (Reference WaldenbergerWaldenberger 2013).

The encrusted structures that this employment system created are now seen as Japan’s biggest challenge to compete in the DX. Younger employees are no longer eager to commit to stable employment for security, especially as opportunities abound in a labor shortage. Many salarymen find themselves stuck in companies past their prime, and this is seen as a loss to productivity and innovation. For CEOs, the challenge is how to shift from lockstep promotion and incremental progress to more diverse patterns that support breakthrough innovation, so as to compete with agility at the DX technology frontier. The matter of “corporate culture change” emerged as one of the management buzzwords around 2020.

3.2.3 The State: Coordination and the Elite Bureaucracy

In the catenation of industrial policy, the core government actors were not the politicians but the bureaucrats in the large ministries, in particular METI (MITI at the time), which orchestrated the guidance and coordination of private investment and production (Reference JohnsonJohnson 1982, Reference Johnson and Woo-Cummings1999). Between the 1950s and 1980s, the Economic Planning Agency issued five-year plans that formulated growth goals. These were neither input plans nor output quotas, but guideposts to pave the way for the next cohort of “winning industries.” But the bureaucrats did not rule by decree. Rather, the plans were negotiated with, and implemented by, the companies through their trade associations. Most policies were issued not as law but through guidelines. Because of the careful curation and industry involvement, there was usually little resistance. The occasional maverick faced ostracism by their peers as well as the ministry, which could prove costly in the long run.

Government–business relations were lubricated through a set of institutions based on interpersonal relations and repeated negotiations. The main channels were a multilayered network of trade associations, implementation through “administrative guidance” and voluntary compliance, and personal connections to ensure constant communication between ministries and individual companies.

Trade associations shaped and sanctioned industry policy directives. They were organized in a hierarchy from small, local, narrowly defined groups all the way up to encompassing umbrella associations to create various layers and platforms for industry representation and policy implementation. Trade associations shared information, coordinated their members, and punished the occasional mavericks. Their self-regulation ranged from collecting and sharing industry data to organizing price agreements (Reference SchaedeSchaede 2000). For the ministry in charge of an industry, this multitiered interest organization offered easy access to, and oversight of, each narrowly defined industry.

For implementation, the ministries often relied on “administrative guidance” (gyōsei-shidō), a type of “moral suasion” or “soft law.” Buy-in was created through inclusion and nudging (i.e., the framing of policy options such that regulatees tend to voluntarily comply with the desired one). Lubricating these negotiations and facilitating the necessary flow of information were personal contacts between companies and their cognizant ministries. At the junior level, this was done through regular meetings between the bureaucrats and designated company employees. Over time, as these employees and bureaucrats were promoted through their organizations, these connections created thick networks of relationships between private sector employees and civil servants.

These connections were extended beyond retirement of the bureaucrats, which began at around age fifty-five. The retiring officials assumed new positions in the private sector, the associations, or other industry-based organization, and formed what was called an “Old Boy network,” with “OB” used as an honorific term for an elder with influence (Reference JohnsonJohnson 1974; Reference CalderCalder 1989; Reference SchaedeSchaede 1995). These personal connections reinforced industry-based linkages, and further added to the “Japan Inc.” image.

At the center of this coordination system was Japan’s elite bureaucracy. Being in a position to draft the growth path for the country was an attractive profession that brought high status and esteem. Japan’s smartest young men (rarely women until the turn of the century) were drawn into civil service. The entrance exam was seen as grueling, which created a superelite staff. The civil servants worked long hours at comparatively low pay, and were rewarded with power, status, as well as the highly lucrative postretirement positions.

The notion that the bureaucrats commanded the industrial policymaking process has been challenged by political scientists who see a larger role for politicians (e.g., Reference HaggardHaggard 2018). Although the details of industrial policy were the purview of ministries, politicians were critical, of course, including in identifying policy measures that would appeal to certain groups of voters, such as farmers, shopkeepers, and other small firms. In the view of Reference CalderCalder (1988), the LDP managed to be reelected and stay in power for almost fifty years, thanks to its careful crafting of “circles of compensation.” While the winners were supported and promoted, the losers were compensated in a myriad of ways, from exemption of antitrust statutes (e.g., retail price maintenance and cartels through small firm cooperatives) to subsidies and government-guaranteed loans even to failing companies.

Over time, the government–business connections and coordination mechanisms ossified. They were eventually viewed as harmful when scandals were revealed after the collapse of the bubble economy. How administrative reforms have evolved will be the topic of Section 6. For the context of our discussion here, the most important feature of the postwar industrial policy is that it was at its core domestic and industry-focused. We will see that the relevance of this type of guidance has been in decline for several decades, and with the DX it is approaching irrelevance.

3.3 The End of Postwar Growth: 1990s–2020

The successes of economic growth culminated in a four-year period of exuberant stock and real estate speculations in the late 1980s, referred to as the “bubble economy.” Stepwise financial deregulation fueled aggressive lending and financial pyramid schemes, as banks, businesses, and bureaucrats lost their compass and engaged in increasingly irrational transactions. When the bubble imploded like a house of cards, it wiped out three times the size of Japan’s GDP at the time in stock and real estate investments alone – a financial disaster of global historical dimensions.Footnote 24

The various ways in which bureaucrats had coordinated industry were now viewed as enabling influence peddling and even corruption. A series of reforms around 1995 curtailed administrative guidance and OB retirements. The 1998 financial “Big Bang” reforms brought revisions of accounting and transparency rules (Reference Toya and AmyxToya and Amyx 2006). They also removed the restrictive foreign trade and currency rules, depriving MITI (renamed METI soon thereafter) of one of its strongest coordination tools. In the same year, the Ministry of Finance was stripped of its powers overseeing the financial industry, and the new Financial Services Agency (FSA) took over banking regulation. Financial deregulation allowed large companies to access foreign financial markets and pried open the domestic stock and bond markets. This lessened the large firms’ reliance on domestic banks, and thereby eliminated the bureaucrat’s core lever for picking winners. By 2000, the carrots and sticks wielded by ministries were largely blunted if not completely removed.

The collapse of the bubble economy brought a severe banking crisis in 1998, and a full-blown recession in the years 1998–2003. The economy fell into a twenty-year long period of low economic growth (see Figure 5). All efforts by the government to jump-start economic activity proved insufficient, from zero-level interest rates and fiscal stimulus packages to public works and generous grant programs for all parts of the economy. In combination, however, they raised Japan’s government debt to 266 percent of GDP in 2021, the highest in the developed world. As economic growth remained elusive, the 1990s was labelled Japan’s “lost decade,” and the aughts were seen by many as a “second lost decade.”

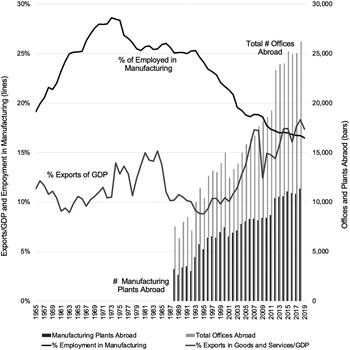

Yet, in the background of this domestic economic malaise, Japan’s largest companies were slowly yet steadily shifting their global business strategies. Whereas the direct postwar years had been anchored on export-driven growth, the 1980s brought a rapid increase in outbound foreign direct investment, that is, the location of production outside Japan (at the time referred to as “hollowing out,” kūdōka). The trade war with the United States from the early 1980s to the mid-1990s further incentivized Japan’s construction of a global production network, as the United States demanded “voluntary export restraints” by Japan’s automobile and electronics companies. In response, Japanese manufacturers opened plants in the United States, Mexico, and Canada (to take advantage of the trade zone called NAFTA, now USMCA), and they took some of their largest suppliers with them. A new period began where corporate success is no longer measured in domestic market share, but profitability and technological leadership, and Japan’s largest companies began to build a global production network to feed into global supply chains. By 2020, more than half of Japanese manufacturing sales were generated in plants located outside of Japan (see Section 4).

The turn of the century brought a sea change in the competitive dynamic in Northeast Asia, Japan’s home turf. In the 1990s, Taiwan and South Korea had successfully caught up with Japan’s mass-manufacturing skills, yet with much lower labor costs. This challenged Japan’s leadership in consumer end products, especially in so-called white goods (kitchen electronics, such as fridges) and brown goods (audio/visual, including TVs). By the year 2000, Japan had also conceded semiconductor manufacturing to competitors in Taiwan and Korea. All three were then challenged by the rise of China as the “world’s assembler.” For Japan, on the one hand, the emerging China presented a huge and growing market just when domestic markets began to shrink, and lower labor costs also invited the move of production capacities to China. On the other, China was also a formidable up-and-coming competitor, just at a time when dramatic technology advances in logistics, freight, and communication brought the globalization of production value chains.

These events – deregulation, the collapse and recession after the bubble, and the new competitive setting – necessitated a wholesale shift in corporate strategy and business models. To compete with China, Japanese companies had to be not larger, but more agile, nimble, and smarter. Even Japan’s largest, most diversified conglomerates could never be large enough to compete with China. This brought the onset of “choose and focus” strategies (Reference SchaedeSchaede 2008, Reference Schaede2020). Domestic stability insurance through business groups became less relevant, and financial deregulation since the 1980s had already greatly reduced the dependence on domestic banks. To operate at the technology frontier and always stay a step ahead of their fast-growing East Asian competitors, many of Japan’s largest companies underwent drastic pivots. For example, Hitachi sold off most of its former businesses, to become a provider of advanced manufacturing service solutions as well as a competitor in smart cities and smart infrastructure.

For employees, the lost decades were a difficult time. Older workers were stuck in companies that were doing poorly. Perhaps worse, because many companies reduced their hiring due to the recession, many young university graduates in the 1990s and aughts were left out of the lifetime career path altogether. The rigidities of the lifetime employment system and its lockstep promotion meant those who started their working careers in nonregular jobs were unlikely to have a chance to become a “salaryman” later. The 1990s came to be called the “ice age of employment” (shūshoku hyōgaki) and initiated slow but ultimately monumental changes in how employees and employers viewed their mutual obligations. We will see in Section 5 how this created the setting before which employer–employee relationships are being redefined in the 2020s to suit the newly emerging needs of post-pandemic workstyles and the DX.

In response to these developments, the state also needed to adjust. The previous infant industry protection and export promotion had run its course. In Section 6, we will see that the new assignment is to support the leading competitors with vast global operations in an uncertain time, while also assuming new roles domestically in terms of compensating those left behind by the DX. For the country’s technology leaders and reformers, the new VUCA world with its unknown technology frontier requires a new conceptualization of state guidance.

There is now a growing recognition that the 1990s and the early 2010s were not so much two “lost” decades, but instead the onset of a full-blown reorganization of Japan’s industrial architecture and industrial policy. Many of the developments we analyze in the following three sections on business, people, and the state originated in this period, in a process of slow, careful, and methodical transition into a new era of competition. The DX is further accelerating these ongoing shifts to usher in the end of the institutions of postwar industrial policy.

4 The DX and Business: New Technologies, Industries, and Global Strategies

This section shows how the DX is bringing tectonic shifts to Japanese industry, thus shaping a new role for business in Japan’s political economy. It showcases the examples of agrotech and digital manufacturing, to explain the technology advances that characterize the arrival of the DX. Since 1953, the ratio of employment in Japan’s primary sector (agriculture, fisheries, forestry, mining) has declined from 43 percent to 3 percent today. Similarly, in the secondary sector (manufacturing, construction, electricity) it has dropped from a high of 40 percent in the 1970s to 24 percent today.Footnote 25 While this leads some observers to view these two sectors as increasingly irrelevant, nothing could be further from the truth. In fact, the DX and its innovations allow companies to give new meaning to these sectors, and to design business models that upend existing categories. Moreover, 50 percent of Japan’s manufacturing revenues are now generated abroad, making advanced manufacturing and the management of global value chains central to how companies compete. Domestically, the DX is phasing out legacy industries such as multilayered distribution, which brings solutions to some of Japan’s long-standing socioeconomic challenges as well as new opportunities for innovative companies.

4.1 Agriculture: The Making of a Twenty-First Century Tomato