3.1 Introduction

Barely ten minutes into the annual United Way Live United event at Prairie Meadows Racetrack and Casino in Altoona, Iowa, on May 10, 2023, KCCI Channel 8 News This Morning anchor Alyx Sacks told the crowd: “If you’ve attended this event in the past you might notice the lunches are being handled a little bit differently this year. Thanks a lot to the work by Prairie Meadows, any lunches that are not served today will be donated to our good friends at Urban dreams so thank you Prairie Meadows” (United Way of Central Iowa 2023).

The statement received warm applause as United Way leadership basked in goodwill from a community where the often unimagined reality that food insecurity could exist in the middle of an agricultural state pulled at the heartstrings of many local leaders. This publicly stated commitment, backed by a secured offtake agreement with Urban Dreams, a local nonprofit working to “overcome obstacles and uplift underserved and underrepresented people” in Des Moines, was a major change from the same awards event one year earlier.

The year 2022 saw many celebrated initiatives designed to fight hunger, from the Greater Des Moines Partnership’s 15th Annual Hunger Fight (Zimmerman Reference Zimmerman2022) to the DSM Fellows Capstone Panel praising initiatives such as the Corporate Giving Garden on Farm Bureau’s West Des Moines office campus (Greater Des Moines Partnership 2022). From the OpportUNITY Plan to Iowa Stops Hunger to the social media campaigns such as #NoHungerCentralIowa, hunger was an inequity that most civic leaders felt they could take on without fear of the common socioeconomic third rails in an overwhelmingly white state then grappling with its place in a pandemic-riddled society still reeling from George Floyd’s murder in Iowa’s northern neighbor. Ending hunger was an environmental, social, and governance (ESG) badge of honor that every local executive could wear proudly at a time when many Des Moines-based diversity, equity, and inclusion (DEI) directors felt required to intentionally censor words such as “diversity” from their public statements. Efforts to end hunger were an ESG currency that many felt comfortable trading in, and the United Way staked their claim that morning to the intangible value of feeding those less fortunate.

Yet, unlike in 2023, less than two hours after the 2022 Live United awards banquet kicked off, more than eighty meals that could have been donated to Urban Dreams that year were in the trash.

Aubrey Alvarez, the Executive Director of United Way-funded food rescue organization Eat Greater Des Moines (EGDM), who was preparing to take those meals to Urban Dreams in 2022, was brought to tears when Prairie Meadows staff intervened, preventing her from taking the perfect edible food to Urban Dreams, and instead threw all of the more than eighty meals into the trash right in front of her. Her tears led to anger at this perceived hypocrisy and fueled Aubrey to pen an emotionally stirring letter sent to EGDM supporters where she mused, “I’m regularly told is to ‘be patient’ … [but] how many more studies, data points, and personal stories will be enough for real change?” (Alvarez Reference Alvarez2022).

By calling out Prairie Meadows banquet staff when writing, “asked if they really wanted this food to go into the garbage instead of to a person, their answer was a resounding yes” (Alvarez Reference Alvarez2022), Aubrey had poked the eye of an organization to which United Way was indebted. By 2022, Prairie Meadows had given $2.1 billion over just six years to local nonprofits and organizations often supported by the United Way (Prairie Meadows 2022), including $1,000,000 to the United Way of Central Iowa directly in 2020 (Stewart Reference Stewart2020). On July 8, 2022, less than sixty days after Aubrey’s call to action for EGDM supporters, United Way of Central Iowa Chief Community Impact Officer Renée Miller sent a letter saying they would no longer provide funding to support EGDM’s efforts to end hunger in central Iowa (Ta Reference Bataille, Hrozensky, Moranta and Campos2022). No additional explanation was given in the letter, though when pressed, Axios was told the defunding was due to “EGDM staff that didn’t align with United Way’s “inclusive, respect-based work,” according to a statement the organization sent to Axios that it declined to attribute to a specific person (Ta Reference Bataille, Hrozensky, Moranta and Campos2022).

United Way of Central Iowa pulling its funding left EGDM with an economic shortfall that exceeded more than half its senior leadership payroll. Less money meant less time to organize fewer resources to distribute, resulting in fewer people getting fed. For Aubrey, it meant many would go hungry because a few were embarrassed.

The core issue evident on May 9, 2022, at Prairie Meadows, which almost directly drove the nationally recognized battle pitting the Food Bank of Iowa against nearly every other nonprofit in Iowa fighting food insecurity,Footnote 1 is the fundamentally asymmetrical nature of ESG value realization and extraction. In short, small organizations such as EGDM struggle to receive fair compensation for the ESG value they create. Yet at the same time, donations to organizations that claim to create ESG value at scale rise exponentially even in the face of proven greenwashing or fraud. Food rescued by EGDM provides their donors with tax credits equal to the market value of the food being donated, a financial windfall for high-margin products such as bread, yet food rescue organizations struggle to convince donors that it is fair to share in the directly identifiable economic benefit those nonprofits provide. At the same time, donations to United Way of Central Iowa exponentially appreciated if donors believe food is being recovered even when it is being thrown away.

Unverified promises made in the opening remarks of a celebratory lunch to generate undue intangible value are at the heart of the greatest threat to ESG. Dependencies on opaque metrics compiled at scale are what lead to scandals such as Verra, where “more than 90% of [their] rainforest carbon offsets … are worthless” (Greenfield Reference Greenfield2023). Lack of ESG standardization for both carbon-based and noncarbon derived value is why verification costs often exceed $40,000 to create a tradeable voluntary carbon offset or credit typically worth less than $6 since 2022 (Carbon Credits.com 2023). These combinations of opacity and uncertainty lead to systems where evidence of effect is so difficult to prove that reputation is used as a proxy for verifying action. Yet when an organization is small, there is no benefit of the doubt, and even less access to the fair value being produced.

Despite its size, calculating EGDM’s ESG value to its community can be done relatively straightforwardly. For example, Feeding America data shows that 7.3 percent of Iowans were food insecure in 2020 (Feeding America 2023). Closing the food security gap that year was projected to require $112,519,000 at an estimated cost of $3.05 per meal. With the average adult needing between 0.9 and 1.2 pounds of food per meal to feel satisfied, this could have been achieved by providing roughly 33 million pounds of food to 229,500 people. The food rescued by EGDM that went directly to reducing food insecurity during 2020 was enough to meet over 12 percent of that projected hunger gap (Eat Greater Des Moines 2023). Yet the cash donations supporting those executing the organization’s mission barely exceeded $186,000 during that year. Using this Feeding America data as a benchmark, the EGDM team solved a $13.6 million problem for less than 1.4 percent of the expected cost.

The net ESG value created by EGDM in 2020 may have arguably exceeded $13.4 million, yet Aubrey struggled to monetize that intangible value. Like any small nonprofit, donor focus rested on covering and containing costs versus rewarding achievement. Food donors saw EGDM’s services as a waste management alternative instead of EGDM being the source creating the near windfall tax credits – equaling the retail value of the food being rescued – providing outsized benefits to food donor bottom lines. Donor reluctance to fairly account for the value EGDM created led Aubrey to seek out ESG markets, yet food rescue never fit nicely into the plethora of nearly exclusively carbon-based ESG credits. While food rescue reduces the number of miles food had to be transported, reduces the energy required for production, and reduces energy conversion at any ingredient’s source, a marketable greenhouse gas (GHG) reduction had too many variables to track. While rescuing the food prevented it from producing GHGs as it decomposed in a landfill, the true net impact compared with its consumption is difficult to truly evaluate. And calculating any GHG reduction estimation for the ESG benefit of feeding food insecure people is a challenge that many then consider void of any discernible starting point.

It was in this effort to find a path for monetizing the ESG value of EGDM food rescue activities that did not nearly conform to carbon-based equivalency calculations that Aubrey came across regenerative authentication credits (RACs) and the Human Impact Unit (Hu) to price them. Through two RAC auctions between fall of 2022 and spring of 2023, Aubrey was able to secure investment from individuals and organizations who would not have otherwise donated to EGDM, directly marketed the intangible value EGDM created instead of losing value by using a carbon-based intermediary, and proved an average market value of $3.53 per pound rescued. Through RAC sales, Aubrey had found a vehicle for moving from a donor appetite of $0.014 per dollar of ESG value created to a market paying a 16 percent premium over Feeding America estimates. For organizations such as EGDM, these kinds of RAC markets priced in Hu may end up being the equalizer that turns today’s nonprofits from being the guests at galas or luncheons to the benefactors through fairly monetizing the intangible value they create in our communities.

3.2 ESG as Knowledge Commons Governance

3.2.1 How EGDM Demonstrated the Broader Issues in ESG

This chapter argues that the fundamental problem limiting community Trust in ESG efforts is its use of modeled data or secondary indicators to prove its Truth. In the case of the disagreement between EGDM and United Way, arguments could be made that EGDM was measuring ESG impact in pounds of food rescued, where United Way was measuring the number of participating organizations. In the ESG industry, more broadly, it will be argued here that the primary measure of success since 1997 has been tied to carbon when the majority of ESG goods does not have a meaningful carbon component. This lack of a carbon component requires valuations to adopt rather tenuous relationships as Truth that are later identified as being in conflict with the same community’s interpretation of objective truth.

While it is commonly perceived that issues of double counting or “greenwashing” are typically products of fraud (Runyon Reference Runyon2022), the framing of limited ESG Trust being due to misaligned communication identified earlier is more likely. For example, very few projects directly model carbon emissions or sequestration, yet carbon credits are awarded and traded based on point estimates of metric tons of carbon. When estimation methods or the input data to these estimates change, which is common, the community interprets this as a modification of its previously accepted objective truth. This chapter argues that Truth must remain immutable in order to facilitate Trust.

Where ESG value is tracked without the use of carbon credit equivalency, historic deficiencies in the definitions of what constitutes ESG value have similarly damaged Trush by again misidentifying Truth that has the ability to align with the community’s interpretation of objective truth. For example, the most common method that early ESG investors used to expand access was to invest in equities of publicly traded companies that were believed to embody the objectives of or were positively contributing to meaningful ESG outcomes. These types of secondary mechanism strategies do not guarantee the desired actions will be taken as seen with the Volkswagen emissions scandal (2015), Theranos fraud (2016), Wells Fargo fake accounts scandal (2016), and the Rio Tinto Juukan Gorge destruction (2020). Identically to carbon credits, these are examples where Truth was applied to items that were more variable than expected, leading to observations of the defined Truth that conflicted with the same community’s perception of their objective truth, leading to losses in Trust.

These issues that emerge when Truth is applied as variables whose performance has a reasonable certainty that they will conflict with the community’s interpretation of objective truth are addressed in this chapter. These issues are contrasted with the Hu valuation methodology and RAC asset, tools that more clearly define Truth using tangible, objective measures, and valuation estimations using relativistic comparisons of measurement units that directly reflect the ESG intentions of a valued action. It is argued herein that these two strategies reduce the prevalence of conflicts between any stated Truth and the community’s ability to recognize it as objectively true.

3.2.2 ESG Governance as Knowledge Commons

ESG governance can be theorized through the linkage between an environmental commons (EC) and a knowledge commons (KC). As explained in Chapter 1, every EC has a corresponding KC for the purpose of managing the shared environmental resources. The relationship between an EC and its associated KC is bidirectional, creating an interdependency between EC governance and KC governance. “Knowledge” refers to “a broad set of intellectual and cultural resources.” As Strandburg, Frischmann, and Madison explain, “The basic characteristic that distinguishes commons from non commons is institutionalized sharing of resources among members of a community” (Strandburg et al. Reference Strandburg, Frischmann, Madison, Strandburg, Frischmann and Madison2017, 10). KC is an institutional approach to governing the management or production of a particular type of resource – knowledge (Strandburg et al. Reference Strandburg, Frischmann, Madison, Strandburg, Frischmann and Madison2017, 10). Overall, KC is the institutionalized community governance of the sharing and creation of information, science, knowledge data, and other intellectual and cultural resources. This includes information, science, knowledge, creative works, data, and so on.

ESG can be perceived as a KC created to manage the EC. The environmental risks ESG aims to govern include declining biodiversity, pollution, resource scarcity; and potential climate change impacts, for instance (Gnanarajah and Shorter Reference Gnanarajah and Shorter2022, 1). ESG factors are considered to be an integral part of discussions about sustainability, “an approach that creates long-term shareholder value through managing opportunities and risks that derive from economic, environmental and social developments” (Gnanarajah and Shorter Reference Gnanarajah and Shorter2022, 1). ESG is typically fulfilled by reporting, such as publishing a sustainability report or disclosing data through their web pages, showcasing the company’s ESG performance.

The March 6, 2024, adoption by the US Securities and Exchange Commission of “rules to enhance and standardize climate-related disclosures by public companies and in public offerings” (US Securities and Exchange Commission 2024a) represented another significant step towards the standardization of ESG and sustainability reporting. The preamble notes that the rules “were modeled on the [Task Force on Climate-related Financial Disclosure] TCFD disclosure framework … that provide a structure for the assessment, management, and disclosure of climate-related financial risks: governance, strategy, risk management, and metrics and targets” (US Securities and Exchange Commission 2024b, 37) and

concepts developed by the [Greenhouse Gas] GHG Protocol for aspects of the final rules, as it has become a leading reporting standard for GHG emissions. Because many registrants have elected to follow the TCFD recommendations when voluntarily providing climate-related disclosures, and/or have relied on the GHG Protocol when reporting their GHG emissions, building off these reporting frameworks will mitigate those registrants’ compliance burdens and help limit costs.

When looking at the other frameworks referenced in the rule such as CDP Worldwide (formerly Carbon Disclosure Project), Sustainability Accounting Standards Board, and Global Reporting Initiative (GRI); or the United Nations Global Compact and its Sustainable Development Goals, the International Sustainability Standards Board International Financial Reporting Standards Sustainable Development Goals, or Climate Disclosure Standards Board framework, the underlying implication across these tools is the risks businesses will face in the future are due to climate change that is most likely a result of GHG emissions, which can be characterized using carbon dioxide (CO2) emissions coefficients or factors (US Energy Information Administration 2024). These frameworks and tools provide access to a perspective that each reporting company will have a cost of someday dealing with the effects of climate change or must now pay a cost for helping to avoid it, with the latter seen in the regulations requirement that a company report on any “carbon offsets and renewable energy credits or certificates (RECs) if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals” (US Securities and Exchange Commission 2024a).

The broad acceptance of climate change being the primary risk that ESG reporting is designed to characterize, and that this risk can be mitigated through GHG emissions reductions, has empowered a robust carbon trading industry. This industry of emissions reductions or carbon sequestration tracking and auditing, leading to a wide range of carbon offset or credit generation and trading programs or markets, has driven most to model any corporate value owing to ESG initiatives in terms of metric tons of CO2 since that metric can be valued using efficient carbon markets.

The carbon data cycle typically goes as follows. First, firms communicate their carbon performance to stakeholders through a variety of channels (In and Schumacher 2021, 4). Firms can adhere to or fall under carbon emissions disclosure regimes, either mandatory or voluntary (In and Schumacher 2021, 4). Once a firm discloses its carbon performance, the data is then analyzed by third-party rating agencies, which act as intermediaries between company disclosures and investors seeking to access and use that data (In and Schumacher 2021, 4). These rating agencies create indicators and metrics based on the data provided by firms, distinguishing between high-carbon performers from low-carbon performers (In and Schumacher 2021, 4).

However, there are several issues with this model. First, while carbon data has been commonly used as an indicator, the majority of ESG goods do not have a meaningful carbon component, leading to a disconnect between ESG goals and actual environmental impact. Most ESG initiatives cannot be appropriately measured using CO2 equivalence. For example, the primary value of food rescue is completely unrelated to carbon emissions reductions. The same can be said for water reclamation, habitat restoration, community literacy, or data governance, just to name a few. The disconnection between meaningful ESG efforts and the most popular method of valuing ESG as a function of carbon credits or offsets results in valuations that are either inaccurate or generally inappropriate for these “beyond carbon” initiatives.

Second, the lack of standardized metrics and reporting frameworks can result in inconsistent data, making it difficult to compare and assess the effectiveness of ESG initiatives across different organizations. Overall, there is an inconsistency of firm-originating carbon data (In and Schumacher 2021, 11). It is likely that companies take advantage of the current systemic inconsistencies (In and Schumacher 2021, 5). Firms have been found to employ a variety of methods for reporting both direct and indirect emissions under voluntary regimes (In and Schumacher 2021, 12). Rating agencies are themselves inconsistent, leading to low convergence between ratings (In and Schumacher 2021, 12). In fact, they are incentivized to highlight their climate mitigation activities or ambitions as more progressive than they actually are (In and Schumacher 2021, 12).

3.3 A Polycentric ESG Knowledge Commons Governance: Hu and RAC

3.3.1 Valuing ESG and Sustainability Efforts: Human Impact Unit

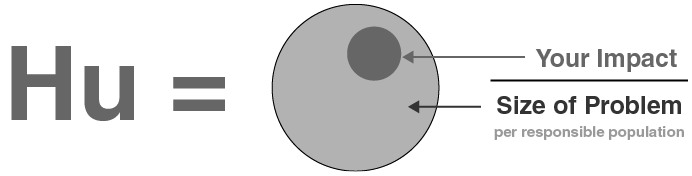

The valuation challenge of ESG has sparked work on the Hu methodology, which was publicly introduced in a 2023 white paper (Gillibrand and Draper Reference Gillibrand and Draper2023). The Hu methodology starts from the assumption that ESG initiatives are intended to address conditions that exist owing to human actions or inactions. It then reasons that, if a normalizing denominator is found for directly comparing these previously disparate actions, valuations for actively traded initiatives such as carbon reduction or sequestration could be directly compared with beyond carbon efforts. This normalizing factor used to calculate a project’s Hu is found by defining the size of problem (SOP) per citizen in the relevant community in terms of the impact’s measurement units (Figure 3.1).

Human Impact Unit (Hu) normalization formula.

Figure 3.1 Long description

Diagram illustrates a normalization formula for the Human Impact Unit. On the left is the text Hu followed by an equals sign. To the right is a large shaded circle representing the Size of Problem per responsible population. Inside this circle is a smaller shaded circle representing Your Impact. Arrows point to each circle with corresponding labels. The layout visually conveys that the Human Impact Unit is based on comparing an individual’s impact to the overall size of the problem.

The SOP is typically a discoverable for many ESG challenges without much effort, as it is most similar to the serviceable addressable market or served available market common within entrepreneurial education (Blank and Dorf Reference Blank and Dorf2012, 226). Finding the SOP is most directly found by the practitioner posting the question: “How much of my fix for this problem would be required before the problem is solved?” For example, if an organization is looking to calculate its impact in Hu for every ton of plastic it removed from the ocean, the SOP would be the total amount of harmful ocean plastic, or 6.1 million tons as of 2019 (Gillibrand and Draper Reference Gillibrand and Draper2023). The more challenging aspect of the analysis is identifying the community that this SOP should be normalized against.

Given the core premise behind the Hu methodology, the community associated with the SOP should be defined as those who could have prevented the problem. In the example of ocean plastic waste, the challenge is fully identifying who truly was capable of preventing the problem. Since it is an international problem, it is the population of the world that is at fault? Or since children are likely not large contributors or capable of supporting laws that would have prevented such waste, should they really be included? Or should the community at fault really be those who are directly causing the waste, even though lawmakers could make the production of such waste far more risky with stricter laws? Or does it come back to the voting public since it is their ambivalence to the issue that enables inaction on the part of our governments? The fact that these are not straightforward questions, and are fraught with consequential trade-offs, provides context for the power of the Hu methodology when supporting the complex and uncertain challenges posed by ESG.

The immediate value of the Hu, though, is that normalizing the impact made by the SOP being addressed allows projects with no public market to price their impact using their Hu equivalence to active markets. For example, agricultural runoff is a significant ESG issue that requires meaningful intervention, yet meaningful impact is measured in nitrogen and phosphorus runoff reductions. Unlike other efforts where improvements can be modeled in GHG reductions, such as energy reduction measures in a commercial office building, the ESG benefit of reducing nitrogen and phosphorus runoff is the improved water quality. The fact that the true benefit does not have a carbon emissions link, even though clean water clearly improves the environment, means valuing this activity cannot use typical approaches that require carbon emissions factors. In the state of Iowa, the SOP for agricultural runoff pollution is massive. Runoff from the state of Iowa alone is estimated at just under 1.1 million tons of the nearly 2 million tons of nitrogen and phosphorus pollution that enters the Mississippi River each year as of 2019 (US Environmental Protection Agency 2023c), and has been modeled as the cause of more than 55 percent of the Gulf of Mexico dead zone (Eller Reference Eller2018). This problem is one that can clearly be addressed through human intervention because its cause can be directly attributable to humans. The vast majority of agricultural runoff issues in the state of Iowa are caused by the approximately 143,000 producers as of 2022 who either directly pour the outputs of their field tile drainage systems directly into state waterways without any treatment, or the runoff is enabled by producers associated with operations that allow such practices to occur (Jordan Reference Jordan2022). By scoping the problem in this manner, the Hu methodology would attribute each individual classified as an Iowan producer as contributing 7.45 tons per year to expansion of the Gulf of Mexico dead zone. This normalizing factor would allow a project that sequesters 10 tons of phosphorus each year from Iowa rivers to define its impact as 1.3 Hu per year. Following a similar process using the average CO2 emissions across the US and carbon credit pricing as of the first financial quarter of 2024 to find a value per Hu of $1,492.40 (Meidh Technologies 2023a) provides a basis for pricing the intangible value of a 10-ton reduction in phosphorus at $14,924. This approach still currently requires active markets such as carbon to provide a guide price, yet the Hu method allows that price to be directly related to the benefits provided in a manner that accounts for the cost and impacts on the communities impacted.

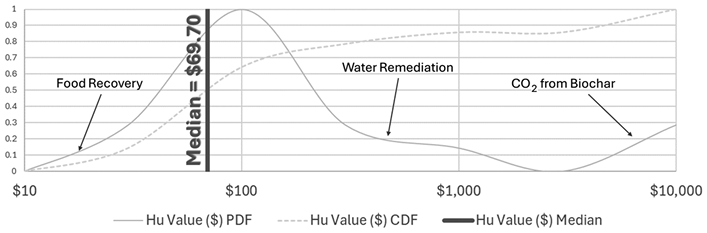

The ability for the Hu to provide a normalizing comparator across disparate ESG efforts is uniquely valuable. Yet an asset is only worth what someone will pay for it. Reexamining the food rescue example from earlier, when the intangible value of EGDM efforts was actually auctioned, it fetched $3.53 per pound. Taking a national view of food rescue, one Hu can be calculated as being worth 23.4 pounds of food (Meidh Technologies 2023a). If accurate, this Hu estimate means the food recovery efforts performed by EGDM given the Hu valuation used in the agricultural runoff example given here should be worth $67.78 per pound versus the $3.53 per pound actually paid by bidders. Similar variations are seen when looking at various market estimates or use cases, as seen in the valuation distribution computed with June 2024 data (Figure 3.2).

Hu valuation, in US dollars, probability density function and cumulative density function as of June 2024.

Figure 3.2 Long description

Figure is a line graph plotting Hu valuation in US dollars on a logarithmic horizontal axis ranging from 10 to 10,000. The vertical axis runs from 0 to 1. Three elements appear: a light solid line showing the Hu Value probability density function (PDF), a dashed line showing the cumulative density function (CDF), and a bold vertical line marking the median at 69.70 dollars. Text labels identify example points along the PDF curve: food recovery near the lower dollar range, water remediation around the mid-range, and CO subscript 2 from biochar in the higher dollar range. The graph illustrates how Hu valuation is distributed and accumulated as of June 2024.

This variation is definitely stark, but does not indicate the Hu model is ineffective. It indicates more that the means of transferring the intangible values associated with ESG efforts, and the evidence supporting the validity of the actions behind the projected values, is highly inefficient and must be better and more transparently understood.

3.3.2 The Regenerative Authentication Credit (RAC)

The paper “The Problem of Social Cost” by Ronald H. Coase (Reference Coase1960, 3) could reasonably be seen as the catalyst for the modern environmental credit and offset trading industry. Its proposal that applying property rights to pollution would encourage actors to efficiently control it through economic arbitrage (Coase Reference Coase1960) appeared influential as the US Environmental Protection Agency (EPA) efforts to reduce sulfur dioxide and nitrogen oxide emissions saw the Agency introduce an “emissions trading system in 1977 that allows emissions from new sources to be offset by reductions from existing sources and later allowed for states to bank ‘excess’ emissions reductions” (Chandrasekhar Reference Chandrasekhar2023). This cap-and-trade strategy was first rolled out successfully with the Leaded Gasoline Phasedown program between 1982 and 1987. With concurrent advocacy around the Montreal Protocol system for tradable permits to reduce chlorofluorocarbon usage (Farber Reference Farber2004), World Resources Institute land-based carbon-offset projects (World Resources Institute 1992), and Project 88 efforts to explore cap-and-trade efforts more broadly (Stavins Reference Stavins1988), successful EPA programs for sulfur dioxide and nitrogen oxide were rolled out through the 1990s and early 2000s in the US (Schmalensee and Stavins Reference Schmalensee and Stavins2015). While early offset discussions were broadly inclusive and wide ranging with regard to the environmental projects that could be solved, the Kyoto Protocol caused inertia to start building in 1997 towards GHG equivalency as the frame through which ESG has been primarily viewed since (Pearce Reference Pearce2021). For example, even the most recognized environmental offset programs of Renewable Energy Certificates introduced in 2001 for renewable electricity, Renewable Identification Numbers approved in 2005 for renewable liquid and organic fuels, and the Low Carbon Fuel Standard approved in 2009 to reduce the carbon intensity of liquid fuels in California are all use-specific proxies for carbon credits.

Even with the growth of voluntary markets since the 1999 launch of International Emissions Trading Association (International Emissions Trading Association 2023), most noncarbon markets have remained academic pricing exercises or conceptual secondary markets, with both typically slowed by the complexity of developing universally accepted models or standards. The realities of proving carbon claims has routinely left many calling for more standardization or Commodity Futures Trading Commission regulation (Fredman and Phillips Reference Fredman and Phillips2022), yet the science of carbon and other environmental phenomena is not straightforward. It was in this environment that RACs were created in 2022 to address the core flaw seen in many carbon-defined offsets.

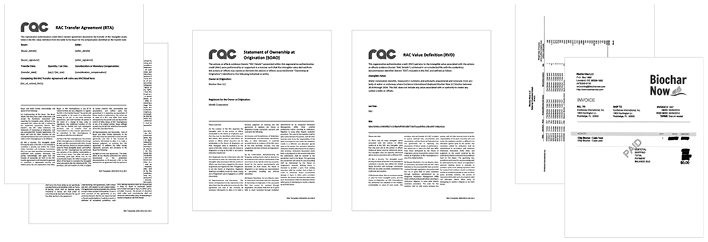

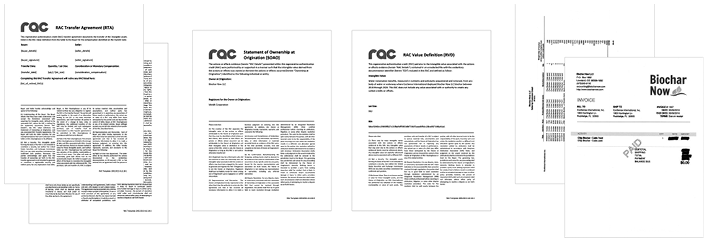

A RAC is a contract for transferring intangible ESG value from the originator to any future buyer (Figure 3.3). Each RAC is a combined document made up of the following components (Packin 2023):

Redacted Evidentiary Documents. The originator has the right to choose what evidence of any claim it makes it included for public viewing. This evidence may be a redacted version of an unredacted copy, or some other form for presenting the sensitive information that is stored elsewhere.

RAC Value Definition (RVD). This document contains the definition of the intangible value represented by the RAC, the evidentiary document identifier (EDI) which is a Secure Hash Algorithm 256-bit (SHA256) hash of the unredacted evidence proving the actions that led to the generation of the defined intangible value, and lot size defining the number of units into which the RAC can be segmented. Between the ability to segment one RAC and for one action to have many different intangible values isolated in separate RACs, an identical EDI may be present in multiple RACs.

Statement of Ownership at Origin (SOAO). This document identifies the owner of the intangible value at the time the actions associated with the RAC were taken, and the registrar who generated the RAC in the clearinghouse on behalf of the owner.

RAC Transfer Agreement (RTA). This document defines the buyer and seller for a RAC, the terms of the sale, and identifies which RAC is retired as a result of the sale. In the case of lot segmentation, two new RACs would both reference the same retired RAC.

Example of the four components that make up a RAC contract (from left to right): RTA, SOAO, RVD, and redacted evidence.

Figure 3.3 Long description

Diagram illustrates four document sets arranged from left to right to represent the components of a RAC contract. The first set shows the RAC Transfer Agreement (RTA). Next is the Statement of Ownership at Origination (SOAO). The third document is the RAC Value Definition (RVD). The final set consists of redacted evidence pages, including an invoice and supporting records. The layout provides a visual example of the four elements that together form a complete RAC contract.

The RAC framework mimics a REC in two very important ways. First, the RAC separates the intangible value of an ESG action identically to a REC, requiring the prior owner to reference any work associated with the RAC to be considered “null work” in the same way that renewably generated electricity for which its RECs are separated is considered “null energy.” Second, a RAC is built around proving the completion of a specific, tangible event in the same way a REC is directly associated with generated electricity. Additionally, the intangible value definition in the RAC mimics a feature retained from its predecessor, the Green Fuels Exchange Land Use Restriction Agreement that was first deployed in 2012 in support of a US Green Building Council Leadership in Energy and Environmental Design certification effort, of defining the intent of any actions taken without specifying or promising any specific effect or its magnitude.

This unique combination of features differs from most other offsets that reference a specific effect of a stated magnitude that can only be determined through modeling. For example, very few carbon credits are generated by direct observation of the emissions reductions they are citing. In the case of Verra, for example, the number, type, and characteristics of trees are audited, and the results of the audit are inputted into a model that projects the amount of carbon sequestered by the observed forest. This use of engineering judgment and modeling provides significant access to both error and fraud (Correa Reference Correa2023).

Excluding intangible value or modeled estimations allows a RAC to avoid this access to errors or fraud. A RAC incorporates evidence about a directly observable, tangible action; allows the originator to define any fraction of the intangible values generated by that tangible action; and then depends on the market to independently define the RAC’s value based on an analyst’s estimate of certainty regarding the claimed action based on the reviewable evidence provided in the RAC. This approach directly acknowledges the existence of uncertainties that are typically buried in the models underlying traditional offsets and provides greater accessibility to markets. For example, a food rescue organization could generate a RAC stating 46,000 pounds-worth of strawberries were rescued, and the intangible value available for sale includes all benefits associated with feeding food-insecure citizens. Since operational standards and budgets vary widely in the food recovery space, the amount of evidence that may be available to prove these tangible actions could also vary widely. The RAC framework does not prevent any organization from generating a RAC with minimal evidence. However, if all that is provided as evidence in the case of a 46,000-pound rescue is an image of strawberries, it is expected that the acceptability of this evidence will be seen in the RAC’s market valuation. In this case, it would be expected that anyone who purchases that RAC based solely on a picture of strawberries would reduce the price paid to account for any uncertainty regarding whether the amount of strawberries was actually received and the uncertainty regarding whether those strawberries made it to food-insecure individuals. Alternatively, if the food rescue organization were to instead include in the RAC a detailed document package identifying the bill of lading for the truck, the name and signature of the truck driver, the location of the offload location, and a signature of the recipient at offload, this type of a RAC would be likely to fetch a higher price.

The evidentiary variations cited in the food recovery example here would typically lead to calls for standardization. Yet the RAC framework assumes modern analytics can allow it to see even greater market efficiency by incorporating a “first principles” approach.

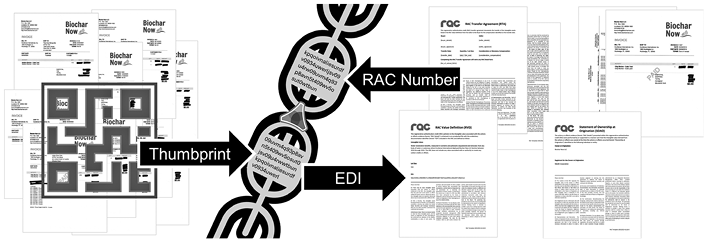

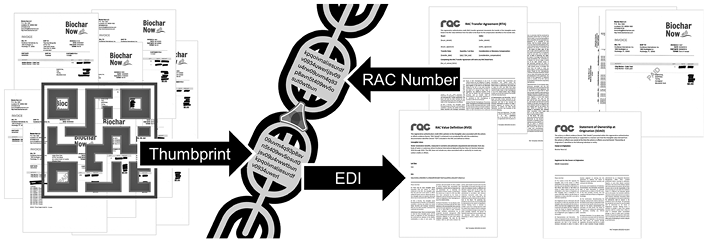

ESG RACs provides blockchain validated RAC contracts accessible via its clearinghouse. Technologically, ESG RACs:

receives the thumbprint of evidentiary documents in the form of a SHA256 hash,

commits that thumbprint token to the Trokt neopublic blockchain network (Meidh Technologies 2023b),

builds a full RAC document that incorporates the evidentiary thumbprint and the redacted evidence defined by the originator,

saves the combined RAC document so it is accessible in the clearinghouse, and

writes the thumbprint of the combined RAC document back into the Trokt network.

This basic architecture and workflow of the RAC technology solution is presented in Figure 3.4.

Process and technology involved in the creation of a RAC.

Figure 3.4 Long description

Diagram illustrates a process for creating a RAC using documents, a digital security step, and two resulting outputs. On the left, a stack of source documents appears, including repeated invoice pages from Biochar Now, with a large block-like graphic on top that serves as a thumbprint. An arrow labeled Thumbprint leads from this stack to the center. The central element is a stylized double-helix structure containing strings of random characters, representing a digital or security mechanism such as encrypted processing or a ledger system. From this mechanism, two arrows move to the right. The upper arrow, labeled RAC Number, points to documents such as the RAC Asset Transfer Agreement. The lower arrow, labeled EDI, points to documents including the RAC Value Definition and the Statement of Ownership or legal registration. The layout shows how original documents pass through a secure digital process to generate both a unique RAC number and standardized EDI outputs.

This structure for generating a RAC allows the originator to control the level of transparency it feels it must meet in order to provide sufficient trust in its ESG efforts to the market, while retaining full control over any information it deems to be commercially sensitive. When the intangible value represented by a RAC is sold, a new RAC is created by prepending an RTA that references the current RAC Number, and the new RAC Number of the new RAC is added to the Trokt network. This technique is commonly considered a “retirement” process. In order to provide the transparency needed that prevent double counting or “greenwashing,” the old RAC number will remain in the system, yet the new RAC will identify that the RAC associated with that prior token no longer represents the intangible value of the associated action.

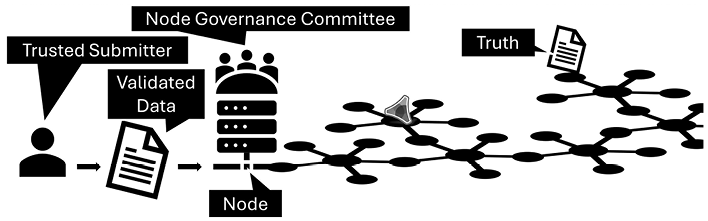

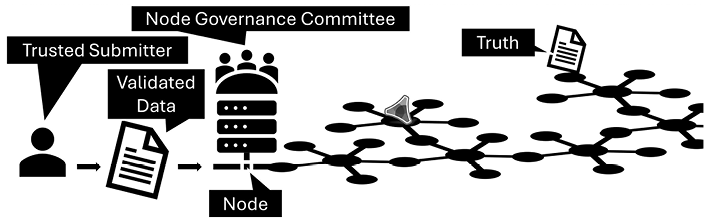

The relationship between the RAC and Truth and Trust as used in this chapter requires an understanding of the Trokt network and its Ostrom-inspired governance (Draper Reference Draper2020). In the Trokt network, all data submitted into the network is equivalently valid, permanent, and contributes to how users perceive Truth within the network. However, each node is managed by its own community that develops its own standards for when validated data is sufficient for representing a Truth that should be incorporated and collaboratively protected by the Trokt blockchain network. The Ostrom inspiration behind the Trokt network constitution is seen in three major ways. First, each community representing each node is allowed to self-organize, defining the rules for membership, operations, and data validation. Second, these self-organized node governance committees are empowered with sufficient sovereignty to initiate their own actions that they deem best for managing the Truth associated with their contributions to the network. And lastly, the wider collective of communities is able to prevent the actions of one node if it is believed those actions would harm the value of the network or wider community. Figure 3.5 presents the primary components of network governance on the left that are responsible for generating what the network considers Truth.

Structure of the Trokt network governance architecture.

Figure 3.5 Long description

Diagram illustrating a network governance process. On the left, a single human figure is labeled Trusted Submitter, and an arrow leads from this figure to an icon of a document labeled Validated Data. Another arrow directs this validated data toward a server stack labeled Node. Above the node is a group of figures labeled Node Governance Committee, indicating an oversight group associated with the node. From the node, a chain of connected dark circles extends horizontally, representing a distributed ledger or network. At the end of this chain is a document labeled Truth. The layout shows validated data submitted by a trusted individual, reviewed through a governed node, and added to a distributed chain that produces a final record called Truth.

The Trokt neopublic network differs from traditional public networks in that all Nodes must be preapproved like a private network, with any data payload arriving at any node being considered appropriate for replicating throughout the network. This differs from systems where a consensus protocol has the potential for rejecting an arriving payload for some reason. If a payload arrives at any node, it is considered validated data that is appropriate for replication.

The public component of the network is its node governance. Each node defines its own rules for what it considers data that is suitably validated such that its token should be allowed to be accepted and replicated within the Trokt network. Compliance is then required of the individuals who operate the system and send data packets of thumbprint tokens into the system. Once the thumbprint arrives and is replicated in the system, it is considered a representation of Truth.

3.3.3 Truth as a Shared Resource

RAC presents a compelling case where “Truth” is a shared resource within the ESG KC, governed by blockchain. The conception of Truth as a shared resource focuses on the fact that a token held in the system, by the nature of the network’s immutability, is permanent. This permanence, meaning that one can prove the immutability of data since the time its thumbprint arrived at the system, does not mean that this system Truth will produce information that is acceptable to all members of the community. It is possible that the data represented by a token in the system can produce misleading or incorrect information either at the time or at some point in the future owing to the discovery of additional data or information. If this situation where items considered network Truth represent data that the community feels capable of generating false or misleading information, Trust in the system will rapidly erode. Because the governance structure counts on its member community to manage the quality of the data entering the system, with parties receiving a share of any financial gain that comes from wider use of the system, the Truth the system is generating can be considered a shared resource that will be eroded in value if overused or misused.

The notion of Truth has been discussed extensively in the marketplace of ideas theory, where the pursuit of Truth serves as an important purpose of speech. In 1644, John Milton, an English poet and essayist, wrote “Areopagitica” to induce Parliament to allow unlicensed printing. He articulated the seminal view that freedom of expression enhances the social good and that unrestricted debate would lead to the discovery of truth. In 1859, John Stuart Mill, an English philosopher and economist, linked liberty to the ability to progress and to avoid social stagnation in “On Liberty” (Smolla Reference Smolla1992). Mill argues that the suppression of opinion is wrong, whether or not the opinion is true: If it is true, society is denied the truth; if it is false, society is denied the fuller understanding of truth which comes from its conflict with error; and when the received opinion is part truth and part error, society can know the whole truth only by allowing the airing of competing views. In other words, society benefits from an exchange of ideas, and people could trade false notions for factual ones, but only if they could encounter them.

Justice Oliver Wendell Holmes further introduced the concept of the marketplace of ideas into American law, following John Milton and John Stuart Mill’s discussion. In Abrams v. United States (1919), Abrams was accused of publishing pamphlets that criticized President Woodrow Wilson’s deployment of troops and advocated a strike against munitions plants. The Supreme Court ruled that publishing such pamphlets during wartime was not protected by the First Amendment. Justice Holmes famously stated in his dissenting opinion that:

When men have realized that time has upset many fighting faiths, they may come to believe even more than they believe the very foundations of their own conduct that the ultimate good desired is better reached by free trade in ideas- that the best test of truth is the power of the thought to get itself accepted in the competition of the market, and that truth is the only ground upon which their wishes safely can be carried out.Footnote 2

This statement has been repeatedly quoted by different courts as the basis of the “Marketplace of Ideas Theory.”

Under the marketplace of ideas theory, a functioning market requires two premises. First, the pursuit of objective “truth.” All the major thinkers articulate the marketplace of ideas theory based on the concept of “truth.” The marketplace of ideas is built on the belief that among all the information disseminated, some ideas are considered as true and others are considered as false. Properly understood, the marketplace of ideas is not linked to certitude that what actually emerges from the market is inviolable, objective “truth” (Smolla Reference Smolla1992). Instead, truth was never meant by “certainty” (Smolla Reference Smolla1992). Justice Oliver Wendell Holmes famously said that “certainty generally is an illusion, and response is not the destiny of man” (Holmes Jr. 1897, 8). Simply put, seeking “truth” is the intended goal while speaking.

Second, the market is functional: “Good ideas” will always survive challenges from lesser ideas. The value of the marketplace of ideas is its capacity to provide “the best test of truth.”Footnote 3 The marketplace is not the end but the quest, not the market’s capacity to arrive at the final and ultimate truth but rather the integrity of the process (Smolla Reference Smolla1992). However, the ideas of the wealthy and powerful will have greater access to the market; the marketplace will inevitably be biased in favor of those with the resources (Holmes Jr 1897, 8; Barron Reference Barron1967; Wellington Reference Wellington1979; Ingber 1984). As American philosopher Herbert Marcuse stated, “the concentration of economic and political power allows effective dissent to be blocked where it could freely emerge” (Wolff et al. Reference Wolff, Moore and Marcuse1969). In the mid 1940s, the Commission on Freedom of the Press also discovered that the press had become increasingly concentrated in the hands of fewer individuals. Therefore, the free market requires regulation, just as a free market for goods needs a law against monopoly (Chafee Reference Chafee1947). For instance, in “A Free and Responsible Press” (1947), the Hutchins Commission suggested the government finance new media outlets and that an independent government agency oversee press performance, and encouraged a subsidized and more-regulated media space, one in which a number of views could be disseminated (Commission on Freedom of the Press 1974).

Under the marketplace of ideas theory, objective truth is not only regarded as a shared belief but also as a shared resource. The puzzle within the marketplace of ideas is that empirically testing the proposition that “truth will triumph over error” would itself require some objective measure of what ideas are true and what ideas are false – a measurement that the marketplace theory itself forbids (Smolla Reference Smolla1992). However, this dilemma is the strength of this theory, which spurs us to accept the noblest challenge of the life of the mind: never to stop searching (Smolla Reference Smolla1992). As John Stuart Mill instructed, even when we are relatively confident in the truth of received opinion, “if it is not fully, frequently, and fearlessly discussed, it will be held as dead dogma, not a living truth” (Mill Reference Mill1986). When conflicting dogmas offer themselves to the market as truth, the modern mind is most comfortable subjecting each to the intellectual acid bath of adversarial contest, for our intuition and experience reveal that truth may lie somewhere in between them (Smolla Reference Smolla1992). Practically speaking, we arrive at a suitably objective truth once belief in that truth can survive all rational objection.

An example of these issues in a more relatable context may be Truth Social, the social media platform launched on February 1, 2022, and used heavily by President Donald Trump. Conceptually similar to Trokt, users who are provided access to contribute to the network generate “Truths” that other people can read. The relationship between these “Truths” and the objective reality they represent or reference is defined by the operator who created the “Truth” in the Truth Social system. As “Truths” are added, the community’s interpretation of how closely the information derived from the “Truths” contained in the network influences the level of Trust the community has in the network’s ability to retain and protect the objective truth of its system Truth. Truth Social very clearly highlights the issues that arise when the community driving the network is able to see validity in its network Truth when the information accepted as objective truth by that community is in direct opposition to what other communities consider objective truth.

3.3.4 Polycentricity in Addressing the Certain Level of Uncertainty

The RACs approach – via Blockchain governance – offers an alternative governance approach from the traditional ESG approach. One important difference is that, as various scholars have identified, blockchain networks exhibit the attribute of polycentricity. Polycentricity is the concept of “multiple centers of decision-making, or multiple authorities, no one of which has ultimate authority for making all collective decisions,” which has been recognized as the work of Vincent and Elinor Ostrom, in collaboration with researchers at the Ostrom Workshop at Indiana University (Stephan et al. 2019, 31). Blockchains are polycentric as “they are governed by rules that provide the basis for interaction in political, socio-economic systems, while establishing the social positions that different individuals may occupy according to their rights, obligations and empowerments to act in specific situations” (Bodon et al. Reference Bodon, Bustamante, Gomez, Krishnamurthy, Madison, Murtazashvili, Murtazashvili, Mylovanov and Weiss2019, 11). Alston and others further highlights that polycentricity is the defining feature of a permissionless blockchain network, where governments, too, are part of blockchain’s polycentricity (Alston et al. Reference Alston, Law, Murtazashvili and Weiss2021).

The polycentricity aspects effectively address the certain level of uncertainty within the ESG industry. ESG and the data underlying much of its quantification has typically struggled with the fact that significant uncertainty is unavoidable. For example, arguably the most successful initiatives at mobilizing climate action have levered the EPA ENERGY STAR program. In the retail space it is broadly known for appliance efficient ratings, and in the commercial building space it is the leading tool for energy, water, and GHG benchmarking among property investment funds. In states such as New York and California and some local jurisdictions any real estate transaction is required to provide energy data in the ENERGY STAR format, and many real estate brokers now voluntarily look to it as a means of third-party validation for communicating the energy usage and efficiency of a property. Its tools for commercial buildings are used by more than 300,000 properties across the US (US Environmental Protection Agency 2023b), nearly 95 percent of all households in the US benefit from an ENERGY STAR program delivered more than 840 utilities, and over 90 percent of Americans recognize ENERGY STAR (US Environmental Protection Agency 2023a). By nearly all accounts, ENERGY STAR is a widely recognized measure that has changed community behavior by offering an understanding of how to choose higher performing equipment and buildings. Yet even practitioners struggle to agree on how to evaluate the accuracy of the ENERGY STAR model. For example, the EPA notes on a frequently asked questions page in response to questions about ENERGY STAR model uncertainty that “there is no standard approach for combining those [model] uncertainties” into a single estimate across the model (US Environmental Protection Agency 2020), and academic research presents opportunities for improving various parameters by between 4.9 percent to 24.9 percent per parameter (Arjunan et al. Reference Arjunan, Poolla and Miller2020).

ENERGY STAR is a great example of a highly complex solution communicated effectively enough that its level of uncertainty is accepted within its relevant community, regardless of whether the community fully understands the underlying complexity or subtleties of the results it produces. Similarly, the RAC framework’s lack of restrictions on intangible value definition and lack of standardization in evidentiary structure and visibility allows RAC originators to dynamically balance the competing forces that drive perceived value and acceptable price in markets where innovation is outpacing community knowledge. For example, originators of nonstandard commodities such as biochar are currently needing to balance how much evidence is visible in redacted form against what data if released would do commercial harm. In the case of the Biochar Now LLC RAC presented in Figure 3.3, the originator elected to provide sales invoices with pricing blacked out as evidence that a particular weight of a specific product was delivered for its stated use. As the Biochar Now LLC product has specific qualities that differentiate it from competitors, yet those qualities are not sufficiently defined by the broader industry to allow for specific definitions, the RAC was constructed in a manner that Biochar Now LLC felt an informed community member would have enough information to validate the type of biochar referenced in the invoices without providing any commercially sensitive specifics about the product. At the same time, for most individuals who considered purchasing all or a portion of that RAC, there was little concern that the product identified in the redacted invoices was not being deployed as intended when it was purchased. Owing to instances such as the Verra fraud highlighted earlier, the community has the ability to lose confidence that the full chain of actions from intent to implementation are completed. In this case of the Biochar Now LLC RAC, Biochar Now LLC believed the community would find the uncertainty that exists between the evidence that a product was purchased and the stated intent of how that product would be used once purchased would be accepted.

In environments more prevalent to pervasive theft of fraud, such as the fats, oils, and greases industry, this connection between an intended action and its completion can often be bolstered with photographic or video evidence that could also be referenced in or built into the RAC. For example, the GreaseTrack compliance software provided by RAC produces a quality label that is integrated into any renewable crude RAC as the redacted evidence (GreaseTrack 2024). This method of providing the community unique references that can be tied to any specific collection, with the images or other tracking data associated with that location collated in a manner that allows for their permanence to be validated using the Trokt neopublic blockchain network, and provides access to trust without full transparency (Figure 3.6).

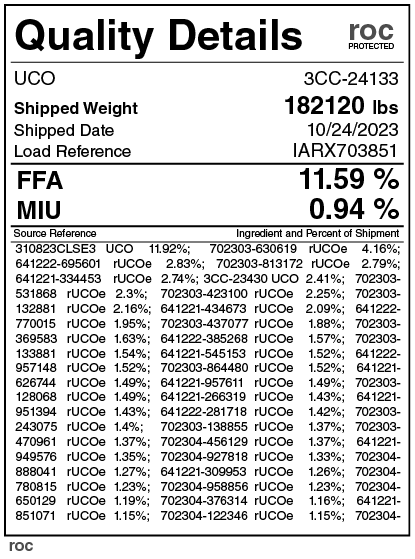

Example of a GreaseTrack quality label that displays the probability of any specific collection event being contained in the total quantity shipped.

Figure 3.6 Long description

Document is titled Quality Details and lists information about a shipment. At the top, it shows a shipment code 3CC-24133, a shipped weight of 182,120 pounds, a shipped date of 10/24/2023, and a load reference number IARX703851. Below this section, two quality values are displayed: free fatty acids at 11.59 percent and moisture, impurities, and unsaponifiables at 0.94 percent. The lower portion of the page contains a table with two columns. One column lists source reference codes, and the other lists ingredient types with their percentage share of the shipment. The ingredients include UCO and rUCOe, with percentages ranging from about 11.92 percent to 1.15 percent. The table contains many individual entries, each representing a portion of the total shipment. The image serves as an example of a GreaseTrack quality label showing the probability of specific collection events being represented in the total quantity shipped.

Like the evidence provided in the Biochar Now LLC example, the valuation of a renewable crude RAC that provides a quality label as its public evidence is influenced by the perceived uncertainty that any token in the quality label may not be corroborated by the underlying evidence upon further investigation. Attempts to minimize this influence of uncertainty on value, which often manifests in a community as a lack of trust, can be seen in the design and implementation of the technology defining a RAC relative to its interpretation of Truth and relationships to Trust.

Transparency plays a crucial role in fostering trust within a polycentric system, as it enables various actors to share information openly, collaborate effectively, and hold each other accountable, thereby strengthening the overall governance structure. Trust serves as a central role in coping with dilemmas (Ostrom Reference Ostrom2010, 661). As explained by Elinor Ostrom, “it is … the structure of the situation [that] generates sufficient information about the likely behavior of others to be trust- worthy reciprocators who will bear their share of the costs of overcoming a dilemma” (Ostrom Reference Ostrom2010, 661). Such disclosure creates a foundation of mutual confidence, where participants are more likely to cooperate and contribute to the collective effort.

3.4 Conclusion

Exploring ESG value realization and the challenges of maintaining truth and trust within the ESG KC makes clear that the current frameworks, particularly those focused on carbon-based metrics, are insufficient for capturing the full scope and impact of ESG initiatives. These problems are best addressed by shifting towards more nimble, simplified presentations of the nuance required for meaningful ESG valuation such as the Hu offering valuation standardization for bespoke intangible value transfer contracts like RACs. These tools offer a way to authenticate and monetize the intangible value created by ESG activities, linking them to tangible, verifiable actions rather than abstract or speculative outcomes. By doing so, they provide a clearer, more reliable connection between ESG claims and their real-world impact, thereby enhancing transparency and trust within the community.

This chapter argues that industry must undertake a rethinking of ESG governance as a KC, where the management of environmental resources is intrinsically linked to the governance of the knowledge and truth that underpin ESG efforts. The concept of polycentric governance is particularly relevant here, as it recognizes the need for multiple stakeholders, each with varying levels of authority, to collaborate and share information openly. In this context, a balanced approach to auditable transparency is not just a desirable attribute but a crucial element for maintaining trust and ensuring that the shared resource of truth is preserved and respected.

The current approach to ESG valuation and governance must evolve to better reflect the diverse impacts of ESG initiatives. By moving away from an overemphasis on carbon metrics and towards frameworks that prioritize truth, transparency, and tangible outcomes, the ESG sector can more effectively align with community values and expectations. The adoption of information sharing tools such as RACs and analysis frameworks such as the Hu, combined with a commitment to transparent and accountable governance, offers a pathway to restoring and enhancing trust in ESG efforts. This, in turn, will ensure that the value created by these initiatives is recognized, respected, and appropriately compensated, paving the way for a more equitable and effective approach to addressing the critical ESG challenges of our time.

Open access

Open access