1. Introduction

Many populations worldwide have experienced significant mortality improvements throughout the last decades, and human mortality has shifted to later ages (see Vaupel et al. Reference Vaupel, Villavicencio and Bergeron-Boucher2021). The advancement of the longevity frontier implies compelling financial challenges for individuals aiming to manage their post-retirement income, as well as for annuity providers. Individuals living longer face the risk of outliving their wealth, and at least theoretically, they should look at the standard life annuity as an optimal vehicle for insuring against the individual longevity risk (Yaari Reference Yaari1965). But in reality, the voluntary annuity market remains thin because of rational and behavioural individual reasons driving the life annuities demand (see, e.g., Brown Reference Brown2001; Reference Brown2009). The downward trend in mortality rates, jointly with the uncertainty of financial markets and the evolving demographic structure of many populations, has led social security schemes and pension funds to revise pension benefits downwards. The shift from Defined Benefit to Defined Contribution plans has also taken hold. Consequently, individuals remain exposed to both individual investment and longevity risks; transferring such risks to a private annuity provider should be perceived as a beneficial strategy for building a suitable and stable retirement income. However, on their side, life insurers suffer the cost of financial and longevity guarantees traditionally embedded in life annuities, and they have become averse to offering non-adjustable longevity guarantees. The aggregate longevity risk cannot be diversified through risk pooling strategies and could require considerable equity capital backing due to risk-based solvency regulations. Then, academics and practitioners have examined alternative longevity risk management solutions. For instance, Blake et al. (Reference Blake, Cairns and Dowd2006) discuss how annuity providers can use mortality/longevity-linked securities to handle the risk of uncertain aggregate mortality. Even with great potential, the demand for the capital market securities proposed over the last decade has been very low, and annuity providers mainly relied on insurance-based solutions, such as buy-outs, buy-ins and insurance-based longevity swaps (Blake et al. Reference Blake, Cairns, Dowd and Kessler2019). Non-financial longevity reinsurance may also be considered, but it is usually costly and ultimately has to be funded by higher insurance premiums. As a workable alternative, longevity-linked arrangements have been proposed in the literature (see, e.g, Olivieri and Pitacco Reference Olivieri and Pitacco2020). Beyond the specific design of these products, the underlying idea is that the insurer shares the risk with the policyholder by linking the life annuity benefits, directly or indirectly, to the mortality experience of a reference population. If unexpected mortality improvements occur, the insurer can mitigate its longevity risk exposure, but in the meantime, the benefits amount would decrease, likely hurting the demand for such insurance products.

Each longevity risk management solution has drawbacks, and insurers are motivated to modify their products by partially shifting risks to the policyholder. In the recent actuarial literature, notable attention has been given to pooling designs as innovative risk-sharing mechanisms to support the post-retirement income of individuals. Their common feature consists of grouping individuals to create a fund, from which each participant will receive periodical benefits adjusted according to the investment returns and mortality experienced by the pool, with no guarantee embedded. As a result, pool participants share among themselves the financial and longevity risk, and the insurer could play the role of administrator, not a guarantor (Dhaene and Milevsky Reference Dhaene and Milevsky2024). Different pooling structures have been proposed in the literature, such as the pooled annuity funds (see, e.g., Donnelly et al., Reference Donnelly, Montserrat and Nielsen2014; Donnelly, Reference Donnelly2015), and tontine annuities (see, e.g., Milevsky and Salisbury, Reference Milevsky and Salisbury2015; Chen et al., Reference Chen, Hieber and Klein2019; Weinert and Grüundl, 2021; Chen et al., Reference Chen, Chen and Xu2022; Hieber and Lucas, Reference Hieber and Lucas2022) among others.

In the present work, we refer to one of the earlier pooling structures, namely the group self-annuitisation (GSA). Introduced by Piggott et al. (Reference Piggott, Valdez and Detzel2005), a GSA scheme is a mutual insurance plan wherein individuals are brought together to pool both their investment and longevity risks. Individuals joining the GSA scheme pay an initial contribution determined according to an annuity payout rate. Therefore, the benefits that GSA members receive periodically account for both the expected mortality dynamics and the expected return on investments. Considering that the pool is required to fully cover its liabilities with its own assets at all times, future benefits have to be adjusted if the actual mortality and/or the realised investments return diverge from their respective expectations. Qiao and Sherris (Reference Qiao and Sherris2013) further study the GSA plan by assessing its effectiveness when systematic longevity risk is also considered. Shedding light on the investment activity of GSA plans, Olivieri et al. (Reference Olivieri, Thirurajah and Ziveyi2022) propose a dynamic target volatility strategy to enhance the survival benefits of the pool participants. Kabuche et al. (Reference Kabuche, Sherris, Villegas and Ziveyi2024) expand the GSA structure, allowing group participants to share both longevity and health risks. To this end, a multi-state GSA plan is proposed to pool heterogeneous individuals and provide annuity benefits updated according to both realised health transitions and mortality experienced. Aragona et al. (Reference Aragona, Regis and Vigna2025) introduce a redistributive GSA fund aiming to optimally share benefits among heterogeneous participants belonging to different socio-economic classes.

There is a growing attention, both in the market and literature, towards annuity and pooling designs providing differentiated benefits by health status, as a lever to foster annuitisation. The background assumption is that individuals who feel to have a shorter life expectancy, due to illnesses or lifestyle habits, may be reluctant to opt into a standard plan, while they might find it convenient to join arrangements that pay higher benefits should a shorter life expectancy be ascertained. Special rate (or underwritten or substandard) annuities are designed to respond to such a preference (see, for example, Pitacco and Tabakova Reference Pitacco and Tabakova2022; Ramsay et al. Reference Ramsay, Oguledo and Krutto2025; de Andrés-Sánchez and González-Vila Puchades Reference de Andrés-Sánchez and González-Vila Puchades2025); in the context of self-insured plans, the pooling arrangement proposed by Kabuche et al. (Reference Kabuche, Sherris, Villegas and Ziveyi2024) is also suitable in this respect.

Against this background, we propose a multi-state framework that explicitly incorporates the mortality heterogeneity characterising GSA members, with the objective of defining a design admitting a benefit differentiation. Our focus, in particular, is on whether the GSA scheme should differentiate benefits so that frailer individuals (with shorter life expectancy and presumably greater current financial needs, due to higher healthcare or care-related expenses) receive higher payments than healthier individuals (who are expected to cash benefits for a longer time).

Individual mortality is influenced by various elements, such as current health status, lifestyles, socio-economic conditions and climate characteristics. Each of these elements could significantly reshape the lifespan of individuals, and in particular, the timing of their ageing. In this paper, we refer to ageing as a continuous-time deterioration process of the human physiological functions necessary for survival. Individuals could bear a series of ageing phases before dying, and the speed at which ageing progresses varies from person to person, generating heterogeneity in the mortality of a population. While in a traditional GSA scheme benefits are adjusted based on aggregate realised mortality, we aim to design a GSA in which benefit adjustments account for both realised ageing transitions and mortality. Accordingly, a mortality model that explicitly accounts for the ageing process must be considered.

Individual’s ageing does not necessarily move in lockstep with calendar time. The so-called biological age is an example of this, that is, the age indicating how old the human mechanism is at both the cellular and molecular levels (see, e.g., Jackson et al. Reference Jackson, Weale and Weale2003). Biological age is usually determined with a microscopic approach, that is, by collecting data concerning physiological and molecular variables for a large sample of people, and, through regression techniques, an increment or a reduction of the corresponding chronological age is inferred. We refer the interested reader to Li et al. (Reference Li, Zhang, Duan, Niu, Chen, Liu, Dong, Zheng, Chen, Feng, Wang, Zhao, Sun, Cai, Jiang and Chen2023) for a discussion on the methods proposed in the literature for calculating biological age; we also refer the reader to Milevsky (Reference Milevsky2020) for an actuarial view on using biological age in mortality analysis. The biological age measurement requires high data granularity, and it is subject to both data collection and processing times. In contrast, annuity providers, as well as the administrators of a pooling fund, usually have access to mortality data only at an aggregate level, without having the possibility to observe biological factors. When there are no detectable biological factors other than age, the ageing process can still be represented, with the so-called Markov ageing model (see Lin and Liu Reference Lin and Liu2007; Liu and Lin Reference Liu and Lin2012; Su and Sherris Reference Su and Sherris2012; Cheng et al. Reference Cheng, Jones, Liu and Ren2020). It is a finite-state continuous-time Markov process suitable for modelling the human ageing evolution. Each state of the Markov process identifies an ageing phase, and the overall ageing process is described through consecutive transitions from one ageing state to a higher one. An absorbing (death) state is also included, and the transition from any ageing state to the absorbing state represents the ageing process termination due to death. The Markov ageing model allows for linking directly the age-specific mortality pattern to the ageing process, and the intrinsic heterogeneity of a cohort can be expressed explicitly. In addition, the stochastic process has desirable analytical properties suitable for mortality analysis.

We define a pooling design, which we refer to as a Markov ageing GSA, in which individuals joining the pool are classified according to their initial ageing state, and their ageing trajectory is reassessed annually. Benefits are differentiated by state; upon transitioning to a higher ageing state, the individual’s benefit is topped up to the level associated with the new state. Each individual contributes an initial capital assessed accounting for the initial state, the expected transition to higher ageing states and to the death state, as well as for the expected investment return. For the sake of simplicity, we assume a deterministic financial setting and a constant return on investments. This enables us to isolate and examine the effects on the benefit profile of the uncertain mortality dynamics in a context of a heterogeneous population. Similarly to a plain GSA, to preserve the actuarial equivalence between benefits and available resources, benefits are adjusted annually if experience deviates from expectation. In our setting, we account for both the realised ageing process pattern and actual mortality. Benefit adjustments are state-specific; any deficit or surplus arising from deviations between expected and realised experience is allocated across states in a way that reflects both the relative value of obligations in each state and the potential severity of deviations within each state. In a first phase of the analysis, benefit differentiation and adjustments are defined so to ensure actuarial equivalence for each state. To this end, making cross-subsidy mechanisms between states explicit is crucial. However, as noted above, the ageing process is not directly observable at the individual level but must be inferred from proxy factors, such as the onset of disabling illnesses or the worsening of lifestyle behaviours. This is a critical issue, in respect of both suitability of the proxy risk factors and potential self-interested behaviours by individuals. Participants, in particular, may have specific targets regarding the degree of benefit differentiation, which are not necessarily ensured by an actuarially equivalent adjustment mechanism. In a second phase of the analysis, we explore the adoption of benefits that are differentiated by the states identified by proxy risk factors (rather than the ageing states) and that keep a predetermined scaling factor between them, chosen according to the desired level of differentiation. Both choices introduce solidarity mechanisms, which we can highlight by comparing the resulting benefits with the ones grounded on actuarial equivalence by ageing state. Our work differs from previous contributions on this topic, such as Kabuche et al. (Reference Kabuche, Sherris, Villegas and Ziveyi2024), in two regards. First, the use of a Markov ageing model allows us to incorporate latent heterogeneity that cannot be directly measured. Second, we address explicitly possible solidarity mechanisms, identifying their magnitude. Understanding the degree of solidarity built into the system is fundamental to ensure transparency and to make any redistribution a deliberate and justifiable design choice. We develop our proposal referring to a GSA closed to the entry of new cohorts. This allows us to understand the extent to which accounting for mortality heterogeneity leads to efficient mortality risk pooling within a single cohort. We test our theoretical framework through a numerical application using a 5-state Markov ageing model and referring to Australian mortality data for both genders. Our findings support that individual longevity risk can be effectively pooled under population heterogeneity, allowing for differentiated benefits reflecting differences in participants’ life expectancies. Our results also indicate that actuarial equivalence requires a sufficiently large population size, whereas implementing solidarity mechanisms may be justified. Indeed, the estimated benefits profile appears generally stable, apart from state-specific fluctuations when the cohort shrinks to a low size. The severity of ageing significantly drives the dynamics of benefits. The last ageing state’s benefit profile is increasing on average; conversely, the intermediate ageing states’ benefit profile, as well as the first, tends to decrease as the maximum duration of the scheme is approached. Such evidence bolsters the introduction of explicit solidarity mechanisms to avoid disincentivising the participation of individuals with better physiological statuses. Then, we numerically investigate the effect of solidarity rules on rearranging benefit levels and preserving the actuarial equivalence between benefits and available resources. Depending on the number of benefit levels the scheme would provide, the benefit profile may increase more or less marked over time and in a consistent way across states, while remaining reasonably differentiated among frailer and healthier individuals.

The paper is organised as follows. In Section 2, we describe in detail the Markov ageing model. In Section 3, we present the actuarial design of the multi-state GSA, in particular addressing cross-subsidies across states and the introduction of solidarity. In Section 4, a numerical application of the proposed theoretical framework is provided, as well as a discussion of the main findings. Finally, Section 5 concludes with some final remarks.

2. The Markov ageing model

Let

$\left(A_t, \, t\geq0\right)$

be a finite-state continuous-time homogeneous Markov process describing the ageing evolution of a population, and let

$\left(A_t, \, t\geq0\right)$

be a finite-state continuous-time homogeneous Markov process describing the ageing evolution of a population, and let

$E=\left\{1,2,\ldots,m\right\}$

, with

$E=\left\{1,2,\ldots,m\right\}$

, with

$m \in \mathbb{N}_{\gt1}$

, be the set of transient states. Each of them identifies an ageing state or phase. The process takes values on the finite state-space

$m \in \mathbb{N}_{\gt1}$

, be the set of transient states. Each of them identifies an ageing state or phase. The process takes values on the finite state-space

$\mathcal{S}=E\cup\{m+1\}$

, where

$\mathcal{S}=E\cup\{m+1\}$

, where

$m+1$

represents the death (absorbing) state. The infinitesimal generator of

$m+1$

represents the death (absorbing) state. The infinitesimal generator of

$\left(A_t, \, t\geq0\right)$

is

$\left(A_t, \, t\geq0\right)$

is

\begin{equation} {} {} {} {}\boldsymbol{\Sigma} = \begin{pmatrix} {} {} {}\boldsymbol{\Lambda} \;\;\;\;\;& \boldsymbol{q} \\ {} {} {}\boldsymbol{0}\;\;\;\;\; & 0 {} {}\end{pmatrix} \in \mathbb{R}^{(m+1) \times (m+1)}, {}\end{equation}

\begin{equation} {} {} {} {}\boldsymbol{\Sigma} = \begin{pmatrix} {} {} {}\boldsymbol{\Lambda} \;\;\;\;\;& \boldsymbol{q} \\ {} {} {}\boldsymbol{0}\;\;\;\;\; & 0 {} {}\end{pmatrix} \in \mathbb{R}^{(m+1) \times (m+1)}, {}\end{equation}

where

$\boldsymbol{\Lambda}$

is the

$\boldsymbol{\Lambda}$

is the

$m\times m$

intensity matrix and

$m\times m$

intensity matrix and

$\boldsymbol{q}=-\boldsymbol{\Lambda}\boldsymbol{e}$

is a m-dimensional column vector of transition intensities to the death state, with

$\boldsymbol{q}=-\boldsymbol{\Lambda}\boldsymbol{e}$

is a m-dimensional column vector of transition intensities to the death state, with

$\boldsymbol{e}$

a column vector of ones.

$\boldsymbol{e}$

a column vector of ones.

Let

$\boldsymbol{\pi}=\left(\pi_1,\pi_2,\ldots,\pi_m\right)$

be a probability vector stating the initial distribution of the process, with

$\boldsymbol{\pi}=\left(\pi_1,\pi_2,\ldots,\pi_m\right)$

be a probability vector stating the initial distribution of the process, with

$\pi_i\;:\!=\;\mathbb{P}\left(A_0=i\right)\geq0, \, i \in E$

, and

$\pi_i\;:\!=\;\mathbb{P}\left(A_0=i\right)\geq0, \, i \in E$

, and

$\mathbb{P}\left(A_0=m+1\right)=0$

. Since the Markov process has only one absorbing state, the time until death is defined as

$\mathbb{P}\left(A_0=m+1\right)=0$

. Since the Markov process has only one absorbing state, the time until death is defined as

\begin{equation} {} {} {} {}\tau \;:\!=\; \inf\left\{t\gt0 \, : \, A_t=m+1\right\}, {}\end{equation}

\begin{equation} {} {} {} {}\tau \;:\!=\; \inf\left\{t\gt0 \, : \, A_t=m+1\right\}, {}\end{equation}

and follows a phase-type (PH) distribution with representation

$\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

, that is,

$\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

, that is,

$\tau \sim \text{PH}\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

. In particular, we deal with a generalised Coxian PH distribution so that the intensity matrix is written in the following form:

$\tau \sim \text{PH}\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

. In particular, we deal with a generalised Coxian PH distribution so that the intensity matrix is written in the following form:

\begin{equation} {} {} {} {}\renewcommand\arraystretch{1.5} {} {}\boldsymbol{\Lambda}=\begin{pmatrix} {} {} {}-\left(\lambda_1+q_1\right) & \quad \lambda_1 & \quad 0 & \quad \cdots & \quad 0 \\ {} {} {}0 & \quad -\left(\lambda_2+q_2\right) & \quad \lambda_2 & \quad \cdots & \quad 0 \\ {} {} {}0 & \quad 0 & \quad -\left(\lambda_3+q_3\right) & \quad \cdots & \quad 0 \\ {} {} {}\vdots & \quad \vdots & \quad \vdots & \quad \ddots & \quad \vdots \\ {} {} {}0 & \quad 0 & \quad 0 & \quad \cdots & \quad -q_m {} {}\end{pmatrix}, {}\end{equation}

\begin{equation} {} {} {} {}\renewcommand\arraystretch{1.5} {} {}\boldsymbol{\Lambda}=\begin{pmatrix} {} {} {}-\left(\lambda_1+q_1\right) & \quad \lambda_1 & \quad 0 & \quad \cdots & \quad 0 \\ {} {} {}0 & \quad -\left(\lambda_2+q_2\right) & \quad \lambda_2 & \quad \cdots & \quad 0 \\ {} {} {}0 & \quad 0 & \quad -\left(\lambda_3+q_3\right) & \quad \cdots & \quad 0 \\ {} {} {}\vdots & \quad \vdots & \quad \vdots & \quad \ddots & \quad \vdots \\ {} {} {}0 & \quad 0 & \quad 0 & \quad \cdots & \quad -q_m {} {}\end{pmatrix}, {}\end{equation}

being

$\lambda_i\geq0$

the transition intensity from the ageing state i to the next ageing state, while

$\lambda_i\geq0$

the transition intensity from the ageing state i to the next ageing state, while

$q_i\gt0$

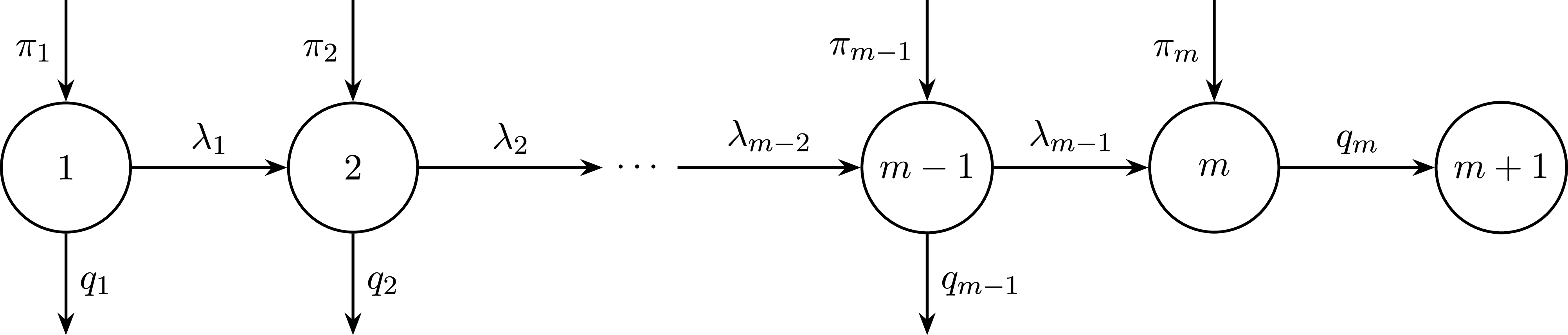

is the transition rate into the absorbing state. The generalised Coxian PH distribution is particularly attractive due to its mathematical tractability and explainability. As shown by the phase diagram in Figure 1, the ageing process is described through a sequence of ageing phases, following a lexicographical order, and the death event may occur with a certain probability in the meantime. The sojourn time in the ageing phase i is exponentially distributed with rate

$q_i\gt0$

is the transition rate into the absorbing state. The generalised Coxian PH distribution is particularly attractive due to its mathematical tractability and explainability. As shown by the phase diagram in Figure 1, the ageing process is described through a sequence of ageing phases, following a lexicographical order, and the death event may occur with a certain probability in the meantime. The sojourn time in the ageing phase i is exponentially distributed with rate

$\lambda_i+q_i$

, and, for

$\lambda_i+q_i$

, and, for

$i=1,\ldots,m-1$

, the process moves to the ageing phase

$i=1,\ldots,m-1$

, the process moves to the ageing phase

$i+1$

with probability

$i+1$

with probability

$\frac{\lambda_i}{\lambda_i+q_i}$

; otherwise, the ageing process terminates due to the death occurrence with probability

$\frac{\lambda_i}{\lambda_i+q_i}$

; otherwise, the ageing process terminates due to the death occurrence with probability

$\frac{q_i}{\lambda_i+q_i}$

. As ageing progresses, the physiological status of the population deteriorates, implying a greater probability of approaching the absorbing state. In particular, when

$\frac{q_i}{\lambda_i+q_i}$

. As ageing progresses, the physiological status of the population deteriorates, implying a greater probability of approaching the absorbing state. In particular, when

$i=m$

, the probability of jumping to the death state is 1.

$i=m$

, the probability of jumping to the death state is 1.

Generalised Coxian distribution’s phase diagram.

A key issue in adopting a PH distribution concerns the dimension of

$\boldsymbol{\Lambda}$

. The PH representation

$\boldsymbol{\Lambda}$

. The PH representation

$\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

is highly parameterised and non-uniqueness problems in parameter specifications could emerge (see, e.g., Asmussen et al. Reference Asmussen, Nerman and Olsson1996). As m increases, numerical issues may also arise in estimating parameters

$\left(\boldsymbol{\pi},\boldsymbol{\Lambda}\right)$

is highly parameterised and non-uniqueness problems in parameter specifications could emerge (see, e.g., Asmussen et al. Reference Asmussen, Nerman and Olsson1996). As m increases, numerical issues may also arise in estimating parameters

$\lambda_i$

and

$\lambda_i$

and

$q_i$

. Focusing on modelling the human mortality schedule, the PH distribution could require a high dimension of the intensity matrix. For instance, Lin and Liu (Reference Lin and Liu2007) adopt the Coxian distribution to fit the mortality schedule from age 0 to age 100, suggesting that 200–250 ageing phases are needed. Cheng et al. (Reference Cheng, Jones, Liu and Ren2020) impose specific structures on

$q_i$

. Focusing on modelling the human mortality schedule, the PH distribution could require a high dimension of the intensity matrix. For instance, Lin and Liu (Reference Lin and Liu2007) adopt the Coxian distribution to fit the mortality schedule from age 0 to age 100, suggesting that 200–250 ageing phases are needed. Cheng et al. (Reference Cheng, Jones, Liu and Ren2020) impose specific structures on

$\lambda_i$

and

$\lambda_i$

and

$q_i$

, finding that 100 phases are pretty reasonable in fitting mortality data. Conversely, Liu and Lin (Reference Liu and Lin2012) argue that if only part of the mortality schedule is relevant, for example, from age 65 onwards, a lower-dimensional PH distribution is enough to achieve an accurate fit. Such an approach could be suitable for our purposes, since we deal with ages falling within the post-retirement life of individuals. Further details concerning the Markov ageing model fitting will be provided in Section 4.

$q_i$

, finding that 100 phases are pretty reasonable in fitting mortality data. Conversely, Liu and Lin (Reference Liu and Lin2012) argue that if only part of the mortality schedule is relevant, for example, from age 65 onwards, a lower-dimensional PH distribution is enough to achieve an accurate fit. Such an approach could be suitable for our purposes, since we deal with ages falling within the post-retirement life of individuals. Further details concerning the Markov ageing model fitting will be provided in Section 4.

Denoting with

$p^{i,j}_t = \mathbb{P}\left(A_t=j | A_0=i\right)$

the time-homogeneous transition probability from the ageing state i to the ageing state j, the transition probability matrix, namely

$p^{i,j}_t = \mathbb{P}\left(A_t=j | A_0=i\right)$

the time-homogeneous transition probability from the ageing state i to the ageing state j, the transition probability matrix, namely

$\boldsymbol{P}(t)=\left(p^{i,j}_t\right)_{i,\, j \in E}$

, satisfies the following Kolmogorov forward equation:

$\boldsymbol{P}(t)=\left(p^{i,j}_t\right)_{i,\, j \in E}$

, satisfies the following Kolmogorov forward equation:

\begin{equation} {} {} {} {}\displaystyle\frac{d}{dt} \boldsymbol{P}(t) =\boldsymbol{P}(t)\boldsymbol{\Lambda}, {}\end{equation}

\begin{equation} {} {} {} {}\displaystyle\frac{d}{dt} \boldsymbol{P}(t) =\boldsymbol{P}(t)\boldsymbol{\Lambda}, {}\end{equation}

with the initial condition

$\boldsymbol{P}(0)=\boldsymbol{I}$

, where

$\boldsymbol{P}(0)=\boldsymbol{I}$

, where

$\boldsymbol{I}$

is the identity matrix. Equation (2.4) admits a unique solution given by

$\boldsymbol{I}$

is the identity matrix. Equation (2.4) admits a unique solution given by

\begin{equation} {} {}\boldsymbol{P}(t)=\exp(\boldsymbol{\Lambda} t), {}\end{equation}

\begin{equation} {} {}\boldsymbol{P}(t)=\exp(\boldsymbol{\Lambda} t), {}\end{equation}

where the exponential matrix is defined by series expansion, that is,

$\exp\left(\boldsymbol{\Lambda}t\right)=\sum_{h=0}^{\infty}\frac{\left(t\boldsymbol{\Lambda}\right)^h}{h!}$

.

$\exp\left(\boldsymbol{\Lambda}t\right)=\sum_{h=0}^{\infty}\frac{\left(t\boldsymbol{\Lambda}\right)^h}{h!}$

.

Under the PH distributions, many quantities of interest concerning the future lifetime are available in closed form. For instance, the survival function for a newborn can be written as:

\begin{equation} {} {} {} {}S_0(t) = \boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}t\right)\boldsymbol{e}, \quad t\gt0. {}\end{equation}

\begin{equation} {} {} {} {}S_0(t) = \boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}t\right)\boldsymbol{e}, \quad t\gt0. {}\end{equation}

Moreover, the conditional survival function given the survival at age

$x\gt0$

is

$x\gt0$

is

\begin{equation} {} {} {} {}S_x(t) = \frac{S_0(x+t)}{S_0(x)} = \frac{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}(x+t)\right)\boldsymbol{e}}{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)\boldsymbol{e}} = \boldsymbol{\pi}^\top_x\exp\left(\boldsymbol{\Lambda}t\right)\boldsymbol{e}, \quad t\gt0, {}\end{equation}

\begin{equation} {} {} {} {}S_x(t) = \frac{S_0(x+t)}{S_0(x)} = \frac{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}(x+t)\right)\boldsymbol{e}}{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)\boldsymbol{e}} = \boldsymbol{\pi}^\top_x\exp\left(\boldsymbol{\Lambda}t\right)\boldsymbol{e}, \quad t\gt0, {}\end{equation}

where

$\boldsymbol{\pi}_x^\top = \frac{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)}{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)\boldsymbol{e}}$

represents the distribution of the ageing phases, given the survival at age x.

$\boldsymbol{\pi}_x^\top = \frac{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)}{\boldsymbol{\pi}^\top\exp\left(\boldsymbol{\Lambda}x\right)\boldsymbol{e}}$

represents the distribution of the ageing phases, given the survival at age x.

Remark 2.1. In the Markov ageing model, once the process leaves an ageing state, it is impossible to return to it. In other words, the Markov ageing model keeps track of the ageing progression in the forward sense, and possible rejuvenations are not considered. Rejuvenation may be biologically possible only following various lifestyle interventions concerning nutrition, physical exercise and the social environment (see, e.g., Félix et al. Reference Félix, Martnez de Toda and Daz-Del Cerro2024). Detailed information at the individual level is crucial to assessing the significance of possible rejuvenation transitions. As explained in Section 1, such data granularity is often unavailable to annuity providers, and rejuvenation transitions cannot be estimated.

To assist the reader, notation adopted in the current section is resumed in Table 1.

Notation, and related meaning, adopted for describing the Markov ageing model.

3. The Markov ageing GSA arrangement

3.1 Pool structure

We consider a GSA scheme that provides post-retirement benefits to its members. Individuals pay an initial capital when joining the scheme; upon death, any residual amount is retained by the pool (i.e., no death benefit is included). In return for their initial contribution, members receive an annual lifetime income, whose amount is differentiated depending on the specific mortality profile of the individual. In fact, the GSA is structured with multiple levels of benefits, with higher benefit amounts provided to those with a shorter life expectancy. The individual’s mortality profile is first assessed at entry and then reviewed annually. Upon a change of the mortality profile, for example, following the onset of a disease, the individual will be assigned the level of benefit consistent with his(her) new status. However, similarly to a traditional GSA, annual amounts for the various benefit levels are not guaranteed but are subject to annual adjustment based on the investment and longevity experience of the pool. In the following, we focus on longevity only, and we propose an approach to define such adjustments, which is motivated by actuarial arguments.

Mortality is modelled adopting the Markov ageing setting described in Section 2. We first assume that it is possible to classify individuals according to the ageing states and to differentiate benefits based on such states. However, as already pointed out in Section 1, biological age (which is at the root of ageing states) is not directly measurable. In the second step of the discussion (in particular, in Section 3.5), we assume that individuals are classified according to proxy risk factors. It is unlikely that risk classes identified this way correspond exactly to the ageing states of the Markov model. The implications are discussed in Section 3.5; for the moment, we assume that both at entry and at any time, a risk classification based on the ageing states of the Markov model can be performed. In particular, we assume that it is possible to describe the dynamics of each individual’s mortality profile in terms of the transition to higher ageing states.

We consider a single cohort consisting of

$L_x$

individuals who join the scheme at time

$L_x$

individuals who join the scheme at time

$t=0$

, at chronological age x, with

$t=0$

, at chronological age x, with

$L_x^i$

individuals placed in state i,

$L_x^i$

individuals placed in state i,

$i\in E$

(clearly,

$i\in E$

(clearly,

$\sum_{i=1}^m L_x^i=L_x$

). The maximum attainable age is

$\sum_{i=1}^m L_x^i=L_x$

). The maximum attainable age is

$\omega$

for each individual; however, we assume that, to avoid the impact of major random fluctuations at later ages (when the cohort will shrink to low size), the scheme is committed to pay benefits up to time

$\omega$

for each individual; however, we assume that, to avoid the impact of major random fluctuations at later ages (when the cohort will shrink to low size), the scheme is committed to pay benefits up to time

$t_{\max}$

(i.e., up to chronological age

$t_{\max}$

(i.e., up to chronological age

$x_{\max}=x+t_{\max}\lt\omega$

). At time

$x_{\max}=x+t_{\max}\lt\omega$

). At time

$t_{\max}$

, the available funds will be transferred to an insurer willing to take charge of the surviving participants and their funds and guarantee them a lifetime annuity. The price and optimal time of such a transfer (which undoubtedly constitute interesting research questions) are not addressed in this paper, as our aim for now is to define acceptable benefit adjustment rules when multiple levels of benefits are involved; addressing also the transfer at time

$t_{\max}$

, the available funds will be transferred to an insurer willing to take charge of the surviving participants and their funds and guarantee them a lifetime annuity. The price and optimal time of such a transfer (which undoubtedly constitute interesting research questions) are not addressed in this paper, as our aim for now is to define acceptable benefit adjustment rules when multiple levels of benefits are involved; addressing also the transfer at time

$t_{\max}$

would excessively broaden the scope of the present study. Thus, in this paper, we simply assume that the scheme will pay an income to survivors at times

$t_{\max}$

would excessively broaden the scope of the present study. Thus, in this paper, we simply assume that the scheme will pay an income to survivors at times

$t=0,1,\ldots,t_{\max}$

, for a chosen (reasonable)

$t=0,1,\ldots,t_{\max}$

, for a chosen (reasonable)

$t_{\max}$

, and the scheme’s payout rate will not account for annuity costs concerning times

$t_{\max}$

, and the scheme’s payout rate will not account for annuity costs concerning times

$t\gt t_{\max}$

.

$t\gt t_{\max}$

.

Let

$B_0^{i}$

be the benefit set at time

$B_0^{i}$

be the benefit set at time

$t=0$

for state

$t=0$

for state

$i \in E$

. An individual entering the scheme in state i will initially get the benefit

$i \in E$

. An individual entering the scheme in state i will initially get the benefit

$B_0^i$

; however, upon transition to a state

$B_0^i$

; however, upon transition to a state

$j\gt i$

,

$j\gt i$

,

$j\in E$

, (s)he is entitled to cash the benefit

$j\in E$

, (s)he is entitled to cash the benefit

$B_0^{j}$

. Based on the usual actuarial arguments, the initial capital to be paid by an individual in state i at time

$B_0^{j}$

. Based on the usual actuarial arguments, the initial capital to be paid by an individual in state i at time

$t=0$

is then assessed as follows:

$t=0$

is then assessed as follows:

\begin{equation} {} {}V_0^{i} = \sum_{j\geq i}^{m} B_0^{j}\, \ddot{a}^{i,j}_{x}, {}\end{equation}

\begin{equation} {} {}V_0^{i} = \sum_{j\geq i}^{m} B_0^{j}\, \ddot{a}^{i,j}_{x}, {}\end{equation}

where

$\ddot{a}^{i,j}_{x} = \sum_{h=0}^{t_{\max}}(1+r)^{-h} {_hp_x^{i,j}}$

is the actuarial value of the annuity paid when in state j, computed using the transition probabilities

$\ddot{a}^{i,j}_{x} = \sum_{h=0}^{t_{\max}}(1+r)^{-h} {_hp_x^{i,j}}$

is the actuarial value of the annuity paid when in state j, computed using the transition probabilities

$_hp_x^{i,j}=\exp(\boldsymbol{\Lambda}h)_{i,j}$

predicted by the mortality model and a given (deterministic) discount rate r. We point out that no loading is embedded in the choice of parameters of (3.1), as it is natural for a GSA scheme. We note also that the differentiation by state concerns not only the benefits but, consistently, the initial capital too.

$_hp_x^{i,j}=\exp(\boldsymbol{\Lambda}h)_{i,j}$

predicted by the mortality model and a given (deterministic) discount rate r. We point out that no loading is embedded in the choice of parameters of (3.1), as it is natural for a GSA scheme. We note also that the differentiation by state concerns not only the benefits but, consistently, the initial capital too.

3.2 Pool funds

A GSA is grounded on the principle of funded liabilities. In other words, it is required that a balance be maintained at all times between available resources and the value of obligations. This is achieved by updating the benefit amount, upwards or downwards, depending on the experience with longevity and investments. We assume that the adjustment is applied annually, right before the benefit is paid at time t,

$t\geq 1$

. Let

$t\geq 1$

. Let

$B_0^i$

be the benefit set at time

$B_0^i$

be the benefit set at time

$t=0$

for state

$t=0$

for state

$i\in E$

; reasonably,

$i\in E$

; reasonably,

$B_0^1\lt B_0^2\lt\ldots\lt B_0^m$

, since higher-indexed states correspond to lower life expectancy. Taking

$B_0^1\lt B_0^2\lt\ldots\lt B_0^m$

, since higher-indexed states correspond to lower life expectancy. Taking

$B_0^1$

as the baseline benefit amount, it may be convenient to express the initial benefit amount for each state

$B_0^1$

as the baseline benefit amount, it may be convenient to express the initial benefit amount for each state

$i, i\gt1$

, as a proportion of

$i, i\gt1$

, as a proportion of

$B_0^1$

, as follows:

$B_0^1$

, as follows:

$B_0^i=c^i B_0^1$

, where the

$B_0^i=c^i B_0^1$

, where the

$c^i$

’s (

$c^i$

’s (

$1\lt c^2\lt c^3\lt\ldots\lt c^m$

) are chosen according to some target. We let

$1\lt c^2\lt c^3\lt\ldots\lt c^m$

) are chosen according to some target. We let

$B_t^{i}$

denote the updated benefit amount at time t for state i, according to an adjustment rule which is described in Section 3.4. In the following, we understand

$B_t^{i}$

denote the updated benefit amount at time t for state i, according to an adjustment rule which is described in Section 3.4. In the following, we understand

$i\in E$

and

$i\in E$

and

$t=0,1,\ldots, t_{\max}$

, unless otherwise stated (the adjustment of the benefit at time

$t=0,1,\ldots, t_{\max}$

, unless otherwise stated (the adjustment of the benefit at time

$t=0$

is, of course, not under consideration;

$t=0$

is, of course, not under consideration;

$B_0^i$

is simply the starting chosen amount).

$B_0^i$

is simply the starting chosen amount).

Following the adjustment of the benefit, the value of the obligation to an individual in state i at time t can be assessed as follows:

\begin{equation} {} {}V_{t}^i= \sum_{\substack{j\geq i}}^m B_{t}^j\, \ddot{a}_{x+t}^{i,j}, {}\end{equation}

\begin{equation} {} {}V_{t}^i= \sum_{\substack{j\geq i}}^m B_{t}^j\, \ddot{a}_{x+t}^{i,j}, {}\end{equation}

with an obvious meaning of

$\ddot{a}_{x+t}^{i,j}$

for

$\ddot{a}_{x+t}^{i,j}$

for

$t\gt0$

. The total value of the obligations of the pool at time t is then

$t\gt0$

. The total value of the obligations of the pool at time t is then

\begin{equation} {} {}F_t^{R} =\sum_{i=1}^m L_{x+t}^{i}V_t^{i}, {}\end{equation}

\begin{equation} {} {}F_t^{R} =\sum_{i=1}^m L_{x+t}^{i}V_t^{i}, {}\end{equation}

where

$L_{x+t}^{i}$

is the (observed) number of individuals in state i at time t. We refer to

$L_{x+t}^{i}$

is the (observed) number of individuals in state i at time t. We refer to

$F_t^{R}$

as the required pool fund at time t (in line with this, we will refer to

$F_t^{R}$

as the required pool fund at time t (in line with this, we will refer to

$V_t^i$

as the individual fund required in state i at time t).

$V_t^i$

as the individual fund required in state i at time t).

The resources available to a GSA, which we call the available pool fund and denote as

$F_t^{A}$

at time t, are the money contributed by members, net of the payments made so far, plus interest. We focus on longevity risk only and assume a deterministic financial setting; we take r as the annual deterministic return on investments. Starting from

$F_t^{A}$

at time t, are the money contributed by members, net of the payments made so far, plus interest. We focus on longevity risk only and assume a deterministic financial setting; we take r as the annual deterministic return on investments. Starting from

$F_0^{A}=\sum_{i=1}^m L_x^{i} V_0^{i}$

, the dynamics of the available pool fund can be described recursively for

$F_0^{A}=\sum_{i=1}^m L_x^{i} V_0^{i}$

, the dynamics of the available pool fund can be described recursively for

$t\gt0$

as follows:

$t\gt0$

as follows:

\begin{equation} {} {}F_t^{A} = \left(F_{t-1}^{A}-\sum_{i=1}^m L_{x+t-1}^{i} B_{t-1}^{i}\right) (1+r). {}\end{equation}

\begin{equation} {} {}F_t^{A} = \left(F_{t-1}^{A}-\sum_{i=1}^m L_{x+t-1}^{i} B_{t-1}^{i}\right) (1+r). {}\end{equation}

The basic requirement for running the GSA can now be written as:

\begin{equation} {} {} {} {}F_t^{R} = F_t^{A}, \quad t\geq0. {}\end{equation}

\begin{equation} {} {} {} {}F_t^{R} = F_t^{A}, \quad t\geq0. {}\end{equation}

If benefits are undifferentiated (i.e., the same benefit amount is provided in all states), Equation (3.5) univocally defines the amount admitted for the benefit at time t (since, in such a case, there is only one unknown). When benefits are differentiated by state, Equation (3.5) admits an infinite number of solutions, as the number of unknowns is now m. The introduction of additional requirements is necessary to identify workable solutions. We point out that the benefit adjustment not necessarily will preserve the initial ratio between benefits, that is, not necessarily we find

$B_t^i=c^i B_t^1$

. If preserving such a ratio is a priority, then we need to impose

$B_t^i=c^i B_t^1$

. If preserving such a ratio is a priority, then we need to impose

$B_t^i=c^i B_t^1$

at all times t; in this case, Equation (3.5) has only one unknown, namely

$B_t^i=c^i B_t^1$

at all times t; in this case, Equation (3.5) has only one unknown, namely

$B_t^1$

. It would follow that, at any time

$B_t^1$

. It would follow that, at any time

$t\gt0$

, benefits would be differentiated by state, but they would all be adjusted in the same proportion.

$t\gt0$

, benefits would be differentiated by state, but they would all be adjusted in the same proportion.

At this point, it is convenient to examine the causes that may result in a mismatch between available and required pool funds. Disregarding financial risks, we may consider the following circumstances: mortality rates in the various states higher or lower than expected; ageing process (i.e., transition rates) higher or lower than expected. It should be taken into account that deviations between expected and observed rates may differ across states. Instead of adopting a common adjustment proportion, we may find it more appropriate to differentiate by state not only the benefits but also the adjustment coefficients. In the following, we investigate this solution. To this end, we split the available and required pool funds by state.

3.3 Splitting the pool funds by state

It is rather natural to identify

\begin{equation} {} {}F_t^{i,R}=L_{x+t}^{i}\,V_t^{i} {}\end{equation}

\begin{equation} {} {}F_t^{i,R}=L_{x+t}^{i}\,V_t^{i} {}\end{equation}

as the pool fund required at time t for state i. Clearly,

$\sum_{i=1}^m F_t^{i,R}=F_t^R$

.

$\sum_{i=1}^m F_t^{i,R}=F_t^R$

.

Let

$F_t^{i,A}$

denote the pool fund made available to state i at time t, such that

$F_t^{i,A}$

denote the pool fund made available to state i at time t, such that

$\sum_{i=1}^m F_t^{i,A}=F_t^A$

.

$\sum_{i=1}^m F_t^{i,A}=F_t^A$

.

We now require that the principle of funded liabilities is applied by state, that is, we impose

\begin{equation} {} {} {} {}F_t^{i,R} = F_t^{i,A}, \quad t \geq 0,\quad i\in E. {}\end{equation}

\begin{equation} {} {} {} {}F_t^{i,R} = F_t^{i,A}, \quad t \geq 0,\quad i\in E. {}\end{equation}

Such a requirement clearly also satisfies (3.5). To proceed further with (3.7), it is useful to note that the amount of resources available per state is affected by cross-subsidy effects between states. Part of these cross-subsidies are embedded in the individual fund required (and available) in state i at time

$t-1$

. To check this, we start by considering that

$t-1$

. To check this, we start by considering that

\begin{equation*}\ddot{a}_{x+t-1}^{i,i}=1+(1+r)^{-1}\, p_{x+t-1}^{i,i}\,\ddot{a}_{x+t}^{i,i}, {}\end{equation*}

\begin{equation*}\ddot{a}_{x+t-1}^{i,i}=1+(1+r)^{-1}\, p_{x+t-1}^{i,i}\,\ddot{a}_{x+t}^{i,i}, {}\end{equation*}

and

\begin{equation*} {} {}\ddot{a}_{x+t-1}^{i,j}=(1+r)^{-1} \sum_{i\leq k\leq j}\,p_{x+t-1}^{i,k}\, \ddot{a}_{x+t}^{k,j}, \quad j\gt i. {}\end{equation*}

\begin{equation*} {} {}\ddot{a}_{x+t-1}^{i,j}=(1+r)^{-1} \sum_{i\leq k\leq j}\,p_{x+t-1}^{i,k}\, \ddot{a}_{x+t}^{k,j}, \quad j\gt i. {}\end{equation*}

Then, we can write the following recursion for the individual fund in state i:

\begin{equation} {} {}V_{t-1}^i=B_{t-1}^i+\sum_{j\geq i}p_{x+t-1}^{i,j}\, V_{t^-}^j\, (1+r)^{-1}, {}\end{equation}

\begin{equation} {} {}V_{t-1}^i=B_{t-1}^i+\sum_{j\geq i}p_{x+t-1}^{i,j}\, V_{t^-}^j\, (1+r)^{-1}, {}\end{equation}

where

\begin{equation*} {} {}V_{t^-}^j= \sum_{\substack{k\geq j}}^m B_{t-1}^k\, \ddot{a}_{x+t}^{j,k} {}\end{equation*}

\begin{equation*} {} {}V_{t^-}^j= \sum_{\substack{k\geq j}}^m B_{t-1}^k\, \ddot{a}_{x+t}^{j,k} {}\end{equation*}

represents the amount of individual fund required in state j at time t, before the adjustment of the benefits at that time.

Let

\begin{equation} {} {}F_{t^-}^{i,A} = \left(F_{t-1}^{i,A}-L_{x+t-1}^i B_{t-1}^i\right)(1+r) {}\end{equation}

\begin{equation} {} {}F_{t^-}^{i,A} = \left(F_{t-1}^{i,A}-L_{x+t-1}^i B_{t-1}^i\right)(1+r) {}\end{equation}

denote the pool fund dragged to state i at time t,

$t\gt0$

, by the pool fund available in such a state at time

$t\gt0$

, by the pool fund available in such a state at time

$t-1$

, net of the benefits paid at time

$t-1$

, net of the benefits paid at time

$t-1$

and credited with interest. Comparing Equation (3.9) with (3.4) it can be easily seen that

$t-1$

and credited with interest. Comparing Equation (3.9) with (3.4) it can be easily seen that

$\sum_{i=1}^m F_{t^-}^{i,A}=F_t^A$

.

$\sum_{i=1}^m F_{t^-}^{i,A}=F_t^A$

.

Since because of (3.7) we have

$F_{t-1}^{i,A}=F_{t-1}^{i,R}$

, using (3.8) we can rearrange (3.9) as:

$F_{t-1}^{i,A}=F_{t-1}^{i,R}$

, using (3.8) we can rearrange (3.9) as:

\begin{eqnarray} {} {}F_{t^-}^{i,A} {} {}& = & L_{x+t-1}^{i}\, p_{x+t-1}^{i,i}\,V_{t^-}^i+ L_{x+t-1}^{i}\sum_{j\gt i}p_{x+t-1}^{i,j}\,V_{t^-}^j , {}\end{eqnarray}

\begin{eqnarray} {} {}F_{t^-}^{i,A} {} {}& = & L_{x+t-1}^{i}\, p_{x+t-1}^{i,i}\,V_{t^-}^i+ L_{x+t-1}^{i}\sum_{j\gt i}p_{x+t-1}^{i,j}\,V_{t^-}^j , {}\end{eqnarray}

that we can interpret as follows. Given

$L_{x+t-1}^{i} $

, the quantity

$L_{x+t-1}^{i} $

, the quantity

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,i}$

represents the number of individuals expected to stay in state i during the year, while

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,i}$

represents the number of individuals expected to stay in state i during the year, while

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,j}$

represents the number of individuals expected to be in state j at the end of the year. Equation (3.10) then shows that

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,j}$

represents the number of individuals expected to be in state j at the end of the year. Equation (3.10) then shows that

$F_{t^-}^{i, A}$

, that is,

$F_{t^-}^{i, A}$

, that is,

$F_{t-1}^{i, A}$

net of the benefits paid at the beginning of the year in state i and credited with interest, consists of the resources required for those expected to remain alive, either in state i or in a higher state

$F_{t-1}^{i, A}$

net of the benefits paid at the beginning of the year in state i and credited with interest, consists of the resources required for those expected to remain alive, either in state i or in a higher state

$j, j\gt i$

(we point out that for

$j, j\gt i$

(we point out that for

$j=m+1$

, that is, for the dead state,

$j=m+1$

, that is, for the dead state,

$V_{t^-}^j=0$

).

$V_{t^-}^j=0$

).

Since

$p_{x+t-1}^{i,i}=1-\sum_{j\gt i}^{m+1} p_{x+t-1}^{i,j}$

, Equation (3.10) can be further rearranged as follows:

$p_{x+t-1}^{i,i}=1-\sum_{j\gt i}^{m+1} p_{x+t-1}^{i,j}$

, Equation (3.10) can be further rearranged as follows:

\begin{equation} {} {}F_{t^-}^{i, A}=L_{x+t-1}^{i}\,\left(1-p_{x+t-1}^{i,m+1}\right)\,V_{t^-}^i+ L_{x+t-1}^{i}\sum_{j\gt i}^m \,p_{x+t-1}^{i,j}\,\left(V_{t^-}^j-V_{t^-}^i\right). {}\end{equation}

\begin{equation} {} {}F_{t^-}^{i, A}=L_{x+t-1}^{i}\,\left(1-p_{x+t-1}^{i,m+1}\right)\,V_{t^-}^i+ L_{x+t-1}^{i}\sum_{j\gt i}^m \,p_{x+t-1}^{i,j}\,\left(V_{t^-}^j-V_{t^-}^i\right). {}\end{equation}

Equation (3.11) allows us to give a further useful interpretation to

$F_{t^-}^{i,A}$

. Since

$F_{t^-}^{i,A}$

. Since

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,m+1}$

is the expected number of deaths reported by those in state i at time

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,m+1}$

is the expected number of deaths reported by those in state i at time

$t-1$

, the amount

$t-1$

, the amount

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,m+1}\, V_{t^-}^i$

can be related to the expected mortality credits in such a state. Conversely,

$L_{x+t-1}^{i}\, p_{x+t-1}^{i,m+1}\, V_{t^-}^i$

can be related to the expected mortality credits in such a state. Conversely,

$L_{x+t-1}^{i}\sum_{j\gt i}^m\, p_{x+t-1}^{i,j}$

is the number of individuals expected to move from state i to a living state

$L_{x+t-1}^{i}\sum_{j\gt i}^m\, p_{x+t-1}^{i,j}$

is the number of individuals expected to move from state i to a living state

$j, j\gt i,$

and

$j, j\gt i,$

and

$L_{x+t-1}^{i}\sum_{j\gt i} \,p_{x+t-1}^{i,j}\,\left(V_{t^-}^i-V_{t^-}^j\right)$

is a measure of the (total) net cross-subsidy ‘cost’ charged to state i for those expected to be alive, but in higher ageing states.

$L_{x+t-1}^{i}\sum_{j\gt i} \,p_{x+t-1}^{i,j}\,\left(V_{t^-}^i-V_{t^-}^j\right)$

is a measure of the (total) net cross-subsidy ‘cost’ charged to state i for those expected to be alive, but in higher ageing states.

The annual dynamics of the population of state i can be described for

$t\gt0$

as follows:

$t\gt0$

as follows:

\begin{equation} {} {} {} {}L_{x+t}^{i} = L_{x+t-1}^{i} + \sum_{j\lt i} L_{x+t-1}^{j,i} - \sum_{j\gt i}^{m+1} L_{x+t-1}^{i,j}, {}\end{equation}

\begin{equation} {} {} {} {}L_{x+t}^{i} = L_{x+t-1}^{i} + \sum_{j\lt i} L_{x+t-1}^{j,i} - \sum_{j\gt i}^{m+1} L_{x+t-1}^{i,j}, {}\end{equation}

where we use the notation

$L_{x+t-1}^{j,i}$

(or

$L_{x+t-1}^{j,i}$

(or

$L_{x+t-1}^{i,j}$

) to denote the observed number of individuals in state i (j) at time t being in state j (i) at time

$L_{x+t-1}^{i,j}$

) to denote the observed number of individuals in state i (j) at time t being in state j (i) at time

$t-1$

. Equation (3.12) makes it clear that the number of individuals in state i at time t is the result of those who left state i (moving to a living state

$t-1$

. Equation (3.12) makes it clear that the number of individuals in state i at time t is the result of those who left state i (moving to a living state

$j, \, i\lt j\leq m$

, or due to death,

$j, \, i\lt j\leq m$

, or due to death,

$j=m+1$

) and those who have entered it from a state

$j=m+1$

) and those who have entered it from a state

$j\lt i$

. Clearly,

$j\lt i$

. Clearly,

$L_{x+t-1}^{j,i}=0$

for

$L_{x+t-1}^{j,i}=0$

for

$i=1$

. Note that situations such as

$i=1$

. Note that situations such as

$L_{x+t-1}^i=0$

and

$L_{x+t-1}^i=0$

and

$L_{x+t}^i\gt0$

or

$L_{x+t}^i\gt0$

or

$L_{x+t-1}^i\gt0$

and

$L_{x+t-1}^i\gt0$

and

$L_{x+t}^i=0$

are possible, as a result of transitions into and out of state i. In the following, we use the notation

$L_{x+t}^i=0$

are possible, as a result of transitions into and out of state i. In the following, we use the notation

$\widetilde{p}$

to denote the realised (observed) transition or permanence rates; for instance,

$\widetilde{p}$

to denote the realised (observed) transition or permanence rates; for instance,

$\widetilde{p}_{x+t-1}^{\ i,j}=\frac{L_{x+t-1}^{i,j}}{L_{x+t-1}^{i}}$

. Such rates are obviously defined for states that are non-empty at time

$\widetilde{p}_{x+t-1}^{\ i,j}=\frac{L_{x+t-1}^{i,j}}{L_{x+t-1}^{i}}$

. Such rates are obviously defined for states that are non-empty at time

$t-1$

, that is, for states i such that

$t-1$

, that is, for states i such that

$L_{x+t-1}^{i}\gt0$

. Using this notation, Equation (3.12) can be rewritten as:

$L_{x+t-1}^{i}\gt0$

. Using this notation, Equation (3.12) can be rewritten as:

\begin{equation} {} {}L_{x+t}^{i}= L_{x+t-1}^i \left(1-\widetilde{p}_{x+t-1}^{\ i,m+1}\right) +\sum_{j\lt i}L_{x+t-1}^{j}\, {}\widetilde{p}_{x+t-1}^{\ j,i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j} . {}\end{equation}

\begin{equation} {} {}L_{x+t}^{i}= L_{x+t-1}^i \left(1-\widetilde{p}_{x+t-1}^{\ i,m+1}\right) +\sum_{j\lt i}L_{x+t-1}^{j}\, {}\widetilde{p}_{x+t-1}^{\ j,i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j} . {}\end{equation}

Let us now compare

$F_{t^-}^{i,A}$

to the pool fund required at time t for state i. As stated by (3.6), such a fund is proportional to

$F_{t^-}^{i,A}$

to the pool fund required at time t for state i. As stated by (3.6), such a fund is proportional to

$L_{x+t}^{i} $

. Its amount before the adjustment of the benefits is represented by:

$L_{x+t}^{i} $

. Its amount before the adjustment of the benefits is represented by:

\begin{equation} {} {}F_{t^-}^{i, R}=L_{x+t}^i\, V_{t^{-}}^i. {}\end{equation}

\begin{equation} {} {}F_{t^-}^{i, R}=L_{x+t}^i\, V_{t^{-}}^i. {}\end{equation}

If we plug (3.13) into (3.14), we obtain the expression:

\begin{equation} {} {}F_{t^-}^{i, R}= L_{x+t-1}^i \left(1-\widetilde{p}_{x+t-1}^{\ i,m+1}\right)\, V_{t^{-}}^i+\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{i}, {}\end{equation}

\begin{equation} {} {}F_{t^-}^{i, R}= L_{x+t-1}^i \left(1-\widetilde{p}_{x+t-1}^{\ i,m+1}\right)\, V_{t^{-}}^i+\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{i}, {}\end{equation}

that we can compare with (3.11) for an interpretation. It is unlikely that

$F_{t^-}^{i,A}=F_{t^-}^{i,R}$

, for a number of reasons:

$F_{t^-}^{i,A}=F_{t^-}^{i,R}$

, for a number of reasons:

-

• The realised number of deaths,

$L_{x+t-1}^i\, \widetilde{p}_{x+t-1}^{\ i,m+1}$

, can be other than what expected,

$L_{x+t-1}^{i} \,p_{x+t-1}^{i,m+1}$

, and then the realised mortality credits in state i can be higher or lower than expected. We may consider it appropriate for any discrepancy to be absorbed by state i, given that this mismatch arises exclusively from mortality in state i.

$L_{x+t-1}^i\, \widetilde{p}_{x+t-1}^{\ i,m+1}$

, can be other than what expected,

$L_{x+t-1}^{i} \,p_{x+t-1}^{i,m+1}$

, and then the realised mortality credits in state i can be higher or lower than expected. We may consider it appropriate for any discrepancy to be absorbed by state i, given that this mismatch arises exclusively from mortality in state i. -

• In face of individuals entering state i during the year, it is required to hold in this state an additional amount

$\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}$

, which is not already included in

$F_{t^-}^{i,A}$

. This is an amount that should be cross-subsidised by the previous states

$j,j\lt i$

. -

• Individual funds

$V_{t^-}^j$

for those moving to a living state

$j,j\gt i$

are no longer required in state i and should be taken out from

$F_{t^-}^{i,A}$

, to cross-subsidise the next states. This is in line with what was discussed with regard to those entering state i (previous point). -

• Finally, we note that when

$L_{x+t}^i=0$

, then

$F_{t^-}^{i,R}=0$

; it can happen, instead, that

$F_{t^-}^{i,A}\gt0$

, given that this latter fund is assessed based on expected number of transitions, in contrast to

$F_{t^-}^{i,R}$

which considers realised transitions. In such a circumstance,

$F_{t^-}^{i,A}$

should be released to non-empty states.

Based on the above considerations, we define the pool fund available for state i at time t as follows:

\begin{equation} {} {}F_{t}^{i, A}= \begin{cases} {} {} {}F_{t^-}^{i, A} +\displaystyle\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{j} +X_t^i & \text{if }L_{x+t}^i\gt0;\\ {} {} {}0 & \text{if }L_{x+t}^i=0. {} {}\end{cases} {}\end{equation}

\begin{equation} {} {}F_{t}^{i, A}= \begin{cases} {} {} {}F_{t^-}^{i, A} +\displaystyle\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}-\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{j} +X_t^i & \text{if }L_{x+t}^i\gt0;\\ {} {} {}0 & \text{if }L_{x+t}^i=0. {} {}\end{cases} {}\end{equation}

With

$X_t^i$

we denote the amount of resources left at time t by empty states, released to state i, so to ensure that

$X_t^i$

we denote the amount of resources left at time t by empty states, released to state i, so to ensure that

$\sum_{i}F_t^{i, A}=F_t^A$

. We assume a redistribution proportional to the required funds before the adjustment of the benefits; more precisely, we assume (for non-empty states i):

$\sum_{i}F_t^{i, A}=F_t^A$

. We assume a redistribution proportional to the required funds before the adjustment of the benefits; more precisely, we assume (for non-empty states i):

\begin{equation*} {} {}X_t^i=\left(F_t^A-\sum_{i:\,L^i_{x+t}\,\gt0} F_{t^-}^{i,A}\right)\,\frac{F_{t^-}^{i,R}}{F_{t^-}^R}. {}\end{equation*}

\begin{equation*} {} {}X_t^i=\left(F_t^A-\sum_{i:\,L^i_{x+t}\,\gt0} F_{t^-}^{i,A}\right)\,\frac{F_{t^-}^{i,R}}{F_{t^-}^R}. {}\end{equation*}

As already noted, definition (3.16) ensures

$\sum_{i}F_t^{i,A}=F_t^A$

. The amounts

$\sum_{i}F_t^{i,A}=F_t^A$

. The amounts

$\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}$

and

$\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,V_{t^{-}}^{i}$

and

$\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{j}$

measure the cross-subsidy, respectively, in favour of and released by state i. These amounts are also present in

$\sum_{j\gt i}^{m}L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,j}\, V_{t^{-}}^{j}$

measure the cross-subsidy, respectively, in favour of and released by state i. These amounts are also present in

$F_t^A$

because, when we deal with multiple states, necessarily cross-subsidy effects between states are involved; however, such cross-subsidies are not explicit in (3.4) because they sum up to zero at the pool level.

$F_t^A$

because, when we deal with multiple states, necessarily cross-subsidy effects between states are involved; however, such cross-subsidies are not explicit in (3.4) because they sum up to zero at the pool level.

3.4 Adjustment of the benefits by state

Once the pool fund available for state i at time t, that is

$F_t^{i, A}$

, is defined, we proceed to the adjustment of benefits imposing (3.7). We point out that this is a set of equations that must be solved backwards, from state m down to state 1. In particular, for

$F_t^{i, A}$

, is defined, we proceed to the adjustment of benefits imposing (3.7). We point out that this is a set of equations that must be solved backwards, from state m down to state 1. In particular, for

$i=m$

, we have

$i=m$

, we have

\begin{equation*} {} {} {}L_{x+t}^m B_{t}^m \ddot{a}_{x+t}^{m,m}=F_t^{m, A}, {} {}\end{equation*}

\begin{equation*} {} {} {}L_{x+t}^m B_{t}^m \ddot{a}_{x+t}^{m,m}=F_t^{m, A}, {} {}\end{equation*}

and the unknown

$B_t^m$

straightforwardly follows:

$B_t^m$

straightforwardly follows:

\begin{equation*} {} {} {}B_t^m=\frac{F_{t}^{m, A}}{L_{x+t}^{m}}\frac{1}{\ddot{a}^{m,m}_{x+t}}. {} {}\end{equation*}

\begin{equation*} {} {} {}B_t^m=\frac{F_{t}^{m, A}}{L_{x+t}^{m}}\frac{1}{\ddot{a}^{m,m}_{x+t}}. {} {}\end{equation*}

For

$i=m-1$

, by imposing

$i=m-1$

, by imposing

\begin{equation*} {} {} {}L_{x+t}^m \left( B_{t}^{m-1} \ddot{a}_{x+t}^{m-1,m-1}+ B_{t}^m \ddot{a}_{x+t}^{m-1,m}\right)=F_t^{m-1, A} {} {}\end{equation*}

\begin{equation*} {} {} {}L_{x+t}^m \left( B_{t}^{m-1} \ddot{a}_{x+t}^{m-1,m-1}+ B_{t}^m \ddot{a}_{x+t}^{m-1,m}\right)=F_t^{m-1, A} {} {}\end{equation*}

the unknown is

$B_t^{m-1}$

, being

$B_t^{m-1}$

, being

$B_t^{m}$

previously determined, and it holds that:

$B_t^{m}$

previously determined, and it holds that:

\begin{equation*} {} {} {}B_t^{m-1}=\left(\frac{F_{t}^{m-1, A}}{L_{x+t}^{m-1}}-B_{t}^m \ddot{a}_{x+t}^{m-1,m}\right)\frac{1}{\ddot{a}^{m-1,m-1}_{x+t}}. {} {}\end{equation*}

\begin{equation*} {} {} {}B_t^{m-1}=\left(\frac{F_{t}^{m-1, A}}{L_{x+t}^{m-1}}-B_{t}^m \ddot{a}_{x+t}^{m-1,m}\right)\frac{1}{\ddot{a}^{m-1,m-1}_{x+t}}. {} {}\end{equation*}

Proceeding iteratively, for the non-empty states, we find

\begin{equation} {} {} {}B_t^i=\left(\frac{F_{t}^{i, A}}{L_{x+t}^{i}}-\sum_{j\gt i}B_t^j\,{\ddot{a}^{i,j}_{x+t}} \right)\frac{1}{\ddot{a}^{i,j}_{x+t}}, {} {}\end{equation}

\begin{equation} {} {} {}B_t^i=\left(\frac{F_{t}^{i, A}}{L_{x+t}^{i}}-\sum_{j\gt i}B_t^j\,{\ddot{a}^{i,j}_{x+t}} \right)\frac{1}{\ddot{a}^{i,j}_{x+t}}, {} {}\end{equation}

while we assume that if

$L_{x+t}^i=0$

, then

$L_{x+t}^i=0$

, then

$B_t^i=B_{t-1}^i$

(i.e., no adjustment is applied to benefits relating to empty states).

$B_t^i=B_{t-1}^i$

(i.e., no adjustment is applied to benefits relating to empty states).

An interesting interpretation of the adjustment can be found in terms of individual fund

$V_t^i$

. For brevity, we develop it under the assumption

$V_t^i$

. For brevity, we develop it under the assumption

$L_{x+t-1}^i\gt0$

and

$L_{x+t-1}^i\gt0$

and

$X_t^i=0$

for all states i.

$X_t^i=0$

for all states i.

If we equate (3.6)–(3.16), and rearrange, we get

\begin{equation} {} {}\begin{aligned} {} {} {}V_t^{i} \left(L_{x+t}^i-\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\right) & = L_{x+t-1}^{i}\,p_{x+t-1}^{i,i}\, V_{t^-}^{i}+ \sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,(V_{t^-}^{i}-V_{t}^{i})\\& \quad- L_{x+t-1}^{i}\sum_{j\gt i}^m\left(\widetilde{p}_{x+t-1}^{\ i,j}-p_{x+t-1}^{i,j}\right)\,V_{t^-}^j. {} {}\end{aligned} {}\end{equation}

\begin{equation} {} {}\begin{aligned} {} {} {}V_t^{i} \left(L_{x+t}^i-\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\right) & = L_{x+t-1}^{i}\,p_{x+t-1}^{i,i}\, V_{t^-}^{i}+ \sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}\,(V_{t^-}^{i}-V_{t}^{i})\\& \quad- L_{x+t-1}^{i}\sum_{j\gt i}^m\left(\widetilde{p}_{x+t-1}^{\ i,j}-p_{x+t-1}^{i,j}\right)\,V_{t^-}^j. {} {}\end{aligned} {}\end{equation}

Since (3.13) can also be written as

\begin{equation*} {} {}L_{x+t}^i= L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,i}+\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}, {}\end{equation*}

\begin{equation*} {} {}L_{x+t}^i= L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,i}+\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}, {}\end{equation*}

from (3.18) we obtain

\begin{equation} {} {}V_t^{i} = \frac{p_{x+t-1}^{i,i}}{\widetilde{p}_{x+t-1}^{\, i,i}}\, V_{t^-}^{i}-\frac{\displaystyle\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}}{L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,i}}\,(V_{t}^{i}-V_{t^-}^{i})-\frac{\displaystyle \sum_{j\gt i}^m\left(\widetilde{p}_{x+t-1}^{\, i,j}-p_{x+t-1}^{i,j}\right)}{\widetilde{p}_{x+t-1}^{\, i,i}}\, V_{t^{-}}^{j}. {}\end{equation}

\begin{equation} {} {}V_t^{i} = \frac{p_{x+t-1}^{i,i}}{\widetilde{p}_{x+t-1}^{\, i,i}}\, V_{t^-}^{i}-\frac{\displaystyle\sum_{j\lt i}L_{x+t-1}^{j}\, \widetilde{p}_{x+t-1}^{\ j,i}}{L_{x+t-1}^{i}\, \widetilde{p}_{x+t-1}^{\ i,i}}\,(V_{t}^{i}-V_{t^-}^{i})-\frac{\displaystyle \sum_{j\gt i}^m\left(\widetilde{p}_{x+t-1}^{\, i,j}-p_{x+t-1}^{i,j}\right)}{\widetilde{p}_{x+t-1}^{\, i,i}}\, V_{t^{-}}^{j}. {}\end{equation}

When adjusting the benefits, clearly, we also need to adjust the individual required funds. Equation (3.19) suggests the following interpretation. The individual fund required at time t for state i must be adjusted because:

-

• The proportion of individuals remaining in state i differs from what was expected (see the first term of Equation (3.19));

-

• The cross-subsidy received for individuals entering state i from lower states

$j,j\lt i$

is based on

$V_{t^-}^i$

, but it must be updated to

$V_t^{i}$

after the adjustment (see the second term of Equation (3.19)); -

• The cross-subsidy transferred to higher states

$j,j\gt i$

is based on the realised transition rates, whereas the amount set aside in

$F_{t^-}^{i, A}$

is based on the expected transition rates (see the third term of Equation (3.19)).

We would like to emphasise that the first term recalls the mortality experience adjustment (MEA) factor introduced in Piggott et al. (Reference Piggott, Valdez and Detzel2005). It expresses the benefit update implied by the discrepancy between expected and realised mortality. In our multi-state framework, such an adjustment applies state-specific, accounting for ageing and mortality deviations. The second and third terms in Equation (3.19) correct the state-specific adjustment by accounting for, respectively, cross-subsidy inflows and outflows. Naturally, cross-subsidy cash flows can be defined in alternative ways; for instance, their amounts may be shaped based on the expected transition rates rather than realised values. Beyond the possible choices and consequent algebraic expressions, individual funds and benefits must be updated when experience differs from expectations, that is, realised cross-subsidies differ from those expected.

3.5 Smoothing benefits across states

The reasons that may lead an individual to prefer participation in a GSA scheme over the purchase of a life annuity are extensively discussed in the literature (see also Section 1); above all, cost savings, albeit at the expense of guarantees. When dealing with a multi-state GSA, one should additionally wonder why an individual should choose it, rather than one offering identical benefits across all states.

Similarly to a standard annuity, an individual who is aware of being in substandard health or maintaining unhealthy lifestyle patterns might feel disadvantaged by the use of undifferentiated annuity rates (see, e.g., Olivieri and Tabakova Reference Olivieri and Tabakova2024 for the case of annuities and Kabuche et al. Reference Kabuche, Sherris, Villegas and Ziveyi2024 for the case of a GSA). On the other hand, an individual currently in good health may feel better protected by a scheme that guarantees an upgrade in the benefit in the event of a deterioration in their health status. In this preference, one may recognise an interest akin to that observed for long-term care insurance products or disability income annuities.

Although GSA members are expected to accept benefit fluctuations across states depending on experience, they may reasonably expect a consistent and coherent ordering of those benefits, that is,

$B_t^1\lt B_t^2\lt\ldots\lt B_t^m$

at all times

$B_t^1\lt B_t^2\lt\ldots\lt B_t^m$

at all times

$t\geq0$

. At time

$t\geq0$

. At time

$t=0$

, this is ensured by the initial choice of the benefit amounts; however, Equation (3.17) does not necessarily maintain such an ordering at later times (

$t=0$

, this is ensured by the initial choice of the benefit amounts; however, Equation (3.17) does not necessarily maintain such an ordering at later times (

$t\gt0$

), as it does not explicitly consider the relative differences among benefit levels. We also note that, even when the ordering of benefits is preserved, the distance between them may fall below desirable thresholds. These considerations suggest the introduction of corrective mechanisms to the adjustment rule described in Section 3.4.

$t\gt0$

), as it does not explicitly consider the relative differences among benefit levels. We also note that, even when the ordering of benefits is preserved, the distance between them may fall below desirable thresholds. These considerations suggest the introduction of corrective mechanisms to the adjustment rule described in Section 3.4.

There is a further circumstance that may require modifications to the adjustment rule. As we have discussed earlier (see Sections 1, 2 and 3.1), ageing states are usually not observable. The current mortality profile of an individual can reasonably be detected based on proxy risk factors, which may lead to a classification of individuals that does not precisely replicate the intended ageing states. Moreover, either by design or in connection with the available proxy risk factors, it could be considered more appropriate to structure benefits across

$m^*$

classes, not necessarily matching the number of ageing states, that is,

$m^*$

classes, not necessarily matching the number of ageing states, that is,

$m^*\leq m$

. In settings where m is large, adopting fewer benefit classes,

$m^*\leq m$

. In settings where m is large, adopting fewer benefit classes,

$m^*\lt m$

, may offer a more practicable implementation. Illustrative proxy risk factors include medical events like the development of diabetes or a heart attack, as well as milder but indicative conditions such as hypertension, elevated glucose or cholesterol levels, or macular disease. They may also encompass functional or cognitive impairments, such as difficulties in performing activities of daily living or the onset of dementia. It should be noted that, given the absence of guarantees, the scheme may allow for a classification based on medical conditions or diseases that are typically excluded from standard insurance coverage. However, since more severe conditions result in access to a higher benefit class, safeguards must be anyhow in place to avoid potential misuse or fraud.

$m^*\lt m$

, may offer a more practicable implementation. Illustrative proxy risk factors include medical events like the development of diabetes or a heart attack, as well as milder but indicative conditions such as hypertension, elevated glucose or cholesterol levels, or macular disease. They may also encompass functional or cognitive impairments, such as difficulties in performing activities of daily living or the onset of dementia. It should be noted that, given the absence of guarantees, the scheme may allow for a classification based on medical conditions or diseases that are typically excluded from standard insurance coverage. However, since more severe conditions result in access to a higher benefit class, safeguards must be anyhow in place to avoid potential misuse or fraud.

In the following, we still refer to E as the set of ageing states and to

$E^*=\{1,2,\ldots, m^*\}$

as the set of benefit classes. Benefits

$E^*=\{1,2,\ldots, m^*\}$

as the set of benefit classes. Benefits

$B_t^i$

assessed as in Equation (3.17) ensure the actuarial equivalence between benefits and available resources by ageing state and for the whole pool, as discussed in Section 3.3. In the following, we refer to them as the notional benefits (or benefits by ageing state). We note that

$B_t^i$

assessed as in Equation (3.17) ensure the actuarial equivalence between benefits and available resources by ageing state and for the whole pool, as discussed in Section 3.3. In the following, we refer to them as the notional benefits (or benefits by ageing state). We note that

\begin{equation} {} {}B_t^{TOT}=\sum_{i\in E} L_{x+t}^i\,B_t^i {}\end{equation}

\begin{equation} {} {}B_t^{TOT}=\sum_{i\in E} L_{x+t}^i\,B_t^i {}\end{equation}

measures the total payout admitted by the actuarial equivalence condition (3.7) at time

$t,t\geq0$

. We denote with

$t,t\geq0$

. We denote with

$\overline{B}_t^k$

the benefit for class

$\overline{B}_t^k$

the benefit for class

$k\in E^*$

, and to keep the actuarial equivalence at the pool level, we require

$k\in E^*$

, and to keep the actuarial equivalence at the pool level, we require

\begin{equation} {} {}\sum_{k\in E^*} l_{x+t}^k\,\overline{B}_t^k = B_t^{TOT} , {}\end{equation}

\begin{equation} {} {}\sum_{k\in E^*} l_{x+t}^k\,\overline{B}_t^k = B_t^{TOT} , {}\end{equation}

where

$l_{x+t}^k$

is the number of survivors placed in benefit class k at time t (note that

$l_{x+t}^k$

is the number of survivors placed in benefit class k at time t (note that

$\sum_{i\in E} L_{x+t}^i=\sum_{k\in E^*}l_{x+t}^k$

). We refer to

$\sum_{i\in E} L_{x+t}^i=\sum_{k\in E^*}l_{x+t}^k$

). We refer to

$\overline{B}_t^k$

also as the actual benefits. Based on the motivations mentioned above, we introduce the further requirement:

$\overline{B}_t^k$

also as the actual benefits. Based on the motivations mentioned above, we introduce the further requirement:

\begin{equation} {} {}\overline{B}_t^k = u^k\,\overline{B}_t^1 , {}\end{equation}

\begin{equation} {} {}\overline{B}_t^k = u^k\,\overline{B}_t^1 , {}\end{equation}

where

$\overline{B}_t^1$

is the benefit amount for the lowest benefit class, and

$\overline{B}_t^1$

is the benefit amount for the lowest benefit class, and

$u^k$

,

$u^k$

,

$k=2,3,\ldots,m^*$

, is a coefficient chosen to achieve the desired differential between the benefit in class k and class 1. Reasonably,

$k=2,3,\ldots,m^*$

, is a coefficient chosen to achieve the desired differential between the benefit in class k and class 1. Reasonably,

$1\lt u^2\lt u^3\lt\ldots \lt u^{m^*}$

. To avoid potential misunderstandings when comparing the coefficients

$1\lt u^2\lt u^3\lt\ldots \lt u^{m^*}$

. To avoid potential misunderstandings when comparing the coefficients

$c^i$

’s introduced in Section 3.2 and the coefficients

$c^i$

’s introduced in Section 3.2 and the coefficients

$u^k$

’s, we stress that, by design,

$u^k$

’s, we stress that, by design,

$u^k$

measures the ratio at any time t between the actual benefit in class k in respect of class 1. The coefficient

$u^k$

measures the ratio at any time t between the actual benefit in class k in respect of class 1. The coefficient

$c^i$