1. Introduction

Optimal insurance contract theory has been one of the research hotspots in actuarial science. An individual bargains with an insurer to design an insurance contract, which typically consists of an indemnity function (coverage) and an upfront premium. Most papers in actuarial science on optimal insurance focus on stop-loss indemnities, as they are often shown to be optimal; see, for example, Arrow (Reference Arrow1963), Van Heerwaarden et al. (Reference Van Heerwaarden, Kaas and Goovaerts1989), Gollier and Schlesinger (Reference Gollier and Schlesinger1996), Gollier (Reference Gollier and Dionne2013), and Chi et al. (Reference Chi, Hu, Zhao and Zheng2024). However, a stop-loss indemnity covers losses above a pre-determined deductible, which can lead to moral hazard. Once the deductible is exceeded, the insured may lack incentives to mitigate further losses (Drèze and Schokkaert Reference Drèze and Schokkaert2013). As an alternative, coinsurance is popular, where the insured covers part of the incremental losses. A common form of coinsurance is proportional insurance. Therefore, this paper focuses on the design of proportional insurance contracts.

Many optimal insurance models rely on the insurer’s indifference pricing or equilibrium arguments. Boonen and Ghossoub (Reference Boonen and Ghossoub2023) show that competitive and Bowley equilibria make the insurer or insured indifferent between insuring or not insuring. As a direct alternative, the asymmetric Nash bargaining solution can guarantee that both parties strictly benefit from the insurance transaction (Kalai Reference Kalai1977). The asymmetric Nash bargaining solution, which generalizes the Nash bargaining solution introduced by Nash (Reference Nash1950), is characterized by Kalai (Reference Kalai1977). More specifically, the Nash bargaining solution is obtained by maximizing the product of the excess utilities of the two parties over the status quo. The asymmetric Nash bargaining solution removes the symmetry axiom from the axiomatization of Nash (Reference Nash1950). This allows for assigning particular powers to the excess utilities, which can be interpreted as the bargaining power of each agent.

In this paper, we investigate the asymmetric Nash bargaining on a proportional insurance contract between a risk-averse insured and a risk-averse insurer,Footnote 1 where the insurer’s initial wealth, subject to fluctuations from existing business operations, is considered random. Following von Neumann and Morgenstern (Reference von Neumann and Morgenstern1953), we assume both agents maximize expected utility. We fully characterize the Pareto optimality of the status quo by introducing a condition. If this condition is not satisfied (i.e., the status quo is Pareto dominated), we derive the optimal asymmetric Nash bargaining solution. If the utility functions of the two agents exhibit decreasing absolute risk aversion (DARA), we show that both the optimal insurance coverage and the optimal insurance premium increase with the insurer’s bargaining power and the degree of the insured’s risk aversion when the insurer’s initial wealth is decreasing with respect to the insurable risk in the sense of reversed hazard rate order. For an insured with an exponential utility function, the optimal insurance coverage increases with the insurer’s constant initial wealth.

This paper is related to Chi et al. (Reference Chi, Hu, Zhao and Zheng2024), who also study Nash insurance bargaining solutions. However, we differ in two fundamental ways. First, we allow for risk aversion of the insurer, while Chi et al. (Reference Chi, Hu, Zhao and Zheng2024) restrict the insurer to be risk neutral. As a result, we get that once the insurer’s initial wealth is negatively dependent with the insurable risk, full insurance cannot be optimal even if the deadweight cost is set to be zero, which contrasts with Chi et al. (Reference Chi, Hu, Zhao and Zheng2024). Second, we focus on proportional insurance treaties, while Chi et al. (Reference Chi, Hu, Zhao and Zheng2024) study stop-loss arrangements. Under the assumption of proportional insurance treaties, we can show that the set of feasible Nash bargaining outcomes is convex such that we can use the characterization of asymmetric Nash bargaining solutions in Kalai (Reference Kalai1977). To be specific, he shows that the asymmetric Nash bargaining solution is the unique solution that satisfies the following four properties: Feasibility, Invariance under change of scale of utilities, Independence of irrelevant alternatives, and Pareto optimality. Three of these properties are clear and intuitive requirements, but only the Independence of irrelevant alternatives can be argued about. This property requires that if some feasible insurance contracts that are not equal to the bargaining solution are removed from our feasible set, then the solution will not change. In other words, removing feasible contracts (other than the bargaining solution) from the feasible set does not alter the solution. Notably, in the bargaining literature, it has been replaced to obtain other bargaining solution concepts, such as the Kalai–Smorodinsky solution (Kalai and Smorodinsky Reference Kalai and Smorodinsky1975). It should also be emphasized that Nash bargaining under other model settings has been extensively studied. Alternative characterizations of the Nash bargaining solution based on non-cooperative games are provided by van Damme (Reference van Damme1986), Britz et al. (Reference Britz, Herings and Predtetchinski2010), and Okada (Reference Okada2010). In a risk-sharing context, Aase (Reference Aase2009) studies the Nash bargaining solution and compares it with the competitive equilibrium. In the context of optimal reinsurance, Boonen et al. (Reference Boonen, Tan and Zhuang2016) and Anthropelos and Boonen (Reference Anthropelos and Boonen2020) study asymmetric Nash bargaining solutions with distortion risk measures, and Anthropelos and Boonen (Reference Anthropelos and Boonen2020) show that it is important for the risk measures to be known by market, as agents have an incentive to misrepresent their risk measures. Moreover, Zhou et al. (Reference Zhou, Li and Tan2015) and Boonen et al. (Reference Boonen, De Waegenaere and Norde2017) study applications to longevity risk transfers with the Nash bargaining solution. Similar to these studies, this paper advances the exploration of Nash bargaining applications in insurance and risk management.

The remainder of this paper is organized as follows. Section 2 defines a proportional insurance contract and provides a brief introduction to the asymmetric Nash bargaining solution. Section 3 provides our main results on the optimal proportional insurance under asymmetric Nash bargaining. Section 4 conducts comparative statics analysis. Section 5 presents detailed examples illustrating our theoretical results. Section 6 concludes, and all the proofs are delegated to the appendix.

2. Model setup

2.1. A proportional insurance contract

An individual endowed with initial wealth

$w_0$

faces an insurable risk X, interpreted as a loss. The risk X, defined on a probability space

$w_0$

faces an insurable risk X, interpreted as a loss. The risk X, defined on a probability space

$(\Omega, \mathcal{G},\mathbb{P})$

, is a non-negative, bounded random variable with an essential infimum of 0 and an essential supremum of

$(\Omega, \mathcal{G},\mathbb{P})$

, is a non-negative, bounded random variable with an essential infimum of 0 and an essential supremum of

$M\gt 0$

.Footnote

2

To reduce her risk exposure, she purchases a proportional insurance contract with indemnity

$M\gt 0$

.Footnote

2

To reduce her risk exposure, she purchases a proportional insurance contract with indemnity

$I_\theta(x)\,:\!=\,\theta x$

for some proportion

$I_\theta(x)\,:\!=\,\theta x$

for some proportion

$\theta\in[0,1]$

and insurance premium P, ceding partial risk to an insurer. Note that the admissible insurance premium must be non-negative and cannot exceed M. Thus, the proportional insurance contract is completely determined by the pair

$\theta\in[0,1]$

and insurance premium P, ceding partial risk to an insurer. Note that the admissible insurance premium must be non-negative and cannot exceed M. Thus, the proportional insurance contract is completely determined by the pair

$(\theta,P)\in[0,1]\times[0,M]$

. The individual is risk averse and is endowed with a utility function u satisfying

$(\theta,P)\in[0,1]\times[0,M]$

. The individual is risk averse and is endowed with a utility function u satisfying

$u'(\cdot)\gt 0$

and

$u'(\cdot)\gt 0$

and

$u''(\cdot)\lt 0$

on the domain

$u''(\cdot)\lt 0$

on the domain

$[w_0-2M,w_0]$

. A rational condition for purchasing this contract is that the individual’s expected utility is enhanced, that is,

$[w_0-2M,w_0]$

. A rational condition for purchasing this contract is that the individual’s expected utility is enhanced, that is,

\begin{align*} \mathbb{E}[u(w_{0}-X+I_\theta(X)-P)] \geqslant\mathbb{E}[u(w_{0}-X)].\end{align*}

\begin{align*} \mathbb{E}[u(w_{0}-X+I_\theta(X)-P)] \geqslant\mathbb{E}[u(w_{0}-X)].\end{align*}

Following Raviv (Reference Raviv1979), we assume that the insurer is risk averse and endowed with bounded initial wealth

$W_1$

and a utility function v satisfying

$W_1$

and a utility function v satisfying

$v'(\cdot) \gt 0 $

and

$v'(\cdot) \gt 0 $

and

$v''(\cdot) \lt 0$

on the relevant domain, where

$v''(\cdot) \lt 0$

on the relevant domain, where

$W_1$

is affected by the fluctuation of his existing business and may be random. The insurer will not offer this contract unless his welfare is weakly improved, that is,

$W_1$

is affected by the fluctuation of his existing business and may be random. The insurer will not offer this contract unless his welfare is weakly improved, that is,

\begin{align*} \mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))] \geqslant \mathbb{E}[v(W_{1})],\end{align*}

\begin{align*} \mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))] \geqslant \mathbb{E}[v(W_{1})],\end{align*}

where

$\tau\geqslant 0$

is the deadweight cost rate. The factor

$\tau\geqslant 0$

is the deadweight cost rate. The factor

$\tau$

is used to include the overhead costs of providing insurance by the insurer, such as marketing and administration costs.

$\tau$

is used to include the overhead costs of providing insurance by the insurer, such as marketing and administration costs.

For any proportion

$\theta\in[0,1]$

, these two rationality conditions are equivalent to

$\theta\in[0,1]$

, these two rationality conditions are equivalent to

\begin{eqnarray}P_{-}(\theta) \leqslant P \leqslant P_{+}(\theta),\end{eqnarray}

\begin{eqnarray}P_{-}(\theta) \leqslant P \leqslant P_{+}(\theta),\end{eqnarray}

where

$P_{-}(\theta)$

and

$P_{-}(\theta)$

and

$P_{+}(\theta)$

are the solutions to the following equations

$P_{+}(\theta)$

are the solutions to the following equations

\begin{eqnarray} \mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))] =\mathbb{E}[v(W_{1})],\, P\geqslant 0,\end{eqnarray}

\begin{eqnarray} \mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))] =\mathbb{E}[v(W_{1})],\, P\geqslant 0,\end{eqnarray}

and

\begin{eqnarray}\mathbb{E}[u(w_{0}-X+I_\theta(X)-P)] = \mathbb{E}[u(w_{0}-X)],\, P\geqslant 0,\end{eqnarray}

\begin{eqnarray}\mathbb{E}[u(w_{0}-X+I_\theta(X)-P)] = \mathbb{E}[u(w_{0}-X)],\, P\geqslant 0,\end{eqnarray}

respectively. In other words, the proportional insurance contract is acceptable only if the insurance premium is less than the maximum amount the insured is willing to pay and exceeds the minimum level required by the insurer. Thus, compared with the status quo (i.e.,

$(\theta, P)=(0,0)$

), Equation (2.1) guarantees that positive insurance is demanded only if both insured and insurer will (weakly) benefit from the insurance transaction. Note that

$(\theta, P)=(0,0)$

), Equation (2.1) guarantees that positive insurance is demanded only if both insured and insurer will (weakly) benefit from the insurance transaction. Note that

$P_{-}(\theta)$

and

$P_{-}(\theta)$

and

$P_{+}(\theta)$

are unique due to the strict increasingness of u and v.

$P_{+}(\theta)$

are unique due to the strict increasingness of u and v.

Clearly, the final insurance contract depends heavily on the negotiation between the insured and the insurer. In the literature, Nash bargaining is widely used to model the negotiation between two parties. Thus, we will give a brief introduction of Nash bargaining in the next subsection.

2.2. Asymmetric Nash bargaining

A two-person Nash bargaining solution was first introduced by Nash (Reference Nash1950) and then extended by Kalai (Reference Kalai1977) to the asymmetric case. Let

$\mathbf{S}$

be the set of all feasible bargaining outcome vectors for the two parties and is a compact convex subset of

$\mathbf{S}$

be the set of all feasible bargaining outcome vectors for the two parties and is a compact convex subset of

$\mathbb{R}^2$

. A bargaining problem is composed of a pair

$\mathbb{R}^2$

. A bargaining problem is composed of a pair

$(\mathbf{a_0},\mathbf{S})$

, where the 2-dimensional vector

$(\mathbf{a_0},\mathbf{S})$

, where the 2-dimensional vector

$\mathbf{a_0}\in \mathbf{S}$

represents the status quo before bargaining (“disagreement point”), and there exists at least one point

$\mathbf{a_0}\in \mathbf{S}$

represents the status quo before bargaining (“disagreement point”), and there exists at least one point

$\mathbf{x}=(x_1,x_2)^T\in\mathbf{S}$

such that

$\mathbf{x}=(x_1,x_2)^T\in\mathbf{S}$

such that

$x_1\gt a_{01}$

and

$x_1\gt a_{01}$

and

$x_2\gt a_{02}$

. Let

$x_2\gt a_{02}$

. Let

$\mathcal{B}$

denote the collection of all 2-person bargaining problems. We use a map

$\mathcal{B}$

denote the collection of all 2-person bargaining problems. We use a map

$\mu: \mathcal{B}\mapsto \mathbb{R}^2$

to characterize the bargaining process. According to Kalai (Reference Kalai1977), the negotiation is referred to as asymmetric Nash bargaining if it satisfies the following four axioms:

$\mu: \mathcal{B}\mapsto \mathbb{R}^2$

to characterize the bargaining process. According to Kalai (Reference Kalai1977), the negotiation is referred to as asymmetric Nash bargaining if it satisfies the following four axioms:

-

• Feasibility:

$\mu(\mathbf{a_0},\mathbf{S})\in \mathbf{S}$

and

$\mu(\mathbf{a_0},\mathbf{S})\gt \mathbf{a_0}$

, where

$\mu(\mathbf{a_0},\mathbf{S})\gt \mathbf{a_0}$

means a strict inequality in both components.

$\mu(\mathbf{a_0},\mathbf{S})\in \mathbf{S}$

and

$\mu(\mathbf{a_0},\mathbf{S})\gt \mathbf{a_0}$

, where

$\mu(\mathbf{a_0},\mathbf{S})\gt \mathbf{a_0}$

means a strict inequality in both components. -

• Invariance under change of scale of utilities: If

$G: \mathbb{R}^2\mapsto\mathbb{R}^2$

is such that

$G (\mathbf{a}) = (c_1a_1 + b_1, c_2a_2 + b_2)^T$

where

$c_i \gt 0$

, then

$G(\mu(\mathbf{a_0},\mathbf{S})) = \mu (G (\mathbf{a_0}), G (\mathbf{S}))$

. -

• Independence of irrelevant alternatives: For all two bargaining problems

$(\mathbf{a_0},\mathbf{S})$

and

$(\mathbf{a_0},\mathbf{U})$

such that

$\mathbf{S}\subset \mathbf{U}$

and

$\mu(\mathbf{a_0},\mathbf{U})\in\mathbf{S}$

, it holds that

$\mu (\mathbf{a_0},\mathbf{S}) = \mu (\mathbf{a_0},\mathbf{U})$

. -

• Pareto optimality: If

$\mu (\mathbf{a_0},\mathbf{S})=(z_1, z_2)^T$

and

$y_i\geqslant z_i$

for

$i=1,2$

, then either

$\mathbf{y}\notin\mathbf{S}$

or

$y_i=z_i$

for

$i=1,2$

.

Kalai (Reference Kalai1977) shows that

$\mu$

satisfies the above four axioms if and only if there exists a

$\mu$

satisfies the above four axioms if and only if there exists a

$\delta\in(0,1)$

such that

$\delta\in(0,1)$

such that

$\mu(\mathbf{a_0},\mathbf{S})$

is the unique point in

$\mu(\mathbf{a_0},\mathbf{S})$

is the unique point in

$\mathbf{S}$

satisfying

$\mathbf{S}$

satisfying

\begin{eqnarray*}\mu(\mathbf{a_0},\mathbf{S})= \arg\max_{\mathbf{x}\in \mathbf{S}}\, (x_1-a_{01})^{1-\delta}(x_2-a_{02})^\delta.\end{eqnarray*}

\begin{eqnarray*}\mu(\mathbf{a_0},\mathbf{S})= \arg\max_{\mathbf{x}\in \mathbf{S}}\, (x_1-a_{01})^{1-\delta}(x_2-a_{02})^\delta.\end{eqnarray*}

This solution is referred to as the asymmetric Nash bargaining solution. Here,

$\delta \in (0,1)$

represents the bargaining power of the second person relative to the first person. This means that the second person has more power in the negotiation if the value of

$\delta \in (0,1)$

represents the bargaining power of the second person relative to the first person. This means that the second person has more power in the negotiation if the value of

$\delta$

becomes larger (see, e.g., Kalai Reference Kalai1977). Feasibility is an attractive property, as it implies that the asymmetric Nash bargaining solution strictly exceeds

$\delta$

becomes larger (see, e.g., Kalai Reference Kalai1977). Feasibility is an attractive property, as it implies that the asymmetric Nash bargaining solution strictly exceeds

$\mathbf{a_0}$

in every component. This strict inequality does not hold true for Bowley or competitive equilibria in the context of distortion risk measures, as shown by Boonen and Ghossoub (Reference Boonen and Ghossoub2023).

$\mathbf{a_0}$

in every component. This strict inequality does not hold true for Bowley or competitive equilibria in the context of distortion risk measures, as shown by Boonen and Ghossoub (Reference Boonen and Ghossoub2023).

3. Nash insurance bargaining

In this paper, we analyze the insurance negotiation between a risk-averse insured and a risk-averse insurer using the asymmetric Nash bargaining framework. More specifically, the status quo is characterized by

\begin{eqnarray*}\mathbf{a_0}=\binom{\mathbb{E}[u(w_0-X)]}{\mathbb{E}[v(W_1)]}.\end{eqnarray*}

\begin{eqnarray*}\mathbf{a_0}=\binom{\mathbb{E}[u(w_0-X)]}{\mathbb{E}[v(W_1)]}.\end{eqnarray*}

Let the feasible set of insurance contracts be given by

\begin{eqnarray*}\mathcal F=\left\{(\theta,P)\,:\,\theta\in[0,1], P_{-}(\theta)\leqslant P\leqslant P_{+}(\theta)\right\}.\end{eqnarray*}

\begin{eqnarray*}\mathcal F=\left\{(\theta,P)\,:\,\theta\in[0,1], P_{-}(\theta)\leqslant P\leqslant P_{+}(\theta)\right\}.\end{eqnarray*}

Then, the set of feasible bargaining outcome vectors under proportional insurance can be given by

\begin{eqnarray*}\mathbf{S}=\left\{\binom{\mathbb{E}[u(w_0-X+I_\theta(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_\theta(X))]}\,:\, (\theta,P)\in\mathcal F \right\}.\end{eqnarray*}

\begin{eqnarray*}\mathbf{S}=\left\{\binom{\mathbb{E}[u(w_0-X+I_\theta(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_\theta(X))]}\,:\, (\theta,P)\in\mathcal F \right\}.\end{eqnarray*}

Since

$(0,0)\in\mathcal{F}$

, it follows that

$(0,0)\in\mathcal{F}$

, it follows that

$\mathbf{a_0}\in \mathbf{S}$

.

$\mathbf{a_0}\in \mathbf{S}$

.

Let

$\mathcal{PO}\subset\mathcal F$

be the class of all

$\mathcal{PO}\subset\mathcal F$

be the class of all

$(\theta,P)$

such that there is no

$(\theta,P)$

such that there is no

$(\theta',P')\in\mathcal F$

satisfying

$(\theta',P')\in\mathcal F$

satisfying

\begin{align} \mathbb{E}[u(w_{0}-X+I_{\theta'}(X)-P')] &\geqslant \mathbb{E}[u(w_{0}-X+I_{\theta}(X)-P)],\end{align}

\begin{align} \mathbb{E}[u(w_{0}-X+I_{\theta'}(X)-P')] &\geqslant \mathbb{E}[u(w_{0}-X+I_{\theta}(X)-P)],\end{align}

\begin{align} \mathbb{E}[v(W_{1}+P'-(1+\tau)I_{\theta'}(X))] &\geqslant \mathbb{E}[v(W_{1}+P-(1+\tau)I_{\theta}(X))], \end{align}

\begin{align} \mathbb{E}[v(W_{1}+P'-(1+\tau)I_{\theta'}(X))] &\geqslant \mathbb{E}[v(W_{1}+P-(1+\tau)I_{\theta}(X))], \end{align}

with at least one inequality being strict. Denoting the frontier of

$\mathbf{S}$

by

$\mathbf{S}$

by

$\partial \mathbf{S}$

, we have

$\partial \mathbf{S}$

, we have

\begin{equation*}\partial \mathbf{S}=\left\{ \binom{\mathbb{E}[u(w_0-X+I_\theta(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_\theta(X))]}\,:\, (\theta,P)\in \mathcal{PO}\right\} . \end{equation*}

\begin{equation*}\partial \mathbf{S}=\left\{ \binom{\mathbb{E}[u(w_0-X+I_\theta(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_\theta(X))]}\,:\, (\theta,P)\in \mathcal{PO}\right\} . \end{equation*}

Next, we analyze whether the status quo

$\mathbf{a_0}$

belongs to the frontier of

$\mathbf{a_0}$

belongs to the frontier of

$\mathbf{S}$

.

$\mathbf{S}$

.

Proposition 1. Under the assumption of proportional insurance, the status quo is Pareto optimal if and only if

\begin{equation}\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]} \leqslant (1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}.\end{equation}

\begin{equation}\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]} \leqslant (1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}.\end{equation}

From the above proposition, we know that no insurance will be purchased if the insured’s marginal welfare improvement

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]}$

is less than the marginal cost from the insurer

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]}$

is less than the marginal cost from the insurer

$(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}$

. In particular, when

$(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}$

. In particular, when

$\tau$

is sufficiently high, insurance becomes unattractive. Furthermore, when

$\tau$

is sufficiently high, insurance becomes unattractive. Furthermore, when

$W_1$

is independent of X, some interesting phenomena can be observed:

$W_1$

is independent of X, some interesting phenomena can be observed:

-

• The right-hand side of Equation (3.3) degenerates to

$(1+\tau)\mathbb{E}[X]$

such that this necessary and sufficient condition is no longer affected by the degree of the risk aversion of the insurer. Notably, Proposition 3 in Braun and Muermann (Reference Braun and Muermann2004) also states that when the insurer is risk neutral, no insurance will be purchased if this condition is satisfied. -

• Note that

$u'(w_{0}-X)$

and X are comonotonic, and thus the left-hand side of Equation (3.3) is larger than

$\mathbb{E}[X]$

by the Hardy-Littlewood inequality (Hardy et al., Reference Hardy, Littlewood and Pólya1952). This means that if

$\tau=0$

, the status quo is Pareto optimal only if X is almost surely deterministic.

Further, if

$W_1$

is stochastically increasing in X (denoted by

$W_1$

is stochastically increasing in X (denoted by

$W_1\uparrow_{st}X$

),Footnote

3

we have

$W_1\uparrow_{st}X$

),Footnote

3

we have

\begin{align*}\mathbb{E}[v'(W_1)X]/\mathbb{E}[v'(W_1)]\leqslant \mathbb{E}[X]\end{align*}

\begin{align*}\mathbb{E}[v'(W_1)X]/\mathbb{E}[v'(W_1)]\leqslant \mathbb{E}[X]\end{align*}

such that Equation (3.3) fails to be satisfied for a relatively small

$\tau$

. This is intuitive: if the insurer can hedge existing business by underwriting new risks, he will provide insurance when the deadweight cost is low. For the opposite case of

$\tau$

. This is intuitive: if the insurer can hedge existing business by underwriting new risks, he will provide insurance when the deadweight cost is low. For the opposite case of

$W_1\downarrow_{st}X$

, it is harder to evaluate because the right-hand side of Equation (3.3) also exceeds

$W_1\downarrow_{st}X$

, it is harder to evaluate because the right-hand side of Equation (3.3) also exceeds

$\mathbb{E}[X]$

.

$\mathbb{E}[X]$

.

To ensure the feasibility of Nash bargaining, we impose the following assumption, which requires the deadweight cost rate

$\tau$

to be sufficiently small.

$\tau$

to be sufficiently small.

Assumption 1.

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]} \gt (1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}$

.

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]} \gt (1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}$

.

In addition to the Pareto inefficiency of the status quo, Nash bargaining problems also require the set

$\mathbf{S}$

to be compact and convex. This is shown in the following proposition.

$\mathbf{S}$

to be compact and convex. This is shown in the following proposition.

Proposition 2. The set

$\mathbf{S}$

is convex and compact.

$\mathbf{S}$

is convex and compact.

From the above proposition, Nash bargaining is feasible if Assumption 1 is satisfied. The asymmetric Nash bargaining solution solves the following optimization problem:

\begin{eqnarray} &&\max _{\theta \in [0,1]\atop P_{-}(\theta) \leqslant P \leqslant P_{+}(\theta)} \left\{\mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))]- \mathbb{E}[v(W_{1})]\right\}^{\delta} \nonumber\\&&\qquad\qquad\qquad\quad \times\left\{\mathbb{E}[u(w_{0}-X +I_{\theta}(X)-P)] -\mathbb{E}[u(w_{0}-X)]\right\}^{1-\delta}\end{eqnarray}

\begin{eqnarray} &&\max _{\theta \in [0,1]\atop P_{-}(\theta) \leqslant P \leqslant P_{+}(\theta)} \left\{\mathbb{E}[v(W_{1}+P-(1+\tau)I_\theta(X))]- \mathbb{E}[v(W_{1})]\right\}^{\delta} \nonumber\\&&\qquad\qquad\qquad\quad \times\left\{\mathbb{E}[u(w_{0}-X +I_{\theta}(X)-P)] -\mathbb{E}[u(w_{0}-X)]\right\}^{1-\delta}\end{eqnarray}

for some

$\delta\in(0,1)$

, where

$\delta\in(0,1)$

, where

$\delta$

represents the bargaining power of the insurer. Obviously, the optimization objective function is continuous in

$\delta$

represents the bargaining power of the insurer. Obviously, the optimization objective function is continuous in

$\theta$

and P and equals to zero if P is equal to either

$\theta$

and P and equals to zero if P is equal to either

$P_{-}(\theta)$

or

$P_{-}(\theta)$

or

$P_{+}(\theta)$

. Thus, the Nash bargaining solutions

$P_{+}(\theta)$

. Thus, the Nash bargaining solutions

$(\theta^*,P^*)$

must exist and satisfy

$(\theta^*,P^*)$

must exist and satisfy

\begin{eqnarray} \theta^*\in\Theta\,:\!=\, \{\theta \in (0,1] \,:\, P_+(\theta) \gt P_-(\theta) \}\quad\text{and}\quad P_{-}(\theta^*)\lt P^*\lt P_{+}(\theta^*)\end{eqnarray}

\begin{eqnarray} \theta^*\in\Theta\,:\!=\, \{\theta \in (0,1] \,:\, P_+(\theta) \gt P_-(\theta) \}\quad\text{and}\quad P_{-}(\theta^*)\lt P^*\lt P_{+}(\theta^*)\end{eqnarray}

due to Assumption 1. The set

$\Theta$

plays an important role in deriving optimal solutions, and we provide an alternative characterization in the following proposition.

$\Theta$

plays an important role in deriving optimal solutions, and we provide an alternative characterization in the following proposition.

Proposition 3. Under Assumption 1,

\[\Theta=\left\{\begin{array}{l@{\quad}l}(0,1],&\text{if}\, P_+(1)\gt P_{-}(1),\\(0,\theta_0),&\text{otherwise}\end{array}\right.\]

\[\Theta=\left\{\begin{array}{l@{\quad}l}(0,1],&\text{if}\, P_+(1)\gt P_{-}(1),\\(0,\theta_0),&\text{otherwise}\end{array}\right.\]

for some

$\theta_0\in(0,1]$

.

$\theta_0\in(0,1]$

.

Example 1. Let

\begin{align*}w_0=20, u(w) =-w^{-1},\, v(w) =w^{0.6},\end{align*}

\begin{align*}w_0=20, u(w) =-w^{-1},\, v(w) =w^{0.6},\end{align*}

and

$W_1=100$

almost surely. Moreover, assume that the loss X has the cumulative distribution function

$W_1=100$

almost surely. Moreover, assume that the loss X has the cumulative distribution function

\begin{align*}F_X(x)=\frac{5}{6}+\frac{4}{7}\int_0^x\frac{10^3}{(y+10)^4}dy,\,x\in[0,10].\end{align*}

\begin{align*}F_X(x)=\frac{5}{6}+\frac{4}{7}\int_0^x\frac{10^3}{(y+10)^4}dy,\,x\in[0,10].\end{align*}

Clearly,

$\mathbb{P}(X=0)=\frac{5}{6}$

and

$\mathbb{P}(X=0)=\frac{5}{6}$

and

$M=10$

. Assumption 1 is satisfied whenever

$M=10$

. Assumption 1 is satisfied whenever

$\tau\lt 0.817$

, since

$\tau\lt 0.817$

, since

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]\mathbb{E}[X]}=1.817$

.

$\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X)]\mathbb{E}[X]}=1.817$

.

The functions

$ P_+(\theta)$

and

$ P_+(\theta)$

and

$P_-(\theta)$

corresponding to Example 1.

$P_-(\theta)$

corresponding to Example 1.

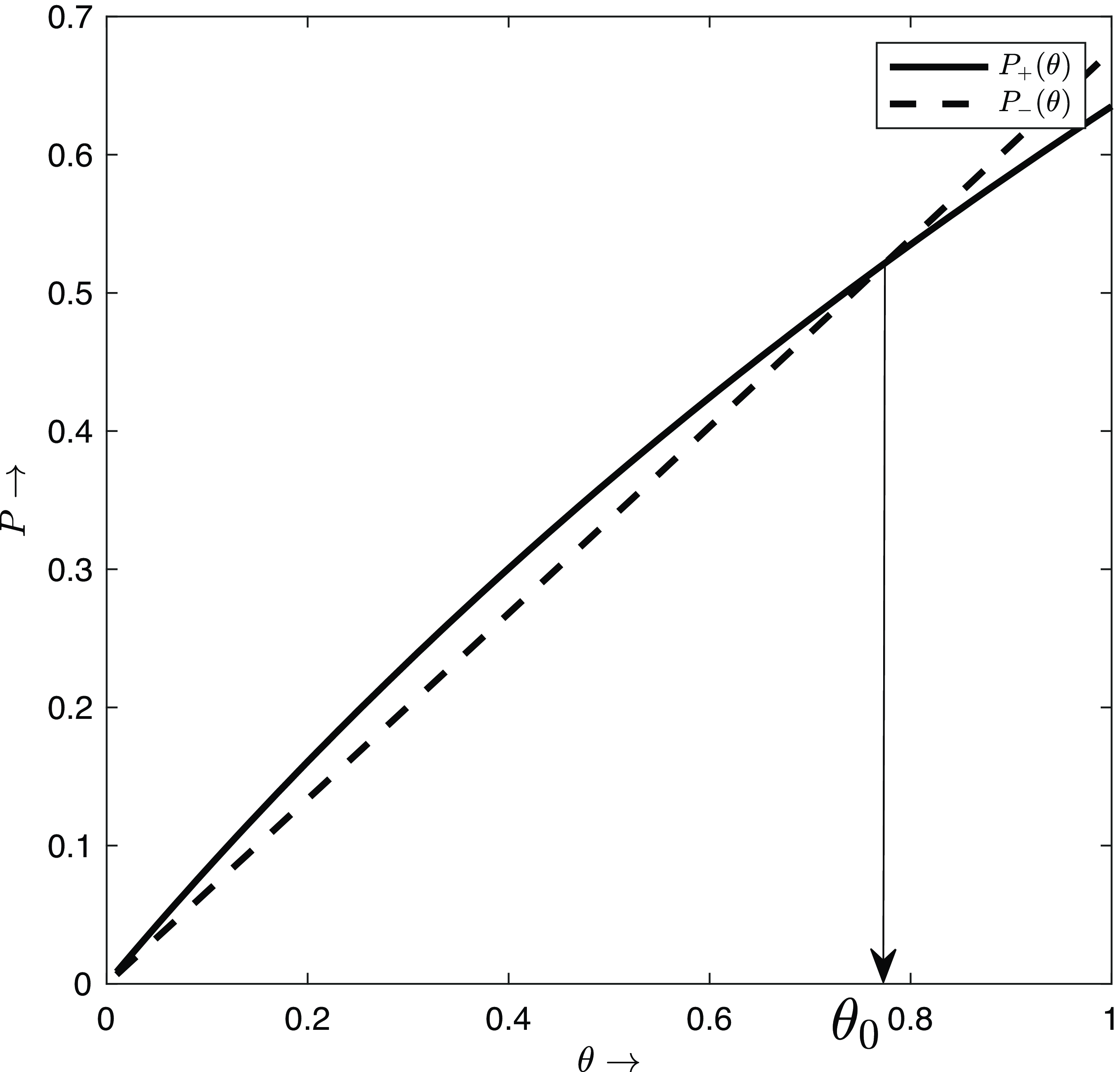

Based on the above assumptions, it is easy to calculate

$ P_+(\theta)$

and

$ P_+(\theta)$

and

$P_-(\theta)$

numerically. For

$P_-(\theta)$

numerically. For

$\tau=0.4$

, we display these two functions in Figure 1. The set

$\tau=0.4$

, we display these two functions in Figure 1. The set

$\Theta$

can be determined for different values of the cost rate

$\Theta$

can be determined for different values of the cost rate

$\tau$

. More specifically, when

$\tau$

. More specifically, when

$\tau=0.3$

, we have

$\tau=0.3$

, we have

$\theta_0=1$

, and thus

$\theta_0=1$

, and thus

$\Theta=(0, 1]$

. The supremum of

$\Theta=(0, 1]$

. The supremum of

$\Theta$

changes to approximately

$\Theta$

changes to approximately

$0.773$

if the value of

$0.773$

if the value of

$\tau$

is set to be

$\tau$

is set to be

$0.4$

(see Figure 1). If

$0.4$

(see Figure 1). If

$\tau$

further increases to

$\tau$

further increases to

$0.5$

, then

$0.5$

, then

$\theta_0$

decreases to approximately

$\theta_0$

decreases to approximately

$0.540 $

. A similar set

$0.540 $

. A similar set

$\Theta$

is obtained when the insurer’s risk attitude is changed from power utility function to

$\Theta$

is obtained when the insurer’s risk attitude is changed from power utility function to

\begin{align*}v(w) =1-e^{-aw}\end{align*}

\begin{align*}v(w) =1-e^{-aw}\end{align*}

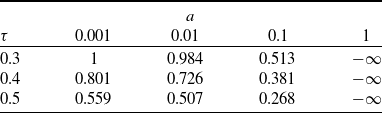

for some positive a. The outcomes of

$\theta_0$

in those experiments are presented in Table 1.

$\theta_0$

in those experiments are presented in Table 1.

The supremum of

$\Theta$

, given by

$\Theta$

, given by

$\theta_0$

, when the insurer’s risk preference follows an exponential utility function. Here, the value

$\theta_0$

, when the insurer’s risk preference follows an exponential utility function. Here, the value

$-\infty$

corresponds to the cases that Assumption 1 is violated.

$-\infty$

corresponds to the cases that Assumption 1 is violated.

Now, we can solve the optimization problem (3.4) and obtain the Nash bargaining solutions in the following proposition.

Proposition 4. Under Assumption 1, the optimal proportional insurance contract

$(\theta^*,P^*)$

that solves Problem (3.4) is unique. It satisfies the first-order condition

$(\theta^*,P^*)$

that solves Problem (3.4) is unique. It satisfies the first-order condition

\begin{align}\left\{\begin{array}{ll}\!(1-\delta) \times\dfrac{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)]}{\mathbb{E}[u(w_{0}-X +I_{\theta^*}(X)-P^*)] -\mathbb{E}[u(w_{0}-X)]}&=\delta\times\dfrac{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]}{\mathbb{E}[v(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]- \mathbb{E}[v(W_{1})]},\\&\\\qquad\qquad\qquad\dfrac{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)X]}{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)]}&=(1+\tau)\dfrac{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))X]}{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]},\end{array}\right.\end{align}

\begin{align}\left\{\begin{array}{ll}\!(1-\delta) \times\dfrac{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)]}{\mathbb{E}[u(w_{0}-X +I_{\theta^*}(X)-P^*)] -\mathbb{E}[u(w_{0}-X)]}&=\delta\times\dfrac{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]}{\mathbb{E}[v(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]- \mathbb{E}[v(W_{1})]},\\&\\\qquad\qquad\qquad\dfrac{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)X]}{\mathbb{E}[u'(w_{0}-X +I_{\theta^*}(X)-P^*)]}&=(1+\tau)\dfrac{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))X]}{\mathbb{E}[v'(W_{1}+P^*-(1+\tau)I_{\theta^*}(X))]},\end{array}\right.\end{align}

if

\begin{equation}P_{+}(1)\leqslant P_{-}(1)\quad\text{or}\quad\mathbb{E}[X]\lt (1+\tau)\frac{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)X\right]}{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)\right]},\end{equation}

\begin{equation}P_{+}(1)\leqslant P_{-}(1)\quad\text{or}\quad\mathbb{E}[X]\lt (1+\tau)\frac{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)X\right]}{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)\right]},\end{equation}

and equals to

$(1, \hat{P})$

otherwise, where

$(1, \hat{P})$

otherwise, where

$\hat{P}$

is a solution to the following equation

$\hat{P}$

is a solution to the following equation

\begin{equation}\frac{(1-\delta)u'(w_{0}-P)}{u(w_{0}-P) -\mathbb{E}[u(w_{0}-X)]}=\frac{\delta\mathbb{E}[v'(W_{1}+P-(1+\tau)X)]}{\mathbb{E}[v(W_{1}+P-(1+\tau)X)]- \mathbb{E}[v(W_{1})]},\,P\geqslant 0.\end{equation}

\begin{equation}\frac{(1-\delta)u'(w_{0}-P)}{u(w_{0}-P) -\mathbb{E}[u(w_{0}-X)]}=\frac{\delta\mathbb{E}[v'(W_{1}+P-(1+\tau)X)]}{\mathbb{E}[v(W_{1}+P-(1+\tau)X)]- \mathbb{E}[v(W_{1})]},\,P\geqslant 0.\end{equation}

From the above proposition, we can see that full insurance is unlikely to be optimal, except for very extreme cases such as that of a quite small

$\tau$

and the insurer’s risk exposure

$\tau$

and the insurer’s risk exposure

$W_1-(1+\tau)X$

being stochastically increasing in X. Especially when

$W_1-(1+\tau)X$

being stochastically increasing in X. Especially when

$W_1\downarrow_{st}X$

, which includes the independent case between

$W_1\downarrow_{st}X$

, which includes the independent case between

$W_1$

and X, we have

$W_1$

and X, we have

\begin{align*}\frac{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)X\right]}{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)\right]}\gt \mathbb{E}[X]\end{align*}

\begin{align*}\frac{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)X\right]}{\mathbb{E}\left[v'(W_1+\hat{P}-(1+\tau)X)\right]}\gt \mathbb{E}[X]\end{align*}

such that condition (3.7) is satisfied even if the deadweight cost rate

$\tau$

is zero, then partial insurance is optimal. Moreover, the optimal insurance solution depends not only on the degree of risk aversion of both parties but also on the bargaining power

$\tau$

is zero, then partial insurance is optimal. Moreover, the optimal insurance solution depends not only on the degree of risk aversion of both parties but also on the bargaining power

$\delta$

.

$\delta$

.

4. Comparative statics analysis

In this section, we will carry out comparative statics analysis to investigate the effect of some interesting factors on the Nash bargaining solution.

First, we investigate the effect of the degree of the insured’s risk aversion on the optimal rate and insurance premium of proportional insurance. In the literature, the insured’s degree of risk aversion is often measured by Arrow-Pratt coefficient of absolute risk aversion

\begin{eqnarray*}\mathcal{A}_u(w)=-\frac{u''(w)}{u'(w)}.\end{eqnarray*}

\begin{eqnarray*}\mathcal{A}_u(w)=-\frac{u''(w)}{u'(w)}.\end{eqnarray*}

The insured’s risk preference is called to exhibit constant absolute risk aversion (CARA) if

$\mathcal{A}_u(w)$

is a constant function. It is equivalent to that the insured has an exponential utility function with

$\mathcal{A}_u(w)$

is a constant function. It is equivalent to that the insured has an exponential utility function with

$\mathcal{A}_u(w)=a$

for some positive

$\mathcal{A}_u(w)=a$

for some positive

$a$

.

$a$

.

To proceed, we consider a very special case. If there are no deadweight costs and risk preferences of the two agents in the contract exhibit CARA, then the optimal proportion has a closed-form expression and is independent of the bargaining power.

Proposition 5. Assume that the insurer’s initial wealth

$W_1$

is independent of X. For

$W_1$

is independent of X. For

$\tau=0$

and CARA utility functions u and v with Arrow-Pratt coefficients of

$\tau=0$

and CARA utility functions u and v with Arrow-Pratt coefficients of

$\lambda_u$

and

$\lambda_u$

and

$\lambda_v$

, the asymmetric Nash bargaining solution is given by

$\lambda_v$

, the asymmetric Nash bargaining solution is given by

$(\theta^*,P^*)$

, where

$(\theta^*,P^*)$

, where

$\theta^*=\frac{1/\lambda_v}{1/\lambda_u+1/\lambda_v}$

and

$\theta^*=\frac{1/\lambda_v}{1/\lambda_u+1/\lambda_v}$

and

$P^*\in(P_-(\theta^*),P_+(\theta^*))$

.

$P^*\in(P_-(\theta^*),P_+(\theta^*))$

.

The result in the above proposition can also be verified through Equation (3.6). Under these strict assumptions, we can see that the optimal proportion

$\theta^*$

does not depend on the bargaining power

$\theta^*$

does not depend on the bargaining power

$\delta$

and increases in

$\delta$

and increases in

$\lambda_u$

. In other words, as the insured becomes more risk averse, more insurance coverage is demanded. We claim that this effect can also be held for general cases, while the optimal parameters

$\lambda_u$

. In other words, as the insured becomes more risk averse, more insurance coverage is demanded. We claim that this effect can also be held for general cases, while the optimal parameters

$\theta^*$

and

$\theta^*$

and

$P^*$

may not have closed-form expressions. Another insured’s risk attitude with increasing and concave utility function

$P^*$

may not have closed-form expressions. Another insured’s risk attitude with increasing and concave utility function

$\tilde{u}$

is called to be more risk averse than the insured’s with utility function u if

$\tilde{u}$

is called to be more risk averse than the insured’s with utility function u if

$\mathcal{A}_{\tilde{u}}(w)\geqslant \mathcal{A}_u(w)$

for any w. Equivalently, there exists a twice differentiable increasing concave function

$\mathcal{A}_{\tilde{u}}(w)\geqslant \mathcal{A}_u(w)$

for any w. Equivalently, there exists a twice differentiable increasing concave function

$\kappa$

such that

$\kappa$

such that

$\tilde{u}(w)=\kappa(u(w))$

; see Proposition 2 in Gollier (Reference Gollier2001). Furthermore, the utility function u is said to exhibit a DARA risk preference if

$\tilde{u}(w)=\kappa(u(w))$

; see Proposition 2 in Gollier (Reference Gollier2001). Furthermore, the utility function u is said to exhibit a DARA risk preference if

$\mathcal{A}_u(w)$

is decreasing.

$\mathcal{A}_u(w)$

is decreasing.

Proposition 6. Let

$-W_1$

be increasing in X in the sense of hazard rate order (i.e.,

$-W_1$

be increasing in X in the sense of hazard rate order (i.e.,

$-W_1\uparrow_{hr}X$

).Footnote 4 Under the DARA assumptions on utility functions u and v, both the optimal proportion and the optimal insurance premium increase as the insured becomes more risk averse in the Arrow-Pratt sense.

$-W_1\uparrow_{hr}X$

).Footnote 4 Under the DARA assumptions on utility functions u and v, both the optimal proportion and the optimal insurance premium increase as the insured becomes more risk averse in the Arrow-Pratt sense.

The above proposition can be explained as follows: As the insured becomes more risk averse, she is willing to pay more insurance premium to mitigate the risk and transfer more risk to the insurer. Notably, a similar finding is obtained by Proposition 2 in Chi et al. (Reference Chi, Hu, Zhao and Zheng2024), which assumes a risk-neutral insurer. The above proposition extends the result to the case of a risk-averse insurer.

Next, we analyze the effects on the welfare improvement and the Nash bargaining solution by the change of the insurance market structure.

Proposition 7. Under Assumption 1, as the insurer becomes more powerful in the bargaining (i.e.,

$\delta$

increases), the increment of the insurer’s expected utility increases while the welfare improvement of the insured decreases. Further, if

$\delta$

increases), the increment of the insurer’s expected utility increases while the welfare improvement of the insured decreases. Further, if

$-W_1\uparrow_{hr}X$

and the risk preferences of the insured and the insurer exhibit DARA, both the optimal insurance premium

$-W_1\uparrow_{hr}X$

and the risk preferences of the insured and the insurer exhibit DARA, both the optimal insurance premium

$P^*$

and the optimal proportion

$P^*$

and the optimal proportion

$\theta^*$

are increasing in

$\theta^*$

are increasing in

$\delta$

.

$\delta$

.

The above proposition indicates that the insurer will receive a larger reward from the contract negotiation as he becomes more powerful. However, this comes at the cost of a reduction in the insured’s welfare improvement. As more reward is asked by the insurer, the insured has to pay more extra cost to cede the risk. Equivalently, the insured’s initial wealth is relatively reduced. Under the DARA assumption of the insured’s risk preference, the insured becomes more risk averse and would like to cede more risk. In other words, the increase in the insurer’s bargaining power leads to more insurance demand. Thus, this proposition can be used to explain the phenomenon of the overinsurance preference observed in practice without incorporating behavioral elements (e.g., Braun and Muermann Reference Braun and Muermann2004). It is necessary to point out that a similar finding is also obtained by Proposition 5 in Chi et al. (Reference Chi, Hu, Zhao and Zheng2024) under the assumption of a risk-neutral insurer. However, we consider a risk-averse insurer with random initial wealth satisfying

$-W_1\uparrow_{hr}X$

instead.

$-W_1\uparrow_{hr}X$

instead.

Finally, we assume that

$W_1=w_1$

almost surely and attempt to analyze the effect on the optimal insurance coverage by the change of the insurer’s initial wealth

$W_1=w_1$

almost surely and attempt to analyze the effect on the optimal insurance coverage by the change of the insurer’s initial wealth

$w_1$

.

$w_1$

.

Proposition 8. Set the insurer’s initial wealth

$W_1$

to be a constant

$W_1$

to be a constant

$w_1$

almost surely, and assume that the insurer’s risk preference exhibits DARA and that the insured has a CARA utility function u. Under Assumption 1, the optimal rate of proportional insurance

$w_1$

almost surely, and assume that the insurer’s risk preference exhibits DARA and that the insured has a CARA utility function u. Under Assumption 1, the optimal rate of proportional insurance

$\theta^*$

increases in the insurer’s initial wealth

$\theta^*$

increases in the insurer’s initial wealth

$w_1$

.

$w_1$

.

When the insurer’s initial wealth increases, he will become less risk averse under the DARA assumption of his risk preference and charge less insurance premium. As the insurance becomes less costly, the insured would cede more risk, as stated in the above proposition.

5. Numerical examples

In this section, we provide examples to illustrate the theoretical results from the previous two sections. Specifically, we adopt the setting of Example 1 as our benchmark assumptions. That is,

\begin{align*}w_0=20, u(w)=-w^{-1},\quad v(w) =w^{0.6}\quad \text{and}\quad\tau=0.4,\end{align*}

\begin{align*}w_0=20, u(w)=-w^{-1},\quad v(w) =w^{0.6}\quad \text{and}\quad\tau=0.4,\end{align*}

and

$W_1=100$

almost surely.

$W_1=100$

almost surely.

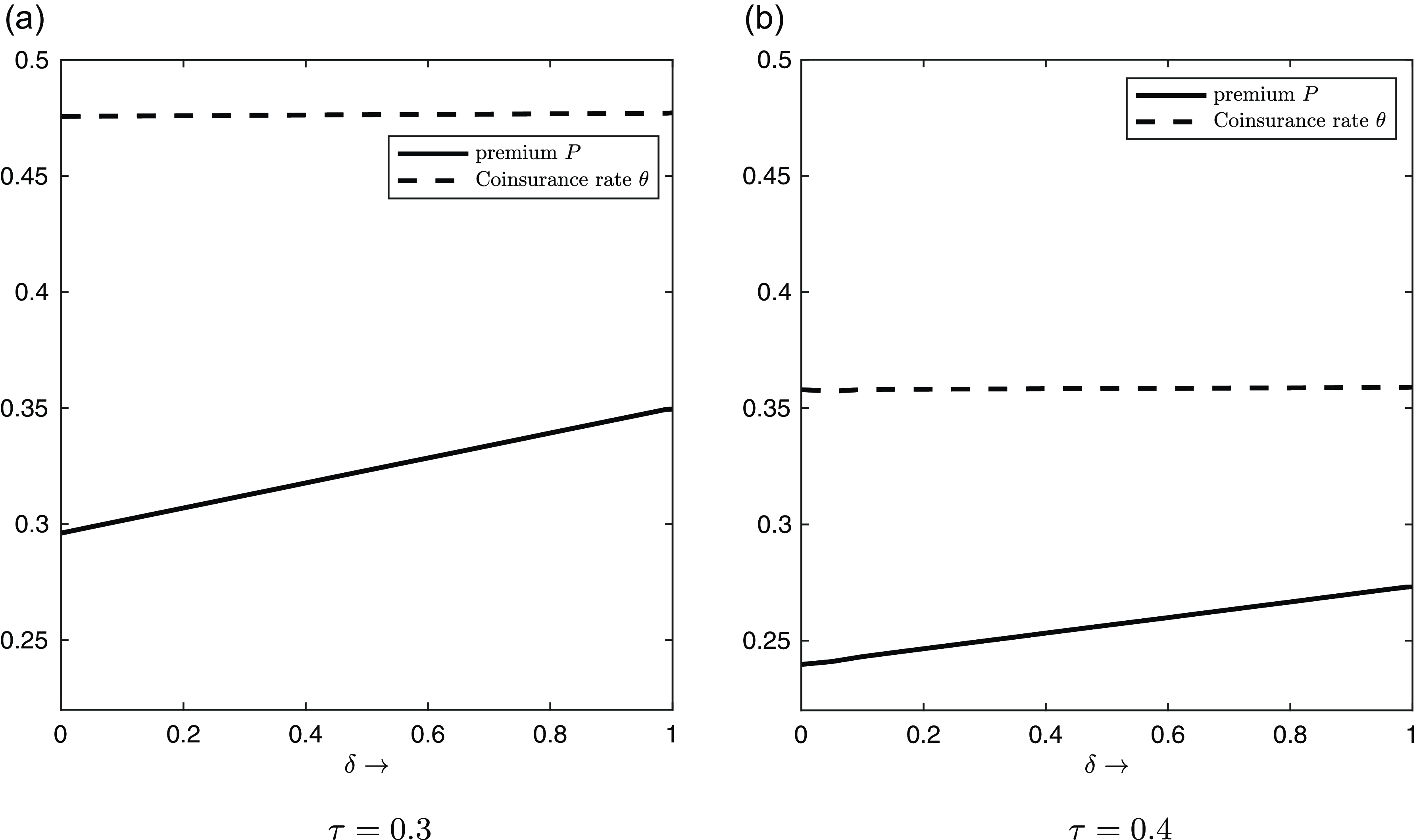

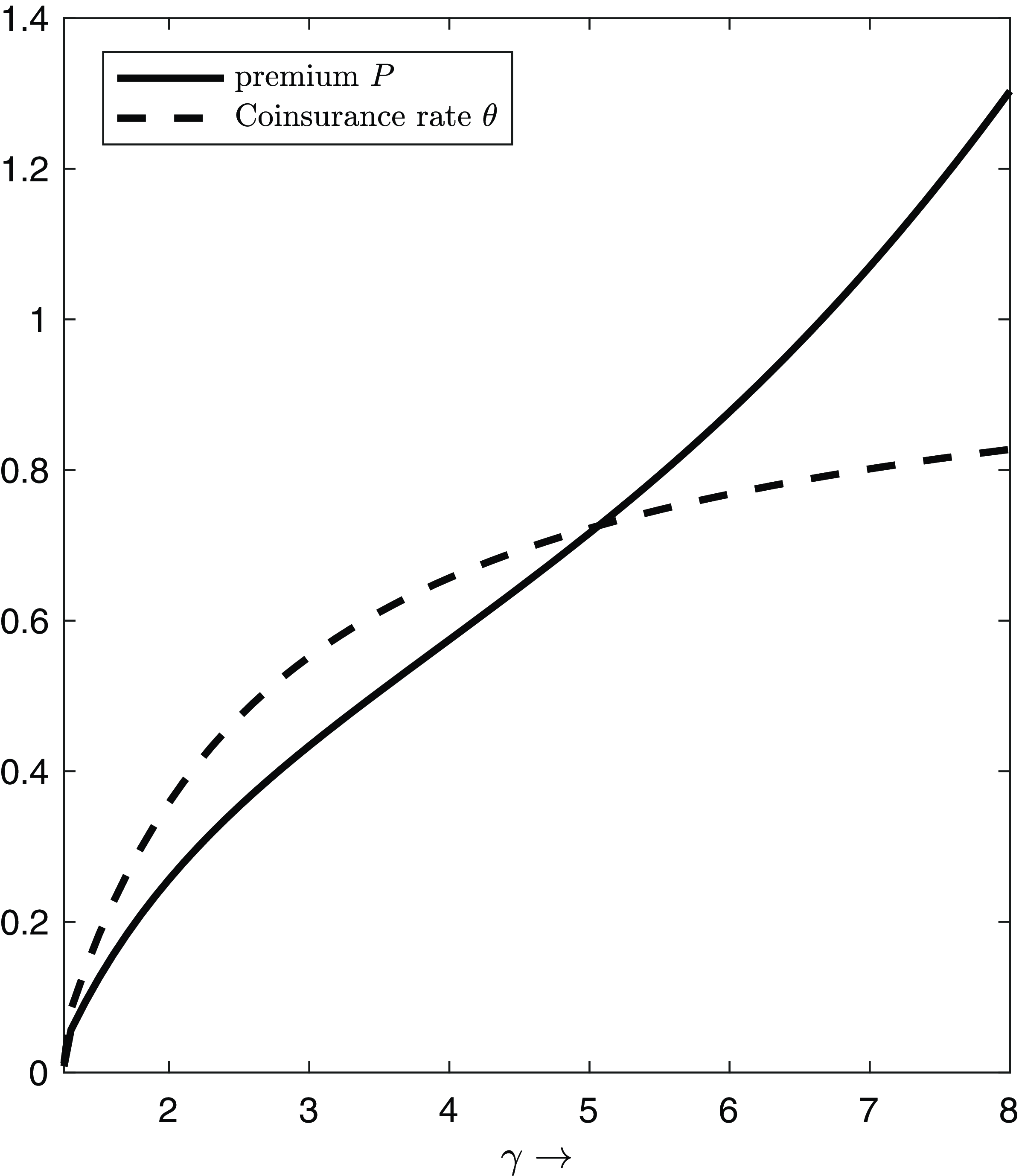

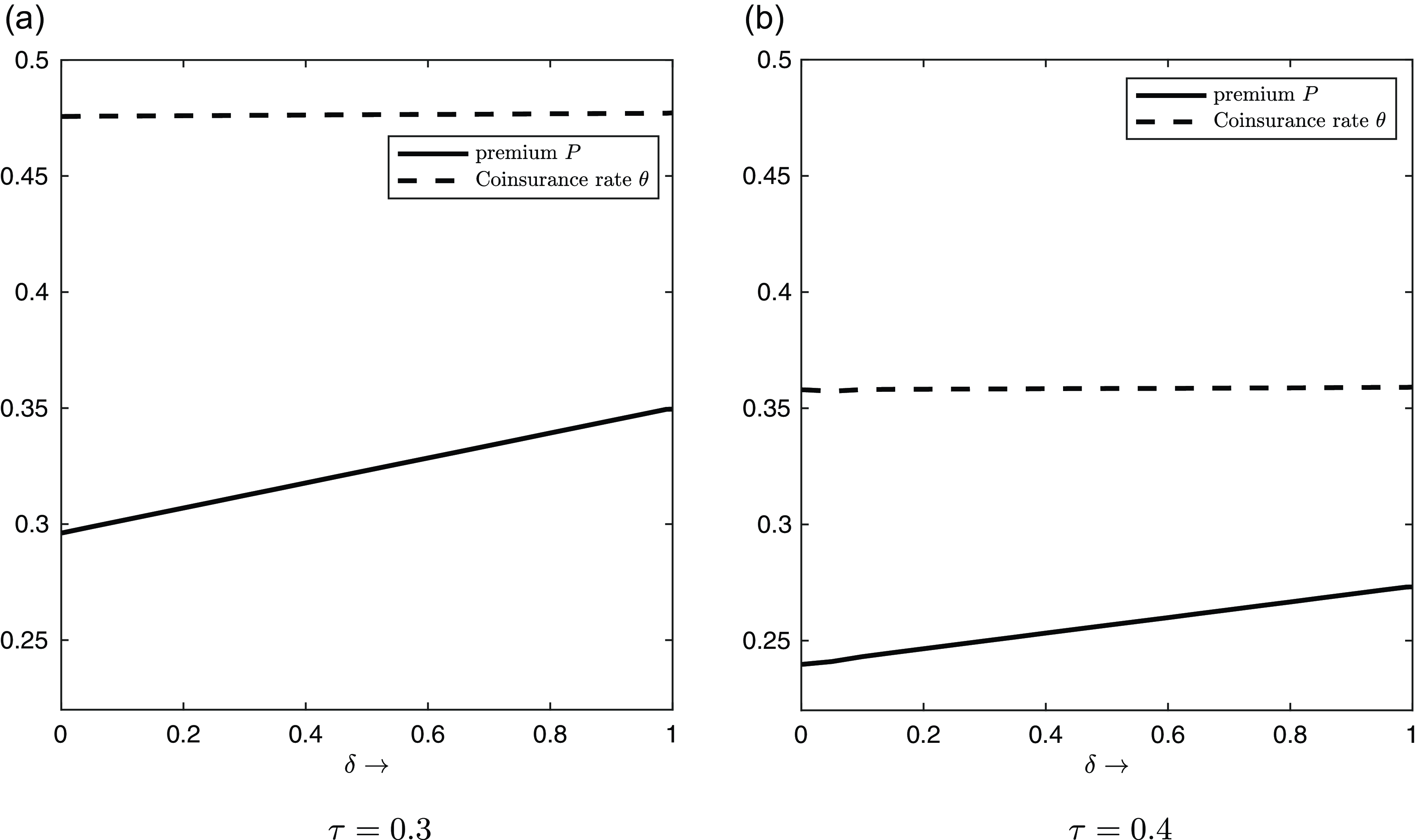

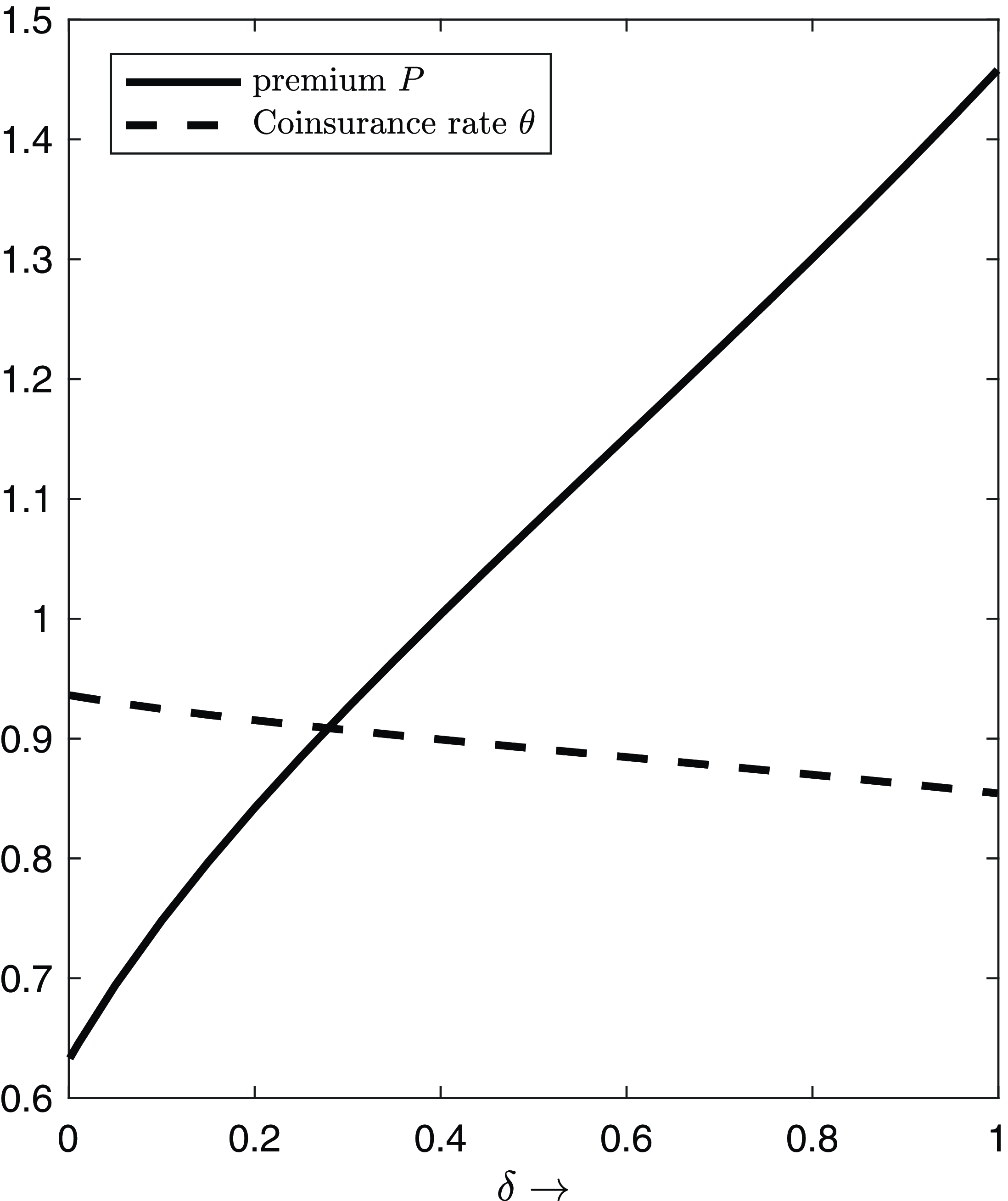

We show the insurance contract corresponding to the asymmetric Nash bargaining solution in Figure 2. In this figure, we display the optimal insurance contract

$(\theta, P)$

under the asymmetric Nash bargaining for

$(\theta, P)$

under the asymmetric Nash bargaining for

$\tau=0.3$

and

$\tau=0.3$

and

$\tau=0.4$

. The contracts are shown as functions of the bargaining power of the insurer

$\tau=0.4$

. The contracts are shown as functions of the bargaining power of the insurer

$\delta$

. Consistent with Proposition 7, the numerical results show that both the coinsurance rate

$\delta$

. Consistent with Proposition 7, the numerical results show that both the coinsurance rate

$\theta$

and the premium P strictly increase with

$\theta$

and the premium P strictly increase with

$\delta$

. Thus, greater insurance coverage is induced when the insurer has more bargaining power. In addition, we note that the result in Proposition 5 may not hold if the assumptions on

$\delta$

. Thus, greater insurance coverage is induced when the insurer has more bargaining power. In addition, we note that the result in Proposition 5 may not hold if the assumptions on

$\tau=0$

and the CARA risk preferences of the insured and the insurer are relaxed. The difference between the cases

$\tau=0$

and the CARA risk preferences of the insured and the insurer are relaxed. The difference between the cases

$\tau=0.3$

and

$\tau=0.3$

and

$\tau=0.4$

can be described as follows. When the deadweight cost rate

$\tau=0.4$

can be described as follows. When the deadweight cost rate

$\tau$

is lower, insurance becomes more attractive, as reflected by a larger coinsurance rate of approximately 0.48 for

$\tau$

is lower, insurance becomes more attractive, as reflected by a larger coinsurance rate of approximately 0.48 for

$\tau=0.3$

, compared to approximately 0.36 when

$\tau=0.3$

, compared to approximately 0.36 when

$\tau=0.4$

. As the insurance coverage gets larger, the corresponding insurance premium also becomes higher.

$\tau=0.4$

. As the insurance coverage gets larger, the corresponding insurance premium also becomes higher.

The optimal parameter pair

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the insurer’s bargaining power

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the insurer’s bargaining power

$\delta\in(0,1)$

, with

$\delta\in(0,1)$

, with

$\tau=0.3$

(left) and

$\tau=0.3$

(left) and

$\tau=0.4$

(right).

$\tau=0.4$

(right).

Next, we present a sensitivity analysis to illustrate the comparative statics. For related problems involving different parameter choices for

$\delta$

or minor adjustments to the relative risk-aversion parameters in u or v, we find that the pattern of the optimal insurance contract

$\delta$

or minor adjustments to the relative risk-aversion parameters in u or v, we find that the pattern of the optimal insurance contract

$(\theta, P)$

is roughly consistent with Figure 2. That is, both

$(\theta, P)$

is roughly consistent with Figure 2. That is, both

$\theta$

and P increase with the bargaining power, albeit only slightly. We now present four additional examples, focusing on the following sensitivities: (1) the impact of the insured’s risk aversion, (2) the use of a different class of utility functions, (3) the effect of the insurer’s initial wealth, and (4) the effect of background risk. Throughout the following examples, we fix

$\theta$

and P increase with the bargaining power, albeit only slightly. We now present four additional examples, focusing on the following sensitivities: (1) the impact of the insured’s risk aversion, (2) the use of a different class of utility functions, (3) the effect of the insurer’s initial wealth, and (4) the effect of background risk. Throughout the following examples, we fix

$\tau=0.4$

and

$\tau=0.4$

and

$w_0=20$

.

$w_0=20$

.

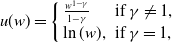

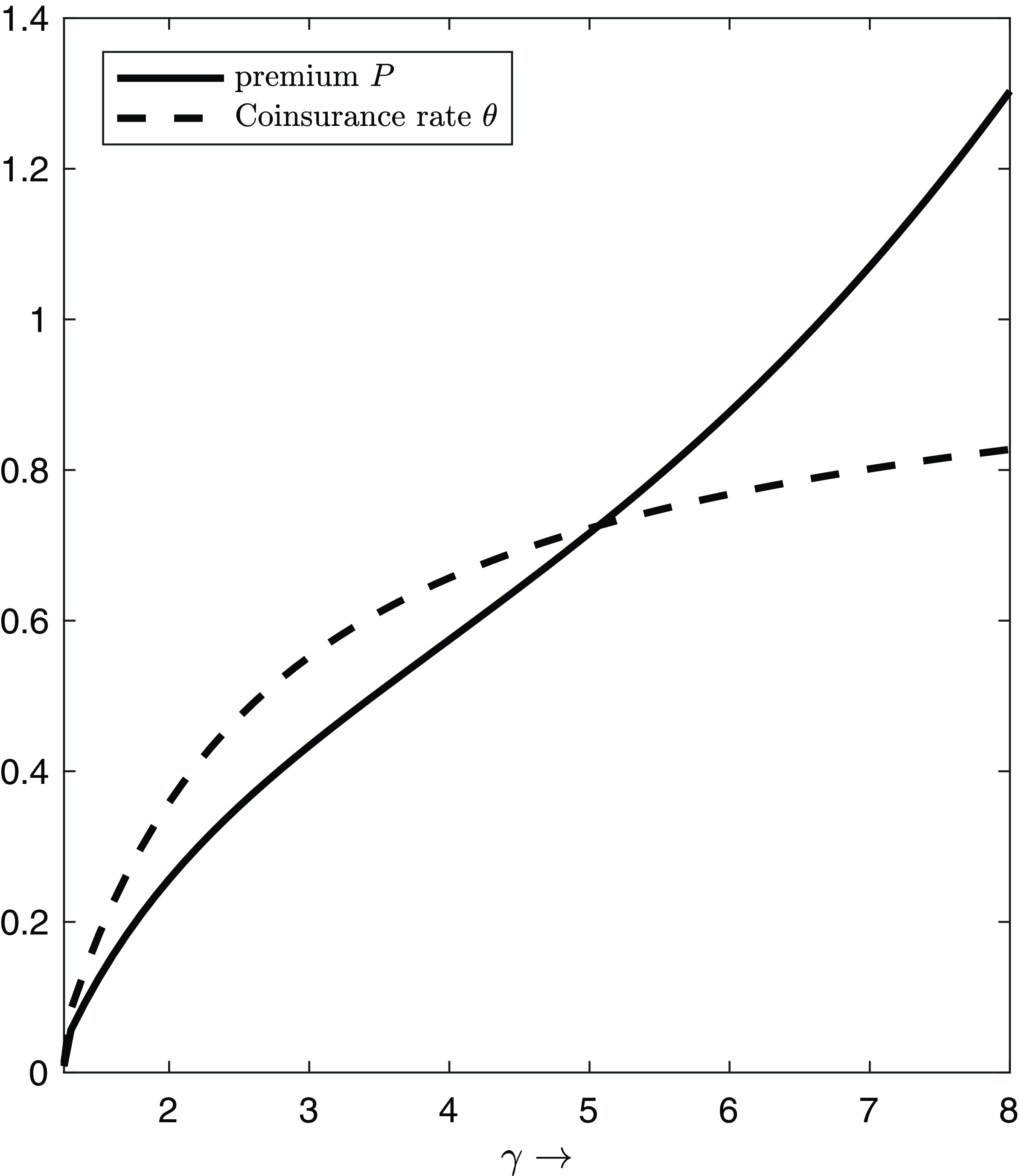

First, we examine the effect of the insured’s risk-aversion parameter. Let

$W_1=100$

a.s.,

$W_1=100$

a.s.,

$v(w)=w^{0.6}$

, and let the bargaining power be

$v(w)=w^{0.6}$

, and let the bargaining power be

$\delta=0.5$

. The utility function u of the insured is given by

$\delta=0.5$

. The utility function u of the insured is given by

\begin{equation} u(w)=\left\{\begin{array}{ll}\frac{w^{1-\gamma}}{1-\gamma}&\text{ if }\gamma\neq 1,\\ \ln(w),&\text{ if }\gamma= 1,\end{array}\right. \end{equation}

\begin{equation} u(w)=\left\{\begin{array}{ll}\frac{w^{1-\gamma}}{1-\gamma}&\text{ if }\gamma\neq 1,\\ \ln(w),&\text{ if }\gamma= 1,\end{array}\right. \end{equation}

which is the constant relative risk aversion (CRRA) utility function with coefficient

$\gamma\gt 0$

. Thus, the utility function of the insurer

$\gamma\gt 0$

. Thus, the utility function of the insurer

$v(w)=w^{0.6}$

belongs to the same class, with parameter

$v(w)=w^{0.6}$

belongs to the same class, with parameter

$\gamma=0.4$

. In Figure 3, we show the optimal insurance contract as a function of the risk-aversion parameter

$\gamma=0.4$

. In Figure 3, we show the optimal insurance contract as a function of the risk-aversion parameter

$\gamma$

of the insured. We observe that as the insured becomes more risk averse, the insurance coverage increases, and the insurance premium rises disproportionately.

$\gamma$

of the insured. We observe that as the insured becomes more risk averse, the insurance coverage increases, and the insurance premium rises disproportionately.

The optimal parameter pair

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the risk-aversion parameter

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the risk-aversion parameter

$\gamma$

of the insured, with

$\gamma$

of the insured, with

$\delta=0.5$

and

$\delta=0.5$

and

$\tau=0.4$

.

$\tau=0.4$

.

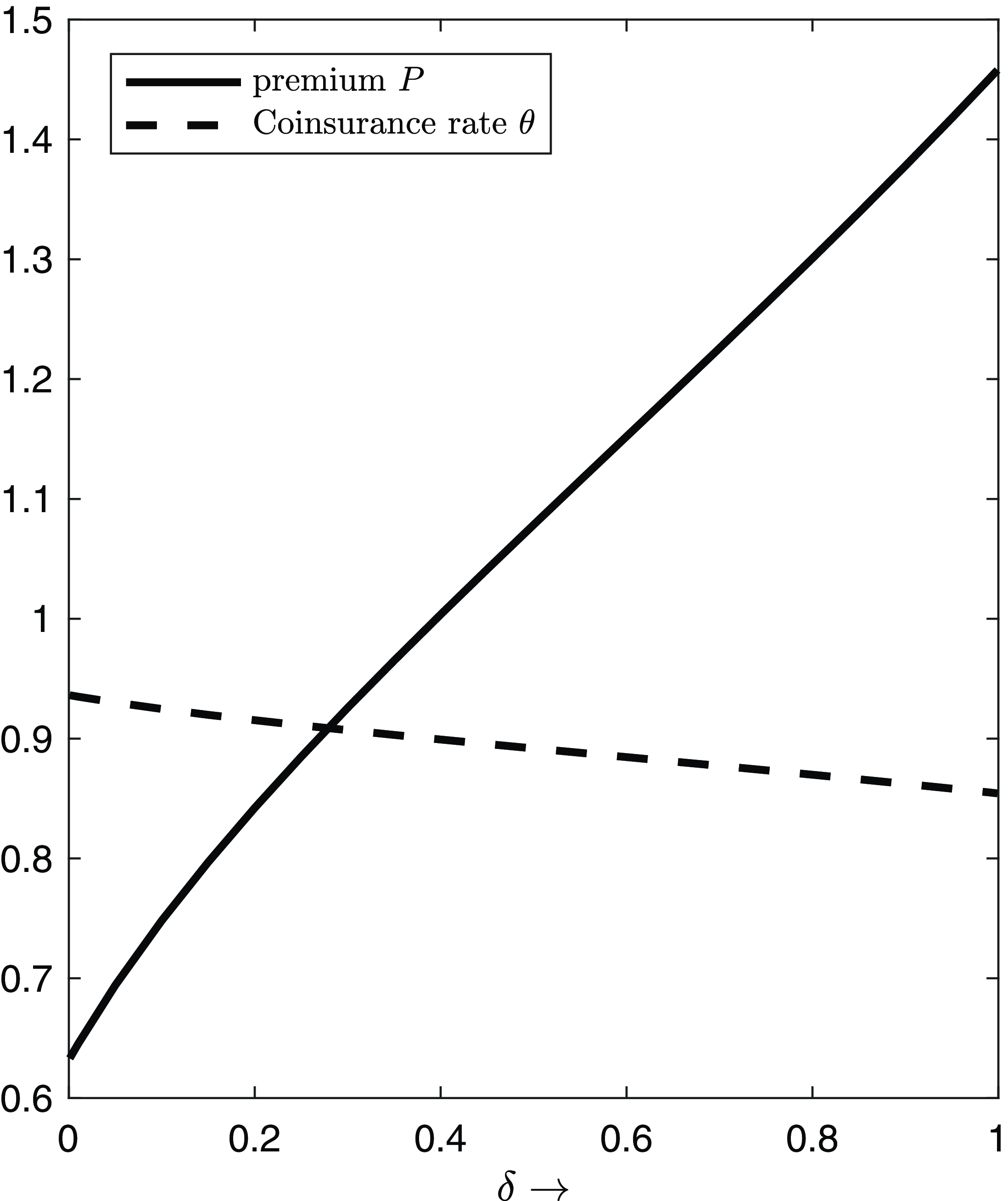

Second, we present a case in which the insurance coverage no longer increases in the bargaining power. We assume that the utility function of the insured is given as

\begin{equation}u(w)=w-\frac{\beta}{2} w^2.\end{equation}

\begin{equation}u(w)=w-\frac{\beta}{2} w^2.\end{equation}

Here,

$\beta=0.05$

controls the degree of risk aversion. We can easily verify that this utility function is increasing for wealth levels within the relevant range. However, the Arrow-Pratt coefficient of absolute risk aversion

$\beta=0.05$

controls the degree of risk aversion. We can easily verify that this utility function is increasing for wealth levels within the relevant range. However, the Arrow-Pratt coefficient of absolute risk aversion

$\mathcal A_u$

is increasing in w and the DARA assumption is not met. The optimal insurance contract is displayed in Figure 4. We find that the optimal insurance coverage

$\mathcal A_u$

is increasing in w and the DARA assumption is not met. The optimal insurance contract is displayed in Figure 4. We find that the optimal insurance coverage

$\theta$

is indeed decreasing in the bargaining power, while the insurance premium is increasing. Thus, if the insurer gets more bargaining power, he will charge a higher premium for less coverage. This represents a clear advantage for the insurer.

$\theta$

is indeed decreasing in the bargaining power, while the insurance premium is increasing. Thus, if the insurer gets more bargaining power, he will charge a higher premium for less coverage. This represents a clear advantage for the insurer.

The optimal parameter pair

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the bargaining power

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the bargaining power

$\delta\in(0,1)$

, where

$\delta\in(0,1)$

, where

$\tau=0.4$

,

$\tau=0.4$

,

$v(w)=w^{0.6}$

, and the utility function u is as in Equation (5.2) with

$v(w)=w^{0.6}$

, and the utility function u is as in Equation (5.2) with

$\beta=0.05$

.

$\beta=0.05$

.

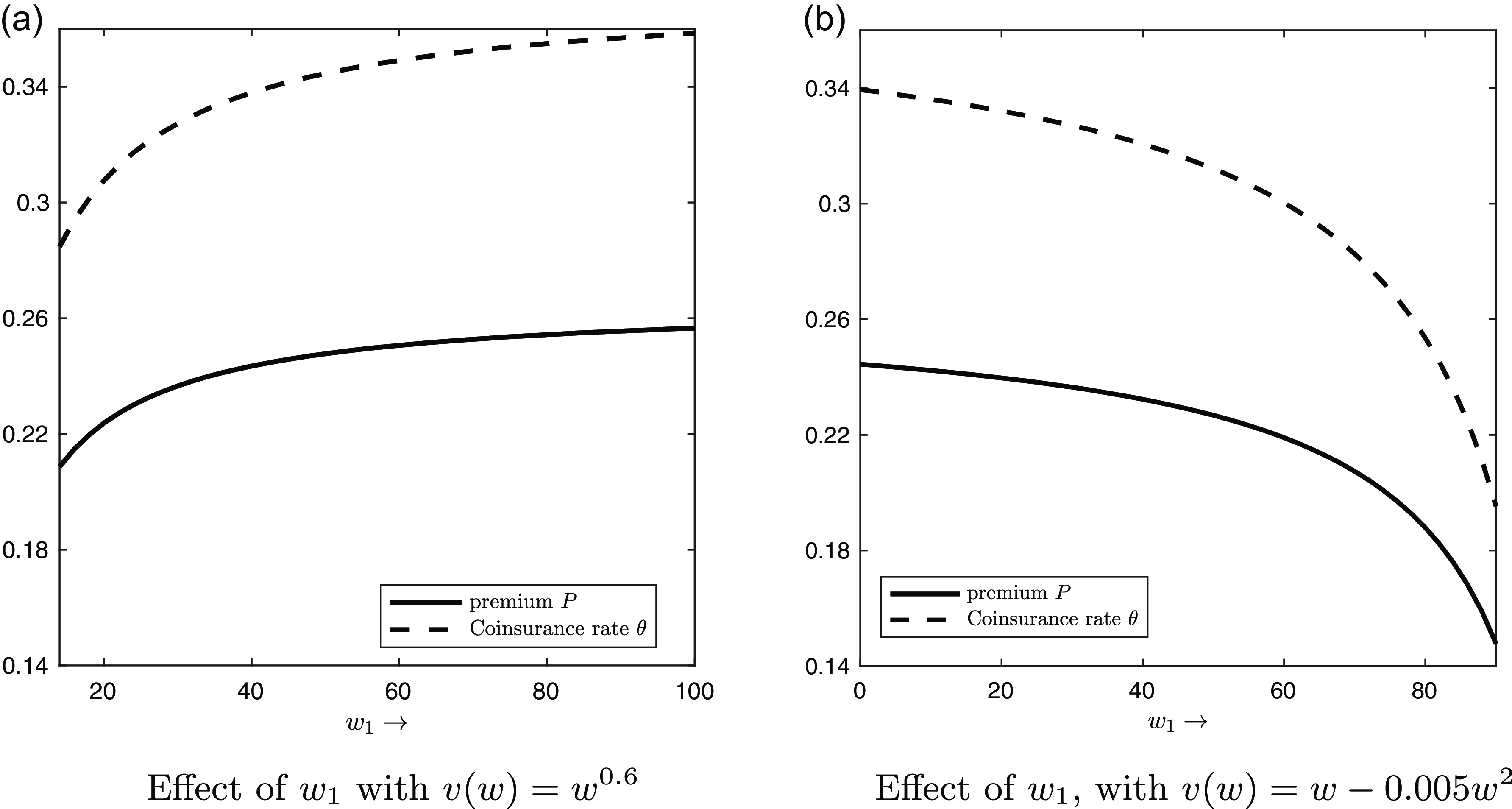

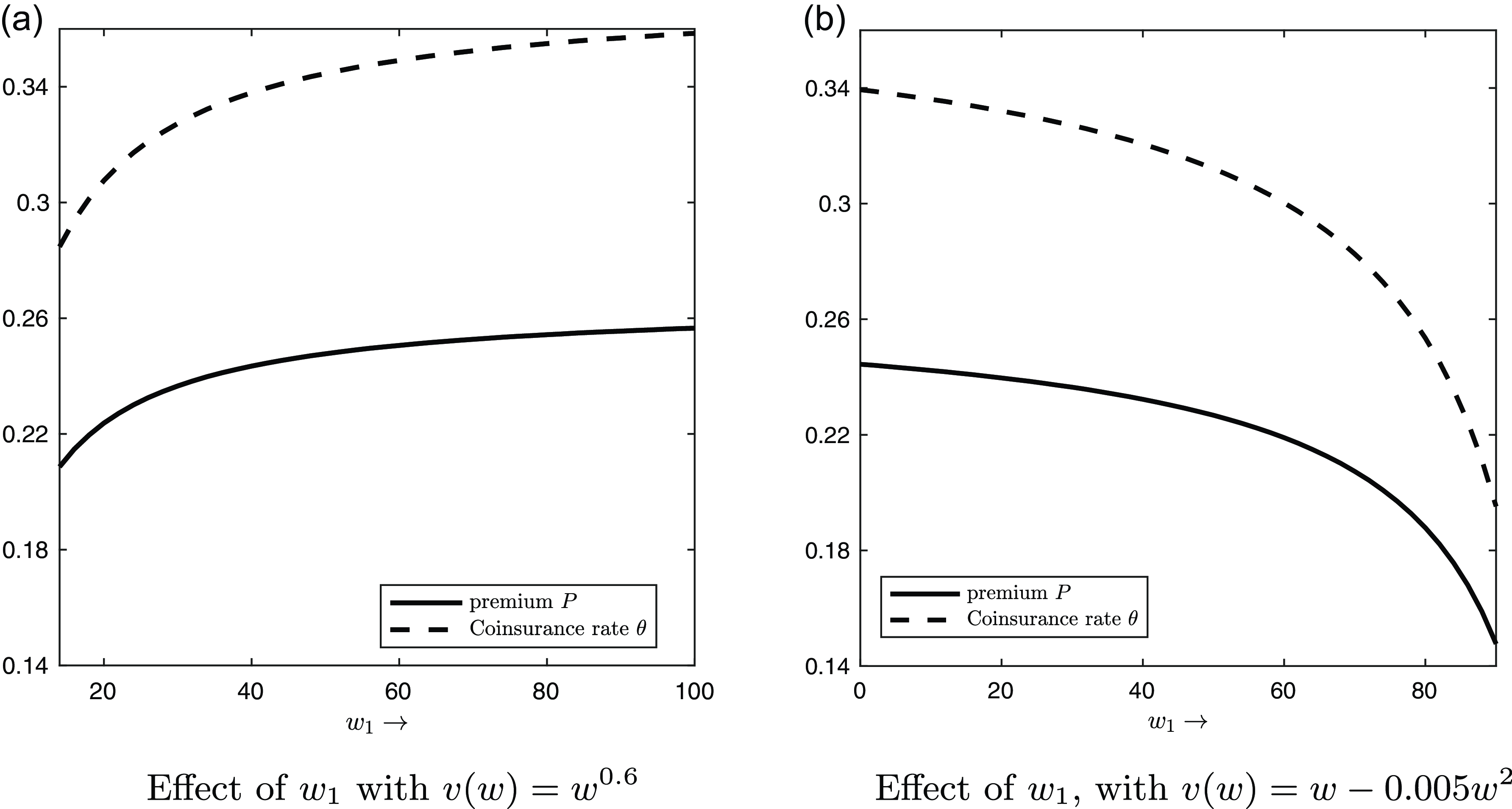

Third, we study the effect of the initial wealth of the insurer. Let the utility function of the insured u be given as in Equation (5.1) with coefficient

$\gamma=2$

. For two different utility functions v of the insurer, we show the optimal insurance contracts as a function of the initial wealth of the insurer in Figure 5. Proposition 8 shows that if v is DARA and u CARA, then under Assumption 1, the optimal rate of proportional insurance

$\gamma=2$

. For two different utility functions v of the insurer, we show the optimal insurance contracts as a function of the initial wealth of the insurer in Figure 5. Proposition 8 shows that if v is DARA and u CARA, then under Assumption 1, the optimal rate of proportional insurance

$\theta^*$

increases in the insurer’s initial wealth

$\theta^*$

increases in the insurer’s initial wealth

$w_1$

. This pattern is also evident in Figure 5(a), where both the insured and the insurer have DARA utility functions. However, Figure 5(b) shows that this pattern does not hold when v is not a DARA utility function but instead takes the functional form in Equation (5.2) with

$w_1$

. This pattern is also evident in Figure 5(a), where both the insured and the insurer have DARA utility functions. However, Figure 5(b) shows that this pattern does not hold when v is not a DARA utility function but instead takes the functional form in Equation (5.2) with

$\beta=0.01$

, which results in an increasing Arrow-Pratt coefficient of absolute risk aversion

$\beta=0.01$

, which results in an increasing Arrow-Pratt coefficient of absolute risk aversion

$\mathcal A_v$

for relevant wealth levels.

$\mathcal A_v$

for relevant wealth levels.

The optimal parameter pair

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the initial wealth of the insurer

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the initial wealth of the insurer

$w_1$

, with

$w_1$

, with

$\tau=0.4$

and

$\tau=0.4$

and

$\delta=0.5$

. Here, we use u as in Equation (5.1) with

$\delta=0.5$

. Here, we use u as in Equation (5.1) with

$\gamma=2$

.

$\gamma=2$

.

Fourth, and finally, we study the effect of background risk of the insurer. Recall that in our baseline example, we let the utility functions of the insured u and the insurer v be given as in Equation (5.1) with

$\gamma=2$

for the insured and

$\gamma=2$

for the insured and

$\gamma=0.4$

for the insurer. We model background risk via the following assumption:

$\gamma=0.4$

for the insurer. We model background risk via the following assumption:

\begin{equation}W_1=100-k X,\end{equation}

\begin{equation}W_1=100-k X,\end{equation}

Here,

$k\in\mathbb{R}$

measures the extent of background risk. If

$k\in\mathbb{R}$

measures the extent of background risk. If

$k\geqslant 0$

, then

$k\geqslant 0$

, then

$-W_1\uparrow_{hr}X$

. We show the optimal insurance contract as a function of

$-W_1\uparrow_{hr}X$

. We show the optimal insurance contract as a function of

$k\in[\!-\!2,2]$

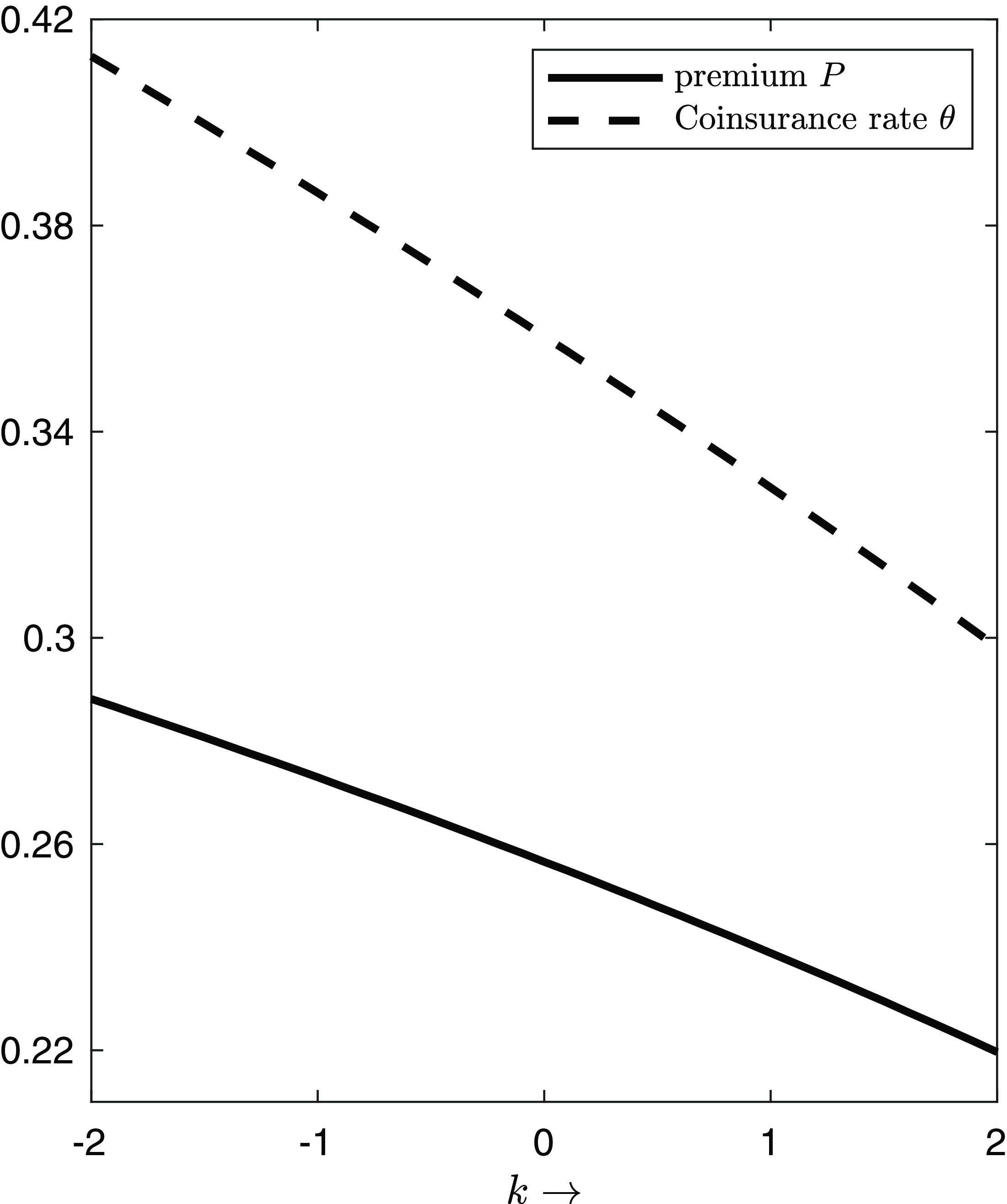

in Figure 6. We interpret a larger value of k as indicating greater background risk. Additionally,

$k\in[\!-\!2,2]$

in Figure 6. We interpret a larger value of k as indicating greater background risk. Additionally,

$k\geqslant0$

implies that new insurance risk is not attractive for the insurer due to a lack of diversification opportunities. From Figure 6, we observe that larger background risk leads to less coverage and a lower corresponding insurance premium. Additionally, we do not observe any discontinuity at

$k\geqslant0$

implies that new insurance risk is not attractive for the insurer due to a lack of diversification opportunities. From Figure 6, we observe that larger background risk leads to less coverage and a lower corresponding insurance premium. Additionally, we do not observe any discontinuity at

$k=0$

. Thus, a small change from positive to negative dependence, or vice versa, has little impact on the optimal insurance contract

$k=0$

. Thus, a small change from positive to negative dependence, or vice versa, has little impact on the optimal insurance contract

The optimal parameter pair

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the weight k that measures background risk (see Equation (5.3)), where

$(\theta, P)$

in the asymmetric Nash bargaining solution as a function of the weight k that measures background risk (see Equation (5.3)), where

$\tau=0.4$

,

$\tau=0.4$

,

$\delta=0.5$

,

$\delta=0.5$

,

$u(w)=-w^{-1}$

, and

$u(w)=-w^{-1}$

, and

$v(w)=w^{0.6}$

.

$v(w)=w^{0.6}$

.

6. Concluding remarks

In this paper, we study optimal insurance design under asymmetric Nash bargaining, assuming that both the insured and the insurer are risk averse and allowing the insurer’s initial wealth to be random. To simplify the analysis, ensure the feasibility of asymmetric Nash bargaining, and facilitate comparative statics, we focus on proportional insurance contracts. After obtaining a necessary and sufficient condition for Pareto optimality of the status quo, we derive the optimal Nash bargaining solutions when this condition is not satisfied. We show that when the insurer’s initial wealth is negatively dependent with the insurable risk, full insurance cannot be optimal, even if the deadweight cost is set to zero. We further find that insurance coverage increases with the insured’s risk aversion or the insurer’s bargaining power if the insurer’s initial wealth decreases in the insurable risk in the sense of the reversed hazard rate order and both parties exhibit DARA risk preferences. In particular, when the insured has a CARA utility function, greater insurance coverage is induced by higher initial wealth of the insurer.

We acknowledge that our analysis relies heavily on the assumption of proportional insurance. It would be interesting to revisit this problem using other types of insurance contracts. However, stop-loss insurance, which is widely used in the actuarial science literature, may not be a suitable choice. This is because the corresponding set of bargaining outcomes may not be convex, which prevents the direct application of the representation theorem for asymmetric Nash bargaining in Kalai (Reference Kalai1977). On the other hand, this paper analyzes the effect of changes in the insurer’s constant initial wealth on the optimal insurance coverage under the strict assumption that the insured has a CARA utility function. It would be valuable to investigate whether this comparative statics result remains valid when the CARA assumption on the insured’s risk preference is relaxed. We leave these questions to future research.

Acknowledgements

The authors would like to thank two anonymous referees and the handling editor for their helpful comments. The authors would also like to thank Tao Hu for his outstanding research assistance. Chi’s work was supported by grants from the National Natural Science Foundation of China (Grant No. 12371479), the MOE (China) Project of Key Research Institute of Humanities and Social Sciences at Universities (Grant No. 22JJD790090), and the Fundamental Research Funds for the Central Universities at the Central University of Finance and Economics.

A Proofs

A.1 Proof of Proposition 1

First, we show that the Pareto optimality of the status quo is equivalent to

\begin{eqnarray}0\in \arg\max _{\theta \in [0,1]}\psi(\theta)\,:\!=\, \mathbb{E}[u(w_{0}-X+I_\theta(X) -P_{-}(\theta))],\end{eqnarray}

\begin{eqnarray}0\in \arg\max _{\theta \in [0,1]}\psi(\theta)\,:\!=\, \mathbb{E}[u(w_{0}-X+I_\theta(X) -P_{-}(\theta))],\end{eqnarray}

where

$P_{-}(\theta)$

is the solution to Equation (2.2). More specifically, according to the definition of

$P_{-}(\theta)$

is the solution to Equation (2.2). More specifically, according to the definition of

$P_{+}(\theta)$

in Equation (2.3), the Pareto optimality of the status quo is equivalent to

$P_{+}(\theta)$

in Equation (2.3), the Pareto optimality of the status quo is equivalent to

$P_{-}(\theta)\geqslant P_{+}(\theta)$

for any

$P_{-}(\theta)\geqslant P_{+}(\theta)$

for any

$\theta\in[0,1]$

. It is further equivalent to

$\theta\in[0,1]$

. It is further equivalent to

\begin{eqnarray*}\mathbb{E}[u(w_{0}-X+\theta X-P_{-}(\theta))]&\leqslant& \mathbb{E}[u(w_{0}-X+\theta X-P_{+}(\theta))]\\&=&\mathbb{E}[u(w_{0}-X)]=\mathbb{E}[u(w_{0}-X-P_{-}(0))],\end{eqnarray*}

\begin{eqnarray*}\mathbb{E}[u(w_{0}-X+\theta X-P_{-}(\theta))]&\leqslant& \mathbb{E}[u(w_{0}-X+\theta X-P_{+}(\theta))]\\&=&\mathbb{E}[u(w_{0}-X)]=\mathbb{E}[u(w_{0}-X-P_{-}(0))],\end{eqnarray*}

where the last equality is derived by the fact

$P_{-}(0)=0$

. In other words, 0 is a solution to the optimization problem

$P_{-}(0)=0$

. In other words, 0 is a solution to the optimization problem

$\max _{\theta \in [0,1]}\psi(\theta)$

.

$\max _{\theta \in [0,1]}\psi(\theta)$

.

Next, we can show that the function

$\psi(\theta)$

is concave. More specifically, for any

$\psi(\theta)$

is concave. More specifically, for any

$\theta_1,\theta_2\in[0,1]$

and any

$\theta_1,\theta_2\in[0,1]$

and any

$\lambda\in[0,1]$

, the concavity of v implies

$\lambda\in[0,1]$

, the concavity of v implies

\begin{eqnarray*}\mathbb{E}[v(W_{1})]&=&\lambda\mathbb{E}[v(W_{1}+P_{-}(\theta_1)-(1+\tau)\theta_1 X)]+(1-\lambda)\mathbb{E}[v(W_{1}+P_{-}(\theta_2)-(1+\tau)\theta_2 X)]\\&\leqslant&\mathbb{E}\left[v(W_{1}+\lambda P_{-}(\theta_1)+(1-\lambda)P_{-}(\theta_2)-(1+\tau)(\lambda\theta_1+(1-\lambda)\theta_2) X)\right],\end{eqnarray*}

\begin{eqnarray*}\mathbb{E}[v(W_{1})]&=&\lambda\mathbb{E}[v(W_{1}+P_{-}(\theta_1)-(1+\tau)\theta_1 X)]+(1-\lambda)\mathbb{E}[v(W_{1}+P_{-}(\theta_2)-(1+\tau)\theta_2 X)]\\&\leqslant&\mathbb{E}\left[v(W_{1}+\lambda P_{-}(\theta_1)+(1-\lambda)P_{-}(\theta_2)-(1+\tau)(\lambda\theta_1+(1-\lambda)\theta_2) X)\right],\end{eqnarray*}

which together with Equation (2.2) implies

\begin{align*}\lambda P_{-}(\theta_1)+(1-\lambda)P_{-}(\theta_2)\geqslant P_{-}(\lambda\theta_1+(1-\lambda)\theta_2).\end{align*}

\begin{align*}\lambda P_{-}(\theta_1)+(1-\lambda)P_{-}(\theta_2)\geqslant P_{-}(\lambda\theta_1+(1-\lambda)\theta_2).\end{align*}

In other words,

$P_{-}(\theta)$

is convex. As a result, the concavity of u implies

$P_{-}(\theta)$

is convex. As a result, the concavity of u implies

\begin{eqnarray*}\psi(\lambda\theta_1+(1-\lambda)\theta_2)&=&\mathbb{E}\left[u(w_{0}-X+(\lambda\theta_1+(1-\lambda)\theta_2)X -P_{-}(\lambda\theta_1+(1-\lambda)\theta_2))\right]\\&\geqslant&\mathbb{E}\left[u\left(w_{0}-X+\lambda(\theta_1X-P_{-}(\theta_1))+(1-\lambda)(\theta_2X - P_{-}(\theta_2))\right)\right]\\&\geqslant&\lambda \mathbb{E}\left[u(w_{0}-X+\theta_1X -P_{-}(\theta_1))\right]+(1-\lambda)\mathbb{E}\left[u(w_{0}-X+\theta_2X -P_{-}(\theta_2))\right]\\&=&\lambda\psi(\theta_1)+(1-\lambda)\psi(\theta_2).\end{eqnarray*}

\begin{eqnarray*}\psi(\lambda\theta_1+(1-\lambda)\theta_2)&=&\mathbb{E}\left[u(w_{0}-X+(\lambda\theta_1+(1-\lambda)\theta_2)X -P_{-}(\lambda\theta_1+(1-\lambda)\theta_2))\right]\\&\geqslant&\mathbb{E}\left[u\left(w_{0}-X+\lambda(\theta_1X-P_{-}(\theta_1))+(1-\lambda)(\theta_2X - P_{-}(\theta_2))\right)\right]\\&\geqslant&\lambda \mathbb{E}\left[u(w_{0}-X+\theta_1X -P_{-}(\theta_1))\right]+(1-\lambda)\mathbb{E}\left[u(w_{0}-X+\theta_2X -P_{-}(\theta_2))\right]\\&=&\lambda\psi(\theta_1)+(1-\lambda)\psi(\theta_2).\end{eqnarray*}

Finally, it is easy to get from Equation (2.2) and the Implicit Function Theorem that

$P_{-}(\theta)$

is differentiable with

$P_{-}(\theta)$

is differentiable with

\begin{eqnarray*}P_{-}'(\theta) = \frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]}\end{eqnarray*}

\begin{eqnarray*}P_{-}'(\theta) = \frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]}\end{eqnarray*}

almost everywhere, which in turn implies

\begin{eqnarray*}\psi'(\theta)&=&\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]\\&&\quad\times\left\{\frac{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))X]}{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]}-\frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]}\right\}.\end{eqnarray*}

\begin{eqnarray*}\psi'(\theta)&=&\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]\\&&\quad\times\left\{\frac{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))X]}{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]}-\frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]}\right\}.\end{eqnarray*}

Recall that

$\psi(\theta)$

is a concave function. A necessary and sufficient condition for Equation (A1) is

$\psi(\theta)$

is a concave function. A necessary and sufficient condition for Equation (A1) is

$ \lim_{\theta \downarrow 0}\psi'(\theta) \leqslant 0$

. Equivalently,

$ \lim_{\theta \downarrow 0}\psi'(\theta) \leqslant 0$

. Equivalently,

\begin{eqnarray*}0&\geqslant& \lim_{\theta \downarrow 0} \left\{\frac{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))X]}{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]}-\frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]} \right\} \\&=& \frac{ \mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X )]} -(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}.\end{eqnarray*}

\begin{eqnarray*}0&\geqslant& \lim_{\theta \downarrow 0} \left\{\frac{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))X]}{\mathbb{E}[u'(w_{0}-X+I_\theta (X) -P_{-}(\theta))]}-\frac{(1+\tau)\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)X]}{\mathbb{E}[v'(W_{1}+P_{-}(\theta)-(1+\tau)\theta X)]} \right\} \\&=& \frac{ \mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X )]} -(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}.\end{eqnarray*}

It is indeed Equation (3.3). The proof is thus completed.

A.2 Proof of Proposition 2

We first show that the set

$\mathbf{S}$

is compact. For any convergence sequence

$\mathbf{S}$

is compact. For any convergence sequence

$\{\mathbf{a}_n\in\mathbf{S}:n=1,2,...\}$

, there exist

$\{\mathbf{a}_n\in\mathbf{S}:n=1,2,...\}$

, there exist

$\theta_n\in[0,1]$

and

$\theta_n\in[0,1]$

and

$P_n\in[P_{-}(\theta_n), P_{+}(\theta_n)]$

such that

$P_n\in[P_{-}(\theta_n), P_{+}(\theta_n)]$

such that

\begin{eqnarray*}\mathbf{a}_n=\binom{\mathbb{E}[u(w_0-X+I_{\theta_n}(X)-P_n)]}{\mathbb{E}[v(W_1+P_n-(1+\tau)I_{\theta_n}(X))]}.\end{eqnarray*}

\begin{eqnarray*}\mathbf{a}_n=\binom{\mathbb{E}[u(w_0-X+I_{\theta_n}(X)-P_n)]}{\mathbb{E}[v(W_1+P_n-(1+\tau)I_{\theta_n}(X))]}.\end{eqnarray*}

Due to

$\theta_n\in[0,1]$

and

$\theta_n\in[0,1]$

and

$P_n\in[0, M]$

, we can get a convergence subsequence

$P_n\in[0, M]$

, we can get a convergence subsequence

$\left\{(\theta_{n_k},P_{n_k})\right\}_{k=1}^{\infty}$

. Without loss of generality, we denote

$\left\{(\theta_{n_k},P_{n_k})\right\}_{k=1}^{\infty}$

. Without loss of generality, we denote

\begin{eqnarray*}\theta=\lim_{k\to\infty}\theta_{n_k}\quad\text{and}\quad P=\lim_{k\to\infty}P_{n_k},\end{eqnarray*}

\begin{eqnarray*}\theta=\lim_{k\to\infty}\theta_{n_k}\quad\text{and}\quad P=\lim_{k\to\infty}P_{n_k},\end{eqnarray*}

then

$\theta\in[0,1]$

and

$\theta\in[0,1]$

and

$P_{-}(\theta)\leqslant P\leqslant P_{+}(\theta)$

. Due to the continuity of the expected utilities with respect to the proportion and the insurance premium, we can get

$P_{-}(\theta)\leqslant P\leqslant P_{+}(\theta)$

. Due to the continuity of the expected utilities with respect to the proportion and the insurance premium, we can get

\begin{eqnarray*}\lim_{n\to\infty}\mathbf{a}_{n}=\lim_{k\to\infty}\mathbf{a}_{n_k}=\binom{\mathbb{E}[u(w_0-X+I_{\theta}(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))]}\in \mathbf{S}.\end{eqnarray*}

\begin{eqnarray*}\lim_{n\to\infty}\mathbf{a}_{n}=\lim_{k\to\infty}\mathbf{a}_{n_k}=\binom{\mathbb{E}[u(w_0-X+I_{\theta}(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))]}\in \mathbf{S}.\end{eqnarray*}

Thus, we can claim that

$\mathbf{S}$

is compact.

$\mathbf{S}$

is compact.

Next, we proceed to prove that

$\mathbf{S}$

is convex. Note that for any

$\mathbf{S}$

is convex. Note that for any

$\mathbf{a}_i\in\mathbf{S}$

, there exist

$\mathbf{a}_i\in\mathbf{S}$

, there exist

$\theta_i\in[0,1]$

and

$\theta_i\in[0,1]$

and

$P_i\in[P_{-}(\theta_i), P_{+}(\theta_i)]$

such that

$P_i\in[P_{-}(\theta_i), P_{+}(\theta_i)]$

such that

\begin{eqnarray*}\mathbf{a}_i=\binom{\mathbb{E}[u(w_0-X+I_{\theta_i}(X)-P_i)]}{\mathbb{E}[v(W_1+P_i-(1+\tau)I_{\theta_i}(X))]},\,i=1,2.\end{eqnarray*}

\begin{eqnarray*}\mathbf{a}_i=\binom{\mathbb{E}[u(w_0-X+I_{\theta_i}(X)-P_i)]}{\mathbb{E}[v(W_1+P_i-(1+\tau)I_{\theta_i}(X))]},\,i=1,2.\end{eqnarray*}

Given any

$\lambda\in(0,1)$

, we define

$\lambda\in(0,1)$

, we define

$\tilde{P}_{-}(\theta)$

and

$\tilde{P}_{-}(\theta)$

and

$\tilde{P}_{+}(\theta)$

as the solutions to the following equations

$\tilde{P}_{+}(\theta)$

as the solutions to the following equations

\begin{eqnarray*}&&\lambda\mathbb{E}[v(W_1+P_1-(1+\tau)I_{\theta_1}(X))]+(1-\lambda)\mathbb{E}[v(W_1+P_2-(1+\tau)I_{\theta_2}(X))]\\&&=\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))],\, P\in \mathbb{R}\end{eqnarray*}

\begin{eqnarray*}&&\lambda\mathbb{E}[v(W_1+P_1-(1+\tau)I_{\theta_1}(X))]+(1-\lambda)\mathbb{E}[v(W_1+P_2-(1+\tau)I_{\theta_2}(X))]\\&&=\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))],\, P\in \mathbb{R}\end{eqnarray*}

and

\begin{eqnarray*}&&\lambda\mathbb{E}[u(w_0-X-P_1+I_{\theta_1}(X))]+(1-\lambda)\mathbb{E}[u(w_0-X-P_2+I_{\theta_2}(X)]\\&&=\mathbb{E}[u(w_0-X-P+I_{\theta}(X)],\, P\in \mathbb{R},\end{eqnarray*}

\begin{eqnarray*}&&\lambda\mathbb{E}[u(w_0-X-P_1+I_{\theta_1}(X))]+(1-\lambda)\mathbb{E}[u(w_0-X-P_2+I_{\theta_2}(X)]\\&&=\mathbb{E}[u(w_0-X-P+I_{\theta}(X)],\, P\in \mathbb{R},\end{eqnarray*}

respectively for each

$\theta\in[0,1]$

. Using the concavity property of u and v, we can easily find that

$\theta\in[0,1]$

. Using the concavity property of u and v, we can easily find that

$\tilde{P}_{-}(\theta)$

is convex while

$\tilde{P}_{-}(\theta)$

is convex while

$\tilde{P}_{+}(\theta)$

is concave, and get

$\tilde{P}_{+}(\theta)$

is concave, and get

\begin{eqnarray*}\tilde{P}_{-}(\lambda\theta_1+(1-\lambda)\theta_2)\leqslant \lambda P_1+(1-\lambda)P_2\leqslant\tilde{P}_{+}(\lambda\theta_1+(1-\lambda)\theta_2).\end{eqnarray*}

\begin{eqnarray*}\tilde{P}_{-}(\lambda\theta_1+(1-\lambda)\theta_2)\leqslant \lambda P_1+(1-\lambda)P_2\leqslant\tilde{P}_{+}(\lambda\theta_1+(1-\lambda)\theta_2).\end{eqnarray*}

Furthermore, due to the rationality conditions (2.2) and (2.3), we obtain

\begin{eqnarray*}\tilde{P}_{+}(0)\leqslant 0\leqslant \tilde{P}_{-}(0).\end{eqnarray*}

\begin{eqnarray*}\tilde{P}_{+}(0)\leqslant 0\leqslant \tilde{P}_{-}(0).\end{eqnarray*}

More precisely,

$\tilde{P}_{+}(\theta)-\tilde{P}_{-}(\theta)$

is a concave function, which is non-positive at 0 and non-negative at

$\tilde{P}_{+}(\theta)-\tilde{P}_{-}(\theta)$

is a concave function, which is non-positive at 0 and non-negative at

$\lambda\theta_1+(1-\lambda)\theta_2$

. Thus, there must exist a

$\lambda\theta_1+(1-\lambda)\theta_2$

. Thus, there must exist a

$\theta\in[0, \lambda\theta_1+(1-\lambda)\theta_2]$

such that

$\theta\in[0, \lambda\theta_1+(1-\lambda)\theta_2]$

such that

$\tilde{P}_{+}(\theta)=\tilde{P}_{-}(\theta)\geqslant \tilde{P}_{-}(0)\geqslant 0$

. Setting

$\tilde{P}_{+}(\theta)=\tilde{P}_{-}(\theta)\geqslant \tilde{P}_{-}(0)\geqslant 0$

. Setting

$P=\tilde{P}_{+}(\theta)$

, we can verify that the rationality condition (2.1) is satisfied by the proportional insurance

$P=\tilde{P}_{+}(\theta)$

, we can verify that the rationality condition (2.1) is satisfied by the proportional insurance

$(I_\theta, P)$

, and

$(I_\theta, P)$

, and

\begin{align*}\binom{\mathbb{E}[u(w_0-X+I_{\theta}(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))]}=\lambda\mathbf{a}_1+(1-\lambda)\mathbf{a}_2.\end{align*}

\begin{align*}\binom{\mathbb{E}[u(w_0-X+I_{\theta}(X)-P)]}{\mathbb{E}[v(W_1+P-(1+\tau)I_{\theta}(X))]}=\lambda\mathbf{a}_1+(1-\lambda)\mathbf{a}_2.\end{align*}

Thus, the set

$\mathbf{S}$

is convex.

$\mathbf{S}$

is convex.

A.3 Proof of Proposition 3

From the proof of Proposition 1 in Appendix A.1, we can see that

\begin{eqnarray*}\lim_{\theta \downarrow 0}\psi'(\theta)=\mathbb{E}[u'(w_{0}-X )]\left(\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X )]} -(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}\right)\gt 0\end{eqnarray*}

\begin{eqnarray*}\lim_{\theta \downarrow 0}\psi'(\theta)=\mathbb{E}[u'(w_{0}-X )]\left(\frac{\mathbb{E}[u'(w_{0}-X)X]}{\mathbb{E}[u'(w_{0}-X )]} -(1+\tau)\frac{\mathbb{E}[v'(W_1)X]}{\mathbb{E}[v'(W_1)]}\right)\gt 0\end{eqnarray*}

under Assumption 1. In other words, for the

$\theta$

very close to 0,

$\theta$

very close to 0,

$\psi'(\theta)\gt 0$

such that

$\psi'(\theta)\gt 0$

such that

\begin{eqnarray*}\psi(\theta)\gt \psi(0)=\mathbb{E}[u(w_0-X)]=\mathbb{E}[u(w_{0}-X+I_\theta(X)-P_{+}(\theta))],\end{eqnarray*}

\begin{eqnarray*}\psi(\theta)\gt \psi(0)=\mathbb{E}[u(w_0-X)]=\mathbb{E}[u(w_{0}-X+I_\theta(X)-P_{+}(\theta))],\end{eqnarray*}

which in turn implies

$P_{-}(\theta)\lt P_{+}(\theta)$

. Therefore, all such

$P_{-}(\theta)\lt P_{+}(\theta)$

. Therefore, all such

$\theta$

belong to the set

$\theta$

belong to the set

$\Theta$

and hence the point 0 is on the boundary of

$\Theta$

and hence the point 0 is on the boundary of

$\Theta$

.

$\Theta$

.

Next, we show that

$P_{+}(\theta)$

is concave. More specifically, for any

$P_{+}(\theta)$

is concave. More specifically, for any

$\theta_1,\theta_2\in[0,1]$

and

$\theta_1,\theta_2\in[0,1]$

and

$\lambda\in[0,1]$

, we have

$\lambda\in[0,1]$

, we have

\begin{eqnarray*}&&\mathbb{E}[u(w_0-X)]\\&&=\lambda \mathbb{E}\left[u(w_0-X-P_{+}(\theta_1)+I_{\theta_1}(X))\right]+(1-\lambda) \mathbb{E}\left[u\left(w_0-X-P_{+}(\theta_2)+I_{\theta_2}(X)\right)\right]\\&&\leqslant\mathbb{E}[u\left(w_0-X-\lambda P_{+}(\theta_1)-(1-\lambda)P_{+}(\theta_2)+I_{\lambda\theta_1+(1-\lambda)\theta_2}(X)\right)\!],\end{eqnarray*}

\begin{eqnarray*}&&\mathbb{E}[u(w_0-X)]\\&&=\lambda \mathbb{E}\left[u(w_0-X-P_{+}(\theta_1)+I_{\theta_1}(X))\right]+(1-\lambda) \mathbb{E}\left[u\left(w_0-X-P_{+}(\theta_2)+I_{\theta_2}(X)\right)\right]\\&&\leqslant\mathbb{E}[u\left(w_0-X-\lambda P_{+}(\theta_1)-(1-\lambda)P_{+}(\theta_2)+I_{\lambda\theta_1+(1-\lambda)\theta_2}(X)\right)\!],\end{eqnarray*}