1. Introduction

We revisit a two-sided stochastic singular control problem, where the objective is to optimally modify a stochastic process to minimize the expected net present value (NPV) of costs. In this setting, the process can be modified in both directions – increased or decreased. The total cost comprises a running cost, represented as a function f of the controlled process accumulated over time, and control costs (or rewards) proportional to the magnitude of the applied control. Problems of this kind have applications in various fields; see [Reference Avram, Kyprianou and Pistorius4, Reference Loeffen15] for examples in finance and insurance, and [Reference Dai and Yao7, Reference Dai and Yao8] for applications in inventory management.

Specifically, the state process in our problem is modeled by a spectrally negative Lévy process (i.e. Lévy process with only downward jumps). The controller can continuously increase the state process but can only decrease it at independent Poisson arrival times. The restriction on downward control to discrete times distinguishes our problem from classical studies of two-sided stochastic control, such as [Reference Baurdoux and Yamazaki5], as well as more recent work like [Reference Mordecki and Oliú18], both of which assume that controls in both directions can be applied continuously. Recently, stochastic control problems with random discrete control opportunities have received much attention in the literature; see, for example, [Reference Albrecher, Bäuerle and Thonhauser1, Reference Avanzi, Cheung, Wong and Woo3, Reference Dong, Yin and Dai9, Reference Noba, Pérez, Yamazaki and Yano19, Reference Pérez, Yamazaki and Bensoussan22, Reference Zhao, Chen and Yang24]. For recent results on Lévy processes observed at Poisson arrival times, see [Reference Albrecher, Ivanovs and Zhou2, Reference Lkabous14].

Restricting downward control opportunities to random discrete times can have useful implications in practice. For instance, in inventory management, selling is often more challenging than replenishing. While replenishment from suppliers may occur continuously, selling surplus stock might not be feasible in continuous time but instead requires some waiting period to find a suitable buyer. In such cases, modeling downward control opportunities with random discrete times is appropriate. More generally, the problem we address is applicable in situations where downward control of the stochastic process is subject to tighter constraints.

The motivation for using Poisson arrival times to model control opportunities is two-fold. First, a semi-explicit solution to the problem can be obtained by leveraging the scale functions and the exponential inter-arrival times of a Poisson process. To the best of our knowledge, explicit analytical solutions fail to exist for other types of discrete random times. In such cases numerical methods are typically employed, as the state space must be expanded to ensure the problem remains Markovian. Additionally, insights from the mathematical finance literature suggest that the solution to the constant inter-arrival model, where controls can only be applied at deterministic, uniformly spaced times, can be approximated by the solution to the Poissonian inter-arrival model. For a study on this topic, we refer readers to [Reference Leung, Yamazaki and Zhang13].

The aim of this study is to establish the optimality of a barrier strategy under the Poisson inter-arrival model. To this end, we follow the standard guess-and-verify approach:

-

(i) The NPV of costs corresponding to the periodic–classical barrier strategy is computed semi-explicitly using scale functions. The control cost has been computed in [Reference Noba, Pérez, Yamazaki and Yano19] and the running cost is computed using a result from [Reference Mata, Moreno-Franco, Noba and Pérez17].

-

(ii) The candidate barriers, denoted by

$(a^*, b^*)$

, are identified using the method proposed in [Reference Noba and Yamazaki20] (see Section 3 of this work), rather than through the classical method based on the smooth-fit principle. Nevertheless, for the current problem the equivalence of the two methods is established.

$(a^*, b^*)$

, are identified using the method proposed in [Reference Noba and Yamazaki20] (see Section 3 of this work), rather than through the classical method based on the smooth-fit principle. Nevertheless, for the current problem the equivalence of the two methods is established. -

(iii) The existence and uniqueness of

$(a^*, b^*)$

is established through a probabilistic argument under a most general condition. -

(iv) The optimality of the candidate periodic–classical barrier strategy is established via a verification lemma, using a conventional argument that leverages the analytical properties of the scale functions and fluctuation identities.

While our approach leverages the scale functions of a spectrally one-sided Lévy process, several alternative methods for solving similar singular control problems have been explored in the literature. For instance, Noba and Yamazaki [Reference Noba and Yamazaki20] solve a one-sided variation of our problem for general Lévy processes. In another direction, Mordecki and Oliú [Reference Mordecki and Oliú18] address a related problem by establishing a connection to Dynkin games, under a different set of assumptions on the function f and the state process.

The remainder of this paper proceeds as follows: Section 2 presents the mathematical formulation of the problem considered. Section 3 introduces the periodic–classical barrier strategies for our problem and states the main result. Section 4 presents a sequence of results that completes the proof of the main result stated in Section 3. Section 5 presents a numerical example. Section 6 concludes this study with a discussion of several directions for potential extensions.

In this paper we use

$x+$

and

$x+$

and

$x-$

to denote the right- and left-hand limits at

$x-$

to denote the right- and left-hand limits at

$x \in \mathbb{R}$

, respectively. Additionally, terms like strictly increasing and strictly decreasing indicate a function’s strict monotonicity, while non-decreasing and non-increasing indicate weak monotonicity. Convexity of a function is always understood in the weak sense.

$x \in \mathbb{R}$

, respectively. Additionally, terms like strictly increasing and strictly decreasing indicate a function’s strict monotonicity, while non-decreasing and non-increasing indicate weak monotonicity. Convexity of a function is always understood in the weak sense.

2. Problem setting

Defined on a probability space

$(\Omega, \mathcal{F}, \mathbb{P})$

, let

$(\Omega, \mathcal{F}, \mathbb{P})$

, let

$X = (X(t);\; t \geq 0)$

be a one-dimensional spectrally negative Lévy process. For

$X = (X(t);\; t \geq 0)$

be a one-dimensional spectrally negative Lévy process. For

$x \in \mathbb{R}$

, we use

$x \in \mathbb{R}$

, we use

$\mathbb{P}_x$

to denote the law of X with initial value x, and

$\mathbb{P}_x$

to denote the law of X with initial value x, and

$\mathbb{E}_x$

to denote the corresponding expectation operator. When

$\mathbb{E}_x$

to denote the corresponding expectation operator. When

$x = 0$

, we drop the subscript and simply write

$x = 0$

, we drop the subscript and simply write

$\mathbb{P}$

and

$\mathbb{P}$

and

$\mathbb{E}$

. The Laplace exponent of X is given by

$\mathbb{E}$

. The Laplace exponent of X is given by

\begin{equation} \psi(s) \;:\!=\; \log\mathbb{E} \big[{\mathrm{e}}^{s X(1)}\big] = \gamma s + \frac{\sigma^2}{2} s^2 + \int_{({-}\infty, 0)} ({\mathrm{e}}^{sz} - 1 - sz\mathbf{1}_{\{z \gt -1\}})\,\mu(\mathrm{d} z), \quad s \geq 0,\end{equation}

\begin{equation} \psi(s) \;:\!=\; \log\mathbb{E} \big[{\mathrm{e}}^{s X(1)}\big] = \gamma s + \frac{\sigma^2}{2} s^2 + \int_{({-}\infty, 0)} ({\mathrm{e}}^{sz} - 1 - sz\mathbf{1}_{\{z \gt -1\}})\,\mu(\mathrm{d} z), \quad s \geq 0,\end{equation}

for some

$\gamma \in \mathbb{R}$

,

$\gamma \in \mathbb{R}$

,

$\sigma \geq 0$

, and a Lévy measure

$\sigma \geq 0$

, and a Lévy measure

$\mu$

on

$\mu$

on

$({-}\infty, 0)$

satisfying

$({-}\infty, 0)$

satisfying

$\int_{({-}\infty, 0)} (1 \wedge z^2) \, \mu(\mathrm{d} z) \lt \infty$

.

$\int_{({-}\infty, 0)} (1 \wedge z^2) \, \mu(\mathrm{d} z) \lt \infty$

.

The process X has paths of bounded variation if and only if

$\sigma = 0$

and

$\sigma = 0$

and

$\int_{({-}\infty, 0)} (1 \wedge |z|) \,\mu(\mathrm{d} z) \lt \infty$

. In the case of bounded variation, X admits the form

$\int_{({-}\infty, 0)} (1 \wedge |z|) \,\mu(\mathrm{d} z) \lt \infty$

. In the case of bounded variation, X admits the form

$X(t) = \delta t - S(t)$

,

$X(t) = \delta t - S(t)$

,

$t\geq 0$

, where

$t\geq 0$

, where

$(S(t);\; t\geq0)$

is a subordinator and

$(S(t);\; t\geq0)$

is a subordinator and

$\delta \;:\!=\; \gamma - \int_{({-}1, 0)} z\, \mu(\mathrm{d} z)$

. We assume that X is not the negative of a subordinator, and therefore

$\delta \;:\!=\; \gamma - \int_{({-}1, 0)} z\, \mu(\mathrm{d} z)$

. We assume that X is not the negative of a subordinator, and therefore

$\delta \gt 0$

.

$\delta \gt 0$

.

In this paper, we consider the following singular control problem. Let

$\mathcal{T}_r \;:\!=\; (T(i);\; i \geq 0)$

be the arrival times of a Poisson process

$\mathcal{T}_r \;:\!=\; (T(i);\; i \geq 0)$

be the arrival times of a Poisson process

$N_r = (N_r(t);\; t \geq 0)$

with intensity

$N_r = (N_r(t);\; t \geq 0)$

with intensity

$r \gt 0$

. The Poisson process

$r \gt 0$

. The Poisson process

$N_r$

and its corresponding arrival times

$N_r$

and its corresponding arrival times

$\mathcal{T}_r$

are independent of X. Let

$\mathcal{T}_r$

are independent of X. Let

$\mathbb{F} \;:\!=\; (\mathcal{F}(t);\; t \geq 0)$

denote the (completed) filtration generated by

$\mathbb{F} \;:\!=\; (\mathcal{F}(t);\; t \geq 0)$

denote the (completed) filtration generated by

$(X, N_r)$

. A strategy

$(X, N_r)$

. A strategy

$\pi = \{(R^\pi(t), L^\pi(t));\; t \geq 0\}$

is a pair of non-decreasing, càdlàg, and

$\pi = \{(R^\pi(t), L^\pi(t));\; t \geq 0\}$

is a pair of non-decreasing, càdlàg, and

$\mathbb{F}$

-adapted processes, with

$\mathbb{F}$

-adapted processes, with

$R^\pi(0{-}) = L^\pi(0{-}) = 0$

. Under

$R^\pi(0{-}) = L^\pi(0{-}) = 0$

. Under

$\pi$

, the controlled process

$\pi$

, the controlled process

$Y^\pi = (Y^\pi(t);\; t \geq 0)$

is given by

$Y^\pi = (Y^\pi(t);\; t \geq 0)$

is given by

\[Y^\pi(t) \;:\!=\; X(t) + R^\pi(t) - L^\pi(t), \quad t \geq 0.\]

\[Y^\pi(t) \;:\!=\; X(t) + R^\pi(t) - L^\pi(t), \quad t \geq 0.\]

Specifically, the process

$R^\pi$

controls the state process in the upward direction and can be activated continuously in time, while the process

$R^\pi$

controls the state process in the upward direction and can be activated continuously in time, while the process

$L^\pi$

controls it in the downward direction and can only be activated at the arrival times

$L^\pi$

controls it in the downward direction and can only be activated at the arrival times

$\mathcal{T}_r$

of the Poisson process

$\mathcal{T}_r$

of the Poisson process

$N_r$

. Mathematically,

$N_r$

. Mathematically,

$L^\pi$

admits the form

$L^\pi$

admits the form

\[L^\pi(t) = \int_{[0, t]}\nu^\pi(s) \, \mathrm{d} N_r(s) = \sum^\infty_{i = 1} \nu^\pi(T(i)) \mathbf{1}_{\{T(i) \leq t\}}\]

\[L^\pi(t) = \int_{[0, t]}\nu^\pi(s) \, \mathrm{d} N_r(s) = \sum^\infty_{i = 1} \nu^\pi(T(i)) \mathbf{1}_{\{T(i) \leq t\}}\]

for an

$\mathbb{F}$

-adapted càglàd process

$\mathbb{F}$

-adapted càglàd process

$(\nu^\pi(t);\; t \geq 0)$

.

$(\nu^\pi(t);\; t \geq 0)$

.

Fix a discount factor

$q \gt 0$

and an initial value

$q \gt 0$

and an initial value

$x \in \mathbb{R}$

for the state process. Associated with each admissible strategy

$x \in \mathbb{R}$

for the state process. Associated with each admissible strategy

$\pi$

, the NPV of costs is given by

$\pi$

, the NPV of costs is given by

\begin{equation*} v^\pi(x) = \mathbb{E}_x \bigg[\int^\infty_0 {\mathrm{e}}^{-qt} f(Y^\pi(t))\, \mathrm{d} t + \int_{[0, \infty)} {\mathrm{e}}^{-qt}(C_{\mathrm{U}} \, \mathrm{d} R^\pi(t) + C_{\mathrm{D}} \, \mathrm{d} L^\pi(t))\bigg].\end{equation*}

\begin{equation*} v^\pi(x) = \mathbb{E}_x \bigg[\int^\infty_0 {\mathrm{e}}^{-qt} f(Y^\pi(t))\, \mathrm{d} t + \int_{[0, \infty)} {\mathrm{e}}^{-qt}(C_{\mathrm{U}} \, \mathrm{d} R^\pi(t) + C_{\mathrm{D}} \, \mathrm{d} L^\pi(t))\bigg].\end{equation*}

Here,

$f\colon \mathbb{R} \to \mathbb{R}$

is a function modeling the running cost, and

$f\colon \mathbb{R} \to \mathbb{R}$

is a function modeling the running cost, and

$C_{\mathrm{U}}$

and

$C_{\mathrm{U}}$

and

$C_{\mathrm{D}}$

are real numbers representing the unit costs or rewards of control. For our problem to be well-defined, we assume

$C_{\mathrm{D}}$

are real numbers representing the unit costs or rewards of control. For our problem to be well-defined, we assume

\begin{equation} C_{\mathrm{U}} + C_{\mathrm{D}} \gt 0. \end{equation}

\begin{equation} C_{\mathrm{U}} + C_{\mathrm{D}} \gt 0. \end{equation}

Assumption (2.2) is standard in the literature, such as in [Reference Baurdoux and Yamazaki5].

We impose the following assumptions.

Assumption 2.1. We assume that

$f\colon \mathbb{R} \to \mathbb{R}$

satisfies the following:

$f\colon \mathbb{R} \to \mathbb{R}$

satisfies the following:

-

(i) f is a convex, piecewise continuously differentiable function. Additionally, it is assumed to be slowly or regularly varying as

$x \to \infty$

(resp.

$x \to -\infty$

) if

$\lim_{x \to \infty} |f(x)| = \infty$

(resp.

$\lim_{x \to -\infty} |f(x)| = \infty$

). -

(ii) There exists a number

$\bar{a} \;:\!=\; \inf\{a\in\mathbb{R}\colon\tilde{f}'(a) \;:\!=\; f'(a) + qC_{\mathrm{U}} \geq 0\}\in\mathbb{R}$

such that the function (2.3)is strictly decreasing on

\begin{equation} \tilde{f}(x) \;:\!=\; f(x) + qC_{\mathrm{U}}x, \quad x\in \mathbb{R}, \end{equation}

$({-}\infty, \bar{a})$

and non-decreasing on

$(\bar{a}, \infty)$

.

-

(iii) There exists a number

$\bar{\bar{a}} \;:\!=\; \inf\{a\in\mathbb{R}\colon f'(a) - qC_{\mathrm{D}} \gt 0\} \in \mathbb{R}$

.

Here and in the remainder of this paper we use f ′(x) to denote the right derivative of f at x, whenever the standard derivative does not exist.

In Assumptions 2.1, the most crucial condition is convexity, which is standard in similar singular control problems (see, for example, [Reference Baurdoux and Yamazaki5] and [Reference Pérez, Yamazaki and Bensoussan22]). The growth condition in (i) is imposed for integrability, and it is satisfied by any convex, piecewise continuously differentiable function f that is a polynomial of degree

$n \geq 1$

outside a compact interval. The growth behavior of f is summarized in the following remark.

$n \geq 1$

outside a compact interval. The growth behavior of f is summarized in the following remark.

Remark 2.1. By Assumption 2.1, the running cost function f grows at most polynomially, and the derivative satisfies

$f'({-}\infty) \;:\!=\; \lim_{x \to -\infty} f'(x) \in [{-}\infty, -qC_{\mathrm{U}})$

and

$f'({-}\infty) \;:\!=\; \lim_{x \to -\infty} f'(x) \in [{-}\infty, -qC_{\mathrm{U}})$

and

$f'(\infty) \;:\!=\; \lim_{x \to \infty} f'(x) \in (qC_{\mathrm{D}}, \infty]$

. Moreover, by (2.2) and the convexity of f, we have

$f'(\infty) \;:\!=\; \lim_{x \to \infty} f'(x) \in (qC_{\mathrm{D}}, \infty]$

. Moreover, by (2.2) and the convexity of f, we have

$\bar{a} \lt \bar{\bar{a}}$

.

$\bar{a} \lt \bar{\bar{a}}$

.

Assumptions 2.1(ii) and (iii) are imposed to avoid cases where it is optimal not to control the process from below or above. In [Reference Baurdoux and Yamazaki5], (ii) is imposed, but (iii) is not explicitly specified. The discussion for cases in which (iii) does not hold is deferred to Remark 4.2.

We also impose the following assumption for integrability. In conjunction with Assumption 2.1(i), it guarantees that

$\mathbb{E}[X(1)] = \psi'(0+) \in ({-}\infty, \infty)$

and

$\mathbb{E}[X(1)] = \psi'(0+) \in ({-}\infty, \infty)$

and

$\mathbb{E}_x[ \int^\infty_{0}{\mathrm{e}}^{-qs} |f(X(s))|\, \mathrm{d} s] \lt \infty$

for all

$\mathbb{E}_x[ \int^\infty_{0}{\mathrm{e}}^{-qs} |f(X(s))|\, \mathrm{d} s] \lt \infty$

for all

$x \in \mathbb{R}$

.

$x \in \mathbb{R}$

.

Assumption 2.2. There exists

$\theta \gt 0$

such that

$\theta \gt 0$

such that

$\int_{({-}\infty, -1]} \exp(\theta |y|)\, \mu(\mathrm{d} y) \lt \infty$

.

$\int_{({-}\infty, -1]} \exp(\theta |y|)\, \mu(\mathrm{d} y) \lt \infty$

.

Let

$\Pi$

be the set of admissible strategies, consisting of all

$\Pi$

be the set of admissible strategies, consisting of all

$\pi$

such that:

$\pi$

such that:

-

•

$\mathbb{E}_x[\!\int^\infty_{0}{\mathrm{e}}^{-qs} |f(Y^\pi(s))|\, \mathrm{d} s] \lt \infty$

, and -

•

$\mathbb{E}_x[\!\int_{[0, \infty)}{\mathrm{e}}^{-qs}\,(\mathrm{d} R^\pi(s) + \mathrm{d} L^\pi(s))] \lt \infty$

.

The objective of this singular control problem is to compute the value function (i.e. the optimal cost function)

\[v(x) \;:\!=\;\inf_{\pi \in \Pi} v^\pi(x), \quad x \in \mathbb{R},\]

\[v(x) \;:\!=\;\inf_{\pi \in \Pi} v^\pi(x), \quad x \in \mathbb{R},\]

and an associated optimal strategy

$\pi^*$

such that

$\pi^*$

such that

$v(x) = v^{\pi^*}(x)$

, if such a strategy exists.

$v(x) = v^{\pi^*}(x)$

, if such a strategy exists.

3. Periodic–classical barrier strategies

We now introduce the set of periodic–classical barrier strategies, comprising strategies of the form

$\pi_{a,b} \;:\!=\; \{(L^{a,b}(t), R^{a,b}(t));\; t \geq 0 \}$

, parameterized by two barriers

$\pi_{a,b} \;:\!=\; \{(L^{a,b}(t), R^{a,b}(t));\; t \geq 0 \}$

, parameterized by two barriers

$a \lt b$

. Under

$a \lt b$

. Under

$\pi_{a, b}$

, the controlled process

$\pi_{a, b}$

, the controlled process

\[ Y^{a,b}(t) \;:\!=\; X(t) + R^{a,b}(t) - L^{a,b}(t), \quad t \geq 0, \]

\[ Y^{a,b}(t) \;:\!=\; X(t) + R^{a,b}(t) - L^{a,b}(t), \quad t \geq 0, \]

is continuously reflected from below at the lower barrier a and periodically reflected from above at the upper barrier b. In other words, the controlled process is never allowed to fall below a and is thus reflected upwards whenever it would fall below this barrier. On the other hand, at any decision time in

$\mathcal{T}_r$

, if the controlled process is observed above b, it is immediately pushed down to b. The process

$\mathcal{T}_r$

, if the controlled process is observed above b, it is immediately pushed down to b. The process

$Y^{a, b}$

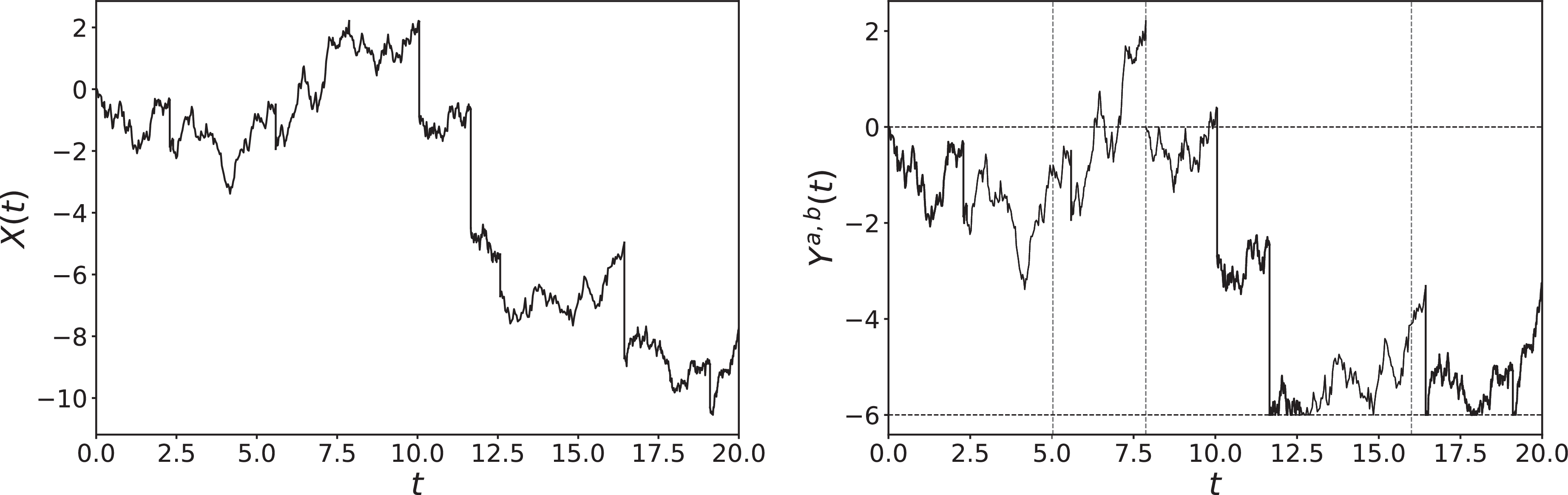

has been studied in works such as [Reference Noba, Pérez, Yamazaki and Yano19], among others. As described in [Reference Noba, Pérez, Yamazaki and Yano19], it can be defined as a concatenation of classical reflected processes with additional downward jumps. An example is provided in Figure 1.

$Y^{a, b}$

has been studied in works such as [Reference Noba, Pérez, Yamazaki and Yano19], among others. As described in [Reference Noba, Pérez, Yamazaki and Yano19], it can be defined as a concatenation of classical reflected processes with additional downward jumps. An example is provided in Figure 1.

Left: A sample path of a spectrally negative Lévy process X. Right: The corresponding controlled process

$Y^{a, b}$

with

$Y^{a, b}$

with

$a = -6$

and

$a = -6$

and

$b = 0$

. Vertical dashed lines indicate the Poisson arrival times

$b = 0$

. Vertical dashed lines indicate the Poisson arrival times

$\mathcal{T}_r$

. Among the three arrival times displayed,

$\mathcal{T}_r$

. Among the three arrival times displayed,

$Y^{a, b}$

exceeds

$Y^{a, b}$

exceeds

$b = 0$

only at the second one, causing downward control to activate there but not at the first or third arrival times.

$b = 0$

only at the second one, causing downward control to activate there but not at the first or third arrival times.

Previous works, such as [Reference Baurdoux and Yamazaki5] and [Reference Pérez, Yamazaki and Bensoussan22], have shown the optimality of barrier-type strategies for one- and two-sided stochastic singular control problems by identifying an optimal barrier, or an optimal pair of barriers, according to the smooth-fit principle. For instance, in the continuous-monitoring version of this problem studied in [Reference Baurdoux and Yamazaki5], an optimal pair of barriers, denoted by

$(a^*, b^*)$

, is selected such that the corresponding NPV of costs satisfies a certain smoothness condition. In this paper, we instead seek

$(a^*, b^*)$

, is selected such that the corresponding NPV of costs satisfies a certain smoothness condition. In this paper, we instead seek

$(a^*, b^*)$

such that

$(a^*, b^*)$

such that

$\mathfrak{C}$

holds:

$\mathfrak{C}$

holds:

\begin{equation*} \mathfrak{C}\colon\mathbb{E}_{a^*}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{a^*, b^*}(t))\,\mathrm{d}t\bigg] = -C_{\mathrm{U}}, \quad \mathbb{E}_{b^*}\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{a^*, b^*}(t))\, \mathrm{d}t\bigg] = C_{\mathrm{D}}.\end{equation*}

\begin{equation*} \mathfrak{C}\colon\mathbb{E}_{a^*}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{a^*, b^*}(t))\,\mathrm{d}t\bigg] = -C_{\mathrm{U}}, \quad \mathbb{E}_{b^*}\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{a^*, b^*}(t))\, \mathrm{d}t\bigg] = C_{\mathrm{D}}.\end{equation*}

A similar approach was recently applied in [Reference Noba and Yamazaki20] to establish the optimality of a single-barrier strategy for the one-sided control problem considered therein. By revisiting the two-sided control problem in [Reference Baurdoux and Yamazaki5] through this approach, we can further confirm that the conditions outlined above are satisfied. Hence, although our problem is more complex than the one studied in [Reference Baurdoux and Yamazaki5], we expect that this approach will be similarly effective in identifying the optimal barriers in our setting.

The advantage of this approach is that it allows for a probabilistic interpretation. We observe that, intuitively,

$\mathbb{E}_{x}\big[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^\pi(t))\,\mathrm{d}t\big]$

represents the rate of change of the running cost when the controlled process

$\mathbb{E}_{x}\big[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^\pi(t))\,\mathrm{d}t\big]$

represents the rate of change of the running cost when the controlled process

$Y^\pi$

with initial value x is shifted to the right by an infinitesimal amount. Thus, it is desirable for a strategy

$Y^\pi$

with initial value x is shifted to the right by an infinitesimal amount. Thus, it is desirable for a strategy

$\pi$

to keep

$\pi$

to keep

$Y^{\pi}$

within the set

$Y^{\pi}$

within the set

$\mathcal{C}^\pi$

for as long as possible, where

$\mathcal{C}^\pi$

for as long as possible, where

\[\mathcal{C}^\pi \;:\!=\; \bigg\{x \in \mathbb{R}\colon -C_{\mathrm{U}} \leq \mathbb{E}_{x}\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{\pi}(t))\, \mathrm{d} t\bigg] \leq C_{\mathrm{D}} \bigg\}.\]

\[\mathcal{C}^\pi \;:\!=\; \bigg\{x \in \mathbb{R}\colon -C_{\mathrm{U}} \leq \mathbb{E}_{x}\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{\pi}(t))\, \mathrm{d} t\bigg] \leq C_{\mathrm{D}} \bigg\}.\]

We now present Theorem 3.1, the main result of this paper.

Theorem 3.1. There exists a unique pair

$(a^*, b^*)$

such that

$(a^*, b^*)$

such that

$\mathfrak{C}$

holds. Furthermore, the strategy

$\mathfrak{C}$

holds. Furthermore, the strategy

$\pi_{a^*,b^*}$

is optimal with

$\pi_{a^*,b^*}$

is optimal with

$v_{a^*, b^*}(x) = \inf_{\pi \in \Pi} v^\pi(x)$

,

$v_{a^*, b^*}(x) = \inf_{\pi \in \Pi} v^\pi(x)$

,

$x\in \mathbb{R}$

, where

$x\in \mathbb{R}$

, where

$v_{a^*, b^*}$

denotes the NPV of costs under the periodic–classical barrier strategy

$v_{a^*, b^*}$

denotes the NPV of costs under the periodic–classical barrier strategy

$\pi_{a^*,b^*}$

.

$\pi_{a^*,b^*}$

.

The proof of Theorem 3.1 is developed in Section 4 through a series of lemmas and propositions. The existence and uniqueness of

$(a^*, b^*)$

are established by first computing, and then analyzing, the expression for

$(a^*, b^*)$

are established by first computing, and then analyzing, the expression for

$v_{a, b}$

for

$v_{a, b}$

for

$a \lt b$

. Specifically, a semi-explicit expression for

$a \lt b$

. Specifically, a semi-explicit expression for

$v_{a, b}$

is obtained using scale functions, and the pair

$v_{a, b}$

is obtained using scale functions, and the pair

$(a^*, b^*)$

is identified as the solution to a pair of equations that also admit semi-explicit expressions (see (4.20)). Once existence has been established, the optimality of

$(a^*, b^*)$

is identified as the solution to a pair of equations that also admit semi-explicit expressions (see (4.20)). Once existence has been established, the optimality of

$v_{a^*, b^*}$

is demonstrated through further analysis of the semi-explicit expression of

$v_{a^*, b^*}$

is demonstrated through further analysis of the semi-explicit expression of

$v_{a, b}$

with

$v_{a, b}$

with

$a = a^*$

and

$a = a^*$

and

$b = b^*$

, in conjunction with a conventional application of Itô’s lemma. The complete proof of Theorem 3.1 is presented at the end of Section 4.

$b = b^*$

, in conjunction with a conventional application of Itô’s lemma. The complete proof of Theorem 3.1 is presented at the end of Section 4.

4. Solution

As a first step towards Theorem 3.1, we compute the expression of the NPV of costs under

$\pi_{a, b}$

. To this end, we introduce the scale functions of a spectrally negative Lévy process and define several auxiliary functions that are relevant to our subsequent computations.

$\pi_{a, b}$

. To this end, we introduce the scale functions of a spectrally negative Lévy process and define several auxiliary functions that are relevant to our subsequent computations.

4.1. Scale functions and fluctuation identities

For

$q \geq 0$

, the scale function

$q \geq 0$

, the scale function

$W^{(q)}\colon \mathbb{R} \to [0 , \infty)$

of the spectrally negative Lévy process X is defined as follows. On the negative half-line,

$W^{(q)}\colon \mathbb{R} \to [0 , \infty)$

of the spectrally negative Lévy process X is defined as follows. On the negative half-line,

$W^{(q)}$

is set to be zero. On the positive half-line, it is a continuous and strictly increasing function that satisfies

$W^{(q)}$

is set to be zero. On the positive half-line, it is a continuous and strictly increasing function that satisfies

\begin{align} \int^\infty_0 {\mathrm{e}}^{-\theta x} W^{(q)}(x)\, \mathrm{d} x = \frac{1}{\psi(\theta) - q}, \quad \theta \gt \Phi_q.\end{align}

\begin{align} \int^\infty_0 {\mathrm{e}}^{-\theta x} W^{(q)}(x)\, \mathrm{d} x = \frac{1}{\psi(\theta) - q}, \quad \theta \gt \Phi_q.\end{align}

Here,

$\psi$

is the Laplace exponent defined in (2.1), and

$\psi$

is the Laplace exponent defined in (2.1), and

$\Phi_q \;:\!=\; \sup \{s \geq 0\colon \psi(s) = q\}$

,

$\Phi_q \;:\!=\; \sup \{s \geq 0\colon \psi(s) = q\}$

,

$q \geq 0$

, is its right inverse. We refer the readers to [Reference Kuznetsov, Kyprianou and Rivero11, Reference Kyprianou12] for a comprehensive review of scale functions. In particular, [Reference Kuznetsov, Kyprianou and Rivero11, Lemmas 2.3, 2.4, 3.1, and 3.2], which expound the smoothness of the scale functions, are of particular importance.

$q \geq 0$

, is its right inverse. We refer the readers to [Reference Kuznetsov, Kyprianou and Rivero11, Reference Kyprianou12] for a comprehensive review of scale functions. In particular, [Reference Kuznetsov, Kyprianou and Rivero11, Lemmas 2.3, 2.4, 3.1, and 3.2], which expound the smoothness of the scale functions, are of particular importance.

We define, for

$x \in \mathbb{R}$

,

$x \in \mathbb{R}$

,

\begin{equation*} \overline{W}^{(q)}(x) \;:\!=\; \int_0^{x} W^{(q)}(y)\, \mathrm{d} y, \qquad \overline{\overline{W}}^{(q)}(x) \;:\!=\; \int_0^{x} \overline{W}^{(q)}(y)\, \mathrm{d} y.\end{equation*}

\begin{equation*} \overline{W}^{(q)}(x) \;:\!=\; \int_0^{x} W^{(q)}(y)\, \mathrm{d} y, \qquad \overline{\overline{W}}^{(q)}(x) \;:\!=\; \int_0^{x} \overline{W}^{(q)}(y)\, \mathrm{d} y.\end{equation*}

For

$x \in \mathbb{R}$

and

$x \in \mathbb{R}$

and

$r \gt 0$

, we also define the second scale function,

$r \gt 0$

, we also define the second scale function,

\begin{equation} Z^{(q)}(x,\Phi_{q + r}) \;:\!=\; {\mathrm{e}}^{\Phi_{q + r}x}\bigg(1-r\int_0^{x}{\mathrm{e}}^{-\Phi_{q + r}z}W^{(q)}(z)\,\mathrm{d}z\bigg) = r\int_0^{\infty}{\mathrm{e}}^{-\Phi_{q + r}z}W^{(q)}(z + x)\,\mathrm{d}z,\end{equation}

\begin{equation} Z^{(q)}(x,\Phi_{q + r}) \;:\!=\; {\mathrm{e}}^{\Phi_{q + r}x}\bigg(1-r\int_0^{x}{\mathrm{e}}^{-\Phi_{q + r}z}W^{(q)}(z)\,\mathrm{d}z\bigg) = r\int_0^{\infty}{\mathrm{e}}^{-\Phi_{q + r}z}W^{(q)}(z + x)\,\mathrm{d}z,\end{equation}

where the second equality holds because (4.1) gives

$\int^\infty_0\mathrm{e}^{-\Phi_{q+r} x} W^{(q)}(x) \, \mathrm{d} x = r^{-1}$

. Differentiating the second scale function with respect to the first argument, we obtain

$\int^\infty_0\mathrm{e}^{-\Phi_{q+r} x} W^{(q)}(x) \, \mathrm{d} x = r^{-1}$

. Differentiating the second scale function with respect to the first argument, we obtain

\begin{equation*} Z^{(q)'}(x,\Phi_{q+r}) \;:\!=\; \frac{\partial}{\partial x} Z^{(q)}(x,\Phi_{q+r}) = \Phi_{q+r} Z^{(q)}(x,\Phi_{q+r}) - rW^{(q)}(x), \quad x \gt 0. \end{equation*}

\begin{equation*} Z^{(q)'}(x,\Phi_{q+r}) \;:\!=\; \frac{\partial}{\partial x} Z^{(q)}(x,\Phi_{q+r}) = \Phi_{q+r} Z^{(q)}(x,\Phi_{q+r}) - rW^{(q)}(x), \quad x \gt 0. \end{equation*}

Moreover, for

$q\geq 0$

and

$q\geq 0$

and

$x \in \mathbb{R}$

, we define

$x \in \mathbb{R}$

, we define

\begin{equation*} Z^{(q)}(x) \;:\!=\; 1 + q\overline{W}^{(q)}(x), \qquad \overline{Z}^{(q)}(x) \;:\!=\; \int^x_0 Z^{(q)}(y)\, \mathrm{d} y = x + q \overline{\overline{W}}^{(q)}(x).\end{equation*}

\begin{equation*} Z^{(q)}(x) \;:\!=\; 1 + q\overline{W}^{(q)}(x), \qquad \overline{Z}^{(q)}(x) \;:\!=\; \int^x_0 Z^{(q)}(y)\, \mathrm{d} y = x + q \overline{\overline{W}}^{(q)}(x).\end{equation*}

For

$b \gt a$

,

$b \gt a$

,

$x \in \mathbb{R}$

, and

$x \in \mathbb{R}$

, and

$h\colon \mathbb{R} \to \mathbb{R}$

, we define

$h\colon \mathbb{R} \to \mathbb{R}$

, we define

\begin{align} \rho_{a, b}^{(q)}(x;\; h) & \;:\!=\; \int^{b}_a W^{(q)}(x - y)h(y)\, \mathrm{d} y, \end{align}

\begin{align} \rho_{a, b}^{(q)}(x;\; h) & \;:\!=\; \int^{b}_a W^{(q)}(x - y)h(y)\, \mathrm{d} y, \end{align}

\begin{align} \rho_{a, b}^{(q, r)}(x;\; h) & \;:\!=\; \rho_{a, b}^{(q)}(x;\; h) + r\int^{x}_bW^{(q + r)}(x - y)\rho_{a, b}^{(q)}(y;\; h)\,\mathrm{d}y. \end{align}

\begin{align} \rho_{a, b}^{(q, r)}(x;\; h) & \;:\!=\; \rho_{a, b}^{(q)}(x;\; h) + r\int^{x}_bW^{(q + r)}(x - y)\rho_{a, b}^{(q)}(y;\; h)\,\mathrm{d}y. \end{align}

Additionally, for

$x \in \mathbb{R}$

, we define

$x \in \mathbb{R}$

, we define

\begin{align} W^{(q, r)}_{a, b}(x) & \;:\!=\; W^{(q)}(x - a) + r\int^x_b W^{(q + r)}(x - y)W^{(q)}(y - a)\,\mathrm{d}y, \end{align}

\begin{align} W^{(q, r)}_{a, b}(x) & \;:\!=\; W^{(q)}(x - a) + r\int^x_b W^{(q + r)}(x - y)W^{(q)}(y - a)\,\mathrm{d}y, \end{align}

\begin{align} Z^{(q, r)}_{a, b}(x) & \;:\!=\; Z^{(q)}(x - a) + r\int^x_bW^{(q + r)}(x - y)Z^{(q)}(y - a)\,\mathrm{d}y, \end{align}

\begin{align} Z^{(q, r)}_{a, b}(x) & \;:\!=\; Z^{(q)}(x - a) + r\int^x_bW^{(q + r)}(x - y)Z^{(q)}(y - a)\,\mathrm{d}y, \end{align}

\begin{align} \overline{Z}^{(q, r)}_{a, b}(x) & \;:\!=\; \overline{Z}^{(q)}(x - a) + r\int^x_bW^{(q + r)}(x - y)\overline{Z}^{(q)}(y - a)\,\mathrm{d}y. \end{align}

\begin{align} \overline{Z}^{(q, r)}_{a, b}(x) & \;:\!=\; \overline{Z}^{(q)}(x - a) + r\int^x_bW^{(q + r)}(x - y)\overline{Z}^{(q)}(y - a)\,\mathrm{d}y. \end{align}

It is convenient to decompose the NPV of costs into the following two components, both of which can be expressed in terms of the scale functions

$W^{(q)}$

and

$W^{(q)}$

and

$W^{(q + r)}$

, as well as the auxiliary functions defined above:

$W^{(q + r)}$

, as well as the auxiliary functions defined above:

\begin{equation*} v_{a,b}(x) = v_{a, b}^{LR}(x) + v_{a, b}^{f}(x), \quad x\in \mathbb{R},\end{equation*}

\begin{equation*} v_{a,b}(x) = v_{a, b}^{LR}(x) + v_{a, b}^{f}(x), \quad x\in \mathbb{R},\end{equation*}

where

\begin{align*} v_{a, b}^{LR}(x) & \;:\!=\; C_{\mathrm{D}}\mathbb{E}_{x}\bigg[\int_{[0,\infty)}{\mathrm{e}}^{-qt}\,\mathrm{d}L^{a, b}(t)\bigg] + C_{\mathrm{U}}\mathbb{E}_{x}\bigg[\int_{[0,\infty)}{\mathrm{e}}^{-qt}\,\mathrm{d}R^{a, b}(t)\bigg], \\[5pt] v_{a, b}^{f}(x) & \;:\!=\; \mathbb{E}_x\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f(Y^{a, b}(t))\,\mathrm{d}t\bigg].\end{align*}

\begin{align*} v_{a, b}^{LR}(x) & \;:\!=\; C_{\mathrm{D}}\mathbb{E}_{x}\bigg[\int_{[0,\infty)}{\mathrm{e}}^{-qt}\,\mathrm{d}L^{a, b}(t)\bigg] + C_{\mathrm{U}}\mathbb{E}_{x}\bigg[\int_{[0,\infty)}{\mathrm{e}}^{-qt}\,\mathrm{d}R^{a, b}(t)\bigg], \\[5pt] v_{a, b}^{f}(x) & \;:\!=\; \mathbb{E}_x\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f(Y^{a, b}(t))\,\mathrm{d}t\bigg].\end{align*}

To compute

$v_{a, b}^{LR}$

, we apply the result established in the proof of [Reference Noba, Pérez, Yamazaki and Yano19, Lemma 3.1], which expresses

$v_{a, b}^{LR}$

, we apply the result established in the proof of [Reference Noba, Pérez, Yamazaki and Yano19, Lemma 3.1], which expresses

$v_{0, b}^{LR}$

for

$v_{0, b}^{LR}$

for

$b \gt 0$

in terms of the scale functions and the auxiliary functions.

$b \gt 0$

in terms of the scale functions and the auxiliary functions.

Lemma 4.1 ([Reference Noba, Pérez, Yamazaki and Yano19, Lemma 3.1].) For

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}$

,

$x \in \mathbb{R}$

,

\begin{align} v_{a, b}^{LR}(x) & = \bigg(\frac{r}{q\Phi_{q+r}}\frac{C_{\mathrm{U}}Z^{(q)}(b-a) + C_{\mathrm{D}}}{Z^{(q)}(b-a,\Phi_{q+r})} + \frac{C_{\mathrm{U}}}{\Phi_{q+r}}\bigg)\Big(Z^{(q,r)}_{a,b}(x) - rZ^{(q)}(b-a)\overline{W}^{(q+r)}(x - b)\Big) \nonumber \\[5pt] & \quad - rC_{\mathrm{D}}\overline{\overline{W}}^{(q+r)}(x - b) - C_{\mathrm{U}}\bigg(\overline{Z}^{(q,r)}_{a,b}(x) + \frac{\psi'(0+)}{q} - r\overline{Z}^{(q)}(b - a) \overline{W}^{(q + r)}(x - b)\bigg). \end{align}

\begin{align} v_{a, b}^{LR}(x) & = \bigg(\frac{r}{q\Phi_{q+r}}\frac{C_{\mathrm{U}}Z^{(q)}(b-a) + C_{\mathrm{D}}}{Z^{(q)}(b-a,\Phi_{q+r})} + \frac{C_{\mathrm{U}}}{\Phi_{q+r}}\bigg)\Big(Z^{(q,r)}_{a,b}(x) - rZ^{(q)}(b-a)\overline{W}^{(q+r)}(x - b)\Big) \nonumber \\[5pt] & \quad - rC_{\mathrm{D}}\overline{\overline{W}}^{(q+r)}(x - b) - C_{\mathrm{U}}\bigg(\overline{Z}^{(q,r)}_{a,b}(x) + \frac{\psi'(0+)}{q} - r\overline{Z}^{(q)}(b - a) \overline{W}^{(q + r)}(x - b)\bigg). \end{align}

The running cost

$v_{a, b}^{f}$

is computed using [Reference Mata, Moreno-Franco, Noba and Pérez17, Proposition 5.1]. Details of the computation are given in Appendix A.1.

$v_{a, b}^{f}$

is computed using [Reference Mata, Moreno-Franco, Noba and Pérez17, Proposition 5.1]. Details of the computation are given in Appendix A.1.

Lemma 4.2. For

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}$

,

$x \in \mathbb{R}$

,

\begin{align} v_{a, b}^{f}(x) & = \frac{1}{q}\bigg(f(a) + \int^{\infty}_af'(y)\frac{Z^{(q)}(b-y,\Phi_{q+r})}{Z^{(q)}(b-a,\Phi_{q+r})}\,\mathrm{d}y\bigg) Z^{(q, r)}_{a, b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt f) \nonumber \\[5pt] & \quad -r\overline{W}^{(q+r)}(x-b)v_{a,b}^{f}(b) - \int^{x}_bf(y)W^{(q+r)}(x-y)\,\mathrm{d}y, \end{align}

\begin{align} v_{a, b}^{f}(x) & = \frac{1}{q}\bigg(f(a) + \int^{\infty}_af'(y)\frac{Z^{(q)}(b-y,\Phi_{q+r})}{Z^{(q)}(b-a,\Phi_{q+r})}\,\mathrm{d}y\bigg) Z^{(q, r)}_{a, b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt f) \nonumber \\[5pt] & \quad -r\overline{W}^{(q+r)}(x-b)v_{a,b}^{f}(b) - \int^{x}_bf(y)W^{(q+r)}(x-y)\,\mathrm{d}y, \end{align}

where

\begin{equation*} v_{a, b}^{f}(b) = -\rho_{a, b}^{(q)}(b;\kern3pt f) + \frac{1}{q}\bigg(f(a) + \int^{\infty}_af'(y)\frac{Z^{(q)}(b-y, \Phi_{q+r})}{Z^{(q)}(b-a,\Phi_{q+r})}\, \mathrm{d}y\bigg)Z^{(q)}(b - a). \end{equation*}

\begin{equation*} v_{a, b}^{f}(b) = -\rho_{a, b}^{(q)}(b;\kern3pt f) + \frac{1}{q}\bigg(f(a) + \int^{\infty}_af'(y)\frac{Z^{(q)}(b-y, \Phi_{q+r})}{Z^{(q)}(b-a,\Phi_{q+r})}\, \mathrm{d}y\bigg)Z^{(q)}(b - a). \end{equation*}

Combining (4.8) and (4.9), and applying integration by parts, we obtain Lemma 4.3, with the proof provided in Appendix A.2. Recall

$\tilde{f}$

as defined in (2.3).

$\tilde{f}$

as defined in (2.3).

Lemma 4.3. For

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}$

,

$x \in \mathbb{R}$

,

\begin{align} v_{a,b}(x) & = \frac{1}{q}\bigg(\tilde{f}(a) + \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})}\bigg) \big(Z^{(q, r)}_{a, b}(x) - r\overline{W}^{(q + r)}(x - b)Z^{(q)}(b - a) \big)\nonumber \\[5pt] & \quad - r(C_{\mathrm{U}} + C_{\mathrm{D}})\overline{\overline{W}}^{(q + r)}(x - b) - C_{\mathrm{U}}x + r\overline{W}^{(q+r)}(x-b)\rho_{a,b}^{(q)}(b;\,\tilde{f}) \nonumber \\[5pt]& \quad - \tilde{f}(b)\overline{W}^{(q+r)}(x-b) - \rho_{a, b}^{(q, r)}(x;\ \tilde{f}) - C_{\mathrm{U}}\frac{\psi'(0+)}{q} - \int^{x}_b\overline{W}^{(q + r)}(x - y)\tilde{f}'(y)\,\mathrm{d}y, \end{align}

\begin{align} v_{a,b}(x) & = \frac{1}{q}\bigg(\tilde{f}(a) + \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})}\bigg) \big(Z^{(q, r)}_{a, b}(x) - r\overline{W}^{(q + r)}(x - b)Z^{(q)}(b - a) \big)\nonumber \\[5pt] & \quad - r(C_{\mathrm{U}} + C_{\mathrm{D}})\overline{\overline{W}}^{(q + r)}(x - b) - C_{\mathrm{U}}x + r\overline{W}^{(q+r)}(x-b)\rho_{a,b}^{(q)}(b;\,\tilde{f}) \nonumber \\[5pt]& \quad - \tilde{f}(b)\overline{W}^{(q+r)}(x-b) - \rho_{a, b}^{(q, r)}(x;\ \tilde{f}) - C_{\mathrm{U}}\frac{\psi'(0+)}{q} - \int^{x}_b\overline{W}^{(q + r)}(x - y)\tilde{f}'(y)\,\mathrm{d}y, \end{align}

where

\begin{equation} \Gamma(a, b) \;:\!=\; \int^{\infty}_a \tilde{f}'(y) Z^{(q)}(b - y, \Phi_{q + r})\, \mathrm{d} y + \frac{r}{\Phi_{q + r}} (C_{\mathrm{U}} + C_{\mathrm{D}}), \quad a \lt b. \end{equation}

\begin{equation} \Gamma(a, b) \;:\!=\; \int^{\infty}_a \tilde{f}'(y) Z^{(q)}(b - y, \Phi_{q + r})\, \mathrm{d} y + \frac{r}{\Phi_{q + r}} (C_{\mathrm{U}} + C_{\mathrm{D}}), \quad a \lt b. \end{equation}

4.2. Smoothness of

$\boldsymbol{{v}}_{\boldsymbol{{a, b}}}$

We now analyze the smoothness of the NPV of costs as computed in (4.10).

Lemma 4.4. For

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}\backslash \{a\}$

,

$x \in \mathbb{R}\backslash \{a\}$

,

\begin{align} v'_{a, b}(x) & = \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q, r)}_{a, b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt \tilde{f}') \nonumber \\[5pt] & \quad - \int^{x}_{b} W^{(q + r)}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) \overline{W}^{(q + r)}(x - b) - C_{\mathrm{U}}. \end{align}

\begin{align} v'_{a, b}(x) & = \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q, r)}_{a, b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt \tilde{f}') \nonumber \\[5pt] & \quad - \int^{x}_{b} W^{(q + r)}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) \overline{W}^{(q + r)}(x - b) - C_{\mathrm{U}}. \end{align}

If X is of unbounded variation, for

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}\backslash \{a\}$

,

$x \in \mathbb{R}\backslash \{a\}$

,

\begin{align} v''_{a, b}(x) & = \frac{\Gamma(a,b)}{Z^{(q)}(b-a,\Phi_{q+r})}\bigg(\frac{\mathrm{d}}{\mathrm{d}x}W^{(q,r)}_{a,b}(x)\bigg) \nonumber \\[5pt] & \quad - \bigg(\int^{b}_a W^{(q)'}(x - y)\tilde{f}'(y)\, \mathrm{d} y + r\int^{x}_b W^{(q + r)'}(x - y)\rho_{a, b}^{(q)}(y;\; \tilde{f}')\, \mathrm{d} y\bigg) \nonumber \\[5pt] & \quad - \int^{x}_{b} W^{(q + r)'}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) W^{(q + r)}(x - b). \end{align}

\begin{align} v''_{a, b}(x) & = \frac{\Gamma(a,b)}{Z^{(q)}(b-a,\Phi_{q+r})}\bigg(\frac{\mathrm{d}}{\mathrm{d}x}W^{(q,r)}_{a,b}(x)\bigg) \nonumber \\[5pt] & \quad - \bigg(\int^{b}_a W^{(q)'}(x - y)\tilde{f}'(y)\, \mathrm{d} y + r\int^{x}_b W^{(q + r)'}(x - y)\rho_{a, b}^{(q)}(y;\; \tilde{f}')\, \mathrm{d} y\bigg) \nonumber \\[5pt] & \quad - \int^{x}_{b} W^{(q + r)'}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) W^{(q + r)}(x - b). \end{align}

The proof of Lemma 4.4 is provided in Appendix A.3. The derivative

$({\mathrm{d}}/{\mathrm{d}x})W^{(q, r)}_{a, b}(x)$

in (4.13) is well-defined for

$({\mathrm{d}}/{\mathrm{d}x})W^{(q, r)}_{a, b}(x)$

in (4.13) is well-defined for

$x \neq a$

in light of (4.5) and the smoothness of scale functions as in [Reference Kuznetsov, Kyprianou and Rivero11, Lemma 2.4]. In the remainder of this paper, we call a function sufficiently smooth if it is continuously differentiable on

$x \neq a$

in light of (4.5) and the smoothness of scale functions as in [Reference Kuznetsov, Kyprianou and Rivero11, Lemma 2.4]. In the remainder of this paper, we call a function sufficiently smooth if it is continuously differentiable on

$\mathbb{R}$

when X is of bounded variation and twice continuously differentiable on

$\mathbb{R}$

when X is of bounded variation and twice continuously differentiable on

$\mathbb{R}$

when X is of unbounded variation.

$\mathbb{R}$

when X is of unbounded variation.

The following results establish the equivalence between our approach and the classical approach based on the smooth-fit principle.

Proposition 4.1. For

$a \lt b$

, the function

$a \lt b$

, the function

$x \mapsto v_{a, b}(x)$

is sufficiently smooth if and only if

$x \mapsto v_{a, b}(x)$

is sufficiently smooth if and only if

$\Gamma(a,b) = 0$

.

$\Gamma(a,b) = 0$

.

Proof. By Lemma 4.4, we have

\begin{equation*} v'_{a, b}(a{-}) = -C_{\mathrm{U}}, \qquad v'_{a, b}(a+) = -C_{\mathrm{U}} + \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q)}(0) \end{equation*}

\begin{equation*} v'_{a, b}(a{-}) = -C_{\mathrm{U}}, \qquad v'_{a, b}(a+) = -C_{\mathrm{U}} + \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q)}(0) \end{equation*}

in the case that X is of bounded variation, and

\begin{equation*} v''_{a, b}(a{-}) = 0, \qquad v''_{a, b}(a+) = \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q)'}(0{+}) \end{equation*}

\begin{equation*} v''_{a, b}(a{-}) = 0, \qquad v''_{a, b}(a+) = \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} W^{(q)'}(0{+}) \end{equation*}

when X is of unbounded variation. Now, by applying [Reference Kuznetsov, Kyprianou and Rivero11, Lemmas 3.1 and 3.2], we find that the function

$x \mapsto v_{a, b}(x)$

is sufficiently smooth if and only if

$x \mapsto v_{a, b}(x)$

is sufficiently smooth if and only if

$\Gamma(a,b) = 0$

.

$\Gamma(a,b) = 0$

.

Define the partial derivative of

$\Gamma$

as follows:

$\Gamma$

as follows:

\begin{align} \gamma(a, b) \;:\!=\; \frac{\partial}{\partial b} \Gamma(a, b) & = \Phi_{q+r}\int^{\infty}_a\tilde{f}'(y)Z^{(q)}(b - y,\Phi_{q + r})\,\mathrm{d}y - r\rho_{a, b}^{(q)}(b;\kern3pt \tilde{f}') \nonumber \\[5pt]& = \Phi_{q+r}\Gamma(a,b) - r\big(C_{\mathrm{U}} + C_{\mathrm{D}} + \rho_{a,b}^{(q)}(b;\kern3pt \tilde{f}')\big), \quad a \lt b. \end{align}

\begin{align} \gamma(a, b) \;:\!=\; \frac{\partial}{\partial b} \Gamma(a, b) & = \Phi_{q+r}\int^{\infty}_a\tilde{f}'(y)Z^{(q)}(b - y,\Phi_{q + r})\,\mathrm{d}y - r\rho_{a, b}^{(q)}(b;\kern3pt \tilde{f}') \nonumber \\[5pt]& = \Phi_{q+r}\Gamma(a,b) - r\big(C_{\mathrm{U}} + C_{\mathrm{D}} + \rho_{a,b}^{(q)}(b;\kern3pt \tilde{f}')\big), \quad a \lt b. \end{align}

Note that

$\gamma(a, b)$

is independent of the values of

$\gamma(a, b)$

is independent of the values of

$C_{\mathrm{U}}$

and

$C_{\mathrm{U}}$

and

$C_{\mathrm{D}}$

, as the second equality of (4.14) holds by adding and subtracting

$C_{\mathrm{D}}$

, as the second equality of (4.14) holds by adding and subtracting

$r(C_{\mathrm{U}} + C_{\mathrm{D}})$

, together with (4.11). This equality is included only to simplify complex expressions that appear later in the paper. The proof of Lemma 4.2 is presented in Appendix A.4.

$r(C_{\mathrm{U}} + C_{\mathrm{D}})$

, together with (4.11). This equality is included only to simplify complex expressions that appear later in the paper. The proof of Lemma 4.2 is presented in Appendix A.4.

Lemma 4.5. For

$a \lt b$

and

$a \lt b$

and

$x \in \mathbb{R}$

, we have

$x \in \mathbb{R}$

, we have

\begin{align} v^{f'}_{a, b}(x) & \;:\!=\; \mathbb{E}_x\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{a, b}(t))\,\mathrm{d}t\bigg] \nonumber \\[5pt]& = \frac{\gamma(a,b)}{qZ^{(q)}(b-a;\,\Phi_{q+r})}Z^{(q,r)}_{a,b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt \tilde{f}') - \int^{x}_b W^{(q + r)}(x - y)\,\tilde{f}'(y)\,\mathrm{d}y \nonumber \\[5pt]& \quad - r\overline{W}^{(q + r)}(x - b)\bigg({-}\rho_{a b}^{(q)}(b;\kern3pt \tilde{f}') + \frac{Z^{(q)}(b - a)}{qZ^{(q)}(b - a;\; \Phi_{q + r})}\gamma(a, b)\bigg) - C_{\mathrm{U}}. \end{align}

\begin{align} v^{f'}_{a, b}(x) & \;:\!=\; \mathbb{E}_x\bigg[\int^\infty_0{\mathrm{e}}^{-qt} f'(Y^{a, b}(t))\,\mathrm{d}t\bigg] \nonumber \\[5pt]& = \frac{\gamma(a,b)}{qZ^{(q)}(b-a;\,\Phi_{q+r})}Z^{(q,r)}_{a,b}(x) - \rho_{a, b}^{(q, r)}(x;\kern3pt \tilde{f}') - \int^{x}_b W^{(q + r)}(x - y)\,\tilde{f}'(y)\,\mathrm{d}y \nonumber \\[5pt]& \quad - r\overline{W}^{(q + r)}(x - b)\bigg({-}\rho_{a b}^{(q)}(b;\kern3pt \tilde{f}') + \frac{Z^{(q)}(b - a)}{qZ^{(q)}(b - a;\; \Phi_{q + r})}\gamma(a, b)\bigg) - C_{\mathrm{U}}. \end{align}

In particular, at

$x = a$

and

$x = a$

and

$x = b$

,

$x = b$

,

\begin{align} v^{f'}_{a, b}(a) & = \frac{\gamma(a, b)}{qZ^{(q)}(b - a;\; \Phi_{q + r})} - C_{\mathrm{U}}, \end{align}

\begin{align} v^{f'}_{a, b}(a) & = \frac{\gamma(a, b)}{qZ^{(q)}(b - a;\; \Phi_{q + r})} - C_{\mathrm{U}}, \end{align}

\begin{align} v^{f'}_{a, b}(b) & = \frac{Z^{(q)}(b - a)}{qZ^{(q)}(b - a;\; \Phi_{q + r})}\gamma(a, b) - \rho_{a, b}^{(q)}(b;\; \tilde{f}') - C_{\mathrm{U}}. \end{align}

\begin{align} v^{f'}_{a, b}(b) & = \frac{Z^{(q)}(b - a)}{qZ^{(q)}(b - a;\; \Phi_{q + r})}\gamma(a, b) - \rho_{a, b}^{(q)}(b;\; \tilde{f}') - C_{\mathrm{U}}. \end{align}

Proposition 4.2. For

$a \lt b$

, the following statements are equivalent:

$a \lt b$

, the following statements are equivalent:

-

(i)

$v^{f'}_{a, b}(a) = -C_{\mathrm{U}}$

and

$v^{f'}_{a, b}(b) = C_{\mathrm{D}}$

. -

(ii)

$\Gamma(a, b) = 0$

and

$\gamma(a,b) = 0$

. -

(iii)

$v_{a, b}$

is sufficiently smooth, with

$v'_{a, b}(a) = -C_{\mathrm{U}}$

and

$v'_{a, b}(b) = C_{\mathrm{D}}$

.

Proof. For (i)

$\Longleftrightarrow$

(ii), first, by (4.16),

$\Longleftrightarrow$

(ii), first, by (4.16),

\begin{equation} v^{f'}_{a, b}(a) = -C_{\mathrm{U}} \Longleftrightarrow \gamma(a, b) = 0. \end{equation}

\begin{equation} v^{f'}_{a, b}(a) = -C_{\mathrm{U}} \Longleftrightarrow \gamma(a, b) = 0. \end{equation}

By (4.14), we have

\begin{equation} \rho_{a, b}^{(q)}(b;\; \tilde{f}') = \frac{\Phi_{q+r}\Gamma(a, b) - \gamma(a,b)}r - (C_{\mathrm{U}} + C_{\mathrm{D}}) . \end{equation}

\begin{equation} \rho_{a, b}^{(q)}(b;\; \tilde{f}') = \frac{\Phi_{q+r}\Gamma(a, b) - \gamma(a,b)}r - (C_{\mathrm{U}} + C_{\mathrm{D}}) . \end{equation}

Substituting (4.19) into (4.17), we have

\begin{equation*} v^{f'}_{a, b}(b) = -\frac{\Phi_{q+r}}{r}\Gamma(a, b) + \bigg(\frac{Z^{(q)}(b-a)}{qZ^{(q)}(b-a;\,\Phi_{q+r})} + \frac{1}{r}\bigg)\gamma(a,b) + C_{\mathrm{D}}. \end{equation*}

\begin{equation*} v^{f'}_{a, b}(b) = -\frac{\Phi_{q+r}}{r}\Gamma(a, b) + \bigg(\frac{Z^{(q)}(b-a)}{qZ^{(q)}(b-a;\,\Phi_{q+r})} + \frac{1}{r}\bigg)\gamma(a,b) + C_{\mathrm{D}}. \end{equation*}

The equivalence follows from the last equality and (4.18).

For (ii)

$\Longleftrightarrow$

(iii), substituting (4.19) in (4.12) with

$\Longleftrightarrow$

(iii), substituting (4.19) in (4.12) with

$x = b$

,

$x = b$

,

\begin{equation*} v'_{a, b}(b) = \bigg(\frac{W^{(q)}(b-a)}{Z^{(q)}(b-a,\Phi_{q+r})} - \frac{\Phi_{q+r}}{r}\bigg)\Gamma(a,b) + \frac{\gamma(a, b)}{r} + C_{\mathrm{D}}. \end{equation*}

\begin{equation*} v'_{a, b}(b) = \bigg(\frac{W^{(q)}(b-a)}{Z^{(q)}(b-a,\Phi_{q+r})} - \frac{\Phi_{q+r}}{r}\bigg)\Gamma(a,b) + \frac{\gamma(a, b)}{r} + C_{\mathrm{D}}. \end{equation*}

Thus,

$v'_{a, b}(b) = C_{\mathrm{D}}$

is equivalent to

$v'_{a, b}(b) = C_{\mathrm{D}}$

is equivalent to

$\gamma(a, b) = 0$

when

$\gamma(a, b) = 0$

when

$\Gamma(a, b) = 0$

. Finally, Lemma 4.1 shows the equivalence.

$\Gamma(a, b) = 0$

. Finally, Lemma 4.1 shows the equivalence.

4.3. Selection of barriers

The next step of our analysis involves establishing the existence of

$(a^*, b^*)$

satisfying

$(a^*, b^*)$

satisfying

\begin{equation*} \mathfrak{C}\colon v^{f'}_{a^*, b^*}(a^*) = -C_{\mathrm{U}} \quad \textrm{and} \quad v^{f'}_{a^*, b^*}(b^*) = C_{\mathrm{D}},\end{equation*}

\begin{equation*} \mathfrak{C}\colon v^{f'}_{a^*, b^*}(a^*) = -C_{\mathrm{U}} \quad \textrm{and} \quad v^{f'}_{a^*, b^*}(b^*) = C_{\mathrm{D}},\end{equation*}

which is, by Proposition 4.2, equivalent to

\begin{equation} \mathfrak{C}'\colon \Gamma(a^*,b^*) = \gamma(a^*, b^*) = 0.\end{equation}

\begin{equation} \mathfrak{C}'\colon \Gamma(a^*,b^*) = \gamma(a^*, b^*) = 0.\end{equation}

Recall

$\bar{a} = \inf\{a \in \mathbb{R}\colon \tilde{f}'(a) \geq 0\}$

as defined in Assumption 2.1(ii). We can immediately eliminate the half-line

$\bar{a} = \inf\{a \in \mathbb{R}\colon \tilde{f}'(a) \geq 0\}$

as defined in Assumption 2.1(ii). We can immediately eliminate the half-line

$[\bar{a}, \infty)$

from consideration for

$[\bar{a}, \infty)$

from consideration for

$a^*$

. Indeed, for

$a^*$

. Indeed, for

$a \geq \overline{a}$

, we have

$a \geq \overline{a}$

, we have

$\tilde{f}'(y + a) \geq \tilde{f}'(y + \bar{a}) \geq 0$

for all

$\tilde{f}'(y + a) \geq \tilde{f}'(y + \bar{a}) \geq 0$

for all

$y \geq 0$

by Assumption 2.1(i). Thus, from (4.11), we have

$y \geq 0$

by Assumption 2.1(i). Thus, from (4.11), we have

$\Gamma(a, b) \gt 0$

for

$\Gamma(a, b) \gt 0$

for

$b \gt a \geq \bar{a}$

. We show that, by decreasing the value of a from

$b \gt a \geq \bar{a}$

. We show that, by decreasing the value of a from

$\bar{a}$

, we reach

$\bar{a}$

, we reach

$a^*$

such that the function

$a^*$

such that the function

$b \mapsto \Gamma(a^*, b)$

starts at

$b \mapsto \Gamma(a^*, b)$

starts at

$\Gamma(a^*, a^*+) \gt 0$

and becomes tangent to the x-axis at

$\Gamma(a^*, a^*+) \gt 0$

and becomes tangent to the x-axis at

$b^*$

, where its partial derivative

$b^*$

, where its partial derivative

$\gamma(a^*, b^*)$

is zero.

$\gamma(a^*, b^*)$

is zero.

To facilitate the proof of the existence of

$(a^*, b^*)$

, we analyze the following auxiliary functions.

$(a^*, b^*)$

, we analyze the following auxiliary functions.

Lemma 4.6. For all

$a \in \mathbb{R}$

,

$a \in \mathbb{R}$

,

\begin{align} \Gamma_1(a) & \;:\!=\; \Gamma(a, a{+}) = \int^\infty_0{\mathrm{e}}^{-\Phi_{q + r} y} \tilde{f}'(y+a) \, \mathrm{d} y + \frac{r}{\Phi_{q+r}}(C_{\mathrm{U}} + C_{\mathrm{D}}), \end{align}

\begin{align} \Gamma_1(a) & \;:\!=\; \Gamma(a, a{+}) = \int^\infty_0{\mathrm{e}}^{-\Phi_{q + r} y} \tilde{f}'(y+a) \, \mathrm{d} y + \frac{r}{\Phi_{q+r}}(C_{\mathrm{U}} + C_{\mathrm{D}}), \end{align}

\begin{align} \Gamma_2(a) & \;:\!=\; \lim_{b \to \infty} \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} = \int^{\infty}_0{\mathrm{e}}^{-\Phi_q y} \tilde{f}'(y + a)\, \mathrm{d} y. \end{align}

\begin{align} \Gamma_2(a) & \;:\!=\; \lim_{b \to \infty} \frac{\Gamma(a, b)}{Z^{(q)}(b - a, \Phi_{q + r})} = \int^{\infty}_0{\mathrm{e}}^{-\Phi_q y} \tilde{f}'(y + a)\, \mathrm{d} y. \end{align}

The proof of Lemma 4.6 is deferred to Appendix A.5. We note that both

$a\mapsto \Gamma_1(a)$

and

$a\mapsto \Gamma_1(a)$

and

$a\mapsto \Gamma_2(a)$

are continuous. Moreover, both are strictly increasing on

$a\mapsto \Gamma_2(a)$

are continuous. Moreover, both are strictly increasing on

$({-}\infty, \bar{a})$

due to the convexity of

$({-}\infty, \bar{a})$

due to the convexity of

$\tilde{f}$

and Assumption 2.1(iii). Define their left inverses,

$\tilde{f}$

and Assumption 2.1(iii). Define their left inverses,

\begin{equation} \underline{a}_i \;:\!=\; \inf\{a \in \mathbb{R}\colon \Gamma_i(a) \geq 0\}, \quad i = 1,2.\end{equation}

\begin{equation} \underline{a}_i \;:\!=\; \inf\{a \in \mathbb{R}\colon \Gamma_i(a) \geq 0\}, \quad i = 1,2.\end{equation}

Observe that

$\underline{a}_1 \in [{-}\infty, \bar{a})$

and

$\underline{a}_1 \in [{-}\infty, \bar{a})$

and

$\underline{a}_2 \in ({-}\infty, \bar{a}).$

To establish that

$\underline{a}_2 \in ({-}\infty, \bar{a}).$

To establish that

$\underline{a}_2 \gt -\infty$

, note that by monotone convergence and the convexity of

$\underline{a}_2 \gt -\infty$

, note that by monotone convergence and the convexity of

$\tilde{f}$

, we have

$\tilde{f}$

, we have

$\Gamma_2(a) \xrightarrow{a \downarrow -\infty}\int^{\infty}_0{\mathrm{e}}^{-\Phi_q z} \tilde{f}'({-}\infty)\, \mathrm{d} z \in [{-}\infty, 0)$

. Hence,

$\Gamma_2(a) \xrightarrow{a \downarrow -\infty}\int^{\infty}_0{\mathrm{e}}^{-\Phi_q z} \tilde{f}'({-}\infty)\, \mathrm{d} z \in [{-}\infty, 0)$

. Hence,

$\underline{a}_2 \gt -\infty$

. To show that both

$\underline{a}_2 \gt -\infty$

. To show that both

$\underline{a}_1$

and

$\underline{a}_1$

and

$\underline{a}_2$

are upper bounded by

$\underline{a}_2$

are upper bounded by

$\bar{a}$

, note that by (2.2) and Assumption 2.1(ii), we have

$\bar{a}$

, note that by (2.2) and Assumption 2.1(ii), we have

\[ \Gamma_1(\bar{a}) = \int^\infty_0{\mathrm{e}}^{-\Phi_{q + r} y} \tilde{f}'(y + \bar{a})\, \mathrm{d} y + \frac{r}{\Phi_{q + r}}(C_{\mathrm{U}} + C_{\mathrm{D}}) \gt 0,\]

\[ \Gamma_1(\bar{a}) = \int^\infty_0{\mathrm{e}}^{-\Phi_{q + r} y} \tilde{f}'(y + \bar{a})\, \mathrm{d} y + \frac{r}{\Phi_{q + r}}(C_{\mathrm{U}} + C_{\mathrm{D}}) \gt 0,\]

which implies

$\bar{a} \gt \underline{a}_1$

. Additionally, by Assumption 2.1(iii),

$\bar{a} \gt \underline{a}_1$

. Additionally, by Assumption 2.1(iii),

$\Gamma_2(\bar{a}) \gt 0$

, which implies

$\Gamma_2(\bar{a}) \gt 0$

, which implies

$\bar{a} \gt \underline{a}_2$

.

$\bar{a} \gt \underline{a}_2$

.

Remark 4.1. The value

$\underline{a}_2$

is the optimal barrier in the setting where only upward control is permitted; see [Reference Yamazaki23, Section 7]. This follows from the definition of

$\underline{a}_2$

is the optimal barrier in the setting where only upward control is permitted; see [Reference Yamazaki23, Section 7]. This follows from the definition of

$\underline{a}_2$

in (4.23), which gives

$\underline{a}_2$

in (4.23), which gives

\begin{equation*} 0 = \frac{\Phi_{q}}{q}\Gamma_2(\underline{a}_2) = \frac{\Phi_{q}}{q}\int^\infty_0{\mathrm{e}}^{-\Phi_{q}y}f'(y + \underline{a}_2)\,\mathrm{d}y + C_{\mathrm{U}} = \mathbb{E}_{\underline{a}_2}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{\underline{a}_2,\infty}(t))\,\mathrm{d}t\bigg] + C_{\mathrm{U}}, \end{equation*}

\begin{equation*} 0 = \frac{\Phi_{q}}{q}\Gamma_2(\underline{a}_2) = \frac{\Phi_{q}}{q}\int^\infty_0{\mathrm{e}}^{-\Phi_{q}y}f'(y + \underline{a}_2)\,\mathrm{d}y + C_{\mathrm{U}} = \mathbb{E}_{\underline{a}_2}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{\underline{a}_2,\infty}(t))\,\mathrm{d}t\bigg] + C_{\mathrm{U}}, \end{equation*}

where

$Y^{\underline{a}_2, \infty}$

denotes the process reflected from below at the level

$Y^{\underline{a}_2, \infty}$

denotes the process reflected from below at the level

$\underline{a}_2$

, and the last equality holds by [Reference Kuznetsov, Kyprianou and Rivero11, Theorem 2.8(iii)]. Thus,

$\underline{a}_2$

, and the last equality holds by [Reference Kuznetsov, Kyprianou and Rivero11, Theorem 2.8(iii)]. Thus,

\begin{align} \mathbb{E}_{\underline{a}_2}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{\underline{a}_2,\infty}(t))\,\mathrm{d}t\bigg] = -C_{\mathrm{U}}. \end{align}

\begin{align} \mathbb{E}_{\underline{a}_2}\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{\underline{a}_2,\infty}(t))\,\mathrm{d}t\bigg] = -C_{\mathrm{U}}. \end{align}

Moreover, under certain conditions in our current setting, an optimal strategy is the barrier strategy that continuously reflects the state process from below at the lower barrier

$\underline{a}_2$

, as summarized in the following remark.

$\underline{a}_2$

, as summarized in the following remark.

Remark 4.2. Suppose that Assumption 2.1(iii) fails to hold (thus

$f' \leq qC_{\mathrm{D}}$

on

$f' \leq qC_{\mathrm{D}}$

on

$\mathbb{R}$

) and all other standing assumptions, including Assumptions 2.1(i) and (ii), hold. Then,

$\mathbb{R}$

) and all other standing assumptions, including Assumptions 2.1(i) and (ii), hold. Then,

-

• not activating the downward control

$(L^\pi(t);\; t \geq 0)$

is optimal; -

•

$v_{\underline{a}_2, \infty}(x) = \inf_{\pi \in \Pi} v^\pi(x)$

for all

$x \in \mathbb{R}$

, where

\begin{equation*} v_{\underline{a}_2, \infty}(x) \;:\!=\; \mathbb{E}_x\bigg[\int^\infty_0{\mathrm{e}}^{-qt}f(Y^{\underline{a}_2,\infty}(t))\,\mathrm{d}t + C_{\mathrm{U}}\int_{[0,\infty)}{\mathrm{e}}^{-qt}\,\mathrm{d}R^{\underline{a}_2,\infty}(t)\bigg]. \end{equation*}

Verifying the above remark is straightforward. The first statement holds since the downward control cost is no less than the reduction in the running cost. The second statement holds due to the first and [Reference Yamazaki23, Theorem 7.1].

As a next step towards establishing the existence of

$(a^*, b^*)$

, we define

$(a^*, b^*)$

, we define

\[ \underline{\Gamma}(a) \;:\!=\; \inf_{b \gt a} \Gamma(a, b), \quad a \in \mathbb{R}.\]

\[ \underline{\Gamma}(a) \;:\!=\; \inf_{b \gt a} \Gamma(a, b), \quad a \in \mathbb{R}.\]

The proofs of the following two lemmas are provided in Appendices A.6 and A.7.

Lemma 4.7. (i)

$\underline{\Gamma}(\bar{a}) \gt 0$

; (ii)

$\underline{\Gamma}(\bar{a}) \gt 0$

; (ii)

$\underline{\Gamma}(\underline{a}_1 \vee \underline{a}_2) \lt 0$

.

$\underline{\Gamma}(\underline{a}_1 \vee \underline{a}_2) \lt 0$

.

Lemma 4.8. The mapping

$a \mapsto \underline{\Gamma}(a)$

is continuous and strictly increasing on

$a \mapsto \underline{\Gamma}(a)$

is continuous and strictly increasing on

$(\underline{a}_1 \vee \underline{a}_2, \bar{a})$

.

$(\underline{a}_1 \vee \underline{a}_2, \bar{a})$

.

We are now ready to establish the existence and uniqueness of the candidate barriers.

Proposition 4.3. There exists a unique pair

$(a^*, b^*)$

such that

$(a^*, b^*)$

such that

$\mathfrak{C}$

holds.

$\mathfrak{C}$

holds.

Proof. By Lemmas 4.7 and 4.8, there exists a unique root

$a^* \in (\underline{a}_1 \vee \underline{a}_2, \infty)$

such that

$a^* \in (\underline{a}_1 \vee \underline{a}_2, \infty)$

such that

$\underline{\Gamma}(a^*) = 0$

. Moreover, because

$\underline{\Gamma}(a^*) = 0$

. Moreover, because

$\Gamma(a^*, a^*+) \gt 0$

and

$\Gamma(a^*, a^*+) \gt 0$

and

$\lim_{b \to \infty}\Gamma(a^*,b) = \infty$

in view of the definitions of

$\lim_{b \to \infty}\Gamma(a^*,b) = \infty$

in view of the definitions of

$\underline{a}_1$

and

$\underline{a}_1$

and

$\underline{a}_2$

, the minimum of

$\underline{a}_2$

, the minimum of

$b \mapsto \Gamma(a^*,b)$

is attained at some

$b \mapsto \Gamma(a^*,b)$

is attained at some

$b^* \in (a^*, \infty)$

. By the continuity of

$b^* \in (a^*, \infty)$

. By the continuity of

$b \mapsto \gamma(a^*,b)$

, it must hold that

$b \mapsto \gamma(a^*,b)$

, it must hold that

$\gamma(a^*,b^*)=0$

. Thus,

$\gamma(a^*,b^*)=0$

. Thus,

$\mathfrak{C}'$

, or equivalently,

$\mathfrak{C}'$

, or equivalently,

$\mathfrak{C}$

, holds. Moreover, such a

$\mathfrak{C}$

, holds. Moreover, such a

$b^*$

is unique. To establish uniqueness, recall that

$b^*$

is unique. To establish uniqueness, recall that

$b^*$

must satisfy

$b^*$

must satisfy

$v^{f'}_{a^*, b^*}(b^*) = C_{\mathrm{D}}$

, as required by

$v^{f'}_{a^*, b^*}(b^*) = C_{\mathrm{D}}$

, as required by

$\mathfrak{C}$

. Given the probabilistic expression

$\mathfrak{C}$

. Given the probabilistic expression

$v^{f'}_{a^*, b}(b) = \mathbb{E}_b \big[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{a^*,b}(t))\,\mathrm{d}t\big]$

, it is clear that the mapping

$v^{f'}_{a^*, b}(b) = \mathbb{E}_b \big[\int^\infty_0{\mathrm{e}}^{-qt}f'(Y^{a^*,b}(t))\,\mathrm{d}t\big]$

, it is clear that the mapping

$b \mapsto v^{f'}_{a^*, b}(b)$

is non-decreasing on

$b \mapsto v^{f'}_{a^*, b}(b)$

is non-decreasing on

$(a^*, \infty)$

. Further, by applying the argument used in the proof of Lemma 4.7, we see that

$(a^*, \infty)$

. Further, by applying the argument used in the proof of Lemma 4.7, we see that

$b \mapsto v^{f'}_{a^*, b}(b)$

is, in fact, strictly increasing. Hence, there is exactly one

$b \mapsto v^{f'}_{a^*, b}(b)$

is, in fact, strictly increasing. Hence, there is exactly one

$b^* \gt a^*$

such that

$b^* \gt a^*$

such that

$\mathfrak{C}'$

(equivalently

$\mathfrak{C}'$

(equivalently

$\mathfrak{C}$

) holds.

$\mathfrak{C}$

) holds.

4.4. Verification

As the final step in completing the proof of Theorem 3.1, we establish the optimality of the periodic–classical barrier strategy

$\pi_{a^*, b^*}$

. This is achieved by applying the conventional verification technique based on Itô’s lemma, which has been employed in previous works such as [Reference Avram, Kyprianou and Pistorius4, Reference Baurdoux and Yamazaki5, Reference Pérez, Yamazaki and Bensoussan22], among others.

$\pi_{a^*, b^*}$

. This is achieved by applying the conventional verification technique based on Itô’s lemma, which has been employed in previous works such as [Reference Avram, Kyprianou and Pistorius4, Reference Baurdoux and Yamazaki5, Reference Pérez, Yamazaki and Bensoussan22], among others.

Let

$\mathcal{L}$

be the infinitesimal generator associated with X. When applied to a sufficiently smooth function

$\mathcal{L}$

be the infinitesimal generator associated with X. When applied to a sufficiently smooth function

$h\colon \mathbb{R} \to \mathbb{R}$

, the following holds for any

$h\colon \mathbb{R} \to \mathbb{R}$

, the following holds for any

$x\in \mathbb{R}$

:

$x\in \mathbb{R}$

:

\begin{equation*} \mathcal{L}h(x) \;:\!=\; \gamma h'(x) + \frac{\sigma^2}{2}h''(x) + \int_{({-}\infty, 0)} h(x + z) - h(x) - h'(x) z \mathbf{1}_{\{-1 \lt z \lt 0\}} \,\mu(\mathrm{d} z).\end{equation*}

\begin{equation*} \mathcal{L}h(x) \;:\!=\; \gamma h'(x) + \frac{\sigma^2}{2}h''(x) + \int_{({-}\infty, 0)} h(x + z) - h(x) - h'(x) z \mathbf{1}_{\{-1 \lt z \lt 0\}} \,\mu(\mathrm{d} z).\end{equation*}

Additionally, we define an operator

$\mathcal{M}$

for a measurable function h,

$\mathcal{M}$

for a measurable function h,

\begin{equation*} \mathcal{M}h(x) \;:\!=\; \inf_{l \geq 0} \{C_{\mathrm{D}}l + h(x - l)\},\end{equation*}

\begin{equation*} \mathcal{M}h(x) \;:\!=\; \inf_{l \geq 0} \{C_{\mathrm{D}}l + h(x - l)\},\end{equation*}

which has been used to establish the optimality of barrier-type strategies in periodic control problems, as in [Reference Mata, Moreno-Franco, Noba and Pérez17, Reference Pérez, Yamazaki and Bensoussan22]. The following lemma gives the conditions that are sufficient for the optimality of

$\pi_{a^*, b^*}$

; its proof is provided in Appendix A.8.

$\pi_{a^*, b^*}$

; its proof is provided in Appendix A.8.

Lemma 4.9. Let

$w\colon \mathbb{R} \to \mathbb{R}$

be the NPV of costs under an admissible strategy. Suppose that w has the following properties:

$w\colon \mathbb{R} \to \mathbb{R}$

be the NPV of costs under an admissible strategy. Suppose that w has the following properties:

-

• it is sufficiently smooth on

$\mathbb{R}$

, -

• it has at most polynomial growth, and

-

• it satisfies

$w' \geq -C_{\mathrm{U}}$

.

Further suppose that

$(\mathcal{L}-q)w(x) + r(\mathcal{M}w(x) - w(x)) + f(x) \geq 0$

,

$(\mathcal{L}-q)w(x) + r(\mathcal{M}w(x) - w(x)) + f(x) \geq 0$

,

$x\in \mathbb{R}$

, and that, for every admissible strategy

$x\in \mathbb{R}$

, and that, for every admissible strategy

$\pi \in \Pi$

,

$\pi \in \Pi$

,

$\limsup_{t, n \uparrow \infty} \mathbb{E}_x[{\mathrm{e}}^{-q(t\wedge \tau_n)} w(Y^\pi(t\wedge \tau_n))] \leq 0,$

where

$\limsup_{t, n \uparrow \infty} \mathbb{E}_x[{\mathrm{e}}^{-q(t\wedge \tau_n)} w(Y^\pi(t\wedge \tau_n))] \leq 0,$

where

$\tau_n \;:\!=\; \inf\{t \geq 0\colon |Y^{\pi}(t)| \gt n\}$

. Under these conditions, w coincides with the value function, i.e.

$\tau_n \;:\!=\; \inf\{t \geq 0\colon |Y^{\pi}(t)| \gt n\}$

. Under these conditions, w coincides with the value function, i.e.

$w(x) = v(x) = \inf_{\pi \in \Pi} v^\pi(x)$

.

$w(x) = v(x) = \inf_{\pi \in \Pi} v^\pi(x)$

.

In the remainder of this section, we show that the conditions in Lemma 4.9 are satisfied for the function

$v_{a^*, b^*}$

. As a first step, by Lemma 4.1,

$v_{a^*, b^*}$

. As a first step, by Lemma 4.1,

$v_{a^*, b^*}$

is sufficiently smooth. Moreover, by Assumption 2.2 in conjunction with the linearity of

$v_{a^*, b^*}$

is sufficiently smooth. Moreover, by Assumption 2.2 in conjunction with the linearity of

$x \mapsto v_{a^*, b^*}(x)$

below

$x \mapsto v_{a^*, b^*}(x)$

below

$a^*$

, the integral component of

$a^*$

, the integral component of

$\mathcal{L}v_{a^*, b^*}$

is finite on

$\mathcal{L}v_{a^*, b^*}$

is finite on

$\mathbb{R}$

. Thus,

$\mathbb{R}$

. Thus,

$\mathcal{L}v_{a^*, b^*}$

makes sense everywhere on

$\mathcal{L}v_{a^*, b^*}$

makes sense everywhere on

$\mathbb{R}$

.

$\mathbb{R}$

.

Next, we establish the related properties for the computation of

$\mathcal{M} v_{a^*,b^*}$

. We note that, with the condition

$\mathcal{M} v_{a^*,b^*}$

. We note that, with the condition

$\mathfrak{C}'$

, the function

$\mathfrak{C}'$

, the function

$v_{a^*, b^*}$

is simplified. By

$v_{a^*, b^*}$

is simplified. By

$\mathfrak{C}'$

and (4.12), we have

$\mathfrak{C}'$

and (4.12), we have

\begin{equation} v'_{a^*, b^*}(x) = - \rho_{a^*, b^*}^{(q, r)}(x;\; \tilde{f}') - \int^{x}_{b^*} W^{(q + r)}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) \overline{W}^{(q + r)}(x - b^*) - C_{\mathrm{U}}.\end{equation}

\begin{equation} v'_{a^*, b^*}(x) = - \rho_{a^*, b^*}^{(q, r)}(x;\; \tilde{f}') - \int^{x}_{b^*} W^{(q + r)}(x - y) \tilde{f}'(y)\, \mathrm{d} y - r(C_{\mathrm{U}} + C_{\mathrm{D}}) \overline{W}^{(q + r)}(x - b^*) - C_{\mathrm{U}}.\end{equation}

Proposition 4.4.

-

(i)

$v^{f'}_{a^*, b^*}(x) = v'_{a^*, b^*}(x)$

for all

$x \in \mathbb{R}$

. -

(ii)

$x \mapsto v_{a^*, b^*}(x)$

is convex on

$\mathbb{R}$

. -

(iii)

$v'_{a^*, b^*}(x) \geq -C_{\mathrm{U}}$

for all

$x \in \mathbb{R}$

.

Proof.

-

(i) By Proposition 4.2, we have

$v'_{a^*, b^*}(b^*) = C_{\mathrm{D}}$

. Combining this with the expression for

$v'_{a^*, b^*}$

in (4.25), we get

$C_{\mathrm{D}} = -\rho_{a^*, b^*}^{(q)}(b^*;\; \tilde{f}') - C_{\mathrm{U}}$

. Substituting this and

$\gamma(a^*, b^*) = 0$

into (4.15), the function

$v^{f'}_{a^*, b^*}$

matches (4.25). -

(ii) By the convexity of f and the monotonicity of

$Y^{a^*, b^*}$

in the starting point, the mapping

$x \mapsto v^{f'}_{a^*, b^*}(x)$

is monotone. Hence, by (i),

$v_{a^*, b^*}$

is convex. -

(iii) By (ii) and as

$v'_{a^*, b^*}(x) = -C_{\mathrm{U}}$

for

$x \in ({-}\infty, a^*]$

,

$v'_{a^*, b^*}(x) \geq -C_{\mathrm{U}}$

for all

$x \in \mathbb{R}$

.

As a direct consequence of Proposition 4.4(ii) and the condition

$\mathfrak{C}$

,

$\mathfrak{C}$

,

$\mathcal{M} v_{a^*,b^*}$

has the following characterization.

$\mathcal{M} v_{a^*,b^*}$

has the following characterization.

Corollary 4.1.

\begin{equation*} \mathcal{M}v_{a^*, b^*}(x) = \begin{cases} v_{a^*, b^*}(x), & x \lt b^*, \\[5pt] C_{\mathrm{D}}(x - b^*) + v_{a^*, b^*}(b^*), & x \geq b^*. \end{cases} \end{equation*}

\begin{equation*} \mathcal{M}v_{a^*, b^*}(x) = \begin{cases} v_{a^*, b^*}(x), & x \lt b^*, \\[5pt] C_{\mathrm{D}}(x - b^*) + v_{a^*, b^*}(b^*), & x \geq b^*. \end{cases} \end{equation*}

Furthermore, standard computations lead to the following characterization of

$(\mathcal{L} - q) v_{a^*, b^*}$

, with the proof given in Appendix A.9.

$(\mathcal{L} - q) v_{a^*, b^*}$

, with the proof given in Appendix A.9.

Lemma 4.10.

\begin{equation*} (\mathcal{L} - q) v_{a^*, b^*}(x) + f(x) = \begin{cases} \tilde{f}(x) - \tilde{f}(a^*), & x \leq a^*, \\[5pt] 0, & a^* \lt x \lt b^*, \\[5pt] -r(v_{a^*, b^*}(b^*) - v_{a^*, b^*}(x) + C_{\mathrm{D}}(x - b^*)), & x \geq b^*. \end{cases} \end{equation*}

\begin{equation*} (\mathcal{L} - q) v_{a^*, b^*}(x) + f(x) = \begin{cases} \tilde{f}(x) - \tilde{f}(a^*), & x \leq a^*, \\[5pt] 0, & a^* \lt x \lt b^*, \\[5pt] -r(v_{a^*, b^*}(b^*) - v_{a^*, b^*}(x) + C_{\mathrm{D}}(x - b^*)), & x \geq b^*. \end{cases} \end{equation*}

The polynomial growth of

$v_{a^*, b^*}$

can be established using the proof technique in [Reference Pérez, Yamazaki and Bensoussan22, Lemma 4.7]. As the method is nearly identical, the proof of Lemma 4.11 is omitted. The proof of Lemma 4.12 is presented in Appendix A.10.

$v_{a^*, b^*}$

can be established using the proof technique in [Reference Pérez, Yamazaki and Bensoussan22, Lemma 4.7]. As the method is nearly identical, the proof of Lemma 4.11 is omitted. The proof of Lemma 4.12 is presented in Appendix A.10.

Lemma 4.11. The function

$x \mapsto v_{a^*, b^*}(x)$

is of polynomial growth.

$x \mapsto v_{a^*, b^*}(x)$

is of polynomial growth.

Lemma 4.12. For all admissible strategies

$\pi \in \Pi$

,

$\pi \in \Pi$

,

$$\limsup_{t,n\uparrow\infty}\mathbb{E}_x[{\mathrm{e}}^{-q(t\wedge\tau_n)}v_{a^*,b^*}(Y^\pi(t\wedge\tau_n))] \leq 0.$$

$$\limsup_{t,n\uparrow\infty}\mathbb{E}_x[{\mathrm{e}}^{-q(t\wedge\tau_n)}v_{a^*,b^*}(Y^\pi(t\wedge\tau_n))] \leq 0.$$

Having verified that

$v_{a^*, b^*}$

satisfies the conditions of Lemma 4.9, its optimality is a direct consequence of the lemma. We now complete the proof of Theorem 3.1, as stated in Section 3.

$v_{a^*, b^*}$

satisfies the conditions of Lemma 4.9, its optimality is a direct consequence of the lemma. We now complete the proof of Theorem 3.1, as stated in Section 3.

Proof of Theorem

3.1. First, by Proposition 4.2 and Lemmas 4.4 and 4.11, the function

$v_{a^*, b^*}$

is sufficiently smooth on

$v_{a^*, b^*}$

is sufficiently smooth on

$\mathbb{R}$

, has polynomial growth, and satisfies

$\mathbb{R}$

, has polynomial growth, and satisfies

$v_{a^*, b^*}'\geq -C_{\mathrm{U}}$

. Additionally, by Corollary 4.1 and Lemma 4.10, we have

$v_{a^*, b^*}'\geq -C_{\mathrm{U}}$

. Additionally, by Corollary 4.1 and Lemma 4.10, we have

-

• For

$x \leq a^*$

,

$(\mathcal{L}-q)v_{a^*, b^*}(x) + r(\mathcal{M}v_{a^*, b^*}(x) - v_{a^*, b^*}(x)) + f(x) = \tilde{f}(x)-\tilde{f}(a^*) \geq 0$

, where the inequality holds because

$a^* \lt \bar{a}$

, and by Assumption 2.1(ii). -

• For

$x \gt a^*$

,

$(\mathcal{L}-q)v_{a^*, b^*}(x) + r(\mathcal{M}v_{a^*, b^*}(x) - v_{a^*, b^*}(x)) + f(x) = 0$

.

Hence,

$(\mathcal{L}-q)v_{a^*, b^*}(x) + r(\mathcal{M}v_{a^*, b^*}(x) - v_{a^*, b^*}(x)) + f(x) \geq 0$

,

$(\mathcal{L}-q)v_{a^*, b^*}(x) + r(\mathcal{M}v_{a^*, b^*}(x) - v_{a^*, b^*}(x)) + f(x) \geq 0$

,

$x\in \mathbb{R}$

. Since

$x\in \mathbb{R}$

. Since

$v_{a^*,b^*}$

is the NPV of costs under the admissible strategy

$v_{a^*,b^*}$

is the NPV of costs under the admissible strategy

$\pi_{a^*, b^*}$

, by applying Lemma 4.9, we have

$\pi_{a^*, b^*}$

, by applying Lemma 4.9, we have

$v_{a^*, b^*}(x) = v(x)$

for all

$v_{a^*, b^*}(x) = v(x)$

for all

$x \in \mathbb{R}$

.

$x \in \mathbb{R}$

.

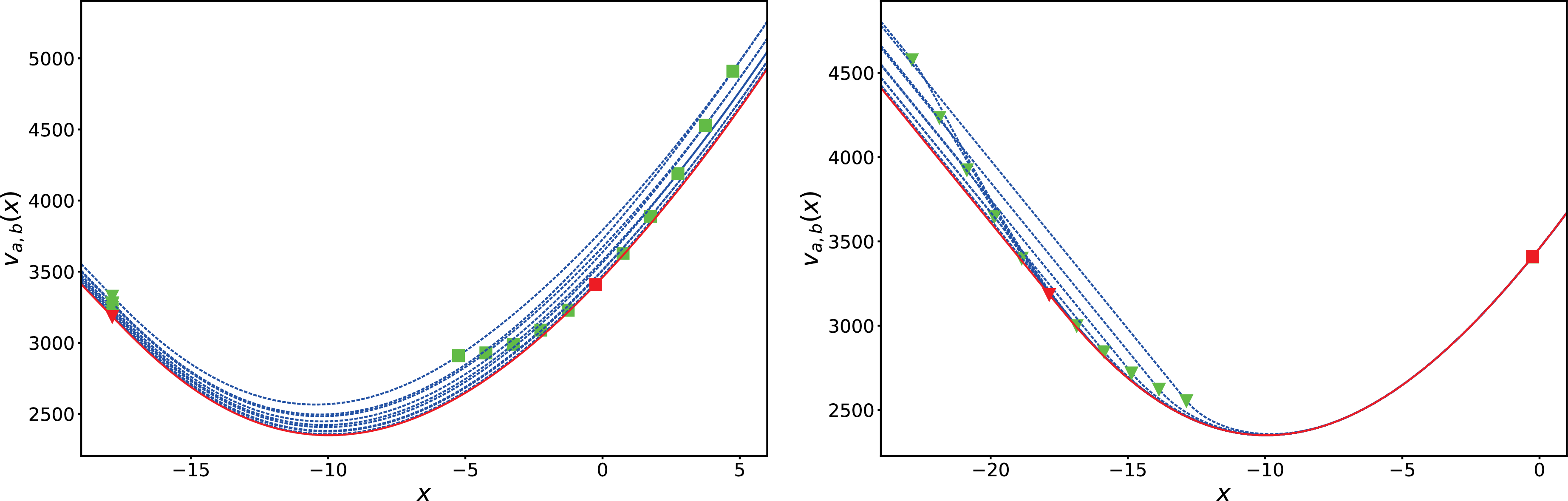

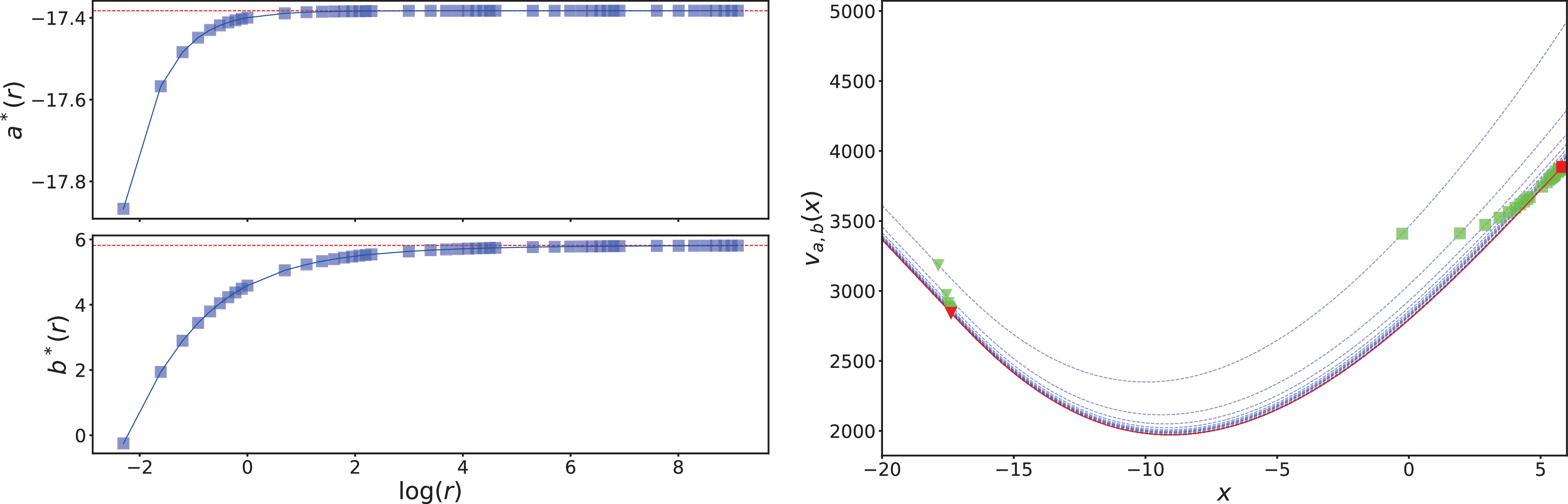

5. Numerical example

This section presents a numerical study. Let

$f(x) = x^2$

and X be a spectrally negative Lévy process with exponential jumps given by

$f(x) = x^2$

and X be a spectrally negative Lévy process with exponential jumps given by

$X(t) = x + t + B(t) - \sum^{N(t)}_{n = 1} Z_n$

, where

$X(t) = x + t + B(t) - \sum^{N(t)}_{n = 1} Z_n$

, where

$B = (B(t);\; t\geq 0)$

is a standard Brownian motion,

$B = (B(t);\; t\geq 0)$

is a standard Brownian motion,

$N = (N(t);\; t\geq 0)$

is a Poisson process with arrival rate

$N = (N(t);\; t\geq 0)$

is a Poisson process with arrival rate

$\lambda = 0.2$

, and

$\lambda = 0.2$

, and

$\{Z_n\}_{n \geq 1}$