Key messages

Chapter 1.3 considers voluntary health insurance (VHI). VHI is paid for privately by or on behalf of individuals and most often provides people with faster access to treatment and greater choice of health care provider. Premiums are not typically based on the policyholder’s income but are likely to vary depending on their risk of ill health. Key learning includes that:

Despite prepayment and risk pooling, VHI has limitations and does not align well with progress towards universal health coverage (UHC) because:

○ risk pools in VHI schemes are typically much smaller than pools established through statutory schemes, which means there are fewer people to share risk;

○ inequities are created because of the cost of premiums, which may not be affordable or accessible to everyone, including those most in need of financial protection.

VHI has wider equity implications because it offers those who can afford to pay faster access to, or greater choice of, services (supplementary insurance) or coverage of excluded services or user charges for statutory care (complementary insurance).

Governments seeking to use VHI to expand coverage typically have to make significant interventions, including through tax subsidies to make premiums more affordable, but this creates market distortions and is inefficient.

Policy-makers can secure better health system performance by improving access to publicly financed health care than by promoting VHI.

Introduction

Economic theory and empirical evidence indicate that it is difficult to get VHI to cover all needed health services for all those who require health care. As a result, countries struggle to make progress towards UHC – ensuring everyone can use quality health care without financial hardship (WHO, 2010) – through VHI alone. Although VHI generally improves financial protection (affordable access to health care) for those who have it, it can undermine the performance of the health system as a whole, particularly where it plays a large role.

It is not always easy to address the challenges posed by VHI; doing so requires political willingness and ability to shape the role VHI plays through careful policy design and implementation, strong regulatory capacity to ensure VHI functions in line with health system goals, and effort to ensure that publicly financed coverage meets the needs of those who are less likely to be covered by VHI, i.e. people with lower incomes or chronic conditions.

This chapter has three sections: understanding the role VHI plays in health system financing; understanding the challenges it brings with it as a policy; and providing advice for any policy-maker contemplating its introduction or, with an existing system of VHI, seeking to make it work better.

In the first section, we explain how VHI works, set out its distinguishing features and compare it with out-of-pocket (OOP) payments and medical savings accounts (MSAs) (see Box 1.3.1), outlining the even-worse-than-VHI failings of the latter. We examine VHI’s relationship with publicly financed health care coverage (supplementary, complementary or substitutive) and look at how much VHI is currently used and where, as well as reasons for changes in its level of use.

Understanding VHI’s role in health system financing

VHI can cover all or some of the risk of a person incurring health care costs. It can be bought by individuals or groups (for example, employers on behalf of their employees) and it can be sold by a wide range of entities – not only by for-profit (commercial) and non-profit-making private organizations, but also by public and quasi-public bodies.

What differentiates VHI from other types of health insurance is that it is taken up voluntarily, i.e. there is no compulsion to buy it, and paid for privately rather than publicly: VHI premiums are typically delinked from a policyholder’s income and often linked to a person’s risk of ill health (Mossialos & Thomson, Reference Mossialos and Thomson2002; Sagan & Thomson, Reference Sagan and Thomson2016a; Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). VHI therefore tends to be more regressive and less efficient in terms of raising revenue than public spending on health, and those who need it the most may not be able to access it or afford the premiums. The benefits offered by VHI can also be subject to user charges (co-payments) or limited in other ways to protect insurers from incurring losses, which means that some people may not be adequately protected from financial hardship caused by out-of-pocket (OOP) payments, even though they have VHI.

VHI is a form of prepayment, alongside other forms of prepayment such as taxes, mandatory health insurance contributions and MSAs (Box 1.3.1). In contrast to OOP payments, VHI premiums are collected in advance to pay for health care when it is needed, spreading the financial risk of ill health over time. In contrast to OOP payments and MSAs, VHI enables funds to be pooled, spreading financial risk across insured people. Financing health care through prepayment with risk pooling supports progress towards UHC by reducing financial barriers to access and financial hardship caused by OOP payments. However, VHI risk pools are generally much smaller than pools established through publicly financed coverage, which means there is less redistribution of financial risk.

MSAs are another form of prepayment, but, unlike VHI, they do not allow the spread of financial risk across insured people and thus typically do not provide sufficient financial protection.

MSAs allow enrollees to withdraw funds set aside to cover eligible health care costs. They are usually coupled with a high-deductible insurance plan to cover very high costs, allowing those who hold such accounts to manage risks over time but not across the broader population. In terms of overall health system policy, MSAs have very limited ability to achieve goals such as efficiency, equity and financial protection.

Although the accounts are expected to enhance efficiency by reducing the use of low-value treatments and controlling health care costs, evidence shows that they can discourage the use of both low- and high-value treatments, leading to reduced adherence to medication and preventive care. People who switch to MSAs tend to spend less on health care initially, but the long-term impact on costs is unclear.

MSAs allow individuals to spread financial risk over time, but they may not be sufficient to cover some health care costs and are likely to discriminate against people who are less able to save, including unemployed, disabled or chronically ill people. Evidence also shows that enrolment in the accounts can lead to a reduction in beneficial care, potentially undermining the health of people with low incomes or chronic conditions.

Despite the policy challenges related to MSAs, policy-makers in some countries continue to regard them as a desirable health financing mechanism. This may be due to the common use of savings for pensions, leading to the mistaken belief that savings alone can cover health care costs, and due to lobbying by financial service providers who offer the accounts. MSAs play a role in health system financing in China, Singapore, South Africa and the USA.

The role of VHI in health system financing is usually defined in relation to gaps in publicly financed coverage (Table 1.3.1). It typically supplements or complements publicly financed coverage; in a few cases it substitutes publicly financed coverage.

Supplementary coverage

Perceived problems with the quality and timeliness of publicly financed health care can motivate people to buy supplementary VHI. Supplementary VHI plays a role in the majority of countries, but its role is usually small both in terms of contribution to spending on health and share of the population covered. Ireland, Israel and South Africa are key exceptions: in these countries supplementary VHI either covers a large share of the population (Ireland, Israel) or only covers a small share of the population but accounts for an unduly large share of current spending on health (South Africa) (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

Complementary coverage

Gaps in the scope of the publicly financed benefits package or the existence of user charges for publicly financed health care can drive demand for complementary VHI coverage. Complementary VHI covering services excluded or not well covered by publicly financed health care usually plays a small role. It often focuses on dental care and is sold alongside supplementary VHI. The two main outliers are Canada, where outpatient medicines are not routinely publicly financed and many employers offer VHI to their employees, and the Netherlands, where over 80% of the population has VHI covering dental care and physiotherapy (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). Complementary VHI covering user charges also usually plays a small role. Globally, Croatia and France are the main countries in which this type of VHI plays a significant role (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). Slovenia was another notable case until 2024, when complementary VHI covering co-payments was abolished and replaced with a fixed compulsory contribution within the public health insurance scheme, and co-payments were removed.

Substitutive

People can buy substitutive VHI if they are excluded from publicly financed coverage or allowed to choose between publicly and privately financed coverage. Usually, only a small share of the population – often those with higher incomes – benefits from this type of coverage, but it can represent a more significant share of current spending on health. Substitutive VHI plays a significant role in a few countries only: Bahamas, Botswana, Brazil, Chile and Germany (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019; Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). It was abolished in the Netherlands in 2006 (Sagan & Thomson, Reference Sagan and Thomson2016b). Over time policy-makers in Chile and Germany have tried to limit the role of substitutive VHI because of its disruptive effect on the wider health system (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

| Role | Nature of coverage | Country examples |

|---|---|---|

| Supplementary | Offers faster access to services, greater choice of health care provider or enhanced amenities | Most countries, with a particularly large role in Ireland, Israel and South Africa |

| Complementary (user charges) | Covers user charges (co-payments) for goods and services in the publicly financed benefits package | Very few countries, but a significant role in Croatia and France |

| Complementary (services) | Covers services excluded from the publicly financed benefits package – typically dental care | Many countries, often sold alongside supplementary VHI but with a significant role in a few countries only, including Canada and the Netherlands |

| Substitutive | Covers people excluded from or allowed to opt out of publicly financed coverage | Very few countries have a significant role for substitutive VHI: Bahamas, Botswana, Brazil, Chile and Germany |

VHI: voluntary health insurance.

How much is VHI currently used and in which countries?

VHI makes a negligible contribution to spending on health in most countries.

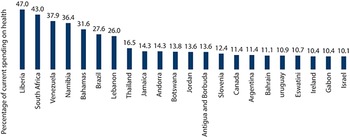

In 2021, the VHI share of current spending on health exceeded 10% in only 22 countries globally (Fig. 1.3.1). VHI accounted for between 5% and 10% of current spending on health in a further 39 countries and was negligible everywhere else (WHO, 2023).

In 2021, the number of countries in which VHI accounted for at least 10% of current spending on health was very small

Note: SHA: System of Health Accounts; VHI: voluntary health insurance, USA: United States of America. VHI here is defined as health insurance schemes that are based upon the purchase of a health insurance policy, which is not made compulsory by government using the SHA code HF2.1. The figure excludes previously voluntary forms of private health insurance in France and the USA, which have been reclassified as compulsory health insurance in health accounts.

Figure 1.3.1 Long description

The y-axis notes the voluntary health insurance schemes as a percentage of current health expenditure, while the x-axis notes the countries. The values are as follows. Liberia: 47.0. South Africa: 43.0. Venezuela: 37.9. Namibia: 36.4. Bahamas: 31.6. Brazil: 27.6. Lebanon: 26.0. Thailand: 16.5. Jamaica: 14.3. Andorra: 14.3. Botswana: 13.8. Jordan: 13.6. Antigua and Barbuda: 13.6. Slovenia: 12.4. Canada: 11.4. Argentina: 11.4. Bahrain: 11.1 Uruguay: 10.9. Eswatini: 10.7. Ireland: 10.4. Gabon: 10.4. Israel: 10.1.

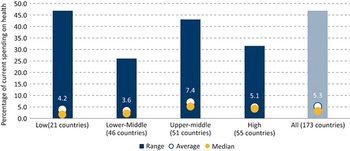

Across all countries for which data are available, on average VHI accounts for only 5.3% of current spending on health, ranging from 3.6% in lower-middle-income countries to 7.4% in upper-middle-income countries (UMICs) (Fig. 1.3.2).

In 2021, the VHI share of current spending on health was highest in UMICs

Note: SHA: System of Health Accounts; VHI: voluntary health insurance. Only includes countries for which VHI data were available. VHI here is defined as SHA code HF2.1.

Figure 1.3.2 Long description

The y-axis notes the Voluntary health insurance schemes as a percentage of current health expenditure from 0 to 50, while the x-axis represents the income groups, each with three values: Range, Average, and Median, respectively. The values are as follows. Low (21 countries): 46.0; 4.2, 2.0. Lowe-middle (46 countries): 25.5; 3.6; 2.5. Upper middle (51 countries): 44.0; 7.4; 5.0. High (55 countries): 31.5; 5.1; 4.9. All (173 countries): 46.0; 5.3; 4.0.

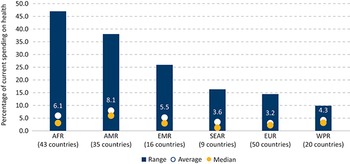

In terms of World Health Organization regions, on average the VHI share of current spending on health was highest in the Americas (8.1%) and the lowest in Europe (3.2%) (Fig. 1.3.3).

In 2021 the VHI share of current spending on health was higher in the Americas than in other parts of the world

AFR: WHO African Region; AMR: WHO Region of the Americas; EMR: WHO Eastern Mediterranean Region; EUR: WHO European Region; SEAR; WHO South-East Asian Region; SHA: System of Health Accounts; VHI: voluntary health insurance; WHO: World Health Organization; WPR: WHO Western Pacific Region.

Notes: Only includes countries for which VHI data were available. VHI here is defined as SHA code HF2.1.

Figure 1.3.3 Long description

The y-axis notes the Voluntary health insurance schemes as a percentage of current health expenditure from 0 to 50, while the x-axis represents the regional groups, each with three values: Range, Average, and Median, respectively. The values are as follows. A F R (43 countries): 47.0; 6.1; 3.0. A M R (35 countries): 27.5; 8.1; 5.5. E M R (16 countries): 25.0; 5.5; 3.0. S E A R (9 countries): 15.5; 3.6; 1.5. E U R: 15.0; 3.3; 3.0. W P R (20 countries): 10.0; 4.3; 4.0.

Changes in levels of use of VHI

Only a handful of countries have seen large changes in VHI’s contribution to current spending on health over time, with decreases usually recorded in high-income countries (HICs) and increases in middle-income countries.

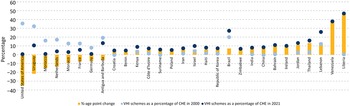

VHI’s share of current spending on health did not change much between 2000 and 2021 in most countries. Looking at changes between two points in time can conceal fluctuations, but during this period the VHI share fell by five or more percentage points in only eight countries globally (mostly HICs) and grew by five or more percentage points in 21 mostly lower-middle or UMICs (Fig. 1.3.4).

Not many countries saw substantial changes in the VHI share of current spending on health between 2000 and 2021

Note: CHE: current health expenditure; SHA: System of Health Accounts; VHI: voluntary health insurance, USA: United States of America. VHI here is defined as SHA code HF2.1. In France, Germany and the USA the changes are due to changes in health accounting that resulted in VHI being reclassified as compulsory health insurance.

Figure 1.3.4 Long description

The y-axis lists the percentages from minus 40 to 60, while the x-axis lists the countries. The countries with negative age point change are: United States of America, Uruguay, Morocco, Netherlands, Monaco, France, Germany, and Antigua and Barbuda. Those with positive age point changes are: Croatia, Benin, Kenya, Côte d’Ivoire, Suriname, Poland, Iran, Israel, Haiti, Republic of Korea, Brazil, Zimbabwe, India, China, Bahrain, Ireland, Jordan, Thailand, Lebanon, Venezuela, and Liberia.

The large drop in the VHI share of current spending on health in France, Germany and the USA was due to changes in health accounting. VHI was reclassified as compulsory health insurance in National Health Accounts in response to reforms making private health insurance compulsory for some groups of people (OECD, Eurostat & WHO, 2017). In France, the VHI share fell from 13% in 2012 to 7% in 2016 following the government’s introduction in January 2013 (with effect from 2016) of a mandate on all employers to offer complementary private health insurance covering user charges to their employees (Couffinhal & Franc, 2020; Bricard, Reference Bricard2024). The introduction of a universal mandate in Germany in 2009, making it compulsory for people who choose to opt out of publicly financed coverage to take up substitutive private health insurance (as opposed to remaining without any coverage), resulted in the VHI share falling from 9% in 2008 to 1% in 2009 (Ettelt & Roman-Urrestarazu, Reference Ettelt, Roman-Urrestarazu, Thomson, Sagan and Mossialos2020). In the USA, the implementation of the Affordable Care Act in 2014 made health insurance mandatory for people under the age of 65 years for the first time, leading the VHI share to fall from 33% in 2013 to 1% 2014 (Brown & Glied, Reference Brown, Glied, Thomson, Sagan and Mossialos2020).

In Morocco, the Netherlands and Uruguay, the decline in the VHI share of current spending on health followed reforms to expand access to publicly financed coverage. A sudden fall in the VHI share in Morocco (from 12% in 2005 to 1% in 2006) followed the creation of a mandatory social health insurance (SHI) scheme, which extended publicly financed coverage from 16% to 30% of the population (Mulvihill, Reference Mulvihill2022). In the Netherlands, a national health insurance scheme introduced in 2006 abolished substitutive VHI for richer people, who had previously been excluded from publicly financed coverage, leading to a fall in the VHI share from 20% in 2005 to 6% in 2006 (Maarse, Jeurissen & North, Reference Maarse, Jeurissen, North, Thomson, Sagan and Mossialos2020). In Uruguay the VHI share fell progressively from 32% in 2000 to 12% in 2020, following the establishment and gradual expansion of publicly financed coverage (Arbulo et al., 2015). The speed of decline in the VHI share was slower than expected, however, partly due to employers continuing to be allowed to provide VHI to their employees (Pettigrew & Mathauer, Reference Pettigrew and Mathauer2016).

The decline in VHI’s share of current spending on health in South Africa is linked to a decline in VHI population coverage due to rising premiums (Pettigrew & Mathauer, Reference Pettigrew and Mathauer2016). Despite this, the VHI share in South Africa remains the highest in the world (43% in 2021), despite the fact that VHI only covers around 16% of the population (see Fig. 1.3.1) (McIntyre & McLeod, Reference Mcintyre, Mcleod, Thomson, Sagan and Mossialos2020).

In countries such as Jordan, Thailand and Venezuela, large increases in the VHI share of current spending on health reflect a combination of factors, including the poor performance of publicly financed coverage, growing purchasing power in the middle class and wider economic trends, including trade liberalization and privatization (Pettigrew & Mathauer, Reference Pettigrew and Mathauer2016).

Growth in public spending on health slowed significantly following the global financial crisis of 2007–2008, leading to an increase in the private share of current spending on health in many countries, but this often occurred due to increased reliance on OOP payments rather than growth in VHI (Thomson et al., 2015). In response to COVID-19, many countries sought to increase public spending on health and some expanded publicly financed coverage, at least for services related to COVID-19 (Thomson et al., 2022; WHO Regional Office for Europe, 2021). Access problems, including large backlogs in health services and higher waiting times, have fuelled interest in purchasing VHI in countries like the United Kingdom (Campbell, Reference Campbell2022). Indeed, per capita spending on VHI in the United Kingdom rose from US$ 123 to 140 between 2019 and 2021 (WHO, 2023). Over this period, 26 countries experienced an increase in per capita VHI spending by more than US$ 10, with the most substantial increases observed in Canada, Australia, Ireland and Liberia (exceeding US$ 50 per capita). Conversely, eight countries noted declines in VHI per capita spending of US$ 10 or more, with the largest falls observed in Cyprus, Lebanon, Monaco and United Arab Emirates (WHO, 2023). However, on the whole, per capita VHI spending changed little in most (80%) countries (WHO, 2023).

Key policy challenges for the use of VHI

VHI on its own cannot help countries to progress towards UHC. It can help to fill some gaps in publicly financed coverage, but it is generally difficult to align VHI with the goal of ensuring that everyone can access health care without experiencing financial hardship. We identify four key policy challenges that explain this difficulty: VHI does not stop reliance on OOP payments; it is difficult to ensure affordable access to VHI for those who need it most; VHI undermines equity and efficiency in the use of resources; and history and politics get in the way of an effective VHI policy. We deal with each of these in turn below.

Policy challenge 1: VHI is unlikely to be helpful in making progress towards UHC in countries that rely heavily on OOP payments

Both economic theory and empirical evidence indicate that VHI is unlikely to provide comprehensive coverage for the whole population.

Economic theory

It is extremely difficult for VHI to provide comprehensive coverage for the whole population, even when it is heavily regulated, due to market failures. Market failures in health insurance are well recognized (Barr, 1992). Problems such as moral hazard and monopoly issues afflict both compulsory and voluntary health insurance (Nyman, 2004; Barr, 2004; Einav & Finkelstein, 2018). In addition, VHI is prone to adverse selection and risk selection.

Adverse selection refers to a situation in which people with higher risks of ill health are more likely to take up VHI, which limits risk pooling and pushes up health care costs, leading insurers to increase premiums or reduce benefits. This in turn may make VHI less accessible for people with high risks and less attractive for people with low risks. If low-risk people stop buying VHI, the ensuing “death spiral” can lead to the collapse of an insurance company. Similarly, it is difficult to sustain VHI among people who are already ill or at high risk of becoming ill and when the risks of becoming ill are linked, such as during epidemics (Barr, 2004). Financial regulation of VHI can provide the necessary stability, but adverse selection is best prevented by making health insurance compulsory. In practice, adverse selection may be less of an issue because richer (and healthier) people are often more likely to buy VHI, especially when it is offered alongside publicly financed coverage.

Insurers typically try to prevent adverse selection by selecting people with lower health risks; for example, by excluding from coverage or charging higher premiums for pre-existing conditions. Again, this means that some people may not be able to obtain any or sufficient coverage through VHI, limiting risk pooling. Material regulation involving rules around premiums, benefits and other contractual conditions can help avoid some of these problems (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

Empirical evidence

The empirical evidence supports economic theory. Historically, as the precursor to publicly financed coverage, VHI never succeeded in covering the whole or even most of the population. The goal of universality was only achieved through the introduction of mandates for publicly financed health care.

We can briefly recap VHI’s history, based on the account of Thomson, Sagan & Mossialos (Reference Thomson, Sagan and Mossialos2020). VHI is the earliest form of prepaid health financing. It first emerged in Europe in the Middle Ages, before the rise of modern medicine, and aimed to compensate people for loss of earnings due to illness, which is why it was linked to employment. VHI offered by mutual-aid associations serving industrial workers had become the norm in Europe by the mid-19th century and spread via colonialism to countries outside Europe (e.g. South Africa, where it initially covered white mine workers).

Medical advances led to an increase in the cost of health care, motivating health care providers in the early 20th century to develop VHI, often in league with hospitals run by the charitable sector, so that people could continue to pay for their services. Provider-driven VHI proliferated in Europe and beyond, including Australia, Canada and the USA. Over time, these largely non-profit schemes were joined by commercial schemes.

Few of these early forms of VHI grew to cover more than a small share of the population, not only because health insurance was voluntary and also usually linked to employment, but also because it was unaffordable for many people. Starting with Germany in 1883, national governments began to introduce compulsory publicly financed schemes to extend coverage to more people, filling gaps that VHI could not cover.

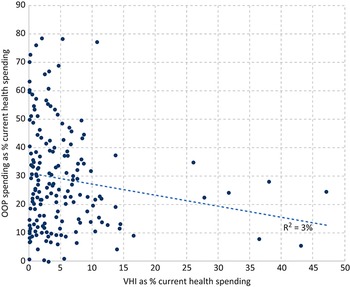

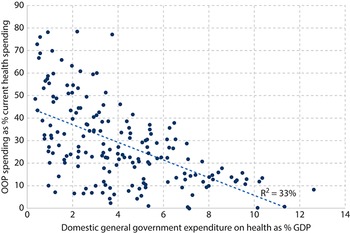

Further empirical evidence is provided by data on health spending, which suggest that public spending on health is more likely to reduce OOP payments than VHI. Across countries there is very little association between spending through VHI and spending through OOP payments (Fig. 1.3.5a). Liberia, Namibia and South Africa are the only countries where the VHI share of current spending on health substantially exceeds the OOP payment share. In South Africa, for example, the decline in the OOP payment share (from 14% in 2000 to 5% in 2020) was accompanied by a small decline in the VHI share (from 47% to 42%) and a large increase in the public share (from 37% to 51%) (WHO, 2023). This means that it is unlikely that it was VHI that drove down OOP payments in South Africa. Across countries there is a much stronger correlation between public spending on health and OOP payments (Fig. 1.3.5b).

Public spending on health is more likely to reduce OOPs than VHI

Figure 1.3.5a Long description

The x-axis represents V H I as percentage of current health spending from 0 to 50, while the y-axis represents O O P spending as percentage of current health spending from 0 to 90. Most of the plots are concentrated between x equals 0 and x equals 15, along the full length of the y-axis. The best-fit line moves straight from (0, 30) to (47, 12), where R-squared equals 3 percent.

Domestic general government spending on health as a percentage of GDP versus OOP payments as percentage of current spending on health, 2021

Note: GDP: gross domestic product; OOP: out-of-pocket; SHA: System of Health Accounts; VHI: voluntary health insurance. VHI here is defined as SHA code HF2.1. Domestic general government spending on health here is defined as health expenditure funded from general government domestic sources (government domestic revenues and SHI contributions). In SHA it is calculated as FS.1 (transfers from government domestic revenue allocated to health purposes) plus FS.3 (social insurance contributions).

Figure 1.3.5b Long description

The x-axis represents Domestic general government expenditure on health as percentage of G D P from 0 to 14, while the y-axis represents O O P spending as percentage of current health spending from 0 to 90. Most of the plots are concentrated between x equals 0 and x equals 4, along the full length of the y-axis. The plots move down the y-axis as the x-axis increase. The best-fit line moves straight from (0.5, 42) to (11.5, 0), where R-squared equals 33 percent.

Policy challenge 2: It is difficult to ensure affordable access to VHI for those who need it most

Empirical evidence shows that VHI is more likely to be taken up by richer people, which exacerbates inequality in financial protection (affordable access to health care) (Sagan & Thomson, Reference Sagan and Thomson2016a; Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). This is sometimes the result of policy design – for example, in countries such as Germany where only richer people are allowed to opt out of publicly financed coverage. More often, it is due to insurer behaviour, perhaps in response to concerns about adverse selection (as described above), which makes VHI less accessible to people with a higher risk of ill health and less affordable for people with lower incomes. As a result, it is generally difficult for VHI to improve financial protection in the health system as a whole – but the degree to which affordability is a problem varies according to whether VHI is playing a supplementary, complementary or substitutive role in the overall health coverage mix.

Where VHI plays a supplementary role

Problems with affordable access to VHI need not be a concern where VHI plays a supplementary role and the policy goal is merely for VHI to offer more choice to a small share of the population – as in the United Kingdom.

Where VHI plays a substitutive or complementary role

Affordability is more of a concern where VHI plays a substitutive role and is the only form of coverage for some groups of people or where VHI plays a complementary role and covers significant gaps in the publicly financed benefits package or user charges. In such cases VHI can be critical to ensuring financial protection and should therefore cover all those who need it, but many countries have struggled to achieve this.

Globally, only three main countries – Croatia, France and Slovenia – have managed to provide complementary VHI covering user charges to almost all those who need it, but this has involved heavy government intervention through regulation and tax subsidies for people with low incomes and, in France, making private health insurance compulsory for employees (WHO Regional Office for Europe, 2019; 2023).

VHI covering co-payments in Croatia, France and – until recently – Slovenia achieves very high rates of population coverage, reaching over 80% of those who have to pay co-payments in Croatia, around 90% of the population in France and around 95% of those with compulsory health insurance in Slovenia. Partly due to high take-up of VHI covering co-payments, the incidence of catastrophic health spending is very low in Slovenia and France and relatively low in Croatia (WHO Regional Office for Europe, 2019; 2023; Voncina & Rubica, 2019; Bricard, Reference Bricard2024; Šarec & Jošar, 2025).

High levels of VHI take-up in these three countries can be attributed to the following factors:

People need VHI covering co-payments because user charges are widely applied in all three countries and are in the form of percentage co-payments for secondary care, meaning that people have to pay 20% of the cost of inpatient care. Although there are caps in place for inpatient care (France) and secondary care (Croatia), these caps are set at a high level; many households would face financial hardship before reaching them.

VHI covering co-payments is accessible to all those who want to buy it due to regulation (open enrolment plus community-rated premiums) in Croatia and until recently in Slovenia and tax subsidies targeting people with low incomes in France (see Box 1.3.2).

VHI covering co-payments is affordable for most people because it is free for people with very low incomes in Croatia and France. In Slovenia, people with very low incomes were exempt from co-payments and did not need VHI. However, for the rest of the population, complementary VHI was financed through flat-rate premiums rather than income-related contributions, raising longstanding equity concerns and making it politically contentious. Premium hikes in early 2023 risked pushing coverage out of reach for some households, prompting the government first to introduce a price cap and ultimately to abolish most co-payments (Šarec & Jošar, 2025).

Using complementary VHI to cover user charges is not a panacea, however. VHI premiums are regressive in comparison to public spending on health, undermining equity in financing health care; VHI does not eliminate inequalities in access to health care; and in spite of regulation and tax subsidies, people with low incomes are still more likely to lack VHI coverage and less likely to have good quality VHI coverage than richer people (e.g. in France) (WHO Regional Office for Europe, 2023; Bricard, Reference Bricard2024).

Government intervention in VHI has generally intensified over time, regardless of VHI’s role, for two reasons: changes in the nature of VHI with the entry of commercial insurers and, in some countries, growth in VHI, which has made its negative effects on health system performance more visible (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

VHI in France is dominated by non-profit mutual associations and predates the establishment of national health insurance in 1945. VHI coverage grew from around 30% of the population in 1950 to 86% in 2000. In 2000, to address concerns about low VHI uptake among poorer households, the government introduced tax subsidies, making VHI free for people with very low incomes and cheaper for people with low incomes. VHI coverage subsequently reached 95% in 2013.

In 2016, the government required all employers to offer VHI to their employees – a measure intended to improve access to group VHI contracts, which are known to be more advantageous than individual contracts. Although this is expected to reduce inequities in VHI access among employees, it may widen disparities between salaried employees and students, pensioners and unemployed or self-employed people. Recent studies suggest that this policy could potentially diminish overall welfare, as employers are likely to pass on the cost of insurance contracts to employees through salary adjustments. The key net beneficiaries of this policy would likely be short-term unemployed individuals (around 7% of the population), who could retain their former complementary health coverage (Benoît & Coron, Reference Benoît and Coron2019). Recent data on population coverage indicates a slight decline from 93% in 2017 to 90% in 2018 (FNIM, 2019).

Policy challenge 3: VHI undermines equity and efficiency in the use of resources

Erosion of equity and efficiency in the use of health system resources is a particular challenge when VHI plays a supplementary or substitutive role.

VHI can undermine equity and efficiency in the use of health system resources in various ways (Box 1.3.3). This is most likely to occur in contexts where, rather than complementing publicly financed coverage, VHI plays a significant supplementary or substitutive role, covering the same services as publicly financed coverage and drawing on the same pool of health care providers. Negative spillover effects are common when the services offered by VHI are more expensive than those offered by publicly financed coverage, creating incentives for providers to prioritize the treatment of people with VHI or to work in the private sector. Spillover effects may be present even where VHI plays a minor role, but they become more visible and more detrimental where VHI plays a more significant role.

Other concerns related to VHI include the inefficiencies that arise from duplication of administrative and other responsibilities for managing different risk pools (Smith & Witter, Reference Smith and Witter2004). Risk-rating requires information and auditing capacity to assess individual health risks, write appropriate contracts and monitor health care use (Smith & Witter, Reference Smith and Witter2004). Available data suggest that administrative costs are almost always higher in VHI than publicly financed coverage (Sagan & Thomson, Reference Sagan and Thomson2016a).

Tax subsidies benefit richer households: Tax subsidies introduced to promote VHI take-up usually benefit richer households. For example, in Brazil and South Africa tax subsidies amount to about 30% of federal government spending on health (Brazil) and all public spending on health (South Africa), despite VHI covering only 24% and 16% of the population respectively (McIntyre & McLeod, Reference Mcintyre, Mcleod, Thomson, Sagan and Mossialos2020; Montoya Diaz et al., 2020). There is no evidence to support the idea that general tax subsidies for VHI are an efficient use of public resources.

Inadequate compensation for VHI’s use of public resources: In some countries, such as Brazil, Chile and Ireland, many people with VHI continue to use public facilities, including as backup cover. While this is permitted by law and private insurers are required to compensate public providers for the use of their facilities, this has been difficult to enforce (Brazil, Chile) or has never reflected the full economic cost (Ireland). Implicit subsidies also arise from public funding of medical education.

Migration of health professionals from public to private facilities: Since services covered by VHI are usually provided in the private sector, where earnings tend to be higher than in the public sector, this may lead to a migration of health professionals from public to private facilities, as in Kenya and South Africa. This can leave public facilities under-staffed, with implications for quality of care.

Increase in waiting times for publicly financed treatment: Failure to align provider incentives leads to increased waiting times for publicly financed treatment because doctors permitted to work in both private and public sectors may face strong financial incentives to prioritize patients with VHI; for example, if they are paid more to treat people with VHI or when waiting times are the main reason for purchasing VHI, as in Ireland.

Loss of financial contributions to publicly financed coverage: In countries where people can choose between publicly financed coverage or substitutive VHI (Chile and Germany), the publicly financed scheme loses contributions from those with higher incomes and better health when they opt for private health insurance. If those who opt for private health insurance are allowed to return to the publicly financed scheme; for example, when they are sicker and their premiums increase, this may put pressure on the publicly financed scheme. On the other hand, if opting out of the publicly financed scheme is irreversible, heavy regulation is required to ensure that private health insurance is accessible and affordable for those who can no longer return to publicly financed coverage.

Policy challenge 4: History and politics are a challenge to effective public policy towards VHI

Once established, VHI markets can be difficult to shape, especially where VHI plays a larger role.

Aligning VHI with the goals of UHC requires effective public policy. A government’s ability to ensure this may be more difficult where VHI plays a large or significant role, which in turn may be the outcome of historical developments (path dependency), political ideology and the relative power and interests of different stakeholders (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

Health care providers and insurers have frequently opposed efforts to expand access to publicly financed coverage or tighten regulation of VHI, sometimes with the support of employers, civil servants and richer people – those most likely to benefit from preserving the status quo. Private interests have blocked or delayed the implementation of universal schemes in a wide range of countries, including Canada, Chile, Germany, Ireland, Kenya, the Netherlands, South Africa, Switzerland and the USA (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020). In some LMICs, the promotion of VHI by donors and other actors has given it disproportionate political power (Pettigrew & Mathauer, Reference Pettigrew and Mathauer2016).

In many countries, VHI does not fall under the purview of the health ministry but is regulated as a financial service by the finance ministry or other ministries concerned more with economic or industrial policy than social policy (Sagan & Thomson, Reference Sagan and Thomson2016a). This is another obstacle to effective public policy and may explain why oversight of VHI is often weak in countries at all income levels (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

Understanding how policy challenges can be addressed

Policy responses using VHI to fill gaps in publicly financed coverage can vary depending on the nature and size of the role VHI plays. We suggest strategies that policy-makers can implement to address the challenges that come with VHI according to two scenarios: where VHI is newly introduced, or plays only a small role, and another, where VHI is already well established.

If VHI does not yet play a role or only plays a small role in the health system

Decision-makers should anticipate the policy challenges that VHI brings and consider whether there is enough capacity to monitor and regulate VHI and manage interests. Alongside this, they must remember that, once established, VHI may be more difficult to shape.

If thinking about introducing VHI, careful consideration should be given to policy design so that it does not undermine publicly financed coverage. Further, clear boundaries between publicly and privately financed health care should be drawn.

Supplementary VHI (offering people faster access to treatment) is best when it is limited to a small share of the population. Keep it that way. Do encourage growth through tax subsidies or material regulation to make VHI more accessible and affordable.

Complementary VHI can protect against OOP payments where there are significant gaps in the publicly financed benefits package or heavy user charges. Globally, only a handful of countries have managed to achieve the high rates of population coverage needed if this type of VHI is to help meet UHC goals. Achieving high rates of population coverage comes at a cost: to ensure VHI is accessible and affordable for those who need it most requires heavy government intervention, including tax subsidies exclusively for people with low incomes.

Do not allow people to opt out of publicly financed coverage. Substitutive VHI does not enhance health system performance. Some countries have abolished substitutive VHI (Netherlands) and others are trying to limit its role (Chile and Germany).

VHI is not a panacea for high OOP payments. Increases in public spending on health are more likely to reduce OOP payments than VHI, so rather than trying to encourage VHI through tax subsidies or other means, policy should focus on improving affordable access to publicly financed health care. Tax subsidies for VHI are generally inequitable and inefficient and waste public resources.

If VHI already plays a significant role in the health system

Ensure there is sufficient capacity and political will to monitor and regulate VHI, enforce boundaries between publicly and privately financed health care and manage stakeholder interests.

Enforce boundaries between publicly and privately financed health care so that VHI does not undermine equity and efficiency in the use of public resources. In practice this can be difficult to achieve due to entrenched stakeholder interests.

Where VHI plays a significant complementary or substitutive role, careful intervention is needed to ensure affordable access to VHI for those who need it. This can be achieved through material regulation involving a wide range of rules, including open enrolment (guaranteed issue); lifetime cover (guaranteed renewal); community rating (delinking premiums from individual risk of ill health); premium review, approval or caps; mandated (usually minimum) benefits; prohibition of exclusion of pre-existing conditions; caps on user charges for VHI-covered services; and prohibition of benefit ceilings (Sagan & Thomson, Reference Sagan and Thomson2016a).

Country experience shows that it is not easy to ensure affordable access to complementary or substitutive VHI for people with low incomes or chronic conditions. Some countries have resorted to making VHI compulsory, but this has not been unproblematic, in part because it is a regressive way of financing health care, placing a disproportionate financial burden on those with lower incomes. A better solution would be to make sure that people with low incomes or chronic conditions do not need VHI.

Conclusions

VHI plays a very minor role in financing health care in most countries, especially in countries that rely heavily on OOP payments. However, due to a combination of market failures and weaknesses in public policy towards VHI, it can have a disproportionately negative effect on health system performance. Although VHI does fill gaps in publicly financed coverage, it often favours richer people, exacerbating inequity in financial protection. It can also draw financial and human resources away from publicly financed coverage, particularly where it plays a substitutive role or a large supplementary role.

Ensuring that those who most need VHI can buy it – and that VHI does not undermine equity and efficiency in the use of public resources – requires significant capacity to monitor and regulate VHI and enforce boundaries between publicly and privately financed health care. Governments often struggle to shape VHI in the face of opposition from entrenched stakeholder interests. Even when VHI improves access and financial protection for people with low incomes, which is generally rare, it remains a regressive form of financing health care.

Given what we know about VHI from economic theory and empirical evidence, countries should lower their expectations about its ability to meet the goals of UHC and focus instead on improving affordable access to publicly financed health care.Footnote 1

Open access

Open access