Introduction

This research essay examines how central banks’ practices of knowledge production reflect mounting pressures to expand beyond narrow monetary mandates while maintaining legitimacy. It argues there is a mutually reinforcing relationship between central banks’ renegotiations of their remit and their ‘scientisation’. Put differently, central banks’ knowledge production on new, non-monetary topics can be construed as a strategic response to mandate uncertainty. By surveying two key domains – climate change and digital currencies – we trace how scientisation accompanies institutional change.

For decades, in most developed countries, central banks have been understood to play a crucial yet delimited role in ensuring price stability, primarily by controlling the money supply. However, they are increasingly tasked with maintaining not just monetary, but also financial (and even economic) stability. The limits of that mission are unclear, however, as the very concept of ‘stability’ has become destabilised. This is what Archer (Reference Archer2016) captures when he remarks of financial stability, that ‘we can only, for now, describe [it] in the negative – the absence of crises, or worse still the absence of “too much” instability’.

Amidst these pressures, central bankers must avoid appearing party-political, given that they are not democratically elected yet are tasked with decisions with profound social consequences. Their legitimacy does not emanate from democratic representation or their pursuit of social welfare, but from a technocratic and socio-scientific ethos that eschews the moral hazard of electoral cycles (De Haan and Eijffinger, Reference de Haan and Eijffinger2016). This type of legitimacy can become strained when their remit expands (explicitly or not), especially in a time of anti-elite sentiment. We argue that scientisation plays a part in easing this strain, along two axes: boundary-pushing/keeping and proactive/reactive.

The paper is structured as follows. We first introduce the literature on central bank scientisation and position this paper’s contribution. The next sections survey two structural challenges to central banking and how they drive scientisation: climate change and digital currencies. A final section reflects on how knowledge production surrounding central banking is crucial not only epistemically, but also strategically.

Scientisation and the limits of central banks’ mandates

The mandate of central banks, at least since the Washington consensus, is generally understood as one of driving monetary policy autonomously from the executive. Many countries have instituted rules to extricate central banks from the political process, assuming this autonomy allows this mission to be pursued ‘scientifically’. Still, since price stability can be achieved in multiple ways, central banks remain continually vulnerable to accusations of politicisation (Honohan, Reference Honohan2019; Arbogast et al., Reference Arbogast, Van Doorslaer and Vermeiren2024).

Despite this limited conception of their mandate, the 2008 global financial crisis evinced that, during critical junctures, central banks are also expected to maintain the stability of the broader financial system (Wellink, Reference Wellink2023). This raises questions about whether orthodox monetary policy can adapt to new social phenomena, and how far this project should extend, especially as political actors who challenge the technocratic authority of central banks emerge (Goodhart and Lastra, Reference Goodhart and Lastra2018). This issue is all the more pressing as we write in 2026.

The new demands faced by central banks, and how they strain central banks’ remit, are crucial drivers of what the literature has labelled ‘scientisation’. This process does not consist in merely applying the scientific method to monetary policy, but also in having the capacity to produce and deploy socio-scientific knowledge authoritatively and legitimately (Marcussen, Reference Marcussen, Dyson and Marcussen2009). Efforts at ‘scientisation’ have been complicated by what Best (Reference Best2022) calls the ‘visibility dilemma’: central banks must display sufficient expertise to project authority, yet not so much that experimental, ad hoc aspects of their work become conspicuous.

This proves even trickier in the context of non-monetary phenomena, especially in areas outside of the traditional purview of Economics and the relative consensus which it enjoys. Not even that discipline’s conception of monetary policy enjoys its previous solidity. After 2008, central banks have become supervisory institutions, employing unconventional monetary policies and indirect macroprudential regulation (Thiemann et al., Reference Thiemann, Aldegwy and Ibrocevic2018; Westermeier, Reference Westermeier2018; Thiemann et al., Reference Thiemann, Melches and Ibrocevic2021; Cassar, Reference Cassar2024). This has led to the emergence of a new, if unvoiced, consensus and de facto institutional redesign, from a predominantly ‘monetary’ regime to a broader ‘financial’ one.

The challenge of maintaining expert legitimacy while expanding into new domains reflects what Coombs and Thiemann (Reference Coombs and Thiemann2022) call the continuous redrawing of the state-economy boundary. According to this account, central banks shape the boundaries between the ‘monetary’ and the ‘political’ through knowledge production and institutional practices. This boundary-making is never neutral, simultaneously enabling and constraining state capacity, creating new forms of economic governance while depoliticising the choices involved. The very ambiguity of concepts like ‘stability’ facilitates such processes of redrawing, while licensing claims to technical neutrality, presenting new interventions as natural extensions of existing scientific expertise.

Goutsmedt and Sergi (Reference Goutsmedt and Sergi2025) consolidate discussion in this area by framing scientisation as boundary work which can operate across three dimensions: policymaking (using science for policy objectives), contributory (producing scientific knowledge), and legitimising (securing authority). The authors examine how central banks operate as boundary organisations that continuously balance their ‘dual accountability’ to scientific and political audiences through different types of intervention. Our concerns extend beyond these categories. We examine central banks under conditions of mandate uncertainty, where scientisation is not only deployed within accepted functions but mobilised to renegotiate what those functions are, beyond the monetary. This shifts our attention from scientisation as the outcome of institutional evolution to scientisation as a strategic response.

In theorising how scientisation operates within this context, we draw on Jessop’s (Reference Jessop2008) concept of strategic selectivity. For Jessop, institutions are structured in ways that privilege certain strategies, actors, and outcomes over others. This selectivity represents the sedimented outcome of past struggles, victories, and defeats crystallised into institutional forms. Actors navigating these institutions must devise strategies to work within, exploit, or transform this inherited selectivity, while new conflicts emerge atop past ones. Central banks forged their strategic selectivity through twentieth-century conflicts. Bretton Woods, the 1970s monetarist turn, and the 1990s consensus produced institutional forms characterised by narrow mandates, autonomy, and technocratic legitimacy. These forms privilege interventions which can be framed as technical, knowledge production rooted in mainstream economics, and expertise that reinforces the boundary between monetary and distributional questions.

Scientisation is a privileged strategy precisely because of this selectivity. Where central bank legitimacy rests on expert authority, knowledge production becomes a key resource for institutional positioning. This can reproduce existing boundaries, for instance by assimilating new phenomena within established frameworks. However, it can also reshape them, producing knowledge that justifies new types of intervention. Which function knowledge production fulfills depends on the pressures faced by the institution in question, the strategies of others, and how new challenges and inherited boundaries clash.

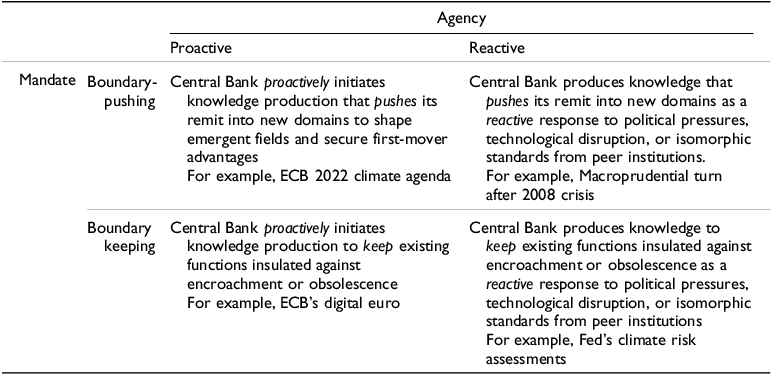

This suggests two dimensions of strategic scientisation. The first concerns mandate boundary-making: whether knowledge production works to push a central bank’s remit into new domains or to keep existing functions insulated against encroachment or obsolescence. The second relates to agency: whether a central bank proactively initiates knowledge production to shape emergent fields and secure first-mover advantages, or reactively responds to political pressures, technological disruption, or isomorphic standards from peer institutions. As is illustrated in Table 1, the combination of these two dimensions generates four potential variants of strategic scientisation, which can be understood as responses to events that challenge the current strategic orientation of the central bank in question.

Strategic scientisation.

By proposing this typology, we do not claim to have access to central banks’ ‘intentions’ – they are complex institutions without a unitary ‘consciousness’. Instead, we aim to capture regularities in the changes of central banks’ mandates, and their connection with expanded knowledge production within and outside of them.

The following sections trace how these dynamics play out across two key domains. We do not offer a comprehensive literature review, but a theoretically driven synthesis, drawing on recent case studies of central bank behaviour to illustrate how the distinctions we develop play out in practice. We draw particularly on case studies examining internal coalition-building, institutional design, and divergent strategic positioning, supplemented by bibliometric data on publication patterns by academia, central banks, and international organisations (provided in two annexes as Supplementary Material; see also Claveau and Dion, Reference Claveau and Dion2018). We argue that central bank scientisation should be understood in relation to how their mandate evolves. The acute, structural crises which central banks have experienced in recent decades (such as those in 2008 and 2020) suggest that they are increasingly exposed to a strain between what is expected of them, their attributions, and the tools and knowledge at their disposal.

Central banking and climate change scientisation

Climate change requires justifying action in a domain where central banks have no prior claim to expertise. The connection between debates on climate change and central banking is recent. Only in 2015 – with the Paris Agreement – did academic and political voices begin advocating more loudly for central banks to play a role in the matter (Dafermos, Reference Dafermos, Kappes, Rochon and Vallet2022; Thiemann et al., Reference Thiemann, Büttner and Kessler2022). Consensus over what this role should consist in has yet to emerge (Dikau and Volz, Reference Dikau and Volz2021). The timing of these developments has been shaped not only by international climate politics, but also by dynamics within central banks themselves. Jabko and Kupzok (Reference Jabko and Kupzok2024) show that the post-2008 turn to unconventional monetary policies eroded central banks’ traditional support base: conservative politicians who once championed their independence increasingly attacked quantitative easing as reckless. Climate action offered European central banks an opportunity to cultivate a broader support base.

This ‘crossover’ between climate and central banking politics helps to explain the timing of green central banking and its geographic variation: where climate was an issue of bipartisan concern (Europe), central banks could act; where it was fiercely contested (USA), they faced more constraint. The dominant position in the US Federal Reserve – which we would label boundary-keeping and reactive – is that central banks should restrict their participation to providing more and better information for decision-making and to improving risk assessment models (Campiglio et al., Reference Campiglio, Dafermos, Monnin, Ryan-Collins, Schotten and Tanaka2018). The ECB’s position – more boundary-pushing and proactive – posits that central banks should actively be involved in a low-carbon transition by helping ‘market-shape’ the greening of finance (Kedward et al., Reference Kedward, Gabor and Ryan-Collins2022).

These positions correspond with different research agendas and institutional goals. The Fed has largely confined climate engagement to risk assessment within existing financial stability functions, producing climate-related research without claiming new policy authority. Chair Jerome Powell has explicitly insisted that ‘decisions about allocating capital to different sectors’ remain beyond the Fed’s remit’ (in Jabko and Kupzok, Reference Jabko and Kupzok2024: 680). Meanwhile, the ECB, Banque de France, and De Nederlandsche Bank have produced knowledge that justifies new interventions, including climate stress tests, green tilting of asset purchases, and revised collateral frameworks that penalise carbon-intensive assets (Siderius, Reference Siderius2022).

These divergent positions coincide with a parallel debate over ‘market neutrality’ (Dikau and Volz, Reference Dikau and Volz2021; Boneva et al., Reference Boneva, Ferrucci and Mongelli2022). Here, the orthodox view is that central banks’ mandates should remain narrow, avoiding interventions which generate price distortions. Otherwise, it is argued, central banks risk ‘mission-creep’ which will result in a growing number of interventions as their remit expands. More critical commentators such as van ‘t Klooster and Fontan (Reference van ‘t Klooster and Fontan2020) counterargue that market neutrality is largely mythical: central bank interventions inevitably involve distributive choices.

These debates played out within central banks as much as they did between them. Deyris (Reference Deyris2023) documents how the ECB’s 2021 climate action plan emerged from a protracted internal struggle. A coalition formed around Christine Lagarde, Isabel Schnabel, and Frank Elderson gradually overcame resistance from the Bundesbank and other orthodox voices. The outcome was a compromise: the action plan accommodated both those seeking active promotion of low-carbon finance and those insisting on a purely risk-based rationale.

Central bank knowledge production on climate change is therefore not purely epistemic. Guided by the research and advocacy of the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) – established in 2017 to pursue the Paris Agreement’s economic goals – the models that central banks use increasingly incorporate climate concerns. Soon after the establishment of the NGFS, the BoE (2021) dedicated its Biennial Exploratory Scenario to quantifying and modelling the monetary consequences of climate change. The ECB’s 2021 economy-wide climate stress test was a similar endeavour, which over time took institutional form in the ECB 2022 Climate Agenda and the creation in 2023 of its Challenges for Monetary Policy Transmission in a Changing World (ChaMP) Research Network (Alogoskoufis et al., Reference Alogoskoufis, Dunz, Emambakhsh, Hennig, Kaijser, Kouratzoglou, Muñoz, Parisi and Salleo2021). In contrast, the Fed carried out its first Pilot Climate Scenario Analysis Exercise in 2023 and has shown less ambition regarding decarbonisation (DiLeo et al., Reference DiLeo, Rudebusch and van ‘t Klooster2023).

Siderius (Reference Siderius2022) traces how a small group of officials within De Nederlandsche Bank cultivated the climate agenda, seeking to build internal support and frame climate in terms of financial risk to claim jurisdictional authority. The NGFS – which has its roots in these efforts – was designed as a ‘coalition of the willing’ in order to bypass external resistance: after Trump’s election, US and Saudi delegates blocked climate discussions in the G20, but the NGFS allowed proactive central banks to continue setting standards independently. Its structure – with low barriers to entry but requiring commitment at the highest institutional level – spread rapidly. By 2024, over 130 central banks had joined.

Our review of the knowledge production on central banking and climate change by academia, central banks themselves, and international organisations shows that interest began around 2015 but only gathered momentum after 2019 (see Annex 1, Supplementary Material). The number of publications published by different sources is highly uneven, with the ECB being most prolific, followed by the US Federal Reserve and national European central banks. There is scant production from other sources, with the exception of the IMF and BIS which have a crucial global role in the coordination of central banking and show healthy numbers (Zapp, Reference Zapp2018).

The case of the People’s Bank of China (PBoC) reflects a different trajectory. It began implementing environment-related policies as early as 2007 (DiLeo et al., Reference DiLeo, Helleiner and Wang2025). Its 2021 Carbon Emission Reduction Facility provides preferential lending rates for low-carbon investments, a policy tool that remains largely unthinkable within Western central banking norms. This difference reflects the influence of what Epstein (Reference Epstein2013) calls ‘developmental’ central banking, characterised by wider mandates supporting closer coordination with government priorities and more aggressive policy instruments. Where Western central banks’ institutional inheritance privileges narrow mandates and market neutrality, the PBoC’s enables the active steering of credit.

Beyond these institutional features and political dynamics, the scientisation of climate change in central banking has also been driven significantly by competitive regime creation. As Helleiner et al. (Reference Helleiner, DiLeo and van ‘t Klooster2024) show, the NGFS was not merely a technocratic response to climate risks but emerged from strategic competition among central banks to shape international standards and secure first-mover advantages. This accelerated the scientisation of climate-finance links, as central banks developed modelling and stress-testing techniques in a race to become the new standard.

Notwithstanding its strategic role in expanding the remit of central banks, boundary-pushing scientisation has its risks. Engaging with climate has required European central banks to cultivate alliances with actors whose epistemic practices and political orientations differ from mainstream economics (scientists, NGOs). Deploying scenario-based climate analysis also challenges central banks’ established modes of expertise grounded in equilibrium modelling (Best et al., Reference Best, Paterson, Alami, Bailey, Bracking, Green, Helleiner, Jackson, Langley, Maechler, Morris, Quorning, Roberts, van ‘t Klooster, Watt and Wilshire2025). It is clear, meanwhile, that European central banks could only pursue climate action because mainstream conservatives had accepted decarbonisation goals; should this change, this permissiveness may erode. The Bank of England’s recent retreat from its climate commitments illustrates how quickly political conditions can shift (Best et al. Reference Best, Paterson, Alami, Bailey, Bracking, Green, Helleiner, Jackson, Langley, Maechler, Morris, Quorning, Roberts, van ‘t Klooster, Watt and Wilshire2025).

Examining climate change scientisation thus reveals how central banks’ knowledge production serves strategic as well as epistemic functions. The same external challenge has prompted markedly different responses, reflecting differences in inherited institutional forms and political contexts, and past strategic choices by key actors. The question of how central banks engage with climate is simultaneously a question of what central banks are for.

Digital currencies and central bank scientisation

In the case of digital currencies, central banks face potential encroachment on their core functions. Central banks have responded by developing new forms of expertise around blockchain technology, digital infrastructure, and payment systems. We find that most have been reactive, responding to perceived external threats. However, some respond through boundary-keeping scientisation (preserving monetary sovereignty), while others pursue boundary-pushing scientisation (enabling new forms of policy intervention).

Over the last two decades, digital payment systems have grown and diversified, even in settings hitherto characterised by informality. Since the creation of Bitcoin in 2009, digital currencies and assets have expanded rapidly, potentially contesting central banks’ monopoly over currency issuance (Pelagidis and Kostika, Reference Pelagidis and Kostika2022). Unregulated private currencies – were they truly to function as such rather than as speculative assets – could diminish the impact of monetary policy and facilitate the avoidance of regulation. Furthermore, given their volatility, they could spur financial instability (Bains et al., Reference Bains, Ismail, Melo and Sugimoto2022; Hermans et al., Reference Hermans, Ianiro, Kochanska, Törmälehto, van der Kraaij and Vendrell2022). Despite these risks, digital currencies have come to be widely traded by both retail and institutional investors.

In June 2019, Facebook announced its Libra stablecoin project. As a global platform with over two billion users proposing to issue a currency, the project seemed to pose an existential challenge to central banking. Central banks that had previously shown only modest interest in digital currencies rapidly mobilised. Within eighteen months, the Libra consortium had been restructured, regulatory pressure having effectively neutralised the threat. The episode catalysed Central Bank Digital Currencies (CBDCs) across the globe (Carapella and Flemming, Reference Carapella and Flemming2020; Zetzsche et al., Reference Zetzsche, Buckley and Arner2021; Elsayed and Nasir, Reference Elsayed and Ali Nasir2022). According to a 2023 BIS Survey (n = 86), by the end of 2023, 94% of responding central banks were engaged in CBDCs (Di Iorio et al., Reference Di Iorio, Kosse and Mattei2024).

The emergence of CBDCs has sparked questions over their potential impact on monetary and financial stability. On one hand, if they are understood as interest-earning assets and not merely a substitute for physical currency, the distinction between central and commercial banks could become moot (Chen and Siklos, Reference Chen and Siklos2022). On the other hand, CBDCs could also enhance the transmission of monetary policy by reducing intermediation. Uncertainty remains over how CBDCs could affect the future structure of financial systems because, as Malherbe and Montalban (Reference Malherbe, Montalban, Vallet, Kappes and Rochon2022: 89) argue, ‘what is at stake [is the] centralization versus decentralization of the monetary system’.

Debates over CBDCs have grappled with three key questions: architecture; environmental effects; and security and privacy (Ozili, Reference Ozili2023). Regarding the first, payments could occur as either: a) a direct claim on the central bank issuing the currency without private intermediaries; b) through private providers handling retail payment services with the claim remaining in the central bank; c) through an indirect architecture in which the claim would rest on an intermediary entity backed with an ‘actual’ CBDC (Malherbe and Montalban, Reference Malherbe, Montalban, Vallet, Kappes and Rochon2022). Second, environmental concerns have emerged given the electricity consumption that cryptocurrency mining entails, especially since this could offset central banks’ own greening efforts (Elsayed and Nasir, Reference Elsayed and Ali Nasir2022). Finally, private cryptocurrencies hinge on a promise of anonymity and decentralisation, while CBDCs are ‘issued, controlled and ledgered by central banks’ (Elsayed and Nasir, Reference Elsayed and Ali Nasir2022: 4). Pursuing this line, Westermeier (Reference Westermeier2024) argues that CBDCs should be understood as infrastructure projects that materialise specific conceptions of security and control. The ECB’s digital euro, for instance, represents an attempt to construct European monetary sovereignty in digital form.

Considering this infrastructural dimension reveals how CBDCs extend central banks’ scientisation strategies into the realm of digital governance, where design choices embed political priorities within seemingly neutral technologies. Chia and Helleiner (Reference Chia and Helleiner2024) argue that CBDCs represent an attempt to strengthen monetary sovereignty against challenges from private digital currencies, foreign CBDCs, and the displacement of cash by private payment systems. This creates a new scientisation imperative: central banks must produce technical knowledge that demonstrates the feasibility and necessity of CBDCs. Central banks’ emphasis on technical features like programmability and privacy can thus be read as an attempt to frame political questions as design problems amenable to expert resolution.

China, as in the previous case of climate change governance, has been more proactive. The PBoC began proposing its own digital currency as early as 2014 and launched pilot programmes in major cities in 2020. Unlike the digital euro, which emphasises privacy protections and explicitly rejects programmability, the digital yuan enables conditional payments, expiration dates on holdings, and targeted stimulus disbursements (Auer et al., Reference Auer, Cornelli and Frost2020). These represent boundary-pushing tools: they create capabilities with no equivalent in traditional central bank operations, extending monetary authority into the micro-management of how money is spent. The PBoC’s posture has also been more proactive in accumulating operational experience and seeking to establish technical standards before Western alternatives materialise (DiLeo et al., Reference DiLeo, Helleiner and Wang2025).

Our survey of the literature shows that knowledge production in this area emerged slowly around 2014, but grew explosively after 2019 (see Annex 2, Supplementary Material). In relation to discussions surrounding climate change, our results demonstrate an even greater dominance of central banks from the ‘Global North’. These topics are much more prevalent in academia than in central banks. Arguably, this is because digital currencies are often discussed in theoretical accounts of central banking, underlining the fact that central banks had to react to the issue’s emergence. Knowledge production from international organisations is also salient in this context. The BIS Innovation Hub, for instance, was founded in 2019 to ‘serve as a focal point for a network of central bank experts on innovation’ (BIS, 2024).

The Fed, meanwhile, remains unconvinced. Board member Michelle Bowman (Reference Bowman2023) stated that: ‘the potential uses of a US CBDC remain unclear and, at the same time, could introduce significant risks and tradeoffs’. The Fed’s stance thus represents an extreme case of boundary-keeping positioning, actively declining to enter a domain where expansion would be politically difficult. CBDCs raise surveillance concerns that unite actors from across the spectrum, while the cryptocurrency industry – a significant political constituency – views CBDCs as a threat. A digital dollar would also be visible to ordinary citizens in ways most monetary policy operations are not, making it even more politically fraught than climate-related interventions.

Overall, while climate scientisation was largely approached by European central banks in a proactive manner which constructed expertise and staked out new modes of governance, digital currency scientisation efforts have been predominantly reactive, responding to threats from private cryptocurrencies and competitive pressure from China. Most Western central banks also seek to maintain their mandate boundaries, pursuing designs that preserve monetary functions in digital form, while the PBoC has implemented a boundary-pushing CBDC with novel policy capabilities. Reactive boundary-keeping therefore carries a risk: ceding standard-setting to more proactive central banks or losing ground to private alternatives such as USD-denominated stablecoins.

Knowledge production on central banking

Our analysis shows how central banks’ efforts at scientisation operate (and vary) as a strategic response to mandate uncertainty. Central banks facing theoretically similar external pressures have sought either to push or maintain their mandate boundaries, either through proactively shaping emerging fields or reacting to external threats. This variation reflects past institutional forms, political contexts, and strategic choices. Scientisation is the mechanism through which these contextual factors are translated into knowledge claims that justify particular institutional positions; this dynamic is itself a symptom of an inherited logic of what central banking is.

According to Marcussen (Reference Marcussen, Dyson and Marcussen2009), the 1990s ‘Washington Consensus’ catalysed central banks’ pursuit of knowledge production, in efforts which sought to legitimise and ‘a-politicise’ their role. While this was happening, the relationship between central banks and academia became increasingly ‘elitist’, ‘internationalised’, and ‘hybrid’. Central banking has always been an elite occupation, but its networks were not always as global in scope or as limited in terms of the credentials it required (Lebaron and Dogan, Reference Lebaron, Dogan, Denord, Palme and Réau2020). Following Eyal (Reference Eyal and Gorski2013), we would suggest that a ‘space between fields’ emerged between organisations working across politics and academia, both at a national and international level. The ECB exemplifies this hybrid character, creating what Mudge and Vauchez (Reference Mudge and Vauchez2016) call a ‘field effect’ that shapes European economic governance.

Still, important differences remain between the knowledge production practices of central banks and academics (Fabo et al., Reference Fabo, Jančoková, Kempf and Pástor2021). This points to the significance of the differing imperatives faced by actors publishing on central banking: career progression and disciplinary advancement for academia; prospecting, surveying, and policy implementation for central banks; and international coordination and standardisation for mainstream central banks and international organisations. These different objectives partly explain why most central banks have produced knowledge on digital currencies after academia – the implications and risks of doing so are very different.

These dynamics vary further across differing political and economic contexts. The discrepancies between the Fed and ECB on climate change reflect different institutional mandates and political environments. Tellingly, knowledge production on both topics is dominated by central banks from wealthier nations, while institutions from non-hegemonic countries remain largely absent. This asymmetry reflects disparities both in research capacity and strategic imperatives: central banks whose legitimacy depends on technocratic authority seek to maintain their positions in international fora, while those facing more urgent constraints lack both the resources and incentives to compete in standard-setting. Even among major central banks, practices remain uneven: not all prioritise academic rigour equally (Dutilleul, Reference Dutilleul2025; Goutsmedt et al., Reference Goutsmedt, Sergi, Claveau and Fontan2025) and many target a blend of scholarly credentials and market experience in their recruitment (Zayim, Reference Zayim2020).

This paper began with the intuition that the consensus over central banks’ remit is silently fraying, partly due to unacknowledged mission-creep when confronted with qualitatively new crises. These phenomena are often initiated externally, compelling central banks to react by either pushing or maintaining their boundaries. This dynamic creates a dilemma: narrow mandates protect central banks’ legitimacy (especially in democratic regimes) and expanded roles invite more dissent, but greater breadth and proactivity carries first-mover advantages and equips central banks to better respond to crises.

Overall, we show that scientisation in the two areas which we scrutinise is highly uneven, dominated by Global North central banks and international organisations, with notable absences among peripheral institutions (Ibrocevic, Reference Ibrocevic2024). While the strategic selectivity inherited from twentieth-century central banking has rendered scientisation a likely response to mandate negotiation, its shape is determined by specific institutional realities. If central banks are autonomous, as is broadly believed, they do not set the terms of this autonomy.

So understood, the scientisation of some central banks – notably the ECB – both reflects and seeks to move beyond this inherited selectivity, constructing knowledge claims that justify expanded interventions. Others – like the Fed – deploy scientisation to contain new pressures within existing boundaries. In Jessop’s terms, scientisation is the privileged strategy through which central banks either renegotiate or reinforce the path-dependent logic of their inherited form. This is how the same political pressures can yield divergent strategic responses, depending on the political context, internal coalitions, and prior commitments.

A crucial driver for central banks’ scientisation, therefore, is the need to continually renegotiate their broader functioning. Even beyond central banking, this conceptualisation offers analytical purchase for studying technocratic institution renegotiating their remits through expertise. Such processes are unavoidably political, in the sense that they set the stage to answer questions about who should decide what. A push towards reaching an expert consensus becomes necessary for surveying the global challenges which emerge and for the nebulous objective of ‘stability’ to be achieved. Such consensus takes time to be formed, if it ever succeeds. Ultimately, central banks’ scientisation reveals a structural dilemma for institutions caught between democratic constraints and crisis imperatives they neither create nor welcome.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/fas.2026.10046.

Acknowledgements

This research was reviewed and approved by the Ethics Committee of Universidad Diego Portales. It received funding under the following grant: Fondecyt Regular 1231356; COES ANID/FONDAP/1523A0005. The authors would like to thank Tobias Arbogast, Frédéric Lebaron, Aris Komporozos-Athanasiou, Rodrigo Cordero, Sebastián Peredo, and Ricardo Valenzuela for their comments on earlier versions of this paper.

Open access

Open access