1 Introduction

The Middle East and North Africa (MENA) region,Footnote 1 gathering countries with different cultures, languages, and economic conditions, plays an important role in the global economy due to its strategic location, its abundant natural resources, and historical significance as a crossroads of trade. The region is located at the crossroads of Europe, Asia, and Africa, making it a vital commerce junction. It is abundant in natural resources, particularly oil and natural gas, therefore playing a significant role in the global energy market. Moreover, it is home to some of the world’s earliest civilizations that developed sophisticated trade networks and maritime routes, contributing to the region’s historical significance as a trade hub.

Indeed, the famous ancient Silk Road and Incense Route, which facilitated the exchange of goods and cultures between the East and the West, passed through the MENA region. The Silk Road connecting China with the Mediterranean passed through MENA cities such as Aleppo in Syria and was famous for trading silk, spices, precious stones, and other luxury goods. The Incense Route, connecting the Arabian Peninsula with the Mediterranean, was known for the trade of frankincense, myrrh, and other valuable goods from Yemen and Oman. During the Islamic Golden Age, between the eighth and fourteenth centuries, the MENA region in general, and Baghdad in particular, became a hub of intellectual, cultural, and economic activities. Later, the Ottoman Empire established trade networks connecting Europe to India and China and passing through MENA cities. MENA’s ports, such as Alexandria and Basra, played significant roles in facilitating the maritime trade of spices, textiles, and precious metals.

Despite the region’s pivotal role in trade and the global economy, MENA’s economic growth is highly volatile due to oil price volatility and political instability. Indeed, MENA’s oil exporters are heavily dependent on oil and hydrocarbon revenues, therefore witnessing rapid growth during periods of high oil prices, and economic slowdowns during periods of low oil prices. To this is added political instability and ongoing conflicts that disrupt trade and investment, hindering the growth prospects in the region.

Therefore, over the past few decades, the MENA region deployed serious efforts to implement economic reforms that promote sustainable growth, focusing on export-led strategies and trade liberalization. Oil-exporting countries, particularly in the Gulf Cooperation Council (GCC),Footnote 2 have engaged in diversification strategies to mitigate dependency on oil exports. Oil-importing countries in the region have focused on being more competitive in sectors like agriculture, tourism, and manufacturing. Trade liberalization measures, such as the reduction of tariff and nontariff barriers, and trade facilitation initiatives, have been implemented to promote trade openness. Moreover, MENA countries have joined different bilateral and regional trade agreements to enhance trade flows among neighboring countries. Examples include the Greater Arab Free Trade Area (GAFTA) aiming at promoting trade openness among Arab countries, and the Euro-Mediterranean Trade Agreement between the European Union and multiple Mediterranean countries.

To what extent are MENA’s efforts effective in building bridges? In other words, to what extent are MENA countries deploying efforts to connect and integrate both regionally and globally? And could some countries be, unintentionally or deliberately, taking actions that break those bridges and hinder the desired regional global integration? While there have been notable achievements in fostering regional and global integration through trade liberalization measures and free trade agreements, significant challenges remain. Political instability, protectionist measures especially for service trade, and limited diversification continue to hinder the full potential of trade policies in the region. To answer clearly these questions, one should keep in mind that the MENA region encompasses countries with varying economic conditions, income levels, and trade performance. Indeed, oil-rich countries, in particular GCC countries possess abundant oil and gas reserves, enjoy higher per capita income levels due to oil revenues, and have more substantial financial reserves to invest in infrastructure projects, support the diversification of their economies away from fossil fuels and enhance their competitiveness on international markets. Non-oil countries, on the other hand, are more diversified but often have lower per capita income levels and face greater economic challenges, such as limited investment opportunities, relatively poor infrastructure, higher unemployment rates, and, in some countries, political instability. Trade policies can also differ significantly between oil exporters and importers due to their contrasting economic structures, trade dependencies, and development policies. Therefore, accounting for those differences between countries is crucial for understanding the trade dynamics in the MENA region.

This Element tells the story of trade in the MENA region, exploring historical backgrounds, the applicability of international trade theories, trade patterns and policies, as well as the relation between trade and economic growth. It is structured as follows: Section 2 explains why this region is rather heterogeneous. Section 3 looks at the history of trade policies in the MENA region, differentiating between resource-rich and poor countries as well as between labor-abundant and labor-importing countries. Section 4 provides a brief overview of international trade theories and their applicability to the MENA region. Section 5 delves into trade patterns at the macro level, distinguishing between trade in goods and services, and explores the concentration of MENA trading partners. Section 6 analyzes the influence of trade on the behavior and performance of firms. Section 7 provides some potential explanations of trade patterns, looking at trade policies and other factors affecting trade such as conflicts and institutional quality. Section 8 examines the link between trade, growth, and business cycles. Section 9 explores the role of trade in shaping development outcomes in the MENA region. Section 10 concludes, and Section 11 provides some policy implications.

Delving into the heterogeneous characteristics of MENA countries can indeed illuminate the applicability of various trade theories, helping to explain trade flows at both macro and micro levels. Moreover, since trade policies, conflicts, and institutional quality are critical factors shaping trade flows in the region, by understanding these factors, one can have a better picture of the complex trade environment in the region – that is highly affected by world business cycles – and recommend strategies to enhance trade relations and economic growth. Based on our analysis of trade in the MENA region, several key conclusions emerge: First, the MENA region experienced liberalization without real integration. Indeed, shallow trade agreements and persistent trade barriers, especially nontariff measures, high tariffs, and costly administrative barriers, in addition to weak institutions and lack of industrial competitiveness, explain the relatively poor performance of trade flows in most of the diversified MENA economies. Second, the MENA region is highly affected by the world business cycles given that the region is highly dependent on oil revenues. Therefore, in order to increase the region resilience, a stronger diversification should take place at the partners and the products levels. Moreover, trade policy should not be limited to the reduction of tariff barriers, but has to be broadened to other nontariff impediments, service regulations, and development-related issues, and should be accompanied by other reforms to improve the business environment and the quality of institutions and infrastructure.

2 A Heterogeneous Region

The MENA region consists of a heterogeneous group of countries that could be classified based on two notable country-related characteristics: the availability of oil resources and the size of their native populations. These country characteristics have shaped MENA’s trade policies over the years. After offering a segmentation of the MENA region depending on countries’ oil-exporting status and labor abundance, this section provides a comparison of MENA trade policies, focusing on the differences between oil-exporting vs. oil-importing countries, and labor-abundant vs. labor-importing countries after their independence.

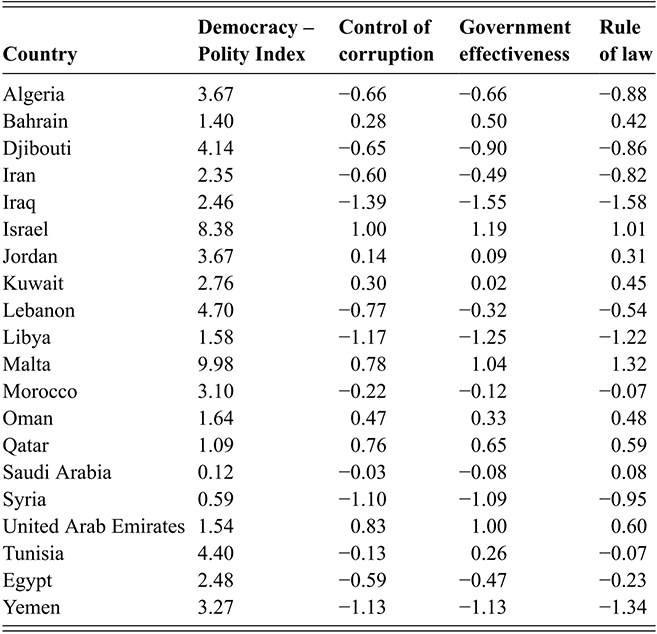

The region encompasses countries with varying income levels, ranging from high-income to lower-income countries (World Bank Country Classification, 2024)Footnote 3. This heterogeneity is even apparent between oil exporters, with GCC countries classified as high-income countries while other oil exporters are counted as upper-middle-income countries (Algeria, Iraq, and Libya), lower-middle income (Iran), and low income (Yemen). Oil importers are also heterogeneous in income levels. They combine high income countries (Israel and Malta), lower-middle income (Djibouti, Algeria, Egypt, Lebanon, Morocco and Tunisia), and low-income countries (Syria).

MENA oil-exporting countries are highly dependent on oil revenues. Indeed, oil exports account 65–95% of total exports in those countries, and oil revenues for more than 60% of their GDP (Karam and Zaki, Reference Karam and Zaki2015). GCC countries have the largest share of oil exports in total exports, with Kuwait (94.63%), Qatar (84.40%), and Saudi Arabia (77.49%) being on the top of the list in 2021 (WDI, 2024).

One structural factor that helps explain why some oil-rich countries remain middle- to lower-income despite abundant natural resources is the phenomenon of Dutch disease, which has profoundly shaped their economic and trade trajectories. The Dutch disease describes the structural economic distortions that arise when resource-rich countries experience large inflows of revenues from oil and gas exports, leading to real exchange rate appreciation and a decline in competitiveness in sectors such as manufacturing and agriculture. This phenomenon became particularly visible following the 1973 oil crisis and the subsequent rise in global oil prices, when resource-rich countries witnessed massive increases in oil revenues.

During this period, public investment and government consumption in these countries expanded rapidly, often financed by oil revenues. However, while GCC countries later used sovereign wealth funds and external investments to partially mitigate Dutch disease effects, much of this spending in non-GCC resource-rich countries was directed toward non-tradable sectors (such as construction, services, and government employment) rather than supporting the development of a diversified manufacturing base. For instance, Algeria pursued ambitious industrialization programs in the 1970s that ultimately failed to create a competitive export sector outside hydrocarbons, due in part to a loss of price competitiveness caused by an appreciated real exchange rate. Similarly, Iraq in the late 1970s used oil revenues for massive infrastructure and military build-up, but its non-oil sectors remained weak and heavily dependent on government demand. Iran also exhibited symptoms of Dutch disease where a booming oil sector fueled rapid urbanization and service sector expansion in the 1970s, but agricultural and manufacturing competitiveness eroded, contributing to rural discontent and structural vulnerabilities that became evident after the 1979 revolution. Libya under Gaddafi, especially during the 1970s and early 1980s, used oil revenues to fund vast public sector employment and social programs, yet developed little export capacity beyond oil, leaving it highly exposed to oil market fluctuations.

The symptoms of Dutch disease have persisted into the 2000s and 2010s. For example, despite periods of high oil prices (such as 2004–2014), Algeria’s non-hydrocarbon exports continued to account for less than 5% of total exports. Iraq, after decades of conflict and sanctions, continues to rely on oil for more than 90% of government revenue and exports, with limited progress in building a competitive non-oil economy.

While lacking natural resources, many oil importers are abundant in human resources due to the size of their native populations. The most populated oil-importing countries in the region are Egypt, Morocco, and Syria (WDI, 2024). Some oil exporters are also labor abundant. Indeed, Iran, Algeria, Iraq, and Yemen appear among the most populated countries in the region. Abundance of human resources presents opportunities for economic growth and development, by increasing labor supply, which translates to lower labor costs, and can lead to higher output and productivity, particularly in labor-intensive sectors. Moreover, a larger population means a higher demand for goods and services, which can stimulate economic growth. Nevertheless, it is noteworthy that labor abundance poses challenges that require effective policy responses, such as investment in education, skill development, infrastructure, and job creation initiatives.

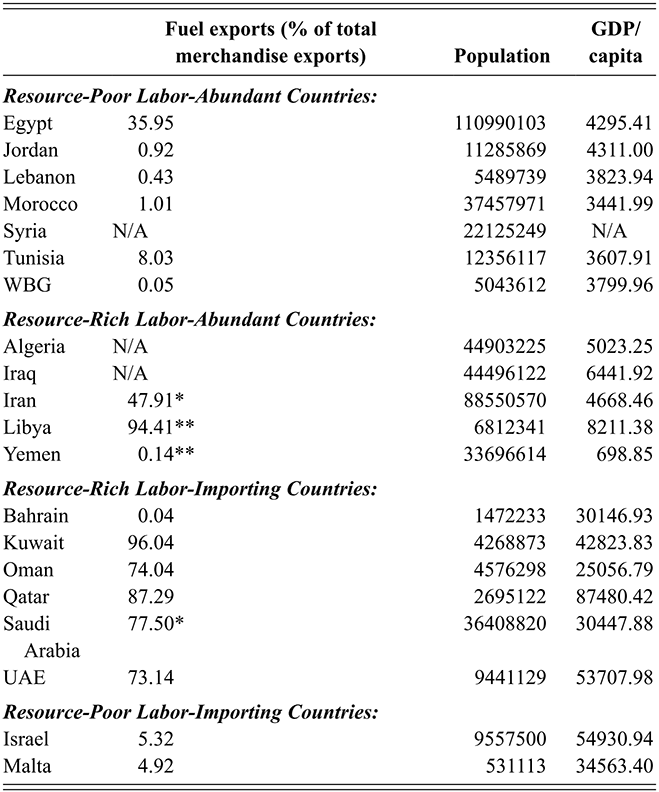

Therefore, we are inspired from Diop et al. (Reference Diop, Marotta and de Melo2012)Footnote 4 to classify MENA countries based on their oil export status and labor abundance according to the following their categories: resource-poor labor-abundant countries, resource-rich labor-abundant countries and resource-rich labor-importing countries (Table 1). To ensure full coverage of all MENA countries in the analysis, we add a fourth category for resource-poor labor-importing countries. To summarize, MENA countries are classified as follows:

– resource-poor labor-abundant countries: Egypt, Jordan, Lebanon, Morocco, Syria, Tunisia, and West Bank and Gaza.

– resource-rich labor-abundant countries: Algeria, Iran, Iraq, Libya,Footnote 5 and Yemen.

– resource-rich labor-importing countries: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and United Arab Emirates (GCC countries).

– resource-poor labor-importing countries: Israel and Malta.

Table 1 Long description

The table highlights the following characteristics of MENA countries: fuel exports as a percentage of total merchandise exports, population, and GDP per capita, classifying countries in 4 categories: Resource-Poor Labor-Abundant Countries (Egypt, Jordan, Lebanon, Morocco, Syria, Tunisia, WBG), Resource-Rich Labor-Abundant Countries (Algeria, Iraq, Iran, Libya, Yemen), Resource-Rich Labor-Importing Countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE), Resource-Poor Labor-Importing Countries (Israel, Malta).

Note: (i) GDP/capita is in current $US. (ii) UAE: United Arab Emirates; WBG: West Bank & Gaza.

* For Iran and Saudi Arabia, the value for the share of fuel exports is for 2021.

** For Libya and Yemen, the value for the share of fuel exports is for 2019.

3 Historical Background

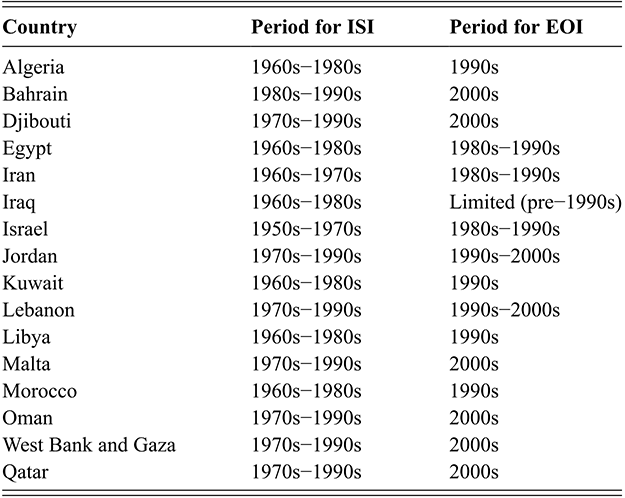

The trade policies of MENA countries have been defined based on their development needs. The region drew inspiration from other countries in shaping its industrialization strategies. Initially, many MENA countries adopted, after their independence, import substitution industrialization (ISI) policies, aimed at reducing dependency on foreign goods by fostering domestic industries. However, over time, these countries began to shift toward export-oriented policies, recognizing the benefits of integrating into the global economy and boosting their international trade.Footnote 6

3.1 Import Substitution Strategies (1950s–1970s)

In the early years after their independence, most MENA countries adopted import substitution industrialization strategies (ISI) (Bruton, Reference Bruton1998), that gained popularity in the middle of the last century, aiming at reducing dependence on imported products by promoting domestic production. ISI policies emphasized the importance of state-owned enterprises, authorized favorable tax treatment for some private investments, high tariffs and quotas on imported goods to protect nascent domestic industries. These ISI strategies varied between oil importers and oil exporters depending on the structure of their economies and their domestic industries (Galal, Reference Galal2008).

The trade policies of resource-rich labor-importing countries have been shaped by their reliance on oil exports and the use of oil revenues to import a wide range of products needed for their development. Therefore, their trade policies were shaped to facilitate the import of goods and services necessary for their development and diversification strategies: tariffs were low on consumer goods and raw materials but high on goods that could compete with local industries that the government aims to promote as part of the diversification strategy (Hvidt, Reference Hvidt2013).

Recognizing the vulnerability of being heavily reliant on oil exports, oil exporters leveraged oil revenues to diversify their economies by developing non-oil industries. Given the limited labor force, these countries, especially GCC countries, set up state-owned enterprises and focused on developing strategic capital-intensive industries such as petrochemicals and refining industries, steel, cement and aluminum. Examples include the establishment of Saudi Basic Industries Corporation in 1976 in Saudi Arabia, aimed at producing petrochemicals domestically, and Kuwait National Petroleum Company and Kuwait Petroleum Corporation to develop the domestic refining capacity in Kuwait and expand petrochemical production. Qatar leveraged its vast natural gas reserves to develop a domestic petrochemical industry. Saudi Arabia invested in steel and cement production to meet domestic construction needs, reducing reliance on imports, while Kuwait invested in local production of construction materials like cement to support the booming construction sector. While the ISI helped in laying the foundation for industrial development, state-owned enterprises often suffered from inefficiencies and lacked competitiveness compared to global standards. In addition, reliance on oil revenues to fund industrial projects made those countries vulnerable to fluctuations in oil prices.

In addition to using oil revenues to develop capital intensive industries such as petrochemicals, steel, automotive, and consumer goods, resource-rich labor-abundant countries have made use of their large labor forces, to foster labor-intensive industries as well, such as textiles, construction materials, and food processing. Algeria and Iran, capitalizing on their large labor forces, have invested in spinning, weaving, and garment production to help build capacity for further growth in the textile and apparel sector. Given the need for reconstruction and infrastructure development (especially in Iraq and Libya), labor-intensive construction materials industries, such as cement, steel, and ceramics, are significant in Algeria, Iran, and Iraq. Algeria, Iran, and Yemen have developed their food processing industry, from agriculture to packaging and logistics, contributing to job creation and reducing dependence on food imports. Traditional handicrafts and small-scale manufacturing (such as leather goods, pottery, and carpets) remain vital for preserving cultural heritage in Yemen and Libya, while creating job opportunities mainly in rural areas.

Resource-poor labor-abundant economies are usually diversified but often suffer from trade deficits due to the fluctuation of the price of energy that they need to import. In those countries, ISI strategies led to the establishment of a variety of industries that are mainly labor intensive such as textiles and other consumer goods. The state established state-owned enterprises with substantial state support, in strategic sectors such as steel, textiles, cement, and chemicals, and imposed high tariff rates as well as nontariff barriers such as import quotas on the imports of those products. For instance, Egypt focused on developing its steel industry and the manufacturing of consumer goods and textiles. Jordan developed its phosphate mining and cement industries to utilize local resources and reduce imports. The country also developed its food processing industry to add value to agricultural products and reduce dependency on imported foodstuffs. Morocco invested in textiles and apparel industry, as well as in processed agricultural products, such as canned goods and beverages, reducing reliance on imported food items. Tunisia focused on developing consumer goods such as electronics, home appliances, and textiles. Lebanon focused on developing light manufacturing industries, such as textiles, garments, and food processing.

ISI strategies in resource-poor labor-importing countries played a crucial role in diversifying the economy and decreasing dependency on imported products. Israel focused on developing domestic industries, particularly in manufacturing and agriculture, to produce goods locally that were previously imported. ISI policies in Malta led to promoting sectors such as textiles, food processing, and manufacturing, reducing dependency on traditional sectors like agriculture and services (Briguglio, Reference Briguglio1995).

While ISI strategies helped lay the foundation for industrial development, state-owned enterprises often suffered from inefficiencies and lacked competitiveness. Moreover, heavy dependence on state support and protectionist measures led to a lack of innovation within domestic industries and made them uncompetitive internationally. As a result, countries faced difficulties in expanding their export markets beyond primary commodities. In addition, ISI often led to persistent balance of payments problems for resource-poor countries: indeed, while the import of consumer goods decreased, the need for imports of machinery, raw materials, and intermediate goods increased, straining foreign exchange reserves. Therefore, ISI was costly to maintain, resulting in debt crises. At the same time, the export-oriented strategies adopted by East Asian economies gained popularity due to their proven success in driving economic growth and industrialization. Those strategies mainly focused on human capital development and strategic investments in education to meet the specific needs of the export-driven economy and enabled the East Asian Tigers to develop a skilled and competitive workforce that survived global competition and contributed to rapid economic growth. The East Asian experience inspired MENA countries, among other developing countries, to use export-oriented policies as the centerpiece of their development strategies.

3.2 Export-Oriented Strategies

With the failure of ISI similar to other developing countries, MENA countries have engaged in trade reforms in the 1990s, relying on export-oriented strategies to boost economic growth. Trade policy has shifted to lower tariff rates, more simplified export and import procedures, the elimination of export licensing requirements, and reduction or suppression of import quotas. Many countries, especially resource-poor ones, have signed in to structural adjustment programs, to secure a loan from the International Monetary Fund and/or the World Bank, where they agree to a set of economic reforms, including reducing government spending, and trade liberalization. For instance, Morocco, Tunisia, and Jordan were among the first countries to implement a structural adjustment program (in 1983, 1986 and 1989 respectively), taking measures to liberalize their trade. Egypt followed in 1990–1991. Kuwait has adopted trade liberalization measures in the aftermath of its membership to the World Trade Organization (WTO) in 1995, as well as Oman in 1996 and Saudi Arabia after the mid-1980s (Droguel and Tekce, Reference Droguel and Tekce2011). Up to the present time, 13 MENA countries are WTO members.Footnote 7

In the context of export-oriented strategies, it is important to acknowledge that many MENA countries have historically pursued a price-competitiveness approach, primarily by maintaining low labor costs and undervalued exchange rates to stimulate export growth. However, as highlighted by Rodrik (Reference Rodrik, Aghion and Durlauf2005), such strategies have often failed to generate sustained export diversification or productivity gains in the absence of strong institutional foundations. Structural problems such as weak governance and inadequate support for innovation, have constrained the effectiveness of price-based strategies. This has left many countries locked into low-value-added export sectors, unable to transition toward more sophisticated, knowledge-intensive industries.

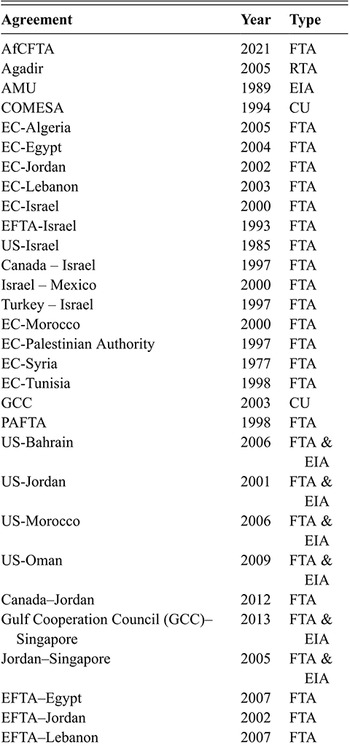

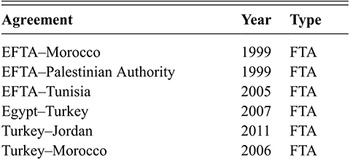

To achieve meaningful export growth, MENA countries had to secure international markets to their products, to benefit from economies of scale that are difficult to achieve on narrow domestic markets. Therefore, countries signed in a variety of bilateral and multilateral trade agreements with each other, African states, the European Union (EU), the United States (US), and Turkey (Rouis and Tabor, Reference Rouis and Tabor2013).

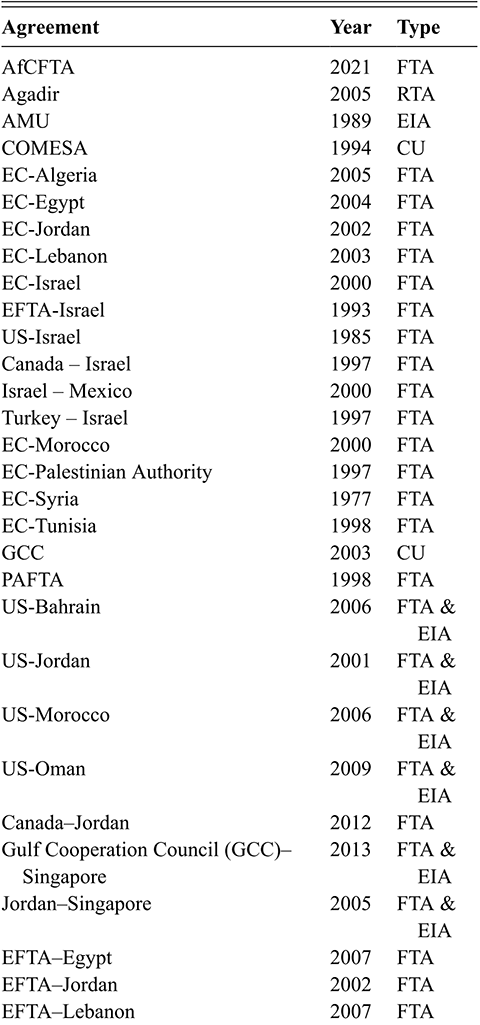

Examples of regional trade agreements include the GAFTA, the Agadir Agreement, and the GCC. GAFTA is a regional trade agreement established in 1997 under the auspices of the Arab League, aimed at promoting economic integration among its members by reducing trade barriers. It was founded initially by seventeen countries: Jordan, Iraq, Saudi Arabia, Kuwait, Yemen, Lebanon, Egypt, Bahrain, Libya, Oman, Qatar, Syria, Morocco, Sudan, Tunisia, the UAE, and Palestine, with Algeria joining in 2005. The agreement, which entered into force in 2005, seeks to foster economic cooperation among member states and increase intra-regional trade through the elimination tariffs, customs duties, and other trade restrictions on goods. Therefore, GAFTA aims to boost economic growth, diversify Arab economies, and reduce their dependence on non-Arab trading partners. However, many challenges persist, including political differences and varying levels of economic development among member states (for instance, Sudan and Yemen are less developed than the other members), and the existence of nontariff barriers. Despite these challenges, GAFTA remains a strategic step toward achieving greater economic integration and cooperation within the Arab world (Abedini and Peridy, Reference Abedini and Peridy2008).

The Agadir Agreement, signed in 2004 by Egypt, Jordan, Morocco, and Tunisia and entering into force in 2007, aims at fostering economic integration and trade cooperation among member countries. It seeks to create a free trade area by eliminating tariffs on industrial products, liberalizing agricultural trade and trade in services, and harmonizing customs procedures and standards. As a regional trade bloc, it also aims to strengthen economic ties between these countries and serves as a steppingstone toward greater economic integration with the EU through the Euro-Mediterranean partnership, which offers access to European Union markets (Droguel and Tekce, Reference Droguel and Tekce2011). While the agreement has achieved some success in boosting trade among member countries, challenges persist, such as bureaucratic procedures at the border, nontariff barriers, and different levels of economic development between members.

The GCC is a regional political and economic alliance established in 1981 by six Gulf Arab states: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates, aiming at fostering economic, political, security, and cultural cooperation among its members. The GCC has pursued initiatives such as a customs union, a common market, and plans for a monetary union to enhance economic integration. In 2003, GCC became a customs union and a common market in 2008, implementing free trade among the members, with common tariffs on imported goods from external trading partners, harmonizing development plans and adopting a common oil policy and coordinating industrial policies. In addition to economic collaboration, the GCC also focuses on regional security, coordinating efforts at responding to regional conflicts and external threats.

In addition to trade agreements among the region’s members, MENA countries have signed trade agreements with developed countries, mainly with the EU and the United States. Euro-Mediterranean Free Trade Agreements (EU-MED FTA) aim at enhancing political, economic and cultural cooperation between the EU and multiple Mediterranean countries in the MENA region. In this context, the agreement was signed by the EU with Tunisia in 1998, Morocco in 2000, Jordan in 2002, Egypt in 2004, Algeria in 2005, and Lebanon in 2006. As the Barcelona Process included the EU associated countries, the mentioned MENA countries have also negotiated/signed free trade agreements with Turkey. EU-MED FTA mainly focuses on the elimination of trade barriers, the adoption of common rules for the rules of origin, with limited liberalization in the agricultural sector (Droguel and Tekce, Reference Droguel and Tekce2011).

Some countries have also signed a free trade agreement (FTA) with the US. The Jordan-US FTA is the first free trade agreement between the United States and an Arab country. It entered into force in 2001 and was fully implemented by 2010. The agreement seeks to gradually liberalize bilateral trade in goods and services between both parties. It covers a wide range of sectors, including agriculture, textiles, and services, and incorporates provisions regarding trade-related issues of the environment, labor, intellectual property rights, and the rules of origin, making it one of the first US trade agreements to include such standards. The agreement also aims to encourage US investment in Jordan, and support Jordan’s broader economic reform and development goals. Since its implementation, the FTA has helped increase bilateral trade and investment, with significant growth in Jordan’s exports to the US, particularly in the textiles and apparel sectors. The US-Jordan FTA is viewed as a model for trade agreements with other countries in the Middle East, such as the Morocco-US and Oman-US FTAs that entered into force in 2006 and 2009 respectively (Droguel and Tekce, Reference Droguel and Tekce2011).

MENA’s efforts in export-oriented industrialization have gone beyond trade agreements. Indeed, countries have been engaged in internal reforms and measures to boost exports in some key sectors. GCC countries, endowed with small populations but rich natural resources, have used oil revenues to invest in sectors such as petrochemicals, aluminum, steel, and plastics, and more recently in renewable energy, tourism, and financial services. Their trade policies have shifted to support this export orientation strategy by establishing free trade zones, and in some countries such as the UAE, allow full foreign ownership and minimal regulations to attract foreign investment. The UAE, especially Dubai, and, more recently, Saudi Arabia have become a major tourism destination. The UAE and Qatar have developed robust financial services sectors and established themselves as financial hubs. Qatar has focused on developing its natural gas industry, making it the world’s largest exporter of liquefied natural gas.

Resource-rich, labor-abundant countries have also employed various export-oriented strategies to diversify their economies, reduce dependency on raw material exports, and harness their human capital for sustainable development. They focused on industries that add value to natural resources, such as petrochemicals, refining, and metals, and invested in various sectors away from oil, some that are labor-intensive like agriculture and textiles and other that are capital-intensive like automotive and electronics industries. Moreover, they have developed many services sectors, such as tourism, education services, banking and insurance services (in Algeria and Iran), medical tourism (in Iran), telecommunication services (in Libya and Yemen), and real estate (in Iraq and Libya). Most importantly, they have gone through regulatory reforms, created tax incentives, and established special economic zones to attract international companies. They have also invested in infrastructure to facilitate exports. Unfortunately, while much effort has been deployed by this group of countries, their export-oriented strategies have been significantly impacted by ongoing conflicts and political instability (Iraq, Yemen, and Libya), or by international sanctions (Iran).

Resource-poor, labor-abundant countries, endowed with relatively large, young, and often well-educated populations, have focused on leveraging their human capital by investing in education and vocational training to support export-oriented strategies. They often rely on labor migration to oil-abundant countries, with remittances playing a significant role in their economies. In this regard, their trade agreements often include provisions facilitating labor movement. Those countries focused on modernizing agriculture, and taking advantage of favorable climate and labor abundance, on promoting agricultural exports such as fruits, vegetables, and flowers. Moreover, they invested in light manufacturing industries, such as textiles, apparel, electronics, and automotive parts, to produce exportable products. They have also developed services sectors like tourism, information and communication technology (ICT) and software services, education, and healthcare. Like other countries, they established special economic zones by offering tax incentives, simplified regulations, and robust infrastructure, to attract foreign direct investment. For instance, Egypt, in addition to developing its textile and apparel industry, ICT sector, and tourism, has leveraged its agricultural potential to become a major exporter of fruits and vegetables. Jordan has developed a strong ICT sector, becoming a regional hub for technology and outsourcing services, and focused on tourism and key export sectors such as pharmaceutical products and garments. Tunisia has diversified its economy through the development of its automotive parts industry, electronics, textiles, and tourism. Morocco has focused on automotive manufacturing, electronics, and aerospace as key export industries. The country has also developed its agricultural exports, particularly in high-value crops such as citrus fruits and vegetables.

Resource-poor labor-importing countries, namely Israel and Malta, pursued export-oriented strategies to enhance the resilience of the economy. Israel has developed a strong high-tech sector and fostered a thriving ecosystem for startups, innovation, and entrepreneurship. The country has also promoted exports in other sectors such as agriculture, pharmaceuticals, and defense technology. With a competitive regulatory framework, tax incentives, a skilled workforce, and a strategic location in the Mediterranean, Malta has developed a strong services-oriented economy, promoting tourism and financial services.

Recognizing the limitations of ISI, and amid fluctuating global oil prices and other external shocks, MENA countries found in export-oriented strategies and diversification a remedy for their development challenges and an opportunity to build more resilient and sustainable economies through the integration of global markets and the attraction of foreign investment. How successful was this integration experience? Before delving into a detailed overview of MENA’s trade flows and specialization, we offer in Section 4 a review of international trade theories and discuss their application to the MENA context.

4 A Refresher of International Trade Theories: MENA Perspective

International trade theories have evolved significantly over time, from classical concepts to contemporary models with more realistic assumptions capturing the complexity of trade patterns, therefore enhancing our understanding of international trade, and guiding policy decisions that can foster economic growth and development. Accordingly, a brief review of the evolution of international trade theories is necessary to elucidate the dynamics of trade patterns and trade policies in the MENA region.

Classical and neoclassical trade theories evaluate the competitiveness of a country by its exogenous factor endowments. Classical theories and represented by the Theory of Absolute Advantage of Adam Smith in 1776 and Ricardo’s Comparative Advantage theory in 1817. The Theory of Absolute Advantage argues that free trade would lead to increased overall wealth and efficiency if countries specialize in producing goods where they have an absolute advantage that they can produce more efficiently than other countries (Smith, Reference Smith1776), The applicability of the absolute advantage theory was questioned in the case of a dominant country with an absolute advantage in all goods that would not benefit from international trade. Consequently, Ricardo’s Theory of Comparative Advantage expanded Smith’s model and argued that trade between a dominant country and a country with no absolute advantage can still benefit both countries, if each country specializes in goods where they have the lowest opportunity cost (Ricardo, Reference Ricardo1817). In Ricardo’s model, labor is the sole production factor, and countries have different technologies that explain the difference in their productivity levels. However, Ricardo did not explain why technology levels should be considered as exogenous.

Graham (Reference Graham1923) argued that the Theory of Comparative Advantage may lead to suboptimal specialization when one sector exhibits increasing returns to scale (such as manufacturing) and another exhibits diminishing returns (such as agriculture or resource extraction), even when potential gains exist in manufacturing sectors that exhibit increasing returns to scale. If a country specializes according to its existing comparative advantage in the diminishing returns sector, it may forego long-term gains from developing the increasing returns sector. Thus, under free trade, economies might be locked into inferior development paths, justifying temporary protection for emerging industries. This argument laid an early foundation for the infant-industry protection rationale and has been a cornerstone of development economics, particularly for countries seeking to industrialize after being locked into primary commodity exports.

Neoclassical trade theories were built on the principles of classical theories, emphasizing the role of comparative advantage, resource allocation, and market equilibrium. The Heckscher-Ohlin model (1933) highlights the role of a country’s factor endowments in determining its production cost and therefore its comparative advantage. Technology is similar between countries, but production methods differ due to different combinations of production factors. According to this model, a country will export the goods that use its abundant factors intensively and import the goods that use its scarce factors intensively. The Stolper-Samuelson Theorem (Stolper and Samuelson, Reference Stolper and Samuelson1941) uses the Heckscher-Ohlin model to examine the impact of trade on income distribution within countries and provides insight into the political economy of trade policy. It shows that free trade benefits the factor of production that a country has in abundance and harms the scarce factor.

How do classical and neoclassical trade theories manifest in the context of the MENA region? Almost half of MENA countries, and especially GCC countries, are abundant in fossil fuels. Benefiting from this comparative advantage, those countries export oil and oil derivatives to other countries lacking these natural resources. Data from the US Energy Information AdministrationFootnote 8 shows that the MENA region includes five of the top ten oil-producing countries (Saudi Arabia, Iraq, United Arab Emirates, Iran, Kuwait) and is responsible for producing about 26% of world production. Except for Iran that suffers from international sanctions, the previous countries are also featured among the major oil-exporting countries. By contrast, MENA non-oil exporters like Egypt, Morocco, and Tunisia are known for their significant labor resources due to various factors such as population size, education levels, and workforce participation rates. That being so, they have a comparative advantage in traditional sectors like agriculture and textiles, as well as tourism due to their geographic conditions, and low labor cost. Moreover, Graham’s argument resonates strongly in many MENA countries, where resource abundance has led to strong dependency on oil and gas exports and limited industrial diversification. For instance, Algeria, Iraq, and Libya have specialized in oil and gas sectors that exhibit diminishing returns to scale and limited spillover effects. Despite possessing large labor forces and potential comparative advantages in labor-intensive manufacturing, these countries became heavily reliant on hydrocarbon exports, which discouraged the development of industries with increasing returns, such as textiles, light manufacturing, or agro-processing. Similarly, the infant-industry argument is highly pertinent for many MENA economies, especially resource-rich, labor-abundant countries such as Algeria, Iraq, or Iran, who have struggled to develop competitive manufacturing sectors due to early exposure to international competition and a lack of sustained policy support. Without temporary protection and sound industrial policies, industries with potential economies of scale have to compete internationally.

The Specific Factor Model, developed by Jones (Reference Jones1971) and Samuelson (Reference Samuelson1971), builds on classical trade theory by introducing the idea that while some factors of production (like labor) are mobile across sectors, others (like capital) are “specific” to particular industries and cannot move easily. In this framework, an economy is composed of multiple sectors, each relying on a specific, immobile factor and a common mobile factor. Changes in trade patterns, prices, or external shocks affect the income distribution between sectors, because specific factors benefit or suffer depending on how their sector is impacted. Applying this to resource-rich MENA countries, when the price of oil rises, the oil sector becomes more profitable. Labor, being mobile, moves toward the booming sector to benefit from higher wages, and workers who stay in the sectors not experiencing the boom (like manufacturing or agriculture) may face declining wages, and the specific factors in those sectors (like agricultural land or industrial machinery) earn lower returns compared to before the shock. Therefore, the Specific Factor Model helps explain the Dutch disease that has profoundly shaped most resource-rich MENA economies, distorting their economic development toward hydrocarbons sectors, and away from other sectors, that are often critical for long-term economic growth and diversification.

Critics argue that neoclassical trade theories rely on simplified assumptions that are not very realistic, such as the assumptions of perfectly competitive markets, factor mobility internally but not internationally, constant returns to scale and the absence of transport costs. Moreover, the static nature of comparative advantage does not account for dynamic gains from trade, such as technological advancement and innovation. The postwar period to the late 1970s was characterized by a rapid growth and structural changes in international trade among industrial countries, leading to modern trade theories recognizing the importance of economies of scale and imperfect competition in the analysis of trade.

Expanding on neoclassical theories, Krugman (Reference Krugman1979) introduced a pivotal framework that highlights how technological leadership in certain industries (usually in developed countries) creates a “leader-follower” dynamic, which can be important for understanding the trade patterns and development outcomes of countries. In Krugman’s model, countries that are more technologically advanced (the leaders) enjoy greater productivity and competitive advantages in certain industries, which allow them to dominate those markets. On the other hand, follower countries may lack the same technological capacity, leading to lower productivity and a reliance on resource extraction or simple manufacturing rather than high-tech industries. This gap can widen over time, especially in economies that don’t invest in technological innovation or education.

Krugman’s model can be applied to many MENA countries, particularly those that are resource-rich. These countries often face a significant gap in technological innovation compared to more advanced economies, which limits their ability to diversify and develop competitive manufacturing or high-tech sectors. As a result, they remain heavily dependent on natural resource exports, such as oil and gas, rather than fostering industries that could drive long-term growth. They may experience difficulty in bridging this technological gap, leading to a reliance on low-value-added sectors and hindering economic diversification.

The New Trade Theory was developed by Paul Krugman in 1980, arguing that trade between countries is driven not just by differences in resources or technology, but also by economies of scale and consumer preferences for variety, and highlighting the role of intra-industry trade (trade in similar products) among similar countries. Krugman (Reference Krugman1980) developed a general equilibrium model of Chamberlinian monopolistic competition where firms can achieve lower production costs through economies of scale and can also differentiate their products to capture different market segments. Intra-industry trade, therefore, occurs due to differentiated products and consumer preferences for variety. Krugman argues that industries with high fixed costs (such as like automobiles, electronics, or pharmaceuticals) benefit from producing on a larger scale. As production expands, average costs decrease, allowing firms to become more competitive globally.

When it comes to MENA countries, it is noteworthy that all countries have devoted substantial effort in designing their export-oriented strategies to benefit from economies of scale stemming from their access to international markets. Although to different extent, MENA countries invested heavily in technology and infrastructure, to improve their productivity and export competitiveness. The most famous examples are the main oil exporters, such as the UAE, Saudi Arabia, and Qatar, that have undertaken serious economic diversification strategies, to reduce dependence on oil and develop sectors where increasing returns to scale can be realized. Heavy investments have been made in renewable energy, financial services, technology, and tourism. Dubai International Financial Centre (DIFC) is an example of a financial hub consolidating financial activities in one location and facilitating economies of scale by accessing larger markets beyond the MENA region. The UAE and Saudi Arabia are investing in large-scale infrastructure projects, such as ports, logistics hubs, and free trade zones, that attract multinational businesses that leverage economies of scale and enhance competition in international markets.

Recent advancements in trade theory have focused on firm-level differences, instead of country differences, to explain variations in export performance across firms and industries. The “New-New Trade Theory” emerged with the seminal work of Melitz (Reference Melitz2003) to highlight the importance of firm heterogeneity in terms of productivity and the existence of a fixed cost to enter export markets, in determining the number and the type of firms that become exporters as well as the gains from trade. Exporters have a productivity advantage before they start exporting – not as a result of exporting – because only the most productive firms are able to overcome the costs of entering export markets. Extensions of the Melitz’s (Reference Melitz2003) model explicitly account for the decision to export, that is, the extensive margin of trade (Chaney, Reference Chaney2008; Helpman et al., Reference Helpman, Melitz and Rubinstein2008; Melitz and Ottaviano, Reference Melitz and Ottaviano2008).

The Melitz model provides a framework for understanding how firm heterogeneity influences trade dynamics in the MENA region. Indeed, most MENA countries have undertaken serious economic and trade reforms by reducing tariffs and nontariff barriers and made strenuous effort in trade integration by joining different bilateral and regional trade agreements. Increased competition due to access to other markets resulted in the exit of less productive firms while allowing more productive firms to access larger markets, where they can leverage their competitive advantages. For example, in countries like Morocco, Tunisia, and Egypt, the growth of export-oriented sectors like automotive parts, electronics, and agricultural products can be seen as an outcome of this dynamic. Energy companies in Qatar and the UAE have made substantial investments in technology and infrastructure necessary to survive global competitiveness. Additionally, both Qatar and the UAE have been trying to diversify their economies beyond oil and gas, with national strategies aimed at enhancing competitiveness and innovation. They have seen a growth in the number of firms exporting goods and services (like tourism, financial services, logistics, and high-tech industries). These firms have access to advanced technology, skilled labor, and efficient production processes, giving them a competitive edge in global markets.

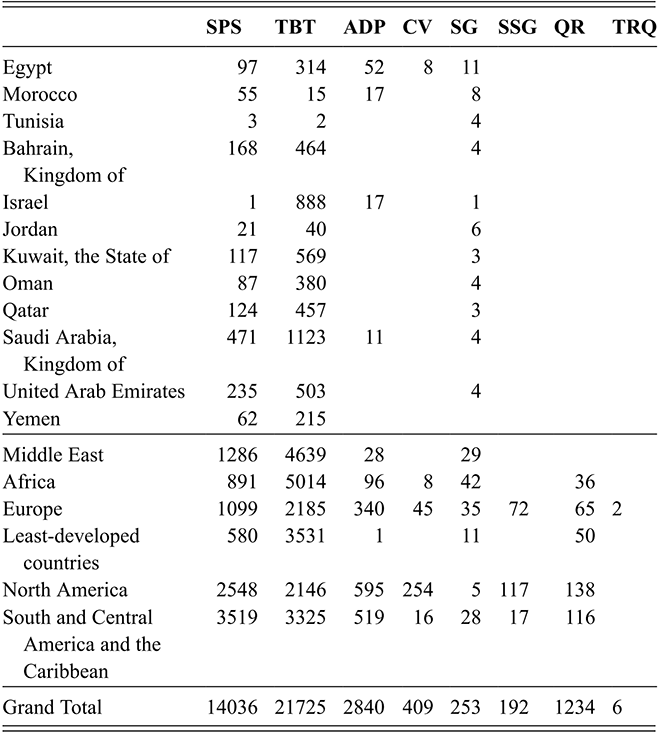

Building on these theoretical foundations, we now turn to the gravity model, which, while rooted in economic theory, is primarily an empirical tool widely used to analyze actual trade flows and quantify the impact of various factors on international trade. The gravity model, initially developed by Tinbergen (Reference Tinbergen1962) and Anderson (Reference Anderson1979), has gained prominence in modern trade theory in analyzing bilateral trade between countries. It suggests that the volume of trade between two countries is directly proportional to their economic sizes and inversely proportional to the distance between them. The gravity model has undergone over years significant theoretical and empirical improvements (Mac Callum, Reference McCallum1995; Feenstra et al., Reference Feenstra, Markusen and Rose2001; Feenstra, Reference Feenstra2002; Anderson and van Wincoop, Reference Anderson and Van Wincoop2003), enforcing its theoretical base, thus narrowing the gap between theoretical and empirical findings. It encompasses many determinants to predict trade patterns, such as GDP of both countries, their populations, geographical distance, whether they have a common border, whether they have a common language or a common colonial background, and whether they are both members of some trade agreements.

The gravity model provides a useful framework for understanding trade patterns in the MENA region. First, countries with larger economies, such as Saudi Arabia, the UAE, and Egypt, have significant trade volumes both within the region and with the rest of the world. Second, geographical proximity is a significant factor influencing trade patterns among MENA countries. Third, MENA countries share cultural and historical ties that enhance trade among them. Examples include the Arab Maghreb Union (AMU)Footnote 9 and countries of the Gulf Cooperation Council (GCC). Finally, and as discussed in the previous section, MENA countries have deployed much effort to promote regional trade integration, such as the GAFTA and the Agadir Agreement, to enhance trade among member countries. Some empirical studies have highlighted the role of other determinants of trade in the MENA region, such as the detrimental effect of war and conflicts (Karam and Zaki, Reference Karam and Zaki2016) and the role of institutional quality (Karam and Zaki, Reference Karam and Zaki2019). Moreover, Karam and Zaki (Reference Karam and Zaki2013) used an augmented gravity model to investigate the trade performance in services of MENA countries. The authors are interested in each country’s trade performance in services instead of bilateral service trade flows, and therefore adapt the gravity model to take into account unilateral variants of the variables that have been found in the literature to influence bilateral trade. They introduce a new determinant of trade performance, namely the number of bound commitments undertaken by a sector in the WTO as well as the availability of those commitments by mode of supply. After controlling for the possible selection bias coming from the fact that WTO bound commitments are only observed for WTO members, the authors found that, beyond traditional trade determinants, WTO membership and the number of bound commitments undertaken by a sector increase exports, imports and trade in services.

Different trade theories offer insights into the trade dynamics of MENA countries. The theory of comparative advantage explains their reliance on oil and gas export, while the New Trade Theory highlights their engagement in intra-industry trade in sectors such as manufacturing, driven by economies of scale and consumer demand for variety. The New-New Trade Theory highlights how trade liberalization efforts enable more productive firms to expand and less productive ones to exit, fostering overall economic efficiency. Together, these theories illustrate the region’s evolving trade patterns shaped by resource endowments, economic reforms, and liberalization efforts. The following section delves into an overview of MENA trade flows to gain deeper insights into trade patterns at the region, country and sector levels, as well as MENA’s key trading partners.

5 Overview of Trade Flows in the MENA Region: A Macro Approach

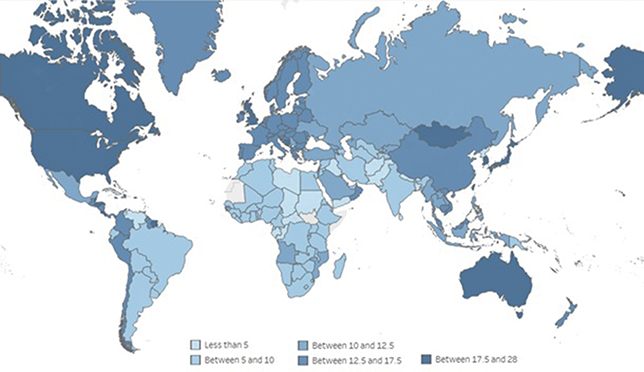

The trade performance of the MENA region appears to be mixed over time. Data from the World Development Indicators, 2023 show that the share of trade in MENA GDP increased substantially between 2000 (69%) and 2008 (91%), then stumbled in 2009 due to the financial crisis. Between 2009 and 2014, trade accounted for around 81–85% of MENA GDP. The share of trade in MENA GDP further decreased to 78% in 2015 due to collapsing oil prices, and to 69% in 2020 and 60% in 2021 due to the COVID-19 pandemic. In 2022, as the world economy was starting to recover from the devastating effects of the pandemic, the share of trade in MENA GDP increased to 66%.

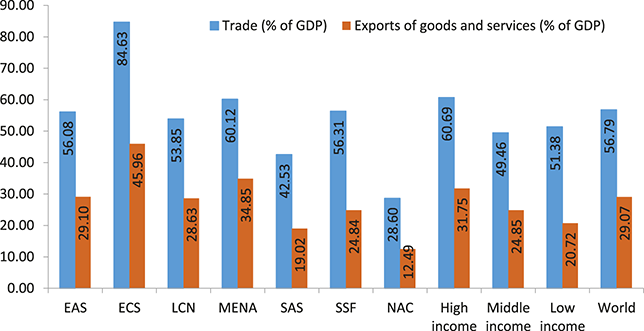

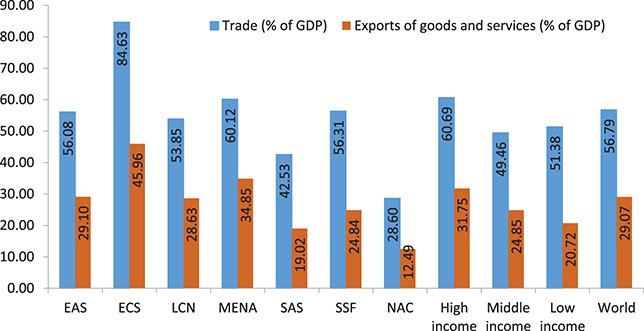

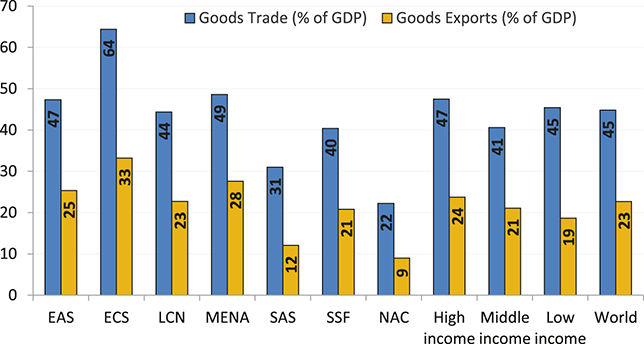

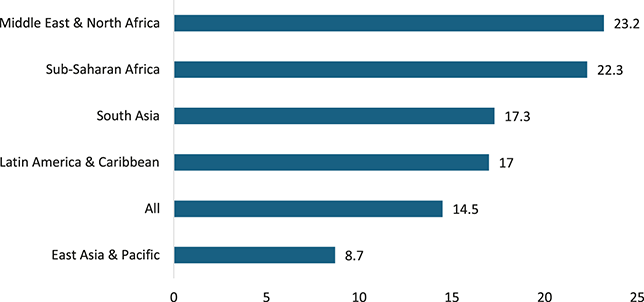

Figure 1 shows that in 2021Footnote 10 the share of trade in MENA GDP (60.12%) was almost comparable to high-income countries, and stood above the world average (56.79%) and above the share of trade in the GDP of middle-income countries. Indeed, the MENA region stands directly after Europe & Central Asia (with a share of 84.63%) and before the other regions, developed ones like North America (28.6%) as well as developing ones like sub-Saharan Africa (56.31%).

Trade as a percentage of GDP, 2021

Note: (i) Trade is the sum of exports and imports divided by the value of GDP.(ii) EAS: East Asia & Pacific; ECS: Europe & Central Asia; LCN: Latin America & Caribbean; MENA: Middle East & North Africa; SAS: South Asia; SSF: Sub-Saharan Africa; NAC: North America.

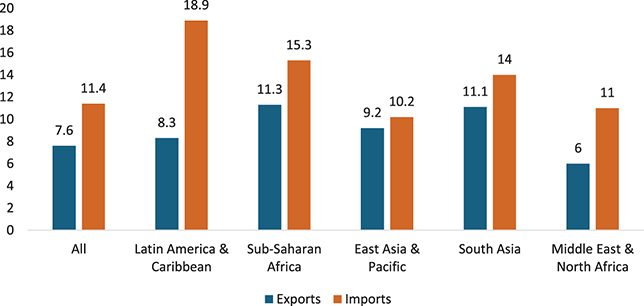

Exports account for 34.85% of MENA GDP and compare favorably, like the share of trade in the region’s GDP, to all regions (except Europe & Central Asia), and especially to high and middle-income countries and the world’s average. However, it is worth mentioning that this bright figure for MENA exports is mainly due to the region’s heavy reliance on petroleum exports. Indeed, Karam and Zaki (Reference Karam and Zaki2015) highlight that MENA trade excluding oil is at about the world average, but exports alone are below the world average. In addition, Behar and Freund (Reference Behar and Freund2011) show that, conditioning on GDP, distance, and a number of other factors, a typical MENA country under-trades with other countries: exports to the outside world are at only a third of their potential. However, intra-MENA trade is conditionally higher than extra-MENA trade. These results hold for aggregate exports, non-natural exports, and non-petroleum exports.

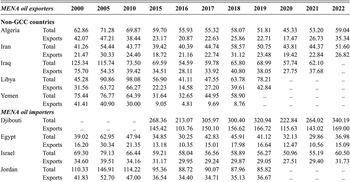

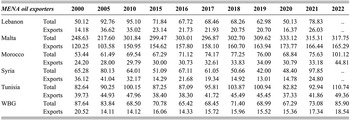

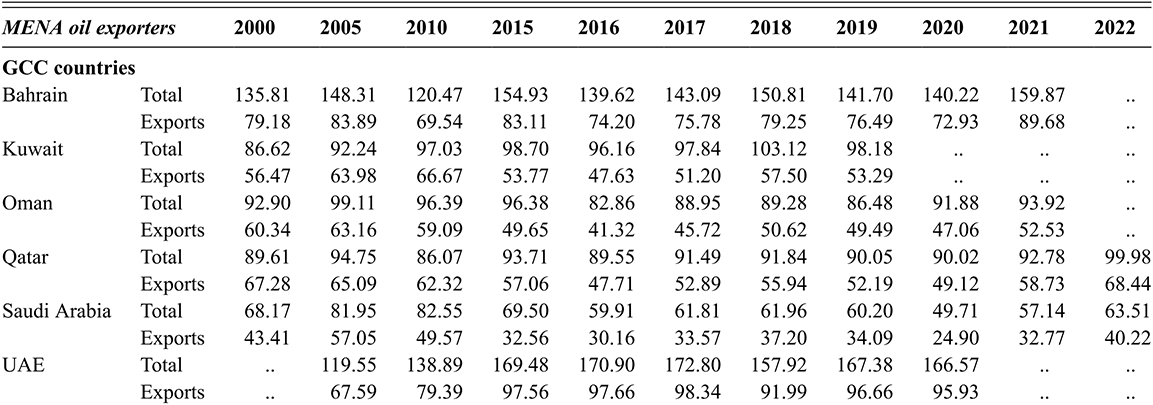

The region’s average masks some heterogeneity at the country level. Table 2 shows that some countries like Saudi Arabia, Algeria, Iran, Iraq, Egypt, Israel, Lebanon, and Syria were behind the region’s average share of trade in GDP in 2021 while other countries exceeded by far the region’s average, such as Malta (315.31%), Djibouti (264.02%), the United Arab Emirates (UAE) (166.57% in 2020), and Bahrain (159.87%).

Table 2a Long description

The table differentiates between oil exporting countries and oil-importing countries. MENA oil exporters among GCC countries include Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE.

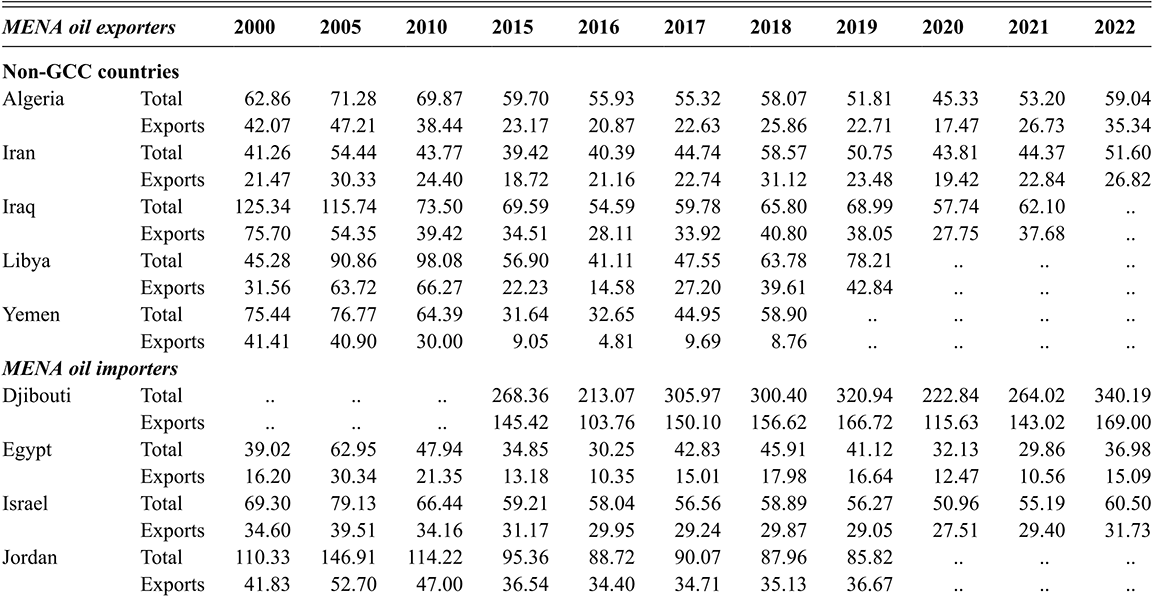

Table 2b Long description

MENA oil exporters among non-GCC countries include Algeria, Iran, Iraq, Libya, Yemen.

Table 2c Long description

MENA oil importers include: Djibouti, Egypt, Israel, Jordan, Lebanon, Malta, Morocco, Syria, Tunisia, and WBG.

Note: (i) Trade is the sum of exports and imports divided by the value of GDP. (ii) UAE: United Arab Emirates; WBG: West Bank & Gaza.

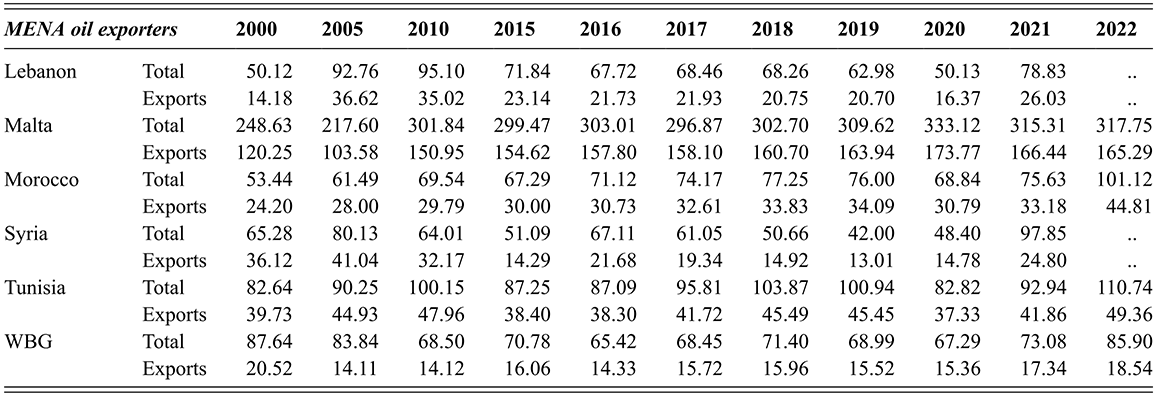

Another characteristic feature of trade’s shares in GDP at the country level is their evolution over the years. While trade’s share in GDP in many countries followed the region’s pattern, some countries witnessed a decrease in trade’s share in GDP while others saw an improvement in this share. For instance, in Libya, the share of trade in GDP doubled between 2000 (45%) and 2010 (98%) before dropping to 78% in 2019. In the UAE, trade’s share in GDP moved up from 120% in 2005 to 167% in 2020. Iraq’s share dropped expectedly following the war, from 125% in 2000 to 62% in 2021, and Yemen’s share from 75% in 2000 to 59% in 2018 due to the devastating effects of the civil war. Similarly, Jordan saw its trade share in GDP declining from 110% in 2000 to 86% in 2019 (Table 2).

Expectedly, most oil exporters exceed the region’s export share in GDP due to the high concentration of exports in petroleum products. The UAE and Bahrain show an export share in GDP that is double the region’s average (95.93% in 2020 for the UAE and 89.68% for Bahrain in 2021 respectively). Despite being oil exporters, Algeria, Iran and Yemen exhibit export shares below the region’s average: indeed, while Iran’s oil exports are vulnerable to sanctions imposed by Western government, Yemen’s civil war have had devastating effects on the economy and international trade since 2014. It is also noteworthy that oil-importing countries like Malta, Djibouti, and Tunisia exhibit higher shares of exports in GDP than the region’s average. The share of exports in GDP in Malta (166.44%) and in Djibouti (143.02%) was more than four times the region’s average in 2021.

5.1 Trade in Goods

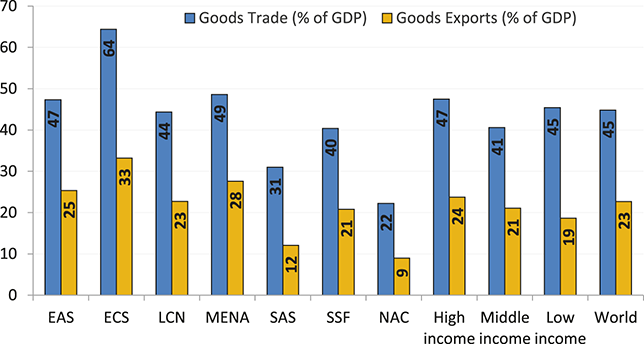

Goods trade accounts for 48.6% of MENA GDP in 2021, standing behind Europe and Central Asia, but exceeding the average of all other regions including high-income countries as well as the world’s average. In particular, the share of goods trade in MENA GDP is more than twice the share for North America. In 2021, the MENA region exported more goods than it imported, exceeding the world’s average share of goods exports in GDP, as well as the share for all regions except Europe and Central Asia, developing as well as developed ones. The share of goods exports in MENA GDP (27.59%) is more than twice the share for South Asia and triple the share for North America (Figure 2). Those bright figures are expected given the heavy reliance of the region on oil exports. Indeed, Reinert (Reference Reinert and Reinert2017) highlights that trade in goods is heavily influenced by regional factors, which is particularly relevant for the MENA region, where natural resource endowments and trade policies shape trade patterns.

Goods trade as a percentage of GDP, 2021

Note: (i) Goods trade in GDP is calculated as the sum of goods imports and goods exports divided by GDP, all in current US$. Goods exports in GDP is calculated as the share of goods exports in GDP, all in current US$. (ii) EAS: East Asia & Pacific; ECS: Europe & Central Asia; LCN: Latin America & Caribbean; MENA: Middle East & North Africa; SAS: South Asia; SSF: Sub-Saharan Africa; NAC: North America.

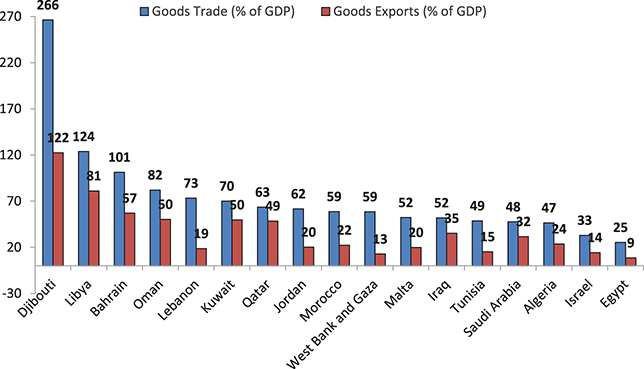

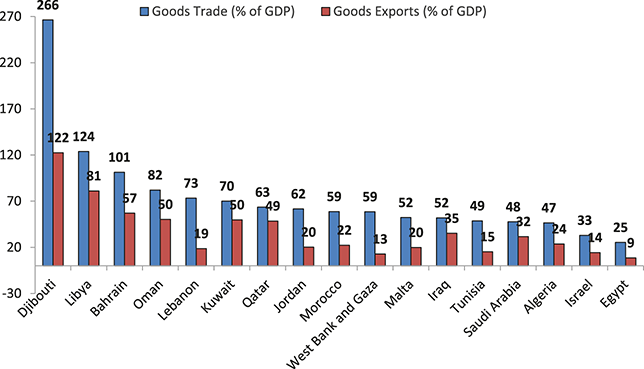

However, the region’s average masks the apparent heterogeneity in goods trade figures at the country level. Figure 3 shows that in 2021, although most oil exporters are on the top in terms of the share of goods trade and exports in GDP, Djibouti, a non-oil-exporting country, ranks first in terms of goods trade and exports in GDP (266.32% and 122.48% respectively), with shares accounting for more than four times the regional averages. The most recent exports in Djibouti are led by Palm Oil ($169 M), Chlorides ($53 M), Sheep and Goats ($16.7 M), Dried Legumes ($10.2 M), and Industrial Fatty Acids, Oils and Alcohols ($8.66 M) (The Observatory of Economic Complexity, OEC (2021) https://oec.world/en/profile/country/dji). In addition, while GCC countries and other oil-exporting countries are net exporters, Djibouti seems to import more than it exports. It is also noteworthy that, while most oil exporters exceed the regional trade averages, the shares of goods trade and goods exports in the GDP of Saudi Arabia, the major oil exporter in the world, are below the region’s average (47.58% and 31.6% respectively). Countries like Lebanon, Jordan, Morocco, and Malta show a share of goods trade in GDP above the region’s average and are all net-importers of goods.

Goods trade as a percentage of GDP by country, 2021

Note: Goods trade in GDP is calculated as the sum of goods imports and goods exports divided by GDP, all in current US$. Goods exports in GDP is calculated as the share of goods exports in GDP, all in current US$.

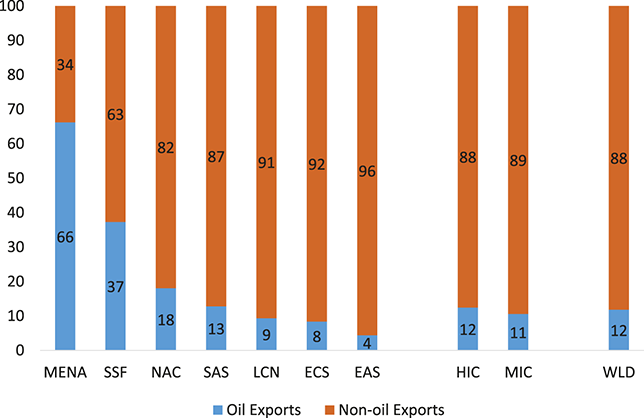

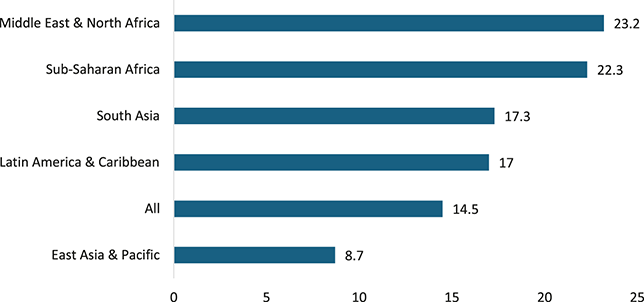

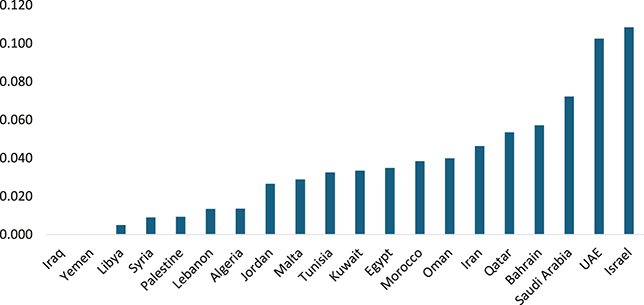

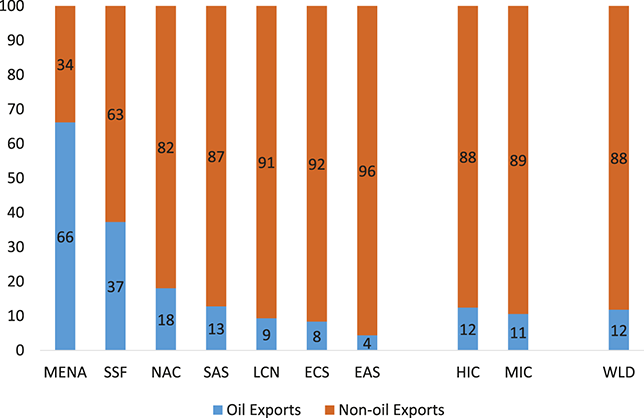

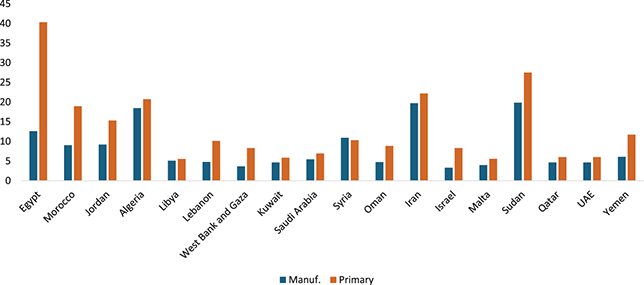

Trade in the MENA region has long been seen as interchangeable with trade in petroleum products, with two-thirds of MENA countries depending on the oil sector as the main source of earnings. Figure 4 shows that the share of oil exports in MENA merchandise exports is 66%, which is more than five times the world’s average and almost double the average of developing regions like sub-Saharan Africa.

Oil v/s non-oil exports as a percentage of merchandise exports, 2021

Note: EAS: East Asia & Pacific; ECS: Europe & Central Asia; LCN: Latin America & Caribbean; MENA: Middle East & North Africa; SAS: South Asia; SSF: Sub-Saharan Africa; NAC: North America.

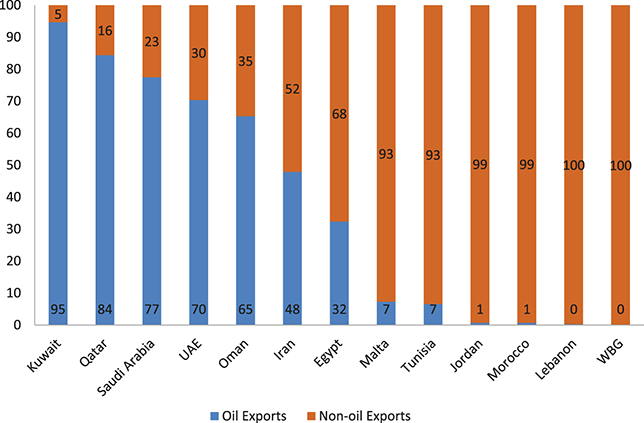

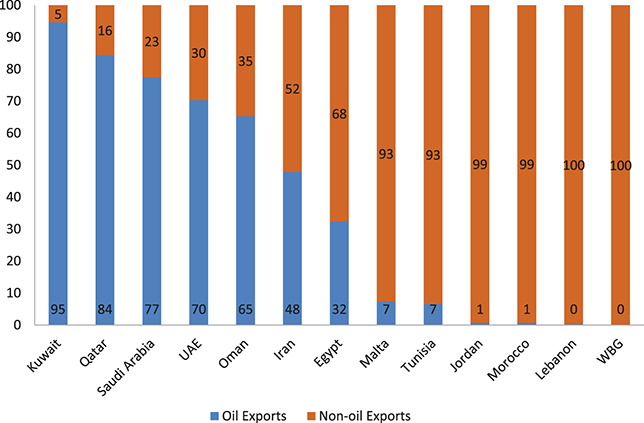

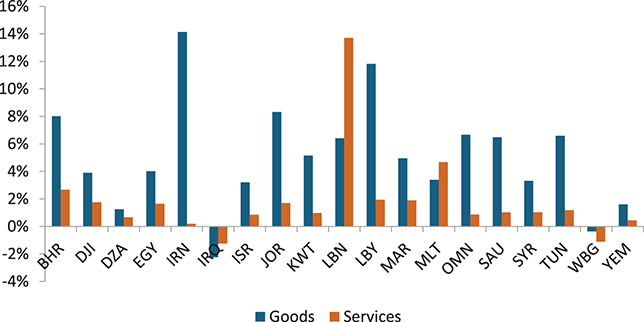

GCC countries expectedly show in 2021 the largest share of oil exports in total exports, reaching 94.63% for Kuwait, 84.40% for Qatar and 77.49% for Saudi Arabia. While the UAE is one of the major oil exporters with oil exports accounting for 70% of total merchandise exports, it stands behind major GCC exporting countries due to the deployed efforts to diversify its economy (Figure 5).

Oil v/s non-oil exports as a percentage of merchandise exports for selected MENA countries, 2021

Note: UAE: United Arab Emirates; WBG: West Bank & Gaza.

Therefore, as shown in Figure 5, the share of oil exports in total exports ranges from 65% to 95% in MENA oil-exporting countries, and oil revenues account for more than 60% of their GDP (Karam and Zaki, Reference Karam and Zaki2015). Heavy dependence on oil is a double-edged sword. While the region’s abundant natural resources have fueled the region’s rapid economic growth for decades, they have relentlessly exposed it to trade shocks and increased growth volatility over time. Consequently, recent years have seen governments embarking on ambitious economic diversification initiatives to decrease their dependence on oil.

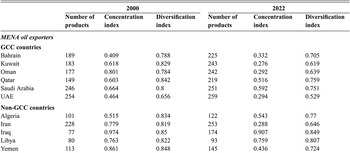

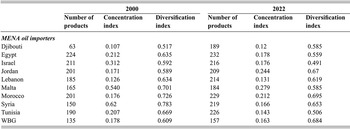

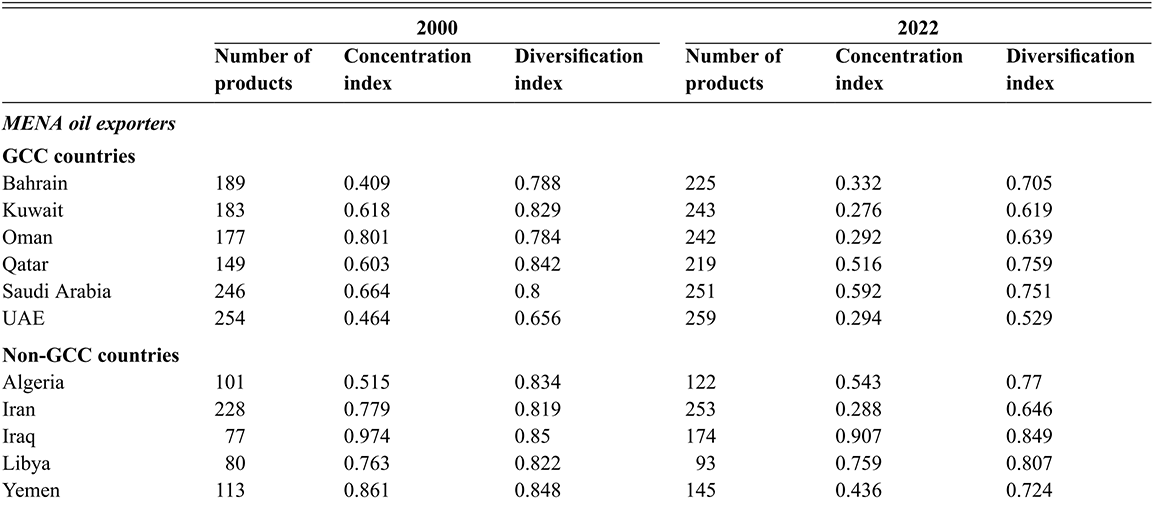

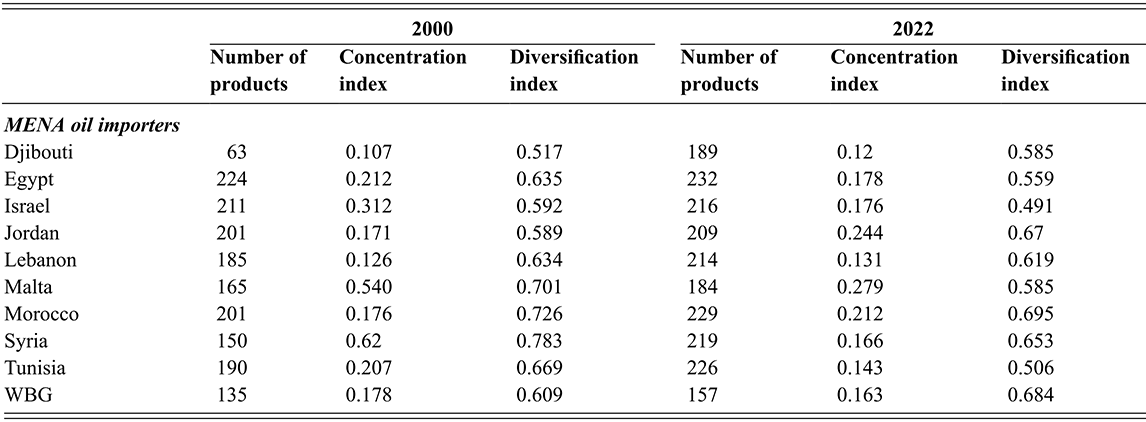

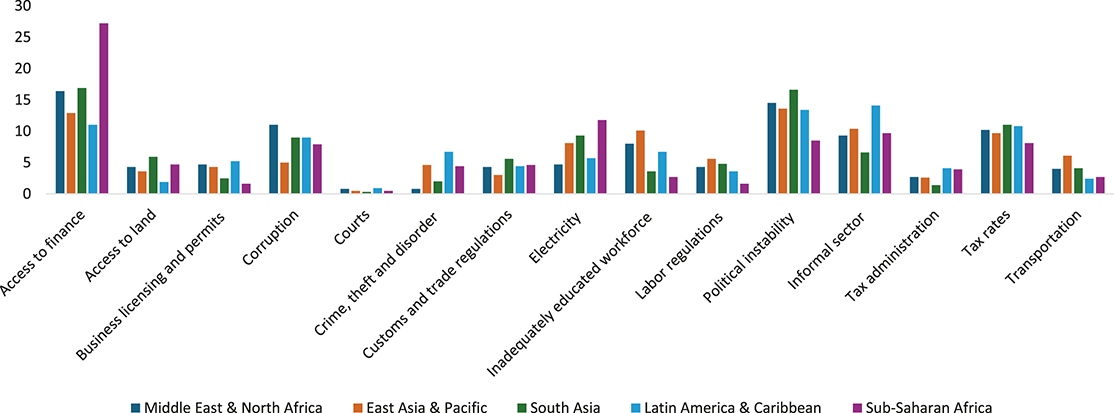

An economy’s vulnerability to external shocks mainly depends on export concentration in a limited number of products and trading partners. Columns 3 and 6 of Table 3 display the product export concentration index in 2000 and 2022 for MENA countries. The export concentration index shows to which degree exports of individual economies or of groups of economies are concentrated on a few products rather than being distributed in a more homogeneous manner among several products (UNCTAD). An index value closer to 1 indicates that exports are highly concentrated in a few products. An index value closer to 0 indicates that exports are more homogeneously distributed among a series of products. Columns 4 and 7 of Table 3 show the export diversification index in 2000 and 2022 for MENA countries. The export diversification index indicates to what extent the structure of exports by product of a given economy or group of economies differs from the world pattern (UNCTAD). The diversification index ranges between 0 and 1: a value of zero means the country’s exports match the world average. Higher values indicate the country’s dependence on a small number of products.

Table 3a Long description

The table comparing the export concentration and diversification indices in MENA countries for 2000 against 2022, differentiating between oil-exporting countries and oil-importing countries. MENA oil exporters include Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE (GCC countries), as well as Algeria, Iran, Iraq, Libya, Yemen (non-GCC countries).

Table 3b Long description

MENA oil importers include: Djibouti, Egypt, Israel, Jordan, Lebanon, Malta, Morocco, Syria, Tunisia, and WBG.

Notes: (i) The export concentration index shows to which degree exports of individual economies or of groups of economies are concentrated on a few products rather than being distributed in a more homogeneous manner among several products (UNCTAD). An index value closer to 1 indicates that exports are highly concentrated in a few products. An index value closer to 0 indicates that exports are more homogeneously distributed among a series of products.

(ii) The export diversification index indicates to what extent the structure of exports by product of a given economy or group of economies differs from the world pattern (UNCTAD). The diversification index ranges between 0 and 1: a value of zero means the country’s exports match the world average. Higher values indicate the country’s dependence on a small number of products.

(iii) UAE: United Arab Emirates; WBG: West Bank & Gaza.

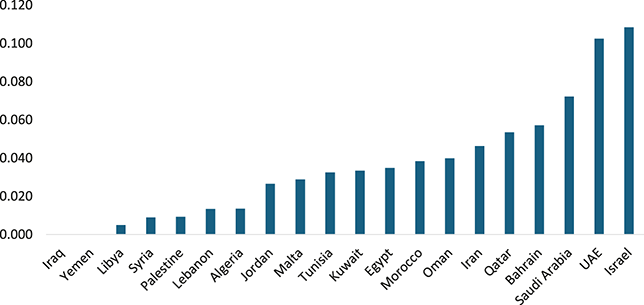

Table 3 shows that oil-exporting countries are more concentrated in their export products than oil-importing countries, and this finding seems to be persistent over time. Indeed, the export concentration index is higher for oil exporters than oil importers in 2000 and in 2022. In 2022, the more concentrated countries in their export products are Iraq, Yemen, Oman, Iran, and Libya with export concentration indices of 0.974, 0.861, 0.801, 0.779, and 0.763 respectively. Non-GCC oil-exporting countries appear to be less concentrated in export products than GGC countries in 2022. It is noteworthy that the export concentration index decreased for most countries between 2000 and 2022, mostly for oil-exporting countries, and particularly GGC countries among oil exporters, relatively to non-oil-exporting countries, highlighting the efforts deployed by the governments to decrease their heavy dependence on natural resources. Indeed, the index decreased significantly for oil exporters like Oman (from 0.801 to 0.292), Iran (from 0.779 to 0.288), Kuwait (from 0.618 to 0.276), and Yemen (from 0.861 to 0.436). One exception to that is Algeria that witnessed a mild increase in its index (from 0.515 to 0.543). Oil importers have seen an increase in their export concentration except for Egypt, Israel, Syria, and Tunisia.

The export diversification index tells a similar story; that is, oil exporters are generally less diversified than oil importers, and that oil exporters became more diversified over time. The United Arab Emirates (UAE) is the most diversified economy among oil exporters and, in 2022, becomes one of the most diversified MENA economies with an export diversification index of 0.529, standing slightly behind Israel (0.491) and Tunisia (0.506). The least diversified oil-exporting countries in 2000 were Iraq (0.85), Yemen (0.48), Qatar (0.842), Algeria (0.834), and Kuwait (0.829). Despite achieving some progress in product diversification, Iraq, Libya, Qatar, and Saudi Arabia are the least diversified oil exporters in 2020 with an export diversification index of 0.849, 0.807, 0.759, and 0.751 respectively. Among oil importers, Syria and Morocco are the least diversified, displaying values of the diversification index around 0.8, similar to most oil exporters. The same countries are on the top of the least diversified economies in 2022, although they have made some progress in this regard. According to Acharyya and Ganguly (Reference Acharyya and Ganguly2023), countries with less diversified exports tend to experience greater income inequality and vulnerability to external shocks. In the case of Morocco and Syria, their limited export base leads to the concentration of wealth and income among a few, such as those in primary sectors like agriculture (in Morocco) or oil (in Syria). Additionally, reliance on agricultural exports in Morocco means that climate change can significantly impact income levels, while dependence on oil in Syria makes it vulnerable to fluctuations in global oil prices. In both countries, the lack of diversification reflects constraints in education, skills development, and technological capabilities, hindering the shift to higher-quality exports that could promote broader economic opportunities and reduce inequality.

5.2 Trade in Services

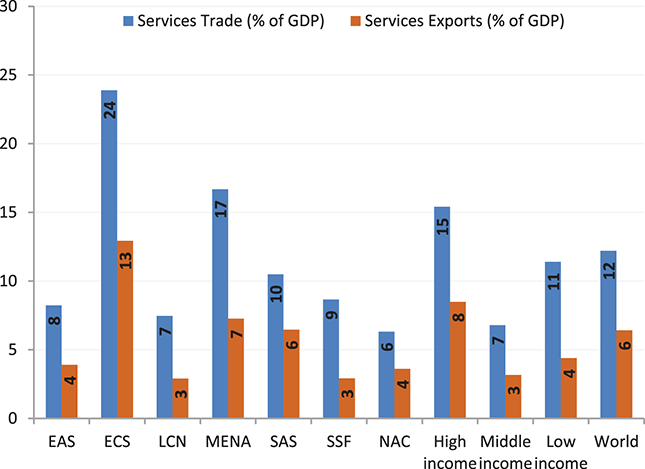

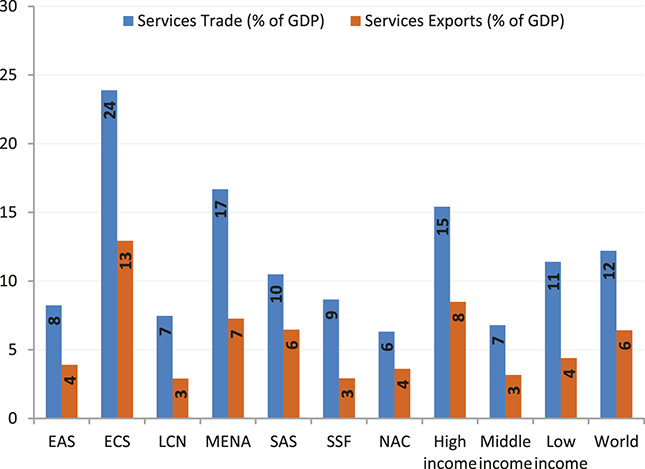

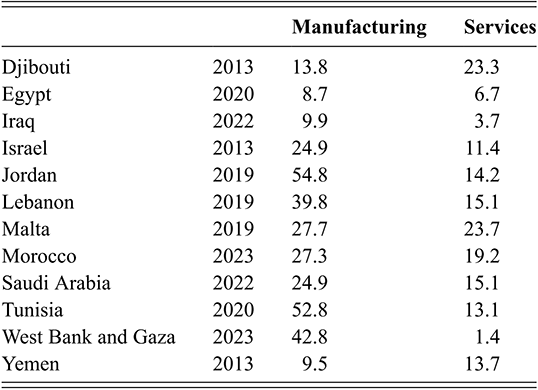

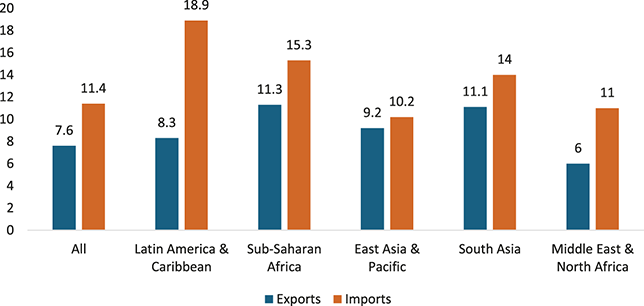

Chanda (Reference Chanda and Reinert2017) emphasizes the growing importance of services trade in the global economy, a trend that is particularly relevant for MENA countries that are increasingly relying on services as part of their development strategies, to drive economic diversification, create jobs, and promote sustainable growth, away from traditional sectors like oil and gas. According to data from the World Development Indicators (WDI), the share of service value added in MENA GDP stands at 52.43% in 2021. Despite the fact that the production of services is a core activity in the MENA region, the share of services in MENA GDP is below the world’s average (63.97%), the average for high-income countries (70%), as well as the average for developed regions like North America (76.58%) and Europe and Central Asia (64,14%). While the share of services in MENA GDP is almost comparable to middle-income countries (52.95%), it exceeds the figure for South Asia (48.87%) and for developing regions like sub-Saharan Africa (47.76%) as well as the average for low-income countries (36.15%).

Although the share of service value added in GDP appears to be positively linked to countries’ income level, standing at 70% for high-income countries, against 53% and 36%, respectively, in middle- and low-income countries, the picture looks different for MENA countries, highlighting significant differences existing between income groups as well as within the same group. Indeed, WDI data show that high-income countries like Qatar, the UAE, Oman, Saudi Arabia, and Bahrain have a share of service value added in GDP below the region’s average, while in Malta and Israel, service value added accounts for 78% and 72% of GDP, respectively, exceeding by far the region’s average. In addition, in some low- and middle-income countries, the share of services in GDP exceeds the region’s average as well as the same share for high-income countries in the region, such as in Lebanon (94%), Djibouti (75%), Tunisia, Jordan, and West Bank and Gaza (around 60%). By contrast, other countries in the same income group show a share of service value added in GDP below the regional average, such as Libya (26%), Iraq, and Syria (43%).

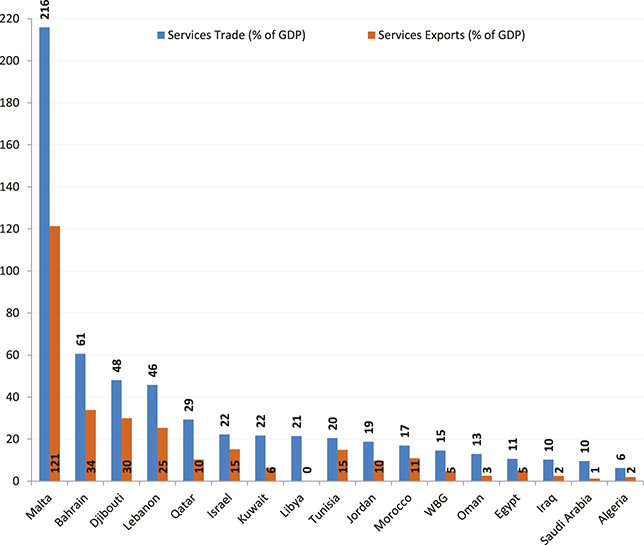

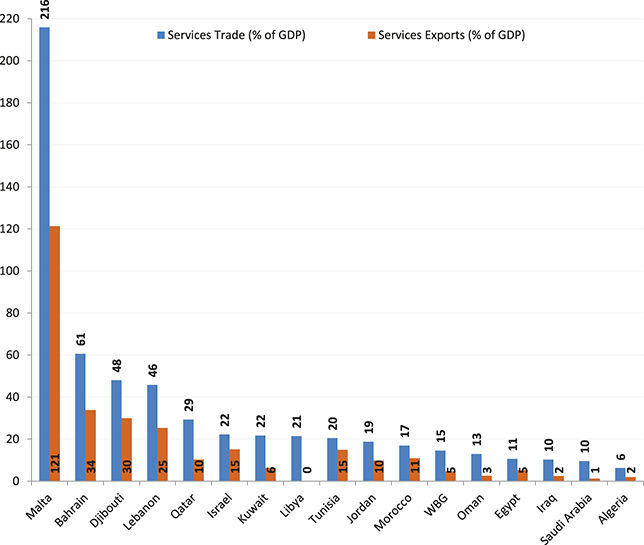

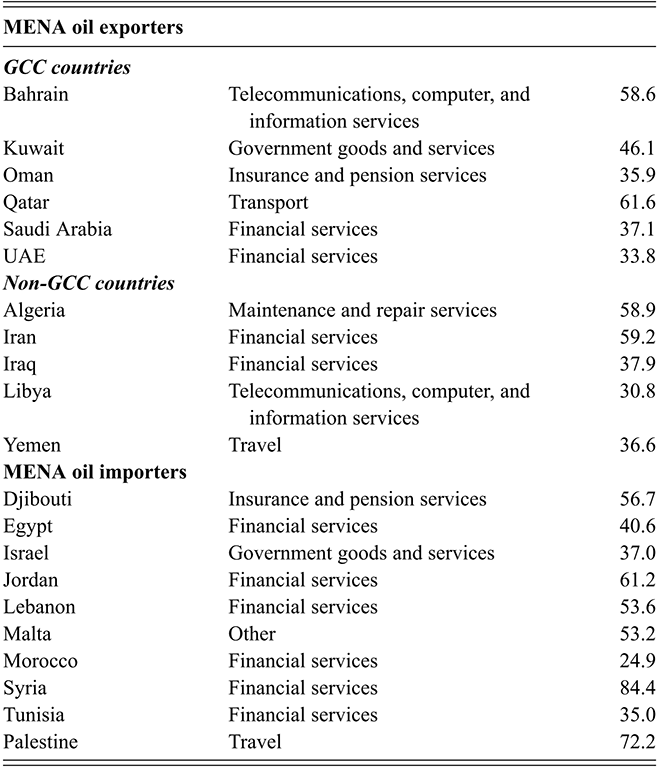

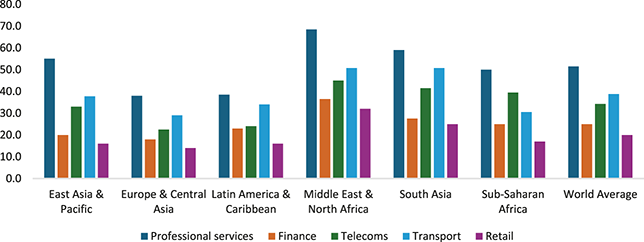

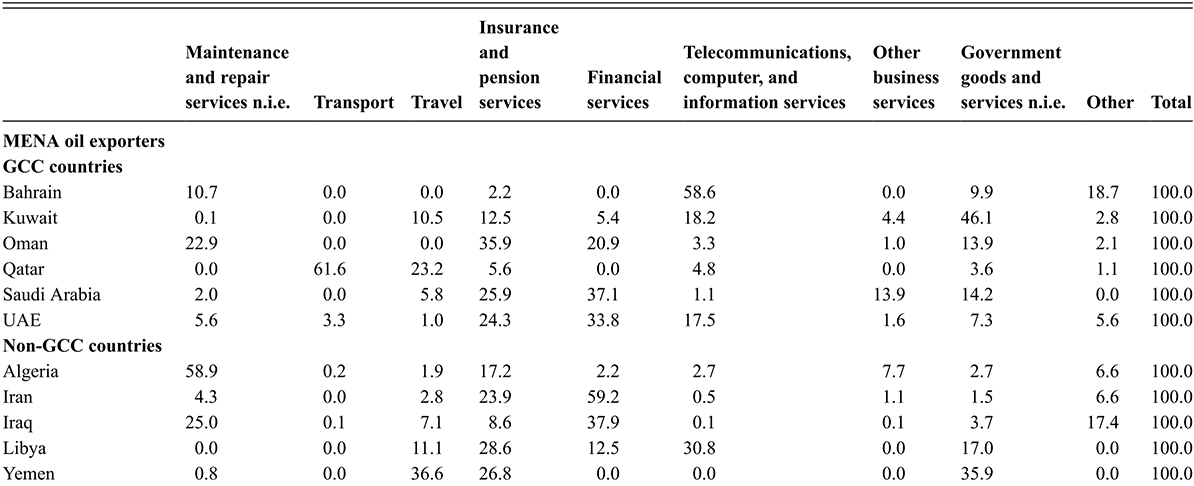

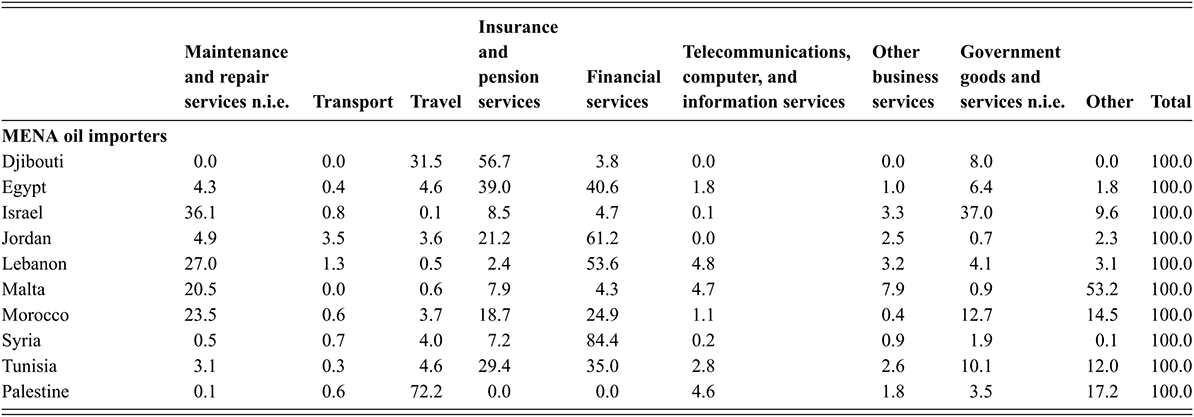

Although the previous figures show that the service sector is a core activity in the MENA region, Figure 6 shows that trade in services as percentage of GDP only accounts for 6.68% of MENA GDP. However, and surprisingly, the share of service trade in MENA GDP exceeds the world’s average (12.19%), the average for high-income countries (15.4%), as well as the average of all other regions, developed and developing ones, except Europe and Central Asia (23.89%). Indeed, Figure 7 shows that this favorable standing of the MENA region is mainly due to countries like Malta where service trade accounted for 215.87% of GDP, Bahrain, Djibouti, and Lebanon where the share of service trade in GDP is almost triple the region’s average (60.62%, 48.04%, and 45.77% respectively). Not only Malta displays the highest figure relatively to all MENA countries, but also this figure is at least 3.5 times the share of the second standing country which is Djibouti. A closer look to Figure 7 reveals significant differences between countries within the same income group. For instance, in high-income countries other than Malta and Bahrain, such as Qatar, Israel, and Kuwait, trade in services accounts for 22–29% of GDP, which is half the figure for Bahrain, and almost one-seventh the figure for Malta. At the same time, high-income countries such as Oman and Saudi Arabia fall behind the region’s average (12.95% and 9.56% respectively). Similarly, while Djibouti and Lebanon stand far from their peers with shares being more than double the regional average, other low- and middle-income countries, like Libya, Tunisia, Jordan, and Morocco, exhibit a share of service trade in GDP that beats the region’s average but is half the share of Djibouti and Lebanon. On the other hand, low- and middle-income countries such as West Bank and Gaza, Egypt, Iraq, and Algeria fall behind the regional average, and Algeria ranks last among MENA countries with a share of service trade in GDP of 6.20%. At the sectoral level, Table 4 shows that financial services dominate MENA exports of services (in both oil-rich and oil-poor countries), followed by insurance, and government services (for more details, see Table A.2 in the appendix).

Services trade as a percentage of GDP, 2021

Note: (i) Trade in services is the sum of service exports and imports divided by the value of GDP, all in current U.S. dollars (data available). Services exports in GDP is calculated as the share of services exports in GDP, all in current US$.

(ii) EAS: East Asia & Pacific; ECS: Europe & Central Asia; LCN: Latin America & Caribbean; MENA: Middle East & North Africa; SAS: South Asia; SSF: Sub-Saharan Africa; NAC: North America.

Services trade as a percentage of GDP by country, 2021

Note: (i) Trade in services is the sum of service exports and imports divided by the value of GDP, all in current U.S. dollars (data available). Services exports in GDP is calculated as the share of services exports in GDP, all in current US$. (ii) WBG: West Bank and Gaza.

Table 4 Long description

The table differentiates between oil-exporting countries and oil-importing countries. MENA oil exporters include Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE (GCC countries), as well as Algeria, Iran, Iraq, Libya, Yemen (non-GCC countries). MENA oil importers include: Djibouti, Egypt, Israel, Jordan, Lebanon, Malta, Morocco, Syria, Tunisia, Palestine.

A closer look at Figure 6 reveals that while high-income countries and developed regions are net exporters of services, the MENA region is a net importer of services, just like middle- and low-income countries, and other developing regions such as Latin America and the Caribbean and sub-Saharan Africa. Indeed, service exports only account for 7.26% of MENA GDP in 2021, although this share beats the world’s average as well as the average for other regions except Europe and Central Asia (12.93%), and all income groups except high-income countries (8.47%). However, not all MENA countries are net importers of services. Figure 7 shows that the following countries are net exporters of services: Malta, Djibouti, Bahrain, Lebanon, Israel, Tunisia, Jordan, and Morocco. In 2021, Malta exhibited the largest share of service exports in GDP (121.35%), which is at least 3.5 times higher than the other major service exporters such as Bahrain (33.81%), Djibouti (29.93%), and Lebanon (25.28%). Malta is a hub for financial services, and has developed a strong regulatory framework to attract international financial institutions. Additionally, it is popular for tourism and business services (legal, accounting, consulting services), and is a leading center for online gaming and iGaming services, with many international gaming companies operating from there. Bahrain is a major exporter of financial services, tourism, business services, logistics and transportation services, and Djibouti is known for port and logistics services, financial services, and tourism. Lebanon is a major exporter of IT services and education services, in addition to tourism and financial services. As expected, GGC countries, excluding Bahrain and Qatar, and non-GCC oil exporters display a modest share of service exports in GDP, below the regional average, with the lowest figures being for Saudi Arabia (1.18%), Algeria (1.97%), and Oman (2.53%).

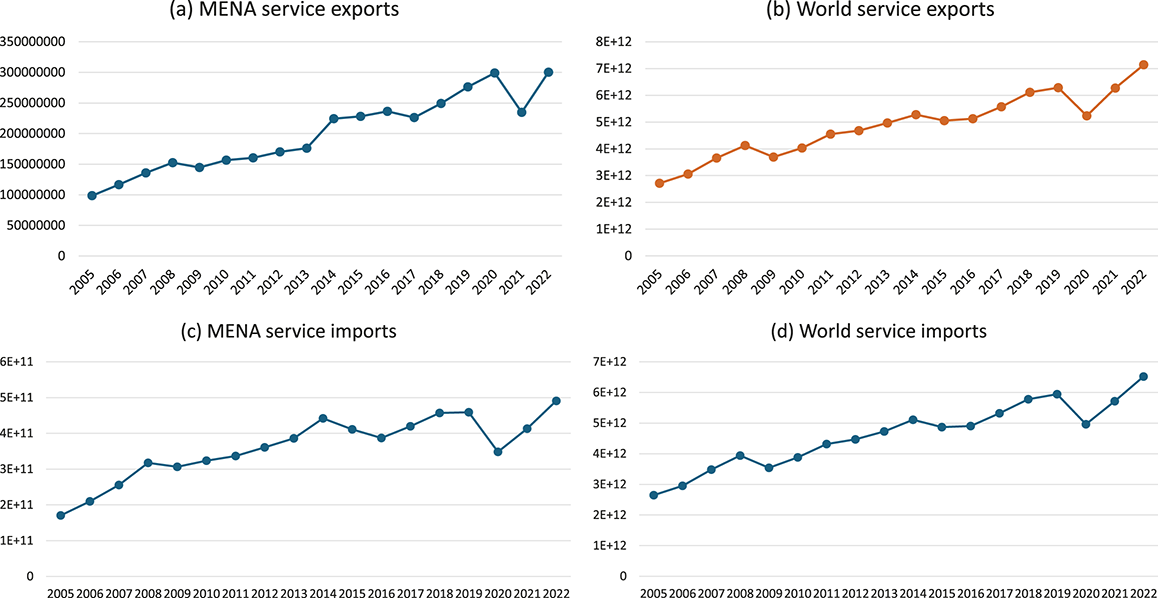

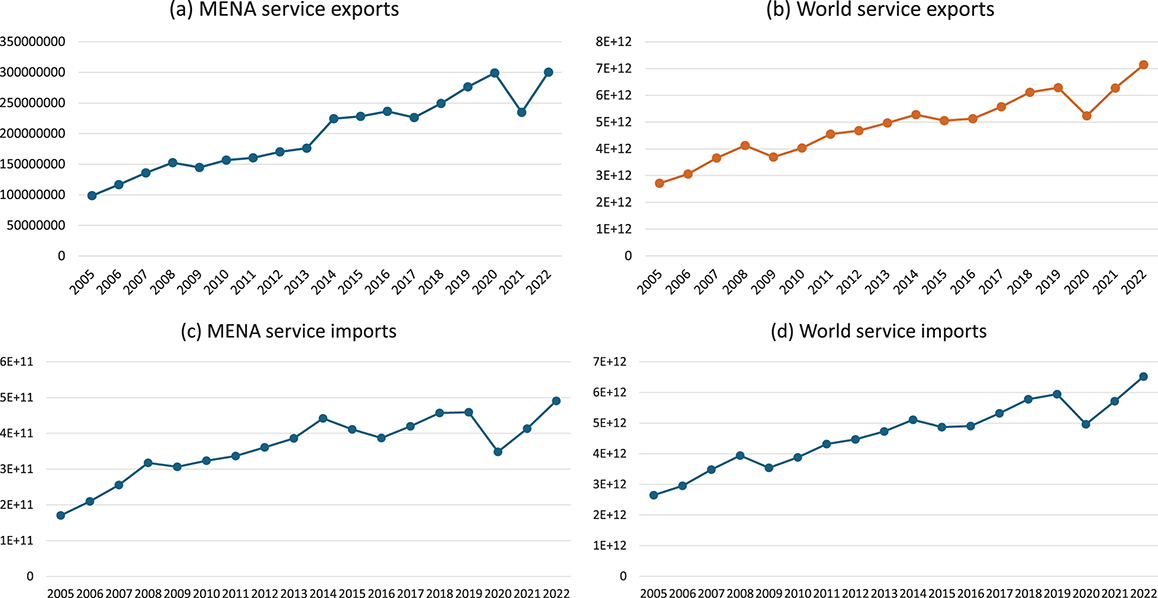

Despite the low share of service trade in GDP and the fact that the MENA region is a net importer of services, as highlighted from the comparison of panels (a) and (c) from Figure 8, it is noteworthy that exports and imports of services have both increased in the MENA region since 2005, before declining sharply in 2020–2021 due to the COVID-19 pandemic. In fact, the evolution over the years of both MENA service exports and imports are comparable to the evolution of world service exports and imports, all bouncing back after the pandemic. However, the growth of MENA exports and imports of services has not kept pace with the growth of world service exports and imports post-pandemic, reflecting losses in market shares of MENA countries (Figure 8). Indeed, while world service exports and imports have reached record levels after the pandemic, MENA service exports only hit the pre-pandemic level in 2022, while MENA service imports surpass the pre-pandemic import level. This observation points to a loss of competitiveness of MENA exporters in key services activities. For instance, Lebanon’s financial sector, once a regional hub, has faced significant challenges due to political instability and an ongoing economic crisis. Improvements in infrastructure and service efficiency in Kenya and Ethiopia have affected Djibouti’s competitiveness in logistics and transportation services. MENA’s tourism exports post-pandemic have seen slower recoveries than other countries such as Greece and Turkey, drawing visitors away from MENA destinations.

Exports and imports of services in the MENA region vs. the world, 2005–2022