6.1 Introduction

This chapter concerns a specific type of knowledge resource, namely common sense. I will explore what types of knowledge, skills, and perspectives make up what is known as common sense and examine what might constitute a common-sense commons in the context of corporate governance. I will then focus on the apparently intuitive notion that shareholders own corporations, which is deeply embedded in public discourse, as an example of an idea that looks like common sense yet is by no means a matter of legal consensus. Using this example, and aided by concepts drawn from pragma-linguistics, I will show how common sense can be shaped to promote ideological precepts, in this case the ideology of shareholder primacy.

6.2 What Is Common Sense?

In a lecture in Edinburgh in 1965, the British philosopher Gilbert Ryle (1965, 3–4) related a conversation on a train with Bertrand Russell: “He said ‘Locke was the spokesman of Common Sense.’ Almost without thinking I retorted impatiently ‘I think Locke invented Common Sense.’ To which Russell rejoined ‘By God, Ryle, I believe you are right. No one ever had Common Sense before John Locke – and no one but Englishmen have ever had it since.’”

I do not have the space here for a comprehensive history of the concept of common sense. Nevertheless, it is safe to assert that, with the greatest respect to Bertrand Russell, common sense over the ages has by no means been the sole preserve of Englishmen (nor English women, for that matter). The first known reference to common sense came from Aristotle (Reference Aristotle2012), who wrote in De Animus of a common sense through which we combine the information received from the five senses to perceive phenomena such as motion. Such phenomena involve the use of more than one of our senses, and without this common sense we would not be able to perceive them.

Our modern understanding of common sense dates back to Descartes, who wrote in Discourse on the Method about le bon sens, which “is, of all things among men, the most equally distributed” (Descartes 1912, 3). While the cognitive aspect of common sense concerns “such obvious truisms as not to be worth stating,” as Moore (Reference Moore and Muirhead1925, 1) put it, early on ideas of common sense combined the cognitive dimension with the social. Drawing on Vico’s (1990) thinking, Gadamer (2013, 19–20) stressed this point in his discussion of what he called sensus communis:

The main thing for our purposes is that here sensus communis obviously does not mean only that general faculty in all men but the sense that founds community. According to Vico, what gives the human will its direction is not the abstract universality of reason but the concrete universality represented by the community of a group, people, a nation, or the whole human race.

Bergson (2002, 346) was even more emphatic about the social element:

Our senses thus serve us, above all, to orient us in space; they are not turned towards science, but towards life. But we do not only live in a material milieu, but also in a social milieu. … It is thus indeed a sense in its own way; but while the other senses place us in relation to things, good sense presides over our relations with persons.

In a not-too-different vein, in an article describing a method for distinguishing thought process of machines and humans, Erion (Reference Erion2001, 33) explained that common sense concerns “the realm of familiar objects that we become acquainted with during ordinary experience.” In this manner, common sense encompasses the knowledge, beliefs, and capabilities that allow us to “survive and thrive during our everyday lives” (Erion Reference Erion2001, 33). Frischmann (Reference Frischmann, Decker and Kuchář2021), who cites Erion, seems to endorse this approach to defining and characterizing common sense, while also incorporating the social aspect. Common sense is essential for coping with everyday life, addressing common problems, and managing social systems. It is, therefore, an important component of knowledge that Strandburg et al. (2017, 10) characterize as “a broad set of intellectual and cultural resources.”

A yet broader approach, echoing the work of Bourdieu, would view common sense as a product of social conditions and practices that are internalized by individuals through what he termed habitus (Bourdieu Reference Bourdieu1977). Such a view of common sense includes its role in creating and upholding social conventions, that is, practices and actions that are commonly regarded as acceptable or desirable (Choi Reference Choi, Decker and Kuchář2021). A broad approach to common sense also encompasses its role in shaping discourse and makes a link between common sense and persuasion. Van Dijk (Reference van Dijk1998) has formulated a clear explanation of common sense that weaves together its cognitive and social aspects. Common sense consists of knowledge, beliefs, and opinions that are taken for granted in a society and therefore tend to be “presupposed” in discourse; it also applies to argumentation strategies as in “a common sense” argument, which is based on commonly shared premises; finally, it has a dimension which is “immediate, unreflected and untheoretical” (Van Dijk Reference van Dijk1998, 104). Common sense is, then, “an implicit, naïve ‘theory’ of the world” (Van Dijk Reference van Dijk1998, 104), which can be more or less right or wrong, and includes habits of thought and persuasion, as well as knowledge and skills.

Common sense thus conceived dovetails with the notion of a common cultural ground. As Van Dijk (Reference van Dijk1998, 105) summarizes:

Common sense is then more or less what we try to conceptualize with the term “cultural beliefs,” that is, the knowledge and opinions, as well as the evaluative criteria, that are common to all or most members of a culture. Like common sense, these cultural beliefs are also used as the basis for specific group beliefs, and also function as the general base of presupposed beliefs in all accounts, explanations and arguments.

Common sense includes what we, as a group, know (or think we know), along with all that we need for discourse to take place within a given social system.

Having explained common sense in terms of belief, knowledge, and skills, as well as the building blocks of discourse, I will now develop the idea of a common-sense commons. Before we examine the nature of what we might consider the common-sense commons related to corporate governance, we need to mark out the contours of the social system relevant for the study of corporate governance and this is what I will attempt to do in the next section.

6.3 The Field of Corporate Control

We can describe the social system of interest for corporate governance with the help of Ostrom’s Institutional Analysis and Development (IAD) framework (Ostrom Reference Ostrom1990, 2005, 2011) if we consider the corporation itself as a shared resource. Deakin (Reference Deakin2012) has set out the legal case for considering the corporation as a shared resource that is governed as a commons, grounding his argument in the commons literature. The action situations of concern are those relating to the governance and control of the corporation as a shared resource. They would include, for example, meetings of corporate boards; meetings of board committees (e.g. on the determination of executive compensation); annual general meetings; discussions on shareholder resolutions; reporting, disclosure, and compliance (e.g. production of financial and non-financial statements); other forms of communication between directors and managers; preparations for board meetings; and analyst conference calls. They would also include all forms of deliberation concerning potential mergers and acquisitions, as well as some communications with stakeholder groups besides voting shareholders. We can think of these as a nested system of interconnected action situations (Ostrom Reference Ostrom2011; McGinnis Reference McGinnis2020) and the set of all the actors as a community.

A useful analytical tool for conceptualizing such a social system, or community, is provided by the theory of strategic action fields (SAF) outlined by Fligstein and McAdam (Reference Fligstein and McAdam2012).Footnote 1 An SAF is “a meso-level social order where actors (who can be individual or collective) interact with knowledge of one another under a set of common understandings about the purpose of the field, the relationships in the field (including who has power and why), and the field’s rules” (Fligstein and McAdam Reference Fligstein and McAdam2011, 3). An SAF may be, for instance, a division within a firm, consisting of individual employees and their managers. It could also be the firm itself, comprising separate divisions. Or it could be the whole market, with different firms cooperating or competing against each other for business. Thus, fields may be contained within ever larger fields.Footnote 2 As a result, a society may have an unlimited number of SAFs, which may also overlap.

The theory of SAFs is helpful for our analysis in two ways. First, Fligstein and McAdam provide a clear method for determining whether a field exists, describing it, and, most importantly, setting its boundaries. For them, “field membership consists of those groups who routinely take each other into account in their actions” (Fligstein and McAdam Reference Fligstein and McAdam2012, 167). This sets a manageable boundary for our community, excluding those groups that are not routinely involved in deliberations regarding corporate control. The SAF related to corporate governance, then, comprises all the actors directly involved in the interconnected network of action situations in which matters of corporate control are resolved. This would include primarily corporate managers, directors, and shareholders (and their representatives).Footnote 3

Parties not included in the SAF, so defined, but who are nevertheless involved include institutions (and individuals) that set standards and guide the work of boards and shareholder meetings, such as the Business Roundtable (BRT) in the United States, but also auditors, accounting standard setters, or proxy advisors. State structures, such as regulators, courts, and legislative bodies are also relevant, as are opinion formers and decision-makers, such as lawyers, academics, and the media. A narrower definition of the SAF does not preclude analysis of the influence of external actors. Fligstein and McAdam (Reference Fligstein and McAdam2012) make clear that this would be a serious omission. They also emphasize the importance of examining the influence of state actors, such as the Securities and Exchange Commission (SEC), that are outside the SAF but nevertheless often play a key role.

Strategic field theory is useful for a second reason, namely that it provides a helpful analytical tool for studying social change within a community. Action situations change when the positions of and relationships between the various actors are transformed, resulting in the emergence of a new status quo. Fligstein and McAdam (Reference Fligstein and McAdam2012) distinguish three types of actors in an SAF: incumbents, challengers, and governance units. Incumbents are those actors who hold power within the SAF and whose views are dominant. Challengers are those who are in a subsidiary position vis-à-vis the incumbents. Despite the designation, “challengers’” may accept their role and position, and are not necessarily in an adversarial relationship towards incumbents. Governance units are responsible for maintaining the rules within the SAF. This chapter looks primarily at incumbents and challengers.

Fligstein (Reference Fligstein2016) has described the field relating to corporate governance and refers to it “the market for corporate control,”Footnote 4 understood in a broad sense. I consider the use of the term “market” to describe this field as problematic for two reasons. First, the strategic action field concerns corporate control in a wider sense than the sale and purchase of shares in mergers and acquisitions transactions. This SAF also concerns the processes through which managers are held to account and the balance of power within corporations is maintained or changed. This includes the structure and functioning of boards, as well as the determination of who sits on boards. These aspects of the determination of control do not involve transactions where assets are exchanged, but encompass a broader range of social interactions than those necessarily associated with markets. When thinking about proxy contests as one means of establishing corporate control (Manne Reference Manne1965), even if we use of term “market” in a metaphorical sense, there is a risk of unnecessary confusion.Footnote 5

Secondly, even in the narrower domain of corporate mergers and acquisitions, the field entails a broader array of actors and institutions than simply the buying and selling of shares in market transactions. The process of takeovers is subject to a complex set of regulations in any developed market and involves an often-baffling range of issues and processes. To talk of a market for corporate control may imply a somewhat simpler perception of corporate mergers and acquisitions, and a greater level of transparency, than the often-messy reality merits. Moreover, we run the risk of exacerbating misconceptions about the link between shareholding and actual control. For this additional reason, I feel it would be preferable to use another term than “market.” I prefer to think of the SAF as the “field of corporate control.”

6.4 Common Sense and the Field of Corporate Control

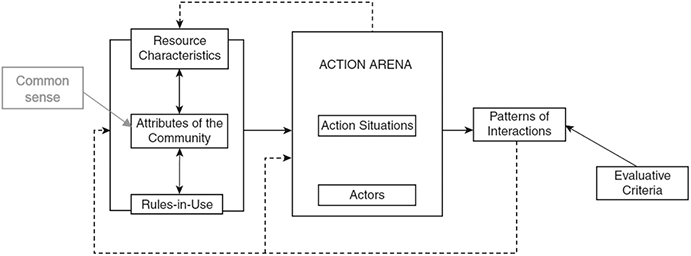

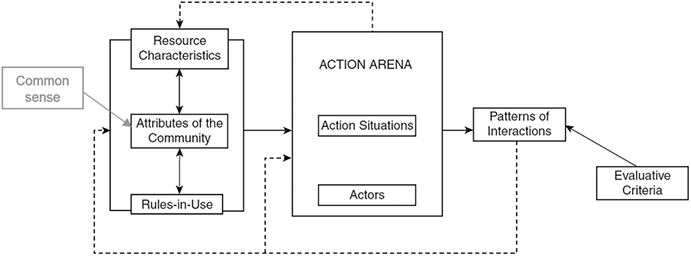

The common sense of a community is that set of common understandings, perspectives, and assumptions that are shared by all its members. Common sense is therefore part of the attributes of the community, contributing, as it does, to its “shared understanding” (Ostrom Reference Ostrom1986). As already explained with reference to the work of Van Dijk (Reference van Dijk1998), it also forms part of the cultural repertoire of the community (McGinnis Reference McGinnis2020).Footnote 6 In an institutional analysis of corporate governance (with the corporation as the shared resource) relying on the governing knowledge commons (GKC) framework (Frischmann et al. Reference Frischmann, Madison and Strandburg2014), the place of common sense is indicated in Figure 6.1.

Common sense in the GKC framework.

Common sense enables both the field and the individuals within it to function. In the field of corporate control, it provides a set of background assumptions that enables discourse to take place, which either maintains stability in the field or drives a process of transformation. This holds for interactions pertaining to the composition and structure of boards, the recruitment of directors, the balance of power within governance systems, the setting of agendas for board meetings or shareholder meetings, the determination of performance metrics, and so on.

The key role of common sense in a social system or field suggests that, besides being part of the attributes of the community, common sense is itself a resource. Since it is a shared resource freely available to all within a social system, such that we can speak of a common-sense commons, the GKC framework appears to be an appropriate analytical tool. Frischmann (Reference Frischmann, Decker and Kuchář2021, 113) characterizes a common-sense commons as a “critical social infrastructure that shapes and enables various social systems.” Action situations in the common-sense commons of corporate control are “adjacent,” to borrow McGinnis’s (Reference McGinnis2020) expression, to those of the field of corporate control.

In my doctoral dissertation (Ali Reference Ali2024), I analysed the discourse of corporate governance in the United States during the 1980s and 1990s. In particular, I selected two genres for examination: speeches on corporate governance made by commissioners of the SEC over the period, and large samples of articles from the Wall Street Journal and New York Times. My analysis revealed how the discourse on corporations and their governance evolved during the period; importantly, the underlying assumptions and presuppositions behind the discourse changed. In other words, the common-sense commons of corporate control underwent a change. My research involved a detailed look at outputs of some of the action situations in the common-sense commons. The drafting of an SEC commissioner’s speech was one such action situation involving the commissioner, their immediate staff, and possibly other SEC employees. The delivery and reporting of the speech to a public audience was another related action situation. The researching, writing, and editing of a newspaper article by a reporter was yet another. Moreover, the work of bodies such as BRT, which regularly publish and publicize statements on corporate governance, constituted a further nested set of action situations.

Common sense as a type of knowledge resource makes for a complex subject of analysis. A framework for analysing knowledge commons has been provided by Ostrom and Hess (Reference Ostrom, Hess, Hess and Ostrom2007) and developed further by the GKC research program (Frischmann et al. Reference Frischmann, Madison and Strandburg2014; Strandburg et al. Reference Strandburg, Frischmann, Madison, Strandburg, Frischmann and Madison2017; Sanfilippo et al. Reference Sanfilippo, Frischmann and Standburg2018). Special attention should be paid to the exogenous variables: material characteristics, the attributes of the community, and the rules-in-use. The material characteristics of a common-sense commons include the means of the dissemination of ideas. Changes brought by developments in technology and communication are of special importance.

A study of a common-sense commons would be concerned with not only the contents and nature of the knowledge but also with the rules-in-use that govern it. Unlike other forms of knowledge commons, it is not subject to clear and formal rules. Nevertheless, that is not to say that it is not subject to any rules. What constitutes common sense is determined – and changed – over time.

An important aspect of the rules-in-use relates to the selection of individuals and institutions – including journalists, academics, public officials, analysts, consultants, and business leaders – that are the most important in defining and refining what constitutes common sense. The views of some key actors enter the media – what Hall et al. (Reference Hall, Critcher, Jefferson, Clarke and Roberts1978) term “primary definers.” Some “experts” – and some opinions – are frequently quoted in prominent media and these are the actors who play an important role in defining mainstream opinion. Meanwhile other views are largely ignored. An important task of an analyst of the rules-in-use of the common sense of the field of corporate control is to identify the action situations in which the primary definers are chosen, and to examine whether there are any unspoken rules or criteria for such choices. This will include not only studying actions related to how journalists and editors select sources to quote but also understanding the media operations of influential organizations and the role of media ownership and control. The rules-in-use of the field of corporate control are closely related to the attributes of the community.

The GKC framework can be used to analyse changing as well as static situations. I will return briefly to questions about the governance of common-sense commons in the concluding section of this chapter. In the next section, I will examine how common sense can be made to include notions that are actually ideological in character. I will then present a case study of how an apparently common-sense notion served to support a transformation in the field of corporate control.

6.5 Common Sense and Ideology

As Frischmann (Reference Frischmann, Decker and Kuchář2021, 125) points out, common sense can be “biased and wrong.” Common-sense assumptions can be misguided and even manipulative. Additionally, there are problems of scale and scope; simplifications and heuristics that may serve as reasonable approximations in one context may be misleading when applied elsewhere. This is a pertinent risk when heuristics that are effective in micro situations are extended to the macro context (Redekop Reference Redekop2009; Frischmann Reference Frischmann, Decker and Kuchář2021).

Discourse analysts, such as Fairclough (Reference Fairclough2015), have explained that common sense can serve as a highly effective tool for promulgating ideologies. Ideology has been defined concisely by Reisigl and Wodak (Reference Reisigl, Wodak, Wodak and Meyer2016, 26) as “a perspective (often one-sided), i.e. a world view and a system composed of related mental representations, convictions, opinions, attitudes, values and evaluations.” It is also important to note that ideologies are “open to normative critique” (Fairclough Reference Fairclough2015, 32). By far the most common conceptualization of ideology as used in Critical Discourse Studies draws inspiration from Gramsci’s (Reference Gramsci1971) concept of hegemony, according to which ideologies serve to reinforce social and power relations, and are at their most effective when disguised and presented as common sense. This allows readers or listeners to be convinced of the necessity of the actions being supported without full deliberation. As Fairclough (Reference Fairclough2015, 108) explains:

Ideology is most effective when its workings are least visible. If one becomes aware that a particular aspect of common sense is sustaining power inequalities at one’s own expense, it ceases to be common sense. … And invisibility is achieved when ideologies are brought to discourse not as explicit elements of the text, but as background assumptions which on the one hand lead the text producer to “textualize” the world in a particular way, and on the other hand leads the interpreter to interpret the text in a particular way. … The more mechanical the functioning of an ideological assumption in the construction of coherent interpretations, the less likely it is to become a focus of conscious awareness, and hence the more secure its ideological status.

As Bourdieu and Wacquant (Reference Bourdieu and Wacquant1992, 250) point out, ideology results in habits of thought which are often hard to overcome, even among scholars.

This explanation of what is meant by ideology and common sense is very much a traditional one used in the field of discourse analysis. But there is an alternative understanding of ideology that is superior in its explanatory power. This theory, developed by Van Dijk (Reference van Dijk1998), is based on social psychology, and takes greater account of the cognitive dimension of discourse (Forchtner Reference Forchtner, Flowerdew and Richardson2018). Van Dijk (Reference van Dijk1998, 8) characterizes ideology as “the basis of the social representations shared by members of a group.” This is not the same as a world view, as it encompasses the set of ideas upon which a world view is formed. Ideology does not equate to common sense; an ideology is shared among groups within the culture, whereas common sense pertains to the whole culture. However, an ideology may over time become – or cease to be – part of common sense.

In this conceptualization, the term ideology does not necessarily have the negative connotations of its use in the Marxist tradition. While ideologies may support power relations and inequality, they may also be emancipatory, in the sense of opposing power and its abuse, or indeed not involve power at all. One individual may be part of different groups sharing different ideologies. For instance, a person may work in the corporate sector and subscribe to the basic competitive profit-seeking ideology of modern business; they might at the same time be part of a religious group sharing a very different set of beliefs regarding charity. In any case, it should be clear that an ideology may change over time; it need not be static.

Van Dijk argues that ideology and common sense can be connected through the process of legitimation, that is, by providing a justification or motivation for actions that may be subject to criticism and challenge (or potential challenge). Of particular interest is the legitimation of action that is taken (or advocated) in an institutional context; legitimation may be provided by individuals as well as official bodies such as organizations, boards, or assemblies. As van Dijk explains (Reference van Dijk1998, 256): “legitimating discourses presuppose norms and values. They implicitly or explicitly state that some course of action, decision or policy is ‘just’ within the given legal or political system, or more broadly within the prevalent moral order of society.” Ideology that encompasses a call for the adoption of a particular set of policies, especially when this entails a break from the past, will be more appealing if accompanied by legitimation that is effective. In summary, presenting claims that are founded on particular ideological assumptions as uncontroversial common sense can represent a powerful legitimation strategy. Effectively, this serves the purpose of “blocking one’s rational device” (Saussure Reference Saussure, de Saussure and Schulz2005, 128). Presenting or effectively disguising an idea as common sense blocks the normal critical faculties that would lead one to examine the validity of the idea.Footnote 7

6.6 The Ideology of Shareholder Value

For at least the period from the end of the Second World War to the late 1970s, the field of corporate control, dominated as it was by managers, was stable. In the framework of strategic field theory, during this era of what Chandler (Reference Chandler1962) termed “managerial capitalism,” managers were the incumbents and the prevailing view of corporate purpose was that the business corporation existed to serve broader social goals, beyond earning financial profits. The dominant view on the purpose of the corporation during the era of managerial capitalism was neatly summarized by the BRT in a statement on corporate responsibility in October 1981. The statement approvingly cited Reginald Jones, who had just completed his term as chairman and chief executive of General Electric (and had been chairman of the BRT until 1980): “Public policy and social issues are no longer adjuncts to business planning and management. They are in the mainstream of it. … Management must be measured for performance in noneconomic and economic areas alike” (The Business Roundtable 1981, 1).

However, the 1980s and 1990s saw a transformation in the field of corporate control. Fligstein (Reference Fligstein2016) cites the high inflation and economic stagnation of the 1970s as external shocks which set in motion the change that was to empower a set of challengers to incumbent corporate managers. Cheffins (Reference Cheffins2019) refers to numerous corporate scandals, a general decline in public confidence in managers to deliver economic prosperity, and increased competition from Japanese firms. Moreover, some external constraints on management, in the form of union power, regulation, and limited access to lending capital, were losing their saliency. As a result, the stability of the field was undermined, and new actors gained the ascendancy. Fligstein (Reference Fligstein2016), Heilbron et al. (Reference Heilbron, Verheul and Quak2014), and Cheffins (Reference Cheffins2021) stress the important role played by so-called corporate raiders, who were relative outsiders in this transformation. Fligstein (Reference Fligstein2016) also describes the many in the financial community as challengers. The credo of the newly empowered actors was “shareholder value maximization” (or “shareholder value” for short), the idea summed up by Friedman (Reference 127Friedman1962, Reference Friedman1970) that corporate managers were obliged to place the interest of shareholders above all other concerns.

Some scholars of corporate governance (Lazonick and O’Sullivan Reference Lazonick and O’Sullivan2000; Stout Reference Stout2012) have referred to shareholder value as an ideology. I believe it is reasonable and methodologically sound to treat it as an ideology. It certainly fits the description of a set of representations shared by a group. The argument made by adherents of shareholder value draws on a number of apparently common-sense assumptions and pre-suppositions, one of the most important of which being the premise that share owners jointly own the corporation.

6.7 Shareholders as Owners of Corporations

The common sense of corporate governance tends to include the pre-supposition that corporations, including actively traded listed companies, are owned by their shareholders. Friedman (Reference Friedman1970) predicated his argument for shareholder primacy on ownership in his famous New York Times Magazine article:

A corporate executive is an employee of the owners of the business. He has direct responsibility to his employers. That responsibility is to conduct the business in accordance with their desires, which generally will be to make as much money as possible while conforming to the basic rules of the society, both those embodied in law and those embodied in ethical custom.

This is reflected in the BRT’s position towards the end of the 1990s, which clearly links shareholder primacy with ownership (The Business Roundtable 1997, 1): “The Business Roundtable wishes to emphasize that the principal objective of a business enterprise is to generate economic returns to its owners. … The Business Roundtable believes that good corporate governance practices provide an important framework for a timely response by a corporation’s board of directors to situations that may directly affect stockholder value.”

At the turn of the millennium Arthur Levitt, President Clinton’s SEC chairman, summed up his view on corporate governance even more succinctly: “This system works brilliantly, provided those in control operate for the sole benefit of the true owners of public companies – the shareholders” (Levitt Reference Levitt2000).

None of these three statements are accompanied by any sort of discussion of ownership and corporations. That shareholders own the corporation is stated but not explained. Friedman, the BRT, and Levitt all simply use ownership as a starting point. It is presented as self-evident and as such is not debatable. In other words, that shareholders own corporations is introduced as common sense. This is to be found throughout the discourse on corporate governance and was especially notable during the rise of the shareholder value norm. Ownership is used as a legitimation strategy, to “shut down the argument” on the place of shareholders in the purpose of the business corporation.

Yet this notion, though frequently unchallenged in public discourse, does not align with specialist knowledge. Common sense is not necessarily the same thing as specialist (or scientific) knowledge, which may be restricted to people with specific educational and professional backgrounds and training. That said, to the extent that specialist knowledge has passed into the sphere of what is taken for granted among the population at large, there is an overlap with common sense. For example, the assertion that the Earth is round has been accepted as part of common sense (with the exception of a small but colourful minority), as has the heliocentric view of the solar system. Similarly, that smoking is an unhealthy habit has also been widely accepted. On the other hand, a significant part of the population and perhaps an even larger part of the political class in many countries have not as yet caught up with the dominant scientific view that climate change is a real phenomenon caused by humans.

While it is a prevalent assumption in management texts and media discourse that shareholders own corporations, it is certainly not an established view among legal scholars. I will explore this legal question of ownership and corporations in the next section.

6.8 The Corporation as a Legal Person

The separate legal personhood of the corporation is key to the argument that they cannot have owners. The meaning of this concept of legal personality is complex but is succinctly summarized in Worthington’s (Reference Worthington2016, 34) company law casebook: “We typically use the word ‘person’ to refer to an individual human being but in law the word has a more technical meaning: ‘a subject of rights and duties.’ In this sense it is possible to speak of a corporation as ‘a person’ and recognize its separate personality.”

The characterization of a corporation as a legal person is not intended to suggest human qualities or agency but to denote legal status. As Gindis (Reference Gindis2016, 508) explains: “when the law treats the firm as a ‘person’ nothing more than the fact that the firm has (not is) a point of imputation for rights and duties that arise in legal relations should be implied.” The separate legal personality of the corporation has a number of important practical consequences.

One of the most important consequences of the corporation’s legal personality is its ability to own assets. Besides having no claim to any of the assets nor a proportionate share, shareholders have no kind of equitable ownership interest of any kind relating to a corporation’s assets (except in insolvency). Therefore, the property of a corporation is totally separate from that of its members or shareholders. This would be true even if there was only one shareholder holding 100 per cent of the equity.

By enabling the separation of the assets of the company from the assets of the shareholders, separate legal personality facilitates limited liability. Limited liability is enabled – though not legally required – for incorporated companies. (Again, this is unrelated to the level of dispersal of the equity holding, applying equally to companies with one shareholder.) Hansmann and Kraakman (Reference Hansmann and Kraakman2000), Hansmann, Kraakman and Squire (Reference Hansmann, Kraakman and Squire2006), and Kraakman et al. (Reference Kraakman, Armour and Davies2017) have shown that this is a two-way relationship, in the sense that assets of the company are also protected against the liabilities of the shareholders, and that the protection of the assets of the company is more significant in terms of enabling the corporation to create value. Shareholders also cannot unilaterally withdraw their equity contribution and cannot force partial liquidation. This is an important practical arrangement that lowers the cost of capital.

A corporation can enter into contracts and can bring cases to court in its own name. Furthermore, the company runs its own business, regardless of the dispersion of the control rights attached to equity holdings: “The fact that one person holds all, or substantially all, of the shares in a company does not, without more, make the company’s business that person’s business in the eyes of the law” (Worthington Reference Worthington2016, 47).

Finally, a corporation’s existence is not subject to any time limits, since its duration is not constrained by the lifespan of any individual or group of individuals. As Bainbridge (Reference Bainbridge2015, 5) explains, the corporation’s “indefinite legal existence” is terminable only in the following circumstances: a voluntary dissolution, a merger, bankruptcy followed by liquidation or dissolution by a court.

There is a widespread view among legal scholars based on the separate legal personality of the corporation that it is an entity which cannot be owned. According to Davies (Reference Davies2010, 61), it is the “modern view that shareholders do not own the company, but only their shares.” Indeed, “the old argument that shareholders have these rights because they are the owners of the company now carries little sway, because its premise is false: shareholders own their shares, not the company” (Davies Reference Davies2010, 266). Dignam (Reference Dignam2011, 256) is even more explicit in linking the conclusion that a corporation cannot be owned to the separation between the assets of the company and its shareholders, which results from the former’s separate legal personality: “It is important to immediately cease to describe shareholders as ‘owners’ of the company as this is incorrect. Shareholders own their shares and the rights attached to them – nothing else. … The company owns its own assets and the shareholders have no legal or equitable interest in the corporate assets.”

In the UK, the clear judgment setting out the position of shareholders was made in Short v Treasury Commissioners,Footnote 8 in which the court ruled that the shareholders “were not part owners of the undertaking” (cited in Davies & Worthington Reference Worthington2016). This position was also underlined by the American Bar Association (Reference Association2009, 5) in a report of its Section of Business Law Corporate Governance Committee on Delineation of Governance Role and Responsibilities:

Shareholders are often referred to as the “owners” of the corporation. However, the corporation is a legal person in its own right rather than a mere asset. Once the separation of equity rights and control occurs in the formation of the corporate entity, the analogy of shareholders to “owners” of the corporate ”asset” is imperfect at best. The asset that shareholders own is the stock that represents their investment interest.

The habitual use of the terms “owner” and “ownership” distorts the debate on corporate governance and the role of the corporation in modern society. As Blair (Reference Blair1995, 16) pointed out, the word “ownership” has highly persuasive emotional connotations: “the problem with calling shareholders the owners of corporations is that the word ‘owner’ has such a powerful, almost moralistic meaning in U.S. culture,” such that “its use in this context cuts off debate by implying that certain rights and prerogatives should, by the very nature of things, flow to shareholders.”Footnote 9 The emotional power of ownership strengthens its use as rhetorical tool. In addition, as Veldman and Willmott (Reference Veldman and Willmott2020) and Johnston (Reference Johnston2024) have pointed out, the notion that shareholders own corporations in debates on corporate governance can play a performative role.Footnote 10

Friedman (Reference 127Friedman1962, 135) articulated an extremely influential argument for shareholder supremacy using the premise that shareholders are owners as a starting point: “the corporation is an instrument of the stockholders who own it.” He did not feel the need to argue the case for ownership but was able to take it for granted that his readers also saw shareholders as owners of businesses. As a method of persuasion, the power of the idea of ownership, especially for ideological goals of promoting the interests of shareholders above all others, is compelling. This raises the question of why and how this notion that shareholders own corporations has proved to be so convincing. This is the question that I will explore in the next section.

6.9 Ownership and “Loose Talk”

The concept of ownership as applied to businesses appears intuitive for at least two reasons. Firstly, seeing firms as having owners may serve as a useful mental shortcut in the case of small entrepreneurial companies, where one individual (or a small group of people) is tied to the enterprise in multiple ways and where the bond has a very personal dimension. It is then a short (and hidden) but flawed step to extend this line of thought to all corporations. Secondly, the historical evolution of the corporate form means that shareholders might indeed have been justifiably regarded as owners in the relatively recent past. Before we explore these reasons in deeper detail, it would be helpful to better understand what is actually going on in linguistic terms when we talk about ownership in the context of the business corporation.

It is perhaps tempting to consider talk of ownership of corporations as metaphorical in nature. Ali (Reference Ali2015) suggested that referring to corporations as being owned might fall into the category of an ontological metaphor, following the Kövecses’s (Reference Kövecses2010, 38) recommendation to “assign a basic status in terms of objects, substances, and the like to many of our experiences.” The categorization here rests on what Honoré (Reference Honoré and Guest1961, 147) described as the “paradigm … of a single human being owning, in the full liberal sense, a single material thing.” Referring to a corporation as being owned would amount to (metaphorically) applying a concept more obviously suited to ordinary material objects – items in one’s personal ownership – to relationships of an abstract nature.

However, this view fails to take into account the complex nature of legal ownership. Fully owning a single material object is just the most obvious and clearly understood instance of ownership, but there is a wide range of types of things that can be owned in varying degrees of complexity. Honoré (Reference Honoré and Guest1961) outlines eleven “incidents” or aspects of ownership, stressing that there is no one single determining feature, and that it is not the case that all eleven incidents need be present for a relationship to constitute ownership. By contrast, authors such as Penner (Reference Penner1996, Reference Penner1997), Smith (Reference Smith2011, Reference Smith2012), and Merrill (Reference Merrill1998) argue that there are some attributes or subsets of attributes of ownership that are decisive in determining whether ownership exists or not. For these authors, exclusion is the deciding characteristic of ownership. This is an important debate, but this still leaves us with forms of legal ownership that are more complex and abstract than a single material object fully owned by an individual. To characterize all forms of legal ownership besides the “full liberal” variety as metaphorical would stretch the concept of metaphor rather too far.

So how should we classify the habit of characterizing shareholders as owners of corporations? For our purposes, Sperber and Wilson (Reference Sperber and Wilson1986, Reference Sperber, Wilson, W. Gibbs and E. Wellbery2008) provide a helpful account of the continuum between literal statements and looser expressions. Metaphors are only one part of this continuum, despite their importance and prevalence in language. And even seemingly literal statements can have different meanings (or implications) in different contexts. In order to understand the meaning of statements, literal or non-literal, context is key, as is implicature, namely the meaning that is contained in a statement though not fully stated (Grice Reference Grice, Cole and Morgan1975). Sperber and Wilson (Reference Sperber, Wilson and B. Bender1990, 145) propose the following principles of relevance:

(a) Everything else being equal, the greater the cognitive effect achieved by the processing of a given piece of information, the greater its relevance for the individual who processes it.

(b) Everything else being equal, the greater the effort involved in the processing of a given piece of information, the smaller its relevance for the individual who processes it.

We claim that humans automatically aim at maximal relevance, that is, maximal cognitive effect for minimal processing effort.

In this scheme, characterizing shareholders as owners of a corporation falls under the category of loose talk (Sperber and Wilson Reference Sperber and Wilson1986). Loose talk occurs when a speaker utters a statement that is not strictly correct but serves as an approximation or verbal shortcut. Much of the time, loose talk has clear meaning under the principles of relevance outlined here. If, for example, one were to say “Mary got lost in Pittsburgh and was walking around in a circle,” it would be clear that the implication was not that Mary’s route formed a geometrically perfect circle. What is meant (the implicature) is that Mary arrived at the point at which she started her walk. Arriving at this conclusion would satisfy the goal of arriving at the maximum cognitive result for the minimum input. Indeed, a more literal statement, describing Mary’s exact path around Pittsburgh, would require a greater than necessary time and effort both for the speaker and the hearer. In this specific context, the loose meaning of “circle” has served a useful purpose in simplifying communication. However, this loose meaning is not necessarily useful in other situations. A loose meaning of the word “circle” would be problematic in a geometry textbook!

The key problem of the loose talk involved in characterizing shareholders as owners is that of scale. In the small entrepreneurial firm, this characterization may indeed work as a reasonable approximation. Consider a very small business, such as a restaurant, where one person owns 100 per cent of the equity of the business, has provided some of their personal property as collateral for the start-up loan that enabled the establishment of the business, is the manager, a worker, and is responsible for ensuring that health and safety laws and regulations are adhered to (so if, for instance, a customer were to be injured on the premises, this person could be held liable in tort). This person shares so many of the features (Honoré’s incidents) of ownership besides owning the equity of the firm that it seems reasonable to label them as the “owner” of the business. None of this is to deny the legal personality of an incorporated company or to suggest that the ownership relationship is necessarily correct in a strict literal legal sense. (A term such as “founder” might be more accurate.) The point is that in such a situation, a reference to an “owner” outside a courtroom or classroom conveys a meaning about the relationship between the owner and the business which is shared by speaker and hearer alike. As loose talk, it serves a useful purpose, avoiding the effort of more complicated formulations, and is not manipulative in intent. This is something that we can consider as common-sense shorthand.

However, if we scale up this loose talk, and look at shareholders of large corporations, which are listed on stock exchanges, the looseness looks less reasonable. In many countries, shareholding is widely dispersed, and shareholders have little influence on management, no responsibilities, and no financial liability beyond their initial investment. Loosely terming one key individual the owner of a small entrepreneurial firm does not transfer well to the case of the large listed company, besides conveying a false sense of intimacy. This common-sense shorthand does not scale well.

The confusion is compounded by the problem of carrying the looseness of everyday conversation into formal academic discourse. In contexts where precision in language use and in defining concepts is important for clarity, loose talk can serve to cause obfuscation, akin to using less than precise definitions of a circle in geometry textbooks. This is what I claim has been achieved in discussions of corporate governance that are predicated on viewing shareholders as owners of corporations. It is probable that the looseness of the application of the concept of ownership in the corporate context has its roots in the historical development of the legal personality of the firm. Legal personality as an institution was not created in a single event but evolved into its present form over a long period of time. Davies and Worthington (Reference Worthington2016, 29) comment on the relatively recent history of the full application of the legal personality of the corporation: “corporate personality became an attribute of the normal joint stock company only at a comparatively late stage in its development, and it was not until Salomon v Salomon at the end of the nineteenth century that its implications were fully grasped even by the courts.” In other words, it took some time before even courts and judges fully understood the meaning and impact of separate legal personality, and made judgments and established precedents which realized the full potential of this concept. Until these precedents were established, many of the attributes of ownership would have fallen on shareholders.

Ireland (Reference Ireland1999, 43) explains that the emergence of large corporations with limited liability and shares traded in liquid markets brought on the modern concept of separate corporate personality, accompanied by the idea that shareholders own shares as opposed to the company:

In underlining the externality of the shareholder, these economic and legal changes laid the foundations for the emergence of the modern doctrine of separate corporate personality. The “complete separation” of company and members that this entailed was not, as company lawyers tend to assume, inherent in the legal act of incorporation. Rather, the legal meaning of incorporation in a business context was reinterpreted in the latter half of the nineteenth century to accommodate the radical economic separation of joint stock companies from their shareholders.

So conceptualizing shareholders as owners might have been a reasonably accurate representation in the past, when the relationship between the corporation and those who held equity positions was very different. Over time, as laws and their interpretations evolved, a new reality took shape; however, through force of habit, shareholders are still commonly thought of as owners. What might have been a correct part of common sense has long ceased to be an accurate representation of the actual legal position of corporate shareholders.

6.10 Concluding Comments: A Research Agenda on Common-Sense Commons and Corporate Governance

This chapter has examined the concepts of common sense and the common-sense commons in the context of the business corporation and its governance. I have considered the role that common sense might play in the strategic action field related to corporate control. While common sense is an essential part of the knowledge infrastructure of a social system, in important ways it can also lead to confusion, manipulation, and a misconception of key relationships. What is generally recognized as common sense may not always be identical to scientifically accepted knowledge. In this chapter, I considered a key idea in the discourse of corporate control, namely that shareholders own corporations. This example, at the centre of recent and contemporary debates on corporate purpose and governances, is widely accepted as received common sense. Indeed, it presents an ideal subject of study, as an idea that seems intuitive, is rooted in everyday experience, has enormous persuasive force, and underpins a dominant ideology – but is nevertheless far from being an established truth in the academic discourse.

A research agenda to further our understanding of how the common-sense commons of the field of corporate control came into existence, and who determines its contents and how, requires the input of several disciplines and methodological approaches. This is why it is important to combine insights from the GKC framework with the strategic field approach of Fligstein and McAdam. The rules-in-use for a common-sense commons will present special challenges. The resource of common-sense is subject to non-rivalry and is not tangible. It does not require allocation mechanisms, but is widely disseminated, or shared, within the community. The sharing of common sense does not require regulating access to it or controlling its use. Neither does a common-sense commons involve proprietary rights like intellectual property. Nevertheless, the creation and dissemination of common sense is also not altogether spontaneous; the common-sense commons is not a free-for-all in which all actors have unlimited potential to influence what is accepted as presupposed knowledge by all or most of the given social system. In other words, informal governance through unwritten rules-in-use plays an important role in determining what is shared, subject to informal rules which determine how common sense is “produced, curated, sustained, and disseminated in social systems” (Frischmann Reference Frischmann, Decker and Kuchář2021, 123).

A key task would be to identify which individuals and institutions are the primary definers, in the sense that they are the most important in defining and refining what constitutes common sense. Bibliometric analysis would contribute to understanding the spread of academic ideas but would need to be combined with media analysis to better understand how ideas from academia filter into public discourse. Ethnographic and anthropological methods, including conducting interviews with key participants, would also be an essential part of any investigation to understand the processes by which a common-sense commons is governed. The rise of the shareholder value ideology might serve as an ideal case study of the evolution of common sense and the underlying power structures.

Open access

Open access