Introduction

In the last few decades, increasing attention has been paid to explaining why human resource (HR) practices might lead to different employee outcomes (Kitt & Sanders, Reference Kitt and Sanders2024). As people can have different insights into the same reality (Fiske & Taylor, Reference Fiske and Taylor1991), employees can perceive and interpret HR practices differently, although such practices are the same for all of them. For this reason, scholars have tried to understand the underlying psychological process through which employees attach meaning to the HR practices (Hewett, Shantz, Mundy & Alfes, Reference Hewett, Shantz, Mundy and Alfes2018; Sanders, Shipton & Gomes, Reference Sanders, Shipton and Gomes2014; Wang, Kim, Rafferty & Sanders, Reference Wang, Kim, Rafferty and Sanders2020).

In this sense, HR attributions refer to the reasons that employees attribute to the organization’s implementation of HR practices (Nishii, Lepak & Schneider, Reference Nishii, Lepak and Schneider2008). Analyzing these HR attributions allows us to understand how employees perceive HR practices and the processes through which such perceptions influence their attitudes and behaviors (Hewett, Reference Hewett, Sanders, Yang and Patel2021; Hewett et al, Reference Hewett, Shantz, Mundy and Alfes2018; Sanders, Guest & Rodrigues, Reference Sanders, Guest and Rodrigues2021). Based on this approach, this study focuses on the reasons employees attribute to the design of pay practices by the organization, which we refer to as employees’ pay attributions.

Among HR practices, compensation has a significant effect on employee behavior, since people act according to the rewards they obtain in exchange for their work (Gomez-Mejia, Berrone & Franco-Santos, Reference Gomez-Mejia, Berrone and Franco-Santos2014). It is therefore important to analyze how employees perceive the compensation system designed by the company, since it will substantially affect how they assess their pay and, consequently, the efforts they will direct toward the achievement of organizational objectives (Williams, McDaniel & Nguyen, Reference Williams, McDaniel and Nguyen2006).

This knowledge holds significant importance, as organizational behavior is deeply impacted by the employee-organization relationship. The way employees interpret workplace events can influence their expectations within the employment relationship by shaping the psychological contract (Kiefer, Barclay, Conway & Briner, Reference Kiefer, Barclay, Conway and Briner2022). Furthermore, previous research has provided evidence that when employees feel supported by their organizations, they tend to exhibit positive attitudes and engage in behaviors that align with organizational goals (Eisenberger et al., Reference Eisenberger, Wen, Zheng, Yu, Liu, Zhang and Kim2023). Understanding these dynamics can prove valuable for employers in effectively managing and nurturing positive workplace relationships that, in turn, enhance both employee and organizational performance (Guest, Reference Guest2017).

Although previous studies have analyzed employees’ attributions toward certain HR practices, such as workload measurement and management practices (Hewett, Shantz & Mundy, Reference Hewett, Shantz and Mundy2019), to the best of our knowledge, studies focusing on specific HR practices are scarce. Analyzing a specific HR practice, rather than bundles of practices, may be necessary to the extent that individuals’ attributions are context-specific (Lord & Smith, Reference Lord and Smith1983) and because employees evaluate specific HR practices differently (Nishii & Wright, Reference Nishii, Wright and Smith2008). Additionally, Özçelik and Uyargil (Reference Özçelik and Uyargil2022) found that different employee groups generate similar perceptions of HR practices, except for the company’s pay system. Hence, pay practices seem to generate specific employee perceptions that deserve special attention.

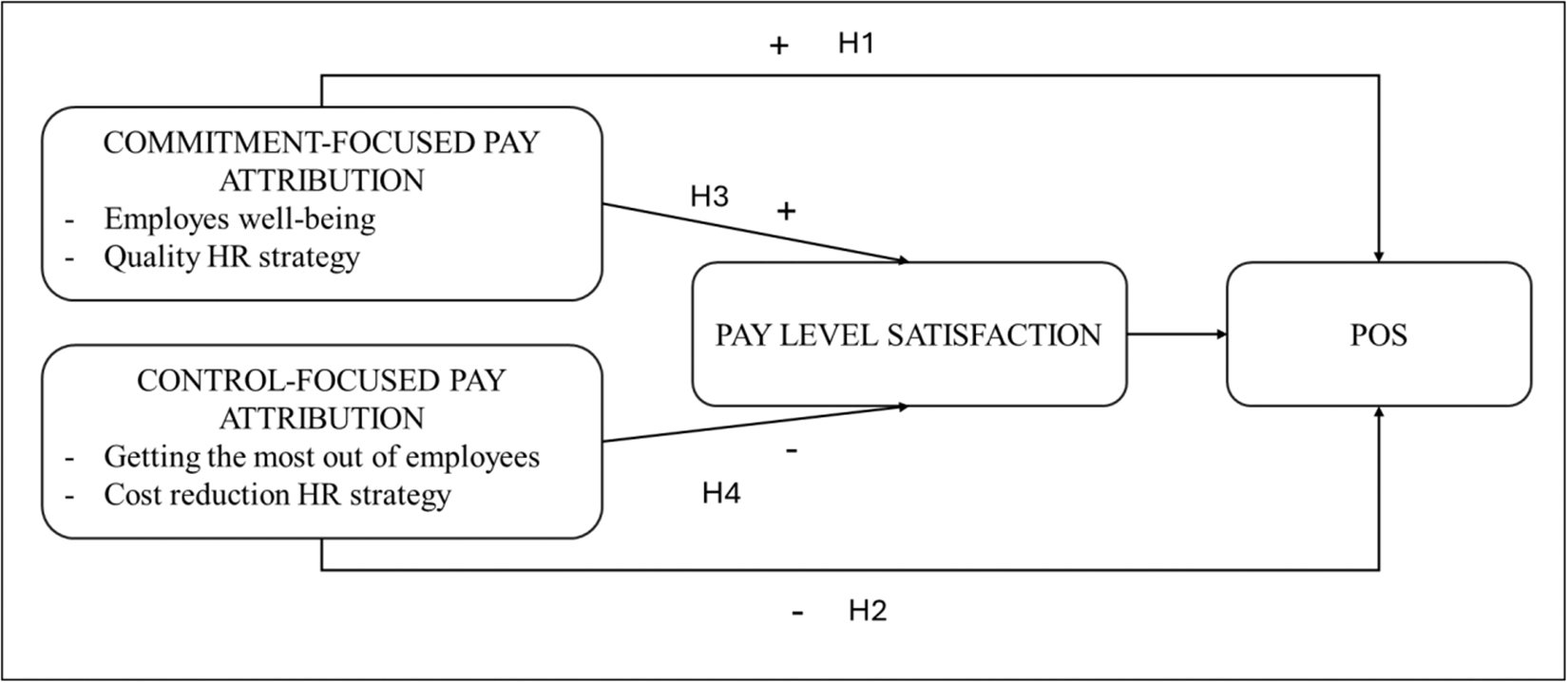

For this reason, drawing on social exchange theories, particularly the organizational support theory (Eisenberger, Huntington, Hutchison & Sowa, Reference Eisenberger, Huntington, Hutchison and Sowa1986) and the psychological contract (Rousseau, Reference Rousseau1989), we propose that internal pay attributions can directly influence employees’ perceived organizational support (POS) and indirectly affect it through employees’ pay level satisfaction.

Thus, this study contributes to the HR attribution literature by focusing on employees’ pay, a practice that has received little attention despite the importance that pay practices can have on employees’ attitudes and behavior, such as organizational commitment (e.g., Miceli & Mulvey, Reference Miceli and Mulvey2000) and job performance or turnover intention (e.g., Tekleab, Bartol & Liu, Reference Tekleab, Bartol and Liu2005).

Second, we contribute to the HR attribution theory by analyzing the mediating effect of pay level satisfaction on the relationship between internal pay attributions and employees’ POS. Understanding the mediating variables of this relationship is essential for building attribution theory.

Theoretical background and hypothesis development

Employees’ HR and pay attributions

HR process research has focused on how HR content is communicated and understood by employees (e.g., Bowen & Ostroff, Reference Bowen and Ostroff2004; Nishii et al., Reference Nishii, Lepak and Schneider2008; Nishii & Wright, Reference Nishii, Wright and Smith2008; Sanders et al., Reference Sanders, Shipton and Gomes2014; Wang et al., Reference Wang, Kim, Rafferty and Sanders2020). According to this process-based approach, employees do not respond to HR practices directly and passively; instead, they need to perceive, recognize, conceive, judge, and reason about HR practices before acting (Colakoglu, Hong & Lepak, Reference Colakoglu, Hong, Lepak, Wilkinson, Bacon, Redman and Snell2010).

In this context, attribution theories (Heider, Reference Heider1958; Kelley, Reference Kelley1973; Weiner, Reference Weiner1979) have established one of the main foundations for the emergence of core streams of HR process research. Attribution refers to the perception or inference of the cause, mainly of one’s own or others’ behavior (Kelley & Michela, Reference Kelley and Michela1980). Attribution theory suggests that attributions produce cognitive and affective reactions from individuals, thus influencing future expectations, emotions, and performance (Weiner, Reference Weiner1979).

By focusing on attributions theories, Nishii et al. (Reference Nishii, Lepak and Schneider2008: 507) define HR attributions ‘as causal explanations that employees make regarding management’s motivations for using particular HR practices’. The core idea underlying attribution theory is that employees respond attitudinally and behaviorally to HR practices based on the intentions they perceive in the actions of others (Lepak, Jiang, Han, Castellano & Hu, Reference Lepak, Jiang, Han, Castellano and Hu2012; Nishii et al., Reference Nishii, Lepak and Schneider2008; Van De Voorde & Beijer, Reference Van De Voorde and Beijer2015). In this sense, Nishii et al. (Reference Nishii, Lepak and Schneider2008) differentiate between five HR attributions: four internal ones, by which employees ascribe the design of HR practices to the intentions of the organization, and one external one, whereby they assign it to a response to situational pressures that are not under the control of managers.

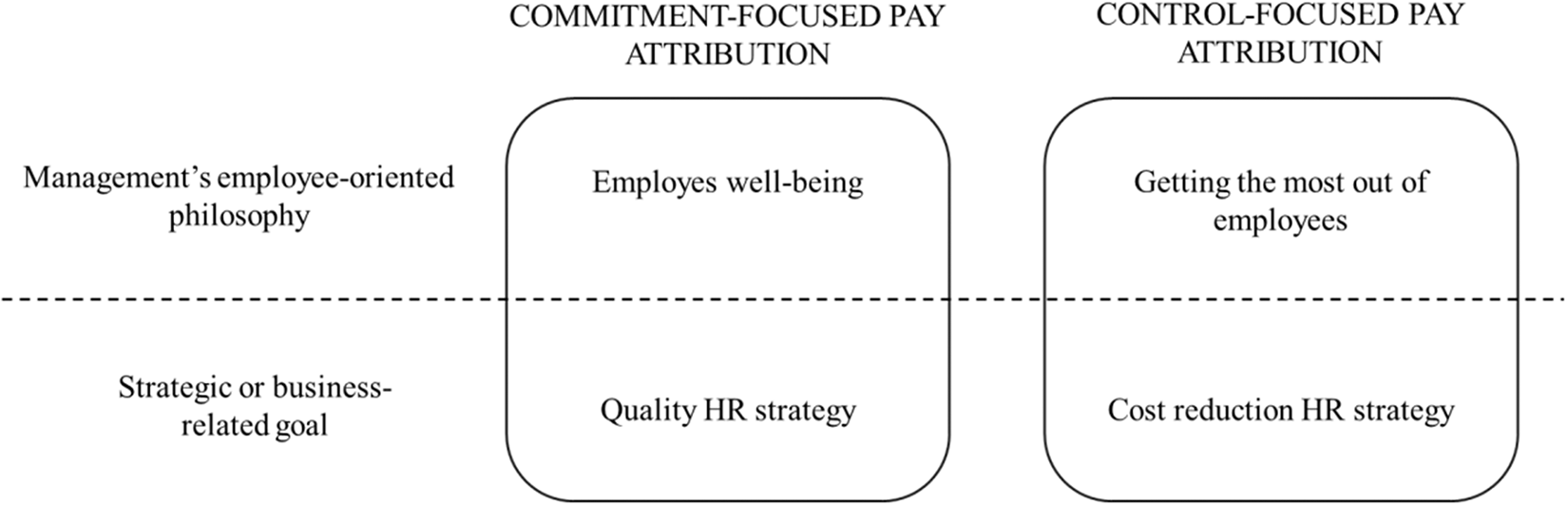

Furthermore, internal attributions are classified into two categories (Nishii et al, Reference Nishii, Lepak and Schneider2008). The first two internal attributions relate to strategic or business-related goals that can underlie HR practices. Drawing from the traditional distinction between ‘quality enhancement’ and ‘cost reduction’ strategies (e.g., Porter, Reference Porter1996; Schuler & Jackson, Reference Schuler and Jackson1987), Nishii et al. (Reference Nishii, Lepak and Schneider2008) identified two internal HR attributions reflecting these dual strategic foci: quality HR strategy and cost reduction HR strategy attributions.

The other two internal attributions are based on management’s employee-oriented philosophy (e.g., Osterman, Reference Osterman1994) and consider whether HR practices have been adopted to maximize employee well-being (i.e., employee well-being attribution) or enhance employee efficiency (i.e., getting the most out of employees’ attribution).

Attribution theory suggests that attributions produce cognitive and affective reactions from individuals, thus influencing future expectations, emotions, and performance (Weiner, Reference Weiner1979). In this sense, employee well-being HR attribution has been shown to be negatively related to external job change intention but positively related to internal job change intention (Lee, Kim, Gong, Zheng & Liu, Reference Lee, Kim, Gong, Zheng and Liu2020), associated with higher levels of commitment and lower levels of job strain (Van De Voorde & Beijer, Reference Van De Voorde and Beijer2015), and positively related to employees’ engagement (Alfes, Veld & Fürstenberg, Reference Alfes, Veld and Fürstenberg2021). On the other hand, previous studies have found that getting the most out of employees’ HR attribution is negatively related to employee engagement (Alfes et al., Reference Alfes, Veld and Fürstenberg2021) and associated with higher levels of job strain (Van De Voorde & Beijer, Reference Van De Voorde and Beijer2015). Similarly, Shantz, Arevshatian, Alfes, and Bailey (Reference Shantz, Arevshatian, Alfes and Bailey2016) found that employees increase their job involvement, which translates into lower levels of emotional exhaustion, when they perceive HR practices to enhance employees’ performance. However, they suffer from work overload when they perceive that HR practices are consequence of a cost-controlled organizational strategy, which leads to higher levels of emotional exhaustion.

These previous studies confirmed that the four internal attributions can be differentiated as positive or negative based on their implications for employees (Hu, Oh & Agolli, Reference Hu, Oh and Agolli2025). Indeed, Nishii et al. (Reference Nishii, Lepak and Schneider2008) conducted a confirmatory factor analysis, which showed that the quality HR strategy attribution (also referred to as performance attribution) and the employee well-being HR attribution loaded onto one factor, labeled ‘commitment-focused attribution’. Similarly, the ‘getting the most out of employees’ and ‘cost reduction’ HR strategy attributions loaded onto another factor, labeled ‘control-focused attribution’.

In this regard, commitment-focused attributions have been shown to induce a positive reaction from employees by reducing turnover intentions through the partially mediated effect of POS (Chen & Wang, Reference Chen and Wang2014) or job satisfaction (Tandung, Reference Tandung2016). Similarly, Fontinha, Chambel, and De Cuyper (Reference Fontinha, Chambel and De Cuyper2012) showed that IT consultants were more committed to both the outsourcing organization and hosting organization, when they attributed HR practices as commitment focused. Further, Guest, Sanders, Rodrigues, and Oliveira (Reference Guest, Sanders, Rodrigues and Oliveira2021) found positive relationships between commitment-focused attributions and engagement and the psychological contract. Finally, Katou, Budhwar, and Patel (Reference Katou, Budhwar and Patel2021) conducted a multilevel path analysis showing that commitment-focused HR attributions positively predicted organizational performance. In all these cases, negative effects were found when control-focused HR attributions are considered as the independent variable.

Despite the high importance of these studies, all of them coincide in considering a bundle of HR practices rather than an isolated practice, which does not allow for identifying differences between them. For this reason, we focus on employees’ attributions regarding a specific HR practice, namely the pay practice.

Studies analyzing employees’ pay attributions are scarce. In this sense, to our knowledge, the only study that has focused on attributions about pay is that of Montag-Smit and Smit (Reference Montag-Smit and Smit2021), which examines pay secrecy attribution and finds that employees increased their trust when they attribute benevolent causes to pay secrecy.

We define employees’ pay attributions as their perceptions of the organization’s intentions when designing pay practices. That is, pay attributions reflect employees’ perceptions of why the organization designs pay practices the way it does.

Following Nishii et al.’s (Reference Nishii, Lepak and Schneider2008) approach, we consider four internal pay attributions that can be aggregated into two categories (Figure 1). Commitment-focused pay attribution refers to employees’ perception that pay practices are driven by employers’ desire to prioritize employee well-being or to enhance the quality of their products/services. In contrast, control-focused pay attribution is linked to employees’ perception that pay practices stem from a managerial philosophy aimed at maximizing employee output or an organizational goal of reducing costs.

Internal pay attributions.

The effect of pay attributions on POS

Employees’ POS refers to the general perception of the extent to which the organization values their contributions and cares about their well-being (Eisenberger et al., Reference Eisenberger, Huntington, Hutchison and Sowa1986; Shore & Shore, Reference Shore, Shore, Cropanzano and Kacmar1995). Findings from previous studies have shown that POS can have a strong, positive effect on employees’ job satisfaction and organizational commitment (Riggle, Edmondson & Hansen, Reference Riggle, Edmondson and Hansen2009).

Regarding the antecedents of POS, prior research has highlighted the importance of factors such as fairness, leader support, and favorable HR practices (Eisenberger, Rhoades Shanock & Wen, Reference Eisenberger, Rhoades Shanock and Wen2020). In this regard, Kurtessis et al.’s (Reference Kurtessis, Eisenberger, Ford, Buffardi, Stewart and Adis2017) meta-analysis reported significant associations between POS and the perceived favorableness of various HR practices, such as developmental opportunities and family-supportive organizational policies. Similarly, job conditions oriented toward enrichment – such as autonomy or participation in decision-making – have also been shown to relate to the development of employees’ POS (Kurtessis et al., Reference Kurtessis, Eisenberger, Ford, Buffardi, Stewart and Adis2017).

These results clearly demonstrate that POS can strongly depend on employees’ attributions regarding the reasons behind the favorable or unfavorable treatment they receive from the organization (Kurtessis et al., Reference Kurtessis, Eisenberger, Ford, Buffardi, Stewart and Adis2017). According to social exchange theories, and specifically organizational support theory, when employees perceive that the organization is investing in their well-being and development, they tend to feel a sense of obligation toward the organization and reciprocate by engaging in pro-organizational affective responses (Fontinha et al., Reference Fontinha, Chambel and De Cuyper2012; Salas-Vallina, Pasamar & Donate, Reference Salas-Vallina, Pasamar and Donate2021; Van De Voorde & Beijer, Reference Van De Voorde and Beijer2015). These reciprocations are often intangible and may include trust, commitment, psychological contract fulfillment, and POS (Chen & Wang, Reference Chen and Wang2014; Colquitt, Baer, Long & Halvorsen-Ganepola, Reference Colquitt, Baer, Long and Halvorsen-Ganepola2014).

Thus, it is expected that if employees perceive that pay practices stem from the organization’s intent to enhance their well-being, as a result, employees are likely to reciprocate, which will be reflected in a more positive attitude toward the organization, thereby increasing their POS.

Further, since pay practices should be designed to support organizational strategies, there are pay practices that can be perceived as more appropriate for implementing certain strategies than others (Miles & Snow, Reference Miles and Snow1984). Drawing from the resource-based view of the firm, it is expected that when a company adopts a quality-based differentiation strategy, employees are seen as assets necessary to produce high-quality goods and services. Organizations will invest in employees’ development and try to maintain high motivation and commitment by, for example, paying attention to their well-being and providing high rewards (Schuler & Jackson, Reference Schuler and Jackson1987). Accordingly, if employees perceive that the underlying reason for determining their pay is to enhance their commitment, by adopting a quality-based HR strategy, they may feel that they are viewed as valuable assets by their employers and that they will be rewarded as they deserve.

Taking this into account, regarding the pay commitment-focused attribution, which includes both employees’ well-being and a quality HR strategy for pay attributions, we propose the following hypothesis:

Hypothesis 1: Commitment-focused pay attribution is positively related to POS.

Conversely, employees’ perceptions that HR practices are motivated by a managerial philosophy focused on getting the most out of employees, or by an HR strategy based on cost reduction, can generate negative reactions (e.g., Alfes et al., Reference Alfes, Veld and Fürstenberg2021; Van De Voorde & Beijer, Reference Van De Voorde and Beijer2015). Under these control-focused pay attributions, employees may perceive that employers are primarily concerned with efficiency, short-term performance, or cost-cutting (Nishii et al., Reference Nishii, Lepak and Schneider2008). In accordance with this business strategy, organizations can be perceived as trying to reduce costs associated with each employee by, for example, offering low salaries (Schuler & Jackson, Reference Schuler and Jackson1987). Employees may perceive themselves as replaceable resources and another cost that must be minimized by the organization (Biron, Boon, Farndale & Bamberger, Reference Biron, Boon, Farndale and Bamberger2024). They may also perceive that the organization expects them to do more for less (Kelliher & Anderson, Reference Kelliher and Anderson2010), while placing less emphasis on employee development and well-being (Nishii et al, Reference Nishii, Lepak and Schneider2008).

Hence, when employees perceive that the organization adopts pay practices aimed at maximizing performance or reducing costs, they may interpret this as a lack of support. Such negative perceptions can diminish employees’ sense of obligation toward the organization, potentially leading to adverse attitudes

This leads us to propose the following hypothesis:

Hypothesis 2: Control-focused pay attribution is negatively related to POS.

The mediating effect of pay level satisfaction

Additionally, in line with previous studies (e.g., Tandung, Reference Tandung2016), we propose that when employees attribute certain causes to HR practices, they undergo a psychological process in which their perception of the HR practice triggers their attitude toward such practices. Hence, pay attributions can influence not only how employees perceive their organization, but also how they assess the outcomes of decisions that affect them.

In this vein, models based on attribution theory, which incorporate judgments about the agent’s intentionality and morality, have shown that such judgments can influence how people assess the consequences they experience from others’ decisions. Previous studies have demonstrated that individuals tend to perceive intended harms as worse than unintended harms, even when the outcomes are identical (Ames & Fiske, Reference Ames and Fiske2013). Furthermore, Malle, Guglielmo & Monroe’s (Reference Malle, Guglielmo and Monroe2014) model proposes that when a person perceives the decision-maker as acting with good intentions – even if the result is objectively negative – they are less likely to assign blame and are more likely to evaluate the decision favorably.

For this reason, we propose that employees who perceive commitment-focused pay attributions may interpret the organization’s pay practices as being implemented with benevolent intentions (i.e., to enhance employee well-being or adopt a high-quality HR strategy). This may lead them to assess the pay they receive more positively, regardless of the actual amount, and to be more satisfied with the pay level.

Moreover, greater satisfaction with pay can lead to an employee’s perception of a positive psychological contract, as the promises and obligations implied by pay practices would have been fulfilled (Rousseau, Reference Rousseau1989). The fulfillment of the psychological contract can, in turn, lead to a positive reaction toward the organization, thus positively impacting employees’ POS (Aselage & Eisenberger, Reference Aselage and Eisenberger2003). Thus, we propose the following hypothesis:

Hypothesis 3: Commitment-focused pay attribution is positively and indirectly related to POS through pay level satisfaction.

Conversely, when employees perceive control-focused pay attributions, they may interpret the organization’s pay practices as being driven by more self-interested intentions and less focus on employees’ interests (i.e., to reduce costs or get the most out of employees). This may lead them to assess the pay they receive more negatively, regardless of the actual amount, and to be less satisfied with their pay level.

Additionally, this may be perceived as a violation of the psychological contract, as employees may feel that their contributions are not being adequately recognized or rewarded (Morrison & Robinson, Reference Morrison and Robinson1997). Moreover, this unfulfillment of the psychological contract can lead to a negative reaction toward the organization, thus negatively impacting employees’ POS (Aselage & Eisenberger, Reference Aselage and Eisenberger2003). Hence, we suggest the following hypothesis:

Hypothesis 4: Control-focused pay attribution is negatively and indirectly related to POS through pay level satisfaction.

Method

Sample

To test the hypotheses, we collected data through a structured questionnaire hosted on a website by the benefits management company Edenred. This allowed us to access a database containing information on 8,236 employees of firms operating in Spain. We focused our research exclusively on Spanish firms to avoid potential biases arising from differences in national labor regulations, which could affect firms’ pay policies and, consequently, employees’ perceptions of their compensation.

We sent an invitation to complete the questionnaire to all employees in the database. From the total, we received 1,200 responses, resulting in a response rate of 14.57%. However, our final sample consisted of 695 employees, as some responses had to be discarded due to incompleteness. Considering the sample size and assuming an infinite population (i.e., all employees of firms operating in Spain), we calculated a sampling error of 3.7% (at a 95% confidence level and assuming p = q = 50%). Most participants were male (61.4%) and Spanish (94%). They were 39.99 years old on average (SD = 8.00), with ages ranging between 21 and 63 years. Finally, they had an average of 9.93 years of experience (SD = 7.68) and a stable contract relationship with their organization (94.7%).

Measures

Perceived organizational support

POS was measured by eight items from a short version of the Survey of POS (Eisenberger, Cummings, Armeli & Lynch, Reference Eisenberger, Cummings, Armeli and Lynch1997). The scale was assessed on a 5-point Likert-type scale ranging from strongly disagree (1) to strongly agree (5). After conducting the analysis of reliability and validity, we had to drop one item (i.e., My organization would forgive an honest mistake on my part) because of a low factor loading. The final scale showed high validity and reliability (Cronbach’s alpha = 0.944; McDonald Omega = 0.935; average extracted variance = 0.708). Additionally, the goodness-of-fit indicators of the estimated model were correct (chi-square = 21.309, df = 12, p-value = .046; CFI = 0.998; TLI = 0.996; RMSEA = 0.033; SRMR = 0.011).

Pay attributions

Following Nishii et al. (Reference Nishii, Lepak and Schneider2008), we used one item to represent each of the four proposed internal HR attributions. Respondents were asked to indicate the degree to which the pay practice was designed to (1) enhance the quality of products or services, (2) reduce costs, (3) promote employee well-being, and (4) maximize employee productivity. All items were measured on a 5-point Likert-type scale ranging from completely disagree (1) to completely agree (5).

Additionally, following Nishii et al. (Reference Nishii, Lepak and Schneider2008), we grouped well-being and quality HR strategy pay attributions into a factor labeled commitment-focused pay attribution, while getting the most out of employees and cost-reduction HR strategy pay attributions were grouped into another factor labeled control-focused pay attribution. We tested the convergent and discriminant validity of these two constructs. While commitment-focused pay attribution showed a good fit, the factor loadings for control-focused pay attribution were below the recommended threshold of 0.7 and were not statistically significant. For this reason, we decided to treat the two items related to control-focused pay attributions individually in our model.

Pay level satisfaction

To measure pay level satisfaction, we used one item in which employees were asked to indicate their satisfaction with the level of pay received on a 5-point Likert-type scale, ranging from completely dissatisfied (1) to completely satisfied (5).

Control variables

To rule out the role of other variables associated with POS, two control variables were included: employees’ organizational tenure and sex. Similarly, since pay satisfaction has been shown to be related to pay comparisons – how employees compare their pay with other external and internal referents – we added two items to account for this possible effect. Specifically, we added one item considering internal pay comparison: ‘Compared with other working for this company, the pay I currently receive is…’; and another item considering external pay comparison: ‘Compared to my friends and family, the pay I currently receive is….’ Respondents used a 5-point response format ranging from ‘much less’ to ‘much more’.

Finally, we also controlled for the possibility that employees perceived pay decisions as being out of the organization’s control, and that such a perception could influence employees’ POS and pay satisfaction. Therefore, we added external pay attribution to reflect employees’ perception that their pay is a consequence of external constraints, such as legal and union requirements.

Common method bias

Although all the variables in the model are self-reported, the likelihood of common method bias affecting our study is relatively low. First, a cross-sectional design is deemed appropriate when the processes being studied have already unfolded and the situation under investigation represents the system’s final state (Spector, Reference Spector2019). In this case, as employees have been receiving their pay for a certain period, they have had enough time to develop their pay attributions, so their effect on POS and pay satisfaction is already present.

Additionally, following the recommendations of Podsakoff, MacKenzie, Lee and Podsakoff (Reference Podsakoff, MacKenzie, Lee and Podsakoff2003), several measures were adopted to reduce the potential risk of common method biases as much as possible. First, the interviewees remained anonymous and were assured that there were no good or bad answers, asking them to be as sincere and honest as possible. This approach aimed to reduce their fear of being evaluated and stop them from giving socially desirable or appropriate answers. Similarly, the construction of the items was very careful when trying to avoid any potential ambiguities. For this purpose, the questionnaire included simple and concise questions as well as definitions of the terms with which interviewees might be less familiar to facilitate their understanding.

Data analysis

We tested our hypotheses using path analysis. Specifically, the model was estimated using the Lavaan package (Rosseel, Reference Rosseel2012) in R (R Core Team, 2018). We first checked whether multivariate normality of the data could be assumed using the MVN package (Korkmaz, Goksuluk & Zararsiz, Reference Korkmaz, Goksuluk and Zararsiz2014). Our model was estimated using the MLM method because the multivariate normality hypothesis was rejected, our data lacked missing observations, and the sample size was not small (Gana & Broc, Reference Gana and Broc2019). In the Lavaan package (Rosseel, Reference Rosseel2012), this estimator is a robust version of the ML method that incorporates Satorra–Bentler chi-squared correction (Satorra & Bentler, Reference Satorra, Bentler, von Eye and Clogg1994) and is one of the recommended estimation methods in cases where the data violate normality (Gana & Broc, Reference Gana and Broc2019). This approach allowed us to test the statistical significance of the direct, indirect, and total effects of the relations tested by the proposed models.

Figure 2 displays a summary of the model and research hypotheses.

Model and hypotheses.

Results

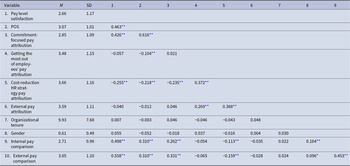

Table 1 presents the descriptive statistics and correlations between the variables involved in the analysis.

Descriptive statistics and observed variable intercorrelations

Note: M and SD are used to represent mean and standard deviation, respectively.

* p < .05, **p < .01.

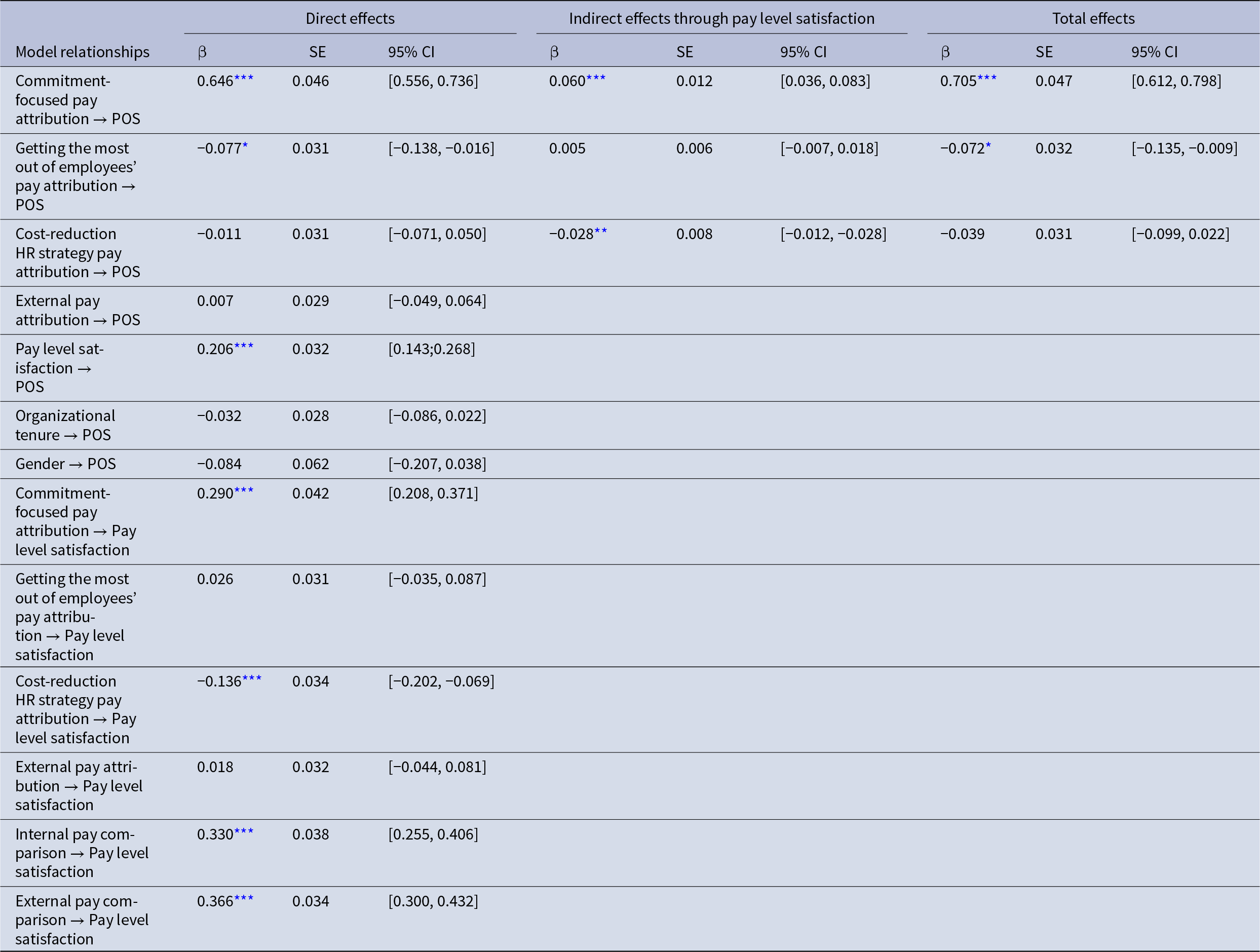

The estimated model exhibits a strong model fit, meeting the required thresholds (Hair, Tatham, Anderson & Black, Reference Hair, Tatham, Anderson and Black2010: chi-square = 275.546, df = 91, p-value = .000; CFI = 0.965; TLI = 0.956; RMSEA = 0.058).

Table 2 presents the results. First, employee commitment-focused pay attribution has a positive and significant relationship with POS (β = 0.646, p < .001), thus supporting Hypothesis 1. Further, regarding employee control-focused pay attributions, while getting the most out of employees’ pay attribution has a direct negative and significant relationship with POS (β = −0.077, p < .05), cost reduction HR strategy pay attribution does not have a statically significant relationship with POS, which implies that Hypothesis 2 is partially supported.

Main model results

* p < .05, **p < .01, ***p < .001.

Additionally, we test whether pay attributions also have an indirect effect on POS through pay level satisfaction. Our results showed that employee commitment-focused pay attribution has an indirect effect on POS by increasing pay level satisfaction (β = 0.290, p < .001). This implies that Hypothesis 3 is supported. On the other hand, when considering employee control-focused pay attributions, the results show that although getting the most out of employees’ pay attribution does not have an indirect effect on POS, cost reduction HR strategy pay attribution has an indirect relationship with POS through pay level satisfaction (β = −0.028, p < .01). Consequently, Hypothesis 4 is partially supported.

Regarding control variables, as can be expected, external pay attribution has no effect on either POS or pay level satisfaction, thus indicating that although employees could perceive that legal and union requirements can influence organizational pay decisions, they know that this influence only affects the minimum salary, and consequently, the organization remains in much control to decide the final pay of their employees.

Similarly, both internal and external pay comparisons are positively related to pay level satisfaction. That is, when employees perceive their pay as being higher than the pay of other coworkers in the same organization or other workers in different organizations, they are more satisfied with their pay.

Discussion

This study aimed to advance our understanding of the effect of pay attributions on POS. To do so, we developed and tested a model to demonstrate how certain internal pay attributions can not only have different effects on employees’ POS but also exert an indirect effect by influencing pay level satisfaction. Specifically, our hypotheses regarding commitment-focused pay attributions are supported, as this type of attribution has both direct and indirect positive effects on POS. However, the hypotheses related to control-focused pay attributions are only partially supported. While getting the most out of employees’ pay attribution has only a direct and negative effect on POS, the cost-reduction HR strategy pay attribution has only an indirect and negative effect on POS through pay level satisfaction.

Theoretical contributions

Our study confirms attribution theory (e.g., Nishii et al, Reference Nishii, Lepak and Schneider2008) by showing that commitment-focused pay attribution has a positive influence on POS, while those that could be classified as control-focused pay attributions have a negative influence on POS. The findings contribute to organizational support theory by showing that employees’ perceptions of why pay decisions are made also play a crucial role in shaping their POS.

Further, the results of our empirical analysis contribute to previous research on HR attributions by examining the pathway through which pay attributions influence employees’ POS. In this context, certain pay attributions have been shown to influence how employees assess the pay they receive, thereby positively or negatively contributing to the perceived fulfillment of the psychological contract and the subsequent perception of the organization’s support. This result contributes to the literature on HR attributions by introducing the idea addressed in more advanced attribution models (e.g., Malle et al., Reference Malle, Guglielmo and Monroe2014), which consider that the morality of the agent’s intentions can influence how the outcomes received are judged. In this sense, when employees perceive the intention behind pay practices as benevolent – i.e., taking employee commitment into account – they tend to be more satisfied with their pay level, regardless of the actual amount they receive. However, when they perceive that the motives behind pay practices are more focused exclusively on organizational interests, specifically cost-cutting, this can lead to greater dissatisfaction with their pay level. This finding can also align with studies that, drawing on organizational justice, have suggested that the perception of appropriate interpersonal treatment may be even more critical than the objective ‘input-outcome’ ratio when employees assess the fairness of the outcome received (Bies, Reference Bies, Cummings and Staw1987). Previous research has confirmed this suggestion by showing how employees’ perceptions of the treatment they receive from their organization influence how they perceive the outcomes received (Al Afari & Elanain, Reference Al Afari and Elanain2014).

On the other hand, contrary to our expectations, although both control-focused pay attributions had a negative influence on POS, getting the most out of employees’ pay attribution has only a negative direct influence, while the cost-reduction HR strategy pay attribution has only an indirect effect through pay level satisfaction. These results suggest that pay attributions can follow different patterns in influencing POS, and they can be explained by considering the cognitive and emotional processes that occur when employees develop pay attributions.

These results suggest that while some pay attributions are better at predicting outcome-referenced variables (i.e., pay level satisfaction), others may have more direct predictive power on organizational-referenced variables (i.e., POS). This is consistent with the two-factor model, which proposes that different organizational justice dimensions can be more predictive of different types of outcomes (Folger & Konovsky, Reference Folger and Konovsky1989). For example, distributive justice has been shown to better predict outcome-referenced dependent variables (i.e., pay satisfaction), while procedural justice is better at predicting system-referenced dependent variables (i.e., organizational commitment) (Sweeney & McFarlin, Reference Sweeney and McFarlin1993). Similarly, in the context of appraising performance, employees’ perceptions of distributive justice have been shown to be significantly more related to individual-referenced outcomes/personal evaluations, specifically rating satisfaction (Taneja, Srivastava & Ravichandran, Reference Taneja, Srivastava and Ravichandran2024).

In the case of pay attributions, our results suggest that employees consider to what extent the intention can have a direct influence on the received outcome. In this sense, a cost-cutting HR strategy can have a clear direct influence on employees’ pay levels, as salary is another cost that organizations want to control under this strategy. However, it is not as clear that getting the most out of employees’ attribution should have a negative impact on employees’ pay levels, and an organization may even adopt a higher salary to enhance employee performance. For this reason, employees perceiving getting the most out of employees’ pay attribution may negatively assess the organization, because they perceive that the organization has more self-interested intentions, but this may not be reflected in a lower salary, thus having no effect on pay level satisfaction.

Therefore, these results contribute also to attribution theory by showing that, although the aggregation of attributions into two dimensions may be valid for analyzing the direction of their effects on employee perceptions, in some cases, if we want to analyze the pathway through which control-focused pay attributions produce such effects, it is necessary to consider them individually.

Practical implications

The findings of this study highlight that employees’ perceptions of their pay – specifically, the reasons they attribute to it – significantly influence their POS. Therefore, to foster a positive POS, it is imperative for organizations to proactively communicate the rationale behind their compensation decisions. This ensures that employees’ perceptions align with the actual intentions of the organization. Transparent communication about the factors considered in determining pay can help mitigate misattributions and promote a sense of fairness. Implementing regular, open dialogues between management and employees about compensation decisions, what Guest (Reference Guest2017) refers to as voice, and emphasizing the organization’s commitment to employee well-being and overall success, can help achieve this goal.

Additionally, the results of this study can suggest that the effectiveness of pay practice is contingent on employees’ attributions. Organizations should recognize that employees’ satisfaction with their pay is influenced not only by the actual pay level, but also by their perception of the underlying motives for setting that pay. Our study indicates that employees’ attributions regarding pay can significantly impact their satisfaction with their pay level. Specifically, attributions linked to employee commitment positively influence pay satisfaction, whereas those associated with cost-reduction strategies have a negative effect. So, managers should strive to ensure that pay decisions are seen as reflecting a genuine commitment to employee well-being. For this purpose, it would be useful to conduct regular surveys or feedback sessions to gauge employees’ perceptions and feelings about their compensation and use this information to refine pay strategies and communicate the organization’s commitment to their well-being.

Finally, the results reveal that when employees perceive pay as a cost-cutting measure, it can lead to dissatisfaction with actual pay levels. In order to mitigate these negative attributions for cost reduction, it is important to explain the rationale behind such decisions and, if possible, explore alternative strategies that minimize the negative impact on employees’ perceptions. Also, when cost-saving measures are necessary, it would also be worth considering involving employees in the decision-making process and explaining the broader organizational context to foster a sense of transparency and trust.

In conclusion, the study’s findings underscore the critical role of employee pay attributions in shaping their perceptions of pay and organizational support. By actively managing these attributions through transparent communication, aligning pay practices with organizational values, and prioritizing employee well-being, organizations can enhance employee satisfaction, commitment, and overall performance, thereby fostering the development of a positive employment relationship.

Limitations and future research directions

Despite the theoretical and practical contributions, it is necessary to be cautious about them and to recognize and address some of the limitations of this study.First, future studies could build on the present research by analyzing whether pay attributions evolve over time and whether changes in POS and pay satisfaction influence these variations.

Second, in this study, we consider that employees can simultaneously develop multiple pay attributions, just as previous studies on HR attributions have considered (e.g., Alfes et al., Reference Alfes, Veld and Fürstenberg2021). However, future studies could consider whether some individual and/or organizational factors can moderate the effect of such pay attributions and make some pay attributions more important than others under certain circumstances.

Related to this, in this study, we only consider the consequences of pay attributions. Future research, in line with previous research on HR attributions (e.g., Alfes et al., Reference Alfes, Veld and Fürstenberg2021; Beijer, Van De Voorde & Tims, Reference Beijer, Van De Voorde and Tims2019; Montag-Smit & Smit, Reference Montag-Smit and Smit2021), could develop this model by analyzing organizational or individual factors that can be antecedents of employees’ pay attributions.

Third, we measured each of the pay attributions using the single-item measures developed by Nishii et al. (Reference Nishii, Lepak and Schneider2008). Although single-item scales can maximize simplicity and readability, and may validly capture a clear impression of a group of workers at a particular point in time (Spector, Reference Spector2019), future studies could develop more comprehensive measurement scales for HR attributions in general, and for pay attributions in particular, in order to obtain a more detailed and specific assessment of these employee attributions.

Fourth, we added two items to control for the effect of both internal and external pay comparisons on pay level satisfaction. Although these items allow us to account for the influence of perceived equity on pay level satisfaction, using other measures that more specifically identify the respondents’ referents in the comparison could not only better control for this effect but also extend the results of this study by analyzing whether specific types of pay comparisons influence the development of pay attributions. For example, the perception that employees are being overpaid compared to employees of other firms in the same industry could influence the development of commitment-focused pay attributions.

Conclusion

The findings reported in this research suggest that the organizational reasons employees attribute to their pay influence their POS. Specifically, whereas commitment-focused pay attributions are positively related to POS, control-focused are negatively related to POS. Furthermore, commitment-focused pay attribution and one specific control-focused pay attribution (i.e., cost-reduction HR strategy pay attribution) influence POS through the mediation of pay level satisfaction. These insights are useful for organizations and academics to the extent that they show how employees’ perceptions of the reasons underlying their pay can not only influence how employees assess their relationship with the organization, but also how they assess their payment. Studying the interaction between pay attribution and POS provides valuable information for organizations seeking to strengthen employee commitment and engagement.

Acknowledgements

We thank Edenred SA for its support in the realization of this research. The authors want to thank the members of the research group, ‘Innovation, Sustainability and Business Development’ (SEJ-481), for their help and comments.

Funding statement

This work was supported by the Consejería de Economía, Innovación, Ciencia y Empleo, Junta de Andalucía, under grant number A-SEJ-268-UGR23; Ministerio de Ciencia e Innovación (España), under grant number TED2021-129829B-100; and funding for language editing: Research Grant Programme of Faculty of Economics and Business (UGR). Funding for open access charge is Universidad de Granada / CBUA.

Conflicts of interest

The authors report there are no competing interests to declare.

Dr. José M. de la Torre-Ruiz is an associate professor in the Management Department at the University of Granada (Spain). He is a full member of the research group Innovation, Sustainability, and Development (ISDE). His primary research interests are human resource management and organizational behavior. He is the author of multiple works in prestigious academic journals such as Business Strategy and the Environment, International Journal of Human Resources Management, Management Decision, Personnel Review, and International Journal of Manpower, among others.

Dr. Eulogio Cordón-Pozo is a professor in the Management Department at the University of Granada (Spain). He holds a PhD in management from the University of Granada. His current research interests include innovation in specific business areas and human resource management. His works have been published in several high-impact journals, such as Management Decision, Industrial Marketing Management, Human Resource Management, International Journal of Human Resource Management, and the International Journal of Technology Management, among others.

Dr. M. Dolores Vidal-Salazar is an associate professor in the Management Department at the University of Granada (Spain). Her research interests include the relationship between several human resource management practices (i.e., personnel training and development, compensation) and firm as well as employees’ performance. Her works have been published in several high-impact journals, such as Human Resource Management, International Journal of Human Resource Management, and Human Relations. She has a broad practical background with several Spanish regional chambers of commerce.

Maria F. Muñoz-Doyague is an associate professor in Human Resource Management and Organizational Behavior at the University of Leon (Spain). She holds a doctorate in Economics and Business Science, and her research interests and publications cover areas of knowledge management and the human resource practices to enhance creativity and innovation in organizations. Also, it includes social networks in organizational settings and their effects on organizational, group, and individual outcome variables. Recently, she has opened up a new research line which aims to link the latter aspects with organizational citizenship behaviors, psychological capital, and well-being, among others.

Open access

Open access