Introduction

In 2019, Booking.com commented on Organisation for Economic Co-operation and Development (OECD) tax evasion regulations. Booking.com stated unequivocally in their comment that the firm does not participate in tax evasion and supports the organization’s efforts to create a unified international tax framework. The firm proceeded to make suggestions to the OECD that certain provisions be optional and flexible for taxpayers and firms. Just two years later, Italian authorities reported that Booking.com had evaded ‘153 million euros of value added tax (VAT)’ (Parodi Reference Parodi2021, p. 1).

How do bureaucrats integrate lobbying information into regulations, given concerns about the veracity and intent of profit-maximizing firm and industry association input? This paper focuses on the question of how, and to what extent, firms and industry associations influence regulatory bodies.Footnote 1 With the rise in multinational corporations and international connectivity, IOs are now regulating issues previously solved at the domestic level (Berman Reference Berman2021). Firms often lobby IOs and other regulatory bodies directly, given that specific changes to the regulations are made at this stage.Footnote 2 Therefore, in consensus-based organizations and amidst conflicting firm and state preferences, regulatory lobbying is particularly influential. In regard to IOs specifically, previous work has suggested that IOs are more independent from private sector influence (Abbott and Snidal Reference Abbott, Snidal, Mattli and Woods2009; Young Reference Young2012); however, in recent years, IOs have increasingly prioritized stakeholder engagement and allowed access for non-state actors to participate (OECD 2021). Therefore, it is important to assess when, how, and which firms shape regulatory decision making.

I argue that firms influence IO regulations by providing comments with high-quality technical information, as well as signaling the comment’s accuracy and alignment with regulators’ goals. Because the majority of firms offer high-quality comments with policy expertise (Yackee and Yackee Reference Yackee and Yackee2006), the latter – a firm’s reputation for accurate technical information sharing – differentiates firms in the commenting process. I argue that a firm’s reputation is formed by providing accurate and quality comments across a broad range of issue areas – beyond those that most intimately affect their business interests. These repeated exchanges build the firm’s reputation with the regulator and increase the likelihood that the firm’s comment will have an influence on the final regulation. While the process of public commenting undoubtedly privileges large, profitable private actors that have the resources to invest in their reputation at IOs, smaller private actors can leverage this process to outperform their market share and expected influence.

The OECD’s international tax regulations over the last decade offer a substantively important case to systematically assess the extent of firms’ influence on regulatory decision making. Despite previous failed attempts to harmonize international tax policy,Footnote 3 the OECD successfully co-ordinated on agreements to alter more than 2,500 bilateral tax treaties, to create a global minimum tax of 15% on corporate income, and to establish a digital services tax on the largest multinational firms. External stakeholders were extensively involved in offering comments on draft regulations, with over 3,000 comments submitted by firms, non-governmental organizations (NGOs), and industry associations, totaling over 27,000 pages in length. Comments from firms were influential, ultimately resulting in the exemption of entire industries and activities as well as altering the regulation’s monetary thresholds and technical details. The OECD is a hard case for firm influence given that firms and associations do not have decision-making or voting powers; therefore, in comparison to regulatory IOs that offer greater firm integration, we would expect limited firm influence in the OECD. This case also allows for generalizability to other regulatory bodies, given the OECD’s representative stakeholder engagement process. The OECD’s unregulated stakeholder consultation process is relatively laissez-faire, as in the majority of IOs in which lobbying takes place (Berman Reference Berman2021).Footnote 4 Despite the relatively small scope of membership in the OECD, the international tax negotiations integrated 147 countries into negotiation and implementation. Therefore, this context provides insight into how this process works in IOs with inclusive membership.

To test the implications of my theory, I use natural language processing methods along with a new data set of the 3,349 public comments on OECD tax evasion regulations. I find that comments with high-quality information and from firms with repeated and broad-based participation are more likely to be implemented, even when controlling for industry, firm size, and country. I find evidence that firms comment strategically with this in mind, providing comments across issue areas with quality technical information. Finally, I leverage qualitative evidence from in-depth author interviews with twenty-one firm professionals and twelve IO bureaucrats to further illustrate this dynamic.

This paper contributes to our understanding of non-state actor influence on global governance (Keck and Sikkink Reference Keck and Sikkink1999). While NGO influence has been investigated (Betsill and Corell Reference Betsill Michele and Corell2007; Hanegraaff Reference Hanegraaff2015; Tallberg et al. Reference Tallberg, Dellmuth, Agné and Duit2018), the influence of profit-motivated firms – the targets of regulation – is less well understood.Footnote 5 The literature on firm lobbying in the EU and United States highlights that business groups are often over-represented in the stakeholder engagement process (Dür et al. Reference Dür, Bernhagen and Marshall2015; Golden Reference Golden1998; Kim Reference Kim2017; Mahoney Reference Mahoney2008; Osgood Reference Osgood2017; Quittkat Reference Quittkat2011; Yackee and Yackee Reference Yackee and Yackee2006) and have a magnified influence on issues of quiet politics (Baumgartner and Leech Reference Baumgartner and Leech2001; Culpepper Reference Culpepper2010; Rasmussen and Carroll Reference Rasmussen and Carroll2014). In this paper, I open the black box of business lobbying to disentangle which types of business actors are most successful at influencing the regulatory process, holding the issue area constant. In addition, I demonstrate how regulatory bodies evaluate the information provided by business actors and decide which proposals to implement, given that comments provided by the business community are more likely to be high quality (Yackee and Yackee Reference Yackee and Yackee2006) and also reflect their control over private information (Kennard Reference Kennard2020; Perlman Reference Perlman2023; Sell Reference Sell2003).

In addition to theorizing and testing how private firms influence regulations, this paper draws attention to the importance of studying tax evasion and subsequent international co-operation on tax policy. Prior to the OECD’s attempts to limit international tax evasion, these ‘practices cost countries 100–240billion USD in lost revenue annually, which is the equivalent to 4–10% of the global corporate income tax revenue’ (OECD 2022). This lost tax revenue could instead have been channeled to provide public services to citizens and ultimately creates an unequal international distribution of taxes, which has been exacerbated by the rise of globalization and economic integration. This paper calls attention to the important efforts by global governance organizations to harmonize international tax policy and constrain the race to the bottom in taxation, during an unlikely time for successful international co-operation. In addition, the paper encourages further attention in the international political economy literature to the creation and outcomes of these ruptures to established international taxation systems, building on our current knowledge of their long-standing structures and second-order effects (Alstadsæter et al. Reference Alstadsæter, Johannesen and Zucman2019; Arel-Bundock Reference Arel-Bundock2017; Thrall Reference Thrall2024).

Theory of Firm Influence in International Organizations

I argue that firms are more influential on IO regulations if they offer comments with new and accurate technical information that are intended to achieve the regulation’s overarching policy goal. In other words, firm comments are more likely to be integrated into the final regulation if they (1) offer quality technical information and (2) are accurate and meaningfully improve the regulation’s ability to achieve its policy goals. First, high-quality comments that provide technical information act as a ‘legislative subsidy’ (Hall and Deardorff Reference Hall and Deardorff2006), enabling the regulatory process and the creation of informed policy. However, providing technical information is not enough to ensure a firm’s influence because the majority of business actors provide high-quality comments, reflecting their enhanced technical capacity and resources (Yackee and Yackee Reference Yackee and Yackee2006). At the same time, the private information shared by business actors can be filtered selectively to benefit the firms’ interests (Perlman Reference Perlman2023; Sell Reference Sell2003) rather than improving the overall regulation. To discern which comments contain information that is accurate and better achieves policy goals, I argue that IO bureaucrats rely on firms’ reputations for trusted expert information sharing. Firms’ reputations are developed by providing repeated information across a breadth of issue areas, even those that are not intimately tied to the firm’s business interests. This breadth of commenting creates a series of repeated exchanges between the regulatory body and the firm, establishing trust and exhibiting the firm’s alignment with the regulator’s goals. This paper therefore contributes to our understanding of the types and strategies of business actors that are most successful in the regulatory process.

There are three primary forms of direct stakeholder engagement.Footnote 6 In this paper, I focus on the most common and direct form: written public comments (OECD 2016). In this process, non-state actors have the opportunity to share feedback on the precise language of a draft regulation through a written contribution. This approach is particularly popular in the context of international organizations, acting as the primary form of stakeholder engagement in forty-seven out of fifty surveyed IOs (OECD 2016).Footnote 7 Second, regulatory bodies host annual fora in which external stakeholders are invited to provide more general feedback and insight to the IO.Footnote 8 Finally, on a limited basis (especially compared to the domestic context), bureaucrats engage in private, bilateral meetings with stakeholdersFootnote 9 – ‘most of the time, [these meetings] are just informational and go nowhere’.Footnote 10 Firm professionals also stressed that private meetings were limited in the regulatory context, which differed markedly from how they freely discussed their casual and personal relationships with domestic legislators.Footnote 11 Given these considerations, I focus on written public comments in this paper because this form of engagement is the most common, direct, and inclusive.

In this paper, I theorize the type and strategy of private actors that are most influential in the stakeholder engagement process. The majority of the literature on firm influence in the EU and the United States considers the business community as a collective, rather than delineating which types of firms and associations are most effective. For example, the business community has been shown to have differential influence based on the issue (Baumgartner and Leech Reference Baumgartner and Leech2001; Culpepper Reference Culpepper2010), institutional context (Mahoney Reference Mahoney2004, Reference Mahoney2007; Marshall Reference Marshall2010), inside v. outside lobbying strategy (Bruycker and Beyers Reference Bruycker and Beyers2019; Dür and and Mateo Reference Dür and Mateo2024; Hanegraaff et al. Reference Hanegraaff, Beyers and De Bruycker2016), and as compared to other interest groups (Dür et al. Reference Dür, Bernhagen and Marshall2015).

Despite this rich literature that considers these external factors, there is a more limited understanding of firm influence when holding these factors constant. In other words, how and which private actors are able to have the most influence in the stakeholder engagement process in the context of a specific issue area and institutional context? This question is of particular importance amongst firms and industry associations, given that these private actors are oftentimes over-represented in stakeholder engagement processes (Mahoney Reference Mahoney2008) and offer high-quality information (Yackee and Yackee Reference Yackee and Yackee2006). These characteristics beg the question of how policy makers delineate between which firms’ information to trust and implement when there is a glut of private information shared.

To answer this question, I assume that regulatory bodies’ objective is to create policy that effectively achieves the overarching policy goal. To do so, the regulation must be technically informed and perceived as legitimate to promote compliance. Amidst resource constraints, regulators provide opportunities for stakeholder input to solve information asymmetries and pre-empt significant opposition. First, due to a lack of policy expertise and resources, regulatory bodies prefer that firms offer insight into proposed regulations and resolve information asymmetries. Given the limited staff and resources of IOs, the technical information provided by stakeholders is invaluable in filling knowledge gaps and creating effective regulations (Chalmers Reference Chalmers, eds. and Richter2019; Sell Reference Sell2003). Information sharing via the stakeholder engagement process is most important on highly technical issues (Coen and Grant Reference Coen and Grant2005) and in institutions lacking resources (Mclaughlin et al. Reference Mclaughlin, Jordan and Maloney1993). In addition, the involvement of non-state actors enables regulators to avoid strong opposition to their policies, pre-empting blame (DeScioli and Bokemper Reference DeScioli and Bokemper2014; Kevins and Vis Reference Kevins and Vis2021) and improving public opinion towards the regulations (Berman Reference Berman2021; Malesky and Taussig Reference Malesky and Taussig2019). The ideal stakeholder comment – from the perspective of IO bureaucrats – offers new and accurate technical information that improves the regulation and enhances its effectiveness at achieving the overarching policy goal. In other words, I argue that comments are more likely to be influential if they provide quality and accurate technical information to the IO.

A firm’s comment must contain quality technical information to influence the IO. In line with the logic of lobbying as a legislative subsidy (Hall and Deardorff Reference Hall and Deardorff2006), firms’ contributions are valuable if they provide expert technical information that helps policy makers make progress on their agenda. By providing in-depth technical information and policy expertise, firms offer a matching grant that encourages policy makers to exert more effort on a certain policy issue. I therefore hypothesize that comments that contain quality technical information will be more likely to influence the regulatory process. I derive three empirical implications that proxy for firms’ comment quality – uniqueness, level of technical information, and tone. These proxies for comment quality are imperfect, but improve upon previous conceptualizations.Footnote 12

First, information is only an effective subsidy if it facilitates the policy-making process through the provision of new and unique analysis. If a firm instead copies the comment of another firm, policy makers will not receive any additional added value from the contribution. I therefore expect that unique comments will be more likely to influence the policy-making process, relative to duplicate comments that echo another firm’s perspective.

Hypothesis 1a: Unique comments are more likely to influence the final rules.

Next, I consider the level of technical information in the comment. Quality comments act as legislative subsidy because they provide additional information, expert analysis, draft text, or suggested amendments that could allow for successful co-ordination on an issue. These types of comments are written with a high level of technical information to communicate this information. As such, I hypothesize the following.

Hypothesis 1b: Comments with high levels of technical information are more likely to influence the final rules.

Finally, to proxy for the quality of the comment, I also consider the tone of the comment. The legislative subsidy argument posits that private actors that are successful at influencing policy makers do so not through persuasion, but rather through the provision of information that allows the policy maker to take action on a particular issue. Therefore, comments that are rhetorically charged and negative in tone are unlikely to help policy makers move forward effectively. In essence, rhetorically charged comments instead often express a particular partisan or ideological opinion on the proposed rule rather than offering effective information and proposed draft texts that could facilitate the successful passage of the rule. I therefore hypothesize the following.

Hypothesis 1c: Comments that are neutral or positive in tone are more likely to influence the final rules.

However, given that the majority of firms provide high-quality comments with technical information (Yackee and Yackee Reference Yackee and Yackee2006), these factors are incomplete in explaining how and which types of private actors are ultimately most influential. In other words, information sharing is necessary, but not sufficient, to explain firm influence. Therefore, it is equally important to consider how regulatory bodies evaluate and prioritize the accuracy of the information provided and its congruency with improving the regulation.

In both domestic and international contexts, firms can selectively provide technical private information that benefits their interests (Kennard Reference Kennard2020; Perlman Reference Perlman2023) and policy makers have limited time and resources to ascertain the impact of a particular suggestion (Chalmers Reference Chalmers, eds. and Richter2019; Sell Reference Sell2003). However, Hall and Deardorff (Reference Hall and Deardorff2006) assert that despite these problems, domestic legislators can easily discern an interest group’s policy objectives through ‘past and present testimony, reports, press releases, website postings, and other activities that publicly commit them to a position’ (Hall and Deardorff Reference Hall and Deardorff2006, p. 75). I argue that in international regulatory bodies, it is more difficult for bureaucrats to discern the goals of interest groups and for firms to target their information to particular aligned legislators. Therefore, firms must adopt alternative strategies to signal that their information is accurate and will improve the effectiveness of the regulation. First, there is a larger universe of participants in international commenting. The breadth of actors involved, and the resource constraints of IO bureaucrats, makes it more difficult to discern the overall policy goals of each participant via the methods discussed above (Hall and Deardorff Reference Hall and Deardorff2006). Second, in international regulatory bodies, it is more difficult to selectively target information to allies because comments are considered by unelected bureaucrats, rather than a particular legislator or state. Therefore, the information must appeal to a broad group of policy makers to influence the regulation (Dür et al. Reference Dür, Marshall and Bernhagen2019; Tallberg Reference Tallberg2008). For both reasons, firms and industry associations cannot simply provide the legislative subsidy to have an impact in this setting. Rather, I argue that in order to demonstrate their alignment with policy makers’ overall policy goals, private actors must build trust and establish a reputation for expert information sharing.

Therefore, I extend this argument of legislative subsidy to argue that firms must also establish a reputation for sharing accurate technical information to influence the final regulation. Firms must signal their alignment with the overall goals of the project by making long-term investments in the policy-making process and subsequently developing ‘a relationship of mutual trust’ with decision makers (Snyder Reference Snyder1992).Footnote 13 While providing information to the IO does not go against the interests of firms per se, the process of commenting regularly with accurate and technical information is exceedingly costly to the firm in terms of time and resources. As one interviewee stated: ‘If you could quantify how much money is being spent on this process, it would shock you … To participate fully, we had to hire a new employee and spend 100s of hours on the process’.Footnote 14

Therefore, the repeated nature of commenting is a costly signal of a firm’s type, establishing their reputation for expert information sharing to create effective and complete rules that fulfill policy-makers’ goals. In other words, firms will provide matching grants to subsidize progress not only on specific issues that are most pertinent to their interests, but throughout the entirety of the process to demonstrate their commitment to empowering the overarching goals of the regulator. As such, firms form a reputation for trusted expert information sharing and alignment of goals with policy makers through this broad-based participation across issue areas.

Broad-based participation signals the firm’s affinity with the goal of regulators – namely, ensuring that the rule is complete and effectively achieves its policy objectives – because firms’ preference intensity varies across different parts of the rule.Footnote 15 In other words, certain portions of the regulation most intimately affect the firm’s business interests, while others are unlikely to affect them substantially. Therefore, firms that want to build a reputation for expert information sharing will comment broadly across different portions, rather than only providing feedback on sections that most affect their business interests. As a result, their comments may be seen by the regulator as contributing to making the regulation as complete and efficient as possible, rather than primarily to benefit their individual interests. This strategy also allows firms to mask their preference intensity on certain issues to the regulator, camouflaging the specific parts of the regulation the firm would most like to change. Furthermore, their breadth of contribution establishes them as an expert on the subject to the regulator and increases the value of their contributions in the future. This reputation builds cumulatively, allowing for expanded influence as the bureaucrats continue to engage with the information provided by the firm over time and across commenting periods.

I provide two examples to illustrate this logic. First, in the case of OECD rules, a firm may be most concerned about how tax incentives are treated under the Pillar 2 proposal, as their investments have benefited from extensive tax cuts. To increase their credibility and reputation, this firm would not simply comment on investment incentives, but also on other issues that do not affect them as directly. In this specific example, the firm might also participate in Pillar 1 commenting periods, even though this policy is only relevant to the largest digital firms and would not affect their direct business interests. Therefore, the firm offers information and insight broadly across issues. Alternatively, this firm could have made a concerted effort to influence Pillar 2 and avoid exerting resources on less important issues. For example, the firm could have provided a particularly extensive comment on Pillar 2 with detailed information about how the OECD should structure the policy. However, this one-time comment reveals to the regulators the firm’s strong preferences on a specific issue, and raises questions about the veracity and intent of the information provided. In sum, rather than only engaging on issues that directly affect the firm’s interests, I argue that firms that are hoping to form a positive reputation will engage broadly in the consultation across many different topics.

In addition to this hypothetical example, I also illustrate how this theoretical logic operates in the context of the OECD tax process and the pharmaceutical industry. AbbVie and AstraZeneca, two pharmaceutical firms, took divergent approaches in their breadth of engagement. Both firms have similar revenue flows (approximately $55 billion) and take advantage of profit-shifting opportunities to minimize their tax bills. AbbVie, for example, booked $11 billion of profit abroad – mostly in Bermuda – while documenting an $8 billion loss in the United States (Setser Reference Setser2025). Despite the firms’ similarities in terms of market structure, there were significant differences in their approach to the OECD process. AbbVie chose to engage in a very minimal way, with only one comment submitted between 2014 and 2024. Their comment addressed the Pillar 1 proposal: how the OECD had defined profit as well as how profits and losses could be deferred or accelerated. In contrast, AstraZeneca – a similarly placed firm in this industry – engaged across eighteen commenting periods between 2014 and 2024. Their comments spanned topics such as BEPS Action 2, 3, 7, 8, 9, 10, and 13; Transfer Pricing Comparability; Transactional Profit Splits; Chapters 4 and 7: Transfer Pricing Guidelines; Transfer Pricing of Financial Transactions; Tax Challenges of the Digital Economy; Pillar 1; and Pillar 2. While both firms offered technical expertise as well as informative and unique suggestions to the OECD, AstraZeneca engaged in repeated interactions with IO bureaucrats through their comments. In many of these comments, AstraZeneca provided specific technical guidance on discussion draft questions that the secretariat had shared in the hopes of gaining clarity from industry to improve the rules. These repeated exchanges not only provided consistent technical information to the OECD, but also created a reputation for AstraZeneca of trusted expert information sharing because the firm was continually involved across the entirety of the process, not just on issues that most pertinently impacted the firm or industry. Therefore, the firm shared its technical expertise broadly to build this reputation with the IO, rather than engaging in a selective way that made clear which issues were most important to the firm’s interests. From these theoretical expectations, I derive the following hypothesis.

Hypothesis 2: Comments from firms and associations that have participated across a greater breadth of issues are more likely to have an influence on IO rules.

The Case of the OECD International Tax Regulations

OECD international tax regulations provide a setting to conduct careful empirical tests of the theory outlined above. First, public comments have been released to the public in full. Second, international tax offers a case in which firm and state preferences are often misaligned. Firms prefer to maximize opportunities to engage in tax planning and bolster profits. The majority of states prefer to maximize public revenue, limit tax evasion, and avoid inequitable distribution of tax revenues.Footnote 16 Despite these modal preferences, some countries, tax havens in particular, which are benefiting from the current system of tax planning may more closely align with the preferences of firms.Footnote 17 However, for the most part, the final versions of the regulations create zero-sum distributional problems – if states benefit in the form of increased tax revenue, firms are generally more constrained in tax planning and may pay higher tax rates. Because of these distributional consequences, states must carefully consider the veracity of firm comments and it is not a most likely case for firm influence in an IO.

The OECD began discussion of base erosion and profit shifting in 2013. The rules were negotiated and adopted by consensus within the Inclusive Framework, a group of 147 developing and developed countries. There were three major outputs from this process. First, states co-ordinated on a Multilateral Instrument in 2015 to update bilateral tax treaties in the context of a digital economy. The Multilateral Instrument included changes to dispute resolution, country-by-country reporting, and anti-abuse rules. Thus far, 102 countries have signed the Multilateral Instrument, which will subsequently alter more than 2,500 bilateral tax treaties.Footnote 18

The OECD next turned to discussions of Pillar 1 and Pillar 2. Pillar 1 establishes a digital services / sales tax for the largest multinational firms, which will re-allocate tax burdens to locations where technology firms do not have a physical presence (Ward Reference Ward2021). The agreement is still being negotiated, but the future of Pillar 1 is tenuous with the Trump administration’s withdrawal from OECD negotiations. Even without international agreement, firms were concerned about the draft text of the agreement because they expected that countries – especially those in the Global South – would use the OECD draft text as the basis for their unilateral digital services taxes.Footnote 19

Pillar 2 establishes a global minimum corporate income tax of 15 per cent calculated on a country-by-country basis. Thus far, sixty-two countries – including all EU countries – have implemented the agreement or introduced draft legislation. The agreement went into effect in the majority of implementing countries on 1 January 2024. The agreement is designed to be effective even if not all countries implement the rule domestically; if a country does not implement the global minimum tax, other implementing countries can collect additional tax revenue from firms through the under-taxed profits rule. The OECD projects that only including the jurisdictions that have implemented Pillar 2 thus far, 90 per cent of multinational corporations would be subject to the global minimum tax (Dettoni and Myles Reference Dettoni and Myles2023). In sum, these changes to international tax rules have extensive impacts on the global economy and on firms’ tax bills.

While firms cannot make decisions in most regulatory bodies, they can offer their thoughts on draft rules through public comments. Figure 1 illustrates the process of a public commenting period in the OECD. Each public commenting period at the OECD discusses a unique draft framework. For example, there was a separate commenting period for each of the fifteen action steps included in the Multilateral Instrument, as well as separate commenting periods for different aspects of Pillars 1 and 2. The public commenting period begins when the OECD shares a new draft framework for comment via their website, social media, and a monthly OECD Civil Society Newsletter. Non-state actors have the opportunity to submit one comment in each period in an open-ended format. These comments provide suggestions and information on how to improve the rule, often sharing suggested wording or draft text. The deadlines for the submission of public comments at the OECD are ‘notoriously short’, ranging from three weeks to two months.Footnote 20 Given the limited time to prepare comments, firms prepared their comments individually without extensive input and conversation from other organizations or their national government.Footnote 21 After the deadline, the comments are posted publicly on the OECD website. OECD bureaucrats are then responsible for reviewing the comments and deciding which feedback to integrate.Footnote 22 Once a revised draft has been completed, with tracked changes made by bureaucrats based on public comments, the secretariat shares the revised version with states.Footnote 23 A new commenting period begins when a new draft framework on a distinct topic is released by the OECD and the process repeats.

OECD commenting and consultation process.

Bureaucrats are praised by both the OECD secretariat and the media for providing open opportunities for public comment and stakeholder engagement.Footnote 24 Given these benefits to the bureaucrats from implementing public commenting both internally and externally, directorates were apt to integrate these consultations and ‘publicize it as much as possible’.Footnote 25 Despite these benefits, the process of reviewing these comments places a serious burden on bureaucrats. All interested parties are welcome to submit comments during the process, resulting in ‘tons of comments … I can’t remember how many thousands of pages we got, but it was thousands of pages’.Footnote 26 Similarly, another bureaucrat shared that the open public commenting process resulted in ‘a lot of reactions. And then it’s very difficult to, or resource intensive to, integrate all of that’.Footnote 27 Figure 2 shows the size and sector of firms that submitted public comments.Footnote 28

Distribution of comments.

Data manually coded by the author using public comments submitted to the OECD. The bar graph represents the number of comments by firm size (measured by the number of employees) and sector (two-digit NAICS codes) as classified by Orbis.

However, bureaucrats implement public consultations, despite these resource constraints, in part because the process is instituted informally rather than being subject to dispute resolution or a third party judicial body (Bouwen Reference Bouwen2007; Quittkat Reference Quittkat2011). While there are internal guidelines for how to manage relations with non-governmental stakeholders in the OECD, interviewees said that ‘they should be read with a lot of caution, as I don’t think that anyone follows them closely and I’m not sure many people know that we actually have them’.Footnote 29 These procedures in the OECD are diametrically opposed to domestic notice and comment processes, which stipulate serious legal consequences if the regulatory body does not carefully consider each comment.Footnote 30 Therefore, IO public consultations offer more flexibility and freedom to use shortcuts to evaluate comments.

Research Design

I test the theory using a new observational dataset of 3,349 public comments at the OECD, natural language processing methods, and in-depth qualitative interviews of firm representatives and IO bureaucrats. I use a mixed method approach to address the trade-offs between methods of measuring firm influence (for a detailed discussion, see Dür (Reference Dür2008)). The qualitative evidence offers a detailed illustration of the strategies that firms and associations employ to maximize their influence in IOs. I then use quantitative tests to understand the extent to which the potential explanations determine firm preference attainment.

First, I conducted interviews with twenty-one professionals at firms and industry associations, with the full list of interviews provided in Appendix A7.Footnote 31 To preserve interviewee anonymity, individuals are identified by a generic title and country of residence. I recruited interviewees from those who had submitted public comments to the OECD. The interviewees work at large multinational corporations, small firms, and trade associations across different sectors. The interviews also highlight a range of geographic perspectives, with interviewees from Africa, Asia, North America, and Europe. More information about interview processes and recruitment can be found in Appendix A7. Next, I conducted twelve semi-structured interviews of IO bureaucrats to understand their perspective in co-ordinating stakeholder engagement and reviewing public comments. The sample was generated through purposive selection, as I aimed to gain diverse perspectives across geographic location, firm size, and subject area within the theoretically relevant population. In the interviews, I asked firm professionals to describe how they maximized the impact of their public comments. If interviewees provided answers that corroborated (or conflicted with) my theoretical mechanisms, I considered this evidence (or lack thereof) for the mechanism at work. Furthermore, if none of the interviewees discussed the mechanism, I consider this evidence that the mechanism was not at work. By granting interviewees anonymity, I aimed to maximize respondents’ ability to speak freely and openly about the strategies they used in IO public commenting.

Second, I test the observable implications of the theory using an original dataset of the 3,349 public comments on the OECD tax evasion process. This dataset includes the name of the commenter, as well as their sector, size, nationality, and type of interest group (e.g. firm, association, civil society, etc). The dataset also includes information about the comment itself (e.g. length of comment) and the commenting period. I do not include the most recent commenting periods for which final regulations have not yet been released. The main analysis focuses solely on firms and industry associations, with the total number of observations therefore being 2,779.

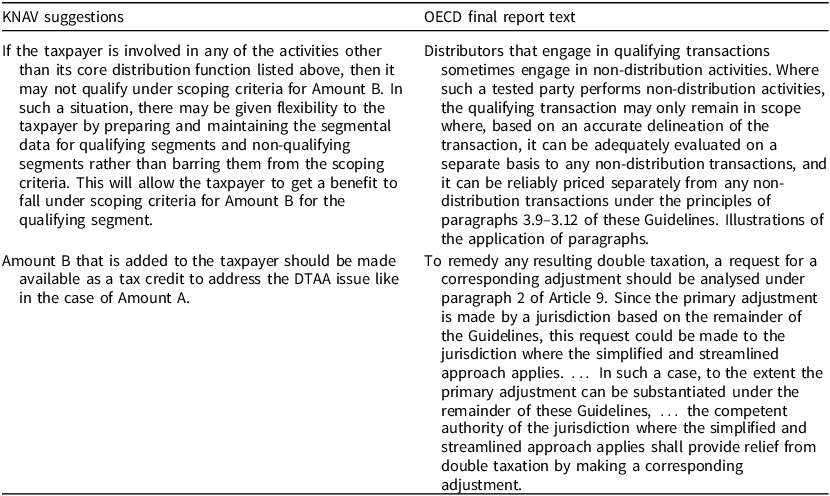

Next, I use natural language processing methods to measure influence on the final regulations. To conceptualize influence, I borrow from the judicial politics literature, which has examined amicus curiae briefs’ influence on Supreme Court decisions. As such, I measure influence as the extent to which a comment is reflected in the final copy of the framework. Therefore, there must be explicit change in the final framework which can be attributed directly to a private actor’s comments. In the judicial politics literature, ‘similarity between a brief and the majority opinion does not necessarily establish a casual link, but such similarity is certainly suggestive of influence’ (Hazelton et al. Reference Hazelton, Hinkle and Spriggs2019, p. 128). Similar to the Supreme Court context, commenters at the OECD often propose specific language to include in the final framework (see Table 1 for examples). This definition of influence is inherently imperfect, as private actors may make comments suggesting the preservation of language already in the draft framework or may exert influence before the draft framework is issued.Footnote 32 Therefore, while this definition of influence does not capture every aspect of the comments’ footprint, it allows for careful empirical analysis and comparison of firm influence.

Example of implemented comments

Note: Both of these comments from KNAV address the draft rules for Pillar 1, Amount B. Under this rule, if a subsidiary is engaged only in distribution activities, the multinational company can then use a simplified pricing matrix to assess the taxes they should pay across various countries. The first comment from KNAV suggested that companies should not be completely excluded from Pillar 1 Amount B if they perform some non-distribution activities, as long as those activities can be segmented and treated separately. The OECD subsequently moved forward with implementing this suggestion, allowing a host of additional companies to get the benefits associated with falling under the simplified pricing matrix. Namely, these companies can now use the simplified matrix rather than having to conduct the compliance work to calculate their tax liability, which also relieves them of potential disputes between countries in which they have operations. Second, KNAV asked the OECD to specify that if one country adjusted the amount of tax due under Amount B for a firm, that the other countries in which the firm operates provide corresponding tax credits or adjustments to ensure that the income is not taxed twice.

To identify the influence of firms on the final framework, I use a natural language processing method: cosine similarity scores. This score measures the similarity between two vectors of an inner product space. Further, cosine similarity scores are a ‘standard mathematical formula conducted by search engines that summarizes the similarity between two documents’ (Hinkle Reference Hinkle2015, p. 137). I compile the draft and final regulations for each public commenting period from 2013 to 2020. Each set of comments corresponds to a specific final framework which allows direct comparison of whether comments were implemented into those rules. I measure the similarity between the firm’s comment and the final framework in each commenting period, with the unit of analysis at the firm-comment period level. These scores are bounded between 0 and 1, with scores closer to 1 being more similar documents.Footnote 33 This method offers a broader view of the similarity between documents than other methods, and has been shown to be more accurate in capturing influence in the context of US Supreme Court briefs (Hazelton et al. Reference Hazelton, Hinkle and Spriggs2019).Footnote 34 I further validate the indicator by hand coding a random set of public comments. More detail about the hand coding can be found in Appendix A8. The hand coding process requires reading the full comment (1–50 pages) and comparing whether there were changes from the draft to final framework in line with their suggestions. This process is extremely time consuming, given the length of the comments (25,000 pages total) and frameworks (80–100 pages each). Therefore, hand coding is not feasible for the full sample. There is a positive and statistically significant relationship between the hand coding scores for influence and the cosine similarity scores. In addition, I re-estimated the models using another popular similarity score measure: jaccard similarity scores. The results can be found in Appendix A8 and are robust to the use of this alternative measure of similarity.

Note: This bar graph illustrates the distribution of the independent variable – the number of commenting periods in which firms and associations commented. Firms and associations participated in a mean of twenty-two commenting periods (median: 19.5). The distribution of the independent variable is broken down further by type of organization, sector, and country in Appendix A5.

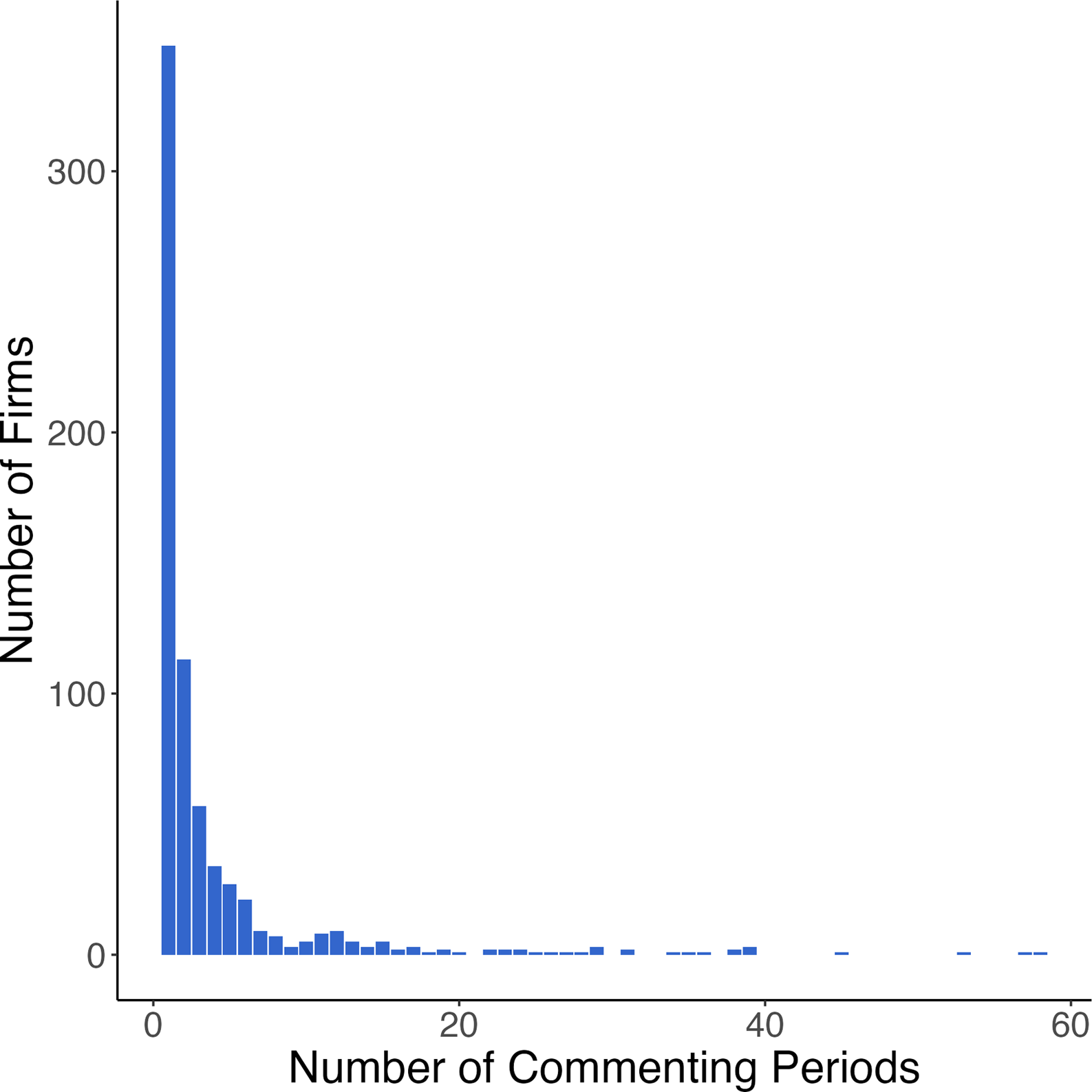

Next, I discuss the operationalization of the independent variables. I use three proxy variables for the comment’s quality and assess each of the subparts to Hypothesis 1. First, I measure uniqueness by calculating the cosine similarity scores of each comment with the other comments in the same period. I consider a comment unique if the maximum cosine similarity score with other comments is less than 0.5. Second, I measure the level of technical information by calculating the Flesch Reading Score for each comment. This score represents the readability of the comment, categorized by the level of education required to understand the comment. I consider high level technical comments to be a Flesch Reading Score of 50 or less, which equates to a college or professional reading level on the topic. Third, I measure the tone of a comment by calculating the Qualitative Discourse Content Analysis sentiment score, with neutral or positive comments ( ≥ 0) coded as 1 and negative comments coded as 0. Next, I evaluate Hypothesis 2 with an independent variable that proxies for the firm’s breadth of participation across issue areas. I measure breadth of participation as the number of commenting periods in which a firm participates. Each public commenting period discusses a new piece of the draft regulation and firms have the opportunity to submit one comment per period. Therefore, the number of commenting periods in which the firm participates captures whether participation was broad based and sustained across issue areas, or selective and volatile on one topic that the firm is most worried about. There is substantial variation in this measure (see Figure 3), ranging from one to fifty-eight commenting periods in which the firm participated.Footnote 35 This measure, while imperfect in fully conceptualizing reputation, offers empirical tractability as an observable implication of the theory. As such, these quantitative tests complement the more robust understanding of reputation gleaned from the qualitative interviews.

Variation in the independent variable.

I include two controls. First, I control for the length of comment, measured by the number of words in the comment. Secondly, I control for firm size, the number of employees from Orbis. This measure most closely proxies a firm’s revenue and market power while limiting missingness in the data. Finally, I include country and sector fixed effects. Country fixed effects account for differences in state power in IOs (Steinberg Reference Steinberg2002) and support for their firms. I also use sector fixed effects to account for differences in the number of employees at firms and to show that the relationship between reputation and influence exists within sectors.

Results

I first consider the qualitative interview evidence. As discussed above, I ask interviewees an open-ended question about the strategies used to maximize the impact of their public comment. Both firm representatives and bureaucrats shared that comments were only influential if they provided unique, technical, and non-rhetorically charged information. Bureaucrats shared that helpful comments consisted of new technical information, suggestions on how to improve the rule, and expert analysis of proposals.Footnote 36 Alternatively, comments were not particularly influential if they were duplicated verbatim from another organizationFootnote 37 or if the comments were rhetorically charged with ‘too much of a lobbying tone’.Footnote 38 In general, if comments ‘are not backed by evidence … we cannot incorporate them’.Footnote 39 Similarly, firms indicated that their approach to commenting was primarily ‘fact based’, ‘well reasoned’, and focused on ‘the effect on markets, industry, or consumers’.Footnote 40 In addition to sharing technical information and expert analysis, firms also shared that they avoided rhetorically charged comments – ‘[we] leave the rhetoric to other people … It is a real turnoff to the audience. And it unnecessarily undermines your credibility’.Footnote 41

However, both bureaucrats and private actors shared that information was not enough, and that reputation for trusted expert information sharing, formed by participating frequently across a breadth of issue areas, was pertinent to the private actors’ level of influence. The evidence therefore supports the hypothesis that reputation as a mechanism is at work. Interviewees explicitly stated the importance of building their reputation to have an impact on the OECD regulations. A US Trade Association Lobbyist described their logic for commenting: ‘We comment on every discussion draft because we wanted to establish ourselves as the leader in that consultation process – and based on feedback from OECD, Treasury, and foreign governments – we were able to establish that. We just kept hearing, “Oh you’re the first letter that we read on this on this consultation”. That’s your goal really to have that kind of reputation’.Footnote 42 In addition, a French industry association representative stated: ‘We regularly respond to consultation published by the OECD … it is very important for us to create communication channels … and [the organization] maximizes the impact of its public comment through … direct and constant dialogues with the IO’.Footnote 43 Even once a reputation has been established, continual effort is needed to maintain it. Another interviewee stressed the following: ‘You have to establish your relationship [with the OECD] and then you have to maintain your relationships. It’s not like something that just, it was handed over, and then, you know, once you establish it, you have to work to maintain it through continued commenting’.Footnote 44

This mechanism does not only operate in developed economies: interviewees in middle income countries also expressed a similar logic to their public commenting. In India, a firm professional expressed that their effort in public commenting was to gain visibility and recognition within the IO. The interviewee stated: ‘We have been regularly contributing since 2019. Our expectation is not of getting anything out of it like financial gainFootnote 45 – we are giving back our knowledge and experience and hopefully it helps in a larger sense … It gives us recognition and visibility. And that’s the reason we contributed – to give back and to gain visibility’.Footnote 46 In addition, interviewees stressed that they felt that their comments allowed them to enhance their status in the IO and avoid being ignored on account of their size or country of origin. A South African firm professional stated: ‘That’s not to say that our smaller organization goes into a black hole … We like to think that the effort that is put [into commenting], we are standing in the crowd with similar views’ rather than being ignored.Footnote 47

Bureaucrats also discussed the different approaches of firms in the public commenting process through their choice of one-time or broad-based participation. There is an explicit understanding from bureaucrats that firms participating on a one-off basis do so because of the importance of a singular issue that intimately affects their business interests. These firms interact with IOs on an infrequent basis, only reaching out ad hoc to the IO when the discussions turn to a particular issue that the firm is most concerned about.Footnote 48 Bureaucrats recognize that these firms’ goal is to affect the rules on a particular issue that is important to their business interests. In contrast, bureaucrats also encounter firms that form a ‘strategic long-term relationship’ by engaging regularly and repeatedly.Footnote 49 An important feature of their engagement is providing private information to bureaucrats across issue areas: ‘reaching out to us on a regular basis to brief us on what’s happening from their perspective, [as well as] how they see certain developments in a particular jurisdiction and other jurisdictions’.Footnote 50 These relationships are systematic and repeated, offer valuable information to bureaucrats, and continue across various issue areas. Bureaucrats recognize these ‘particularly active’ firms when considering the information that they share with the secretariat.Footnote 51 When asked about how the secretariat delineates between comments that might be helpful or unhelpful to the process, bureaucrats referenced the reputation of firms: ‘it’s a lot about trust’.Footnote 52 These reactions by bureaucrats are also reflected in the OECD Secretariat Guidelines for Consultations with Stakeholders, which emphasize: ‘stakeholder engagement is undertaken most credibly and effectively with a long-term perspective … with the aim of building trust and mutual understanding between an entity and its stakeholders’ (OECD N.d.).

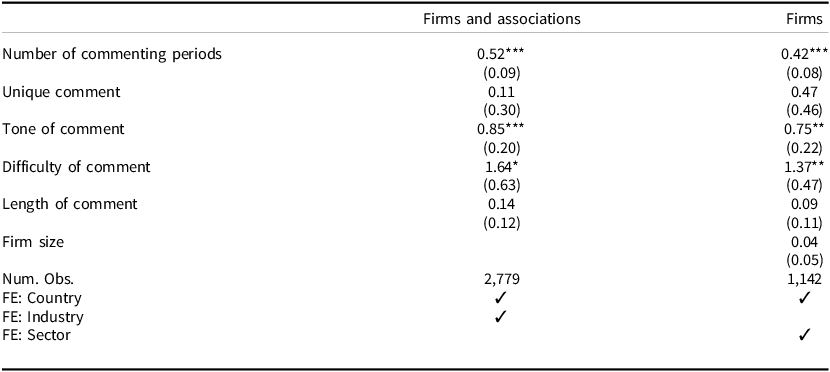

Next, I test the observable implications of the theory using ordinary least squares (OLS) regression at the firm-comment period unit of analysis. Table 2 shows the full results. First, I find that comment quality, proxied by uniqueness, tone, and technical information, is positively associated with the influence of the comment. However, the majority of comments submitted by business actors are high quality, in line with Yackee and Yackee (Reference Yackee and Yackee2006). Therefore, while the quality of a comment affects its influence on IO rules, these factors do not tell the full story. Therefore, I also consider how breadth of participation affects firm influence. The interview evidence corroborates that firms’ decision to participate across commenting periods reflects a strategic decision to build a reputation.Footnote 53 There is a positive and statistically significant association between the breadth of participation and influence on the IO, providing support for Hypothesis 2. While the coefficient estimate is small, it is substantively large.Footnote 54 Even small changes to the text of a final regulation have a profound influence on the tax consequences for firms. Important examples include firms’ successful efforts to exempt their industries from certain OECD international tax regulations. I illustrate in Appendix A8 how comments from shipping associations, airlines, and pension funds resulted in successful carve-outs for their broader industry, with significant impacts on their subsequent tax liability.

Influence on IO rules

* p < 0.05, ** p < 0.01, *** p < 0.001.

Note: This table provides the ordinary least square regressions of the main results. The dependent variable is the cosine similarity score of the comment and the final framework. The main independent variable is the number of comments submitted by the firm during the public commenting process (logged). I also include variables to proxy the comment quality: unique comment (max similarity score with another comment <= 0.5), comment sentiment (QDAP score ≥ 0), and technical information (Flesch Reading Score <= 50). This model includes the following control variables: firm size (logged) (from Orbis) and the length of the comment (logged). I also include sector (two-digit NAICS codes from Orbis), country (headquarters of the firm from Orbis), and industry fixed effects.

In the Appendix, I provide additional robustness tests. The results are robust to alternative modeling specifications, with and without fixed effects and controls (see Appendix A4). The results of the main analysis hold when filtering to informative, technical comments – those which bureaucrats primarily need heuristics to evaluate as resource constraints prevent them from independently verifying the information (Table 7). Next, I show that these results are not driven purely by firms that specialize in tax – the results hold when excluding the Big 4 accounting firms and I find that comments from the professional and technical services sector are not more influential than those from other sectors (see Appendix A4). Finally, I show that comments are less influential if the firm only participates on one issue (Table 9).

Conclusion

In sum, I argue that firms’ comments are more influential if they are high quality and intended to meaningfully improve the regulation. Because the majority of firms offer comments with quality technical information, bureaucrats use a firm’s reputation for expert information sharing as a heuristic for which comments to focus on and subsequently implement. While these processes are open to all, it undoubtedly privileges large and profitable private actors who have the ability to participate regularly in this costly process.

This paper illustrates a case of potentially unintended firm influence. Even with the most transparent form of stakeholder engagement, there are still active firm strategies to increase their influence. This paper finds that IO stakeholder engagement might be a double edged sword. While intended to democratize access to the policy-making process, these fora are still susceptible to strategic firm behavior to influence regulations. In another respect, this form of firm influence is unique in that it does not depend inextricably on firm size. Small firms that invest heavily in the process are able to have an outsized influence, which is unique from findings in the domestic lobbying context.

These results speak broadly to non-state actor influence in global governance. I expect these results to be generalizable to regulatory bodies that offer public consultationsFootnote 55 on topics that (1) affect firms’ interests and (2) require private information to create effective regulations. Examples of other potential issue areas that meet these scope conditions are diverse, including health / public safety, climate change, and corporate responsibility, among others. Firm reputation is likely more important for influence in regulatory bodies with broad membership or when working on an issue with international implications, as there is a larger universe of potential private actors that could participate. In this context, it is more difficult for policy makers to independently verify information and it is more likely that policy makers will rely on the reputation heuristic. In sum, this paper has demonstrated that firms have an important and substantive influence on regulations even under the most unlikely conditions.

In the context of our broader understanding of firm influence in global governance, this paper also demonstrates that there are important differences within interest groups on policy making influence and strategy. This project provides a call to further open up the black box within interest groups, delineating which actors in broad categories of interest groups – like business actors and NGOs – are most influential. In addition, this paper illustrates the importance of relational and ideational aspects of firm influence, rather than focusing solely on the material characteristics of interest groups. In particular, this case highlights not only how private actors participate in stakeholder engagement, but also how these contributions are then subsequently considered by bureaucrats. While this paper focuses on why certain private interests are most effective in attaining their preferences on global regulations, it remains an open question why particular firms choose to invest resources to build a reputation with regulators, while other similarly placed firms in a particular industry choose not to. Future research could investigate which particular firms choose to act as entrepreneurs in this process and their motivations for doing so, outside of market-oriented explanations.

Understanding the internal processes of regulation formation has important implications for democratic legitimacy in the international system. In the increasingly globalized world, global governance mechanisms have far-reaching influence and utility. Furthermore, IO regulations are often viewed as a model for domestic governments (Arel-Bundock and Lechner Reference Arel-Bundock and Lechner2024), especially in cases of technical or economic policies which are costly to construct independently.Footnote 56 Therefore, the results of these policies are far reaching and reverberate throughout the international community. Future research should expand beyond the focus on firms and further disaggregate this process. Evaluating the relative influence of firms versus civil society could offer important insight into which voices are being heard within IO decision-making processes.

Additionally, the case of tax evasion in the OECD has long-range implications for citizens’ public services and the evolution of firm power in the international system. The ability of firms to shield themselves from appropriate levels of taxation has direct consequences on the public revenue of states, the social services offered to citizens, and the tax rates of individuals. This paper demonstrates that non-state actors – in particular firms and business associations – played an integral role in the revision and rewriting of important international tax regulations. Despite previous literature that suggested IOs are more independent from private sector influence (Abbott and Snidal Reference Abbott, Snidal, Mattli and Woods2009; Young Reference Young2012), this paper demonstrates a case in which private actors were influential in the process of writing international rules. Tax regulations are substantively important, and can be seen as one of the most important tools of state policy that affect the everyday lives of citizens. Future research should consider how these new international taxation rules affect other political outcomes both internationally and domestically.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S0007123426101434.

Data availability statement

Replication data for this article can be found in Harvard Dataverse at: https://doi.org/10.7910/DVN/QNZWDY.

Acknowledgments

I thank Vinod Aggarwal, Ryan Brutger, Susan Hyde, Aila Matanock, Michaela Mattes, Layna Mosley, Iain Osgood, Rebecca Perlman, Emmanuel Saez, and Calvin Thrall for helpful feedback and advice on this research. I also thank audiences at APSA 2023, PEIO 2024, the University of Texas at Austin, UC Berkeley IR/CP, and University of Michigan PEEG. Finally, I thank the three anonymous reviewers and the editorial team at the British Journal of Political Science.

Financial support

This research received no specific grant from any funding agency, commercial, or not-for-profit sectors.

Competing interests

None to disclose.

Ethical standards

The qualitative interviews comply with the APSA Principles and Guidance for Human Subjects Research and were approved in IRB protocol 2022-10-15694 by the University of California, Berkeley.

Open access

Open access