1. Introduction

1.1. Background and motivation

A typical reinsurance contract involves two parties, an insurer (buyer of reinsurance) and a reinsurer (seller of reinsurance), and it is uniquely identified by its indemnity function I, which specifies the indemnification amount I(x) to the insurer in case of a covered loss with size

$x{\gt}0$

. The design of optimal reinsurance contracts aims to identify the optimal indemnity function under a chosen criterion and has long been a pivotal topic in insurance economics and actuarial science (see Arrow Reference Arrow1963). The goal of this paper is to derive an optimal reinsurance contract for a utility-maximizing insurer, subject to the reinsurer’s endogenous default and background risk.

$x{\gt}0$

. The design of optimal reinsurance contracts aims to identify the optimal indemnity function under a chosen criterion and has long been a pivotal topic in insurance economics and actuarial science (see Arrow Reference Arrow1963). The goal of this paper is to derive an optimal reinsurance contract for a utility-maximizing insurer, subject to the reinsurer’s endogenous default and background risk.

The classical literature on optimal (re)insurance makes an implicit assumption that the seller of contract can always fulfill its promised contract payment, specified by I, to the buyer. However, this assumption is challenged in real-world reinsurance markets because many factors, such as catastrophic climate events or systemic risk in the financial markets, could lead to the partial (or even no) payment on covered losses from the seller (Cummins and Mahul, Reference Cummins and Mahul2003). The failure to pay the contractual indemnity I from the seller is a particular case of contract nonperformance (Doherty and Schlesinger, Reference Doherty and Schlesinger1990) and, as one would expect, has a significant impact on the buyer’s (re)insurance demand (Peter and Ying, Reference Peter and Ying2020).

There are two main contributors to the failure of reinsurance companies. The first one is a catastrophic event that results in a large realization of insured losses. In a recent example, Hurricanes Helene and Milton hit Florida within a 2-week period, together causing insured losses estimated between $30 billion and $50 billion, and put several small, Florida-based reinsurance companies under huge financial stress. The second contributor comes from the reinsurer’s background risk, broadly defined as random sources that impact the reinsurer’s reserve for settling claims. One particular source of background risk is the reinsurer’s exposure to financial risks, but it can also include, for instance, geopolitical and social risks, and even pandemic risk (International Association of Insurance Supervisors (IAIS), 2012). To understand the nonperformance of reinsurance contracts in theory, note that contractual indemnity I is often an increasing function of the insurer’s loss, and there exists a threshold

$\bar{x}$

, potentially depending on the reinsurer’s background risk, such that for all

$\bar{x}$

, potentially depending on the reinsurer’s background risk, such that for all

$x \,{\gt}\, \bar{x}$

, the contractual indemnity I(x) exceeds the reinsurer’s available reserve, resulting in an endogenous default. To summarize, both empirical and theoretical evidence motivate us to incorporate the reinsurer’s endogenous default and background risk in the study of optimal reinsurance.

$x \,{\gt}\, \bar{x}$

, the contractual indemnity I(x) exceeds the reinsurer’s available reserve, resulting in an endogenous default. To summarize, both empirical and theoretical evidence motivate us to incorporate the reinsurer’s endogenous default and background risk in the study of optimal reinsurance.

1.2. Summary and contributions of the paper

We study an optimal reinsurance problem in a one-period model for a utility-maximizing insurer who is exposed to an insurable loss X. For a reinsurance contract with indemnity function I, denote

$\mathcal{I}$

as the indemnity payment (traditionally

$\mathcal{I}$

as the indemnity payment (traditionally

$\mathcal{I}\;:\!=\;I(X)$

); the reinsurer charges a premium

$\mathcal{I}\;:\!=\;I(X)$

); the reinsurer charges a premium

$ \pi(I) = (1 + \eta)\mathbb{E}[\mathcal{I}] $

under the expected-value principle, with loading factor

$ \pi(I) = (1 + \eta)\mathbb{E}[\mathcal{I}] $

under the expected-value principle, with loading factor

$ \eta \geq 0 $

. The reinsurer’s terminal reserve is

$ \eta \geq 0 $

. The reinsurer’s terminal reserve is

$R = (S + \pi(I))^+$

, in which S is a random variable and captures the reinsurer’s background risk. With this setting, the reinsurer’s initial reserve r at time 0 evolves stochastically to S at time 1; as such,

$R = (S + \pi(I))^+$

, in which S is a random variable and captures the reinsurer’s background risk. With this setting, the reinsurer’s initial reserve r at time 0 evolves stochastically to S at time 1; as such,

$ S - r $

is the background risk, but mathematically, it is equivalent to directly call S the reinsurer’s background risk. As argued in Section 1.1, we consider the reinsurer’s endogenous default and define it as an event whenever the indemnity payment

$ S - r $

is the background risk, but mathematically, it is equivalent to directly call S the reinsurer’s background risk. As argued in Section 1.1, we consider the reinsurer’s endogenous default and define it as an event whenever the indemnity payment

$\mathcal{I}$

exceeds the reinsurer’s reserve R. As such, for a contract I, the indemnity payment received by the insurer changes from “contractual amount”

$\mathcal{I}$

exceeds the reinsurer’s reserve R. As such, for a contract I, the indemnity payment received by the insurer changes from “contractual amount”

$\mathcal{I}$

to “actual amount”

$\mathcal{I}$

to “actual amount”

$\mathbb{I} = \mathcal{I} \cdot \mathbf{1}_{\{ \mathcal{I} \leq R \}} + \tau R \cdot \mathbf{1}_{\{ \mathcal{I} \,{\gt}\, R \}}$

, in which

$\mathbb{I} = \mathcal{I} \cdot \mathbf{1}_{\{ \mathcal{I} \leq R \}} + \tau R \cdot \mathbf{1}_{\{ \mathcal{I} \,{\gt}\, R \}}$

, in which

$\tau \in [0,1]$

is the recovery rate in case of an endogenous default. The insurer is aware that its reinsurance contract may be nonperforming and seeks an optimal contract

$\tau \in [0,1]$

is the recovery rate in case of an endogenous default. The insurer is aware that its reinsurance contract may be nonperforming and seeks an optimal contract

$I^*$

to maximize the expected utility of its terminal wealth.

$I^*$

to maximize the expected utility of its terminal wealth.

In Section 3, the insurer is allowed to choose contracts in the form of

$I \;:\!=\; I (x, s)$

; that is, the indemnity I can be a function of both the insurer’s loss size x and the reinsurer’s background risk (random reserve) level s. We follow a two-step approach to obtain the insurer’s globally optimal contract

$I \;:\!=\; I (x, s)$

; that is, the indemnity I can be a function of both the insurer’s loss size x and the reinsurer’s background risk (random reserve) level s. We follow a two-step approach to obtain the insurer’s globally optimal contract

$I^*$

. In the first step, we fix the contract premium at a given level a and obtain the locally optimal contract

$I^*$

. In the first step, we fix the contract premium at a given level a and obtain the locally optimal contract

$I_a^*$

(see Theorem 3.3). In the second step, we optimize over all feasible a and identify the optimal premium level

$I_a^*$

(see Theorem 3.3). In the second step, we optimize over all feasible a and identify the optimal premium level

$a^*$

. The globally optimal contract is then given by

$a^*$

. The globally optimal contract is then given by

$I^* = I^*_{a^*}$

(see Theorem 3.5). We obtain

$I^* = I^*_{a^*}$

(see Theorem 3.5). We obtain

$I^*$

in a semiclosed form and show that it is a single deductible reinsurance with a policy limit; in addition, the reinsurer will never default under contract

$I^*$

in a semiclosed form and show that it is a single deductible reinsurance with a policy limit; in addition, the reinsurer will never default under contract

$I^*$

. These results are obtained over the largest possible set of admissible indemnities (see Remark 3.1) and require only mild conditions on X and S (Assumption 1); to the best of our knowledge, they are new to the optimal reinsurance literature. We also derive analytical results on the comparative statics of the optimal contract, including its deductible, policy limit, and premium (see Proposition 3.7), while the existing literature obtains limited results, mostly relying on numerical analysis. In particular, we show that the optimal deductible decreases with respect to the reinsurer’s reserve and the insurer’s risk aversion but increases with respect to the insurer’s initial wealth.

$I^*$

. These results are obtained over the largest possible set of admissible indemnities (see Remark 3.1) and require only mild conditions on X and S (Assumption 1); to the best of our knowledge, they are new to the optimal reinsurance literature. We also derive analytical results on the comparative statics of the optimal contract, including its deductible, policy limit, and premium (see Proposition 3.7), while the existing literature obtains limited results, mostly relying on numerical analysis. In particular, we show that the optimal deductible decreases with respect to the reinsurer’s reserve and the insurer’s risk aversion but increases with respect to the insurer’s initial wealth.

In Section 4, the insurer can only choose contracts in the form of

$I \;:\!=\; I(x)$

, depending only on the loss size x, which form a subclass of the contracts considered in Section 3. However, the resulting optimal reinsurance problem is challenging to solve, and the two-approach approach in Section 3 cannot be applied here. To our awareness, such an optimal reinsurance problem has not been studied previously in the literature. Imposing the incentive compatible (IC) condition on I and assuming that the discrete S is independent of X, we characterize the (locally) optimal contract

$I \;:\!=\; I(x)$

, depending only on the loss size x, which form a subclass of the contracts considered in Section 3. However, the resulting optimal reinsurance problem is challenging to solve, and the two-approach approach in Section 3 cannot be applied here. To our awareness, such an optimal reinsurance problem has not been studied previously in the literature. Imposing the incentive compatible (IC) condition on I and assuming that the discrete S is independent of X, we characterize the (locally) optimal contract

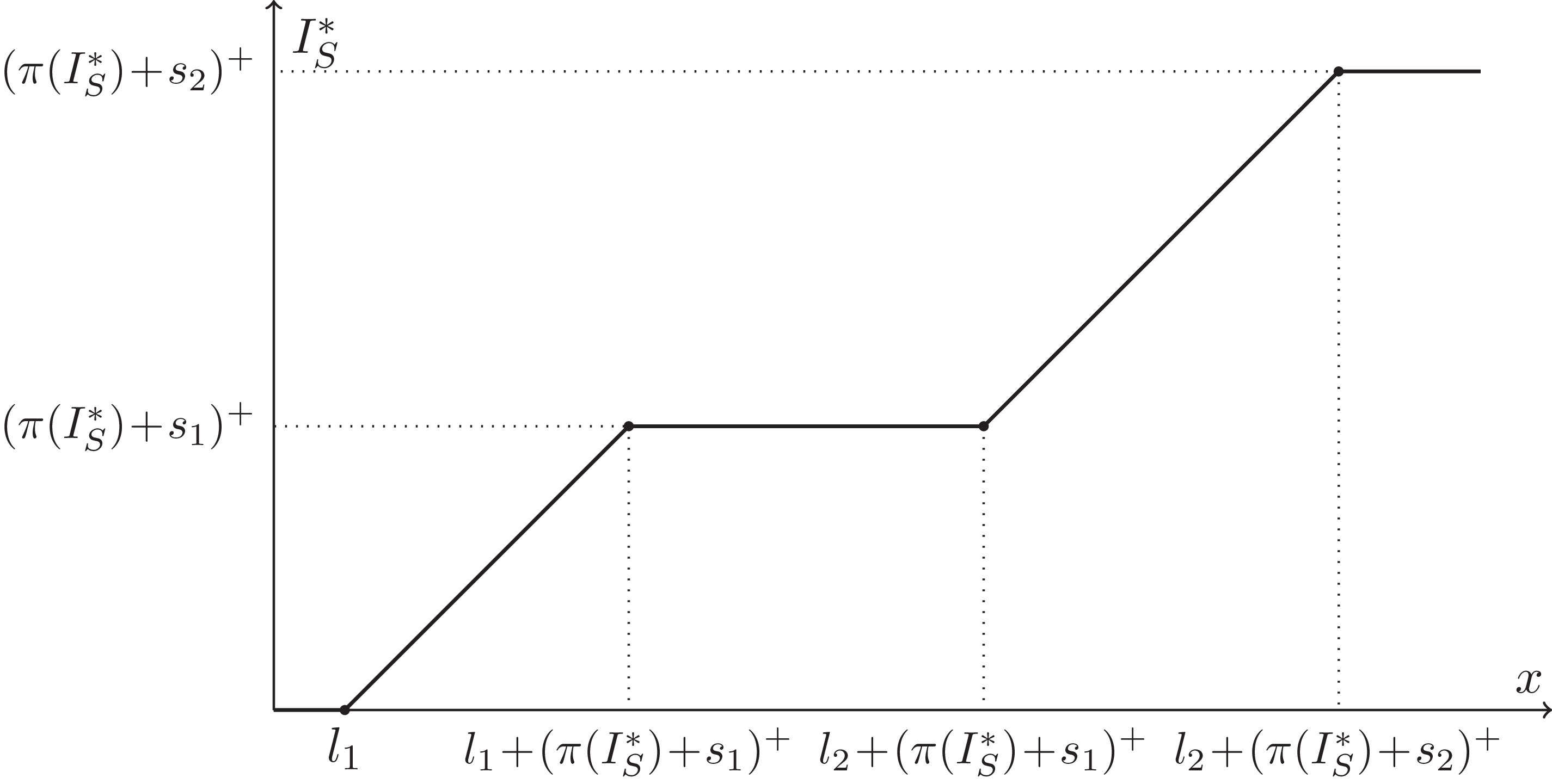

$I_S^* \;:\!=\; I_S^*(x)$

in a parametric form (see Theorem 4.3). We show that

$I_S^* \;:\!=\; I_S^*(x)$

in a parametric form (see Theorem 4.3). We show that

$I_S^*$

is a multi-layer reinsurance contract, and each layer involves a deductible and a policy limit, both depending on a free parameter

$I_S^*$

is a multi-layer reinsurance contract, and each layer involves a deductible and a policy limit, both depending on a free parameter

$l_i$

. With additional conditions (e.g.,

$l_i$

. With additional conditions (e.g.,

$I_S^*$

has two layers), we can further obtain the optimal parameters,

$I_S^*$

has two layers), we can further obtain the optimal parameters,

$l_1^*$

and

$l_1^*$

and

$l_2^*$

, and fully identify the optimal contract

$l_2^*$

, and fully identify the optimal contract

$I_S^*$

(see Proposition 4.4). We remark that endogenous default may occur under

$I_S^*$

(see Proposition 4.4). We remark that endogenous default may occur under

$I_S^*$

in Section 4, but

$I_S^*$

in Section 4, but

$I^*$

obtained in Section 3 is a default-free contract. This striking difference highlights the impact of the reinsurer’s background risk and the choice of contracts on decision-making.

$I^*$

obtained in Section 3 is a default-free contract. This striking difference highlights the impact of the reinsurer’s background risk and the choice of contracts on decision-making.

1.3. Related literature

The seminal work of Arrow (Reference Arrow1963) considers a one-period insurance model without the counterparty default and background risk, and it shows that the optimal contract is a deductible insurance for a utility-maximizing insured under the expected-value premium principle. A significant body of the literature on optimal (re)insurance aims to extend Arrow’s model by exploring different optimization criteria or premium principles (see, e.g., Bernard et al., Reference Bernard, He, Yan and Zhou2015 for rank-dependent utility (RDU) and Birghila et al., Reference Birghila, Boonen and Ghossoub2023 for maximin expected utility; Asimit et al., Reference Asimit, Badescu and Cheung2013 for distortion premium principles); we refer to Gollier (Reference Gollier and Dionne2013) and Cai and Chi (Reference Cai and Chi2020) for an overview of the research on optimal (re)insurance. This paper, on the other hand, incorporates the counterparty default risk and background risk into Arrow’s model and studies the insurer’s optimal reinsurance problem accordingly. As such, we focus on reviewing related works that consider default or background risk.

In terms of modeling default risk, there are two main approaches. The first approach models the seller’s default as an exogenous event, often by a binary random variable independent of the contract. Doherty and Schlesinger (Reference Doherty and Schlesinger1990) follow this approach in their model and are among the earliest to study insurance demand under default risk (restricting to proportional contracts). In addition, they assume that the default probability is known to both parties, and when default occurs, no indemnity payment is made to the buyer (i.e., the recovery rate is

$\tau = 0$

). As they write, “A nonzero probability of default renders most of the standard insurance results invalid” (p. 244), and their findings demonstrate the profound impact of default risk on insurance demand. Subsequent studies extend Doherty and Schlesinger (Reference Doherty and Schlesinger1990) by considering heterogeneous beliefs (Cummins and Mahul, Reference Cummins and Mahul2003), ambiguity preferences (Peter and Ying, Reference Peter and Ying2020), hedging strategies (Reichel et al. Reference Reichel, Schmeiser and Schreiber2022; Chi et al., Reference Chi, Hu and Huang2023), and distortion risk measures (Yong et al., Reference Yong, Cheung and Zhang2024), among many others.

$\tau = 0$

). As they write, “A nonzero probability of default renders most of the standard insurance results invalid” (p. 244), and their findings demonstrate the profound impact of default risk on insurance demand. Subsequent studies extend Doherty and Schlesinger (Reference Doherty and Schlesinger1990) by considering heterogeneous beliefs (Cummins and Mahul, Reference Cummins and Mahul2003), ambiguity preferences (Peter and Ying, Reference Peter and Ying2020), hedging strategies (Reichel et al. Reference Reichel, Schmeiser and Schreiber2022; Chi et al., Reference Chi, Hu and Huang2023), and distortion risk measures (Yong et al., Reference Yong, Cheung and Zhang2024), among many others.

The second approach, adopted by this paper, models the seller’s default as an endogenous event which occurs when the seller’s reserve is less than the contractual indemnity. This approach is arguably more realistic than the first one but leads to a more challenging optimal (re)insurance problem, which may explain why there is only limited study under endogenous default. In an early attempt, Biffis and Millossovich (Reference Biffis and Millossovich2012) study a Pareto optimal insurance problem under endogenous default (and background risk) for a risk-averse insured and a risk-neutral insurer. They derive several properties of the optimal insurance, should it exist, but fail to find an analytical solution to the optimal contract. Asimit et al. (Reference Asimit, Badescu and Cheung2013) consider a more concrete setup (but without background risk) in which the reinsurer’s reserve is based on the Value-at-Risk (VaR) rule, and reinsurance contracts are priced by the distortion premium principle. When the insurer aims to minimize its risk (measured by either VaR or a distortion risk measure), they obtain the optimal contract in (semi)closed form. Cai et al. (Reference Cai, Lemieux and Liu2014) conduct a similar study as Asimit et al. (Reference Asimit, Badescu and Cheung2013) but assume the expected-value premium principle and no bankruptcy costs (

$\tau = 1$

); they find an analytical solution for the optimal contract that maximizes the insurer’s expected utility or minimizes the VaR. Note that neither Asimit et al. (Reference Asimit, Badescu and Cheung2013) nor Cai et al. (Reference Cai, Lemieux and Liu2014) consider the reinsurer’s background risk. More recently, Chen et al. (Reference Chen, Cheung and Zhang2024) seek a Bowley solution to a reinsurance game in the presence of endogenous default risk.

$\tau = 1$

); they find an analytical solution for the optimal contract that maximizes the insurer’s expected utility or minimizes the VaR. Note that neither Asimit et al. (Reference Asimit, Badescu and Cheung2013) nor Cai et al. (Reference Cai, Lemieux and Liu2014) consider the reinsurer’s background risk. More recently, Chen et al. (Reference Chen, Cheung and Zhang2024) seek a Bowley solution to a reinsurance game in the presence of endogenous default risk.

Next, we discuss existing research on optimal (re)insurance problems that considers background risk. The surplus of a company (e.g., the seller of (re)insurance policies) or the wealth of an individual insured is exposed to various risks. Here, we broadly define background risk as random risks that impact the seller’s or buyer’s surplus, and they are either uninsurable or not insured. Recall that the initial wealth of the (re)insurance buyer is a constant in the classical models (see Borch, Reference Borch1962 and Arrow, Reference Arrow1963); much of the effort is devoted to incorporating the buyer’s (referring to the insurer in a reinsurance context or the insured in an insurance setting) background risk into the model. Doherty and Schlesinger (Reference Doherty and Schlesinger1983) study optimal deductible insurance when the insured’s initial wealth is random (due to background risk). Mayers and Smith (Reference Mayers and Smith1983) consider a particular case in which the insured’s background risk comes from the financial market, and they study the optimal demand for proportional insurance and financial assets. Chi and Wei (Reference Chi and Wei2020) and Chen (Reference Chen2024) explore the optimal insurance problem under a general dependence structure between the insured’s insurable and background risks. However, the seller’s (corresponding to the reinsurer of reinsurance or the insurer of insurance contracts) background risk is at least as important as the buyer’s background risk, if not more so; however, related research is quite limited. The model in Biffis and Millossovich (Reference Biffis and Millossovich2012) is a rare example and considers both the buyer’s and seller’s background risk; but they do not obtain an explicit optimal contract. Filipović et al. (Reference Filipović, Kremslehner and Muermann2015) consider the seller’s background risk and allow it to invest in a risky asset, while Boonen (Reference Boonen2019) extends their work to an equilibrium model with multiple insureds (buyers).

2. Model

We consider a one-period model and study the optimal reinsurance problem for an insurer. We fix a complete probability space

$(\Omega, \mathcal{F}, \mathbb{P})$

and denote by

$(\Omega, \mathcal{F}, \mathbb{P})$

and denote by

$\mathbb{E}[\!\cdot\!]$

the expectation taken under

$\mathbb{E}[\!\cdot\!]$

the expectation taken under

$\mathbb{P}$

. All (in)equalities involving random variables should be understood in the

$\mathbb{P}$

. All (in)equalities involving random variables should be understood in the

$\mathbb{P}$

almost surely sense. The insurer’s aggregate loss (or a portfolio of risks) is modeled by a nonnegative

$\mathbb{P}$

almost surely sense. The insurer’s aggregate loss (or a portfolio of risks) is modeled by a nonnegative

$\mathcal{F}$

-measurable random variable X, and we assume that X is bounded from above,

$\mathcal{F}$

-measurable random variable X, and we assume that X is bounded from above,

$0\,{\lt}\, M\;:\!=\;\operatorname{ess \, sup}\,X\lt\infty$

. This assumption is common in the literature (see, e.g., Chi et al., Reference Chi, Hu and Huang2023), and it is rather mild, because M can be arbitrarily large. The main results can be readily extended to the case of

$0\,{\lt}\, M\;:\!=\;\operatorname{ess \, sup}\,X\lt\infty$

. This assumption is common in the literature (see, e.g., Chi et al., Reference Chi, Hu and Huang2023), and it is rather mild, because M can be arbitrarily large. The main results can be readily extended to the case of

$M = \infty$

under certain integrability conditions (see Online Companion for full details on this extension), while

$M = \infty$

under certain integrability conditions (see Online Companion for full details on this extension), while

$M=0$

trivializes the problem. To mitigate the risk exposure, the insurer purchases reinsurance from the reinsurance market, and we denote the indemnity function of a reinsurance contract by I and the corresponding stochastic indemnity payment by

$M=0$

trivializes the problem. To mitigate the risk exposure, the insurer purchases reinsurance from the reinsurance market, and we denote the indemnity function of a reinsurance contract by I and the corresponding stochastic indemnity payment by

$\mathcal{I}$

(traditionally

$\mathcal{I}$

(traditionally

$\mathcal{I}\;:\!=\;I(X)$

). Given the one-to-one relation between a reinsurance contract and its indemnity function I, we often call I a contract. We assume that the reinsurer applies the expected-value premium principle to calculate the contract premium by

$\mathcal{I}\;:\!=\;I(X)$

). Given the one-to-one relation between a reinsurance contract and its indemnity function I, we often call I a contract. We assume that the reinsurer applies the expected-value premium principle to calculate the contract premium by

\begin{align} \pi(I) = (1 + \eta) \, \mathbb{E}[ I(X) ],\end{align}

\begin{align} \pi(I) = (1 + \eta) \, \mathbb{E}[ I(X) ],\end{align}

in which

$\eta \ge 0$

is the premium loading factor. Using the actual indemnity

$\eta \ge 0$

is the premium loading factor. Using the actual indemnity

$\mathbb{I}$

to determine the premium leads to a “loop” issue, because the actual indemnity and premium are intertwined through the reinsurer’s random reserve. This explains the standard form of the premium in (2.1); see Cai et al. (Reference Cai, Lemieux and Liu2014) for the same premium principle when the seller’s default is present. Because the reinsurer may default on indemnity payment, the loading factor

$\mathbb{I}$

to determine the premium leads to a “loop” issue, because the actual indemnity and premium are intertwined through the reinsurer’s random reserve. This explains the standard form of the premium in (2.1); see Cai et al. (Reference Cai, Lemieux and Liu2014) for the same premium principle when the seller’s default is present. Because the reinsurer may default on indemnity payment, the loading factor

$\eta$

should reflect this default risk.Footnote

1

$\eta$

should reflect this default risk.Footnote

1

Once a contract I is chosen by the insurer, the reinsurer’s terminal available reserve, R, for settling claims is given by

\begin{align} R = (S+\pi(I))^+,\end{align}

\begin{align} R = (S+\pi(I))^+,\end{align}

in which S is an

$\mathcal{F}$

-measurable random variable capturing the reinsurer’s background risk, and

$\mathcal{F}$

-measurable random variable capturing the reinsurer’s background risk, and

$y^+ \;:\!=\; \max\{0, y\}$

for all

$y^+ \;:\!=\; \max\{0, y\}$

for all

$y \in \mathbb{R}$

. The rationale is that the reinsurer sets aside an initial reserve of amount r at time 0, which consists of both “cash” and “risky assets,” and thus its value at time 1, S, is random. In that regard, one can also call S the reinsurer’s random reserve (excluding premium), and the difference

$y \in \mathbb{R}$

. The rationale is that the reinsurer sets aside an initial reserve of amount r at time 0, which consists of both “cash” and “risky assets,” and thus its value at time 1, S, is random. In that regard, one can also call S the reinsurer’s random reserve (excluding premium), and the difference

$S - r$

models the reinsurer’s additive background risk. But for notational simplicity, we call S the reinsurer’s background risk in the sequel.

$S - r$

models the reinsurer’s additive background risk. But for notational simplicity, we call S the reinsurer’s background risk in the sequel.

An endogenous default from the reinsurer occurs if (and only if)

$R\,{\lt}\, \mathcal{I}$

, namely when the reinsurer’s terminal reserve falls short of the contractual indemnity. We assume that in case of an endogenous default, the insurer receives a fraction,

$R\,{\lt}\, \mathcal{I}$

, namely when the reinsurer’s terminal reserve falls short of the contractual indemnity. We assume that in case of an endogenous default, the insurer receives a fraction,

$\tau \in [0,1]$

, of the reinsurer’s available reserve.Footnote

2

Note that our setup allows for large negative shocks of S that result in a negative value of

$\tau \in [0,1]$

, of the reinsurer’s available reserve.Footnote

2

Note that our setup allows for large negative shocks of S that result in a negative value of

$S + \pi(I)$

, which is why we take the positive part in (2.2). Mathematically, we introduce a binary variable,

$S + \pi(I)$

, which is why we take the positive part in (2.2). Mathematically, we introduce a binary variable,

$D\;:\!=\; D(I)$

, to track the reinsurer’s solvency status by

$D\;:\!=\; D(I)$

, to track the reinsurer’s solvency status by

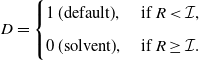

\begin{align} D = \begin{cases} 1 \text{ (default)}, & \text{ if } R \,{\lt}\, \mathcal{I}, \\[5pt] 0 \text{ (solvent)}, & \text{ if } R \ge \mathcal{I}. \end{cases}\end{align}

\begin{align} D = \begin{cases} 1 \text{ (default)}, & \text{ if } R \,{\lt}\, \mathcal{I}, \\[5pt] 0 \text{ (solvent)}, & \text{ if } R \ge \mathcal{I}. \end{cases}\end{align}

D depends on the insurer’s loss X and contract I, and also the reinsurer’s background risk S.

Because reinsurance contracts may be nonperforming due to the reinsurer’s endogenous default, the actual indemnity payment,

$\mathbb{I}$

, that the insurer receives from a contract I is given by

$\mathbb{I}$

, that the insurer receives from a contract I is given by

\begin{align} \mathbb{I}(I) = \mathcal{I} \cdot \mathbf{1}_{\{ D = 0 \} } + \tau R \cdot \mathbf{1}_{ \{ D = 1 \}},\end{align}

\begin{align} \mathbb{I}(I) = \mathcal{I} \cdot \mathbf{1}_{\{ D = 0 \} } + \tau R \cdot \mathbf{1}_{ \{ D = 1 \}},\end{align}

in which

$\mathbf{1}$

denotes an indicator function, and R and D are defined by (2.2) and (2.3), respectively. Therefore, for a chosen contract I, the insurer’s terminal wealth, W, equals

$\mathbf{1}$

denotes an indicator function, and R and D are defined by (2.2) and (2.3), respectively. Therefore, for a chosen contract I, the insurer’s terminal wealth, W, equals

\begin{align} W(I) = w - X - \pi(I) + \mathbb{I}(I),\end{align}

\begin{align} W(I) = w - X - \pi(I) + \mathbb{I}(I),\end{align}

in which w is the insurer’s initial wealth,

$\pi(I)$

is given by (2.1), and

$\pi(I)$

is given by (2.1), and

$\mathbb{I}$

is the actual indemnity defined in (2.4). Following the classical literature on (re)insurance economics (e.g., Arrow, Reference Arrow1963 and Mossin, Reference Mossin1968), we assume that the insurer’s preferences are modeled by the expected utility theory with a twice differentiable utility function u that is strictly increasing and strictly concave (i.e.,

$\mathbb{I}$

is the actual indemnity defined in (2.4). Following the classical literature on (re)insurance economics (e.g., Arrow, Reference Arrow1963 and Mossin, Reference Mossin1968), we assume that the insurer’s preferences are modeled by the expected utility theory with a twice differentiable utility function u that is strictly increasing and strictly concave (i.e.,

$u'{\gt}0$

and

$u'{\gt}0$

and

$u''\lt0$

). We formulate the main problem of the paper as follows.

$u''\lt0$

). We formulate the main problem of the paper as follows.

Problem 1. The insurer seeks an optimal reinsurance contract

$I^* $

to maximize the expected utility of its terminal wealth under the reinsurer’s endogenous default and background risk, that is,

$I^* $

to maximize the expected utility of its terminal wealth under the reinsurer’s endogenous default and background risk, that is,

\begin{align*}I^* = \mathop{\operatorname{argsup}}_{I \in \widetilde{\mathcal{A}}}\, \mathbb{E}[u(W(I))],\end{align*}

\begin{align*}I^* = \mathop{\operatorname{argsup}}_{I \in \widetilde{\mathcal{A}}}\, \mathbb{E}[u(W(I))],\end{align*}

in which

$\widetilde{\mathcal{A}}$

is the admissible set to be specified later, and W(I) is given by (2.5).

$\widetilde{\mathcal{A}}$

is the admissible set to be specified later, and W(I) is given by (2.5).

Remark 2.1. In Problem 1, the premium of a reinsurance contract

$\pi(I)$

is computed by the expected-value premium principle in (2.1). As is standard in the study of optimal (re)insurance, the form of the optimal contract often depends on the chosen premium principle. For example, Chen and Shen (Reference Chen and Shen2019) show that the optimal contract (in their setting) is of deductible form under the expected-value premium principle, but it is of proportional form under the variance premium principle. Among the results obtained in this paper, Propositions 2.1 and 3.2 remain valid under general premium principles, but other results likely are limited to the expected-value premium principle. It is an interesting direction to revisit Problem 1 under different premium principles.

$\pi(I)$

is computed by the expected-value premium principle in (2.1). As is standard in the study of optimal (re)insurance, the form of the optimal contract often depends on the chosen premium principle. For example, Chen and Shen (Reference Chen and Shen2019) show that the optimal contract (in their setting) is of deductible form under the expected-value premium principle, but it is of proportional form under the variance premium principle. Among the results obtained in this paper, Propositions 2.1 and 3.2 remain valid under general premium principles, but other results likely are limited to the expected-value premium principle. It is an interesting direction to revisit Problem 1 under different premium principles.

By definition, the reinsurer defaults if

$(S + \pi(I) )^+\,{\lt}\, \mathcal{I}$

, suggesting that the reinsurer’s background risk S plays a key role in its solvency. Because

$(S + \pi(I) )^+\,{\lt}\, \mathcal{I}$

, suggesting that the reinsurer’s background risk S plays a key role in its solvency. Because

$I\ge 0$

, we first consider an extreme scenario of

$I\ge 0$

, we first consider an extreme scenario of

$S\le 0$

and show that the optimal strategy is to not purchase any reinsurance.

$S\le 0$

and show that the optimal strategy is to not purchase any reinsurance.

Proposition 2.1. If

$S \le 0$

almost surely (i.e.,

$S \le 0$

almost surely (i.e.,

$\mathbb{P}(S \le 0) = 1$

), then the optimal strategy to Problem 1 is no reinsurance with

$\mathbb{P}(S \le 0) = 1$

), then the optimal strategy to Problem 1 is no reinsurance with

$I^* \equiv 0$

.

$I^* \equiv 0$

.

Proof. For any nonnegative indemnity function

$I\ge 0$

(thus,

$I\ge 0$

(thus,

$\pi(I) \ge 0$

), we obtain

$\pi(I) \ge 0$

), we obtain

\begin{align*} W(I)&=w - X - \pi(I) + \mathcal{I} \cdot \mathbf{1}_{\{\mathcal{I} \le (S+\pi(I))^+\}} + \tau (S+\pi(I))^+ \cdot \mathbf{1}_{\{\mathcal{I} {\gt}(S+\pi(I))^+\}} \\[5pt] &\le w - X - \pi(I) + (S+\pi(I))^+ \\[5pt] &\le w - X - \pi(I) + \pi(I)=w-X=W(0). \end{align*}

\begin{align*} W(I)&=w - X - \pi(I) + \mathcal{I} \cdot \mathbf{1}_{\{\mathcal{I} \le (S+\pi(I))^+\}} + \tau (S+\pi(I))^+ \cdot \mathbf{1}_{\{\mathcal{I} {\gt}(S+\pi(I))^+\}} \\[5pt] &\le w - X - \pi(I) + (S+\pi(I))^+ \\[5pt] &\le w - X - \pi(I) + \pi(I)=w-X=W(0). \end{align*}

Because

$u' {\gt}0$

,

$u' {\gt}0$

,

$\mathbb{E}[u(W(I))] \le \mathbb{E}[u(W(0))]$

, and the result follows.

$\mathbb{E}[u(W(I))] \le \mathbb{E}[u(W(0))]$

, and the result follows.

The result in Proposition 2.1 already showcases the important impact of counterparty default on decision-making. We know from, for instance, Arrow (Reference Arrow1963) that, if the reinsurer’s default risk is ignored, the optimal contract is a deductible reinsurance. However, as Proposition 2.1 shows, when the insurer is aware of the counterparty default risk, and the reinsurer’s reserve is nonpositive, the optimal decision is to not purchase any reinsurance but to fully rely on self-insurance. Because the case of

$S \le 0$

is solved by Proposition 2.1, and it is likely unrealistic in practice, we study Problem 1 under the standing assumption that

$S \le 0$

is solved by Proposition 2.1, and it is likely unrealistic in practice, we study Problem 1 under the standing assumption that

$\mathbb{P}(S \,{\gt}\, 0)\, {\gt}\, 0$

in the rest of the paper.

$\mathbb{P}(S \,{\gt}\, 0)\, {\gt}\, 0$

in the rest of the paper.

Because there are two random sources, X and S, in the model, we consider two types of indemnity functions in the analysis:

-

1. Loss- and background-risk-dependent indemnities

$I \;:\!=\; I(x, s)$

(denoting

$\mathcal{I} \;:\!=\; I(X, S)$

).

$I \;:\!=\; I(x, s)$

(denoting

$\mathcal{I} \;:\!=\; I(X, S)$

). -

2. Loss-dependent indemnities

$I\;:\!=\;I(x)$

(denoting

$\mathcal{I}\;:\!=\;I(X)$

).

Reinsurance contracts with indemnities in the form of I(x, s) are examples of the so-called randomized contracts in the reinsurance literature. Similar randomized (re)insurance contracts are considered in Albrecher and Cani (Reference Albrecher and Cani2019) with an independent Bernoulli random variable and in Asimit et al. (Reference Asimit, Boonen, Chi and Chong2021) within multiple indemnity environments. Moreover, we also consider the second type of contracts with indemnity I(x) depending only on the insurer’s own loss size x, but independent of the reinsurer’s background risk level s. Note that the second type is the more conventional contract form and constitutes a subclass of the first type I(x, s), and the two types coincide when there is no background risk (S reduces to a constant). In either type of contracts, the reinsurer’s endogenous default is induced by large losses from the insurer or negative shocks from its background risk.

We discuss the actual indemnity payments of these two contract types as follows.

-

1.

$ \mathcal{I} = I(X, S) $

: The contractual payment

$ \mathcal{I} $

depends on the realized values of both X and S. Consequently, the actual indemnity payment

$ \mathbb{I} $

in (2.4) is contingent on S even when no default occurs, necessitating regulatory disclosure of the reinsurer’s reserve S at time 1 (e.g., audited financial statements or quarterly reports) to ensure execution of the contract. -

2.

$ \mathcal{I} = I(X) $

: The contractual payment

$ \mathcal{I} $

depends only on X, and thus the actual payment

$ \mathbb{I} $

in (2.4) is independent of S unless default occurs. Because default is readily observable, this contract aligns with conventional regulatory frameworks that focus on solvency verification rather than continuous reserve monitoring.

The above distinction in payment mechanism underscores the fact that the first contract type—while offering enhanced risk sharing—requires stricter regulations and transparency, whereas the second type remains prevalent in practice due to their operational simplicity.

3. Optimal loss- and background-risk-dependent indemnities

In this section, we consider loss- and background-risk-dependent indemnities in the form of

$ I=I(x, s)$

; that is, the insurer is allowed to choose reinsurance contracts that depend on both its own loss size x and the reinsurer’s background risk level s. We impose the minimum condition—the so-called “principle of indemnity”—on the indemnity function I, which leads to the following admissible set

$ I=I(x, s)$

; that is, the insurer is allowed to choose reinsurance contracts that depend on both its own loss size x and the reinsurer’s background risk level s. We impose the minimum condition—the so-called “principle of indemnity”—on the indemnity function I, which leads to the following admissible set

$\widetilde{\mathcal{A}} = \mathcal{A}$

:

$\widetilde{\mathcal{A}} = \mathcal{A}$

:

\begin{align} \mathcal{A} \;:\!=\; \{I\;:\; [0,M]\times\mathbb{R} \mapsto \mathbb{R}_+ \, | \, 0 \le I(x,s) \le x \text{ for all } x \ge 0 \text{ and all } s\in \mathbb{R}\}.\end{align}

\begin{align} \mathcal{A} \;:\!=\; \{I\;:\; [0,M]\times\mathbb{R} \mapsto \mathbb{R}_+ \, | \, 0 \le I(x,s) \le x \text{ for all } x \ge 0 \text{ and all } s\in \mathbb{R}\}.\end{align}

For every

$I \in \mathcal{A}$

, noting

$I \in \mathcal{A}$

, noting

$R = (S+\pi(I))^+$

, the insurer’s terminal wealth W is given by

$R = (S+\pi(I))^+$

, the insurer’s terminal wealth W is given by

\begin{align} W(I) = w - X - \pi(I) + I(X,S) \cdot \mathbf{1}_{ \{R \ge I(X,S)\} } + \tau R \cdot \mathbf{1}_{ \{ R \,{\lt}\, I(X,S) \} }.\end{align}

\begin{align} W(I) = w - X - \pi(I) + I(X,S) \cdot \mathbf{1}_{ \{R \ge I(X,S)\} } + \tau R \cdot \mathbf{1}_{ \{ R \,{\lt}\, I(X,S) \} }.\end{align}

We state the first concrete version of Problem 1 as follows.

Problem 2. The insurer seeks an optimal loss- and background-risk-dependent reinsurance contract

$I^*\;:\!=\;I^*(x, s) \in \mathcal{A}$

to maximize the expected utility of its terminal wealth under the reinsurer’s endogenous default and background risk, that is,

$I^*\;:\!=\;I^*(x, s) \in \mathcal{A}$

to maximize the expected utility of its terminal wealth under the reinsurer’s endogenous default and background risk, that is,

\begin{align*}I^* = \mathop{\operatorname{argsup}}_{I \in \mathcal{A}} \, \mathbb{E}[u(W(I))],\end{align*}

\begin{align*}I^* = \mathop{\operatorname{argsup}}_{I \in \mathcal{A}} \, \mathbb{E}[u(W(I))],\end{align*}

in which the admissible set

$\mathcal{A}$

is defined in (3.1), and W(I) is given by (3.2).

$\mathcal{A}$

is defined in (3.1), and W(I) is given by (3.2).

Remark 3.1. The admissible set

$\mathcal{A}$

in (3.1) can be seen as an extension to the one,

$\mathcal{A}$

in (3.1) can be seen as an extension to the one,

$\{I\;:\; [0,M] \mapsto \mathbb{R}_+ \, | \, 0 \le I(x) \le x \text{ for all } x \ge 0 \}$

, used in the classical literature (see Arrow, 1963 and Mossin, 1968), and is likely the largest admissible set one can consider for a meaningful optimal (re)insurance problem. Indeed, related research often imposes further conditions on admissible indemnities. A prime example is the so-called incentive compatibility (IC) condition, which reads as

$\{I\;:\; [0,M] \mapsto \mathbb{R}_+ \, | \, 0 \le I(x) \le x \text{ for all } x \ge 0 \}$

, used in the classical literature (see Arrow, 1963 and Mossin, 1968), and is likely the largest admissible set one can consider for a meaningful optimal (re)insurance problem. Indeed, related research often imposes further conditions on admissible indemnities. A prime example is the so-called incentive compatibility (IC) condition, which reads as

$0 \le I(x) - I(x') \le x - x'$

for all

$0 \le I(x) - I(x') \le x - x'$

for all

$x \ge x' \ge 0$

, and is imposed to rule out certain ex post moral hazard (see Huberman et al., 1983). Under the IC condition, both the indemnity function I and the retained loss function

$x \ge x' \ge 0$

, and is imposed to rule out certain ex post moral hazard (see Huberman et al., 1983). Under the IC condition, both the indemnity function I and the retained loss function

$x - I$

are nondecreasing and satisfy the 1-Lipschitz condition (implying that they are differentiable almost everywhere with the first-order derivatives bounded between 0 and 1). These desirable properties often help simplify the analysis and may even be necessary to obtain an optimal contract in analytical form. We choose to work with

$x - I$

are nondecreasing and satisfy the 1-Lipschitz condition (implying that they are differentiable almost everywhere with the first-order derivatives bounded between 0 and 1). These desirable properties often help simplify the analysis and may even be necessary to obtain an optimal contract in analytical form. We choose to work with

$\mathcal{A}$

in (3.1) to formulate Problem 2 for at least two reasons. First, our method does not need the extra properties on I derived from the IC condition. Second, the optimal contract

$\mathcal{A}$

in (3.1) to formulate Problem 2 for at least two reasons. First, our method does not need the extra properties on I derived from the IC condition. Second, the optimal contract

$I^* \in \mathcal{A}$

we obtain automatically satisfies the IC condition (see Theorem 3.5); therefore, there is no need to impose it a priori. Put differently, if we were to impose the IC condition upfront, we would obtain exactly the same result.

$I^* \in \mathcal{A}$

we obtain automatically satisfies the IC condition (see Theorem 3.5); therefore, there is no need to impose it a priori. Put differently, if we were to impose the IC condition upfront, we would obtain exactly the same result.

3.1. Optimal contract

The goal of this section is to solve Problem 2, and we obtain the optimal reinsurance contract in semiclosed form in Theorem 3.5. We explain the key methodology of solving Problem 2 in a two-step procedure as follows. For ease of presentation, denote by

$\pi_{f}$

the premium of a full reinsurance contract, which, according to (2.1), equals

$\pi_{f}$

the premium of a full reinsurance contract, which, according to (2.1), equals

\begin{align} \pi_{f} = (1 + \eta) \mathbb{E}[X].\end{align}

\begin{align} \pi_{f} = (1 + \eta) \mathbb{E}[X].\end{align}

By the definition of admissible indemnities in (3.1), the premium of an admissible contract must be between 0 (no reinsurance) and

$\pi_{f}$

(full reinsurance).

$\pi_{f}$

(full reinsurance).

-

1. In the first step, we fix a premium level

$a \in [0, \pi_{f}]$

and only consider admissible reinsurance contracts whose premium is equal to a. This leads to a reduced admissible set (3.4)We solve Problem 2 over

\begin{align} \mathcal{A}_a \;:\!=\; \{ I \in \mathcal{A} \, | \, \pi(I) = a \}, \quad a \in [0, \pi_{f}]. \end{align}

$\mathcal{A}_a$

and call the solution (3.5)a locally optimal reinsurance contract.

\begin{align} I^*_a = \mathop{\operatorname{argsup}}_{I \in \mathcal{A}_a} \, \mathbb{E}[u(W(I))] \end{align}

-

2. In the second step, we search over all premium levels

$a \in [0, \pi_{f}]$

to find the optimal premium level

$a^*$

, defined by (3.6)We call

\begin{align} a^* = \mathop{\operatorname{argsup}}_{a \in [0, \pi_{f}]} \, \mathbb{E}[u(W(I_a^*))]. \end{align}

$I^* = I^*_{a^*}$

a globally optimal reinsurance contract because it solves Problem 2 over

$\mathcal{A} = {\cup}_{a \in [0, \pi_{f}]} \mathcal{A}_a$

.

Step 1. We first identify a key threshold

$\bar{a}$

for the premium level and show that the optimal premium

$\bar{a}$

for the premium level and show that the optimal premium

$a^*$

lies in the interval

$a^*$

lies in the interval

$[0, \bar{a}]$

. As such, we only need to solve Problem (3.5) over all

$[0, \bar{a}]$

. As such, we only need to solve Problem (3.5) over all

$a \in [0, \bar{a}]$

in Step 1. To begin, we present a technical lemma for finding

$a \in [0, \bar{a}]$

in Step 1. To begin, we present a technical lemma for finding

$\bar{a}$

. Recall that

$\bar{a}$

. Recall that

$\pi_{f}$

is defined in (3.3).

$\pi_{f}$

is defined in (3.3).

Lemma 3.1. Let

$g\;:\; [0, \pi_{f}] \mapsto \mathbb{R}$

be defined by

$g\;:\; [0, \pi_{f}] \mapsto \mathbb{R}$

be defined by

\begin{align} g(a) \;:\!=\; (1 + \eta) \, \mathbb{E} \left[ X - (X - (S + a)^+)^+ \right] - a, \end{align}

\begin{align} g(a) \;:\!=\; (1 + \eta) \, \mathbb{E} \left[ X - (X - (S + a)^+)^+ \right] - a, \end{align}

and define

\begin{align} \bar{a}\;:\!=\;\inf \left\{a\in[0,\pi_f]\mid g(a)\le 0 \right\}\!. \end{align}

\begin{align} \bar{a}\;:\!=\;\inf \left\{a\in[0,\pi_f]\mid g(a)\le 0 \right\}\!. \end{align}

Then,

$g(\bar{a})=0$

and

$g(\bar{a})=0$

and

$g(a) \,{\gt}\, 0$

for all

$g(a) \,{\gt}\, 0$

for all

$a \in [0,\bar{a})$

.

$a \in [0,\bar{a})$

.

Proof. See Appendix A.1.

Recall that once the insurer chooses an admissible contract

$I \in \mathcal{A}_a$

, the total available reserve from the reinsurer is

$I \in \mathcal{A}_a$

, the total available reserve from the reinsurer is

$R = (S + a)^+$

by (2.2). Because the contract indemnity cannot exceed the loss X itself or the reinsurer’s reserve R, it follows that for all

$R = (S + a)^+$

by (2.2). Because the contract indemnity cannot exceed the loss X itself or the reinsurer’s reserve R, it follows that for all

$I \in \mathcal{A}_a$

, the actual indemnity satisfies

$I \in \mathcal{A}_a$

, the actual indemnity satisfies

$\mathbb{I}(I) \le X \wedge (S+a)^+ = X - (X - ( S+ a)^+)^+$

. Therefore, to account for the possible counterparty default,

$\mathbb{I}(I) \le X \wedge (S+a)^+ = X - (X - ( S+ a)^+)^+$

. Therefore, to account for the possible counterparty default,

$I(x, s) = x - (x - (s + a)^+)^+ \in \mathcal{A}_a$

is the maximum indemnity coverage the insurer may choose among all contracts in

$I(x, s) = x - (x - (s + a)^+)^+ \in \mathcal{A}_a$

is the maximum indemnity coverage the insurer may choose among all contracts in

$\mathcal{A}_a$

. Note that such maximum contracts are defined for all

$\mathcal{A}_a$

. Note that such maximum contracts are defined for all

$a \in [0, \pi_{f}]$

, and they are increasing in a. However, Lemma 3.1 intuitively suggests that there exists a threshold

$a \in [0, \pi_{f}]$

, and they are increasing in a. However, Lemma 3.1 intuitively suggests that there exists a threshold

$\bar{a}$

on the premium level, and the maximum contract at level

$\bar{a}$

on the premium level, and the maximum contract at level

$\bar{a}$

thus serves as the absolute upper bound among all contracts in

$\bar{a}$

thus serves as the absolute upper bound among all contracts in

$\mathcal{A}$

. To be specific, the above discussion motivates us to consider a reinsurance contract with the following indemnity function:

$\mathcal{A}$

. To be specific, the above discussion motivates us to consider a reinsurance contract with the following indemnity function:

\begin{align} \bar{I}(x,s) = x - (x - ( s +\bar{a})^+)^+, \end{align}

\begin{align} \bar{I}(x,s) = x - (x - ( s +\bar{a})^+)^+, \end{align}

in which

$\bar{a}$

is defined in (3.8). The premium of contract

$\bar{a}$

is defined in (3.8). The premium of contract

$\bar{I}$

is

$\bar{I}$

is

$\pi(\bar{I}) = \bar{a}$

because

$\pi(\bar{I}) = \bar{a}$

because

$g(\bar{a}) = 0$

. Furthermore, as

$g(\bar{a}) = 0$

. Furthermore, as

$\bar{I}(x,s) \le (s + \bar{a})^+$

for all

$\bar{I}(x,s) \le (s + \bar{a})^+$

for all

$x \ge 0$

, we have

$x \ge 0$

, we have

$\mathbb{I}(\bar{I}) \equiv \bar{I}(X,S)$

and

$\mathbb{I}(\bar{I}) \equiv \bar{I}(X,S)$

and

$D (\bar{I}) \equiv 0$

for contract

$D (\bar{I}) \equiv 0$

for contract

$\bar{I}$

, implying that

$\bar{I}$

, implying that

$\bar{I}$

in (3.9) is a default-free contract (we call I a default-free contract if the reinsurer will not default when the insurer chooses contract I). The discussion so far suggests that contract

$\bar{I}$

in (3.9) is a default-free contract (we call I a default-free contract if the reinsurer will not default when the insurer chooses contract I). The discussion so far suggests that contract

$\bar{I}$

in (3.9) serves as a “threshold” on the admissible indemnities, as confirmed below.

$\bar{I}$

in (3.9) serves as a “threshold” on the admissible indemnities, as confirmed below.

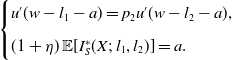

Proposition 3.2. For all

$a \in [\bar{a}, \pi_{f}]$

and all

$a \in [\bar{a}, \pi_{f}]$

and all

$I \in \mathcal{A}_a$

, we have

$I \in \mathcal{A}_a$

, we have

\begin{align} \mathbb{E} \big[ u(W(\bar{I}))\big] \ge \mathbb{E} \big[ u(W(I))\big], \end{align}

\begin{align} \mathbb{E} \big[ u(W(\bar{I}))\big] \ge \mathbb{E} \big[ u(W(I))\big], \end{align}

in which

$\bar{I} \in \mathcal{A}_{\bar{a}}$

is defined by (3.9). In addition, if

$\bar{I} \in \mathcal{A}_{\bar{a}}$

is defined by (3.9). In addition, if

$S\ge 0$

almost surely (i.e.,

$S\ge 0$

almost surely (i.e.,

$\mathbb{P}(S\ge 0)=1$

) and

$\mathbb{P}(S\ge 0)=1$

) and

$\eta=0$

, then

$\eta=0$

, then

$ \bar{I}=I^*$

is the globally optimal reinsurance contract to Problem 2.

$ \bar{I}=I^*$

is the globally optimal reinsurance contract to Problem 2.

Proof. See Appendix A.2.

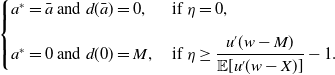

Proposition 3.2 offers two important insights. First, consider the case of

$S\ge 0$

and

$S\ge 0$

and

$\eta = 0$

; the proposition shows that the optimal reinsurance is

$\eta = 0$

; the proposition shows that the optimal reinsurance is

$\bar{I}$

, a contract with partial coverage. If the reinsurer’s default is otherwise ignored, Mossin (Reference Mossin1968) shows that the optimal contract when

$\bar{I}$

, a contract with partial coverage. If the reinsurer’s default is otherwise ignored, Mossin (Reference Mossin1968) shows that the optimal contract when

$\eta = 0$

is full coverage (

$\eta = 0$

is full coverage (

$I^*(x) = x$

). As such, Proposition 3.2 extends Mossin’s result by incorporating the counterparty default risk. Note that the default risk does not impact the deductible choice, as

$I^*(x) = x$

). As such, Proposition 3.2 extends Mossin’s result by incorporating the counterparty default risk. Note that the default risk does not impact the deductible choice, as

$\bar{I}$

has a zero deductible (noting

$\bar{I}$

has a zero deductible (noting

$\bar{I}(x,s) = x$

for all

$\bar{I}(x,s) = x$

for all

$x \,{\lt}\, (s + \bar{a})^+$

), the same as in Mossin (Reference Mossin1968). However, because of the possible default from the reinsurer, the insurer will not seek full coverage even when the loading

$x \,{\lt}\, (s + \bar{a})^+$

), the same as in Mossin (Reference Mossin1968). However, because of the possible default from the reinsurer, the insurer will not seek full coverage even when the loading

$\eta$

is zero. Instead, the optimal contract has a policy limit of

$\eta$

is zero. Instead, the optimal contract has a policy limit of

$(S + \bar{a})^+$

, which equals the reinsurer’s reserve. Second, as

$(S + \bar{a})^+$

, which equals the reinsurer’s reserve. Second, as

$\bar{I}$

dominates all admissible I with premiums greater than

$\bar{I}$

dominates all admissible I with premiums greater than

$\bar{a}$

, the optimal premium level

$\bar{a}$

, the optimal premium level

$a^*$

defined in (3.6) is achieved in

$a^*$

defined in (3.6) is achieved in

$[0, \bar{a}]$

. As such, the remaining task in Step 1 is to solve (3.5) for all

$[0, \bar{a}]$

. As such, the remaining task in Step 1 is to solve (3.5) for all

$a \in [0, \bar{a}]$

, and the next theorem completes this task.

$a \in [0, \bar{a}]$

, and the next theorem completes this task.

Theorem 3.3. For every

$a \in [0, \bar{a}]$

, the locally optimal reinsurance contract

$a \in [0, \bar{a}]$

, the locally optimal reinsurance contract

$I^*_a$

to Problem 2 over the constrained set

$I^*_a$

to Problem 2 over the constrained set

$\mathcal{A}_a$

in (3.4) is given by

$\mathcal{A}_a$

in (3.4) is given by

\begin{align} I_a^*(x,s) = (x - d(a))^+ - (x - d(a) - (s + a)^+)^+, \end{align}

\begin{align} I_a^*(x,s) = (x - d(a))^+ - (x - d(a) - (s + a)^+)^+, \end{align}

in which the deductible amount

$ d(a) \in [0, M] $

solves the equation

$ d(a) \in [0, M] $

solves the equation

\begin{align} g_a(y)\;:\!=\; (1+\eta)\mathbb{E}[(X- y)^+-(X-y-(S+a)^+)^+] - a = 0. \end{align}

\begin{align} g_a(y)\;:\!=\; (1+\eta)\mathbb{E}[(X- y)^+-(X-y-(S+a)^+)^+] - a = 0. \end{align}

Proof. See Appendix A.3.

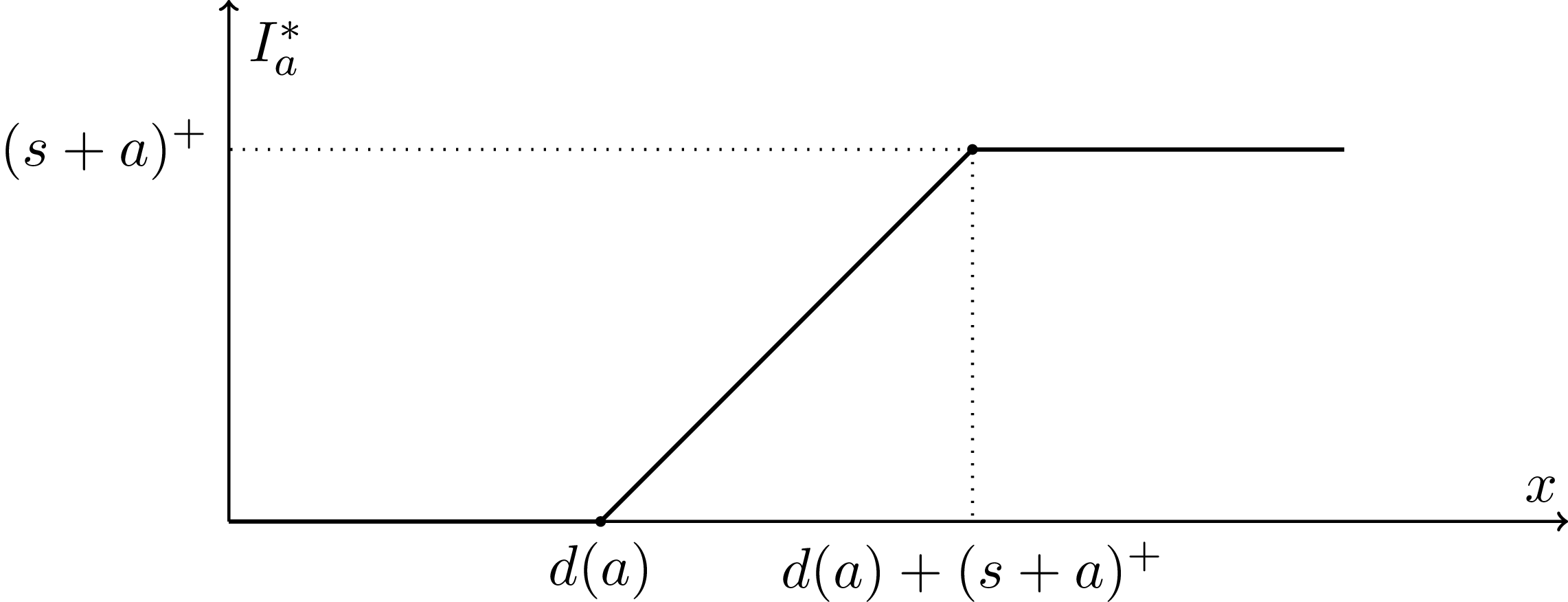

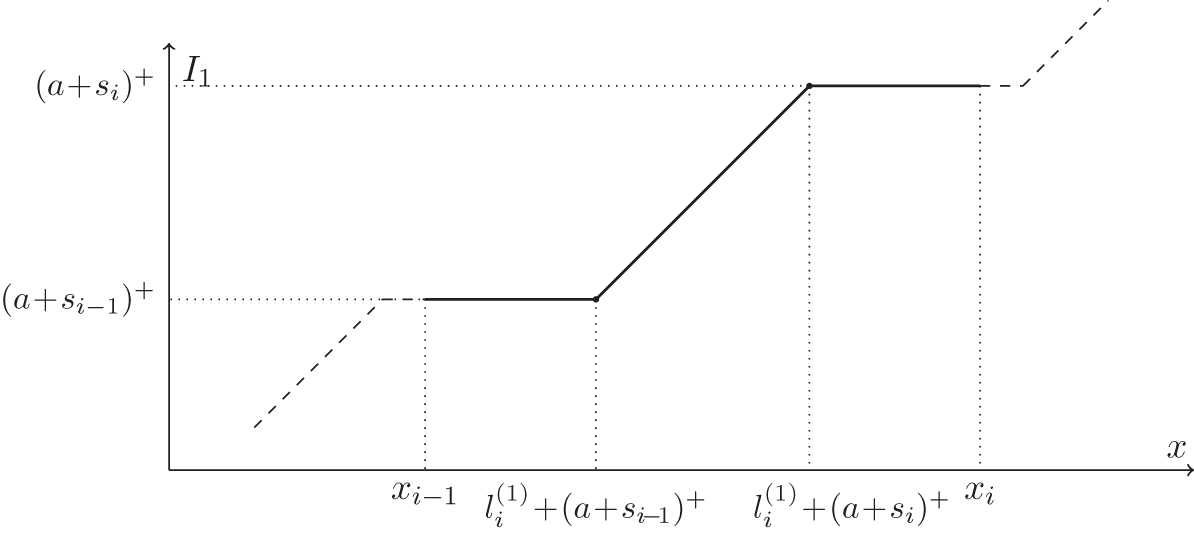

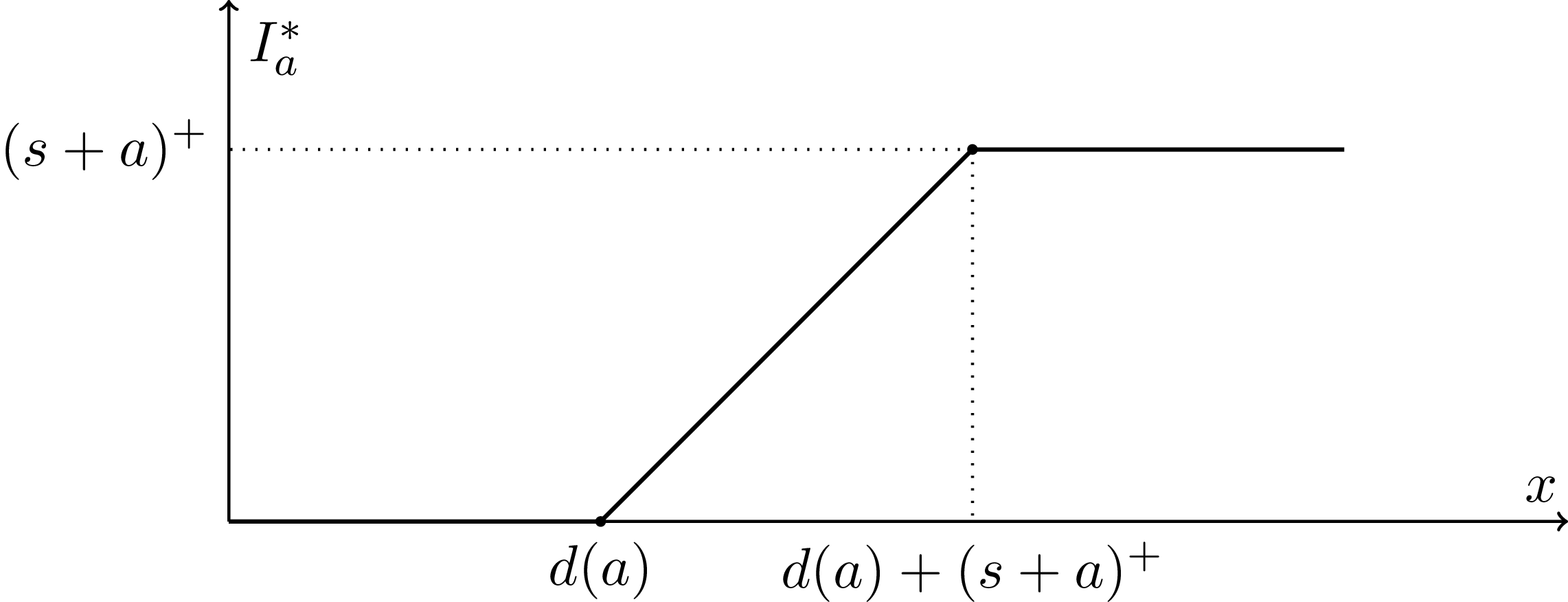

Several remarks on Theorem 3.3 are due as follows. The optimal contract

$I^*_a$

is obtained in semiclosed form in (3.11), and the only unknown d(a) can be easily computed by a numerical method. As easily seen from Figure 1,

$I^*_a$

is obtained in semiclosed form in (3.11), and the only unknown d(a) can be easily computed by a numerical method. As easily seen from Figure 1,

$I^*_a$

is a deductible reinsurance contract with a policy limit; the deductible amount is d(a), and the maximum covered loss is

$I^*_a$

is a deductible reinsurance contract with a policy limit; the deductible amount is d(a), and the maximum covered loss is

$d(a) + (s + a)^+$

, yielding a cap of

$d(a) + (s + a)^+$

, yielding a cap of

$(s + a)^+$

on the contractual indemnity. Such a contract structure is economically justifiable and commonly used in practice. On the one hand, the deductible is present due to the cost of risk transferring and indeed vanishes when

$(s + a)^+$

on the contractual indemnity. Such a contract structure is economically justifiable and commonly used in practice. On the one hand, the deductible is present due to the cost of risk transferring and indeed vanishes when

$\eta = 0$

(i.e., we have

$\eta = 0$

(i.e., we have

$d(a) = 0$

in (3.11) when

$d(a) = 0$

in (3.11) when

$\eta = 0$

, and this result is proved in Proposition 3.2). On the other hand, the policy limit is the direct consequence of the reinsurer’s default risk. We observe from Figure 1 that

$\eta = 0$

, and this result is proved in Proposition 3.2). On the other hand, the policy limit is the direct consequence of the reinsurer’s default risk. We observe from Figure 1 that

$I^*_a(x, s) \le (s + a)^+$

for all

$I^*_a(x, s) \le (s + a)^+$

for all

$x \ge 0$

, and thus

$x \ge 0$

, and thus

$I^*_a$

is a default-free contract (i.e.,

$I^*_a$

is a default-free contract (i.e.,

$D(I^*_a) \equiv 0$

in (2.3)).

$D(I^*_a) \equiv 0$

in (2.3)).

Optimal contract

$I^*_a$

in (3.11).

$I^*_a$

in (3.11).

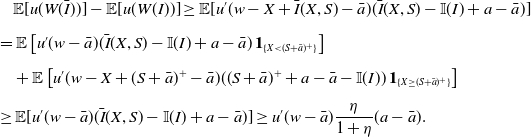

Indeed, a contract that depends on the reinsurer’s background risk S is efficient because it allows the insurer to tailor the coverage to the reinsurer’s ability to pay. Default occurs when the promised indemnity I(X, S) exceeds the reinsurer’s available resources

$(S + \pi(I))^+$

. If the insurer chooses a contract that may extend the reinsurer’s reserve, this would create a deadweight cost in default states, in the sense that the insurer pays for a coverage I(X, S) but receives strictly smaller

$(S + \pi(I))^+$

. If the insurer chooses a contract that may extend the reinsurer’s reserve, this would create a deadweight cost in default states, in the sense that the insurer pays for a coverage I(X, S) but receives strictly smaller

$\tau (S + \pi(I))^+$

. As such, the optimal contract

$\tau (S + \pi(I))^+$

. As such, the optimal contract

$I^*_a$

should always be within the reinsurer’s reserve (i.e., it is default-free); otherwise, for general premium principles, one can easily construct a default-free contract that strictly dominates

$I^*_a$

should always be within the reinsurer’s reserve (i.e., it is default-free); otherwise, for general premium principles, one can easily construct a default-free contract that strictly dominates

$I^*_a$

, contracting its optimality (the exact proof is available upon request).

$I^*_a$

, contracting its optimality (the exact proof is available upon request).

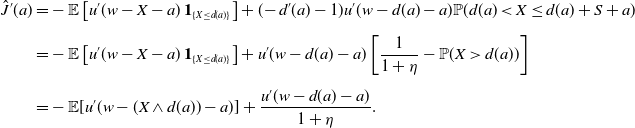

Thanks to Theorem 3.3, we can reduce Problem 2, an infinite-dimensional optimization problem, into a one-dimensional scalar optimization problem in (3.6), which we study in the next step. The solution d(a) to (3.12) may not be unique in general. However, with mild assumptions imposed on the insurer’s loss X (see Corollary 3.4), the uniqueness of d(a) is gained.

Step 2. We solve (3.6) to obtain the optimal premium level

$a^*$

and identify the globally optimal reinsurance contract to Problem 2 as

$a^*$

and identify the globally optimal reinsurance contract to Problem 2 as

$I^* = I^*_{a^*}$

. To that end, we make rather mild assumptions on the insurer’s loss X and the reinsurer’s background risk S and discuss them in Remark 3.2.

$I^* = I^*_{a^*}$

. To that end, we make rather mild assumptions on the insurer’s loss X and the reinsurer’s background risk S and discuss them in Remark 3.2.

Assumption 1. The insurer’s loss X and the reinsurer’s background risk S satisfy the following conditions: (1)

$S \ge 0$

almost surely (i.e.,

$S \ge 0$

almost surely (i.e.,

$\mathbb{P}(S\ge 0)=1$

); (2) both X and

$\mathbb{P}(S\ge 0)=1$

); (2) both X and

$X-S$

have a finite number of jump points on [0, M]; (3)

$X-S$

have a finite number of jump points on [0, M]; (3)

$\mathbb{P}(X\le x)$

strictly increases with respect to

$\mathbb{P}(X\le x)$

strictly increases with respect to

$x \in[0,M]$

; (4)

$x \in[0,M]$

; (4)

$\mathbb{E}[(X-y)^+-(X-y-S)^+]{\gt}0$

holds for all

$\mathbb{E}[(X-y)^+-(X-y-S)^+]{\gt}0$

holds for all

$y\in[0,M)$

.

$y\in[0,M)$

.

Remark 3.2. The reinsurer is required to set aside a strictly positive initial reserve at time 0 (the inception time of a contract), then Condition (1) in Assumption 1, also imposed in Biffis and Millossovich (Reference Biffis and Millossovich2012), simply means that risky investments in the reinsurer’s reserve, such as equities, have limited liabilities, consistent with most real-life scenarios. By Condition (2), both X and

$X-S$

can have jumps at any point, but the total number of jumps on [0, M] must be finite. In the literature, similar, but stronger, assumptions are often imposed in the study of optimal (re)insurance problems. For instance, Bernard et al. (Reference Bernard, He, Yan and Zhou2015) assume that X has no atom, while Cai et al. (Reference Cai, Lemieux and Liu2014) assume that X only has a jump at 0. Condition (3) is also imposed in Asimit et al. (Reference Asimit, Badescu and Cheung2013) and Cai et al. (Reference Cai, Lemieux and Liu2014). Condition (4) is a rather mild condition and holds in real markets, because Condition (3), along with

$X-S$

can have jumps at any point, but the total number of jumps on [0, M] must be finite. In the literature, similar, but stronger, assumptions are often imposed in the study of optimal (re)insurance problems. For instance, Bernard et al. (Reference Bernard, He, Yan and Zhou2015) assume that X has no atom, while Cai et al. (Reference Cai, Lemieux and Liu2014) assume that X only has a jump at 0. Condition (3) is also imposed in Asimit et al. (Reference Asimit, Badescu and Cheung2013) and Cai et al. (Reference Cai, Lemieux and Liu2014). Condition (4) is a rather mild condition and holds in real markets, because Condition (3), along with

$S \,{\gt}\, 0$

, implies Condition (4).

$S \,{\gt}\, 0$

, implies Condition (4).

On the technical side, because of

$S \ge 0$

, we have

$S \ge 0$

, we have

$ (S + a)^+ = (S + a) $

for all

$ (S + a)^+ = (S + a) $

for all

$a \ge 0$

, and it helps avoid discontinuities when taking derivatives with respect to a. Condition (2) is used to show that certain functions are continuously differentiable, except for a finite set. Conditions (3) and (4) ensure the uniqueness of some solutions. These properties are used in the proofs of Corollary 3.4, Theorem 3.5, and Proposition 3.7.

$a \ge 0$

, and it helps avoid discontinuities when taking derivatives with respect to a. Condition (2) is used to show that certain functions are continuously differentiable, except for a finite set. Conditions (3) and (4) ensure the uniqueness of some solutions. These properties are used in the proofs of Corollary 3.4, Theorem 3.5, and Proposition 3.7.

In the special case without the reinsurer’s background risk, we have

$S \equiv r \,{\gt}\, 0$

, the initial reserve; recall that

$S \equiv r \,{\gt}\, 0$

, the initial reserve; recall that

$S \le 0$

is already analyzed in Proposition 2.1. In this case, we can further remove the conditions on S in Assumption 1.

$S \le 0$

is already analyzed in Proposition 2.1. In this case, we can further remove the conditions on S in Assumption 1.

Recall that for a fixed

$a \in [0, \bar{a}]$

, the deductible d(a) that solves

$a \in [0, \bar{a}]$

, the deductible d(a) that solves

$g_a(y) = 0$

in Theorem 3.3 may not be unique. However, under Assumption 1, the next corollary shows that d(a) is unique.

$g_a(y) = 0$

in Theorem 3.3 may not be unique. However, under Assumption 1, the next corollary shows that d(a) is unique.

Corollary 3.4. Let Assumption 1 hold. For every

$a \in [0, \bar{a}]$

, there exists a unique solution

$a \in [0, \bar{a}]$

, there exists a unique solution

$d(a) \in [0, M]$

to

$d(a) \in [0, M]$

to

$g_a (y) = 0$

in (3.12).

$g_a (y) = 0$

in (3.12).

Proof. See Appendix A.4.

We now solve for the optimal premium level

$a^*$

and obtain a full solution to the insurer’s optimal reinsurance problem (see Problem 2). Note that when

$a^*$

and obtain a full solution to the insurer’s optimal reinsurance problem (see Problem 2). Note that when

$S \ge 0$

and

$S \ge 0$

and

$\eta = 0$

, Proposition 3.2 shows that

$\eta = 0$

, Proposition 3.2 shows that

$\bar{I}$

in (3.9) is the optimal contract to Problem 2. Also, recall that

$\bar{I}$

in (3.9) is the optimal contract to Problem 2. Also, recall that

$\bar{a}$

is defined by (3.8).

$\bar{a}$

is defined by (3.8).

Theorem 3.5. Let Assumption 1 hold. The globally optimal reinsurance contract

$I^*$

to Problem 2 is given by

$I^*$

to Problem 2 is given by

\begin{align} I^*(x,s) = \begin{cases} x-(x-(s+\bar{a}))^+, & \text{if } \eta = 0, \\[5pt] (x-d(a^*))^+-(x-(d(a^*)+s+a^*))^+, & \text{if } 0\lt\eta\lt\dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1, \\[10pt] 0, & \text{if } \eta\ge \dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1, \end{cases} \end{align}

\begin{align} I^*(x,s) = \begin{cases} x-(x-(s+\bar{a}))^+, & \text{if } \eta = 0, \\[5pt] (x-d(a^*))^+-(x-(d(a^*)+s+a^*))^+, & \text{if } 0\lt\eta\lt\dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1, \\[10pt] 0, & \text{if } \eta\ge \dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1, \end{cases} \end{align}

in which

$M = \operatorname{ess \, sup} \, X \,{\lt}\, \infty$

, d(a) is established in Corollary 3.4 for all

$M = \operatorname{ess \, sup} \, X \,{\lt}\, \infty$

, d(a) is established in Corollary 3.4 for all

$a \in [0, \bar{a}]$

, and

$a \in [0, \bar{a}]$

, and

$a^*\in (0,\bar{a})$

is the unique solution to

$a^*\in (0,\bar{a})$

is the unique solution to

\begin{align} \mathbb{E}[u'(w-(X\wedge d(a))-a)]-\frac{u'(w-d(a)-a)}{1+\eta}=0.\end{align}

\begin{align} \mathbb{E}[u'(w-(X\wedge d(a))-a)]-\frac{u'(w-d(a)-a)}{1+\eta}=0.\end{align}

Proof. See Appendix A.5.

Theorem 3.5 presents the optimal contract

$I^*$

case by case based on the value of the premium loading

$I^*$

case by case based on the value of the premium loading

$\eta$

. Alternatively, we can write

$\eta$

. Alternatively, we can write

$I^*$

in the following uniform expression:

$I^*$

in the following uniform expression:

\begin{align*} I^*(x,s) = (x-d(a^*))^+-(x-(d(a^*)+s+a^*))^+, \end{align*}

\begin{align*} I^*(x,s) = (x-d(a^*))^+-(x-(d(a^*)+s+a^*))^+, \end{align*}

because

\begin{align} \begin{cases} a^* = \bar{a} \text{ and } d(\bar{a}) = 0, & \text{ if } \eta = 0, \\[9pt] a^* = 0 \text{ and } d(0) = M, & \text{ if } \eta\ge \dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1. \end{cases} \end{align}

\begin{align} \begin{cases} a^* = \bar{a} \text{ and } d(\bar{a}) = 0, & \text{ if } \eta = 0, \\[9pt] a^* = 0 \text{ and } d(0) = M, & \text{ if } \eta\ge \dfrac{u'(w-M)}{\mathbb{E}[u'(w-X)]}-1. \end{cases} \end{align}

As suggested by the uniform expression, the optimal contract

$I^*$

is a deductible reinsurance with a policy limit, just as

$I^*$

is a deductible reinsurance with a policy limit, just as

$I^*_a$

in (3.11) (see Figure 1). We remark that the presence of the policy limit in

$I^*_a$

in (3.11) (see Figure 1). We remark that the presence of the policy limit in

$I^*$

reflects the impact of counterparty default on the insurer’s decision-making; the policy limit vanishes when the reinsurer’s reserve is sufficiently large (so that default never occurs). The first case in (3.13) shows that the deductible in

$I^*$

reflects the impact of counterparty default on the insurer’s decision-making; the policy limit vanishes when the reinsurer’s reserve is sufficiently large (so that default never occurs). The first case in (3.13) shows that the deductible in

$I^*$

vanishes when the premium loading

$I^*$

vanishes when the premium loading

$\eta$

equals zero. From the last case in (3.13), we see that if the premium loading

$\eta$

equals zero. From the last case in (3.13), we see that if the premium loading

$\eta$

is too high, the insurer is better off with 100% self-insurance than purchasing reinsurance from the reinsurer. If reinsurance is reasonably priced as in the second case of (3.13), endogenous default may occur if the insurer chooses an arbitrary contract among all admissible choices in (3.1). However, if the insurer chooses the optimal contract

$\eta$

is too high, the insurer is better off with 100% self-insurance than purchasing reinsurance from the reinsurer. If reinsurance is reasonably priced as in the second case of (3.13), endogenous default may occur if the insurer chooses an arbitrary contract among all admissible choices in (3.1). However, if the insurer chooses the optimal contract

$I^*$

, we always have

$I^*$

, we always have

$D(I^*) \equiv 0$

, and the reinsurer will never default on

$D(I^*) \equiv 0$

, and the reinsurer will never default on

$I^*$

. On a technical note, for the second case, we need to solve a nonlinear Equation (3.14) to get the optimal premium

$I^*$

. On a technical note, for the second case, we need to solve a nonlinear Equation (3.14) to get the optimal premium

$a^*$

, which may seem to be a challenging task. Luckily, we can show that both

$a^*$

, which may seem to be a challenging task. Luckily, we can show that both

$g_a$

in (3.12) and the left-hand side of (3.14) are strictly decreasing functions, which allows us to efficiently compute

$g_a$

in (3.12) and the left-hand side of (3.14) are strictly decreasing functions, which allows us to efficiently compute

$a^*$

and

$a^*$

and

$d(a^*)$

(see Example 3.1 below). Last, we observe that the optimal contract

$d(a^*)$

(see Example 3.1 below). Last, we observe that the optimal contract

$I^*$

satisfies the IC constraint automatically (i.e.,

$I^*$

satisfies the IC constraint automatically (i.e.,

$0 \le I^*(x,s) - I^*(x',s) \le x - x'$

for all

$0 \le I^*(x,s) - I^*(x',s) \le x - x'$

for all

$0 \le x' \le x \le M$

), which is why we do not impose the IC constraint upfront in defining the admissible set

$0 \le x' \le x \le M$

), which is why we do not impose the IC constraint upfront in defining the admissible set

$\mathcal{A}$

in (3.1).

$\mathcal{A}$

in (3.1).

Due to the presence of endogenous default, we cannot establish the strict concavity of the functional

$ \mathcal{J}(I)\;:\!=\; \mathbb{E}[u(W(I))] $

. Fortunately, we can show that under Assumption 1,

$ \mathcal{J}(I)\;:\!=\; \mathbb{E}[u(W(I))] $

. Fortunately, we can show that under Assumption 1,

$ I^* $

in (3.13) is the unique globally optimal reinsurance contract.

$ I^* $

in (3.13) is the unique globally optimal reinsurance contract.

Proposition 3.6. Let Assumption 1 hold. Then,

$I^*$

in (3.13) is the unique globally optimal reinsurance contract to Problem 2.

$I^*$

in (3.13) is the unique globally optimal reinsurance contract to Problem 2.

Proof. See Appendix A.6.

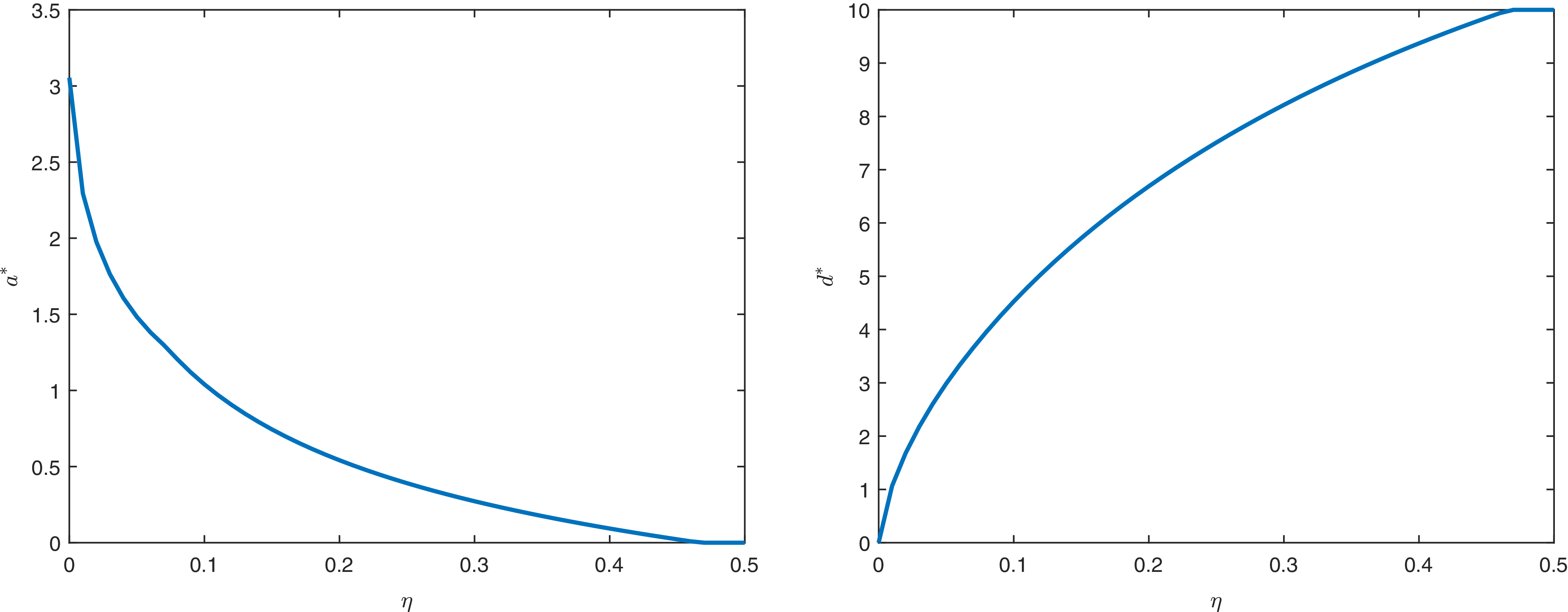

3.2. Comparative statics

In this section, we conduct a comparative statics analysis on the optimal reinsurance contract

$I^*$

obtained in Theorem 3.5. This goal can be easily achieved by a numerical method once the model is given, but it is challenging to obtain analytical results, which we are able to achieve under mild conditions (see Proposition 3.7). Note that certain, but not all, results in Proposition 3.7 require a condition on the insurer’s utility function, as stated below.

$I^*$

obtained in Theorem 3.5. This goal can be easily achieved by a numerical method once the model is given, but it is challenging to obtain analytical results, which we are able to achieve under mild conditions (see Proposition 3.7). Note that certain, but not all, results in Proposition 3.7 require a condition on the insurer’s utility function, as stated below.

Assumption 2. The insurer’s utility function u satisfies the decreasing absolute risk aversion (DARA) condition; that is, the Arrow–Pratt coefficient of absolute risk aversion, defined by

$\mathbb{A}_u= - \frac{u''}{u'}$

, is a decreasing function.

$\mathbb{A}_u= - \frac{u''}{u'}$

, is a decreasing function.

By definition, agents with DARA risk preferences have reduced risk aversion when their wealth increases. This result is mostly consistent with empirical findings (see Levy Reference Levy1994). A prominent example of DARA risk preferences is the family of power utility functions

$u(x) = \frac{1}{1 - \gamma} \, x^{1 - \gamma}$

, in which

$u(x) = \frac{1}{1 - \gamma} \, x^{1 - \gamma}$

, in which

$\gamma \,{\gt}\, 0$

and

$\gamma \,{\gt}\, 0$

and

$\gamma \neq 1$

.

$\gamma \neq 1$

.

Before we present the key results on comparative statics, we introduce the following notations: let

$a^*$

denote the optimal premium level for all

$a^*$

denote the optimal premium level for all

$\eta \ge 0$

(as defined in (3.6) and calculated by (3.14) or (3.15)); for the optimal reinsurance contract,

$\eta \ge 0$

(as defined in (3.6) and calculated by (3.14) or (3.15)); for the optimal reinsurance contract,

$d^*\;:\!=\; d(a^*)$

is the deductible amount, and

$d^*\;:\!=\; d(a^*)$

is the deductible amount, and

$U^* \;:\!=\; a^* + d^* + S$

is the policy limit (maximum covered loss). The following proposition summarizes the analytical results on how the specifications of the insurer’s optimal contract (

$U^* \;:\!=\; a^* + d^* + S$

is the policy limit (maximum covered loss). The following proposition summarizes the analytical results on how the specifications of the insurer’s optimal contract (

$a^*$

,

$a^*$

,

$d^*$

, and

$d^*$

, and

$U^*$

) are affected by model inputs. Because we allow discontinuities in the distribution of the insurer’s loss X, the proof is technical and lengthy, and thus we defer it to Online Companion.

$U^*$

) are affected by model inputs. Because we allow discontinuities in the distribution of the insurer’s loss X, the proof is technical and lengthy, and thus we defer it to Online Companion.

Proposition 3.7. Let Assumption 1 hold. We have the following comparative statics results on the optimal reinsurance contract

$I^*$

in (3.13).

$I^*$

in (3.13).

-

1. The optimal premium level

$a^*$

increases with respect to the reinsurer’s background risk S (in the pointwise sense), so is

$a^* + d^*$

. Furthermore, if Assumption 2 holds, then the optimal deductible

$d^*$

decreases with respect to S. -

2. If Assumption 2 holds, then the optimal premium level

$a^*$

decreases with respect to the insurer’s initial wealth w, but both the optimal deductible

$d^*$

and

$a^* + d^*$

increase with respect to w. -

3. The optimal premium level

$a^*$

increases with respect to the insurer’s (Arrow–Pratt) degree of risk aversion

$\mathbb{A}_u$

, but both the optimal deductible

$d^*$

and

$a^* + d^*$

decrease with respect to

$\mathbb{A}_u$

.

Proof. See Online Companion II.

In the first item of Proposition 3.7, we analyze the impact of the reinsurer’s background risk S on the optimal contract; note that “increase” or “decrease” is in the pointwise sense (i.e., if

$S_1$

increases to

$S_1$

increases to

$S_2$

, we have

$S_2$

, we have

$S_2(\omega) \ge S_1(\omega)$

for all

$S_2(\omega) \ge S_1(\omega)$

for all

$\omega \in \Omega$

, except for a negligible set). Recall that

$\omega \in \Omega$

, except for a negligible set). Recall that

$S + \pi(I)$

is the total available reserve for settling claims at time 1, thus the larger the S, the lower the default possibility. As such, when S increases, we expect the insurer to seek more coverage for its risk exposure, which is confirmed by the decrease of the deductible

$S + \pi(I)$

is the total available reserve for settling claims at time 1, thus the larger the S, the lower the default possibility. As such, when S increases, we expect the insurer to seek more coverage for its risk exposure, which is confirmed by the decrease of the deductible

$d^*$

and the increase of the policy limit

$d^*$

and the increase of the policy limit

$U^*$

(recall

$U^*$

(recall

$U^* = a^* + d^* + S$

); the increase of coverage naturally means a higher premium paid to the reinsurer.

$U^* = a^* + d^* + S$

); the increase of coverage naturally means a higher premium paid to the reinsurer.