The Agrarian Challenge in Rwanda

Multilateral development policy assumes that rural livelihoods can be improved through supporting projects that facilitate improvements in the security and productive base of smallholder farmers (Harrison Reference Harrison2001). Lipton’s (Reference Lipton and Harriss1982) arguments informed these approaches. He popularised the idea that there was an inverse relationship between farm size and productivity. Assumptions that smaller farmers are more productive than larger farmers also exist within the Marxian-inspired literature on agrarian change. Chayanov (Reference Chayanov1986) was among those who argued that under pre-capitalist conditions, small peasants resorted to self-exploitation, where family farms did not count the costs of their own labour, and farmed their own plots more intensively than capitalist farmers despite their lower labour productivity. Many scholars, regardless of their ideological persuasion, often rely on idealised notions of ‘small farmers’ and ‘cooperatives’ referring to homogeneous actors, with less recognition of the inequalities that may be obfuscated as a result.

IFIs, certification standards firms (such as Fair Trade or Rainforest Alliance), trading companies and retailers propose policies and present ‘feel good’ stories aimed at empowering cooperatives. These cooperatives are usually presented as comprising poor ‘small farmers’ who produce food or cash crops for domestic and international markets. These policies assume cooperatives to be homogeneous groups, with benefits being redistributed equally to members who have similar wealth and own similar sizes of land. However, imagined categories of ‘small farmers’ and ‘cooperative members’ do not represent the realities of rural African households (Cramer & Pontara Reference Cramer and Pontara1998; Sender & Johnston Reference Sender and Johnston2004). Cooperatives are often controlled by elites and prone to corruption. The imagined category of ‘small farmers’ does not include the poorest rural people who depend on wage work to meet subsistence (Cramer et al. Reference Cramer, Oya and Sender2008; Oya Reference Oya2013).

The focus on the plight of imagined groups of ‘small farmers’ is mirrored in the scholarly debate about Rwanda’s agrarian transformation. Ansoms et al. (Reference Ansoms2008) even directly employed Lipton’s arguments to show that Rwanda’s small farmers are more productive than larger farms. Scholars criticise the RPF’s focus on ‘larger’ farmers or commercialised farming, arguing that the RPF’s interventions are primarily motivated by the goal of extending control over rural society (Ansoms Reference Ansoms2008; Newbury Reference Newbury, Straus and Waldorf2011; Van Damme et al. Reference Van Damme, Ansoms and Baret2014). They highlight that the RPF’s prioritisation of cooperative formation is motivated by the goal of engineering control grabs and institutionalising control over society through top-down policymaking (Huggins Reference Huggins2017). A large share of the agrarian studies literature romanticises farmer resistance against RPF reforms (Ansoms et al. Reference Ansoms, Wagemakers, Walker and Murison2014, Reference Ansoms, Cioffo, Dawson, Desiere, Huggins, Leegwater, Murison, Bisoka, Triedl and Van Damme2018), arguing that coercive policies have detrimentally affected the agency of small farmers. Others have defended RPF rural policies (Booth & Golooba-Mutebi Reference Booth and Golooba-Mutebi2014b), arguing that they have resulted in benefits for ‘small farmers’. Those who have been positive about Rwanda’s agrarian transformation (Booth & Golooba-Mutebi Reference Booth and Golooba-Mutebi2014b; Harrison Reference Harrison2016) have based their judgments on what appeared to be impressive agriculture production data, which was later shown to be vastly overestimated (Heinen Reference Heinen2022).

This focus on the plight of ‘small farmers’ has misdirected analysis of the kind of agrarian transformation being achieved and how the RPF has managed to contain the threat posed by rural resistance. Agrarian transformation has resulted in significant inequality but increased diversification in agricultural production. Rural resistance has not been mobilised into a larger threat because intermediate classes or other groups that could finance or unite collective grievances remain disorganised.

For most of Rwanda’s history, more than 80 per cent of the population has been employed in agriculture. In 2023, Rwandan government statistics reported that only 64.4 per cent of the Rwandan workforce was employed in agriculture (NISR 2024). Agriculture is where most of Rwanda’s population is employed. For at least the last three decades, the average landholding in rural Rwanda has gradually decreased from 2 hectares in 1960 to less than half a hectare in the 2010s (Jayne et al. Reference Jayne, Yamano, Weber, Tschirley, Benfica, Chapoto and Zulu2003; Musahara Reference Musahara2006; Pritchard Reference Pritchard2013; Sagashya & English Reference Sagashya and English2009). Rwanda’s rural sector has long been characterised by its small landholdings, high population density, low-productivity technologies and low incomes. However, Rwanda’s rural communities are not ‘stable timeless collectives but rather mixtures of new and old social ties tenaciously trying to find modes of livelihood in the midst of enduring social trauma’ (Harrison Reference Harrison2016, p. 365).

This chapter examines how the RPF has sought to reorganise rural society, ensuring any rural resistance is contained while also reorganising agrarian accumulation. In 1994, the RPF assumed power in a relationship of mutual distrust with the rural population. The reorganising of rural society has often been characterised by rural resistance to the RPF’s agrarian policies (Ansoms Reference Ansoms2009; Huggins Reference Huggins2009; Ingelaere Reference Ingelaere2014; Van Damme et al. Reference Van Damme, Ansoms and Baret2014). However, the RPF has not only contained social unrest but also adapted its policies on occasion to respond to the demands of rural producers. Yet the government has shown itself to be caught between priorities: of finding new agriculture exports while failing to combat food insecurity and rural inequalities. The clearest evidence of this is that while non-traditional agriculture exports increased significantly, food inflation soared recently (with Rwanda among the top ten countries worst hit by food inflation in 2023). A 2021 national survey listed food insecurity at 21 per cent. Since the pandemic, food inflation has increased between 10 and 25 per cent between November 2022 and 2024, particularly for dairy products and vegetables, likely making more people food insecure (Kagina Reference Kagina2023a; NISR 2021). Despite pre-1994 governments’ peasant-centred ideologies, they also failed to deal with food insecurity (Newbury & Newbury Reference Newbury and Newbury2001; Pottier Reference Pottier2002).

This chapter begins by outlining the nature of agrarian vulnerabilities in Rwanda, based on the large and growing scholarship on Rwanda’s agriculture sector (Ansoms Reference Ansoms2009; Ansoms et al. Reference Ansoms, Cioffo, Dawson, Desiere, Huggins, Leegwater, Murison, Bisoka, Triedl and Van Damme2018; Huggins Reference Huggins2017; Illien & Bieri Reference Illien and Bieri2024). Increased land differentiation and rural inequality has characterised RPF rule. In subsequent sections, it highlights how the RPF has embarked on a strategy of diversifying agricultural exports. This includes upgrading traditional coffee and tea exports to extract higher revenues domestically and investing in new agricultural exports. There has been some success in this regard, with the government or government-affiliated companies (sometimes in partnership with foreign investors) usually being the key partners. This is in line with the broader elite vulnerability characterising Rwanda’s political settlement and has meant that structural transformation remains elusive (especially since few firms have acquired technological capabilities to be internationally competitive). The chapter highlights that the government has sustained political order because few actors have the capacity to finance and mobilise domestic grievances into collective action against the RPF. There are doubts about the veracity of agriculture statistics in Rwanda (Desiere et al. Reference Desiere, Staelens and D’Haese2016; Heinen Reference Heinen2022). There are also inconsistencies in Rwanda’s official agriculture export statistics. Where relevant to the overall argument, these data inconsistencies are mentioned.

Agrarian Vulnerabilities and Possibilities in Rwanda

RPF leadership has embarked on an ambitious agricultural reform strategy, which included a new land law and a market-oriented crop intensification programme (CIP). RPF officials initially reasoned that low agricultural productivity was because of the small size of holdings, dispersed settlement patterns and the scattered nature of cultivation (Des Forges Reference Des Forges, Reyntjens and Marysse2006; GoR 2000). According to some, the RPF government primarily intended ‘to get more people off the land’ (Ansoms Reference Ansoms2009, p. 300) and pioneer a shortcut to development that would bypass peasant agriculture.

In 1994, we did not see farming and agriculture as our area. Many didn’t trust us. We knew it. But we know that without agriculture, there will be no future for Rwanda. So we knew we had to do big changes. We couldn’t make the same mistakes as others. We had to fully transform our agriculture and even now, that is still in process.Footnote 1

RPF policies echo the advice of IFIs and donors but also depart from it in some ways: retaining significant control over prioritising production of certain food groups, managing land tenure closely (and sometimes through direct ownership of land through the military or the government) and exporting higher-value cash crops (coffee, tea, pyrethrum) rather than exporting unprocessed agricultural commodities. These reforms formalised and individualised property relations. Before these decisions, population increases had exacerbated land fragmentation and reduced the average size of holdings. Increasing fragmentation of land holdings led to conflict over land and a growing landless class (Musahara Reference Musahara2006). Publicly, the RPF claimed that establishing a formal system of land rights was a way to avoid conflict and promote agricultural transformation. Such decisions were based on the reasoning that decreasing agricultural output was due to informal land tenure systems and subsistence production (Pritchard Reference Pritchard2013). The government abolished every form of customary tenure through land laws, encouraging families to cultivate land in common rather than through inheritance, and retained the right to confiscate land if subsistence farmers were not exploiting it efficiently (Pottier Reference Pottier2006).Footnote 2 The government also established a land tenure regularisation system in 2009, which was among the most low-cost and ambitious interventions of its kind worldwide (Ali et al. Reference Ali, Deininger and Goldstein2014). By 2014, 10.6 million parcels had been demarcated (85 per cent with full information); only 1.6 million parcels had not been assigned.Footnote 3 These processes have also resulted in conflicts (Ansoms et al. Reference Ansoms, Wagemakers, Walker and Murison2014; Pritchard Reference Pritchard2013). For a period, elites gained control over large land areas, especially in the Eastern Province (Musahara & Huggins Reference Musahara, Huggins, Huggins and Clover2005). Initial ‘land grabs’ took place in the 1990s and the early 2000s. Critics (Ansoms et al. Reference Ansoms, Wagemakers, Walker and Murison2014) acknowledged that such practices have been monitored. By the 2000s, as the RPF began to centralise control over the distribution of rents and political decision-making, some of these elites faced legal measures. In doing so, the RPF showed its public commitment to containing land accumulation by individual RPF elites.

In 2008, land consolidation was introduced to prevent further fragmentation of land. Land consolidation was designed to ensure farmers received benefits of scale ‘in conservation measures, input utilisation and harvesting without undermining the principles of family land ownership and individual cultivation’ (Booth and Golooba-Mutebi Reference Booth and Golooba-Mutebi2014b, p. S187). Under this programme, farmers retained ownership over their land but joined cooperatives and undertook synchronised planting and harvesting of certain crops. The land consolidation programme also aimed at achieving food security. Concerns over food security were confirmed when Rwanda’s 2006 Comprehensive Food Security and Vulnerability Analysis listed 52 per cent of households (43 per cent rural, 9 per cent urban) as food insecure or vulnerable. The CIP was introduced to address such concerns. Farmers, who opted to join, worked on consolidated plots and were organised into cooperatives. The government provided agriculture inputs, with extension services organised through cooperatives. Six priority food crops were identified (maize, wheat, rice, Irish potato, cassava and beans). There is some disagreement about whether farmers could join voluntarily or whether they were forced to join cooperatives (Ansoms et al. Reference Ansoms, Wagemakers, Walker and Murison2014; Kathiresan Reference Kathiresan2012). Cooperatives became arenas of political contestation, since membership came with benefits in accessing inputs and extension services (Huggins Reference Huggins2014). Government officials acknowledged that cooperative leaders may wield too much power in cooperatives but highlighted that they did their best to minimise any negative impact:

The influence some cooperative leaders have over cooperatives can tilt things in their favour. Sometimes, these people can keep the profits for themselves. Other times, they help farmers in seeing benefits. We want to edge out the corrupt managers and make sure cooperatives work for all members.Footnote 4

Cooperatives were organised within the Rwanda Cooperative Agency (RCA), which was established in 2008. By 2012, 4,600 cooperatives had officially registered. Positive interpretations of Rwanda’s agrarian transformation were associated with land consolidation and the portrayal of significant productivity gains. Later, it became clear that these statistics were exaggerated. Some scholars (Desiere et al. Reference Desiere, Staelens and D’Haese2016; Heinen Reference Heinen2022) have highlighted that food production stagnated between 2005 and 2018, with a significant overestimation of production volumes and yields of key food crops. Literature on Rwanda’s agriculture sector (Heinen Reference Heinen2022), though highlighting the overestimation of food production, acknowledged the immense efforts of the state in increasing yields and productivity. More recently, the government has claimed that there have been significant increases in the production of several food crops (including as an export). However, about 20 per cent of Rwandans are still estimated to be food insecure (WFP 2024). The RPF government’s agrarian transformation strategy focused on land consolidation, as well as empowering groups of ‘small farmers’ through joining cooperatives. However, this obscures processes of land differentiation that persist in rural areas.

The existence of a landless population (or a population that requires access to wage work to meet subsistence) has been recognised within the academic literature on Rwanda (De Lame Reference De Lame2005; Illien Reference Illien and Bieri2024). Government documents (MINECOFIN 2002) and scholarly work (Ansoms Reference Ansoms2010; Lemarchand Reference Lemarchand2013; Sommers Reference Sommers2012) have detailed differentiation in the rural areas, particularly in terms of how individuals are viewed by others in relation to their control over means of production. Ubudehe Public Works programmes also recognise the existence of landlessness. Ubudehe initially listed six categories, including rural Rwandans who do not own a field or land and work on farms to gain wages to survive.Footnote 5

In 2002, national surveys indicated that 11 per cent of all households were landless, while another 70 per cent of households owned plots less than 1 ha (Musahara Reference Musahara2006). Women, widows and children headed around 43 per cent of vulnerable households (MINECOFIN 2007). In 2012, the government recognised that poverty was highest (76.6 per cent) among households that obtained half their income from farm wage work, followed by those with diversified livelihoods who obtained more than 30 per cent of their income from farm wage work (MINECOFIN 2013). Many Batwas (the third ethnicity in Rwanda) are also landless (Beswick Reference Beswick2011). The trend of rural differentiation has continued, with recent studies highlighting that land inequality is increasing while there was also evidence of worsening landlessness (Bird et al. Reference Bird, Chabe-Ferret and Simons2022; Illien & Bieri Reference Illien and Bieri2024).

The government has not succeeded in resolving food insecurity or in creating sufficient employment opportunities. The CIP was intended to achieve that. Existing literature has blamed the CIP’s failures on coercive state policies, as well as the rigidity with which such policies have been implemented and the incentives to overestimate achievements within the performance contract (imihigo) system (Ansoms et al. Reference Ansoms, Cioffo, Dawson, Desiere, Huggins, Leegwater, Murison, Bisoka, Triedl and Van Damme2018; Heinen Reference Heinen2022). The rest of this chapter highlights the progress made by the government in diversifying its agricultural exports while also upgrading primary commodities. Yet this progress has been marked by increased rural differentiation and inequality. Success has been shaped by Rwanda’s evolving political settlement, with heavy reliance on RPF-affiliated investments for the most ambitious upgrading attempts but reduced evidence of domestic capitalists being integrated in such strategies.

Reorganising Rural Society for Processing Traditional Primary Commodities

The primary concern of the GVC/GPN literature is analysing economic upgrading strategies in developing countries. Economic upgrading focuses on the possibilities for firms in developing countries to move into higher-value activities in GVCs to gain more revenues for the products they produce. The literature discusses four types of economic upgrading: process upgrading (inputs are transformed into outputs by reorganising the production system and introducing technology), product upgrading (moving into more specific product lines), functional upgrading (acquiring new functions to increase the skill content of activities) and chain or inter-sectoral upgrading (moving into new but related industries) (Humphrey & Schmitz Reference Humphrey and Schmitz2002).

For centuries, colonial administrations and then foreign trading companies have extracted raw materials from former colonies. Companies outside the countries where the products were extracted or produced have extracted most of the revenues from commodities. As GVCs have become increasingly fragmented and dispersed in recent decades, the task of capturing more of the value of exported products has become more difficult for firms in developing countries. The desire of Global South countries to capture more of the value of products they export seems logical and fair. Where governments prioritise upgrading, they tend to argue that farmers would automatically receive a fairer price. However, even successful upgrading strategies rarely result in equitable benefits for all farmers (Neilson Reference Neilson2008). Process upgrading requires increased efficiency of production processes and adherence to standards. Product and functional upgrading require firms to have technological capabilities and access to markets while also being competitive against producers elsewhere. Consequently, actors with better resources are better placed to invest in technological capabilities to meet standards and access higher-value markets (Cramer et al. Reference Cramer, Johnston, Mueller, Oya and Sender2017; Whitfield Reference Whitfield2017).

The RPF government’s priorities within the agrarian sector have been to invest in increasing productivity within agriculture, diversify its domestic food production with the aim of exporting food (through specialisation in specific crops) and reduce dependence on the export of unprocessed coffee, tea and other agricultural exports that are vulnerable to fluctuations in global prices. The RPF has achieved progress in upgrading its coffee and tea exports (and being less dependent on global market prices). Though the scale of this progress may not be accurately presented in data, there have been significant achievements in terms of upgrading. Additionally, the RPF government has invested strategically in high-value agriculture exports, which show characteristics of industrial goods or what Cramer and Sender (Reference Cramer, Sender, Kanbur, Noman and Stiglitz2019) describe as the ‘industrialization of freshness’. The RPF has also been very successful recently in exporting food crops to neighbouring markets in the DRC. The government drove investment into upgrading and diversification by first providing loans and incentives to closely affiliated private businesspeople. Later, this reliance on private businesspeople shifted to an increasing reliance on state-owned or party-owned enterprises sometimes in partnership with foreign investors, aligning with the increased elite vulnerability shaping the political settlement. In the cases that individual businesspeople have become prominent, they are either in partnership with the government or in joint ventures with foreign investors.

On the surface, there is much to be positive about Rwanda’s agrarian transformation since 1994. However, this success has been based on the government tapping into the ‘quality’ narratives of high-end consumer markets, based on idealised images of ‘small farmers’ and ‘cooperatives’, which have masked the inequality that has characterised agrarian transformation. Crucially, for the multi-scalar analysis presented here, global certification standards and the policy suggestions of donors have contributed to structuring that inequality rather than combating it. The upgrading strategy evolving in the sector presents a significant political challenge for the RPF, particularly since employment has not been found elsewhere in the economy (in manufacturing or through its services-based hub strategy).

Coffee

The Rwandan economy has heavily depended on coffee exports for most of its independent history. The RPF government’s paradigmatic ideological goals of achieving self-reliance are inextricably linked to reducing the economy’s reliance on fluctuations of global international coffee prices. Since 1994, the Rwandan government has achieved some success in promoting the reputation of Rwandan coffee in specialty markets and has also achieved substantial progress in reducing the proportion of Rwandan coffee sold in semi-processed and low-value forms. Rwanda’s success has been discussed in academic literature and the international press (Boudreaux Reference Boudreaux, Chuhan-Pole and Angwafo2011; Easterly & Reshef Reference Easterly and Reshef2010; Gambino Reference Gambino2018). However, as will be shown in this section, success has been characterised by state support and benefits for some but coercion and inequality for others. When the government has made its most risky upgrading investments, it has done so through state finance (with support from foreign charitable foundations).

Unlike Brazil, Ethiopia or Vietnam – countries that comprise a large share of global coffee production – Rwanda has never produced more than 1 per cent of global coffee production. Thus, even in its traditionally most important export sector, Rwanda remains a ‘price taker’ in relation to the global economy. Coffee and other primary commodities (tea and minerals) have traditionally comprised over 90 per cent of Rwanda’s exports. The first two independent Rwandan governments used coffee and other primary commodity sectors as avenues through which rents were distributed to their allies. Consequently, revenues obtained from the sector became a source of political contestation. In Kayibanda’s case, a marketing board (TRAFIPRO) was the avenue through which coffee revenues were controlled. Habyarimana abolished TRAFIPRO when he assumed power. He replaced it with a monopsony coffee-export agency – Rwandex. For most of Habyarimana’s reign, Rwandex exported around 80 per cent of domestically produced coffee. As coffee prices began to fall in the early 1980s, the government responded to its widening trade deficit by placing more emphasis on coffee cultivation rather than prioritising diversification. The 1978 law on coffee cultivation made the neglect of coffee trees punishable by law. When coffee prices fell again in 1985, the area of land under coffee cultivation increased and yield dropped significantly, with evidence of increasing resistance to forced coffee cultivation (Verwimp Reference Verwimp2013). Both pre-1994 governments developed peasant-centred ideologies, where coffee occupied a prominent role in nationalist rhetoric, with Habyarimana calling on farmers to grow coffee for the good of the nation (Verwimp Reference Verwimp2013). In Habyarimana’s speeches, he linked the external threat of ‘Tutsi invaders’ to the interests of pastoralists, which he cast as contradictory to the interests of Hutu farmers (Verwimp Reference Verwimp2000).

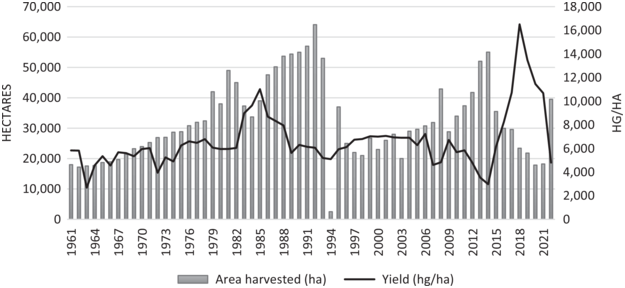

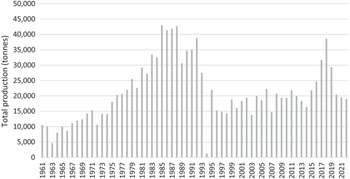

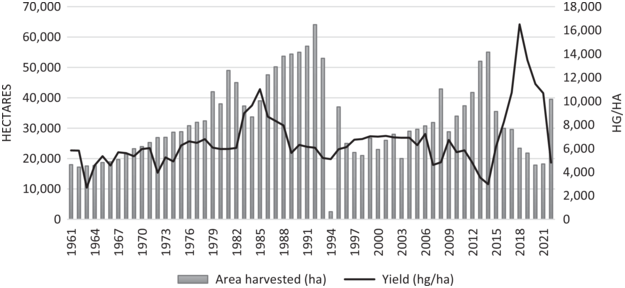

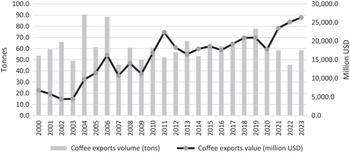

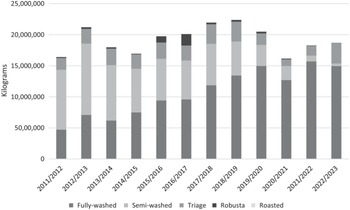

The RPF government has made significant progress in transforming its coffee sector. Most coffee produced and exported in Rwanda was traditionally unprocessed, semi-washed or broken beans (triage) varieties. Coffee production is much lower than it was in the 1980s (Figure 6.1). The area under coffee cultivation has reduced, but the value of coffee exports has increased over time (Figures 6.2 and 6.3). This suggests progress in process and product upgrading. This is evidenced further in Figure 6.4, which shows that the proportion of fully washed Rwandan coffee exported has increased from virtually nothing in 2000 to over 80 per cent in 2023. This has been achieved through the government’s interventions in ensuring increases in the amount of coffee processed domestically in washing stations and through developing relationships with a range of buyers of specialty coffee worldwide. The government has also invested in the marketing of Rwandan coffee abroad through participation in Cup of Excellence events and direct engagement with leading coffee retailers (like Starbucks). The government has also been innovative in encouraging the domestic production of new varieties of coffee (Figure 6.5). Taking advantage of growing international demand, Rwanda has begun to export honey, cascara and naturally produced coffees, which offer higher prices and are less vulnerable to global coffee price fluctuations.

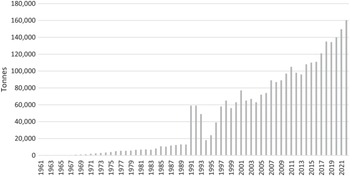

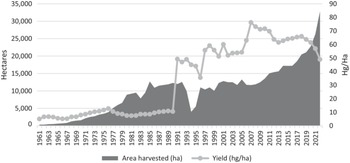

Total Rwanda coffee production: 1961–2022.

Area harvested and yield of Rwanda’s coffee production: 1961–2022.

Rwanda coffee exports volume and value: 2000–2023.

Rwanda coffee production by type: 2011/2012–2022/2023.

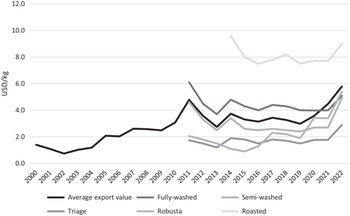

Rwanda coffee prices by type: 2000–2022.

In contrast to some GVC understandings (Gereffi Reference Gereffi1999), success has not been achieved purely by engaging with lead buyers. Instead, the RPF government’s progress has been characterised by state intervention, trial-and-error and engaging with a wide range of buyers and selling coffee in a range of different markets. Strikingly, though the government has encouraged the formation of cooperatives, these cooperatives show signs of ‘control grabs’ where the richest cooperative members control decision-making in the cooperatives and keep most of the profits (Huggins Reference Huggins2017). The broader transformation of the coffee sector highlights unequal outcomes for producers, both within cooperatives and among producers who sell coffee to different markets (Clay et al. Reference Clay, Bro, Church, Bizoza and Ortega2018). As Figure 6.5 shows, Rwanda’s upgrading strategies have resulted in specialty coffee (or fully washed coffee) and roasted coffee being sold at higher prices than semi-washed or triage coffee.

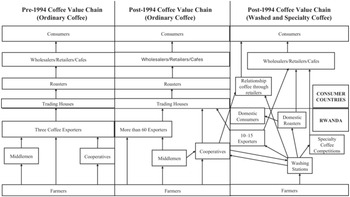

The RPF government’s upgrading attempts have been successful through reorganising how coffee producers engage with international markets. Figure 6.6 highlights the reorganisation of the coffee value chain in Rwanda. The remaining part of this section will first describe how the process to produce higher-value coffee has been characterised by coercion and unequal outcomes. It will then show how the RPF government first began reforming the sector through partnering with closely affiliated businesspeople but now largely depends on foreign-owned companies or government-owned companies (particularly for its most ambitious attempts at upgrading). These characteristics of Rwanda’s agriculture reforms are aligned with broader national dynamics. These shifts include the increasing reliance on RPF-affiliated firms and foreign investors rather than domestic capitalists. Similar dynamics also exist in other sectors.

Rwanda’s pre-1994 and post-1994 coffee value chain.

Figure 6.6 Long description

Three side-by-side flowcharts illustrate how the coffee value chain changed from pre-1994 to the post-1994 period. Each column shows the path coffee takes from farmers to consumers, with boxes and arrows indicating actors and movement of coffee.

Left column: Pre-1994 Coffee Value Chain, Ordinary Coffee.

At the bottom are Farmers, who sell coffee either to Middlemen or Cooperatives. Both groups feed into Three Coffee Exporters. Exporters supply Trading Houses, which then supply Roasters. Roasted coffee moves to Wholesalers, Retailers, World Shops, and Cafés, and finally to Consumers. The chain is linear and centralized.

Middle column: Post-1994 Coffee Value Chain, Ordinary Coffee.

Farmers still sell to Middlemen and Cooperatives, but instead of three exporters there are more than 60 exporting companies. These feed into Trading Houses, then Roasters, then Wholesalers/Retailers/Cafés, and finally Consumers. The chain is expanded but still largely linear.

Right column: Post-1994 Coffee Value Chain, Washed, Specialty, Relationship Coffee.

At the base are Farmers, who sell their coffee to Washing Stations. From here, coffee may go to 10–15 exporting companies, Cooperatives, or directly toward specialty channels. Arrows show multiple parallel pathways, Washing stations supply Domestic Roasters, which sell to Domestic Consumers, Specialty pathways link washing stations and exporters to Cup of Excellence/Specialty Coffee Competitions, Relationship coffee channels connect producers directly to Retailers and then to Consumers in Consumer Countries, Trading houses still interact with some exporters and retailers.

Inequality amid Upgrading

Until about 2000, most coffee exported from Rwanda was unprocessed. In 2000, there were just two CWS. As of 2023, there were 312 CWS. Government officials closely managed the reorganisation of domestic coffee production, punishing farmers who resisted sending coffee cherries to CWS. The military, RSSB and donor-supported cooperatives invested in the construction of the first washing stations, creating a demonstration effect for other investors (Behuria Reference Behuria2020). However, the government also faced resistance from existing coffee exporters who had long-standing relationships with coffee producers and middlemen (who acted as conduits between farmers and exporting companies). In this way, the RPF initiated a significant break from the production structures that had shaped the financing of pre-1994 political settlements, altering domestic coffee production and finding new buyers for Rwandan coffee.

Changing production systems domestically and constructing CWS was a crucial initial task. The strategy to construct CWS evolved in a haphazard way. By the mid-2010s, several were largely defunct, while a few CWS were receiving more coffee cherries than they could process. In 2016, the government – through its National Agriculture Export Development Board (NAEB), a government department responsible for overseeing the governance of the coffee, tea and horticulture sectors – implemented a zoning policy with farmers required to sell coffee to designated washing stations (Gerard et al. Reference Gerard, Clay and Lopez2017). NAEB has maintained a minimum price at which CWS have to buy coffee cherries (and CWS often pay a premium). Gradually, the government has encouraged the privately run Coffee Exporters and Processors Association of Rwanda to assume responsibility over the distribution of pesticides and fertilisers to farmers.

Sustainability initiatives – like Fairtrade, Rainforest Alliance and Utz Kapeh – have been central to promoting the growth of specialty coffee markets, with certification standard companies occupying ‘a flagship position in value chain organization’ (Grabs Reference Grabs2020a, p. 363). Nearly all ‘specialty coffee’ is sustainably certified, with numerous certification schemes emerging as prominent private governance actors within the GVC/GPN (Giovannucci & Ponte Reference Giovannucci and Ponte2005). A growing trend of ‘relationship coffee’ has also emerged where roasters/retailers engage in direct trading relationships with coffee producers, bypassing traditional certification and mobilising quality tropes (Vicol et al. Reference Vicol, Neilson, Hartari and Cooper2018). This is often referred to as the ‘Third Wave’ of global coffee markets, with more direct trade, as well as increased emphasis on sustainability and innovative methods, linking farmers to retailers more directly. Part of the ‘Third Wave’ changes in the global coffee markets have contributed to the importance of presenting ‘feel good stories of how coffee is produced in a globally competitive market’.Footnote 6 This has also contributed to increasing global demand for honey, naturally produced, cascara and other specialty coffees, which Rwandan exporters and farmers have begun to tap into.

The variety of relationships between producers, traders and roasters within the coffee GVC/GPN may suggest the sector is characterised by ‘multipolar governance’ (Ponte & Sturgeon Reference Ponte and Sturgeon2014). Grabs (Reference Grabs2020b) has recently shown that roasters and retailers like Nestlé and Starbucks have rolled out their own certification schemes, highlighting how retailers and roasters are now increasingly in direct competition with one another. Buyers of specialty coffee – as well as all sustainability initiatives – only source coffee from cooperatives. Yet only 8.2 per cent of Rwandan coffee producers were cooperative members in 2006, and, by 2015, this had only increased to 14 per cent (NAEB 2016; OCIR-Café 2009). This highlights another clear inequality in Rwanda’s coffee upgrading strategy, with only a small proportion of coffee farmers being able to gain the benefits of exporting to specialty coffee markets. Though ‘multipolar governance’ characterises the coffee GVC and it creates increased opportunities for some countries and firms to access specialty markets, ‘specialty’ standards only apply to those farmers with comparatively more resources, who can meet minimum standards of farm sizes and qualities. Even within cooperatives, not all members benefit equally. Huggins (Reference Huggins2014) cites several examples where better-resourced farmers establish cooperatives to engineer ‘control grabs’, gaining a large share of the profits.

There are numerous examples of how the government has worked with foreign buyers to directly engage with Rwandan coffee cooperatives. The Abahuzamugambi cooperative, which was founded in 1999 and was supported by USAID, found a market for specialty coffees through UK-based Union Coffee Roasters and US-based Community Coffee. Their coffee is bought at premiums and exported as single-source/traceable coffee, selling at retailers, including Whole Foods, Intelligentsia Coffee and Third Rail Coffee in New York (Easterly & Reshef Reference Easterly and Reshef2010). Starbucks-supported Rwashoscco operates as a marketing alliance, with members retaining their own brands. Members keep all profits, except for a commission paid to Rwashoscco (Heinen Reference Heinen2023). Starbucks facilitated Rwashoscco and its members in developing direct relationships with foreign buyers, particularly in the US markets. American NGO Sustainable Harvest partnered with cooperatives of female coffee farmers to sell their high-value coffee in the United States. US-based Peet’s Coffee’s limited edition 2018 Annual Blend of Rwandan coffee was produced by a female-only cooperative of coffee farmers with the promise that 5 per cent of proceeds would provide clean water to Rwandan coffee producers.

Such examples highlight how certain Rwandan coffee cooperatives have successfully gained benefits from Rwanda’s progress in accessing specialty markets and comparatively higher prices than the global market price. Yet, as previous sections have shown, this has occurred within a broader environment of increased rural differentiation. Since domestic roasters can only partner with a small number of cooperatives because of limited sales, only a small segment of farmers benefits from such initiatives.

Evolving Capitalist Partners

Before the RPF assumed power, a single marketing board (TRAFIPRO) and then a monopsony export company (Rwandex) were responsible for organising the production and managing the export of coffee to a small number of European buyers. For most of Habyarimana’s reign, Rwandex exported around 80 per cent of domestically produced coffee. The government exported about 15–18 per cent via its coffee agency, OCIR-Café (which later became NAEB). Etiru, a small Belgian company, exported the remainder. Rwandex was a public–private partnership: the government owned 51 per cent and the other shares were divided between British investors (Carr Reference Carr1999). Rwandex sold its exports to British-based Drucafe, as did OCIR-Café, while Etiru sold only to Sobelder in Belgium (Ngabitsinze et al. Reference Ngabitsinze, Mukashema, Ikirezi and Niyitanga2012). In comparison, in 2023, Rwandan coffee was exported to over thirty countries, though more than 50 per cent of its coffee was exported to Switzerland, the United Kingdom and Finland (NAEB 2023).

When the RPF government assumed power in 1994, transforming the coffee sector and becoming less reliant on exporters and farmers, who were perceived to have participated in the genocide, was a priority.Footnote 7 In January 1995, the government ‘opened up’ the sector to private (both local and foreign) investors. There was a sharp turnover within the sector, as exporting companies entered and disappeared rapidly. In 2000, for instance, there were only four exporting companies (Schluter & Finney Reference Schluter and Finney2000). Swiss-based RwaCof, owned by Sucafina, entered Rwanda in 1995 and captured significant market share, partly because of its foreign contacts. Rwandex’s market share was under increasing threat from new entrants, but it remained a significant player, with about 65–75 per cent of the domestic market in the early 2000s. As with the first investments in washing stations, some closely affiliated domestic capitalists like Faustin Mbundu and Hatari Sekoko also established exporting companies.

As liberalisation continued, there was growing friction between exporting companies that prioritised traditional production (including the export of unprocessed coffee) and closely affiliated export companies, which prioritised buying washed coffee from CWS. After one of the Rwandex owners’ deaths in the early 2000s, Scott Ford, an American billionaire, bought Rwandex in 2009 and stated his intention to export only fully washed coffee to the United States. The entry of new exporting companies was crucial in strategically shifting Rwanda’s coffee exports from unwashed to washed coffee and linking with new international roasters and retailers. In the mid-2010s, there were over sixty exporting companies (including cooperatives and military-owned companies) operating in Rwanda. There was significant consolidation in the sector with six companies exporting over 70 per cent of Rwanda’s coffee. This trend has continued with a significant turnover in exporting companies in the 2020s but consolidation of control among a few exporting companies.

All of Rwanda’s most ambitious attempts at upgrading – whether through exporting packaged coffee or establishing retail cafes in Rwanda and abroad – were led by government-owned or party-owned firms. In Table 6.1, Rwanda’s attempts at upgrading are summarised. RPF-owned Bourbon Coffee established the first coffee outlets in Kigali. Bourbon Coffee was established in 2006 by Arthur Karuletwa – a Rwandan who moved to America in 1995 and worked for Procter & Gamble, and then for the Rwandan government, including as a consultant at OCIR-Café. Bourbon initially aimed to be the ‘Starbucks of Rwanda’. Bourbon has three stores in Kigali and initially had one each in Washington, DC, New York, Boston and London. Since then, its American operations have expanded, but the London coffee shop has shut down. Bourbon’s investments were a demonstration effect to others, with seventeen new coffee shops established across Rwanda by others. Other prominent coffee shops include Mauritian–Rwandan-owned Brioche and Kaizen’s Neo.

| Upgrading strategy | Type of upgrading | Role of the state | Economic partners |

|---|---|---|---|

| Coffee washing stations | Process and product upgrading | Initially, state was a producer but later shifted to regulator and facilitator. | Initially, the military, state-owned institutions like Rwanda Social Security Board and donor-partnered cooperatives. |

| Liberalisation of exports | Contributed to process and product upgrading | Active facilitator; strategic liberalisation to attract more exporters who would export washed and specialty coffee. Later, exporters tapped into other specialty markets (such as honey, cascara and natural coffee). | Select cooperatives that have now developed links with foreign traders and roasters. Some donor-funded cooperatives ran into difficulties once donor funding ended. |

| Cooperatives’ links to foreign roasters/retailers | Process and product upgrading | Active facilitator (in partnership with donors and leading roasters like Starbucks, Peet’s Coffee). | Select cooperatives that have developed links with foreign traders and roasters. |

| Coffee marketing campaigns | Contributed to product upgrading (moving into specialty coffee); functional upgrading | Active facilitator; also a producer through establishing Cup of Excellence competitions. | The government has engaged in marketing Rwandan coffee, along with some donors like USAID and international roasters. |

| Entering retail markets domestically and globally | Functional upgrading | Producer through party-affiliated investment. | Party-affiliated Bourbon Coffee (part of Crystal Ventures Ltd); acted as demonstration effect for other domestic coffee retailers. |

| Roasting coffee for domestic and export markets | Functional upgrading | Producer through toll-roasting abroad and then through RFCC. | Government established RFCC (in partnership with philanthropists). |

Donors have been reluctant to support functional upgrading. Instead, donors like USAID, have prioritised supporting partnerships with lead firms while helping organise cooperatives to access international markets. However, the government has long been cognisant that roasted coffee will ‘at a minimum, provide double what even specialty coffee offers’.Footnote 8 As a result, the government took the lead in investing in roasting coffee. By 2009, there were six main coffee roasters. By 2018, there were eighteen roasters. Some roasters are individual Rwandan capitalists (although their investments are small). Some are foreign investors, targeting ‘interstices’ (Ponte Reference Ponte2002) within the coffee value-chain, selling its coffee in Middle Eastern and Ugandan supermarkets. As a major strategic investment within the coffee sector, the government – through NAEB and BRD – has worked with partners, the Clinton Hunter Development Initiative (CHDI) and the Hunter Foundation, to create a coffee company – the Rwandan Farmers Coffee Company (RFCC) – and invested in a $3 million coffee-processing factory in Kigali. The day-to-day management of RFCC is managed by government employees, but the RFCC benefits from technical expertise and networks, supported by CHDI and the Hunter Foundation. RFCC sources coffee directly from government-selected cooperatives. In 2015, the RFCC began operations and started producing under the brand Gorilla’s Coffee, selling to local, African, Asian and European markets. By 2020, RFCC was exporting coffee to the United Kingdom, Germany, South Korea and the United States (Behuria Reference Behuria2020).

Rwanda’s coffee sector has been transformed with the RPF’s paradigmatic ideological goals in mind: achieving self-reliance. The sector’s trajectory has been marked by elite vulnerability: initially, the Rwandan government was partnering more with closely allied domestic capitalists. Later, nearly all its ambitious interventions have been undertaken on its own (and sometimes in alliance with external partners who agree to work in line with their prioritisation of upgrading). Elite vulnerability has also been accompanied by inequality across the sector, with the benefits of upgrading unequally shared across Rwanda’s coffee producers. As Illien et al. (Reference Illien, Perez-Nino and Bieri2022, p. 1202) highlight, while coffee ‘provides an avenue of accumulation for some’, most households ‘engage in a variety of precarious small-scale work arrangements subject to strong seasonal pressures and different time scales’. The next section shows how the tea sector tells a similar story.

Tea

The first tea plantations were only established in Rwanda in 1961 in Mulindi and a few years later in Cyangugu. Tea was highlighted as the ‘ideal crop for Rwanda’ with ‘42,000 acres of land, with an estimated productive capacity of 19,000 metric tonnes potentially suitable for tea cultivation (with half of this land comprised of swamp and marshes)’ (Nyrop et al. Reference Nyrop, Brenneman, Hibbs, James, MacKnight and McDonald1969, p. 158). However, the Belgian colonial administration never explored tea cultivation and instead preferred to focus on coffee and mining. While the Kayibanda government put in place plans to establish tea factories, it was only during Habyarimana’s reign that eight new tea factories were constructed. The total acreage devoted to tea cultivation increased from approximately 285 ha in 1962 to 10,120 ha in 1984 (Von Braun et al. Reference Von Braun, De Haen and Blanken1991). This rapid expansion of tea cultivation was also accompanied by expropriation of land. Peasants resisted tea expansion, complaining that tea plantations claimed the most fertile tracts of land (Pottier Reference Pottier1986; Verwimp Reference Verwimp2011). Rwandan tea, most of which has historically been sold at the Mombasa tea auction, has fetched the region’s highest prices since the 1980s (Behuria Reference Behuria2015a).

Tea has always been well suited for cultivation in Rwanda. During the Habyarimana and RPF governments, production and area under tea cultivation have expanded while yield has improved (though it has fluctuated) (Figures 6.7 and 6.8). The RPF government has continually expanded the area under tea cultivation. Recently, tea cultivation was expanded from 26,879 ha in 2017/2018 to 32,800 in 2023/2024 (NAEB 2023).Footnote 9 This expansion has often been met with resistance from rural producers (Pasgaard et al. Reference Pasgaard, Sung Kyu, Dawson and Fold2022).

Total made tea production in Rwanda: 1961–2022.

Area under tea cultivation and yield in Rwanda: 1961–2022

Unlike previous governments, the RPF has heavily prioritised upgrading within the tea sector. As the quotes further down indicate, the government justifies this in line with its ideological goals of achieving self-reliance. In addition, the government, as with its policies in all commodity sectors, highlights the unfairness associated with most profits from commodity exports being retained in consumer countries, with buyers and retailers benefiting the most.

Think about this tea you are buying in Tesco. The Rwandan farmer gets almost nothing as a percentage of that. Our President wants us to make sure that the Rwandan farmer gets the most money possible. That is what value-addition will enable us to do.Footnote 10

On average, Kenya produces over 350,000 metric tonnes of tea. Kenya earns between 250 million and 350 million USD out of tea. They are doing value-addition of say 1–2 per cent. Their strategy has been for the short-term and export earnings are still low. Sri Lanka produces roughly the same amount. They are doing value- addition for about 35 per cent of what they produce. They are getting 960 million USD, maybe a billion. Value-addition is difficult but it is the only way to go.Footnote 11

In Rwanda, we get about two dollars for our tea. In some shops in Dubai, teas fetch about $20. What we want to do is capture as much of the difference as possible.Footnote 12

The GVC/GPN literature suggests that upgrading within the global tea sector has been rare, as tea remains dominated by a small number of lead firms (Talbot Reference Talbot2002). Very few firms have successfully achieved functional upgrading by competing with Western brands and selling exported blended and packaged tea. The most obvious exceptions are Sri Lanka’s Dilmah Tea and large Indian tea companies, all of which benefited from significant government incentives and marketing (Ganewatta et al. Reference Ganewatta, Waschik, Jayasuriya and Edwards2005). Scholarship argues that upgrading success is only likely to be achieved after local production has been expanded and then partnerships are sought with established global brand names (Raynolds & Ngcwangu Reference Raynolds and Ngcwangu2010). Most of Rwandan tea production is processed using the Black CTC (crush, tear and curl) method. Farmers pluck green leaves, which are transported to the factory before they are withered (or partially dried), cut (or rolled) and later fermented. During fermentation, the leaf develops flavour and a black colour. The tea is then dried to stop oxidation and then sorted. The final product of black-sorted tea is packed (according to specific grades) into paper sacks. Black CTC tea involves the rolling of tea between two rollers. The CTC process ends with small grains that are used mostly for tea bags. Orthodox black tea, which is also produced in Rwanda, involves rolling tea against a cutting table, rather than two rollers. Orthodox teas are small, curled tea leaves, which are generally used for high-quality loose teas. Bulk tea is transported for sale to the Mombasa auction or sold directly to foreign buyers. Black CTC tea is more widely produced in East Africa because its production is more cost-effective than the methods used to produce Orthodox tea (OCIR-Thé 2006).

The RPF’s upgrading strategy is to reduce the amount of Rwandan tea sent to the Mombasa tea auction and thereby reduce the economy’s vulnerability to fluctuations in global tea prices. To achieve this, the RPF government has prioritised facilitating direct sales (outside the Mombasa auction) directly between factories and foreign buyers, with increased interest from European and Asian markets highlighted in consultancy reports since the early 2000s.Footnote 13 From only having very limited direct sales in the 2000s, by 2022, Rwanda exported over 27 per cent of its tea through direct sales (NAEB 2023). Another central focus has been encouraging diversification into specialty teas (including green, white, orthodox and spicy teas), which were assumed to fetch premiums in comparison to bulk tea sold at the Mombasa auction. The most ambitious functional upgrading strategy was to sell blended and packaged tea domestically and internationally. The government’s strategy assumes that prices for blended and packaged tea ranged from $7.50/kg to $22/kg compared to roughly $2/kg paid at the Mombasa auction (MINAGRI 2008).

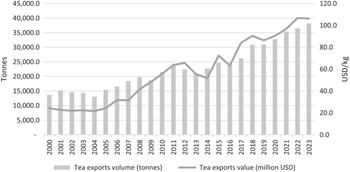

The RPF government has achieved significant progress in increasing tea production and capturing higher tea prices than neighbouring countries while also achieving some upgrading. Figure 6.9 shows how both the volume and value of Rwanda’s tea exports have increased substantially over the last two decades. However, as with the coffee sector, these policies have been characterised by inequalities among both tea producers and workers, with not all cultivators receiving the same benefits from producing tea. As more land is being sought to cultivate tea, evidence suggests that only wealthier farmers or those with larger land-holdings opt for tea production. Poorer farmers cannot take up the option because of limited access to fertilisers and pesticides (Pasgaard et al. Reference Pasgaard, Sung Kyu, Dawson and Fold2022).

Volume and value of Rwanda’s tea exports: 2000–2023.

As the government has sought to prioritise upgrading, its choice of capitalist partners has been shaped by elite vulnerabilities. Initially, the RPF relied on domestic capitalists to own factories while also selling factories to some prominent foreign tea companies. The government has been reluctant to partner with large multinational tea firms, given the concentration in the blending and packaging segment of the tea GVC.Footnote 14 Since dominant global buyers have been less interested in value addition, the government has sought to rely more on a specific national champion (Rwanda Mountain Tea (RMT)) and some strategic partnerships (with an American investor, SORWATHE, and philanthropic investors like the Wood Family Trust (WFT) and Gatsby Foundation). At the same time, the RPF has fallen out with at least one leading domestic capitalist with interests in the tea sector (Tribert Rujugiro). This highlights continued difficulties in building effective national state-business partnerships for value addition. In comparison to coffee, there has been less success in value addition, particularly in blended and packaged tea, with only 1 per cent of Rwanda-produced tea currently sold as blended and packaged tea (NAEB 2023). Most government officials and industry experts agree that this is because of how the tea sector is heavily controlled by a smaller number of packaging companies and retailers, as compared to coffee, which is much more dispersed. The following section describes how advances in value addition has been characterised by inequalities within rural areas, but sustaining success depends on managing delicate domestic state–business relationships.

Inequalities within Rwanda’s Tea Sector

The reorganisation of Rwanda’s tea sector has been partially modelled on the experience of the Kenya Tea Development Authority (KTDA) – particularly, the KTDA’s emphasis on empowering cooperatives made up of ‘smallholder’ farmers. Yet presenting the KTDA as a success obscures the rural differentiation that characterises tea production globally and in Kenya’s tea sector. The KTDA’s share of the national tea supply increased from 6 per cent in 1965 to 33 per cent in 1980. The KTDA’s organisational approach was based on a ‘one-acre ideal’, where plantings below the minimum of one acre were assumed not to be worth the farmer’s time and care (Leonard Reference Leonard1991, p. 127). Such requirements favoured the farmers who already had land, ignoring the position of wageworkers on tea farms who were landless. Since the 1970s, literature had highlighted the emergence of increasing rural differentiation, as well as the presence of landless workers on tea farms (Steeves Reference Steeves1978). Even within the KTDA example, there were signs of inequities along with the emergence of rural capitalists (Swainson Reference Swainson1977).

In Rwanda, tea production is characterised by significant rural inequalities and differentiation. Each tea factory enjoys a monopoly over the supply of tea produced in specific areas. Tea growers are organised to produce tea in three ways: (1) wageworkers are employed by the Bloque Industriel (BI) or Industrial Estate run by tea factories. BIs are situated adjoining the factory and owned by the factory owners; (2) COOPTHEs (tea cooperatives), which are blocks of large sizes owned by tea cooperatives. In COOPTHEs, land is consolidated and distributed by the government for the purpose of growing tea exclusively. Cooperatives are professionally managed. Farmers employ both family labour and wage labour; (3) Thé Villageois (TV), which are small independent tea plots owned by farmers who have tiny plots of land (official average of 0.25 ha).Footnote 15 These farmers are organised into cooperatives, with the cooperative responsible for distributing fertilisers, providing access to credit, transporting tea leaves to the factory and maintaining roads.

BIs are usually under shared ownership between cooperatives and factories. However, owners of Mulindi and Shagasha (the first two factories built in Rwanda) do not own any of the land in the BI. In these factories, COOPTHEs have full ownership of the BI. Cooperatives comprise a variety of farmers who own different sizes of land. Mirroring the KTDA, the government directed tea cooperatives to form a federation – Fédération Rwandaise des Coopératives de Théiculteurs (FERWACOTHE) – in 2000, which was legally recognised in 2007. In 2023, over 43,000 tea growers were FERWACOTHE members. FERWACOTHE’s main responsibilities include lobbying and advocating for better prices for green leaf tea, assisting in cheap access to fertilisers, improving transport infrastructure to and from factories and advocating for farmers to be allowed to buy shares in privatised tea factories.

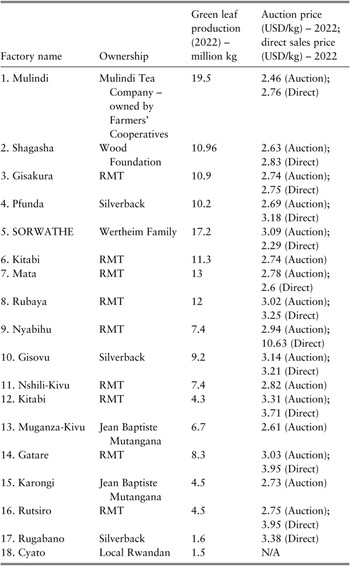

In 2023, the Rwandan tea sector comprised eighteen tea factories, with more than 43,000 tea farmers organised in twenty-one cooperatives. Table 6.2 details the ownership of the factories. Though multinational tea companies were involved briefly, there is now significant concentration of ownership. A government-affiliated investment group, RMT, owns nine of the eighteen factories. Four factories are owned by a philanthropic investor (Wood Foundation), with three of the four including investments from an Indian investor (Luxmi Tea), which has committed to scaling up factories and investing in direct sales, diversifying tea production and value addition. RPF-affiliated capitalist Jean Bapiste Mutangana owns two other factories. Long-standing American investors, the Wertheim family, have owned SORWATHE for over fifty years. An unnamed local investor owns another factory, and the last factory, Mulindi (Rwanda’s oldest factory), was gifted to local tea cooperatives by the Wood Foundation in 2022.

Table 6.2 Long description

The table contains four columns, Upgrading Strategy, Type of Upgrading, Role of the State, and Economic Partners. It lists six major strategies used in Rwanda's coffee sector and explains how state actions and partnerships supported each one.

Row 1, Coffee Washing Stations

Type of Upgrading: Process and product upgrading

Role of the State: Initially acted as a producer; later transitioned to regulator and facilitator

Economic Partners: Military, state-owned institutions such as the Rwanda Social Security Board, and donor-partnered cooperatives

Row 2, Liberalisation of Exports

Type of Upgrading: Contributed to process and product upgrading

Role of the State: Active facilitator; implemented strategic liberalization to attract new exporters; encouraged washed and specialty coffee exports; later enabled diversification into markets for honey, cascara, and natural coffee

Economic Partners: Select cooperatives developing foreign roaster and trader links; some donor-funded cooperatives faced challenges after donor exit

Row 3, Cooperatives’ Links to Foreign Roasters/Retailers

Type of Upgrading: Process and product upgrading

Role of the State: Active facilitator in partnership with donors and major roasters such as Starbucks and Peet’s Coffee

Economic Partners: Cooperatives that successfully established direct links with international roasters and traders

Row 4, Coffee Marketing Campaigns

Type of Upgrading: Contributed to product upgrading by moving into specialty coffee; also functional upgrading

Role of the State: Active facilitator; also acted as producer by organising Cup of Excellence competitions

Economic Partners: Government agencies, USAID, and international roasters collaborating on coffee promotion

Row 5, Entering Retail Markets Domestically and Globally

Type of Upgrading: Functional upgrading

Role of the State: Producer role through party-affiliated investment

Economic Partners: Bourbon Coffee, part of Crystal Ventures Limited, served as a demonstration model for other domestic retailers

Row 6, Roasting Coffee for Domestic and Export Markets

Type of Upgrading: Functional upgrading

Role of the State: Producer role first through toll-roasting abroad, then locally through the Rwanda Farmers Coffee Company, RFCC.

Economic Partners: Government-established RFCC, created in partnership with philanthropists.

As Table 6.2 shows, many tea factories have been involved in direct sales. Most of these factories (though not all) are receiving better prices for direct sales than through the Mombasa tea auction. The consolidation of tea ownership in the sector highlights how strategic investments are only entrusted to closely affiliated RPF businesspeople, as well as philanthropic investors who commit to working in line with ideological goals of self-reliance. Though the RPF has attempted functional upgrading in the sector, there has been limited success. There have been failed experiments with trying to package and blend tea abroad. However, process and product upgrading, through investing in tea cultivation practices (including fertiliser and pesticide distribution), has resulted in Rwandan tea receiving significantly higher prices. Given the rapid expansion of area under cultivation, there is evidence that the government is increasingly prioritising tea more than other export crops (particularly coffee in the future). This has not yet resulted in substantially increased production, since tea takes three or four years to reach first harvest, and the large-scale expansion of tea cultivation has only increased in the 2020s.

Yet there is evidence that tea expansion has been accompanied by increasing inequality and has only benefited wealthier farmers, with associated costs for food security. In the 2000s, tea growers’ share of the price of made tea was lower in Rwanda than in Tanzania (27 per cent) or Kenya (75 per cent).Footnote 16 In 2010, World Bank evaluations indicated that ‘for coffee and limited land of less than 0.5 ha, there was a risk that expansion of coffee and tea production would be at the cost of food security’.Footnote 17 More recently, Pasgaard et al. (Reference Pasgaard, Sung Kyu, Dawson and Fold2022) have shown that farmers who opted for tea tended to be wealthier than those who chose not to. Tea growers were expected to join a cooperative and pay for it. Often, they also had to pay for fertilisers, and there was a long period during which they did not receive income for the tea they planted. More than half of those they interviewed highlighted that tea production had led to lost labour opportunities, disruption of local food production, tenure insecurity and higher food prices (Pasgaard et al. Reference Pasgaard, Sung Kyu, Dawson and Fold2022). Their interviewees suggest that the allocation of land for tea growing ‘was about who you knew and what you had’, supporting the argument that ‘people who already had land got more’ (Pasgaard et al. Reference Pasgaard, Sung Kyu, Dawson and Fold2022, p. 112).

Evolving Capitalist Partners

After the genocide, the tea sector was rehabilitated significantly. Though some tea factories were in operation even in the first few months of 1994, the directors of some tea factories also led killings during the genocide, using factory-owned trucks and cars to transport Interahamwe to massacre sites (Verwimp Reference Verwimp2004). One factory was dismantled, and the machinery was taken to the DRC (EIU 1994). After 1994, IFIs and donors pressured the Rwandan government to privatise tea factories. However, in the tea sector, the clash between paradigmatic goals of self-reliance (through achieving value addition) and the need to meet donor demands has been visible. The government recognises several positives associated with foreign ownership. These include the possibilities of developing direct sales contacts with international buyers, connections with international experts and the introduction of new technology to modernise agricultural practices and processing equipment. While the government acknowledges the importance of bringing in foreign expertise, it has never been convinced that large foreign multinationals would embrace value-addition strategies (e.g. packaging single-origin tea, which would be competitive with their own teas abroad). Several foreign factory owners have criticised the Rwandan government’s upgrading ambitions.

We are doing our part – we invested a lot and we produce one of the best quality teas in East Africa. It was difficult to win the government’s trust but we are not interested in the kinds of value-addition the government wants.Footnote 18

Unlike in the coffee and mining sectors, the government has worked with a national champion: RMT. RMT owns nine tea factories in Rwanda. Egide Gatera is the majority shareholder of RMT and Petrocom Ltd.Footnote 19 Egide Gatera is one of the few businesspeople who remains a trusted partner of the Rwandan government. Tribert Rujugiro, another investor in Rwanda’s tea sector, had shares in two factories until he fell out with the RPF. Later, his tea factories were seized. Jean Baptiste Mutangana, a founding member of RIG, also owns two tea factories and several apartment complexes in Kigali. George Rubagumya, owner of a US-based Rwandan company, Olyana Holdings, owned the Gisovu tea factory. However, in 2009, Rubagumya is argued to have sold the company ‘behind the government’s back’ to Borelli holdings, a subsidiary of global tea giant, McLeod Russell.Footnote 20 The Rwandan government tried to cancel the sale, but after international arbitration, the deal was confirmed in 2011.Footnote 21

Since Borelli were not interested in value addition, it was perceived as a ‘wrong’ investor by the government. Eventually, in 2017, Silverback Tea Company assumed control of Borelli’s two tea factories. Silverback was owned by Rwanda Tea Investments (RTI), led by the Wood Family Trust (WFT). Luxmi Tea, an Indian investor, had been in discussions with the Rwandan government since 2012 regarding packaging single-origin tea, as well as investing in process and product upgrading. Luxmi was brought on as a partner in WFT’s investments. The RPF government trusted WFT as the ‘right’ philanthropic investor in the sector because WFT committed to investing in functional upgrading. Previously, WFT was granted Rwanda’s two oldest factories under shared ownership. The Shagasha Tea Estate was granted to RTI (60 per cent), cooperatives (30 per cent) and the government (10 per cent). The Mulindi Tea Estate was granted to RTI (55 per cent) and farmers (45 per cent). In 2022, WFT donated its share of ownership in Mulindi to farmer cooperatives, making Mulindi Rwanda’s first fully farmer- and cooperative-owned factory.

An American investor, Joe Wertheim, who had bought the SORWATHE Tea Factory in the 1980s, was one of the key supporters of Rwanda’s value-addition strategy. Initially, he offered to find buyers for all of Rwanda’s tea through direct sales to the United States. SORWATHE (despite being a foreign-owned company) led the way in diversification into specialty teas. In the early 2000s, SORWATHE began producing small quantities of orthodox white and green teas. SORWATHE also built a tea factory exclusively to produce orthodox and green tea. A sum of $2.2 million was invested in this factory. SORWATHE was the first company to get Fairtrade and International Organisation for Standardisation (ISO) certification for its factories. The company also introduced organic growing practices (without using pesticides or fertilisers) and was organic-certified in January 2012. SORWATHE also converted 116 hectares of company-owned land for organic tea production. Wertheim’s interests in tea were not on the scale of Borelli or Imporient globally. Though SORWATHE was ‘foreign-owned’, it had a historical interest in the sector, having set up the factory over forty years ago. SORWATHE was unlike other foreign-owned firms that were close to the Habyarimana regime because it quite quickly aligned itself with the RPF’s value-addition strategy, thereby not only becoming an effective partner but also showing leadership where foreign firms (like Borelli) questioned the RPF’s strategy.

However, the government’s most ambitious attempts at functional upgrading through blending and packaging tea happened through government investments in partnership with RMT. In 2009, RMT (60 per cent) and the government (40 per cent) entered a joint-venture partnership to create Rwanda Tea Packers (RTP). Originally, RMT was supposed to work with Olyana Holdings, but after Borelli took over the company, they declined to take part (highlighting a failure of domestic state–business partnerships). RTP decided to blend tea in Rwanda and outsource packaging to Dubai-based DTC teas. RTP was responsible for marketing the tea in Dubai. However, RTP failed to consider the high import duties on value-added teas, highlighting its limited managerial capabilities at the time. There were also difficulties in obtaining shelf space in supermarkets. A large share of tea that was produced and transported to Dubai was never sold. By April 2011, RTP operations in Dubai closed.

RTP didn’t have knowledge of the market. It didn’t work because Dubai was just not the right market. There is an acknowledgement that we may need a strategic partner or that we may have to find new markets. It will take time. I visited Dilmah in Sri Lanka and learned about the company’s story. When Dilmah started, it was a company with one tea bagging machine. Developed countries tried to sabotage them. What was helpful was the benefits given by the Sri Lankan government e.g. tax holidays, incentives. The government did intensive branding campaigns (nationally and internationally). Our attempts need to be deliberate and considered. Patience is also required. When we meet challenges, it doesn’t mean that we’ve failed. We shouldn’t lose heart, we just have to keep going.Footnote 22

After the failed experience in Dubai, RTP concentrated on unexplored markets where the oligopolistic control of large firms was less obstructive. Additionally, more emphasis was placed on capturing the domestic tea market. In 2001, 58 per cent of locally consumed tea was imported from neighbouring countries (Tanzania, Kenya, Burundi and Uganda). SORWATHE, Highland Tea and OCIR-Thé (in the form of loose tea or tea bags) produced tea for local consumption. By 2012, four domestic firms had begun packaging tea for domestic consumption (and some of this tea was exported). Foreign owners of tea factories continued to criticise Rwanda’s strategy. A manager of one company said:

The Government has got value-addition in its head. When we did our study, value-addition came up as zero. You’ll never make money; you can try as much as you can. When I pack tea in Rwanda, the weight and volume is low. Transportation costs are extremely high. However, we add value for the domestic market because there is a small opportunity here. But it would be cheaper for me to send the tea in bulk from Rwanda and package it in London. The paper and packaging material in Rwanda is ten times the cost of what it is in Mombasa. If the government wants us to add value, they must give us more incentives.Footnote 23

The RPF relies on two types of capitalist partners to deliver its strategic goals: party-affiliated investors and philanthropic investors. Rwanda’s attempts at functional upgrading failed. Yet the quality and reputation of Rwandan tea remain high compared to regional competitors. As a result, the government has focused on increasing tea production while slowing attempts to diversify into new teas and waiting before embracing more ambitious attempts at exporting single-origin or blended and packaged tea.

It is fair to say that Rwanda Tea Packers did not work well. But there is a lot of hope in tea. Leadership thinks it has a bright future. So we will now scale up production and invest more in quality. Then we will see again in the future.Footnote 24

Though there is some evidence of effective state–business partnerships in the case of RMT, significant ruptures in domestic state–business partnerships have hampered upgrading attempts (as with the case of Rujugiro). Crucially, the tea example highlights the limits of trying to upgrade within a sector that is traditionally dominated by powerful multinational buyers. Given that tea was a highly competitive sector dominated by a few multinational firms, the government strategised to selectively partner with philanthropic capital who were willing to support domestic firms (like RMT) to invest in technological capabilities, diversify into new teas and access foreign markets. This strategy would not have been achieved without a clear national champion in the sector. In supporting Gatera’s RMT, which also works closely in partnership with government-owned companies, there has been some limited success. Still, the failure to be able to pool investments because of the RPF’s elite vulnerability has also constrained progress to some degree. Rujugiro’s companies were seized, and other investors like Rubagumya were also unable to build effective relationships. In the remainder of this chapter, alternative agriculture exports are discussed. These examples tell a similar story, with some export success through supporting state-affiliated firms (or foreign investors) within an environment of elite vulnerability and rural inequality.

Alternative Agriculture Exports: The Future Source of Diversification?

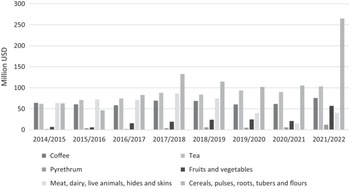

Rwanda’s agricultural export drive has been partially driven by an urgent need to find new exports in line with the RPF’s paradigmatic ideological goals of self-reliance. Between 1976 and 1991, coffee exports comprised between 65 per cent and 82 per cent of total export earnings. Perhaps, the most significant change to Rwanda’s export composition has been the increasing export of new agricultural products (particularly cereals and pulses, livestock products, fruits and vegetables and vegetable oils). Figure 6.10 shows how some of these products have become more significant exports than traditional exports like coffee and tea. Since the 2018/2019 fiscal year, nearly 60 per cent of generated revenues have been from non-traditional exports, with the exports (and re-export) of cereals and pulses, live animals, dairy products and oleaginous products (like soya, groundnuts and sunflower) growing at a range of nearly 103–147 per cent (NAEB 2023). This section first discusses the evolution of pyrethrum exports, Rwanda’s third-highest agricultural export historically (outside coffee and tea). It then describes the evolution of non-traditional agriculture exports.

Traditional and new agriculture exports in Rwanda: 2014/2015–2021/2022.

Pyrethrum

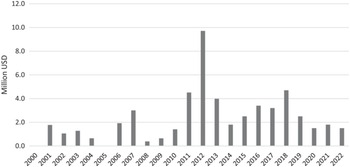

Traditionally, aside from coffee and tea, Rwanda’s third-largest agricultural export has been pyrethrum. Pyrethrum is a natural flower-based pesticide, used as an alternative to synthetic chemical pesticides to control a wide range of insects. Pyrethrum was introduced in Rwanda in 1936. Since then, Rwanda has been among the top five pyrethrum producers in the world. Under pre-1994 governments, the OPYRWA pyrethrum factory, which was jointly controlled by a government-owned industrial facility and planters’ association, was responsible for processing flowers into exported raw pyrethrum extract. In the 1990s, the RPF government first privatised OPYRWA (which was renamed SOPYRWA), selling it to four Rwandan businessmen. After the company went bankrupt, Horizon – the military-owned investment group – assumed ownership in 2011. Pyrethrum exports spiked in 2012 and then oscillated between $1 million and $5 million since then (Figure 6.11). Unlike individual private investors, Horizon has prioritised investments in refining pyrethrum. More than 75 per cent of Rwanda’s 5.5 million USD pyrethrum exports in 2022/2023 were in refined form, as compared to negligible amounts before Horizon’s takeover (NAEB 2023). Yet overall, export revenues have reduced, suggesting that the upgrading strategy has not yielded the dividends that were expected. Horizon’s prioritisation of processing was criticised, with some accusing the firm of engineering ‘control grabs’ within the sector (Huggins Reference Huggins2014). Research highlighted how farmers have been forced into producing pyrethrum (Huggins Reference Huggins2017). When Horizon took ownership, farmers in Musanze and other areas were forced to dedicate 40 per cent of their land to pyrethrum even though other crops like potatoes provided higher revenues (Huggins Reference Huggins2014). Many rural producers also chose not to join cooperatives because cooperatives were dominated by a few farmers with large landholdings (Behuria Reference Behuria2015b; Huggins Reference Huggins2014).

Rwanda’s pyrethrum exports: 2000–2022.