1. Introduction

Adam Smith was a brilliant analyst of monetary institutions and policies. We believe economists and policymakers still have much to learn from him in this area. We are not alone. Economists often ask what Adam Smith would recommend. After the recent financial crisis, for example, Bholat (Reference Bholat2009) did exactly that in a paper titled, ‘How Would Adam Smith Fix the Financial Crisis?’

Our central theme is that one of the most important lessons we can learn from Smith is that economists and policy makers should base their conclusions about a monetary institution or policy on a careful study of the history of that institution or policy, a study that includes the experiences of other countries. Of course, the methods for studying monetary history have changed since Smith’s Day. Contemporary monetary historians rely heavily on quantitative data and abstract models. Smith’s approach was different. Smith made limited use of quantitative data, although he did make use of it when it was available. In Section 2, we examine one case in which he compiled quantitative data. He also did not employ abstract models of the type often used by contemporary students of monetary history. The technology for formally modeling historical processes did not exist in Smith’s day. Smith did employ some striking analogies. His comparison of fractional-reserve banking with a ‘waggon-way in the air,’ for example, has attracted attention (Rockoff, Reference Rockoff and Forman-Barzilai2018). Analogies do seem to have stimulated Smith’s thinking. However, he seems to have used them mainly for conveying his thinking about a particular institution or policy, rather than as a convincing reason for adopting or rejecting it.

Instead of quantitative data and abstract models, Smith based his recommendations for monetary institutions and policies on narrative histories of their evolution in Britain and other countries. In this, he resembled Irving Fisher, Milton Friedman, Anna J. Schwartz, Charles Kindleberger, Barry Eichengreen and other practitioners of the historical approach to monetary economics.

To illustrate Smith’s reliance on financial history we will cover five current monetary problems that have close analogies with problems Smith discussed: (1) Inflation, (2) banking panics, (3) public debts, (4) usury laws, and (5) central bank digital currencies.

As we explore these issues, we will find many examples in which Smith’s recommendations differed from what might be expected from a champion of free markets. These departures, of course, have been noted and analyzed before, for example, by Viner (Reference Viner1927) and West (Reference West1997). Our explanation for the many exceptions Smith made to the rule that Laissez Faire is best is simply that for the most part Smith followed where his thorough and thoughtful reading of monetary history led him. If there were many examples of a law or policy that had interfered with the free functioning of markets but had produced positive results, Smith recommended adopting it. Smith’s emphasis on historical data has been noted before—for example, by Rockoff (Reference Rockoff, Berry, Paganelli and Smith2013)—but in our view is not as widely recognised as it should be.

It may seem odd to suggest that Smith can help us with (5), central bank digital currencies; a change in the structure of our monetary system that is possible only with modern technologies. However, Smith had much to say about the evolution of money and the positive role that government can play in the payments system. One close analogy that he discussed in detail is with the Bank of Amsterdam, a government project founded in 1609. Smith, as we will discuss below, believed that the Bank of Amsterdam had substantially improved the functioning of the payments system. In Section 5, we suggest how a contemporary economist could study central bank digital currencies using Smith’s methodology.

2. Money and inflation

Smith thought that a sufficiently large increase in the monetary base would produce inflation. His evidence was the episode that led to the development of the quantity-theory of money: the Price Revolution in Europe between the 15th and 17th centuries.

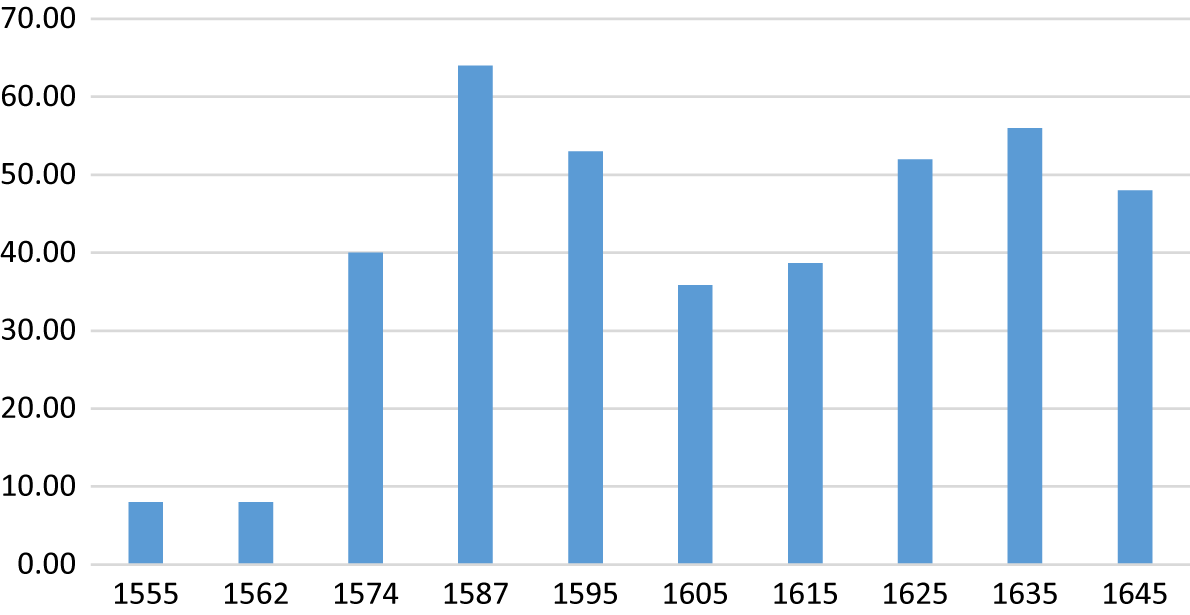

Here Smith undertook some interesting quantitative research. He used the price of wheat as a proxy for the price level because he thought that it was the major source of food for the laborer. Essentially, he was heading toward a consumer price index. (He frequently referred to the price of wheat as the price of corn, using the British term for the most important food crop.) He compiled data from published and unpublished sources. He then looked at the resulting time series and concluded that…

From about 1570 to about 1640, during a period of about seventy years, the variation in the proportion between the value of silver and that of corn, held a quite opposite course [compared with previous years]. Silver sunk in its real value, or would exchange for a smaller quantity of labour than before; and corn rose in its nominal price, and instead of being commonly sold for about two ounces of silver the quarter, or about ten shillings of our present money, came to be sold for six and eight ounces of silver the quarter, or about thirty and forty shillings of our present money. (WN 210)

He did not have data for every year. Figure 1 shows his data for years close to the midpoints of the decades Smith was focusing on in the paragraph above. We suspect that Smith would have made good use of modern data and Excel spreadsheets.

The price of a quarter of wheat, shillings

What caused the increase in the price of wheat?

The discovery of the abundant mines of America, seems to have been the sole cause of this diminution in the value of silver in proportion to that of corn. It is accounted for accordingly in the same manner by every body; and there never has been any dispute either about the fact, or about the cause of it. The greater part of Europe was, during this period, advancing in industry and improvement, and the demand for silver must consequently have been increasing. But the increase of the supply had, it seems, so far exceeded that of the demand, that the value of that metal sunk considerably. (WN 210)

What about a fiat currency? Smith lived in a world where most people assumed that gold and silver were the ultimate form of money. He noted, however, that there had been experiments with legal-tender paper currencies in the American colonies (WN 326–9). Smith concluded that these experiments had typically ended badly, although he noted that ‘Pennsylvania was always more moderate in its emissions of paper money than any of the other colonies.’ The main problem was that debtors could pay their debts with the government-issued paper at face value, even though that paper was circulating far below par against British pounds. A merchant could always refuse to sell a commodity for colonial paper at face value, but a judge had to follow the legal tender law. Smith relied, it seems, mainly on Douglass (Reference Douglass1755) for his understanding of Colonial paper money. Douglass, it must be said, impresses with his detailed knowledge of the histories of the North American Colonies. Based on Douglas, Smith concluded that …

No law, therefore, could be more equitable than the Act of Parliament, so unjustly complained of in the colonies, which declared that no paper currency to be emitted there in time coming should be a legal tender of payment. (WN 327)

Subsequently, there has been a good deal of work on the Colonial paper monies and some of it has reached conclusions that are more favorable. Farley Grubb, an expert on the Colonial currencies, recently argued that Smith relied too heavily on Douglass, who Grubb (Reference Grubb2023, 83) describes as a ‘strident anti-paper money polemicist from New England.’

In addition, the colonial experience has been used as evidence for both the quantity theory of money (McCallum, Reference McCallum1992; Mitchener, Reference Mitchener1987) which Adam Smith would have approved, and the fiscal theory of the price level (Smith, Reference Smith1984, Reference Smith1985; Cochrane, 2023).

3. Banking panics and the real bills doctrine

Smith understood the problem of banking panics. In 1772, a large Scottish Bank, the Ayr Bank failed, intensifying a financial panic that was gripping Britain. Smith was well acquainted with this failure in part because he advised several of the major investors. Indeed, it has been suggested that Smith’s efforts to help friends involved with the Ayr Bank failure may have delayed publication of the Wealth of Nations.

A modern monetary-policy economist would immediately think of lender of last resort operations to bailout failing banks, such as the Ayr Bank, to arrest or at least ameliorate the panic. Smith, however, cannot be enlisted as an advocate of a lender of last resort. He recognised that the Bank of England had lent heavily during the crisis. However, he did not go on to approve the lending, let alone call for such lending in future panics. The reason may be that the institutions that we would now think of as candidates to take on the role of lender of last resort, such as the Bank of England, lacked the resources for such actions. They were, after all, fractional reserve banks that held finite amounts of specie. Indeed, the Ayr Bank had been set up by moneyed interests in Scotland to provide aid to existing Scottish banks that were experiencing difficulties. However, Smith considered codes of conduct and regulations that would prevent banks from adopting imprudent lending policies, such as those that had produced the fall of the Ayr Bank, and thus prevent the damage done by bank failures.

Smith argued that there was a specific form of bank lending that was best.

When a bank discounts to a merchant a real bill of exchange drawn by a real creditor upon a real debtor, and which, as soon as it becomes due, is really paid by that debtor, it only advances to him a part of the value which he would otherwise be obliged to keep by him unemployed and in ready money for answering occasional demands. The payment of the bill, when it becomes due, replaces to the bank the value of what it had advanced, together with the interest. The coffers of the bank, so far as its dealings are confined to such customers, resemble a water pond, from which, though a stream is continually running out, yet another is continually running in, fully equal to that which runs out; so that, without any further care or attention, the pond keeps always equally, or very near equally full. Little or no expence can ever be necessary for replenishing the coffers of such a bank. (WN 304)

By repeatedly using the term ‘real’ Smith was hoping to discourage banks from financing speculative transactions, and in referring to a ‘bill,’ Smith was referring to short-term instruments. One of the main forms of investment excluded by an adherence to real bills was long-term investments in real estate. Smith is clear about the danger.

the capital which the undertaker of a mine employs in sinking his shafts, in erecting engines for drawing out the water, in making roads and waggon-ways, &c.; of the capital which the person who undertakes to improve land employs in clearing, draining, enclosing, manuring, and ploughing waste and uncultivated fields, in building farm-houses, with all their necessary appendages of stables, granaries, &c. … such expences, even when laid out with the greatest prudence and judgment, very seldom return to the undertaker till after a period of many years, a period by far too distant to suit the conveniency of a bank. (WN 307)

The idea that banks should restrict their investments to real bills as defined by Smith has been termed the ‘real-bills doctrine.’ Mints (Reference Mints1945, 9), the historian of the doctrine, tells us that the doctrine was ‘Given its most elegant statement in all its history by Adam Smith in the Wealth of Nations,’ and that ‘He was in fact, the first thoroughgoing exponent of the real-bills doctrine’ (Mints, Reference Mints1945, 9, 25). Mints goes on to show that the doctrine was eventually adopted widely with the view that financial and monetary stability could be achieved if banks were forced to follow the doctrine. Mints is highly critical of this understanding of the doctrine and attributes considerable mischief to it. In his view real bills was not a route to monetary stability and faith in it discouraged policy makers from following other policies, such as controlling the growth of the stock of money, which would have worked.

As Laidler (Reference Laidler1981) and Perlman (Reference Perlman1989) showed, however, Smith’s endorsement of real bills is defensible because Smith was thinking of real bills simply as a code of conduct for banks that would minimise their risk of failure, not as a policy for controlling the overall quantity of money or the price level. In this respect, Smith’s willingness to look closely and with an open mind at the effects of the failure of the Ayr Bank was echoed by the emphasis that Friedman and Schwartz (Reference Friedman and Schwartz1963, 309 and passim) placed on the failure of the Bank of United States (Rockoff, Reference Rockoff2011).

Smith’s willingness to regulate banks, partly by explaining to them the policies that would be in their interest and partly by legislating restrictions remains controversial. The ‘free banking school’—see, for example, Selgin and White (Reference Selgin and White1994)—has maintained that a Laissez Faire policy would work. On the other hand, the vast history of banking crises, most recently the 2008 Global Financial Crisis (Bordo et al., Reference Bordo, Eichengreen, Klingebiel and Peria2001; Reinhart and Rogoff, Reference Reinhart and Rogoff2009) has convinced other analysts for example Bernanke (Reference Bernanke2022) and Wigmore (Reference Wigmore2022) that subjecting bank investment policies to more regulation would be a good idea.

4. Public debts

Smith believed that in the emergency of a war it would be necessary for a government to borrow.

But the moment the war begins, or, rather, the moment in which it appears likely to begin, the army must be augmented, the fleet must be fitted out, the garrisoned towns must be put in a posture of defence; that army, that fleet, those garrisoned towns must be furnished with arms, ammunition and provisions. An immediate and great expense must be incurred, in that moment of immediate danger, which will not wait for the gradual and slow return of the new taxes. In this exigency the Government can have no other resource but in borrowing. (WN 909)

Smith did not elaborate on why taxes cannot be raised high enough and fast enough to finance a war without borrowing. Contemporary economists have discovered some plausible economic reasons. Barro (Reference Barro1979) introduced the idea of ‘tax smoothing’ and showed that in wartime, such as during the many wars that Britain fought in the 18th century, the government would finance the war by issuing sovereign debt during the war and then service and repay the debt in peacetime. This would be a more efficient method of war finance than raising taxes on present labor income leading to substitution of labor effort into leisure rather than work at a time when maximum effort was needed (Bordo and Kydland, Reference Bordo and Kydland1995). Bordo and White (Reference Bordo and White1991) showed that a credible commitment to the gold standard and its corollary a long-run balanced budget allowed Britain to engage in tax smoothing and successfully finance and win the wars against France in the 18th and 19th centuries.

The need to borrow raises an important question, what type of security should the government issue? Any form of borrowing would mean the government would have to raise taxes to pay the interest on the security and for most securities the value of the bond when it matured.

However, the government would not have to fix a definite maturity date. It could fund its borrowing by promising to pay the interest on the debt until the government chose to repay the principle, what Smith called ‘perpetual funding.’ In the extreme case, the government could, and eventually did, issue consols. With perpetual funding taxes would need to be raised only by the small amount necessary to pay the interest on the debt. Low annual taxes obviously made this form of borrowing attractive to politicians, but it carried a risk. If the public did not fully recognise the cost of wars, they would be too eager to support them.

The ordinary expense of the greater part of modern governments in time of peace being equal or nearly equal to their ordinary revenue, when war comes they are both unwilling and unable to increase their revenue in proportion to the increase of their expense. They are unwilling for fear of offending the people, who, by so great and so sudden an increase of taxes, would soon be disgusted with the war; and they are unable from not well knowing what taxes would be sufficient to produce the revenue wanted. The facility of borrowing delivers them from the embarrassment which this fear and inability would otherwise occasion. By means of borrowing they are enabled, with a very moderate increase of taxes, to raise, from year to year, money sufficient for carrying on the war, and by the practice of perpetually funding they are enabled, with the smallest possible increase of taxes, to raise annually the largest possible sum of money. In great empires the people who live in the capital, and in the provinces remote from the scene of action, feel, many of them, scarce any inconveniency from the war; but enjoy, at their ease, the amusement of reading in the newspapers the exploits of their own fleets and armies. To them this amusement compensates the small difference between the taxes which they pay on account of the war, and those which they had been accustomed to pay in time of peace. They are commonly dissatisfied with the return of peace, which puts an end to their amusement, and to a thousand visionary hopes of conquest and national glory from a longer continuance of the war. (WN 919–20)

Smith does not tell us precisely what evidence he has to back up this claim. A modern academic social scientist would probably feel compelled to cite opinion polls or other forms of quantitative data. However, Smith conveys a strong impression that he had the historical evidence to back up this claim. Smith’s generalisation occurs in the chapter ‘Of publick Debts’ in the Wealth of Nations. There Smith presents a detailed chronological history of the growth of Britain’s public debt frequently citing the impact of wars. He begins in the 17th century noting, for example, that.

It was in the war which began in 1688 and was concluded by the treaty of Ryswick in 1697 [the Nine Years War] that the foundation of the present enormous debt of Great Britain was first laid. (WN 921)

He then makes his way forward to the last date mentioned in the chronology, January 5, 1775 (WN 923). In the course of this discussion, moreover, there are many brief passages describing aspects of the evolution of public finance in France, Spain, Holland, Genoa, and Venice. The evidence is not presented in a way that a modern scholar would find persuasive. Smith does not hold the reader’s hand and explain in detail each case that supports a particular generalisation. However, one comes away convinced, as Smith probably hoped his readers would be, that his generalisations about the determinants of the growth of Britain’s public debt were derived from a deep and careful reading of the historical record.

5. Usury laws

Usury laws are one of the clearest examples of Smith’s willingness to depart from the idea that Laissez Faire is best. Smith endorsed usury laws, of a certain sort. Surely, one might argue, if you trust markets, you should trust financial markets because they are crowded with large numbers of well-informed buyers and sellers. Smith’s endorsement of usury laws troubled many subsequent economists and doctrinal historians. Smith, however, was clear. Legal maximums were a good idea. He recognised that there would be problems if the legal maximum was set too low. The point was to set a legal maximum at a level that would maximise economic growth. That could be achieved by setting a legal maximum that was above, but not too far above, the lowest common market rate of interest. A legal maximum set according to Smith’s criteria would ensure, he believed, that capital would end up in the hands of those who would make the best use of it. He explained this clearly in the following passage.

The legal rate, it is to be observed, though it ought to be somewhat above, ought not to be much above the lowest market rate. If the legal rate of interest in Great Britain, for example, was fixed so high as eight or ten per cent, the greater part of the money which was to be lent would be lent to prodigals and projectors, who alone would be willing to give this high interest. Sober people, who will give for the use of money no more than a part of what they are likely to make by the use of it, would not venture into the competition. A great part of the capital of the country would thus be kept out of the hands which were most likely to make a profitable and advantageous use of it, and thrown into those which were most likely to waste and destroy it. Where the legal rate of interest, on the contrary, is fixed but a very little above the lowest market rate, sober people are universally preferred, as borrowers, to prodigals and projectors. The person who lends money gets nearly as much interest from the former as he dares to take from the latter, and his money is much safer in the hands of the one set of people than in those of the other. A great part of the capital of the country is thus thrown into the hands in which it is most likely to be profitably employed. (WN 357)

Smith’s endorsement of usury laws has had many critics. One of the first and most famous was the philosopher Jeremy Bentham who took Smith to task in a famous essay: ‘Defence of Usury’ (Bentham, Reference Bentham1787).

Levy (Reference Levy1987) and Paganelli (Reference Paganelli, Peart and Levy2008) have shown that Smith’s endorsement of usury laws was consistent with his moral and legal philosophies. But what evidence did Smith have that a rate of usury set according to his rules would increase the rate of economic growth? Inevitably, he turned to economic history for the answer. Although he does not share all the details of his reading, he presents a detailed chronology of English usury laws in chapter IX ‘Of the Profits of Stock,’ listing both those occasions when the legal maximum was set too low or too high, and those when it was set with ‘great propriety’ (WN 106). He goes on to discuss the rate of usury in France, Holland, and the North American and West Indian colonies. His main purpose in looking at these usury laws was to get a sense of normal market rates of interest; that is a sense of the normal yield of capital. Nevertheless, it is clear to the reader of the Wealth of Nations that Smith’s judgment about the wisdom of deploying legal limits on interest rates was based on a substantial knowledge of the history of usury laws and their effects. Once again, it is Adam Smith the monetary historian who convinces us that the policy he advocates is the right one.

6. Central bank digital currency and the evolution of the monetary system

In some ways, the development of central bank digital currencies recreates the evolution from metallic money to paper money that Smith discussed in the Wealth of Nations. A striking analogy with the introduction of a central bank digital currency is to be found in Smith’s discussion of the origin and value to commerce of the Bank of Amsterdam. This was a government project, founded in 1609. Smith (WN 479–88) explains that the Bank improved the functioning of the payments mechanism by replacing a mixture of coins with transferable credits on the Bank. Merchants found it much easier to complete transactions with these receipts than with the mixture of foreign and domestic coins of uncertain value (often worn or deliberately altered) that were the main instrument for making payments before the Bank was established.

Although the Bank of Amsterdam was able to provide some revenues to the state—essentially warehouse fees—Smith thought that it was essentially a 100 per cent reserve bank and did not augment its earnings by making loans. However, Quinn and Roberds (Reference Quinn and Roberds2024) relate the downfall of the Bank of Amsterdam in the 18th century to its moving in the direction of fractional reserve banking but without adequate specie or fiscal backing. The Bank of England and other private banks in England, were fractional reserve banks. Fractional-reserve banking had both advantages and disadvantages compared with the 100 percent reserve policy that Smith attributed to the Bank of Amsterdam. Fractional reserve banking saved on specie reserves, a valuable asset, but the banks were vulnerable to debilitating runs.

The Bank of England, Smith believed, was ‘a great engine of state’ (WN 320). It could aid the state by marketing its debt and lending to it. However, there was also a risk. Smith thought that …

In those different operations its duty to the publick may sometimes have obliged it, without any fault to the directors, to overstock the circulation with paper money. (WN 320)

Smith, evidently, would have immediately understood the role of the Federal Reserve in creating inflation in the United States and why, for example, it changed course in 2015 and began a policy of raising rates. He might have added the Federal Reserve policy in recent years as another example to reinforce the point made in the quotation above if he was writing a new edition of the Wealth of Nations.

The other commercial banks in Britain were also fractional reserve banks, so most transactions were carried out with bank-issued paper money rather than specie. In explaining the costs and benefits of fractional-reserve banking, Smith created one of his most memorable metaphors.

The judicious operations of banking, by providing, if I may be allowed so violent a metaphor, a sort of waggon-way through the air, enable the country to convert, as it were, a great part of its highways into good pastures and corn-fields, and thereby to increase very considerably the annual produce of its land and labour. The commerce and industry of the country, however, it must be acknowledged, though they may be somewhat augmented, cannot be altogether so secure when they are thus, as it were, suspended upon the Dædalian wings of paper money as when they travel about upon the solid ground of gold and silver. Over and above the accidents to which they are exposed from the unskillfulness of the conductors of this paper money, they are liable to several others, from which no prudence or skill of those conductors can guard them. (WN 321)

Recognising both the potential benefits and costs of moving from a metallic currency to a currency based primarily on private bank paper, Smith did not shy from calling for regulations that he thought would permit society to reap the benefits while minimising the risks.

If bankers are restrained from issuing any circulating bank notes, or notes payable to the bearer, for less than a certain sum, and if they are subjected to the obligation of an immediate and unconditional payment of such bank notes as soon as presented, their trade may, with safety to the public, be rendered in all other respects perfectly free. (WN 329)

All of this suggests that Smith would have been open to the possibility that digitisation of currency could improve the productivity of the economy, just as fiduciary money did compared to specie. He might also have favored the central bank issuance of digital currencies (CBDC) rather than leaving it to the private sector on the same grounds that Friedman (Reference Friedman1960) who made the case for a government monopoly of the issuance of fiduciary currency—that the issue of private currency would lead to overissue and inflation as competition would reduce the exchange value of money to its marginal cost of production, which was close to zero. In other words, that money is a public good (Bordo, Reference Bordo2022; Bordo and Roberds, Reference Bordo and Roberds2022).

However, in thinking about how Adam Smith would approach the question of whether it would be worthwhile to create a central bank digital currency, we should remember is that he would also want to take an in-depth look at the experiences of countries that had experimented with central bank digital currencies. Several have begun doing so, and Smith would have been very interested in the results, as we should be.

7. Conclusion

Adam Smith was a keen observer of the monetary and banking problems of his time. He developed analytical insights, often explained with striking metaphors, to understand them. But what the case studies discussed above show, we believe, is that one of the most important lessons we can learn from Adam Smith is his methodology. Ultimately, he relied on economic history to determine which institutions and policies were worth adopting and which should be rejected. In this respect, he was a forerunner of Irving Fisher, Milton Friedman, Anna J. Schwartz, Charles Kindleberger, Barry Eichengreen and other successful practitioners of monetary history.

This aspect of Smith’s thinking has been noted before; for example by Viner (Reference Viner1927, 216 and passim) and Gherity (Reference Gherity1994). However, too often the assumption is that Smith reached his conclusions simply by deciding how closely they followed from a pro-market ideology.

Smith did not eschew quantitative research; witness his collection of price data to support his analysis of the effects of gold and silver from the new world on the price level. Moreover, unlike much of the economics profession today, he did not start with an abstract, stylised model and then apply it to the real world. To reiterate, we can gain many useful insights into current monetary problems by considering analogies between the problems Smith analyzed and those of our own time. However, the most important lesson we can learn is the value of careful generalisations based on intense examination of the origin and evolution of monetary institutions and policies.

Open access

Open access