Key messages

Chapter 3.2 covers the way hospitals are paid. Methods for paying hospitals vary across countries and include fee-for-service (FFS), block contracts, line-item budgeting (where purchasers specify exactly what funds are used for) and activity-based funding (with a fixed rate for each episode of care independent of the hospital’s costs of care). Increasingly, pay for performance (P4P) elements are also used. Key learning includes that:

Third-party purchasers: government agencies, social health insurance (SHI) funds or insurance companies provide the bulk of hospital revenue giving them levers to shape provision.

Purchasers and hospitals have distinct objectives that are not always aligned – purchasers will pursue the best quality of care at the lowest price for their covered population while hospitals seek stable revenue streams to cover their costs.

Information asymmetries give hospitals advantages over purchasers.

Purchasers use payment methods and financial rewards to incentivize the volume and quality of care, patient-mix and management effort they want. There are complex challenges around:

○ specifying the details;

○ negotiating effective contracts; and

○ managing payment systems.

Monitoring outputs and safeguarding quality requires structures and systems which are costly.

Reforming funding or transitioning from one payment model to another is often a long process that demands sophisticated design and careful implementation.

Introduction

In most countries the greater proportion of hospital income does not come from patients themselves paying for the care they received. Instead, as detailed in section 1 of this volume, it comes from third-party payers: in tax-based health systems, these payers are government agencies; in social and private insurance-based systems, the payers are sickness funds and insurance companies (see chapters 1.1 and 1.3). Whatever their form, payers share a common set of general funding objectives when it comes to how they pay hospitals, but they may prioritize these objectives differently, and their priorities may change over time.

In this chapter, we discuss the dynamics of the payer–hospital relationship: how payers can use the financial rewards or incentives built into contracts to try and reach their goals and how hospitals use informational advantages about the provision of care to pursue their objectives.

We begin by discussing the relationship between the payer and the hospital and key considerations in any funding policy. Next, we outline the respective funding objectives of payers and hospitals and set out four distinct payment models: line-item budgeting, FFS, block contracts and activity-based funding. We then go on to examine the factors influencing design choice, namely the number of payers and hospitals in the system, what weight payers attach to each objective, and the effort involved in designing and managing the payment mechanism. We consider the issues involved in transitioning from one payment mechanism to another and discuss how to incorporate quality in payment design. Finally, we review the practical issues involved in paying hospitals, by way of a case study of changes in England’s National Health Service (NHS) hospital payment methods between 2002 and 2021. We conclude that there is no “best” payment model, the choice being critically dependent on system characteristics and capacity and related to which objectives the payer wishes to prioritize.

The payer–hospital relationship

Health systems differ widely in their number of payers and hospitals. At one extreme, in a health system in which everybody pays the full cost of care themselves, there are as many payers as there are patients. At the other extreme, patients pay nothing out of pocket (OOP) but instead a single payer, usually a government body, takes responsibility for paying for care. Between these extremes, other health systems feature multiple payers, such as insurance companies, sickness funds or regional health authorities. On the hospital side, some small countries have only a single hospital; in other countries there are many hospitals, sometimes located quite close to each other and, perhaps, in competition with one another. In due course, we shall argue that the number of payers, in particular, and, to a lesser extent, the number of hospitals, are key factors in the choice of payment method.

The choice of payment method is also determined by what payers and hospitals wish to achieve and the system context. To help shape the discussion that follows, we start with a stylized health system with a representative payer and a representative hospital, each with their own set of interests and objectives. We use a principal–agent set-up to describe their relationship, in which the principal (here, the payer) uses a contract (the payment method) to encourage the agent (the hospital) to work in the principal’s interest.

This principal–agent relationship is likely to be imperfect, for two main reasons. First, even if the payer and hospital share some common objectives, they will not coincide exactly. The payer and hospital may attach different weights to those objectives that they have in common, and there might be some objectives that they do not share. The payer uses the contract to better align the interests of the hospital with its own objectives, offering the hospital some form of reward (usually financial) if the hospital does what the payer wants.

Second, the hospital will enjoy informational advantages over the payer: the skills of the payer (priority-setting, pricing, benchmarking) are normally quite different from those of the hospital (operational management and service delivery). As such, the hospital will normally be better placed than the payer to know which combination of inputs (skills, technology) is most likely to lead to the best outcome for an individual patient, and the average and marginal cost to the hospital of treating the patient in this way. But the hospital might exploit informational advantages to further its own interests, both during contract negotiation and in contract delivery (Mühlbacher, Amelung & Juhnke, Reference Mühlbacher, Amelung and Juhnke2018; Jiang, Pang & Savin, Reference Jiang, Pang and Savin2020). During negotiations, the hospital might be able to secure a more generous contract by quoting a higher price than if both parties were equally informed about precisely what work was involved and the marginal cost of that work. If the hospital exploits this advantage, it would mean the payer ends up paying more than it needs to get the job done. Alternatively, or additionally, the hospital might fail to fulfil its contractual obligations in full, perhaps by not delivering contracted services to a professional standard, or perhaps, discharging patients before they have recovered sufficiently to be able to cope at home. To guard against such possibilities, the payer might include specific incentives in payment method design, notably to safeguard quality, as we shall discuss later, and may need to monitor delivery and threaten sanctions if delivery is not to the desired standard.

Key elements of hospital funding policy

In an ideal world hospital funding policy would ensure that the right member of the health care team enables the right care to be delivered, in the right setting, on time, every time, at the right cost (see e.g. Nowak et al., Reference Nowak2012). Hospital funding design should also anticipate and address potentially perverse incentives which militate against achieving the broad overall policy; for example, by encouraging hospital admissions rather than care in the community when the latter might be more cost-effective.

Funding policy has two key elements: the design of payment flows, and the conditions or rules associated with the payment flow. These need to reinforce each other, reduce the risk of gaming and perverse incentives (Steinbusch et al., Reference Steinbusch2007) and capture the nuances required in a comprehensive funding policy. Policy-makers in different jurisdictions undertaking funding reform will face different challenges – including availability of information, industrial relations constraints, providers’ management skills – and, consequently, the choice of payment model will partly reflect these local issues.

Different funding designs can emphasize one objective over another, and the priorities for different objectives will change over time, but we can consider the main objectives typically seen in hospital funding policy (Geissler et al., Reference Geissler and Busse2011).

Payer objectives: how they affect payment model design

From the payer´s perspective, there are four key issues to consider when designing how to pay hospitals: the number and type of patients to pay for, the quality of care, how much to pay hospitals, and how much effort the payer has to put into managing the payment method(s).

Issue 1: number and type of patients

Payers want the payment model to provide incentives for hospitals to treat patients, but specifying this incentive is challenging, again for two main reasons. First, while it is straightforward to quantify patient numbers, it is more difficult to take account of differences between patients: some are admitted for fairly routine operations, many are admitted without warning in need of immediate emergency care, some require ongoing care for multiple long-term conditions. As we shall see, one of the key distinguishing features of alternative hospital payment models is in how different types of patients are described.

The second difficulty in designing a payment model to incentivize treatment is that it might be better for some people to receive their care in settings other than the hospital. Payers want to ensure that unnecessary admissions are minimized, these being potentially preventable hospitalizations and those offering no or low-value care. However, there is information asymmetry between the payer and hospital on the need for admission, as hospitals will have more information about the patient’s health status at the point of admission than the payer. Measurement tools for no and low-value care and potentially preventable admissions are not sufficiently refined to make case-by-case determination of the potential benefit of admissions but may be able to be used for retrospective monitoring.

Issue 2: quality of care

Defining quality of care is also tricky. Its definition needs to capture concepts associated with how hospitals are organized (structure), how patients are managed (process), and how health problems are addressed (outcome). Typically, quality has been poorly defined in the design of hospital payment arrangements, though that is beginning to change.

The simplest funding design includes an implicit assumption about the quality of service provision, the hope being that payers and hospitals attach equal weight to quality, such that it will not be compromised. However, because it might be costly to provide higher-quality services and quality is difficult to measure, hospitals might reduce quality in order to treat more patients, especially if this generates higher revenue. This might be manifested as poorer process quality, such as patients having to wait a long time before their hospital appointment. Delayed access may then exacerbate their health problem, thereby proving more costly than quicker access, and long waits for access could cause reputational damage to payers and their political overseers; and/or health outcomes might be compromised. Alternatively, hospitals might discharge patients from hospital too early, transferring responsibility for care and shifting costs onto the family and primary or community care providers, a phenomenon dubbed “quicker and sicker discharge”, which has been the subject of many studies (Kosecoff et al., Reference Kosecoff1990; Qian et al., Reference Qian2011). Other adverse quality consequences are harder to assess, but recently funding policies have elaborated on the quality dimensions of funding design so as to explicitly incorporate factors related to clinical quality, patient experience, patient-reported outcomes, timeliness, appropriateness and other aspects of care valued by patients and payers. We discuss incentives for high-quality care below (sometimes called P4P).

Issue 3: size of payment

The payer’s utility is decreasing in the amount it pays to the hospital: given the choice, the payer would prefer to make lower payments to the hospital and this might motivate the payer to design a payment system that encourages efficient practice by the hospital. These payments will be related to the amount of money that the payer has available to meet its objectives. Ensuring that the payer pays the “right” amount to hospitals is an important overall policy goal. But there are two quite distinct ways in which the “right amount” can be expressed: the total amount to be paid for all patients to be treated, or the amount for each patient individually. If the payer is a government agency, the total amount may take the form of a budget constraint imposed by the government, and might reflect the size and composition of the population served. If the payer is a sickness fund or insurance company, the amount will depend on the insurance premiums made by its enrollees but also other contributions such as co-payments. If there is no third-party funding, with patients having to pay for everything themselves, the constraint reflects the financial resources each individual patient has available.

In any system – whether tax-based, insurance-based or privately funded – there are trade-offs in how money is spent. More spending on hospital care means individuals or societies have less to spend on other types of health care or on other individual or social goals. The ideal is that the marginal benefit of any increment in spending on hospitals yields the same marginal benefit as an investment in public health, primary care, education, defence, transport or anything else. In a publicly funded system, governments make decisions about total spending on health, and within health portfolios, on hospitals, given the budget constraints of the payer. The calculus behind these decisions might involve sophisticated analysis of marginal benefits and marginal costs using techniques such as programme budgeting and marginal analysis (Tsourapas & Frew, Reference Tsourapas and Frew2011; Kapiriri & Razavi, Reference Kapiriri and Razavi2017), but are more likely to be shaped by path dependency, history and politics in assessing what marginal changes can be implemented in the current budget.

Recognizing that resources are scarce and choices have to be made, an objective of hospital funding policy might be to control total hospital spending, to keep within the resources available to the payer. A related funding objective would be to give hospitals incentives via the payment system to pursue technical efficiency, namely to treat patients at lowest cost, subject to there being no adverse quality consequences. Objectives about promoting efficiency can only be pursued with reasonable amounts of effort by the payer if there are robust ways of measuring the quantity and quality of care that hospitals provide. These two funding ambitions – about controlling total expenditure or ensuring optimal efficiency – can be met simultaneously. However, it is much more common for one objective to be emphasized over another, or for efficiency objectives to be seen as part of the strategy to achieve expenditure control.

Issue 4: amount of management effort needed

In designing a payment model, the payer will also consider how much effort they – and hospitals – have to put into negotiating and managing the contract, making the payer averse to implementing a payment system with overly complex design features or contract monitoring requirements, especially in places where the capabilities to implement and manage a complex payment system are in short supply. We discuss this issue in more detail below.

Hospital objectives

We turn now to what hospitals wish to achieve. Like the payer, the hospital also cares about the number and type of patients treated and the quality of care they receive. If the payer and hospital attach exactly the same weight to these concerns and provision of care is costless, there would be no need for a contract: the hospital would do what the payer wants, without needing to be asked. This situation is referred to as perfect agency. But, in practice, the interests of the payer and hospital are likely to differ. They might disagree about how many and which type of patients should be admitted to hospital; they might also have different views about the appropriate quality of care. In addition, hospitals are concerned that their income covers their costs and enables them to function; and that the payment system can be managed to serve their interests.

Sufficient income to cover costs

The main reason that the interests of payer and hospital differ is that provision of health care is not costless. The hospital has to employ a variety of labour and capital resources in order to deliver care, incurring various costs in the process. Consequently, the hospital requires a stream of revenue to ensure that it can function. The hospital will be concerned that the money received from the payer is at least sufficient to cover these costs. The more that the hospital is driven to make its income from the payer exceed its costs – be that by increasing the former or by reducing the latter – the greater the weight it will place on this element in its objective function.

A manageable model

It also takes effort to manage the contract with the payer – directly (in terms of the hospital’s administrative burden) and indirectly (in terms of how stretching the contract’s terms are on the hospital’s staff). Like the payer, the hospital might prefer a simpler payment model, with minimal reporting requirements. This preference will be driven partly by a desire to reduce its administrative burden, but a simpler model might also provide greater scope for the hospital to increase the surplus of its revenue over its costs, by exploiting its information advantages. For this reason, the payer might not choose to adopt the simplest payment model.

Hospitals as “multi-product” firms

Hospitals may be characterized as multi-product firms, and so payment policy must recognize and pay fairly for all appropriate services, with “appropriate” here being from the perspective of the payer. If paying for activity, payers will need to ensure that activity is appropriately described. Diagnosis-related groups (DRGs) are the most common classification for inpatient activity but cannot be used for outpatient activity, and have poor explanatory power for mental health activity and other activity, such as rehabilitation, so service-specific classifications have been proposed in these areas (Jackson & Sevil, Reference Jackson and Sevil1997; Mason et al., Reference Mason2011; Sutherland & Walker, Reference Sutherland2007). As well as caring for patients, some teaching hospitals engage in the education and training of future generations of health professionals and undertake research, which also need to be paid for in some way.

Better payment models minimize the extent to which the characteristics of providers are used in funding design, emphasizing payment for what is provided rather than who provides it. The one exception to this rule is for smaller hospitals – typically located in rural areas – where a key role of the hospital is ensuring access in these areas. Here, alternatives to standard payment methods will be required to protect viability and ensure an appropriate service response to community need (Holmes, Pink & Friedman, Reference Holmes, Pink and Friedman2013; Murphy, Hughes & Conway, Reference Murphy, Hughes and Conway2018).

Payment methods for hospitals: four key types

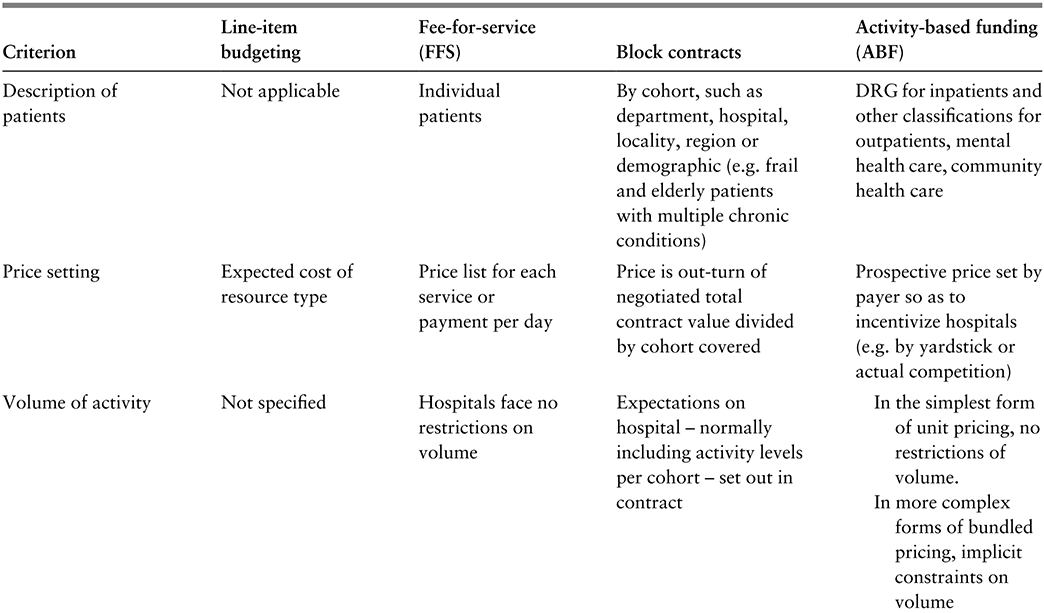

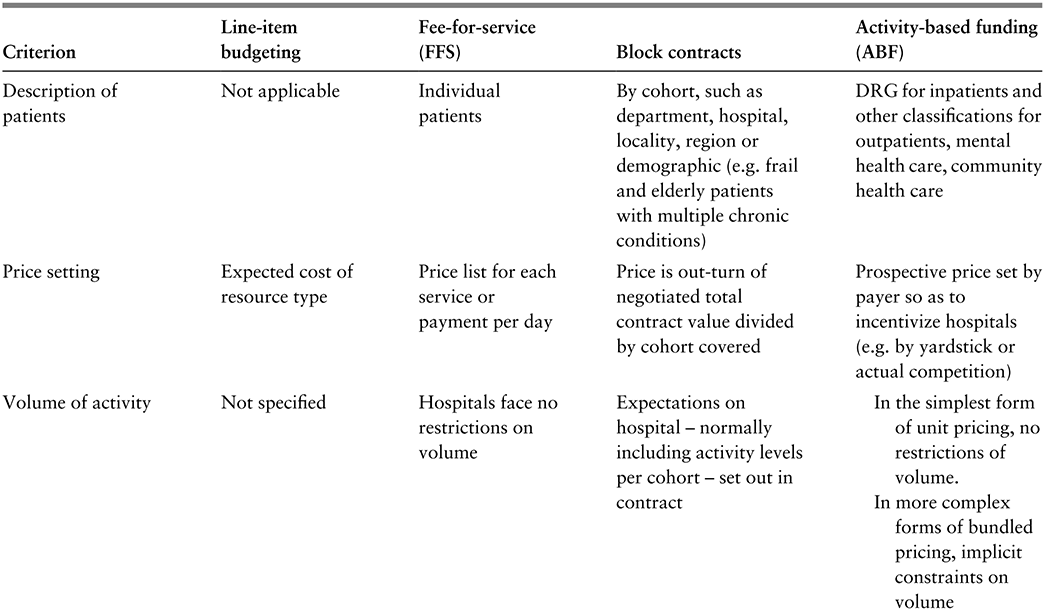

Hospital payment methods can be categorized into four archetypal groups. In this section we set out the key features of each, summarized in Table 3.2.1, allowing us then to discuss the factors influencing which model payers are likely to adopt.

Table 3.2.1a Long description

The table has 5 columns: Criterion, Line-item budgeting, Fee-for-service (F F S), Block contracts, and Activity-based funding (A B F). It reads as follows. Row 1: Description of patients. Line-item budgeting: Not applicable. F F S: Individual patients. Block contracts: By cohort, such as department, hospital, locality, region or demographic (e.g. frail and elderly patients with multiple chronic conditions). A B F: D R G for inpatients and other classifications for outpatients, mental health care, community health care.

Row 2: Price setting. Line-item budgeting: Expected cost of resource type. F F S: Price list for each service or payment per day. Block contracts: Price is out-turn of negotiated total contract value divided by cohort covered. A B F: Prospective price set by payer so as to incentivize hospitals (for example, by yardstick or actual competition).

Row 3: Volume of activity. Line-item budgeting: Not specified. F F S: Hospitals face no restrictions on volume. Block contracts: Expectations on hospital - normally including activity levels per cohort - set out in contract. A B F: In the simplest form of unit pricing, no restrictions of volume. In more complex forms of bundled pricing, implicit constraints on volume.

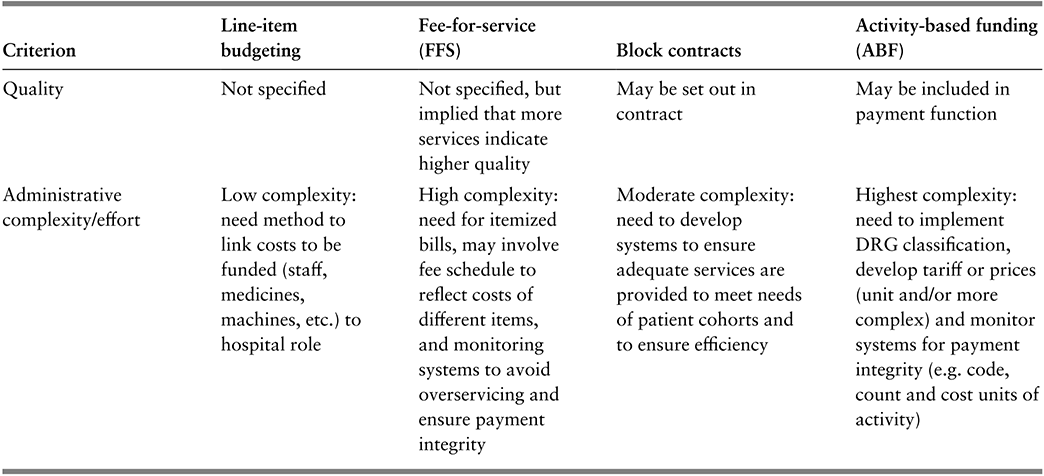

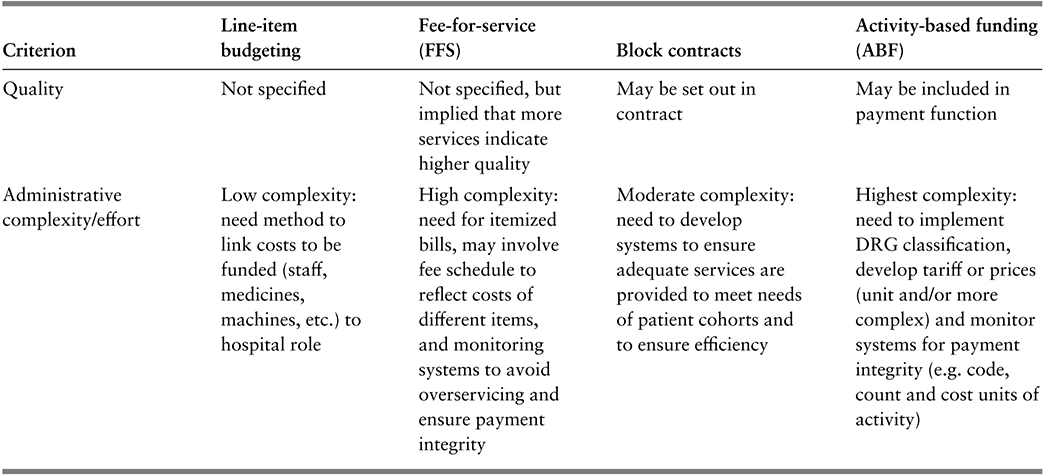

Table 3.2.1b Long description

The table has 5 columns: Criterion, Line-item budgeting, Fee-for-service (F F S), Block contracts, and Activity-based funding (A B F). It reads as follows. Row 4: Quality. Line-item budgeting: Not specified. F F S: Not specified, but implied that more services indicate higher quality. Block contracts: May be set out in contract. A B F: May be included in payment function.

Row 5: Administrative complexity or effort. Line-item budgeting: Low complexity: need method to link costs to be funded (staff, medicines, machines, etc.) to hospital role. F F S: High complexity: need for itemized bills, may involve fee schedule to reflect costs of different items, and monitoring systems to avoid overservicing and ensure payment integrity. Block contracts: Moderate complexity: need to develop systems to ensure adequate services are provided to meet needs of patient cohorts and to ensure efficiency. A B F: Highest complexity: need to implement D R G classification, develop tariff or prices (unit and/or more complex) and monitor systems for payment integrity (for example, code, count and cost units of activity).

DRG: diagnosis-related group.

Line-item budgeting

Under line-item budgeting hospitals are funded according to the type and amount of resource inputs used in delivering care. Budget lines tend to be itemized in fairly crude terms as inputs, such as medical and nursing staff, medicines, meals, laundry, materials, equipment, energy, estate and management costs. The payer, usually a government agency, sets the budget in advance, often built up by categories of inputs (e.g. approval to employ a specific number of nurses for a given amount of money) so that the hospital has clarity about the money it will receive to pay for these items.

This was the form of funding across the former Soviet Union in which central government determined the quantity of resources available to each hospital and fixed wages and prices (Mikesell & Mullins, Reference Mikesell and Mullins2001; Street & Haycock, Reference Street and Haycock1999; Moreno-Serra & Wagstaff, Reference Moreno-Serra and Wagstaff2010).

Advantages

The principal attraction of line-item budgeting is that it provides certainty to both the payer and hospital about the amount of revenue to be made available over the coming budgetary period, with tight expenditure control being the guiding principle. It also comes with a low administrative burden, the budget being based on readily measurable inputs and with monitoring usually limited to ensuring that the budget was spent on the inputs as specified.

Disadvantages

This funding arrangement has several drawbacks (Langenbrunner & Wiley, Reference Langenbrunner, Wiley, Mckee and Healy2002). First, hospitals have no incentive to reduce the use of inputs – indeed the reverse, because any input reductions would probably be met with subsequent budget reductions. Second, just as the overall budget is tightly controlled, so is each line item, thereby ruling out substitution of one type of input for another. Third, the budget says nothing about how the money should be spent on those requiring care: the budget is unrelated to the number and type of people treated at the hospital. Overall, viewed in these terms, line-item budgeting provides little or no incentive for innovation, is unresponsive to the needs of patients and can be viewed as a simple, static payment system.

FFS

FFS is particularly common in health systems in which patients (or their insurers) pay for care themselves, with hospitals issuing bills for the care and treatment provided. Under FFS, hospitals receive a fee for each medical service provided to each patient, these being itemized on the bill. The services will include diagnostic tests, operative procedures, medications and a daily “hotel” charge to cover such costs as laundry, cleaning, meals, energy and general overheads. Hospitals in some health systems use a simple billing arrangement, loading everything onto the daily charge, with hospitals receiving daily payments rather than a price for each itemized service.

Advantages/disadvantages

Under FFS, the more medical services provided and the longer the length of stay, the more a hospital earns in revenue. Hence, as long as it believes that patients are able to settle their bills, the hospital may be incentivized to treat every patient seeking care and to do as much as possible for them. For those able to pay, FFS might provide access to better amenities and more services (Ikegami, Reference Ikegami2015). If so, and if “more is better”, FFS provides greater incentives to provide higher-quality care than the alternative payment models. But it could also lead to overtreatment and the provision of low-value services (Zhao et al., Reference Zhao2018; Chalmers et al., Reference Chalmers2019).

The hospital issues its bills retrospectively, after services have been rendered, either to the patient or the patient’s insurer. Whoever the payer is, there is little choice but to settle the bill, putting the payer at high financial risk. In countries without universal health insurance, this can lead to catastrophic health expenditures for patients, whereby patients may receive bills amounting to anything between 10–40% of family income, or bankruptcies due to health care costs (Himmelstein et al., Reference Himmelstein2019; Dobkin et al., Reference Dobkin2018; Xu et al., Reference Xu2003a; Reference Xu, Murray and Evans2003b; Reference Xu, Murray and Evans2003c; Wagstaff, Eozenu & Smitz, Reference Wagstaff, Eozenou and Smitz2020).

Sometimes insurers question whether particular services given were necessary. Utilization reviews are the most common way to do this, but these are expensive and have little effect on the volume of services provided (Rosenberg et al., Reference Rosenberg1995). In practice, then, the quantity of services is largely determined by the hospital. Most usually, insurers try to limit financial risk by imposing a fee or price schedule, detailing the price per service that they are prepared to pay. This would mean that the price for each service is determined by the payer. In the absence of insurance, patients have no ability to influence these prices.

Block contracts

The key idea of the block contract funding model is that the amount to be paid is determined in advance. As a minimum, block contracts stipulate the delivery timescale, the total amount of money to be paid, and the cohort (that is, type and number) of patients to be treated. There might also be some specification of quality. Sometimes the block contract will take the form of a capitation payment model covering a particular patient population, with the amount reflecting expectations about utilization among that cohort. The capitation payment (or price per patient) is simply the total amount of money specified in the contract divided by the number of patients in the cohort. The payer and hospital are likely to enter into several contracts, differentiated according to how cohorts are described. The cohort might reflect the hospital department with primary responsibility for delivering the particular type of care, the hospital’s catchment area, the wider geographical region the hospital serves, or some indication of the type of patient in the cohort (e.g. frail and elderly patients with multiple chronic conditions). Sometimes a hospital might enter into a single contract for an especially large patient cohort, this special case being referred to as a “global budget”. Where capitation payments rely on the clinical characteristics of enrollees, the payer has to be wary of gaming risks where the funded entity artificially inflates diagnoses (Geruso & Layton, Reference Geruso and Layton2020; Porter & Kaplan, Reference Porter and Kaplan2016; Chernew et al., Reference Chernew2021).

A block contract can be used in a variety of different circumstances, with different effects. For instance, block contracts might be the historical form of the payer–hospital relationship, with contracts determined by history or past negotiations. Here payers put a high value on their effort in determining and monitoring contracts, with less emphasis on quantity or quality. Negotiation-based block contracts might involve an expected quantity to set the value of the contract, but with little scope for variation from the total spend if volume exceeds expectations. If so, activity-related cost risk sits with the hospital, not the payer. So this form of block contract might be preferred by payers with tight budget constraints. Because of their relative simplicity, block contracts are often used for services which cannot be described particularly well, such as where an activity measure has not yet been developed (e.g. mental health services); it is a unique service (e.g. highly specialized care); or the service would be unviable under other methods of payment, but the payer wants to ensure the service continues (e.g. small rural hospitals necessary for access). With this form of block contract, the activity-related cost risk sits with the payer.

Advantages/disadvantages

Block contracts provide financial certainty for both the payer and the hospital, as the total contractual value is decided in advance, particularly if the payer imposes a “hard” cap where activity beyond the contracted amount is not reimbursed. The danger of a hard cap is that the hospital risks being unable to cover its costs if demand exceeds the contracted volume, because they will not receive extra funding. This might encourage hospitals to do just enough to fulfil their contractual obligations and refuse to treat more patients than the contracted volume. This would result in either denied or delayed care. Indeed, hospital waiting lists are often evident where block contracts are the dominant form of hospital funding (Iversen, Reference Iversen1993; Street & Duckett, Reference Street and Duckett1996). This problem might be mitigated if the contract allows for a “soft” cap, permitting partial reimbursement of extra activity (Chen & Fan, Reference Chen and Fan2016).

Although contracts provide certainty, payers may still make excessive payments. This is because the values for both the target volume of patients and the price are a matter of negotiation between payer and hospital. As the hospital enjoys an informational advantage on both counts, it may be able to secure a higher contract value than if both parties were equally informed.

Activity-based funding

The fourth payment type is activity-based funding, which is sometimes referred to as case mix funding, DRG funding or the prospective payment system.

In terms of how patients are described, activity-based funding can be considered a half-way house between FFS and block contracts. Under FFS, a personalized bill is drawn up for each individual patient. Under block contracts, the contract is usually specified at cohort – often departmental – level, implying that patients are described in fairly large and heterogeneous groups in the contract. Under activity-based funding, patients admitted to hospital are usually described using DRGs for patients, though other DRG-like classifications might be used for activity conducted in emergency departments, outpatient or other (e.g. mental health, community) settings. DRGs were first developed by Fetter et al. (Reference Fetter1980) as a means to identify groups of admitted patients with similar diagnoses who were expected to have similar resource requirements during their hospital stay. This design principle has guided the development of DRG systems around the world (e.g. Busse et al., Reference Busse2011; Kimberly & de Pouvourville, Reference Kimberly1993). The design of the DRG classification aims to maximize within-group homogeneity but, because there is a limited number of groups in the DRG classification, inevitably each group is still somewhat heterogeneous. Consequently, activity-based funding entails a less precise description of patient specificity than under FFS (where effectively each patient is their own group) but a more precise description than under block contracts.

Importance of clinical accounting skills: coding, counting and costing

Activity-based funding cannot be adopted without some form of system for classifying activity – known as coding, counting and costing – and countries have to decide whether to adopt or adapt systems developed elsewhere or create their own (Mathauer & Wittenbecher, Reference Mathauer and Wittenbecher2013). Usually there is quite a protracted transitional period between introducing a coding-counting-costing classification system to describe hospital activity to its being used for payment purposes (Bredenkamp, Bales & Kahur, Reference Bredenkamp, Bales and Kahur2020). The choice of classification system is dependent on the underlying information infrastructure for coding, counting and costing activity, which influences how electronic data are collated from each patient’s medical record, how data are shared between hospitals and payers, and how these data are verified. Developing and maintaining coding-counting-costing classifications across the range of hospital activities – including acute inpatients, outpatients, mental health patients, activity in emergency departments, ambulatory patients and others – requires good information systems and technical clinical recording, i.e. clinical documentation and coding skills.

All classification systems begin with good clinical recording. This is not a minor issue, even in high-income countries (HICs) with a long tradition of clinical coding and using patient records for research (e.g. the English NHS), but in low- and middle-income countries (LMICs) a patient’s complexity may not be fully reflected in diagnoses recorded in routine data sets, which may especially miss out on comorbidities (Dyers et al., Reference Dyers2016). Preparing for activity-based funding in these countries should include strategies to improve clinical accounting skills (Moghaddasi, Rabiei & Sadeghi, Reference Moghaddasi, Rabiei and Sadeghi2014).

Mis-recording of comorbidities will weaken the discriminatory power of a classification system but will not necessarily preclude the use of activity-based funding. Kyrgyzstan, for example, started its transition from line-item budgeting to activity-based funding in 1997 with a home-grown classification system comprising just 28 DRGs (known there as clinical costing groups), expanding to 144 DRGs in 1998 and to 284 in 2019 as information systems better recorded diagnoses and procedures (Bredenkamp, Bales & Kahur, Reference Bredenkamp, Bales and Kahur2020).

Price setting

As with block contracts, activity-based funding prices are set in advance and are not related to the costs of any specific hospital but rather are set by the payer, usually following its review of the totality of costs for each DRG reported by all or a large selection of hospitals in the payer’s jurisdiction. This form of price setting is known as “yardstick competition”, a term coined by Shleifer (Reference Shleifer1985). Crucially this means that each hospital is a “price-taker”, unable to influence the price it faces, mirroring what would be the case in a perfectly competitive market. By translating the cost information into prices, the payer effectively is making hospitals benchmark themselves against each other to reduce their costs, the price acting as a yardstick to which higher-cost hospitals should aspire. This should encourage hospitals to improve efficiency and minimize overprovision of services to the patient (Vladeck & Kramer, Reference Vladeck and Kramer1988). The payment system is also perceived as fair, offering “equal pay for equal work”, with hospitals receiving the same price for each patient allocated to the same DRG. To function, this arrangement requires cost information from a sufficient number of hospitals for the benchmark to bite, the more the better. Of course, some health systems have very few hospitals, in which case the payer might need to seek benchmark information from elsewhere, perhaps from other health systems. For example, when activity-based funding was introduced to fund the main Landspítali University Hospital in Iceland, benchmarking information about hospitals in Sweden was used to inform prices (Hafsteinsdóttir & Siciliani, Reference Hafsteinsdóttir and Siciliani2012).

Advantages/disadvantages

As hospitals receive a predetermined DRG price for each patient assigned to that DRG, regardless of the actual cost, some of the financial risk is shifted from the payer to the hospital. This happens because, although patient volume remains a risk for the payer, the hospital assumes risk for its case mix. The more complex (and therefore costly) that the hospital’s patients are in a given DRG, the less likely it is that the predetermined DRG price will cover its cost of treating them.

Activity-based funding could stimulate undesirable behaviour; for example, hospitals might engage in coding-creep, “cream-skimming” or skimping. Coding-creep arises when a hospital classifies “a patient in a DRG that produces a higher reimbursement” (Herwartz & Strumann, Reference Herwartz and Strumann2014; Simborg, Reference Simborg1981; Steinbusch et al., Reference Steinbusch2007; Carter, Newhouse & Relles, Reference Carter, Newhouse and Relles1990; Steinwald & Dummit, Reference Steinwald and Dummit1989), evidence suggesting such practices do occur (Jürges & Köberlein, Reference Jürges and Köberlein2015). With cream-skimming, hospitals actively select patients that are cheaper to treat. Hospitals might be able to do this because they have better information about the patient´s condition and prospects than those designing the DRG categories. Cream-skimming allows a hospital to identify more profitable patients, i.e. those with expected costs lower than the prospective price. Skimping involves underproviding services, perhaps by discharging a patient too early (Ellis, Reference Ellis1998). These undesirable responses can occur with other funding models too. However, because the link between clinical accounting and income is more pronounced under activity-based funding and FFS than block contracts or line-item budgeting, these responses are more of a risk under activity-based funding and FFS than for the other funding models.

In combination with other methods

Activity-based funding is often coupled with one of the other types of payment system, as not every type of hospital activity can be described using activity measures. For example, Kwon and Shon (Reference Kwon, Shon, Annear and Huntington2015) report that hospital income in Australia, Japan, Korea, New Zealand and Singapore is a mixture of activity-based funding and FFS, with hospital income in Thailand a mixture of activity-based funding, FFS and block contract. Especially in early phases of activity-based funding implementation, it may be coupled with FFS or block contract to pay for services to describe teaching and research activity, or services which may span inpatient and community care boundaries.

Influences on choice of payment model

There are four key factors influencing the choice of payment model: the number of payers, the number of hospitals, the relative importance the payer attaches to their objectives, and payer (and to a lesser extent, hospital) effort in managing the system.

Key factor 1: number of payers

The first and most important factor is the number of payers in the health system. The fewer payers there are, the more power they are able to exercise in negotiations with hospitals. In health systems with no third-party payers, each patient is a payer, with minimal bargaining power. In such circumstances, patients are price-takers, having to pay what hospitals ask, with FFS being the typical payment model. If the health system features third-party payers in the form of insurance companies or sickness funds, FFS is also common, but these payers may be able to exert collective influence on hospitals in the form of a fee schedule in order to contain overall payments. But, even so, hospitals enjoy considerable power in deciding what volume of services to provide to each insured individual.

In other health systems, notably where health care is funded via taxation, third-party payers often take the form of government agencies with responsibility for specific populations, perhaps defined on the basis of geography, income or age. These payers receive a share of national tax funds to fulfil these responsibilities, this share usually calculated using a capitation formula reflecting the size and composition of the population. If there are only a few hospitals in their area, agencies may prefer to negotiate block contracts with hospitals (because of their lower administrative burden) which will likely reflect the volume (number) and type (composition) of hospital patients covered by the contract. As there are just two parties to each contract, the hospital may be able to exploit its information advantage to secure favourable terms.

Some health systems feature just a single payer. This shifts the balance of bargaining power from hospitals to the single payer, who is able to exploit its monopsony purchasing power and force hospitals into being “price-takers” rather than “price-makers” by imposing either line-item budgeting or activity-based funding payment models.

Key factor 2: number of hospitals

The second factor influencing the choice of payment model is the number of hospitals to which payments are to be made. If there were a very large number of hospitals, all providing similar services and competing with one another to attract fully informed patients, FFS would be an efficient choice. This competitive environment would ensure that high-quality services were provided and fees were kept low. But this is not the customary environment that prevails in the hospital sector because of the asymmetry in information between hospitals and their patients. Rather, it is much more common for hospitals to face little competition, instead enjoying a degree of local monopoly power. A hospital might even have national monopoly power, in smaller countries or if they are the only providers of specialized care. The greater its monopoly power, the more ability a hospital has to set its own fees, thus making the FFS model less attractive to payers.

The other three payment models impose more financial control over hospitals than the FFS model, and line-item budgeting and block contract can be applied irrespective of the number of hospitals in the health system. However, under activity-based funding prices are set by comparing costs across hospitals, so there needs to be a sufficient number of hospitals from which the payer collects comparative data. As with FFS, the fewer the hospitals, the greater the scope for a hospital to influence prices advantageously, because its own data will have greater influence on the price it faces. To limit this influence, payers implementing activity-based funding may set prices using comparative cost or pricing information from hospitals in other jurisdictions.

Key factor 3: relative importance of payer objectives

The third determinant of the choice of payment model is the relative weight that payers attach to their different objectives, in particular: controlling hospital costs, volume of activity and quality of service.

Budget constraint

The greater the weight attached to controlling hospital costs (especially for payers subject to a hard budget constraint), the more likely that line-item budgeting and the less likely FFS and activity-based funding will be adopted. This is because FFS and activity-based funding both encourage additional activity, unless explicit activity capping mechanisms are introduced. Block contracts make management of the budget constraint easier for the payer than FFS and activity-based funding, but not as easy as line-item budgeting.

Volume of activity

FFS exercises no restriction on the volume of activity. Neither does activity-based funding, at least in its simplest form (i.e. with unit prices). Because line-item budgeting is concerned with resources more than quantity and quality, it neither specifies activity levels nor places restrictions on them. Again, block contracts lie somewhere in the middle from the payers’ perspective, depending on how the contract is specified. At its crudest, the block contract could be whatever was agreed financially between payer and hospital for the last contracting period, increased for anticipated inflation (in activity and/or costs) over the current contracting period and decreased for expected efficiency (in activity and/or costs) over the current period. Here, the payer’s target level of activity is included only in an aggregate sense, through the interaction of the last contracting period’s activity and the uplift and reduction for the current period. In other cases, however, the block contract may be built bottom-up and not top-down. In this case, the payer’s target level of activity is explicitly included at a disaggregated level (e.g. by hospital department or point of delivery).

Quality

From the payer’s perspective neither line-item budgeting nor FFS inherently specify quality. That said, under FFS, hospitals earn more revenue by providing more care so, provided more care is better care, then FFS incentivizes quality. The same argument applies to activity-based funding, which incentivizes hospital activity, if more activity equates to better quality. In practice, however, more care may not equal better care. That said, if there is head-to-head competition between hospitals, by setting prices prospectively both activity-based funding and block contracts ensure that competition drives quality up rather than driving prices down. In addition to this inherent quality assurance mechanism, both block contracts and activity-based funding can incorporate specific payment for quality.

Key factor 4: administrative effort

The final relevant factor is the effort involved in managing the payment methods (Baxter et al., Reference Baxter2015). Payers and hospitals need to optimize the amount of effort involved. Payment arrangements are not frictionless: both payers and hospitals need to exert effort in agreeing and managing the contractual relationship between the two parties. For hospitals, this will require ensuring that internal structures of the hospital make it easy to address the exogenous incentives – control of the mix of services used in treating a patient typically rests in the hands of the medical staff and so the job of hospital senior management includes ensuring that hospital doctors recognize the hospital’s funding constraints (Young & Saltman, Reference Young and Saltman1985).

Payers also need to exert effort to ensure that the funding design delivers on the objectives that they have prioritized. The more complex the funding model, the more effort is expended by both hospitals and payers in managing and monitoring it. Payers, especially, have to be wary of making the funding model overly complex. The more complex the model, the more difficult it will be for hospitals to understand the nature of the incentives at play and the more likely they are to ignore the incentives or respond to what they perceive the incentives to be (Abeler & Jäger, Reference Abeler and Jäger2015). Moreover, if the incentives are unstable – for example if prices vary widely from year to year – hospitals may decide that the effort in responding to a given year’s incentives is not worth the benefit, and so they might ignore the incentive.

Line-item budgeting involves minimal administrative complexity, both in terms of how the budget is specified and in how spending is monitored. As such, this payment method is likely to be preferred in places where information systems are poorly developed. Activity-based funding is the most complex of the payment methods, requiring implementation and maintenance of a classification system to describe patients, a pricing schedule and a monitoring system to verify the integrity of payments made by payers to hospitals. FFS and block contracts lie between these extremes.

The importance of management and policy skills can be seen in the results of the implementation of activity-based funding in central and eastern Europe, and central Asia. In their study of the system-wide impacts of hospital payment reform, Moreno-Serra and Wagstaff (Reference Moreno-Serra and Wagstaff2010) found that, contrary to theory, total health expenditure increased following implementation of activity-based funding. Moreno-Serra and Wagstaff hypothesized that this may have been due to DRG coding-creep. The potential for coding-creep should have been foreseen and its effect mitigated through a variety of strategies such as assuming a DRG effect of a particular size and factoring that into the price in advance, or through rigorous auditing of coding. The impact of coding-creep could also be ameliorated by imposing lagged soft expenditure caps (Hahn, Reference Hahn2014; Holahan & Zukerman, Reference Holahan and Zukerman1993).

Transitioning from one payment method to another

The choice of payment method and its specific design features is context dependent and that context may change (D’Aunno, Kimberly & De Pouvourville, Reference D’Aunno, Kimberly, De Pouvourville, Kimberly, De Pouvourville and D’Aunno2008; Mathauer & Wittenbecher, Reference Mathauer and Wittenbecher2013). Funding reform often adopts the twin system objectives of transparency of processes and outcomes, and fairness between hospitals, to facilitate support for implementation of the system change. In these circumstances, the key design elements of the payment method need to be clear and understood, and there needs to be a clear line of sight between the work performed by the hospital and the payment flow.

We have set out the key drivers of the choice of model in the previous sections, but other factors also play a part, perhaps relating to management, policy, information system readiness or path dependence. The payer’s objectives, however, are the dominant driver, and these might change over time, triggering a move away from one type of payment method to another.

The process of transition: what is involved?

The transition process is often a long one, as the preconditions are developed (Annear et al., Reference Annear2018), or the right policy window appears. Improved provision of comparative information to providers – to allow them to see where they stand on efficiency and other variables – is often part of a capacity-building phase.

A common next step is that this comparative information is used to inform budget setting – benchmarking here is an input into the budget negotiating process or used to inform the block contract. For example, in their review of the development of activity-based funding in 12 countries in Europe, Busse and Quentin (Reference Busse, Quentin and Busse2011) showed that in half the countries the original use of the DRG classification system was simply descriptive or to inform budget allocation. Bredenkamp, Bales and Kahur (Reference Bredenkamp, Bales and Kahur2020) drew a similar conclusion in their review of the transition to activity-based funding in nine countries. Indeed, the possibility for such benchmarking was one of the drivers of the initial development of DRGs (Fetter, Brand & Gamache, Reference Fetter and Brand1991).

Transitioning: key questions and trends

Payers normally will have objectives about how the health system transitions from the old funding system to the new. These objectives might be about the pace of the transition. Over how many years is the phase-in? What proportion of funding is on the old versus new basis? And what should be the ordering of the transition – for example, starting with patients having elective procedures, or particular classes of patients or particular types of costs (Duckett, Reference Duckett, Annear and Huntington2015)? Because there will be winners and losers from any transition between funding systems, the payer’s objectives about the pace and phasing will often also factor in how to manage these gains and losses (Short & Goldfarb, Reference Short and Goldfarb1987).

The introduction of new funding systems also often provides the opportunity to revisit the nature of the relationship between the payer and the hospital–- what types of controls might be kept or changed? How much autonomy will hospitals have in the new environment? What constraints might there be on hospital innovation? Introducing new funding systems may even be driven by a desire to change that relationship.

Payers might try to pursue multiple objectives simultaneously, although this will require a more sophisticated design pursuant to the Tinbergen Rule, that multiple objectives require multiple instruments (Tinbergen, Reference Tinbergen1952). For example, one of the early implementations in 1993 of activity-based funding, in Victoria, Australia, had three objectives: to reduce total hospital expenditure; to improve the efficiency of hospitals; and to increase the number of patients treated and reduce elective procedure waiting lists (Duckett, Reference Duckett1995). Activity-based funding in Victoria replaced a system of negotiated block contracts. The stimulus for the introduction was a significant budget cut (15% over three years), effectively a tightening of the budget constraint, and a recognition that a reduction in the budget of that magnitude would, under a block contract system, probably result in a significant reduction in the quantity of services provided (and hence access). An activity-based funding model for acute inpatient activity was implemented – with hospital-specific activity caps but a potential to share in a capped allocation of extra funds for extra activity (Street & Duckett, Reference Street and Duckett1996) – with all other hospital services paid on a block contract in the absence of robust activity measures for those services.

Preconditions for transitioning from simpler to more complex methods

In view of the considerations set out in this section, it is common in practice to see a mix of funding methods used within any given health system, thereby moderating the extreme effects of any single method. “Transition” then means altering the mix of methods, rather than shifting wholesale from one to another. Yet regardless of whether transition is from one method to another or is a shift in the mix of methods from one to another, there are four preconditions for shifting from simpler funding methods (line-item budgeting, block contracts) to more complex ones (FFS, activity-based funding):

1. The development of robust risk-adjustment measures, generally based on an already established version of the DRG classification; but the larger the jurisdiction, the more likely an internationally imported version will be adapted to reflect local clinical practice.

2. The implementation of information systems – notably coding systems and grouping software. This is required to ensure that hospital managers have the appropriate information to identify where there is scope for performance improvements.

3. The development of administrative skills in the payer to design and manage the new system. This is a nontrivial task as poorly designed payment systems may not be seen as legitimate and are unlikely to gain acceptance; or may fail to anticipate the full range of perverse provider responses, including gaming. Poor ongoing management of a new funding system may not incorporate appropriate monitoring and interventions to sanction poor performance and again undermine confidence in the system, or may not incorporate adaptation for new technology.

4. The development of management skills in hospitals. A change of budget processes will also require a different set of skills – perhaps from managing negotiations with the payer to managing efficiencies within the organization more tightly.

The scarcer that administrative and management skills are, and the more challenging the development of risk-adjustment measures and information systems is, the more likely it is that the funding model or mix of models will gravitate towards simpler forms (Baxter et al., Reference Baxter2015).

Ensuring quality: P4P

Increasingly, hospital payment models incorporate elements of P4P, either to address additional adjunct goals – most commonly quality or timeliness of care – or to mitigate design risks inherent in the payment system (Duckett, Reference Duckett2008). P4P comes in many different forms with different objectives, including paying for additional information provision, paying for adherence to standards, or paying for meeting a particular quality threshold or quality improvement (Milstein & Schreyoegg, Reference Milstein and Schreyoegg2016). A P4P approach has been proposed as a way of paying for better outcomes (Siciliani et al., Reference Siciliani2021).

P4P: what it is

Health care funding contracts are often “incomplete” in the sense that they are not able to specify fully what is to be provided, especially in terms of quality, and this carries an inherent risk that providers might skimp on quality to reduce costs. In addition to evidence-based governance strategies to encourage quality improvement (Donabedian, Reference Donabedian2002; Langley et al., Reference Langley2009; Tello, Barbazza & Waddell, Reference Tello and Waddell2020), payers mitigate this risk by incorporating into payment design additional payments against additional metrics. Importantly, P4P is described here as a supplement: the basic stream of revenue needs to be adequate for all hospitals and the P4P supplement is an add-on, to reward superior performance on the relevant dimension (Cattel, Eijkenaar & Schut, Reference Cattel, Eijkenaar and Schut2020; Cattel & Eijkenaar, Reference Cattel and Eijkenaar2020). There is now an extensive literature about P4P, and an array of potential P4P designs (Cromwell et al., Reference Cromwell2011; Conrad, Reference Conrad2015), with the net impact of a specific implementation the result of the interplay of several factors including gaming, target and reward setting, and health increasing and health decreasing substitutions (Friedman & Scheffler, Reference Friedman, Scheffler and Scheffler2016). Perverse responses – including gaming (Carter, Newhouse & Relles, Reference Carter, Newhouse and Relles1990; Rosenberg, Fryback & Katz, Reference Rosenberg, Fryback and Katz2000; Bevan & Hood, Reference Bevan and Hood2006; Steinbusch et al., Reference Steinbusch2007; Mannion & Braithwaite, Reference Mannion and Braithwaite2012; Georgescu & Hartmann, Reference Georgescu and Hartmann2013) – can be mitigated with regulatory strategies including monitoring, and penalties.

Difficulties with P4P

Although intuitively and theoretically sound, in practice P4P implementations – especially those which focus on changing a single provider type (hospital or primary care) or specialty – have generally not lived up to the expectations and rhetoric (Mendelson et al., Reference Mendelson2017; Scott, Liu & Yong, Reference Scott, Liu and Yong2018; Cattel, Eijkenaar & Schut, Reference Cattel, Eijkenaar and Schut2020; Cattel & Eijkenaar, Reference Cattel and Eijkenaar2020; Singh et al., Reference Singh2021). Song’s summary of the state of evidence about “accountable care” in the USA can equally apply to P4P:

Today, a verdict on payment reform resembles less the fork in the road between success or failure and more a work-in-progress that has improved the value of care in some situations but needs refinement

Unfortunately, P4P, especially when poorly designed, may crowd out intrinsic professional motivation and can create perverse incentives as evidenced in both the mid-Staffordshire scandal in England (Francis, Reference Francis2013; Powell, Reference Powell2019; Smith & Chambers, Reference Smith and Chambers2019; Entwistle & Doering, Reference Entwistle and Doering2024) and the Bundaberg Hospital scandal in Queensland, Australia (van der Weyden, Reference van der Weyden2005; Thomas, Reference Thomas2007; Casali & Day, Reference Casali and Day2010; Edwards, Lawrence & Ashkanasy, Reference Edwards, Lawrence, Ashkanasy, Ashkanasy, Härtel and Zerbe2016), where organizational targets and incentives for budget control or additional activity created environments where safety concerns were ignored. However, well-designed performance monitoring and P4P incentives can help to ensure that organizations pay appropriate attention to their processes and outcomes (Conrad & Perry, Reference Conrad and Perry2009; Conrad, Reference Conrad2015; Young & Conrad, Reference Young and Conrad2007; Smith et al., Reference Smith2009), particularly as they impact on the most vulnerable.

The evidence suggests, therefore, that careful consideration has to be given to how to incorporate P4P arrangements within the hospital payment model. The cost of including a P4P component may be modest, especially where the cost of the ostensible reward is transferred from other streams of the hospital revenue. In these circumstances, P4P simply leads to a slightly different distribution of a capped budget. P4P incentives serve a political and rhetorical purpose signalling that the payer values the metric rewarded and directing hospitals – who could be expected to respond to incentives at the margin – to pay attention to this metric too.

Evidence in practice: paying hospitals in the English NHS

In this section we consider how the discussion thus far has played out in practice, by considering how payments to hospitals in the English NHS have changed since 2002.

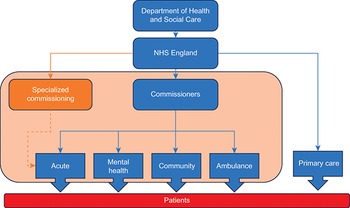

The NHS is taxpayer funded and universal. Fig. 3.2.1 below gives a simple schematic of how NHS care is paid for in England since 2021. The accountable government department (currently the Department of Health and Social Care) allocates funding agreed by Parliament to a government agency, NHS England. NHS England distributes funding to several hundred local buyers of health care, known as commissioners. In addition, NHS England distributes funding to primary care and buys specialized health care itself. Commissioners pay for health care from acute care providers (hospitals) as well as providers of NHS mental health services, community services and ambulance services. The NHS payment system in this schematic is represented by the shaded box. To give an idea of scale, in 2019/20 NHS England allocated nearly £79 billion to commissioners, £18 billion to specialized services and £8 billion to primary care (Bell, Charlesworth & Lewis, Reference Bell, Charlesworth and Lewis2021).

Schema of payment flows in England

Figure 3.2.1 Long description

The first step is Department of Health and Social Care, from where the flow moves to N H S England. From the N H S, the flow can move to Primary Care, which is received by Patients. The flow can also move to Commissioners, from where it can go to Acute, Mental Health, Community, or Ambulance, all of which are then received by Patients. Additionally, from the N H S, the flow can also move to Specialized commissioning, from where it flows to Acute.

There have been four major changes since 2002 in how hospitals are paid: the move from block contracts to activity-based funding for hospitals; changes in the number of payers; increasing complexity in activity-based funding for hospitals; and replacing competition between hospitals with collaboration as the main driver of improvement. Each is discussed below.

From block contracts to activity-based funding

Until 2002, acute-care services and mental health, community and ambulance services were paid for with block contracts. From 2003, activity-based funding began to be phased in to gradually replace block contracts for acute hospital care. It began on a small scale, with just 15 prices for elective surgery (and just 0.2% of commissioners’ budgets) during a time of increases in NHS funding. It did so to address growing waiting lists and a so-called postcode lottery in access to care (Martin et al., Reference Martin2003). Activity-based funding expanded steadily until by 2012 it had grown to 3000 prices for 1400 DRGs, covering 34% of payers’ budgets. It grew further from 2013 following an expansion in the scope for payment to follow patients’ choices; to 9000 prices for 2800 DRGs and 40% of commissioners’ budgets. It included P4P elements linked to quality.

As it expanded, activity-based funding for acute care promoted productivity in hospitals (Farrar et al., Reference Farrar2009). Its P4P schemes improved quality (Meacock, Kristensen & Sutton, Reference Meacock, Kristensen and Sutton2014). It also helped amass rigorous data on activity, costs and outcomes. Set against this, it rewarded unilateral interest and not collaboration (Cooper et al., Reference Cooper2011; Bevan & Skellern, Reference Bevan and Skellern2011). It hampered management of expenditure and of unwarranted variation in activity (Mannion & Street, Reference Mannion and Street2009) and it was burdensome to administer (Marini & Street, Reference Street2007). In addition, the mix of activity-based funding for hospitals with block contracts for community, mental health and ambulance services frustrated better integration of health care (Bevan & Janus, Reference Bevan and Janus2011).

Changes in the number of payers

Until 2005 each hospital entered into contracts with around two dozen payers, then termed district health authorities. Tax funding was allocated to authorities according to estimates of the health needs for the population of each district. From 2006 the landscape for payers changed from district health authorities to over 300 local, primary care-led clinical commissioning groups. Hospitals then entered into thousands of contracts with these payers. As these contracts moved from block contract to activity-based funding, the system’s demands on management skills and information systems increased.

At its peak in 2015, 88% by value of contracts between hospitals and payers used activity-based funding. By 2018 that had reduced to 58%. There were two drivers for this reduction: administrative burden and budget. In a typical year in this period, hospitals issued some 600 000 monthly invoices to payers. Almost 200 000 of these were for less than £1000 as hospitals and payers argued about month-end bills. A shared desire by some local hospitals and payers to reduce this administrative effort saw many move reimbursement away from activity-based funding.

A sustained period of austerity in United Kingdom government spending followed the 2008 global financial crisis (Ford, Reference Ford2013). This reduced the rate of annual funding growth to the NHS to less than half its long-run average (Walshe & Smith, Reference Walshe and Smith2015; Charlesworth & Bloor, Reference Charlesworth and Bloor2018). By 2015 this manifested itself in a lack of hospital capacity and in large and growing hospital deficits, as prices for DRGs were scaled down by more than 10% below average unit costs. As a consequence, the incentives for head-to-head competition between hospitals declined, as did the desire of payers and hospitals to contract using activity-based funding.

Increasing complexity in activity-based funding

Initially, as activity-based funding was expanded to support patient choice and head-to-head competition between hospitals, it became more complex (Marshall, Charlesworth & Hurst, Reference Marshall, Charlesworth and Hurst2014). As well as the number of DRGs attracting activity-based prices expanding greatly, four types of financial incentives for quality were added to the payment system. The first enabled hospitals to reclaim funding held back by payers (of a few percentage points of their budgets) when they achieved improvements in process quality (e.g. ensuring hospital staff had winter flu vaccinations) and patterns of care, especially preventive care (e.g. screening infants for malnutrition). The second rewarded outcome quality, with hospitals paid a higher price for “best practice” (meaning high-quality and cost-effective) care, with the goal of reducing unexplained variation in hospitals’ clinical quality in areas such as adult stroke care and children’s diabetes care. The third enabled payers to claw back activity-based funding (of a few percentage points of their budgets) if hospitals did not meet standards for quality on metrics such as hospital-acquired infections, waiting times for elective care or emergency admissions for non-elective care. And the fourth gave hospitals top-up payments, either for extra cost incurred (e.g. on long staying or very complex patients) or for exceeding activity thresholds in certain areas (e.g. faster emergency care, more elective care). Later versions of these top-up payments included risk-sharing mechanisms, to help ensure spending did not exceed payers’ funding allocations.

Even where head-to-head competition between hospitals was not possible (or became less desirable), activity-based funding was used to underpin comparative competition. This is because prices were based on reported costs. Each year hospitals submitted to NHS England data on the cost of each unit of activity for each DRG. Subject to adjustments, the average unit cost for each DRG was the activity-based price for that DRG (Street & Maynard, Reference Street2007). A hospital whose cost lay below the activity-based price it received earned a surplus on each unit of that activity; one whose cost lay above was incentivized to reduce its unit costs.

Replacing competition with collaboration as the main driver of improvement

To incentivize increased activity, activity-based funding introduced unit prices for individual DRGs. As activity-based funding expanded to support patient choice, prices continued to be unitary to ensure the right type of head-to-head competition between hospitals. Because in reality English hospitals faced little competition, they had influence over the prices they faced. Competition between hospitals then had two countervailing effects on quality. On the one hand, it encouraged hospitals to improve quality for a given price in order to attract patients and funding. On the other hand, higher quality may be costly to provide and is hard for patients and payers to judge. So by reducing profitability, competition discouraged hospitals from spending on (hard-to-judge) quality, in order to keep costs and (easy-to-judge) prices down. The overall impact of competition on quality is the net of these two effects. To ensure patient choice drove quality up rather than prices down, activity-based funding prevented price competition by fixing unit prices above average unit costs.

As the impact of government austerity on NHS funding was felt, hospitals lacked capacity and financial deficits grew. With little incentive for hospitals to compete, there was little head-to-head competition between them. Collaboration and not competition became the principal driver of improvement in hospital performance (Allen et al., Reference Allen2017; Alderwick & Ham, Reference Alderwick and Ham2016). The 2019 NHS Long Term Plan cemented this, foreshadowing multilateral, integrated local care systems to replace bilateral commissioner-provider relationships, the better to promote integrated care (NHS England, 2019). To support this multilateralism, the Long Term Plan ushered in population-based funding and a return to block contracts to replace activity-based funding.

Policy relevance and conclusions

In this chapter we have set out a stylized description of the relationship between those who pay and those who provide hospital care. This recognizes that both parties have an interest in the quantity and quality of care provided, and the costs incurred in providing it, but are likely to attach different weights to these interests. Payers use payment arrangements to align the hospitals’ interests with their own, and we described four archetypal methods: line-item budgeting, FFS, block contracts and activity-based funding. We then set out the reasons why one of these methods may be adopted rather than another, and considered issues involved in transitioning from one to another and how each might evolve to capture more complex elements in the payment model, notably quality.

We draw three conclusions from this assessment. First, there is no “best” payment model. Rather, the choice is service and context specific, depending on the number of payers and providers in the health system, the objectives that they wish to achieve, and the relative weights attached to these objectives.

Second, the payment model is not a static set of immutable rules. Rather, the details of how the model operates are regularly updated, with payers and hospitals agreeing specific arrangements, usually for the year ahead. This evolution will be driven by various factors, particularly during the transition phase from one payment model to another. Payment adaptations will also be required to reflect new technologies and innovations in the ways that care is delivered, particularly if it becomes possible to provide care in alternative settings. But a key driver of this evolution is changes in the relative weights that payers attach to their objectives. Even small changes in emphasis can have a large impact on payment design, to the extent that previous preference for one method might shift to another, as evidenced by the English case study. A change of government might also lead to tectonic shifts in weights.

The third conclusion is that, even though we have described these payment methods in stylized, simplified forms, in practice paying hospitals is a complex process and difficult to get right. This is not surprising because providing hospital care is complicated, tailored to the specific needs and characteristics of each patient. A simple payment method will be easy to implement and monitor but comes at the risk that patients will not receive the right care, at the right time, in the right setting. More complex payment models aim to protect against this risk, but at the cost of extra effort that needs to be exerted by payers and hospitals in understanding and abiding by the contractual arrangements.Footnote 1

Open access

Open access