1 INTRODUCTION

Bilateral bargaining is one of the most important forms of trade. Despite there has been a large literature of bargaining in theory and in laboratory experiments over the past 60 years, we have seen a burst of empirical investigations of bargaining only in the past decade. This surge is mainly due to the increasing availability of bargaining data to the academic community. For instance, online bargaining interaction data from eBay’s best offer platform have been studied by Backus et al. (Reference Backus, Blake, Larsen and Tadelis2020) to document some facts consistent with bargaining theory by using some reduced form approach. Similarly, Larsen (Reference Larsen2021) utilizes wholesale used-auto auctions data to examine ascending auctions followed by bargaining under minimal assumptions of rational behavior. Finally, data on union-management negotiations collected by Treble (Reference Treble1990) provide reduced form evidence regarding conciliation board negotiations in the historical British coal industry. In this article, we study the identification and estimation of the structural double auction model which explicitly characterizes the bargaining process between buyer and seller. It is therefore a good alternative to the Nash bargaining framework.

A bargaining framework with two-sided incomplete information allows for inefficient outcome which occurs in real-world trade but is excluded by a framework with complete information. As an influential candidate of the former, the double auction with bargaining (or k-double auction) considers linear strategies for both the buyer and the seller. The linearity of the strategies has been confirmed by experimental studies (see, e.g., Radner and Schotter, Reference Radner and Schotter1989). This article nonparametrically identifies and estimates the double auction model with bargaining. Our framework can be used to recover the updated value distributions of the buyer and the seller based on the last round of bids, since previous rounds of bids are usually used to reveal limited information about the value of the reservation. For instance, our method can be employed to estimate the buyer’s and the seller’s (most updated) value distributions by using the last round of offers from the bargaining data of eBay’s best offer platform (or wholesale used-auto auctions, or union-management negotiations).

This article contributes to the literature of noncooperative bargaining games with incomplete information. On the theoretical side, such games have been extensively studied since Chatterjee and Samuelson (Reference Chatterjee and Samuelson1983). In addition, there is also a large experimental literature that examines the theoretical properties of bargaining with incomplete information (see, e.g., Radner and Schotter, Reference Radner and Schotter1989, among others). Empirically, there is a fast growing literature to investigate the role of asymmetric information in bargaining.Footnote 1 See Larsen (Reference Larsen2021) for wholesale used-auto market and Keniston (Reference Keniston2011) for local autorickshaw transportation. Our article belongs to the second research line (of the structural approach) and provides an empirical methodology to use the data on offers and asks at the last round of the bargaining process to estimate the updated valuation distributions of both participating parties. Our method can be applied to field data to quantify ex ante and ex post inefficiency introduced by private information (see Satterthwaite and Williams, Reference Satterthwaite and Williams1989).

Our article is also related to the literature that examines nonparametric identification and estimation of one-sided auctions. This work was pioneered by Guerre, Perrigne, and Vuong (Reference Guerre, Perrigne and Vuong2000) for the identification and estimation of first-price auctions, and has been followed by many other papers. For comprehensive surveys, see Athey and Haile (Reference Athey, Haile, Heckman and Leamer2007), Hendricks and Porter (Reference Hendricks and Porter2007), Hickman, Hubbard, and Sağlam (Reference Hickman, Hubbard and Sağlam2012), Gentry et al. (Reference Gentry, Hubbard, Nekipelov and Paarsch2018), Perrigne and Vuong (Reference Perrigne and Vuong2019), and Hortaçsu and Perrigne (Reference Hortaçsu and Perrigne2021). In the identification part, we generalize the Guerre et al.’s (Reference Guerre, Perrigne and Vuong2000) nonparametric identification strategy to the double auction setup. The model primitives are shown to be partially identified when only transacted bids are available, but to be point-identifiable when the failed bids are also available. Our identification results are hence similar to Gentry and Li (Reference Gentry and Li2014), who obtained constructive bounds on model fundamentals which collapse to point identification when available entry variation is continuous in auctions with selective entry.Footnote 2 There are other papers obtaining partial identification in the context of one-sided auctions (see, e.g., Haile and Tamer, Reference Haile and Tamer2003; McAdams, Reference McAdams2008; Tang, Reference Tang2011; Aradillas-López, Gandhi, and Quint, Reference Aradillas-López, Gandhi and Quint2013; Komarova, Reference Komarova2013; Chen et al., Reference Chen, Gentry, Li and Lu2020). However, compared to this research line, we consider identification in a different auction setting (namely, double auctions with bargaining) that introduces not only asymmetric information but also asymmetric bidding strategies.Footnote 3 In the estimation part, our article is closely related to Hickman and Hubbard (Reference Hickman and Hubbard2014) who adapted the bias correction method of Zhang, Karunamuni, and Jones (Reference Zhang, Karunamuni and Jones1999) and Karunamuni and Zhang (Reference Karunamuni and Zhang2008) to correct the boundary bias of the two-step value density estimator, which was first proposed by Guerre et al. (Reference Guerre, Perrigne and Vuong2000), of (one-sided) first-price auctions. Their bias correction approach (and most other related approaches) needs to introduce additional tuning parameters for data modification and to know the true boundary location for defining the estimators and asymptotic analysis. In contrast, we apply Cattaneo, Jansson, and Ma’s (Reference Cattaneo, Jansson and Ma2020) local polynomial density estimators to correct both boundary and interior biases of bid and value densities, which exist in the equilibrium outcome of our double auction model. Our method is easy-to-implement and fully boundary adaptive. It introduces only one tuning parameter and does not need the knowledge of true support boundaries for estimator definition and asymptotic results.

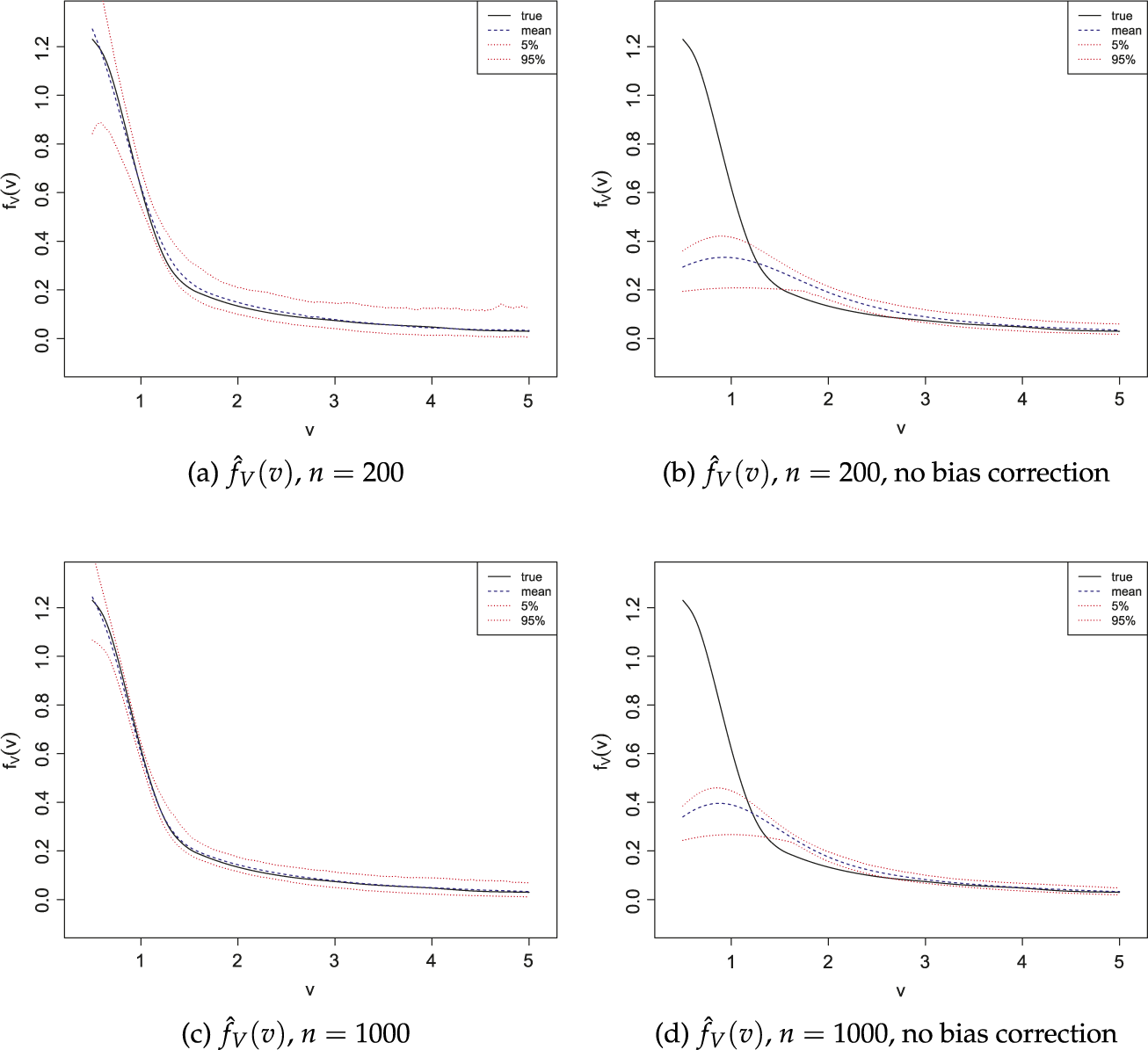

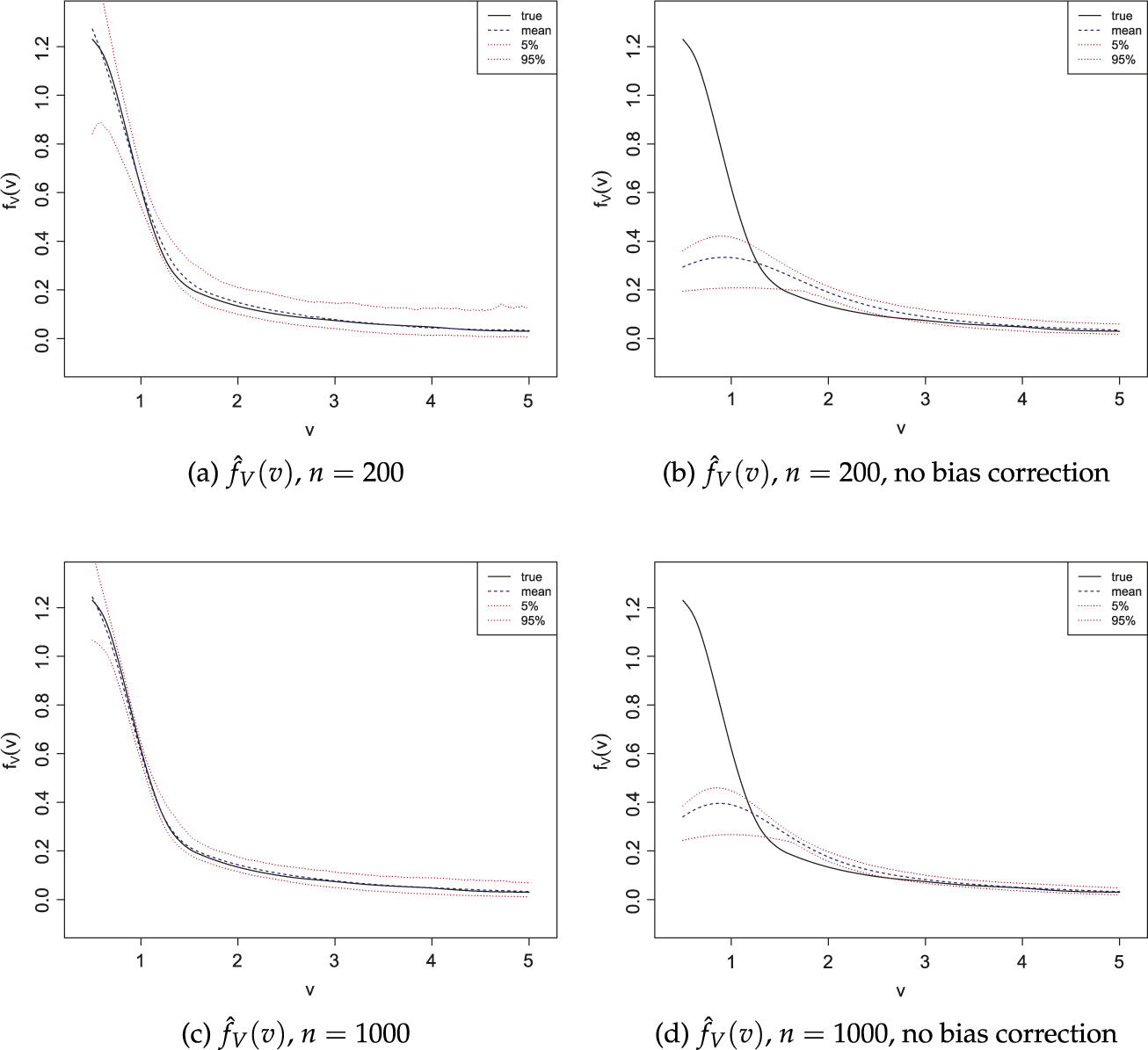

In view of the preceding results, we consider nonparametric identification and estimation of double auction with bargaining. First, in addition to characterizing all the restrictions on the observables (i.e., bid distributions) imposed by the theoretical double auction model with bargaining, we establish the point identification of model primitives (i.e., value distributions) from the observables in the case where all bids are observed. In the case when only transacted bids are observed,Footnote 4 we provide a sharp identified set of bidders’ value distributions (in Theorem 4). We show that, in the latter case, the conditional distributions of bidders’ valuations given positive (conditional) probability of trade are point identified. Second, we propose the (boundary and interior) bias-corrected two-step estimators of the buyer’s and the seller’s value densities. In a double auction setting, we show that our estimators achieve the optimal convergence rate. Third, using Monte Carlo experiments, we show that it is important to implement bias correction (especially bias correction in the interior of the support) in the two-step estimation of value densities. In particular, we show that, without bias correction, the statistical inference is almost infeasible, not only on the boundaries but also in the interior.

The remainder of this article is organized as follows. In Section 2, we present the sealed bid double auction model with bargaining and characterize its equilibrium. Section 3 then studies the identification of private value distributions. In Section 4, we estimate both the bid and the value densities with bias correction and establish their uniform convergence rates. Section 5 uses Monte Carlo experiments to illustrate the finite sample performance of our estimators. Section 6 concludes the article. Appendix A collects the proofs of our main results in the text. Supplemental Material contains some additional results (as well as their proofs).

2 THE k-DOUBLE AUCTION MODEL

We consider a k-double auction in which a single and indivisible object is auctioned between a buyer and a seller. Each of them simultaneously submits a bid. If the buyer’s offer is no lower than the seller’s request, a transaction is made at a price of their weighted average, that is, at a price

$ p(B,S) = k B+(1-k) S, $

where k is a constant in

$ p(B,S) = k B+(1-k) S, $

where k is a constant in

$[0,1]$

, B is the buyer’s offer, and S is the seller’s request. Otherwise, there is no transaction. The buyer has a value V for the auctioned object, and the seller has a reservation value C. Consequently, the buyer’s payoff is

$[0,1]$

, B is the buyer’s offer, and S is the seller’s request. Otherwise, there is no transaction. The buyer has a value V for the auctioned object, and the seller has a reservation value C. Consequently, the buyer’s payoff is

$V-p(B,S)$

and the seller’s payoff is

$V-p(B,S)$

and the seller’s payoff is

$p(B,S)-C$

if a trade occurs; their payoffs are zero otherwise. Each of them does not know the valuation of her opponent, but only knows that it is drawn from a distribution

$p(B,S)-C$

if a trade occurs; their payoffs are zero otherwise. Each of them does not know the valuation of her opponent, but only knows that it is drawn from a distribution

$F_j (j=C,V)$

. Distributions

$F_j (j=C,V)$

. Distributions

$F_V$

and

$F_V$

and

$F_C$

and the payment rule are all common knowledge between the buyer and the seller.

$F_C$

and the payment rule are all common knowledge between the buyer and the seller.

Notice that the weight k measures the bargaining power of the buyer and the seller: the larger k is, the stronger (or weaker) the bargaining power of the buyer (or seller). In particular, the case of

$k = 1$

(resp.

$k = 1$

(resp.

$k = 0$

) corresponds to the buyer (resp. seller) having all the bargaining power.

$k = 0$

) corresponds to the buyer (resp. seller) having all the bargaining power.

We impose the following assumption on the private values and their distributions.

Assumption A. (i) V and C are independent. (ii)

$F_V$

and

$F_V$

and

$F_C$

are twice continuously differentiable with densities

$F_C$

are twice continuously differentiable with densities

$f_V$

and

$f_V$

and

$f_C$

on

$f_C$

on

$[\underline {v},\overline {v}]\subset \mathbb {R}_+$

and

$[\underline {v},\overline {v}]\subset \mathbb {R}_+$

and

$[\underline {c},\overline {c}]\subset \mathbb {R}_+$

, respectively. In addition,

$[\underline {c},\overline {c}]\subset \mathbb {R}_+$

, respectively. In addition,

$f_V(v)\geq \alpha _V>0$

for all

$f_V(v)\geq \alpha _V>0$

for all

$v\in [\underline {v},\overline {v}]$

;

$v\in [\underline {v},\overline {v}]$

;

$f_C(c)\geq \alpha _C>0$

for all

$f_C(c)\geq \alpha _C>0$

for all

$c\in [\underline {c},\overline {c}]$

.

$c\in [\underline {c},\overline {c}]$

.

Under Assumption A, the private value of the seller is independent of the buyer’s, and the value distributions are twice continuously differentiable with densities being bounded away from zero on compact supports. Similar assumption has been adopted by most theoretical papers on double auctions with bargaining (see, e.g., Satterthwaite and Williams, Reference Satterthwaite and Williams1989).

We also impose the following restriction on the supports of

$F_V$

and

$F_V$

and

$F_C$

.

$F_C$

.

Assumption B. The supports of

$F_V$

and

$F_V$

and

$F_C$

satisfy

$F_C$

satisfy

$\underline {c}<\overline {v}$

.

$\underline {c}<\overline {v}$

.

This assumption requires that the buyer’s maximum value must be higher than the seller’s minimum cost. It rules out the trivial case of

$\overline {v}\leq \underline {c}$

in which there is zero probability of trade in any equilibrium. The special cases of such a support condition have been commonly adopted by the theoretical double auction literature (see, e.g., Leininger, Linhart, and Radner, Reference Leininger, Linhart and Radner1989).

$\overline {v}\leq \underline {c}$

in which there is zero probability of trade in any equilibrium. The special cases of such a support condition have been commonly adopted by the theoretical double auction literature (see, e.g., Leininger, Linhart, and Radner, Reference Leininger, Linhart and Radner1989).

Denote by

$\beta _B: [\underline {v},\overline {v}]\to \mathbb {R}_+$

and

$\beta _B: [\underline {v},\overline {v}]\to \mathbb {R}_+$

and

$\beta _S: [\underline {c},\overline {c}]\to \mathbb {R}_+$

the buyer’s and seller’s strategies, respectively. Let

$\beta _S: [\underline {c},\overline {c}]\to \mathbb {R}_+$

the buyer’s and seller’s strategies, respectively. Let

$b=\beta _B(v)$

denote the bid of a buyer with realized private value v under strategy

$b=\beta _B(v)$

denote the bid of a buyer with realized private value v under strategy

$\beta _B$

. Then, the expected profit of the buyer given the seller’s strategy is

$\beta _B$

. Then, the expected profit of the buyer given the seller’s strategy is

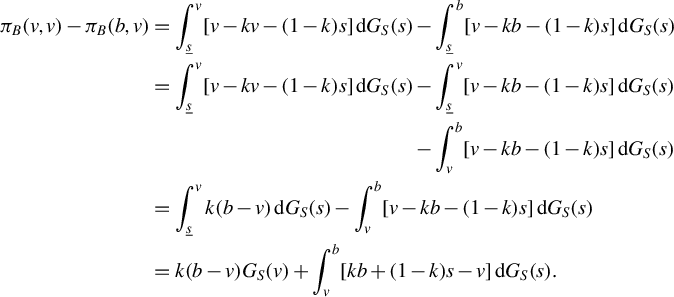

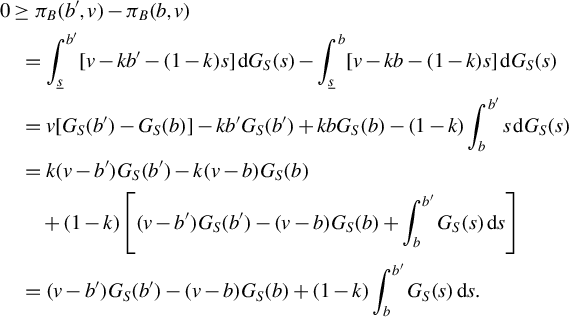

$$ \begin{align} \pi_B(b,v)=\begin{cases} \displaystyle \int_{\underline{s}}^b [v-p(b,s)]\,\mathrm{d} G_S(s)=\int_{\underline{s}}^b [v-kb-(1-k)s]\,\mathrm{d} G_S(s), & \text{if } b\geq\underline{s},\\ 0, & \text{if } b<\underline{s}, \end{cases} \end{align} $$

$$ \begin{align} \pi_B(b,v)=\begin{cases} \displaystyle \int_{\underline{s}}^b [v-p(b,s)]\,\mathrm{d} G_S(s)=\int_{\underline{s}}^b [v-kb-(1-k)s]\,\mathrm{d} G_S(s), & \text{if } b\geq\underline{s},\\ 0, & \text{if } b<\underline{s}, \end{cases} \end{align} $$

where

$G_S$

is the distribution function of the seller’s bid and

$G_S$

is the distribution function of the seller’s bid and

$\underline {s}$

is the lower end point of its support. Similarly, let

$\underline {s}$

is the lower end point of its support. Similarly, let

$s=\beta _S(c)$

denote the request of a seller with realized private reservation value c under strategy

$s=\beta _S(c)$

denote the request of a seller with realized private reservation value c under strategy

$\beta _S$

. Then, the expected profit of the seller given the buyer’s strategy is

$\beta _S$

. Then, the expected profit of the seller given the buyer’s strategy is

$$ \begin{align} \pi_S(s,c)=\begin{cases} \displaystyle \int_s^{\overline{b}} [p(b,s)-c]\,\mathrm{d} G_B(b)=\int_s^{\overline{b}} [kb+(1-k)s-c]\,\mathrm{d} G_B(b), & \text{if } s\leq\overline{b},\\ 0, & \text{if } s>\overline{b}, \end{cases} \end{align} $$

$$ \begin{align} \pi_S(s,c)=\begin{cases} \displaystyle \int_s^{\overline{b}} [p(b,s)-c]\,\mathrm{d} G_B(b)=\int_s^{\overline{b}} [kb+(1-k)s-c]\,\mathrm{d} G_B(b), & \text{if } s\leq\overline{b},\\ 0, & \text{if } s>\overline{b}, \end{cases} \end{align} $$

where

$G_B$

is the distribution function of the buyer’s bid and

$G_B$

is the distribution function of the buyer’s bid and

$\overline {b}$

is the upper end point of its support.

$\overline {b}$

is the upper end point of its support.

We adopt the Bayesian Nash equilibrium (BNE) concept throughout.

Definition 1 (Best Response).

A buyer strategy

$\beta _B$

is the best response to

$\beta _B$

is the best response to

$\beta _S$

if, for any buyer strategy

$\beta _S$

if, for any buyer strategy

$\tilde \beta _B: [\underline v, \overline v]\rightarrow \mathbb R_+$

and each value

$\tilde \beta _B: [\underline v, \overline v]\rightarrow \mathbb R_+$

and each value

$v\in [\underline v,\overline v]$

,

$v\in [\underline v,\overline v]$

,

$\pi _B(\beta _B(v),v)\geq \pi _B(\tilde \beta _B(v),v)$

. The seller’s best response is defined in an analogous way.

$\pi _B(\beta _B(v),v)\geq \pi _B(\tilde \beta _B(v),v)$

. The seller’s best response is defined in an analogous way.

Definition 2 (Bayesian Nash Equilibrium).

A strategy profile

$(\beta _B,\beta _S)$

constitutes a BNE if

$(\beta _B,\beta _S)$

constitutes a BNE if

$\beta _B$

and

$\beta _B$

and

$\beta _S$

are the best responses to each other.

$\beta _S$

are the best responses to each other.

Similar to other bargaining models under incomplete information, the BNE is not unique in our k-double auction model (with bargaining). This is considerably different from an auction model, which has a unique BNE within the symmetric independent private value paradigm. Thus, we exclude some irregular equilibria and focus on those which are well behaved as described in Chatterjee and Samuelson (Reference Chatterjee and Samuelson1983). Precisely, we impose the following restrictions on the equilibrium.

Assumption C (Regular Equilibrium).

The equilibrium strategy profile

$(\beta _B,\beta _S)$

satisfies:

$(\beta _B,\beta _S)$

satisfies:

-

A1.

$\beta _B$

and

$\beta _S$

are continuous on their whole domains;

$\beta _B$

and

$\beta _S$

are continuous on their whole domains; -

A2.

$\beta _B$

is continuously differentiable with positive derivative on

$[\underline {s},\overline {v}]$

if

$\underline {s}<\overline {v}$

;

$\beta _S$

is continuously differentiable with positive derivative on

$[\underline {c},\overline {b}]$

if

$\underline {c}<\overline {b}$

; -

A3.

$\beta _B(v)=v$

if

$v\leq \underline {s}$

;

$\beta _S(c)=c$

if

$c\geq \overline {b}$

.

We say that an equilibrium satisfying Assumption C is regular. Assumption C basically restricts us to strictly monotone and (piecewise) differentiable strategy equilibria that are quite intuitive in bilateral k-double auctions. Furthermore, the regularity conditions of the equilibrium strategy in Assumption C imply that the value densities

$f_V(\cdot )$

and

$f_V(\cdot )$

and

$f_C(\cdot )$

are continuous and bounded away from zero. As demonstrated by Satterthwaite and Williams (Reference Satterthwaite and Williams1989, Thm. 3.2), there exists a continuum of regular equilibria when

$f_C(\cdot )$

are continuous and bounded away from zero. As demonstrated by Satterthwaite and Williams (Reference Satterthwaite and Williams1989, Thm. 3.2), there exists a continuum of regular equilibria when

$k\in (0,1)$

and

$k\in (0,1)$

and

$[\underline {v},\overline {v}]=[\underline {c},\overline {c}]=[0,1]$

.Footnote

5

Following most of the empirical studies in game theory, we adopt the following equilibrium selection mechanism when multiple regular equilibria exist.

$[\underline {v},\overline {v}]=[\underline {c},\overline {c}]=[0,1]$

.Footnote

5

Following most of the empirical studies in game theory, we adopt the following equilibrium selection mechanism when multiple regular equilibria exist.

Assumption D. In all observed auctions, buyers and sellers play the same regular equilibrium.

The same regular equilibrium of Assumption D means a common pair of regular equilibrium strategy functions across observed auctions. If there are multiple regular equilibria across observed auctions according to an equilibrium selection rule, then the distribution of all observed bids will be a mixture of multiple equilibrium bid distributions following the selection rule. In this case, we will need to identify the equilibrium selection mechanism besides the value distributions.

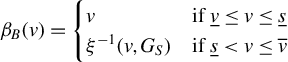

The following lemma characterizes some basic properties of the equilibrium strategy profile.

Lemma 1. Under Assumptions A–C, for any equilibrium

$(\beta _B,\beta _S)$

,

$(\beta _B,\beta _S)$

,

-

(i) when

$v>\underline {s}$

,

$\beta _B(v)\leq v$

with strict inequality if

$k>0$

; -

(ii) when

$c<\overline {b}$

,

$\beta _S(c)\geq c$

with strict inequality if

$k <1$

.

Proof. See Appendix A.1.

Note that the conclusion of Lemma 1 holds for any BNE (i.e., not only for regular BNE). With Condition A3 of Assumption C, it implies that, in regular equilibrium, the buyer will never bid higher than her private value, and the seller will never bid lower than her private value. In the special case of

$k=1/2$

, Leininger et al. (Reference Leininger, Linhart and Radner1989) constructed a lemma similar to our Lemma 1.

$k=1/2$

, Leininger et al. (Reference Leininger, Linhart and Radner1989) constructed a lemma similar to our Lemma 1.

3 NONPARAMETRIC IDENTIFICATION

We study the nonparametric identification of private value distributions in two cases which differ in the degree of available data. In the first case, researchers can observe both the transacted bids and the bids where no transaction takes place.Footnote 6 In the second case, researchers can only observe the transacted bids.

3.1 Identification of Bargaining Power Parameter k

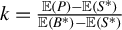

We first identify the bargaining power parameter k. The value of k can be recovered by using additional information on the transaction price, given that the transacted bids are observed. For example, when the mean transaction price is observed, the parameter k is determined by

$k=\frac {\mathbb {E}(P)-\mathbb {E}(S^*)}{\mathbb {E}(B^*)-\mathbb {E}(S^*)}$

since

$k=\frac {\mathbb {E}(P)-\mathbb {E}(S^*)}{\mathbb {E}(B^*)-\mathbb {E}(S^*)}$

since

$\mathbb {E}(P)=k\mathbb {E}(B^*)+(1-k)\mathbb {E}(S^*),$

where

$\mathbb {E}(P)=k\mathbb {E}(B^*)+(1-k)\mathbb {E}(S^*),$

where

$(B^*,S^*)$

are the bids transacted.

$(B^*,S^*)$

are the bids transacted.

Alternatively, k can be identified by using a quantile of the transaction price. This quantile approach is useful when the mean transaction price

$\mathbb {E}(P)$

is not available. For example, we cannot recover the mean transaction price if the transaction prices are censored by some threshold value from above or below. Nevertheless, we can still recover a transaction price quantile in this case. Let

$\mathbb {E}(P)$

is not available. For example, we cannot recover the mean transaction price if the transaction prices are censored by some threshold value from above or below. Nevertheless, we can still recover a transaction price quantile in this case. Let

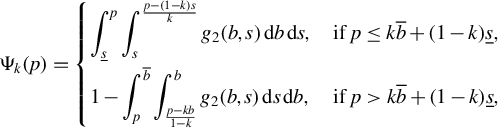

$\Psi _k(p)$

be the transaction price distribution function, where the subscript k indicates that the value of this function could also depend on the price weight k. We can express the transaction price distribution

$\Psi _k(p)$

be the transaction price distribution function, where the subscript k indicates that the value of this function could also depend on the price weight k. We can express the transaction price distribution

$\Psi _k(p)$

in terms of the distribution of transacted bids as follows: (i) when

$\Psi _k(p)$

in terms of the distribution of transacted bids as follows: (i) when

$0<k<1$

, we haveFootnote

7

$0<k<1$

, we haveFootnote

7

$$ \begin{align} \Psi_k(p)=\begin{cases} \displaystyle\int_{\underline{s}}^p \displaystyle\int_s^{\frac{p-(1-k)s}{k}} g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s, & \text{if } p\le k\overline{b}+(1-k)\underline{s},\\[2ex] 1-\displaystyle\int_p^{\overline{b}} \displaystyle\int_{\frac{p-kb}{1-k}}^b g_2(b,s)\,\mathrm{d} s\,\mathrm{d} b, & \text{if } p> k\overline{b}+(1-k)\underline{s}, \end{cases} \end{align} $$

$$ \begin{align} \Psi_k(p)=\begin{cases} \displaystyle\int_{\underline{s}}^p \displaystyle\int_s^{\frac{p-(1-k)s}{k}} g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s, & \text{if } p\le k\overline{b}+(1-k)\underline{s},\\[2ex] 1-\displaystyle\int_p^{\overline{b}} \displaystyle\int_{\frac{p-kb}{1-k}}^b g_2(b,s)\,\mathrm{d} s\,\mathrm{d} b, & \text{if } p> k\overline{b}+(1-k)\underline{s}, \end{cases} \end{align} $$

where

$g_2(b,s) = g(b,s) / \Pr (\underline {s} \leq S \leq B\leq \overline {b})$

is the joint density of transacted bids; (ii) when

$g_2(b,s) = g(b,s) / \Pr (\underline {s} \leq S \leq B\leq \overline {b})$

is the joint density of transacted bids; (ii) when

$k=0$

,Footnote

8

$k=0$

,Footnote

8

$$ \begin{align} \Psi_0(p)=\int_{\underline{s}}^p\int_s^{\overline{b}} g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s; \end{align} $$

$$ \begin{align} \Psi_0(p)=\int_{\underline{s}}^p\int_s^{\overline{b}} g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s; \end{align} $$

and (iii) when

$k=1$

,

$k=1$

,

$$ \begin{align} \Psi_1(p)=\int_{\underline{s}}^p\int_{\underline{s}}^b g_2(b,s)\,\mathrm{d} s\,\mathrm{d} b=\int_{\underline{s}}^p \int_s^p g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s. \end{align} $$

$$ \begin{align} \Psi_1(p)=\int_{\underline{s}}^p\int_{\underline{s}}^b g_2(b,s)\,\mathrm{d} s\,\mathrm{d} b=\int_{\underline{s}}^p \int_s^p g_2(b,s)\,\mathrm{d} b\,\mathrm{d} s. \end{align} $$

The next lemma is the key to identify k using a transaction price quantile. It establishes the monotonicity of the transaction price distribution

$\Psi _k(p)$

in k (for a fixed p).

$\Psi _k(p)$

in k (for a fixed p).

Lemma 2. Under Assumptions A–C, for any fixed

$p\in (\underline {s},\overline {b})$

,

$p\in (\underline {s},\overline {b})$

,

$\Psi _k(p)$

is continuous and strictly decreasing in

$\Psi _k(p)$

is continuous and strictly decreasing in

$k\in [0,1]$

.

$k\in [0,1]$

.

Proof. See Appendix A.2.

The monotonicity of

$\Psi _k(p)$

in k can be seen in (3.1), because both

$\Psi _k(p)$

in k can be seen in (3.1), because both

$[p-(1-k)s]/k$

and

$[p-(1-k)s]/k$

and

$(p-kb)/(1-k)$

are decreasing in k. Based on the monotonicity of

$(p-kb)/(1-k)$

are decreasing in k. Based on the monotonicity of

$\Psi _k(p)$

in k, we can identify the bargaining power parameter k by

$\Psi _k(p)$

in k, we can identify the bargaining power parameter k by

$$ \begin{align} \Psi_{k}(p_\alpha)=\alpha \end{align} $$

$$ \begin{align} \Psi_{k}(p_\alpha)=\alpha \end{align} $$

if an

$\alpha $

-th quantile of the transaction price, say

$\alpha $

-th quantile of the transaction price, say

$p_\alpha $

, is observed.Footnote

9

$p_\alpha $

, is observed.Footnote

9

3.2 Identification with All Submitted Bids

We next consider the nonparametric identification of the k-double auction model with bargaining when researchers observe the distribution of all submitted bids (including the bids that are not transacted).

As shown in Chatterjee and Samuelson (Reference Chatterjee and Samuelson1983) and Satterthwaite and Williams (Reference Satterthwaite and Williams1989), a regular equilibrium

$(\beta _B,\beta _S)$

in a k-double auction with bargaining can be characterized by the following two differential equations for

$(\beta _B,\beta _S)$

in a k-double auction with bargaining can be characterized by the following two differential equations for

$v\geq \underline {s}$

and

$v\geq \underline {s}$

and

$c\leq \overline {b}$

:

$c\leq \overline {b}$

:

$$ \begin{align} \beta_B^{-1}(\beta_S(c))&=\beta_S(c)+k \beta_S'(c)\frac{F_C(c)}{f_C(c)}, \end{align} $$

$$ \begin{align} \beta_B^{-1}(\beta_S(c))&=\beta_S(c)+k \beta_S'(c)\frac{F_C(c)}{f_C(c)}, \end{align} $$

$$ \begin{align} \beta_S^{-1}(\beta_B(v))&=\beta_B(v)-(1-k) \beta_B'(v)\frac{1-F_V(v)}{f_V(v)}, \end{align} $$

$$ \begin{align} \beta_S^{-1}(\beta_B(v))&=\beta_B(v)-(1-k) \beta_B'(v)\frac{1-F_V(v)}{f_V(v)}, \end{align} $$

where

$\beta _B^{-1}(\mkern 2mu\cdot \mkern 2mu)$

and

$\beta _B^{-1}(\mkern 2mu\cdot \mkern 2mu)$

and

$\beta _S^{-1}(\mkern 2mu\cdot \mkern 2mu)$

are the inverse bidding strategies.Footnote

10

To see this, consider the first-order condition of buyer’s payoff maximization for

$\beta _S^{-1}(\mkern 2mu\cdot \mkern 2mu)$

are the inverse bidding strategies.Footnote

10

To see this, consider the first-order condition of buyer’s payoff maximization for

$b\geq \underline s$

:

$b\geq \underline s$

:

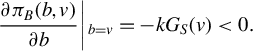

$$ \begin{align*} \frac{\partial\pi_B(b,v)}{\partial b} = (v-b)\cdot g_S(b) - k G_S(b) = 0, \end{align*} $$

$$ \begin{align*} \frac{\partial\pi_B(b,v)}{\partial b} = (v-b)\cdot g_S(b) - k G_S(b) = 0, \end{align*} $$

which yields

$v = b + k G_S(b)/g_S(b) = b + k F_C\big (\beta _S^{-1}(b)\big )\cdot \beta _S'\big (\beta _S^{-1}(b)\big )\big /f_C(\beta _S^{-1}(b))$

due to

$v = b + k G_S(b)/g_S(b) = b + k F_C\big (\beta _S^{-1}(b)\big )\cdot \beta _S'\big (\beta _S^{-1}(b)\big )\big /f_C(\beta _S^{-1}(b))$

due to

$G_S(b) = F_C(\beta _S^{-1}(b))$

and

$G_S(b) = F_C(\beta _S^{-1}(b))$

and

$g_S(b) = f_C(\beta _S^{-1}(b))\big /\beta _S'\big (\beta _S^{-1}(b)\big )$

. In equilibrium, there is

$g_S(b) = f_C(\beta _S^{-1}(b))\big /\beta _S'\big (\beta _S^{-1}(b)\big )$

. In equilibrium, there is

$v=\beta _B^{-1}(b)$

. Thus, we have

$v=\beta _B^{-1}(b)$

. Thus, we have

$$ \begin{align*} \beta_B^{-1}(b) = b + k F_C\big(\beta_S^{-1}(b)\big)\cdot \beta_S'\big(\beta_S^{-1}(b)\big)\big/f_C(\beta_S^{-1}(b)), \end{align*} $$

$$ \begin{align*} \beta_B^{-1}(b) = b + k F_C\big(\beta_S^{-1}(b)\big)\cdot \beta_S'\big(\beta_S^{-1}(b)\big)\big/f_C(\beta_S^{-1}(b)), \end{align*} $$

which implies (3.5) by let

$b=\beta _S(c)$

. A similar argument will yield (3.6).

$b=\beta _S(c)$

. A similar argument will yield (3.6).

As shown in the following lemma, Assumption A implies that the equilibrium bid distributions generated will also satisfy a similar smoothness condition.

Lemma 3. Under Assumptions A–C, the distributions of regular equilibrium bids

$G_B$

and

$G_B$

and

$G_S$

satisfy:

$G_S$

satisfy:

-

(i) for any

$b\in [\underline {b},\overline {b}]$

and any

$s\in [\underline {s},\overline {s}]$

,

$g_B(b)\geq \alpha _B>0$

,

$g_S(s)\geq \alpha _S>0$

; -

(ii)

$g_B$

and

$g_S$

are twice continuously differentiable on

$[\underline {s},\overline {b}]$

.

Proof. See Appendix A.3.

The striking feature of Lemma 3 is part (ii). It shows that the bid densities are smoother than their corresponding latent value densities. A similar result is obtained by Guerre et al. (Reference Guerre, Perrigne and Vuong2000) in first-price auctions.

For the buyer with value

$v\geq \underline {s}$

, the equilibrium bid under strategy

$v\geq \underline {s}$

, the equilibrium bid under strategy

$\beta _B$

is

$\beta _B$

is

$b=\beta _B(v)$

. Let

$b=\beta _B(v)$

. Let

$\tilde {c}=\beta _S^{-1}(b)$

. Since strategy

$\tilde {c}=\beta _S^{-1}(b)$

. Since strategy

$\beta _S$

is strictly increasing,

$\beta _S$

is strictly increasing,

$G_S(b)=F_C(\beta _S^{-1}(b))=F_C(\tilde {c})$

. Noting that

$G_S(b)=F_C(\beta _S^{-1}(b))=F_C(\tilde {c})$

. Noting that

$$\begin{align*}g_S(b)=\frac{f_C(\beta_S^{-1}(b))}{\beta_S'(\beta_S^{-1}(b))}=\frac{f_C(\tilde{c})}{\beta_S'(\tilde{c})}, \quad v=\beta_B^{-1}(b)=\beta_B^{-1}(\beta_S(\tilde{c})),\end{align*}$$

$$\begin{align*}g_S(b)=\frac{f_C(\beta_S^{-1}(b))}{\beta_S'(\beta_S^{-1}(b))}=\frac{f_C(\tilde{c})}{\beta_S'(\tilde{c})}, \quad v=\beta_B^{-1}(b)=\beta_B^{-1}(\beta_S(\tilde{c})),\end{align*}$$

by (3.5), we have

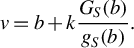

$$ \begin{align} v=b+k\frac{G_S(b)}{g_S(b)}. \end{align} $$

$$ \begin{align} v=b+k\frac{G_S(b)}{g_S(b)}. \end{align} $$

Similarly, for the seller with value

$c\leq \overline {b}$

, we have the following condition by (3.6):

$c\leq \overline {b}$

, we have the following condition by (3.6):

$$ \begin{align} c=s-(1-k)\frac{1-G_B(s)}{g_B(s)}. \end{align} $$

$$ \begin{align} c=s-(1-k)\frac{1-G_B(s)}{g_B(s)}. \end{align} $$

Note that (3.7) and (3.8) only hold for

$v\geq \underline {s}$

and

$v\geq \underline {s}$

and

$c\leq \overline {b}$

. In such a case, we have

$c\leq \overline {b}$

. In such a case, we have

$\Pr (\beta _B(V)\geq \beta _S(C)\mid V=v)>0$

when

$\Pr (\beta _B(V)\geq \beta _S(C)\mid V=v)>0$

when

$v>\underline {s}$

and

$v>\underline {s}$

and

$\Pr (\beta _B(V)\geq \beta _S(C)\mid C=c)>0$

when

$\Pr (\beta _B(V)\geq \beta _S(C)\mid C=c)>0$

when

$c<\overline {b}$

. In other words, given the private values, both the buyer and the seller expect that the trade will occur with a positive probability.Footnote

11

For the buyer with value

$c<\overline {b}$

. In other words, given the private values, both the buyer and the seller expect that the trade will occur with a positive probability.Footnote

11

For the buyer with value

$v<\underline {s}$

or the seller with value

$v<\underline {s}$

or the seller with value

$c>\overline {b}$

, there will be no transaction under strategy profile

$c>\overline {b}$

, there will be no transaction under strategy profile

$(\beta _B,\beta _S)$

. We define the functions

$(\beta _B,\beta _S)$

. We define the functions

$\xi (b,G_S)$

and

$\xi (b,G_S)$

and

$\eta (s,G_B)$

as the right-hand sides of (3.7) and (3.8), respectively. That is,

$\eta (s,G_B)$

as the right-hand sides of (3.7) and (3.8), respectively. That is,

$$ \begin{align} \xi(b,G_S) &\equiv b+k\frac{G_S(b)}{g_S(b)}, \quad \underline{s}\leq b\leq \overline{s}, \end{align} $$

$$ \begin{align} \xi(b,G_S) &\equiv b+k\frac{G_S(b)}{g_S(b)}, \quad \underline{s}\leq b\leq \overline{s}, \end{align} $$

$$ \begin{align} \eta(s,G_B) &\equiv s-(1-k)\frac{1-G_B(s)}{g_B(s)}, \quad \underline{b}\leq s\leq \overline{b}. \end{align} $$

$$ \begin{align} \eta(s,G_B) &\equiv s-(1-k)\frac{1-G_B(s)}{g_B(s)}, \quad \underline{b}\leq s\leq \overline{b}. \end{align} $$

By definition, it is straightforward that

$\xi (\underline s,G_S)=\underline s$

and

$\xi (\underline s,G_S)=\underline s$

and

$\eta (\overline b, G_B)=\overline b$

.

$\eta (\overline b, G_B)=\overline b$

.

We define

$\mathscr {P}_{\mathscr {A}}$

as the collection of absolutely continuous probability distributions with support

$\mathscr {P}_{\mathscr {A}}$

as the collection of absolutely continuous probability distributions with support

$\mathscr {A}$

. Let G denote the joint distribution of

$\mathscr {A}$

. Let G denote the joint distribution of

$(B,S)$

. Here, we restrict ourselves to the regular equilibrium strategies which are strictly increasing and (piecewise) differentiable.

$(B,S)$

. Here, we restrict ourselves to the regular equilibrium strategies which are strictly increasing and (piecewise) differentiable.

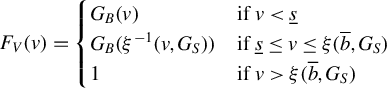

Theorem 1. Under Assumptions C and D, if

$G\in \mathscr {P}_{\mathscr {D}}$

is the joint distribution of regular equilibrium bids

$G\in \mathscr {P}_{\mathscr {D}}$

is the joint distribution of regular equilibrium bids

$(B,S)$

in a sealed-bid k-double auction with some

$(B,S)$

in a sealed-bid k-double auction with some

$(F_V,F_C)$

satisfying Assumptions A and B, then

$(F_V,F_C)$

satisfying Assumptions A and B, then

-

C1. the support

$\mathscr {D}=[\underline {b},\overline {b}] \times [\underline {s},\overline {s}]$

with

$\underline {b} \leq \underline {s} < \overline {b} \leq \overline {s}$

; -

C2.

$G(b,s)=G_B(b)\cdot G_S(s)$

and

$G_B\in \mathscr {P}_{[\underline {b},\overline {b}]}$

,

$G_S\in \mathscr {P}_{[\underline {s},\overline {s}]}$

; -

C3. the function

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

defined in (3.9) is strictly increasing on

$[\underline {s},\overline {b}]$

and its inverse is differentiable on

$[\xi (\underline {s},G_S),\xi (\overline {b},G_S)]$

; -

C4. the function

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

defined in (3.10) is strictly increasing on

$[\underline {s},\overline {b}]$

and its inverse is differentiable on

$[\eta (\underline {s},G_B),\eta (\overline {b},G_B)]$

; -

C5. for any

$b\in [\underline s,\overline b]$

and any

$b'\in [\overline b,\overline s]$

, (3.11)

$$ \begin{align} [\xi(b,G_S)-b']G_S(b')-[\xi(b,G_S)-b]G_S(b) + (1-k)\int_{b}^{b'} G_S(s)\,\mathrm{d} s \leq 0; \end{align} $$

-

C6. for any

$s\in [\underline s,\overline b]$

and any

$s'\in [\underline b,\underline s]$

, (3.12)

$$ \begin{align} [s'-\eta(s,G_B)][1-G_B(s')] &-[s-\eta(s,G_B)][1-G_B(s)] \nonumber \\ & + k\int_{s'}^{s} [1-G_B(b)]\,\mathrm{d} b \leq 0. \end{align} $$

Proof. See Appendix A.4.

Theorem 1 shows that the theoretical model of a k-double auction with bargaining does impose some restrictions on the joint distribution of observed bids.Footnote

12

Together with Theorem 2 which will be shown immediately, these restrictions can be used to establish a formal test of the theory of k-double auction with bargaining. Specifically, condition C1 of Theorem 1 shows that the buyer’s minimum (or maximum) bid is not higher than the seller’s minimum (or maximum) bid, and the intersection between the buyer’s and the seller’s bid supports has a nonempty interior. The latter is mainly due to Assumption B about the supports of private value distributions, which implies that there is always a positive probability of trade in any regular equilibrium. Condition C2 shows that the buyer’s bid is independent of the seller’s. This independence result is intuitive given that the buyer’s value is independent of the seller’s. Conditions C3 and C4 say that the functions

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

and

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

and

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

, which can be regarded as the inverse bidding strategies, are strictly increasing and differentiable in the interval where there is a positive probability of trade. The strict monotonicity property of the inverse bidding strategies comes from the fact that the equilibrium strategies are strictly increasing. As shown in the proof of Theorem 1, condition C5 is equivalent to a non-profitable deviation for the buyer with a value of

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

, which can be regarded as the inverse bidding strategies, are strictly increasing and differentiable in the interval where there is a positive probability of trade. The strict monotonicity property of the inverse bidding strategies comes from the fact that the equilibrium strategies are strictly increasing. As shown in the proof of Theorem 1, condition C5 is equivalent to a non-profitable deviation for the buyer with a value of

$\xi (b,G_S)$

from the equilibrium offer

$\xi (b,G_S)$

from the equilibrium offer

$b\in [\underline s,\overline b]$

to an offer

$b\in [\underline s,\overline b]$

to an offer

$b'$

higher than the maximum offer

$b'$

higher than the maximum offer

$\overline b$

; and condition C6 is equivalent to a no profitable deviation for the seller with a reservation value of

$\overline b$

; and condition C6 is equivalent to a no profitable deviation for the seller with a reservation value of

$\eta (s,G_B)$

from the equilibrium ask

$\eta (s,G_B)$

from the equilibrium ask

$s\in [\underline s,\overline b]$

to an ask

$s\in [\underline s,\overline b]$

to an ask

$s'$

lower than the minimum ask

$s'$

lower than the minimum ask

$\underline s$

.

$\underline s$

.

The following theorem establishes our first identification result regarding private value distributions.

Theorem 2. Under Assumptions A–D,

$F_V$

and

$F_V$

and

$F_C$

are point identified from any given

$F_C$

are point identified from any given

$G\in \mathscr {P}_{\mathscr {D}}$

that satisfy C1–C6.

$G\in \mathscr {P}_{\mathscr {D}}$

that satisfy C1–C6.

Proof. See Appendix A.5.

Theorem 2 shows that the private value distributions

$F_V$

and

$F_V$

and

$F_C$

are point identified from the joint distribution of the observed bids. In particular, if any of the conditions C1–C6 does not hold, then there is no

$F_C$

are point identified from the joint distribution of the observed bids. In particular, if any of the conditions C1–C6 does not hold, then there is no

$(F_V,F_C)$

satisfying Assumptions A and B to rationalize the bid distribution G according to Theorem 1. In other words, the identified set is empty when any of those conditions (including conditions C5 and C6) fails. In addition, inverse bidding strategies

$(F_V,F_C)$

satisfying Assumptions A and B to rationalize the bid distribution G according to Theorem 1. In other words, the identified set is empty when any of those conditions (including conditions C5 and C6) fails. In addition, inverse bidding strategies

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

and

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

and

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

are based only on knowledge of the distribution G. We can therefore avoid solving the linked differential equations (3.5) and (3.6) in our identification.

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

are based only on knowledge of the distribution G. We can therefore avoid solving the linked differential equations (3.5) and (3.6) in our identification.

Conditions C5 and C6 are less intuitive and could be difficult to check in practice. It will be helpful to provide their sufficient conditions that are easy to verify. Our next lemma provides such sufficient conditions.

Lemma 4. Under Assumptions A and B, conditions C3–C6 are implied by:

-

C7. the function

$\xi (\mkern 2mu\cdot \mkern 2mu,G_S)$

defined in (3.9) is strictly increasing on

$[\underline {s},\overline {s}]$

and its inverse is differentiable on

$[\xi (\underline {s},G_S),\xi (\overline {b},G_S)]$

; -

C8. the function

$\eta (\mkern 2mu\cdot \mkern 2mu,G_B)$

defined in (3.10) is strictly increasing on

$[\underline {b},\overline {b}]$

and its inverse is differentiable on

$[\eta (\underline {s},G_B),\eta (\overline {b},G_B)]$

.

Proof. See Appendix A.6.

Conditions C7 and C8 in Lemma 4 are related to conditions C5 and C6 in Theorem 1. The monotonicity of

$\xi (\cdot ,G_S)$

in

$\xi (\cdot ,G_S)$

in

$[\underline s,\overline s]$

of condition C7 guarantees that the buyer has no profitable deviation from the equilibrium offer to any other offer in

$[\underline s,\overline s]$

of condition C7 guarantees that the buyer has no profitable deviation from the equilibrium offer to any other offer in

$[\underline s,\overline s]$

, including any other offer in

$[\underline s,\overline s]$

, including any other offer in

$[\overline b,\overline s]$

as stated in condition C5. Similarly, the monotonicity of

$[\overline b,\overline s]$

as stated in condition C5. Similarly, the monotonicity of

$\eta (\cdot ,G_B)$

in

$\eta (\cdot ,G_B)$

in

$[\underline b,\overline b]$

of condition C8 guarantees that the seller has no profitable deviation from the equilibrium ask to any other ask in

$[\underline b,\overline b]$

of condition C8 guarantees that the seller has no profitable deviation from the equilibrium ask to any other ask in

$[\underline b,\overline b]$

, including any other ask in

$[\underline b,\overline b]$

, including any other ask in

$[\underline b,\underline s]$

as stated in condition C6. Notice that Assumptions C and D are not needed in Lemma 4.

$[\underline b,\underline s]$

as stated in condition C6. Notice that Assumptions C and D are not needed in Lemma 4.

3.3 Identification with Only Transacted Bids

We now discuss the nonparametric identification of value distributions when only transacted bids are available. To better understand our identification results, we first provide the rationalization results as follows.

Theorem 3. Under Assumptions C and D: If

$G_2\in \mathscr {P}_{\mathscr {D'}}$

is the joint distribution of transacted bids under some regular equilibrium in a sealed bid k-double auction with

$G_2\in \mathscr {P}_{\mathscr {D'}}$

is the joint distribution of transacted bids under some regular equilibrium in a sealed bid k-double auction with

$(F_V,F_C)$

satisfying Assumptions A and B, then:

$(F_V,F_C)$

satisfying Assumptions A and B, then:

-

D1. the support

$\mathscr {D'}=\left \{(b,s)\mid \underline {s}\leq s\leq b\leq \overline {b}\right \}$

with

$\underline {s}<\overline {b}$

; -

D2. for any

$\underline {s}\leq s'\leq s\leq b\leq b'\leq \overline {b}$

, the density of

$G_2$

satisfies

$g_2(b,s)\cdot g_2(b',s')=g_2(b,s')\cdot g_2(b',s)$

; -

D3. the function

$\xi (\mkern 2mu\cdot \mkern 2mu,G_{S})$

defined in (3.9) is strictly increasing on

$[\underline {s},\overline {b}]$

and its inverse is differentiable on

$[\xi (\underline {s},G_{S}),\xi (\overline {b},G_{S})]$

; -

D4. the function

$\eta (\mkern 2mu\cdot \mkern 2mu,G_{B})$

defined in (3.10) is strictly increasing on

$[\underline {s},\overline {b}]$

and its inverse is differentiable on

$[\eta (\underline {s},G_{B}),\eta (\overline {b},G_{B})]$

.

Proof. See Appendix A.7.

The rationalization results of Theorem 3 are similar to those of Theorem 1 in the case of using all bids. Specifically, condition D1 says that the support of the distribution of observed (transacted) bids is a triangle in which the buyer’s bid is no less than the seller’s. Condition D2 means that the multiplication of conditional densities evaluated at

$(b,s)$

and

$(b,s)$

and

$(b',s')$

is the same as the multiplication of conditional densities evaluated at

$(b',s')$

is the same as the multiplication of conditional densities evaluated at

$(b,s')$

and

$(b,s')$

and

$(b',s)$

as long as these four points are located in the transacted bid area. This condition arises mainly due to the independence of private values. Conditions D3 and D4 state that both the buyer’s and the seller’s inverse bidding strategies are strictly increasing and differentiable on the interval of all possible transacted bid values, namely,

$(b',s)$

as long as these four points are located in the transacted bid area. This condition arises mainly due to the independence of private values. Conditions D3 and D4 state that both the buyer’s and the seller’s inverse bidding strategies are strictly increasing and differentiable on the interval of all possible transacted bid values, namely,

$[\underline s, \overline b]$

.

$[\underline s, \overline b]$

.

We next turn to the identification formally. To clarify the idea, we first lay out our identification strategy and then discuss our identification results. Let

$G_2$

denote the joint distribution of the transacted bids.Footnote

13

A two-step procedure is employed to accomplish the identification. In the first step, we identify both marginal bid distributions

$G_2$

denote the joint distribution of the transacted bids.Footnote

13

A two-step procedure is employed to accomplish the identification. In the first step, we identify both marginal bid distributions

$G_B$

and

$G_B$

and

$G_S$

on

$G_S$

on

$[\underline {s},\overline {b}]$

from the distribution

$[\underline {s},\overline {b}]$

from the distribution

$G_2$

of the transacted bids. For any

$G_2$

of the transacted bids. For any

$s\leq \overline {b}$

,

$s\leq \overline {b}$

,

$G_S(s) = \Pr (S\leq s | B=\overline {b})$

by the independence between B and S.

$G_S(s) = \Pr (S\leq s | B=\overline {b})$

by the independence between B and S.

$\Pr (S\leq s | B=\overline {b})$

is identified from the distribution

$\Pr (S\leq s | B=\overline {b})$

is identified from the distribution

$G_2$

of the transacted bids, because the transaction is always successful in this case by

$G_2$

of the transacted bids, because the transaction is always successful in this case by

$S\leq s\leq \overline {b} = B$

. The seller’s marginal bid distribution

$S\leq s\leq \overline {b} = B$

. The seller’s marginal bid distribution

$G_S(\cdot )$

and its density

$G_S(\cdot )$

and its density

$g_S(\cdot )$

are therefore identified on

$g_S(\cdot )$

are therefore identified on

$[\underline {s},\overline {b}]$

. Similarly, the marginal bid distribution of the buyer

$[\underline {s},\overline {b}]$

. Similarly, the marginal bid distribution of the buyer

$G_B(\cdot )$

and its density

$G_B(\cdot )$

and its density

$g_B(\cdot )$

are also identified on

$g_B(\cdot )$

are also identified on

$[\underline {s},\overline {b}]$

by

$[\underline {s},\overline {b}]$

by

$1-G_B(b) = \Pr (B>b | S = \underline {s})$

for any

$1-G_B(b) = \Pr (B>b | S = \underline {s})$

for any

$b\geq \underline {s}$

. In the second step, we recover the corresponding private values for the buyer and the seller by the inverse bidding strategies of (3.9) and (3.10) for the bids on

$b\geq \underline {s}$

. In the second step, we recover the corresponding private values for the buyer and the seller by the inverse bidding strategies of (3.9) and (3.10) for the bids on

$[\underline {s},\overline {b}]$

. We formally state the results of this identification strategy as follows.

$[\underline {s},\overline {b}]$

. We formally state the results of this identification strategy as follows.

Theorem 4. Suppose that Assumptions A–D hold. For any joint distribution of transacted bids

$G_2\in \mathscr {P}_{\mathscr {D'}}$

satisfying D1–D4, the identified set of value distributions contains all

$G_2\in \mathscr {P}_{\mathscr {D'}}$

satisfying D1–D4, the identified set of value distributions contains all

$F_V$

and

$F_V$

and

$F_C$

that satisfy

$F_C$

that satisfy

-

E1.

$\underline {c}\leq \underline {s}<\overline {b}\leq \overline {v}$

; -

E2. for all

$(v,c)\in [\underline s,\xi (\overline b,G_{S})]\times [\eta (\underline s,G_{B}),\overline b]$

,Footnote

14

(3.13)where

$$ \begin{align} \Pr\left(V\leq v \mid V\geq \underline s \right) &= \frac{G_B(\xi^{-1}(v,G_{S})) - G_{B}(\underline{s})}{1-G_B(\underline{s})} , \quad \Pr\left(C\leq c \mid C\leq \overline b\right) \nonumber \\ &= \frac{G_S(\eta^{-1}(c,G_{B}))}{G_S(\overline{b})}, \end{align} $$

$\Pr \left (V\leq v\mid V\geq \underline {s}\right )=\dfrac {F_V(v)-F_V(\underline {s})}{1-F_V(\underline {s})}$

, and

$\Pr \left (C\leq c\mid C\leq \overline {b}\right )=\dfrac {F_C(c)}{F_C(\overline {b})}$

.

Proof. See Appendix A.8.

Theorem 4 provides the identified set of model primitives

$(F_V,F_C)$

in an implicit way, namely, that the identified set does not have a closed-form expression. In particular, condition E2 provides the main identification restrictions on

$(F_V,F_C)$

in an implicit way, namely, that the identified set does not have a closed-form expression. In particular, condition E2 provides the main identification restrictions on

$(F_V,F_C)$

. It provides the (point) identified expressions for

$(F_V,F_C)$

. It provides the (point) identified expressions for

$\Pr (V\leq \cdot |V\geq \underline s)$

and

$\Pr (V\leq \cdot |V\geq \underline s)$

and

$\Pr (C\leq \cdot | C\leq \overline b)$

that are mappings of

$\Pr (C\leq \cdot | C\leq \overline b)$

that are mappings of

$F_V$

and

$F_V$

and

$F_C$

.

$F_C$

.

In the parametric case, condition E2 of Theorem 4 is actually useful to obtain the point identification of the parameter of interest under a condition on the Jacobian matrix.Footnote

15

This is summarized by the following theorem. Let

$F_V(\cdot )=F_V(\cdot ;\theta _B)$

and

$F_V(\cdot )=F_V(\cdot ;\theta _B)$

and

$F_C(\cdot ) = F_C(\cdot ;\theta _S),$

where

$F_C(\cdot ) = F_C(\cdot ;\theta _S),$

where

$\theta _B\in \Theta _B \subset \mathbb {R}^{d_B}$

,

$\theta _B\in \Theta _B \subset \mathbb {R}^{d_B}$

,

$\theta _S\in \Theta _S \subset \mathbb {R}^{d_S}$

with

$\theta _S\in \Theta _S \subset \mathbb {R}^{d_S}$

with

$\Theta _B$

and

$\Theta _B$

and

$\Theta _S$

being open sets. Denote

$\Theta _S$

being open sets. Denote

${\mathcal Q}_B(\theta _B;v) \equiv \Pr (V\leq v| V\geq \underline {s})$

,

${\mathcal Q}_B(\theta _B;v) \equiv \Pr (V\leq v| V\geq \underline {s})$

,

${\mathcal Q}_S(\theta _S;c) \equiv \Pr (C\leq c| C\leq \overline {b})$

, and

${\mathcal Q}_S(\theta _S;c) \equiv \Pr (C\leq c| C\leq \overline {b})$

, and

$\Theta _B'$

(resp.

$\Theta _B'$

(resp.

$\Theta _S'$

) be the collection of

$\Theta _S'$

) be the collection of

$\theta _B\in \Theta _B$

(resp.

$\theta _B\in \Theta _B$

(resp.

$\theta _S\in \Theta _S$

) such that condition E2 of Theorem 4 holds. In addition, for any

$\theta _S\in \Theta _S$

) such that condition E2 of Theorem 4 holds. In addition, for any

$v^m \equiv (v_1,\dots ,v_m)$

and

$v^m \equiv (v_1,\dots ,v_m)$

and

$ c^{m'} \equiv (c_1,\dots ,c_{m'})$

, let

$ c^{m'} \equiv (c_1,\dots ,c_{m'})$

, let

$J{\mathcal Q}_B(\theta _B;v^m)$

and

$J{\mathcal Q}_B(\theta _B;v^m)$

and

$J{\mathcal Q}_S(\theta _S;c^{m'})$

be the Jacobian matrices of

$J{\mathcal Q}_S(\theta _S;c^{m'})$

be the Jacobian matrices of

$({\mathcal Q}_B(\theta _B;v_1),\dots ,{\mathcal Q}_B(\theta _B;v_m))$

(w.r.t.

$({\mathcal Q}_B(\theta _B;v_1),\dots ,{\mathcal Q}_B(\theta _B;v_m))$

(w.r.t.

$\theta _B$

) and

$\theta _B$

) and

$({\mathcal Q}_S(\theta _S;c_1),\dots ,{\mathcal Q}_S(\theta _S;c_{m'}))$

(w.r.t.

$({\mathcal Q}_S(\theta _S;c_1),\dots ,{\mathcal Q}_S(\theta _S;c_{m'}))$

(w.r.t.

$\theta _S$

).

$\theta _S$

).

Theorem 5. Suppose that Assumptions A–D hold. Then

$\theta _B$

(resp.

$\theta _B$

(resp.

$\theta _S$

) is identified if the following two conditions hold: (i)

$\theta _S$

) is identified if the following two conditions hold: (i)

$\Theta _B'$

(resp.

$\Theta _B'$

(resp.

$\Theta _S'$

) is convex and (ii) there exists a

$\Theta _S'$

) is convex and (ii) there exists a

$v^m$

(resp.

$v^m$

(resp.

$c^{m'}$

) and a

$c^{m'}$

) and a

$d_B\times d_B$

submatrix

$d_B\times d_B$

submatrix

$\overline {JQ}_B$

of

$\overline {JQ}_B$

of

$J{\mathcal Q}_B(\theta _B;v^m)$

(resp. a

$J{\mathcal Q}_B(\theta _B;v^m)$

(resp. a

$d_S\times d_S$

submatrix

$d_S\times d_S$

submatrix

$\overline {JQ}_S$

of

$\overline {JQ}_S$

of

$J{\mathcal Q}_S(\theta _S;c^{m'})$

) such that the determinant of

$J{\mathcal Q}_S(\theta _S;c^{m'})$

) such that the determinant of

$\overline {JQ}_B$

(resp.

$\overline {JQ}_B$

(resp.

$\overline {JQ}_S$

) is positive and

$\overline {JQ}_S$

) is positive and

$\overline {JQ}_B + \overline {JQ}_B'$

(resp.

$\overline {JQ}_B + \overline {JQ}_B'$

(resp.

$\overline {JQ}_S + \overline {JQ}_S'$

) is positive semi-definite for all

$\overline {JQ}_S + \overline {JQ}_S'$

) is positive semi-definite for all

$\theta _B\in \Theta _B'$

(resp.

$\theta _B\in \Theta _B'$

(resp.

$\theta _S\in \Theta _S'$

).

$\theta _S\in \Theta _S'$

).

Proof. See Appendix A.9.

Theorem 5 establishes the identification of

$\theta _B$

and

$\theta _B$

and

$\theta _S$

under some condition to guarantee the global univalence of the mappings due to Gale and Nikaido (Reference Gale and Nikaido1965). We can show the identification of

$\theta _S$

under some condition to guarantee the global univalence of the mappings due to Gale and Nikaido (Reference Gale and Nikaido1965). We can show the identification of

$\theta _B$

and

$\theta _B$

and

$\theta _S$

in the neighborhood of their true values under a weaker condition, such as the full column rank of the Jacobian matrix at the true value of parameter (see, e.g., Theorem 6 of Rothenberg, Reference Rothenberg1971).

$\theta _S$

in the neighborhood of their true values under a weaker condition, such as the full column rank of the Jacobian matrix at the true value of parameter (see, e.g., Theorem 6 of Rothenberg, Reference Rothenberg1971).

4 ESTIMATION

Based on the identification strategy, we provide a nonparametric estimation procedure as well as its asymptotic properties when all bids can be observed by the researchers. We will briefly discuss the estimation of the case with only transacted bids in Section S.2.3 of the Supplementary Material.Footnote 16 To present the basic ideas, we further assume that all the observed k-double auctions are homogeneous. Section S.2.1 of the Supplementary Material extends our estimation method to allow auction-specific heterogeneity.

Our estimation procedure extends the two-step estimator proposed by Guerre et al. (Reference Guerre, Perrigne and Vuong2000) for the estimation of sealed-bid first-price auctions: In the first step, a sample of buyers’ and sellers’ “pseudo private values” is constructed by (3.7) and (3.8), where

$G_S$

and

$G_S$

and

$G_B$

are estimated by their empirical distribution functions, and

$G_B$

are estimated by their empirical distribution functions, and

$g_S$

and

$g_S$

and

$g_B$

are estimated by their kernel density estimators with boundary and interior bias correction. In the second step, this sample of pseudo private values is used to nonparametrically estimate the densities of buyers’ and sellers’ private values with boundary and interior bias correction. Notice that, due to the regular equilibrium assumption, a bidder’s private value is equal to her bid (in the first step) if the bidder is a buyer offering less than

$g_B$

are estimated by their kernel density estimators with boundary and interior bias correction. In the second step, this sample of pseudo private values is used to nonparametrically estimate the densities of buyers’ and sellers’ private values with boundary and interior bias correction. Notice that, due to the regular equilibrium assumption, a bidder’s private value is equal to her bid (in the first step) if the bidder is a buyer offering less than

$\underline s$

or if the bidder is a seller asking more than

$\underline s$

or if the bidder is a seller asking more than

$\overline b$

.

$\overline b$

.

It is worth pointing out that both boundary and interior bias correction are implemented in all kernel density estimators of our two-step procedure. This is motivated by the fact that the boundary and interior biases are worse in double auctions than in first-price auctions. Specifically, as pointed out by Guerre et al. (Reference Guerre, Perrigne and Vuong2000), the estimators of bid density and private value density suffer from boundary bias (on the two endpoints of each support) in the two-step estimation of first-price auctions, since these two densities are bounded away from zero on finite supports. This issue carries over to the double auction setup and is made worse by the discontinuity of bid densities in the interior of their supports. The interior discontinuity of bid densities occurs because bidding strategies have interior kinks in regular equilibrium. Consequently, the two-step estimator of private value density with boundary and interior bias correction will have a better performance than the one without any bias correction (e.g., the one with sample trimming instead) in finite samples. This is similar to Hickman and Hubbard (Reference Hickman and Hubbard2014) who corrected the bias on the boundaries (not in the interior) of the bid and value densities, and is confirmed by our Monte Carlo experiments in Section 5 as well.

We apply the boundary-adaptive local polynomial density estimators proposed by Cattaneo et al. (Reference Cattaneo, Jansson and Ma2020) to our double auction setup, and focus on the case of continuously differentiable private value density (and hence twice continuously differentiable bid density by Lemma 3).Footnote 17 The case of smoother private value densities is discussed in Section S.1 of the Supplementary Material.

4.1 Definition of the Estimator

To clarify our idea, we consider n homogeneous k-double auctions. In each auction

$i=1,2,\ldots ,n$

, there is one buyer with private value

$i=1,2,\ldots ,n$

, there is one buyer with private value

$V_i$

and one seller with private value

$V_i$

and one seller with private value

$C_i$

. We observe a sample consisting of all the buyers’ bids

$C_i$

. We observe a sample consisting of all the buyers’ bids

$\{B_1,B_2,\ldots ,B_n\}$

and all the sellers’ bids

$\{B_1,B_2,\ldots ,B_n\}$

and all the sellers’ bids

$\{S_1,S_2,\ldots ,S_n\}$

. Let

$\{S_1,S_2,\ldots ,S_n\}$

. Let

$\hat {\underline b}$

and

$\hat {\underline b}$

and

$\hat {\overline b}$

(

$\hat {\overline b}$

(

$\hat {\underline s}$

and

$\hat {\underline s}$

and

$\hat {\overline s}$

) be the minimum and maximum of the n observed bids of buyers (sellers).

$\hat {\overline s}$

) be the minimum and maximum of the n observed bids of buyers (sellers).

Our estimation proceeds as follows. In the first step, we use the observed sample of all bids to estimate the distribution and density functions of the buyers’ and sellers’ bids by their empirical distribution functions and (boundary and interior) bias-corrected kernel density estimators on the interval of

$[\underline s,\overline b]$

, respectively, that is, by

$[\underline s,\overline b]$

, respectively, that is, by

$$\begin{align*}\hat{G}_B(b) = \frac{1}{n}\sum_{i=1}^n \mathbb{1} (B_i\leq b),\quad \hat{G}_S(s) = \frac{1}{n}\sum_{i=1}^n \mathbb{1}(S_i\leq s), \end{align*}$$

$$\begin{align*}\hat{G}_B(b) = \frac{1}{n}\sum_{i=1}^n \mathbb{1} (B_i\leq b),\quad \hat{G}_S(s) = \frac{1}{n}\sum_{i=1}^n \mathbb{1}(S_i\leq s), \end{align*}$$

and local quadratic density estimators

$\hat {g}_B(b)$

and

$\hat {g}_B(b)$

and

$\hat {g}_S(s)$

for all

$\hat {g}_S(s)$

for all

$b,s\in [\underline s,\overline b]$

. Specifically, the estimator of the buyer bid density

$b,s\in [\underline s,\overline b]$

. Specifically, the estimator of the buyer bid density

$\hat {g}_B$

is defined as followsFootnote

18

:

$\hat {g}_B$

is defined as followsFootnote

18

:

$$ \begin{align} \hat g_B(b) = \frac{n_B^{+}}{n}\cdot \hat g_B^{+}(b),\quad b\in [\underline s,\overline b], \end{align} $$

$$ \begin{align} \hat g_B(b) = \frac{n_B^{+}}{n}\cdot \hat g_B^{+}(b),\quad b\in [\underline s,\overline b], \end{align} $$

where

$\hat g_{B}^{+}(\cdot )$

is a local quadratic density estimator using a kernel function of

$\hat g_{B}^{+}(\cdot )$

is a local quadratic density estimator using a kernel function of

$K_B$

and a bandwidth of

$K_B$

and a bandwidth of

$h_B$

from a subsample

$h_B$

from a subsample

$\{B_i: B_i> \hat {\underline s} \}$

(with a size of

$\{B_i: B_i> \hat {\underline s} \}$

(with a size of

$n_B^{+}$

). Following Cattaneo et al. (Reference Cattaneo, Jansson and Ma2020), for a given random sample of

$n_B^{+}$

). Following Cattaneo et al. (Reference Cattaneo, Jansson and Ma2020), for a given random sample of

$\{Z_1,Z_2,\dots ,Z_m\}$

from a distribution with a density of

$\{Z_1,Z_2,\dots ,Z_m\}$

from a distribution with a density of

$g_Z(\cdot )$

on

$g_Z(\cdot )$

on

$[\underline z,\overline z]$

, the boundary-adaptive local polynomial density estimator (with a polynomial of order p) is defined as

$[\underline z,\overline z]$

, the boundary-adaptive local polynomial density estimator (with a polynomial of order p) is defined as

$\hat g_Z(z) = \hat {\theta }_2(z),$

where

$\hat g_Z(z) = \hat {\theta }_2(z),$

where

$\hat \theta (z) = \text {argmin}_{\theta \in \mathbb {R}^{p+1}} \sum _{i=1}^m \big [ \hat {G}_Z(Z_i) - \theta _1 - \theta _2\cdot (Z_i-z) - \dots - \theta _{p+1}\cdot (Z_i-z)^p \big ]^2\cdot K\big ((Z_i-z)/h\big )$

with

$\hat \theta (z) = \text {argmin}_{\theta \in \mathbb {R}^{p+1}} \sum _{i=1}^m \big [ \hat {G}_Z(Z_i) - \theta _1 - \theta _2\cdot (Z_i-z) - \dots - \theta _{p+1}\cdot (Z_i-z)^p \big ]^2\cdot K\big ((Z_i-z)/h\big )$

with

$\hat G_Z(z) = (1/m)\sum _{i=1}^m \mathbf {1} (Z_i\leq z)$

,

$\hat G_Z(z) = (1/m)\sum _{i=1}^m \mathbf {1} (Z_i\leq z)$

,

$K(\cdot )$

being a kernel function, and h being a bandwidth. Similarly, we can define the seller bid density estimator

$K(\cdot )$

being a kernel function, and h being a bandwidth. Similarly, we can define the seller bid density estimator

$\hat g_S$

with a cutoff of

$\hat g_S$

with a cutoff of

$\hat {\overline b}$

(instead of

$\hat {\overline b}$

(instead of

$\hat {\underline s}$

) to split the sample, a kernel function of

$\hat {\underline s}$

) to split the sample, a kernel function of

$K_S$

and a bandwidth of

$K_S$

and a bandwidth of

$h_S$

, namely,

$h_S$

, namely,

$$ \begin{align} \hat g_S(s) = \frac{n_S^{-}}{n}\cdot \hat g_S^{-}(s),\quad s\in [\underline s,\overline b], \end{align} $$

$$ \begin{align} \hat g_S(s) = \frac{n_S^{-}}{n}\cdot \hat g_S^{-}(s),\quad s\in [\underline s,\overline b], \end{align} $$

where

$\hat g_{S}^{-}(\cdot )$

is a local quadratic density estimator from a subsample

$\hat g_{S}^{-}(\cdot )$

is a local quadratic density estimator from a subsample

$\{S_i: S_i \leq \hat {\overline b} \}$

(with a size of

$\{S_i: S_i \leq \hat {\overline b} \}$

(with a size of

$n_S^{-}$

).

$n_S^{-}$

).

Our bid density estimators

$\hat g_B$

and

$\hat g_B$

and

$\hat g_S$

, respectively, involve

$\hat g_S$

, respectively, involve

$\hat g_B^+$

and

$\hat g_B^+$

and

$\hat g_S^-$

which are based on the local quadratic approach (i.e.,

$\hat g_S^-$

which are based on the local quadratic approach (i.e.,

$p=2$

).Footnote

19

Local quadratic density estimator (with a bandwidth of h) is boundary adaptive and achieves a uniform rate of

$p=2$

).Footnote

19

Local quadratic density estimator (with a bandwidth of h) is boundary adaptive and achieves a uniform rate of

$O(h^2)$

while the kernel density estimator (with a bandwidth of h) based on boundary kernel method (e.g., the one discussed in Chapter 1 of Li and Racine, Reference Li and Racine2007) can only achieve a uniform rate of

$O(h^2)$

while the kernel density estimator (with a bandwidth of h) based on boundary kernel method (e.g., the one discussed in Chapter 1 of Li and Racine, Reference Li and Racine2007) can only achieve a uniform rate of

$O(h)$

, because the bias of local quadratic method has a rate of

$O(h)$

, because the bias of local quadratic method has a rate of

$O(h^2)$

at both the interior and (near) boundary points while the boundary kernel method has a rate of

$O(h^2)$

at both the interior and (near) boundary points while the boundary kernel method has a rate of

$O(h)$

at the (near) boundary points (and a rate of

$O(h)$

at the (near) boundary points (and a rate of

$O(h^2)$

in the interior).

$O(h^2)$

in the interior).

We then define the buyer’s pseudo private value

$\hat V_i$

corresponding to

$\hat V_i$

corresponding to

$B_i$

and the seller’s pseudo private value

$B_i$

and the seller’s pseudo private value

$\hat C_i$

corresponding to

$\hat C_i$

corresponding to

$S_i$

, respectively, as

$S_i$

, respectively, as

$$ \begin{align} \hat{V}_i &= \begin{cases} B_i + k\dfrac{\hat{G}_S(B_i)}{\hat{g}_S(B_i)} & \text{if } B_i\geq\hat{\underline{s}},\\ B_i & \text{otherwise}, \end{cases}\quad \hat{C}_i = \begin{cases} S_i - (1-k)\dfrac{1-\hat{G}_B(S_i)}{\hat{g}_B(S_i)} & \text{if } S_i\leq\hat{\overline{b}},\\ S_i & \text{otherwise}, \end{cases} \end{align} $$

$$ \begin{align} \hat{V}_i &= \begin{cases} B_i + k\dfrac{\hat{G}_S(B_i)}{\hat{g}_S(B_i)} & \text{if } B_i\geq\hat{\underline{s}},\\ B_i & \text{otherwise}, \end{cases}\quad \hat{C}_i = \begin{cases} S_i - (1-k)\dfrac{1-\hat{G}_B(S_i)}{\hat{g}_B(S_i)} & \text{if } S_i\leq\hat{\overline{b}},\\ S_i & \text{otherwise}, \end{cases} \end{align} $$

where

$\hat {G}_B(\mkern 2mu\cdot \mkern 2mu),\hat {G}_S(\mkern 2mu\cdot \mkern 2mu),\hat {g}_B(\mkern 2mu\cdot \mkern 2mu)$

, and

$\hat {G}_B(\mkern 2mu\cdot \mkern 2mu),\hat {G}_S(\mkern 2mu\cdot \mkern 2mu),\hat {g}_B(\mkern 2mu\cdot \mkern 2mu)$

, and

$\hat {g}_S(\mkern 2mu\cdot \mkern 2mu)$

are the empirical distribution functions and bias-corrected local quadratic density estimators defined earlier.Footnote

20

Note that we have

$\hat {g}_S(\mkern 2mu\cdot \mkern 2mu)$

are the empirical distribution functions and bias-corrected local quadratic density estimators defined earlier.Footnote

20

Note that we have

$V_i = B_i$

(resp.

$V_i = B_i$

(resp.

$C_i = S_i$

) when

$C_i = S_i$

) when

$B_i < \underline {s}$

(resp.

$B_i < \underline {s}$

(resp.

$S_i> \overline {b}$

) in regular equilibrium.

$S_i> \overline {b}$

) in regular equilibrium.

In the second step, we use the pseudo private value samples,

$\{\hat {V}_1,\ldots ,\hat {V}_n\}$

and

$\{\hat {V}_1,\ldots ,\hat {V}_n\}$

and

$\{\hat {C}_1,\ldots ,\hat {C}_n\}$

, to estimate the buyers’ and sellers’ respective value densities. Specifically, the estimator of the buyer value density

$\{\hat {C}_1,\ldots ,\hat {C}_n\}$

, to estimate the buyers’ and sellers’ respective value densities. Specifically, the estimator of the buyer value density

$\hat {f}_V$

is obtained by applying the local linear approach (as described previously with

$\hat {f}_V$

is obtained by applying the local linear approach (as described previously with

$p=1$

) to the sample of the buyers’ pseudo private values on

$p=1$

) to the sample of the buyers’ pseudo private values on

$[\hat {\underline {v}},\hat {\overline {v}}]$

, where

$[\hat {\underline {v}},\hat {\overline {v}}]$

, where

$\hat {\underline {v}}$

and

$\hat {\underline {v}}$

and

$\hat {\overline {v}}$

are, respectively, the minimum and maximum of the buyers’ pseudo private values, with kernel function

$\hat {\overline {v}}$

are, respectively, the minimum and maximum of the buyers’ pseudo private values, with kernel function

$K_V$

and bandwidth

$K_V$

and bandwidth

$h_V$

. Similarly, we get the estimator of the sellers’ value density

$h_V$

. Similarly, we get the estimator of the sellers’ value density

$\hat {f}_C$

on interval

$\hat {f}_C$

on interval

$[\hat {\underline {c}},\hat {\overline {c}}]$

by the sample of the sellers’ pseudo private values with kernel function

$[\hat {\underline {c}},\hat {\overline {c}}]$

by the sample of the sellers’ pseudo private values with kernel function

$K_C$

, and bandwidth

$K_C$

, and bandwidth

$h_C$

.Footnote

21

$h_C$

.Footnote

21

Remark 1: Our bid density estimators

$\hat {g}_B$

and

$\hat {g}_B$

and

$\hat {g}_S$

do not include boundaries in their definitions. Our bid density estimator

$\hat {g}_S$

do not include boundaries in their definitions. Our bid density estimator

$\hat g_B(\cdot )$

(resp.

$\hat g_B(\cdot )$

(resp.

$\hat g_S(\cdot )$

) achieves an asymptotic uniform rate of

$\hat g_S(\cdot )$

) achieves an asymptotic uniform rate of

$O_p\big (h_B^2+\sqrt {log(n)/(nh_B)}\big )$

(resp.

$O_p\big (h_B^2+\sqrt {log(n)/(nh_B)}\big )$

(resp.

$O_p\big (h_S^2+\sqrt {log(n)/(nh_S)}\big )$

) on the interval of

$O_p\big (h_S^2+\sqrt {log(n)/(nh_S)}\big )$

) on the interval of

$[\underline s,\overline b]$

. Note that in our two-step estimation procedure, we only need to estimate

$[\underline s,\overline b]$

. Note that in our two-step estimation procedure, we only need to estimate

$g_B(\cdot )$

and

$g_B(\cdot )$

and

$g_S(\cdot )$

, respectively, by

$g_S(\cdot )$

, respectively, by

$\hat g_B(\cdot )$

and

$\hat g_B(\cdot )$

and

$\hat g_S(\cdot )$

in the interval of

$\hat g_S(\cdot )$

in the interval of

$[\underline s,\overline b]$

.

$[\underline s,\overline b]$

.

4.2 Asymptotic Properties

The next assumption concerns the process of generating the private values of buyers and sellers

$(V_i,C_i), i=1,\dots ,n$

.

$(V_i,C_i), i=1,\dots ,n$

.

Assumption E.

$V_i$

,

$V_i$

,

$i=1,2,\ldots ,n$

, are independently and identically distributed as

$i=1,2,\ldots ,n$

, are independently and identically distributed as

$F_V$

with density

$F_V$

with density

$f_V$

;

$f_V$

;

$C_i$

,

$C_i$

,

$i=1,2,\ldots ,n$

, are independently and identically distributed as

$i=1,2,\ldots ,n$

, are independently and identically distributed as

$F_C$

with density

$F_C$

with density

$f_C$

.

$f_C$

.

This assumes that the bidders’ private values are independent across auctions.

We turn to the choice of kernels in the following assumption.

Assumption F.

$K_B, K_S, K_V$

, and

$K_B, K_S, K_V$

, and

$K_C$