Introduction

The fusion of financial services and digital technology has given rise to transformative socio-technical dynamics, where finance becomes increasingly embedded in everyday life through technological infrastructures. The prominent ‘financialisation’ hypothesis not only refers to the emergence of a new, finance-based economy (Fligstein, Reference Fligstein1990; Krippner, Reference Krippner2011). It also addresses how finance is increasingly embedded in the everyday practices of ordinary savers and investors (Martin, Reference Martin2002; Langley, Reference Langley2008; Davis, Reference Davis2009). This latter process reflects the widespread incorporation of households into global finance and their embracing of a new financial risk culture (Fligstein and Goldstein, Reference Fligstein and Goldstein2015; Ailon, Reference Ailon2021). But as financial transactions migrate onto platforms (Westermeier, Reference Westermeier2020), the financialisation of everyday life increasingly takes place in the interaction of small investors with digital technologies, such as trading apps or social media platforms.

Against this backdrop, more people develop the skills and dispositions of investors, thereby becoming more disposed to see themselves as investors and their economic resources as assets they can leverage to get ahead. This ‘financialisation of the self’ is related to the emergence of new subjectivities and new concepts of identity. Financialisation thus appears as a phenomenon taking place beyond status and class, as research on young passive investors or the followers of finfluencers suggests (Hayes and Ben-Shmuel, Reference Hayes and Ben-Shmuel2024; de Jong McKenzie, Reference De Jong McKenzie2025). For some, the financialisation of everyday life means taking advantage of professional advice from financial experts, while others come together in formally organised investment clubs. Some follow the recommendations from self-help guides, rely on AI generated financial decisions provided by financial intermediaries, or follow the advice and forecasts of ‘financial gurus’ on social media. Others join decentralised ‘hypercommunities’ (Kozinets, Reference Kozinets2002) and form their own ‘crowd trading’ digital subcultures in which they collectively develop, negotiate, and enact their own financial expectations, decisions, and subjectivities. This decoupling of socially structured fixed classes and socially universal orientations for action means that emerging milieus (and subcultures) translate imperatives of financialisation in different ways.

Extant research on retail investors (also known as small investors, amateur investors or lay investors) addresses the relevance of professional financial advice (Lai, Reference Lai2016), investment clubs (Harrington, Reference Harrington2008; Preda, Reference Preda2017), moral beliefs (Peifer, Reference Peifer2012), trading apps (Lai and Langley, Reference Lai and Langley2024), robo-advisors (Hayes, Reference Hayes2021) or influencers on social media (Hayes and Ben-Shmuel, Reference Hayes and Ben-Shmuel2024) for the translation of a financial market orientation into the practices and knowledge repertoires of ordinary people. However, with only a few exceptions, we know little about how retail investor subjectivities are constituted, negotiated, and practised in the context of social media. How are financial subjectivities constructed in online communities of retail investors? In which ways do community members understand themselves in relation to financial realities and investment matters? How do social media platforms contribute to the suffusion of finance into daily life? In what ways do online investing communities on social media platforms challenge dominant repertoires of financial knowledge and authority?

This article examines how digital platforms have harnessed the power of digital technology to disrupt traditional financial structures, drive financial inclusion, and facilitate the emergence of sociocultural variations of the financialisation of everyday life. Following the case of the 2021 GameStop (GME) frenzy through to its smaller rerun in June 2024, our analysis of meme culture in the sub-forum r/WallStreetBets (WSB) within the social media platform Reddit explores how the fusion of finance and digital culture enables new forms of financial engagement and impacts the shaping of financial subjectivities.

In mainstream commentary, the GME phenomenon is typically described in terms of herd behaviour. Journalists tend to speak of this herding either in the form of a so-called ‘pump-and-dump’ scheme or a ‘short squeeze’. In the first case, communication in online communities on social media platforms is said to have triggered behavioural cascades as retail investors pumped up the stock price (e.g., CNBC, 2021; CNN, 2021). In the latter, it is claimed that a crowd of decentralised retail investors self-organised on social media and engaged in predatory trading by betting against those short selling GME stock (New York Times, 2021). Economic research supports each of these interpretations. Some studies conclude that the GME stock was subject to a decentralised short squeeze that exploited the short positions of institutional investors (Lyócsa et al., Reference Lyócsa, Baumöhl and Výrost2022; Long et al., Reference Long, Lucey, Xie and Yarovaya2023), while others suggest that the GME incident was an instance of speculative-predatory trading by a group of young male retail investors with a high-risk appetite (Hasso et al., Reference Hasso, Müller, Pelster and Warkulat2022). In all of the above, profit-seeking is taken to be the ultimate motivation for investing in GME stocks. Yet GME’s prolonged elevated trading levels, even after 2021, remain difficult to reconcile with either a classic ‘short squeeze’ or a one-time ‘pump-and-dump’ scenario.

Social science research instead views the GME phenomenon as a novel form of digital activism in financial times, where identity work, affect, and platform design co-produce economic action. Gregersen and Ørmen (Reference Gregersen and Ørmen2025) show how an ‘idioculture’ of memes, jargon, and in-group rituals mobilised participants and politicised personal finance. They address WSB’s idioculture as a binding mechanism that turned retail trading into a quasi-collective project of politicising finance. Similarly, Kozinets and Seraj-Aksit (Reference Kozinets and Seraj-Aksit2024), interpret the GME phenomenon as a form of ‘everyday activism’, wherein memes, humour, and irony functioned as tools of political mobilisation. Others characterise the movement in a variety of ways, from symbolic-political struggle to disconnected activism and reactionary cultural politics (Haiven et al., Reference Haiven, Kingmsith and Komporozos-Athanasiou2022; Di Muzio, Reference Di Muzio, Chohan and Van Kerckhoven2023; Paliewicz, Reference Paliewicz2023; Vaughan et al., Reference Vaughan, Gruber and Langer2025). But the broader suggestion in the literature is that the politics of GME are complex and ambivalent. Samman and Sgambati (Reference Samman and Sgambati2023), for example, speak of ‘financial class warfare’ but conceptualise the phenomenon through the lens of what they call the libidinal economy of leverage. From this perspective, the enthusiasm around GME indicates how speculative desire intertwines financialisation with affective investment, illustrating how markets are as much about belief, desire, and fantasy as they are about rational calculation.

Rather than conceptually narrowing down the phenomenon to its political implications (in some cases bypassing the perspectives of field participants), we instead place it in a broader context of the financialisation of everyday life and the merger of digital technology with finance. Not only did the GME incident trigger a new wave of mass participation in financial activities; it also supported a normalisation of retail financial culture and a novel form of political activism, at least in parts. Our analysis of the WSB meme culture during the GME incident demonstrates how retail investors created a new collective ‘investor subjectivity’ (Langley, Reference Langley2008) via a Manichean market conception. We show how retail investors coped with the problem of fundamental uncertainty in financial decision-making by belief in a ‘charismatic’ idea and collectively shared ‘fictional expectations’ about future gains (Weber, Reference Weber1978; Beckert, Reference Beckert2016). This idea was transported and stabilised by meme posts. Our analysis reveals how the digital subculture associated financial investment with an ‘experience seeking orientation’ (Schulze, Reference Schulze, Sundbo and Sørensen2013; Schneickert et al., Reference Schneickert, Hess and Delhey2024) which diverges from conventional standards of prudent and rational economic behaviour. This orientation is performed as an ironic exaggeration of discourses on financial risk-taking and is embedded in emotions and subcultural specific value structures. Lastly, we present a methodological extension, since we make use of longitudinal data (2021 GME incident, 2024 GME rerun, and tracking evolving community culture), combining sociology of knowledge discourse analysis (external framing in media and scientific field) with immersive ethnographic semantics (internal meaning-making on WSB) and giving stronger attention to emic meaning-making.

Retail investors and digital life

The diagnosis made by existing discussions of the financialisation of everyday life is that individual subjectivity, practices, and knowledge repertoires are increasingly intertwined with financial structures and logics. Extant research mostly addresses how a cultural shift towards risk-taking and the adoption of new modes of self-management has shaped the formation of financial subjects, and how institutional change in state responsibilities has impacted the financial horizons of ordinary people (see Mader et al., Reference Mader, Mertens and van der Zwan2020). Less focus has fallen on the role played by digital technologies provided by intermediaries, which have increased the resonance of finance in everyday life. This is surprising, since sociological accounts highlight the relevance of digital technologies for social life (Castells, Reference Castells2009; Mau, Reference Mau2019; Brubaker, Reference Brubaker2023) while retail investors have already been empowered by digital technologies for years. Technology products and services have for decades transformed trading and investment – from dematerialised settlement, through to online stockbroker accounts, portfolio analytics, direct market access, retail derivatives, and algorithmic retail trading. The platformisation of financial markets erodes boundaries between Wall Street and Main Street (Westermeier, Reference Westermeier2020), not only facilitating mass participation in retail investing via mobile apps and web interfaces, but also creating new dynamics and temporalities of participation through the emergence of social-media-style trading technologies. Whilst typical face-to-face investment clubs in the late 1990s met every month for about two hours to decide which stocks to hold, buy, or sell (Harrington, Reference Harrington2008), and internet groups for retail trading meet at least once a month (Preda, Reference Preda2017), low-barrier, informal online investing communities – operating on social media platforms like Reddit, X (formerly Twitter), Discord, and TikTok – differ radically from these older forms because they combine speed and impermanence and are thus far more decentralised, loose, and flexible.

While a great deal of literature is attentive to the function of technology in financial markets, this literature mostly comes from the social studies of finance and focuses on high finance. Such studies examine the technological fabrication of global finance by studying professionals (traders or analysts) in hedge funds or investment banks, trading rooms, or high-frequency trading firms (see e.g., Beunza and Stark, Reference Beunza and Stark2004; Knorr Cetina and Brügger, Reference Knorr Cetina and Brügger2002). In the context of lay finance, issues surrounding digital technologies are addressed in research on robo-advisors (Hayes, Reference Hayes2021), trading apps (Lai and Langley, Reference Lai and Langley2024; Chua, Reference Chua2025), financial influencers on social media (Hayes and Ben-Shmuel, Reference Hayes and Ben-Shmuel2024), retail investor mobilisation enabled by new digital market-expanding technologies (Hansen, Reference Hansen2022; Gregersen and Ørmen, Reference Gregersen and Ørmen2025; Gendron et al., Reference Gendron, Madelaine, Paugam and Stolowy2025; Vaughan et al., Reference Vaughan, Gruber and Langer2025; Welbers, Reference Welbers2018), and ‘noise traders’ in electronic markets (Preda, Reference Preda2017) as well as the emergence of a new homo speculans in the digital world (Komporozos-Athanasiou, Reference Komporozos-Athanasiou2022). This research shows how technology and digital intermediaries are both an expression and driver of the financialisation of everyday life.

In the following section, we use the GME incident and the social interaction during the incident in the WSB subreddit to showcase how financial subjectivity and alternative epistemologies are created, stabilised, and performed by actors making use of digital technology. Thereby, our analysis offers a broader cultural sociology of finance in digital spaces.

The GameStop meme stock and the WallStreetBets digital subculture

In early 2021, the struggling American video game retailer GameStop (GME) became the epicentre of an unprecedented financial phenomenon, fuelled by the Reddit community WallStreetBets (WSB). The company’s share price, which had hovered around $5 throughout most of 2020, began to climb rapidly in January 2021, an ascent that defied conventional market logic. Before the surge, GME’s daily trading volume averaged under 10 million shares, reflecting its status as a declining brick-and-mortar company with minimal investor interest. That changed drastically in January 2021. The rally gained momentum with GME reaching $15.50 on 7 January and $39.36 by 22 January, accompanied by a trading volume of approximately 197 million shares – nearly 20 times its usual average. A significant turning point occurred on 26 January, when Elon Musk tweeted the word ‘Gamestonk!!’ along with a link to the WSB subreddit. By 27 January, the share price had peaked at an astonishing $347.51 (with an intraday high of $483), and trading volume reached around 93 million shares. This volatility triggered increasing concern among brokerage platforms and regulators. On 28 January, several trading apps – including Robinhood – temporarily restricted purchases of GME and other so-called ‘meme stocks’, citing clearinghouse collateral requirements. These limitations were met with fierce backlash and accusations of market manipulation, fuelling even greater media attention and public scrutiny. On that day, the stock closed at $193.60, with a trading volume of 58 million shares. By way of comparison, the S&P 500 index closed January 2021 down 1.3%, while the MSCI World index closed down 12.3%. By 1 February, GME’s price had dropped to $225.00, with a trading volume of approximately 37 million shares. The following day, 2 February, saw a significant decline to $90.00, accompanied by a volume of about 78 million shares. On 3 February, the stock closed at $92.41 with a volume of around 42 million shares. The downward trend continued 4 February, closing at $53.50 with approximately 62 million shares traded. By 5 February, GME closed at $63.77, with a trading volume of about 81 million shares.

This was not the end of the episode’s cultural and regulatory impact, however. In response to the market turmoil, the US House Committee on Financial Services held a hearing on 18 February 2021, titled ‘Game Stopped? Who Wins and Loses When Short Sellers, Social Media, and Retail Investors Collide’. A second hearing followed in March. Meanwhile, the US Securities and Exchange Commission (SEC) released an official report on 18 October 2021. While it found no evidence of market manipulation or criminal activity, the report acknowledged that social-media-driven trading had exposed significant weaknesses in market infrastructure and oversight. As the report notes, ‘it was the positive sentiment, not the buying-to-cover, that sustained the weeks-long price appreciation of GameStop stock’ (SEC, 2021).

Another spike in GME trading activity emerged in May 2024 when Keith Gill, an instrumental player in the initial frenzy, returned to the social media platform X after a nearly three-year hiatus. On 12 May, Gill – also known as ‘u/DeepFuckingValue’ (on Reddit) or ‘@RoaringKitty’ (on YouTube) – posted a cryptic image of a man leaning forward in a chair, a visual call-back to a meme associated with anticipation. The following day, he shared a video clip from V for Vendetta titled ‘Overture’, further fuelling speculation of a resurgence of the GameStop saga. On 14 May, Gill posted a brief clip from Avengers: Age of Ultron, showing the villain Thanos declaring, ‘Fine, I’ll do it myself’. Mirroring the dramatised hero-villain tropes often embedded in WSB narratives, this post was widely interpreted as a symbolic statement of intent, signalling that Gill was re-engaging personally with the stock. In the immediate aftermath of these posts, the stock was extremely volatile. On 14 May, the stock closed at $48.75, marking a 60.1% increase from the previous day. The trading volume that day was approximately 105 million shares, the highest since March 2021, though it is important to note that these values cannot be directly compared to the 2021 peak prices due to a 4-for-1 stock split that occurred in mid-2022. While the percentage-based movement echoed previous memetic surges, the scale was tempered, and the cultural momentum more cautious than during the original squeeze.

Emic and etic perspective: A dual approach

Understanding the GME phenomenon and the role of WSB requires attention to both internal and external systems of meaning. Its dynamics call for an interpretive approach that can capture how meaning is produced, stabilised, and negotiated both within and beyond the boundaries of specific social fields. Because actors draw upon cultural codes in ways that are both performative and contested, we combine emic (participant-generated) and etic (analytically-distanced) perspectives to explore how WSB participants construct cultural rationalities, and how such rationalities are reframed or misrecognised by external observers. These disjunctures are produced not merely by misunderstanding, but also deeper asymmetries in cultural authority and epistemic legitimacy. Couldry and Hepp (Reference Couldry and Hepp2016) underscore how digitally-mediated environments, where institutional logics and vernacular meaning-making frequently collide, foster contested constructions of reality. Understanding such collisions and taking subcultural meaning-making seriously requires a methodological design capable of grasping both sides of the symbolic interface.

Our study therefore employs a dual qualitative approach to capture both the internal discourse of WSB and its external framing in media. We combine sociology of knowledge discourse analysis (Keller, Reference Keller2011) with a lifeworld-oriented (n)ethnography (Eisewicht and Kirschner, Reference Eisewicht and Kirschner2015; Honer and Hitzler, Reference Honer and Hitzler2015; Kozinets, Reference Kozinets2020) of the WSB digital subculture. The rationale for this two-pronged design is to contrast how WSB participants make sense of events with how outsider narratives (e.g., news media, financial institutions) have framed these same events. By examining both perspectives, we address the hypothesis that mainstream interpretations misunderstood WSB’s behaviour – a misreading that dissolves once the phenomenon is seen as rooted in digital subculture rather than in traditional understandings of rational behaviour in financial markets.

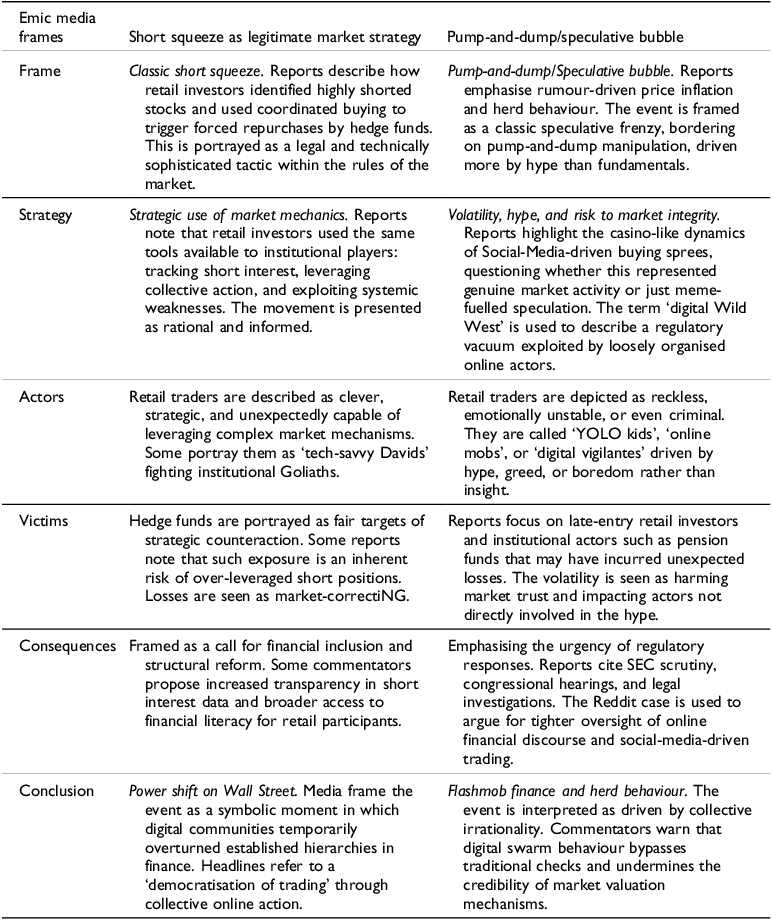

In practical terms, one analytical track (Table A1 in the Appendix) focused on external discourse by collecting and reviewing media reports about the initial GME frenzy (January-February 2021). We analysed these reports for recurring interpretive frames (e.g., ‘short squeeze’, ‘pump-and-dump’), and examined how key financial narratives, such as ‘short squeeze’, ‘pump-and-dump’, or portrayals of WSB participants as ‘irrational’, ‘young’, ‘destructive’, or ‘criminal speculators’, were constructed, repeated, and moralised across outlets. Our aim was to understand how these frames and narratives articulated a media-emic perspective on WSB: one that embedded the subreddit’s activity within a conventional logic of market behaviour and/or moral responsibility. This allowed us to contrast the dominant symbolic order of financial reporting with the WSB-emic cultural logic reconstructed through the ethnographic strand.

The second strand – unfolded here – focused on immersive engagement with WSB as a digital field of cultural production. Rather than treating the subreddit as a passive archive, we examined it as a dynamic social environment in which actors collectively perform, contest, and reaffirm symbolic meanings. Our primary data comes from an in-depth netnography (Kozinets, Reference Kozinets2020) of WSB during the peak of the GME event. From January to April 2021, we actively observed and participated in the subreddit, ultimately sampling and archiving approximately 700 posts (including text, image memes, and video links). After the initial frenzy subsided, we monitored WSB more sporadically, while exploring subreddits that had split off in the meantime (especially r/superstonk, created on 15 March 2021 with currently about 1,100,000 members, but also r/GME, or r/gGmeStop, and anti-communities like r/gme_meltdown). In May/June 2024, when the GME stock price oscillated again, we returned our focus to WSB. Following the tenets of lifeworld-analytic ethnography (Hitzler and Eisewicht, Reference Hitzler and Eisewicht2020), we not only took on a passive observer role but also an existentially-engaged stance. This involved creating a Reddit account to interact with community content and even undertaking a small financial investment aligned with the GME ‘YOLO’ trade. This engagement helped us to experience the field’s inherent risk-taking ethos first-hand, in line with ethnographic principles that emphasise understanding participants’ lifeworld from within. It also built trust and insight, as purely observational approaches might have missed subtleties of meaning. All interactions were conducted under a pseudonymous identity, and posts were collected in compliance with Reddit’s public data policies.

Sampling in the fast-moving, high-volume WSB forum required strategic filtering. We focused on threads directly related to GME during its volatility spike, prioritising high-engagement posts (by upvotes/comments) as well as emblematic memes and discussion threads frequently referenced by users (e.g., ‘DD’ analysis posts and popular meme posts). This purposive sampling aimed to capture both the substantive investment talk and the memetic humour that coalesced around the event. A significant methodological challenge was the multimodality of the data – posts often mixed text with images, GIFs, or emojis, and users frequently linked to or drew on content from other platforms (Twitter screenshots, YouTube clips, etc.).

Ethnographic semantic coding

Central to our analysis of the WSB communication was ethnographic semantics (Spradley, Reference Spradley2016), a coding technique that treats emic terms not as slang or affective noise but as a coherent symbolic system. We identified emic terms as semantic keys – nodes around which practices, values, and group identities were articulated. By using domain and componential analysis, we organised these terms into contrast sets and relational networks that reflected the internal moral economy of WSB. These semantic fields structured how users interpreted success and failure, risk and loyalty, intelligence and deviance. Throughout this process, we used MAXQDA to organise and refine semantic categories through iterative coding and constant comparison. Our aim was not to produce an exhaustive dictionary of WSB language, but to map its semantic architecture and reconstruct the cultural models that oriented participant behaviour. In doing so, we positioned language as both a cognitive schema and a performative medium – one that enables users to navigate uncertainty, affirm belonging, and ritualise economic action.

While recent research in digital finance ethnography increasingly acknowledges the importance of discourse and narrative (e.g., Preda, Reference Preda2017; Ailon, Reference Ailon2019; Hayes and Ben-Shmuel, Reference Hayes and Ben-Shmuel2024; Gregersen and Ørmen, Reference Gregersen and Ørmen2025), few have taken up Spradley’s (Reference Spradley2016) semantic method in a systematic way. Given the growing complexity and density of symbolic practices in digital subcultures, we propose a reactivation of ethnographic semantics as a critical tool. It offers not only methodological precision but also an epistemological stance that treats participants’ own categories of understanding as analytically central. In high-stakes environments such as social media platforms, this attention to vernacular meaning-making becomes essential for capturing the logic that standard rationalist frameworks tend to overlook or dismiss. The following results concentrate on the WSB case, highlighting the semantic and symbolic patterns that characterise this subreddit’s culture during the GME incident.

The collective formation of investor subjects on r/Wallstreetbets

Self-minoritisation in a Manichean world

WSB participants construct a shared identity through distinctive self-minoritisation and the creation of a Manichean world which consists of ‘good but naïve’ retail traders and ‘selfish and reckless’ high financiers (Kozinets and Seraj-Aksit, Reference Kozinets and Seraj-Aksit2024). The most common self-minoritising term is ‘apes’ (Figure 1). In the phrase ‘Apes together strong!’, community members make use of the plural, emphasising unity, and conjuring the image of a loyal, if naïve, collective force. Users also describe themselves as ‘boiz’ or provocatively as ‘degenerates’, ‘autists’, or ‘retards’, adopting ableist slurs in acts of radical self-irony and exclusion from mainstream respectability. Under pressure from the platform operators, the usage of ‘retarded’ was later prohibited by the platform. Users replaced the ableist slur with the term ‘regarded’ because of its similar written form. Expressions implying that users need explanations drawn with crayons to understand them, or that they eat crayons as small children do (‘crayon eaters’ or ‘crayon munchers’), are similarly derogatory. These terms seem to be adapted from their earlier use to mock members of the United States Marine Corps which emerged in the 2010s. While controversial, these labels function as in-group markers celebrating irrationality and emotional decision-making over analytical detachment and prudent financial behaviour. The emphasis on being ‘retail’ rather than professional is worn as a badge of honour, signalling a populist and defiant outsider status. This re-appropriation of terms and images that are used pejoratively in everyday life is a central phenomenon of subculturalisation (Galinsky et al., Reference Galinsky, Hugenberg, Groom, Bodenhausen, Neale and Mannix2003).

Presentation as a community (of Green Wojaks on the left and apes on the right).

Figure 1. Long description

The image consists of two distinct illustrations placed side by side. On the left, there is an illustration of a group of green cartoon characters, known as Green Wojaks, embracing each other. The background features financial charts with various numbers and symbols, indicating a financial context. The right illustration shows a group of apes standing in a line, with the letters W S B prominently displayed above them. The combination of these illustrations suggests a presentation of communities, with the Green Wojaks on the left and the apes on the right, likely representing different groups within the financial or investment sphere.

The community defines itself in juxtaposition to high finance (Figure 2). WSB’s antagonistic stance toward professional finance (particularly institutional investors) is expressed through a range of symbolic enemies and oppositional language (see also Kozinets and Seraj-Aksit, Reference Kozinets and Seraj-Aksit2024; Gendron et al., Reference Gendron, Madelaine, Paugam and Stolowy2025).

Presentation as a community juxtaposed to high finance.

Figure 2. Long description

The collage consists of six images related to finance and investment. The first image shows a Reddit logo with text suggesting financial loss in a hedge fund. The second image features animated characters celebrating with a billion-dollar hedge fund. The third image depicts a person looking at flames with the text ‘IT’S ABOUT SENDING A MESSAGE’. The fourth image shows a young girl looking at a large robot labeled ‘Hedge funds’ with the text ‘Robinhood traders with $600 stimmy checks’. The fifth image is a tweet from Susan of Texas showing Wall Streeters looking down on Occupy Wall Street protesters in 2008. The sixth image shows two people in conversation, with one saying, ‘Let me get this straight, you think that rich people losing money is funny?’ and the other responding, ‘I do, and I’m tired of pretending it’s not.’

The catch-all term ‘suits’ disparages professional investors, particularly hedge fund managers and bankers, who are portrayed as manipulative, reckless, and predatory. During the GME episode this antagonistic worldview transformed the initial play into a mythic battle, dramatised through pop cultural references, memes, and edited movie clips. This gave birth to a highly referential, platform-specific historiography, reinforcing the community’s collective identity and worldview. Specific antagonists during the GME incident included Melvin Capital, Citadel Securities, and Robinhood, the latter vilified for restricting trades at a crucial moment (Figure 3). The sense of a common enemy and the framing of retail traders as a collective fighting against a powerful elite (in the style of referenced movies like The Avengers, Lord of the Rings, 300, and The Matrix) all contributed to the sense of strong group cohesion. The emotional investment which such framing inculcated not only legitimised high-risk strategies but also provided the motivation to buy and hold GME shares.

Presentation as a community juxtaposed towards distinctive financial actors.

Figure 3. Long description

The collage consists of eight images arranged in a grid. The first row features two images: one with an elderly man labeled Citadel and another with a large, armored figure labeled Melvin. The second row includes an image of a man in armor labeled Melvin Capital with the text ‘Sell your positions!’ and another image of a group of soldiers with labels such as Point72, Vlad Tenev, Citadel, and Melvin Capital. The third row shows a man in a hat with a Melvin Capital logo and the text ‘SHUT THEM DOWN-UH!’ alongside an image of a group of people with labels like SEC, CNBC, Hedge funds, Discord, Robinhood Shorts, Melvin, Citadel, and Citron Research. The fourth row features an image of a grotesque creature labeled Melvin Capital and another image of a futuristic scene with the Melvin Capital logo.

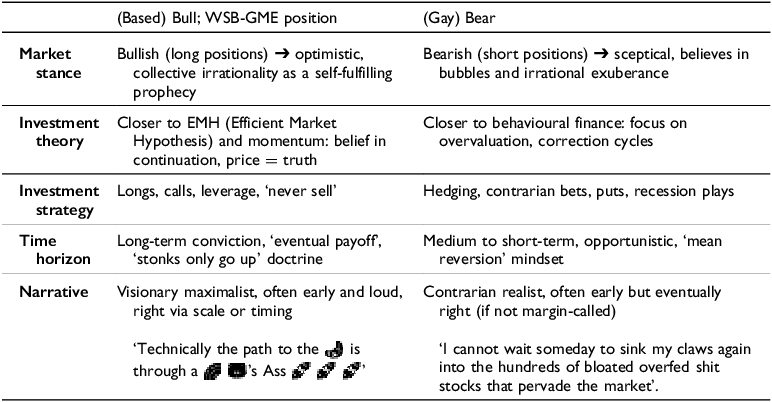

Additional epithets such as ‘snakes’ or ‘boomers’ are used to express perceived generational and ethical divides. ‘Gay bears’ is another enemy label; the ‘bear’ represents falling markets and the people who try to profit from them via short selling (Table 1; see also Table 4). It is important to note that WSB prominently covered plays from both long and short strategies prior to the GME event, and strategies from both sides were well received. However, as developments unfolded, the GME play became the template for a series of bull strategies. It was precisely this one-sided focus that later led to the GME play being split off into own subreddits.

‘Bulls’ versus ‘Bears’.

Table 1. Long description

A table with two columns and five rows comparing bullish and bearish market stances, investment theories, strategies, time horizons, and narratives. The first column represents the bullish stance, labeled as ‘Based Bull; WSB-GME position,’ and the second column represents the bearish stance, labeled as ‘Gay Bear.’ The table details the market stance, investment theory, investment strategy, time horizon, and narrative for both stances. The bullish stance is optimistic, believes in collective irrationality, and follows the Efficient Market Hypothesis and momentum. The bearish stance is skeptical, focuses on overvaluation and correction cycles, and uses hedging and contrarian bets. The bullish strategy involves longs, calls, leverage, and a long-term horizon, while the bearish strategy involves hedging, puts, and a medium to short-term horizon. The narratives differ, with the bullish stance being visionary and maximalist, and the bearish stance being contrarian and realistic.

‘Suits’ employ ‘interns’ and ‘shills’ to watch the ‘apes’, to gather information and spread misinformation, and to sow ‘FUD’ (Fear, Uncertainty, Doubt) and ‘FOMO’ (Fear of Missing Out). These figures enable the construction of a moralised dichotomy: the irrational but good insider versus the manipulative and evil outsider. Even within these groups, specific narrative roles emerge: the ‘bagholder’, for instance, represents the tragic hero who remains loyal to the cause and suffers losses but remains respected. These roles transform the market into a Manichean world in which community belonging is as central as financial action, and where practices are governed more by group morale than market logic.

The intersection of financial orientation and internet meme culture in the group is also reflected in the community’s core communication practices. Contributions are often categorised by fixed themes, indicated through thread filters (‘flairs’). Two prototypical types of posts can be distinguished: on the one hand, posts that present and thoroughly discuss securities and investment ideas (e.g., DD, discussion, charts), often employing technical chart analysis and referencing external sources; on the other hand, posts that utilise visual and textual memes, videos, and references drawn from pop and internet culture. Notably, community-specific terminology and ironic expressions rooted in meme culture frequently appear even in more elaborate strategic discussions, such as in the context of ‘due diligence’, understood as a careful and comprehensive analysis. The proliferation of pseudo-DD during the rally further illustrates the community’s ambivalent relationship with financial expertise, welcoming rigorous research, but always laced with irreverence.

Contrasting the antagonists which it constructs, WSB populates its own universe with supporting characters and symbolic spaces that reinforce its cultural distinctiveness. The figure of the ‘wife’s boyfriend’ serves as a humorous and self-deprecating embodiment of emasculation and failure, often invoked to dramatise personal loss or humiliation. Other cultural references include the ‘Wendy’s employee’ as a symbol of post-failure employment, and the catchphrase ‘Sir, this is a casino’ as a sardonic admission of the speculative, game-like nature of meme-stock investing. These figures and settings operate as both coping mechanisms and group markers, transforming trading from a private, financial act into a public, theatrical performance.

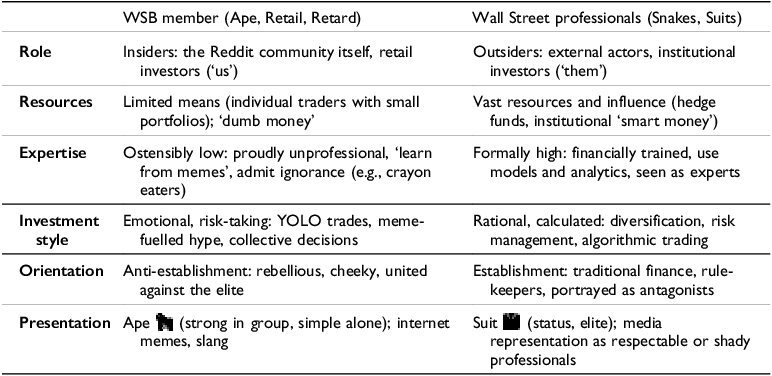

Langley (Reference Langley2008: 93) observes that the ‘the financial self-discipline of today’s investor subjects is seemingly elemental and highly self-serving, performed in the name of individual autonomy and welfare like never before’. Even if financialisation and individualisation go hand in hand, however, ordinary people may yet make ‘use of social networks to achieve and enforce instrumental goals’ (Harrington, Reference Harrington2008: 176). From this vantage point, the function of WSB for its members becomes clear: The community’s meme culture creates a symbolic order which governs collective action and in which financial success and savviness in trading strategies is juxtaposed with self-minorising and self-deprecation (Table 2).

‘Apes’ versus ‘Suits’.

Table 2. Long description

A table comparing characteristics of WSB members and Wall Street professionals. The table has six rows and two columns. The first column lists categories such as Role, Resources, Expertise, Investment style, Orientation, and Presentation. The second column describes the characteristics of WSB members and Wall Street professionals in each category. WSB members are described as insiders with limited means and ostensibly low expertise, while Wall Street professionals are described as outsiders with vast resources and high expertise. The table highlights differences in investment styles, orientations, and presentations between the two groups.

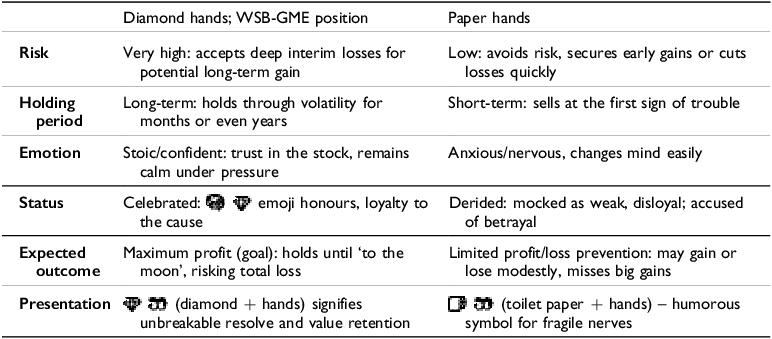

Within WSB, risk and investment are reinterpreted through cultural frames. The market becomes a symbolic battlefield. Humour and irony act as coping mechanisms. Moral norms valorise loyalty and community over individual gain. Selling early equates to betrayal, holding (‘Hold’, ‘hodl’) signifies virtue. Having ‘diamond hands’ is a celebrated virtue, symbolising courage, conviction, and loyalty to the shared narrative. By contrast, having ‘paper hands’ is a vice, symbolsing cowardice or lack of belief (Table 3). Interestingly, this value system reverses traditional financial logic: whereas conservative investors aim to minimise risk, WSB shames such prudence as weakness, privileging collective perseverance over individual caution. Language (e.g., hand metaphors) here functions to enforce behavioural norms and apply peer pressure. What is more, the simple and, above all, unlikely, expectation that prices will exclusively rise and do so significantly – to the exlusion of alternative actions or an exit strategy – is what makes the coordination of such a large number of anonymous users possible in the first place (on ‘simplifying frames’ for mass mobilisation see Snow and Benford, Reference Snow and Benford1988). The apparent stupidity of the strategy is precisely what ensures that all participants can act collectively, rendering detailed planning unnecessary.

‘Diamond hands’ versus ‘paper hands’.

Table 3. Long description

A table comparing diamond hands and paper hands in terms of risk, holding period, emotion, status, expected outcome, and presentation. The table has two columns: Diamond hands; WSB-GME position and Paper hands. It has six rows labeled Risk, Holding period, Emotion, Status, Expected outcome, and Presentation. Diamond hands are described as having very high risk, long-term holding period, stoic/confident emotion, celebrated status, maximum profit expected outcome, and diamond hands presentation. Paper hands are described as having low risk, short-term holding period, anxious/nervous emotion, derided status, limited profit/loss prevention expected outcome, and toilet paper and hands presentation.

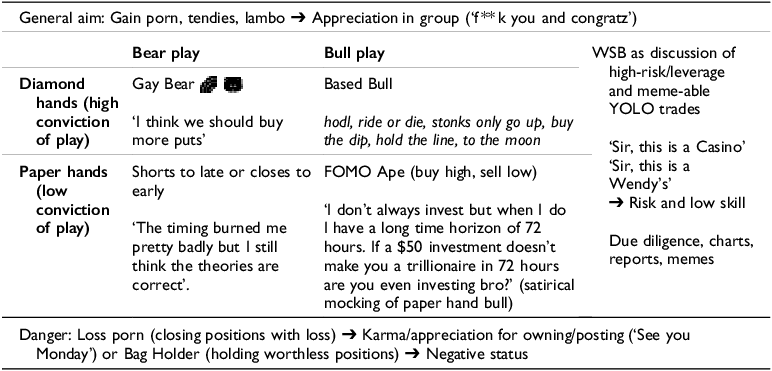

Considered as a whole, the semantic domain of WSB produces an internally coherent meaning system (Table 4). The goal of members is to earn money (so-called ‘gain porn’ or ‘tendies’) and gain recognition in the group. The danger is closing positions with a loss (so-called ‘loss porn’) or holding worthless positions (‘bag holder’). This can be achieved through ‘Bear plays’ (on declining share value) or ‘Bull plays’ (in hope of rising share value, typically leveraged through financial instruments). The conviction of the play is represented through ‘Diamond hands’ (holding, doubling down, etc.) and ‘Paper hands’ (panic selling, closing position too early). What may appear externally to be an incoherent slang reveals itself as a full-fledged cultural code, structuring identity, action, emotion, and opposition. This language operates as a symbolic infrastructure for decentralised participation, offering members not just terms for financial activity, but a framework for belonging, rebellion, and collective catharsis.

Cultural model matrix of WSB (pre-GME).

Table 4. Long description

Table 4 presents a cultural model matrix of WallStreetBets (WSB), focusing on different play strategies and their outcomes. It is divided into three main sections: Bear play, Bull play, and WSB as a discussion of high-risk/leverage and meme-able YOLO trades. The table has four rows and three columns. The columns are labeled Diamond hands (high conviction of play), Paper hands (low conviction of play), and WSB as discussion of high-risk/leverage and meme-able YOLO trades. The rows are labeled Bear play, Bull play, and Danger. Under Bear play, Diamond hands include Gay Bear and I think we should buy more puts, while Paper hands include Shorts to late or closes to early and The timing burned me pretty badly but I still think the theories are correct. Under Bull play, Diamond hands include Based Bull and hodl, ride or die, stonks only go up, buy the dip, hold the line, to the moon, while Paper hands include FOMO Ape (buy high, sell low) and I don’t always invest but when I do I have a long time horizon of 72 hours. If a $50 investment doesn’t make you a trillionaire in 72 hours are you even investing bro? (satirical mocking of paper hand bull). Under Danger, it lists Loss porn (closing positions with loss) Karma/appreciation for owning/posting (See you Monday) or Bag Holder (holding worthless positions) Negative status. The table aims to highlight the general aim of gaining porn, tendies, lambo appreciation in group (fk you and congratz), and the associated risks and outcomes.

WSB articulates its financial motivations through an ironic and memetic reimagining of market success. Profits are colloquially referred to as ‘tendies’, a term derived from chicken tenders, symbolising a childish yet emotionally-resonant reward for risk-taking behaviour. This metaphor is rooted in the self-deprecating stereotype of the unemployed, basement-dwelling trader, and humorously reframes financial gain as a kind of personal validation. ‘Bananas’ serve a similar symbolic function for apes evoking the idea of basic but cherished gains in a collective system. And there is the goal of the ‘Lambo’ (the Lamborghini as a luxury car and a target for big profits). The rallying cry ‘To the moon’, accompanied by rocket emojis or the onomatopoetic ‘Brrrrrr’ for money printing, captures the collective hope of dramatic upward price movements, functioning both as aspiration and affirmation of group momentum. ‘Stonks’, a deliberate misspelling of stocks, plays a similar role; here too (as with the terms ‘tendies’, ‘crayons’, etc.), there is explicit self-infantilisation.

Coping with uncertainty and forming fictional expectations

In financial markets investors are confronted with fundamental uncertainty, since they must decide whether to buy, sell, or hold without being able to anticipate the economic outcome. Attempting to estimate the value of future investments, people can invent more or less rigorous methods of testing their imaginations, but they cannot know. In such a context, collectively shared stories work to reduce the ‘hypercomplexity’ in which retail investors’ decision-making is embedded (Schimank, Reference Schimank2011; Shiller Reference Shiller2019). In contrast to accounts from economics which conceive of financial actors as rational investors (e.g., Fama, Reference Fama1970) and offer cognitive and psychological explanations where irrationalities and anomalies arise (e.g., Shefrin, Reference Shefrin2007), economic sociology views the value of financial assets as formed through collective beliefs which are supported and socially stabilised by ideas that are typically not of an economic nature (for an account of how ‘ideas’ are understood here see Weber, Reference Weber1978). As Harrington (Reference Harrington2008: 48) shows, stories orient retail investors by constructing links between the signifiers (stocks) and the signified (values); they therefore represent ‘literally the lingua franca of investing’, underpinning the lines of reasoning which direct the focus of attention to specific assets and direct modifications or deviations from commonly-accepted models of asset valuation.

‘Fictional expectations’ (Beckert, Reference Beckert2016) and imaginaries of the future, governed by socially plausible, socially available ideas – like described above – are imperative, not because retail investors are directed by them irrationally in the sense of behavioural economics, but because as retail investors struggle to make decisions when they cannot know the outcome, they draw on ‘charismatic ideas’ to facilitate subjective certainty. A community of believers, a ‘charismatic community’ according to Weber (Reference Weber1978), follows a non-economic idea to modify and perhaps even radically overturn the prevailing frame of interpretation underlying the valuation of a stock or whole asset class. In the case of WSB, such a charismatic idea was the ‘M.O.A.S.S.’ (Mother of All Short Squeezes), which represents the mythic endgame in WSB’s shared story (sometimes associated with a potential collapse of the market as an ‘end of the world’). Although the WSB community has a loose, decentralised organisation, it is inspired by charismatic leaders from within the subreddit community, who use their logical exposition and financial analysis to encourage members to invest as a larger collective (Figure 4).

Presentation of a charismatic leader and WSB as a movement.

Figure 4. Long description

The collage consists of six distinct images arranged in a grid. The first image is a stylized portrait of a person with the word ‘HOLD’ beneath it. The second image shows a person typing on a keyboard in a dimly lit room. The third image features a quote that reads, ‘What’s an exit strategy?’ attributed to ‘u/deepfuckingvalue.’ The fourth image depicts a protest scene with a person in a suit and a red cap labeled ‘WSB’ holding a sign that reads ‘THE ROARING KITTY OF WALL STREET.’ The fifth image shows a battle formation with soldiers holding spears, labeled ‘wsbAutist’ and ‘DeepFuckingValue,’ with the text ‘This is where we double down.’ The sixth image portrays a historical military charge with soldiers holding flags, labeled ‘19 Year Olds’ and ‘Poor People,’ with the text ‘HOLD THE LIIIINNNE!!!’ The collage conveys themes of financial activism and collective action.

WSB played a major role in the GME episode both because it was host to such charismatic leaders – most notably, Keith Gill, who attained an almost prophet-like status – and because it provided a channel which could disseminate the story so effectively. Digitalised communities of believers on social media platforms are characterised by the overabundance and ultrafast circulation of memes which transport ideas; thus the effects of fictions, and particularly of speculative fictions, become even more potent. Keith Gill provided the community with a vision of a profitable new investment opportunity (squeezing the GME short and crushing the short-sellers by forcing them to buy back the stock at ever increasing stock prices) which deviated from commonly shared expectations of market developments. While short-sellers (several Wall Street hedge funds) based their strategies on negative prognostications about the company, Gill postulated that the market had mispriced a reasonable stock and identified that GME had accrued a 140% short interest. Within WSB, the belief was established that the investment opportunity would be successful only if the vision was followed. This vision was linked to hopes of personal prosperity and gaining ‘a slice of the pie’, but also a desire to ‘stick it to the man’ and to make ‘suits’ pay. The investment idea was loaded with a vision of revenge for haute finance’s deprivation and exclusion of retail investors (Samman and Sgambati, Reference Samman and Sgambati2023; Gendron et al., Reference Gendron, Madelaine, Paugam and Stolowy2025).

Keith Gill was not the only charismatic leader on WSB. Although they both lost that status later on, ‘Papa Elon’ (Elon Musk) and ‘Papa Chamath’ (Chamath Palihapitiya) were mythologised as father-figures: wealthy, charismatic allies who lent legitimacy and moral support to the cause of the apes. Indeed, a significant turning point during the GME incident was Elon Musk tweeting the word ‘Gamestonk!!’ along with a link to the WSB subreddit on January 26, 2021. This attention and endorsement from one of the world’s most influential tech tycoons helped the stock go viral in a parabolic trajectory.

YOLO: Stabilising the event character

As the meme culture on WSB demonstrates, ambivalent profit-seeking and commitment to an in-group are important elements of its digital retail investor subculture; another is a life orientation with revolves around experience seeking (Schulze, Reference Schulze, Sundbo and Sørensen2013; Schneickert et al., Reference Schneickert, Hess and Delhey2024). This life orientation is performed through a ‘fun morality’ (Bell, Reference Bell1976)) which pursues the pleasures attached to high-risk financial decisions. WSB’s self-description – ‘Like 4chan found a Bloomberg Terminal’ – succinctly captures the hybrid nature of the community’s identity. This phrase alludes to two contrasting cultural references: 4chan, a controversial online imageboard known for its anarchic, provocative, and often borderline or illegal content, and the Bloomberg Terminal, a high-end financial data platform used by institutional investors. The juxtaposition of 4chan and Bloomberg signals a paradoxical investment ethos: one that combines irreverent internet subculture with real-time access to professional market analyses and investment tools. WSB thus positions itself between meme-driven chaos and technical sophistication. In contrast to WSB’s high-risk trading culture, subreddits such as r/investing, r/stocks, or r/personal finance promote more conservative financial strategies – often advocating passive investment in ETFs and non-leveraged instruments. WSB emphasises the distinction between investing and trading, with the latter defined by active, short-term speculation in equities and options. This difference marks a clear cultural divergence within Reddit’s financial communities: WSB is unapologetically speculative, performative, and meme-infused, whereas other subreddits follow the logic of long-term, prudent and disciplined financial planning.

WSB posts are typically devoted to irrational trading strategies (Figure 5), projecting an investment approach characterised by high risk-taking and the willingness to accept substantial losses in pursuit of potentially enormous gains (Gendron et al., Reference Gendron, Madelaine, Paugam and Stolowy2025). This ethos, often explicitly referred to as ‘gambling’ by users themselves, serves as a prerequisite for being recognised as a legitimate member of the group. The open display and celebratory sharing of evidence of large financial losses – referred to as ‘loss porn’ – is common, frequently accompanied by affirming comments such as ‘one of us’ or ‘a true ape’. In this way, users gain community recognition and translate their loss of financial capital into ‘symbolic capital’ (Bourdieu, Reference Bourdieu1984). Similarly, unbalanced portfolios – those lacking any sign of risk mitigation and often fully invested in highly speculative options tied to a single security – are valorised via terms such as ‘YOLO’ (you only live once) or ‘Yolo Money’. By upvoting (‘karma’) and awarding digital gifts (‘awards’) to posts, the community rewards members for useful advice on stocks as well as for YOLOing their finances.

Ironic self-presentation as risky, loss-taking, and less successful investors.

Figure 5. Long description

The collage consists of six images with captions related to WallStreetBets and personal finance. The first image shows a group of people smiling with the caption ‘WSB when 60 percent of your options expire worthless.’ The second image features a person in a historical costume with a sign that reads ‘Wall Street’ and the caption ‘You are without doubt the worst stock trader I’ve over heard of.’ The third image depicts a person looking concerned with the caption ‘r/personalfinance when VTSAX goes down by 0.4 percent.’ The fourth image shows a person with sunglasses and the caption ‘But you have heard of me.’ The fifth image is split into two parts: one showing a person with the caption ‘New money finding WSB and buying GME at 350’ and the other showing an older person with the caption ‘New money finding out what WSB actually does.’ The sixth image shows a person inside a cardboard box with the caption ‘Just bought my first home. Thank you Wallstreetbets!’

Slogans like ‘YOLO’ or ‘Lambo or homeless’ serve as an invitation to risky actions. YOLO encapsulates the WSB ideal of high-stakes, all-in investing, where entire portfolios are risked in a single move. YOLO is less a financial tactic than a cultural ritual, a public commitment to bravery, irrationality, and resistance. As Samman and Sgambati (Reference Samman and Sgambati2023) note, the slogan expresses the apocalyptic form of financial nihilism that motivates WSB members.

Dynamics and pluralisation of digital finance cultures

The cultural model of WSB

WSB is a digital subculture situated at the intersection of speculative finance, internet memetics, and performative identity (see e.g., Kozinets and Seraj-Aksit, Reference Kozinets and Seraj-Aksit2024; Gregersen and Ørmen, Reference Gregersen and Ørmen2025). Unlike conventional investing communities, WSB exhibits a distinctive tolerance of strategic pluralism, allowing for divergent approaches to financial markets while maintaining a cohesive, symbolically charged discourse. WSB plays are typically defined by their high-risk, high-leverage nature, often involving out-of-the-money options, margin trading, and concentrated positions. Yet beyond the financial exposure which they produce, these plays are also culturally coded as performative acts, often intentionally absurd. The ‘play’ becomes a stage for irony, spectacle, and digital identity-making, where economic rationality is entangled with meme aesthetics, nihilism, and communal entertainment. WSB itself emerged in 2012 as a reaction to the perceived conservatism of more traditional subreddits such as r/investing and r/personalfinance, from which users were criticised for proposing risky or unconventional strategies. This foundational tension between formal finance discourse and irreverent speculation shaped WSB into a space where reckless trading is not only tolerated but valorised, and where failure is aestheticised through memes, screenshots, and ritualised storytelling. The reconstructed logic is structured by two orthogonal dimensions: strategic orientation (bullish vs. bearish) and convictional stance (‘diamond hands’ vs. ‘paper hands’).

Bull plays, representing long-biased positions such as calls, shares, or leveraged longs, are the dominant form of speculation within WSB. However, bearish plays, including puts, volatility trades, and hedged short positions, are also respected when executed with rhetorical flair and contrarian insight. This legitimisation of both upward and downward speculation distinguishes WSB from ideologically homogenous financial communities. Parallel to the axis of strategic orientation is the axis of conviction. ‘Diamond hands’ refers to a high-conviction posture, characterised by holding through volatility, resisting temptation to sell, and often embracing unrealised losses as a badge of honour. In contrast, ‘paper hands’ denotes early exits, risk aversion, or failure to maintain conviction, frequently stigmatised within the community as a form of moral weakness.

These two dimensions intersect to produce culturally coded archetypes. The diamond-handed bull occupies the community’s moral and affective centre, whether rewarded with massive returns (‘gain porn’) or enduring loss with stoic commitment (‘bagholding’). The diamond-handed bear is valorised for ironic detachment, embodying a kind of stylish contrarianism. Underlying this framework is a nuanced blend of financial theory and internet-native epistemology. ‘Based bulls’ tend to operate with implicit faith in momentum, trend continuation, and narrative-driven catalysts – closely aligned with certain interpretations of the Efficient Market Hypothesis (EMH) and behavioural finance accounts. ‘Gay bears’, on the other hand, reflect a sceptical posture: they search for inefficiencies, anticipate reversals, and construct hedged portfolios designed to capture dislocations. While both sides pursue alpha (an overperformance compared to an index), they do so through divergent epistemic and stylistic lenses.

Paper-handed bulls, by contrast, are seen as tragicomic figures: those who exit too early, miss the payoff, and post regret-laden ‘loss porn’. Paper-handed bears, lacking both conviction and timing, tend to be culturally invisible or openly derided. Importantly, these outcomes (‘gain porn’, ‘loss porn’, and ‘bagholding’) do not merely reflect financial results, but function as ritualised closures, codified in screenshots, memes, and self-narratives that circulate as acts of cultural belonging. Posting one’s losses is as significant as posting one’s gains, as both reaffirm the stakes of participation. The community thus operates not only as a space of speculative activity, but also as a symbolic economy in which financial positions are transfigured into memes, reputational capital, and communal affect.

Through this cultural matrix, WSB becomes a speculative stage on which style, strategy, and symbolic capital co-produce meaning. The forum sustains not only trades, but also personae, embodied in screenshots, language, and lore, that persist well beyond any individual play. What begins as an investment choice thus becomes an identity performance of belonging to the subculture of WSB.

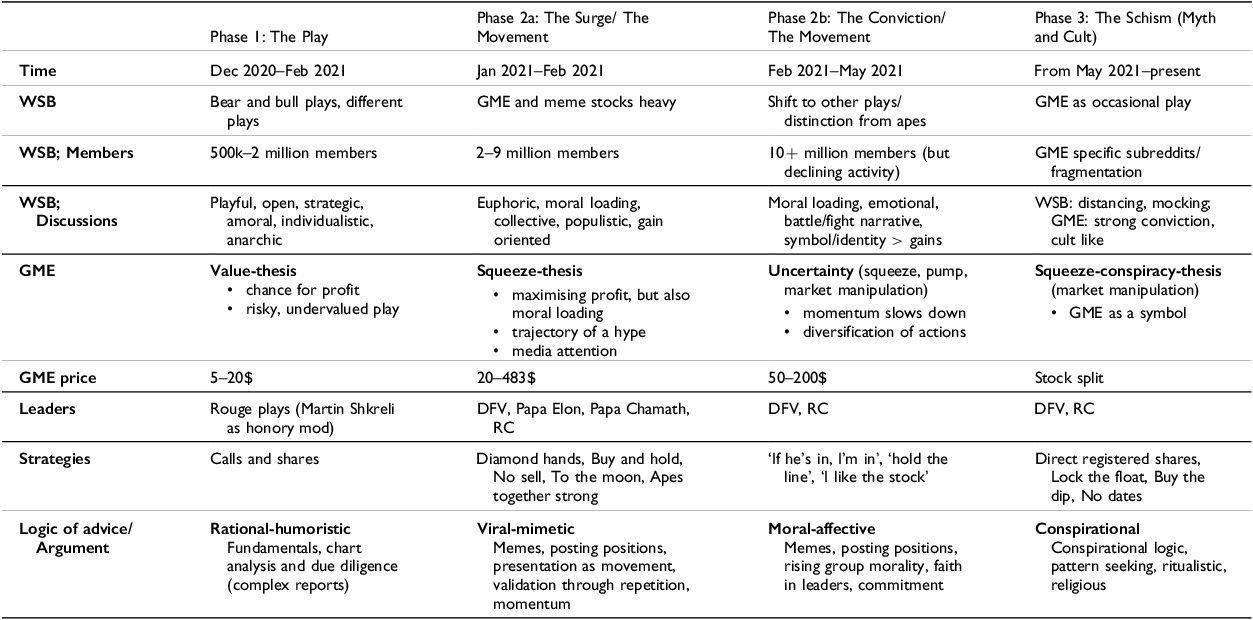

Phases of GME and the cultural dynamics of financial subcultures

The rise of GME as a symbolic asset within WSB marks one of the most significant cultural transformations in the recent history of online finance. What began as a contrarian value play evolved into a global media spectacle, a collective resistance narrative, and eventually a distinct subcultural offshoot. This trajectory can be understood in four phases, which we reconstructed from our data (Table 5): The Play, The Surge, The Conviction, and The Schism. Each phase is defined by its market behaviour and cultural tone, but also by a shifting logic of advice and knowledge production: who speaks with authority, what counts as evidence, and how truth is performed and shared.

-

• Phase 1: The Play (Dec 2020–early Jan 2021). In its earliest stage, GME was a niche contrarian play discussed in reports (‘DD’). Users shared financial statements, short interest metrics, and technical charts to support the thesis that GME was undervalued and heavily shorted. This rational framework was embedded in a deeply ironic discourse. Financial advice was both sincere and laced with meme-driven absurdism; epistemically, the dominant style was rational-humoristic. Posters and emerging leading figures such as ‘DeepFuckingValue’ (DFV) combined spreadsheet analysis with deadpan humour.

-

• Phase 2a: The Surge (Jan 2021). In late January 2021, GME exploded into public consciousness. The stock surged from under $20 to an intraday high of $483, fuelled by mass participation, viral memes, and exponential growth in WSB membership (from 2 million to over 8 million within days). This was a moment of collective ecstasy. Elon Musk’s tweet (‘Gamestonk!!’) and Chamath Palihapitiya’s call-buying added legitimacy and momentum. Advice and communication became performative; users no longer argued with charts but with memes, screenshots, and collective slogans. The dominant epistemic style became viral-mimetic. Truth was what went viral, what was upvoted, what the crowd believed. The act of holding GME was framed less as an investment and more as a rebellion against institutional finance. Knowledge was legitimised by social displays and shared emotion. In this moment, WSB briefly transitioned from a trading forum into a populist digital movement. GME became a battlefield in a populist struggle between ‘retail’ and institutional finance.

-

• Phase 2b: The Conviction (Feb–May 2021). After the initial surge, GME’s price stabilised at a higher but more volatile plateau. With this development came a shift in tone. DD gave way to faith, and memes gave way to moral slogans. DFV was no longer merely an analyst, but an avatar of collective endurance. ‘Hold the line’ became a moral imperative, and ‘diamond hands’ signified loyalty to a shared story. Argumentation in this phase took on a morally-affective style: truth was what felt right, what proved one’s commitment to the community and its cause. Rational arguments were still present but subordinated to emotional loyalty. Dissent or scepticism was often framed as betrayal. The subreddit r/GME began to grow, attracting users who wanted to focus solely on GME, often with greater seriousness and an ideological focus. While still culturally adjacent to WSB, this marked the beginning of an epistemic divergence. The narrative shifted from short-term speculation to long-term conviction and tension emerged. While some users doubled down on holding, others began to question the coherence of the strategy and/or the movement, sold the stock or options, or diversified into other plays.

-

• Phase 3: The Schism (mid-2021–present). Eventually, GME ceased to be a central WSB play. As its trajectory flattened, its cultural aura intensified within newly formed communities like r/Superstonk, with their own research cultures, language codes, and hierarchies of belief. In this phase, the epistemic style turned conspiratorial. Truth was hidden, not obvious. Those who ‘did the DD’ were praised not for producing falsifiable knowledge but for revealing insight through symbolic pattern recognition. DRS (Direct Registration System) of shares became a new strategy and ritual, a litmus test for belief. Within this offshoot, argumentation became highly recursive, self-referential, and resistant to external critique. Meanwhile, WSB itself drifted back toward its broader roots: pluralistic, ironic, and strategically diverse. GME remained part of its lore, but no longer of its practice.

Phase model of GME and WSB.

Table 5. Long description

A table comparing the phases of GME and WSB from Dec 2020 to present. The table is divided into four phases: The Play, The Surge, The Conviction, and The Schism. Each phase is characterized by different market behaviors, cultural tones, and logics of advice and knowledge production. The table includes columns for time, WSB activities, WSB members, WSB discussions, GME thesis, GME price, leaders, strategies, and logic of advice or argument. Notable trends include the shift from rational-humoristic advice in Phase 1 to viral-mimetic and moral-affective styles in Phases 2a and 2b, and finally to a conspiratorial style in Phase 3. The table also shows the evolution of GME’s price and the strategies used by members.

This model illustrates the pluralisation of subjectivities within the emerging landscape of digital financial participation. Across the four phases, we observe not a unified investor identity, but a proliferation of culturally coded roles: the ironic speculator, the memetic insurgent, the moral holder, the conspiratorial initiate. Each phase sustains a distinct mode of knowing, a form of belonging, and a narrative of agency – ranging from tactical cynicism to sacrificial conviction. Rather than treating the retail investor as a singular figure, the GME phenomenon demonstrates how financial actors online are shaped by aesthetic practices, affective bonds, epistemic rituals, and platform-specific norms. In doing so, it challenges classical notions of rational economic agency and invites a more nuanced, culturally embedded understanding of market participation in the digital age.

Conclusion

Online communities such as WSB are the product of both the ‘platformisation of financial transactions’ (Westermeier, Reference Westermeier2020) and new contexts of hyperconnectivity (Brubaker, Reference Brubaker2023). These online communities mark an acceleration of the financialisation of everyday life, and a transformation of how finance is practised, experienced, and understood by retail investors. Because new digital technologies guarantee easy access to financial markets and create interactional spaces for digital subcultures to exchange advice, the ways in which information and expertise can spread, communities can emerge and disperse, and charismatic ideas can translate into economic action, differ radically from the times of the telegraph or the Bloomberg terminal. This becomes evident in three interrelated processes: culturalisation, normalisation, and mediatisation. Each process represents a critical dimension of the shift from conventional, professional financial spaces to digitally networked, participatory, and culturally-mediated arenas of investment. WSB offers a compelling empirical case to explore how these dynamics intersect with identity, fictional expectations, and symbolic practice.

While previous research has addressed the investment identities of middle-class retail investors (Schimank, Reference Schimank2011; Fligstein and Goldstein, Reference Fligstein and Goldstein2015), in the present context financial activity becomes increasingly embedded in and shaped by subcultural meaning systems which go far beyond cultural repertoires of professionals and experts (Preda, Reference Preda2017). Rather than being dismissed as market anomalies or political activism, phenomena such as the GME incident (and other related plays at the time like AMC, Nokia, and BlackBerry) must be read as expressions of a cultural logic – one in which narrative, symbolism, and collective identification redefine financial participation. The divergence between internal cultural models and external economic interpretations renders GME not just a financial event, but a cultural phenomenon. The subreddit’s lexicon is a semiotic toolkit that encodes cultural norms, emotional orientations, and moral expectations. Central to this is the paradoxical self-positioning of users as both financially savvy and cognitively deviant, epitomised in self-referential labels such as ‘autists’, ‘degenerates’, and ‘retards’. Rather than functioning as marginalising or exclusionary, these terms create a symbolic grammar of belonging, drawing on irony and strategic self-deprecation to signal both solidarity and resistance to external norms. Users culturalise finance through a reinterpretation of financial practices within which trading becomes a medium of symbolic labour, subcultural capital, and affective meaning-making. Investment is reframed as cultural participation in a stylised, memetic, and ideologically charged performance of a collective identity. In this era of the financialisation of the self, we witness the development of new collective subjectivities within digital communities.

Closely linked to this phenomenon is the normalisation of financial practices (Langley, Reference Langley2008). Digital trading platforms like Robinhood, eToro, or Trade Republic have minimised technical and economic access barriers and have empowered a broader population to engage in investment practices once reserved for professional elites or the affluent. The automation of trading interfaces, proliferation of mobile access, and integration of gamified features contribute to the casualisation and domestication of financial activity. This infrastructural transformation has rendered finance an everyday activity for millions of users – particularly younger investors – who engage in trading alongside other forms of digital participation. On WSB, this normalisation is visible in the ritualised posting of ‘loss porn’ or ‘YOLO’ trades, which blur the distinction between financial decision-making and daily content production. These practices normalise high-risk speculation as a routine component of online self-expression. Thus, what used to be a domain of deliberative, expert-based action has become reconfigured as a mundane mode of affective engagement, experienced as part of digital everyday life (with drastic consequences when losing money).

The WSB case also demonstrates that investment practices are shaped by and through media logics, particularly meme culture and virality-driven communication dynamics. On WSB, the performativity of finance is closely intertwined with its media ecology. Meme culture functions as a vehicle for ideas and ‘collectively shared stories’ (Schimank, Reference Schimank2011) which provide retail investors with justification for financial decisions. However, investment decisions are not only economic acts but content events – subject to likes, upvotes, shares, and memeification. This transformation aligns with broader trends in social trading, where decision-making is no longer confined to individual research but is shaped by algorithmically filtered, publicly visible information flows. Platforms like Reddit, X, Discord, or TikTok function as both sites of financial information and stages for identity performance. In this context, trust is derived from symbolic fluency and affective alignment with the group’s shared story. On WSB, community membership is performatively constructed through participation in key rituals: posting losses or gains, affirming collective identity (‘Apes together strong!’), and endorsing charismatic leaders like Roaring Kitty. Identity formation is thus structured by adherence to shared symbolic codes and a willingness to engage in performative acts of belief and group loyalty. The culture’s language, symbols, and heroes circulate not only across Reddit but also broader media ecosystems, producing a recursive loop where finance becomes spectacle, and spectacle becomes financial action. Media logic also inflects the temporal orientation of investment. Fictional expectations of the future like the ‘M.O.A.S.S.’ are framed in epic, almost apocalyptic terms, fostering a sense of impending collective climax. This time horizon is not rooted in financial models but on narrative payoff, emotional climax, and potential for virality. As such, mediatisation fuses trading with entertainment, moralisation, and aesthetic experience.

Taken together, the culturalisation, normalisation, and mediatisation of finance – exemplified in WSB – mark a significant transformation in contemporary retail investment practices. What was once a specialised, expert-driven domain has become a participatory, expressive, and culturally embedded field of action. On WSB, investment is not only evaluated in terms of financial return, but also in terms of symbolic capital: affective resonance, narrative coherence, meme virality, and group belonging. Far from being irrational, these practices articulate a distinct rationality – one that merges financial speculation with moral positioning, social performance, and collective storytelling. To understand such phenomena requires not only technical or regulatory analysis but also a cultural-semiotic perspective attuned to the lived meanings, discursive practices, and performative rituals of digital finance communities. Acknowledgements

Acknowledgements

The authors would like to thank the two anonymous reviewers for their helpful comments, suggestions, and critiques, and the journal’s editorial team for their exceptionally diligent work in finalising the article, going beyond mere formalities.

Author contributions

Both authors contributed equally to the design and implementation of the research, to the analysis of the results, and to the writing of the manuscript.

Funding statement

The authors received no financial support for the research, authorship, and/or publication of this article.

Competing interests

The authors declare no potential conflicts of interest.

Appendix

Emic frames in media.

Table A1. Long description

A table comparing emic media frames of short squeeze and pump-and-dump/speculative bubble. The table has six rows and five columns, including Frame, Strategy, Actors, Victims, Consequences, and Conclusion. Row 1: Frame, Classic short squeeze. Reports describe how retail investors identified highly shorted stocks and used coordinated buying to trigger forced repurchases by hedge funds. This is portrayed as a legal and technically sophisticated tactic within the rules of the market. Pump-and-dump/Speculative bubble. Reports emphasise rumour-driven price inflation and herd behaviour. The event is framed as a classic speculative frenzy, bordering on pump-and-dump manipulation, driven more by hype than fundamentals. Row 2: Strategy, Strategic use of market mechanics. Reports note that retail investors used the same tools available to institutional players: tracking short interest, leveraging collective action, and exploiting systemic weaknesses. The movement is presented as rational and informed. Volatility, hype, and risk to market integrity. Reports highlight the casino-like dynamics of Social-Media-driven buying sprees, questioning whether this represented genuine market activity or just meme-fuelled speculation. The term digital Wild West is used to describe a regulatory vacuum exploited by loosely organised online actors. Row 3: Actors, Retail traders are described as clever, strategic, and unexpectedly capable of leveraging complex market mechanisms. Some portray them as tech-savvy Davids fighting institutional Goliaths. Retail traders are depicted as reckless, emotionally unstable, or even criminal. They are called YOLO kids, online mobs, or digital vigilantes driven by hype, greed, or boredom rather than insight. Row 4: Victims, Hedge funds are portrayed as fair targets of strategic counteraction. Some reports note that such exposure is an inherent risk of over-leveraged short positions. Losses are seen as market-correctiNG. Reports focus on late-entry retail investors and institutional actors such as pension funds that may have incurred unexpected losses. The volatility is seen as harming market trust and impacting actors not directly involved in the hype. Row 5: Consequences, Framed as a call for financial inclusion and structural reform. Some commentators propose increased transparency in short interest data and broader access to financial literacy for retail participants. Emphasising the urgency of regulatory responses. Reports cite SEC scrutiny, congressional hearings, and legal investigations. The Reddit case is used to argue for tighter oversight of online financial discourse and social-media-driven trading. Row 6: Conclusion, Power shift on Wall Street. Media frame the event as a symbolic moment in which digital communities temporarily overturned established hierarchies in finance. Headlines refer to a democratisation of trading through collective online action. Flashmob finance and herd behaviour. The event is interpreted as driven by collective irrationality. Commentators warn that digital swarm behaviour bypasses traditional checks and undermines the credibility of market valuation mechanisms.

Open access

Open access