1. Background

Financialisation is a broad term often defined as an increasing role of financial actors, markets, or logics within a sector of the economy or across world economies (Epstein, Reference Epstein2005; Mader et al., Reference Mader, Mertens and van der Zwan2020; van der Zwan, Reference van der Zwan2014). It has been used to describe a wide range of interconnected phenomena within contemporary life, including the expansion of financial markets; the rise of institutional investors, such as pension funds; and the expansion of financial profits within non-financial firms (Braun, Reference Braun2022; Lapavitsas, Reference Lapavitsas2013, Reference Lapavitsas2014). The term implies a shift beyond the mere quantitative growth of finance, and towards a qualitative change in the ways in which capital is accumulated. These changes have corresponding economic, social and political implications for households, organisations and firms, and states.

Recently, health system and policy scholars have drawn attention to the financialisation of health care. Examples are varied, but include the use of vaccine bonds to front-load financing for global immunisation programmes (e.g., Ebola vaccination campaign) (Hughes-McLure and Mawdsley, Reference Hughes-McLure and Mawdsley2022); the use of financial metrics by private health insurance funds (Mulligan, Reference Mulligan2016); and investment firms, including venture capital and private equity firms, acquiring and operating health care services (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023). In particular, investment firms – which pool and manage institutional investment funds – have drawn the attention of health systems scholars over the past decade, as they raised substantial funds for health services in many high- and middle-income countries (Bain & Company, 2024; Bruch et al., Reference Bruch, Roy and Grogan2024; Gondi and Song, Reference Gondi and Song2019). Proponents argue that financial markets and actors provide health systems with the needed capital and private-sector partnerships to address funding gaps. The Organization for Economic Co-Operation and Development (OECD, 2025) has warned that the rising levels of health spending, along with the need to develop more resilient healthcare systems, will put pressure on government budgets over the medium-term. Raising private funds from financial markets can potentially alleviate the public’s burden of fundraising via taxation and out-of-pocket payments (Kullberg et al., Reference Kullberg, Blomqvist and Winblad2022), support the pursuit of ambitious Social Development Goals, and foster innovation and entrepreneurship within the health sector (Kickbusch et al., Reference Kickbusch, Krech, Franz and Wells2018; Krech et al., Reference Krech, Kickbusch, Franz and Wells2018). However, policy experts and clinical providers have expressed concerns about the potential harms of financialisation (Applebaum and Batt, Reference Applebaum and Batt2020, Reference Applebaum and Batt2021; Bruch et al., Reference Bruch, Gondi and Song2021; Cai and Song, Reference Cai and Song2023). Recent systematic reviews have demonstrated that, while financial investment in health care may carry benefits, there are negative impacts on the costs and quality of care (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023; Unruh and Rice, Reference Unruh and Rice2025). In addition, there have been cases of service closures within the United States and the Netherlands, raising concerns over system stability (Fenne et al., Reference Fenne, O’Grady and Bugbee2025; Kroneman et al., Reference Kroneman, de Jong and Beerman2025; O’Grady, Reference O’Grady2022).

Despite the growth in research regarding financial actors within health systems, the theoretical foundations of financialisation, including the drivers and implications of financialisation within health systems, remain underdeveloped (Rabinovich and Reddy, Reference Rabinovich and Reddy2025). Health system governance is an important factor in providing comprehensive and equitable health services to populations (Reidpath and Allotey, Reference Reidpath and Allotey2006; Sun et al., Reference Sun, Ahn, Lievens and Zeng2017). In the early 2000s, the World Health Organization (WHO) called on governments to act as stewards of their health systems and ensure that resources are equitably distributed across their populations (World Health Organization, 2000; Travis et al., Reference Travis, Egger, Davies and Mechbal2002). Amongst other tasks, good governance requires leadership and oversight over private actors within health systems. Evidence suggests that, in the case of private equity ownership, outcomes such as the rate of mortality, adverse effects, and the costs of care are poorer than other for-profit ownership models (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023; Unruh and Rice, Reference Unruh and Rice2025). Governments have specifically targeted regulatory actions toward financial actors within health systems to address these poorer outcomes (Tracey et al., Reference Tracey, Schulmann, Tille, Rice, Mercille, Timans, Allin, Dottin, Syrjälä, Sotamaa, Keskimäki and Rechel2025). Given these possible risks of financialised healthcare it is important to consider what challenges this trend may present for governance over health systems.

In this paper, we provide a synthesis of pre-existing theories of financialisation in health systems, and consider the implications of financialisation for health system governance. In order to do so, we draw on theories of financialisation from the critical political economy literature, where the term financialisation has been subject to extensive debate (Lapavitsas, Reference Lapavitsas2013, Reference Lapavitsas2014). The remainder of this section will provide an overview of this literature. The subsequent sections detail the methodology, followed by a narrative account of the findings, and a brief discussion summarising the results, strengths, limitations and implications of this work.

1.1. Theories of financialisation

Epstein’s (Reference Epstein2005) definition of financialisation is perhaps the most common. He defines it as ‘the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’ (3). It can be distinguished from the related concepts of commodification, which refers to the assignment of an exchange-value (i.e., price) to an object or service on the market (Timmermans and Almeling, Reference Timmermans and Almeling2009); and privatisation, referring to the transfer of a property or service from public to private hands (Starr, Reference Starr1988). Use of the term financialisation has expanded since the 2008 financial crisis, and largely within the critical political economy literature (Mader et al., Reference Mader, Mertens and van der Zwan2020; Rabinovich and Reddy, Reference Rabinovich and Reddy2025). Different definitions have emerged as authors use the term more. van der Zwan (Reference van der Zwan2014) categorised three interrelated conceptualisations within the literature: it is considered 1) a regime of accumulation; 2) the ascendency of shareholder value; and 3) a feature of everyday life.

First, financialisation can be conceptualised as a shift in the regime of accumulation, defined by the increasing dominance of finance and financial profits within the world economy (Epstein, Reference Epstein2005). Krippner (Reference Krippner2012) describes it as ‘a pattern of accumulation where profits accrue primarily through … interest, dividends and capital gains, rather than trade and commodity production’ (174). Krippner points to the growth of financial firms’ profits within the US economy, and the proportion of financial profits reported by non-financial firms (e.g., manufacturing firms, hospitals, etc.) as signs of this transformation. Financial profits are not considered ‘real’, in that they do not derive from the production and sale of commodities or services, but from ‘transfers of income away from those activities that do produce value’ (83).

The tension between financial and productive activity runs through much of this literature. Financial firms and markets are thought of as a double-edged sword: on the one hand, they act as an economy’s central nervous system, and direct idle funds towards new innovations; while, on the other hand, they can act ‘parasitically’ on firms by directing capital funds away from investment and towards financial payments (Campbell and Bakir, Reference Campbell and Bakir2022; Durand, Reference Durand2017). Drawing on the work of Arrighi (Reference Arrighi2010), many of these authors see the expansion of financial accumulation as a sign of economic stagnation and a source of social inequality (Durand, Reference Durand2017; Krippner, Reference Krippner2012; Lapavitsas, Reference Lapavitsas2013; Lee and Siddique, Reference Lee and Siddique2021).

However, not all are convinced that financialisation signals decline within capitalist economies. Maher and Aquanno (Reference Maher and Aquanno2022) argue that it ‘provides managers with the tools to pursue new profit-maximizing strategies’ (20). Within their historical account of the United States, they demonstrate that finance has played a major role in expanding productive economies prior to the current period to which other researchers restrict their analyses of financialisation. The emergence of modern banking in the 19th century allowed society to efficiently pool and allocate capital across industries and lowered the transaction costs for capital investment. Contrary to the so-called parasite thesis that finance diverts funds away from production, these authors claim that highly mobile capital spurs competitiveness and discipline between firms. In this way, it represents a fundamental and historical dynamic of capitalism. This should not be mistaken as an argument in favour of financialisation, but rather it is an acknowledgement of tensions immanent within capitalism that produce unwanted externalities, e.g., income inequality, in the pursuit of profits.

In addition to the broader changes in economic activity, financialisation has been characterised by the emergence of shareholder value orientation within non-financial firms (van der Zwan, Reference van der Zwan2014). Shareholder value is the expression of financialisation within corporate governance and can be seen as an ideology and set of business practices which prioritise maximising short-term profits and share values over long-term growth and capital expenditures (Fligstein and Goldstein, Reference Fligstein and Goldstein2022; Rabinovich and Reddy, Reference Rabinovich and Reddy2025). Lazonick and O’Sullivan (Reference Lazonick and O’Sullivan2000) describe it as a shift in corporate practices away from ‘retain and invest’ strategies towards distributing an increasing share of corporate earnings to shareholders. In practice, this is achieved via the expansion of managerial tactics intended to maintain high share prices, including – but not limited to – aligning the objectives of management and shareholders, downsizing labour forces, and stock buybacks. These tactics consequently worsen economic inequality between top and bottom income and wealth earners (Fligstein and Goldstein, Reference Fligstein and Goldstein2022; Lazonick and O’Sullivan, Reference Lazonick and O’Sullivan2000). In their recent critiques of corporate financialisation and shareholder value, Rabinovich and Reddy (Rabinovich and Reddy, Reference Rabinovich and Reddy2025; Reddy and Rabinovich, Reference Reddy and Rabinovich2025) argue that the empirical evidence does not demonstrate that shareholder value orientation negatively affects a firm’s long-term growth in general, but only in particular cases – namely, when hedge funds own a majority of firms’ funds.

Finally, financialisation can be framed as a feature of everyday life (van der Zwan, Reference van der Zwan2014). Individuals within lower and middle-income brackets are increasingly exposed to credit, insurance and retail investment products (Montgomerie, Reference Montgomerie2006). Furthermore, in countries like the United States, many individuals are exposed to financial markets through instruments like credit cards and reverse mortgages. As welfare states have receded, these financial instruments become more important in how households secure their future (Montgomerie, Reference Montgomerie2009).

Two points can be made. First, these framings are not mutually exclusive, e.g., changes in shareholder value orientation are considered a meso-level mechanism corresponding to macro-level changes in capital accumulation. Given financialisation’s broad definitions, scholars may choose to emphasise certain phenomena over others without necessarily refuting other framings. Second, different framings may share implications. For example, most scholars agree that financialisation is the product of government policies (Copley, Reference Copley and Copley2021; Krippner, Reference Krippner2012; Maher and Aquanno, Reference Maher and Aquanno2022; Montgomerie, Reference Montgomerie2009), including banking regulation or monetary responses to economic downturns. However, there is debate regarding whether financialisation is the result of laissez-faire, deregulatory styles of governance (e.g., Krippner, Reference Krippner2012), allowing financial actors more freedom; or whether states adopted new forms of regulation to facilitate the growth of the finance and ensure continued profitability (e.g., Maher and Aquanno, Reference Maher and Aquanno2022; Montgomerie, Reference Montgomerie2009).

Given the varieties, there have been attempts to clarify and strengthen financialisation theories. In their survey, Mader et al. (Reference Mader, Mertens and van der Zwan2020) provided three criteria which to evaluate the analytic value of a theory. They argue that definitions must (a) set limits on the scope of phenomenon categorised; (b) propose causal mechanisms that explain how and why financialisation happens; and (c) consider the role of context in explaining variation in financialisation in different regions or sectors. The authors hope that by using these criteria, along with a focus on the ‘so what’ of financialisation, that this literature will be of greater use to policymakers.

In summary, the concept of financialisation is used in the critical political economic literature to describe a range of overlapping phenomena, and the different theories often share implications, while some points of contention exist between them. As the use of the term expands, there have been conceptual critiques, and attempts to systematize and assess its analytical strength. Our study builds on this previous work, while focusing specifically within health systems. It reviews theories of financialisation and health systems and health systems governance, utilising critical political economy to classify and reflect upon how this concept is employed within scholarship on health systems.

1.2. Objectives

As summarised above, some scholars have begun to describe health systems as financialised. The objective of this review was to critically interpret and synthesise theories of financialisation within health systems, and its implications for health system governance.

2. Methods

This work was the product of a critical interpretative synthesis (CIS) (Dixon-Woods et al., Reference Dixon-Woods, Cavers and Agarwal2006) of theories of financialisation within health systems. Compared to systematic review methodologies, a CIS allows for iterative search methods and is useful for studying ‘fuzzy’ concepts. While systematic reviews are suited for answering questions with specific parameters, not all questions can be formulated with precision. As summarised above, the term financialisation refers to many related but distinct phenomena, and precise inclusion and exclusion criteria may exclude relevant materials. Furthermore, the literature on financialisation is methodologically diverse, thus we anticipated that it would be challenging to assess studies using standard, aggregate systematic review methodology. Instead, our objective was to qualitatively synthesise the literature and examine its definitions, assumptions, and implications. Finally, the CIS framework allowed us to identify which themes from critical political economy were absent within health systems research. The CIS process took place between March and June 2025. This protocol was not registered but was presented at a scholarly workshop in May 2025, where feedback was provided.

2.1. Search strategy

The first step was to conduct a search for literature on financialisation and health systems. The full details of how the CIS search strategy was developed can be found in Appendix A. In brief, our search considered peer-reviewed and grey literature identified from two databases: MEDLINE (Ovid) and Sociological Abstracts (ProQuest). Two team members (MT and DH) screened the search results for eligibility in Covidence (Veritas Health Innovation, 2022). Articles were eligible if they included a conceptual framework or theory which related financialisation to health systems. Non-English literature was excluded due to team capacity. Disagreements between the two reviewers were resolved through discussion until consensus was reached. The results of the search and review process are reported within a PRISMA-ScR flow diagram for records screened in databases and other media (See appendix Figure A1) (Page et al., Reference Page, McKenzie, Bossuyt, Boutron, Hoffmann, Mulrow, Shamseer, Tetzlaff, Akl, Brennan, Chou, Glanville, Grimshaw, Aørn, Lalu, Li, Loder, Mayo-Wilson, McDonald, McGuinness, Stewart, Thomas, Tricco, Welch, Whiting and Moher2021).

2.2. Data analysis

Descriptive data was extracted from eligible full-text articles using an original data collection form, derived from Campbell et al.’s (Reference Campbell, Egan, Lorenc, Bond, Popham, Fenton and Benzeval2014) work on scoping reviews of theoretical frameworks, and from several key texts on financialisation (Mader et al., Reference Mader, Mertens and van der Zwan2020; van der Zwan, Reference van der Zwan2014). Furthermore, we extracted initial data on financialisation’s implications for governance using the TAPIC (transparency, accountability, participation, integrity and policy capacity) framework (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019). A qualitative synthesis of the data was conducted, identifying themes within the literature using NVivo (Lumivero, 2025). A largely inductive approach was taken by generating codes from the data, however, some key codes were developed a priori, including ‘definition of financialisation’, ‘conceptual limits’ and the categories of health system governance. Relevant quotations were also extracted from the articles. Finally, the literature reviewed in this work was compared to scholarship on financialisation from the critical political economy literature (e.g., Epstein, Reference Epstein2005; Krippner, Reference Krippner2012; Lapavitsas, Reference Lapavitsas2013; Maher and Aquanno, Reference Maher and Aquanno2022, Reference Maher and Aquanno2024; Durand, Reference Durand2017). This scholarship was used to identify common themes between articles reviewed in the CIS, and to identify gaps in their theoretical formulations.

3. Results

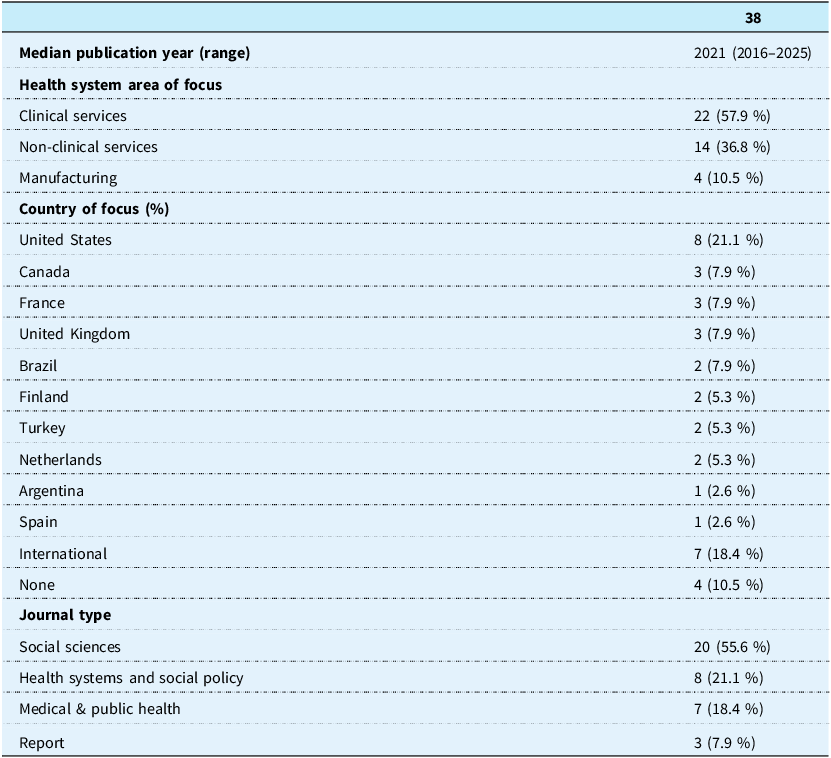

The search within the two selected databases resulted in 4618 titles (See appendix Figure A1). The two reviewers independently screened titles and abstracts, and they identified 109 titles eligible for full-text review. A total of 38 articles were eligible for the analysis: 10 from the initial search, 22 from the structured search, and 6 from the reference search. Publication dates ranged from 2006–2025, and 27 studies were published in 2020 or afterwards (Table 1). Twenty were published in social science journals: 8 in health systems or policy journals, 7 were published in medical or public health journals, and 3 were reports. Most articles focused on high-income countries. Twenty-two articles addressed the financialisation of clinical services (especially long-term care), 14 addressed non-clinical services (e.g., insurance), and 4 addressed manufacturing.

Characteristics of literature reviewed

3.1. Conceptualising financialisation

3.1.1. Definitions

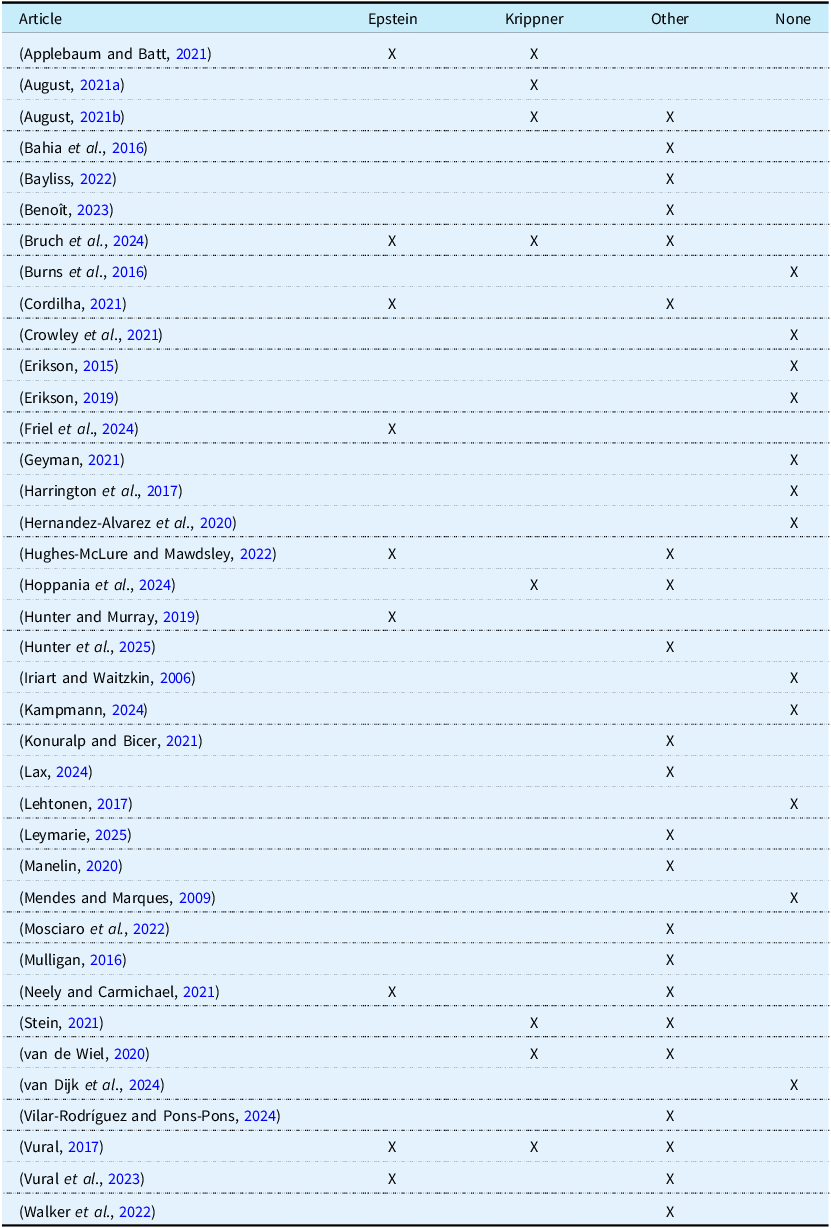

Twenty-five articles included in this review contained an explicit definition of financialisation (see Table 2). The remaining 13 addressed some components of financialisation without providing an explicit definition. Nine articles relied on Epstein’s (Reference Epstein2005) definition, and Krippner’s (Reference Krippner2012) was the second most-cited. Regardless of which definition the 25 articles drew on, they all described financialisation as a transformative process in which finance, financial actors, or financial instruments grow in proportion to the larger economy. This growth is accompanied by the influence or dominance of financial actors over the ‘real’ economy which manufactures goods and provides services (e.g., August, Reference August2021a, Reference August2021b).

Definitions of financialisation

Bruch et al. (Reference Bruch, Roy and Grogan2024) defined financialisation within health systems as a turn ‘away from trade and commodity production toward new financial channels and maneuvers’ (178). Stein (Reference Stein2021) referred to the financialisation of global health as a process by which it becomes ‘oriented more and more towards financial concepts, motives, practices and institutions’ (2). In a study of fertility clinics, van de Wiel (Reference van de Wiel2020) defined it as a shift in business practices that ‘orient firms to financial markets’ (309) and investments. These are strategies that prioritise shareholder value, and include: the use of financial instruments that divert profits away from productive processes to investors; the consolidation of services via mergers and acquisitions to increase market power; or changes to organisational strategies and service provision to enhance profitability. Other definitions emphasised the changes in the behaviour of non-financial firms and states. Cordilha (Reference Cordilha2021) defined it as the domination of certain types of practices or narratives within states, firms, and households. Mosciaro et al. (Reference Mosciaro, Kaika and Engelen2022) argued it is the adoption of ‘outside’, financial instruments within healthcare.

While most of the articles within this review did not explicitly draw on Marxian theory to define financialisation, most cited scholars, e.g., Epstein or Krippner, influenced by it. Lapavitsas (Reference Lapavitsas2013, Reference Lapavitsas2014) argued that the concept of financialisation is intimately tied to Marxian theory, as it is used to describe an epochal transformation within capitalist economies, often with a critical view of this process. Articles included in this review drew on these themes as well. They periodised financialisation as a recent development within health systems. As with some strains of Marxian theory – especially those influenced by Arrighi (Reference Arrighi2010) – they also considered it a sign of system dysfunction. Two authors explicitly drew on Marxian concepts: Eren Vural (Reference Vural2017) described financialisation as an ‘expansion of scale and scope of … the money form of capital’ (277), which she later referred to as fictitious capital, as did Konuralp and Bicer (Reference Konuralp and Bicer2021). While the term predates Marx, he and contemporary Marxist scholars used it to refer to a present valuation of claims on future revenue (Durand, Reference Durand2017; Marx, Reference Marx1993; Wilhans et al., Reference Wilhans, Palludeto and Rossi2022). This concept will be discussed in greater detail later.

The articles included in this review defined financialisation as either the growing presence of financial outsiders, e.g., private equity firms, within healthcare systems; and as insiders adopting of certain practices, e.g., revenues from financial instruments, within healthcare systems. Vilar-Rodríguez and Pons-Pons (Reference Vilar-Rodríguez and Pons-Pons2024) argued that, over time, the ownership of Spanish insurance companies shifted from clinicians to investors (e.g., banks, investment funds) who prioritised financial returns over health. Similarly, Benoît’s (Reference Benoît2023) case study of changes in French mutual funds demonstrated that financialised regulatory changes within the European Union led to the growth of financial experts employed by French health insurance firms.

3.1.2. Conceptual distinctions

The limits of a theory refers to the conceptual distinction that the authors make between financialisation and other, related, concepts (Mader et al., Reference Mader, Mertens and van der Zwan2020). Most of the articles included in this review made no attempt to differentiate financialisation from other concepts. Three papers made a distinction between financialisation and marketisation, which refers to outsourcing, or to the introduction of competition and price mechanisms into public services (Hoppania et al., Reference Hoppania, Karsio, Näre, Vaittinen and Zechner2024; Konuralp and Bicer, Reference Konuralp and Bicer2021; Stein, Reference Stein2021). For example, Hoppina et al., argued that to marketise public healthcare means to convert it into a commodity to be sold on the market, or to purchase or sell care on the market. Similarly, three authors differentiated privatisation and financialisation (Bayliss, Reference Bayliss2022; Bruch et al., Reference Bruch, Roy and Grogan2024; Konuralp and Bicer, Reference Konuralp and Bicer2021). Konuralp and Bicer (Reference Konuralp and Bicer2021) defined privatisation, or the transfer of publicly owned assets to private ownership, as the most extreme form of marketisation, and Bruch et al. (Reference Bruch, Roy and Grogan2024) referred to privatisation as ‘the growing role of private-sector actors in the provision of health care resources’ (178). These authors made a point to distinguish between marketisation and financialisation; arguing that ‘not all marketized care is financialised’ (2). Stein (Reference Stein2021) claimed that financialisation is distinct from market mechanisms because it is a regime of accumulation defined by debt relationships, and that healthcare services can be outsourced to private, for-profit firms without necessarily being financialised.

3.1.3. Drivers of financialisation within health systems

All studies identified at least one driver of financialisation within health systems. The most common mechanisms identified were insufficient, or declining public funding for healthcare, and policies which deregulated and marketized healthcare. Reduced public spending on social services generates a need for new forms of funding, which financial actors can provide. Stein (Reference Stein2021) argued that financialisation in healthcare is driven by the lack of funds available for health services, and a surplus of private capital available to address that shortage. Cordilha (Reference Cordilha2021) provided an example of this in a case study of the financialisation of French social service funding. First, financial instruments are introduced within the ‘funding circuit’ of state programmes, which ‘allow[s] the public sector to mobilize funds voluntarily in the financial system, as opposed to using coercive means such as taxation’ (6). In turn, the state becomes dependent on financial capital for continued operations. Similarly, Applebaum and Batt (Reference Applebaum and Batt2021) argued that, in the United States, reduced public expenditure spurred hospitals to utilise speculative, financial tactics to address funding gaps, which imbricated hospitals and health systems in financial logics and incentives. The growth of new health sectors – specifically the digital health and biotechnology sectors – is another potential driver. van de Wiel (Reference van de Wiel2020) argued that biotechnology firms pursuing novel drugs or treatments attracts investment via venture capital firms. Kampmann’s (Reference Kampmann2024) identified the UK government’s desire for cost-saving, value-based care strategies as a impetus for venture capital to move into the digital health sector. Finally, while marketisation and privatisation are considered distinct from financialisation, these processes within health systems provide opportunities for financial actors and logics to enter health systems.

Several authors considered financialisation to be the product – or extension of – neoliberal reforms. Neoliberalism is another term that describes a range of phenomena, but generally refers to an ideology that favours markets as means of achieving social order and prosperity. Neoliberals call for ‘insulating’ markets from democratic mechanisms and oversight (Slobodan, Reference Slobodan2018). Vural et al. (Reference Vural, Herder, Doll and Graham2023) referred to financialisation as ‘spreading neoliberal ideas and governance models’ (2), whereas Bayliss (Reference Bayliss2022) depicted financialisation and neoliberalism as moving in tandem.

The literature reviewed in this study consistently defined financialisation as a transformational process in which financial actors, instruments, and logics become more prominent within health systems. The influence or dominance of financial actors over health systems was a common theme across definitions, and agents of financialisation were either characterised as outsiders or insiders to health systems. Finally, a minority of papers made efforts to distinguish it from other phenomena, including privatisation or marketisation. These latter processes are considered to be part of a larger neoliberal project that preceded and enabled finance to grow within healthcare, via the state’s need to address funding gaps in order to maintain services.

3.2. Emergent themes

This section addresses two of the most salient themes which emerged within the literature reviewed as part of the CIS.

3.2.1. Financial instruments, profits, and health systems

Financial profits are key to understanding the financialisation of health systems. While profit is rarely the focus of these articles, it is considered an underlying motivation of financial actors (i.e., outsiders) to invest within the health sector, and a motivation of health care systems (i.e., insiders) seek financing and adopt financial logics. This section will provide an overview of how financial profits are conceptualised within the critical political economy literature.

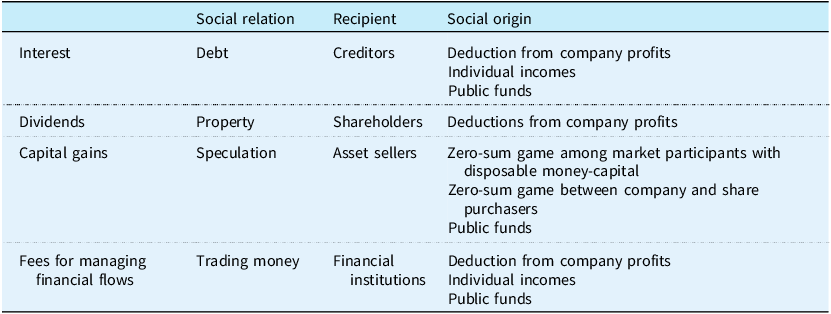

First, financial profits are derived from different instruments, which are tradable equity, debts or financial assets (Durand, Reference Durand2017; Krippner, Reference Krippner2012; Lapavitsas, Reference Lapavitsas2014; Maher and Aquanno, Reference Maher and Aquanno2022). The basic forms of instruments include loans, government or corporate bonds, corporate shares, or properties. The source of profit differs, and Table 3 – adapted from Durand (Reference Durand2017) – lists the source of profits for each type of instrument. Durand characterises these instruments as ‘fictitious capital’, a term used within the Marxian tradition to denote assets which are capitalised based on anticipated future revenues as opposed to current valuation (Lapavitsas, Reference Lapavitsas2014; Wilhans et al., Reference Wilhans, Palludeto and Rossi2022). For Durand, financial instruments generate profits through two basic routes: via parasitism, or the direct deductions of a company’s profits towards entities outside of the productive process (e.g., shareholders, including institutional investors via private equity funds or venture capital funds); and via dispossession, or the indirect deduction of funds, e.g., tax funds used to pay bondholders. In both streams, financial profits are a deduction of funds generated through the so-called ‘real’ economy of goods and services towards investors who are removed from this process.

The articles reviewed in this CIS align with Durand’s (Reference Durand2017) framework. Most articles characterise financialisation as an extractive process diverting value away from production or the quality of care, towards shareholders (Applebaum and Batt, Reference Applebaum and Batt2021; Cordilha, Reference Cordilha2021; Hunter and Murray, Reference Hunter and Murray2019; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025; Sell, Reference Sell2020), and financial instruments are the means by which value is extracted. Cordilha (Reference Cordilha2021) showed that the use of bond issuances to finance France’s public health systems has resulted in increasing transfer of tax funds to investors via interest payments. In their analysis of the International Finance Facility for Immunisation, Hughes-McLure and Mawdsley (Reference Hughes-McLure and Mawdsley2022) demonstrated that a substantial amount of funds raised by the facility are used to pay interest on bonds the facility has issued instead of purchasing vaccines. Other papers highlighted extractive processes such as dividend recapitalizations – where health services pay dividends to shareholders through new debt or bond issuances; or through lease buybacks where properties are sold and then leased back to a healthcare service (Applebaum and Batt, Reference Applebaum and Batt2021). Finally, intellectual property rights become means of extracting rents from companies or public institutions (Bayliss, Reference Bayliss2022; Sell, Reference Sell2020). As a function of this extractive process, health care services are restructured to ensure that profitability is maintained, including reduced staffing, reducing the costs of care and lowering the cost-to-charge ratios (Applebaum and Batt, Reference Applebaum and Batt2021; Bruch et al., Reference Bruch, Roy and Grogan2024; Eren Vural, Reference Vural2017). This, it is argued, can threaten a state’s ability to provide accessible and quality healthcare to its population (Konuralp and Bicer, Reference Konuralp and Bicer2021).

Within these accounts, financial instruments function as an extractive mechanism, diverting funds from productive activity towards investors, with potentially destabilising effects. However, Maher and Aquanno (Reference Maher and Aquanno2022) – also within the Marxist tradition – cautioned against conceptualising financialisation as a distinctly dysfunctional economic order. Drawing on Marx (Reference Marx1993), as well as the Austrian economist Rudolph Hilferding (Reference Hilferding1981), they offered a historical account of the role of finance within capitalist development. Financial institutions, namely banks, developed as an efficient means of distributing financing across firms and industries through loans or through share purchases. Banks were also able to help steer firms by placing their own representatives on corporate boards over long-term periods. Historically, financial institutions were not simply extractive but acted to direct industrial activity and support profitability (Maher and Aquanno, Reference Maher and Aquanno2024). These authors argue that finance can help maintain profitability.

One of the works included in the CIS explicitly addressed relationship between financial and real (productive) value within health systems. Within a case study of venture capital in the United Kingdom, Kampmann (Reference Kampmann2024) found that the valuation of the company was intrinsically tied to its ability to produce viable products in the present. In other words, while financial value of a company may be relatively autonomous from productive capacities, the latter ultimately acts as the anchor for the former.

The question of financial profits within health systems re-occurs within the reviewed literature. Financial profits are characterised as parasitical or extractive, often diverting funds away from health care financing or services towards investors in the form of interest, dividends, rents or financial management fees. Most scholars of financialisation agree that these ‘fictitious’ forms of capital are – to some extent – necessary for capitalism to function. This has several implications for theorising financialisation within health systems. First, finance may not merely be extractive, but tied up in the productivity of healthcare services in more complex ways – as demonstrated by Kampmann (Reference Kampmann2024). Second, financial tactics to maximise the profitability of a healthcare system may negatively correlate with the accessibility and quality of care.

3.2.2. Competition and monopoly

Four of the works included in this CIS argued that financialisation corresponds to a rise in monopolies in healthcare systems (Applebaum and Batt, Reference Applebaum and Batt2021; Bayliss, Reference Bayliss2022; Sell, Reference Sell2020; Vilar-Rodríguez and Pons-Pons, Reference Vilar-Rodríguez and Pons-Pons2024). Applebaum and Batt (Reference Applebaum and Batt2021) do so in several ways. First, they identified the relaxation of anti-trust legislation in the United States as a key causal factor in the rise of financialisation. Second, financial investment firms, especially private equity firms, acquire and consolidate health services into large networks. This, consequentially, concentrates their market power, and thereby increasing healthcare prices. Empirical studies – external to this review – have demonstrated that the costs of healthcare increases after services are acquired by private equity firms (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023; Unruh and Rice, Reference Unruh and Rice2025), and this is especially true when a single private equity firm has acquired a number of services within a metropolitan area (Scheffler et al., Reference Scheffler, Alexander and Godwin2021). While some scholars consider financialisation as anti-competitive and a driver of monopolisation, others argue that it has the opposite effect (Maher and Aquanno, Reference Maher and Aquanno2022). In this telling, highly mobile financial capital acts to build competitive pressures across firms and nations. When health systems become dependent upon financial markets for funding, they must compete with other firms across industrial sectors to attract investors. While two of the articles reviewed here considered the effects of financialisation, i.e., consolidation, on patients (Bruch et al., Reference Bruch, Roy and Grogan2024; Lehtonen, Reference Lehtonen2017), no articles included in this review considered whether, or how, competitive pressures between financialized firms may affect health systems. Nor did they consider whether or not consolidation of services equates to a smaller number of firms claiming a larger share of profits.

3.3. Financialisation and health system governance

The previous section provided a summary of how scholars have defined and conceptualised financialisation within health systems, and highlighted emergent themes within the reviewed articles. This section reviews the implications of financialisation for health system governance from the reviewed articles. We structure the findings using the TAPIC model of governance to identify themes relating to transparency, accountability, participation, integrity and policy capacity (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019).

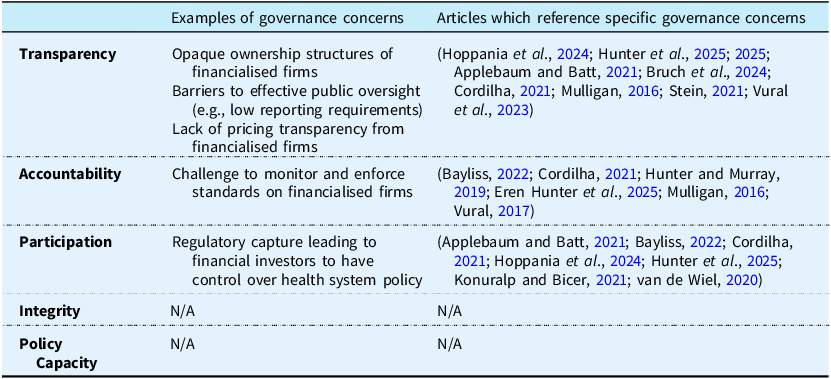

3.3.1. Transparency

Many of the papers reviewed as part of this CIS identified transparency concerns (Applebaum and Batt, Reference Applebaum and Batt2021; Bayliss, Reference Bayliss2022; Bruch et al., Reference Bruch, Roy and Grogan2024; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025; Mulligan, Reference Mulligan2016; Stein, Reference Stein2021), including the challenges that publics have in identifying who owns specific services, e.g., via the use of shell companies which can obscure ownership (Table 4). This can potentially hamper proper oversight (Bruch et al., Reference Bruch, Roy and Grogan2024) and effective taxation (Bayliss, Reference Bayliss2022). In a case study on the French Government’s use of institutional financing to service public debts, Cordilha (Reference Cordilha2021) claimed that ‘the origins of funds and the destination of reimbursements cannot be fully known due to confidentiality agreements and exchanges on secondary markets‘ (23). Cordilha argued that the very use of financial markets reduces the transparency of financing.

Health system governance challenges

Financialisation can also threaten the transparency of pricing. Stein (Reference Stein2021) argued that, for the COVAX programme,

Contractual details [regarding] subsidies have been mostly kept secret. While UNICEF and Gavi assure the public that the vaccines COVAX buys cost a mere $1.66 per dose, hardly any information about vaccine manufacturing costs, advance payment contracts or “push” and “pull” subsidies have been made public (7).

Mulligan (Reference Mulligan2016) argued that opacity is a deliberate strategy within finance – or a form of ‘creative play’ – which allows firms to be selective when representing the costs of care. Mulligan argues that within the US context, this strategy proliferated after the Affordable Care Act was implemented, which included rules to ensure that private insurance firms committed that a certain per cent of premiums were spent on health services over administrative fees. Insurance firms adapted to this legislation by redesignating what constituted medical services and hide administrative fees. Together, these papers suggest that actors within financialised health systems may strategically obscure information, for the purposes of bypassing scrutiny and regulation, or for tax avoidance.

3.3.2. Accountability

Authors have also identified concerns for the accountability of financialised healthcare services (Applebaum and Batt, Reference Applebaum and Batt2021; Hunter and Murray, Reference Hunter and Murray2019; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025). Several authors argued that the transparency concerns hinder governments’ ability to hold financial actors accountable. However, these scholars did not elaborate on how financialisation impacts accountability. Hoppania et al. (Reference Hoppania, Karsio, Näre, Vaittinen and Zechner2024) argued that,

Decisions on care provision and resources are made in the interest of offshore owners rather than clients or workers, in complex corporate structures which democratic governance of the welfare state cannot reach. As their market shares grow, these undemocratic financialised actors are gradually gaining significant political influence in political decisions regarding welfare service provision (14).

Accountability is therefore connected to the opacity of ownership models, as well as their use of offshore headquarters to avoid state accountability processes.

3.3.3. Participation

Within health system governance, participation refers to the capacity of different stakeholders and parties to have input into health system policy and design (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019). There are concerns financialisation leads to regulatory capture which provides financial actors within health systems greater influence over policy, which they will use to prioritise shareholders’ interests (Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025). Specifically, institutional investors such as private equity firms or large, passive index funds with investments within health systems will have influence or control over service provision and policy as a function of their market share (Applebaum and Batt, Reference Applebaum and Batt2021). As cited in the section above, Hoppania et al. (Reference Hoppania, Karsio, Näre, Vaittinen and Zechner2024) argued that democratic control over large, offshore chains is challenging. Konuralp and Bicer (Reference Konuralp and Bicer2021) referred to ‘subordinated financialisation’ in which Turkish healthcare reform was shaped by international financial elites, although they did not elaborate on how such outside actors shaped healthcare reform in Turkey.

3.3.4. Integrity

Integrity refers to the clarity of roles and responsibilities within health systems (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019). No study included in the review identified concerns regarding the integrity of financialised health systems.

3.3.5. Policy capacity

Policy capacity refers to the ability to diagnose and address policy failures (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019). While many of the studies included in this CIS considered the policies that facilitated the financialisation of health services, no studies considered its effects on policy capacity.

In summary, many articles included in the initial review addressed the relationship between financialisation and health system governance, and, generally, considered it a challenge to governance. Some provided more robust and clear examples, while others only mentioned brief, potential implications. Concerns regarding the transparency and participation and accountability were the most common, while integrity and policy capacity were not addressed.

4. Discussion

While some authors and policymakers consider financial investors as a means to address funding gaps and foster innovation in health systems (Enekwechi, Reference Enekwechi2023; Kickbusch et al., Reference Kickbusch, Krech, Franz and Wells2018; Krech et al., Reference Krech, Kickbusch, Franz and Wells2018), there are growing concerns regarding the financialisation of healthcare financing and delivery (Applebaum and Batt, Reference Applebaum and Batt2021; August, Reference August2021b; Bruch et al., Reference Bruch, Gondi and Song2021; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025; Tracey et al., Reference Tracey, Schulmann, Tille, Rice, Mercille, Timans, Allin, Dottin, Syrjälä, Sotamaa, Keskimäki and Rechel2025). An emergent body of literature has demonstrated that these actors can have important, often negative consequences for health care systems (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023; Unruh and Rice, Reference Unruh and Rice2025).

The purpose of this study was to synthesise and critically interpret themes within the literature on financialisation and health systems and its implications for health systems governance. The reviewed articles generally defined financialisation as a structural transformation of health systems characterised by the increased role of financial investors, instruments and logics. Most studies did not provide distinctions between financialisation and related concepts, such as marketisation and corporatisation. Twenty-four studies identified at least one driver of financialisation, and several articles provided detailed accounts of how these drivers led to financialisation (Applebaum and Batt, Reference Applebaum and Batt2021; Bayliss, Reference Bayliss2022; Benoît, Reference Benoît2023; Vilar-Rodríguez and Pons-Pons, Reference Vilar-Rodríguez and Pons-Pons2024).

We argue that, underlying all of the definitions, is a focus on the role of financial instruments which direct private, profit-seeking investment, directly or indirectly, into health care. In many of the articles, finance is assumed to extract or divert funds away from health care services towards investors in the form of financial profits, such as interest and dividends. It is either an ‘outside’ force penetrating health systems, or a force ‘inside’ healthcare services which turn to financial instruments as a source of funding. This process may be quite literal, as in Vilar-Rodríguez and Pons-Pons (Reference Vilar-Rodríguez and Pons-Pons2024) case, in which the composition boards of Spanish health insurance companies gradually shifted away from health professional towards investor representation, or indirectly by which investment firms acquired healthcare firms (Applebaum and Batt, Reference Applebaum and Batt2021).

Consistent with critical political economy scholarship, the articles reviewed here emphasised financialisation’s potential negative effects on health systems. Several employed this term to mobilise publics against private healthcare financing, and towards public sources (August, Reference August2021b; Bayliss, Reference Bayliss2022; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025). There in a consensus that financial agents extract profits by diverting funds from the ‘real’ economy, or the production of goods and services – what is generally referred to as shareholder value orientation. Shareholder value, which emphasises investor profits via ‘fictitious’ sources over long-term growth, offers a potential causal mechanism linking financial instruments with the poor outcomes which can occur after investment firms acquire clinical services (Borsa et al., Reference Borsa, Bejarano, Ellen and Bruch2023; Kannan et al., Reference Kannan, Bruch, Zubizarreta, Stevens and Song2025; Unruh and Rice, Reference Unruh and Rice2025). Several articles reviewed here demonstrate that financial actors do accrue profits within health systems through these sources (Cordilha, Reference Cordilha2021; Hughes-McLure and Mawdsley, Reference Hughes-McLure and Mawdsley2022), however, to our knowledge, this has not been directly linked to outcomes. Recent critical political economic scholarship does not supported the claim that, in general, shareholder value orientation is associated with a decline in firms’ capital expenditure (Rabinovich and Reddy, Reference Rabinovich and Reddy2025; Reddy and Rabinovich, Reference Reddy and Rabinovich2025), and more work is required to untangle possible causal relationships between financialisation and service provision, and any potential mediating factors (e.g., policies addressing financial actors within health systems).

The articles generally associated financialisation with consolidation, leading to anti-competitive conditions and monopolisation. While there is evidence that financial actors do consolidate healthcare services (Scheffler et al., Reference Scheffler, Alexander and Godwin2021) and insurance firms (Vilar-Rodríguez and Pons-Pons, Reference Vilar-Rodríguez and Pons-Pons2024), this does not necessarily demonstrate a reduction in competition. Some critical political economy theorists have pointed to the ways in which finance helps to maintain competitiveness between firms, and help maintain profitability (Maher and Aquanno, Reference Maher and Aquanno2022). When large investment firms hold a diverse range of assets, they can direct funds away from less profitable assets towards more profitable ones, spurring firms to maximise efficiency. The relationship between financialisation, competition and profits within health systems remains an open question. Finance may act as a mechanism for putting health care services in competition with other industries, potentially intensifying competitive pressures on health care services to be more efficient. In turn, competition can potentially impact the quality, accessibility, and stability of care.

One of the strengths of this work is its focus on the implications of financialisation for health system governance. Many articles reviewed cited at least one governance concern. Transparency and accountability concerns were common, and particularly the opacity of service ownership. There were also concerns regarding how democratic or participatory financialised services are, and whether they prioritise profitable services over services aligned with a state’s healthcare goals. More attention to these aspects of governance are required. The articles reviewed in this study argue that financialisation carries risk for health systems, including quality and accessibility of care, the diversion of public funds towards investors and regulatory capture. Case studies of policy successes and failures in addressing these risks would be valuable, both for scholars and policymakers. Studies on the integrity of financialised systems would help us understand how financial actors affect (or do not affect) the design and implementation of health system policies; or whether roles and responsibilities in governance are impacted. While studies of policy capacity might examine, for example, the technical expertise of governments in developing regulations to effectively mitigate the potential risks of financial markets and actors.

Overall, understandings of the role of the state in financialisation are underdeveloped. Articles in this review argued that states have enabled financialisation through policy reforms which expanded private healthcare markets, the use of private funds in public programme financing or by developing public–private partnerships with financialised services to deliver care (Applebaum and Batt, Reference Applebaum and Batt2021). While this is aligned with critical political economy theorists (Lapavitsas, Reference Lapavitsas2014), the question of why states enable health systems to become financialised remains open. This question is especially pertinent, given that the reviewed articles understand financialisation as a threat to health systems and their governance (Appelbaum and Batt, Reference Appelbaum and Batt2020; August, Reference August2021b; Bruch et al., Reference Bruch, Roy and Grogan2024; Hunter et al., Reference Hunter, McCoy, Cordilha, Marriott, Stein and Wood2025). There seems to be an interesting tension in the state’s role, which both relies upon financial investment to maintain or expand health systems while attempting to manage the challenges this creates. These dual, perhaps contradictory, motives could be explored using comparative policy studies. In particular, close examinations of the emerging regulatory efforts to mitigate the risks of financial investors within health systems (Tracey et al., Reference Tracey, Schulmann, Tille, Rice, Mercille, Timans, Allin, Dottin, Syrjälä, Sotamaa, Keskimäki and Rechel2025) could prove fruitful for understanding the role of the state in financialisation.

4.1. Limitations

First, this work derives from a critical interpretive synthesis, and the methodology used in this paper did not allow for a systematic review of all eligible papers (Dixon-Woods et al., Reference Dixon-Woods, Cavers and Agarwal2006). Given the level of saturation during data collection, we remain confident that our methods are robust and yielded a representative – if not exhaustive – sample of papers. Second, we have selected the TAPIC framework on health system governance (Greer et al., Reference Greer, Vasev, Jarman, Wismar and Figueras2019), which does not align with all possible definitions of governance important for this topic. However, the literature reviewed for this study consistently raised concerns that conformed to the TAPIC mode, which gives us confidence that the major implications of financialisation for health system governance are represented. Nevertheless, additional scholarship addressing the ways in which financialisation impacts health systems governance is welcome.

Furthermore, this review only included English language papers. Our search indicates that non-English scholarship on the financialisation exists and likely offers important insights into these processes within other contexts, especially in low- and middle-income countries. More work is required to fully appreciate the global implications of financialisation on health.

Finally, the papers included in this review were analysed with financialisation scholarship drawn from critical political economy. This is a broad field of study which assumes that power relations between different actors within society shape inequalities in social outcomes. We found that the articles reviewed here employ the term financialisation in ways similar to this literature. This does not invalidate claims that private financing and delivery of healthcare may achieve some of its objectives, including reducing the burden of public healthcare expenditures. However, a critical political economic framework can help interpret empirical evidence of risks associated with private financing, including threats to the democratic control over health systems, and help set an agenda for further evaluation.

5. Conclusions

Scholars have begun to theorise what it means for health systems to be financialised, and what implications this has for health system governance. These articles often draw on works of critical political economy on financialisation, and largely consider the negative consequences of this phenomenon. We agree with health system scholars that finance has transformed health systems, yet, based on our review, we argue that major theoretical questions still remain. Topics of further inquiry include the role of financial profits within health systems and their relationship to the ‘real’ process of service delivery and the role of monopoly power within these systems. We also require more empirical work, especially comparative approaches, assessing financialisation impacts the governance of health systems. The articles reviews here provide an excellent agenda for future research.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S1744133126100474.

Data availability statement

Not applicable

Acknowledgements

We would like to thank Kaitlyn Merriman for providing consultations when developing the original protocol. We would also like to thank Alexander Borsa for contributing to the initial search terms used for developing the search strategy. An earlier version of this work was presented at the North Americas Meeting of the European Health Policy Group. We would like to thank the participants for their feedback on that earlier draft.

Authors’ contribution

MT conceptualised the original formulation of the research goals and aims of this protocol. MT and SA contributed to the methodology. MT prepared the original draft of this manuscript, and administered the project. All authors reviewed and edited each version.

Financial support

This work was supported by a Catalyst and Research Development Grant from the Institute for Pandemics, University of Toronto (Principal Investigator: Teresa Kramarz). The funders had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript.

Competing interests

The authors declare that they have no competing interests.

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Open access

Open access