In 1954, F. D. Wharton applied for a Federal Housing Administration (FHA)-insured loan. These affordable arrangements, along with similarly generous loans guaranteed by the Veterans Administration (VA), both guarded lenders against loss and facilitated profits for suburban developers who secured financing through them. By means of this market intervention, the federal government stimulated mass-produced housing after World War II, simultaneously driving mortgage interest rates lower on longer borrowing intervals while reducing down payments, and thereby placed homeownership within reach of numerous white, working-class families that, just a generation before, could not have contemplated purchasing brand-new single-family homes. However, Wharton was Black, and similar to many African Americans, he encountered difficulties accessing this government-backed loan type. However, rather than capitulating, Wharton utilized his knowledge of how the mortgage market worked, information about a seemingly promising new federal initiative, and his personal connection to the North Carolina Mutual Life Insurance Company, a Black-owned firm, in attempting to secure the loan he felt he deserved. Perhaps Wharton was emboldened by the US Supreme Court’s landmark Brown v. Board of Education ruling earlier that year as well, sensing that the federal government was pivoting toward greater support for African American civil rights.Footnote 1

A resident of Tarboro, North Carolina—a mid-sized town east of Raleigh—Wharton first penned a complaint to a large, New York-based life insurance company. “Very recently,” he explained, “a builder who claims to be getting Metropolitan Life Insurance Company money for FHA loans on the individual homes he is constructing, stated that the company’s policy is not to make loans on homes for Negroes.” Wharton thereby demonstrated some understanding of the secondary mortgage market, where large institutional investors such as life insurance companies and mutual savings banks bought home loans as long-term assets. By so doing, they freed up smaller, short-term mortgage “originators”—who lent directly to consumers—to re-lend their funds for additional home purchases. Wharton rejected the builder’s explanation that Black borrowers were credit risks, relating three local instances he felt illustrated the unfair and arbitrary basis on which loan decisions were being made. In the first case, a “principal of a four-teacher school in another county” somehow obtained FHA-backed financing for his home to be built “outside the city limits on an unimproved street” lacking water and sewer service. In contrast to this Black applicant, a second had been denied a FHA-insured loan, despite being a master’s-degree-holding “principal of [a] thirteen teacher consolidated high school in this county” who planned to build just outside the town’s main business district. Wharton called this area Tarboro’s “most desirable section,” noting it contained “some of the largest and best homes among Negroes in town.” While the first applicant’s wife did not hold a job, the second’s was “a college graduate and teaches in the same school with her husband.” The third case involved four applicants: “an older man and wife, daughter and son-in-law,” who were likewise denied FHA support for the house they wanted to build on a lot adjoining that of the second applicant. Wharton extolled these applicants’ qualifications, claiming, “The father has a most excellent record as a leader and is known throughout the state and in several others.”Footnote 2

Strategically, Wharton did not divulge that he was the father from the third example, nor that the second applicant was his son-in-law.Footnote 3 Wharton’s claims regarding the father (in actuality, himself) do not seem exaggerated; a self-employed businessman, he had only recently retired from his long career as an agent with the historically-Black North Carolina Agricultural & Technical College’s extension service. “Negroes in the state own millions of dollars[’] worth of homes and other real estate,” Wharton informed Metropolitan Life, noting that “the property purchased was not on terms as liberal as FHA loans.” Days later, Wharton sought redress from the FHA, asking, “I am wondering if it is possible for your administration to, in some way, give some needed assistance to minority groups, especially Negroes who wish to take advantage of FHA financing?” “It appears that [FHA] loans are more apt to be considered, locally, for second rate borrowers, on third rate property than on first rate applicants with first rate home sites,” he observed, adding, “No doubt that much of this is a local matter but we do feel that it could be improved upon by those in authority.”Footnote 4

The Eisenhower administration had in fact introduced a new initiative to improve racial minorities’ access to FHA- and VA-backed credit, as well as increase the flow of mortgage monies to underserved areas of the country more generally: the Voluntary Home Mortgage Credit Program (VHMCP), established as a provision of the 1954 Housing Act. The program connected interested borrowers with willing lenders, and was administered through the Housing and Home Finance Agency that oversaw the FHA. Responding to Wharton, the FHA’s Acting Regional Director urged him to seek VHMCP assistance.Footnote 5 Wharton then reached out to Asa T. Spaulding of the North Carolina Mutual Life Insurance Company, who served on North Carolina’s regional VHMCP subcommittee as one of some dozen Black members appointed to such positions nationwide. Vice president of the country’s largest African American-owned insurance company—headquartered on Durham, North Carolina’s “Black Wall Street”—Spaulding would soon be appointed the only African American member of the VHMCP’s national board, a position he retained until the program’s discontinuation in 1965. Wharton congratulated Spaulding on his appointment, then requested Spaulding’s help in obtaining his desired FHA loan—while adding a personal touch that he had been “very well acquainted” with Spaulding’s cousin, North Carolina Mutual’s recently deceased longtime president. In response, Spaulding reassured Wharton that “I believe our committee will be able to do much to help alleviate the conditions complained of.”Footnote 6

Although Wharton was subsequently approved by the FHA, it is unclear whether he ultimately got his loan. A Metropolitan Life supervisor wrote him back to deny the company’s mortgage investment policy was in any way discriminatory; in fact, Metropolitan had “bought quite a few loans on negro properties” from a bank in nearby Wilson, which the supervisor strongly recommended. That bank’s vice president subsequently encouraged Wharton to apply for a loan, after personally inspecting his landholdings. Soon thereafter, Wharton was approached by a white builder who had erected houses for Black buyers in the area, although in Wharton’s assessment, “not of first class material and the locations from poor to bad.” Although this builder typically built in the $3,200 to $4,500 range—between $38,000 and $54,000 in today’s dollars—he assured Wharton he “could build a $5000.00 to $6000.00 house that would meet FHA approval.” Nevertheless, the exchange reinforced Wharton’s suspicion that whites assumed Black borrowers could only afford lower-priced homes of lesser quality, appropriately sited in locations conforming to the racial status quo.Footnote 7 Six months later, Wharton’s FHA paperwork had cleared; however, the bank then sat on it for nearly a month, necessitating a follow-up visit by Wharton. After two more weeks of delays, Wharton wrote Spaulding in frustration, asking, “Do I have to wait all this time on them? Is there nothing I can do? I have been thinking of writing the Metropolitan Life Insurance office again but did not wish to seem to be breaking faith with or doubting its officials in Wilson, [although] actually I do.” In the end, the loan may have gone through, after Spaulding promised to involve someone he knew in Metropolitan’s New York office.Footnote 8

For decades, middle-class African Americans like F. D. Wharton had struggled to get mortgage financing in the face of lender discrimination, long before the federal government’s belated turn to legitimize their pursuit of the American Dream. And it was by no coincidence that Wharton reached out to North Carolina Mutual, because Black-owned insurance companies were among the few reliable financial streams available to support Black homeownership from the early twentieth century onward. As Harry H. Pace, president of the Chicago-based Supreme Liberty Life Insurance Company had put it in 1934: “One thing stands out and has stood out in the insurance business as it is conducted by our people, and that is that we were organized largely in the beginning to furnish … a place where they could go to get mortgage money.”Footnote 9 Business historians have profiled individual African American insurance companies, and the industry’s unmatched significance as a source of white-collar jobs has long been recognized.Footnote 10 However, scant attention has been devoted to these companies’ investment strategies, and their role in facilitating Black homeownership through involvement in mortgage markets.Footnote 11 The current article addresses this oversight by tracing the two largest African American life insurance companies’ post-World War II experiences investing in mortgages, amid the federal government’s insistent promotion of home loans backstopped by the FHA and VA. It further evaluates the barely studied VHMCP, detailing its ineffectiveness at increasing Black homeownership.

Black-owned firms represented only a tiny fraction of an industry dominated by white-controlled behemoths such as Metropolitan Life; however, they behaved similarly, pooling their policyholders’ premiums into substantial reserves of capital for investment in safe, reliable securities.Footnote 12 As state and federal regulations loosened around the turn of the twentieth century, mortgage loans, whether on farms, commercial buildings, or homes, became increasingly attractive investments, due to their generally favorable rates of return relative to other comparatively safe investment vehicles such as bonds. Mortgages, as protracted debt contracts with set repayment schedules, provide their holders with a steady stream of income so long as borrowers remain financially solvent. Prior to World War I, governmental involvement in mortgage lending was confined to setting regulatory guidelines.Footnote 13 Nor did any formalized secondary market yet exist. Larger life insurance companies relied on mortgage companies to “originate” (initiate) the loans they purchased and “service” (collect payments on) them, whereas smaller life firms including Black-owned ones typically extended mortgages to individual borrowers and managed their loans themselves.Footnote 14

However, periodic economic downturns revealed that despite their relative safety, mortgages still carried risks. Indeed, the strict terms of pre-1930s mortgage contracts recognized the possibility of loss—being short-term, 2–5 years in duration, and also unamortized with payments going entirely toward the loan’s interest, the principal being due at the end of term. While borrowers paid extra to reduce the balance and normally could renew a mortgage upon expiration, lenders were empowered to regularly reconsider their investment. In 1896, life insurance companies had held 6% of the $2.7 billion in residential mortgage debt; after a frenzy of mortgage lending that accompanied the 1920s construction boom, their share rose to 10% of the now $27.6 billion total, only to end with staggering losses when the Great Depression hit.Footnote 15 Black-owned insurance companies had followed the general trend in more prosperous times, and similar to their larger counterparts, learned to be warier thereafter. The New Deal’s subsequent interventions in the housing market encouraged amortization, dramatically extended repayment intervals, and lowered interest rates—thereby reducing mortgage risk for homeowners and investors alike. As their coffers refilled during World War II, and postwar suburbanization took off with new federal protections against loss, life insurance companies waxed optimistic and reentered the mortgage market. However, considering segregation, racial discrimination, and unequal access—enabled to some extent by the federal government itself—the results were predictably mixed. Black life insurance companies continued to be disadvantaged in the changed postwar environment for two longstanding reasons: information asymmetries due to a dearth of financial intermediaries able to advise their investment decisions, and the structural inequalities African Americans faced more generally, which induced greater investment risks.

Black-Owned Insurance Companies through World War II

While African Americans’ involvement in insurance-related endeavors can be traced to the founding of the Free African Society in Philadelphia in 1778, it was really only after the Civil War that Black-owned insurance companies (and other forms of mutual aid) gained prominence amid the general explosion of organizational life at the time. With many among them impoverished, African Americans turned to each other and pooled their resources in search of protection against the vagaries of life, facing social rejection from whites and increasingly motivated by stirrings of race pride. Mainstream insurance companies discriminated against Black people, overcharging or outright refusing to cover them. In fact, it was the Prudential and Metropolitan life insurance companies’ 1881 decision to unilaterally raise premiums on Black policyholders that two years later spurred in Richmond, Virginia the founding of the first modern Black-owned insurance venture, the Grand Fountain of the United Order of True Reformers.Footnote 16 Early Black-owned insurance companies—like other African American entrepreneurship in cosmetics, funerary services, or newspapers—thus filled economic niches by specializing in goods and services that white society declined to provide. In these early decades, the most widespread form of life insurance among African Americans was low-cost, “industrial” policies with premiums collected door-to-door on a weekly or monthly basis, and paid out in the event of sickness, injury, or death to provide a modicum of security and dignity in the face of all-too-common tragedy.Footnote 17

However, Black-owned insurance companies represented a miniscule portion of the overall industry, with assets that paled in comparison with the largest white-owned firms. Due to increasing state regulation, it took African Americans until 1893 to found their first “legal reserve” life company—one certified as meeting the minimum of funds to cover its fiduciary obligations to policyholders. Nevertheless, the industry’s growth continued, with its two largest companies sinking roots during this era: the North Carolina Mutual Life Insurance Company (founded 1898) and the Atlanta Life Insurance Company (founded 1905). Through mergers and stock issuances, both transitioned from selling industrial premiums to becoming legal reserve companies with multi-state operations by 1913 and 1922, respectively. Black firms on the whole were successful enough to form the National Negro Insurance Association in 1921. The 1920s were particularly prosperous for such companies—following the generally strong economy of that decade, and with growth rates that actually exceeded those of white firms. In 1920, the number of Black-owned legal reserve companies stood at 6, increasing further to 15 by 1930. In Los Angeles, the Golden State Mutual Life Insurance Company used a community-based campaign to raise capital for its guaranty fund in 1925, in the process surmounting the California legislature’s tightening of requirements in an attempt to foil their efforts. Even in this era of rampant discrimination, however, white-owned firms carried vastly more coverage on African American lives, underlining just how small the Black-controlled segment of the market actually was. Whereas Metropolitan held policies amounting to $900 million just on its Black customers in 1927, the combined insurance coverage underwritten by the top 32 African American-owned firms that same year was only $316 million.Footnote 18

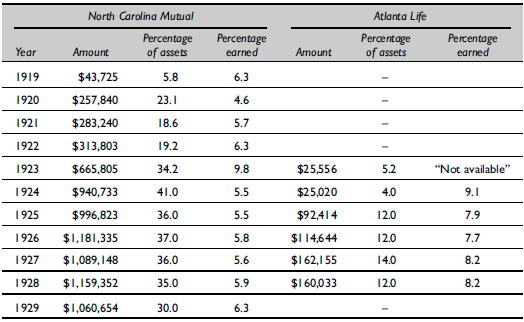

Similar to all life insurance companies, Black-owned ones sought outlets for capital generated by their policyholders’ premiums, and the relative profitability and seeming safety of mortgages made these a logical investment choice amid the 1920s real estate boom.Footnote 19 African American homeownership rose to approximately 25%—in keeping with the decade’s general trend, although with a significant gap relative to the white rate which approached one half.Footnote 20 Because racism made it so difficult for African Americans to secure home financing, insurance companies, along with the small number of Black-owned savings banks and savings and loan associations (“thrifts”), served as lifelines to the fortunate few.Footnote 21 Black life insurance companies increased their residential mortgage holdings along with the general industry trend, although with significant variation in terms of the relative portion that individual firms invested in these securities. The two industry leaders pursued strikingly different approaches, with North Carolina Mutual investing far more heavily in mortgages than Atlanta Life (see Table 1). In 1924, North Carolina Mutual took out a full-page advertisement in the National Association for the Advancement of Colored People (NAACP)’s magazine The Crisis, trumpeting its “$850,000 In Mortgage Loans” and declaring itself to be “primarily a SERVICE ORGANIZATION.” Judging by a spreadsheet listing 75 past due mortgage loans held by North Carolina Mutual in the late 1920s, the company was still making loans overwhelmingly on the local level, with just 6 issued to out-of-state mortgagors. All but three were made to individuals—although similar to its rival Atlanta Life, North Carolina Mutual also extended mortgages to Black churches, underlining these enterprises’ community-minded ethos.Footnote 22 On the eve of the 1929 Crash, North Carolina Mutual was sanguine enough about business prospects to form the Mortgage Company of Durham, as a sort of financial clearinghouse for aspiring Black homeowners.Footnote 23

Mortgages Held by North Carolina Mutual and Atlanta Life, 1919–1929

Source: Best’s Life Insurance Reports (New York), 1920–1930. Since Best’s reported only on legal reserve companies, Atlanta Life was not listed prior to achieving that status in 1922, and for 1929, its “statement had not been received when this portion of the volume went to press.”

But just like it did for mainstream, white-run life companies, the Great Depression delivered a sobering jolt to the previous decade’s optimism. While job loss made it difficult for all mortgagors to pay—and deflation made their debts even more burdensome—these problems were compounded for African Americans who faced higher unemployment. As these difficulties got passed along to their creditors, Black insurance companies experienced financial losses, and some outright failed.Footnote 24 Indeed, the very reputation of mortgages as safe investments was severely damaged. Responding to a mortgage-seeking Alabama policyholder in early 1932, Atlanta Life explained that “due to the present economic depression, we have been out of the loan market,” while offering hopes that “some Negro Corporation there in Alabama … can handle the matter for you.” With collections on its existing loans increasingly difficult, the company subsequently declared it was foregoing investment in real estate, a policy that remained in effect as late as 1939.Footnote 25 Meanwhile, Atlanta Life and other Black firms adapted by granting borrowers forbearance, reducing interest charges, and implementing amortization payments. Similar to its white counterparts, Atlanta Life unloaded as many delinquent mortgages as possible onto the federal government.Footnote 26 Nor was the company yet participating in the long-distance secondary market, judging by its response to an inquiry from a town in Georgia’s far southwest: “We regret to inform you that such loans as are made by this Company are confined to Atlanta where appraisal can be made personally by our Loan Committee.” Atlanta Life would maintain its cautious stance even as the market improved after 1935, politely declining offers of FHA-insured Title II mortgages from realtors and correspondents with mortgage companies and thrifts as far afield as New York, Florida, Texas, and Indiana.Footnote 27 Operating within a less-developed Black financial sector, life insurance companies often had to do their own analysis, having few trustworthy financial intermediaries to turn to for reliable investment advice.Footnote 28 And although Atlanta Life had not invested in mortgages as aggressively as some other Black-owned companies, more than $100,000 in Depression-related foreclosures remained on its ledgers until the 1970s.Footnote 29

A study of African American life insurance companies’ investments from the Depression into the early postwar period further reveals they invested less in mortgages and bonds than white-controlled firms, and more in real estate and stocks while maintaining larger portions of cash on hand. Even so, the study observed, “A considerable number of mortgage loans had been made on property habitated [sic] by Negro persons,” an apparent reference to mortgages these companies had originated directly to their own policyholders before World War II.Footnote 30 Again underlining their community-mindedness, African American life insurance companies tended to purchase stock in Black-owned banks, thrifts, and insurance companies, as well as bonds issued by Black churches and schools. Across the board, the seven companies studied had seen foreclosure-related losses on real estate and mortgages, but profits on stocks and bonds during the period under study. In 1930, the mainstream life insurance industry held an average of 40% of its assets in mortgages as compared with just 20% among Black-owned life companies. However, by 1945 mainstream companies had reduced their holdings to just 15%, whereas Black-owned companies’ portion still stood at 14%. Even prior to the Crash, widespread assumptions held that “The most formidable stumbling-block in the way of home owning by Negroes is the unsaleability of their mortgages. Except in a limited field these loans have no market.”Footnote 31 By 1944 some Black-owned financial institutions were proving “difficult to interest” in mortgages, due to higher returns available elsewhere. In fact, the FHA, which was just contemplating an approach to Black life insurance companies, noted these firms’ “reticence” regarding federally insured mortgages and “apparent apathy” toward its “Negro Housing” projects. Only 9 of the National Negro Insurance Association’s 45 members had registered as FHA-approved mortgagees by that point.Footnote 32

Not all Black-owned insurance companies felt as burned as Atlanta Life by their Depression-era experience, however. In 1938, North Carolina Mutual’s subsidiary the Mortgage Company of Durham was still making loans nearly a decade after its founding, and the following year its parent company enthused about building houses for Black buyers on land it owned using another affiliated firm, the Home Development Company. Yet this reliance on self-created subsidiaries underlines the disadvantage Black firms faced: to the extent that mainstream white brokers, underwriters, realtors, or developers were interested in the African American housing market, they could not be trusted to convey good information about profitable, low-risk investment opportunities. As Black wartime earnings picked up, the company sold off hundreds of its vacant lots in Durham and elsewhere around the state; North Carolina Mutual additionally reduced the proportion of its mortgage holdings from 41% in 1942 to just 23% in 1944.Footnote 33 Similarly, the Metropolitan Funeral System Association—precursor to the Chicago Metropolitan Assurance Company—ramped up its mortgage lending amid the wartime housing shortage, its holdings exploding from just $6,000 in 1938, to some $281,000 by 1945. During the Depression and war, Black-owned firms felt a continuing obligation to lend to community members in need of financing, but many lacked familiarity with the premium industrial bonds favored by large white-owned firms; hence they invested in mortgages, real estate, and government bonds in hopes of treading water. Most Black-owned insurance companies survived the Depression, with 19 legal reserve companies by 1940, and 24 by 1945. In fact, starting in 1940, the assets of Black-owned insurance companies began to increase by 18% per annum, compared with the overall industry’s growth rate, which averaged 7.5%. Furthermore, despite reducing their mortgage investments and shifting toward war bonds during the conflict, Black-owned insurance companies saw yields on their mortgages rise to 5.2% by 1945, compared with just 2.5% for bonds. Thus North Carolina Mutual and indeed the Black insurance industry on the whole could face the postwar period with cautious optimism—but little chance of competing forcefully and nationally beyond their already-established niche markets.Footnote 34

Black-Owned Insurance Companies in the Postwar Housing and Mortgage Markets

The economy’s reconversion to consumer-oriented production, and the pent-up wartime savings of Black and white Americans alike, brought some hope that postwar prosperity—including homeownership—might be distributed more equitably. Wartime fair employment policy further raised hopes, and the Truman Administration’s rhetoric supporting racial fairness partially offset the unfolding Red Scare that would quickly shatter the left-led, interracial pro-civil rights coalition from the Depression and war years. By helping to institutionalize the long-term, low-interest, self-amortizing mortgage, the federal government’s New Deal reforms now stood to both increase homeowning access and reassure lenders about the safety of their investments. However, evidence had already come to light that the Federal Housing Administration’s (FHA) programs, in particular, were being administered on a racially unequal basis.Footnote 35 Meanwhile, legal challenges to racist deed restrictions and covenants were winding their way through the courts, culminating in the Supreme Court’s landmark Shelley v. Kraemer (1948) decision that deemed these legal devices unenforceable; ever since its debut in 1934, the FHA had encouraged such restrictions to maintain supposed white neighborhood “stability.”Footnote 36 African Americans and particularly the aspiring Black middle class, then, stood at an uncertain crossroads; the Black-owned insurance companies holding their policies likewise confronted the postwar landscape with questions about how to help facilitate Black homeownership while pursuing profitable investment strategies.

More generally, the life insurance industry pivoted to reinvest in mortgages during the Truman years, particularly FHA-insured mortgages and those guaranteed by the Veterans Administration (VA) through the 1944 G.I. Bill (Servicemen’s Readjustment Act). With increased policy sales as the postwar “baby boom” took off, these companies liquidated their government securities to meet increasing demand for mortgage credit among other lucrative investment opportunities. Establishing relationships with a new, postwar crop of mortgage companies, large life firms relied on such “correspondents” to originate and service the loans going into their portfolios, in exchange for a small fee. In this pre-securitization era, large insurers would typically buy up all acceptable loans on offer until reaching their investment quota for a given quarter or year (known as making “advance commitments”). They also preferred sizeable single-family residential projects or apartment complexes, especially during the 1946–1950 interval when FHA’s overly generous Section 608 program incentivizing multifamily construction remained in effect. Prioritizing large projects kept administrative costs down, while the shift toward regular, self-amortizing payments additionally reassured lenders. By the end of Truman’s term, residential mortgages comprised fully 77% of mainstream life insurers’ nonfarm holdings. With the inflow of policyholders’ premiums lowering their costs of acquiring money, life insurance companies soon reclaimed their place as the largest players on the secondary mortgage market. Even so, they were increasingly joined by other institutional actors such as mutual savings banks, commercial banks, and pension and trust funds, which also entered the field.Footnote 37

In a dramatic shift, and even as they maintained more than half their holdings in higher-interest, “conventional” (uninsured) loans, life insurance companies in the immediate postwar era ramped up their purchases of FHA-insured, and to a lesser extent VA-guaranteed, mortgages. Not only were these investments protected by the government, but mainstream life companies, due to their large size and lower money costs, were also better positioned to turn profits on such low-interest debt instruments, at least until the Federal Reserve raised interest rates to counter inflation. Furthermore, life firms could now buy and sell FHA–VA mortgages when market conditions were optimal through the intermediary of the Federal National Mortgage Association (“Fannie Mae”).Footnote 38 While the market for conventional loans continued to be larger, about half of all home loans had either FHA or VA backing by 1948, up from just a fifth in 1940. Some 500 institutions, many of them insurance companies, held FHA loan portfolios valued at more than $1 million by 1950, together accounting for 70% of all FHA-insured mortgages; more than 8,500 small mortgagees constituted the remainder, most of them owning FHA loan portfolios of less than $100,000. In addition, even after a 1951 change in monetary policy made these low-interest investments less attractive, many life companies honored their previous commitments to purchase FHA- and VA-backed mortgages. One analysis summarized the situation: “[I]nsured and guaranteed loans provide insurance companies with protection which they previously did not have and also permits them to move their funds more expediently throughout the nation.”Footnote 39

Life insurance companies thus supplied substantial capital for postwar suburbanization, which further advantaged white prospective homeowners over Black. During this era, federal housing agencies continued to discriminate and to countenance discriminatory practices by private industry, thereby earning vocal condemnations as early as 1948 from civil rights advocates like Robert Weaver, one of a mere handful of African Americans with New Deal policymaking experience.Footnote 40 In the aftermath of the Shelley ruling, the FHA ceased requiring racial restrictions and removed explicitly racist language from its Underwriting Manual. However, into the 1960s, the agency continued to utilize redlining for its mortgage insurance determinations, provide mortgage insurance to developers who discriminated, and promote segregated “minority housing” developments in marginal locations. Thus despite an increased sensitivity to the issue of racial discrimination in housing, the FHA and VA themselves discriminated and did essentially nothing to compel lenders to extend financing, or developers to build housing for African Americans on an equal footing.Footnote 41 By 1960, the FHA had insured more than $67 billion in home loans, while the VA had guaranteed around $50 billion’s worth. Yet of the 6 million single-family homes with FHA-insured mortgages, only some 108,000—comprising about 2%—were occupied by people of color; of the nearly 3 million with VA guarantees, around 87,000 were nonwhite-occupied, approximately 3% of the total.Footnote 42 Perhaps ironically, the FHA and VA had together backed some 40% of the new housing built for African Americans during the 1950s—much of it Section 608-financed apartment buildings. Meanwhile, FHA- and VA-backed loans on single-family homes often remained out of reach for aspiring Black buyers like F. D. Wharton.Footnote 43

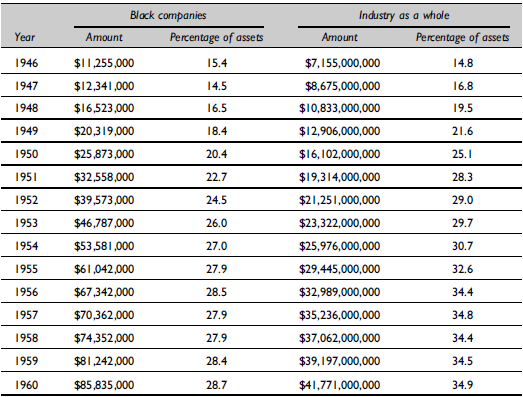

Considering the racialized postwar US housing market, African American life insurance companies pursued their mortgage purchasing activities as best as they could, supporting Black homeownership even in ways that sometimes contributed to the further entrenchment of residential segregation. By 1952, the number of Black legal reserve insurance companies had increased to 29, twice as many as at the start of the Depression in 1930. Meanwhile, these companies’ assets had grown to $161 million, from just $22 million at the start of World War II—a 632% increase—with North Carolina Mutual and Atlanta Life at the head of the pack.Footnote 44 To reemphasize, these companies had quite limited funds compared with the largest life insurance firms. Putting it into perspective, all African American legal reserve life companies combined held just $11 million in mortgages in 1946, compared with $7 billion by the industry as a whole (see Table 2). By 1960, Black firms’ mortgage portfolios had grown to $86 million; this represented significantly faster growth than the industry average, although the Black-controlled share of the $42 billion market still constituted only 0.2% of the total. Furthermore, African American life insurance companies lagged mainstream ones in terms of mortgage investments, at 29% compared with 35%; for reasons discussed below, Black firms continued to prefer bonds (see Table 3). Black life companies additionally had a lower uptake of FHA and especially VA mortgages relative to conventional ones (see Table 4), partly due to the lesser extent of Black homebuyer access to these loans. Despite the government’s description of their FHA holdings as “impressive” in a 1955 report, historian Preston Smith II explains further that Black-owned life insurance companies favored more lucrative (but riskier) conventional mortgages because “as small firms they needed a higher return on their investment to build their small capital base[.]” Thus even as Black-owned companies increased their mortgage lending, they disproportionately invested in conventional loans—as did the mainstream life insurance industry, for that matter. While Atlanta Life’s total mortgage holdings quadrupled from 1949 to 1956 to around $4.1 million, in the latter year $2.1 million of these were in conventional loans, as compared with $1.0 million in FHA loans and $826,000 in VA loans. Predictably, the 1956 return on its investments was 5.7% for conventional mortgages, compared with 4.2% and 4.6% for its FHA and VA loans, respectively.Footnote 45

Mortgages Held by Black Legal Reserve Companies versus the Life Insurance Industry as a Whole, 1946–1960

Source: David Abner III, “Some Aspects of the Growth of Negro Legal Reserve Life Insurance Companies, 1930–1960,” D.B.A dissertation (Indiana University, 1962), 193.

Selected Assets of Ten Largest Black Life Insurance Companies, 1957

Source: Racial Relations Service (HHFA), “Selected Assets of 31 Negro-Owned Life Insurance Companies as of December 31, 1957,” October 1958, in North Carolina Mutual Life Insurance Company Archives, box 32, “Mortgage loans, 1952, 1957–1959” folder.

Composition of Mortgage Portfolios Held by Black Legal Reserve Companies versus the Life Insurance Industry as a Whole, 1947–1960 (percentages by mortgage type)

Source: David Abner III, “Some Aspects of the Growth of Negro Legal Reserve Life Insurance Companies, 1930–1960,” D.B.A dissertation (Indiana University, 1962), 198, 199.

This investment approach was largely motivated by two major disadvantages Black life insurance companies faced. First, they did not have the same access to trustworthy financial intermediaries that white firms did. Second, if they wanted to invest in Black residences, the US employment structure and housing market was racialized in ways that made these undertakings both riskier and less profitable—the result of African Americans’ lower earnings and tenuous job security, and such projects’ siting in what tended to be the least desirable, most racially segregated and financially deprived locations. Without a doubt, Black life insurance companies were deluged in the early postwar decades with requests for mortgage investments, whether conventional, FHA-insured, or VA-guaranteed, illustrating why loan originators were traditionally known in the industry as “correspondents.”Footnote 46 Dozens of such letters populate Atlanta Life’s company records, underlining that a lack of attention was not the problem. Most of these inquiries came from mortgage and investment companies, savings and loans, building contractors, real estate and insurance agents, lawyers, and business associations—both Black and white.

Those from African American correspondents speak to the particular challenges they faced, and especially financing difficulties. A letter from the Dallas Negro Chamber of Commerce, seeking backing for a subdivision then under negotiation with city officials, reported: “We cannot escape being asked if the insurance companies of our race … will be interested in these mortgages.” A Black business club in Macon, Georgia sent a photograph of an initial house in a planned development, explaining: “We have lots of buyers, but the down payment supplied by several Loan Companies here is too high. So we would appreciate it to the highest if you would grant us a loan.” An African American builder in Houston noted: “The white banks of Houston, frankly are reluctant—they refuse to finance such housing for Negroes…. For this reason … the field of financing is open to Negro capitol [sic] alone to take over completely. They [whites] will of course follow, as they do not, I find, deem it advisable to lose a dollar after they find such a venture profitable.” And the president of Central Life, another Black-owned company based in Tampa, wrote to ask whether Atlanta Life would be interested in some preapproved FHA mortgages on a subdivision it was underwriting. “Very likely you have been approached by a number of our sister companies as well as white lending agencies throughout the country which discloses the fact that it is becoming more difficult to find money to finance Negro home building,” he ventured. Finally, some of the inquiries were internal, continuing an earlier tradition of direct loans. For example, a cashier from Atlanta Life’s Corpus Christi, Texas office wrote: “We have so many inquiries from our policy holders that the following inquiry is very necessary. Does our company offer any type of Home Loan? Is our company in a position to take or offer FHA loans?”Footnote 47

Far more numerous were inquiries from white correspondents.Footnote 48 Most of them referenced race; that is, they were aware that Atlanta Life was a Black-owned insurance company and sought to persuade on that basis. Thus a Detroit mortgage company offering $250,000 of FHA loans enclosed a recommendation letter from the local NAACP branch. A Dayton, Ohio mortgage broker emphasized the “great need … for popular priced homes … for the particular use of colored people,” claiming “The Federal Housing Administration is willing and anxious to insure mortgages on these properties[.]” “This is not a lot selling scheme, but a proposition to provide better homes for the ever increasing colored population of Houston,” wrote another, seemingly referencing the prevalence of unscrupulous practices. Some of the inquiries were quite patronizing. “Unfortunately, none of the white insurance companies have been taking colored G.I. Loans or F.H.A. Would you be interested in making these loans here direct[ly] to your people[?]” a Daytona Beach attorney inquired, while a Kentucky mortgage officer sought financing for a FHA-approved Louisville development by suggesting “this property would offer a good investment and would also be excellent from the standpoint of public relations in this area for your company.” “If you are familiar with Dallas you will know that … the colored [people] over here can afford nice places to live and they will buy the houses and rent the nice apartments,” another mortgage broker wrote. Conversely, some correspondents made no mention of race whatsoever. One particularly tone-deaf inquiry, written 4 years after the Shelley decision, offered mortgages on Murfreesboro, Tennessee properties “in the best residential sections covered by zoning laws and also protected by restrictive covenants in the deeds.”Footnote 49 Around this time, other Black-owned life companies, such as Universal Life of Memphis and Victory Mutual of Chicago, were investing substantially in FHA-backed projects for African American occupancy developed by white firms.Footnote 50 FHA-insured loans at least protected against foreclosure, and the real possibility that white operators might seek to originate and then unload subpar loans onto their books.

Unfortunately, much of Atlanta Life’s return correspondence—and in particular that relating to the projects and properties it chose to support—remains closed to researchers. But in mid-1951 the company turned down an offer of Texas FHA–VA loans with its typical explanation: “After considering our maturing current commitments as well as others that will fall due in the near future … we would not be in [a] position to purchase these loans at the present time.” Later that same year, Fannie Mae noted that Atlanta Life had invested in just over 600 FHA-insured mortgages up to that point. In a further hint at its activities, an FHA staffer wrote offering mortgages on individual Fort Worth homes, following up on prior company instructions to pass along “good” FHA mortgages.Footnote 51 Without access to Atlanta Life’s decision-making process, some aggregate statistics help to sketch the overall picture. From 1949 to 1956, the company’s mortgage portfolio skyrocketed, from just under $100,000 to around $4 million. In 1949, mortgage loans represented only 1% of its assets, as compared with some 86% (more than $18 million) in bonds. However, by 1955 the company had increased its mortgage holdings to a still-modest 8% of total assets, underlining Atlanta Life’s relatively cautious investing even compared with other Black-owned firms.Footnote 52 Caution was additionally evident in the company’s initial postwar mix of mortgage products, with safe FHA-insured loans representing by far the largest portion (the company also started buying VA-guaranteed loans in 1950). Not until 1953 did Atlanta Life conform to the typical pattern of holding a greater proportion of higher-interest conventional mortgages—a pattern that continued even as FHA “minority loan applications” increased substantially by mid-decade.Footnote 53

Reflecting its longstanding commitment to community uplift, North Carolina Mutual Life pursued a more aggressive strategy than Atlanta Life of acquiring both conventional and government-backed mortgages. As early as 1946, the company had contacted FHA to express its interest in investment opportunities on “housing developments in states serviced by their company.” By 1951 the company’s mortgage portfolio—which included properties in 14 different states—was already valued at $7.8 million, representing 23% of its overall assets, of which nearly $2.2 million were in FHA–VA loans. Indeed, the company was trying to devote one-quarter of its entire holdings to mortgages, as recommended by Moody’s Investors Service. It also discontinued loans to churches, and aimed to put 75% of its holdings in federally insured paper, to align with industry norms.Footnote 54 North Carolina Mutual retained some clout in FHA negotiations, as evidenced by its purchase of mortgages in Savannah’s Carver Village “on condition they are transfer[red] from Title 6 to Title 2 … [to meet our] need for a 4½% net interest earning.” FHA granted the request. And similar to its white counterparts, North Carolina Mutual relied on loan originators to service its FHA-insured mortgages, including Black-owned firms such as the Atlanta Mutual Building & Loan Savings Association. The company did continue to service all of its higher-yield conventional loans, however, along with “purchase money” (owner-financed) mortgages issued on its foreclosed properties.Footnote 55

Black-owned life insurance companies operated in a competitive economic landscape, facing more vexing investment decisions than mainstream life companies.Footnote 56 In seeking to remain profitable, they utilized business practices specific to the niche markets in which they operated. To reemphasize, even middle-class African Americans faced inordinate economic insecurity, especially in cities entering the “urban crisis.” To fathom these unique challenges, consider North Carolina Mutual’s 1953 bid to acquire $500,000 of mortgages in New Jersey, with a focus on Newark. In preparation for that move, the company conducted a detailed study of income levels and demographic shifts in the city’s Black neighborhoods. Despite its overall goal of increasing Black Newarkers’ financing access and its targeting of “professional classes and workers in industrial plants that are the chief beneficiaries of the social revolution,” the company exhibited several accommodations to the unfortunate realities of profitmaking in a deeply unequal, racially structured housing market. For one, it identified “some heavily populated areas in which we will definitely not want loans,” even making a redlining-reminiscent map indicating “the undesirable sections as well as the desirable sections.” Considering “the present difficulty in placing Negro loans,” North Carolina Mutual additionally sought to bolster its profit margins, since the interest rate on conventional loans in Newark was up to a point and a half lower than its base of 6%. However, to avoid “the impression that we are taking advantage of an unfortunate situation,” the company resolved to “consider favorably” requests for loans at 5% interest. Finally, North Carolina Mutual decided its mortgages should cover no more than 60% of a home’s value, leaving most borrowers to cover the shortfall with higher-interest junior liens.Footnote 57

Black-owned insurance companies also financed some of the “Negro housing” (increasingly termed “minority housing” after World War II) built with FHA supports. Though understudied, this approach to increasing the available housing supply for African Americans defined the agency’s focus through the 1950s, and essentially involved negotiating for “acceptable” development sites that were less likely to generate white opposition. Many of the peripheral areas utilized had locational disadvantages; not surprisingly, this policy prompted criticism soon after the war.Footnote 58 From 1942 onward FHA had a Racial Relations Service (RRS) headed by Frank Smith Horne, a former member of President Roosevelt’s “Black Cabinet” who had served in the National Youth Administration’s Division of Negro Affairs.Footnote 59 Though fully cognizant of the segregationist implications, Horne and his RRS Advisers—all of whom were Black, with each assigned to a single FHA region—helped to facilitate the construction of thousands of private apartment units and single-family homes for Black occupancy, simultaneously voicing an internal critique of FHA policy to white higher-ups.Footnote 60 Although further research will determine how many federally supported “minority housing” projects were financed by Black insurance companies, the majority were actually funded by white firms—such as Prudential and New York Life, which underwrote the FHA-insured mortgages for Pontchartrain Park, a modern New Orleans subdivision that included a private golf course.Footnote 61

Nevertheless, the postwar FHA sought to actively involve African American life insurance companies as a way of increasing the available housing supply, aiming to connect them with Black real estate promoters and construction firms. By December 1948 this initiative was fully in place, focused on “the area of the largest untouched need—the middle-income sector of the minority group housing market,” and with RRS as the conduit for a “united cooperative effort” among these Black housing interests. The brainchild of Horne’s deputy Booker T. McGraw, this strategy launched following McGraw’s June meeting with North Carolina Mutual’s Asa T. Spaulding, then chair of the National Negro Insurance Association (NNIA). Nevertheless, it built upon efforts dating to 1946 by Walter H. Aiken, the country’s largest Black builder based in Atlanta. With Congress considering major housing legislation in early 1949, an RRS-coordinated committee led by Aiken—which included an NNIA representative from North Carolina Mutual—sought an audience with President Truman himself, to discuss “financing private housing available to Negroes.”Footnote 62 Though that meeting never happened, RRS staffers continued their outreach, with Horne regularly attending NNIA meetings and Aiken working to mobilize Black investment capital. In October 1951, Aiken wrote FHA Commissioner Franklin Richards concerning his efforts to “pool some of the building and financing resources among Negroes in order to make a greater contribution ourselves to meeting the needs of the growing middle-income market among minority groups.” Several months later, Aiken proposed to Horne that a national “Mortgage Banking Company” be established, to “break bottlenecks with reference to financing mortgages for Negroes” but which would serve “lower income bracket groups … regardless to [sic] race, color, or creed.”Footnote 63

Although this plan never materialized either, individual Black-owned life insurance companies proceeded to fund housing developments that were periodically featured in the FHA’s magazine Insured Mortgage Portfolio. In a 1953 article showcasing some such projects, Black life insurers were reported to have “all found that such financing is good, profitable business.” The article went on to name North Carolina Mutual, Atlanta Life, Universal Life, and Pilgrim Health & Life, along with some specific subdivisions in Memphis, Atlanta, Fort Worth, and Augusta, Georgia that had received financial backing from these companies. In a particularly notable example, North Carolina Mutual, Atlanta Life, and Memphis’s Universal Life had joined in financing that city’s Elliston Heights, a 200-home subdivision “located in a very desirable section” and lauded as “one of the best of its kind in the South.” North Carolina Mutual pre-committed to purchase $800,000 worth of the project’s FHA/VA-backed mortgages, while Atlanta Life agreed to buy $350,000.Footnote 64 RRS weekly reports under Truman are filled with mentions of projects planned and executed by life insurance companies and other Black financiers, from individual apartment buildings to entire subdivisions. Unsurprisingly, however, they also reveal some difficulties associated with these endeavors. For example, Horne reported tersely in 1948 that the Mutual Benefit Society of Baltimore “may abandon plans for a 144-unit project … as a result of its experience with two 4-unit apartment buildings [it] completed under Section 608.” And in 1951, FHA characterized the Chicago financing situation as “inordinately difficult” and beset by “many obstacles.” Despite ongoing talks with the Metropolitan Mutual Assurance Company, FHA lamented that Chicago Black financial institutions had not “invest[ed] more fully … in the private housing market among Negroes particularly, utilizing the benefits of the insured mortgage programs of this agency.”Footnote 65 Amid a more generalized minority housing push, federal housing agencies’ insistence that African Americans should shoulder additional responsibility for solving race-based housing inequality would grow even louder in the Eisenhower years that followed.

Eisenhower’s Minority Housing Policy and the Voluntary Home Mortgage Credit Program

Under Truman and Eisenhower, US housing policy demonstrated mostly continuity in terms of progress toward racially equitable access, revealing the limits of liberalism in this era of political consensus.Footnote 66 There were, however, palpable differences in each administration’s tone and preferred approach. Harry Truman had established the President’s Committee on Civil Rights by executive order in 1946, which subsequently issued a strong condemnation of housing discrimination, restrictive covenants in particular. In early 1948, Truman urged Congress to strengthen civil rights protections, and his Office of the Solicitor General filed an unprecedented amicus curiae brief supporting the Shelley plaintiffs. Even so, Truman’s FHA administrators dragged their feet in revising the agency’s regulations regarding “protective” covenants, and balked at using its police power to enforce nondiscrimination. Any talk of denying FHA mortgage insurance to developers who discriminated ended with Dwight Eisenhower’s 1953 accession, and his appointment of conservative former Kansas Congressman Albert M. Cole to head the Housing and Home Finance Agency (HHFA) that oversaw FHA. Cole, whose view on racial integration was that it was impossible to “legislate the acceptance of an idea,” immediately demoted RRS head Frank S. Horne. When Horne and his assistant Corienne Morrow demanded an end to the FHA’s “separate but equal” approach—in the wake of the Brown v. Board decision—Cole fired them. Even after a 1955 federal court ruling that the FHA could withhold its backing in the face of noncompliance with federal or state civil rights statutes, Cole remained adamant; the following year he even attempted, unsuccessfully, to disband the hamstrung RRS altogether. While Cole’s successor Norman P. Mason acted to restore the RRS in 1959 and implement fairer federal housing policies—such as authorizing FHA support of more racially-integrated projects—he nevertheless “shared the administration’s philosophical opposition to either legislation or executive action guaranteeing open occupancy in federally assisted housing.”Footnote 67

In actuality, the bigger distinction between the two administrations’ policies was that Truman had advocated for direct lending (through the VA and Fannie Mae), whereas Eisenhower favored a business-led expansion of the public-private arrangements initiated under Franklin D. Roosevelt. Amid growing criticism from civil rights advocates like the NAACP and Urban League, Cole and Mason pursued this emphasis through increased outreach to the construction and home finance industries. Soon after taking office, Eisenhower convened an Advisory Committee on Government Housing Policies and Programs, its members heavily recruited from the private sector.Footnote 68 However, the committee’s massive December 1953 report barely mentioned race except for a one-page section on “Housing for Minority Groups” that acknowledged Black families’ “greater inability to secure standard private housing within their means.” Its chief recommendation, in fact, was to make FHA rehabilitation (Section 203) loans more readily available. In other words, it advocated easing renovation of the secondhand housing where most Black homeowners already lived, instead of facilitating their access to new, suburban housing.Footnote 69 Then, in a focused effort to tackle the “problem” as Cole understood it, HHFA sponsored a December 1954 “Minority Housing Conference” where mainstream life insurance companies pledged to improve mortgage access, and the National Association of Home Builders (NAHB) declared itself ready to set aside 10% of all new housing for nonwhite occupancy—but only if “suitable” sites could be found. Both before and after the December conference, federal housing officials networked with the NAHB, Mortgage Bankers Association of America, and US Savings and Loan League to discuss ways of facilitating new (but segregated) housing along these lines.Footnote 70

The new administration’s attitude toward African American financial concerns, and life insurance companies in particular, was even more striking. Under Eisenhower, Black homebuilding interests were expected to undertake a “self-help” program, following the guidance of Joseph R. Ray, Horne’s replacement as head of the RRS. A former board member of the Black-led National Association of Real Estate Brokers as well as a loyal Republican, Ray’s take on segregated new minority housing was that “half [a] loaf” was better than “no bread at all.”Footnote 71 With more nonwhite applicants seeking FHA-insured mortgages, Cole and other federal housing officials pressured Black life insurance companies to purchase a greater share of these loans on the secondary market—thereby not only underwriting, but ostensibly legitimizing the FHA’s approach of accommodating racial segregation. While African Americans were present at the HHFA’s December 1954 Minority Housing Conference, they made up barely one-fifth of the conferees, with M. C. Clarke of the National Insurance Association (NIA, formerly the National Negro Insurance Association) as the sole representative for Black life insurance companies. Therefore, in May 1955, Cole convened a more targeted, “shirt sleeve” session on the topic, with attendees from 16 leading Black financial institutions. Here, in what can be regarded retrospectively as an ill-advised move, Cole leveled accusations that Black lenders were shirking their “responsibility” by failing to purchase enough FHA-insured loans. Compounding matters, he pointed to the higher interest rates Black financial institutions charged for conventional loans, stating that “minority-owned lending agencies, in particular, cannot afford to have a finger pointed at them as exploiters of prospective Negro home buyers.”Footnote 72

In addition to higher rates of return, Black-owned firms—like life insurers in general—tended to prefer conventional mortgages over FHA–VA-backed ones. Although insured against default, the smaller down payments on these loans meant borrowers had less equity tied up in them, making them more likely to bolt in the event of a financial setback. Furthermore, FHA–VA mortgages carried higher overhead costs due to the associated paperwork, and inflation eroded their already thin profit margins. In any case, Black representatives took offense to Cole’s remarks, pushing back both at the conference as well as in private correspondence. NIA president C. L. Townes, for one, pointed out that the 26% of their assets Black life insurance companies had in mortgages lagged the overall industry by less than 4% (recall Table 2). Furthermore, HHFA data showed that Black life companies’ FHA-insured holdings had grown substantially since 1951, actually surpassing those of similarly sized white firms by 1954. As for higher-cost conventional loans, Townes ventured to ask “whether or not your investigators or informers also investigated the charges and interest rates being charged by comparable white lending agencies in the same communities?” Again, in a highly competitive environment, Black lenders felt compelled to charge higher rates to remain financially viable; tellingly, one attendee remarked: “If Negro insurance companies went into the FHA mortgage business on a large scale, the low interest rate allowed by the Government would run us out of business.” As historian Preston Smith II explains, Cole’s expectations were unrealistic, because in a racially discriminatory housing market, Black lenders could neither generate enough business nor accumulate enough capital to successfully compete with white firms. Cole subsequently sent follow-up letters clarifying his remarks to several Black representatives who felt he had unfairly characterized their record.Footnote 73

Besides pressuring Black and white financial interests to participate in FHA-sponsored lending, the Eisenhower administration’s plan to improve housing access for minority buyers involved the Voluntary Home Mortgage Credit Program (VHMCP), fittingly titled to make clear its emphasis on noncoercive measures acceptable to business interests. The VHMCP was established as part of the 1954 Housing Act, an omnibus housing bill mostly remembered for having initiated urban renewal as a federal government program. However, the legislation also aimed to increase the flow of home mortgage credit through a rechartering of Fannie Mae. In this new arrangement, Fannie’s secondary market operations were separated out and privatized to increase its capitalization and improve its performance as a facility for FHA-insured and VA-guaranteed mortgages.Footnote 74 The Act established the VHMCP as a “clearinghouse” to connect applicants seeking FHA- or VA-backed mortgages with lenders—intended as help for minority borrowers, as well as all applicants from small towns and remote areas with less access to credit. Individuals like F. D. Wharton, who had twice been refused home loans, could seek VHMCP assistance at one of its 16 offices, one for each FHA region. These offices maintained lists of lenders willing to finance minority and rural borrowers, for use in trying to place the loans. Yet as Preston Smith II has emphasized, “there were no disincentives or penalties for nonparticipation.” Each FHA region had a VHMCP committee with members from private lending and real estate interests, Black as well as white, and including secondary market players such as life insurance companies. In addition, there was a national VHMCP committee, which incidentally did not initially include any Black members until the elevation of North Carolina Mutual’s Asa T. Spaulding in late 1956.Footnote 75

Intended to rebut demands for more direct lending and government-built public housing—and to demonstrate that public–private partnerships could flourish—the VHMCP was promoted by both the Eisenhower administration as well as the construction and home finance industries as a solution to the difficulties nonwhite borrowers faced. The VHMCP had been established largely at the life insurance industry’s behest, both as a way to address calls for wider access to mortgage credit and as a means of undercutting an expanded program of direct loans to underserved locations (in 1950, the Veterans Administration had begun lending directly to veterans living in rural areas). In the hearings leading up to the 1954 Act’s passage, Prudential president Carrol M. Shanks voiced the life insurance industry’s demand to liquidate Fannie Mae, even as he promised “a voluntary but well organized effort” to extend FHA–VA loans “to the maximum extent possible to all good credit risks … in every community of the United States.” From the government’s side, deputy RRS adviser Booker T. McGraw wrote reassuringly, in an article that appeared in the NAACP’s journal Phylon: “[T]he new voluntary home credit extension program should enable the average citizen seeking to borrow money for a home from a local lender to be much more likely to get it—wherever he may live or whatever may be his race.”Footnote 76

However, the VHMCP never met expectations, instead exposing the shortcomings of this voluntary approach to expanding housing access for African Americans and other racial minorities. When 1955 statistics showed Black applicants had vastly underutilized the program in its first year, McGraw’s boss Joseph Ray assigned him to remedy this “lack of awareness” through collaboration with the VHMCP’s national secretary. Although applications subsequently increased, George S. Harris, president of the Black-led National Association of Real Estate Brokers, testified before Congress that “the VHMCP has hardly scratched the surface insofar as the nonwhite housing market is concerned,” and expressed concern the program might be “operating under the so-called gentlemen’s agreement,” in other words, the racial discrimination commonplace in private industry.Footnote 77 And certainly, nothing much had changed, judging by the 1955 case of Lieutenant Commander Dennis D. Nelson II, a decorated military man among the first cohort of Black navy officers commissioned during World War II, who sought to build a house in San Diego’s exclusive Point Loma neighborhood. Nelson struggled to arrange financing—notwithstanding FHA preapproval, VHMCP mediation, and the RRS directly handling his case. Not only did the Bank of America deny Nelson because “it would not be proper … to extend financing to a member of a minority race when he is the first to enter a given area,” but the Black-owned Golden State Mutual Life Insurance Company also rebuffed RRS entreaties, stating they had ceased buying FHA- and VA-backed mortgages, and thus could only offer Nelson a conventional loan covering two-thirds the value of his property.Footnote 78 Additional criticism reached Cole from a Black Detroit accountant who complained FHA was devaluing appraisals on homes in the “transitional” neighborhoods to which African Americans were moving, despite inflated asking prices from white sellers: “Does this partly explain the question that you posed as to why the Voluntary Mortgage Program does not receive many applications from negroes, and why some of our own lending agencies are not making FHA loans?” he asked.Footnote 79

Such failures served to confirm Black lenders’ hunch, according to former RRS head Frank Horne, that “FHA was not for them or their clients.” Yet even so, HHFA administrators continued to insist on the VHMCP’s efficacy, appearing mystified as to why African American lending institutions withheld more “active cooperation.” At Ray’s insistence, McGraw wrote in early 1955 to all 14 Black VHMCP regional subcommittee members, seeking their “knowledge and ‘know-how’ … in getting the message across and activating the fuller flow of qualified applications” needing assistance. As for what HHFA imagined as the difficulty, McGraw ventured that “minorities either lack adequate information about the VHMCP or they are being served by real estate brokers and builders and lenders who have a decided preference for conventional financing and reluctance to use FHA and VA aids.” However, McGraw’s own data indicated that despite the receipt of 4,340 applications, the VHMCP had facilitated just 85 loans to that point, with a paltry 35 “made for housing to serve minority groups.” Only one regional subcommittee member responded to McGraw’s inquiry, leading to his frustrated report back to Ray that “the dearth of VHMCP applications received in behalf of Negroes indicates that their … home financing problem is a ‘myth.’”Footnote 80 Ultimately, from the launch of the program until the end of Eisenhower’s tenure, the VHMCP facilitated around 47,000 mortgages, with only 10,000 of these going to minority borrowers in metropolitan areas. Hardly effective by any measure, the program clearly served rural whites better than African Americans.Footnote 81 Yet federal housing officials as late as 1959 were characterizing VHMCP as “a practical mortgage financing aid,” despite admitting that the number of minority applicants helped by the program was “smaller than was originally anticipated,” in the words of then-executive director Joseph B. Graves.Footnote 82

The HHFA’s expectation that African American financial interests participating in the VHMCP could significantly expand Black homeownership appears especially unreasonable considering its utilization by mainstream lenders. Indeed, the program was hamstrung by the financial industry’s failure to secure favorable changes in response to shifting monetary policy. From the outset, the VHMCP’s organizers intended to preempt any further “use of public funds” for mortgages originated directly by the Veterans Administration or Fannie Mae—whose activities they perceived as unfair competition due to these loans’ generous terms and low interest rates. Life insurance companies were initially the VHMCP’s most active promoters—and also its largest users over the duration of the program, accounting for more than 80% of the total loans placed.Footnote 83 Yet Eisenhower’s time in office coincided with a generally contractionary monetary policy, as the Federal Reserve raised interest rates to check inflation, which in turn reduced profit margins on FHA-insured and VA-guaranteed mortgages.Footnote 84 By 1956 the trade publication Mortgage Banker was running opinion pieces demanding adjustments to these fixed-interest instruments to counter the rising federal funds rate. Perhaps most outspoken was Miles Colean—the FHA’s former assistant administrator turned consultant—who accused housing advocates of attempting to create “an ideal society” in the mistaken belief “that government should and could, by grant and subsidy, give every family in the nation a good home[.]”Footnote 85 By the end of Eisenhower’s time in office, institutional lenders’ views had soured to the point where Life Insurance Association of America economist James J. O’Leary asserted “it was never the intention … that the VHMCP would be a giveaway program.” Explaining it “couldn’t be expected to operate on other than a market basis,” O’Leary expressed the industry’s position that “When life insurance companies have plenty of other places to put their money, 40-year loans are very unattractive investmentwise.”Footnote 86

Conclusions

Under Truman and especially Eisenhower, government officials strongly pressured white as well as Black financial concerns to underwrite more FHA- and VA-backed loans, including ones to improve racial minorities’ housing access. Historian Preston H. Smith II neatly summarizes the predicament that life insurance companies and other financial interests run by African Americans faced, in a post-World War II housing field remade by New Deal era market interventions: “There is no reason to believe that the black real estate industry was not equally satisfied with this arrangement of socialized costs and private profits. What they were not happy with … was the fact that they could not fully participate in the government-subsidized, private housing market in the way that white firms could.”Footnote 87 Operating in a less-connected portion of the financial sector, Black-owned life insurance companies were informationally disadvantaged and so could not rely on the same constellation of financial intermediaries for investment guidance that white-run firms did.Footnote 88 They remained committed to serve in their traditional role as credit reserves for aspiring African American homeowners—who stood in a more precarious financial position due to discrimination. But in doing so, they accommodated segregationist approaches demanded by the federal government itself, and utilized some questionable profitmaking practices they deemed necessary to compete in a racially-structured housing market. Black-owned insurance companies would endure, despite their diminishing importance following the 1964 Civil Rights Act, the larger mortgage market’s shift toward securitization, and the financial ups and downs of the 1970s and 1980s. The successor firm to Atlanta Life survives to this very day, in fact, while North Carolina Mutual only recently met its demise in 2022.Footnote 89 While such companies helped to partially offset the discriminatory treatment African Americans often encountered when seeking mortgage financing, racial disparities in access would nevertheless remain, as a new generation of Black middle-class homebuyers painfully found out when the Great Recession crested in 2008.Footnote 90

Acknowledgements

The author would like to acknowledge, and thank for their feedback on earlier drafts Amanda Boston, Richard Harris, Seumalu Elora Lee Raymond, Thomas Storrs, Steven Usselman, and the anonymous reviewers for Business History Review. Initial findings were presented to the Yale Economic History Workshop in October 2022, with thanks due to José-Antonio Espín-Sánchez and Gerald Jaynes for graciously facilitating that opportunity.

Author biography

Todd M. Michney is an associate professor in the School of History and Sociology at the Georgia Institute of Technology, whose work has appeared in the Journal of American History, Journal of Urban History, Journal of Planning History, and Journal of Social History. Michney is the author of Surrogate Suburbs: Black Upward Mobility and Neighborhood Change in Cleveland, 1900–1980 (University of North Carolina Press, 2017). He is currently working on a book tentatively titled Black Builders: African Americans, Construction, and Community, 1865–1965.

Open access

Open access