During the Jiading era of the Song Dynasty, the local government in Taizhou encountered a complex problem: a growing accumulation of silk, collected as the summer tax, threatened to decay if stored too long. In response, the court issued a special decree allowing half of the silk tax to be commuted to cash, pushing a tax system originally based on payments in kind towards monetisation.Footnote 1 However, during the Yuan Dynasty, this trend was rapidly reversed, as Mongol rule led to a fiscal reconstruction in Jiangnan. Although they retained the name ‘Two Taxes’ (两税), the Yuan fundamentally altered the Song system’s flexibility, reimposing payment in kind, calculated from the autumn grain tax, and eliminating the monetised mechanisms familiar to the Song.Footnote 2 These contrasting episodes, one a shift to monetisation, the other a reversion to taxation in kind, point to the article’s core question: What drove these fundamental changes in the structure of state finance from the Song to the Yuan Dynasty?

The monetisation during the Song–Yuan period has generated rich academic debate, with scholars offering diverse interpretations of this crucial transition in Chinese economic history. Quan Hansheng laid the early groundwork by identifying the Tang–Song transition as a important moment when the gradual decline of the natural economy gave way to the emergence of the monetary economy. While this observation opened discussions about economic transformation, subsequent scholars have significantly complicated this narrative.Footnote 3 Wu Chengming challenged linear development models by emphasising the cyclical nature of economic change. He argued that financial development has fluctuations and periodicity.Footnote 4 The debate then deepened as scholars examined the driving forces behind monetary transformation. William Guanglin Liu’s research demonstrated how military-fiscal demands shaped monetary development. He argued that monetisation during the Song Dynasty was primarily driven by the financial needs of a growing mercenary system.Footnote 5 This military-fiscal perspective added crucial context to Quan’s observations about the emergence of diverse monetary instruments, including copper coins, gold, silver, and various certificates. Ray Huang Renyu further enriched this discussion by examining how Song officials actively adjusted fiscal policies to promote economic growth and increase fiscal revenue while maintaining strong state control over the monetary system.Footnote 6

While these historians have identified key dynamics in the monetisation process, their debates often remain confined to the empirical question of whether the state or the market is more effective. To move beyond this debate, it is helpful to refer to theoretical perspectives that redefine money not simply as a medium of exchange but as an institution of credit, rules, and state power.

Monetisation was not just a means of settlement but an instrument that reshaped power structures and state–society relations. This article examines how the state’s use of money, beyond its function as a medium of exchange, became a central mechanism for managing taxation, regulating prices, and reconfiguring power. Based on the perspectives of Geoffrey Ingham, Richard von Glahn, Harry A. Miskimin, Jin Xu, and Helen Wang, this article demonstrates that the significance of money extends beyond facilitating trade. For example, Ingham emphasises that money’s role goes beyond its circulation as a physical medium. Societies rely on money to establish units of value, maintain accounts, and clear payments.Footnote 7 To connect this with the historical practice of China, fiscal reforms such as the Two-Tax Reforms of the Song Dynasty institutionalised commuted payments, like ‘folding’ (折變), and fixed quotas in silk or cash, demonstrating how monetary logic was systematically embedded into state finance. Von Glahn further shows that the uses of money were inseparable from the evolution of its forms. The transition from copper coins to paper currency during the Song–Yuan period, along with the shift from in-kind to monetary taxation, marked a transformation driven by institutional design, monetary supply, and market dynamics. These changes were not uniform; differences in the scope and intensity of monetisation between the Song and Yuan highlight a continual renegotiation of state and market relations.Footnote 8 Looking beyond China, Miskimin’s studies of medieval Europe show that money was not only a transactional device but a tool for states to expand fiscal control and administrative centralisation.Footnote 9 Correspondingly, the Song Dynasty’s shanggong 上供 system, with standardised monetary levies such as jingzongzhi money (經總制錢) and zhebo money (折帛錢), shows how the state enhanced its extractive capacity through monetary mechanisms. Bringing a comparative perspective, Xu’s work on Song–Yuan monetisation adds an important point: the success of this process did not depend on the abundance of precious metals. Instead, it relied on the state’s ability to create effective systems of credit and settlement.Footnote 10 In the Southern Song, fiscal operations used coins, paper currency huizi 会子, and silver. This supports Xu’s view that the efficacy of money comes not from its substance but from institutional consensus and regulatory frameworks. To reinforce this logic, Wang’s study of the monetary functions of textiles emphasises the importance of distinguishing between money as a general equivalent and currency as its official form.Footnote 11 This echoes Xu and Ingham’s idea that the essence of money lies in credit and rules, not material substance.

Existing scholarly perspectives demonstrate important aspects of monetisation during the Song and Yuan periods, but they do not fully capture its complexity. I propose a cyclical framework in which monetary expansion and contraction were fundamentally shaped by the interplay of government fiscal policies, market forces, and regional variation. The Song government’s reliance on indirect taxes and monopolies, primarily to fund military ventures, significantly accelerated monetisation. In contrast, the Yuan Dynasty’s more controlled economic policies partially reversed this trend, leading to episodes of demonetisation. This was not simply a shift in currency use but a profound transformation of economic structures with far-reaching consequences. Commercialisation and urbanisation increased demand for advanced monetary tools. Conversely, the Mongol conquest disrupted this dynamic, forcing monetary adaptations that reflected new political realities. My study of places like Taizhou in Zhejiang province shows how local fiscal systems strongly influenced this process, emphasising that examining regional variation simultaneously with broader trends is essential to understanding the whole picture.

I argue that monetisation during the Song and Yuan dynasties followed intricate cycles. The Song period saw monetary expansion; whereas the Yuan’s policies led to a contraction and demonetisation of certain currencies, effectively reversing earlier trends. These alternating phases of financial growth and retrenchment closely tracked shifts in fiscal structures. This framework questions linear models of economic development. It demonstrates the cyclical interplay between continuity and change in medieval China’s economic transformations.

A tax system based on assets during the Song Dynasty

In the development process of various asset evaluations, the tax system had undergone a long period of evolution. For example, the ‘Two-Tax Law’ (兩稅法), implemented in the first year of the Jianzhong period in the Tang Dynasty (780), consolidated the previously complex tax types into land tax and household tax, resulting in a revised taxation system. Building on this foundation, the Southern Song Dynasty established a comprehensive tax levy system, which took into account the production capacity and property ownership of taxpayers.Footnote 12

According to the research of Sibo Yoshinobu and Umehara Yu, the taxation standards of the Two-Tax Law in the Song Dynasty include:Footnote 13

a. Field

b. Property or tax money

c. Seed

d. Number of mulberry trees planted in the mulberry zone

e. Cattle (a household farming capacity)

f. Rental income

g. Family property

These criteria were assessed at the county level, with the household serving as the basic unit of taxation, and household property, such as landholdings and movable (‘floating’) assets, constituting the primary objects of assessment.

However, actual implementation is complex. Officials must evaluate agricultural income and total assets across tens of millions of households. Factors such as hidden property, officials’ corruption, and changes in land ownership complicate the registration process. These issues make accurate registration and the prevention of tax evasion challenging.Footnote 14 For these reasons, Chen Qiqing from Linhai, Taizhou, editor of Chicheng zhi 赤城志, pointed out:

Tax burdens should reflect the land’s productive capacity and yield. Yet the registers contain no trace of actual fields or acreage. Instead, they record only the ‘strength of resources’ [wuli 物力], measured abstractly in strings of cash—obscuring, from the outset, the very foundation of taxation. Officials levy taxes based on the wuli registers but collect them according to the two-tax rolls—a system that, in principle, should be aligned. In practice, however, the two have become entirely disconnected from each other. Each year, as new taxation books are compiled, clerks simply copy the figures from prior years, perpetuating old data without any fresh verification.

稅之厚薄, 當視其物力之高下, 當視其產。今田頃畝初不見於簿, 而物力之貫陌, 獨載之簿, 若是則其源既失矣。過割用物力簿, 起催用二稅簿, 二者所當相關, 而今初不相知, 歲遇攢造, 不過以往年陳籍沿襲抄轉而已。Footnote 15

Chen Qiqing stated that the so-called wuli registers should be a record of family wealth, based on each household’s fields and other assets. Because the wuli registers only included the family’s financial records and did not specify the number of acres of land, he suggested to Emperor Ningzong that Taizhou’s taxation registration schedule be updated.

Moreover, despite many problems, Chen Qiqing said that the taxation standard based on assets of each household could be implemented in Taizhou.Footnote 16 At the beginning of the Yuanyou period, Lü Tao said that different counties have different asset assessment methods, which also demonstrates the gradual maturity and diversity of the asset assessment system of the Song Dynasty:

Across the empire’s counties, tax registers reflect local customs, with standards varying widely: some reckon liability by cash payments (in strings), others by land acreage, household wealth, or even the volume of seed grain a plot can hold—each system dividing households into five classes.

天下郡縣所定版籍, 隨其風俗, 各有不同。或以稅錢貫百, 或以地之頃畝, 或以家之積財, 或以田之受種, 立為五等。Footnote 17

The variation in property assessment methods across Song Dynasty prefectures and counties points to a flexible tax system. Its core principle was to base tax on a taxpayer’s capacity and property, using monetary cash to quantify economic differences among households. This approach, which considered wealth disparities, allowed for the discretionary use of progressive taxation.Footnote 18 In this context, ‘monetisation’ refers not merely to the circulation of bronze currency but more broadly to the conversion of various forms of tax and corvée obligations, whether in the form of land, labour, or grain into a unified money of account. By the Southern Song period, taxation had become increasingly monetised, which in turn encouraged producers to sell goods on the market in order to obtain cash for tax payments. This monetisation of taxes was closely linked to the dynasty’s expansionary fiscal and monetary policies. Local governments were required to remit currency to the central government in order to finance military recruitment, thereby reinforcing both the expansion of the market economy and the fiscal monetisation of the state.

Monetisation, folding, and Zhu Xi’s debate with Tang Zhongyou

As mentioned above, the collection of land taxes during the Song Dynasty took into account the differences in farmers’ production statuses under the market economy and social stratification. Consequently, the taxpayer’s production capacity and property ownership were assessed as the basis for calculating their tax. Taxes were paid twice, in the summer and autumn. Specifically, the summer tax was levied on silk and cotton, while the autumn tax was imposed on grain. In actual practice, due to the fiscal needs of the government and fluctuations in market prices, it was common for the summer tax to be commuted into payments made in money. This process, known as ‘folding’ (折變), refers to the conversion of tax obligations between commodities and cash at officially assessed rates. The most frequent form of folding was the commutation of silk textiles into copper cash, a conversion that further promoted the development of the monetary economy. Under such circumstances, the ‘string’ (guan 貫, a standardised unit of one string of copper cash) became the unified accounting measure, thereby ensuring consistency in fiscal calculations.Footnote 19 The Song Huiyao 宋会要 records such instances of folding:

Autumn and summer taxes were inflated through the use of contrived categories and illicit conversions. Take silk, for example: one bolt was first ‘folded’ into a set sum of cash—then that cash was ‘folded’ again into a fixed measure of wheat. Cash was valued at double the silk, wheat at double the money, so that one bolt of silk became worth four times its value in grain. What began as silk ended as four times the burden, all through bureaucratic resources.

夏秋稅賦巧立名目, 非法折變。如絹一匹折納錢若干, 錢又折麥若干, 以絹較錢, 錢倍於絹, 以錢較麥, 麥又倍於錢。Footnote 20

Folding was originally adopted as an expedient measure to meet the government’s temporary fiscal needs and to avoid collecting goods of little use. However, it soon evolved into a standard method for the state to unify tax collection. The usual practice was to overvalue the original phisical goods and undervalue the commuted substitute, thereby increasing the actual amount of tax revenue. Therefore, taxpayers who were required to convert their tax obligations into cash often found that the income earned from selling agricultural products at market prices was insufficient to cover the taxes they owed, and this burden was particularly heavy for households with limited surplus income. For example, in the Northern Song, Officer Bao Zheng criticised the folding of the wheat tax in the Jianghuai and Liangzhe regions: in principle, one dou of wheat should have been folded at 34 wen, yet the transport commissioner calculated it at 94 wen—more than double the market purchase price.Footnote 21 Such folding practices became a common mechanism for levying monetary taxes within the Song fiscal system.

For Taizhou, records in the local gazetteers regarding tax collection are minimal. Nevertheless, some information can be gained from the Chunxi period, when Zhu Xi’s six-time impeachment against Tang Zhongyou, the prefect of Taizhou, provides clues that help better understand both the local situation and the disputes in the process of folding.

When Zhu Xi travelled in Taizhou, he found that Prefect Tang Zhongyou was forcing citizens to pay taxes. This led people to flee the region. Zhu Xi sent six consecutive reports to Emperor Xiaozong about Tang Zhongyou’s crimes. These reports reveal details about Taizhou’s fiscal operations during the monetisation process.

In his first report, Zhu Xi recounted that on his way to Taizhou he encountered 47 refugees, supporting the elderly and carrying the young as they struggled along in distress. When he asked why they were leaving, they explained that their prefecture had suffered severe drought, yet officials were still asking urgently for tax payments, forcing them to abandon their homes. Further inquiry confirmed that Tang Zhongyou, the Taizhou prefect responsible for tax collection, had indeed been harsh and excessive.Footnote 22

Regarding Tang Zhongyou’s urgency to tax the county charges, Zhu Xi wrote the second report to impeach him:

During my inspection tour in Tiantai County, local households intercepted me to present grievances. They stated that the county’s summer tax quota was over 12,000 bolts of silk and 36,000 strings of cash; by the end of the sixth month, more than 5,500 bolts of silk and 24,000 strings of cash had already been paid under harsh demands. Prefect Tang Zhongyou expressed anger that County Magistrate Zhao Gongzhi was too slow in tax collection and summoned Zhao back to the prefecture. The county people, fearing his removal, blocked the road and pleaded for Zhao’s return, offering to pay the arrears quickly in exchange. Tang Zhongyou then issued direct orders for accelerated collections, disregarding procedures and recent directives, demanding all payments by the end of the sixth month.

今巡歷到本州天台縣, 據人戶遮道陳訴, 本縣夏稅絹一萬二千余匹, 錢三萬六千余貫, 緣本州催促嚴峻, 六月下旬已納絹五千五百余匹, 錢二萬四千余貫。而守臣唐仲友嗔恠知縣趙公植催理遲緩, 差人下縣追請赴州。縣人聞之, 相與號泣, 遮欄公植回縣, 情願各催戶下所欠零稅絹二千五百匹, 限十日內赴州送納, 方得放免。仲友遂專牒縣尉康及祖催納零欠, 更不照應三限條法及近日累降指揮, 牒內明言要在六月終以前一切數足。Footnote 23

Zhu Xi’s case to impeach Tang Zhongyou centred on issues related to tax collection. He found that while Tiantai County was supposed to pay the summer tax in silk and copper coins by 30 August, Tang Zhongyou forced households to pay 5,500 bolts of silk and 24,000 guan of copper coins early, in late June, to comply with the Ministry of Households’ deadline. Later, when Zhao Gongzhi, the magistrate of Tiantai County, delayed the next round of tax collection, Tang Zhongyou sent a messenger to the prefecture demanding that the local people pay another 2,500 bolts of silk within ten days. At the same time, according to the report, Tang Zhongyou instructed Tiantai County’s chief secretary, Zhang Bowen, along with officials Zheng Chun and Jiang Yun, to collect taxes from the fifth-class households in Ninghai County. These actions overwhelmed the people of Tiantai County.Footnote 24

Zhu Xi’s two reports sharply criticise Tang Zhongyou’s approach to taxation, showing a fundamental disagreement. Zhu Xi opposed Tang’s push for early tax payments, arguing that such actions neglected the people’s hardships, especially during severe droughts that left Taizhou unable to muster resources. Zhu Xi appealed to the imperial court to punish Tang for these practices. Despite the scarcity, Tang Zhongyou and other local officials pressed for urgent tax collection, converted grain taxes to cash, and required payment in copper coins or silk, driving many residents to flee.

In fact, before Zhu Xi’s impeachment, Tang Zhongyou had written an article stating that taxes should be paid on time and that fiscal and political affairs are inseparable. In his article, Tang Zhongyou presented taxation as the core of local finance. In contrast to Zhu Xi’s critique of Tang’s policies, Tang focused on maximising fiscal revenue. He required the timely payment of summer and autumn taxes, enforced household-based tax collection, and strictly punished officials who delayed registrations or allowed omissions in household registers.Footnote 25 Zhu Xi, however, advocated greater leniency; he believed taxes should sometimes be deferred or exempted and opposed placing excessive burdens on the people.

To be more specific, the issue of the household tax collected by Tang Zhongyou, which Zhu Xi opposed, primarily centred on the discussion of whether to tax fifth-class households. In the Song Dynasty, households were categorised into five classes based on their wealth and property. In Taizhou, first-class households had to pay 2,535 bolts of silk and 28,914 taels of cotton, second- and third-class households had to pay 11,112 bolts of silk, and fourth-class households had to pay 11,434 bolts of silk.Footnote 26 Fifth-class households had to pay a total of 28,700 guan of copper coins in shending 身丁 tax, with half rendered in kind as silk, amounting to 16,590 bolts, and the other half paid in cash, totalling 14,035 guan of copper coins. In the ninth year of the Chunxi period (1182), Zhu Xi discussed whether the shending tax collected by Tang Zhongyou from the fifth-class households should be exempted:

When I inspected Taizhou, I found that each registered adult male was required to pay a salt tax of 141 wen, commuted into seven bolts of silk. Since the third year of Shaoxing (1133), fifth-class households have been allowed to commute half the levy: three-and-a-half bolts of silk are paid in kind, and 70 wen and five fen are paid in money. This reduced the silk available for official expenditures, resulting in shortages. In 1134, the prefecture addressed the deficit by allocating government funds to purchase silk and reported it to the court. An imperial edict required officials to give cash to taxpayers and collect the full amount of silk, which would then be sold. The edict also forbade extra charges or disturbances. However, from 1134 onwards, officials instead required fifth-class households to convert the cash portion back to silk, demanding three-and-a-half additional bolts per person. Registers show 199,084 fifth-class adult males owing 28,700 strings and 844 wen; half was to be paid in cash (14,035 strings and 422 wen), but all was demanded in silk, totalling over 16,590 bolts. This prompted many complaints. If half of the silk was remitted, taxpayers should pay 7,018 strings and 211 wen in money. The prefecture already sets aside a surplus of more than 16,200 bolts annually, sufficient for soldiers and expenses, and the tribute quotas to the capital remain unaffected.

臣巡歷至台州… 台州人戶身丁每丁供鹽稅錢一百四十一文足, 折納絹七尺。自紹興三年, 首正將第五等人戶丁鹽錢除一半折納絹三尺五寸外, 有一半折納見錢七十文足五分, 計減退本色絹數, 是致缺少絹帛支遣, 本州於紹興四年相度, 貼支官錢湊納, 具申朝廷, 獲奉聖旨, 令台州樁管見錢與人戶, 納到數目, 依市價賣發, 不得科敷騷擾。本州自紹興四年以後, 卻將第五等人戶合納一半丁錢七十文五分足, 紐納絹三尺五寸。照得第五等人戶計一十九萬九千八十四丁, 合納丁鹽錢二萬八千七百貫八百四十四文, 除一半納本色外, 有一半止合納丁錢一萬四千三十五貫四百二十二文足。本州卻將上件丁錢紐作本色絹三尺五寸催納, 計絹一萬六千五百九十匹一丈二尺, 以致人戶陳理, 今來若放免一半丁絹, 卻合催納一半丁錢一萬四千三十五貫四百二十二文足, 其所免上件丁絹, 本州逐年自有支用, 趲剩紬絹一萬六千二百餘匹, 可以通那充官兵等支遣, 不礙起發上供綱運之數。Footnote 27

In the article, Zhu Xi traced the development and evolution of the Taizhou shending tax. Initially, under the Northern Song government’s policy to encourage silk production, Taizhou’s shending tax was set at seven bolts of silk. With the outbreak of war between the Song and Jin in the Southern Song Dynasty, demand for cash and military support grew, leading to a rise in silk prices. In 1129, the third year of the Jianyan period, the court ordered fifth-class households to pay the shending tax in half silk and half copper coins. By 1133, the start of the third year of the Shaoxing period, the imperial court required the Taizhou government to collect 70 wen of cash from fifth-class households as half of the shending tax, while the silk portion became the responsibility of the state and county governments. This left county governments lacking silk, so they had to purchase it from the market to deliver to the court. After the fourth year of the Shaoxing period (1134), this policy changed. Local prefectures and counties stopped offering this discount and began requiring fifth-class people to pay half the shending tax, equivalent to 70 wen, and 3 feet 5 inches of silk. At that time, 199,084 people paid a total of 28,700 guan of copper coins; households paid about half in silk and half in coins, totalling roughly 14,035 guan each. Since Taizhou had over 270,000 males, with 199,084 in the fifth class, this group comprised 70 per cent of the total male population and made up most of those participating in Taizhou’s monetisation process due to the cash discount policy. In 1182, the ninth year of the Chunxi period, the Southern Song war eased, and Zhu Xi visited Taizhou during a drought and famine. He oversaw tax exemptions, proposing a return to the Jianyan (1129) and Shaoxing (1133) policies: the shending tax should be discounted by half, with fifth-class households paying only half the amount in copper coins and being exempt from the silk portion (see Table 1).

Tax payments by fifth-class households (1133–1182)

Source: Zhu Xi, Hui’an xiansheng Zhu Wengong wenji, juan 17, p. 1263, ‘Zou Taizhou mian na ding juan zhuang’.

Zhu Xi’s concern extended beyond reducing the tax burden to ensuring fairness, advocating that tax assessments be based on households’ financial capacity. His complaint to the court ultimately contributed to a broader movement for tax exemptions that spread across the empire. In 1186, the thirteenth year of Chunxi, Emperor Xiaozong waived the shending tax for the fifth class.Footnote 28 In 1205, the first year of the Kaixi period, Emperor Ningzong further reduced and waived the shending tax and ultimately merged it into the field tax,Footnote 29 a reform that preserved the government’s monetary revenue while easing the tax burden on households.

The case between Zhu Xi and Tang Zhongyou reflects Taizhou’s process of monetisation during the Southern Song Dynasty. However, this transformation did not occur overnight. The method of ‘people paying money to prefectures and counties’ was accompanied by the assessment and calculation of family property, which itself was based on a comprehensive consideration of taxpayers’ production capacity. Moreover, as this hierarchical tax system was implemented, local officials held varying views on the policy. As a result, fierce disputes arose. Nevertheless, despite these disputes, the process of monetisation continued to advance. The folding tax practice of Taizhou during the Shaoxing era clearly demonstrates the fiscal logic of monetisation during the Song Dynasty. This system was originally based on silk and cloth as an in-kind tax in Taizhou. Later, these taxes could be converted into copper coins. The government would then purchase silk ‘at market prices’. This not only demonstrates that currency had become the unified standard for accounting and a medium of payment in fiscal operations, it also shows the direct linkage between state finances and market prices. Within this ‘half-in-kind, half-monetary’ institutional arrangement, currency gradually replaced physical goods, propelling the monetisation of the Song Dynasty’s fiscal system.

Shanggong: the centralisation of local monetary revenues

With the gradual implementation of the taxation standard in Taizhou, the process of fiscal monetisation continued to develop through continuous adjustment. This local transformation raises a broader question: In the process of monetisation at the national level, how did the Song government further achieve its purpose of collecting money from local governments? In other words, how was the central government’s demand for monetisation realised locally?

Regarding Taizhou’s local fiscal system, the Chicheng Gazetteer of Jiading records the process of fiscal supply and currency transmission in Taizhou in the Jiading year:

Since the reforms of the Xining era, down to the wars of the Jianyan reign, flames of conflict have been stirred up, and demands for provisions and transport have become endless. The people can no longer endure, and the state itself is unable to support them. Although in more recent times, peace with the northern tribes has brought some temporary remissions, the long-established quotas and entrenched levies can hardly be lightened all at once. The people deliver their taxes to the prefectures and counties, which then offer them to the court. Now, since what is delivered to the court has not been reduced, how can what is delivered to the prefectures and counties be lessened?

自熙寧變法, 至建炎用兵, 洪焰所掀, 供億無藝, 民則不競, 而上亦莫之支焉。蓋自近世和戎, 始時有蠲弛, 而宿窠痼額, 固未易以驟輕之也。民輸州縣, 州縣輸朝廷, 今輸朝廷者既不輕, 則輸州縣者亦安得而省耶?Footnote 30

The Song government established local financial institutions, including the Transshipment Division, the Criminal Division, and the Judicial Division, and recorded an item called shanggong in the financial revenue records. Shanggong was an essential part of the national economic system in the Song Dynasty.Footnote 31 Generally speaking, it refers to the financial revenue paid by the local government to the central government, and each county had a prescribed amount that they had to pay. In the Southern Song Dynasty, shanggong was divided into ‘official money’ and ‘supply money’, which were used to cover the central economic expenses.Footnote 32

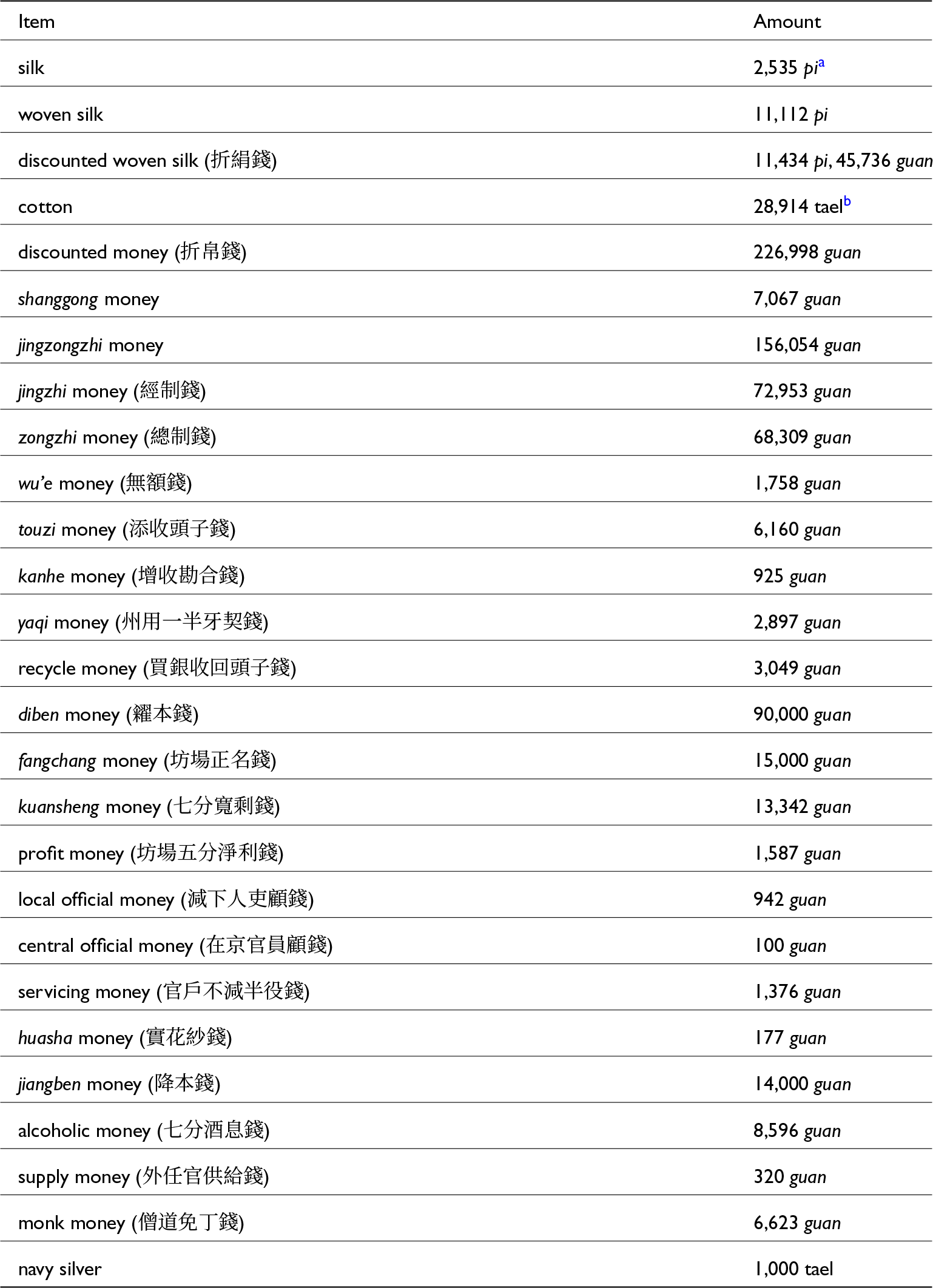

The items of shanggong given in the Chicheng Gazetteer of Jiading include silk, cotton, jingzongzhi money, zhebo money, and many other items. As shown in Table 2, shanggong in the Chicheng Gazetteer of Jiading refers to the financial contributions paid from Taizhou to the Southern Song government. This is the most critical part of Taizhou’s financial revenue, indicating the development of monetisation during the Southern Song Dynasty.

The records of shanggong in the Gazetteer of Taizhou

Notes:

a In the Tang and Song monetary system, silk textiles circulated with copper cash, forming a dual standard often described as a ‘cash-and-cloth’ (錢帛本位) system. Within this framework, the pi 匹 was the primary unit for measuring silk, commonly used to account for high-grade textiles such as silk (絹), fine silk (缣), damask (綾), and gauze (羅). A single pi typically measured four zhang 丈, or about 13 metres, representing a standard-width piece of silk cloth. In official documents, pi frequently appeared with other units such as duan 端, which generally referred to cloth measuring six zhang, but in practice pi was by far the most widely used unit. See Peng Xinwei, Zhongguo huobi shi, pp. 374–376. bIn the system of weights and measures in ancient China, the tael (liang 两) was originally a unit of weight and gradually became the primary unit for measuring precious metals, particularly silver. Its origins can be traced back to early weight systems based on grains of millet, which gradually evolved through the progression of ‘zhu—tael—jin’ to become established. After the Han Dynasty, the tael became an official state standard used for weighing metals such as copper and iron, and more extensively for measuring silver. With the commercial and fiscal development during the Song and Yuan dynasties, silver gradually replaced copper coins as the main form of currency for large transactions and tax payments, and the tael evolved from a mere unit of weight into a monetary unit. Typically, one jin was equivalent to sixteen taels, making one tael approximately equivalent to over 30 grams. In the taxation, trade, and official accounting of the Ming and Qing dynasties, silver was uniformly calculated using the tael as the basic unit. See Peng, Zhongguo huobi shi, pp. 89–90. Source: Chicheng zhi (Jiading), juan 16, p. 546.

The method of monetising land tax in the Southern Song Dynasty involved the government continuously increasing various kinds of surcharges and then integrating them under the summer tax. Take the summer tax category in the shanggong in Table 3, for example.

The summer tax records in the Gazetteer of Taizhou

Source: Chicheng zhi (Jiading), juan 16, p. 546.

The Southern Song government implemented a complex and flexible tax levy system based on assessing and calculating family property. In Table 3, silk, zhebo money, and cotton are listed under the summer tax item. Among the categories of taxes, currency taxes accounted for a considerable proportion. As shown in Table 3, the sum of zhebo money and shanggong money totalled more than 279,801 guan. Under such circumstances, the Taizhou people participated in monetised market operations to meet the tax payment requirements.

Take the monetised zhebo money as an example; in the Gazetteer of Huangyan, it records that zhebo money evolved from hemai 和買, which was also known as heyu mai 和預買. During the reign of Song Taizong, the central government adopted an advance-purchase system whereby it paid cash in advance to poor households to secure silk, which households were required to deliver later when remitting their land tax and summer tax. Later, in the third year of the Chongning period (1104), a change in the currency law caused hemai to become the surcharge for the land tax and summer tax, which were included in the shanggong.Footnote 33

Subsequently, in the third year of the Jianyan period (1129), a period marked by tight warfare, officer Wang Cong wrote:

Previously, I requested that each prefecture this year deliver the required shanggong hemai summer tax in silk, totalling 1,177,804 bolts. Households are to commute each bolt at the fixed price of two strings of cash, amounting to a total of 3,059,228 strings and 110 wen. Since the proposed price is indeed a fair median, it is difficult to either increase or reduce it. Now the deadline for collecting the hemai summer-tax cloth is closing. If an order were promptly issued to the prefectures and counties, then the funds could be collected on schedule, thereby yielding ready cash to assist state expenditures.

昨乞將本路逐州今年合發上供和買夏稅綢絹, 共計一百一十七萬七千八百四匹, 令人戶每匹折納價錢二貫文足, 計三百五萬九千二百二十八貫一百一十文省。未承回降指揮。緣上件價錢委是酌中, 難以增減, 今來和買夏稅物帛, 起催條限逼近, 若前期行下州縣即可如期, 便得見錢, 仰助國用。Footnote 34

The central government required Zhejiang Prefecture to convert 1,177,804 bolts of silk into cash. Each bolt was valued at two full guan; the report above lists a total of 3,059,208 guan calculated in accounting currency. The households were required to pay the tax, which the court referred to as zhebo money. The practice of zhebo, which transformed silk into a form of currency tax, was a typical form of folding practice and a manifestation of monetisation. The government needed currency to cover state and military costs, not to reserve physical silk. Consequently, while the nominal levy form remained on silk, the actual fiscal operations revolved around currency, demonstrating its reliance on monetary income.

In the first year of the Shaoxing period (1131), the minister of household Meng Geng said:

I request that, in the first year of the Shaoxing period (1131), the two Zhe circuits jointly deliver the summer-tax hemai silk, which, after deductions for exemptions and tribute, amounts to a total of 1,064,050 bolts in cloth. In accordance with precedent, half shall be commuted into cash at the rate of two strings of cash per bolt.

乞將紹興元年兩浙合發夏稅和買綢絹, 除減免並進奉外, 綢絹本色共一百六萬四千五十匹, 並一半依例折納價錢, 每匹兩貫文足。Footnote 35

It is evident that by 1131 half of the summer tax and hemai levy items had been commuted into monetary payments through zhebo 折帛 tax,Footnote 36 which refers to an administrative price-folding mechanism. It entailed converting taxes in kind, such as silk, cloth, and grain, into the cash accounting unit of copper cash strings (贯). Officials could then demand settlement in copper coin, paper money, or silver, based on the state treasury’s needs and local conditions.Footnote 37 In the thirteenth year of the Jiading period (1220), zhebo money became one of the official fixed currency tax categories in Taizhou.

However, as a representative of the Elite Eastern Zhejiang School (浙东学派), Ye Shi criticised the implementation of the zhebo tax:

What is meant by the zhebo? In earlier times, there were already many abuses, but none has become more grievous than this practice. Owing to military campaigns, the price of silk rose sharply, while the court itself faced financial shortages. At that time, fiscal officials first devised the system of folding, arguing that it would ‘ease the people while benefiting the state’. Yet once the price of silk had stabilised, the money that the people paid in zhebo tax was three times the value of the actual silk.

何謂折帛之患? 支移折變, 昔者之弊事固多矣, 而今莫甚於折帛。折帛之始, 以兵興絹價大踴, 至十余千, 而朝廷又方乏用, 於是計臣始創為折帛。其說曰「寬民而利公」。其後絹價既平, 而民之所納折帛錢乃三倍於本色。Footnote 38

During the Song Dynasty, when the imperial court faced a problem of insufficient revenue, people were required to pay monetised zhebo money instead of physical silk. However, when the situation improved, people still had to pay the zhebo money. Since the zhebo money tax was calculated in this way, its amount was equivalent to three times the original physical silk price. Therefore, Ye Shi believed that the expropriation of zhebo money had increased the burden of the people. During the Jiading period, the amount of zhebo money contributed by Taizhou reached as much as 226,998 guan, which became a substantial monetary income for the court. The utilisation of zhebo demonstrates that monetisation in the Song was not merely a spontaneous economic evolution but an institutional transformation driven by state fiscal needs. In this process, money functioned as a unit of account, standardising tax assessments and, at the same time, triggering tension in society.

In addition to the zhebo money mentioned above, which became a significant source of monetised income in Taizhou,Footnote 39 jingzongzhi tax also became another important source of monetary income in Taizhou. Such a levy was an expedient measure adopted by the Southern Song government to solve the problem of war and military expenditure.Footnote 40

In the items of shanggong in the Gazetteer of Taizhou, jingzongzhi tax is given as 156,054 strings:

The total amount of jingzongzhi money came to 156,054 strings and 344 wen. This was raised from the prefectural and county wine tax, the two main taxes, and allocations from brokerage-contract fees, and was assigned under the quota of 206,236 strings and 176 wen. Of this, 19,500 strings were entirely deposited into the Fengchu granary and the government grain market. The remaining 136,054 strings and 344 wen were converted half into silver and submitted to the Left Treasury.

經總制錢一十五萬六千五十四貫三百四十四文。以本州與諸縣酒稅及二稅分撥頭合併牙契等錢起發, 下項窠名, 祖額二十萬六千二百三十六貫一百七十六文……實發上件內一萬九千五百貫文, 全會撥充, 降本錢納豐儲倉和糴場, 其余一十三萬六千五十四貫三百四十四文, 銀會中半, 納左藏庫。Footnote 41

The jingzongzhi tax is a collective term for several types of local tax revenues paid to the central government. In Taizhou, the components of the jingzongzhi money included the summer and autumn tax, which was levied on agricultural output; the land tax, based on landholdings; and the alcohol tax, applied to the production or sale of alcohol. The monetary collection of the jingzongzhi tax indicates that state finance in the Song Dynasty was already based on a comprehensive monetary accounting system. The fiscal objective was no longer to collect specific quantities of goods in kind, such as grain or silk. Instead, the state used currency as both a unit of account and a medium of payment. The data above shows that the total jingzongzhi tax in Taizhou was 206,236 strings and 176 wen. Of the final amount, 19,500 strings were settled entirely using paper currency such as huizi. The remaining 136,054 strings were settled half in silver and half in huizi, and these funds were deposited into the Left Treasury (左藏庫). This indicates that fiscal operations in the Southern Song Dynasty had begun to integrate copper coins, silver, and huizi as means of fiscal payment. The large-scale use of huizi, in particular, marked an advanced stage of fiscal monetisation, relying on state-issued credit-based paper currency. A big portion of the jingzongzhi tax was derived from monetised sources such as the alcohol tax and transaction taxes (牙契), amounting to 206,236 strings and 176 wen. The Song state no longer relied solely on direct levies in kind. Instead, it systematically drew monetary taxes from the growing commodity economy and formalised this process into a permanent fiscal structure.

However, from the Qiandao period to the Jiading period, the total amount of jingzongzhi money decreased from 206,236 guan to 156,054 guan.Footnote 42 This decline in jingzongzhi tax can be attributed to changes in the region’s circumstances. Specifically, the amount of money changed with the easing of the war in the Southern Song Dynasty. According to the Taizhou Gazetteer, jingzongzhi money decreased by more than 9,782 guan in the fourth year of the Qiandao period (1168). In the sixth year of the Chunxi period (1179), it decreased by more than 200 guan. In the ninth year of the Chunxi period (1182), Zhu Xi proposed halving the income tax per household and reducing the total amount of money by 5,267 guan.Footnote 43 Paradoxically, these frequent decreases show the jingzongzhi tax’s origin as a government-imposed tax, created to serve court fiscal requirements. Its subsequent adjustments were fundamentally motivated by state financial needs, demonstrating the state-driven character of this monetisation process.

Building on these prior reforms, in the sixteenth year of the Chunxi period (1189), Emperor Xiaozong announced that he would amend the jingzongzhi tax to reduce the burden on the people,Footnote 44 nevertheless, these monetised taxes—the jingzongzhi tax, yuezhuang tax (月樁錢), and dibeng tax (糴本錢)—still constituted a substantial portion of total fiscal revenue.

Through the ongoing changes in the amounts of the jingzongzhi money in the fourth year of the Qiandao period (1168), the sixth year of the Chunxi period (1179), the ninth year of the Chunxi period (1182), the sixteenth year of the Chunxi period (1189), and the first year of the Kaixi period (1205), the total amount changed from 206,236 guan to 156,054 guan.Footnote 45 Except for 19,500 guan used for storage, the rest of the jingzongzhi money was handed over to the central government in the form of silver and paper money,Footnote 46 totalling 136,054 guan. Although the amount of jingzongzhi money has varied over years, it has always been a fixed monetary tax category of the government.Footnote 47

In the Gazetteer of Taizhou, the records of the taxation refer to the financial contributions paid from the Taizhou prefecture to the Southern Song government, which demonstrated the imperial court’s substantial financial demands. However, Chen Qiqing wrote to Emperor Ningzong to express his views on the issue of monetisation:

I humbly reflect on the methods of taxation and levies. Grain and silk are what the people actually possess, while money is what they do not have, but the government instead compels them to pay in cash … Beyond the regular tax money, there are additional charges, such as head money, money for substitute drafts, as well as various fees, including transportation surcharges.

臣竊惟今日科斂之法, 大概極矣。而極之中又有輕重焉。夫粟帛者, 民之所有也, 錢者, 民之所無也, 民合輸粟與帛, 而官俾之輸錢……正錢之外, 有頭錢, 有代鈔發納錢, 有綱腳暗腳等錢。Footnote 48

Chen Qiqing pointed out that, in the process of monetisation, households were supposed to pay with grain and silk but the government forced them to use money instead. In addition to regular taxes, ordinary people also had to pay extra taxes, so they often had to sell their products in the market to obtain cash, a process that inadvertently advanced the process of monetisation. Yet this shift also generated numerous problems. Officials found opportunities to profit during tax collection by imposing a variety of additional charges—such as head money, fees for substitute drafts, and various surcharges for transportation and other expenses. These levies all revolved around ‘money’ as the object of collection. Under a system of in-kind taxation, there were certainly losses and transport costs, but the procedures were comparatively straightforward. In the monetised system, however, the process of tax collection became far more complex.

In sum, the above discussion highlights the complex facets of ‘monetisation’. The Song Dynasty fiscal system used copper cash strings (贯) as its unit of account. Through ‘folding’, corvee obligations and in-kind taxes, such as silk, cloth, and grain, were converted into monetary values. Several monetised tax items existed, including zhejuan, zhebo, shanggong, and jingzongzhi money. Ordinary people were allowed to fulfill these obligations through various exchange media, including copper coins, paper money (huizi), and silver. Thus, although accounts were kept in ‘strings’, actual collections often used silver or huizi. As noted in the Gazetteer of Taizhou, ‘The jingzongzhi money, 136,054 strings, was to be paid half in silver, half in huizi, and deposited in the Left Treasury’,Footnote 49 clearly demonstrating this practice. Therefore, on the one hand, monetisation refers to the unified accounting in ‘strings’, and on the other, it involves the conversion of in-kind taxes and corvée into payments in multiple types of currency.

As Chen Qingqing observed, the four prefectures of Taizhou, Xinzhou, Jianchang, and Shaowu needed to submit up to 15,600 taels of silver.Footnote 50 This policy ensured government revenues and brought the people into a market-based system. Regarding the Southern Song court’s overall fiscal revenue, Ye Shi conducted an investigation during the Chunxi reign period, stating: ‘Today, the wealth of the empire, that which is in terms of coin strings—tea, salt, and monopoly goods—accounts for 24 million; the jingzongzhi money accounts for 15 million; shanggong, hemai, and zhebo account for over 10 million.’Footnote 51 Ye Shi’s narrative illustrates the formation of a money-centric fiscal state in the Southern Song, which was closely tied to commerce and monetary circulation. The core of central revenue depended not on land taxes but on massive monetary taxes: at least 25 million strings came from cash-specific taxes, such as the jingzongzhi money and zhebo money, which, with monopoly revenues, formed the empire’s financial core.

Thus, from a national financial perspective, the Song government’s significant demand for currency can be viewed as an expansion, including the establishment of taxation standards, the implementation of monetisation, and the formation of monetised forms, all of which reflect the development of the national monetised economy.

A demonetising turn centred on the autumn grain during the Yuan Dynasty

Between the Song and Yuan dynasties, southern China experienced disruption. After the establishment of the Yuan government, the financial structure underwent significant changes. The Yuan government did not inherit the summer tax system of the Southern Song; instead, they calculated the summer tax according to the proportion of the autumn tax, which is known as the ‘Jiangnan’ summer tax (江南夏税). That being said, in the Yuan Dynasty, the method of collecting the summer tax was primarily based on the autumn grain levy and no longer calculated according to the diversified income sources of households through assessments of family property. The various supplementary summer taxes of the Song Dynasty, such as the zhebo money, also disappeared. This marked the establishment of a two-tax system centred on autumn grain and characterised by demonetisation. Thus, compared with the Song Dynasty, the basis of taxation in Taizhou during the Yuan Dynasty had already undergone a great transformation. Take the taxation data of Xianju County as an example:

The summer tax amounted to a total of 186 ding, 30 tael, and 5 qian in Zhongtong paper currency, together with 7,676 dan, 9 dou, 4 sheng, and 3 he of autumn grain.

夏稅共中統鈔一百八十六錠三十兩五錢秋米七千六百七十六石九斗四升三合。Footnote 52

From the information above, the autumn tax yield during the Zhida period of the Yuan Dynasty was 7,676 dan, and the summer tax was more than 186 dian. According to the unified taxation principles for the Jiangnan region in the Yuan Dynasty:

The amount to be paid was determined in proportion to the grain. For each dan of grain, one might pay three strings of paper currency, or two strings, or one string, or one string and 500 wen, or one string and 700 wen. Those who paid three strings included such circuits as Wuzhou 婺州 in Jiangzhe and Longxing 龍興 in Jiangxi. Those who paid two strings included the five circuits of Quanzhou 泉州 in Fujian. Those who paid one string and 500 wen included such circuits as Shaoxing 紹興 in Jiangzhe and Zhangzhou 漳州 in Fujian.

其所輸之數, 視糧以為差。糧一石或輸鈔三貫、二貫、一貫, 或一貫五百文、一貫七百文。輸三貫者, 若江浙省婺州等路、江西省龍興等路 是已。輸二貫者, 若福建省泉州等五路是已。輸一貫五百文者, 若江浙省紹興 路、福建省漳州等五路是已。

It shows that although paper currency was still formally collected in Jiangnan, including Taizhou, the summer tax had already been linked to physical grain, with a fixed folding rate based on grain as the unit (視糧以為差). As for the autumn tax in Taizhou shown above, it was already entirely collected in kind as grain. This process of folding using physical goods as the value standard reflects the loss of monetary function in Yuan Dynasty taxation. The establishment of a demonetised tax system, centred on the grain in Taizhou during the Yuan Dynasty, meant that the practice of calculating taxes based on family property had been discontinued.

The decline in the share of monetary taxation

Regarding the taxes paid by the Taizhou government to the imperial court, the Gazetteer of Taizhou did not have a system of shanggong during the Yuan Dynasty. Instead, the taxation of Taizhou is classified into summer and autumn taxes, as well as miscellaneous taxes. The Gazetteer of Taizhou recorded Taizhou tax revenue from the 27th year of the Zhiyuan period (1290):

The summer tax amounted to 2,991 ding, 19 tael, 2 qian, 1 fen, and 3 li in Zhongtong paper currency. The autumn grain totalled 70,340 dan, 9 dou, 1 sheng, and 8 he. Of this, the principal grain (正米) was 66,112 dan, 5 dou, 7 sheng, and 5 he, while the deducted grain (耗米) came to 4,212 dan, 5 dou, 7 sheng, and 5 he.

夏稅中統鈔二千九伯九十一錠一十九兩二錢一分三釐, 秋糧七萬三百四十石九斗一升八合, 正米六萬六千一百一十二石五斗七升五合, 耗米四千二百一十二石五斗七升五合。Footnote 53

According to the above information, when the tax was collected in Taizhou during the Yuan Dynasty, the summer tax totalled more than 2,991 dian of paper money, equivalent to 149,569 guan, and the autumn tax amounted to more than 70,340 dan of rice. According to the price of rice in the coastal area of Zhejiang, 10 guan of Zhongtong paper money could buy 1 dan of rice, and according to Japanese scholar Yuki Sugimura’s research, the price of 1 dan of rice in eastern Zhejiang during the mid Yuan Dynasty was approximately 20 guan of paper money. Therefore, according to the ratio of 10 to 20, 149,569 guan of Zhongtong paper money could buy about 7,478–14,957 dan of grains. This is equivalent to 10–21 per cent of the 70,340 dan of autumn rice. It shows that the proportion of monetised tax was much lower than that of the physical tax.

Here is the data from Xianju County:

The summer tax amounted to a total of 186 ding, 30 tael, and 5 qian in Zhongtong paper currency, while the autumn grain came to 7,676 dan, 9 dou, 4 sheng, and 3 he.

夏稅共中統鈔一百八十六錠三十兩五錢,秋米七千六百七十六石九斗四升三合。Footnote 54

This indicates that the summer tax on Zhongtong paper money during the Zhida period was 186 dian, equivalent to 9,330 guan. According to the above-mentioned ratio in the Zhedong region, where 10–20 strings of cash could purchase 1 dan of grain, 9,330 guan of Zhongtong paper money was equivalent to 467–933 dan of grain, which was comparable to 6–12 per cent of the 7,676 dan of autumn rice. This shows that Xianju County’s monetised summer tax accounts for a negligible proportion of the total tax revenue compared to the autumn grain tax.

These were the taxes in Huangyan County in the fourth year of the Zhida period (1311):

The summer tax amounted to 1,486 ding, 24 tael, 7 qian, 4 fen, and 6 li in Zhongtong paper currency, while the autumn grain came to 36,996 dan, 5 dou, 8 sheng, and 1 he of rice.

夏稅中統鈔一千四百八十六錠二十四兩七錢四分六釐,秋糧米三萬六千九百九十六石五斗八升一合。Footnote 55

According to the information above, it is evident that Zhongtong paper money was collected in Huangyan County during the Yuan Dynasty. The summer tax was 1,486 dian and the autumn tax was 36,996 dan, of which the summer tax was equivalent to 74,324 guan and 3,716–7,432 dan of grain during the Zhida period. The summer tax was equivalent to 10–20 per cent of the 70,340 dan of autumn grain. It shows that the proportion of monetised taxes in Huangyan County was far lower than that of the autumn tax.

According to the data from the Taizhou prefectures and counties above, it is evident that the proportion of monetised taxes in Taizhou during the Yuan Dynasty declined significantly compared to during the Song Dynasty. The monetised tax was relatively simple during the Yuan Dynasty because the autumn tax in kind was the primary tax category collected at that time. This indicates that the government’s demand for various types of monetised taxes was relatively low.

At the same time, the taxes of hemai and zhebo money were also converted into a physical tax category during the Yuan Dynasty:

During the Yuan Dynasty, the hemai system had no fixed prices. When the government needed to make a purchase, it paid the value directly with the goods. The people found this system beneficial.

元時和買無定價, 但欲買時, 對物支直, 民便之。

Compared with the Southern Song Dynasty, the taxation of the Yuan Dynasty showed a significant trend of demonetisation.Footnote 56 With regard to the tax system and the monetisation process, Taizhou’s taxation in the Southern Song Dynasty evolved by adding various surcharges to the regular summer and autumn taxes. However, in the Yuan Dynasty, the summer and autumn tax collection focused on the autumn tax in kind. The tax system was no longer progressive or based on family property. People did not need to pay as many monetised taxes as in the Song Dynasty; instead, most payments were made with physical goods. Compared with the Song Dynasty, the Yuan Dynasty showed a trend of demonetisation in its tax system.

Conclusion

In summary, compared to the Yuan Dynasty, the Southern Song Dynasty established a comprehensive taxation system that fully considered taxpayers’ production capacity and property status. Its core principle was to quantify taxes monetarily based on the taxpayers’ assets and market activities. The term ‘monetisation’ referred not only to the circulation of copper coins but also broadly meant the use of currency as a unit of measurement and taxation. The Song Dynasty’s fiscal system used the copper coin as the accounting unit, converting land, labour, and taxes in kind, such as silk, cloth, and grain, into monetary value through the practice of ‘folding’. At the time, there were various monetised tax categories, including zhejuan, zhebo, shanggong, and jingzongzhi tax. Ordinary people could fulfill these obligations using various media of exchange, such as copper coins, paper money, and silver. By the Southern Song, the degree of monetisation had deepened, further promoting the vigorous development of a commodity economy. This tax monetisation was closely linked to the Song Dynasty’s expansionary fiscal and monetary policies. Local governments were required to pay currency to the central government and raise funds for military expenses, thereby reinforcing the expansion of the market economy and the monetisation of state finances. In contrast, the Yuan Dynasty’s autumn tax collection was primarily in kind, and its tax system was no longer based on household property and currency. The people were not required to pay large amounts of monetary taxes as they were during the Song Dynasty, with most taxes being paid in kind. The Song Dynasty experienced monetary expansion, while the policies of the Yuan Dynasty led to monetary contraction and the devaluation of currencies, effectively reversing the earlier trend. This fundamental divergence in fiscal policy marks a transformation in Chinese economic history, where the Song Dynasty’s advanced monetary mechanisms were replaced by the Yuan’s more rudimentary and demonetised management.

Conflicts of interest

None.

Open access

Open access