Home ownership is the West’s biggest economic-policy mistake.

In January 2006, two months after taking office, German Chancellor Angela Merkel eliminated the country’s largest government program for subsidizing homeownership. It was one of her first major policy initiatives as chancellor and marked a significant shift from a key conservative policy she had passionately defended just a few years earlier. In a 2002 parliamentary debate, Merkel had rebuked her leftwing opponents for proposing just such a reform, saying: “You do not at all comprehend what you are doing to the people! Do you know what this means for a family who wants to build a house?”Footnote 1

Merkel’s center-right party, the Christian Democratic Union (Christlich Demokratische Union, CDU), had been the country’s strongest advocate of the homeownership program (the Eigenheimzulage or homeownership allowance) since the founding of the Federal Republic of Germany in 1949. It was a stunning U-turn, made in the context of a reeling German economy. A decade after reunification, Germany faced skyrocketing unemployment, exploding fiscal deficits, a collapsing housing market, and back-to-back recessions. These economic problems led to a deep crisis of confidence in the German model of capitalism, which had previously been envied by its European neighbors. As part of larger efforts to save that model, the Merkel government sacrificed the homeownership subsidy, the country’s largest tax subsidy, which was costing taxpayers EUR 11.5 billion annually.Footnote 2 The policy shift was permanent: German homeownership programs have never returned to their previous levels despite the country’s return to prosperity during the 2010s.

Meanwhile, a house-price bubble of epic proportions was about to burst on the other side of the Atlantic. When it did, the American economy collapsed. The 2008–2009 housing crash was America’s own systems-threatening crisis, as economic growth plummeted, unemployment doubled, and house prices were in freefall.

But the American response could not have been more different. A housing bust of this magnitude could – and arguably should – have led policymakers to question the generous homeownership programs that had helped to inflate the bubble. Instead, American politicians did the opposite: They expanded government support for housing. In response to the crash, Republican President George W. Bush effectively nationalized the country’s mortgage lending system. In September 2008, President Bush placed the battered Wall Street mortgage giants Fannie Mae and Freddie Mac under direct government control, assuming all their commitments and obligations – a staggering USD 5.2 trillion in mortgage debt at the time.Footnote 3 The president felt deeply uneasy about his course of action, as he confessed in a speech: “I’m a strong believer in free enterprise. So my natural instinct is to oppose government intervention. I believe companies that make bad decisions should be allowed to go out of business.”Footnote 4 More than fifteen years after the crash, and several American presidents later, the country’s mortgage market remains de facto nationalized even though the US housing market has long returned to growth. In 2024, the American state directly backed USD 9 trillion or 70 percent of all homeowner debt through public agencies, meaning that millions of indebted American homeowners receive a massive subsidy via lower mortgage rates.Footnote 5

These contrasting German and American policy responses violate widely held assumptions about these two global economic powerhouses. The United States is the world’s quintessential liberal market economy and rhetorical champion of free markets, emphasizing minimal government interference in capitalist activity. In contrast, Germany is the archetypal social market economy with a stronger tradition of government involvement in market affairs. An entire research agenda in political economy, the influential “varieties of capitalism” framework (Hall and Soskice Reference Hall and Soskice2001), is based on the two countries’ differing economic models. In the case of housing, however, both German and American responses deviated from these well-established academic expectations. Germany eliminated what economists consider market-distorting subsidies, while the United States entrenched major subsidies for American homeowners by effectively nationalizing one of the world’s largest debt markets in response to the 2008 crash.

These divergent policy decisions exemplify a much broader historical pattern of government support for housing markets in the United States and Germany. In good economic times and bad from the Great Depression onward, American policymakers have added layer upon layer of support for mortgages through generous tax subsidies and the government’s backing of private mortgage debt. The culmination of this decades-long process of policy expansion was the nationalization of America’s mortgage market. When it comes to subsidizing mortgage debt, the United States occupies one end of the spectrum. Germany occupies the other, as the country’s policymakers have outright retrenched tax subsidies and credit programs for homeownership over time. It was America, not Germany, that socialized housing finance. This book asks why.

The book’s argument, in brief, is that the different natures of American and German capitalism – demand-led in the United States and export-oriented in Germany – created different housing policymaking trajectories over the past century. The American political economy is demand-led and relies heavily on institutions and government programs that promote consumption and credit, and housing is a key sector through which American policymakers can generate such consumption and credit. From the Great Depression onward, successive US governments have concluded that housing programs fuel the overall level of demand in the economy through a virtuous cycle: Subsidizing households’ mortgage debt boosts mortgage lending, housing activity, house prices, and household wealth, which in turn stimulates more consumer lending and spending. Central to this cycle are rising house prices that allow American homeowners to use their homes as credit cards, borrowing money against the value of their homes for consumer spending. Over time, American housing programs have become interwoven with the very functioning of the US economy; withdrawing housing support would be an assault on the economy itself. Housing finance, in short, is America’s unnamed national champion, able to deliver demand-led growth via credit and consumption.

By contrast, the German political economy is export-oriented, relying on institutions and government programs that restrain inflation and wages, which in turn keeps German exports competitive compared to those of nations with higher inflation and wage growth. For German policymakers, housing programs were thus not American-style engines of domestic growth but served the opposite purpose: To restrain growth in house prices and housing costs, consumer credit, and personal consumption, often with the implicit or explicit goal of keeping inflation and wages in check. In the decades after World War II (WWII), which were characterized by massive housing shortages, German housing programs for both rental and owner-occupied housing reinforced the export-oriented economy by producing more affordable housing supply that also prevented wage-cost spirals detrimental to export-led growth.Footnote 6 Once housing shortages were overcome in the 1970s, however, policymakers soon attacked many of these programs for contradicting the priorities of the export-oriented economy by channeling capital away from the country’s avowed national champion: Manufacturing. Over time, politicians duly retrenched homeownership programs in the name of strengthening Germany’s export-oriented economy.

In explaining the radically contrasting approaches to housing in the United States and Germany, this book also relates to some of the defining challenges of our day: Financial instability, racialized wealth inequality, and a chronic shortage of affordable accommodation in cities across Europe and North America. Housing finance programs directly shape the world’s largest asset class – residential housing with an estimated value of USD 288 trillion in 2022Footnote 7 – by encouraging or deterring housing investments. In good times, such programs can help create massive private wealth, as housing is the most important asset that most households will ever own. However, such programs can also fuel overinvestment, resulting in speculative bubbles, financial turmoil, and sudden losses in household wealth, as evidenced by the well-known American housing crash of 2008 and the lesser-known German housing slump of the late 1990s.

Housing is also a significant driver of wealth inequality. In recent decades, the return on capital has risen faster than wages, particularly from housing assets (Piketty Reference Piketty2014; Rognlie Reference Rognlie2015; Fuller et al. Reference Fuller, Johnston and Regan2020). As a result, inequality between the haves and the have-nots is on the rise. In the United States, housing also contributes to racial wealth disparities. In 2024, 74% of white households owned their homes, compared to only 46% of Black, 50% of Latino, and 62% of Asian households.Footnote 8 In the case of Black Americans, this is largely a consequence of policy choice. For decades, the federal government deliberately excluded them from homeownership programs (Thurston Reference Thurston2018). When federal policy finally included racialized minorities from the late 1960s, it often drove them into the hands of predatory lenders (Taylor Reference Taylor2019).

German and American policy approaches to housing have been highly divergent, but they recently converged on one outcome: A lack of affordable accommodation. Between 2012 and 2022, real house prices increased by a staggering 60% in Germany and 70% in the United States.Footnote 9 American real house prices have since continued to climb, standing 80% above their 2012 levels at the time of writing, while German house prices have declined from their 2021 peak (although German prices remained 25% above their 2012 levels in mid-2024). Both the German withdrawal of housing support and the American expansion of that support exacerbated the crisis of affordable housing supply in such cities as Berlin, Munich, New York, and San Francisco, where both buyers and renters are being pushed out of the market. The American failure was one of omission: Housing policy favored single-family homes in suburbs to the detriment of affordable multifamily rental housing in cities. The German failure was one of commission: In its zeal to remove distorting subsidies, the country withdrew them from both homeowners and rental landlords. Paradoxically, these policy actions ultimately harmed the growth regimes that they were meant to serve in their respective countries, as they inflated property prices into bubble territory in the United States and crippled affordable housing programs that could have helped to deflate housing costs in Germany.

Diverging Housing Finance POLICIES in America and Germany

Despite housing’s role in the economy, personal wealth, and inequality, scholars have long treated housing as a technical and apolitical arena. It is, however, a deeply political one. All governments intervene in their housing sectors to varying degrees, making political choices about whether to subsidize the cost of homeownership or rental housing, control or liberalize rents, expand or restrict access to credit, raise or lower taxes on property, and tighten or loosen land-use regulations (cp. Vogel Reference Vogel2018; Quinn Reference Quinn2019; Fligstein and Goldstein Reference Fligstein, Goldstein, Knorr Cetina and Preda2012; Schwartz Reference Schwartz2020; Fligstein Reference Fligstein2021). To provide a focused comparison, this book’s emphasis is on housing finance programs – those that subsidize the cost of financing owner-occupied housing and, to a lesser degree, rental housing. As the preceding discussion shows, the United States and Germany have adopted radically different housing policy approaches, and it is the goal of this book to make sense of these differences.

Housing finance programs are complicated webs of fiscal policies and credit programs. Both types of policy reduce the cost of financing homes, which in turn stimulates housing investment relative to other investments (Schelkle Reference Schelkle2012). In other words, policymakers can deploy the infrastructural power of the state – using state capacity to achieve desired private-market outcomes – to steer private capital into or away from housing (cp. Mann Reference Mann1984; Krippner Reference Krippner2011; Hyman Reference Hyman2011; Braun Reference Braun2020; Wansleben Reference Wansleben2022; Schwartz Reference Schwartz2020). Fiscal policies are tax subsidies or direct spending programs for households, builders, or financial institutions that subsidize the costs associated with building or acquiring homes. Credit programs can take the form of cheap government loans to households or government guarantees on homeowners’ mortgages that protect banks against mortgage defaults, which in turn allows banks to offer mortgages at lower rates.

Cross-National Variation

Comparing housing finance programs in the United States and Germany reveals two puzzling dimensions of variation: One cross-national and the other historical. The United States has developed a government-sponsored housing finance model, generously subsidizing the cost of financing homeownership through a plethora of fiscal and credit programs. In contrast, Germany offers few fiscal and credit subsidies for financing homeownership. This characterization is consistent with recent studies that compare housing finance programs in advanced economies, concurring that the United States stands out in its generosity and Germany in its restrictiveness (International Monetary Fund 2011; Fuller Reference Fuller2015; Wiedemann Reference Wiedemann2021; Johnston et al. Reference Johnston, Fuller and Regan2021).

The degree of American government support for housing finance is remarkable. In 2022 alone, the American government provided USD 72 billion in tax subsidies for homeowners through mortgage interest deduction and capital gains exclusion.Footnote 10 In the primary mortgage market, where banks loan mortgages to consumers, the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) together insured 1.6 million new mortgages worth USD 483 billion in 2022, guaranteeing 22 percent of all new mortgage debt that year.Footnote 11 In the secondary market, where mortgages are pooled together and traded as bonds in financial markets, the American state has an even larger presence. In fact, the American government dominates one of the largest bond markets in the world: US mortgage-backed securities. In 2024, the US government directly backed USD 9 trillion in mortgage-backed securities, or 70 percent of the entire US mortgage market, through quasi-public agencies such as Fannie Mae and Freddie Mac.Footnote 12 Even the country’s independent central bank, the US Federal Reserve (the Fed), which usually does not attempt to pick winners in the economy, has joined the federal government in providing direct housing support. By the end of 2024, the Fed held USD 2.2 trillion in mortgage-backed securities issued by Fannie and Freddie, artificially lowering the cost of mortgages for homeowners.

The German state provides marginal government support for financing homeownership. In fact, there are currently only two permanent programs that do so, and both are limited. The first is the exclusion of capital gains tax on the sale of homes, but only after ten years of ownership (as opposed to just two years in the United States).Footnote 13 The second is a set of small-scale, subsidized homeownership loans, offered by the country’s development bank, Kreditanstalt für Wiederaufbau (KfW), amounting to merely EUR 4.5 billion in credit volume in 2023 – just 2 percent of all new mortgage debt in Germany that year.Footnote 14 These programs pale in comparison to American ones. In Germany, one is hard-pressed to find something akin to the American mortgage interest deduction, although the country briefly experimented with it on two separate occasions in the 1980s and 1990s, as Chapters 5 and 7 detail. The German government similarly does not offer large-scale government guarantees to protect financial markets against losses in the case of mortgage defaults. In Germany, housing finance receives few privileges relative to other sectors.

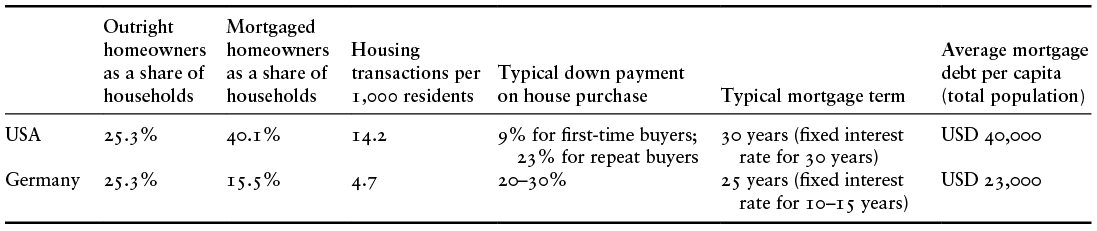

These different housing finance models have profoundly shaped the two countries’ political economies. As the American state absorbs a great deal of risk in financial markets, US banks can offer the country’s beloved thirty-year, fixed-rate mortgage as a standard option – making the US an outlier among wealthy democracies. With fewer government protections, German banks tend to offer shorter mortgage durations (twenty-five years) with a fixed interest rate for only ten to fifteen years. As Table 1.1 shows, the abundance of American mortgage subsidies has contributed to generally higher mortgage indebtedness among American households compared to German ones.

Relatedly, Germany’s restrictive mortgage system, which requires relatively high down payments for home purchases, partly explains the lower number of German housing transactions per capita compared to those in the United States. In addition, low government support for homeownership is an important factor in why Germany’s homeownership rate is lower than that of the United States.

Historical Variation

The historical dimension of variation is no less intriguing. In the early and mid-twentieth century, both the United States and Germany started in a similar place of offering a high degree of government support for housing finance. However, their policy trajectories diverged over time. While the United States incrementally expanded housing finance programs, German policymakers had retrenched theirs to a minimum by the early twenty-first century.

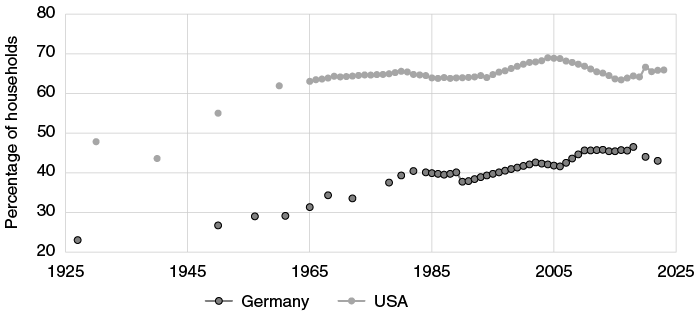

The American government-sponsored housing finance model originated in response to the Great Depression. While the country went into the depression with virtually no national housing finance programs, it emerged with an expansive toolkit of programs that would forever change the American housing market. At the height of the depression between 1929 and 1933, millions of households lost their homes, housing prices and construction plummeted, and mortgage lending came to a halt. In response, American policymakers adopted federal homeownership programs – such as FHA mortgage insurance – to resuscitate the housing market. After the depression, however, policymakers did not withdraw the government from housing finance as originally planned. On the contrary, they kept expanding the state’s role. As the country emerged from the depression during the WWII years – a period marked by significant housing shortages of 3.7 million homes as civilian housing production stalled to secure resources for military production – policymakers broadened homeownership support to returning veterans. By the early 1950s, the US government was directly subsidizing half of all new residential construction and directly backing 44 percent of all mortgage debt through federal credit programs (Grebler et al. Reference Grebler, Blank and Winnick1956, 146; see Figure 2.1).

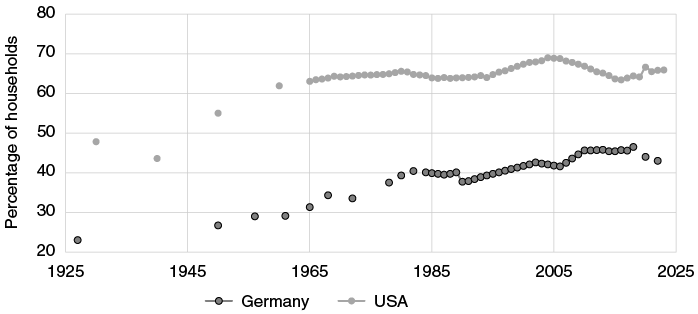

Importantly, as Figure 1.1 shows, America’s generous housing finance programs originated in the depression era when the country was still a nation of renters. Even with a majority-renter population at that time, though, the US government prioritized support for homeowners over renters; it has continued to do so to this day. The reason, as this book will go on to argue in more detail, lies in the macroeconomic heft of homeownership finance programs vis-à-vis rental housing programs, the latter of which have remained a footnote in the American political economy.

Homeownership rates in the United States and Germany, 1925–2023: Percentage of households living in owner-occupied housing

US policymakers’ relentless expansion of the state in housing finance has continued well into the twenty-first century. First, from the late 1960s to the 1990s, American policymakers developed a new government-backed housing bond market, one in which domestic and global investors started trading mortgage-backed securities equipped with a government guarantee. This market, centered around the quasi-public agencies Fannie Mae and Freddie Mac, grew to over USD 2 trillion and was providing close to 50 percent of all mortgage funding in the country by the late 1990s.Footnote 15 Second, American politicians repeatedly strengthened tax breaks for homeowners, such as the mortgage interest deduction. During rare moments of comprehensive tax reform, such as President Ronald Reagan’s 1986 Tax Reform Act, they retained housing tax breaks while eliminating those for other consumer loans. Third, the housing crash of 2008–2009 led policymakers to expand housing programs yet again: They bailed out Fannie Mae and Freddie Mac, effectively nationalizing America’s housing finance system. For its part, the Fed started to directly support American mortgages through large-scale housing-bond-buying programs as a crisis measure in 2008 and has sustained that support ever since. Supporting US mortgages with ever more government programs is a constant in the history of the American political economy.

Germany’s policy path similarly started with generous housing finance programs, but it diverged over time. Like their American counterparts, in the early to mid-twentieth century German policymakers adopted large-scale housing programs to stimulate homebuilding. After WWII, their priority was to overcome the severe shortage of 4.6 million homes. Unlike their American counterparts – who, as noted, also faced considerable post-WWII housing shortages – German policymakers chose to strongly support the construction of both rental and owner-occupied housing. Landmark social housing programs, for example, offered cheap loans to homeowners and rental investors alike. With private capital scarce, the German government directly provided close to 50 percent of all mortgage funding in the early 1950s. Until the late 1960s, the federal government subsidized more than 5.6 million homes (51 percent of the 10.9 million total new homes) through social housing programs alone, including 1.4 million homes for homeowners and 4.2 million rental units.Footnote 16 The German government also offered tax subsidies for both owner-occupied and rental markets to encourage housing investments. In short, the German state dominated the country’s postwar housing finance market – arguably even more so than the American state in this period – offering generous housing finance programs for homeowners and rental investors as part of the country’s broader effort to build more houses after the war.

During the mid-1970s, however, German housing programs reached a turning point. As the housing market recovered from postwar shortages, German policymakers wound down rental housing programs to a minimum by the late 1980s. At the same time, they initially protected homeownership programs, including tax breaks and social housing loans for homeowners. Like President Reagan’s 1986 tax reform, Chancellor Helmut Kohl’s tax reform in the same year strengthened the homeownership allowance, making it a “sacred cow” in the German tax code (Stimpel Reference Stimpel1990, 62). Germany’s reunification led to a temporary revival of housing programs in the early 1990s, aimed at modernizing the housing stock in eastern Germany and remedying shortages in the west. To that end, German policymakers even briefly experimented with a mortgage interest deduction. However, these programs contributed to a crisis, now often forgotten, of housing overproduction in the late 1990s. Instead of responding with ever more subsidies, as the Americans did in response to their own 2008 housing crisis that included large-scale vacancies, German policymakers retrenched homeownership programs. Despite the popularity of the homeownership allowance among voters and the housing lobby, the Merkel government eliminated it. Since then, housing finance programs have remained marginal in Germany.

What explains these contrasting housing policy trajectories in the United States and Germany? Why has the United States continuously expanded housing programs, while Germany has ceased offering such generous programs?

Argument

This book’s argument is that the differing natures of American and German capitalism – demand-led in the United States and export-oriented in Germany – produced contrasting political dynamics that have resulted in diverging housing policy trajectories over the past century. Policymakers and governments are the primary drivers of policy action in this book’s historical account. They have repeatedly wielded state power to pursue different housing market objectives in the name of strengthening their respective political economies. Before delving further into the historical argument, it is important to establish how the American and German political economies differ, and how their housing markets exhibit different macroeconomic complementarities.

Macroeconomic Complementarities: Growth Regimes and Housing

The two countries’ economic models rely on distinct sources of economic growth – demand-led in the United States and export-oriented in Germany – and different economic institutions and macroeconomic policies that support these different patterns of growth. To capture these differences, I use the term “growth regimes” (Hall Reference Hall2020, Reference Hall, Hassel and Palier2021, Reference Hall2024; Hassel and Palier Reference Hassel and Palier2021; Thelen Reference Thelen2019). A growth regime can be defined as the components of an economy that are key for producing growth and prosperity – chiefly exports or domestic demand (Baccaro and Pontusson Reference Baccaro and Pontusson2016; Baccaro et al. Reference Baccaro, Blyth and Pontusson2022; Stockhammer Reference Stockhammer2015) – and the economic institutions and government actions that support these components (Amable Reference Amable2003; Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012; Prasad Reference Prasad2012).Footnote 17 While some advanced economies such as Germany are organized in ways that promote exports, others including the United States have developed an institutional shape that promotes domestic demand as a source of economic growth. Importantly, as Peter Hall (Reference Hall2024, 262) notes, “[w]hat renders a growth regime more than a disparate collection of practices, however, is how the practices of firms and governments interlock to reinforce each other and yield distinctive patterns of growth” (also cp. Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012). In other words, economic activity is structured by economic institutions and government programs that are often – but not always – mutually reinforcing parts of a coherent growth regime. Setting aside, for now, the question of whether governments intentionally design such complementarities, I will detail here the macroeconomic complementarities between the American and German growth regimes and their respective housing sectors.

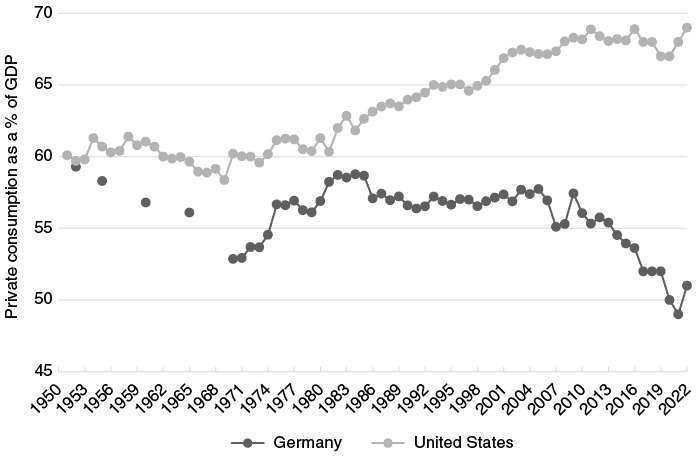

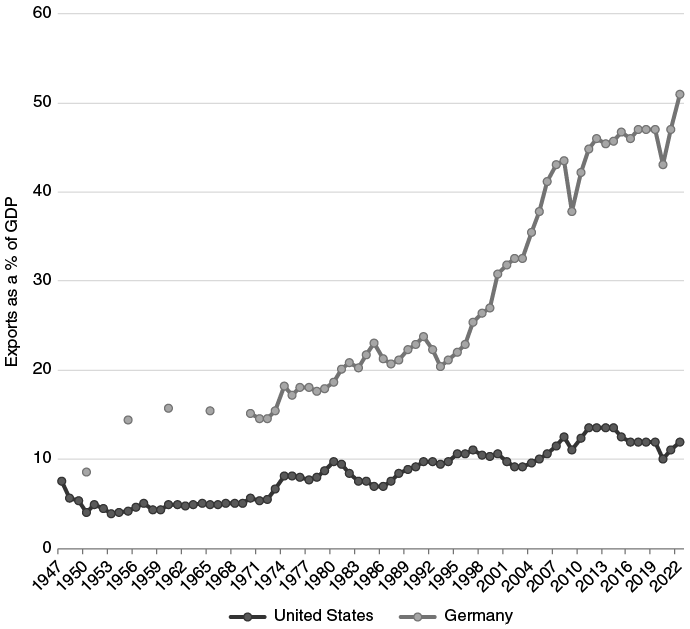

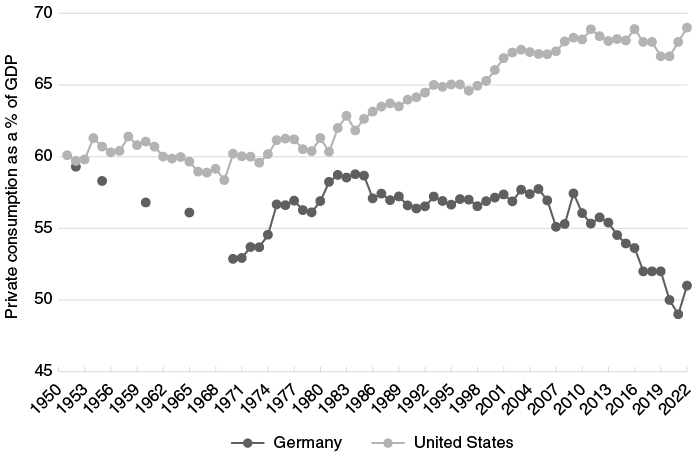

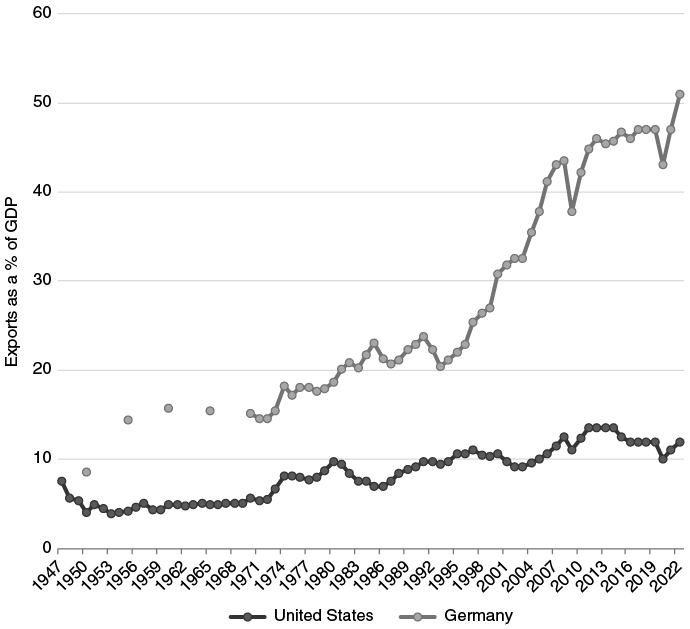

The American economy is a quintessential demand-led growth regime, whereas Germany’s is an archetypal export-led growth regime. Germany’s institutional economic foundations first arose in the late nineteenth century (Abelshauser Reference Abelshauser2005; Manow Reference Manow2020; Herrigel Reference Herrigel1996) and the United States’ in the early twentieth century (Prasad Reference Prasad2012; see Chapters 2 and 3 of this book). From the post-WWII years, as Figures 1.2 and 1.3 show, private consumption as a share of the economy tended to be much higher in the United States than in Germany, while exports as a share of the economy have been significantly larger in Germany than in the United States, and the contrast has become starker over time. By 2022, private consumption was 68% of gross domestic product (GDP) in the United States and 51% in Germany, whereas exports were only 12% of GDP in the US and 51% in Germany.

Private consumption as a percentage of GDP, United States and Germany, 1950–2022

Exports as a percentage of GDP, United States and Germany, 1947–2022

The American demand-led economy relies, above all, on household consumption for economic growth. From the depression era to today, consumption of goods and services in the large domestic market – such as healthcare, education, consumer goods, entertainment, real estate, and financial services – has been the strongest driver of US economic growth. Underlying the American growth regime are institutional features that promote domestic demand. Importantly, the country has developed a large and liquid credit system in which households have relatively easy access to credit for purchasing homes, financing consumer spending, smoothing income losses, or “keeping up with the Joneses” (Wiedemann Reference Wiedemann2021; SoRelle Reference SoRelle2020; Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012). Debt-financed household spending became particularly important from the mid-1970s, when the postdepression period of wage and welfare growth gave way to a post-Keynesian period of stagnating wages and declining welfare (Baccaro et al. Reference Baccaro, Blyth and Pontusson2022; Stockhammer Reference Stockhammer2015). In 2021, the finance, insurance, and real estate sectors made up a much larger share of the American economy (21% of GDP) than manufacturing (11% of GDP).Footnote 18

This is not to reduce the complex US economy to just household consumption and credit. Knowledge-intensive sectors – such as information and communication technology (ICT), education, computing, and software – have driven employment, innovation, cutting-edge technology, investment, and economic growth both domestically and globally (Iversen and Soskice Reference Iversen and Soskice2019; Soskice Reference Soskice2022; Hacker et al. Reference Hacker, Hertel-Fernandez, Pierson and Thelen2021; Mazzucato Reference Mazzucato2015). The United States is also the world’s largest funder of research and development, having spent USD 658 billion in 2019, while Germany spent USD 147.5 billion (both representing approximately 3% of GDP).Footnote 19 While manufacturing has declined as a share of the US economy in recent decades, the country remains a major producer and exporter of cars, airplanes, energy, and pharmaceuticals, making it the world’s second-largest exporter overall.Footnote 20 However, within the massive US economy, it is private consumption, not exports, that remains the most important driver of growth.

Housing is a key sector reinforcing the American growth regime. The housing sector itself is a large component of the US economy, with housing construction, home improvements, and rental payments making up a share of 16% of GDP in 2022.Footnote 21 Moreover, housing is also central to the country’s business cycle. Edward Leamer (Reference Leamer2015) famously noted that “housing really is the business cycle,” indicating that housing downturns often preceded economic recessions in the postwar US economy and thus served as reliable warnings signs (cp. Jordà et al. Reference Jordà, Schularick and Taylor2016b).

Moreover, housing also indirectly stimulates the key elements of the American growth regime: Credit and consumption. The first mechanism is the wealth effect, where growing house and asset prices boost homeowners’ sense of their own wealth, increasing their propensity to consume and discouraging them from saving (Case et al. Reference Case, Quigley and Shiller2013; Calomiris et al. Reference Calomiris, Longhofer and Miles2013).Footnote 22 The second mechanism is the credit effect, suggesting that growing house prices – and the associated growth in homeowners’ equity – allow homeowners to borrow money against their homes. American homeowners can leverage growing home equity by taking out home equity loans or refinancing their existing mortgages with larger ones, using these funds for consumer spending, home improvements, financial emergencies, health care, education, or travel (Aron et al. Reference Aron, Duca, Muellbauer, Murata and Murph2012; Greenspan and Kennedy Reference Greenspan and Kennedy2008; Mian and Sufi Reference Mian and Sufi2011).Footnote 23 The third mechanism is the global capital flow effect. As the world’s financial hegemon, the United States finances its large current account deficits via foreign savings, such as through mortgage-backed securities or Treasury bonds. In 2022, foreign countries – above all, China, Taiwan, and Japan – owned USD 1.2 trillion in US mortgage-backed securities, a share of 13 percent of the entire mortgage-backed securities market.Footnote 24 When foreign capital flows into US bonds, long-term interest and mortgage rates fall, stimulating house prices, credit, and consumption (Ansell et al. Reference Ansell, Broz and Flaherty2018; Schwartz Reference Schwartz2009; Schwartz and Blyth Reference Schwartz, Blyth, Baccaro, Blyth and Pontusson2022). However, as seen during the 2008–2009 crash, declining house prices can also produce a vicious cycle of falling consumer spending (Mian et al. Reference Mian, Rao and Sufi2013).Footnote 25 Housing is thus deeply interlinked with America’s large and globally competitive financial sector (Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012).

By contrast, the German growth regime is export-oriented, with a strong focus on manufactured goods. From the postwar period to today, Germany has been far more reliant on exports for growth and prosperity than the United States (Wallich Reference Wallich1955; Kreile Reference Kreile1977; Eichengreen Reference Eichengreen1994; Lindlar and Holtfrerich Reference Lindlar and Holtfrerich1997; Giersch et al. Reference Giersch, Paqué and Schmieding1992). As Lucio Baccaro and Martin Höpner (Reference Baccaro, Höpner, Baccaro, Blyth and Pontusson2022, 240–241) show, export-led growth has been especially strong in the post-unification period from the 1990s, when exports became by far the most important contributor to growth (cp. Stockhammer Reference Stockhammer2015; Baccaro and Pontusson Reference Baccaro and Pontusson2016).Footnote 26 Germany is a major exporter of high-value-added manufacturing goods such as cars, machine tools, chemicals, pharmaceuticals, and, increasingly, renewable energy components such as wind turbines (Nahm Reference Nahm2021). The manufacturing sector constituted 20% of the economy in 2022, while the finance, insurance, and real estate sector’s share was considerably smaller at 14%.Footnote 27 Germany’s information and communication sector (5% of GDP in 2022) is also smaller than its American counterpart (7.5% of GDP). In short, Germany’s export-oriented manufacturing sector is the backbone of the economy, whereas the service sector remains underdeveloped and less productive compared to that of the United States (Falck and Wölfl Reference Falck and Wölfl2018).

The foundation of the German growth regime lies in a set of economic institutions that have enhanced the nation’s export competitiveness by restraining wages, private consumption, and household credit. From the post-WWII years, this moderation of domestic demand has maintained low inflation, resulting in competitive prices for German exports due to lower production and labor costs. Three institutional features stand out in restraining domestic demand and inflation. First, the country’s coordinated wage bargaining system has successfully limited real wage growth and kept labor costs low relative to its European competitors (Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012). The collective bargaining system gives Germany a competitive edge in the eurozone, as many of its southern neighbors lack similar structures to limit wage growth (see, e.g., Höpner Reference Höpner2019; Matthijs and Blyth Reference Matthijs and Blyth2015). Second, strict fiscal and monetary policies have reinforced Germany’s low inflation regime, a regime in which the country’s conservative central bank, the Bundesbank, historically threatened monetary tightening should unions demand higher wages or governments engage in inflationary fiscal spending (Hall and Franzese Reference Hall and Franzese1998; Manow Reference Manow2020). Even within the eurozone, the Bundesbank continued to promote hawkish monetary policy (Reisenbichler Reference Reisenbichler2020b). Third, the country has developed a restrictive credit and mortgage lending system that limits credit expansion and debt-financed consumption (Mertens Reference Mertens2015; Wiedemann Reference Wiedemann2021). Instead of going into debt, German households have high levels of savings. In 2023, German households saved 10.4% of disposable income, while American households saved just 4.7%.Footnote 28 In short, since the post-WWII years, these institutions have protected export-oriented industries by systematically lowering domestic costs and boosting export competitiveness (Baccaro and Höpner Reference Baccaro, Höpner, Baccaro, Blyth and Pontusson2022; Höpner Reference Höpner2019).

In Germany, the housing system serves the opposite economic purpose to that of the United States: It restrains housing demand and prices, household credit, and consumption. As in the United States, housing is an important component of the German economy. In 2023, it comprised a share of 19 percent of the country’s economy, including housing construction, housing services, the real estate industry, and mortgage lending sectors.Footnote 29 However, the key difference between the two countries is that German property is not a transmission belt to stimulate household spending or borrowing in the wider economy. Unlike the American case, there is no evidence for wealth or credit effects in Germany, meaning that rising house prices do not produce higher consumer spending or lending (Voigtländer Reference Voigtländer2014; Kofner Reference Kofner2014; Geiger et al. Reference Geiger, Muellbauer and Rupprecht2016; Stockhammer et al. Reference Stockhammer, Rabinovich and Reddy2021). If anything, high down payments and rising property prices incentivize aspiring German homeowners to save more (Geiger et al. Reference Geiger, Muellbauer and Rupprecht2016). The absence of wealth and credit effects is the result of the country’s conservative mortgage system, which does not routinely offer home equity loans to fund personal spending. In contrast to American homeowners, Germans do not use their homes as credit cards.

Germany’s conservative mortgage market complements the macroeconomic priorities of the export-oriented growth regime. First, stable house prices and housing costs – achieved through restricted access to credit and rent controls – help keep down wage demands and inflation, which are conducive to export competitiveness (cp. Muellbauer Reference Muellbauer2018; Führer Reference Führer1995; 2015). The country’s wage bargaining institutions not only restrain wages but also depresses demand for mortgage-financed homeownership (Johnston and Regan Reference Johnston and Regan2017). Second, rising house prices and the associated profit-making opportunities in real estate can shift labor and capital into housing and away from Germany’s key manufacturing sector, thereby hurting the sector’s export competitiveness (Égert and Kierzenkowski Reference Égert and Kierzenkowski2014). Sebastian Kohl and Alexander Spielau (Reference Kohl and Spielau2022) identify a trade-off between the strengths of a country’s housing sector vis-à-vis its export sector. The two sectors tend to have contradictory macroeconomic needs: The housing sector might favor stronger mortgage lending or higher wages to stimulate housing, while the export sector benefits from low wages and low domestic demand. For these and other reasons, export-oriented Germany has had a “repressed” housing market, especially in recent decades (Kohl and Spielau Reference Kohl and Spielau2022).

A Historical Institutionalist Explanation: Growth Regimes and Policy Feedback

These macroeconomic complementarities between the two countries’ growth regimes and housing markets were the cumulative result of political actions and policy feedback that unfolded over long periods of time. The historical account in this book suggests that each country’s growth regime initiated distinct policy actions and feedback effects, which expanded American housing programs while undermining German ones over time. In the American case, early housing programs reshaped the demand-led growth regime by making it more dependent on housing-based growth. As housing became ever more central to American capitalism over time, political leaders retained or expanded housing programs in subsequent policymaking rounds. In Germany, early housing programs initially reinforced the country’s export-oriented growth regime by addressing post-WWII housing shortages, reducing housing costs, and keeping wages low. However, rather than increasing the German economy’s reliance on housing-based growth, policymakers started viewing housing programs as creating frictions with the export-oriented growth regime once housing shortages were resolved. The increasingly peripheral role of housing to the German export-oriented economy ultimately enabled policymakers to retrench housing programs.

Governments drove this long-term policy divergence, using state power to shift public and private resources either into housing or away from it. As Torben Iversen and David Soskice (Reference Iversen, Soskice, Bermeo and Pontusson2012, 37) note, “governments … are deeply concerned with promoting the high value-added sectors of their economies, in which they enjoy comparative institutional advantage.” In other words, governments tend to create policy landscapes that they believe benefit the key sectors of their economies (Hall Reference Hall2024). While housing finance is a core sector in the American demand-led economy, it is more peripheral in Germany’s export-oriented economy in which manufacturing industries are the national champions. The different positioning of housing within each country’s growth regime has created distinct housing policy dynamics in the two countries, including a century-long American bipartisan consensus supporting housing programs and a German cross-party consensus favoring the eventual retrenchment of these programs.

The American demand-led growth regime fostered political dynamics that led to a century-long expansion of housing programs. During the Great Depression, US politicians across the spectrum viewed the struggling housing market as holding back domestic demand. In response, they adopted policies to steer capital into housing and boost domestic demand by stimulating housing construction, employment, and wages. Importantly, depression-era housing programs fundamentally transformed American capitalism. First, the new housing-based growth machine relied on government support for its functioning and survival. Indeed, these programs created a new market for consumer-friendly and cheap mortgages that private actors were unable to provide on their own. Second, they made housing finance a national champion deeply intertwined with the emerging American demand-led growth regime to the point where their economic priorities became indistinguishable. Following the depression, successive governments expanded these housing programs as a routine measure to stimulate the economy well into the postwar period, including providing support for veterans.

From the 1960s to the 1990s, US politicians across the spectrum continued expanding housing programs, which made them ever more integral to the financializing American growth regime in this period. When inflation and rising interest rates threatened housing-based growth, policymakers sprang into action to rescue the housing finance architecture they had helped build in earlier decades. Their actions once again transformed the American growth regime by further deepening its dependence on housing-based growth. First, policymakers utilized the power of the state to create what would become a multi-trillion-dollar market for mortgage-backed securities, which relied on government support for its survival. This move also elevated the quasi-public agencies Fannie Mae and Freddie Mac to become America’s most important mortgage players and pro-housing-policy lobbyists. Second, policymakers expanded housing programs to stimulate economic activity in marginalized communities. However, this growth strategy was fraught with challenges, as racialized minorities remained disproportionately targeted for predatory lending. Third, these housing programs turned American homes into credit cards. As homeowners experienced massive gains in home values, they began borrowing against their homes for consumer spending, all while policymakers subsidized this practice through the mortgage interest deduction. The growing role of housing in America’s financializing economy thus gave policymakers additional reasons to expand housing programs.

By the time of the 2008–2009 housing crash, American housing programs were already deeply embedded in the demand-led growth regime. Even though housing programs had contributed to the housing bubble, policymakers felt compelled to double down on these programs. Politicians expanded the programs with bipartisan support, as they saw housing as both the root of economic disaster and the key to recovery. They bailed out Fannie Mae and Freddie Mac – institutions created and championed by earlier generations of policymakers and housing programs – which effectively quasi-nationalized America’s multi-trillion-dollar mortgage market. Additionally, the Fed offered unusual support for housing. Remarkably, these housing policy expansions, intended as temporary measures, became entrenched. The “new normal” of a quasi-nationalized mortgage market and direct central bank support is the culmination of a century-long process of housing policy expansion to promote housing-based growth. Despite growing discomfort among policymakers about the American state’s excessive role in the housing sector, its importance to the demand-led growth regime led policymakers to retain expanded housing programs. Even long after the country’s economic recovery, policymakers feared that reducing the state’s role could disrupt the housing sector and the American growth regime; such fears trapped them in the expanded housing policy landscape.

This is not to discount other factors reinforcing America’s spectacular housing policy expansion. As these programs helped increase the number of homeowners over time, policymakers had strong incentives to protect the interests of a growing homeowning voting constituency. In addition, well-organized housing groups lobbied aggressively for retaining or expanding housing programs. Crucially, the central positioning of homeowners and these interest groups within the American demand-led growth regime made politicians responsive to their demands. In other words, these groups’ material interests were perfectly congruent with the larger macroeconomic objectives of the American demand-led economy. In short, these political factors reinforced macroeconomic ones, creating a multiplicity of forces that drove policymakers to expand housing programs over time.

In contrast, the German export-oriented growth regime fostered political dynamics that undermined housing programs over time (cp. Jacobs and Weaver Reference Jacobs and Weaver2015). Early post-WWII housing programs were initially highly complementary to the export-oriented economy. With broad support from across the political spectrum, German policymakers established generous housing programs for both owner-occupied (favored by right-leaning parties) and rental housing (favored by the left) to address postwar housing shortages. Importantly, these policies simultaneously strengthened the fundamentals of the country’s export-oriented economy. First, early housing programs alleviated labor shortages in industrial areas and improved labor mobility. Second, they were anti-inflationary policies that limited housing costs and thus curbed inflationary wage demands that would have been detrimental to export-driven growth. Third, policymakers retained a restrictive housing finance system that encouraged household savings over easy access to credit. In essence, early German housing programs were more than just housing initiatives – they functioned as a form of wage and industrial policy, supporting the needs of the export-oriented economy.

From the mid-1970s, however, policymakers’ perception of postwar-era housing programs changed: They came to view them as contradicting the German export-oriented growth regime. When housing shortages abated and the country experienced rising unemployment, public debt, and inflation, policymakers increasingly viewed these programs as structural economic problems rather than solutions. They started criticizing them for creating fiscal deficits, steering capital away from manufacturing, and creating excess demand and house-price inflation in times of sufficient housing supply. The influential Bundesbank and Council of Economic Experts (Sachverständigenrat für Wirtschaft) provided the economic rationale for these criticisms. As a result, German politicians on the left and right started scaling down housing programs, especially those for rental housing. For the time being, however, they retained homeownership support to promote conservative family life, create household wealth, and privatize old-age provision, yet decidedly not as a long-term economic growth strategy.

In the 2000s, German policymakers developed a broad-based consensus in favor of retrenching the remaining large-scale homeownership and rental housing programs, perceiving them as clashing with the export-oriented growth regime. Unlike in the United States, early German housing programs had not transformed the country’s model of capitalism into one reliant on housing-based growth. Quite the opposite. When German policymakers experimented with American-style housing policies, such as a mortgage interest deduction, to stimulate the eastern economy in the post-unification years, it resulted in a prolonged housing slump that exacerbated the country’s economic problems of the late 1990s and early 2000s. To strengthen the core of the German economy – export-oriented manufacturing – Christian Democrats and Social Democrats decided to retrench these programs and utilized the power of the state to redirect capital from housing to the industrial sector. The peripheral, and to some extent even contradictory, role of housing programs within the export-oriented economy facilitated their retrenchment.

The existing literature on policy feedback provides several reasons for why German policy retrenchment should not have occurred. German homeownership programs, for example, enjoyed support from a powerful housing lobby, (aspiring) homeowners, and the mass public, as well as ideological backing from the Christian Democrats (Pierson Reference Pierson1993; van Kersbergen Reference van Kersbergen1995; Campbell Reference Campbell2012; Mettler and SoRelle Reference Mettler, SoRelle, Sabatier and Weible2018; Béland et al. Reference Béland, Campbell and Weaver2022). However, the macroeconomic imperatives of the country’s export-oriented growth regime ultimately prevailed over these factors.

Contributions and Implications

This book adds to an established literature that places housing squarely in the center of the comparative and American political economy scholarship on capitalism, welfare states, and financial markets (Aalbers Reference Aalbers2016; Ansell Reference Ansell2019; Einstein et al. Reference Einstein, Glick and Palmer2020; Fligstein Reference Fligstein2021; Fuller Reference Fuller2019; Hankinson Reference Hankinson2018; Hyman Reference Hyman2011; Immergluck Reference Immergluck2009; Johnston and Kurzer Reference Johnston and Kurzer2021; Kohl Reference Kohl2017; Krippner Reference Krippner2011; Logemann Reference Logemann2012; Marble and Nall Reference Marble and Nall2021; McCabe Reference McCabe2016; Mertens Reference Mertens2015; Prasad Reference Prasad2012; Quinn Reference Quinn2019; Schwartz and Seabrooke Reference Schwartz and Seabrooke2009; Schwartz Reference Schwartz2009; Taylor Reference Taylor2019; Thompson Reference Thompson2010; Thurston Reference Thurston2018; Wiedemann Reference Wiedemann2021). This is a curiously recent development. While news outlets have repeatedly emphasized the importance of housing, social scientists have paid much less attention to it. This book highlights the massive macroeconomic and distributive consequences of housing programs: They shape the world’s largest asset and financial markets, influence the distribution of wealth in society, and spur economic activity well beyond the housing sector itself.

This book first advances upon an important literature on diverse capitalist models by investigating the politics of economic policy behind these models with rich historical detail. The paradigmatic “varieties of capitalism” (Hall and Soskice Reference Hall and Soskice2001; Amable Reference Amable2003) and “growth model” literatures (Baccaro et al. Reference Baccaro, Höpner, Baccaro, Blyth and Pontusson2022; Hassel and Palier Reference Hassel and Palier2021) offer systematic understandings of how the German “coordinated” or “export-led” and the American “liberal” or “demand-led” economies operate and differ. While numerous studies have investigated the ever-changing institutional arrangements of these models (e.g., Thelen Reference Thelen2014; Streeck Reference Streeck2009), fewer have focused on the role of the state – that is, the politics and history of economic policy behind these models (exceptions are Manow Reference Manow2020 and Prasad Reference Prasad2012).Footnote 30 This book delves into the co-evolution of the two countries’ growth regimes and key economic policies over the past century through the lens of housing. It shows that American and German policymakers embarked on different housing policy paths, because they viewed stimulative housing programs respectively as constitutive to American demand-generated prosperity and, by contrast, as inimical to German export-generated prosperity. These divergent state actions have subsequently transformed the very natures of American and German capitalism.

Relatedly, the literature on capitalist diversity has rarely investigated in-depth sectoral government policy within and across countries over long periods of time. While existing studies have privileged the role of sectoral producer groups – and coalitions between them – in bringing about institutional changes in collective bargaining, vocational training, and the labor market (e.g., Thelen Reference Thelen2014), this book emphasizes the role of the state through sectoral government policy (Ornston and Vail Reference Ornston and Vail2016; Nahm Reference Nahm2021). The book demonstrates that different economic models rely on different sectors for producing prosperity and that policymakers tend to privilege core sectors over peripheral ones in aiming to generate prosperity (cp. Bohle and Regan Reference Bohle and Regan2021; Iversen and Soskice Reference Iversen, Soskice, Bermeo and Pontusson2012; Haffert and Mertens Reference Haffert and Mertens2021; Hall Reference Hall2024; Hassel and Palier Reference Hassel and Palier2021; Prasad Reference Prasad2012; Thelen Reference Thelen2019). This book’s sectoral logic is as follows: The contrasting American and German growth regimes, in which housing plays different macroeconomic roles, led to contrasting political dynamics and sharply divergent policy trajectories in the two countries. In the United States, housing is a key sector for producing growth, prosperity, and employment, whereas it is much less significant in Germany. Consequently, housing finance became a policy-privileged national champion in America, but not in Germany, where export industries remain the national champions.

Second, the book contributes to scholarship on policy feedback in historical institutionalism by treating growth regimes as a novel source of policy feedback. Existing studies have fruitfully examined how new policies create constituencies, mass publics, interest groups, and state capacities that in turn strengthen or undermine these same policies over time (Béland et al. Reference Béland, Campbell and Weaver2022; Pierson Reference Pierson1993; Campbell Reference Campbell2012; Thurston Reference Thurston2015; Busemeyer et al. Reference Busemeyer, Abrassart and Nezi2021; Mettler and SoRelle Reference Mettler, SoRelle, Sabatier and Weible2018; SoRelle Reference SoRelle2020). Yet such studies rarely directly compare the feedback effects of similar policies across countries. This book shows that American and German homeownership programs exhibited contrasting feedback effects, attributable to policymakers’ different macroeconomic priorities, leading to the expansion of American programs and the retrenchment of German ones over time. Without discounting the influence of interest groups or homeowning constituencies, this book argues that American policymakers expanded homeownership programs mainly because they viewed such support as congruent with, if not constitutive of, the demand-led growth regime. In contrast, against the opposition of lobby groups and homeowning constituencies, German policymakers eliminated homeowner programs, as they ultimately viewed such subsidies as contradicting the export-oriented economy.

Relatedly, the book shows the importance of considering the positioning of interest groups within a growth regime. My findings suggest that similar kinds of interest groups can have varying degrees of political influence across countries, based on their positioning at the core or periphery of a growth regime. Both the United States and Germany are home to powerful housing lobbies, such as realtors, homebuilders, and mortgage bankers in the United States (e.g., Howard Reference Howard1997) and Germany’s building societies and construction firms and unions (e.g., Egner et al. Reference Egner, Georgakis, Heinelt and Bartholomäi2004). The centrality of the housing sector within the American growth regime places the housing lobby in a comparatively powerful position, enabling it to advocate demands that are congruent with the objectives of the growth regime. Nonetheless, as the empirical discussion in this book demonstrates, the American housing lobby did not dictate housing policy; policymakers often pursued their own strategies of supporting the country’s housing market autonomously. While American policymakers and the housing lobby generally pursued the same goal of supporting the country’s housing market, they often differed on how to achieve it. In Germany, where housing plays a less central role to the growth regime, the housing lobby held a comparatively weaker structural position from which to defend housing programs over time, as their demands and interests were less congruent with the objectives of the export-oriented economy (cp. Kohl and Spielau Reference Kohl and Spielau2022).

Third, the book demonstrates important yet previously neglected differences in how policymakers deploy the infrastructural power of the state for economic objectives (cp. Mann Reference Mann1984; King and Lieberman Reference King and Lieberman2009; Krippner Reference Krippner2011; Morgan and Orloff Reference Morgan and Orloff2017; Vogel Reference Vogel2018; Quinn Reference Quinn2019; Schwartz Reference Schwartz2020; Braun Reference Braun2020; Wansleben Reference Wansleben2022). American policymakers have repeatedly used state power to absorb risk in financial markets to channel private capital, which otherwise might have gone elsewhere, into housing. In doing so, the American state crafted a financialized home lending system that became addicted to government support. In Germany, policymakers ultimately used state power to steer capital away from housing – preventing a financialization of the sector – and into manufacturing. As this book suggests, the difference can be explained by policymakers’ different macroeconomic priorities: Boosting domestic demand in the United States versus export-oriented manufacturing in Germany.

Fourth, my findings challenge political economy scholarship on party politics by showing that party positions regarding housing are not fixed and are more nuanced than merely reflecting the material interests of a party’s core constituencies (Beramendi et al. Reference Beramendi, Häusermann, Kitschelt and Kriesi2015; Ansell Reference Ansell2014). The common wisdom is that center-right parties favor homeownership programs, as they represent affluent asset owners, while left-of-center parties support rental housing programs, given their propertyless constituencies. Scholarship has also described homeownership as an ideological mainstay of center-right Christian Democratic parties in Europe, as homeownership is seen as promoting conservative values such as traditional family life in single-family homes and private ownership over public welfare (Esping-Andersen Reference Esping-Andersen1990; van Kersbergen Reference van Kersbergen1995). Yet macroeconomic imperatives can override constituency concerns and party ideology, resulting in high levels of bipartisanship. In Germany, the center-right Christian Democrats and the center-left Social Democrats agreed to eliminate homeownership programs. In the United States, Democrats and Republicans share a consensus in favor of supporting homeownership despite intense polarization in many other policy areas (Schelkle Reference Schelkle2012; McCarty et al. Reference McCarty, Poole and Rosenthal2013). Contrasting macroeconomic imperatives explain both the degree of bipartisan consensus and the divergent policy outcomes in both countries.

Fifth, the book contends that housing is an important yet overlooked element of Germany’s capitalist model (Logemann Reference Logemann2012; Mertens Reference Mertens2015; Kohl Reference Kohl2017). Recent scholarship on the United States has successfully integrated housing as an area of investigation in the American political economy (Prasad Reference Prasad2012; Thurston Reference Thurston2018; Quinn Reference Quinn2019). In contrast, influential scholarship on the German political economy has rarely investigated housing, focusing instead on other areas of the economy: Collective bargaining, welfare and labor programs, vocational training, corporate governance, and monetary and fiscal policy (Manow Reference Manow2020; Hall and Franzese Reference Hall and Franzese1998; Streeck Reference Streeck2009; Thelen Reference Thelen2014). Yet housing is an important part of the German model, as government actions have helped to establish low-cost housing that contributed to wage compression, low inflation, productivity, and restrained credit and consumption. It is partly for this reason that Germany remains, to the mystification of Anglo-American observers, a nation of renters.

Organization of this Book

The book traces the co-evolution of each country’s housing programs and growth regime across three distinct historical periods (cp. Hall Reference Hall2020, Reference Hall, Hassel and Palier2021, Reference Hall2022). It begins with the Great Depression in the United States and WWII in Germany, extending into the postwar “Golden Age” of capitalism through the late 1960s. It then examines the turbulent post-Keynesian period from the early 1970s to the 1990s. The book concludes with the Great Recession of 2008–2009 and its aftermath up to today. Each historical era, along with its developments in the international political economy, produced distinct economic challenges for the American and German growth regimes that profoundly influenced the housing policymaking context (Blyth and Matthijs Reference Blyth and Matthijs2017).

The first part of the book compares the origins and early evolutions of the two countries’ growth regimes and housing programs. Chapter 2 tells the story of how American policymakers established housing programs as an engine of economic growth during the Great Depression. They discovered that subsidizing mortgage debt via government guarantees was an effective countercyclical tool to help overcome the depression and even permanently stimulate the economy. While the country went into the depression with virtually no national housing programs, it emerged from it with an expansive toolkit of demand-side housing programs deeply interlinked with the American demand-led growth regime.

Chapter 3 discusses the origins of housing programs in post-WWII Germany and how these programs reinforced the country’s postwar export-oriented economy. To overcome severe housing shortages after the war, the German government implemented a range of generous housing programs for rental housing and homeownership. Critically, these programs strengthened the export-oriented growth regime and contributed to the country’s postwar economic miracle. They established low-cost housing for workers and the middle class, which helped improve both competitiveness by limiting wage inflation and productivity by improving labor mobility.

The second part of the book analyzes the diverging housing policy trajectories in the United States and Germany during the post-Keynesian period. Chapter 4 details how American policymakers expanded housing programs into new areas of the home lending market between the late 1960s and the early 1990s. Amid rising inflation and interest rates, they feared that impaired mortgage lending could threaten housing-based growth. In response, they established a new market for housing bonds underwritten by the American state to ensure the availability of cheap mortgages. As mortgage credit became ever more plentiful, policymakers discovered the growth potential of leveraging homes for consumer spending in times of stagnating wages.

Chapter 5 shows that German housing programs reached a turning point in the mid-1970s. While these programs had reinforced the country’s postwar export-oriented growth regime during severe housing shortages, policymakers later came to view them as increasingly conflicting with the economy’s needs once shortages abated. German economic elites and policymakers criticized these programs for increasing public debt, diverting capital from export-oriented manufacturing, and creating inflation. Consequently, policymakers started withdrawing rental programs. However, they retained homeownership programs, prioritizing ideological factors – such as creating household wealth or old-age security through homeownership – over the potentially damaging effects of these programs on the German growth regime.

The final part of the book contrasts the retrenchment of German housing programs with the striking expansion of American housing programs during and after the Great Recession of 2008–2009. Chapter 6 demonstrates that American policymakers doubled down on housing programs in response to the housing crash. By bailing out Fannie Mae and Freddie Mac, they nationalized the country’s housing finance market. Their goal was to rescue and revive the country’s reeling economy. Even the Fed established a new layer of government support for housing in the postcrisis period. Remarkably, these crisis measures, initially designed to be temporary, became entrenched features of the American demand-led growth regime.

Chapter 7 explains the retrenchment of German housing programs in the mid-2000s. After reunification, the country experienced a housing boom and bust that left it with one million vacant homes. In response, German policymakers eliminated the remaining large-scale housing programs for homeownership and rental housing. At a time when Germany was considered the sick man of Europe, they viewed these programs as structural economic problems that contradicted the macroeconomic needs of the reeling German export-oriented economy.

The book’s conclusion, Chapter 8, highlights paradoxes of American and German housing policymaking amid surging house prices during the 2010s and early 2020s. While the US housing market is one of the country’s greatest economic strengths, it could also be the source of its undoing, as housing programs can fuel financial bubbles and create turmoil. In contrast, German policymakers retrenched the housing programs that once supported the country’s growth regime by deflating housing costs. This retrenchment left them grappling with mounting housing affordability problems that threatened inflation and wage demands detrimental to export competitiveness. The conclusion also extends this book’s lessons to other advanced economies such as Austria, Canada, the Netherlands, Sweden, and the United Kingdom.