2.1 Intro

The shift from analogue to digital has revolutionised the music industry. The constant rise and fall of new methods of exploitation and associated evolving business models ensure that any researcher only has one certainty, namely that the results of their research will become outdated. Specialised volumes on the ever-changing structure of the music industry require almost yearly updates.Footnote 1

This chapter nevertheless takes up the gauntlet. It first analyses the rights and interests of the primary stakeholders and introduces the various contracts entered into between musicians and their corporate partners (Section 2.2). It then discusses the music value chain that results from such contracts in the streaming age (Section 2.3). Two separate sections are dedicated to, respectively, the division of revenues (Section 2.4) and the ongoing quest towards enhanced transparency (Section 2.5). A concluding ‘Bridge’ (Section 2.6) brings together the most relevant findings that lead into the analysis of the relevant legal framework in the subsequent chapters.

2.2 Rights and Interests of the Primary Stakeholders

2.2.1 Overview

The basic structure of the music industry may be presented on the basis of the distinction between composition, performance and phonogram. First, on an abstract level, there is a musical ‘composition’. This is an intangible work that consists of a melody, chord progressions and a certain instrumentation; is structured in a certain way; and is often accompanied by specific lyrics. However, music is more than notation alone. A ‘performance’ brings a composition to life. Performers are the driving force of this activity. They transform paper notes into real-life action on stage. A performance may be recorded in one way or another, resulting in a ‘sound recording’,Footnote 2 referred to throughout this book as a ‘phonogram’.

A distinction thus arises between a composition, a performance and a phonogram. This distinction results in a three-way division of the music industry into (1) music publishing, (2) live performances and (3) recorded music sectors. The music publishing sector revolves around the exploitation of the composition, the live performances sector is engaged with the commercial organisation of performances, and the recorded music industry seeks to distribute and monetise phonograms.

The relationship between composers and publishers is situated in the music publishing sector, as it relates to the exploitation of the composition. The second sector, the live performances industry, builds on the activities (that is, the performances) of performers. The recorded music industry, finally, requires the cooperation of both performers and record companies since it centres around the fixation of a performance (or another sound) in a phonogram.

While bearing in mind this fundamental three-way division, this book opts for a characterisation of the music industry on the basis of its primary categories of stakeholders. The rights and interests of these heterogenous groups are analysed in the following sections, focusing respectively on musicians, their corporate partners and users. After a brief typology, their rights and underlying interests are treated.

2.2.2 Musicians

2.2.2.1 Typology

While artistry is not susceptible to exhaustive categorisation, it is first useful to take a closer look at different ‘types’ of musicians. There are two main broad categories, namely composers/lyricists (jointly referred to as ‘composers’) and performers.Footnote 3

In the category of composers, artists who write both music and lyrics are referred to as songwriters. Singer-songwriters are songwriters who also perform their music and are credited as such. Within the category of musical performers, there are two main types of musician, namely featured artists and session musicians. Featured artists’ work is credited on a phonogram, while session musicians are hired on either a freelance or a more lasting contractual basis to perform in recording sessions or live performances without receiving express credit.Footnote 4 Within these two types, an enormous variety exists, from singers to multi-instrumentalists.Footnote 5 Musicians that are featured on a certain phonogram may be session musicians on another, and vice versa. A final important subcategory of the broad range of session musicians includes orchestral musiciansFootnote 6 and chamber music players, active in the genre of classical music. This typology may be schematically represented as shown in Table 2.1.

| Musician | |||

| Composer (sensu lato) | Performer | ||

| Composer (sensu stricto) | Lyricist | Featured artist | Session musician |

| Songwriter | |||

| Singer-songwriter | |||

The process of making music varies significantly across different genres. Classical musicians most often either perform or compose music and are thus easy to categorise on that basis.Footnote 7 Contemporary classical musicians are an exception, as they often create dedicated works and perform these works themselves. This seems especially true for creations with a significant conceptual aspect. Jazz musicians combine existing music structures with their own improvisations, thus continuously crossing the line between being a performer and a composer-performer.Footnote 8 In modern music, there is a large variety of artistic processes, ranging from singer-songwriters and indie folk bands who write their own music, to pop stars who perform melodies composed entirely by a team of collaborating songwriters. A final group is populated by DJs, whose status as creating and/or performing musicians is disputed.Footnote 9

2.2.2.2 Rights

In their capacity as either composers (and thus authors) or performers, musicians are granted initial ownership of rights in music: copyright sensu stricto in the composition and a neighbouring right in (the fixation of) a performance.

Authorship leads to initial ownership of copyright sensu stricto. It may only be claimed in the event of a contribution that fulfils the conditions for copyright protection.Footnote 10 Copyright protection is available to ‘literary and artistic works’,Footnote 11 including music.Footnote 12 It is not granted to mere abstract ideas and principles. These must be expressed in a concrete way, identifiable with sufficient precision and objectivity.Footnote 13 Copyright protection only arises if the condition of originality is fulfilled. In accordance with established case law of the European Court of Justice (ECJ),Footnote 14 this implies that the work must be an intellectual creation of the author(s) expressing free and creative choices and reflecting their personality.Footnote 15 The work must show the personal stamp of the author – that is, their authorship. The determination of authorship in a specific case is a matter of national law.Footnote 16 The concepts of ‘joint’, ‘collective’ or ‘co-’ authorship differ by country and are not harmonised at the EU level.Footnote 17

A particular dimension arises in case a work or performance is created in an employment context. Under Belgian, French and German law, the employee is awarded initial ownership.Footnote 18 In the Netherlands and the United Kingdom, the opposite rule applies to works (not performances): copyright is deemed to vest in the employer, unless contrary contractual arrangements have been made.Footnote 19

This brief analysis of authorship and the person of the author(s) may be contrasted with the concepts of performance and performers.Footnote 20 Article 2(a) WIPO Performances and Phonograms Treaty (WPPT)Footnote 21 defines ‘performers’ by enumeration as ‘actors, singers, musicians,Footnote 22 dancers, and other persons who act, sing, deliver, declaim, play in, interpret or otherwise perform literary or artistic works’, that is, works that are susceptible to – but not necessarily subject to – copyright protection. A certain degree of artistry is required. Mere technical contributions, such as those by sound engineers, are generally deemed insufficient.Footnote 23 Ancillary performers are excluded in some jurisdictions.Footnote 24 Finally, while a performance must not necessarily take place during a live concert, the performer’s contribution must take place at the same time as the performance.Footnote 25 Thus, performers are persons who perform.Footnote 26 A clearer definition could conceptualise performers as artists whose contribution is not deemed sufficiently original to give rise to copyright, who merely interpret the work of somebody else and operate within the boundaries of such work. This would detract from the possibility of performers also being the composers of the works they perform. In any case, the legal consequence of a musician’s categorisation as a performer is the acquisition of a neighbouring right relating to (the fixation of) the performance.

Thus, the legal qualification of a musician’s contribution depends on its nature and creative intensity. If a particular contribution attains the threshold of originality, the musician surpasses the bounds of performance and may in theory claim (joint) authorship of the creative musical work.Footnote 27 Many musicians fulfil a wide array of roles that may be situated somewhere on the continuum between authorship and performance, somewhere along the sliding scale of creativity.Footnote 28 Consequently, the application of legal concepts to this composer–performer spectrum may prove to be problematic. Maintaining an overly strict line in the sand between the legal regimes applicable to composing and performing musicians may be untenable in the long run. Instead, an argument may be made in favour of a largely uniform interpretation where this is possible.Footnote 29

When sheet music leaves sufficient leeway to the performer to make free and creative choices that express their personality in the context of the performance, it could be argued that the performer may fulfil the requirement of originality and thus legitimately claim copyright protection.Footnote 30 Even outside the realm of aleatoric music, the performance of a piece of music may legitimately influence the essence of a work itself, not only inspiring future performances but also leaving a creative, lasting imprint on the score.Footnote 31 For example, over the last decades, cellists everywhere have been inspired by the specific choices made in performances of the Bach Suites by Pablo Casals, and (later) Anner Bijlsma, Pierre Fournier, Yo-Yo Ma, Pieter Wispelwey and so forth. While the desirability of requalifying such ground-breaking performances as protected works may be disputed, a consistent application of the originality criterion may yet result in such a legal requalification.Footnote 32 In that case, performance and authorship would essentially merge.Footnote 33 A valid counterargument could be that an increased (legal) valuation of musical performance and an ensuing increase in potential joint authors would lead to both an increase in disputes on copyright ownership and an undue extension of the scope of copyright protection.Footnote 34 Taking the Bach analogy one step further, it could legitimately be asked whether any sort of exclusivity may be claimed on innovative bowings, nuances, rubatoes and/or fingerings. Yet the position set out above merely pleads for a consistent application of the law de lege lata of the existing criterion of originality. Many performers make free and creative choices in the context of their performance(s). In a way, objections against a revaluation of musical performance may be seen as objecting to the criterion of originality as such.Footnote 35

Independently of the above, in order to avoid unnecessary friction in the long run, it is advisable for collaborating musicians to make clear, prior written arrangements regarding the initial allocation of ownership of any rights that result from their collaboration, as well as the distribution of any ensuing revenues.Footnote 36 Whether a theoretical claim to (joint) authorship translates into ownership of copyright largely depends on the socio-legal bargaining power of the performer.Footnote 37 Only musicians with sufficient soft power and ensuing leverage in a contractual negotiation context will be able to claim rights.Footnote 38 It appears that contributions made by performers in a collaborative music-making context, such as during a ‘jam session’, are traditionally undervalued in such situations precisely as a result of the imbalance in negotiating power on the part of performers.Footnote 39 In case no arrangements on ownership are spelled out in advance – and in writing, given the difficulties of proving the existence and content of oral agreementsFootnote 40 – and a dispute arises after the fact, the consequences of power relations may be even more pronounced.Footnote 41 This rings all the more true where the music at issue ultimately achieves economic success.

Finally, a specific place in the popular music-making process is occupied by music producers (also known as ‘studio producers’).Footnote 42 They are involved in the process of recording music, but occupy a more artistic than commercial position. They oversee the recording process and seek to ensure that all parties involved contribute to the best of their abilities.Footnote 43 In other words, producers function as a kind of personified quality control.Footnote 44 Their task requires detailed knowledge of recording techniques as well as a strong affinity with music. However, unless an original contribution to the composition may be proven, music producers have no right to copyright protection sensu stricto. The Court of Appeal of Amsterdam held that music producers are not entitled to claim neighbouring rights protection as either a performing artist or a phonogram producer.Footnote 45 Producers may only claim performing artist status if the sounds they produce with their voice and/or with an instrument are incorporated into the performance and, thus, the phonogram.Footnote 46 The intervention of a music producer is not a prerequisite in the music recording process – musicians may also perform the tasks of a music producer themselves. Music producers often make their intervention in the recording process dependent on receiving credit and/or part of the exploitation rights in the composition and/or the phonogram, independent of the nature of their intervention(s).Footnote 47

As initial rights owners, musicians obtain the exclusive, negative right to either prohibit or authorise certain acts on the part of third parties.Footnote 48 Both copyright sensu stricto and the neighbouring right of performing musicians have an economic and a moral dimension. On the one hand, the economic prerogatives allow musicians to extract (commercial) value from their work(s)/performance(s) by granting certain rights to other parties through exploitation contracts. This book refers to the economic prerogatives assigned under copyright law sensu lato as ‘exploitation rights’.Footnote 49 These exploitation rights are curtailed by certain exceptions and limitations.Footnote 50 On the other hand, moral rights protect the link between authors or performers and their output.

The first and primary exclusive exploitation right is the right to make reproductions of their protected work and/or the fixation(s) of their performance(s). This right is to be interpreted broadly and is largely harmonised at the EU level.Footnote 51 The music industry wields the term ‘mechanical rights’.Footnote 52 The mechanical rights granted to composers differ from those enjoyed by performers.

Composers have the exclusive right of authorising the reproduction of their work(s) in any matter or form (by making copies), such as by recording a phonogram or by digitally storing a protected work.Footnote 53 A copy subject to the author’s consent exists when it takes over original elements of the initial work.Footnote 54 While coincidental resemblance is not actionable, no bad faith is required for an infringement to arise.Footnote 55 Illicit copying may take place subconsciously.Footnote 56 The reproduction right sensu lato further includes the right to adaptation (making musical arrangementsFootnote 57).Footnote 58 Authors also obtain a right of translation.Footnote 59 For music, this right only bears relevance for a composition’s lyrics (for example, an opera libretto).

Performing musicians first obtain a right to authorise or prevent the fixation of their performance(s).Footnote 60 Second, they are granted a right of reproduction relating to such fixations. This means that they may prevent a third party from making copies, including digital storage of such copies.Footnote 61 Performing musicians do not acquire an express right of adaptation or translation.Footnote 62

The mechanical rights granted to both composers and performing musicians further include the rental and lending right as to works embodied in phonograms and fixations of performances.Footnote 63 Finally, composers and performers acquire the exclusive right to either authorise or prohibit the distribution to the public of the original or copies of their works and/or fixations of their performances, which is limited by the principle of exhaustion.Footnote 64

Musicians also acquire certain performing rights. First, composers obtain the exclusive right to authorise the public performance of their works by any means or process.Footnote 65 This right of public performance implies the presence of a live audience at the place of the performance.Footnote 66 In addition, composers acquire exclusive rights relating to the communication to the public of their compositions by wire or wireless means.Footnote 67 This broad concept implies a transmission to a public that is not present in the same location.Footnote 68 The scope of this right includes music played in shops, restaurants and music venues, as well as broadcasts via radio and/or TV or by satelliteFootnote 69 and cable retransmissionFootnote 70 (as provided for under Member State lawFootnote 71).Footnote 72 A final subset of this right is the right to make their works available to the public in a way that allows individualised access by the public.Footnote 73

Performers may authorise or prevent the broadcasting by wireless meansFootnote 74 (including by satelliteFootnote 75 and cable retransmissionFootnote 76 as provided for under Member State law) and/or the communication to the public of their performance.Footnote 77 As for composers, the right to communication to the public includes an exclusive right to making available.Footnote 78 Save this making available right, performers’ right to communication to the public largely equates to an unwaivable remuneration right, subject to mandatory collective management.Footnote 79

Following the no formalities rule, the rights granted under copyright law sensu lato are generated automatically, upon either the creation of the work, (the fixation of) the performance or the creation of the phonogram at issue.Footnote 80 The term of protection starts then.

Copyright sensu stricto in the European Union as well as in the United Kingdom lasts for seventy years after the death of the (last surviving) author, subject to a limited number of exceptions.Footnote 81 The term of protection is different for anonymous or pseudonymous works. Unless the identity of the author becomes clear within seventy years after the work has been lawfully made available to the public (starting from the first of January following that eventFootnote 82), the protection lapses after that period.Footnote 83

The term of the rights granted to performers is somewhat more complex and has also changed over the past decades: while these rights traditionally expire fifty years after the event giving rise to the protection (for example, in case of unfixed performances),Footnote 84 a longer period of protection is granted in case of fixation on a phonogram, namely seventy years after its publication.Footnote 85 The relatively recentFootnote 86 term extension from fifty to seventy years was prompted by the EU legislator’s wish to improve the social situation of (session) musicians in view of their increased life expectancy.Footnote 87 It was controversial in view of its perceived ineffectiveness and the intrusion on the public domain that it entailed.Footnote 88

In addition to exploitation rights, musicians acquire certain moral rights.Footnote 89 First, in some jurisdictions composers acquire a right of first disclosure, which entails the right to divulge their work(s) to the public.Footnote 90 This right does not apply to performers, which is logical, given that the performance itself constitutes a disclosure thereof. Second, the right of paternity or attribution implies that both composers and performers may (dis)claim paternity of their work and/or performance.Footnote 91 Notably, performers’ right to paternity is limited by honest trade practices. By way of example, not all members of a symphony orchestra can claim acknowledgement on a CD cover or in the metadata of a digital music file. This privilege is reserved to the conductor, the concertmaster and possible soloists.Footnote 92 Even so, many instances of infringement of the paternity right arise, largely due to the poor quality of metadata.Footnote 93 The third moral right is referred to as the right to integrity. It implies that composers and performers may object to actions relating to their output that would bring them into disrepute.Footnote 94 In the music industry, cases regarding this moral right may, for example, relate to the combination of a pre-existing work or performance fixation with offensive lyrics.Footnote 95 Finally, German and French law provide for an express, albeit very limited, ‘right to repent’ for authors, as a result of which a composer may withdraw or retract their work subsequent to its initial disclosure – in other words, reverse the exercise of their moral right of disclosure.Footnote 96

The term of moral rights varies. This term is usually linked to the duration of the exploitation rights. This is the case in Belgium, Germany, the Netherlands and the United Kingdom, the latter with a caveat as to the right to false attribution.Footnote 97 By contrast, moral rights have no limitation in time under French copyright law and thus apply in perpetuity, for composers as well as performers.Footnote 98

If third parties want to use a musical composition, (a fixation of) a performance and/or a phonogram, consent must be acquired from the relevant right owner(s).Footnote 99 In this context, the distinction between exclusive rights and remuneration rights bears particular relevance.Footnote 100 This distinction applies to both copyright and neighbouring rights.

Exclusive rights may usually be transferred or licensed out. Consent is either granted on an individual basis or, optionally, through a collective management organisation (CMO). A CMO is an organisation tasked by their members-rightsholders with the management of their copyright or neighbouring rights through the grant of licences to third parties.Footnote 101 There is a large number of active CMOs.Footnote 102

The exclusive rights of composers include almost all of the mechanical rights and the performing rights set out above. This explains why voluntary collective management is of particular importance in the music publishing industry.Footnote 103 Performers only (initially and thus subject to further transfer) acquire the exclusive right to reproduce fixations of their performances, distribute these and make them available to the public.

In the context of optional (or ‘voluntary’) collective management, prospective users approach the relevant CMO(s) to obtain a licence relating to the exploitation rights of protected content. The user pays the rate set by the CMO, which retains a commission-based compensation for administrative costs and transfers the remainder of the fee to the rightsholder(s).

For the exploitation of remuneration rights, no express consent from the rightsholder(s) is required. Consequently, the relevant rightsholders do not have the opportunity to prevent the exploitation at issue. Instead, in such cases, a compulsory licensing system subject to mandatory collective management applies. An equitable remuneration is collected by CMOs and subsequently transferred to the rightsholder(s) after deduction of administrative costs. Remuneration rights are unwaivable.Footnote 104 Rental and lending rights are in principle both exclusive rights, but the EU framework leaves room for a qualification of the lending right as a remuneration right under national law.Footnote 105 As to the rental right, in case a transfer of this right occurs, an equitable remuneration through a system of mandatory collective management is required.Footnote 106

A larger proportion of performers’ rights has the status of a remuneration right compared with the rights granted to authors. This explains the importance of mandatory collective management in the recorded music industry. Indeed, in addition to the above, performers’ right to broadcasting and communication to the public of fixations of their performances in a phonogram are largely treated as remuneration rights (except for the making available right, which is an exclusive right).Footnote 107 This is referred to as the compulsory licence for secondary use.

The cable retransmission right has a particular status as an exclusive right that is nevertheless subject to mandatory collective management.Footnote 108 The equitable remunerations for private copying and reprography also occupy a specific position, since they function as compensation to the rightsholders for the harm inflicted through the application of private copying and reprography exceptions.Footnote 109 These two equitable remuneration regimes are also subject to mandatory collective management.

Musicians may transfer (or ‘assign’Footnote 110) their exclusive exploitation rights to third parties, be it a natural person or a legal entity.Footnote 111 Consequently, these rights have traditionally been divested to commercial players, with the copyright in musical works being assigned from composers to music publishers and the neighbouring right of performers to record companies for the entire term of protection.Footnote 112 In return, the initial rightsholder(s) usually obtain(s) a form of compensation, either by way of a flat fee or through recurring royalty payments.Footnote 113 As a result, most copyright is owned by corporations instead of artists.Footnote 114

As an alternative to the full transfer of rights, it is possible to grant a licence. Hereby, the counterparty obtains the right to use the object of the licence within certain limits, again usually in return for monetary compensation to the initial rights owner(s) – but not always, as is proven by open licences.Footnote 115 As opposed to a transfer of rights, which is always of an exclusive nature, a licence may be either exclusive or non-exclusive. In the latter case, the licensor(s) retain(s) the right to exploit the object of the licence and/or to grant other licences to third parties, who may then perform actions of exploitation in parallel with the initial licensee. Drawing the line between an exclusive licence and a transfer of copyright can be difficult.Footnote 116

In this book, contracts that establish a transfer of or a licence to the exploitation rights associated with works protected by copyright and/or fixations of performances protected by the neighbouring right of performing artists are referred to by the umbrella terms ‘copyright exploitation contracts’ or ‘exploitation contracts’.

The exploitation of a phonogram has an impact on both the neighbouring rights associated with said phonogram and the copyright in the underlying composition embodied in the phonogram. As a result, a single exploitation activity requires permission under both copyright and neighbouring rights law.Footnote 117

The exploitation of the exclusive rights associated with a jointly owned work and/or performance in principle requires express consent from all parties, especially if the individual contributions are not discernible. In such a case, a single rightsholder can stop others from exploiting the work and/or performance. To mitigate this, rules have been established that modulate the requirement of consent relating to live performances by large groups of performing musicians, such as orchestras or large chamber music ensembles.Footnote 118 These rules designate specific musicians as representative(s) of the group, allowing the possibility of efficient contracting in large live productions. The applicable regimes differ, from the appointment of soloists, directors and conductors (Belgium and the Netherlands) to group leaders (Belgium and Germany) or elected representatives (Germany).Footnote 119 While French and UK law do not appear to expressly regulate such situations, musicians may provide a mandate to another party for this purpose.

2.2.2.3 Interests

Several internal and external factors incentivise musicians to create and/or perform music.Footnote 120 The intrinsic wish to make music for the sake of personal developmentFootnote 121 and/or participation in cultural lifeFootnote 122 is a significant and primary driver,Footnote 123 but only constitutes part of the equation.Footnote 124 In addition, musicians are driven by a number of external incentives. A first important motivating factor is remuneration. This is especially true for professional musicians, whose income depends on music-related revenues.Footnote 125 However, this incentive applies across the board. Indeed, all musicians seek a certain degree of valuation of their work, of which proper remuneration constitutes an important part.Footnote 126 However, ‘money isn’t everything’.Footnote 127 Beyond the purely monetary self-interest, a number of non-economic external incentives play a role. Many of these incentives are covered by the broad concept of (self-)agency.Footnote 128 This includes, first and foremost, credit where credit is due.Footnote 129 Musicians want to receive acknowledgement for their work.Footnote 130 The value of music must not only translate into money, but also into attribution and ensuing personal recognition.Footnote 131 Second, musicians want their music to be heard. This implies access to audiences through exploitation of the work and the wish to build a relationship with their audience in order to nurture a fan base.Footnote 132 Third, agency may be associated with artistic integrity and reputation, as well as the wish to retain a certain degree of control over the exploitation of their work.Footnote 133 Both credit and reputation may be linked with moral rights protection – the right to paternity and integrity respectively.Footnote 134

Internal motives to make music and external incentives to achieve artistic and commercial success ensure a continuous stream of hopeful music market entrants, forming a supply that significantly outstrips demand.Footnote 135 The consequences of this mismatch between supply and demand on artist income are palpable.Footnote 136 Several authoritative research projects may be mentioned, such as the study conducted by Dutch Institute for Information Law (IViR).Footnote 137 That study pointed towards an average net annual income of composers in the EU per country between approximately €15,000 and €45,000 – the higher numbers being due to a number of significant outliers.Footnote 138 The corresponding figures for performers lay between approximately €4,000 and €16,000.Footnote 139 More recently, reference may be made to the 2023 Musicians’ Census in the United Kingdom, which found the average annual income from music work to be around €24,000.Footnote 140 In many cases, the income of musicians appears to lie below the minimum wage level, and certainly below the median wage level in the jurisdictions researched in the context of this book.Footnote 141

As regards the position of musicians vis-à-vis other legitimate interests, three aspects are noted. First, there is an inherent, inescapable tension between the protection of the commercial interests of musicians and those of their corporate partners. Second, musicians attach great importance to the way in which they are perceived by users.Footnote 142 Third, and importantly, the heterogeneity of the group of musicians implies a large variety of perspectives and interests, which appear to overlap only partially. The fault line runs along the boundaries of the concepts of authorship and performance and the ensuing distinction between copyright sensu stricto and the neighbouring rights of performing artists. The interests of composers and performers are not necessarily aligned. Since both categories receive a part of the same ‘pie’, there is a persisting belief that increased focus on one subset of the broad category of musicians will lead to the other subset losing out.Footnote 143 Moreover, the categories of authors and performers are themselves quite fragmented, given the large amount of and variety within the cultural and creative industries (CCIs) as well as cultural differences between different (national or regional) territories.Footnote 144 Finally, for the category of performers, a significant divergence exists between the small number of well-known featured artists and the vast majority of relatively anonymous session musicians, orchestral musicians and self-releasing artists, with the former being seemingly inclined to align their views with the interests of corporate partners.Footnote 145 Musicians have therefore traditionally found it difficult to speak with a unified voice. This contributes to an underrepresentation of their interests in the music industry debate.

The primary objective of continental copyright sensu lato is to protect and stimulate creativity.Footnote 146 Artists are at the centre of copyright and neighbouring rights protection.Footnote 147 Only they are granted the initial right to exploit their work.Footnote 148 Moreover, the ‘high level of protection’ that serves as a guiding principle for EU copyright law refers to the rights of artists, whose ‘independence and dignity’ must be safeguarded.Footnote 149 While the importance of internal incentives should be acknowledged, the primary objective of copyright protection is to further the external incentives for musicians to make music. This implies due attention to monetary as well as non-monetary aspects, to both agency and remuneration.

2.2.3 Corporate Partners

2.2.3.1 Typology

On the more commercially inclined side of the music industry, there is a wealth of individuals and (mostly) companies that perform a diverse array of intermediary services. Throughout this book, they are indicated as corporate partners.

A first important player is the music publisher, who grants licences to content providers for the use of original musical compositions in a commercial context, either directly or via a CMO.Footnote 150 This includes (part of) the copyright in the composition or a licence from the composer(s).Footnote 151 The tasks of a music publisher include pitching a piece of music to record companies, to facilitate its recording or to incentivise covers of it, contacting radio stations to ensure airplay, promoting synchronisation of the music with music supervisors, and so forth.Footnote 152 Traditionally, music publishers have also been in charge of the commercialisation of sheet music.Footnote 153

The music publisher must acquire the exploitation rights necessary to provide licences to third parties from the composer(s), either in the form of a (partialFootnote 154 and/or temporary) transfer of the composer’s copyright or in the form of a licence.Footnote 155 Exploitation agreements entered into between a composer and a publisher may take various different forms. While a ‘title agreement’ is limited to the rights in one or more specific pre-existing compositions, a (usually exclusive) ‘songwriter agreement’ or ‘exclusivity agreement’ relates to works that have yet to be composed during a specific time period.Footnote 156 It is also possible to limit the publisher’s intervention to the administration of copyright revenue and call upon the services of a PR company for promotion and marketing purposes.Footnote 157 In the context of such an ‘administration agreement’ with a publishing administrator, the composer retains their copyright and the music publisher only acquires a licence.Footnote 158 Such arrangements are becoming increasingly common.Footnote 159 Composers are in no way obliged to enter into an agreement with a music publisher and may decide to perform the activities of a music publisher themselves.Footnote 160 The composers then retain their rights.

A relatively new player seeking to disrupt music publishing is Hipgnosis,Footnote 161 an investment company that purchases music publishing rights directly from (primarily established) artists and allows investment in their catalogue in a way similar to a stock or asset portfolio.Footnote 162

Second, the record company or (record) label invests in the discovery and development of musicians, as well as in the production and distribution of phonograms.Footnote 163 An important division in a record company is often called A&R (Artist & Repertoire), which focuses on the discovery and signing of artists.Footnote 164 The record company is usually responsible for the production of phonograms, the manufacture of physical copies (if applicable), physical and/or digital distribution (the latter through digital service providers (DSPs)) as well as promotion and marketing of the finished product.Footnote 165 It functions as an investor and risk aggregator.Footnote 166 In this capacity, a record company acquires a neighbouring right as a producer of the phonogram(s) at issue.Footnote 167

Exploitation contracts with record companies take various different forms. The traditional contract model is a so-called record contract or artist deal. This exclusive deal usually entails a full transfer of rights from the musician to the record company, in return for monetary compensation.Footnote 168 In recent years, an evolving practice may be discerned, whereby musicians have more margin for negotiation and may agree on a rights transfer that is limited in time or sign an exclusive or non-exclusive licence or distribution contract.Footnote 169 For session musicians, buyouts – with a full transfer of exclusive rights against a modest one-off fee – are still the norm.Footnote 170 Finally, as is the case for music publishing, it is not mandatory for a musician to enter into a contractual relationship with a record company.

Digitisation has given rise to a new type of corporate partners, namely DSPs, a broad category of providers of services that are provided digitally, via the internet. Examples of DSPs include online content and/or social media platforms (such as YouTube, Spotify, FacebookFootnote 171), digital aggregators (for example, TuneCore, CD BabyFootnote 172) and their counterparts, music publishing administrators (such as TuneCore Publishing, CD Baby ProFootnote 173), the latter two aiding in the online distribution of recorded music and the administration of composition royalties respectively.

A final, very broad category of relevant corporate partners includes managers, concert promoters, distributors, entertainment lawyers and booking agents.Footnote 174 Among the corporate partners in this final, broad category, the manager holds a privileged position, being the corporate partner whose interests are the most closely aligned with those of the musicians they represent.Footnote 175 Indeed, a music manager’s income is usually made up of a percentage of the revenues amassed by ‘their’ musician(s). Thus, the manager sits on the fence between the artistic and commercial sides of the music industry.Footnote 176

This book uses the umbrella term music value chain to refer to musicians and their managers, music publishers, record companies, CMOs, digital aggregators and music publishing administrators. Managers, publishers, record companies, CMOs, digital aggregators and music publishing administrators are referred to as music industry corporate partners. Other corporate partners are referred to as external corporate partners.

2.2.3.2 Rights

Music producers are to be distinguished from the legal concept of ‘producer’ under copyright law sensu lato. The WPPT defines a producer of phonograms as ‘the person, or the legal entity, who or which takes the initiative and has the responsibility for the first fixation of the sounds of a performance or other sounds, or the representations of sounds’.Footnote 177 A ‘phonogram’ refers to ‘the fixation of the sounds of a performance or of other sounds, or of a representation of sounds, other than in the form of a fixation incorporated in a cinematographic or other audio-visual work’.Footnote 178 The sounds at issue must not necessarily relate to a work that is protected by copyright – in other words, the phonogram’s content is, as such, irrelevant.Footnote 179 In the music industry, the status of producer of a phonogram accrues to the record company, unless the musicians themselves take this position. DIY (do-it-yourself) musicians may be qualified as producers and thus acquire rights in that capacity, in addition to their status as performing artists.Footnote 180 The neighbouring right granted to producers of phonograms protects financial investments in phonograms.Footnote 181 Such investments are considered to be high in both amount and risk and necessary to secure the creation of new content.Footnote 182

A particularity of UK law are the special provisions relating to exclusive recording contracts – contracts with a performer that exclusively entitle a person to record certain performances with a view to their commercial exploitation.Footnote 183 Record companies that qualify as such persons acquire rights under UK law similar to certain rights granted to performers.Footnote 184

2.2.3.3 Interests

The music industry is characterised by an inherent tension between the legitimate interests of musicians and those of their corporate partners.Footnote 185 While the former have a primordial interest in the dissemination of their music, the latter are primarily interested in their ultimate return-on-investment.Footnote 186 The revenue ultimately accruing to corporate partners does not flow to musicians and vice versa. Put somewhat crassly by former industry executive Walter Yetnikoff: ‘Most of the majors are in the fast food business and the artists are hamburgers.’Footnote 187 The interests of both sides dictate a struggle for a bigger proportion of total revenues. Corporate partners have a clear and justifiable interest in keeping the level of regulation down and maintaining the status quo for revenue distribution.Footnote 188 Their emphasis on the importance of freedom of contract is unsurprising and, moreover, legitimate.Footnote 189 Indeed, if the price demanded in the context of contract negotiations is too high, demand drops and everybody loses out – including musicians.Footnote 190

Given their essentially commercial focus, the perspective of music industry corporate partners on musicians (and users) is largely driven by the laws of supply and demand. As a result, they more readily accept the music market’s winner-takes-all tendencies.Footnote 191 Their business models leave no room for mediocrity and/or lack of success.Footnote 192 Corporate partners have an interest in acquiring a considerable share of the revenues garnered by an artist that has struck gold and in retaining that artist’s ‘services’ for as long as possible.Footnote 193 By contrast, corporate partners are likely to seek to drop artists that have proven to be less lucky and not be required to exploit their (unsuccessful) music.Footnote 194

The broad category of music industry corporate partners lacks homogeneity. Not only is the wealth of intermediary functions mirrored by a variety of business models, the relevant corporate partners also show an impressive range of structures and sizes, from a one-man show to mammoth multinational media conglomerates. Contrary to what is the case for musicians, however, it appears that this heterogeneity has not translated into a lack of leverage in the legislative process. Instead, the major rights owners have played an important role in the push towards greater protection of copyright over recent decades.

The position of corporate partners corresponds with the objective of the neighbouring rights of producers of phonograms.Footnote 195 While copyright’s primary theoretical focus lies with the creative incentives of artists, the added value of actively risk-taking commercial intermediaries should be acknowledged, and met with the opportunity to obtain an equitable return on investment and a reasonable profit margin.Footnote 196 To this end, music publishers and record companies must be able to acquire the rights necessary to effectively exploit a composition and/or a phonogram and retain a proportion of the revenues garnered through such exploitation.Footnote 197 The inherent uncertainty present in CCIs such as the music industry already makes for a tricky investment climate. The revenues obtained from successful hits serve as a subsidy for failed releases and as much as 90 per cent of all released music fails to break even.Footnote 198 Thus, disappointing financial results for musicians may be due to the ‘unfavourable economics of the music industry’Footnote 199 as much as to instances of unfairness in music contracts. Due care must be shown not to overemphasise either the perspective of musicians or their corporate partners. The perverse effect of far-reaching protective mechanisms would be a sharp decrease in corporate partners’ activity, which could in turn be detrimental to cultural diversity and musicians themselves.

Similar to the case of musicians, the structure and size of a corporate partner significantly affect their market position and bargaining power, vis-à-vis both musicians and external corporate partners. The heterogeneous nature of the category of corporate partners should be borne in mind. Particular reference may be made to the status of small and medium-sized enterprises (SMEs).

2.2.4 Users

The value of music is limited without its audience. Therefore, due account must be taken of the legitimate interests of users. This is all the more so given the rise of user-generated content (UGC) and the ensuing difficulty of drawing a line between mere consumers of analogue and/or digital music and actual creators – and thus potential copyright owners.Footnote 200 First, users have a clear interest in obtaining convenient, cheap access to protected content as well as legal certainty as to the licit nature of their activities.Footnote 201 Freedom of expression is paramount.Footnote 202 A second incentive, which mainly applies to active music fans and less so to mere passive listeners, is the wish to connect with music and the people behind it.Footnote 203

The position of users may be linked with the secondary objective of copyright to ensure the dissemination of creative works and the ensuing access to them.Footnote 204 This objective may be linked to the socio-cultural right to participate in cultural life and ‘enjoy the arts’.Footnote 205 As opposed to the debate on the appropriate balance between copyright and consumer rights such as freedom of information and expression and the right to participate in cultural life, the legitimate interests of users only play a background role in the debate surrounding the contractual dynamics within the music industry. Even so, many users attach a certain degree of importance to the remuneration of artists, in line with humankind’s instinctive inclination towards the underdog.Footnote 206 A copyright framework that places due stress on the position of the artist may benefit from enhanced societal legitimacy.Footnote 207 Therefore, it is important to ensure awareness as to the division of ownership and value within the music value chain.Footnote 208 Users who feel that revenue garnered through licit exploitation of protected content largely accrues to commercial corporations might view copyright protection as illegitimate and could potentially have a larger incentive to resort to online piracy as a form of civil disobedience.Footnote 209 Moreover, increased cultural diversity stemming from a healthy music ecosystem would benefit users’ access to music.Footnote 210

2.3 The Music Value Chain in the Streaming Age

2.3.1 Digitisation in the Music Industry

An analysis of the music industry in the streaming age would be incomplete without a brief glance at the first stages of digitisation that preceded this (r)evolution.Footnote 211 At the turn of the millennium, the widespread use of the internet, allowing for reproductions of protected works and/or performances to be instantly transferred across the globe through peer-to-peer (P2P) file-sharing, led to uncurbed piracy of artistic content. While the direct link between illegal file-sharing and the sharp decline in physical record salesFootnote 212 is disputed by some,Footnote 213 it is difficult to deny the difficulties of the recorded music industry in particular during that period.Footnote 214 The figures do not lie: in 2020, global revenues from physical music sales were five times lower than in 2001, while the global recorded music industry lost over one-third of its total revenues in the 2001–2014 period.Footnote 215 The music industry was left wondering how it could bend the forces of digitisation to its will. Continuing losses in analogue music sales were only offset by the rise in digital revenues in 2015, over a decade later.

On the music industry’s side, it was repeatedly argued that the widespread use of the internet led to an ‘everything is free culture’, in which it became more and more difficult to monetise artistic content.Footnote 216 When the first digitisation wave hit, record companies in particular took a primarily negative view and were slow to adapt to the newfound digital reality.Footnote 217 On the other side, pitted squarely against the vested interests of the music industry, were the proponents of a free internet.Footnote 218 From their perspective, online file-sharing presents itself as an opportunity to enhance access to creative content at a lower price – and, ideally, even for free.Footnote 219 These diametrically opposed positions clash vehemently, not least regarding copyright enforcement and the legislative reform that took place as a response to digitisation and the rise of online piracy.

The instinctive reaction of the media industries to online piracy was to double down on copyright enforcement. Initial efforts focused on the repression of piracy by private users, such as through the threat of criminal sanctions.Footnote 220 Graduated response strategies such as the ‘three strikes and you’re out’ approach vis-à-vis illicit file-sharers were the subject of intense discussions in the first decade of the millennium.Footnote 221 Gradually, the industry’s enforcement focus shifted to internet service providers (ISPs), obtaining injunctions against piracy websites such as The Pirate Bay and MegaUpload, and suing new DSPs.Footnote 222 Moreover, as a rule, online content platforms now provide ‘notice and take down’ procedures (for example, Content ID on YouTube) allowing rights owners to put a stop to particular instances of online copyright infringement. The next step is ‘notice and stay down’ procedures, whereby infringing content is taken down and subsequently prevented from being re-uploaded to the platform.

Over the years, several regulatory options have been explored, ranging from stronger enforcement of existing copyright rules over the introduction of new rules to the abolition of copyright altogether.Footnote 223 However, the vast amount of interests involved made – and make – for a strenuous legislative process with intensive lobbying.Footnote 224

Major rightsholders have traditionally been able to retain the upper hand, leading to a gradual but obvious increase in protection.Footnote 225 By contrast, the interests of musicians and their audiences have traditionally remained underexposed.Footnote 226 The significant increase in the term of protection over the past few decades serves as a first example. The term extension for phonograms mainly benefited the major record companies.Footnote 227 The same appears to be true for the exclusive making available right, which is usually transferred from the initial owners to their corporate partners.Footnote 228 A third notable legislative evolution spurred by digitisation and again heavily influenced by lobbyists was the establishment of anti-circumvention laws regarding digital rights management (DRM).Footnote 229 Finally, a more recent legislative evolution in the field of copyright law is the adoption of the Digital Single Market (DSM) Directive at the EU level and its ensuing implementation into Member State law.Footnote 230

The music industry’s reactionary attitude in the first stages of the internet revolution has given way to resilience and resourcefulness. While the internet revolution was first only perceived as a threat, the focus broadened to mining the opportunities presented by the new digital reality and monetising music online. This led to the development of numerous new business models, with the establishment of new digital players and a significant impact on consumer consumption patterns.Footnote 231

The first notable development was the establishment of the ‘some rights reserved’ Creative CommonsFootnote 232 (CC) licences in 2001. The next was the development of digital downloads, whereby users buy a licence to a digital copy of a music file that is then permanently downloaded to the user’s personal device(s).Footnote 233 Downloads have a bearing on both mechanical rights and performing rights (in particular the right to making available).Footnote 234 Further, while users may download entire albums, in reality there was a notable shift to unbundling of such albums and a propensity toward single-track downloading.Footnote 235

Both MusicNet and PressPlay, the legal digital music services set up by record companies at the beginning of the 2000s, failed, leaving ample room for new business models.Footnote 236 The first to rise to the occasion of providing users with a sound legal alternative to online piracy was Apple’s iTunes store, which launched in 2003 and was ultimately shut down in 2019 to the benefit of streaming service Apple Music.Footnote 237 In theory, iTunes provided a greater opportunity for musicians to reach their audience directly, bypassing traditional intermediaries. This potential for disintermediation went by largely untapped, with network effects favouring the commercial interests of major record companies.Footnote 238 Moreover, independent musicians could not directly upload their music to iTunes. This led to the emergence of online distributors such as CD Baby and The Orchard, which still exist.Footnote 239

The gap left by iTunes allowed for the emergence of new models in subsequent years. These saw the establishment of, for example, YouTube (2005), the online platform that enables users to upload and stream video content. This in turn led to the emergence of the concept of UGC, whereby users can create and share their own content, thereby becoming artists in their own right. UGC is still on the rise: it is impossible to keep track of the growing number of blogs, podcasts, social networks and other mediums used to share photos, videos and music. As a result, the line between ‘makers’ and ‘consumers’ of musical content is growing ever thinner. However, the most viewed videos on YouTube are and have almost always been those provided by traditional media, often the major record companies.Footnote 240 Moreover, YouTube has traditionally been completely free for users. Consequently, this did not counter the global decline in music sales. Again, there was room for innovation, which led to the rise of music streaming services.

The term ‘streaming’ refers to a method of transmitting or receiving data, such as audio and/or video material, without actually downloading any media files.Footnote 241 The data flows through the network in a continuous way, allowing the consumer to start viewing and/or listening to the content while the remainder of the data is still being received. As is the case for downloads, streaming has a bearing on both mechanical rights and performing rights (in particular the making available right).Footnote 242 While the stream itself primarily constitutes a communication to the public – a form of making available – streaming also entails a technical reproduction from the source file to the DSP’s server. In addition, many DSPs allow users to save – and thus copy – certain songs to their personal (offline) library.Footnote 243 Finally, the (partial) reproduction of lyrics, which occurs on some streaming services as the song is played, also constitutes a copyright-relevant act, with a bearing on the right of reproduction of the owner of the copyright in the lyrics.

The rise of streaming indicates the advent of a post-ownership mentality on the part of users, whereby access to music, by ‘renting’ it through a streaming platform for example, is seen as more important than actual ownership of a physical CD or a digital MP3 file. In other words, the sale of music is seeing a shift from product to services, from ownership to access. Users no longer feel the need to secure a physical and/or digital copy of artistic content, but rather opt for convenience and unlimited, real-time access.Footnote 244 This shift from ownership to access also implies another change. While the focus used to lie with securing a successful, high-sales launch for new music, the aim now is to build an audience and achieve sustained listening over time rather than immediate success, since each listen is connected with economic value.Footnote 245 This explains the rising importance of catalogues in the music streaming market, which is further underscored by the notable spike in catalogue acquisitions, including deals regarding the music of David Bowie, Bob Dylan, Bruce Springsteen and Sting.Footnote 246 Moreover, streaming entails yet a further shift away from albums and toward single tracks.

Streaming services now constitute the main driver for revenue growth in the music industry. While there are a number of big streaming platforms, including Spotify,Footnote 247 Apple Music, Tencent Music and Amazon Music, the diversity that is available on the music streaming market is notable.Footnote 248 While SoundCloud is known for its pioneering shift to the user-centric model,Footnote 249 Napster (formerly Rhapsody, the first ‘real’ music streaming serviceFootnote 250) and Qobuz seek to distinguish themselves by offering both digital downloads and music streaming, Tidal focuses on sound quality, iHeartRadio offers radio, streaming and podcasts, and Resonate uses a ‘stream-to-own’ model.Footnote 251 Niche streaming services, such as Idagio and Primephonic for classical music, are also available.Footnote 252 Moreover, most streaming services offer a wide variety of options for users, ranging from fully ad-supported services to a variety of subscription models with multiple price tiers.Footnote 253 Prices for music are now being set by DSPs instead of by the music industry itself – a seismic shift set in motion by iTunes.Footnote 254

The shift towards music streaming affects the music that people listen to and thus also the music that is composed, performed and recorded. First, the importance of streaming playlists that guide users through an oversupply in music is noted.Footnote 255 While some playlists are actively curated by DSPs, others are generated through automated recommendation systems based on perceived user preferences.Footnote 256 Second, the fact that rightsholders only receive royalties for music that is streamed for at least thirty seconds negatively affects certain musical genres where lengthy pieces are the norm – such as classical music and certain types of electronic dance music (EDM) – and has a direct impact on the structure of new music.Footnote 257 Songs are generally shorter, with early choruses and interventions by famous featuring artists instead of lengthy buildups.Footnote 258 The objectives for rightsholders are clear: find a way into a successful playlist, grasp people’s fleeting attention and maintain it for at least thirty seconds.

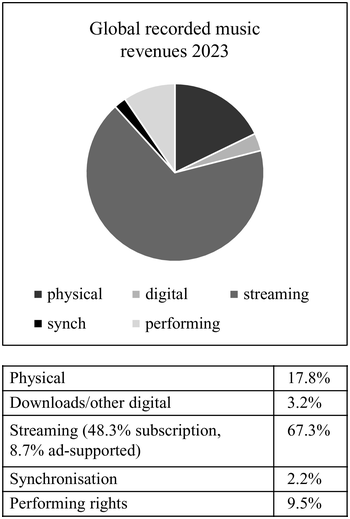

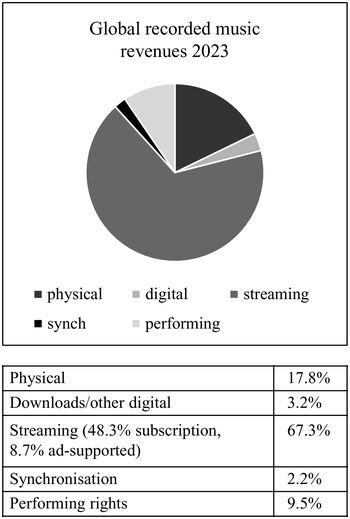

In addition to the rise of streaming, the past decade has also seen an increase in revenue from synchronisation rights.Footnote 259 This refers to fees paid in return for rightsholders’ permission to link audio and video in order to use music in the context of advertising, film, games and TV.Footnote 260 The required permission relates to the exclusive right of reproduction of composers, performers and producers of phonograms, and thus has a bearing on the total revenues of both the recorded music and music publishing sectors.Footnote 261 Synchronisation deals are highly fact-specific and the conditions for them are usually subject to stringent confidentiality requirements.Footnote 262

2.3.2 The Majors’ Place in the Recorded Music and Music Publishing Sectors

Our focus now shifts to the structure of the music value chain in which contracts between musicians, record companies and publishers are embedded. Three main layers may be discerned: the levels occupied by the majors, the independent corporate partners and the independent artists.

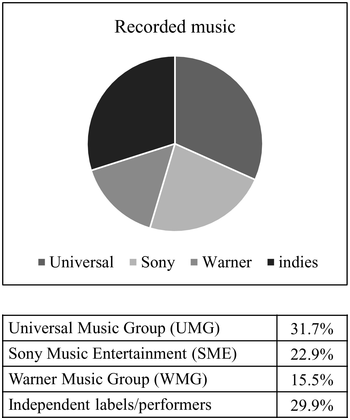

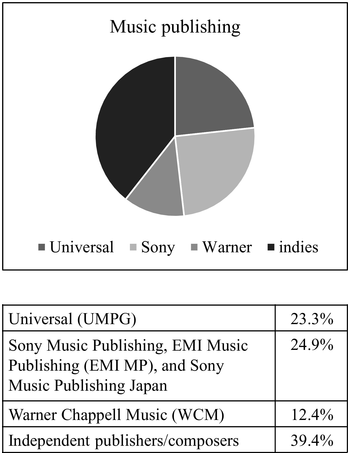

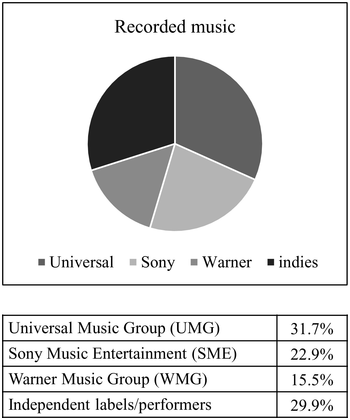

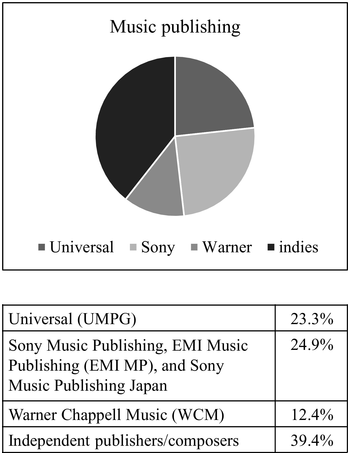

The recorded music and music publishing sectors are characterised by a significant degree of concentration and centralisation of power. The major record companies (or ‘majors’), who have traditionally enjoyed a significant degree of power in the music industry, have cemented their place at the table through horizontal as well as vertical integration.Footnote 263 On the horizontal level, the three remaining majors, namely Sony, Universal Music and Warner Music, hold a combined global market share of almost 70 per cent in the recorded music market at the time of writing.Footnote 264 From a vertical perspective, all three of these major labels have a music publishing division alongside functioning as a record company.Footnote 265 This means that, in addition to serving as a risk aggregator that provides money for the development of aspiring artists, these labels play an active role in monetising creative content for licensing purposes. Together, the music publishing divisions of the majors hold a market share of almost 60 per cent.Footnote 266 Signing a contract with the record division of a major may imply an inevitable publishing deal with the same major music company. On various occasions, the majors go even further and acquire partial or even full ownership of ‘new’, digital intermediaries in the marketing and distribution sector.Footnote 267

The higher the degree of consolidation and centralisation of power, the more difficult it is for musicians to run their musical careers in a purely independent manner. Buyer power is susceptible to abuse on the part of those wielding it.Footnote 268 Major corporate partners can leverage their catalogue and use their strong market position to force disadvantageous and inflexible deals on musicians. The apparent omnipresence of SpotifyFootnote 269 and the rise of curated streaming playlists has consolidated and even augmented the market power of the majors.Footnote 270 Industry powerhouses are simply much better placed than independent artists to get ‘their’ music onto such playlists. They have the marketing budget required to pay for extensive promotional campaigns and may moreover leverage the success of their catalogue.Footnote 271 Artists with the backing of a major label can therefore reach a broader audience on streaming services. In turn, this ensures the majors’ future leverage, even though the protection for some of the popular back catalogue held by the majors is on its last legs.

Thus, instead of democratising the music industry, streaming appears to have led to a replication of traditional music industry dynamics. Such practices may be likened to the now illegal practice of ‘payola’, whereby radio DJs were paid to play certain songs on the radio.Footnote 272 Direct ties between streaming services and the majors in the form of ownership stakes give an additional reason for concern. Finally, the power of the majors is also consolidated through the technique of direct licensing between DSPs and major rights owners, which has led to the (partial) withdrawal of their catalogues from voluntary collective management. This has unfavourable consequences for independent artists and small corporate partners. They have neither the resources nor the leverage to engage in direct licensing themselves and are left with CMOs that are less potent due to the withdrawal of major right owners’ repertoire.Footnote 273 Thus, music industry concentration risks negatively impacting cultural diversity.Footnote 274 In practice, therefore, the majors still play a vital role in deciding on the scope and modalities of exploitation of a work/performance – as well as the ensuing remuneration – by entering into contracts with providers of musical content, such as online content platforms, to which musicians are not a party.Footnote 275 The market power of a rightsholder is inversely proportionate to its accountability vis-à-vis musicians, DSPs and CMOs alike. The possible preventive intervention of merger control is noted in this context, as well as the potential application of the prohibition on abuse of (individual or collective) dominance of major media conglomerates under Article 102 TFEU.Footnote 276

2.3.3 The Rise of Independent Music Companies

In addition to the majors, there is a large number of independent music companies, which are generally referred to as the ‘indies’.Footnote 277 The market share of such independent companies is rising.Footnote 278 Among big indie names in the recorded music sector are Beggars Group (including labels such as Rough Trade and XL Recordings) and BMG, while two of the biggest independent music publishing administration companies are Kobalt and Peermusic.Footnote 279

Independent music companies usually operate on a more limited territorial basis than the majors and moreover do not have the benefit of vertical integration, in the sense that they do not include a distribution division.Footnote 280 In order to overcome this, many indies have entered into a distribution or partnership deal with one of the majorsFootnote 281 or make use of the wide array of so-called artist and label services.Footnote 282 Such arrangements are to be distinguished from seemingly independent record companies that are in fact subsidiaries of major record companies.Footnote 283 Once an independent label becomes particularly successful, a takeover by a major may be around the corner, past examples being the acquisition of independent labels Motown, Island and Virgin.Footnote 284

Another notable development in the independent music sector over the past few decades is a marked increase in cooperation. On the European front, reference may be made to the Independent Music Companies Association (IMPALA), a non-profit trade association that represents the interests of both independent record companies and music publishers, for example by opposing further consolidation of the majors.Footnote 285 Independent music bodies such as IMPALA are linked on a global level through the Worldwide Independent Network (WIN).Footnote 286

In addition, the indies’ answer to the rise in direct licensing on the part of the majors in the recorded music sector was the establishment of ‘Merlin’, a direct licensing entity for digital use that represents around 15 per cent of the total recorded music market at the time of writing.Footnote 287 It seeks to level the playing field vis-à-vis DSPs and allow independent music companies to compete with the majors in their dealings relating to digital rights by way of a collective licence, thus enhancing the value of independent music.Footnote 288 Now that Merlin has matured into an established market player, the indies’ objective is to further expand the scope of cooperation within the Merlin network, such as by developing analytical tools on the basis of customer data. For music publishing, reference may be made to IMPEL (which stands for Independent Music Publishers European Licensing), which seeks to fulfil a similar role to Merlin, but for mechanical music publishing rights.Footnote 289

2.3.4 Independent Artists and Artist and Label Services

It has been argued repeatedly that technological developments will bring – and to a certain extent already have brought – an end to the need for ‘middlemen’ in the music industry.Footnote 290 The promise of disintermediation challenges the traditional music value chain and seeks to empower musicians on the global music market. Using the opportunities that the internet has to offer, musicians can indeed mine a new, broad and diverse audience via the so-called celestial jukeboxFootnote 291 of streaming services, enter into direct contact with their listeners, get involved in the production, marketing and distribution of music, as well as build and maintain their own global audience.Footnote 292 Several established mainstream artists have already taken to distributing their music directly to fans.Footnote 293 Additionally, the (apparently faltering) interest in the opportunities offered by blockchain technology and smart contracts has led to an explosion of startups promising a disintermediated online music market where musicians automatically and quasi-instantly receive 100 per cent of royalty payments in a fully transparent way.Footnote 294

However, the growing DIY mentality appears not to have led to large-scale disintermediation in practice.Footnote 295 The combined market share of majors and indies is significant, as is the catalogue leveraged by those commercial players vis-à-vis DSPs.Footnote 296 Mainstream commercial DIY success appears to be largely reserved to artists that have already achieved popularity under the wings of a corporate partner.Footnote 297

In addition, a form of ‘re-intermediation’ may be identified, whereby DSPs have crafted their place next to the major record companies and assumed an identity as new barriers to entry for independent artists.Footnote 298 True disintermediation is, as yet, a mirage, with new ‘middlemen’ having squarely positioned themselves on the online music market. Reference may be made to social media and content platforms,Footnote 299 leading music blogsFootnote 300 and digital distributors.Footnote 301 While the online environment initially presented itself as a way to foster a direct relationship with fans (direct to consumer or D2CFootnote 302), many DSPs provide no such direct access for truly independent artists, with the exception of DIY platforms such as SoundCloud.Footnote 303 Instead, artists who seek to add their music to a DSP’s catalogue for exploitation purposes call upon the services of digital distributorsFootnote 304 (for phonograms) and publishing administratorsFootnote 305 (for compositions) that serve as go-betweens and allow DIY artists to monetise the use of their music by DSPs, again usually in return for a commission-based remuneration.Footnote 306

Even so, the digital context appears to be more favourable to independent artists than the analogue world. While artist independence used to be associated with an inability to get signed – and thus access an audience – it is now increasingly linked with empowerment and the possibility to enter into partnerships with a wide variety of service providers, under contract terms that are more tailored to the artist’s needs and without excessive rights transfers.Footnote 307 These new types of intermediaries are grouped under the umbrella term ‘artist and label services’ (ALS). Notably, both majors and large indies acknowledge the worth of such new business models and now also offer ALS to a certain extent, either directly or through subsidiaries.Footnote 308 Thus, artists who would prefer to eschew a contractual relationship with a major music company may in practice call upon the services of ALS companies that are owned by majors.Footnote 309

Instead of entering into a full-service contract, artists may pick and choose the services they require, depending on their goals and the specificities of their career. Services offered include marketing and promotion, financing, distribution, music publishing administration, and so forth. ALS may also be combined with a partnership contract with an independent music company. In such a case, the deal between musician and corporate partner may be characterised as a business partnership based on a services model, whereby artists retain their rights and thus control over their work, while the corporate partner only acquires a licence.Footnote 310 Independent artists who seek to become global superstars are likely to take the leap to a deal with either a big independent music company or one of the three majors at some point, in a bid to achieve global exposure.Footnote 311 An investment on the part of one of the major music companies is likely to depend on pre-existing viral and/or commercial success garnered through prior investment of the artist(s), collaborating music producer(s) and/or their manager.Footnote 312 This puts a slightly different light on the traditional function of such initial corporate partners as an investor and thus a risk-taker.Footnote 313

At the fully DIY side of the spectrum are direct support, crowdfunding, pay-per-play and purchase sites, such as Bandcamp, Patreon, Resonate, Sonstream and SoundCloud.Footnote 314 Artists fully retain their rights and pay a modest commission-based fee to the online platform. Such platforms may function as fruitful ‘hunting grounds’ for the A&R departments of record companies.

DIY composers, digital distributors and publishing administrators may call upon the services of ALS companies that focus on monetisation and royalty managementFootnote 315 or content and data tracking.Footnote 316 ALS companies may also provide a full service akin to but conceptually separate from a record company.Footnote 317 A common thread is an increased reliance on and faith in technology such as big data and artificial intelligence (AI), whereby technological developments are seen as a choice opportunity to increase efficiency and (distribution of) revenues.

Musicians dispose of a vast range of tools to acquire and maintain their (online and offline) audience. Significant barriers to entry have disappeared. However, the wide availability of these tools implies fierce and unrelenting competition to get and maintain audiences’ attention.Footnote 318 Users are faced with a veritable ‘tyranny of choice’, where navigating a way between the millions and millions of available songs becomes simply impossible.Footnote 319 The road to artistic and commercial success is paved with uncertainty.Footnote 320 Moreover, in the fast-paced environment of the music industry, a lack of quasi-immediate success risks equating to equally rapid failure.Footnote 321 Many variables are at play, not all of which are directly related to musical quality. Both luck and leverage have a role to play.Footnote 322 Leverage, the latter factor, may be linked to the lasting market power of the major music companies. Moreover, the limited size of the catalogue held by an independent, DIY musician in itself carries significant disadvantages in the context of contractual negotiations with DSPs. Indeed, the combination of an oversupply of music with a fragmentation of repertoire on the supply side negatively affects the leverage of smaller, independent industry players. This logic applies to both DIY musicians and small independent corporate partners. This situation is exacerbated by the rapid evolution on the music ‘market’: since today’s hype may already be forgotten tomorrow, smaller players risk falling behind. As a result, artists are left with a dilemma: either they choose the DIY or ALS way and are likely to collect fewer total streams but a higher proportion of streaming revenue, or they seek a major label record deal that may potentially lead to much more streams in total, but a significantly lower proportionate return in terms of streaming revenue.

Moreover, the music industry is inherently structured as a ‘superstar’, ‘winner-takes-all’ economy.Footnote 323 There is a small number of global superstars, whose situation starkly contrasts with the large majority of musicians who struggle to make a living, who suffer from the casualisation of creative labour in the so-called gig economy – coincidentally, musicians may be qualified as the ‘original’ gig workers – and whose (legal) situation is precarious.Footnote 324 This situation is enhanced by network effects and a tendency towards the mainstream.Footnote 325 The increased use of automated recommendation systems for music streaming based on prior listening data risks further exacerbating this evolution, since such playlists may function as an ‘echo chamber’ that makes it harder to discover new music and, moreover, entail a risk of discrimination on the basis of nationality, gender and genre.Footnote 326 There is an ensuing risk of barriers to entry for emerging artists, of decreasing diversity and of a reduction of the cultural landscape. However, recently, a trend is noted towards a consumption model that favours diversity and local artists singing in their own language rather than purely focusing on global Anglo-American superstars.Footnote 327 This evolution runs parallel with the slightly increasing market share of independent record companies and DIY artists. In view of this, it has been argued that, in order for the majors to retain their pole position, a transformation of their business model is required, including a primordial focus on all things digital and a more balanced, empowering relationship with artists. The first stages of such a shift are already visible, such as in the artist-friendly deal between US singer-songwriter Taylor Swift and (a sub-label of) Universal, according to which Swift retains ownership of the rights in phonograms of her new music.Footnote 328

2.4 Remuneration in the Streaming Age

2.4.1 Revenue Streams in the Streaming Age

Following the outline of the music value chain in the streaming age, we move on to an analysis of the revenue streams that flow from the exploitation of rights in music for the recorded music and publishing sectors.