Introduction

Money and the City of Edinburgh share a long history. The “goldsmiths of Eidynn” appear as early as the seventh century CE in the epic poem Gododdin. Footnote 1 Bank of Scotland, the first recognizably modern financial institution in the city, was founded by royal charter in 1695, just a year after the Bank of England. It was, “the first instance in Europe…of a joint-stock bank formed by private persons for the express purpose of making a trade of banking… wholly unconnected with the state.”Footnote 2 The Royal Bank of Scotland followed in 1727, also by royal charter.Footnote 3 It quickly invented the “cash credit,” better known today as the overdraft, “one of the most ingenious ideas that has been executed in commerce,” according to David Hume, Edinburgh’s most celebrated philosopher.Footnote 4 The two banks together went on to normalize the use of bank notes as day-to-day currency long before the rest of Europe.Footnote 5 By the time of the boom and bust which followed the conclusion of the Napoleonic wars, they were powerful enough to prevent the UK government from removing the right to print their own bank notes.Footnote 6 So admired were their practices that delegations arrived from as far apart as the Paris Chamber of Commerce and the new government of Chile to find out how it was doneFootnote 7 while banks on the other side of the world were founded on “sound Scottish banking principles.”Footnote 8

Meanwhile, in the eighteenth century, two ministers of the Church of Scotland, concerned for the well-being of ministers’ widows, collaborated with the then professor of mathematics at the University of Edinburgh to devise the statistical analysis which, to this day, underpins the life assurance industry.Footnote 9 Life assurance went on to become the second constituent of Edinburgh’s financial trinity. Of the dozen or so firms which sprang up, Standard Life was, at its height in the late twentieth century, the largest such concern in Europe.Footnote 10

The twentieth century saw the development of the third constituent, the asset managers. They grew out of the legal and accounting professions that had been looking after the wealth of Scotland’s landed gentry for generations.Footnote 11 Effective deployment of a new device called an Investment TrustFootnote 12 (not invented but arguably perfected in EdinburghFootnote 13) led to the growth of partnerships of professional asset managers such as Ivory and Sime and Baillie Gifford. Baillie Gifford launched Scottish Mortgage Trust, for example, in 1909 with a subscribed capital of £50,000. Still managed by Baillie Gifford, it is currently capitalized at around £8 billion. By the 1980s, 20% of all investment funds under management in the UK and much the same share of life assurance funds were being managed in Edinburgh, putting it on a par with Zurich, Boston, and New York.Footnote 14 The Global Financial Centres Index (GFCI) did not appear until well after the periodization of this paper (see below) but when it did, in 2007, Edinburgh was fifteenth in the world rankings, second only to London in the UK, and sixth in Europe.Footnote 15 Subsequently, the Royal Bank of Scotland, briefly styled RBS in an attempt to broaden its appeal internationally, became for a brief moment the largest bank in the world before it crashed, burned, and partly caused the Global Financial Crisis (GFC) of 2008. As will become apparent, that story is not part of this paper.

What was it that had enabled this small city, remote from other centers of financial and political power, with only a modest manufacturing or trading base, to develop an array of financial expertise on such a scale? Why could its near neighbor, Glasgow, only manage one life assurer (Scottish Amicable), one asset manager (Murray Johnstone), and one durable bank (the Clydesdale) of any scale? By the mid-nineteenth century, it was bigger, more heavily industrialized, throwing off mountains of cash, and better placed to take advantage of the lucrative trans-Atlantic trade. Instead, it became notorious for bank failures, including the City of Glasgow Bank in 1878, the UK’s worst until the GFC, developing “an ugly reputation for speculative business.”Footnote 16 Researchers appear to have largely side-stepped the question. H.C. Reed’s study of international financial centers 50 years ago includes such modest locales as Bergen, Cadiz, and Lima but ignores the Scottish capital.Footnote 17 More recent studies of “capitals of capital” have concentrated on a handful of larger players, from New York to Singapore, and focused on banking rather than taking on the sector as a whole.Footnote 18 General historians have relegated Edinburgh’s financial sector to little more than a footnote.Footnote 19 There are a handful of specialist Scottish accounts, again focusing on bankingFootnote 20 and some uncritical anniversary accounts of individual firms.Footnote 21 The only serious attempt at a narrative history of the city as a single financial center arrived relatively recently.Footnote 22 It does not flinch from the unravelling of much of this success story in the GFC in which those two original Edinburgh banks played such disastrous roles. But it left critics wanting more; “it doesn’t really explain why this city of money was unique to this place.”Footnote 23

This paper seeks to address exactly that challenge. It does so by collecting oral history from the leadership of Edinburgh’s financial sector over 40 years in the mid-twentieth century, treating this elite across banking, life assurance, and asset management as a single entity. Then, working within the relatively new paradigm of Historical Organisation Studies and its call for “dual integrity,”Footnote 24 it applies the theoretical framework of “field,” “capital,” and “habitus” developed by Pierre Bourdieu, and in particular his concept of habitus, to this data.Footnote 25

The following sections proceed as follows. First, Bourdieu’s concept of habitus and its applicability to historically based research are outlined. Thereafter the basis on which the historical data was gathered and the period selected are set out. After presenting the findings, their implications are discussed. Finally, the conclusion considers the value of this contribution and speculates on the challenges of extending the period of study deeper into the past.

Theory and Practice

Bourdieu did not invent habitus. His contribution was to broaden and deepen the central concept of an idea that reaches back to Aristotle,Footnote 26 incorporating it into his quasi-mathematical master theory of (Habitus × Capital) + Field = Practice.Footnote 27 The basic principle is simple: “Society becomes deposited in persons in the form of lasting dispositions, or trained capacities and structured propensities, to think, feel and act in determinant ways, which then guide them.”Footnote 28 Later, in response to the observable reality of agents adopting rules and standards of a given specialized field, he came to acknowledge the possibility that a secondary, possibly contradictory, habitus could develop. This secondary habitus remains largely unexplored outside Bourdieu’s preoccupation with education.Footnote 29 Findings in this paper, however, show evidence of it operating in workplaces through custom and practice in ways that imply a sustained level of what Bourdieu called “symbolic violence,” discreet, unspoken but effective systems for controlling behaviors.Footnote 30

Freshly gathered oral history provided a basis on which to operationalize the concept of habitus. Oral history has long been recognized as a legitimate primary source, albeit with obvious provisos as to its inevitable subjectivity and uncertainty of memory.Footnote 31 In the present case, subjectivity works to the historian’s advantage. No one is better placed to describe what living and working within this field felt like at the time than those who were there.Footnote 32 Where, though, to begin? There seemed little value in revisiting Edinburgh’s immediate past. Those still actively involved in financial services would be constrained by issues of confidentiality, fiduciary responsibility, and stakeholder obligations. Further back, it seemed unambitious to add to the tsunami of accounts of what went wrong and what may have led to the GFCFootnote 33 which already include detailed and prize-winning accounts of Edinburgh’s part in the catastrophe.Footnote 34 Furthermore, for reasons not directly related to the GFC, other jewels in the crown of Edinburgh’s financial sector have lost some of their luster in the twenty-first century such that Edinburgh’s position in the latest (38th) GFCI has now declined to 32nd.

The challenge to any arbitrary periodization, as Koselleck made clear, is that history does not begin or end at convenient fixed points.Footnote 35 Yet, as it happened, there was a fixed point in the late twentieth century which, by common consent, did usher in a new paradigm for financial services in the UK. The consequences of the enactment of the Financial Services Act on October 27, 1986,Footnote 36 popularly known as ‘the Big Bang’, did not materialize immediately. But a wide range of literature takes this momentous deregulatory shift, along with the parallel move to digital on-screen trading, as its point of departure. Two months later, the Building Societies Act,Footnote 37 which enabled banks and building societies to compete directly, completed the transformation of financial services in the UK.Footnote 38 Most of those interviewed for this research saw 1986 in just such a light. “It’s the obvious caesura,” was how Roger (one of the interviewees—see below) described it. If this were the beginning of a new world, a better understanding of the older world as it arrived at that point might yield meaningful insights. This research therefore used 1986 as an end point. As a start point, the even bigger caesura of the end of World War II was the inescapable candidate. The sample was therefore made up of people mostly born in the 1930s and 40s (the oldest was 93 at the time of the interview) who reached the zenith of their career in their respective firms generally either before or shortly after 1986. Only those who reached the most senior positions were approached. As well as their own firm, almost all of them had non-executive roles on boards of other Edinburgh financial institutions so they all had a city-wide perspective. Only when a degree of saturation set in, with fewer fresh insights, was the scope broadened slightly to include a few contributions from less exalted positions, to get a view from below.

Recollections at that age need to be treated with caution, both in terms of straightforward memory loss and a natural tendency to a degree of ex post facto rationalization.Footnote 39 By triangulating with published and unpublished sources over the same period, it was clear that, at least as far as external public events were introduced, very few significant details were misremembered. A further opportunity for corroboration was that many of the subjects, as one might anticipate in a small circle of senior managers, either personally knew or knew of the others. However, it is worth reiterating that eliminating subjectivity was not the goal. What mattered was what the subjects themselves believed to be true and what that demonstrated of their subconscious habitus.

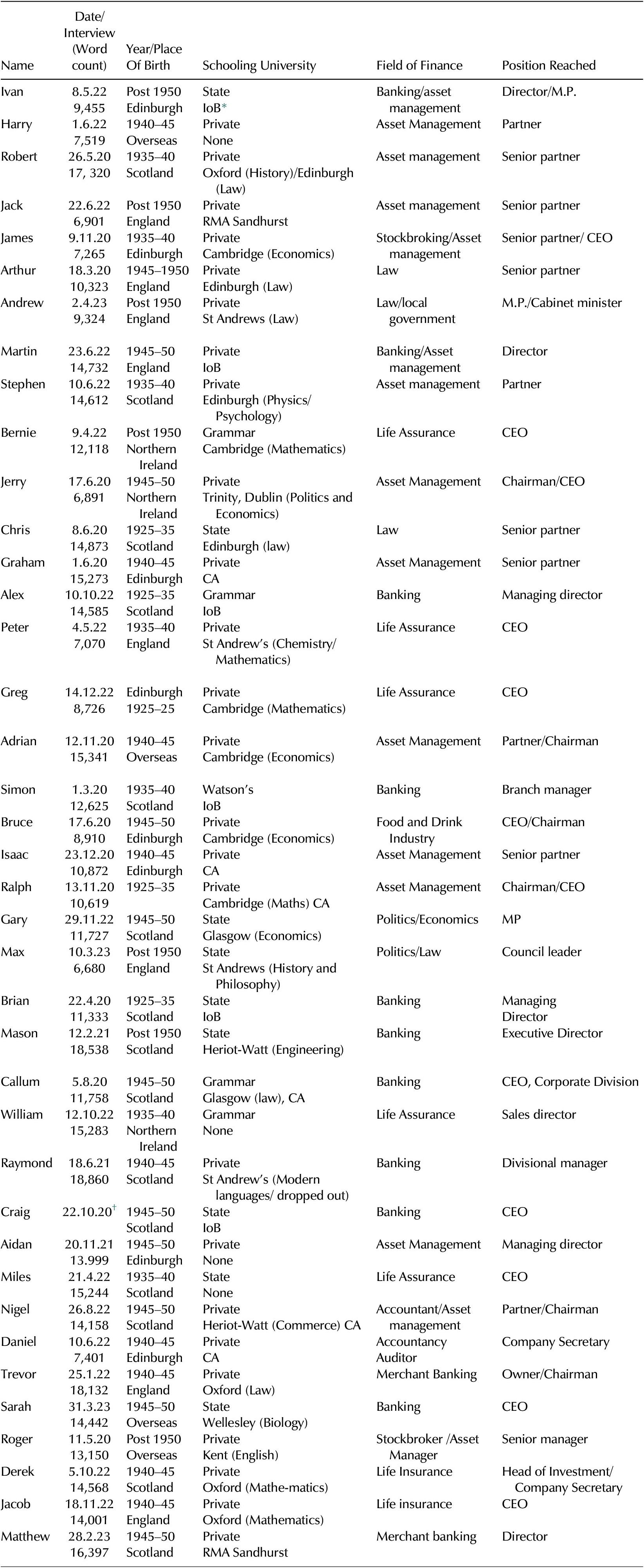

With one exception, the list of interviewees is made up entirely of white men. This was but a reflection of the times; women were not present except as wives or a limited quota of clerical staff. A rare female actuary was located but declined to be interviewed. The former (female) PA of a leading figure in Edinburgh’s financial elite was also approached but was similarly reluctant. Their instinct, not to say their habitus, for discretion prevailed. The exception was a banking executive who was in the same age group and seniority but came to Scotland (from the United States) at the end of the period. In addition to her own history, she also provided a useful additional triangulation point. A list of interviewees is attached in Table 1: Interviewees. The following pages identify the subjects by (not their real) first name only.

Interviewees

* Institute of Bankers.

† Interview not recorded. Contemporaneous notes taken.

Given that habitus is subconscious and can only be established by analyzing the subject of the research, the approach has necessarily been a qualitative, inductive one, based on a series of semi-structured, first-person interviews. While the sample was random at an individual level, the intention was to get a balance across the city’s main three financial sectors. The interviews were conducted during and after the COVID pandemic, many via Zoom. Accessing these people was not straightforward. Whatever their previous distinction, few of them needed or wanted public profiles. For them too, discretion had always been a virtue. Even when the access hurdle had been overcome, other challenges in studying elites remained.Footnote 40 Questions requiring internal reflection were commonly deflected with anecdote or disingenuousness. Nevertheless, the resulting data produced a usable diachronic insight into the trajectories of the subjects’ lives and professional practices during the period in question.

The interviews were recorded, transcribed, and coded for a number of indicators.Footnote 41 This relied on intensive reading and re-reading rather than mechanical textual analysis because, first, there is no suggestion that this was a quantitatively adequate sample, and second, what was said required individual scrutiny. In line with Bourdieu’s strictures on the reflexivity of the researcher,Footnote 42 I declare that I had no pre-existing specialist knowledge of finance in general or Edinburgh’s financial elite in particular. I was neither born in nor live in Edinburgh.

Before proceeding to the empirical findings, it is worth calling to mind, as context, external events which impacted the financial services sector during this period. These included the discovery, of particular interest in Edinburgh, of substantial oil and gas reserves in the North Sea in the 1960sFootnote 43; the end of post-war currency controls (1959); the emergence of the Eurobond market (1960s); the introduction of capital gains tax (1965); the secondary banking crisis (1973–75); the oil price shock (1973); the UK’s accession to what was then the European Economic Community, now the EU (1973); and the abolition of the investment income surcharge (1985). The biggest structural change was technological. Banks, with their many routine tasks, were early adopters of computers. Bank of Scotland claims to have been the first, in 1959,Footnote 44 though the full impact of digitization was only to become apparent after the period of study.Footnote 45

The research subjects naturally had suggestions of their own for what one might call Edinburgh’s long bull run up to this point. These included its lower cost base, its ability to retain quality staff, its separation from the rumor mill of the City of London, its long-term, value-based approach (investment operations in Edinburgh held stock for twice as long as the national averageFootnote 46), and its internationalism (see, for example, Turrentine Jackson on early Scottish investments in the American railway networkFootnote 47). While these observations are not without value, the technical skill or otherwise with which the sector dealt with external events is not the subject of this paper. The focus is on the dispositions of the people at the apex of the elite rather than on the details of this or that transaction.

Findings and Analysis

In the Beginning

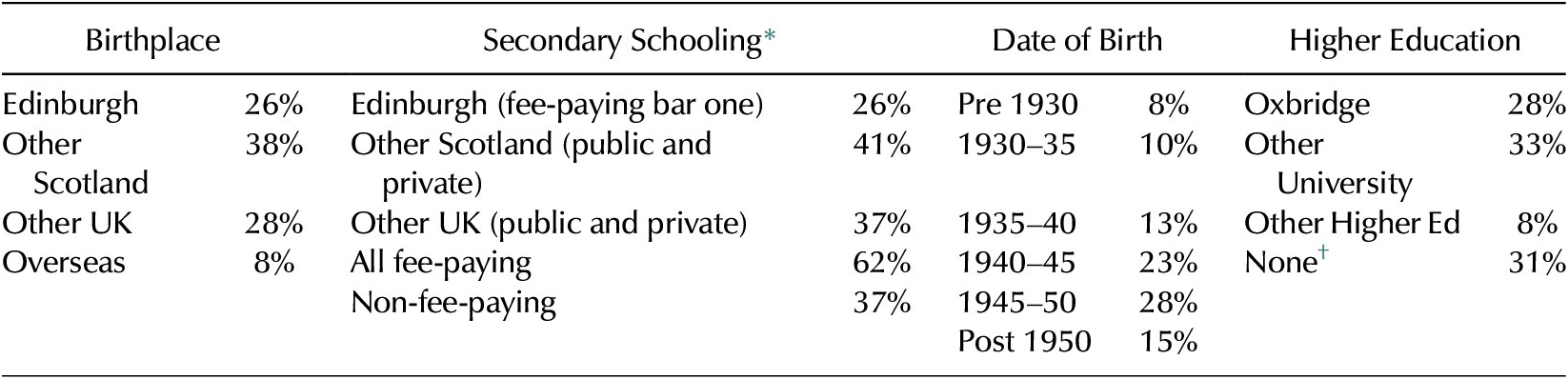

Habitus begins at home, to paraphrase the old proverb. Had Edinburgh been the birthplace of all the members of the sample, it would have been tempting to propose some sort of genius loci, a common geographic factor. In fact, no such homogeneity was apparent. As already indicated, this was a random sample, apart from the attempt at balancing the disciplines. It makes no claim for statistical validity. Even so, it was striking that only a quarter of the sample were born in Edinburgh. Of the remainder, another third was not even born in Scotland. Three of them, Harry, Archie, and Roger, were born overseas (see Table 2: “Origins and Schooling”). Family backgrounds also varied widely, from the armed services to the medical profession. Barely a third had fathers or grandfathers connected with financial services. Alex and Brian, two of the most senior bankers, had fathers who were, respectively, a structural engineer and a small-scale company secretary in the construction sector. Moreover, parents who were in the sector did not necessarily encourage their offspring to follow suit. Callum and Simon were both actively advised by their banker fathers to follow other career paths. Could Edinburgh’s financial elite really have been drawn from such a diverse base?

Origins and schooling

* Numbers add up to more than sample size as categories overlap.

† Includes apprenticeships, professional qualifications, etcetera.

Percentages do not all add up to 100 because of rounding.

On closer inspection, another picture develops. All three of those born overseas (two of them in military families with strong links to Scotland) were sent back to boarding schools in Scotland for their education. Two who were born in England moved to Scotland as infants. Three more had extended families with landed estates in Scotland which they visited regularly. Ralph, though neither born nor schooled in Edinburgh, spent much of his school holidays at the Edinburgh home of an uncle who was a judge in Edinburgh’s highest court. Edinburgh might not have been their home but they had ample opportunity to acquire its dispositions and ideologies. Similarly, while they may not have been universal, powerful family connections were evident. Isaac was the grandson of the founder of one leading asset management firm of which his father was still chairman. James, a stockbroker, had a father who chaired an investment trust and an uncle in one of the asset management firms. Matthew’s father, the proprietor of several thousand acres of north-east Scotland, sat on the board of the Clydesdale Bank among a host of other boardroom appointments.

Other connections were more oblique but no less material. Arthur got a start at the law firm of which he eventually became senior partner because he crewed on a yacht owned by the father of an Edinburgh University friend. The father was a partner in the firm. Raymond was able to join a stockbroking firm because his father chanced to encounter one of the firm’s partners, with whom he himself had previously served in the Royal Navy, while they were out shooting. Christopher’s father, a minister in the Church of Scotland, wrote to a friend in a law firm saying, “I have a son who’s not altogether an idiot. Could he come for an interview with a view to possibly doing his apprenticeship there?” No interview was required. The reply read, “Tell your son to begin on the 1st of September.” Christopher excused himself by explaining: “That was the way things were done in those days.” In saying so, he revealed more of the importance of class and caste (see below) than he may have intended.

Another primary source of habitus is education. Here again, initial expectations were confounded. The privileged status of pupils at certain fee-paying schools in the UK is familiar.Footnote 48 Across the UK, about 6% of children attend them. In Edinburgh, which has long had an exceptional concentration of such schools, that figure is 25%.Footnote 49 It might therefore have been anticipated that a high proportion of this elite group would have attended such schools. Sure enough, if you exclude the Americans and the four who attended state-funded but selective grammar schools (which, at this period, tended to model themselves on the codes and protocols of private schools), only six were educated in the state system. Yet a good proportion of those born in the city, such as Bruce, Isaac, and James, were sent away to arguably more prestigious boarding schools in England. Recent research suggests that the physical location of such schools is not as significant as the recognizably repeating patterns of rituals, hierarchies, and standards they maintain. Those who attend them, wherever they are geographically, automatically become citizens of the same country of the mind that they create.Footnote 50

In short, a modest re-framing of what is understood by home and class embraces a much larger proportion of the group. Most of them enjoyed an upbringing that was at least comfortably middle-class or respectably bourgeois. Some were in the lower reaches of the peerage. Not everybody came from a household where their father routinely dressed formally for dinner (as Bruce and Isaac did) but only two, Mason and Aidan, had parents who worked in manual labor. Mason grew up in what was then a mining village just outside Edinburgh. For clever boys, the best way to avoid going down the local coal mine was to look to the city:

Mason: … [they] joined banks, insurance companies, because you’re close to Edinburgh and there was lots of jobs for it. Companies like Standard Life or Scottish Equitable, all these types of companies.

Aidan, growing up within the city limits, joined one of the asset management companies as an office boy. Among his daily tasks when he began was to lay the fire in the managing director’s office. He went on to become managing director of the same firm himself, a remarkable trajectory.

There was one overwhelmingly common formative influence shared by almost the entire sample: the Church of Scotland. A few were from other Protestant denominations but there was not a Catholic, never mind a Jew or a Muslim, to be seen. In one sense, this is entirely unexceptional; it was the national church after all and most people born in this period were brought up within one church or another. But just because it is widespread does not make the habitus effect any less real. We shall return to this important institutional influence in the sections on prevailing ideologies below. Suffice to say, for the moment, that the extent to which Mason’s primary habitus stayed with him may be judged by the fact that when he eventually left banking altogether, weary of what he saw as its excesses, it was to become a minister in the Church of Scotland.

Growing up

When it comes to higher education, a more uniform picture begins to take shape. Most of this cohort, whether they had degrees or not, acquired professional qualifications as lawyers, accountants, actuaries, et cetera, via relevant institutional bodies (see “The Professionals” below). Banks at this time recruited directly from schools and sent their recruits to the Institute of Bankers for training. Simon recalls the headmaster of his private school in Edinburgh announcing at morning assembly that if any boy of 16 or over wanted to work for Bank of Scotland, there would be an examination in the school hall that afternoon. It was a scene repeated in other private schools but Simon’s school had a better claim than most to supply the bankers of the future. In another instance of the city’s long relationship with finance, the school’s eponymous founder had been Bank of Scotland’s first chief accountant.

However, over half did go to university and, of those, a high proportion went to Oxbridge. This is more significant than it would be today. Fewer than 3% of school leavers went to university in 1950, rising only to 8% by 1970.Footnote 51 University degrees were not the key to managerial positions they later became. For those who did go, subjects ranged from Physics to Law. The demanding nature of the Faculty of Actuaries’ examinations meant that their candidates were likely to have studied mathematics. But a facility with numbers was a common characteristic right across this elite. Aidan, the working-class lad made good in asset management, had to take an arithmetic test as part of his initial application for office boy. He finished 20 minutes before the allotted time and was the only candidate who answered all the questions correctly. Few went as far as Isaac, who decided not to take up a place at Cambridge to read mathematics as, he claimed, it was not going to be sufficiently challenging. Instead, he went straight to a firm of accountants, describing the Chartered Accountancy exams, with characteristic braggadocio, as “a doddle”.

The dispositions which follow from these early formative experiences suggest, first, a familiarity with order; these are anything but chaotic backgrounds, regardless of the field of parental employment. Second, there is an ease with formal structures and authority. This was certainly evident among those who went to private and grammar schools but it was also true of those with service or professional backgrounds. (Census data shows that employment in the professions and ancillary roles in Edinburgh is consistently 15% higher than the UK average.Footnote 52) Such backgrounds for would-be bankers are hardly unique to Edinburgh in this period. These people are, as Raymond described himself, “rule-takers,” a useful quality to take into organizations with long-established hierarchies. However, as with the role of the Church of Scotland in their upbringing, commonality does not lessen individual impact. Having noted some of the routes into those organizations, what did they encounter when they got there?

Joining the Workplace

The workplace was a very different environment in the 1950s and 60s from even the end of the period under review, still less the workplace today. The phrase “white-collar” had long become a shorthand for office jobs generallyFootnote 53 but it still had literal meaning. White shirts were required during the week; a blue shirt was allowed in some cases at weekends when a “sports coat” might be allowed instead of a suit (Saturday morning working was normal for banks). Some of these rules were explicitly handed down but many others were neither stated nor formally enforced. Callum, one of the first graduate recruits at Bank of Scotland in 1961, remembers turning up on his first day with hair down to his shoulders. Although no one said anything, he confirmed, “it wasn’t there on the second day.” Effectively, the norm he encountered enforced itself—a clear example of Bourdieu’s “symbolic violence” at work.

Such self-regulating behavior was both commonplace and deeply ingrained. 20 years later, the late Bruce Pattullo, another of that first graduate intake at Bank of Scotland, had become its chief executive, widely recognized as Scotland’s best banker.Footnote 54 One of his more modest innovations was to commission a new bank tie. There was no requirement to wear it but Simon confirmed that almost everybody did so, down to the humblest clerk. This and Callum’s haircut are examples of what Bourdieu calls “doxa,” a set of implicit assumptions, rarely questioned or challenged, that are taken for granted in a given environment. Doxa is embedded in an individual habitus but it is followed because of the corresponding “illusio,” the anticipated rewards. This may not be a conscious calculation but, even if it had been, it is not difficult to predict the outcome. On the one hand, there was a whole industry supporting the doxa of this particular field. On the other hand, following the rules had done those who adopted them no harm and much good so far.

With the acquisition of the necessary technical competencies routinely offshored to professional bodies, firms relied heavily on this unspoken doxa. The word “osmosis” was frequently cited as the main induction method. Brian recalled, “Absorbing the atmosphere and the culture from your seniors was very, very important. We acquired the knowledge just without any effort because it was part of the culture.” Was this a secondary habitus they were acquiring? It turns out, while it may have felt like osmosis, this description was as much a reflection of the subjects’ lack of reflexivity as it was an absence of any controlling mechanisms. Craig recalled a martinet of a chief clerk who, not content with actively policing branch staff, was known to refuse loans to clients whose shoes he considered inadequately shined. It turned out that his parade-ground manner stemmed from his service as a sergeant-major in World War I. Ivan was told, not long after he started his apprenticeship at Bank of Scotland, that his political activity (he was a member of the Scottish National Party, at the time a fringe affair of little consequence) would be an impediment to his career. This clashed so directly with his own habitus—which included his commitment to Scottish independence—that the illusio the bank offered in his case was insufficient. He left to join a merchant bank in London but later, when he was senior enough to make policy, his habitus was part of what drove him to use Edinburgh’s financial reputation to persuade his new employer to move his department back to the city.

Different Strokes

The three sectors each had their own peculiarities. Banks specialized in hierarchies; as many as 14 grades at the Bank of Scotland.Footnote 55 Modernization came slowly, spreading out from the center. When Brian first joined the Royal Bank of Scotland branch in his rural hometown in north-east Scotland, he found clerks perched on high stools writing into leather-bound ledgers; “I don’t think much had changed since Dickens’ time,” was his first impression.Footnote 56

The power of this hierarchy was directly expressed from the center. Most feared were the unannounced visits from the central Inspection Department, at which every detail of the branch, from pound notes to paper clips, had to be reconciled. Within the elegant Italianate Bank of Scotland headquarters building which still dominates Edinburgh’s skyline,Footnote 57 the symbolic violence was further reified in the reservation of certain staircases for different levels of employees, a detail straight out of the private school play-book. These rituals endured; they were still in place when Sarah, the American, arrived there in 1986, long after the Inspection Department had given way to a formal internal audit process. Meanwhile the cocktail of paternalism and authoritarianism which had been revealed in the notorious Notman case in the 1930s, where a Bank of Scotland clerk had been refused permission to marry,Footnote 58 lingered on at least into the late 1950s. Simon found that while his branch manager did not actively deny his right to get married, he would not allow him to book holiday time far enough in advance to make wedding plans. Happily, as is often the case in authoritarian regimes, there were back channels. Simon’s father (manager of another branch) was able, via a friend at head office, to engineer a transfer to a more matrimonially sympathetic department.

The life houses stood slightly less on ceremony. Everyone knew that the actuaries were the Brahmins.Footnote 59 Qualification via the Faculty of Advocates was the only route to promotion at this time. But while some had different canteens for senior and junior staff, the atmosphere was generally described as “quiet” and “friendly.” It was not improper for juniors to speak to senior staff. Accuracy, rather than entrepreneurial flair, was the most highly prized quality, unconsciously becoming another means of control. Having prepared a client brief on a complex financial transaction, Nigel’s manager would not let him send it out. The financial advice was impeccable; it was the rogue comma in the client’s address which was his downfall. Correspondence in general turned out to be a repository of power. “You’ll soon find out if your face fits around here,” Roger was told on joining his asset management firm, not by his senior manager but by the woman who ran the post-room, technically his subordinate. She herself would have been subject to another aspect of the doxa, namely that women were not to be found in positions outside the clerical (as the difficulty in finding female research subjects underlined). In her acceptance of her role, she was herself indicating her subjection to the doxa and the illusio.

In asset management, the workplace atmosphere was ostensibly more relaxed. (A recent survey of a present-day firm suggests that it is very different now.Footnote 60) Robert and Graham described it as “donnish.” Jerry recalled it as “gentlemanly.” Training procedures were even less formalized. “You must be joking” was Jerry’s response when asked whether he had been offered or required to take any formal training on joining. Such nonchalance is beguiling but it exemplifies the instinct for deflection mentioned above. Jerry came from a family which for several generations owned and operated a large textile corporation. He himself had studied economics at university and had an uncle who was a stockbroker in London. In short, he was not quite the ingenu he suggested. More telling still is Bruce’s memory of his mentor who reminded him that: “as a private company we pride ourselves on our friendliness. Never make the mistake of confusing friendliness with weakness.”

Observations so far generally relate to early-stage careers. Once qualified, though, most of the sample stayed with their main employer for the bulk of their working lives, as was commonplace in the period. The prevailing mood was conservative and not just over dress codes. On his rise to the top, Callum had been dispatched to the London office for some time. On his return towards the end of the study period, he found both the city and the bank a bit of a backwater: “You had to make a bloody good case to change anything. They weren’t just going to, you know, roll over if it had worked for 200 years.” One might argue that such conservatism in financial circles was by no means unique to Edinburgh.Footnote 61 But this leads us to the wider context of the city in which the sector was nested. Edinburgh was not London, not just in finance but in everything from restaurants to entertainment, and there were plenty in the finance sector who liked it that way. As we shall see, they felt that difference was important. But they had to reckon with three potent and in many cases controlling ideologies which kept it that way. We shall examine each of them in turn, and then consider how they might be challenged.

1. The Professionals

The first of these is the surfeit of professionals spread through the city. Census data which confirms the long-standing dominance of white-collar professional jobs in the city (well over 30%) has already been noted as has the presence of professional examining and training bodies. These engines of rationalizationFootnote 62 had all been in existence for the best part of a century by the time of our focus.Footnote 63 In each case, they were in the vanguard, anywhere in the world, of such institutions but their roots were long-standing even at their inception. The citation on the royal charter of the Society of Accountants in Edinburgh, issued in 1855, referred to “the depth of accounting expertise and the esteem in which the craft has been held north of the Border for a century.”Footnote 64 The long traditions of Edinburgh’s legal fraternity reach back even further to the fifteenth century. Lawyers and accountants had been integral to the creation of the banks, as well as the life companies and the asset managers.

As Abbott identified in his seminal work on professions, this kind of development can be as much about protectionism as innovation.Footnote 65 Edinburgh was no exception. At the time these associations were being set up, there were threats to Scotland’s legal system (distinct from the rest of the UK and maintained as such under the 1707 Treaty of Union between England and Scotland) on which the professions all depended.Footnote 66 On the other hand, the claims that Edinburgh’s institutions have always made of raising and maintaining standards in the relevant professionsFootnote 67 are clearly not entirely without justification, given their continuing presence. The Institute of Chartered Accountants of Scotland (ICAS), for example, now promotes itself as “the global professional body for Chartered Accountants.”Footnote 68 Either way, it is not hard to see, in a relatively small city, how they also acted to maintain certain class divisions (see Castes, below). Professional associations maintain their exclusivity in several ways, including formal codes of conduct and sanctions in the event of breaches. In the smaller but integrated field of Edinburgh finance, it may be that formal sanctions were less important than social ones (see the Atlantic Assets affair, below). The growth in breaches of those codes since the deregulation of the Big Bang, and the apparent impotence of the available sanctions, is beyond the scope of this paper but the comparison is there to be made.

Another manifestation of this ideology is that asset managers and stockbrokers, like the long-standing firms of accountants and lawyers out of which they grew, operated as partnerships. There was no corporate veil to hide behind here; liability was personal and unlimited. Previous commentators on Edinburgh’s asset management sector have seen this as another of the pillars of its long-running success, arguing that, as a result, risk management and stock-picking were approached with due diligence.Footnote 69 Later incorporation and demutualization certainly spelled the end for some of Edinburgh’s most storied institutions. Larger, better capitalized, and above all external competitors, unconcerned with Edinburgh’s reputation and heritage, were eager to help themselves to the value lurking in the underlying assets. Only one asset manager of scale now remains in Edinburgh. The fact that it and the remaining selection of smaller boutique operations are still partnerships cannot simply be coincidental. That said, the potency of certain Edinburgh brand names cannot be dismissed either. The policies business of Standard Life was acquired by the Phoenix Group after Standard Life demutualized in 2006. Its new owner has recently announced it is to change the name of the whole group back to Standard Life from 2026.Footnote 70

There was, however, one other institution whose brand underpinned adherence to these codes from a very different direction.

2. The Kirk

The Church of Scotland, or Kirk, has dominated Edinburgh since it became the official national religion in 1560.Footnote 71 Its dominance is powered by, on the one hand, the most potent illusio of all, access to the kingdom of heaven and, on the other, the most threatening of all symbolic violence, eternal damnation. As already indicated, the one almost universal shared experience of my fieldwork cohort was that they were brought up within the moral and spiritual universe of this Presbyterian order, through family or school, and usually both. The grip that its stern doctrines exercised over Edinburgh should not be casually shrugged off. Christmas was not a public holiday until 1958. Children’s swings were still chained up in parks on Sundays well into the 1960s.

Most of this has nothing to do with faith. As it happens, the point at which Christian church attendances across Europe began their slow but apparently inexorable decline sits roughly in the middle of the period under review.Footnote 72 But by then, the Kirk was not so much a religious organization as a social one and a bourgeois one at that.Footnote 73 It exercised its authority not just from the pulpit but through its lay Elders, some of whom could be more zealous than the local minister. When Peter brought his English-born wife home in the 1980s, the local Kirk session made it clear they expected her to worship in a different church.

When this future financial elite brought the Kirk’s ideology, absorbed from family, school, and social class, with them into the workplace, they found it already in place. Pattullo, the star manager of the Bank of Scotland mentioned above, once said, while ruing the bank’s failure to take full advantage of the opportunities brought by computerization, “We still had a Presbyterian culture. We didn’t believe that we were that much ahead of any other bank.”Footnote 74 Bruce (from my research cohort, not Pattullo), who became a director of the same bank, described the “overwhelming tradition within Scottish banking of not taking risks.” Callum gave a concrete example of how Presbyterian modesty and mistrust of display could impact on specific decisions:

Bruce: “(W)e had an opportunity to do some business with one of Richard Branson’s companies. And it was a reasonably credit-worthy proposal which we had to send up to the board for approval. And when Bruce Pattullo got it, he said ‘I am not lending to Richard Branson. I don’t care if it’s a good deal or not’…. he just didn’t trust him or didn’t like him. The business was not worth getting if you didn’t think the borrower was worth dealing with.”

This is more than a useful observation of a primary habitus at work. For asset managers, life companies, most of whom were operating on the mutual model at this time,Footnote 75 and bankers alike, it was tantamount to an investment strategy.

Adrian: “[The senior partner’s] idea of responsible investing was investing with people that could be trusted. If we invested in something where there was any doubt about the moral fibre of the people running the business, he didn’t give a damn whether the outlook for the business was good or bad, you were not allowed to invest in it. We would not be allowed to invest in a Maxwell, we would not be allowed to invest in a Murdoch.”Footnote 76

More than anything, however, what emerged most clearly from their individual relationship with the Kirk was that, faith or not, it formed the moral and ethical basis of their own sense of personal integrity. From the outside, this already looks like a desirable quality in an individual or organization which is offering to look after one’s money. But inside it ran deep:

Robert: “There was a sense in Scotland, if you’re looking after other people’s money … you should behave properly … you’ve got to do it in a responsible way. And I think that’s very deeply felt … I think it was to do with the sort of moral upbringing you got in your education and probably, in years gone by, the influence of the church when it was strong.”

Once again this was not merely a question of personal primary habitus; it became a defining factor of what Edinburgh had to offer. James spoke for many when he said that while the principle of “my word is my bond” had lip service paid to it elsewhere, “in Edinburgh, we really meant it.” Members of other financial elites at the time including the City of London,Footnote 77 may take issue with this piece of local exceptionalism but it was real enough to those working in Edinburgh. The late Sir Angus Grossart, founder in 1969 of the merchant bank Noble Grossart and widely recognized as an éminence grise of the Scottish financial scene during this period, was interviewed just before the Big Bang. He too was keen to stress how different, in terms of probity and trustworthiness, Edinburgh was from the “macho atmosphere” in London:

There has been pressure to explore what is permissible. A number of people feel it is quite clever to test the boundary line. The danger is that if you keep skirting along the boundary line, you’ll sooner or later overstep it.Footnote 78

Even allowing for a certain amount of promotional bias, he must have felt this was a credible position to hold.

No sooner had those remarks been published than members of Edinburgh’s financial elite had a chance to demonstrate these credentials. The notorious Guinness affairFootnote 79 began with the takeover of Bells, a whisky company, in a transaction which Edinburgh’s financial community took in its stride. They looked to be doing the same with Guinness’ next target, the much bigger Distillers Company until, after the takeover had been agreed, the directors of Guinness began to resile from commitments they had made in their formal offer documents. These included the location of a new corporate headquarters in Scotland and the appointment of a new chairman who, at the time, was the Governor of the Bank of Scotland. Later, directors of Guinness were imprisoned for fraudulently manipulating the share price. But long before that, Guinness’ Edinburgh-based stockbrokers resigned and publicly distanced themselves from Guinness. Some of them later gave evidence for the prosecution in the criminal trial. By contrast, senior figures at Cazenove, Guinness’ London-based brokers, were heavily criticized in the subsequent Department of Trade and Industry inquiry.Footnote 80 It is worth noting that the executive brought in by Guinness to clear up the mess was another Scot, Lord Macfarlane of Bearsden. Macfarlane was not a financier but a highly respected industrialist. He was also Glaswegian to his fingertips. Did that mean he had a more pragmatic, less high-minded sensibility than his opposite numbers in Edinburgh? The two cities, barely 50 miles apart, rarely tire of comparisons with each other over everything from football to the weather. In this paper, however, the focus remains on Edinburgh in its own words. For James, who was the senior partner in the whistle-blowing Edinburgh firm, the whole saga was emblematic of Edinburgh’s integrity:

James: We guarded our integrity with our lives. People in the firm were brought up that way. And we’ve had people … you may not believe this, but we had people coming to us in London, saying, ‘I don’t like the firm I’m working for. And I want somebody with integrity, and I’m offering my services.’

Anyone who had such an offer taken up had one more institution to grapple with: the subtle caste system of the city itself.

3. The city and its castes

The concept of castes has been used to describe Edinburgh’s subtle social gradations for 150 years.Footnote 81 David McCrone, Scotland’s pre-eminent sociologist, who was born in Aberdeen but rose to distinction at the University of Edinburgh, recently tried to get at the heart of it:

We outsiders long felt that there was something intriguing and unknown about our adopted city; we know we don’t quite “belong”…We did not quite fit in, we could not be placed, as the saying goes.Footnote 82

If scholars of McCrone’s distinction note them, such perceptions must be worth considering. The experiences of our research cohort suggest similar concerns. Some were physical. For much of this period, Edinburgh was drab, even by the standards of post-war austerity, its Georgian architecture blackened by soot.Footnote 83 Licensing laws were stricter than in the rest of the UK. Luxuries were few and far between. Cultural cliches about the Scots being generally tight-fisted persisted, as did the city’s reputation for offering a cool welcome.Footnote 84 Robert had grown up in Dundee, gone to a boarding school in Perthshire, and then to university at Oxford. He still found Edinburgh tricky:

Robert: It took quite a long time to get into Edinburgh society … Edinburgh is actually a very social place once you get into it, but it’s quite hard to get into it because there are these social circles. And they intersect with each other, but if you are not in any one of them, you find it quite hard to get started, I would say.

Eventually extended family connections, in the form of a better-established uncle, came to his rescue. Raymond, who grew up in south-west Scotland, had no such connections on which to draw even though he had attended one of the city’s famous private schools. He found himself socializing with others who were not Edinburgh natives. Jeremy, who came to Edinburgh from Northern Ireland for personal reasons rather than career ones, thought that his entry into Edinburgh’s social circles was aided by not being English. A decent golf swing could be an asset but the incidence of golfers or field sports enthusiasts, both often associated with business and Scotland, was far from uniform across the sample. Another consequence of these close-knit social circles was that, once you were in them, there was nowhere to hide. When he was still quite junior, Roger expressed to a friend at a private party which, as far as he was aware, had no connection whatever to his work circle, the view that the stock market was “a bit toppy” (i.e. overvalued). If we take his memory at face value, that was all he said. Somehow, even such a generalized remark had found its way back to the senior partner by Monday morning. Robert was threatened with dismissal if he were to speak out of turn again.

Some of this can be attributed to plain, old-fashioned snobbery. When Arthur became chairman of the governors of one of those Edinburgh private schools, he was accosted—to the point of being shoved in the chest—by other parents who told him that, despite the record of public service which had seen him installed in the position, he had no right to it as he was not himself a former pupil. It spilled over into business practice as well. Trevor, the merchant banker, explained his jewellery-inflected approach to screening new employees or clients:

Trevor: We used to have what we called the gold bracelet test. If somebody came along wearing a gold bracelet … [sentence left unfinished]. That was … old fashioned values. You don’t always go with old fashioned values but you clearly wanted somebody who was honest, trustworthy, etc. …

Whatever difficulties they may have encountered socially, members of the elite could hardly avoid each other professionally, increasingly so as they neared the apex of their respective organizations. At the top of the banks since 1828 was the General Management Council, set up by Bank of Scotland managers in as close to a cartel as they could get without being one. It finally broke up in 1971 in a wave of consolidations and a series of questionable decisions on how best to engage with the postwar economy.Footnote 85 The leaders of both the banks and the insurance companies continued to meet regularly. The main purpose was to agree on what line to take in representations to government in London. There were also less formal fora. One was the frequent lunches hosted at one or other of the city’s grander hotels by companies seeking investment from the substantial funds that were under management in Edinburgh. Actual decisions were not discussed. Indeed, one of the distinctions several respondents made between Edinburgh and London was that there was no herd mentality in Edinburgh. So independent were they all from each other that it took until 1986 to establish Scottish Financial Enterprise, a formal representative body, that could speak for and on behalf of (and therefore promote) the sector.

Hunting the essence of a city, even a closely defined sub-section such as its financial elite, is a job as much for artists and poets as ethnographers and sociologists.Footnote 86 Sometimes it is easier to see a prevailing ideology when it is challenged or ignored.

4. Challenging the illlusio, changing the doxa

Challenges, both individual and institutional, to this backdrop of conservatism and stability certainly did arise. Three instances indicate how the primary habitus could prove more enduring than a secondary one absorbed in the workplace.

Jeremy’s primary habitus, from his family background described above, led him to grow weary of the lack of aspiration in the laid-back atmosphere at his asset management firm. Astute and ambitious, he eventually took control of the firm, swapping stagnation for growth and becoming chief executive himself. He still maintained that he had learned more at the racetrack as a student in Dublin than at his workplace but, again, one needs to be wary of such disingenuous flippancy.

Isaac left the family firm he had joined after gaining those easy Chartered Accountant qualifications for almost exactly opposite reasons. His primary habitus came from his father and grandfather, who had founded the business. He liked the gentlemanly way his father ran the business. A distant relative had been brought in after the war to modernize the firm’s practices, changing its doxa so much that Isaac felt thoroughly alienated. It was not the illusio of the sector that let him down; on the contrary, he stayed in it, moving to another asset management concern more attuned to the kind of private client fund management he had grown up in. It was the firm which, he felt, changed around him.

Our third example, the banker who became a minister, had his illusio shattered by the role he was required to play in specific situations, strictly speaking beyond the time frame of this study. One was managing the brutal reorganization of the bank and the thousands of redundancies involved. Later still, though still long before the whole edifice came tumbling down in 2008, the disastrous lending strategies, especially in personal mortgages, that he was required to implement drove him out of finance altogether.

The levels of symbolic violence this elite could call on or indeed were subject to appeared to be dominant, overwhelming even. The reinvention of Isaac’s family firm described above provides an institutional example of what happened when it was unleashed. In the words of an unpublished history of the firm:

It was a time of metamorphosis of the most radical kind; in 1945, it might be argued, investment trusts were all about trusteeship - in 1965, as far as [the firm] were concerned, they were all about professional investment management carried out by talented individuals for profit. It was nothing less than a revolution in the investment world.Footnote 87

Apart from driving away one of the founder’s family members, the revolution was a success, for a while at least. The firm became the poster child of Edinburgh’s financial services, lauded on both sides of the Atlantic as the hot young gunslingers of Charlotte Square.Footnote 88 The dénouement, when internal squabbles and personal ambition led to the abandonment of its partnership structure for incorporation, its eventual sale and break up, falls outside the period of study (and within the new, post Big Bang paradigm). But one earlier episode in this reinvention emphasizes how far it departed from Edinburgh norms. This was the so-called Atlantic Assets affair.Footnote 89 Essentially, a new investment trust was offered, buried in whose prospectus was a modest incentive scheme for the trust’s managers. This innovation, the brainchild of the firm’s new leader and long before the deregulation of the Big Bang, could be seen as the first faint breeze of entrepreneurialism in the city’s professions. To put it into context, this was at a time when any kind of marketing, or “touting for business,” in Arthur’s words, was simply not done. While still junior, Arthur had persuaded his firm that issuing business cards would make client interaction easier. He was later disciplined for actually handing them out. Robert returned from an analyst visit to a substantial chemical firm in England with a suggestion that his asset management firm might like to manage the chemical company’s pension fund. The senior partner refused to discuss the proposal on the grounds that his firm had not been approached in the correct way.

Such high-toned complacency explains why, for a decade after Atlantic Assets had been launched, nobody noticed the incentive scheme. When somebody did, Edinburgh’s financial elite was scandalized.Footnote 90 Such a departure from the established order could not be allowed to pass. Resignations of directors from associated trusts were demanded and conceded. One of the central trust’s directors, who had seats on the boards of both one of the city’s banks and its second biggest life assurer, was blackballed from his exclusive golf club. Commercial and social ostracism marched hand in hand. “[D]inner invitations were withdrawn and there was said to be ‘much weeping’ among the women of the [controlling] family.”Footnote 91 Other members of the elite, such as James, said they literally crossed the street to avoid the partners. Perhaps the biggest scandal, for this profession where discretion was all important, was that it was picked up by the mainstream media, splashed across the front page of the Daily Express. As Bruce, Isaac’s brother, who was not working at the firm, put it, it made for “uncomfortable breakfast reading.”

The affair also underlined the interlocking nature of the many investment trusts in the city (Atlantic Assets was partly owned by two other trusts, all three run by the same asset management company). At higher levels, each of the many Investment Trust companies required directors, company secretaries (almost always lawyers), and auditors, as did the asset management firms who managed them. Christopher thought that, because of these overlaps, if you could identify the right 50 people, you would know absolutely everything that was going on in the city. That was not enough to prevent bad blood coming between individuals or organizations at times. And yet, as the fuss and bluster died down, another more surprising and arguably more important outcome unfolded. It did not matter. Both the trust and the firm that managed it continued to prosper. On a personal level, Christopher, who made known his disapproval of the man behind the whole affair by refusing a request to chair another of his unrelated ventures, later gave the eulogy at his funeral in 1999. Could it be that the carefully nurtured city-wide doxa was more fragile than it looked? This leads us to a wider consideration of what can be drawn from these individual narratives.

Discussion

It would be an oversight, especially since Bourdieu himself quotes him approvingly, not to return to the thoughts of David Hume:

Nothing is as astonishing for those who consider human affairs with a philosophic eye than to see the ease with which the many will be governed by the few and observe the implicit submission with which men revoke their own sentiments and passions in favour of their leaders.Footnote 92

Hume was talking about the State. But he was writing just at the point in the eighteenth century where Edinburgh’s importance as a financial center was beginning to take off. As Bourdieu goes on to say, the principle applies to any established order.

[It] does not have to give orders or to exercise physical coercion in order to produce an ordered social world as long as it is capable of producing embodied cognitive structures that accord with objective structures and thus of ensuring …doxic submission to the established order.Footnote 93

Despite the recent rise in applications of habitus, it remains a challenging concept to deploy.Footnote 94 This is not because of difficulties in defining or comprehending it but because, empirically, any individual’s background contains many more variables than could be elicited in a 90-minute interview. The temptation to cherry-pick an individual detail to make a point is ever-present. In this case, as judicious an evaluation as possible of what the subjects said about themselves, the external circumstances, and their subsequent patterns of behavior has had to suffice.

What we have observed of Edinburgh’s financial elite surely fulfils Bourdieu’s model of a “structured structure predisposed to function as [a] structuring structure.”Footnote 95 It certainly empowered the field to reproduce its values and practices over long periods. In this small sample we have already reached back as far as Dickens. There is no shortage of examples of the field’s members contentedly (if unknowingly) submitting to the doxa and buying into the illusio. Does this amount to their developing a secondary habitus? Bourdieu and some of his followers tend to assume that the acquisition of secondary habitus begins in higher education. In this financial elite, however, the education that most of them enjoyed, far from obliterating their primary, bourgeois-attuned habitus, would have built on and extended it. By the time they arrived in the individual institutions that made up the city’s financial sector, they were, as rule-takers, ready to acquire a disposition that backed up its doxa with very similar versions of symbolic violence. Absorbing the required professionalism, order, duty, trusteeship, integrity, discretion, and caution of the secondary habitus would, in most cases, have required a barely noticeable adjustment. This mechanism, where training in one field prepares the individual for another, has been observed in other contexts.Footnote 96 Nevertheless, as the examples given above indicate, the secondary habitus is different enough from the primary that individuals can actively reject it.

This study in no way excludes the possibility that other social forces may also have been in play. Membership of an exclusive golf club, as we have seen, was one but there are other organizations which demand “honesty and integrity in personal, business, and public life.” The Freemasons, for example, part of whose pledge that is, have 32 branches, or Lodges, in Edinburgh as well as the movement’s Scottish headquarters, the Provincial Grand Lodge.Footnote 97 The Order has amended its secretive ways somewhat of late, but such sensitivity still surrounds membership that it remains a tricky subject to research. Other more theoretical approaches are available. Homophily, for example, like habitus, developed from commonly observable phenomena (since Bourdieu has been our guide, we might cite the elegant French expression of it: qui se ressemble, s’assemble—those who resemble one another tend to assemble). As well as identifying the positive mechanisms of this tendency, homophily also usefully points out negatives—a lack of diversity of knowledge and perspective and a limit to potential network building.Footnote 98

The habitus of the elite that maintained Edinburgh’s position as a city of financial excellence included rule-taking, familiarity with authority, quick learning, adaptability, and high levels of numeracy. In some cases, especially in the higher reaches, there was a self-confidence which presents as a mixture of airy nonchalance and lordly arrogance. It did not hurt that many of those qualities dovetailed neatly with the moral and ethical universe they had internalized from their childhood exposure to the Kirk. Several of the sample were still actively involved, as Elders, organists, local treasurers, or managers, on a pro bono basis, of the Kirk’s investment portfolio. A few directly denied any role for religion or faith in their professional lives but this may be attributable to the previously noted lack of reflexivity. Christopher, the most vehement denier, was descended from no fewer than five generations of ministers. It seems unlikely that such a heritage would leave no trace.

The Kirk is inextricably linked to Edinburgh’s financial history in other ways, ways that do not link, for example, the Church of England to the City of London (notwithstanding the role of Quakers, for example, in the foundation of several banks). It instigated a universal education system from its earliest days so that its congregations could read their bibles and encounter the word of God directly, a central principle of the Reformation. This in turn generated a steady stream of people who could write, take notes, count, run meetings, and organize the local Kirk session, skills which lie at the base of any bureaucracy.Footnote 99 Is Edinburgh’s success as a financial center entirely attributable to the influence of the Kirk? It is after all the city to which John Knox brought the Presbyterian principles of John Calvin. And it was Calvinism specifically that spurred Max Weber’s influential thoughts on Protestantism and the spirit of capitalism.Footnote 100 But to pursue that connection would require at least another paper to unravel.

There is one odd lacuna in the consequences of this habitus for the field. We expect elite groups to have power and financial elites especially so.Footnote 101 Unlike the City of London, which offers a well-trodden path to Parliament (including, at the time of writing, the current Chancellor of the Exchequer), there seems to have been little interest in the messy and often thankless business of civic government. Lists of Lords Provost of the city, for example, (roughly equivalent to a mayor) or local Members of Parliament include few names connected with the finance industry.Footnote 102 The support of Edinburgh’s financial elite for Scotland’s economy has also waxed and waned over the years.Footnote 103 Since the financial elite was largely managing other people’s money and, as we have seen, took that responsibility seriously, they were bound to seek the most advantageous investment opportunities. These were not always at home.

Conclusion

Bringing a period of oral history of Edinburgh’s financial high command within the framework of Bourdieu’s theory of habitus opens a window onto understanding the values and practices of this sequestered elite. At the very least, it offers fresh material to any consideration of Edinburgh’s long-standing but under-examined reputation as a financial center. First-hand accounts of this mid-twentieth-century period are disappearing fast; 15% of my sample have already passed on. There is certainly a degree of similarity in the primary habitus though it is by no means as uniform as one might have supposed. It was the doxa and illusio of the workplace that brought them together, albeit an outcome for which their primary habitus had prepared them. Even here, one must beware of imposing a homogeneity that never really existed. The Atlantic Assets affair had its roots in decisions taken in the 1950s when the fund was launched. Was it the first harbinger of change in Edinburgh’s way of doing things? Was the principled stand in the Guinness affair the last stand of the old school? Neither verdict is sustainable. There was nothing unprincipled, less still illegal, in the Atlantic Assets prospectus. As we have seen, once the fuss died down, business went on. The actions of the Guinness board, by contrast, were clearly improper, were illegal, and would have got short shrift almost anywhere at almost any point in the last half century. External events, on a worldwide scale, have been far more potent engines of change for financial services everywhere. This was never designed as a comparative study. What it does highlight is what Edinburgh’s financial elite thought about themselves, and part of what they thought was that they were better. Not just better than England, although London cropped up a lot, but in a kind of absolute, exceptionalist way. Perhaps they still do. Perhaps they always did. If one of the tricks of winning teams is believing in themselves, they certainly did that in this period. It must be a lot harder, post the GFC, to believe in it now

The approach taken here, itself partly the outcome of practical realities, has of necessity meant that only a relatively short span of Edinburgh’s financial elite has been under consideration, barely half a century of the city’s life as a financial center. How might one open this limited window a little wider? Deriving habitus without access to the principal becomes exponentially more speculative. Nevertheless, one generational step backward seems possible. All these interviewees had mentors, managers, and families of their own—sometimes, as we have seen, one and the same—from whom their own habitus is derived. Most of them identified one or more specific individuals who were an important influence. What they say about those figures, again with the help of contemporary sources, reveals at least flashes of a living habitus as far back as the end of World War I. Beyond that, even setting the scene for analyzing the current data has required reference to eighteenth-century events and practices. Because of its importance as a literary and philosophical hub, the city has many narratives and extensive records on which to draw, both individual and organizational. The scale of the task to address even what is known, never mind that which is yet to be discovered, is daunting.

Open access

Open access