1 Introduction

The corporation is the greatest single discovery of modern times, whether you judge it by its social, by its ethical, by its industrial or, in the long run … by its political, effects. Steam and electricity would be reduced to comparative impotence without it.

Corporations are indeed the engine of the modern economy – organizing production, generating goods and services, creating jobs, and sustaining a vast network of related industries. As the primary coordinators of manufacturing and services, their rise and expansion have propelled global economic growth. In one of the few studies quantifying their economic contribution, a 2021 McKinsey report estimated that in Organization for Economic Cooperation and Development (OECD) economies, the business sector accounted for roughly 72% of Gross Domestic Product.Footnote 1

Corporations also stand at the center of income distribution through their different payments for labor, materials, equipment, rents, interest, taxes, dividends, and retained earnings for investment. These distributive dynamics are deeply intertwined with the social, ethical, and political effects that Butler identified. Moreover, corporations contribute substantially to social welfare as major employers of people. Few factors shape human well-being more profoundly than earning wages, receiving recognition for one’s work, and seeing both improve over time.

1.1 Neither Shareholder Value Theory nor Stakeholder Theory

Despite their central role in modern economies, however, corporations have been the subject of intense public controversies, polarized between two opposing perspectives: the shareholder value theory and the stakeholder theory. A central thesis of this study is that the dominance of these extremes has produced widespread misunderstanding and undue criticism of corporations, often leading to misguided corporate reforms.

The shareholder value theory, or maximizing shareholder value (MSV) view, holds that corporations exist to maximize shareholder value because shareholders are the sole constituency the corporation must serve.Footnote 2 This view often legitimizes restructuring, layoffs, or even closures so long as share prices rise. MSV has also become a convenient weapon to chastise managers for “underperformance,” even when operational results are sound – an easy criticism when critics can arbitrarily define what counts as “maximum effort.”

The stakeholder theory, by contrast, argues that corporations should pursue social values for the benefit of their stakeholders. Environmental, Social, and Governance(ESG ) investing, championed by institutional investors and civic groups, represents one prominent variant.Footnote 3 Yet like MSV, it provides a pretext for reproaching managers – this time for failing to meet arbitrarily defined social expectations. Because people value social goals differently, no corporation can satisfy them all. Nevertheless, stakeholder theory proponents often denounce firms for not advancing their preferred values, even when these companies contribute meaningfully to society in their own ways.

1.2 The Ontological Foundation of the Corporation: The Two Corporate Axioms

I take here a different approach: examining corporate purpose by starting from its ontological foundation. Shareholder and stakeholder theories only raise the teleological question, “What ends should the corporation serve?” without connecting it to the means to achieve the ends. In contrast, I begin by asking: “What is the nature of the corporation?” “How does it exist?” and “What does it do to survive and prosper?” This ontological approach integrates means and ends, revealing a corporate purpose overlooked by both teleological views.

The ontological foundation rests on Two Corporate Axioms, two undeniable realities that any informed observer must acknowledge. First, the dominance of the corporate form: In modern economies, most sizable enterprises are organized as corporations – joint-stock companies recognized as legal persons. Second, the existence of market competition: Corporations must compete and can survive only by satisfying customers through continuous innovation.

The idea of a legal person with perpetual existence can be traced back to Roman law and had taken institutional shape in Europe by the fourteenth century.Footnote 4 Today, incorporation is simple in most jurisdictions – requiring only minimal capital and a few individuals – and has become the dominant form of enterprise. Legal personality allows a corporation to exist beyond the lifetimes of its founders, providing the foundation for long-term economic growth.

Yet legal personality alone does not ensure survival. Continuity depends on competitiveness: Corporations must attract and retain customers by delivering low-cost, high-quality goods and services. Ownership by a legal person is a necessary but not sufficient condition for perpetuity. The sufficient condition is met only when the corporation competes successfully in the market. The average lifespan of large US firms was just eighteen years as of 2016.Footnote 5 Many fail because they cannot sustain innovation, but this continual exit of losers and rise of winners keeps the economy dynamic. As Joseph Schumpeter observed, such “creative destruction” is the essential fact of capitalism.Footnote 6

1.3 The Eight Corporate Theorems

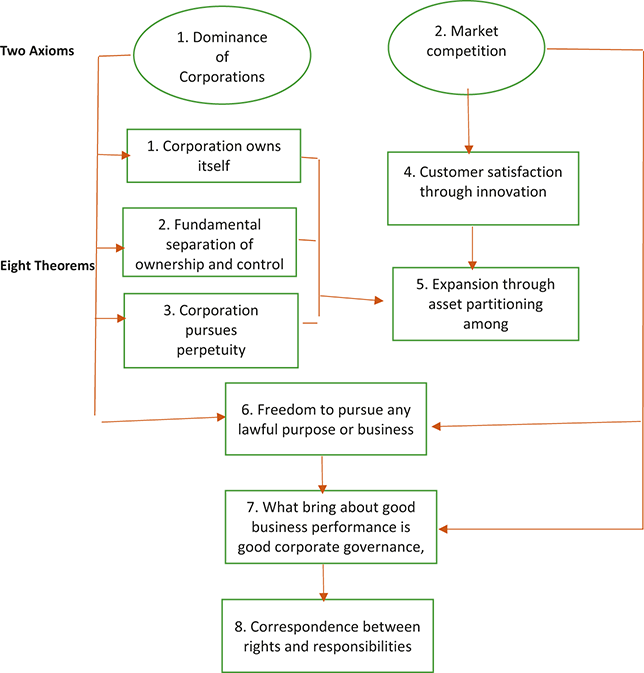

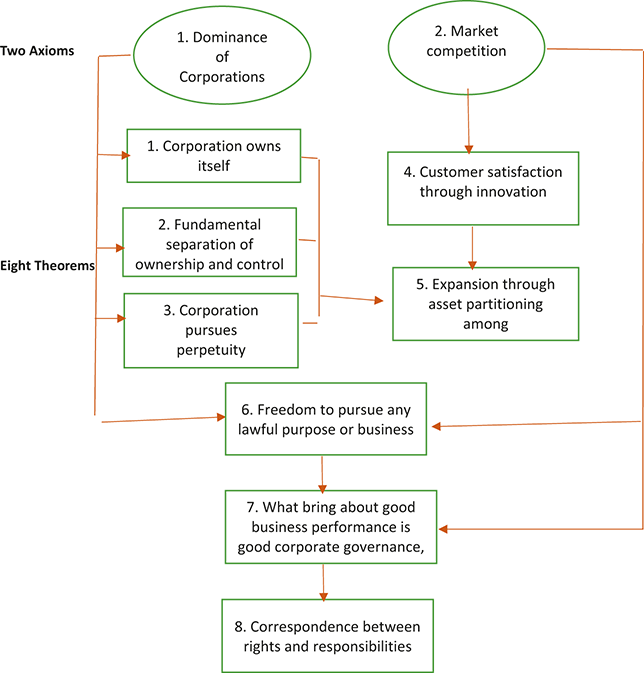

From these two axioms, we can derive the Eight Corporate Theorems. Their schematic relationship is illustrated in Figure 1. Throughout this study, the theorems serve as foundational reference points, enabling readers to develop a comprehensive yet nuanced understanding of corporations through reasoning and common sense.

CT 1 Shareholders are owners of shares – not the corporation. The corporation owns itself.

CT 2 Ownership and control are fundamentally separated when a company is incorporated.

CT 3 The corporation seeks perpetuity.

CT 4 The existential imperative of the corporation is to satisfy customers through innovation.

CT 5 Business groups expand through asset partitioning in the same way as a new company is incorporated.

CT 6 Corporations are free to pursue any lawful purpose or business.

CT 7 What brings about good business performance is good corporate governance, not vice versa.

CT 8 The basic principle of corporate control is the correspondence between rights and responsibilities.

The relationship between the two axioms and the eight theorems.

To illustrate how corporations operate in the real world, I have integrated the corporate theorems into the story of an imaginary company, My Love Co. Initially founded as an artificial intelligence (AI) pet company, My Love grows into a multinational business group and eventually a multiplanetary enterprise. This story is a faction: Fictional in that the company does not exist and the technologies described are slightly ahead of our time, yet factual in that it is grounded in the real-world principles of building and managing a corporation today. By interweaving this narrative with the corporate theorems, I hope to engage a broad audience – businesspeople, financiers, lawyers, policymakers, scholars, and students alike.

1.4 The Ontological Foundation Ahead of the Teleology of the Corporation

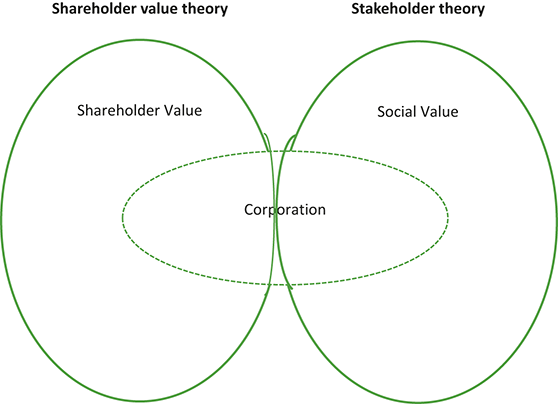

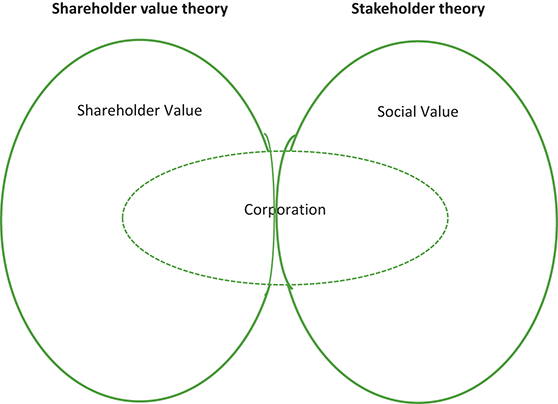

A common flaw shared by both teleological views of the corporation is their neglect of its ontological foundation. First, they deny that the corporation is a real entity. The shareholder value theory treats it merely as a legal “fiction” or shell representing shareholders’ interests.Footnote 7 The stakeholder theory, in turn, arbitrarily dissolves the boundary between the corporation and society, assuming that the corporation should pursue social values prescribed by “stakeholders.”Footnote 8 Second, by denying the corporation’s autonomy, both theories seek its purpose outside the corporation rather than within it, overlooking the social contributions inherent in its very survival. Seen through the lenses of shareholder value and stakeholder theories, the corporation appears as in Figure 2.

The corporation hidden from the two teleological views.

By contrast, this analysis begins with the ontological foundation. The first corporate axiom – the dominance of corporations – is an undeniable reality, not a fiction. Although the legal person originated as a conceptual construct, it has evolved into a social reality by performing vital social functions: enabling the creation, growth, and perpetuation of firms. Over time, the legal person has solidified its existence by assuming unlimited liabilities in business while limiting those of shareholders. Like nations, religions, and cultures, it has evolved into a social reality performing significant functions.Footnote 9

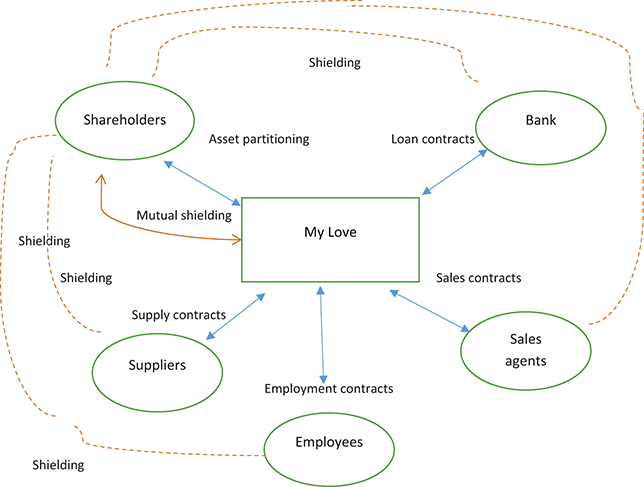

From the first corporate axiom, we derive the three corporate theorems. Through incorporation, founders transfer business-related assets to the legal person in exchange for shares issued by the corporation. In doing so, they become shareholders – owners of shares, not of the corporation – and the corporation assumes a self-owning structure (CT 1). At the same time, ownership and control are permanently separated (CT 2), while both shareholders and the corporation are protected through “asset partitioning” and “entity shielding.” This corporate form thereby enables a company to pursue perpetuity (CT 3).

From the second corporate axiom – the existence of market competition – combined with CTs 1, 2, and 3, we derive CTs 4 and 5. In a market economy, the corporation’s long-term survival depends on satisfying customers through continuous innovation (CT 4). This is the existential imperative of the corporation. To survive and grow amid competition, a corporation expands by creating new entities through asset partitioning, just as natural persons form corporations through asset partitioning (CT 5).

This study emphasizes that the corporation’s ontological foundation precedes its teleology, for it cannot pursue any higher values if it ceases to exist. Moreover, by fulfilling its existential imperative, the corporation already contributes greatly to society. Above all, it delivers customer satisfaction, enhancing human welfare through the provision of desired – and often previously unimagined – goods and services. Beyond that, corporations create jobs, nurture partner firms, enable financial institutions to prosper, build infrastructure, and contribute to public welfare through taxation. These are more intrinsic and substantial social contributions than those achieved by pursuing separate social goals.

Proponents of shareholder value and stakeholder theories overlook this ontological foundation. The former theory illogically claims that maximizing shareholder value automatically enhances corporate efficiency and benefits the economy, reducing the corporation’s ontology to a mere derivative of its teleology.Footnote 10 The latter theory confines the discussion entirely to teleology – social values – ignoring the corporation’s existential imperative and dissolving the boundary between corporation and society.Footnote 11

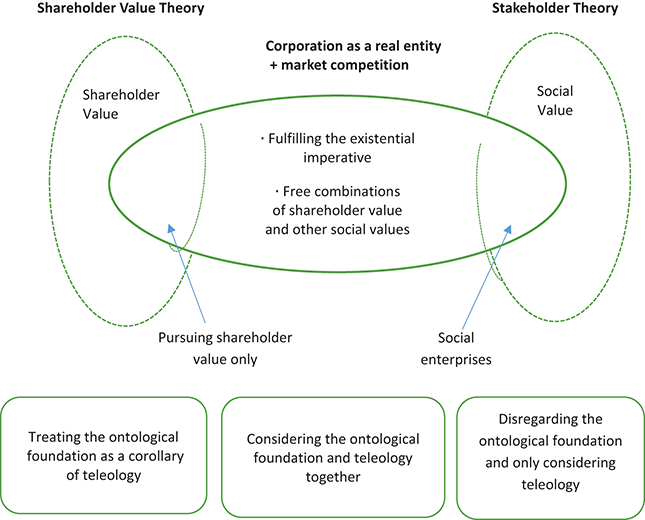

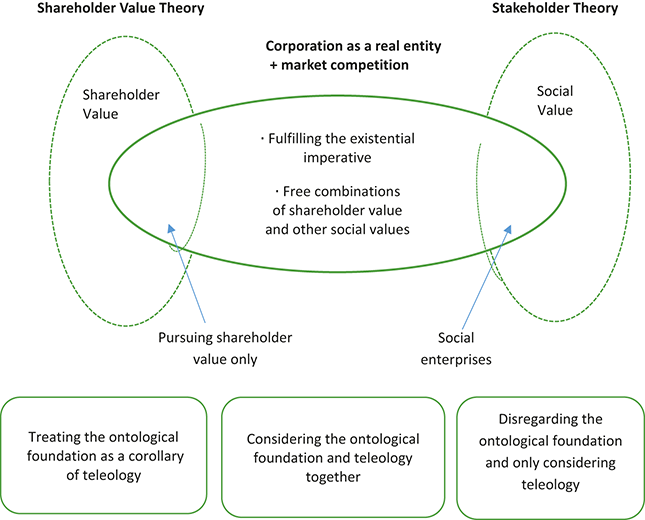

In contrast, this study posits that the corporation considers its ontological foundation and teleology together. It is up to the corporation itself to determine whether to confine its purpose to fulfilling its ontological role, to pursue social values, or combine both (Figure 3). Hence, corporate theorem 6 (CT 6): Corporations are free to pursue any lawful purpose or business.Footnote 12

The corporation seen from the ontological foundation.

Only by recognizing the ontological foundation of the corporation can we develop a coherent understanding of key corporate issues – including the relationship between the board of directors and shareholders, the role of the board in guiding managerial decisions, and the growth of business groups. A realistic understanding of the corporation, grounded in its ontology, should also help reduce the wasteful controversies surrounding corporate governance.

This study also postulates that the widely held belief in a universal, ex ante standard of “good governance” is fundamentally flawed. Instead, it advances corporate theorem 7 (CT 7): What brings about good business performance is good corporate governance. Governance structures vary across countries and corporate contexts, and their effectiveness can only be assessed in retrospect – by observing whether a particular system of control has worked well for a given corporation.Footnote 13

Finally, this study reaffirms a general principle of organizational control that applies equally to corporate control – the correspondence between rights and responsibilities (CT 8). A common flaw in both shareholder and stakeholder theories is the mismatch between the rights and responsibilities. In any organization, greater control entails greater responsibility, while lesser control entails lesser responsibility. This principle must apply equally to managers, shareholders, and stakeholders. Aligning rights with responsibilities thus becomes a cornerstone for developing the corporation as a community of long-term co-prosperity.Footnote 14

1.5 Readers of this volume

I hope this research appeals to a broad audience. Businesspeople form the first group of readers. As a work on the philosophy and guiding principles of the corporation, it invites them to reflect on why they work for their companies and how they make business decisions. I hope the Eight Corporate Theorems and the story of My Love Group will help them recognize and address practical issues in managing their companies.

The second group is finance professionals. With the rise of fund capitalism and the spread of corporate governance activism, financial investors increasingly influence companies through proxy voting and engagement. However, financial investors are largely money-managing trustees – responsible for managing clients’ assets – whereas corporate managers are business-managing trustees, responsible for fulfilling the corporation’s existential imperatives. The fact that these two groups of trustees have different “customers” often leads to conflicts of interest,Footnote 15 which investors should acknowledge when intervening in corporate affairs. I hope the discussion here fosters mutual understanding and better communication between the two.

The third group is scholars. Academia today suffers from overspecialization: Universities praise interdisciplinarity in words but maintain silos in practice. I hope this analysist bridges the divide, laying the foundation for a more integrated understanding of the corporation that connects law, business, and economics. In doing so, it aims to help resolve the century-old debate over corporate purpose – long dominated by studies of large US corporations and the managerial model of Berle and Means (Reference Berle and Means1932).Footnote 16

Last, but not least, politicians and policymakers are part of intended audience. Public policies should be grounded in realities. Yet many corporate regulations are based on misunderstandings, and some even contradict each other in the same economic and legal systems. I hope this discussion serves as a useful reference when policymakers consider corporate regulations.

In undertaking this research, I have received invaluable support from colleagues, family, friends, and acquaintances. While space does not permit me to thank everyone individually, I am deeply grateful for their help. I would also like to express my gratitude to the National University of Singapore (E-122–00–0004–01) and to the Globalization Lab Project (AKS-2018-LAB-1250001) of the Academy of Korean Studies for their support.

2 The Birth of New Owners of Companies

The greatest confusion about the purpose of the corporation arises from a misunderstanding of its ownership. If a business is owned by natural persons, it exists for them. But in modern economies, the dominant organizational form is the corporation, in which a legal person owns all business-related assets. In most developed countries, incorporation is a simple process – anyone can form a corporation by meeting minimal legal requirements. It has therefore become a universal feature of modern enterprise.

Yet many still assume that natural persons own corporations. People casually say, “Tesla is Elon Musk’s company” or “Samsung is the Lee family’s business,” and even scholars often construct theories on the mistaken premise that natural persons ultimately own corporations, overlooking the legal logic of incorporation. Misnomers such as “owner-manager” persist because of this confusion. To clarify who truly owns the corporation – and what that means for its purpose – this section examines the corporation’s legal structure through the lens of three corporate theorems.

CT 1 Shareholders are owners of shares – not the corporation. The corporation owns itself.

CT 2 Ownership and control are fundamentally separated when a company is incorporated.

CT 3 The corporation pursues perpetuity.

These theorems represent different facets of the same legal structure. Upon incorporation, ownership changes fundamentally and irrevocably. The founders transfer all business-related assets to the corporation, which becomes their legal owner – and thus owns itself. In return, the corporation issues shares to the founders, who become shareholders. This transformation limits the founders’ liabilities while giving the corporation a legal foundation for perpetuity. Ownership of assets by a legal person is the institutional basis that has powered the rapid expansion of capitalist economies – what Butler (Reference 90Butler1911) called “the greatest single discovery of modern times.”

2.1 Shareholders Are Owners of Shares – The Corporation Owns Itself

Michael Kim, a data and computer scientist, and Susan Lee, a bio- and neuroscientist, have teamed up to create an AI pet company.Footnote 17 They believe the potential market is vast and will grow rapidly. In Korea, where they are based, about one in four households owns a pet, and the pet industry is valued at about $5.9 billion (KRW8 trillion).Footnote 18 In the US, the pet-dog industry alone is worth about $136.8 billion.Footnote 19

Michael and Susan expect the AI-pet market to grow faster than the market for real pets and ultimately to surpass it. Many people hesitate to own pets because of limited time, money, or space, or emotional strain. Michael’s mother, for instance, adores puppies but avoids raising one because she is meticulous about cleanliness and sensitive about parting with pets – yet she would gladly keep an AI puppy that sheds no fur and poses little emotional burden.

Although AI pets already exist, their appeal remains limited because they still look and feel artificial. Michael and Susan believe they are close to creating AI puppies that will be almost indistinguishable from real ones. Michael has developed an algorithm that enables emotional communication between AI puppies and humans, while Susan has engineered artificial skin and fur that mimic real dogs. Confident that their inventions will work, they prepare to file patents.

Funding, however, is a problem. Patent filing, production facilities, and scaling require millions, and banks or venture capitalists are unwilling to invest in mere ideas. Fortunately, Michael’s wealthy cousin, Collin Park, admires his intelligence and drive and is eager to invest and build his own reputation as a venture capitalist.

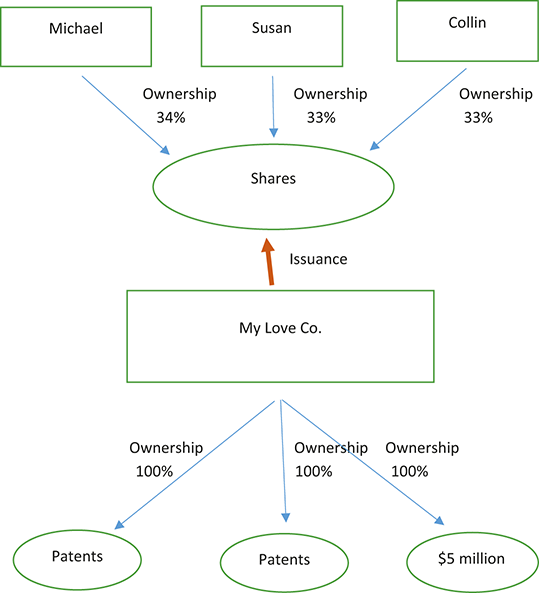

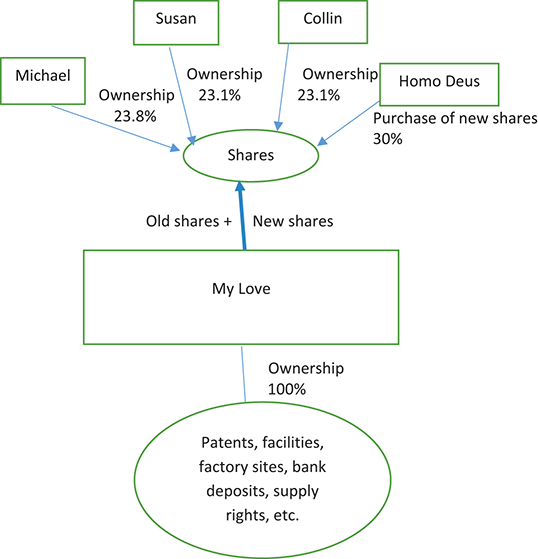

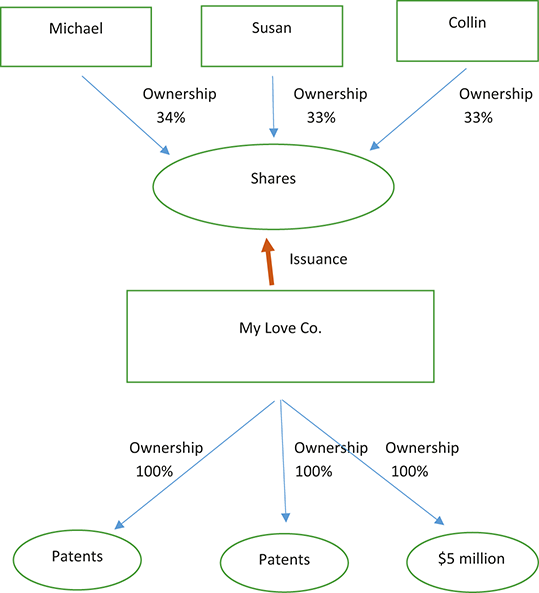

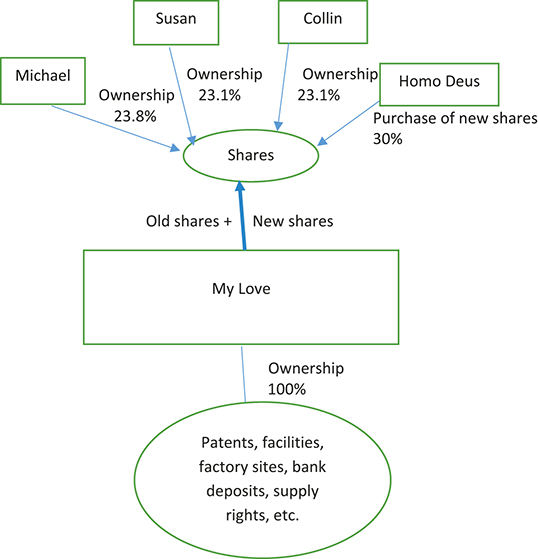

The three partners estimate they will need $5 million to develop patents and prototypes. Collin agrees to provide the funds; they allocate 34% of the company to Michael for his technology, 33% to Susan for hers, and 33% to Collin for his capital. Following a lawyer’s advice, they incorporated My Love Co., Ltd. The ownership and structure of the new company are as shown in Figure 4.

The ownership structure after the establishment of My Love Co.

Note that Michael’s and Susan’s (potential) patents and Collin’s $5 million have been transferred to the corporation. This transfer, known as “asset partitioning,” separates the patents and cash from the founders’ personal assets. The partitioning is permanent – there is no way for the founders to recover the assets once handed over. In legal terminology, this process is also called “capital lock-in,” “affirmative asset partitioning,” “asset separation from shareholders,” or “the absence of a repurchase condition.”Footnote 20

In return, the founders receive shares issued by the corporation and become shareholders. They no longer own the assets held by the corporation and therefore are not its owners. Instead, they exercise control through the rights attached to their shares. Thus, the first corporate theorem (CT 1) states: Shareholders are owners of shares, not the corporation. The corporation owns itself.

The relationship between shareholders and the corporation resembles that between bondholders and the corporation. Bondholders own bonds, not the corporation; shareholders own shares, not the corporation. The difference lies in the nature of their securities. Bondholders’ rights are secured by the corporation’s obligation to repay principal and interest – if it fails, they may liquidate assets in bankruptcy. Shareholders, by contrast, have no guaranteed returns: stock prices may fall, dividends may not be paid, yet bankruptcy is not triggered. Their potential reward is capital gains and dividends, and their formal rights are limited to voting on certain matters such as appointing directors and approving mergers and acquisitions (M&As).

How is the corporation managed? Before incorporation, founders own and manage their assets directly. Once incorporated, all business-related assets belong to the corporation, which requires an organizational structure to oversee and manage them. At the top sits the board of directors, responsible for appointing the Chief Executive Officer (CEO) and other executives and guiding the company’s strategic direction. The founders of My Love Co. agree to form a three-member board: Michael, Susan, and Collin. The board elects Michael as Chairman, and President and CEO, Susan as Vice President and Chief Technology Officer (CTO), and, at Collin’s recommendation, his relative Jeremy – a retired executive – as Chief Financial Officer (CFO).

2.2 The Fundamental Separation of Control from Ownership

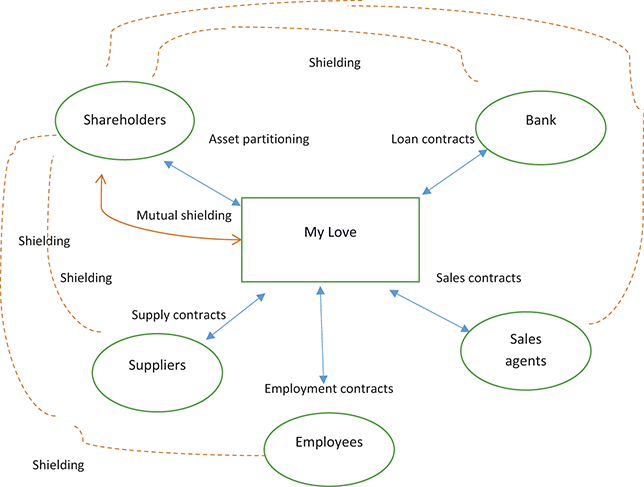

Why do most companies adopt the corporate form? Because it offers exceptional convenience and protection for both founders and the enterprise. Suppose the three founders of My Love launched their venture without incorporating it. To run operations, they would need to make numerous contracts – employment agreements, bank loans, and supplier deals. But who would bear responsibility for them? Without incorporation, the founders would have to sign them personally, exposing themselves to complex legal and financial risks.

Take employment contracts, for instance. My Love is an ambitious AI company that must hire highly skilled engineers and scientists. If it were unincorporated, prospective employees would hesitate to sign contracts with individuals of uncertain financial standing. Michael and Susan, with limited personal assets, could not inspire confidence, and while Collin’s wealth might provide credibility, he would not want to assume unlimited personal liability for salaries or other obligations beyond his $5 million investment.

Incorporation resolves this elegantly. By transferring assets to My Love Co. and making the corporation itself the contracting party, the founders limit their liabilities to the amount they have contributed. Their personal assets are partitioned and shielded from corporate assets. At the same time, employees are protected from risks associated with shareholders’ personal financial affairs – they only need to assess the company’s assets and prospects.

The same logic applies to banks and other creditors. When My Love seeks a loan, the bank prefers to contract with the corporation, not with individuals who hold few tangible assets. With its promising patents and Collin’s capital, the corporation offers a credible counterparty. If Michael later faces personal financial troubles, his creditors cannot seize “Patent 1,” as it has already been transferred to My Love. This entity shielding ensures that lenders can rely on the corporation’s own balance sheet rather than on that of its shareholders. These principles extend to all corporate transactions, including bond issuance, insurance contracts, and supplier agreements, as illustrated in Figure 5.

Asset partitioning and entity shielding surrounding My Love.

It is important to note that the process of incorporation involves the permanent and irrevocable separation of ownership and control. The founders transfer their assets to the corporation and, in so doing, permanently transform themselves into shareholders. They can no longer reclaim those assets; instead, they hold rights attached to their shares. I call this a “fundamental separation of ownership and control” because it is often misunderstood in academic and legal circles.

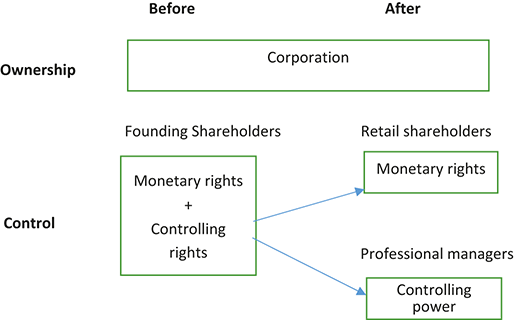

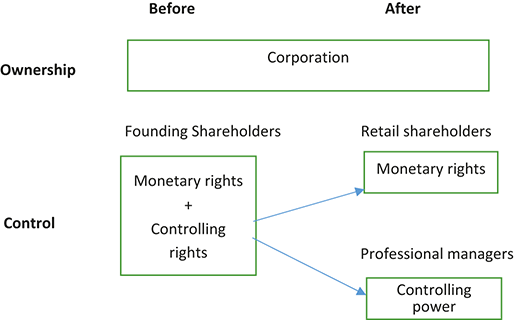

The phrase “separation of ownership and control” was popularized by Berle and Means (Reference Berle and Means1932), who described it as a historical process in which founders of major US corporations sold their shares to the public, leading to dispersed ownership in the early twentieth century. Their work became the canonical reference for discussions of ownership and control, almost a “bible” of corporate governance. For nearly a century, scholars and lawyers have adopted this interpretation, producing a vast body of literature based on it.Footnote 21

However, the term is incorrect – both legally and historically. The separation of ownership and control had already occurred in those US companies at the time of their incorporation. The change that took place in the late nineteenth and early twentieth centuries was the passing of control from founding shareholders to professional managers, as shown in Figure 6. During those decades, the founding shareholders sold their shares in the market and retired from management. But institutional shareholders hardly existed, and the shares were mostly purchased by individuals who were dispersed and only interested in the monetary rights attached to their shares – prospective dividends and capital gains. Those individuals lacked both the will and capacity to exercise control. The control thus passed to professional managers who had worked for the founders, and the US entered the era of “managerial capitalism.”Footnote 22

Ownership and control at the birth of managerial capitalism.

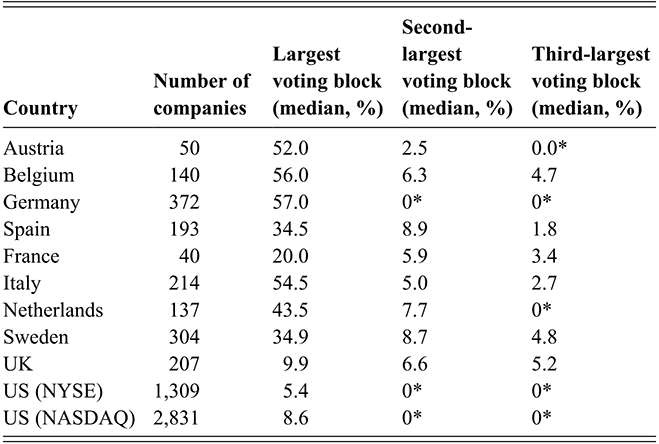

It should also be noted that the conventional claim about the dispersion of share ownership is exaggerated. Even in the US, it is doubtful that managerial capitalism is the dominant form. Approximately one-third of the companies listed are still controlled by major shareholders.Footnote 23 Among unlisted firms, the overwhelming majority are controlled by major shareholders. In numerical terms, corporations without major shareholders account for less than 0.2% of all US corporations.Footnote 24 Outside the US, even among large corporations, managerial capitalism is far from the norm – it is found mainly in the United Kingdom and rarely in continental Europe or in developing economies. It has never been a globally generalized phenomenon.Footnote 25

Furthermore, managerial capitalism has been in decline in the US in recent decades. Financial investors – pension funds, hedge funds, private equity firms, and mutual funds – have gained significant influence. These “minority shareholders” are no longer small and passive; they are now big and increasingly active.Footnote 26 As a result, professional managers no longer hold exclusive control. Managerial capitalism today looks markedly different from its earlier form.

Recognizing the problems in Berle and Means’s terminology, Robé (Reference Robé2011: 25–28) distinguishes between “the first separation of ownership and control,” achieved through incorporation, and “the second separation,” associated with the rise of managerial capitalism. Yet this distinction only adds confusion. The so-called “second separation” never actually occurred: ownership was already vested in the legal person at the time of incorporation (CT 1), and this structure remained intact even as control shifted from founding shareholders to professional managers in the late nineteenth and early twentieth centuries.

Accordingly, this study proposes corporate theorem 2 (CT 2): Ownership and control are fundamentally separated when a company is incorporated.” This is the other side of the coin to CT 1. The separation underpins entity shielding and limited liability and remains in place for as long as the corporation exists. As will be discussed later, understanding this fundamental separation is key to grasping the corporation’s purpose and behavior.

2.3 The Corporation Pursues Perpetuity

The wheels of incorporation, asset partitioning, entity shielding, and limited liability are designed to keep a company rolling for an eternity. They insulate corporate assets from the mortality of natural persons by vesting them in legal persons capable of perpetual existence. This legal foundation enables corporations to accumulate capital and prosper across generations. The story of Singer Manufacturing Co. illustrates this principle.

Isaac Merritt Singer was a renowned industrialist who, in 1851, produced the world’s first sewing machine for domestic use. He partnered with Edward Clark, a lawyer who had successfully defended his patents, to form I.M. Singer & Company. Their partnership flourished, and Singer, already wealthy, became even richer. But he led a complicated personal life, having several extramarital relationships and fathering numerous children, including eight with one long-term partner he never married.

Clark grew worried about the company’s future. What would happen after Singer’s death? He foresaw bitter legal disputes among Singer’s heirs over claims to his estate. Around this time, the corporate form was gaining traction in the US, and Clark began urging Singer to convert the partnership into a corporation. By transferring the business’s assets to an immortal legal entity, he argued, they could protect the firm from inheritance conflicts and ensure its survival beyond the founders’ lifetimes.

Under this structure, Singer’s heirs would receive shares rather than direct ownership of business assets. They would become passive shareholders, living on dividends or by selling their shares, while professional managers handled the company’s operations. Persuaded by Clark’s reasoning, Singer agreed, and in 1863, their partnership was incorporated as the Singer Manufacturing Co. After Singer’s death, professional managers continued to run the company, securing its continuity and its rise as a world-leading sewing machine brand.Footnote 27

Entity shielding through asset partitioning is a cornerstone of long-term corporate success. In traditional agrarian societies, the key productive asset – land – was typically divided among heirs, fragmenting holdings and hindering productivity growth over generations. By contrast, corporations preserve business integrity through asset partitioning: Founders’ family members inherit shares rather than pieces of the enterprise. These shares can be freely sold to relatives or outside investors without impairing the corporation’s continuity. As long as the corporation remains competitive, it possesses a legal foundation for indefinite growth, regardless of who holds its shares.

The corporation has historically evolved into an entity to pursue perpetuity by acquiring legal attributes such as ownership of property and the ability to sue and be sued. The notion of a legal person originated in Roman law.Footnote 28 Early corporate forms, which emerged in medieval Italy, “allowed for the pooling of capital, vesting its control in a manager and providing some sort of shelter limiting the liability of individual investors.”Footnote 29 In the eighteenth century, when the British East India Company was the world’s largest corporation, legal persons were clearly defined as “artificial persons, who may maintain a perpetual succession, and enjoy a kind of legal immortality.”Footnote 30

In modern times, the courts of Delaware State, where more than 60% of large US corporations are headquartered, continue to recognize the corporation as an entity designed for perpetuity. A vice chancellor, J. Travis Laster, notes “the existence of the typical corporation is perpetual and the capital provided by common and preferred stockholders … is permanent.”Footnote 31

Legal personality alone does not guarantee perpetual existence, of course. Exposed to market competition, a corporation may cease to exist if it fails to remain competitive. To survive and thrive, it must continuously innovate and remain competitive. This existential imperative (CT 4) will be discussed in the next section. Legal personality provides a necessary condition for perpetuity: Innovation and competitiveness supply the sufficient condition.

When Michael, Susan, and Collin incorporated My Love, they only dimly grasped these implications. They were unaware that Korean commercial law explicitly stipulates that “the corporate governance structure presupposes the separation of ownership and management.”Footnote 32 They would later come to appreciate the vital importance of asset partitioning for survival and growth – particularly after launching the overseas joint venture My Love Cutie and the affiliate My Love Children, transforming their company into a multinational business group.

2.4 The Legal Person Is a Real Entity

Despite the legal person’s importance, there is a strong tendency among academics and policymakers to dismiss it as a “fictional” or “artificial” entity. This view is particularly prominent among proponents of the nexus of contracts theory.Footnote 33 A seminal example is Jensen and Meckling (Reference Jensen and Meckling1976)’s “Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure,” a foundational text of shareholder value theory.

They wrote: “It is important to recognize that most organizations are simply legal fictions which serve as a nexus for a set of contracting relationships among individuals.” Here, the firm is treated as a fiction, while the contracts among individuals – inside and outside the firm – are seen as the real entities. They even claim: “it makes little or no sense to try to distinguish those things which are ‘inside’ the firm from those things that are ‘outside’ of it.”Footnote 34

However, dismissing the legal person as a fiction is equivalent to ignoring how human society actually functions. Though invisible and intangible, the legal person is a social reality essential to organizing economic activities. Around this conceptual entity, concrete transactions – labor contracts, production, financing, and exchange – are structured and executed. Corporate accounting itself presupposes that the corporation is a real entity.

This is no different from how nations, religions, and cultures, though conceptual, have evolved into powerful social realities. Likewise, the legal person, which began as a legal concept, has become a real social actor – owning property, incurring liabilities, and appearing as a responsible party in court, much like a natural person.Footnote 35 Thus, Jensen and Meckling’s assertion that the corporation is a fiction is itself a fiction.

For businesspeople, it is self-evident that the legal person is a real entity. The founders of My Love also come to grasp this reality through experience. Their managerial responsibilities are greatly simplified by the existence of the legal person. From the outset, they realize that corporate accounting depends entirely on it: All contracts and financial transactions are executed in the name of the legal person, and external auditors review financial statements prepared under its name.

Legal personality and corporate accounting are two sides of the same coin. As Gindis (Reference Gindis, Biondi, Canziani and Kirat2007: 266) aptly observes, the harmonious operation of a corporation’s components – working together as parts of one integrated whole – is held together by the “ontological glue” of business accounting. If the legal person were dismissed as a fiction or façade, business accounting would lose its foundation, and any substantive understanding of the corporation would be impossible.

2.5 The Corporate Board and the Shareholders’ Meeting

Recognizing the legal person as a real entity is also key to understanding the relationship between the corporate board and the shareholders’ meeting. Those who misunderstand the corporation’s legal structure make the mistake of viewing the shareholders’ meeting as the highest decision-making body and the board as its subordinate. This misconception arises when CTs 1, 2, and 3 are ignored or misunderstood. Shareholders are merely owners of shares – they possess certain rights, but not management rights.

Corporate laws worldwide consistently affirm that the board of directors is the corporation’s supreme decision-making body. The Delaware General Corporation Law (DGCL) stipulates that a company’s business and affairs “shall be managed by or under the direction of a board of directors.”Footnote 36 Similarly, Korean corporate law states that “the board of directors has authority to make decisions on all matters regarding a company’s business other than those reserved to the shareholders’ meeting by law or the articles of incorporation, and to supervise the performance of executives.”Footnote 37

The board’s authority derives directly from the process of incorporation, not from any delegation by shareholders. Through asset partitioning and entity shielding, shareholders enjoy limited liability, while the task of management is assigned to the corporation as a separate legal entity. Consequently, shareholders have no power to delegate corporate functions to the board. This principle was firmly established in early twentieth-century US jurisprudence. Several courts ruled that the board’s authority to shape corporate policies is “original and undelegated,”Footnote 38 or “the citation of authorities in its support is unnecessary.”Footnote 39

Similarly, the Supreme Court of Korea held that “the board of directors is an independent corporate body with its own authority, and, therefore, the shareholders’ meeting cannot make matters decided by the board’s unique authority null or void.”Footnote 40 If the shareholders’ meeting were the highest authority, it could overturn board decisions. But because the board is the top decision-making body, it is only natural that the shareholders’ meeting cannot overrule or nullify board decisions.

While recognizing the board as the highest decision-making authority, commercial laws grant limited rights to the shareholders’ meeting in four broadly defined areas. First, shareholders have the right to elect and dismiss directors. Second, they may revise or approve the articles of incorporation. Third, M&As or significant sales of corporate assets require shareholder approval. Fourth, dissolution of the corporation must be approved by the shareholders’ meeting.

Granting only these limited rights is appropriate because shareholders enjoy limited liability. In any organization, rights and responsibilities must correspond. This principle will be explored further as corporate theorem 8 (CT 8): “the basic principle of corporate control is the correspondence between rights and responsibilities.”

Given these clear distinctions between managers and shareholders, the term “owner-manager” is a misnomer. The correct term is “major shareholder-manager.” They do not own the corporation (CT 1) – only exercise control through a substantial shareholding. Such a shareholder becomes a manager only by entering into a contract with the corporation, just as any professional manager would. For the same reason, the expression “a corporation’s ownership has changed” is misleading. The legal person – the corporation – remains the perpetual owner of itself; what has changed are the majority shareholders who exercise control rights.

The shareholder value theory assumes that managers are agents of shareholders. Applied to shareholder-managers, this assumption leads to the absurd conclusion that they are their own agents. This paradox stems from treating the legal person as a fiction and imagining shareholders as corporate owners.Footnote 41 Once the corporation is recognized as a real entity, the paradox dissolves: both shareholder-managers and professional managers are agents of the corporation.

The distinction between managers and shareholders also clarifies why the shareholders’ right to appoint and dismiss directors should not be regarded as a management right. If it were, shareholders would bear responsibility for management performance just as managers do. Yet they are shielded from such responsibility. Therefore, their right to appoint and dismiss directors should be understood as a mechanism to protect their monetary rights, not a managerial right.

Since shareholder rights are not management rights, they are exercised “intermittently”, typically after business performance has been reported. As Arrow (Reference Arrow1974: 78) explains, “[Accountability mechanisms] must be capable of correcting errors but should not be such as to destroy the genuine values of authority … If every decision of A is to be reviewed by B, then all we have really is a shift in the locus of authority from A to B and hence no solution to the original problem.”

It is a general organizational principle to grant executives discretionary authority to manage operations, subject to periodic review. Simply intensifying oversight does not improve business performance; on the contrary, excessive surveillance can undermine executives’ competency and erode the authority required for effective decision-making, leaving the original problem unsolved. The same holds for the relationship between the corporate board and the shareholders’ meeting. The board exercises executive powers, while the shareholders’ meeting reviews and constrains them intermittently.

2.6 Hierarchy and Order in the Corporation

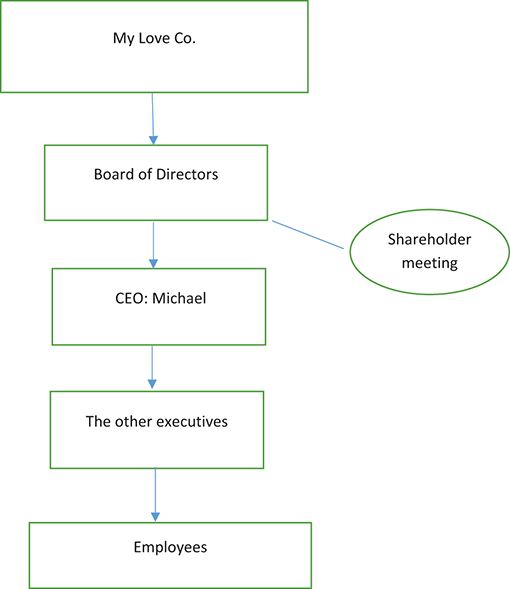

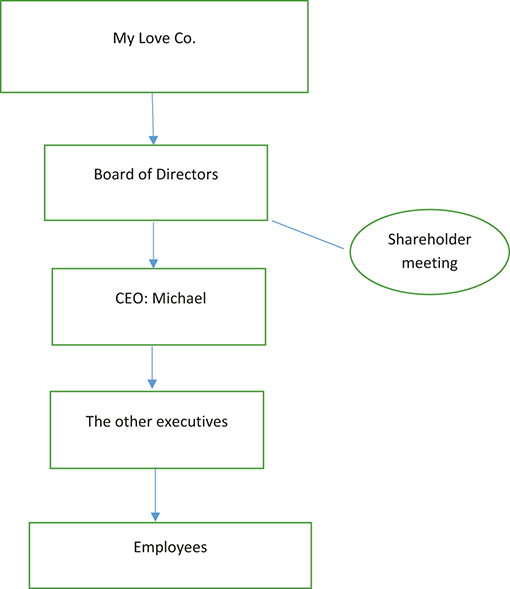

How, then, are management rights exercised in a corporation? To understand this, it is essential to recognize that a corporation is a hierarchical organization, with the board of directors at the top (Figure 7). Decision-making within the board, however, is not hierarchical. For instance, even if Michael serves as chair, he cannot force through a resolution opposed by Susan and Collin; board decisions are normally made by majority vote. But the majority rule ends there: once the board reaches a decision, everyone – including the CEO – must comply. This hierarchical principle extends throughout the organization, defining authority and accountability at every level of the corporation.

Hierarchical chart of My Love’s management.

Corporations adopt a hierarchical structure because it is best suited to managing the uncertainties inherent in business decision-making. As discussed in the next section, a manager’s existential task is to satisfy customers through innovation (CT 4). Innovation – creating “New Combinations” – is inherently uncertain and is often a bet on what appears to have a low probability. Most people tend to cling to “Old Combinations,” which are less risky and uncertain. If the decisions were left to majority vote, innovation would hardly occur. It requires strong leadership and judgment from individuals with experience and capability.

The role of hierarchy becomes clearer if we examine the employment contract. It is essentially “a contract of subordination” in which employees agree to follow the employer’s orders “in the sphere in which they accept to be subordinated,” or “in areas of acceptance,” in exchange for compensation.Footnote 42 The contract does not specify all the employee’s tasks in detail. This lack of specificity serves to protect both the employee and the employer from uncertain circumstances that may arise during employment.

At the time of hiring, employees cannot foresee every aspect of their future responsibilities. Only after they begin working for the corporation do they gain clarity about the scope of their tasks. They may also value the flexibility to explore different roles and responsibilities rather than being confined to specific tasks from the outset. Employers face similar uncertainties: Before observing employees’ actual performance, it is difficult to determine which role best suits them. They also need flexibility to reassign employees if their initial placement proves unsuitable. It is, therefore, more practical for an employment contract to be framed in broad terms of subordination, rather than attempting to specify every detail in advance.

Market-oriented theorists often overlook these uncertainties, treating the employment contract as a simple marketplace transaction of goods with perfect knowledge and bargaining conditions. For instance, Alchian and Demsetz (2009: 173–174) argue that “the content of the [employers’] presumed power to manage and assign workers to various tasks … [is] exactly the same as one little consumer’s power to manage and assign his grocer to various tasks,” even calling the view of the corporation as a hierarchical organization a “delusion.”

Their view is, however, a market fundamentalist delusion. One little consumer visiting a marketplace, asking to be shown this and that, and buying one item is a one-time event. It is an exchange in a world of little uncertainty and simply a market transaction, not a contract. Contracts are signed only when necessary, as in the case of employment arrangements, where uncertainty is significant. Yet, the nexus of contract theorists obliterates the distinction between a market transaction and a contract and calls the former a “contract.”

My Love needs many electronic engineers for design and production activities, but does not want to limit their role to electronic engineering. Its products and services integrate diverse disciplines – electronics, data science, biology, and material science. The company benefits when electronic engineers expand their knowledge across fields. Newly hired electronic engineers may also seek to broaden their experience beyond the field they majored in at university, in order to enhance their promotion prospects. Restricting their roles to their initial specialization would run counter to both innovation and personal development.

2.7 Business Judgment Rule

To what extent are managers held responsible for their managerial failures? A principle that has been firmly established for over a century is the “business judgment rule.”Footnote 43 Under this rule, as long as executives fulfill their fiduciary duties of good faith, loyalty, and care, they are not liable to litigation for managerial failures. Managers are, of course, dismissed or penalized for poor performance. But managers are only legally accountable if they are found to have harmed the corporation by violating their fiduciary duties.

The business judgment rule is a necessary safeguard, enabling corporate managers to focus on fulfilling the corporation’s existential imperative: remaining competitive by satisfying customers through continuous innovation (CT 4). For innovations to materialize, managers must be willing to take calculated risks. If they were held legally accountable for business failures, they would become risk-averse, ultimately stifling innovation. In this context, Bainbridge (Reference Bainbridge2002: 67) points out that “the business judgment rule is the offspring of the fundamental principle [that] … the business and affairs [of a corporation] are managed by or under its board of directors,” and it “exists to protect and promote the full and free exercise of the managerial power.”

The founders of My Love have yet to fully grasp the importance of the business judgment rule. At this stage, they own 100% of the shares, serve as directors and top executives, and exercise absolute control. They work collaboratively, sharing the same fate, and it is difficult for any one of them to hold another legally accountable for mishandling the corporation’s affairs. If something goes wrong with My Love, they collectively feel responsible.

However, as new shareholders join following a stock market listing, the business judgment rule will become invaluable to them. For example, suppose My Love invests heavily in a new product that ultimately fails. Its stock price plummets, causing significant losses to new shareholders. What happens if they sue Michael? As founder and CEO, Michael has made numerous contributions to the company, and this failure might be one of only a few missteps in his career. The cofounders and long-term investors might overlook this rare mistake. But new shareholders are not so forgiving. They may focus on recovering their losses or penalizing those they deem responsible.

Without the business judgment rule, lawsuits against management could arise frequently, incurring substantial costs in terms of money, time, and energy – resources better spent on running the business effectively. If Michael were to face such a lawsuit, he might become overly cautious in his decision-making. This would seriously undermine My Love’s innovation capabilities. The business judgment rule shields Michael from this pressure, allowing him to focus on innovation.

3 The Ontological Foundation and Purpose of the Corporation

When Michael, Susan, and Collin launched My Love, they never paused to ponder the philosophical question of why corporations exist. For Michael and Susan, their initial motivation was simple: to make money – ideally a fortune. They could have led stable lives in academia or industry as salaried professionals, but wanted to be successful entrepreneurs, to taste the excitement and prestige that come with building something extraordinary. Collin, already wealthy, was less driven by money. He was already well-off. It would still be fun to multiply his wealth. But he was more thrilled by the prospect of gaining recognition as a successful venture capitalist.

Yet the fun and glamour are now distant dreams. The existential tasks are taking over their lives. My Love must survive. It needs to secure patents, test prototypes, ramp up production, and launch its AI puppies. Michael knows speed is everything in business. The story of how Bill Gates and Paul Allen developed an operating system on the flight to meet their first customer, Ed Roberts, the founder of Micro Instrumentation and Telemetry Systems, made a deep impression on him.Footnote 44 So he applies for patents and starts preparing production simultaneously rather than waiting for the patents to be approved. My Love is in a race against time to release its AI puppies and capture the market ahead of competitors.

3.1 Customer Satisfaction through Innovation

Our Corporate Axiom 2 is the existence of market competition. What are businesses competing for? In a word – customers. They must attract and retain customers by satisfying their needs. Without customers, corporations cannot survive. “The customer is King.” Before the rise of the shareholder value and stakeholder theories in the 1980s, business thinkers and practitioners widely regarded customer satisfaction as the very purpose of the corporation.

Peter Drucker (Reference Drucker1954/2006: 31–32) famously stated: “There is only one valid definition of business purpose: to create a customer. The purpose of business is to create and keep a customer.” Sam Walton, founder of Walmart, echoed his view, “There is only one boss – the customer. And he can fire everybody in the company from the chairman on down, simply by spending his money somewhere else.”Footnote 45

This fundamental dependence on customers is expressed in corporate theorem 4 (CT 4): The existential imperative of the corporation is to satisfy customers through innovation. Corporate theorem 4 naturally follows from CT 3: The only sustainable path to achieving corporate perpetuity in a market economy is to satisfy customers through innovation. Having a legal personality is a necessary condition for perpetuity; satisfying customers through innovation is a sufficient condition.

However, meeting this sufficient condition is far from easy. In the US, the average lifespan of large corporations was sixty-one years in 1958 and dropped to eighteen years by 2016.Footnote 46 Out of the 500 largest companies in 1955, only fifty-three remained on the list in 2018.Footnote 47 Corporations are in relentless struggles for innovation to survive the competitive hell. Yet, this “hell” for corporations becomes a “heaven” for customers, as the competition provides customers with a diverse array of products and services.

We should prioritize the ontological foundation for corporate survival over corporate teleology – the question of whom the corporation serves.Footnote 48 The reason is simple: The ontological foundation is straightforward and indisputable, whereas teleological perspectives vary widely, from shareholder value to stakeholder theory. Framing the question “Why corporations exist” in teleological terms makes it difficult for people with differing values to find common ground.

By contrast, beginning from the ontological foundation offers a common ground from which agreement – or at least constructive compromise – can emerge. Few would deny that a corporation survives and prospers by satisfying customers through innovation (CT 4). Customer satisfaction can therefore be recognized as the immediate and primary purpose of the corporation, a shared starting point for any broader discussion of corporate purpose.

It is important to note that CT 4 is not merely an existential necessity; it already embodies a major part of the corporation’s social contribution. While corporations endure the “hell” of competition, they deliver the “heaven” of consumer welfare. In doing so, they create jobs, enhance employee well-being, support contractors, generate profits that increase shareholder value, and contribute to wider economic and social development.

3.2 Business Group and Multinational Corporation

My Love has made rapid progress. Within just one year, it successfully secured all the necessary international patents and developed a prototype AI puppy named “Dasomi.” Dasomi has since been showcased at several AI exhibitions and pet fairs. Although some organizers objected to an AI puppy’s participation, it was overwhelmingly well-received. Enthusiasm about Dasomi’s upcoming release is palpable, and My Love is flooded with purchase orders and partnership inquiries.

Having confirmed the strong market demand for Dasomi, My Love is now ramping up its production. To offer the product at an affordable price – below $500 for the mass market – it must produce at least 10,000 units annually. It also plans to diversify its product line to include AI cats, monkeys, and panda bears. Jeremy, the CFO, estimates that approximately $50 million will be required to build production facilities, invest in R&D, and establish sales networks.

Impressed by the excitement around Dasomi, a venture capital firm, Homo Deus offers $50 million for a 30% stake in My Love – valuing the company at eleven times its original share price. Homo Deus also requests the right to appoint a CFO. Following this investment, My Love’s shareholding structure is reconfigured, as shown in Figure 8.

The ownership structure of My Love after the first external funding.

My Love successfully scales up production of Dasomi. Advances in biotechnology and material engineering make sourcing materials for Dasomi’s fur and skin easier than expected. Susan and her team work tirelessly to make Dasomi’s skin soft and lifelike, while Michael develops technologies that dramatically enhance the puppies’ emotional communication with humans. My Love also begins building its sales force, opening direct sales outlets in affluent districts populated by wealthy and young professionals, while relying on sales agents elsewhere.

One salesperson proposes an ingenious idea – launching a beta test website called the “My Love Puppies (MLP) Community” before the official release. Members can interact with a holographic Dasomi in a virtual environment. Although they cannot physically touch it, they experience its 3D presence and can engage with it virtually. MLP Community members, having a virtual preview of Dasomi, are expected to become enthusiastic buyers and brand ambassadors, spreading excitement among friends and family. The proposal is unanimously adopted.

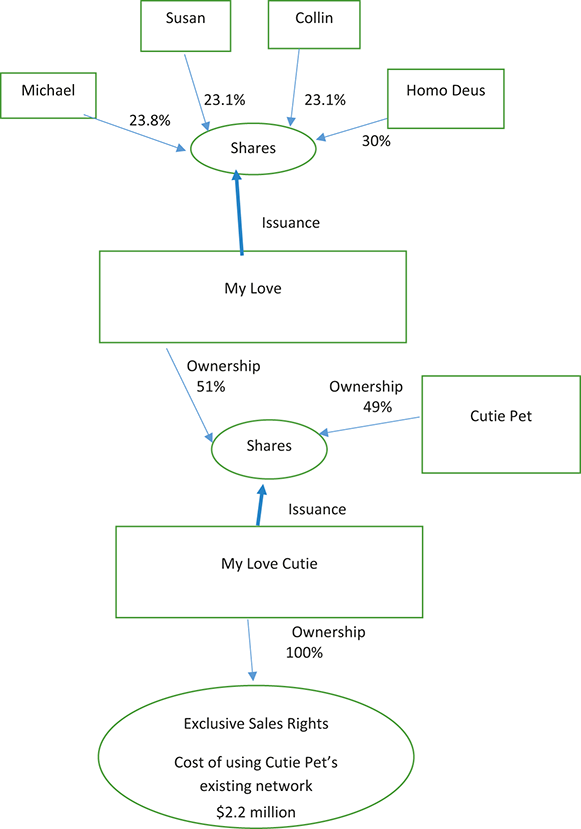

My Love is eager to expand overseas. However, building international sales networks from scratch is costly and risky, so the company begins searching for foreign partners. At a pet show, a US company, Cutie Pet, proposes to acquire exclusive distribution rights for the American market. Michael, however, envisions more than just sales – he wants to build manufacturing facilities in the world’s largest market and technology testbed. He counters with a proposal to establish a joint venture.

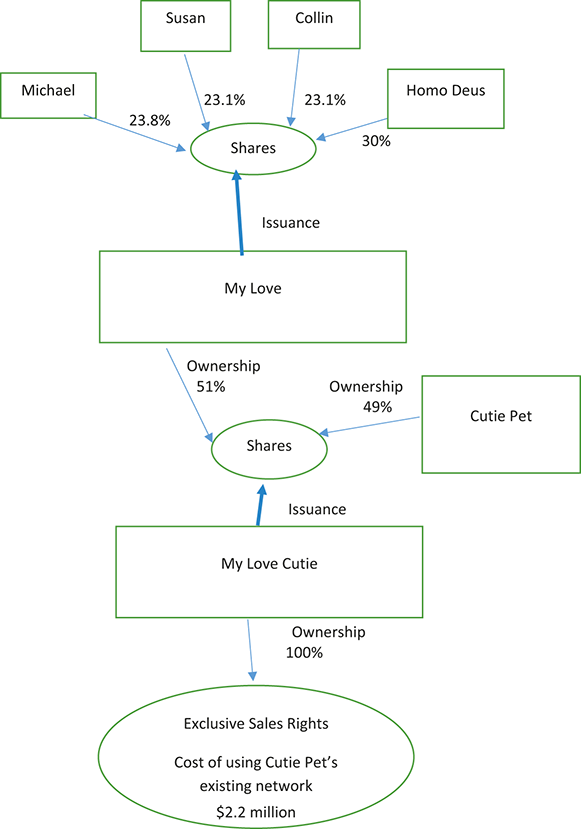

After intense negotiations, the two sides reach an agreement: My Love will hold 51% of the joint venture, named My Love Cutie Co., and Cutie Pet the remaining 49%. My Love Cutie will hold exclusive rights to sell My Love products in the US for five years. Cutie Pet will invest $2 million to establish the venture and its sales network, while My Love will second a manager from Korea to My Love Cutie for the first year at a cost of about $200,000. The board will comprise three members – one from My Love and two from Cutie Pet – with the president selected from Cutie Pet-appointed executives. By forming this joint venture, My Love becomes a multinational business group even before launching its first product. Linked through shareholdings, My Love Co. and My Love Cutie Co. now constitute a business group, as shown in Figure 9.

My Love Group after the first asset partitioning.

An important feature of this group structure is that the affiliates are created through asset partitioning. My Love divides its corporate assets and permanently transfers a partitioned portion to My Love Cutie. In return, My Love receives shares issued by My Love Cutie. A key difference from My Love’s initial incorporation process is that this time, the partitioned assets originate from a corporation, not natural persons.

Yet the same wheel turns: incorporation, asset partitioning, entity shielding, and limited liability. My Love is shielded by limited liability from My Love Cutie’s business risks. If My Love Cutie fails, My Love’s maximum loss is limited to the five-year exclusive sales rights and the $200,000 secondment expenses. In the same way, entity shielding protects My Love Cutie from My Love’s liabilities.

This principle – creating an affiliate through asset partitioning – applies equally to overseas expansion. Establishing a foreign subsidiary makes a company both a business group and a multinational corporation. Thus, when My Love forms the joint venture My Love Cutie, it becomes both. This logic underpins corporate theorem 5 (CT 5): Business groups expand through asset partitioning among corporations, just as new corporations are created through asset partitioning by natural persons.

Just as natural persons have varying relationships – with family, friends, colleagues, or strangers – corporations interact with one another in different ways. Some corporations are closely connected, while others are loosely affiliated. Some operate domestically, while others expand overseas. A corporation may have first-tier subsidiaries (children) and second-tier subsidiaries (grandchildren), or it may choose to remain independent. In a nutshell, corporations develop varied relational networks shaped by strategy, geography, and degrees of interconnection.

3.3 Perpetual Innovation and Corporate Expansion

Dasomi finally launches, igniting a frenzy among consumers. Eager to own one, people line up outside My Love’s flagship showroom in Myeong-dong, Seoul. Demand far exceeds production capacity. Amazon, initially lukewarm when My Love first approached, now offers to feature Dasomi on its homepage. Meanwhile, the MLP Community buzzes with excitement. Owners share their joy and pet care tips, while others – still waiting – interact with holographic Dasomis, eagerly anticipating the day they can welcome a real one.

Yet Michael is not satisfied with Dasomi’s success. His ambitions stretch far beyond AI pets. Working secretly with Susan, he develops a new product under the code name MLBMLG – short for My Love Boy, My Love Girl. Their goal is to create robot babies indistinguishable from human infants. They know the storm this will unleash. Critics will accuse My Love of “destroying human dignity” or “creating a new robot species destined to dominate humanity.” Some will warn that such robots could “be misused as sex robots.”Footnote 49 Protests outside My Love’s headquarters and large-scale boycotts appear inevitable.

Despite the looming controversy, Michael remains confident in MLBMLG’s potential. He envisions it as a low-cost, high-quality alternative to raising a human child. Many people who love children are choosing not to become parents because of the financial burden of private education or the pressures of child-rearing in hypercompetitive societies. Others struggle with infertility due to delayed marriage or medical complications. For them, MLBMLG could fulfill their longing for parenthood.

Families with children could welcome an AI son or daughter to bring new warmth into their homes. Singles could experience the joy of raising a child without the heavy obligations of marriage, and the elderly might rediscover purpose and comfort in caring for an AI baby – almost like an extra grandchild. Michael believes that nurturing an MLBMLG will be a profoundly human experience – more so than raising a pet. He is convinced that these AI children will not only possess intelligence but also develop a soul that grows and matures over time, much like their physical form.

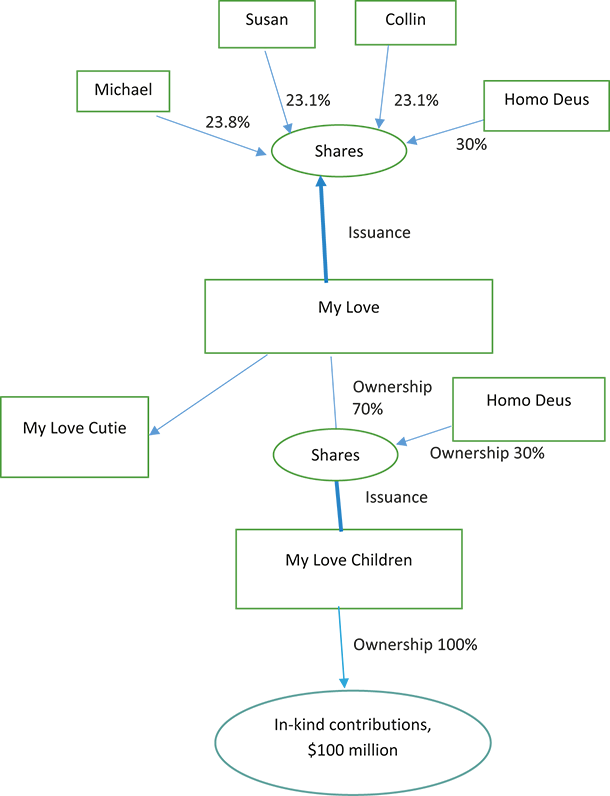

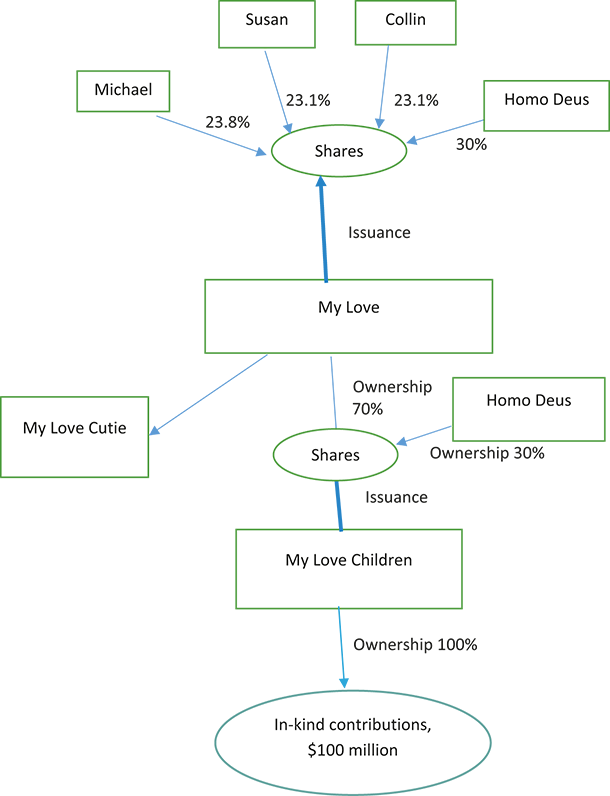

With this in mind, My Love’s leadership convenes a secret meeting and secures board approval to establish a separate corporation, My Love Children Co. Homo Deus eagerly joins the project. My Love already possesses most of the technologies required to produce MLBMLG. My Love Children will utilize My Love’s established sales and marketing networks, production sites, and talented employees – many of whom are eager to join the new venture.

Negotiations with Homo Deus move swiftly. My Love contributes technology, production facilities, and marketing networks in kind, while Homo Deus invests $100 million. They agree on a share distribution of 70% for My Love Co. and 30% for Homo Deus. With this structure, the My Love Group evolves into a multinational business conglomerate, comprising three subsidiaries: My Love, My Love Children, and My Love Cutie – as shown in Figure 10.

My Love Group’s structure after the second asset partitioning.

Note: The relationship between My Love and My Love Cutie is simplified.

3.4 Diversification, Economies of Scope, and Asset Partitioning

Why has My Love chosen to form a business group at the very beginning of its expansion? Why has it opted to add subsidiaries rather than grow the existing company? To answer these questions, let us first examine the options available to an existing company for expanding its business. There are only three options:

(1) Diversification by establishing an entirely new, independent corporation.

(2) Diversification by creating a new business division within the existing corporation.

(3) Diversification by setting up a subsidiary corporation controlled by the existing corporation.

Nascent entrepreneurs can only choose Option (1), as they have no existing corporation to leverage. In contrast, an established corporation can build on its accumulated capabilities, assets, and reputation to pursue Options (2) or (3). The general rationale for preferring these latter options lies in the concept of economies of scope – the efficiency gained from using shared resources and capabilities across related businesses. Option (3) offers an additional advantage: It combines economies of scope with the benefits of asset partitioning, enabling legal separation of risks while maintaining operational synergies.

“Economies of scope” can be divided into two types: nonfinancial and financial economies of scope. The former arises when a corporation reuses its existing technological, managerial, and marketing capabilities for new ventures. My Love, having developed advanced technologies for AI puppies, can apply many of them to AI children. This can be done either by forming a new business division within the company (Option (2)) or by establishing a subsidiary (Option (3)). Both save substantial time and cost compared to Option (1).

Reputation and branding also generate nonfinancial economies of scope. A new business team established within an existing corporation can naturally benefit from the company’s reputation and brand. Similarly, if My Love sets up My Love Children as a subsidiary, My Love’s reputation and brands are great assets that the new company can leverage. Consumers who trust My Love’s products and services are likely to extend that trust to My Love Children’s offerings.

Financial economies of scope operate through a similar mechanism. It is challenging for an independent new corporation to secure funding from external sources because it typically lacks creditworthiness in financial markets. This is why My Love was initially funded with Collin’s money. In contrast, existing corporations have the flexibility to choose Option (2) or Option (3). A new business team simply uses its company’s credit. A subsidiary corporation can leverage the parent company’s credit. Financial institutions are generally more willing to support subsidiaries if they have confidence in the parent company. If the parent company guarantees its subsidiary’s debts, it becomes significantly easier for the subsidiary to secure external funding. In other words, My Love’s creditworthiness is recycled in My Love Children. This is why Homo Deus confidently agrees to invest $100 million in My Love Children.

Corporations will choose Option (3) rather than Option (2) when they seek additional benefits from asset partitioning. If a new business team established within a company fails, the company must assume unlimited liability, potentially being pushed into a financial crisis. Option (3) offers a structured way to manage risks to the parent company through entity shielding and limited liability.

My Love has already achieved success with its AI puppies, and diversification into other AI pets is relatively low risk. Option (2) works well for such cases. But diversification into AI children entails far greater risks and requires careful strategic consideration. The most serious risks stem from public apprehensions about AI children – concerns that are likely to intensify as they become more humanlike. Potential threats include large-scale public boycotts, governmental restrictions, or even an outright ban on AI children production.

Without entity shielding, banks that lent to My Love would become increasingly cautious, shareholders would grow uneasy, and employees might lose focus amid looming risks – undermining morale and productivity. Establishing My Love Children as a subsidiary (Option (3)) is an effective way to limit My Love’s exposure to these risks.

Option (3) also provides significant advantages in developing new businesses because the legally independent subsidiary is less distracted or overshadowed by the parent company’s ongoing priorities. AI children require far more sophisticated technologies than AI puppies because they must develop intellectually, which requires continuous research in language algorithms and big data integration. Yet My Love’s engineers remain focused on the physical and emotional development of AI pets – the company’s current profit center. If the AI-children project were to remain within the parent company, it would risk being treated as peripheral, limiting both motivation and innovation.

Michael vividly remembers how Intel began its journey – a story he learned in the “Technology and Innovation” lecture as an exchange student at the National University of Singapore.Footnote 50 Gordon Moore and other semiconductor engineers were pioneers in their field and proud of their work. However, within AT&T, the focus was on telecommunications, and semiconductors were treated as a peripheral business. US antitrust regulations also prevented AT&T from selling semiconductors on the open market, restricting its semiconductor production to internal consumption.

These constraints severely hindered the semiconductor engineers’ prospects of promotion to executive positions within AT&T. Frustrated by these limitations and driven by their ambition, Moore and his colleagues left AT&T and eventually established Intel – a significant loss for AT&T. Michael has fully grasped the lesson: For innovative, high-risk ventures such as AI children, it is better to establish an independent entity that can focus on its unique technological and strategic goals without being overshadowed by the parent company’s priorities.

Establishing a subsidiary corporation is also an effective way to maintain corporate control. If My Love were to receive another large-scale capital injection from Homo Deus, it would destabilize the company’s control structure. The founders’ shares would be diluted, and Homo Deus could potentially become the largest shareholder. The founders, therefore, wish to retain control over My Love while still securing funding from Homo Deus.

The solution to this dilemma is to establish a subsidiary – My Love Children – and let Homo Deus invest in the subsidiary. As a venture capitalist, Homo Deus has repeatedly emphasized that it does not seek managerial control. So there is no issue with its investment in My Love Children, as it expects a sufficiently high return on investment from the new company. Managing a business is fundamentally about navigating uncertainty. A sound strategy is to prepare multiple options and maintain flexibility in response. The same applies to diversification: Options (2) and (3) remain open, and the corporation chooses between them after weighing internal and external factors.

Michael has made it a rule since founding My Love to sit in interviews with new applicants as much as possible. When My Love Children begins hiring employees, he is in the interview room as usual, listening to the conversations between interviewers and candidates.

During one session, an interviewer raises his voice with an applicant. The company requires male applicants to have completed military service, yet Brian Choo, a fourth-year student at Seoul National University, has not done this. “How could an educated man like you apply for a job without checking the requirements?” the interviewer scolds. Brian calmly replies, “Wouldn’t it be beneficial for both of us if you hire me now? I’ll begin my ROTC (Reserve Officers’ Training Corps) service right after graduation. If you hire me in advance, you’ll secure a capable employee for three years without any cost in the meantime. I can spend my spare time in the army preparing to work at my favorite company, where I’ve already earned a position.”

The interviewer is momentarily speechless. Michael interjects decisively: “You’re hired!” He then asks when Brian’s military service will begin. “I’m in my final semester, just a few months from graduation,” Brian answers. “Then you don’t need to attend classes so diligently anymore,” Michael tells him. “Come and start working here tomorrow. Learn the ropes before you enter the army.” Brian Choo thus becomes the first full-time employee at My Love Group to be hired before graduating from college. After completing his ROTC service, Brian will return to the company and eventually rise to become one of My Love Group’s most successful professional managers.Footnote 51

4 The Teleology of the Corporation

My Love Children grows rapidly, just as My Love once did. It maintains a first-mover strategy – developing the most humanlike AI children – focusing particularly on mental and intellectual growth. While competitors sell AI children with fixed emotional and cognitive levels and later offer upgrade services, Michael takes a different path. He is determined to create an algorithm that enables gradual mental and intellectual development, mirroring the natural growth of human children.

To achieve this, Michael launches a global headhunting drive, recruiting top AI designers and neuroscientists, who work tirelessly and eventually succeed in creating two AI children – “Minjun” and “Songi.”Footnote 52 Like real children, these two grow and learn over time. Their debut at the World Artificial Intelligence Congress draws global attention, and Time magazine names them “Persons of the Year.”

When they founded My Love Children, My Love and Homo Deus agreed on an exit plan allowing investors to sell their shares after five years. As the valuation of My Love companies soars, many Homo Deus clients seek to realize their gains. Collin, still recovering from heavy derivatives losses, also wishes to sell his shares. Susan, facing declining health, decides to liquidate part of hers and transition to a quieter life.

4.1 Initial Public Offerings (IPOs)

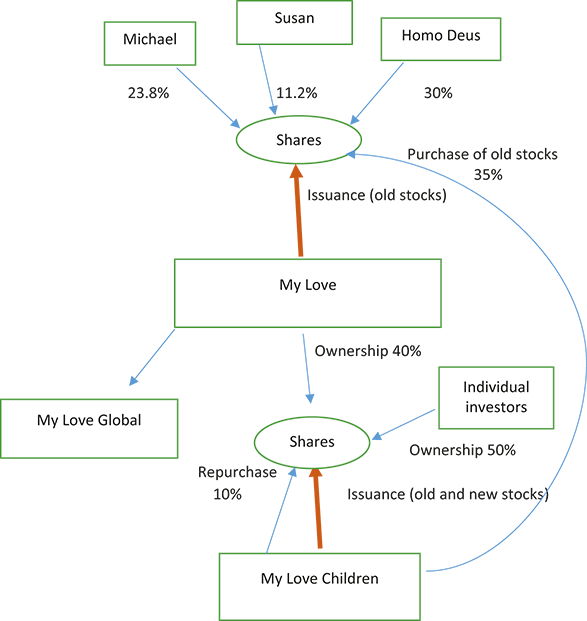

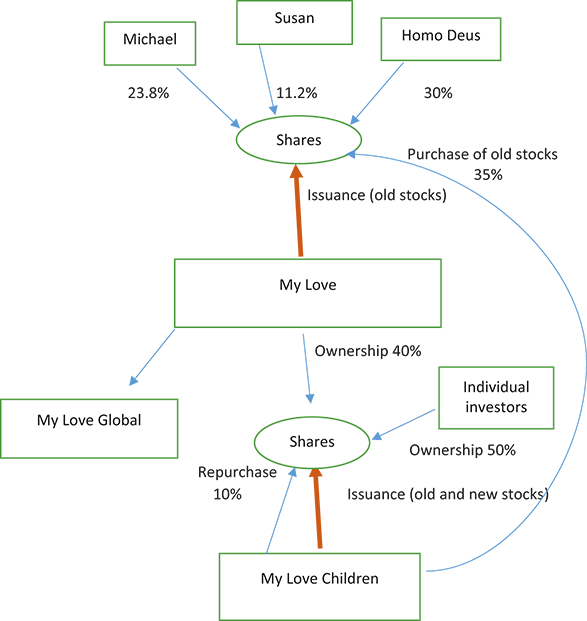

My Love Group decides to list My Love Children on the stock exchange. My Love Co., the group’s operational holding company, remains unlisted. Homo Deus plans to sell its 30% stake in My Love Children through the IPO. Susan and Collin will be compensated via stock swaps: My Love Children will purchase their shares in My Love using funds raised from the new share issuance. The swap ratio between My Love’s old stock and My Love Children’s new stock is set at 1:1.

Under Korea Stock Exchange (KSE) regulations, no shareholder may hold 50% or more of a listed company’s shares. Accordingly, My Love reduces its 70% stake in My Love Children to 40% by issuing and selling new shares on the market. The proceeds are primarily earmarked for future investments, with a portion allocated to purchase Collin’s and Susan’s shares in My Love. At the same time, My Love Children uses part of its newly raised capital to repurchase 10% of its shares, which are reserved for stock options, stock awards, and an Employee Stock Ownership Plan to attract and motivate top managerial and engineering talent.

The listing of My Love Children is an instant market sensation. Its share price hits the daily upper limit for ten consecutive days. Following the IPO, My Love Group’s ownership structure changes dramatically (see Figure 11). Most notably, financial investors now hold 50% of My Love Children’s shares – a shift that introduces new dynamics and potential tensions between financial investors and corporate management over goals, governance, and the use of retained earnings.Footnote 53

My Love Group’s shareholding structure after the IPO.

Another notable change is the emergence of cross-shareholding between My Love and My Love Children. My Love holds 40% of My Love Children’s shares, while My Love Children owns 35% of My Love’s shares. This structure is adopted as the most practical way of reconciling the differing needs of shareholders, while simultaneously promoting a long-term perspective and safeguarding the group against potential hostile takeovers.

4.2 The Reality of the “Contract” at the IPO

Michael had a multidimensional view about the purpose of the corporation when he founded My Love. Making a lot of money was, of course, part of his thinking. But he was also interested in exploring and creating new things, as he had been from his younger days. For him, the process of developing AI pets and children was itself exciting. And he believed that My Love would enhance people’s happiness by offering affordable and high-quality products that met their needs. Neither Michael nor Susan would have set up a company whose profit came from making people unhappy.

Their outlook remains unchanged after the IPO. They have already earned enough money to live comfortably – indeed luxuriously. But they do not want to step away. This is not because they are waiting for their share value to maximize before selling out. They enjoy the thrill of achieving what others cannot and are proud of being recognized as successful entrepreneurs. Michael and Susan cannot imagine their future without My Love Group. They assume that other managerial shareholders feel the same way about their companies and their lives.

Those who buy My Love Children’s shares after the IPO, however, view the corporation through a different lens. They are primarily financial shareholders – institutional investors and retail traders – whose chief objective is to earn the highest possible return on investment. Their interest in the corporation extends only as far as its performance influences the market value of their shares. Unlike corporate managers, who devote their full-time effort to a single enterprise, financial shareholders diversify their capital across multiple firms and manage diversified portfolios.

Naturally, they expect managers to focus on raising share prices, and the shareholder value theory mirrors this collective expectation. It is true that, once a company goes public, its stock price becomes an important indicator that management cannot ignore. Yet it is not true that a corporation’s purpose is thereby reduced to maximizing shareholder value. Its most fundamental task remains to satisfy customers through innovation – fulfilling its existential imperative (CTs 3 and 4). Furthermore, founders typically build corporations with broader goals in mind. The founders of My Love may not have defined a specific “social mission,” but they firmly believe that running their business itself constitutes a meaningful contribution to society.