1. Introduction

1.1 Preliminaries

The heavy-tailed distributions accurately describe complicated situations. One of the most important applications is related to the risk theory in actuarial science. Although several one-dimensional problems remain still open, the multidimensional case has gained popularity from both theoretical and practical aspects. Especially, with respect to a practical point of view, the modern insurance industry does not operate with a single portfolio.

On this line, there are some recent papers, as, for example, Hu and Jiang (Reference Hu and Jiang2013), Konstantinides and Li (Reference Konstantinides and Li2016), and Yang and Su (Reference Yang and Su2023). In this direction, we introduce some two-dimensional distribution classes, with heavy tails, that are convenient for calculations and permit direct and consistent generalization of the one-dimensional concepts.

In Subsection 1.2, we remind some basic definitions for one-dimensional heavy-tailed distributions, for easy comparison with the two-dimensional ones. In Section 2, we introduce the closure property with respect to the two-dimensional convolution and the two-dimensional max-sum equivalence. Next, we present some results on these classes of distributions. In Section 3, we estimate the joint-tail asymptotic behavior of two random sums, under a dependence structure that generalizes the tail asymptotic independence, and we establish an asymptotic expression for the ruin probabilities, in a discrete-time two-dimensional risk model without stochastic discount factors. Furthermore in Section 5, we study the closure property of some of new classes with respect to scalar product, and in Section 6, we extended some of our results in Section 4, in the case which we have a common discount factor for the two portfolios. Last but not least, we limited ourselves to the non-negative case, and we study the closure property of new classes with respect to product convolution in two dimensions, and some previous results are extended.

Before passing to the next subsection, we give some notations that we need for the rest of the paper. We denote by

${\overline {F}}\,:\!=\,1-F$

the distribution tail, hence

${\overline {F}}\,:\!=\,1-F$

the distribution tail, hence

${\overline {F}}(x)={\mathbf{P}}[X\gt x]$

and holds

${\overline {F}}(x)={\mathbf{P}}[X\gt x]$

and holds

${\overline {F}}(x)\gt 0$

for any

${\overline {F}}(x)\gt 0$

for any

$x \geq 0$

, except it is referred to differently. For two positive functions

$x \geq 0$

, except it is referred to differently. For two positive functions

$f(x)$

and

$f(x)$

and

$g(x)$

, the asymptotic relation

$g(x)$

, the asymptotic relation

$f(x)=o[g(x)]$

, as

$f(x)=o[g(x)]$

, as

$x\to \infty$

means

$x\to \infty$

means

\begin{eqnarray*} \lim _{x\to \infty }\dfrac {f(x)}{g(x)} = 0, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty }\dfrac {f(x)}{g(x)} = 0, \end{eqnarray*}

the asymptotic relation

$f(x)=O[g(x)]$

, as

$f(x)=O[g(x)]$

, as

$x\to \infty$

holds if

$x\to \infty$

holds if

\begin{eqnarray*} \limsup _{x\to \infty } \dfrac {f(x)}{g(x)} \lt \infty . \end{eqnarray*}

\begin{eqnarray*} \limsup _{x\to \infty } \dfrac {f(x)}{g(x)} \lt \infty . \end{eqnarray*}

and the asymptotic relation

$f(x)\asymp g(x)$

, as

$f(x)\asymp g(x)$

, as

$x\to \infty$

if both

$x\to \infty$

if both

$f(x)=O[g(x)]$

and

$f(x)=O[g(x)]$

and

$g(x)=O[f(x)]$

. Similarly, for the bivariate functions

$g(x)=O[f(x)]$

. Similarly, for the bivariate functions

$f(x,\,y)$

,

$f(x,\,y)$

,

$g(x,\,y)$

, the corresponding asymptotic relations hold with

$g(x,\,y)$

, the corresponding asymptotic relations hold with

$\min \{x,\,y\} \to \infty$

, as, for example,

$\min \{x,\,y\} \to \infty$

, as, for example,

$f(x,\,y) = o[g(x,\,y)]$

, if it holds

$f(x,\,y) = o[g(x,\,y)]$

, if it holds

\begin{eqnarray*} \lim _{x \wedge y \to \infty } \dfrac {f(x,\,y) }{g(x,\,y) }=0. \end{eqnarray*}

\begin{eqnarray*} \lim _{x \wedge y \to \infty } \dfrac {f(x,\,y) }{g(x,\,y) }=0. \end{eqnarray*}

For a real number

$x,y$

, we denote

$x,y$

, we denote

$x^{+}\,:\!=\,\max \{x,0\}$

,

$x^{+}\,:\!=\,\max \{x,0\}$

,

$x\wedge y\,:\!=\,\min \{x,y\}$

,

$x\wedge y\,:\!=\,\min \{x,y\}$

,

$x\vee y\,:\!=\,\max \{x,y\}$

. With bold letters, we denote vectors, and further for the unit and zero vectors, we write

$x\vee y\,:\!=\,\max \{x,y\}$

. With bold letters, we denote vectors, and further for the unit and zero vectors, we write

$\textbf { 1}$

and

$\textbf { 1}$

and

$\textbf { 0}$

, respectively.

$\textbf { 0}$

, respectively.

1.2 One-dimensional heavy-tailed distributions

The following properties are to be extended in two dimensions:

-

(1) For two random variables

$X_1$

,

$X_2$

with distributions

$F_1$

,

$F_2$

, respectively, the distribution of the sum is defined by

$F_{X_1+X_2}(x)={\mathbf{P}}[X_1 + X_2 \leq x]$

with tail

$\overline {F_{X_1+X_2}}(x)={\mathbf{P}}[X_1+X_2 \gt x]$

. If

$X_1$

,

$X_2$

are independent, we write

$F_1*F_2$

instead of

$F_{X_1+X_2}$

.

$X_1$

,

$X_2$

with distributions

$F_1$

,

$F_2$

, respectively, the distribution of the sum is defined by

$F_{X_1+X_2}(x)={\mathbf{P}}[X_1 + X_2 \leq x]$

with tail

$\overline {F_{X_1+X_2}}(x)={\mathbf{P}}[X_1+X_2 \gt x]$

. If

$X_1$

,

$X_2$

are independent, we write

$F_1*F_2$

instead of

$F_{X_1+X_2}$

. -

(2) We say that the random variables

$X_1$

,

$X_2$

or their distributions

$F_1$

,

$F_2$

are max-sum equivalent if

$\overline {F_1*F_2}(x) \sim {\overline {F}}_1(x)+{\overline {F}}_2(x)$

, as

$x\to \infty$

. (In some cases, the max-sum equivalence is extended also to

${\overline {F}}_{X_1+X_2}(x) \sim {\overline {F}}_1(x) + {\overline {F}}_2(x)$

, for weakly dependent random variables

$X_1$

,

$X_2$

).

Now we consider some classes of heavy-tailed distributions. We say that a distribution

$F$

is heavy-tailed, and we write

$F$

is heavy-tailed, and we write

$F \in \mathcal{K}$

, if it holds

$F \in \mathcal{K}$

, if it holds

\begin{eqnarray*} \int _{-\infty }^{\infty } e^{\varepsilon \,x}\,F(dx) = \infty, \end{eqnarray*}

\begin{eqnarray*} \int _{-\infty }^{\infty } e^{\varepsilon \,x}\,F(dx) = \infty, \end{eqnarray*}

for any

$\varepsilon \gt 0$

. A large enough class of heavy-tailed distributions is the class of long tails, denoted by

$\varepsilon \gt 0$

. A large enough class of heavy-tailed distributions is the class of long tails, denoted by

$\mathcal{L}$

. We have

$\mathcal{L}$

. We have

$F \in \mathcal{L}$

if it holds

$F \in \mathcal{L}$

if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(x-a)}{{\overline {F}}(x)}=1, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(x-a)}{{\overline {F}}(x)}=1, \end{eqnarray*}

for any (or, equivalently, for some)

$a\gt 0$

. It is well-known that if

$a\gt 0$

. It is well-known that if

$F \in \mathcal{L}$

, then there exists a function

$F \in \mathcal{L}$

, then there exists a function

$a\;:\;[0,\,\infty ) \longrightarrow [0,\,\infty )$

, such that

$a\;:\;[0,\,\infty ) \longrightarrow [0,\,\infty )$

, such that

$a(x) \rightarrow \infty$

,

$a(x) \rightarrow \infty$

,

${\overline {F}}(x\pm a(x)) \sim {\overline {F}}(x)$

, as

${\overline {F}}(x\pm a(x)) \sim {\overline {F}}(x)$

, as

$x\to \infty$

. This kind of function

$x\to \infty$

. This kind of function

$a(x)$

is called an insensitivity function for

$a(x)$

is called an insensitivity function for

$F$

; see further in Cline and Samorodnitsky (Reference Cline and Samorodnitsky1994), Foss et al. (Reference Foss, Korshunov and Zachary2013), or Konstantinides (Reference Konstantinides2018).

$F$

; see further in Cline and Samorodnitsky (Reference Cline and Samorodnitsky1994), Foss et al. (Reference Foss, Korshunov and Zachary2013), or Konstantinides (Reference Konstantinides2018).

A little smaller class than

$\mathcal{L}$

is the class of subexponential distributions, introduced in Chistyakov (Reference Chistyakov1964). We say that a distribution

$\mathcal{L}$

is the class of subexponential distributions, introduced in Chistyakov (Reference Chistyakov1964). We say that a distribution

$F$

with support on the interval

$F$

with support on the interval

$[0,\,\infty )$

belongs to the class of subexponential distributions, symbolically

$[0,\,\infty )$

belongs to the class of subexponential distributions, symbolically

$F \in \mathcal{S}$

if it holds

$F \in \mathcal{S}$

if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {\overline {F^{n*}}(x)}{{\overline {F}}(x)}=n, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {\overline {F^{n*}}(x)}{{\overline {F}}(x)}=n, \end{eqnarray*}

for any

$n \in {\mathbb{N}}$

, where

$n \in {\mathbb{N}}$

, where

$F^{n*}$

represents the

$F^{n*}$

represents the

$n$

-th order convolution power for

$n$

-th order convolution power for

$F$

. The class

$F$

. The class

$\mathcal{S}$

has found several applications in the risk models, as, for example, in Li et al. (Reference Li, Tang and Wu2010), Geng et al. (Reference Geng, Liu and Wang2023), and Ji et al. (Reference Ji, Wang, Yan and Cheng2023).

$\mathcal{S}$

has found several applications in the risk models, as, for example, in Li et al. (Reference Li, Tang and Wu2010), Geng et al. (Reference Geng, Liu and Wang2023), and Ji et al. (Reference Ji, Wang, Yan and Cheng2023).

We say that the distribution

$F$

belongs to the class of the dominatedly varying distributions, symbolically

$F$

belongs to the class of the dominatedly varying distributions, symbolically

$F \in \mathcal{D}$

, if it holds

$F \in \mathcal{D}$

, if it holds

\begin{eqnarray*} \limsup _{x\to \infty } \dfrac {{\overline {F}}(b\,x)}{{\overline {F}}(x)} \lt \infty, \end{eqnarray*}

\begin{eqnarray*} \limsup _{x\to \infty } \dfrac {{\overline {F}}(b\,x)}{{\overline {F}}(x)} \lt \infty, \end{eqnarray*}

for some (or equivalently, for all)

$b\in (0,\,1)$

. It is well known that

$b\in (0,\,1)$

. It is well known that

$\mathcal{D}\cap \mathcal{L}=\mathcal{D}\cap \mathcal{S} \subset \mathcal{K}$

; see Goldie (Reference Goldie1978,Th. 1).

$\mathcal{D}\cap \mathcal{L}=\mathcal{D}\cap \mathcal{S} \subset \mathcal{K}$

; see Goldie (Reference Goldie1978,Th. 1).

Further, a smaller class of heavy-tailed distributions represents the class of consistently varying distributions, symbolically

$F\in \mathcal{C}$

. We say that

$F\in \mathcal{C}$

. We say that

$F\in \mathcal{C}$

, if it holds

$F\in \mathcal{C}$

, if it holds

\begin{eqnarray*} \lim _{y\uparrow 1}\limsup _{x\to \infty } \dfrac {{\overline {F}}(y\,x)}{{\overline {F}}(x)} =1, \end{eqnarray*}

\begin{eqnarray*} \lim _{y\uparrow 1}\limsup _{x\to \infty } \dfrac {{\overline {F}}(y\,x)}{{\overline {F}}(x)} =1, \end{eqnarray*}

or equivalently

\begin{eqnarray*} \lim _{y\downarrow 1}\liminf _{x\to \infty } \dfrac {{\overline {F}}(y\,x)}{{\overline {F}}(x)} =1. \end{eqnarray*}

\begin{eqnarray*} \lim _{y\downarrow 1}\liminf _{x\to \infty } \dfrac {{\overline {F}}(y\,x)}{{\overline {F}}(x)} =1. \end{eqnarray*}

Finally, we say that a distribution

$F$

belongs to the class of regularly varying distributions, with index

$F$

belongs to the class of regularly varying distributions, with index

$\alpha \gt 0$

, symbolically

$\alpha \gt 0$

, symbolically

$F \in \mathcal{R}_{-\alpha }$

if it holds

$F \in \mathcal{R}_{-\alpha }$

if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(t\,x)}{{\overline {F}}(x)} =t^{-\alpha }, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(t\,x)}{{\overline {F}}(x)} =t^{-\alpha }, \end{eqnarray*}

for any

$t\gt 0$

.

$t\gt 0$

.

For these classes, we obtain the following inclusions (see Bingham et al., Reference Bingham, Goldie and Teugels1987; Leipus et al., Reference Leipus, Šiaulys and Konstantinides2023):

\begin{eqnarray*} \mathcal{R}\,:\!=\,\bigcup _{\alpha \geq 0} \mathcal{R}_{-\alpha } \subsetneq \mathcal{C} \subsetneq \mathcal{D}\cap \mathcal{L} \subsetneq \mathcal{S} \subsetneq \mathcal{L} \subsetneq \mathcal{K}, \end{eqnarray*}

\begin{eqnarray*} \mathcal{R}\,:\!=\,\bigcup _{\alpha \geq 0} \mathcal{R}_{-\alpha } \subsetneq \mathcal{C} \subsetneq \mathcal{D}\cap \mathcal{L} \subsetneq \mathcal{S} \subsetneq \mathcal{L} \subsetneq \mathcal{K}, \end{eqnarray*}

where

$\mathcal{R}_0$

is the class of slowly varying distributions. We can find numerous classes of heavy-tailed distributions; however, we mentioned the most popular in the literature. In this paper, we extend into two dimensions the classes

$\mathcal{R}_0$

is the class of slowly varying distributions. We can find numerous classes of heavy-tailed distributions; however, we mentioned the most popular in the literature. In this paper, we extend into two dimensions the classes

$ \mathcal{C}$

,

$ \mathcal{C}$

,

$ \mathcal{D}$

, and

$ \mathcal{D}$

, and

$ \mathcal{L}$

.

$ \mathcal{L}$

.

In Cai and Tang (Reference Cai and Tang2004), we find the following results.

Proposition 1.1.

If

$F_1 \in \mathcal{D}$

and

$F_1 \in \mathcal{D}$

and

$F_2 \in \mathcal{D}$

are distributions with support on the interval

$F_2 \in \mathcal{D}$

are distributions with support on the interval

$[0,\,\infty )$

, then

$[0,\,\infty )$

, then

$F_{X_1+X_2} \in \mathcal{D}$

.

$F_{X_1+X_2} \in \mathcal{D}$

.

In Proposition1.1 we find that for non-negative random variables, the class

$\mathcal{D}$

satisfies the closure property with respect to sum. As was mentioned in Cai and Tang (Reference Cai and Tang2004), the class

$\mathcal{D}$

satisfies the closure property with respect to sum. As was mentioned in Cai and Tang (Reference Cai and Tang2004), the class

$\mathcal{D}$

does NOT satisfy the max-sum equivalence, as it follows from the fact that

$\mathcal{D}$

does NOT satisfy the max-sum equivalence, as it follows from the fact that

$\mathcal{D} \not \subset \mathcal{S}$

and

$\mathcal{D} \not \subset \mathcal{S}$

and

$\mathcal{S} \not \subset \mathcal{D}$

; therefore, the relation

$\mathcal{S} \not \subset \mathcal{D}$

; therefore, the relation

$\overline {F^{2*}}(x) \sim 2\,{\overline {F}}(x)$

, as

$\overline {F^{2*}}(x) \sim 2\,{\overline {F}}(x)$

, as

$x\to \infty$

, does NOT hold for

$x\to \infty$

, does NOT hold for

$F\in \mathcal{D} \setminus \mathcal{S}$

. In opposite to the dominated variation, the class of the consistently varying distributions satisfies both these properties.

$F\in \mathcal{D} \setminus \mathcal{S}$

. In opposite to the dominated variation, the class of the consistently varying distributions satisfies both these properties.

Proposition 1.2.

If

$F_1 \in \mathcal{C}$

and

$F_1 \in \mathcal{C}$

and

$F_2 \in \mathcal{C}$

are distributions with support on the interval

$F_2 \in \mathcal{C}$

are distributions with support on the interval

$[0,\,\infty )$

, then it holds

$[0,\,\infty )$

, then it holds

$F_1 * F_2 \in \mathcal{C}$

and

$F_1 * F_2 \in \mathcal{C}$

and

$\overline {F_1* F_2}(x) \sim {\overline {F}}_1(x) + {\overline {F}}_2(x)$

, as

$\overline {F_1* F_2}(x) \sim {\overline {F}}_1(x) + {\overline {F}}_2(x)$

, as

$x\to \infty$

.

$x\to \infty$

.

2. Two-dimensional heavy tails

The reason why the multivariate distributions have been so popular is their ability to describe better multidimensional phenomena. This happens because of the interdependence among the components of the random vectors, which affect significantly the final outcome.

The first heavy-tailed distributions class that was extended to a multidimensional frame is the regular variation. We say that the random vector

$\textbf { X}=(X_1,\,\ldots, \,X_d)$

represents a multivariate regularly varying vector with index

$\textbf { X}=(X_1,\,\ldots, \,X_d)$

represents a multivariate regularly varying vector with index

$\alpha$

and non-degenerate, Radon measure

$\alpha$

and non-degenerate, Radon measure

$\nu$

, symbolically

$\nu$

, symbolically

$\textbf { X} \in MRV(\alpha, \,F,\,\nu )$

if it holds

$\textbf { X} \in MRV(\alpha, \,F,\,\nu )$

if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac 1{{\overline {F}}(x)}{\mathbf{P}}\left [ \dfrac {\textbf { X}}x \in {\mathbb{B}} \right ]=\nu ({\mathbb{B}}), \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac 1{{\overline {F}}(x)}{\mathbf{P}}\left [ \dfrac {\textbf { X}}x \in {\mathbb{B}} \right ]=\nu ({\mathbb{B}}), \end{eqnarray*}

for any

$\nu$

-continuous Borel set

$\nu$

-continuous Borel set

${\mathbb{B}} \subset [0,\,\infty ]^d\setminus \{ \textbf { 0}\}$

, with

${\mathbb{B}} \subset [0,\,\infty ]^d\setminus \{ \textbf { 0}\}$

, with

$F \in \mathcal{R}_{-\alpha }$

. The measure

$F \in \mathcal{R}_{-\alpha }$

. The measure

$\nu$

is homogeneous; namely, it holds

$\nu$

is homogeneous; namely, it holds

$\nu (\lambda \,{\mathbb{B}}) = \lambda ^{-\alpha }\,\nu ({\mathbb{B}})$

, for any

$\nu (\lambda \,{\mathbb{B}}) = \lambda ^{-\alpha }\,\nu ({\mathbb{B}})$

, for any

$\lambda \gt 0$

.

$\lambda \gt 0$

.

The frame of multivariate regular variation was introduced in De Haan and Resnick (Reference De Haan and Resnick1981). Under this definition, the multivariate regular variation was used in the study of several issues in multivariate risk models and in risk management, as, for example, in Li (Reference Li2016), Tang and Yang (Reference Tang and Yang2019), and Yang and Su (Reference Yang and Su2023).

Although this kind of extension to multidimensional setup is well-established, it does not happen to other multidimensional distribution classes. Most of the extensions cover the multivariate subexponential distribution class and the multivariate long-tailed distribution class.

Initially, these two distribution classes were introduced in Cline and Resnick (Reference Cline and Resnick1992) as essential extension of the multivariate regular variation, namely, using vague convergence and point processes. Later, in Omey (Reference Omey2006), three different formulations appear for the multivariate subexponentiality and the multivariate long-tailedness. The formulations, which are close to our definitions, are given in classes

$\mathcal{S}({\mathbb{R}}^d)$

and

$\mathcal{S}({\mathbb{R}}^d)$

and

$\mathcal{L}({\mathbb{R}}^d)$

. We say that the multivariate distribution

$\mathcal{L}({\mathbb{R}}^d)$

. We say that the multivariate distribution

$F$

belongs to class

$F$

belongs to class

$\mathcal{S}({\mathbb{R}}^d)$

, if it holds

$\mathcal{S}({\mathbb{R}}^d)$

, if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {\overline {F^{2*}}(\textbf { t}\,x)}{{\overline {F}}(\textbf { t}\,x)}=2, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {\overline {F^{2*}}(\textbf { t}\,x)}{{\overline {F}}(\textbf { t}\,x)}=2, \end{eqnarray*}

for any

$\textbf { t} \gt \textbf { 0}$

, with

$\textbf { t} \gt \textbf { 0}$

, with

$\min _{1\leq i \leq d} \{t_i\} \lt \infty$

, and that the multivariate distribution

$\min _{1\leq i \leq d} \{t_i\} \lt \infty$

, and that the multivariate distribution

$F$

belongs to class

$F$

belongs to class

$\mathcal{L}({\mathbb{R}}^d)$

, if it holds

$\mathcal{L}({\mathbb{R}}^d)$

, if it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(\textbf { t}\,x-\textbf { a})}{{\overline {F}}(\textbf { t}\,x)}=1, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\overline {F}}(\textbf { t}\,x-\textbf { a})}{{\overline {F}}(\textbf { t}\,x)}=1, \end{eqnarray*}

for any

$\textbf { a} \geq \textbf { 0}$

and for any

$\textbf { a} \geq \textbf { 0}$

and for any

$\textbf { t} \gt \textbf { 0}$

, with

$\textbf { t} \gt \textbf { 0}$

, with

$\min _{1\leq i \leq d} \{t_i\} \lt \infty$

.

$\min _{1\leq i \leq d} \{t_i\} \lt \infty$

.

This approach was used to study the asymptotic behavior of the tail of a randomly stopped sum of random vectors, namely,

$S_{N}=\sum _{i=1}^N \textbf { X}_i$

, where

$S_{N}=\sum _{i=1}^N \textbf { X}_i$

, where

$N$

is a discrete random variable with support

$N$

is a discrete random variable with support

${\mathbb{N}}_0={\mathbb{N}} \cup \{0\}$

and the

${\mathbb{N}}_0={\mathbb{N}} \cup \{0\}$

and the

$ \textbf { X}_i$

are independent, identically distributed random vectors with multivariate distribution

$ \textbf { X}_i$

are independent, identically distributed random vectors with multivariate distribution

$F$

. For applications of this class, see Omey et al. (Reference Omey, Mallor and Santos2006).

$F$

. For applications of this class, see Omey et al. (Reference Omey, Mallor and Santos2006).

Finally, another formulation of multivariate subexponential distributions was provided in Samorodnitsky and Sun (Reference Samorodnitsky and Sun2016), which represents the only approach with results for the ruin probability in a multivariate continuous-time risk model. Although the approach by Samorodnitsky and Sun (Reference Samorodnitsky and Sun2016) is clearly stronger than the previous two, it describes in some sense the linear multivariate single big jump, but it cannot cover the distributions through their joint tail; see Konstantinides and Passalidis (Reference Konstantinides and Passalidis2024, Sec. 5) for comments about this approach, indicating the complementary function to Samorodnitsky and Sun (Reference Samorodnitsky and Sun2016) of our approach, found below. In the present paper, we confine ourselves to the two dimensions, and we stay close to the formulation in Omey (Reference Omey2006); however, we keep two important differences.

First, we follow a direct approach to the one-dimensional distribution classes’ definitions.

Second, in the case of

$d=2$

, the formulation in Omey (Reference Omey2006), and in the definition of multivariate regular variation, the convention

$d=2$

, the formulation in Omey (Reference Omey2006), and in the definition of multivariate regular variation, the convention

$\textbf { F}(x,\,y)={\mathbf{P}}[X\leq x,\,Y\leq y]$

is adopted, and the distribution tail

$\textbf { F}(x,\,y)={\mathbf{P}}[X\leq x,\,Y\leq y]$

is adopted, and the distribution tail

$1-\textbf { F}(x,\,y)$

, denoted

$1-\textbf { F}(x,\,y)$

, denoted

$\overline {\textbf { F}}(x,\,y)$

, is applied on the event

$\overline {\textbf { F}}(x,\,y)$

, is applied on the event

$\{X\gt x\} \cup \{Y\gt y\}$

. We consider only the case in which there exist excesses of both random variables

$\{X\gt x\} \cup \{Y\gt y\}$

. We consider only the case in which there exist excesses of both random variables

$\{X\gt x\} \cap \{Y\gt y\}$

; namely, we define by

$\{X\gt x\} \cap \{Y\gt y\}$

; namely, we define by

${ {\overline {\mathbf{F}}}_1}(x,\,y)\,:\!=\,{\mathbf{P}}[X\gt x,\,Y\gt y]$

, as the distribution tail of

${ {\overline {\mathbf{F}}}_1}(x,\,y)\,:\!=\,{\mathbf{P}}[X\gt x,\,Y\gt y]$

, as the distribution tail of

$\textbf { F}$

, with notation

$\textbf { F}$

, with notation

$ { {\overline {\mathbf{F}}}_b}(x,\,y)\,:\!=\,{\mathbf{P}}[X\gt b_1\,x,\,Y\gt b_2\,y]$

, for all

$ { {\overline {\mathbf{F}}}_b}(x,\,y)\,:\!=\,{\mathbf{P}}[X\gt b_1\,x,\,Y\gt b_2\,y]$

, for all

$\textbf { b}=(b_1,\,b_2) \in (0,\,\infty )^2$

. The choice of such a definition is due to both the consistency with the univariate case and the ease in asymptotic calculation of the joint tail of random sums as well. We intend that our approach becomes more consistent with the ruin of all portfolios, which represents the worst event that can happen for an insurance company with multiple businesses. In some sense, this is the reason why our classes lead to a nonlinear approach of the single big jump in multidimensional setup.

$\textbf { b}=(b_1,\,b_2) \in (0,\,\infty )^2$

. The choice of such a definition is due to both the consistency with the univariate case and the ease in asymptotic calculation of the joint tail of random sums as well. We intend that our approach becomes more consistent with the ruin of all portfolios, which represents the worst event that can happen for an insurance company with multiple businesses. In some sense, this is the reason why our classes lead to a nonlinear approach of the single big jump in multidimensional setup.

Next, we introduce the first bivariate heavy-tailed distribution class. From now on and further by the notation

$\textbf { a}=(a_1,\,a_2)\gt (0,\,0)$

, we mean that

$\textbf { a}=(a_1,\,a_2)\gt (0,\,0)$

, we mean that

$(a_1,\,a_2) \in [0,\,\infty )^2 \setminus \{\textbf { 0}\}$

, except it is referred to differently.

$(a_1,\,a_2) \in [0,\,\infty )^2 \setminus \{\textbf { 0}\}$

, except it is referred to differently.

Definition 2.1.

We say that the random pair (X, Y) with marginal distributions

$F$

,

$F$

,

$G$

belongs to the bivariate long-tailed distributions, symbolically

$G$

belongs to the bivariate long-tailed distributions, symbolically

$(X,\,Y) \in \mathcal{L}^{(2)}$

, if the following conditions hold

$(X,\,Y) \in \mathcal{L}^{(2)}$

, if the following conditions hold

-

(1)

$F \in \mathcal{L}$

and

$G \in \mathcal{L}$

. -

(2) It holds

for some, or equivalently for any,

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac { { {\overline {\mathbf{F}}}_1}(x-a_1,\,y-a_2)}{{ {\overline {\mathbf{F}}}_1}(x,\,y)}=\lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]} =1, \end{eqnarray*}

$\textbf { a}=(a_1,\,a_2) \gt (0,0)$

, with

$a_1$

not necessarily equal to

$a_2$

.

Remark 2.1.

From the previous definition we wonder if by the two-dimensional property of class

$\mathcal{L}^{(2)}$

follows directly the inclusion

$\mathcal{L}^{(2)}$

follows directly the inclusion

$F,\,G \in \mathcal{L}$

. The answer to this question is no because it holds for any, or equivalently for some,

$F,\,G \in \mathcal{L}$

. The answer to this question is no because it holds for any, or equivalently for some,

$(a_1,\,a_2) \gt (0,\,0)$

, as follows from Definition

2.1

.

$(a_1,\,a_2) \gt (0,\,0)$

, as follows from Definition

2.1

.

Let

$F \in \mathcal{L}$

be a distribution and

$F \in \mathcal{L}$

be a distribution and

$G$

be another distribution, not necessarily from class

$G$

be another distribution, not necessarily from class

$\mathcal{L}$

. We assume that the two distributions stem from the independent random variables

$\mathcal{L}$

. We assume that the two distributions stem from the independent random variables

$X$

and

$X$

and

$Y$

; thus, if

$Y$

; thus, if

$a_1\gt 0$

and

$a_1\gt 0$

and

$a_2=0$

, we find that

$a_2=0$

, we find that

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1, \;Y\gt y]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}=\lim _{x\wedge y \to \infty } \dfrac {{\overline {F}}(x-a_1)\,\overline {G}(y)}{{\overline {F}}(x)\,\overline {G}(y)}=1, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1, \;Y\gt y]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}=\lim _{x\wedge y \to \infty } \dfrac {{\overline {F}}(x-a_1)\,\overline {G}(y)}{{\overline {F}}(x)\,\overline {G}(y)}=1, \end{eqnarray*}

however, if it holds

$G \notin \mathcal{L}$

, then we have not this pair in the class

$G \notin \mathcal{L}$

, then we have not this pair in the class

$\mathcal{L}^{(2)}$

.

$\mathcal{L}^{(2)}$

.

The reason why we require that the marginals belong to class

$\mathcal{L}$

is to secure some two-dimensional closure properties that could fail if the

$\mathcal{L}$

is to secure some two-dimensional closure properties that could fail if the

$\mathcal{L}$

condition is missing.

$\mathcal{L}$

condition is missing.

From Definition2.1 we obtain that if

$(F,\,G) \in \mathcal{L}^{(2)}$

, then for any

$(F,\,G) \in \mathcal{L}^{(2)}$

, then for any

$(A_1,\,A_2)\gt (0,\,0)$

, it holds

$(A_1,\,A_2)\gt (0,\,0)$

, it holds

\begin{eqnarray} \sup _{|a_1|\lt A_1,\,|a_2|\lt A_2}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |=o\left ( {\mathbf{P}}[X\gt x,\,Y\gt y]\right ), \end{eqnarray}

\begin{eqnarray} \sup _{|a_1|\lt A_1,\,|a_2|\lt A_2}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |=o\left ( {\mathbf{P}}[X\gt x,\,Y\gt y]\right ), \end{eqnarray}

as

$x\wedge y \to \infty$

, which follows from the uniformity of the convergence

$x\wedge y \to \infty$

, which follows from the uniformity of the convergence

\begin{eqnarray*} \lim _{x\wedge y \to \infty }\dfrac { {\mathbf{P}}[X\gt x-a_1,\;Y \gt y-a_2]}{{\mathbf{P}}[X\gt x,\;Y\gt y]}=1, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\wedge y \to \infty }\dfrac { {\mathbf{P}}[X\gt x-a_1,\;Y \gt y-a_2]}{{\mathbf{P}}[X\gt x,\;Y\gt y]}=1, \end{eqnarray*}

over the parallelogram

$[\!-A_1,\;A_1]\times [\!-A_2,\;A_2]$

. Indeed, for

$[\!-A_1,\;A_1]\times [\!-A_2,\;A_2]$

. Indeed, for

$-A_1 \leq a_1 \leq A_1$

and

$-A_1 \leq a_1 \leq A_1$

and

$-A_2 \leq a_2 \leq A_2$

, we obtain

$-A_2 \leq a_2 \leq A_2$

, we obtain

$x-A_1 \leq x+a_1 \leq x+A_1$

and

$x-A_1 \leq x+a_1 \leq x+A_1$

and

$y-A_2 \leq y+a_2 \leq y+A_2$

. Hence,

$y-A_2 \leq y+a_2 \leq y+A_2$

. Hence,

\begin{eqnarray*} \dfrac {{\mathbf{P}}[X\gt x-A_1, \;Y\gt y-A_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}&\geq & \dfrac {{\mathbf{P}}[X\gt x+a_1, \;Y\gt y+a_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}\\[2mm] &\geq & \dfrac {{\mathbf{P}}[X\gt x+A_1, \;Y\gt y+A_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}, \end{eqnarray*}

\begin{eqnarray*} \dfrac {{\mathbf{P}}[X\gt x-A_1, \;Y\gt y-A_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}&\geq & \dfrac {{\mathbf{P}}[X\gt x+a_1, \;Y\gt y+a_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}\\[2mm] &\geq & \dfrac {{\mathbf{P}}[X\gt x+A_1, \;Y\gt y+A_2]}{{\mathbf{P}}[X\gt x, \;Y\gt y]}, \end{eqnarray*}

where the first fraction tends to unity, as

$x\wedge y \to \infty$

, by Definition2.1, and the last fraction also tends to unity, as

$x\wedge y \to \infty$

, by Definition2.1, and the last fraction also tends to unity, as

$x\wedge y \to \infty$

, after the change of variables

$x\wedge y \to \infty$

, after the change of variables

$x'=x+A_1$

and

$x'=x+A_1$

and

$y'=y+A_2$

and by Definition2.1.

$y'=y+A_2$

and by Definition2.1.

Definition2.2 provides the insensitivity property in joint distributions; see the univariate analogue, for example, in Foss et al. (Reference Foss, Korshunov and Zachary2013) or in Konstantinides (Reference Konstantinides2018).

Definition 2.2.

Let

$a_F(x),\,a_G(y)\gt 0$

for any

$a_F(x),\,a_G(y)\gt 0$

for any

$x\gt 0,\,y\gt 0$

be two non-decreasing function. We say that the joint distribution

$x\gt 0,\,y\gt 0$

be two non-decreasing function. We say that the joint distribution

$\textbf { F}=(F,\,G)$

of

$\textbf { F}=(F,\,G)$

of

$(X,\,Y)$

, with right endpoint

$(X,\,Y)$

, with right endpoint

$r_{\textbf { F}}\,:\!=\,(r_F,\,r_G)=(\infty, \,\infty )$

, satisfies

$r_{\textbf { F}}\,:\!=\,(r_F,\,r_G)=(\infty, \,\infty )$

, satisfies

$(a_F,\,a_G)$

-joint insensitivity, if

$(a_F,\,a_G)$

-joint insensitivity, if

\begin{eqnarray*} &&\sup _{|a_1|\leq a_F(x),\,|a_2| \leq a_G(y)}\left | {\mathbf{P}}[X\gt x-a_1, Y \gt y-a_2]-{\mathbf{P}}[X\gt x, Y\gt y]\right |\\[2mm] &&\qquad \qquad \qquad =o\left ( {\mathbf{P}}[X\gt x,Y\gt y]\right ), \end{eqnarray*}

\begin{eqnarray*} &&\sup _{|a_1|\leq a_F(x),\,|a_2| \leq a_G(y)}\left | {\mathbf{P}}[X\gt x-a_1, Y \gt y-a_2]-{\mathbf{P}}[X\gt x, Y\gt y]\right |\\[2mm] &&\qquad \qquad \qquad =o\left ( {\mathbf{P}}[X\gt x,Y\gt y]\right ), \end{eqnarray*}

as

$x\wedge y \to \infty$

.

$x\wedge y \to \infty$

.

Now we show that class

$ \mathcal{L}^{(2)}$

satisfies the

$ \mathcal{L}^{(2)}$

satisfies the

$(a_F,\,a_G)$

-joint insensitive property.

$(a_F,\,a_G)$

-joint insensitive property.

Lemma 2.1.

Let assume that

$ (X,\,Y) \in \mathcal{L}^{(2)}$

. Then there exist some functions

$ (X,\,Y) \in \mathcal{L}^{(2)}$

. Then there exist some functions

$a_F(x),\,a_G(y)$

such that

$a_F(x),\,a_G(y)$

such that

$a_F(x) \to \infty$

and

$a_F(x) \to \infty$

and

$a_G(y) \to \infty$

, as

$a_G(y) \to \infty$

, as

$x\wedge y \to \infty$

, and

$x\wedge y \to \infty$

, and

$(F,\,G)$

satisfies the

$(F,\,G)$

satisfies the

$(a_F,\,a_G)$

-joint insensitive property.

$(a_F,\,a_G)$

-joint insensitive property.

Proof. For any integer

$n \in {\mathbb{N}}$

, from relation (2.1), we can choose an increasing to infinity sequence

$n \in {\mathbb{N}}$

, from relation (2.1), we can choose an increasing to infinity sequence

$\{u_n\}$

, such that the inequality

$\{u_n\}$

, such that the inequality

\begin{eqnarray*} \sup _{|a_1|\leq n,\,|a_2| \leq n}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |\leq \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt y]}n, \end{eqnarray*}

\begin{eqnarray*} \sup _{|a_1|\leq n,\,|a_2| \leq n}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |\leq \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt y]}n, \end{eqnarray*}

holds for any

$x\geq u_n$

and any

$x\geq u_n$

and any

$y\geq u_n$

. Without loss of generality, we consider that the sequence

$y\geq u_n$

. Without loss of generality, we consider that the sequence

$\{u_n\}$

increases to infinity. We put

$\{u_n\}$

increases to infinity. We put

$a_F(x)=a_G(y)=n$

, for any

$a_F(x)=a_G(y)=n$

, for any

$(x,\,y)\in (u_n,\,u_{n+1}]^2$

. From the fact that

$(x,\,y)\in (u_n,\,u_{n+1}]^2$

. From the fact that

$u_n \to \infty$

, as

$u_n \to \infty$

, as

$n\to \infty$

, we obtain that

$n\to \infty$

, we obtain that

$a_F(x) \to \infty$

, as

$a_F(x) \to \infty$

, as

$x\to \infty$

, and

$x\to \infty$

, and

$a_G(y) \to \infty$

, as

$a_G(y) \to \infty$

, as

$y\to \infty$

.

$y\to \infty$

.

So, from the construction of

$a(\cdot )$

, we conclude that

$a(\cdot )$

, we conclude that

\begin{eqnarray*} \sup _{|a_1|\leq a_F(x),\,|a_2| \leq a_G(y)}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |\leq \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt y]}{n}, \end{eqnarray*}

\begin{eqnarray*} \sup _{|a_1|\leq a_F(x),\,|a_2| \leq a_G(y)}\left | {\mathbf{P}}[X\gt x-a_1,\,Y \gt y-a_2]-{\mathbf{P}}[X\gt x,\,Y\gt y]\right |\leq \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt y]}{n}, \end{eqnarray*}

for any

$x \gt u_n$

and any

$x \gt u_n$

and any

$y\gt u_n$

, which is the required result.

$y\gt u_n$

, which is the required result.

Remark 2.2.

From the

$(a_F,\,a_G)$

-joint insensitivity, it does not follow necessarily that

$(a_F,\,a_G)$

-joint insensitivity, it does not follow necessarily that

$a_F$

and

$a_F$

and

$a_G$

are insensitivity functions for the marginal distributions

$a_G$

are insensitivity functions for the marginal distributions

$F,\,G$

, respectively. Furthermore, Lemma

2.1

asserts that

$F,\,G$

, respectively. Furthermore, Lemma

2.1

asserts that

\begin{eqnarray*} \lim _{x\wedge y \to \infty }\dfrac { {\mathbf{P}}[X\gt x\pm a_F(x),\;Y \gt y \pm a_G(y)]}{{\mathbf{P}}[X\gt x,\;Y\gt y]}=1. \end{eqnarray*}

\begin{eqnarray*} \lim _{x\wedge y \to \infty }\dfrac { {\mathbf{P}}[X\gt x\pm a_F(x),\;Y \gt y \pm a_G(y)]}{{\mathbf{P}}[X\gt x,\;Y\gt y]}=1. \end{eqnarray*}

Let us see now two examples that help either to understanding or to constructing of such bivariate distributions. The first case is the simplest, as we construct

$(X,\,Y) \in \mathcal{L}^{(2)}$

through the independence between

$(X,\,Y) \in \mathcal{L}^{(2)}$

through the independence between

$X$

and

$X$

and

$Y$

.

$Y$

.

Example 2.1.

Let

$X$

and

$X$

and

$Y$

be random variables with distributions

$Y$

be random variables with distributions

$F \in \mathcal{L}$

and

$F \in \mathcal{L}$

and

$G \in \mathcal{L}$

, respectively. We assume that

$G \in \mathcal{L}$

, respectively. We assume that

$X$

and

$X$

and

$Y$

are independent, to obtain

$Y$

are independent, to obtain

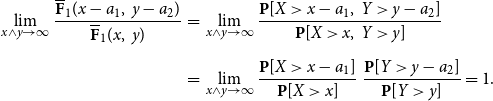

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{ {\overline {\mathbf{F}}}_1}(x-a_1,\,y-a_2)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}&=&\lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\\[2mm] &=&\lim _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}[X\gt x-a_1]}{{\mathbf{P}}[X\gt x]}\,\dfrac {{\mathbf{P}}[Y\gt y-a_2]}{{\mathbf{P}}[Y\gt y]}=1. \end{eqnarray*}

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{ {\overline {\mathbf{F}}}_1}(x-a_1,\,y-a_2)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}&=&\lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\\[2mm] &=&\lim _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}[X\gt x-a_1]}{{\mathbf{P}}[X\gt x]}\,\dfrac {{\mathbf{P}}[Y\gt y-a_2]}{{\mathbf{P}}[Y\gt y]}=1. \end{eqnarray*}

Therefore

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

The next example makes sense, as it cannot be reduced into univariate distributions. The following dependence structure can be found in Li (Reference Li2018). We say that the random variables

$X$

and

$X$

and

$Y$

are strongly asymptotic independent (SAI) if

$Y$

are strongly asymptotic independent (SAI) if

${\mathbf{P}}[X^- \gt x,\,Y\gt y]=O[F(\!-x)\,\overline {G}(y)]$

,

${\mathbf{P}}[X^- \gt x,\,Y\gt y]=O[F(\!-x)\,\overline {G}(y)]$

,

${\mathbf{P}}[X \gt x,\,Y^-\gt y]=O[{\overline {F}}(x)\,G(\!-y)]$

hold as

${\mathbf{P}}[X \gt x,\,Y^-\gt y]=O[{\overline {F}}(x)\,G(\!-y)]$

hold as

$x\wedge y \to \infty$

, and there exists a constant

$x\wedge y \to \infty$

, and there exists a constant

$C\gt 0$

such that if it holds

$C\gt 0$

such that if it holds

\begin{eqnarray} {\mathbf{P}}[X\gt x,\,Y\gt y] \sim C\,{\overline {F}}(x)\,\overline {G}(y), \end{eqnarray}

\begin{eqnarray} {\mathbf{P}}[X\gt x,\,Y\gt y] \sim C\,{\overline {F}}(x)\,\overline {G}(y), \end{eqnarray}

as

$x\wedge y \to \infty$

.

$x\wedge y \to \infty$

.

If the

$X$

and

$X$

and

$Y$

are bounded from below, then (2.2) is enough to be SAI.

$Y$

are bounded from below, then (2.2) is enough to be SAI.

Example 2.2.

Let

$X$

and

$X$

and

$Y$

be random variables with strongly asymptotic independence, with some constant

$Y$

be random variables with strongly asymptotic independence, with some constant

$C\gt 0$

and distributions

$C\gt 0$

and distributions

$F \in \mathcal{L}$

and

$F \in \mathcal{L}$

and

$G \in \mathcal{L}$

, respectively. Then

$G \in \mathcal{L}$

, respectively. Then

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{ {\overline {\mathbf{F}}}_1}(x-a_1,\,y-a_2)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}&=&\lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\\[2mm] &=&\lim _{x\wedge y \to \infty }\dfrac {C\,{\overline {F}}(x-a_1)\,\overline {G}(y-a_2)}{C\,{\overline {F}}(x)\,\overline {G}(y)}=1. \end{eqnarray*}

\begin{eqnarray*} \lim _{x\wedge y \to \infty } \dfrac {{ {\overline {\mathbf{F}}}_1}(x-a_1,\,y-a_2)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}&=&\lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\\[2mm] &=&\lim _{x\wedge y \to \infty }\dfrac {C\,{\overline {F}}(x-a_1)\,\overline {G}(y-a_2)}{C\,{\overline {F}}(x)\,\overline {G}(y)}=1. \end{eqnarray*}

Therefore

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

The first two examples restrict themselves either in the independent case or in some kind of asymptotic independence. Notice that in the next example as class

$ \mathcal{L}^{(2)}$

, we understand the class from Definition2.1, but with a restriction with respect to convergence, instead of

$ \mathcal{L}^{(2)}$

, we understand the class from Definition2.1, but with a restriction with respect to convergence, instead of

$x \wedge y$

to

$x \wedge y$

to

$x=y$

only. In Li and Yang (Reference Li and Yang2015), the dependence structure from relation (2.3) was used, through the survival copula

$x=y$

only. In Li and Yang (Reference Li and Yang2015), the dependence structure from relation (2.3) was used, through the survival copula

$\widehat {C}$

, to depict the dependence relation among claims in a bivariate, continuous-time risk model. We assume that for two random variables

$\widehat {C}$

, to depict the dependence relation among claims in a bivariate, continuous-time risk model. We assume that for two random variables

$X,\,Y$

following a survival copula

$X,\,Y$

following a survival copula

$\widehat {C}$

, there exists some constant

$\widehat {C}$

, there exists some constant

$\gamma \geq 1$

and a positive measurable function

$\gamma \geq 1$

and a positive measurable function

$h(\cdot, \,\cdot )$

, such that the asymptotic relation holds

$h(\cdot, \,\cdot )$

, such that the asymptotic relation holds

\begin{eqnarray} \widehat {C}(t_1\,x,\,t_2\,x) \sim x^{\gamma }\,h(t_1,\,t_2), \end{eqnarray}

\begin{eqnarray} \widehat {C}(t_1\,x,\,t_2\,x) \sim x^{\gamma }\,h(t_1,\,t_2), \end{eqnarray}

as

$x \downarrow 0$

holds, for any

$x \downarrow 0$

holds, for any

$(t_1,\,t_2) \in (0,\,\infty )$

.

$(t_1,\,t_2) \in (0,\,\infty )$

.

Example 2.3.

Let the random variables

$X,\,Y$

follow a survival copula from relation

(2.3)

and

$X,\,Y$

follow a survival copula from relation

(2.3)

and

$F,\,G$

be their marginal distributions. Furthermore, we assume that it holds

$F,\,G$

be their marginal distributions. Furthermore, we assume that it holds

\begin{eqnarray} \lim _{x\to \infty } \dfrac {\overline {G}(x)}{{\overline {F}}(x)}=c, \end{eqnarray}

\begin{eqnarray} \lim _{x\to \infty } \dfrac {\overline {G}(x)}{{\overline {F}}(x)}=c, \end{eqnarray}

for some positive constant

$c\gt 0$

and either

$c\gt 0$

and either

$F\in \mathcal{L}$

or

$F\in \mathcal{L}$

or

$G\in \mathcal{L}$

is true. Finally, we suppose that relation

(2.3)

holds with

$G\in \mathcal{L}$

is true. Finally, we suppose that relation

(2.3)

holds with

$\gamma =1$

. Then we obtain

$\gamma =1$

. Then we obtain

$F,\,G \in \mathcal{L}$

, which follows from the closure property of class

$F,\,G \in \mathcal{L}$

, which follows from the closure property of class

$ \mathcal{L}$

with respect to strong equivalence of (2.4); see Leipus et al. (Reference Leipus, Šiaulys and Konstantinides2023). From Li and Yang (Reference Li and Yang2015, Prop. 3.1), we have the random variables

$ \mathcal{L}$

with respect to strong equivalence of (2.4); see Leipus et al. (Reference Leipus, Šiaulys and Konstantinides2023). From Li and Yang (Reference Li and Yang2015, Prop. 3.1), we have the random variables

$X,\,Y$

to be asymptotic dependent, and further, they satisfy

$X,\,Y$

to be asymptotic dependent, and further, they satisfy

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt x]}{{\mathbf{P}}[X\gt x]} =h(1,\,c)\gt 0, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\mathbf{P}}[X\gt x,\,Y\gt x]}{{\mathbf{P}}[X\gt x]} =h(1,\,c)\gt 0, \end{eqnarray*}

hence by the last formulas, for any

$(a_1,\,a_2)\gt (0,\,0)$

, it holds

$(a_1,\,a_2)\gt (0,\,0)$

, it holds

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt x-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt x]} =\lim _{x\to \infty } \dfrac {h(1,\,c)\,{\mathbf{P}}[X\gt x-a_1]}{h(1,\,c)\,{\mathbf{P}}[X\gt x]}=1, \end{eqnarray*}

\begin{eqnarray*} \lim _{x\to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt x-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt x]} =\lim _{x\to \infty } \dfrac {h(1,\,c)\,{\mathbf{P}}[X\gt x-a_1]}{h(1,\,c)\,{\mathbf{P}}[X\gt x]}=1, \end{eqnarray*}

so we find

$ (X,\,Y) \in \mathcal{L}^{(2)}$

, in the sense that in Definition

2.1

, the convergence is valid with

$ (X,\,Y) \in \mathcal{L}^{(2)}$

, in the sense that in Definition

2.1

, the convergence is valid with

$x=y$

.

$x=y$

.

We can find several dependence structures that satisfy the

$\mathcal{L}^{(2)}$

condition. However, we choose to pursue theoretical results.

$\mathcal{L}^{(2)}$

condition. However, we choose to pursue theoretical results.

Now we pass to the bivariate subexponential distribution class

$\mathcal{S}^{(2)}$

.

$\mathcal{S}^{(2)}$

.

Definition 2.3.

We say that the random pair

$(X,\,Y)$

, with marginal distributions

$(X,\,Y)$

, with marginal distributions

$F$

and

$F$

and

$G$

, respectively, belongs to the class of bivariate subexponential distributions, symbolically

$G$

, respectively, belongs to the class of bivariate subexponential distributions, symbolically

$(X,\,Y) \in \mathcal{S}^{(2)}$

, if

$(X,\,Y) \in \mathcal{S}^{(2)}$

, if

-

(1)

$F \in \mathcal{S}$

and

$G \in \mathcal{S}$

. -

(2)

$(X,\,Y) \in \mathcal{L}^{(2)}$

. -

(3) It holds

(2.5)where

\begin{eqnarray} \lim _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X_1+X_2\gt x,\;Y_1+Y_2\gt y]}{{\mathbf{P}}[X\gt x,\;Y\gt y]}=2^2, \end{eqnarray}

$(X_1,\,Y_1)$

and

$(X_2,\,Y_2)$

are independent and identically distributed copies of

$(X,\,Y)$

.

Remark 2.3.

In case of

$d$

-variate distribution, relation

(2.5)

becomes

$d$

-variate distribution, relation

(2.5)

becomes

\begin{eqnarray*} \lim _{x_1\wedge \ldots \wedge x_n\; to\; \infty} \dfrac {{\mathbf{P}}[X_{1,1}+X_{1,2}\gt x_1,\;\ldots, \,X_{d,1}+X_{d,2}\gt x_d]}{{\mathbf{P}}[X_{1,1}\gt x_1,\;\ldots, \,X_{d,1}\gt x_d]}=2^d. \end{eqnarray*}

\begin{eqnarray*} \lim _{x_1\wedge \ldots \wedge x_n\; to\; \infty} \dfrac {{\mathbf{P}}[X_{1,1}+X_{1,2}\gt x_1,\;\ldots, \,X_{d,1}+X_{d,2}\gt x_d]}{{\mathbf{P}}[X_{1,1}\gt x_1,\;\ldots, \,X_{d,1}\gt x_d]}=2^d. \end{eqnarray*}

Conjecture 2.1.

In Definition

2.3

, we suppose that the

$(1)$

,

$(1)$

,

$(3)$

do NOT imply directly the property

$(3)$

do NOT imply directly the property

$(2)$

and the membership in

$(2)$

and the membership in

$\mathcal{L}^{(2)}$

. Although it is not proved, we consider that this conjecture could be established through a special counterexample, in which the

$\mathcal{L}^{(2)}$

. Although it is not proved, we consider that this conjecture could be established through a special counterexample, in which the

$(1)$

,

$(1)$

,

$(3)$

are satisfied, and the

$(3)$

are satisfied, and the

$(X,\,Y)$

satisfy properties of some special kind of copulas that belong to

$(X,\,Y)$

satisfy properties of some special kind of copulas that belong to

$SAI$

in

(2.2)

, but now with

$SAI$

in

(2.2)

, but now with

$C=0$

; see Li (Reference Li2018b), Ji et al. (Reference Ji, Wang, Yan and Cheng2023), and Li (Reference Li2024) for examples of such dependence through copulas.

$C=0$

; see Li (Reference Li2018b), Ji et al. (Reference Ji, Wang, Yan and Cheng2023), and Li (Reference Li2024) for examples of such dependence through copulas.

Now we come to the bivariate dominatedly varying distribution class

$\mathcal{D}^{(2)}$

.

$\mathcal{D}^{(2)}$

.

Definition 2.4.

We say that the random pair

$(X,\,Y)$

, with marginal distributions

$(X,\,Y)$

, with marginal distributions

$F$

and

$F$

and

$G$

, respectively, belongs to the class of bivariate dominatedly varying distributions, symbolically

$G$

, respectively, belongs to the class of bivariate dominatedly varying distributions, symbolically

$(X,\,Y) \in \mathcal{D}^{(2)}$

, if

$(X,\,Y) \in \mathcal{D}^{(2)}$

, if

-

(1)

$F \in \mathcal{D}$

and

$G \in \mathcal{D}$

. -

(2) It holds

(2.6)for some, or equivalently for all

\begin{eqnarray} \limsup _{x\wedge y \to \infty } \dfrac { { {\overline {\mathbf{F}}}_b}(x,\,y)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}=\limsup _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt b_1\,x,\,Y\gt b_2\,y]}{{\mathbf{P}}[X\gt x,\,Y\gt y]} \lt \infty, \end{eqnarray}

$\textbf { b}=(b_1,\,b_2) \in (0,\,1)^2$

, with

$b_1$

not necessarily equal to

$b_2$

.

It is obvious that 2.6 is equivalently with:

\begin{eqnarray*} \liminf _{x\wedge y \to \infty }\dfrac { { {\overline {\mathbf{F}}}_b}(x,\, y)}{ { {\overline {\mathbf{F}}}_1}(x, y)}\gt 0 \end{eqnarray*}

\begin{eqnarray*} \liminf _{x\wedge y \to \infty }\dfrac { { {\overline {\mathbf{F}}}_b}(x,\, y)}{ { {\overline {\mathbf{F}}}_1}(x, y)}\gt 0 \end{eqnarray*}

for some, or equivalently for all

$\textbf { b}=(b_1,\,b_2) \in (1,\,\infty )^2$

, with

$\textbf { b}=(b_1,\,b_2) \in (1,\,\infty )^2$

, with

$b_1$

not necessarily equal to

$b_1$

not necessarily equal to

$b_2$

.

$b_2$

.

Remark 2.4.

In Konstantinides and Passalidis (Reference Konstantinides and Passalidis2024b), the class

$\mathcal{D}_{n}$

(for some

$\mathcal{D}_{n}$

(for some

$n\in \mathbb{N}$

) of multivariate dominatedly varying random vectors was introduced. It is obvious that in case

$n\in \mathbb{N}$

) of multivariate dominatedly varying random vectors was introduced. It is obvious that in case

$n=2$

, our approach includesthis definition. Specifically

$n=2$

, our approach includesthis definition. Specifically

\begin{equation*} \mathcal{D}_{2}\subset \mathcal{D}^{(2)} \end{equation*}

\begin{equation*} \mathcal{D}_{2}\subset \mathcal{D}^{(2)} \end{equation*}

Definition 2.5.

We say that the random pair

$(X,\,Y)$

, with marginal distributions

$(X,\,Y)$

, with marginal distributions

$F$

and

$F$

and

$G$

, respectively, belongs to the class of bivariate consistently varying distributions, symbolically

$G$

, respectively, belongs to the class of bivariate consistently varying distributions, symbolically

$(X,\,Y) \in \mathcal{C}^{(2)}$

, if

$(X,\,Y) \in \mathcal{C}^{(2)}$

, if

-

(1)

$F \in \mathcal{C}$

and

$G \in \mathcal{C}$

. -

(2) It holds

or equivalently

\begin{eqnarray*} \lim _{\textbf { z} \uparrow \textbf { 1}}\limsup _{x\wedge y \to \infty } \dfrac { { {\overline {\mathbf{F}}}_z}(x,\,y)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}=1, \end{eqnarray*}

where

\begin{eqnarray*} \lim _{\textbf { z} \downarrow \textbf { 1}}\liminf _{x\wedge y \to \infty } \dfrac { { {\overline {\mathbf{F}}}_z}(x,\,y)}{ { {\overline {\mathbf{F}}}_1}(x,\,y)}=1, \end{eqnarray*}

$\textbf { z}=(z_1,\,z_2)$

, and

$\textbf { 1}=(1,\,1)$

.

Examples2.1 and 2.2 remain intact in classes

$\mathcal{D}^{(2)}$

and

$\mathcal{D}^{(2)}$

and

$\mathcal{C}^{(2)}$

; hence, they keep functioning in class

$\mathcal{C}^{(2)}$

; hence, they keep functioning in class

$(\mathcal{D}\cap \mathcal{L})^{(2)}\,:\!=\,\mathcal{D}^{(2)} \cap \mathcal{L}^{(2)}$

.

$(\mathcal{D}\cap \mathcal{L})^{(2)}\,:\!=\,\mathcal{D}^{(2)} \cap \mathcal{L}^{(2)}$

.

Theorem 2.1.

It holds

$\mathcal{C}^{(2)} \subsetneq \mathcal{L}^{(2)}$

.

$\mathcal{C}^{(2)} \subsetneq \mathcal{L}^{(2)}$

.

Proof. Let consider that

$(F,\,G) \in \mathcal{C}^{(2)}$

. Then, for

$(F,\,G) \in \mathcal{C}^{(2)}$

. Then, for

$\textbf { a}=(a_1,\,a_2)>(0,\,0)$

for any distributions

$\textbf { a}=(a_1,\,a_2)>(0,\,0)$

for any distributions

$F,\,G$

, we obtain

$F,\,G$

, we obtain

\begin{eqnarray} 1\leq \liminf _{x \wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}. \end{eqnarray}

\begin{eqnarray} 1\leq \liminf _{x \wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1,\,Y\gt y-a_2]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}. \end{eqnarray}

Hence, we have to show that the upper bound of the last fraction is equal to unity. We observe that for any small enough

$\delta _1,\,\delta _2 \gt 0$

, there exist some

$\delta _1,\,\delta _2 \gt 0$

, there exist some

$x_0\gt 0$

, such that

$x_0\gt 0$

, such that

$x\,(1-\delta _1) \leq x- a_1$

and

$x\,(1-\delta _1) \leq x- a_1$

and

$y\,(1-\delta _2) \leq y- a_2$

, for any

$y\,(1-\delta _2) \leq y- a_2$

, for any

$x \wedge y \geq x_0$

. Therefore, we find

$x \wedge y \geq x_0$

. Therefore, we find

\begin{eqnarray} \limsup _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1, Y\gt y-a_2]}{{\mathbf{P}}[X\gt x, Y\gt y]}\leq \limsup _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x (1-\delta _1),\,Y\gt y (1-\delta _2)]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\to 1, \end{eqnarray}

\begin{eqnarray} \limsup _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x-a_1, Y\gt y-a_2]}{{\mathbf{P}}[X\gt x, Y\gt y]}\leq \limsup _{x\wedge y \to \infty } \dfrac {{\mathbf{P}}[X\gt x (1-\delta _1),\,Y\gt y (1-\delta _2)]}{{\mathbf{P}}[X\gt x,\,Y\gt y]}\to 1, \end{eqnarray}

as

$(\delta _1,\,\delta _2) \to (0,\,0)$

, where in the last step, we use the properties of class

$(\delta _1,\,\delta _2) \to (0,\,0)$

, where in the last step, we use the properties of class

$\mathcal{C}^{(2)}$

for the pair of distributions

$\mathcal{C}^{(2)}$

for the pair of distributions

$(F,\,G)$

. So, by relations (2.7) and (2.8), we conclude that

$(F,\,G)$

. So, by relations (2.7) and (2.8), we conclude that

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

$(X,\,Y) \in \mathcal{L}^{(2)}$

.

3. Max-sum equivalence and closure properties with respect to convolution

Now, we present two definitions. In the first one, we define the closure property with respect to convolution in bivariate distributions. In this case, we formulate the main result, showing that the class

$\mathcal{D}^{(2)}$

is closed. The second definition, given at the end of the section, under concrete dependence structures, also presented later, is fulfilled with respect to classes

$\mathcal{D}^{(2)}$

is closed. The second definition, given at the end of the section, under concrete dependence structures, also presented later, is fulfilled with respect to classes

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

and

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

and

$\mathcal{C}^{(2)}$

.

$\mathcal{C}^{(2)}$

.

Definition 3.1.

Let

$X_1,\,X_2,\,Y_1,\,Y_2$

be random variables, with distributions

$X_1,\,X_2,\,Y_1,\,Y_2$

be random variables, with distributions

$F_1$

,

$F_1$

,

$F_2$

,

$F_2$

,

$G_1$

and

$G_1$

and

$G_2$

, respectively. If the following conditions are true

$G_2$

, respectively. If the following conditions are true

-

(1)

$F_1 \in \mathcal{B}$

,

$F_2 \in \mathcal{B}$

,

$G_1 \in \mathcal{B}$

,

$G_2 \in \mathcal{B}$

and for any

$k,\,l \in \{1,\,2\}$

, holds

$(X_k,\,Y_l) \in \mathcal{B}^{(2)}$

, -

(2) Holds

$(X_1+X_2,\,Y_1+Y_2) \in \mathcal{B}^{(2)}$

,

where

$\mathcal{B}^{(2)}$

is some bivariate class, defined in Section

2

, then we say that the class

$\mathcal{B}^{(2)}$

is some bivariate class, defined in Section

2

, then we say that the class

$\mathcal{B}^{(2)}$

is closed with respect to sum. If

$\mathcal{B}^{(2)}$

is closed with respect to sum. If

$X_1$

,

$X_1$

,

$X_2$

are independent random variables, and

$X_2$

are independent random variables, and

$Y_1$

,

$Y_1$

,

$Y_2$

are also independent, then we say that

$Y_2$

are also independent, then we say that

$\mathcal{B}^{(2)}$

is closed with respect to convolution, symbolically

$\mathcal{B}^{(2)}$

is closed with respect to convolution, symbolically

$(F_1*F_1, \,G_1*G_2) \in \mathcal{B}^{(2)}$

.

$(F_1*F_1, \,G_1*G_2) \in \mathcal{B}^{(2)}$

.

In the last definition, although the check of

$F_{X_1+X_2} \in \mathcal{B}$

,

$F_{X_1+X_2} \in \mathcal{B}$

,

$G_{Y_1+Y_2} \in \mathcal{B}$

is implied directly by the univariate closure properties, the check of

$G_{Y_1+Y_2} \in \mathcal{B}$

is implied directly by the univariate closure properties, the check of

$(F_k,\,G_l) \in \mathcal{B}^{(2)}$

, for any

$(F_k,\,G_l) \in \mathcal{B}^{(2)}$

, for any

$k,\,l \in \{1,\,2\}$

, is still NOT implied. Also, it is NOT implied that the joint tail of

$k,\,l \in \{1,\,2\}$

, is still NOT implied. Also, it is NOT implied that the joint tail of

$(X_1+X_2,\,Y_1+Y_2)$

has the desired property of

$(X_1+X_2,\,Y_1+Y_2)$

has the desired property of

$\mathcal{B}^{(2)}$

. Hence, we find out that the dependence structures among the components play a crucial role in the closure properties of bivariate vectors.

$\mathcal{B}^{(2)}$

. Hence, we find out that the dependence structures among the components play a crucial role in the closure properties of bivariate vectors.

Next we see that the class

$\mathcal{D}^{(2)}$

is closed with respect to sum (of arbitrarily dependent random vectors with arbitrarily non-negative dependent components), under the condition that the point

$\mathcal{D}^{(2)}$

is closed with respect to sum (of arbitrarily dependent random vectors with arbitrarily non-negative dependent components), under the condition that the point

$(1)$

in Definition3.1 is satisfied.

$(1)$

in Definition3.1 is satisfied.

Theorem 3.1.

Let non-negative random variables

$X_1,\,X_2,\,Y_1,\,Y_2$

with distributions

$X_1,\,X_2,\,Y_1,\,Y_2$

with distributions

$F_1$

,

$F_1$

,

$F_2$

,

$F_2$

,

$G_1$

, and

$G_1$

, and

$G_2$

, from class

$G_2$

, from class

$\mathcal{D}$

, respectively. We assume that

$\mathcal{D}$

, respectively. We assume that

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$k,\,l\,\in \{1,\,2\}$

, then

$k,\,l\,\in \{1,\,2\}$

, then

$(X_1+X_2,\,Y_1+Y_2) \in \mathcal{D}^{(2)}$

.

$(X_1+X_2,\,Y_1+Y_2) \in \mathcal{D}^{(2)}$

.

Proof. At first, for the first condition of

$\mathcal{D}^{(2)}$

, we obtain

$\mathcal{D}^{(2)}$

, we obtain

$F_{X_1+X_2} \in \mathcal{D}$

and

$F_{X_1+X_2} \in \mathcal{D}$

and

$G_{Y_1+Y_2} \in \mathcal{D}$

because of Proposition1.1.

$G_{Y_1+Y_2} \in \mathcal{D}$

because of Proposition1.1.

Taking into consideration that all the distributions have support on the interval

$[0,\,\infty )$

, by the elementary inequalities

$[0,\,\infty )$

, by the elementary inequalities

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x] \leq {\mathbf{P}}\left [X_1\gt \dfrac x2 \right ]+ {\mathbf{P}}\left [X_2 \gt \dfrac x2\right ],\\[2mm] {\mathbf{P}}[X_1+X_2\gt x] \geq \dfrac 12 \left ({\mathbf{P}}[X_1\gt x]+ {\mathbf{P}}[X_2 \gt x]\right ), \end{eqnarray*}

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x] \leq {\mathbf{P}}\left [X_1\gt \dfrac x2 \right ]+ {\mathbf{P}}\left [X_2 \gt \dfrac x2\right ],\\[2mm] {\mathbf{P}}[X_1+X_2\gt x] \geq \dfrac 12 \left ({\mathbf{P}}[X_1\gt x]+ {\mathbf{P}}[X_2 \gt x]\right ), \end{eqnarray*}

we find

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y] &\leq & {\mathbf{P}}[X_1\gt x/2,\,Y_1+Y_2\gt y]+ {\mathbf{P}}[X_2\gt x/2,\,Y_1+Y_2\gt y]\\[2mm] &\leq & {\mathbf{P}}\left [X_1\gt \dfrac x2,\,Y_1\gt \dfrac y2\right ]+ {\mathbf{P}}\left [X_1\gt \dfrac x2,\,Y_2\gt \dfrac y2\right ]\\[2mm] &&+{\mathbf{P}}\left [X_2\gt \dfrac x2,\,Y_1\gt \dfrac y2\right ]+{\mathbf{P}}\left [X_2\gt \dfrac x2,\,Y_2\gt \dfrac y2\right ], \end{eqnarray*}

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y] &\leq & {\mathbf{P}}[X_1\gt x/2,\,Y_1+Y_2\gt y]+ {\mathbf{P}}[X_2\gt x/2,\,Y_1+Y_2\gt y]\\[2mm] &\leq & {\mathbf{P}}\left [X_1\gt \dfrac x2,\,Y_1\gt \dfrac y2\right ]+ {\mathbf{P}}\left [X_1\gt \dfrac x2,\,Y_2\gt \dfrac y2\right ]\\[2mm] &&+{\mathbf{P}}\left [X_2\gt \dfrac x2,\,Y_1\gt \dfrac y2\right ]+{\mathbf{P}}\left [X_2\gt \dfrac x2,\,Y_2\gt \dfrac y2\right ], \end{eqnarray*}

hence

\begin{eqnarray} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\leq \sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}\left [X_k\gt \dfrac x2,\,Y_l\gt \dfrac y2\right ]. \end{eqnarray}

\begin{eqnarray} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\leq \sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}\left [X_k\gt \dfrac x2,\,Y_l\gt \dfrac y2\right ]. \end{eqnarray}

From the other side

\begin{eqnarray*} &&{\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y] \geq \dfrac {{\mathbf{P}}[X_1\gt x,\,Y_1+Y_2\gt y]+ {\mathbf{P}}[X_2\gt x,\,Y_1+Y_2\gt y]}2 \\[2mm] &&\geq \dfrac {{\mathbf{P}}[X_1\gt x,\,Y_1\gt y]+ {\mathbf{P}}[X_1\gt x,\,Y_2\gt y]+{\mathbf{P}}[X_2\gt x,\,Y_1\gt y]+{\mathbf{P}}[X_2\gt x,\,Y_2\gt y]}4, \end{eqnarray*}

\begin{eqnarray*} &&{\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y] \geq \dfrac {{\mathbf{P}}[X_1\gt x,\,Y_1+Y_2\gt y]+ {\mathbf{P}}[X_2\gt x,\,Y_1+Y_2\gt y]}2 \\[2mm] &&\geq \dfrac {{\mathbf{P}}[X_1\gt x,\,Y_1\gt y]+ {\mathbf{P}}[X_1\gt x,\,Y_2\gt y]+{\mathbf{P}}[X_2\gt x,\,Y_1\gt y]+{\mathbf{P}}[X_2\gt x,\,Y_2\gt y]}4, \end{eqnarray*}

from where we obtain

\begin{eqnarray} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\geq \dfrac 14\,\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y]. \end{eqnarray}

\begin{eqnarray} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\geq \dfrac 14\,\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y]. \end{eqnarray}

Therefore by relations (3.1) and (3.2), due to

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$k,\,l\,\in \{1,\,2\}$

, and

$k,\,l\,\in \{1,\,2\}$

, and

$\textbf { b}=(b_1,\,b_2) \in (0,\,1)^2$

, we find

$\textbf { b}=(b_1,\,b_2) \in (0,\,1)^2$

, we find

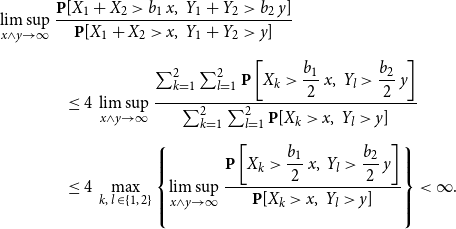

\begin{eqnarray*} &&\limsup _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}[X_1+X_2\gt b_1\,x,\,Y_1+Y_2\gt b_2\,y]}{{\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]}\\[2mm] &&\qquad \qquad \leq 4\,\limsup _{x\wedge y \to \infty }\dfrac {\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}\left [X_k\gt \dfrac {b_1}2\,x,\,Y_l\gt \dfrac {b_2}2\,y\right ]}{\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y]}\\[2mm] &&\qquad \qquad \leq 4\,\max _{k,\,l\,\in \{1,\,2\}}\left \{ \limsup _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}\left [X_k\gt \dfrac {b_1}2\,x,\,Y_l\gt \dfrac {b_2}2\,y\right ]}{{\mathbf{P}}[X_k\gt x,\,Y_l\gt y]}\right \} \lt \infty . \end{eqnarray*}

\begin{eqnarray*} &&\limsup _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}[X_1+X_2\gt b_1\,x,\,Y_1+Y_2\gt b_2\,y]}{{\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]}\\[2mm] &&\qquad \qquad \leq 4\,\limsup _{x\wedge y \to \infty }\dfrac {\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}\left [X_k\gt \dfrac {b_1}2\,x,\,Y_l\gt \dfrac {b_2}2\,y\right ]}{\sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y]}\\[2mm] &&\qquad \qquad \leq 4\,\max _{k,\,l\,\in \{1,\,2\}}\left \{ \limsup _{x\wedge y \to \infty }\dfrac {{\mathbf{P}}\left [X_k\gt \dfrac {b_1}2\,x,\,Y_l\gt \dfrac {b_2}2\,y\right ]}{{\mathbf{P}}[X_k\gt x,\,Y_l\gt y]}\right \} \lt \infty . \end{eqnarray*}

So we conclude

$(X_1+X_2,\,Y_1+Y_2) \in \mathcal{D}^{(2)}$

.

$(X_1+X_2,\,Y_1+Y_2) \in \mathcal{D}^{(2)}$

.

Remark 3.1.

Let us notice here that the vectors

$(X_k,\,Y_l)$

for

$(X_k,\,Y_l)$

for

$k,\,l =1,\,2$

are NOT necessarily under the same dependence structure; for example, we can have

$k,\,l =1,\,2$

are NOT necessarily under the same dependence structure; for example, we can have

$(X_1,\,Y_1)$

with independent components and

$(X_1,\,Y_1)$

with independent components and

$(X_1,\,Y_2)$

to be

$(X_1,\,Y_2)$

to be

$SAI$

, with

$SAI$

, with

$C\gt 0$

. A case where we see that

$C\gt 0$

. A case where we see that

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$(X_k,\,Y_l) \in \mathcal{D}^{(2)}$

for any

$k,\,l =1,\,2$

is the following. Let

$k,\,l =1,\,2$

is the following. Let

$X_1,\,X_2,\,Y_1,\,Y_2$

with distributions from class

$X_1,\,X_2,\,Y_1,\,Y_2$

with distributions from class

$\mathcal{D}$

and also the

$\mathcal{D}$

and also the

$X_1,\,X_2$

and the

$X_1,\,X_2$

and the

$Y_1,\,Y_2$

are arbitrarily dependent. If

$Y_1,\,Y_2$

are arbitrarily dependent. If

$(X_k,\,Y_l)$

are

$(X_k,\,Y_l)$

are

$SAI$

with

$SAI$

with

$C_{k,l}\gt 0$

, not necessarily the same for each pair, then

$C_{k,l}\gt 0$

, not necessarily the same for each pair, then

$(X_k,\,Y_l)\in \mathcal{D}^{(2)}$

for any

$(X_k,\,Y_l)\in \mathcal{D}^{(2)}$

for any

$k,\,l =1,\,2$

.

$k,\,l =1,\,2$

.

Now we are ready to define the max-sum equivalence in two dimensions.

Definition 3.2.

Let

$X_1,\,X_2,\,Y_1,\,Y_2$

be random variables. Then we say that they are joint max-sum equivalent if

$X_1,\,X_2,\,Y_1,\,Y_2$

be random variables. Then we say that they are joint max-sum equivalent if

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\sim \sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y], \end{eqnarray*}

\begin{eqnarray*} {\mathbf{P}}[X_1+X_2\gt x,\,Y_1+Y_2\gt y]\sim \sum _{k=1}^2 \sum _{l=1}^2 {\mathbf{P}}[X_k\gt x,\,Y_l\gt y], \end{eqnarray*}

as

$x\wedge y \to \infty$

.

$x\wedge y \to \infty$

.

This kind of asymptotic relation will be established for classes

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

and

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

and

$\mathcal{C}^{(2)}$

, under the assumption of some specific dependence structure.

$\mathcal{C}^{(2)}$

, under the assumption of some specific dependence structure.

4. Joint behavior of random sums

In one dimension, the following asymptotic relation attracted attention:

\begin{eqnarray} {\mathbf{P}}\left [ \sum _{i=1}^n X_i\gt x \right ]\sim \sum _{i=1}^n {\mathbf{P}}[X_i\gt x], \end{eqnarray}

\begin{eqnarray} {\mathbf{P}}\left [ \sum _{i=1}^n X_i\gt x \right ]\sim \sum _{i=1}^n {\mathbf{P}}[X_i\gt x], \end{eqnarray}

as

$x\to \infty$

. Therefore, we study the behavior of both the maximum

$x\to \infty$

. Therefore, we study the behavior of both the maximum

$\bigvee _{i=1}^n X_i$

and the maximum of sums

$\bigvee _{i=1}^n X_i$

and the maximum of sums

\begin{eqnarray*} \bigvee _{i=1}^n S_i\,:\!=\,\max _{1\leq k \leq n}\sum _{i=1}^k X_i, \end{eqnarray*}

\begin{eqnarray*} \bigvee _{i=1}^n S_i\,:\!=\,\max _{1\leq k \leq n}\sum _{i=1}^k X_i, \end{eqnarray*}

for some distributions and correspondingly with some dependence structures to examine if it holds

\begin{eqnarray} {\mathbf{P}}\left [\sum _{i=1}^n X_i\gt x\right ] \sim {\mathbf{P}}\left [ \bigvee _{i=1}^n X_i\gt x \right ]\sim {\mathbf{P}}\left [ \bigvee _{i=1}^n S_i\gt x \right ]\sim \sum _{i=1}^n{\mathbf{P}}\left [ X_i\gt x \right ], \end{eqnarray}

\begin{eqnarray} {\mathbf{P}}\left [\sum _{i=1}^n X_i\gt x\right ] \sim {\mathbf{P}}\left [ \bigvee _{i=1}^n X_i\gt x \right ]\sim {\mathbf{P}}\left [ \bigvee _{i=1}^n S_i\gt x \right ]\sim \sum _{i=1}^n{\mathbf{P}}\left [ X_i\gt x \right ], \end{eqnarray}

as

$x\to \infty$

. Relations (4.1) and (4.2) have been studied extensively; see, for example, in Geluk and Ng (Reference Geluk and Ng2006), Geluk and Tang (Reference Geluk and Tang2009), Ng et al. (Reference Ng, Tang and Yang2002), and Jiang et al. (Reference Jiang, Gao and Wang2014). A similar interest has been appeared for weighted sums of the form

$x\to \infty$

. Relations (4.1) and (4.2) have been studied extensively; see, for example, in Geluk and Ng (Reference Geluk and Ng2006), Geluk and Tang (Reference Geluk and Tang2009), Ng et al. (Reference Ng, Tang and Yang2002), and Jiang et al. (Reference Jiang, Gao and Wang2014). A similar interest has been appeared for weighted sums of the form

\begin{eqnarray*} S_n^{\Theta } \,:\!=\, \sum _{i=1}^n \Theta _i\,X_i,\qquad \bigvee _{i=1}^n S_i^{\Theta }\,:\!=\,\max _{1\leq k \leq n} \sum _{i=1}^k \Theta _i\,X_i, \end{eqnarray*}

\begin{eqnarray*} S_n^{\Theta } \,:\!=\, \sum _{i=1}^n \Theta _i\,X_i,\qquad \bigvee _{i=1}^n S_i^{\Theta }\,:\!=\,\max _{1\leq k \leq n} \sum _{i=1}^k \Theta _i\,X_i, \end{eqnarray*}

and for the circumstances when they satisfy relations (4.1) and (4.2), see, for example, Tang and Yuan (Reference Tang and Yuan2014), Tang and Tsitsiashvili (Reference Tang and Tsitsiashvili2003), Yang et al. (Reference Yang, Leipus and Šiaulys2012), and Zhang et al. (Reference Zhang, Shen and Weng2009).

In this section, we study relation (4.2) in two dimensions. This can be achieved for the class

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

under generalized tail asymptotic independence (GTAI). Although the univariate randomly weighted sums are well studied, this is not true for the multivariate case.

$(\mathcal{D}\cap \mathcal{L})^{(2)}$

under generalized tail asymptotic independence (GTAI). Although the univariate randomly weighted sums are well studied, this is not true for the multivariate case.

Let us mention some papers involved in the asymptotic behavior of the joint-tail probability

\begin{eqnarray*} {\mathbf{P}}\left [ \sum _{i=1}^n \Theta _i\,X_i \gt x,\;\sum _{j=1}^n \Delta _i\,Y_i \gt y \right ], \end{eqnarray*}

\begin{eqnarray*} {\mathbf{P}}\left [ \sum _{i=1}^n \Theta _i\,X_i \gt x,\;\sum _{j=1}^n \Delta _i\,Y_i \gt y \right ], \end{eqnarray*}

as, for example, Chen and Yang (Reference Chen and Yang2019), Li (Reference Li2018), Shen and Du (Reference Shen and Du2023), Shen et al. (Reference Shen, Ge and Fu2020), and Yang et al. (Reference Yang, Chen and Yuen2024).

We restrict ourselves at the moment in the study of non-weighted random sums of the following form:

\begin{eqnarray*} {\mathbf{P}}\left [ \sum _{i=1}^n X_i\gt x,\;\sum _{j=1}^n Y_j \gt y \right ]. \end{eqnarray*}

\begin{eqnarray*} {\mathbf{P}}\left [ \sum _{i=1}^n X_i\gt x,\;\sum _{j=1}^n Y_j \gt y \right ]. \end{eqnarray*}

Let us remind that, as before, the

$X_i$

,

$X_i$

,

$Y_j$

follow distributions with infinite right endpoint.

$Y_j$

follow distributions with infinite right endpoint.

We note that, in almost all existing papers, the dependence structure for the main variables

$X_i$

,

$X_i$

,

$Y_j$

is either of the form:

$Y_j$

is either of the form:

$\{(X_i,\,Y_i),\;i \in {\mathbb{N}}\}$

independent random vectors, and there exists some dependence structure in each random pair, or there exists dependence among

$\{(X_i,\,Y_i),\;i \in {\mathbb{N}}\}$

independent random vectors, and there exists some dependence structure in each random pair, or there exists dependence among

$X_1,\,\ldots, \,X_n$

and

$X_1,\,\ldots, \,X_n$

and

$Y_1,\,\ldots, \,Y_n$

, but the

$Y_1,\,\ldots, \,Y_n$

, but the

$X_i$

and

$X_i$

and

$Y_j$

are independent for any

$Y_j$

are independent for any

$i,\,j$

. Using GTAI, introduced in Konstantinides and Passalidis (Reference Konstantinides and Passalidis2024), both dependence structures are simultaneously permitted. GTAI is defined as follows. Let us consider two sequences of random variables

$i,\,j$

. Using GTAI, introduced in Konstantinides and Passalidis (Reference Konstantinides and Passalidis2024), both dependence structures are simultaneously permitted. GTAI is defined as follows. Let us consider two sequences of random variables

$\{X_n,\;n\in {\mathbb{N}}\},\; \{Y_m,\;m\in {\mathbb{N}}\}$

. We say that the random variables