Global finance is subject to cycles: changes in U.S. monetary conditions are transmitted abroad through the international banking system. Expansive credit conditions in the U.S. encourage capital to flow into the periphery, resulting in credit expansions but also more troubling asset bubbles and volatility.Footnote 1 Restrictive financial conditions in the U.S. reduce the availability of capital abroad, as dollars flow out of the financial periphery and into U.S. capital markets.Footnote 2

The political–economic implications of these cycles—and, more generally, of a network model of global finance emphasizing hierarchy and U.S. centralityFootnote 3 —have been a substantial topic in the literature over the past decade, with a focus on economic outcomes and how governments engage with foreign markets and bond investors. For example, previous work links these cycles to macroeconomic fragility and growth;Footnote 4 to volatile economic and credit conditions;Footnote 5 to more pro-active attempts by governments to attract foreign capital;Footnote 6 to bond markets’ willingness to take on risks;Footnote 7 and to changing borrowing strategies by governments.Footnote 8 A core implication of this line of work is that governments cannot separate themselves from these cycles short of closing capital accounts. Any country with a financial system relying on dollar funding is subject to cycles originating in U.S. credit conditions, shaping how governments engage with global markets.

We contend that these cycles have additional, more overtly political implications, beyond how governments engage with global (bond) markets. We focus particularly on the domestic political implications of credit cycles.Footnote 9 Consider the positions that peripheral governments find themselves in during these moments. Tighter U.S. credit conditions increase the costs of capital, making it harder for firms to expand and compete. This is particularly painful for smaller or newer firms without substantial access to retained earnings. The business sector is an important political constituency—for some, the political constituencyFootnote 10 —and broadly felt discomfort like this would typically provoke a political response aimed at their interests. Politicians inside and outside of government would want to signal their sympathy for and utility to the business sector. However, there is little that a government can directly do about these cycles short of (counter-productively) withdrawing from global financial markets. Governments can subsidize credit to specific firms and industries,Footnote 11 but only at high cost and in targeted ways,Footnote 12 because the discontent of credit-dependent businesses is rooted in monetary policy choices over which governments retain little influence.

We argue that politicians address this tension with a form of political substitution. Politicians looking to offer broadly appealing pro-business political stances will substitute monetary policies that they cannot control for business-friendly policy stances on tax and regulatory policies that they can control. The result is a global political cycle that mirrors the more widely understood global credit cycle: tighter credit conditions in the U.S. lead to tighter credit conditions and, through that, more business-friendly politics from parties across the ideological spectrum; looser credit conditions in the U.S. do the opposite, allowing parties to promise more labor-friendly and regulatory policies that impose costs on firms.Footnote 13

We provide evidence for our framework by analyzing the business-friendliness of political parties using data from the Manifesto Project, which codes parties’ programmatic pledges during election campaigns.Footnote 14 These data allow us to characterize shifts in the business-friendliness of party rhetoric in comparable ways across countries and over time. They also allow us to assess effects across several policy domains and determine whether some parties are more responsive than others to policy pressures. Electoral pledges are, in our view, directly controlled by coherent political parties that can respond to changing economic conditions, making them a direct implication of the theory. In contrast, while there is evidence that pledges correlate with subsequent behavior,Footnote 15 the timing of changes in policy outcomes is difficult to compare due to different domestic institutional constraints across countries.Footnote 16 Looking at actual regulatory relief also implies complex substitutions across different domains (labor, environment, financial, antitrust, licensing) and, potentially, coalition partners, which is difficult to capture in cross-country settings.Footnote 17 Even more, countries may not change policies but shirk on regulatory enforcement in accordance with their programmatic positions.Footnote 18

Our evidence shows that party manifestos—for both left- and right-wing parties—become more business-friendly during financial tightening cycles. Moreover, political parties’ credit-cycle-induced business-friendliness extends beyond issues of immediate concern to globally mobile lenders, indicating that this is a causal mechanism that plays out within domestic politics, distinct from politicians’ desire to encourage and court globally mobile investors, and distinct from a broader turn toward neo-liberal policy-making.Footnote 19 Politicians appeal to domestic business interests, specifically, by softening their commitments to labor in response to rising U.S. interest rates and the global credit cycles they trigger. In additional analyses, we report that while we observe similar shifts in their overall stance for left- and right-wing parties, this change comes about in different ways: compared to right-wing parties, left-wing parties tend to pare down previously supportive statements toward labor groups, rather than including more outright anti-labor statements.

We also provide evidence for several supporting conditional hypotheses. We demonstrate that the relationship between credit cycles and party positions becomes more pronounced when U.S. banking is more globally dominant, and particularly in countries where private borrowers face immediate financing needs. Both findings support our theory. We find no evidence that the relationship between business-friendly positions and U.S. interest rates is affected by the government’s financing needs, which further aligns with our theory that the financing needs of domestic firms, rather than of sovereigns, drive the shift in party positions.

Additionally, we show that the effects are most prominent in countries with more open capital accounts and, consequently, less insulation from U.S. interest rates. These distinctions primarily speak to historical variation—for the past two decades, nearly all countries in our sample have experienced levels of capital account openness at which we observe the anticipated effects of U.S. interest rates on party manifestos—but they emphasize that the globalized financial system that begets these effects is the result of policy choices around capital mobility, and not inevitable.

Our paper makes several contributions. First, it expands the scope of financial globalization’s policy impact beyond footloose bond investors’ “strong but narrow” interest in low inflation and fiscal restraint.Footnote 20 International financial markets have direct implications for all borrowers, even those who borrow domestically. But those domestic businesses care about domestic labor markets, deregulation, and the whole gamut of policies that affect their other business costs besides the price of credit. This means that financial globalization that hurts the interests of domestic businesses can push politics in a pro-business direction different from what follows by focusing narrowly on foreign bond investors. We show evidence of business-friendly rhetoric on a global scale accompanying U.S. tight monetary policy. And even though we look at just party statements and not policies, it is suggestive for the policy thrust that parties across the ideological spectrum embrace.

Moreover, focusing on domestic business interests shapes how we think about financial globalization’s political constraints.Footnote 21 Footloose bond investors are economically significant but often have unpopular political priorities.Footnote 22 The literature on the populist backlash against globalization highlights the challenges of catering to foreign economic interests at the expense of domestic political actors. Our work suggests that the policy impacts of financial globalization are not always politically restrictive. They can sometimes push governments toward lighter tax and regulatory regimes that, while not universally popular, typically have strong domestic political constituencies and are considerably less politically toxic than austerity.Footnote 23

Finally, we also add to the literature on the political economy of party programs, which is more typically focused on reactions to domestic economic conditionsFootnote 24 or crises.Footnote 25 Work on globalization’s connection to party programs emphasizes how economic integration (measured variously as realized trade or investment flows or the absence of tariffs or capital controls)Footnote 26 reduces programmatic differences across partiesFootnote 27 and limits accountability to voters.Footnote 28 To our knowledge, our emphasis on programmatic response to global financial cycles is a novel addition to this literature. It is an important addition for two reasons. First, it shifts focus from public opinion to firms, which are more directly impacted by economic globalization and whose political preferences are more directly linked to global finance. Second, the credit cycles we focus on are more reliably exogenous to domestic politics than is often possible in this literature.

U.S. interest rates and global financial cycles

Global finance is anchored in U.S. dollar markets and is sensitive to fluctuations in those markets.Footnote 29 Approximately 70 percent of global trade over the past two decades was invoiced in U.S. dollars, along with about 40 percent of over-the-counter foreign exchange transactions and 60 percent of global central bank reserves. Nearly 70 percent of non-U.S. bonds were denominated in U.S. dollars.Footnote 30 The global banking system is likewise dominated by the dollar. U.S.-based financial institutions and their subsidiaries lend worldwide, with the U.S. dollar representing about 50 percent of cross-border bank claims.Footnote 31 Dollar-denominated credit outside the U.S. reached $12 trillion in 2023, which corresponds to roughly 40 percent of U.S. GDP.

The central role of the dollar and the U.S. banking sector in the global financial system transmits U.S. credit conditions worldwide. This mechanism, as described by Rey (Reference Rey2016),Footnote 32 illustrates a global credit cycle that operates as follows. First, consider the scenario of easing U.S. monetary conditions. Looser U.S. credit markets reduce the cost of capital for dollar-based financial intermediaries, allowing them to borrow more cheaply.Footnote 33 Those monetary conditions lead to a rise in U.S. equity prices, thereby increasing the value of the equity they can leverage. This generates additional borrowing capacity and expands credit further. Simultaneously, the lower returns on safe domestic lending encourage dollar-based financial intermediaries to seek higher yields outside of the United States. This global credit expansion lowers the financing costs for foreign borrowers and boosts their equity prices. As a result, the process improves foreign borrowers’ debt-to-equity ratios, facilitating more and less expensive borrowing.Footnote 34 A credit boom in the U.S. thus alleviates financing conditions wherever dollar-based commercial banks lend, enhancing credit to the private sector abroad. These booms in the credit cycle are not always welcome and have been linked to higher volatility and asset bubbles that inevitably burst when the financial cycle reverses.Footnote 35 Seen solely from the perspective of firms’ ability to raise capital, however, these cyclical credit expansions are surely welcome.

Tight credit conditions in the U.S. put the above-described dynamics in reverse. Higher U.S. interest rates increase dollar-based financial intermediaries’ borrowing costs while decreasing their risk appetite and the equity values they can lend against. This prompts them to deleverage, pulling capital back into the U.S. and limiting credit access abroad. As a result, foreign equity prices decline, and foreign balance sheets weaken. Foreign borrowers seem less creditworthy, leading to increased costs of capital.Footnote 36 The now more financially strained firms must pay higher interest to increase their debt load or refinance existing debt.

Two key elements of this process are worth highlighting. First, this mechanism impacts all borrowers, not just those accessing foreign capital directly. Any firm that borrows in dollars or borrows from a bank that borrows in dollars (or borrows from a bank that, in turn, borrows from a bank that borrows in dollars) will see their credit conditions fluctuate with U.S. credit conditions. Second, countries cannot escape these dynamics through external adjustment.Footnote 37 The transmission of U.S. interest rates globally through bank lending and the credit channel renders exchange rate adjustment irrelevant. Governments can maintain control over domestic interest rates only by decoupling from the global financial system.Footnote 38 External adjustment may help compensate firms in tradable sectors, but it does not address domestic credit conditions directly and has little consequence for non-tradable sectors.

Political reactions to global credit cycles

Rey’s “dilemma” just described is both political and economic. Tight credit conditions negatively impact businesses, which are a crucial constituency for political parties across the ideological spectrum.Footnote 39 Businesses require access to credit to stimulate domestic production and employment, which politicians aim to maintain. The literature on political business cycles indicates that pressures can lead to looser monetary policy before elections. However, this literature also indicates that this strategy is highly dependent on the political, economic, and institutional context, and perhaps not effective in general—especially in a world of global financial markets and widespread central bank independence.Footnote 40 Indeed, Rey’s “dilemma” suggests that tight U.S. credit conditions will affect other countries regardless of what governments do, short of separating from the dollar financial system.

That puts politicians in a bind. Politicians (in and out of office) want to signal to the business community that they will help alleviate the burden of a tightening credit cycle but lack a meaningful way to do it. Where they exist, governments could lean on state-directed development banks to manage credit counter-cyclically, but even then, such efforts are typically expensive if the state subsidizes credit and are often narrowly directed to larger incumbent firms, and often those with political ties.Footnote 41

Politicians thus need alternative means to signal their willingness to compensate broad swaths of businesses for tightened credit conditions. They do so, we argue, by promoting lower regulatory compliance costs and tax burdens, which help offset higher financing costs. This substitution is the core of our argument: Politicians adopt deregulatory, anti-tax, and broadly pro-business politics in reaction to tightening global credit cycles they cannot directly control.Footnote 42 These policies include relaxing price controls, antitrust and financial regulations, licensing requirements, emission standards, food safety rules, and labor protections, but also fiscally costly policies outside the traditional bundle of neo-liberal reforms.

Adopting pro-business policies is not costless and, thus, would not necessarily be implemented without a push to make them more politically appealing. In our framework, an increase in U.S. interest rates, by tightening local credit markets and deteriorating economic conditions, upends the existing political equilibrium. Parties use pro-business and anti-regulatory policy to convince voters that they have the right policy mix to promote economic and job growth in an environment in which high U.S. interest rates are the source of domestic business failure and economic pressure.

This allows governments to tap into a large political constituency of voters who view business as a key driver of economic growth (Przeworski and Wallerstein Reference Przeworski and Wallerstein1988; Boix Reference Boix1998). Indeed, concessions from labor in response to challenging economic environments are not atypical: Diwan (Reference Diwan2001) points out that labor may agree to wage restraints during crises to restore the profitability of firms and to avoid layoffs. Moreover, business owners, especially small business owners, are a large political constituency themselves, even when compared to manufacturing workers and unions (Malhotra et al. Reference Malhotra, Margalit and Saikun2025). Absent economic pressures, however, the demands of business are kept in check by labor pressuring for social protection, labor market regulation, and workplace safety, and by societal concerns for the environment, product safety, or financial stability. The broader reasons to not give in to business thus relate to fairness norms (Plümper et al. Reference Plümper, Tröger and Winner2009), the need to extract from capital sufficient resources to provide public goods (Devereux et al. Reference Devereux, Lockwood and Redoano2008), or the government regulating in accordance with the public interest (Skovgaard and Aisbett Reference Skovgaard Poulsen and Aisbett2013).

That balance is shaken when job numbers are at stake, as in an environment in which high U.S. interest rates are the source of domestic business failure and economic struggles and governments are left with few options to respond. In that scenario, politicians and voters alike are more inclined to trade off more employment allowed by cost savings deregulation, for lower quality jobs,Footnote 43 more pollution, or additional risks far out into the future. Put differently, we expect not so much that parties will pursue these policies against labor, but rather that—recognizing the importance of supporting business during challenging economic times—labor may acquiesce to and at times even agree with policies that support business and employment.

Several well-known cases suggest a link between higher borrowing costs and pro-business politics. Most famously, the high borrowing costs of the early 1980s resulted in demands by firms across the OECD to deregulate labor markets, reduce unions’ influence, and lower employment standards. Governments—including François Mitterrand in France and Helmut Schmidt in France—followed suit by supporting exemptions of firms from existing regulations, increasing provisions for short-term and temporary labor contracts, and allowing firms to circumvent collective bargaining agreements.Footnote 44 These policies did not directly address the systematic drivers of high borrowing costs (high U.S. interest rates, high capital mobility), but they enabled firms to better manage them by boosting revenue and redirecting it towards capital rather than other stakeholders, including labor, the state and society at large. This approach may spur new investments that higher capital costs might otherwise discourage. Our claims resonate with common explanations for political shifts during the first Clinton administration and in France under François Mitterrand.

Measuring pro-business politics

We assess the extent of business-friendly politics by analyzing shifts in party programmatic positions derived (as described below) from Manifestos Project data. We view these statements by parties as attempts to showcase their ability to find an appropriate bundle of policies to navigate a challenging economic environment, in response to changes in U.S. interest rates.

Focusing on policy programs—rather than the enacted policies—has several advantages. For one, it avoids considerations of how quickly and to what extent political institutions permit rapid policy adoption.Footnote 45 Similarly, while we might expect a uniform embrace shift toward “pro-business” politics, such a shift might lead to materially quite distinct policies in an already lightly regulated economy than in a more regulated economy, in countries with and without heavily unionized labor markets, or in economies with different industrial compositions. These might still affect intent, as described in party rhetoric. Yet, compared to policy outcomes, party rhetoric offers a more immediate evaluation of our argument on terms that are comparable across economic contexts, institutional structure, or available policy levers.

Focusing on party statements also allows us to measure “continued support,” which is different from maintaining the status quo. When looking at policy and policy change, indifference and support for maintaining the status quo are difficult to disentangle. In contrast, parties can positively mention deregulation, regardless of the current state of regulatory politics or which regulations are applicable. In particular, our approach allows us to capture the behavior not just of governing parties and coalitions, but of opposition parties as well. For policy outcomes, this would not be feasible.

Moreover, the government may cater to business interests through non-legislative means, like lax enforcement, when institutional obstacles hinder legislation. These avenues vary across countries and resist straightforward operationalization. Cataloging political shifts, gauged through party statements, promises a more reliable method for cross-country comparisons. Our focus leaves the causal relationship between politics and specific policy outcomes unexamined, though previous work indicates that public policy commitments guide policies,Footnote 46 and voters penalize governments for failing to deliver on them.Footnote 47

This leads us to our first hypothesis.

H1: Higher U.S. interest rates will yield more business-friendly party programs.

Our theory also suggests several conditional hypotheses. H1 presumes that borrowers need access to credit, such that tightening cycles create excess business costs and, consequently, a political problem that needs to be addressed. However, this reliance is variable. Credit needs vary according to the maturity structure of a borrower’s debt load. Borrowers who depend on short-term credit—which is typical of marginal borrowers seeking cheaper access financing—are particularly impacted by a tightening credit cycle. These borrowers are more likely to be forced to refinance under these tighter conditions. In contrast, borrowers with longer debt maturities are less likely to face significant refinancing needs at any given time. With more firms able to endure temporarily tight conditions, their governments will encounter fewer pressures to alter policies.

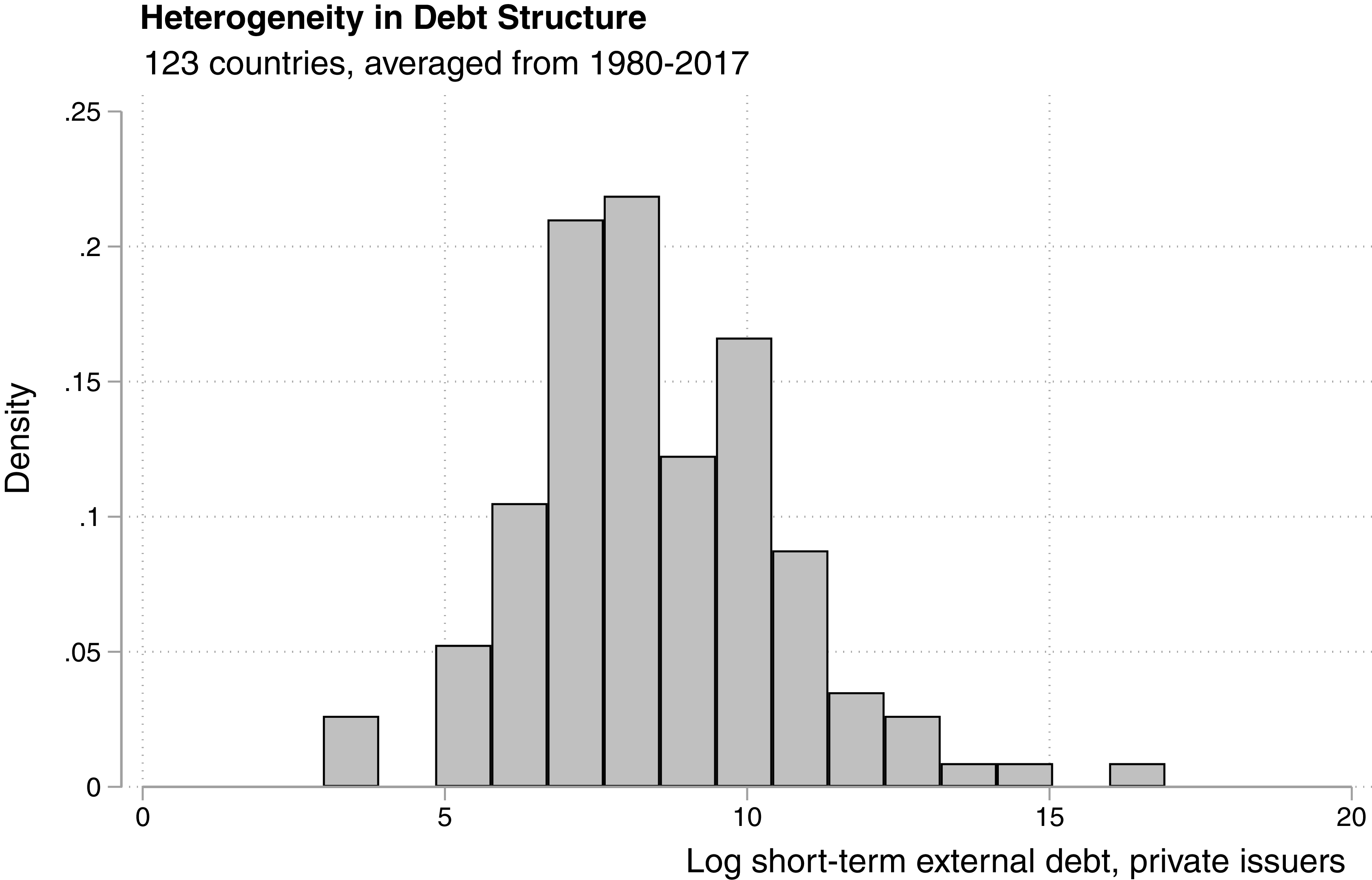

In practice, corporate debt structures vary significantly across countries. Figure 1 shows the log-transformed stock of short-term external debt (defined as debt with a maturity of less than one year) issued by private borrowers as a percentage of GDP for a sample of 123 countries, averaged from 1980 to 2017.Footnote 48 The higher the short-term debt-to-GDP ratio, the more a country’s debt structure compels its borrowers to refinance under adverse credit conditions, and the more its politicians should prioritize a political message that addresses the related financial implications. This underlines our second hypothesis.

Histogram of log short-term external debt issued by private borrowers relative to GDP. Data from Bank of International Settlements, 123 countries, 1980–2017.

H2: The relationship between U.S. interest rates and business-friendly party programs will increase with a country’s short-term external liabilities.

Our theory asserts that U.S. financial hegemony transmits dollar conditions internationally. The U.S. is the financial hegemon throughout our sample, but its dominance in global banking varies during this period. Changes in the U.S. credit market should have the most significant political consequences when U.S. banks have the greatest reach into other countries’ financial markets. Our sample extends back to 1963, well before the emergence of post-Bretton Woods financial globalization, where our theories’ presumptions about U.S. dominance most readily apply. The influence of U.S. credit conditions on local credit markets (and thus the political sensitivity to changes in those conditions) should increase as U.S. financial institutions expand their overseas investments.

H3: The relationship between U.S. interest rates and business-friendly party programs will increase in the presence of U.S. financial institutions abroad.

Empirical evidence

Dependent variables

We measure the business-friendliness of party programs using data from the Manifesto Project.Footnote 49 The Manifesto Project records and codes the electoral programs published by individual parties during election campaigns in over 60 countries. Coders parsed each electoral program into quasi-sentences, classified these quasi-sentences into different categories, and calculated the proportion of a document’s quasi-sentences devoted to each category. In our sample, the data covers an average of eight parties per election, with a maximum of 16 parties.Footnote 50

We rely on a composite measure that reflects dimensions of party programs that are especially relevant to domestic firms. Following standard practices established by the Manifesto Project for similar composite variables, our variable, pro-business statements, calculates the proportion of statements supporting a free market economy and deregulation, opposing welfare state expenditures, and opposing labor rights and wage increases; we then subtract the proportion of statements in favor of market regulation, supporting the welfare state, and supporting labor groups.Footnote 51 Our overriding concern is to construct a measure that reflects the particular policy priorities of domestic businesses rather than bond investors. To that end, we exclude references to budget deficits, fiscal retrenchment, or economic orthodoxy (like low inflation) from our measure. While these are included in standard conceptualizations of neo-liberal politics and with bond investors’ preferences, such forms of austerity often lack popularity among domestic businesses and voters alike.Footnote 52 Additionally, we exclude statements supporting free trade, which should be particularly relevant to foreign direct investors, as well as statements in support of the financial system, which are especially relevant to foreign stock investors.Footnote 53 In the appendix, we also follow Lowe et al. (Reference Lowe, Benoit, Mikhaylov and Laver2011), distinguishing in our measure between party positions on an issue and the political salience of an issue, and we show that the results are robust to using the log ratio instead of the simple difference between statements.Footnote 54

The left panel of Figure 2 plots the distribution of pro-business statements in party platforms from our sample. Almost all parties include at least some references supporting or opposing the policies we examine. The overall distribution shows a predominance of negative values, indicating a bias toward rhetoric that supports regulation, welfare states, and labor groups. The right panel of Figure 2 illustrates the distribution of pro-business statements in relation to the Manifesto Project’s residual partisanship indexFootnote 55 (which is created by removing from the Manifesto Project’s partisanship index those statements that also oppose or support business). The scatterplot reveals that pro-business statements correlate somewhat with other elements typical of the right-left distinction—the correlation coefficient for the two variables is 0.274—but the two variables represent distinct aspects of party programs. In other words, a shift toward pro-business politics in response to credit conditions would largely occur independently of other dimensions typically associated with a shift toward right-wing politics. Furthermore, we present results for the Manifesto Project’s partisanship index, which distinguishes our findings from a broader change in partisanship.

Histogram of pro-business statements (left panel) and a scatterplot of pro-business statements vs. residual components of right-left partisanship index (right panel). Data based on the Manifesto Project (Krause et al. Reference Krause, Lehmann, Matthieß, Merz, Regel and Weßels2018; Volkens et al. Reference Volkens, Krause, Lehmann, Matthieß, Merz, Regel and Weßels2018).

Independent variable

Our independent variable captures global credit conditions. Our primary measure are U.S. interest rates, which are plausibly exogenous to political rhetoric in other countries and appropriately reflect ultimate causes, consistent with our framework that emphasizes the central role of the U.S. dollar.

At the same time, relying on U.S. interest rates comes with trade-offs. They are somewhat removed from domestic political conditions and require assumptions about the speed of transmission between changes in U.S. interest rates and local lending conditions. We therefore present additional results using measures of new credit extension within a country and new credit extension globally. These measures of new credit extension—our global measure uses World Bank data on average credit growth (as a percent of GDP) across countries; our domestic measure uses domestic credit growth (as a percent of GDP) within countries—capture the relevant local economic conditions directly, but they do not ensure exogeneity from concurrent political events. As much as credit conditions drive politics, politics, in turn, affects credit extension.Footnote 56 Domestic credit growth, in particular, is also shaped by a host of other concurrent political and economic conditions.

We therefore focus the empirical work in this paper mostly on short-term U.S. interest rates, for their more obvious exogeneity to country-specific conditions. We represent these rates by the yields (based on market bid prices) on one-year U.S. government bonds. We compute the yearly average interest rate yield from monthly yield data provided by Thomson Reuters Eikon. We lag the variable by one year. The results remain robust whether we use current values, end-of-year interest rates from the previous year, or the beginning-of-year interest rate for the current year. The appendix confirms that the results are also robust when using ten-year U.S. government bonds, which reflect longer-term borrowing costs.

Figure 3 plots the interest rate yield on 1-year and 10-year U.S. government bonds over time. It shows substantial variation in the U.S. interest rate over time, including the sharp increase in the early 1980s, the drop to near-zero rates following the Great Recession, and the persistence of these low rates until the end of our sample period. The figure also indicates the smoother movement of long-term interest rates compared to short-term interest rates.

U.S. government bond yields for 1-year (solid line) and 10-year bonds (dashed line) during the sample period, 1963–2017. Average bond yield per year, based on monthly data. Source: Authors’ calculations, based on Thomson Reuters Eikon.

Sample

We exclude the United States from our sample for theoretical reasons—we want to understand the effects of U.S. credit conditions on non-U.S. policymaking—but otherwise include data from as many countries as available through the Manifesto Project. Figure 4 displays the countries included in the sample. The sample comprises high- and middle-income countries and both OECD and non-OECD members. With control variables included, our sample covers 930 parties from 57 countries between 1963 and 2017. This amounts to 3,335 observations over 525 elections, with each observation corresponding to one party in one election-year. We retain the sample at this level of the party-election year because party manifestos are fundamentally a party-level phenomenon, and because this unit of observation allows us to address party-specific information (such as fixed effects or lagged outcome variables). Our results are robust to aggregating the data to the election-level, as we report in the appendix. Almost all countries in the sample—driven by choices made as part of the Manifesto Project—hold competitive elections (based on the corresponding index from the Database of Political Institutions) and are democracies (based on polity scores). We present results in the appendix when limiting the sample based on these variables.

Countries included in the sample (in gray) and countries without data on party programs (in white).

Our sample includes only election-years. This is not a concern for our independent variable, U.S. interest rates: they are plausibly exogenous to individual countries, and because elections happen at different points in time across countries, our sample is not limited to specific years or time intervals. The limitation to election-years might be an issue for our dependent variable, because we cannot observe party positions in-between elections. Even there, however, we have no reasons to expect systematic biases (and we lack systematic, cross-country data to assess any such biases): Our argument simply asserts that party manifestos are responsive to U.S. interest rates, regardless of when elections happen or what party positioning in-between elections looked like. In the appendix, we additionally show that our results are robust to limiting the sample to countries with presidential systems of government, where the timing of elections is largely exogenous (as opposed to parliamentary systems, with more discretion over the timing of elections through, for example, dissolution of the legislature and votes of no confidence).

Figure 5 shows the unconditional correlation between U.S. interest rates and the annual average of pro-business statements across all parties in the sample, with one observation per year. The figure reveals a strong correlation between the two variables. The linear correlation coefficient of 0.657 provides initial evidence that pro-business statements and U.S. interest rates are connected. Bivariate OLS regression on these annual data, consisting of 55 observations, yields a coefficient estimate for U.S. interest rates of 0.551, which, with a t-statistic of 3.73, is statistically significant at the 1 percent level. As noted before, U.S. interest rates almost certainly do not respond to party programs in individual countries, nor are they likely affected by the economic conditions of any single country, all of which reduce the likelihood of reverse causality as an explanation for the patterns observed in Figure 5.

Scatterplot of U.S. government bond yields and the annual average of pro-business statements during the sample period, 1963–2017; each dot represents one year in the sample. Pro-business statements are, on average, negative toward business. They become more pro-business (but remain negative overall) as U.S. interest rates increase.

We next turn to empirical specifications at the party-election year level, enabling us to include country-, party-, and time-specific control variables.

Specification

Our empirical models include a standard set of control variables, all lagged by one year. These include two correlates of U.S. interest rates: the annual U.S. GDP growth rate and the annual U.S. inflation rate (CPI).Footnote 57 Given the U.S.’s dominant role in the global economy, both variables are also linked to the global business cycle and, consequently, potentially to party programs. We also account for the domestic economic environment in each country by including the GDP growth rate, the domestic inflation rate (CPI), log GDP, and GDP per capita. All control variables are sourced from the World Bank. The baseline regression model is as follows:

$$\textit{party}\ \textit{statement}s_{p,i,t}=\alpha +\beta\ \textit{credit}\ \textit{condition}s_{t-1}+\gamma\ \textit{control}s_{i,t-1}+\epsilon _{p,i,t}$$

$$\textit{party}\ \textit{statement}s_{p,i,t}=\alpha +\beta\ \textit{credit}\ \textit{condition}s_{t-1}+\gamma\ \textit{control}s_{i,t-1}+\epsilon _{p,i,t}$$

where p denotes party, i denotes country, t denotes time, and controls is the vector of control variables. Our baseline estimate uses linear regression models with standard errors clustered by party to account for the persistence in party programs over time.

Regression results

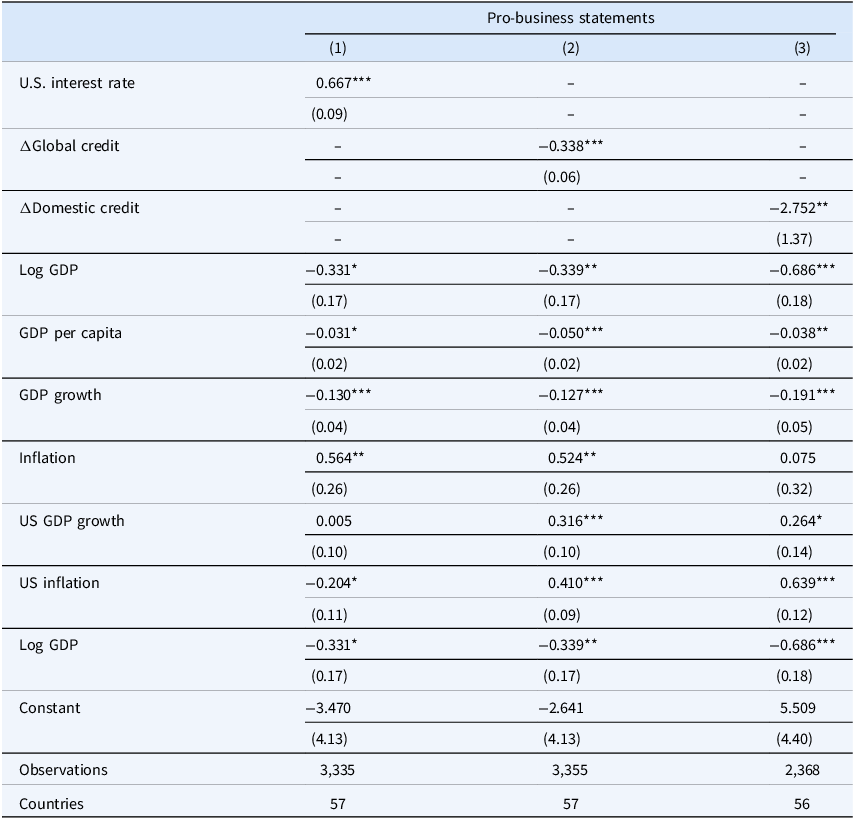

Table 1 shows our main regression results. As predicted by Hypothesis 1, higher U.S. interest rates correlate with a systematic shift toward pro-business party programs. The effects are also substantively meaningful. A one-standard-deviation increase in the interest rate on U.S. government bonds raises pro-business statements in other countries by approximately 2.14 percentage points, representing a 22 percent increase compared to the sample average.

Credit conditions and pro-business statements

Linear regression models, coefficient estimates and standard errors.

Significance: ***1%, **5%, *10%. Robust standard errors, clustered by party.

We observe similar findings for global credit conditions, measured by the extension of new credit across countries (column 2), and domestic credit conditions, assessed by the extension of new credit within each country (column 3). The results indicate that as domestic borrowers worldwide (column 2) and within a specific country (column 3) gain easier access to new credit, pro-business statements tend to decline; conversely, as access to credit diminishes, pro-business statements tend to rise.

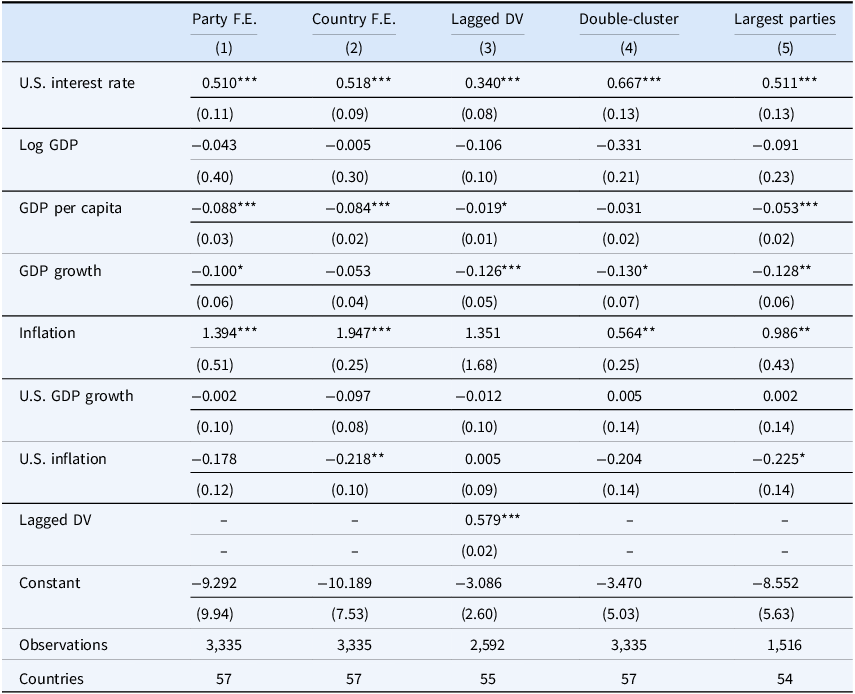

Table 2 presents a series of extensions and robustness checks. Column 1 in Table 2 includes party-fixed effects, such that the results are identified from changes within parties over time. This model accounts for baseline differences in pro-business statements across parties, and thus also for a party’s overall stance on partisanship or economic policy-making. We find that changes in U.S. interest rates lead to shifts in pro-market statements by the same parties.

Additional results—U.S. interest rates and pro-business statements

Linear regression models, coefficient estimates and standard errors.

Significance: ***1%, **5%, *10%. Robust standard errors, clustered by party.

Column 2 replaces party-fixed effects with country-fixed effects. These capture time-invariant country-specific variables, including aspects around the party system and electoral system, at least to the extent that these remain relatively constant over time, which might shape the ability of parties to move in the ideological space created by the party system. Column 3 includes a lagged dependent variable. This variable captures stickiness in party manifestos, and incorporates a range of potentially omitted variables ranging from the structure of the party system to time trends that in turn influence party manifestos. Column 4 estimates standard errors clustered by party and year to address the non-nested structure of our data. The impact of U.S. interest rates remains positive and statistically significant across all four models.

Column 5 in Table 2 includes only the three largest parties by vote share in each election. The effects of U.S. interest rates on pro-business statements are not substantively different in this sample, nor are they statistically significant when including an interaction instead of splitting the sample (not reported). This result indicates that the effects of U.S. interest rates are not limited to fringe parties or driven by the emergence of new ones. Changes in U.S. interest rates instead also influence how mainstream political parties discuss business interests.

In the appendix, we repeat these same modifications for the other two measures of credit conditions. We obtain similar results for global credit conditions (the coefficient estimates fails to reach statistical significance at 5 percent in one specification). For domestic credit conditions, the results are more mixed: we obtain similar coefficient sizes as before, but the coefficients fail to reach statistical significance at conventional levels. These patterns arguably reflect that domestic credit conditions are stickier than U.S. interest rates, because they involve (slow-moving and country-specific) debt stocks.Footnote 58 As a consequence, any changes in domestic credit conditions over time within countries are far from exogenous but virtually guaranteed to be a response to country-specific political and economic conditions. In the following, we restrict our models to using U.S. interest rates as a reliably exogenous indicator of credit conditions.

Additional analyses

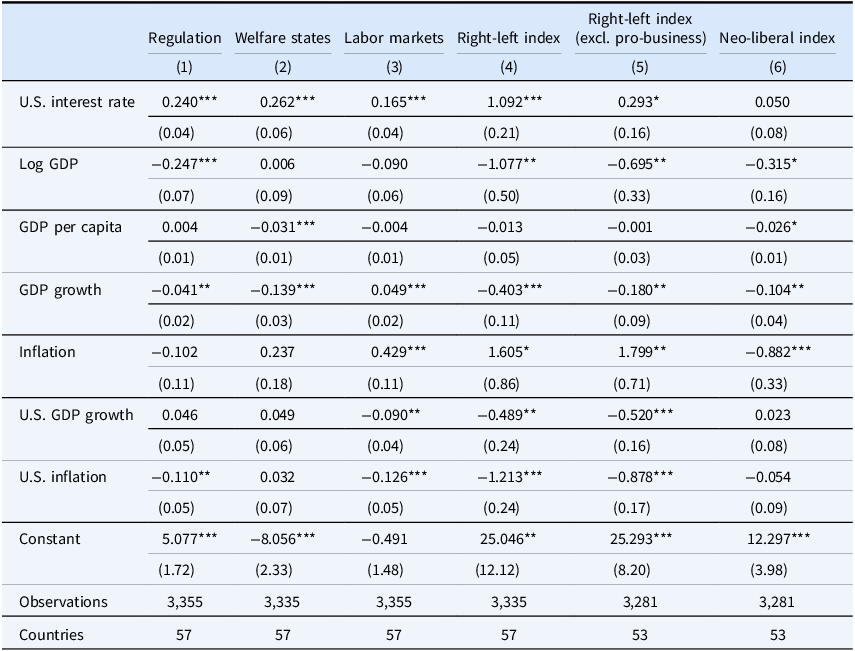

In Table 3, we examine more closely the different components of our measure of pro-business statements and provide additional results for context. Columns 1, 2, and 3 present results for the individual components of the composite measure, focusing on regulation, welfare states, and labor markets, respectively. The impact of U.S. interest rates is statistically significant at the 1 percent level in all three models, indicating that these effects span key political domains.

U.S. interest rates and pro-business statements—components and context

Table 3. Long description

A table with six columns and six rows of data, plus a row for constants and observations. The columns are labeled Regulation, Welfare states, Labor markets, Right-left index, Right-left index excluding pro-business, and Neo-liberal index. The rows represent different variables: U.S. interest rate, Log GDP, GDP per capita, GDP growth, Inflation, U.S. GDP growth, U.S. inflation, and Constant. Each cell contains numerical values with standard errors in parentheses. The table shows the impact of these variables on different political and economic components, with statistical significance indicated by asterisks. The observations and number of countries are also listed at the bottom.

Linear regression models, coefficient estimates and standard errors.

Significance: ***1%, **5%, *10%. Robust standard errors, clustered by party.

The model in column 4 considers whether the “pro-business” movement noted above is better understood as a more general move towards the political right, using the Manifesto Project’s right-left partisanship index as the dependent variable. The results indicate that an increase in U.S. interest rates correlates with a general rightward shift in party programs. However, this rightward shift is primarily driven by a transition toward pro-business statements rather than a move toward other policies typically associated with the right-left dimension. When we exclude components from the right-left index that are also part of pro-business statements (as shown in column 5), the effect of U.S. interest rates significantly decreases and loses statistical significance at the 5 percent level.Footnote 59

A final model in column 6 examines whether the relationships we interpret as evidence that politicians are catering to domestic businesses might be better understood as politicians catering to capital interests in general, creating a turn toward neo-liberal politics more broadly. We use a dependent variable that combines support for supply-side policies, free trade, open markets, pro-growth paradigms, and economic orthodoxy while subtracting support for economic planning, protectionist trade policies, demand-side strategies, government control of the economy, and anti-growth paradigms.Footnote 60 These variables align with a neo-liberal policy paradigm but are less clearly demanded by domestic businesses. They reflect generalized capital interests rather than those held by domestic firms. As expected, we find a substantively small and statistically insignificant effect of U.S. interest rates on this variable, indicating that U.S. interest rates do not lead to a broader shift toward neo-liberal politics. The change in rhetoric seems targeted at the interests of domestic firms facing higher credit costs rather than mobile foreign investors.Footnote 61

Salience vs. content

To further explore the interpretation of our results, we replace our dependent variable with the “policy importance” measure developed by Lowe et al. (2011), which reflects how much space parties allocate to a specific topic in their manifestos, regardless of their stance. Instead of calculating the difference between statements that support and oppose specific topics, we calculate the total sum and take the log.

The results, reported in the appendix, indicate that parties allocate significantly less space to discussions of the welfare state or labor markets as U.S. interest rates rise. This suggests that the effects we identified above reflect less a shift toward anti-welfare state and anti-labor politics and more a reduction in any pro-welfare state and pro-labor remarks. In contrast, we observe a substitution effect for statements regarding regulation and laissez-faire politics, resulting in more statements supporting deregulation and fewer statement supporting regulation. The shift toward pro-business politics we uncovered therefore happens through a combination of emphasizing deregulation and downplaying a commitment to welfare states and labor.

Partisanship

In the appendix, we include a series of additional results exploring the role of partisanship. First, we show that we observe similar shifts toward pro-business statements during periods of high U.S. interest rates regardless of a party’s left-right position in the previous election, resulting in shifts toward pro-business statements across the entire party system. We find, similarly, no significant differences across parties when considering the components of pro-business statements separately (welfare policies, labor policies, regulatory policies), replicating the models in the first half of Table 2.

Second, and strikingly, we do find differences when it comes to the importance that parties attach to these dimensions (using again the approach proposed by Lowe et al. (2011), as above), revealing a subtle pattern: An increase in global interest rates has similar effects for left-wing and right-wing parties in moving their overall stance, but left-wing and right-wing parties do so in different ways: compared to right-wing parties, left-wing parties respond by devoting less space to discussing labor and regulatory policies in their manifestos. We thus observe a difference between a more “pro-business” right and a less “anti-business” left, which results in similar movements in the aggregate stance of parties on the left and right toward business.

These results offer a middle ground between two different strands of literature. On the one hand, right-wing parties are expected to be more beholden to business interests, and might thus be more responsive to high U.S. interest rates.Footnote 62 On the other hand, partisanship might a limited role in the context of financial globalization, which exerts pressures on governments across the board.Footnote 63 Partisan differences might be further muted if left parties perceive a stronger need to signal that they are not anti-business;Footnote 64 if they are better able than right-wing parties to compromise with labor groups on support for pro-business policies;Footnote 65 or if left-wing parties need to be less concerned about losing loyal voters, in part because there are few viable alternative parties voters could defect to.Footnote 66 Our results suggest, while partisan differences do indeed disappear in the aggregate, partisan still exist on perhaps more subtle dimensions, consistent with recent work on enduring partisan differences in government interactions with global bond markets.Footnote 67

Time trends and interest rate shocks

Our main analyses associate interest rate levels with party manifestos. In the appendix, we present a series of additional results to address time trends and the role of unusual interest rate movements.

Binary interest rates. Our main analysis relied on a continuous measure of U.S. interest rates. In the appendix, we show that our results are robust to dichotomizing this variable, with a value of 1 when U.S. interest rates are above 5 percent (which corresponds to the sample median). We additionally present results when using alternative cut-offs for “high” interest rates. We have no clear-cut expectations about the resulting patterns, and interpret these purely descriptively: a movement from 2 percent to 3 percent happens in an environment of persistent low interest rates but indicates a large relative change, suggesting that lower thresholds might be more meaningful; a movement from 6 percent to 7 percent represents a modest relative change but occurs at a point where interest rates already present a major strain on markets, suggesting that a higher threshold might be more meaningful.

Time trends. It is challenging to separate the correlations we report from other time trends that might induce both cycles in U.S. monetary policy and pro-business statements. While we sought to account for the dominant alternative explanations, including macro-economic trends, we cannot rule out other time-varying variables driving this association, such as a broader move toward neo-liberal politics during the sample time frame. Our results are robust to including a linear time trend, which is, however, fairly restrictive. As Figure 3 indicates, U.S. interest rates during our sample period follow a quadratic trend; accordingly, including a quadratic or cubic year trend is highly correlated with U.S. interest rates and the results lose statistical significance.

We pursue several alternative approaches to separate the association we report from other trends. First, the results are robust when dichotomizing the variable for U.S. interest rates, as described above, and then including a cubic year trend. Second, the results are robust when controlling for neo-liberal party statements. We report these results in the appendix. Third, we reported above results using a lagged dependent variable, which captures temporal dynamics as well. Fourth, while the results for U.S. interest rates lose significance when including a year polynomial, the results for short-term credit exposure retain significance. Finally, we discuss several results in the following based on changes in interest rates and interest rate shocks, which capture deviations from trends and thus effectively account for time trends.

Changes in interest rates. We also present results from a first-difference model that associates election-to-election changes in party manifestos with election-to-election changes in U.S. interest rates. We obtain similar results in this model: increases in U.S. interest rates are associated with movements toward more business-friendly party manifestos.

Interest rate shocks. Sudden movements in interest rates, as deviations from what markets expected, should be particularly relevant in our framework. In the appendix, we consider three approaches to identify such deviations from market expectations. First, we present results when using a Hodrick-Prescott filter, a common approach to address cyclical fluctuations in economic data, to detrend interest rates. Second, we present results when calculating deviations from the predicted interest rate based on monthly interest rates in the preceding 12 months. This measure captures deviations from the contemporaneous trend using a continuous measure. Third, to identify sharp discontinuities, we consider whether the interest rate is outside the 95 percent confidence interval of the predicted interest rate, again based on monthly interest rates over the preceding 12 months. This yields a dichotomous measure of interest shocks and reflects not just the trend but also the variability of interest rates over the past 12 months: if interest rates fluctuate more around the trend line, the uncertainty around the prediction increases, and we would need to observe even larger deviations from the trend to fall outside the confidence interval of the prediction. The results remain robust to all three measures. These models also effectively address concerns over time trends, because they model the key predictor as a deviation from pre-existing trends.

Additional results

In the appendix, we present several additional results. These models corroborate the key findings: higher US interest rates are associated with more business-friendly party programs.

Aggregation. Our models so far are estimated at the level of the party-election year. These allowed us to consider party-specific information. In the appendix, we instead aggregate the data to the election-level, averaging information across parties. We also present results from weighted regression models, using a party’s vote share as weight, to capture the relative political relevance of each party and arrive at a measure of the political “center of gravity.”Footnote 68

Political and institutional context. Above, we already controlled for country-specific context through fixed effects. However, because our sample covers a time span of over half a century, few aspects of politics might be time-invariant. For example, party systems in many countries have undergone dramatic change over this time frame, and even some established democracies have seen institutional change to the electoral system, for example. In the appendix, we explicitly account for some of these contextual factors by including control variables for the system of government (presidential vs. parliamentary), the electoral rule (plurality vs proportional representation), the number of parties, and central bank independence.

Sample. In the appendix, we present results when dropping high-income OECD countries from the sample. Additionally, we present results when limiting the sample to countries with presidential systems of government, where elections are plausibly exogenously timed. This rules out that election timing responds to local economic conditions, which in turn might be responsive both to U.S. interest rates and drive the business-friendliness of party programs. We also show that the results are robust to limiting the sample to left-wing parties only, which are the parties that are not already leaning toward pro-business statements. Finally, we present results when limiting the sample to democracies (as defined by polity scores) and when limiting the sample to countries with competitive elections (as defined by the corresponding indicator from the Database of Political Institutions), as well as when including these as control variables in the full sample.

Conditional hypotheses

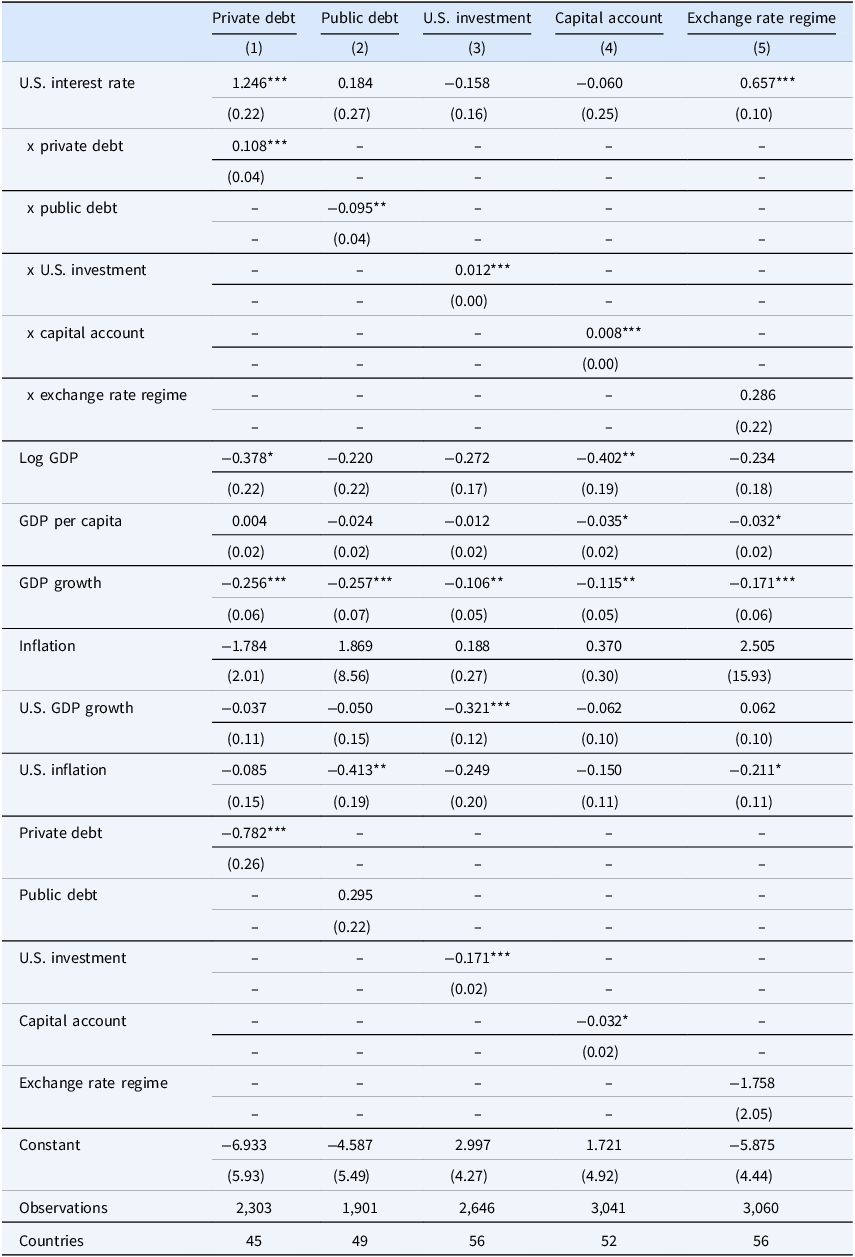

Our final set of models turns to the conditional hypotheses that examine the credit channel of transmission of U.S. financial conditions. The regression results are reported in Table 4. We show the marginal effects in Figure 6.

Conditional models—U.S. interest rates and pro-business statements

Linear regression models, coefficient estimates and standard errors.

Significance: ***1%, **5%, *10%. Robust standard errors, clustered by party.

Marginal effect of a one standard deviation increase in 1-year U.S. interest rates across short-term private debt, U.S. investment position abroad, and capital account openness, based on Table 4, column 1 (left panel), column 3 (middle panel), and column 4 (right panel).

Figure 6. Long description

Three separate line graphs illustrate the marginal effects of different economic factors. Panel A: The line graph shows the effect by short-term private debt. The x-axis represents short-term private debt with values ranging from -12.5 to 2.5, and the y-axis represents the marginal effect ranging from -2 to 4. The data points show an upward trend as short-term private debt increases. Panel B: The line graph shows the effect by U.S. investment position. The x-axis represents the U.S. investment position with values ranging from 0 to 60, and the y-axis represents the marginal effect ranging from -2 to 2. The data points show a slight upward trend as the U.S. investment position increases. Panel C: The line graph shows the effect by capital account openness. The x-axis represents capital account openness with values ranging from 0 to 100, and the y-axis represents the marginal effect ranging from -2 to 2. The data points show a slight upward trend as capital account openness increases.

Short-term domestic financing needs

Our first conditional hypothesis (Hypothesis 2) suggests that the impact of U.S. interest rates should be largest where domestic borrowers have immediate financing needs. Economies with borrowers who depend on short-term debt should be most sensitive to tightening credit conditions, and political parties in these countries should be likeliest to adjust their politics as credit markets shift. We test Hypothesis 2 by interacting U.S. interest rates with a country’s short-term external debt position. We identify short-term debt by focusing on the remaining debt maturity rather than the maturity at the time the debt was issued. The benefit of using the remaining maturity is that it captures the immediate refinancing needs of borrowers, regardless of their past ability to issue long-term debt, which depends on their perceived creditworthiness and the prevailing interest rate environment. We adhere to standard classifications, considering debt as short-term if the remaining maturity is one year or less.

We create two short-term debt exposure variables using data from the Bank of International Settlements: debt securities issued by private borrowers and debt securities issued by the central government. We normalize both variables by GDP and log the resulting measures. The distinction between debt issued by private borrowers and debt issued by governments allows us to identify whether changes in U.S. interest rates are indeed associated with pro-business statements because domestic firms feel more squeezed by higher borrowing costs, as our framework emphasizes.Footnote 69

The first two columns of Table 4 present results using our primary dependent variable, pro-business statements. The findings indicate that U.S. interest rates have more significant effects on pro-business statements when domestic private borrowers face more immediate financing needs (column 1) but not when the domestic government has more extensive immediate financing needs (column 2). In this latter model, the interaction term is negative; however, the marginal effect remains positive and statistically significant at the 5 percent level across the full range of public debt loads in the sample.

The left panel in Figure 6 displays the marginal effect of a one standard deviation increase in U.S. interest rates, evaluated across observed values of short-term external debt by private issuers. The histogram in the figure’s background displays the distribution of debt loads in the sample. The effect of U.S. interest rates is almost precisely zero and statistically insignificant for observations with the least short-term external debt. That effect increases substantially as debt loads increase. U.S. interest rates’ marginal effect on political rhetoric is statistically significant and positive beyond a value of about −9 (the debt variable is on the log scale), which applies to over 95 percent of the sample. This is also in line with our theory. Higher borrowing costs should not lead to more business-friendly political politics if private-sector borrowers do not have much debt that needs to be refinanced.

Prominence of U.S. banking

Our second conditional hypothesis (Hypothesis 3) suggests that the impact of U.S. interest rates on party manifestos should increase as U.S. banking becomes more prominent in the international financial system. We evaluate this hypothesis by interacting U.S. interest rates with the U.S.’s international investment position in banking and finance as a percentage of GDP. We obtain data on the U.S. investment position from the Bureau of Economic Analysis, which captures U.S. investment abroad. These are systemic indicators that vary only by year. U.S. banking’s role increases over time nearly every year.

The results of these regressions are in column 3 of Table 4. The interaction term is positive and statistically significant, indicating that party manifestos’ response to U.S. interest rates increases with the prominence of U.S. finance. The middle panel of Figure 6 displays the substantive size of these effects for a one-standard-deviation increase in U.S. interest rates. The background histogram shows the variable’s distribution in the sample. The impact of U.S. interest rates is close to zero and statistically insignificant when U.S. finance occupies a less critical role and increases considerably with the growing dominance of U.S. finance in global markets.

The dilemma: the capital account and the credit channel

Finally, we consider whether the effects of U.S. interest rates depend on the openness of the capital account. This conditional relationship is relevant because our framework looks for the transmission of U.S. monetary shocks to domestic firms through the credit channel, which requires open capital accounts.Footnote 70 Without open capital accounts, there is less of a plausible connection between U.S. interest rates and the business-friendliness of politics outside the U.S. We assess the role of capital account openness by interacting U.S. interest rates with the CAP100 measure of capital account openness.Footnote 71 CAP100 ranges from 0 to 100, with 0 indicating a wholly closed capital account and 100 indicating a fully open one. The right panel of Figure 6 shows the marginal effect of a one-standard-deviation increase in U.S. interest rates evaluated across a range of values for capital account openness. As can be seen, the effect increases for countries with more open capital accounts and is statistically significant at values of CAP100 above 50. No such impact is indicated in countries with closed capital accounts.

We emphasize two key observations. First, this effect becomes statistically significant precisely at the point that binary definitions of capital account openness distinguish between “open” and “closed” capital accounts. Second, these low values become increasingly rare in our sample over time. While 25 percent of the pre-1975 sample has a CAP100 score below 50, less than 10 percent of the post-1975 sample does. Only one country in the sample—Sri Lanka—has a score after 1975 in one of the two lowest categories, where the effect is nearly zero. Even more strikingly, after 2000, less than 5 percent of the sample (7 elections from four countries: Albania, Greece, Hungary, and Ukraine) have CAP100 scores below 50, and no country has a score lower than 25. Put differently, U.S. interest rates have had a statistically significant effect for almost the entire past two decades. The widespread shift to open capital accounts since the end of Bretton Woods has created an environment for a nearly universal effect of U.S. interest rates on the domestic politics of countries worldwide.

Finally, the model reported in column 6 of Table 4 shows that the effect of U.S. interest rates is not conditional on the exchange rate regime. We interact U.S. interest rates with an indicator coded 1 if a country’s exchange rate is floating and 0 otherwise.Footnote 72 We find no evidence of a conditional effect. These results provide further evidence consistent with Rey’s “dilemma” framework—governments can hardly insulate themselves from global markets through capital account policies, and not at all through the exchange rate regime.

In the appendix, we also consider the role of central bank independence. Here, one might have more mixed expectations. On the one hand, central banks are effectively constrained by global monetary conditions, whether they are independent or not (Rey Reference Rey2015). On the other hand, policy-makers might nonetheless attempt to manipulate monetary policy to convey that they are “doing something”—even if that “something” eventually turns out to be ineffective and would have to be reversed in the face of capital outflows. It is not clear, a priori, whether policy-makers would consider this a worthwhile trade-off, and a full assessment of such mostly symbolic policy-making through ineffective monetary policy would require a more developed account of the domestic politics behind such choices. Empirically, we find mixed evidence for a moderating role of central bank independence. We find evidence for some sub-components of central bank independence,Footnote 73 in particular for independence of policy formulation, but not for overall levels of central bank independence.

Section IV: Conclusion

Global credit cycles, influenced by U.S. interest rates, shape businesses’ access to capital. Consequently, we argue, these cycles compel governments to adopt business-friendly political positions to mitigate costs for firms. We highlight how these global financial cycles affect politics through a domestic constituency channel, complementing significant literature that illustrates how financial globalization influences politics through the necessity for governments to attract mobile international investors.

Our account of financial globalization’s political impact offers several innovations. First, we locate the origins of globalization’s impact in the U.S. financial system and U.S. monetary policies. This approach aligns with Oatley et al. (Reference Oatley, Winecoff, Bauerle Danzman and Pennock2013), Winecoff (Reference Winecoff2015) and other studies on global growth and financial stability, but introduces a novel perspective for understanding globalization-induced policy convergence. Second, we highlight the government’s support for domestic firms as the primary mechanism through which financial globalization influences politics. Third, we explain how this leads to a distinct style of pro-business, but not necessarily neo-liberal, politics.

This account has the potential to explain changes in an era of largely unfettered capital mobility, where existing accounts tied more closely to the needs of mobile investors would be more limited. Indeed, our results indicate that U.S. monetary policies have the strongest effects precisely when existing accounts would lead us to expect little variance in outcomes: in the past few decades, when capital accounts were almost universally open across our sample.

Our results also highlight how financial hegemony interweaves U.S. political and economic power. The global economic order, supported by the U.S. since World War II, is consistent with business-friendly politics. These same policies have buttressed the U.S. financial system’s dominant role globally. During periods of high interest rates, that dominant role, in turn, has facilitated the spread of business-friendly policy positions.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/bap.2026.10025.

Data availability statement

All data and code to replicate the analyses will be made publicly available upon publication.

Acknowledgements

We appreciate many helpful comments from Timon Forster, Dennis Quinn, participants at the Center for Political Studies Workshop at the University of Michigan, and audiences at the Annual Conferences of the American Political Science Association, the Midwest Political Science Association, the European Political Science Association, and the International Political Economy Society.

Funding statement

Timm Betz acknowledges support from the In_Equality Cluster of Excellence at the University of Konstanz, funded by the Deutsche Forschungsgemeinschaft (DFG—German Research Foundation) under Germany’s ExcellenceStrategy—EXC-2035/2 – 390681379.

Competing interests

The authors have no conflict of interest or competing interest to disclose.

Open access

Open access