Despite the important role played by intermediation in most markets, it is largely ignored by the standard theoretical literature. This is because a study of intermediation requires a basic model that describes explicitly the trade frictions that give rise to the function of intermediation. But this is missing from the standard market models, where the actual process of trading is left unmodeled.

Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987)

1 Introduction

This Element surveys the theoretical economic literature on middlemen (i.e., intermediaries in the exchange process). This is relevant because, as is well recognized, intermediation plays a big role in many (if not most) markets for consumption goods, productive inputs, and assets, yet the activity is absent in standard general equilibrium theory. We present modern developments using search theory to study middlemen in markets with explicit frictions. The goal is not to discuss every paper in detail, but to develop a consistent framework that can be used to illustrate various models and ideas.Footnote 1

Starting with Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987), this research builds models where intermediation emerges because certain agents have comparative advantages along some dimension. A general version of the Rubinstein–Wolinsky model is presented in Section 3, but here is an outline. There are consumers and producers of something called

, plus other agents that neither consume nor produce

, plus other agents that neither consume nor produce

, but potentially could act as middlemen by buying it from producers and selling it to consumers. In many (but not all) models agents meet bilaterally at random. In the original formulation, these other agents perform a middleman function when they have an advantage in search (i.e., they meet consumers faster than producers meet consumers).

, but potentially could act as middlemen by buying it from producers and selling it to consumers. In many (but not all) models agents meet bilaterally at random. In the original formulation, these other agents perform a middleman function when they have an advantage in search (i.e., they meet consumers faster than producers meet consumers).

Further studies generalize the framework’s technical specification by allowing different bargaining powers (in the original specification all agents have the same bargaining power); general populations (in the original the measures of buyers and sellers are the same); endogenous entry (participation is fixed in the original); production, search, and storage costs (these are absent from the original model); goods that are divisible (goods are indivisible in the original); and payment frictions (the original has transferable utility).

Further studies also explore different assumptions about the kinds of advantage middlemen might have, including superior information that lets them better recognize quality, a technology that lets them hold larger or more diverse inventories, and a superior ability to better enforce debt repayment. A main goal is to characterize the set of parameters consistent with the existence of equilibria with active intermediaries. Papers also investigate whether there is uniqueness or multiplicity of equilibria, as well as how intermediation affects efficiency. They also analyze if it attenuates or accentuates volatility. Of particular interest is finding conditions under which there emerge different patterns of exchange – only direct trade, only indirect trade, or both. Some papers also consider how multiple middlemen enter into intermediation chains. We review all of these in what follows.

While this Element mainly concerns theory, some facts help the motivation. In an early contribution, Spulber (Reference Spulber1996a) documented that intermediated exchange accounted for over 25% of GDP in the US in 1993, including retail trade (9.33%), wholesale trade (6.51%), finance/insurance (7.28%), and selected services (1.89%). Updating this from 1993 to 2025, 25% increased to 35.1% (BEA, US Department of Commerce, Federal Reserve Bank of St. Louis). For food, from 1993 to 2023, the share of dollars going to farmers and manufacturers declined from about 34% to 29%, while the share going to wholesale (distribution), retailing (supermarkets and grocery stores), and food services (restaurants, cafeterias, etc.) rose from 48% to 58% (USDA ERS Food Dollar Series). Switching from food to drink, in 2017 direct-to-consumer wine sales in the US were around 10% of the market, with the rest accounted for by retailers (Rhodes et al. Reference Rhodes, Watanabe and Zhou2021). In real estate, intermediated trade accounts for 91% of sales. In the labor market, recruitment and staffing firms account for two-thirds of all postings and attract most of the applications (Davis and de la Parra Reference Davis and de la Parra2025).

Philippon (Reference Philippon2015) discusses the share of financial intermediation in GDP and how it changes over time. As Lagos and Rocheteau (Reference Lagos and Rocheteau2006) report, different asset markets feature different microstructures – that is, while intermediated trade in the fed funds market is about 40%, NASDAQ is closer to 100%, and many OTC (over-the-counter) markets are in between, including markets for corporate, municipal, and emerging-market debt. In international trade, the impact of intermediation shows up in various ways, such as the fact that in the US wholesale and retail firms account for approximately 11% and 24% of exports and imports (Bernard et al. Reference Bernard, Jensen, Redding and Schott2007). The use of intermediary firms is especially important in developing economies, especially in Asia – for example, in the 1980s 300 trading (nonmanufacturing) Japanese firms accounted for 80% of trade (Rossman Reference Rossman1984).

In China today, Ahn et al. (Reference Ahn, Khandelwal and Wei2011) show 22% of exports are handled by intermediaries. In firm-level data, they also show that small or less productive firms rely disproportionately on intermediaries to access foreign markets. Those firms using intermediaries are significantly more likely to eventually become direct exporters, implying intermediaries lower entry barriers and boost overall trade. In the used-car market, Biglaiser et al. (Reference Biglaiser, Li, Murry and Zhao2020) document that dealer-mediated transactions command a consistent price premium over private sales, especially for older vehicles, and that cars sold through dealers exhibit higher quality. Together, all these findings demonstrate that middlemen can affect both the quantity and the quality of trade, and that suggests they are worth studying seriously.

Monieson (Reference Monieson2010) provides historical perspective on middlemen. While there are many interesting facets of this history that could be mentioned, one issue going back a long way is this: Do they provide a useful service, or simply profit from buying low and selling high? An extreme view is epitomized by Benjamin Disraeli, who said “It is well-known what a middleman is: he is a man who bamboozles one party and plunders the other.”Footnote 2 An alternative possibility is that they facilitate the process of exchange, which can enhance efficiency and welfare. As Ayn Rand (1971, p. 313) put it, “The shortest distance between two points is not a straight line – it’s a middleman.”Footnote 3

Reality may be somewhere between these extremes. While theory alone does not definitively resolve this debate, modeling intermediated trade formally in economic theory helps us understand the relevant factors. Before getting into formal models, we offer this story from Turner (Reference Turner1836, pp. 115–16), quoting a source from the eleventh century on the practice of buying low and selling high:

In the Saxon dialogues, the merchant (mancgere) is introduced: “I say that I am useful to the king, and to ealdormen, and to the rich, and to all people. I ascend my ship with my merchandise, and sail over the sea-like places, and sell my things, and buy dear things which are not produced in this land, and I bring them to you here with great danger over the sea; and sometimes I suffer shipwreck, with the loss of all my things, scarcely escaping myself.”

“What things do you bring to us?”

“Skins, silks, costly gems, and gold; various garments, pigment, wine, oil, ivory, and orichalcus, copper, and tin, silver, glass, and suchlike.”

“Will you sell your things here as you brought them here?”

“I will not, because what would my labour benefit me? I will sell them dearer here than I bought them there, that I may get some profit, to feed me, my wife, and children.”

The rest of the Element is organized as follows. Section 2 presents a rudimentary environment by way of introducing some basic terminology, notation, and ideas. Section 3 extends this to a generalization of the environment in Rubinstein–Wolinsky. Section 4 considers alternative assumptions and analyzes the possibility of multiple equilibria and endogenous dynamics. Sections 5 and 6 discuss information frictions and intermediation chains. Section 7 considers papers on inventories and directed rather than random search, while Section 8 summarizes some work focusing on OTC asset markets. Section 9 focuses on the relationship between middlemen, money, and credit. Section 10 mentions papers that do not fit elsewhere in the Element but are still relevant. Section 11 concludes.

2 A Simple Model

Before discussing the literature, it is useful to construct a simple two-period model that captures some of the main ideas, and, in particular, provides a clean version of the classic result in Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987). It also lets us introduce notation, labeling, etcetera.

There are three agents – a producer

, a middleman

, a middleman

, and a consumer

, and a consumer

– that are interested in trading an indivisible good

– that are interested in trading an indivisible good

. The producer

. The producer

produces one unit of

produces one unit of

at cost

at cost

, which we set to zero for now (for some applications it is better to think of

, which we set to zero for now (for some applications it is better to think of

as being endowed with

as being endowed with

). The consumer

). The consumer

derives utility

derives utility

from consuming one unit (for some applications it is better to think of

from consuming one unit (for some applications it is better to think of

as an input or asset and

as an input or asset and

as

as

’s profit or return to acquiring it). The middleman

’s profit or return to acquiring it). The middleman

neither produces nor consumes

neither produces nor consumes

, but could acquire it from

, but could acquire it from

and resell it to

and resell it to

; that is intermediated trade.

; that is intermediated trade.

There are two periods, or stages, to the trading process, with

indifferent between getting

indifferent between getting

in the first or second stage. Trade is bilateral, with the terms of trade determined here by generalized Nash bargaining, where the share of agent

in the first or second stage. Trade is bilateral, with the terms of trade determined here by generalized Nash bargaining, where the share of agent

when bargaining with

when bargaining with

is denoted

is denoted

. There is at most one meeting per period, and the probability agent

. There is at most one meeting per period, and the probability agent

meets agent

meets agent

in each period is

in each period is

, or equivalently

, or equivalently

, by the bilateral nature of meetings. For now the

, by the bilateral nature of meetings. For now the

’s are parameters; later, they come from an underlying meeting technology. If

’s are parameters; later, they come from an underlying meeting technology. If

meets

meets

in the first stage, they trade, and the game is over. What is to be determined: Do

in the first stage, they trade, and the game is over. What is to be determined: Do

and

and

trade if they meet in the first stage?

trade if they meet in the first stage?

Let there be returns to holding

for

for

and

and

in the second stage, denoted

in the second stage, denoted

and

and

, where

, where

stands for storage costs in goods markets, while

stands for storage costs in goods markets, while

stands for dividends in asset markets. For now we assume

stands for dividends in asset markets. For now we assume

(but see Section 4), with the cost incurred between the first and second stage, so it is sunk when

(but see Section 4), with the cost incurred between the first and second stage, so it is sunk when

or

or

with

with

meets

meets

in stage 2. In addition to

in stage 2. In addition to

, there is a second tradable object,

, there is a second tradable object,

, that is divisible and serves as a payment instrument. The most generous way to think about this is the following: Any agent can produce or consume

, that is divisible and serves as a payment instrument. The most generous way to think about this is the following: Any agent can produce or consume

at constant marginal cost, or constant marginal utility, both normalized to

at constant marginal cost, or constant marginal utility, both normalized to

, and when

, and when

acquires

acquires

from

from

, the former makes a payment

, the former makes a payment

that increases

that increases

’s payoff and decreases

’s payoff and decreases

’s payoff by the same amount.

’s payoff by the same amount.

This way of sharing the trade surplus, using

as a means of payment, is essentially what is usually called transferable utility. Our interpretation is generous in the sense that the direct transfer of utility is problematic. Consider Binmore (Reference Binmore and Health1992):

as a means of payment, is essentially what is usually called transferable utility. Our interpretation is generous in the sense that the direct transfer of utility is problematic. Consider Binmore (Reference Binmore and Health1992):

Sometimes it is assumed that contracts can be written that specify that some utils are to be transferred from one player to another

Alert readers will be suspicious about such transfers

Alert readers will be suspicious about such transfers

Utils are not real objects and so cannot really be transferred; only physical commodities can actually be exchanged. Transferable utility therefore only makes proper sense in special cases. The leading case is that in which both players are risk-neutral and their von Neumann and Morgenstern utility scales have been chosen so that their utility from a sum of money

Utils are not real objects and so cannot really be transferred; only physical commodities can actually be exchanged. Transferable utility therefore only makes proper sense in special cases. The leading case is that in which both players are risk-neutral and their von Neumann and Morgenstern utility scales have been chosen so that their utility from a sum of money

[in our notation,

[in our notation,

] is simply

] is simply

[in our notation,

[in our notation,

]. Transferring one util from one player to another is then just the same as transferring one dollar.

]. Transferring one util from one player to another is then just the same as transferring one dollar.

We agree that “Utils are not real objects and so cannot really be transferred,” although we are less sure that “only physical commodities can actually be exchanged” since it seems clear that, for example, information or ideas can also be exchanged. A bigger issue concerns the claim that transferable utility is the same as paying with money. In serious monetary models, agents have a value function, or indirect utility function, over money holdings, but it is not generally linear (see surveys by Lagos et al. Reference Lagos, Rocheteau and Wright2017 and Rocheteau and Nosal Reference Rocheteau and Nosal2017). Well, in some models, sometimes money actually does enter linearly but up to a point, which does not correspond to transferable utility for the simple reason that buyers tend to run out of money, while in transferable utility models they never run out of utils.

Therefore, instead of pretending that

is money, it is better to say there is a good

is money, it is better to say there is a good

that anyone can consume and produce. This avoids Binmore’s justified complaint about utils being transferred without doing a disservice to monetary/payment economics. At the risk of sounding pedantic, we emphasize this because work in the area is concerned with microfoundations, so it is important to think through such details, although we try not to dwell on it too much in what follows.

that anyone can consume and produce. This avoids Binmore’s justified complaint about utils being transferred without doing a disservice to monetary/payment economics. At the risk of sounding pedantic, we emphasize this because work in the area is concerned with microfoundations, so it is important to think through such details, although we try not to dwell on it too much in what follows.

So, when

changes hands,

changes hands,

pays

pays

to

to

,

,

pays

pays

to

to

, and

, and

pays

pays

to

to

. Interpreting these as prices, we call

. Interpreting these as prices, we call

the direct price,

the direct price,

the wholesale price, and

the wholesale price, and

the retail price. However, this is not as obvious as it may appear. First, if

the retail price. However, this is not as obvious as it may appear. First, if

is divisible, and endogenous, as it is in some of the models presented in Sections 5, 7, and 9, in principle it might be better to call

is divisible, and endogenous, as it is in some of the models presented in Sections 5, 7, and 9, in principle it might be better to call

the price. Having said that, in practice it could be that we see (in the data)

the price. Having said that, in practice it could be that we see (in the data)

but not

but not

, which is especially relevant when

, which is especially relevant when

corresponds to quality rather than quantity. Second, while

corresponds to quality rather than quantity. Second, while

is the price of

is the price of

in terms of

in terms of

, it makes as much sense to say

, it makes as much sense to say

is the price of

is the price of

in terms of

in terms of

.

.

In standard usage the price refers to the amount of money a buyer pays to get

, which is hard to understand in models without money. Indeed, without money changing hands, it is not at all clear who is the buyer and who is the seller, any more than those labels make sense when

, which is hard to understand in models without money. Indeed, without money changing hands, it is not at all clear who is the buyer and who is the seller, any more than those labels make sense when

gives

gives

apples in trade for bananas. This may or may not matter, depending on context (see Wright and Wong Reference Wright and Wong2014 for an extended discussion). In any case, if we call the

apples in trade for bananas. This may or may not matter, depending on context (see Wright and Wong Reference Wright and Wong2014 for an extended discussion). In any case, if we call the

s prices, there arise several other interesting variables, like the spread

s prices, there arise several other interesting variables, like the spread

and markup

and markup

.

.

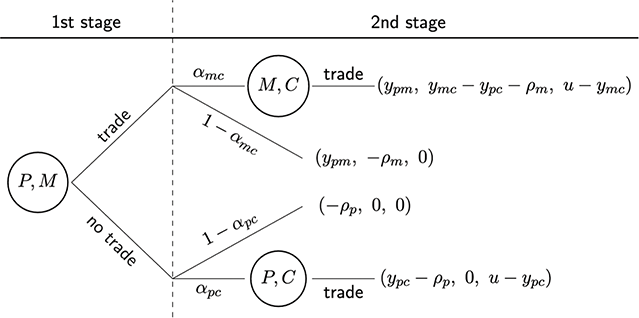

In the first period,

is assumed to produce

is assumed to produce

before meetings occur. If

before meetings occur. If

meets

meets

they always trade, as mentioned. If

they always trade, as mentioned. If

meets no one, or

meets no one, or

meets

meets

and they decide not to trade,

and they decide not to trade,

and

and

proceed to stage 2, while

proceed to stage 2, while

is assumed to drop out, which, by assumption, does not affect the probability

is assumed to drop out, which, by assumption, does not affect the probability

and

and

meet. If

meet. If

meets

meets

and they trade,

and they trade,

and

and

proceed to stage 2 while

proceed to stage 2 while

drops out, since, by assumption,

drops out, since, by assumption,

can only produce once here. Note that in a stage 1 meeting,

can only produce once here. Note that in a stage 1 meeting,

and

and

can differ along three dimensions:

can differ along three dimensions:

, their probability of meeting

, their probability of meeting

in stage 2;

in stage 2;

, their bargaining power; and

, their bargaining power; and

, their return to holding

, their return to holding

, which for the purposes of this discussion satisfies

, which for the purposes of this discussion satisfies

(but see Section 4).

(but see Section 4).

Let

,

,

, and

, and

be the value functions of

be the value functions of

,

,

, and

, and

in the second stage. Then, the surpluses

in the second stage. Then, the surpluses

when

when

trades with

trades with

, using the labels direct, retail, and wholesale suggested earlier, are:

, using the labels direct, retail, and wholesale suggested earlier, are:

(1)

(1)

(2)

(2)

(3)

(3)

In each trade

solves the bargaining problem

solves the bargaining problem

(4)

(4)

However, with transferable utility (in the sense discussed earlier, where

produces and

produces and

consumes it with equal marginal cost and utility), the bargaining protocol, as long as it is reasonable, does not matter. So, we simply say

consumes it with equal marginal cost and utility), the bargaining protocol, as long as it is reasonable, does not matter. So, we simply say

gets a share

gets a share

of total surplus

of total surplus

, which leads to

, which leads to

(5)

(5)

Let the probability

and

and

trade at stage 1 be

trade at stage 1 be

. Then the second-stage value functions are

. Then the second-stage value functions are

(6)

(6)

(7)

(7)

(8)

(8)

In other words, these values are the product of meeting probabilities and surpluses, minus storage cost. Note that for now it is taken for granted that all agents participate in the market, but that will be checked in Section 3.

Then, after inserting the

s and

s and

s, we have

s, we have

(9)

(9)

(10)

(10)

(11)

(11)

Note that

and

and

do not enter the second stage simultaneously. At least one of

do not enter the second stage simultaneously. At least one of

or

or

is an off-equilibrium value. Nonetheless, we need to track both in order to determine

is an off-equilibrium value. Nonetheless, we need to track both in order to determine

, the probability of wholesale trade. Here

, the probability of wholesale trade. Here

only depends on the sign of the total surplus

only depends on the sign of the total surplus

; that is, whether there are gains from trade between

; that is, whether there are gains from trade between

and

and

. What we call the best response conditions are then:

. What we call the best response conditions are then:

(12)

(12)

When all agents participate,

is the only decision. Thus, an equilibrium is given by

is the only decision. Thus, an equilibrium is given by

’s and

’s and

satisfying (9)–(12), from which other variables, like the

satisfying (9)–(12), from which other variables, like the

s, are easily determined.

s, are easily determined.

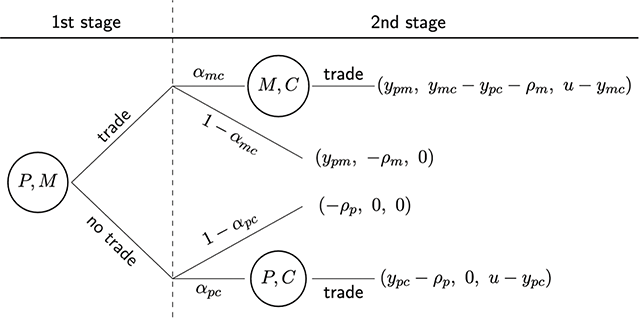

Figure 1 shows the structure of the model. It is easy to see that equilibrium exists and is unique. Letting

, in equilibrium

, in equilibrium

if

if

and

and

if

if

.Footnote 4 Intuitively,

.Footnote 4 Intuitively,

means

means

is active, intermediating by buying

is active, intermediating by buying

from

from

and selling it to

and selling it to

, if and only if

, if and only if

has some advantage over

has some advantage over

. This in general means

. This in general means

has some combination of being better at search,

has some combination of being better at search,

, or bargaining,

, or bargaining,

, or storage,

, or storage,

. Although their environment is more complicated in some ways, Rubinstein–Wolinsky (Reference Rubinstein and Wolinsky1987) is, in our notation, the special case where

. Although their environment is more complicated in some ways, Rubinstein–Wolinsky (Reference Rubinstein and Wolinsky1987) is, in our notation, the special case where

and

and

, which gives their classic result:

, which gives their classic result:

is active if and only if

is active if and only if

. More generally,

. More generally,

can be fundamentally inferior to

can be fundamentally inferior to

in terms of search or storage,

in terms of search or storage,

or

or

, and equilibrium can still have

, and equilibrium can still have

, if

, if

has an advantage over

has an advantage over

squeezing surplus out of

squeezing surplus out of

, which looks like inefficient rent-seeking activity.

, which looks like inefficient rent-seeking activity.

Structure of the simple model.

To be precise, we can measure welfare by the sum of the

s, which equals the expected utility of

s, which equals the expected utility of

minus the cost of

minus the cost of

or

or

delivering the goods. The optimal wholesale trade maximizes welfare:

delivering the goods. The optimal wholesale trade maximizes welfare:

Letting

, it follows that

, it follows that

if

if

and

and

otherwise. Note that

otherwise. Note that

depends on the

depends on the

s while

s while

does not. Given

does not. Given

and

and

, we can evaluate when equilibrium is efficient. In the special Rubinstein–Wolinsky (Reference Rubinstein and Wolinsky1987) case,

, we can evaluate when equilibrium is efficient. In the special Rubinstein–Wolinsky (Reference Rubinstein and Wolinsky1987) case,

and

and

, equilibrium and efficiency coincide: Both imply middlemen should be active if and only if

, equilibrium and efficiency coincide: Both imply middlemen should be active if and only if

. However, going beyond their special case, we can have

. However, going beyond their special case, we can have

when

when

or vice versa, depending on parameters, and in particular depending on the

or vice versa, depending on parameters, and in particular depending on the

s.Footnote 5

s.Footnote 5

The aforementioned analysis is predicated on

and

and

participating in the market, which must be checked. For stage 1, everyone participates, since it is costless. For stage 2, while

participating in the market, which must be checked. For stage 1, everyone participates, since it is costless. For stage 2, while

still participates for free, for

still participates for free, for

we need

we need

, or, in terms of primitives,

, or, in terms of primitives,

. In general, there are four possibilities for the equilibrium pattern of exchange, or what we call the equilibrium regime, in stage 2: Regime N, for no trade, occurs if

. In general, there are four possibilities for the equilibrium pattern of exchange, or what we call the equilibrium regime, in stage 2: Regime N, for no trade, occurs if

for both

for both

, so expected profit does not justify the cost. Regime D, for direct trade, occurs if

, so expected profit does not justify the cost. Regime D, for direct trade, occurs if

for

for

but not

but not

. Regime I, for indirect trade only, occurs if

. Regime I, for indirect trade only, occurs if

for

for

but not

but not

. Regime B, for both direct and indirect trade, occurs if

. Regime B, for both direct and indirect trade, occurs if

for

for

and

and

. These four regimes appear in several other models discussed in Sections 4, 5, 6, and 9.

. These four regimes appear in several other models discussed in Sections 4, 5, 6, and 9.

Equilibrium features a classic holdup problem since the search/storage cost is sunk when

or

or

meets

meets

at stage 2. Likewise, the wholesale price

at stage 2. Likewise, the wholesale price

at which

at which

gets

gets

from

from

in stage 1 is sunk when

in stage 1 is sunk when

meets

meets

. Agents cannot recoup sunk costs in bargaining for the usual reason: These costs are paid whether or not they trade, so they cancel out of the surplus (the payoff to trade minus the payoff to no trade). This distorts equilibrium as follows: In equilibrium

. Agents cannot recoup sunk costs in bargaining for the usual reason: These costs are paid whether or not they trade, so they cancel out of the surplus (the payoff to trade minus the payoff to no trade). This distorts equilibrium as follows: In equilibrium

and

and

participate as stage 2 sellers when

participate as stage 2 sellers when

, while efficiency suggests they should participate when

, while efficiency suggests they should participate when

. For the equilibrium and efficiency conditions to coincide for all values of the parameters we need

. For the equilibrium and efficiency conditions to coincide for all values of the parameters we need

.Footnote 6

.Footnote 6

Holdup problems exist in many economic models with bargaining. One take on this is that they can be avoided by having agents contract the terms of trade before incurring sunk costs. That is sometimes ruled out exogenously. In search theory, ruling it out seems less ad hoc once one recognizes that you cannot contract with someone before you contact them. We can eliminate part of the problem by an assumption on exogenous parameters,

, but the endogenous wholesale price

, but the endogenous wholesale price

is still sunk when

is still sunk when

and

and

meet. Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987) propose a consignment procedure to deal with that:

meet. Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987) propose a consignment procedure to deal with that:

only pays

only pays

after

after

pays

pays

. Whether this is feasible depends on assumptions – can

. Whether this is feasible depends on assumptions – can

and

and

stay in contact while waiting for

stay in contact while waiting for

? In any case, it does not affect their main result: Given

? In any case, it does not affect their main result: Given

and

and

, activity by

, activity by

depends solely on the sign of

depends solely on the sign of

.

.

In what follows we consider other advantages middlemen may have. We also consider going beyond two periods, sometimes to an infinite horizon, which is interesting and even crucial in some applications (e.g., introducing money or endogenous debt limits). A goal is to characterize the equilibrium set to see when we can support different regimes. Another is to discuss existence, uniqueness or multiplicity, and dynamics in various extensions of the basic framework.

3 Extending the Simple Model

We now present (a generalized version of) the framework used in Rubinstein and Wolinsky (Reference Rubinstein and Wolinsky1987). Time

is continuous and the horizon is infinite. A continuum of agents come in three types,

is continuous and the horizon is infinite. A continuum of agents come in three types,

,

,

, and

, and

, acting in the roles played in Section 2. They all discount future payoffs at rate

, acting in the roles played in Section 2. They all discount future payoffs at rate

. While different versions presented in this section make different assumptions about this, in the original specification type

. While different versions presented in this section make different assumptions about this, in the original specification type

stay in the market forever while

stay in the market forever while

and

and

exit after one trade, with an exogenous inflow of new

exit after one trade, with an exogenous inflow of new

and

and

agents so the market can be open in the long run.Footnote 7

agents so the market can be open in the long run.Footnote 7

At any

the state of the system is given by the distribution of inventories across type

the state of the system is given by the distribution of inventories across type

. With

. With

indivisible, an individual

indivisible, an individual

has inventory

has inventory

, where

, where

may be finite or infinite. Many papers (though not all) set

may be finite or infinite. Many papers (though not all) set

, so there are just two kinds of middlemen; let us call them

, so there are just two kinds of middlemen; let us call them

and

and

, with the subscript indicating inventory. Hence, at any

, with the subscript indicating inventory. Hence, at any

a measure

a measure

are type

are type

with

with

unit of

unit of

, and a measure

, and a measure

are type

are type

with

with

inventory, where

inventory, where

. Restricting

. Restricting

is a technological assumption that

is a technological assumption that

can store at most one unit of

can store at most one unit of

, and

, and

can produce and

can produce and

can consume at most one unit at a time. This assumption has precedent in search theory,Footnote 8 and Section 7 discusses papers that relax it.

can consume at most one unit at a time. This assumption has precedent in search theory,Footnote 8 and Section 7 discusses papers that relax it.

Given

, the return to

, the return to

from holding a unit of

from holding a unit of

is again

is again

. We can also add a fixed entry cost

. We can also add a fixed entry cost

for type

for type

, different from

, different from

in that it is paid once and not each period, but

in that it is paid once and not each period, but

for now. Meetings are characterized by Poisson processes with arrival rates

for now. Meetings are characterized by Poisson processes with arrival rates

denoting the probability per unit time that type

denoting the probability per unit time that type

meets

meets

, and bilateral meetings imply the identities

, and bilateral meetings imply the identities

.

.

The meeting process in Rubinstein–Wolinsky can be interpreted in terms of spatial separation, even if they were not specific about it. A significant feature of their formulation is that the measure of type

does not affect the probability

does not affect the probability

meets

meets

when

when

and

and

. Other papers proceed differently, and a common specification has the probability that

. Other papers proceed differently, and a common specification has the probability that

meets

meets

proportional to the fraction of type

proportional to the fraction of type

among the total population of participating agents in the market. This is sometimes called uniform random meetings, and implies the measure of

among the total population of participating agents in the market. This is sometimes called uniform random meetings, and implies the measure of

in the market, for example, affects the probability

in the market, for example, affects the probability

meets

meets

, which can be understood as a congestion effect that is assumed away in the original model.

, which can be understood as a congestion effect that is assumed away in the original model.

Let

be the probability of trade when

be the probability of trade when

meets

meets

. With transferable utility, as described earlier,

. With transferable utility, as described earlier,

wants to trade with

wants to trade with

if and only if

if and only if

wants to trade with

wants to trade with

if and only if the joint surplus is positive, so we can use either

if and only if the joint surplus is positive, so we can use either

or

or

to indicate the probability they trade. Some of the

to indicate the probability they trade. Some of the

s are trivial; for example,

s are trivial; for example,

is automatic since when

is automatic since when

meets

meets

with inventory

with inventory

, or

, or

meets

meets

with inventory

with inventory

, trade is impossible. The rate at which

, trade is impossible. The rate at which

switches from

switches from

to

to

is

is

, and the rate at which

, and the rate at which

switches back is

switches back is

. In general, both are the product of chance (a meeting) and choice (a trade).

. In general, both are the product of chance (a meeting) and choice (a trade).

Let

and

and

be the value functions for

be the value functions for

and

and

, and let

, and let

or

or

be the value functions for

be the value functions for

holding

holding

or

or

unit of

unit of

. As mentioned, here

. As mentioned, here

and

and

leave after trading while

leave after trading while

stays. The surplus

stays. The surplus

when

when

trades with

trades with

is:

is:

(13)

(13)

(14)

(14)

(15)

(15)

where

is assumed to produce upon meeting as in Rubinstein–Wolinsky.

is assumed to produce upon meeting as in Rubinstein–Wolinsky.

For the terms of trade, with transferable utility, reasonable bargaining solutions all give similar results. Here we use generalized Nash bargaining: In each trade, the payment

solves

solves

(16)

(16)

This yields:

(17)

(17)

(18)

(18)

(19)

(19)

Thus, payment

is a weighted average of the benefit to the agent receiving

is a weighted average of the benefit to the agent receiving

and the cost to the agent giving it up; for example, when

and the cost to the agent giving it up; for example, when

gets

gets

from

from

the benefit to the former is

the benefit to the former is

while the cost for the latter is

while the cost for the latter is

.

.

Also, with transferable utility, the best response conditions for whether

and

and

trade are given by:

trade are given by:

(20)

(20)

The original Rubinstein–Wolinsky setup has new

and

and

agents flowing into the market at an exogenous rate

agents flowing into the market at an exogenous rate

, making the stocks

, making the stocks

and

and

endogenous. The stocks

endogenous. The stocks

and

and

are also endogenous, but of course we only need to keep track of

are also endogenous, but of course we only need to keep track of

since

since

with

with

fixed. Hence, the relevant laws of motion or the state of the system are

fixed. Hence, the relevant laws of motion or the state of the system are

(21)

(21)

(22)

(22)

(23)

(23)

where the

s are derivatives with respect to time.

s are derivatives with respect to time.

The value functions expressed in terms of

satisfy

satisfy

(24)

(24)

(25)

(25)

(26)

(26)

(27)

(27)

Consider (24). In words, it says the flow value

is the rate

is the rate

at which

at which

meets

meets

, times the probability

, times the probability

they trade, times

they trade, times

’s surplus from that trade; plus the rate

’s surplus from that trade; plus the rate

at which

at which

meets

meets

with inventory, times the probability

with inventory, times the probability

they trade, times

they trade, times

’s surplus from that trade; plus the pure rate of time change

’s surplus from that trade; plus the pure rate of time change

, which is

, which is

in steady state but not in general. The other equations have similar interpretations.

in steady state but not in general. The other equations have similar interpretations.

With dynamic models we have to be a little more careful in defining things. An equilibrium here consists of paths for: the value functions

, the terms of trade, which with

, the terms of trade, which with

indivisible are given by

indivisible are given by

, the trading strategies

, the trading strategies

, and the state variables

, and the state variables

, satisfying the dynamic programming equations, bargaining solutions, best response conditions, and laws of motion. Equilibrium must also satisfy an initial condition saying where the system starts in terms of N, plus the usual nonnegativity and boundedness conditions.Footnote 9 A stationary equilibrium is a special case where

, satisfying the dynamic programming equations, bargaining solutions, best response conditions, and laws of motion. Equilibrium must also satisfy an initial condition saying where the system starts in terms of N, plus the usual nonnegativity and boundedness conditions.Footnote 9 A stationary equilibrium is a special case where

,

,

, and

, and

are time-invariant functions of

are time-invariant functions of

(they can depend on the state but not the date). A steady state is a solution to the equilibrium conditions other than the initial condition where endogenous variables are constant.

(they can depend on the state but not the date). A steady state is a solution to the equilibrium conditions other than the initial condition where endogenous variables are constant.

In Rubinstein–Wolinsky, as mentioned earlier, the arrival rate

depends on

depends on

and

and

, the measures of

, the measures of

and

and

, but not on other

, but not on other

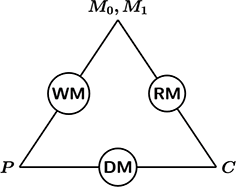

s. This rules out third-party congestion in the meeting process, which is convenient, but the microfoundations may not be obvious. Figure 2 depicts a market structure consistent with their assumptions, featuring spatial separation, as in Gong et al. (Reference Gong, Qiao and Wright2024).

s. This rules out third-party congestion in the meeting process, which is convenient, but the microfoundations may not be obvious. Figure 2 depicts a market structure consistent with their assumptions, featuring spatial separation, as in Gong et al. (Reference Gong, Qiao and Wright2024).

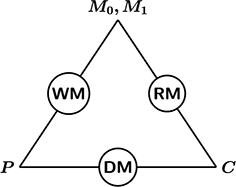

Market structure consistent with Rubinstein–Wolinsky (Reference Rubinstein and Wolinsky1987).

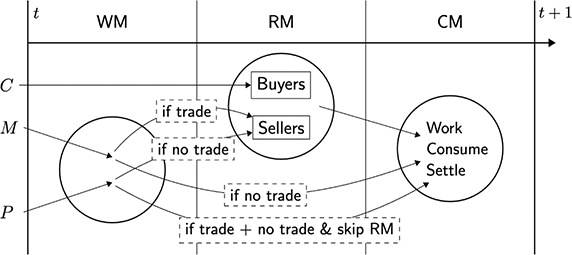

In Figure 2 different types are located at distinct locations represented by nodes on a triangle. Agents visit both of their nearby markets, represented by the edges, but not the third – it’s just too far. One can interpret this as saying there are three submarkets labeled as follows: a direct market (DM) with

and

and

; a wholesale market (WM) with

; a wholesale market (WM) with

and

and

; and a retail market (RM) with

; and a retail market (RM) with

and

and

. This spatial separation is consistent with the Rubinstein–Wolinsky paper.

. This spatial separation is consistent with the Rubinstein–Wolinsky paper.

Now is a good time to discuss meeting technologies. Following textbook methods (e.g., Pissarides Reference Pissarides2000), consider a two-sided market with measures

of buyers and

of buyers and

of sellers. The number of meetings is assumed to be an increasing, concave function

of sellers. The number of meetings is assumed to be an increasing, concave function

, implying arrival rates

, implying arrival rates

. A common assumption that we adopt is that

. A common assumption that we adopt is that

displays constant returns to scale, which implies the arrival rates depend only on market tightness,

displays constant returns to scale, which implies the arrival rates depend only on market tightness,

. As mentioned earlier, and as Figure 2 shows, agents participate in both of their nearby markets but not the third.Footnote 10

. As mentioned earlier, and as Figure 2 shows, agents participate in both of their nearby markets but not the third.Footnote 10

This allows us to use a general two-sided meeting technology in each of the submarkets, which is convenient because it is not clear how to use a general meeting technology in a three-sided market (more on this in Sections 4, 6, 8, and 9). To proceed, let the DM, WM, and RM meetings technologies be

, for

, for

, where the

, where the

s are constants describing search efficiency. Then, as in Rubinstein–Wolinsky, assume

s are constants describing search efficiency. Then, as in Rubinstein–Wolinsky, assume

, but

, but

can be different, and in particular

can be different, and in particular

is better than

is better than

at meeting

at meeting

based on the fundamental technology when

based on the fundamental technology when

, although the equilibrium arrival rates depend on tightness.

, although the equilibrium arrival rates depend on tightness.

Now, as in Rubinstein–Wolinsky, we focus on steady states that are symmetric in the sense that

, which implies

, which implies

,

,

,

,

, and

, and

. Also, as in their original model, we set

. Also, as in their original model, we set

. The goal is to determine the trading pattern given by the

. The goal is to determine the trading pattern given by the

s. It is clear that

s. It is clear that

and

and

always trade (

always trade (

). The more interesting questions are whether

). The more interesting questions are whether

without inventory trade with

without inventory trade with

(determined by

(determined by

), and whether

), and whether

with inventory trade with

with inventory trade with

(determined by

(determined by

). Clearly, if

). Clearly, if

then

then

, since a buy-and-hold strategy for

, since a buy-and-hold strategy for

is not a good idea when

is not a good idea when

. What remains to determine is whether

. What remains to determine is whether

and

and

trade, as determined by

trade, as determined by

.

.

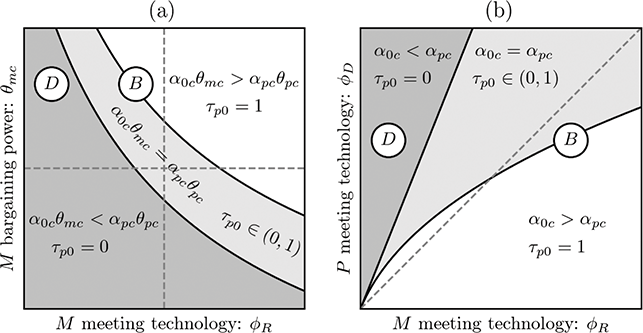

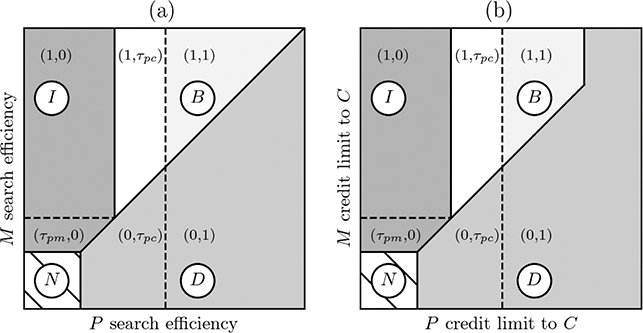

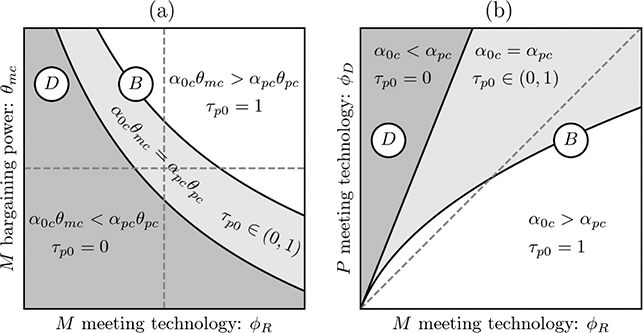

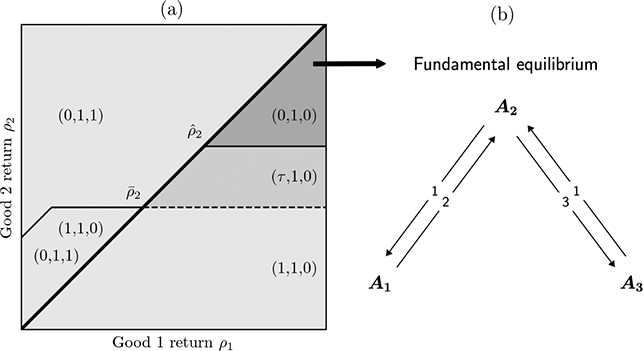

Although the Rubinstein–Wolinsky paper does not mention existence or uniqueness, from Gong et al. (Reference Gong, Qiao and Wright2024) we know that a symmetric steady state exists and is unique. This is illustrated in Figure 3. In the panel (a), on the vertical axis is

’s bargaining power, with the horizontal dashed line giving

’s bargaining power, with the horizontal dashed line giving

’s bargaining power, so that above the line

’s bargaining power, so that above the line

is better than

is better than

at extracting surplus from

at extracting surplus from

. On the horizontal axis is

. On the horizontal axis is

’s search efficiency, defined by

’s search efficiency, defined by

in meeting technology,

in meeting technology,

, while the vertical dashed line represents

, while the vertical dashed line represents

–so to the right of this line

–so to the right of this line

has a fundamental advantage in search. Panel (b) is similar but drawn in

has a fundamental advantage in search. Panel (b) is similar but drawn in

space.

space.

Equilibrium set as a function of parameters.

Figure 3 shows there are regions of parameter space where

and

and

trade with probability

trade with probability

, where they trade with probability

, where they trade with probability

, and where they trade with probability

, and where they trade with probability

. In terms of the language introduced earlier, there are two possible outcomes: Regime D or B emerges when

. In terms of the language introduced earlier, there are two possible outcomes: Regime D or B emerges when

or

or

. (Regimes

. (Regimes

and

and

for now cannot emerge because

for now cannot emerge because

is always in the market and happy to trade with

is always in the market and happy to trade with

for now – but see Sections 4 and 9) Related to Section 2, the result can be stated as follows:

for now – but see Sections 4 and 9) Related to Section 2, the result can be stated as follows:

implies

implies

, so

, so

and

and

trade whenever they meet;

trade whenever they meet;

implies

implies

and

and

never trade when they meet; and

never trade when they meet; and

implies they sometimes trade when they meet.Footnote 11

implies they sometimes trade when they meet.Footnote 11

This is a generalization of the Rubinstein–Wolinsky result, but as intuitive as it may be, the result is not totally satisfactory because it gives a relationship between the

s and

s and

s, both of which are equilibrium outcomes. Hence, it must be interpreted carefully. In particular, it is possible for

s, both of which are equilibrium outcomes. Hence, it must be interpreted carefully. In particular, it is possible for

to face a less efficient meeting technology, in the sense that

to face a less efficient meeting technology, in the sense that

is low, but due to endogenous tightness

is low, but due to endogenous tightness

can still be high and hence

can still be high and hence

still active. Indeed, as panel (a) of Figure 3 shows,

still active. Indeed, as panel (a) of Figure 3 shows,

is active when

is active when

and

and

have the same meeting technology and bargaining power, at the intersection of the two dashed lines, so by continuity

have the same meeting technology and bargaining power, at the intersection of the two dashed lines, so by continuity

is active with a moderate disadvantage in their meetings and bargaining. Similarly,

is active with a moderate disadvantage in their meetings and bargaining. Similarly,

might have a better

might have a better

and better

and better

than

than

, yet

, yet

.

.

So while the result is correct, it could easily be misinterpreted. However, the bigger point is that we now have a characterization of the

s and

s and

s in terms of parameters, as shown in Figure 3. In other words, there is a relationship between the

s in terms of parameters, as shown in Figure 3. In other words, there is a relationship between the

s and

s and

s, but it is not causal, since both are functions of other, more fundamental, factors.

s, but it is not causal, since both are functions of other, more fundamental, factors.

Having made that point, beyond characterizing

’s activity, the theory has implications for how the terms of trade depend on fundamentals. One can check that both

’s activity, the theory has implications for how the terms of trade depend on fundamentals. One can check that both

and

and

decrease with an improvement in the meeting technology indexed by the

decrease with an improvement in the meeting technology indexed by the

s, which seems natural. However, the average

s, which seems natural. However, the average

paid by

paid by

is nonmonotone because of composition effects – namely, faster search encourages participation by

is nonmonotone because of composition effects – namely, faster search encourages participation by

, and since

, and since

charges more than

charges more than

, the average price paid by

, the average price paid by

might increase. One can also check that price dispersion (as measured by, e.g., the coefficient of variation) can be nonmonotone.Footnote 12

might increase. One can also check that price dispersion (as measured by, e.g., the coefficient of variation) can be nonmonotone.Footnote 12

We close this part of the discussion with an important modeling detail. The original Rubinstein–Wolinsky formulation has long-lived

(they stay in the market forever) but short-lived

(they stay in the market forever) but short-lived

and

and

(they leave after one trade), with an exogenous inflow

(they leave after one trade), with an exogenous inflow

of the short-lived types. Consider an environment that is similar except

of the short-lived types. Consider an environment that is similar except

and

and

, as well as

, as well as

, stay forever, and in the interest of stationarity set

, stay forever, and in the interest of stationarity set

. This makes the surpluses simpler because continuation values cancel with threat points,

. This makes the surpluses simpler because continuation values cancel with threat points,

(28)

(28)

and the payments become

(29)

(29)

(30)

(30)

(31)

(31)

Having all agents in the market forever has consequences. If, for example, type

agents leave after trading, when they meet

agents leave after trading, when they meet

they may pass on trade to wait for a meeting with

they may pass on trade to wait for a meeting with

; but if type

; but if type

stays after trading, at least with

stays after trading, at least with

, we must have

, we must have

, allowing us to shift the focus elsewhere, like endogenous entry. Due to its relative tractability, several models presented herein have all agents in the market forever. A general point that one should always keep in mind is that modeling details like this can matter when exploring microfoundations.Footnote 13

, allowing us to shift the focus elsewhere, like endogenous entry. Due to its relative tractability, several models presented herein have all agents in the market forever. A general point that one should always keep in mind is that modeling details like this can matter when exploring microfoundations.Footnote 13

4 Multiplicity and Dynamics

Some papers are concerned with whether we get uniqueness or multiplicity of steady state, and whether there are dynamic equilibria with fluctuations based solely on beliefs. This issue is obviously related to the venerable notion that intermediation, perhaps especially financial intermediation, might engender instability or volatility.Footnote 14 Now models based on Rubinstein–Wolinsky have dynamics: If the initial condition for

is not at its steady state value, then the unique equilibrium is stationary and converges to steady state, so there is no instability or volatility. What happens if we deviate from the original formulation?

is not at its steady state value, then the unique equilibrium is stationary and converges to steady state, so there is no instability or volatility. What happens if we deviate from the original formulation?

Nosal et al. (Reference Nosal, Wong and Wright2019) study a three-sided market where

,

,

, and

, and

interact via a uniform random meeting specification: conditional on

interact via a uniform random meeting specification: conditional on

meeting someone, the probability it is type

meeting someone, the probability it is type

is proportional to the fraction of type

is proportional to the fraction of type

in the market. Normalizing

in the market. Normalizing

, the rate at which type

, the rate at which type

meets

meets

is

is

, where

, where

is a baseline arrival rate that is the same for all agents. Notice that rules out something that was the focus of the above analysis: It means

is a baseline arrival rate that is the same for all agents. Notice that rules out something that was the focus of the above analysis: It means

and therefore

and therefore

cannot have an advantage over

cannot have an advantage over

in finding type

in finding type

.Footnote 15

.Footnote 15

Even without an advantage in finding type

,

,

can still be active for other reasons in Nosal et al. (Reference Nosal, Wong and Wright2019). In that paper, all agents stay in the market forever, which, as mentioned earlier, means that

can still be active for other reasons in Nosal et al. (Reference Nosal, Wong and Wright2019). In that paper, all agents stay in the market forever, which, as mentioned earlier, means that

always trades with

always trades with

since there is no opportunity cost. This might suggest that

since there is no opportunity cost. This might suggest that

agents are doing something socially valuable: When

agents are doing something socially valuable: When

trades

trades

to

to

they both become sellers, increasing the probability

they both become sellers, increasing the probability

gets

gets

. However, rather than having agents acting as

. However, rather than having agents acting as

to exploit this idea, it might be better to have them act as

to exploit this idea, it might be better to have them act as

, because the best

, because the best

can do is to give

can do is to give

to

to

if

if

has it in its inventory, while

has it in its inventory, while

can give

can give

to

to

whenever they meet. To pursue this, Nosal et al. (Reference Nosal, Wong and Wright2019) incorporate occupational choice: Anyone who is not type

whenever they meet. To pursue this, Nosal et al. (Reference Nosal, Wong and Wright2019) incorporate occupational choice: Anyone who is not type

can choose to act as

can choose to act as

or

or

, or to opt out of the market entirely.

, or to opt out of the market entirely.

That paper also plays up the distinction between markets for goods and markets for assets by identifying the former with

and the latter with

and the latter with

(although that is less relevant given an extension discussed later in this section). It is further assumed that

(although that is less relevant given an extension discussed later in this section). It is further assumed that

produces a new unit of

produces a new unit of

immediately after trading, before the next meeting, as opposed to producing in a meeting. Hence,

immediately after trading, before the next meeting, as opposed to producing in a meeting. Hence,

as well as

as well as

agents carry inventory. It is useful to have inventories depreciate – that is, vanish – at rate

agents carry inventory. It is useful to have inventories depreciate – that is, vanish – at rate

. Thus, a fundamental advantage for

. Thus, a fundamental advantage for

could be captured by

could be captured by

or

or

, although for simplicity we set

, although for simplicity we set

.

.

Let us start with

. Focusing for now on steady state, there are three possible outcomes: Regime

. Focusing for now on steady state, there are three possible outcomes: Regime

, where the market shuts down; Regime D, where the market is open but no one chooses to act as

, where the market shuts down; Regime D, where the market is open but no one chooses to act as

, so there is only direct trade; and Regime B, where some agents choose to act as

, so there is only direct trade; and Regime B, where some agents choose to act as

, so there is both direct and indirect trade. (Regime I is ruled out here because

, so there is both direct and indirect trade. (Regime I is ruled out here because

can only be active if some agents act as

can only be active if some agents act as

, since

, since

gets inventory from

gets inventory from

.) It can be shown that equilibrium exists uniquely: There is a unique steady state, and if we start away from steady state there is a unique transition path converging to it.

.) It can be shown that equilibrium exists uniquely: There is a unique steady state, and if we start away from steady state there is a unique transition path converging to it.

To give more detail, consider parameter space summarized by storage costs

of

of

and

and

. It partitions into three regions: When

. It partitions into three regions: When

is big for both

is big for both

, Regime N emerges, since storage costs are too high to make participation in the market worthwhile; when

, Regime N emerges, since storage costs are too high to make participation in the market worthwhile; when

is below a threshold and

is below a threshold and

above a (generally different) threshold, Regime D emerges; and when

above a (generally different) threshold, Regime D emerges; and when

is somewhat higher and

is somewhat higher and

lower, Regime B emerges with both direct and indirect trade.

lower, Regime B emerges with both direct and indirect trade.

Now consider

. This turns out to be rather different. First, Regime N cannot emerge for a production cost

. This turns out to be rather different. First, Regime N cannot emerge for a production cost

, or, more generally, for any

, or, more generally, for any

that is not too big, since

that is not too big, since

can always produce and hoard

can always produce and hoard

for its return

for its return

. Therefore

. Therefore

must produce, and when

must produce, and when

meets

meets

they must trade, since

they must trade, since

can produce again. The possible outcomes are shown in panel (a) of Figure 4.Footnote 16

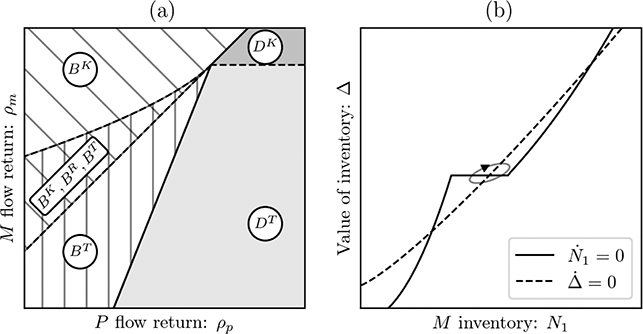

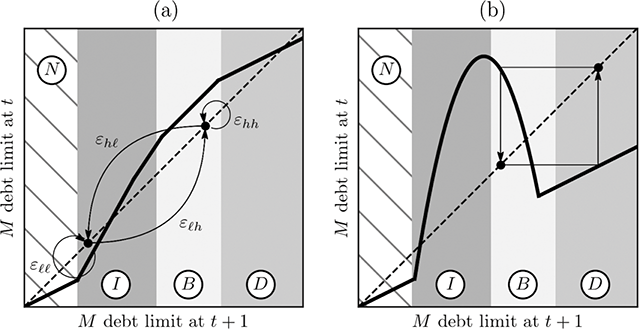

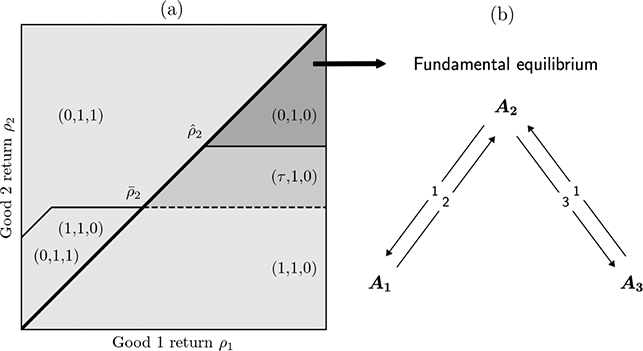

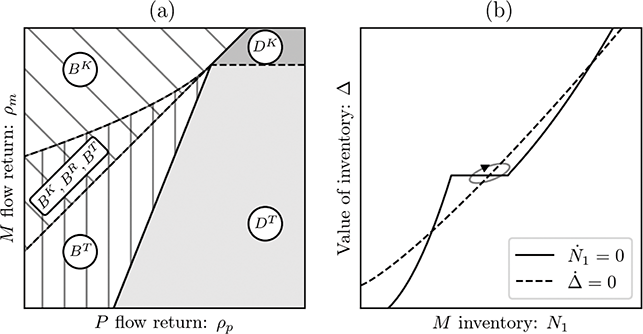

can produce again. The possible outcomes are shown in panel (a) of Figure 4.Footnote 16

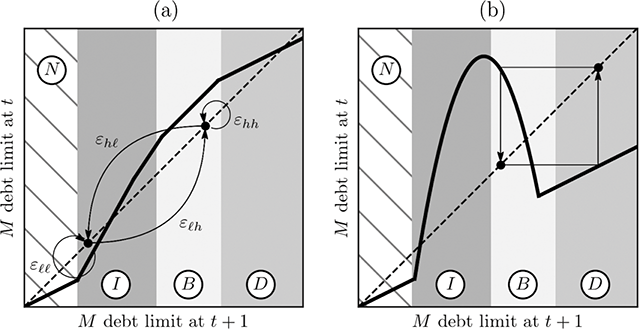

Multiplicity and dynamics.

In the graph, there are steady states with

, which is labeled as region

, which is labeled as region

or

or

, where

, where

indicates direct trade and the superscript indicates what happens off the equilibrium path: If there were a type

indicates direct trade and the superscript indicates what happens off the equilibrium path: If there were a type

with

with

, superscript

, superscript

says

says

would trade it to

would trade it to

, while superscript

, while superscript

says

says

would keep it (while these are the same on the equilibrium path, to show it is an equilibrium, as usual one has to know what happens off the equilibrium path).

would keep it (while these are the same on the equilibrium path, to show it is an equilibrium, as usual one has to know what happens off the equilibrium path).

Now consider steady states with

. These are labeled

. These are labeled

,

,

, and

, and

, where the

, where the

indicates there is both direct and indirect trade, and the superscripts mean this:

indicates there is both direct and indirect trade, and the superscripts mean this:

says

says

trades

trades

to

to

;

;

says

says

keeps

keeps

; and

; and

says

says

randomizes. Naturally,

randomizes. Naturally,

obtains when

obtains when

is big and

is big and

obtains when

obtains when

is small. What is interesting is that over some range, where

is small. What is interesting is that over some range, where

is neither too big nor too small, there is multiplicity: two steady states coexist in pure strategies, one with

is neither too big nor too small, there is multiplicity: two steady states coexist in pure strategies, one with

and one with

and one with

, and, as usual, when there are two pure strategy equilibria there is also a mixed strategy equilibrium with

, and, as usual, when there are two pure strategy equilibria there is also a mixed strategy equilibrium with

.

.

This multiplicity arises only for some parameters; for others there is a unique steady state with

, which is

, which is

if

if

is small,

is small,

if

if

is big, and

is big, and

if

if

is in between. But at least for some nondegenerate set of parameters there is multiplicity. Why? There are two necessary ingredients:

is in between. But at least for some nondegenerate set of parameters there is multiplicity. Why? There are two necessary ingredients:

, and

, and

endogenous.

endogenous.

Here is the intuition. Suppose

, which is like a buy-and-hold strategy by

, which is like a buy-and-hold strategy by

. That makes

. That makes

low (in fact, it is

low (in fact, it is

in steady state, although that changes if there is depreciation,

in steady state, although that changes if there is depreciation,

). When

). When

is low it is hard for

is low it is hard for

to trade, so few agents choose to act as

to trade, so few agents choose to act as

. That makes it hard for

. That makes it hard for

to get

to get

and hence makes

and hence makes

reluctant to trade it away, so

reluctant to trade it away, so

is a best response. Now, suppose

is a best response. Now, suppose

. Then

. Then

is high, making it easier for

is high, making it easier for

to trade, so more agents act as

to trade, so more agents act as

. Then it is easier for

. Then it is easier for

to get

to get

and so

and so

is a best response. For some parameters both outcomes are possible.

is a best response. For some parameters both outcomes are possible.

This discussion and Figure 4 concern steady states, but when there are multiple steady states there can also be multiple dynamic equilibria. These equilibria can display fluctuations even when fundamentals are constant: They are driven purely by beliefs, as self-fulfilling prophecies. Moreover, one can describe the outcomes in terms of market liquidity, which is greater with higher

since that means more trade. Again, for this multiplicity to arise we need endogenous market composition, plus

since that means more trade. Again, for this multiplicity to arise we need endogenous market composition, plus

, since a buy-and-hold strategy is never a good idea when

, since a buy-and-hold strategy is never a good idea when

. This can be interpreted as saying that intermediated markets for assets, with

. This can be interpreted as saying that intermediated markets for assets, with

, can be fragile or volatile, but not intermediated markets for goods, with

, can be fragile or volatile, but not intermediated markets for goods, with

.

.

Gu et al. (Reference Gu, Wang and Wright2026) change that result and interpretation. They show in a generalized environment that similar multiplicity and volatility can arise with

. There are various differences between the papers. One is that instead of endogenizing market composition by having some agents choose to act as either

. There are various differences between the papers. One is that instead of endogenizing market composition by having some agents choose to act as either

or

or

, Gu et al. (Reference Gu, Wang and Wright2026) fix the measure of each type but let type

, Gu et al. (Reference Gu, Wang and Wright2026) fix the measure of each type but let type

participate in the market only if they pay a cost

participate in the market only if they pay a cost

. This is more standard than having agents choose to act as

. This is more standard than having agents choose to act as

or

or

, at least in the sense that it is similar to labor models following Pissarides (Reference Pissarides2000), where firms choose whether to enter, rather than having agents choose whether to be a worker or a firm (which is not to say that models of occupational choice are uninteresting).

, at least in the sense that it is similar to labor models following Pissarides (Reference Pissarides2000), where firms choose whether to enter, rather than having agents choose whether to be a worker or a firm (which is not to say that models of occupational choice are uninteresting).

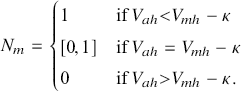

A bigger difference is that Gu et al. (Reference Gu, Wang and Wright2026) have match-specific heterogeneity in buyers’ valuations: When a seller,

or

or

, meets

, meets

the pair draw

the pair draw

at random. This is interesting for its own sake and delivers nice results. First,

at random. This is interesting for its own sake and delivers nice results. First,

’s decision about trading with

’s decision about trading with

is characterized by a reservation value,

is characterized by a reservation value,

, such that they trade when

, such that they trade when

and not when

and not when

, analogous to a reservation wage strategy in job search. It is immediate that

, analogous to a reservation wage strategy in job search. It is immediate that

since

since

must be enough to cover

must be enough to cover

’s loss from giving up inventory. Moreover, this is nice because

’s loss from giving up inventory. Moreover, this is nice because

, and hence the probability of trade between

, and hence the probability of trade between

and

and

, varies smoothly with parameter changes and over time.

, varies smoothly with parameter changes and over time.

This introduces a new reason for

and

and

to not trade: The match-specific

to not trade: The match-specific

is too low. Of course,

is too low. Of course,

wants to trade even at low

wants to trade even at low

as long as

as long as

is low, but

is low, but

means

means

would have to be too low for

would have to be too low for

to agree (the point is that trade requires mutual agreement). This effect is absent in Nosal et al. (Reference Nosal, Wong and Wright2019), where

to agree (the point is that trade requires mutual agreement). This effect is absent in Nosal et al. (Reference Nosal, Wong and Wright2019), where

’s alternative to trading with

’s alternative to trading with

is to enjoy the flow

is to enjoy the flow

, which is never a good alternative when

, which is never a good alternative when

. To be sure,

. To be sure,

discourages trade between

discourages trade between

and

and

– the way unemployment insurance discourages acceptance in job search, say – but we do not need

– the way unemployment insurance discourages acceptance in job search, say – but we do not need

to get

to get

and

and

to pass on trade.

to pass on trade.

The enhanced version of the story is this: Suppose

agents adopt a high reservation value

agents adopt a high reservation value

, which is not a buy-and-hold strategy, but a buy-and-hold-out (for a higher

, which is not a buy-and-hold strategy, but a buy-and-hold-out (for a higher

) strategy. Then

) strategy. Then

is high and

is high and

low, making it hard for

low, making it hard for

to trade so fewer

to trade so fewer

agents enter, replacing the effect described earlier, which is that fewer agents choose to act as

agents enter, replacing the effect described earlier, which is that fewer agents choose to act as

. Still, the outcome is similar: a low

. Still, the outcome is similar: a low

, making it hard for

, making it hard for

to get

to get

and rationalizing high

and rationalizing high

. But if instead

. But if instead

chooses low

chooses low

then

then

will be low and

will be low and

high, making it easier for type

high, making it easier for type

to trade, so more

to trade, so more

enter the market, making it easier for

enter the market, making it easier for

to get inventory and rationalizing low

to get inventory and rationalizing low

.

.

Hence, in this environment, multiplicity due to beliefs does not require

. Not only can there be multiple steady states here, there can be dynamic equilibria where trading strategies and market composition vary over time. Gu et al. (Reference Gu, Wang and Wright2026) use dynamical system theory to prove the existence of continuous time limit cycles – that is, equilibria where endogenous variables fluctuate in the long run – but since the methods are somewhat technical, using bifurcation theory, we do not go into detail (it is not that the math is especially difficult, with Azariadis Reference Azariadis1993, e.g., providing a textbook treatment geared to economists, but we think in this Element our time and space are better spent on other issues).

. Not only can there be multiple steady states here, there can be dynamic equilibria where trading strategies and market composition vary over time. Gu et al. (Reference Gu, Wang and Wright2026) use dynamical system theory to prove the existence of continuous time limit cycles – that is, equilibria where endogenous variables fluctuate in the long run – but since the methods are somewhat technical, using bifurcation theory, we do not go into detail (it is not that the math is especially difficult, with Azariadis Reference Azariadis1993, e.g., providing a textbook treatment geared to economists, but we think in this Element our time and space are better spent on other issues).

However, it is worth noting that the methods used by Gu et al. (Reference Gu, Wang and Wright2026) are difficult (if not impossible) to apply in Nosal et al. (Reference Nosal, Wong and Wright2019), where

is degenerate, because with

is degenerate, because with

degenerate the dynamical system is not smooth: The probability that

degenerate the dynamical system is not smooth: The probability that

trades with

trades with

jumps from

jumps from

to

to

as the system goes from

as the system goes from

to

to