Introduction

Sustainable finance is the endeavour to redirect capital flows from unsustainable to sustainable economic activities.Footnote 1 In the face of the worsening climate and biodiversity crises and the enormous social challenges that we are facing, this endeavour has received a great deal of attention. Although sustainable finance policies are currently facing backlash in some jurisdictions, such as in the United States (US) and the European Union (EU), many policymakers still regard them as a crucial lever for the transformation of the real economy. After all, today’s investments will determine production patterns and production technologies for decades to come. Access to information about environmental, social, or governance (ESG) issues related to investment projects should allow investors to take these issues into account in their decision-making. The hope is that this will lead to a redirection of capital flows to economic activities that are important for the realisation of sustainability goals and set incentives for all firms to pursue more sustainable business models. Policymakers thus associate great promise with sustainable finance policies: Relatively limited adjustments to the ways in which sustainability information is collected and transmitted on financial markets should translate into far-reaching transformational change in the real economy.

This article focuses on the EU and analyses the approach to sustainable finance that it follows in terms of the concepts of ‘epistemic infrastructure’ (Herzog, Reference Herzog2020, Reference Herzog2024) and ‘reflexive law’ (Teubner, Reference Teubner1983). The epistemic infrastructure of financial markets comprises the practices and institutions that collect information and transmit it between market participants. In recent years, governance actors have increasingly tried to shape this infrastructure with the intention to promote sustainability goals. The EU sustainable finance strategy includes, among many other policies, the establishment of a complex sustainable finance taxonomy that defines in a detailed manner what counts as sustainable economic activity. This taxonomy serves, for instance, as a basis for reporting obligations of financial and real economy actors and should thereby increase transparency in financial markets. Another example of a policy in this area is the proposed EU regulation on sustainability ratings, which aims to improve the reliability and transparency of these ratings and reduce conflicts of interest of rating providers.

Such policies follow a reflexive law approach. Unlike conventional forms of governance, reflexive law does not outlaw certain actions (in this case investments in types of projects) or influence market prices via taxes or subsidies. Rather, reflexive law confines itself to setting organisational and procedural norms but leaves market participants the autonomy to decide on substantive issues.

Analysing sustainable finance policies in terms of the concept of reflexive law allows us to derive insights from the conceptual and empirical literature on the use of reflexive law in other policy areas, such as labour law or environmental regulation of the real economy, for the assessment of sustainable finance policies. While the concept of reflexive law has been applied to sustainable finance policies by Boudewijn de Bruin (Reference De Bruin, Sandberg and Warenski2024), so far no investigation of the question exists as to how the well-known advantages and shortcomings of reflexive law policies play out in the area of sustainable finance.

This article argues that sustainable finance is a policy area with characteristics typical of those for which proponents of reflexive law recommend this approach. Many contributors to the multidisciplinary literature on reflexive law argue that this governance approach is better able to deal with highly complex and dynamic situations than alternative forms of governance. At the same time, many existing sustainable finance policies suffer also from the shortcomings of reflexive law identified in the literature. These policies often leave too much discretion to agents with vested interests not aligned with the governance aims. The sustainable finance policies of the EU usually do not create incentives for financial market participants to change their investment decisions in the desired way. The success of sustainable finance policies following a reflexive law approach depends on other policy measures that create such incentives. By introducing conceptual arguments and empirical evidence from a different body of literature to the research debate on sustainable finance, the article lends support to existing research that finds that policies that increase transparency on financial markets regarding sustainability issues are important but alone insufficient to achieve a large-scale redirection of capital flows (Ameli et al., Reference Ameli, Drummond, Bisaro, Grubb and Chenet2020; Christophers, Reference Christophers2017; Kedward et al., Reference Kedward, Gabor and Ryan-Collins2024).

In addition, the discretion reflexive law policies leave to agents with vested interests can prevent these policies even from succeeding in establishing a well-functioning epistemic infrastructure. Financial market participants can often use the leeway provided by these policies to engage in greenwashing (i.e., the misleading or false presentation of an economic product or activity as sustainable). Sustainable finance policies that set very concrete, detailed, and binding norms can to some extent avoid this shortcoming. However, these policies also lose some of the (epistemic) advantages in dealing with complex and dynamic situations that are ascribed in the literature to reflexive law policies in comparison to alternative ways of public interventions in markets.

The article proceeds as follows. The next section clarifies two central concepts of this article, namely the epistemic infrastructure of markets and reflexive law. The subsequent section explains how the sustainable finance policies of the EU address the epistemic infrastructure of financial markets and take a reflexive law approach. The two main sections then provide an overview of the merits and shortcomings of reflexive law as described in the academic literature and apply these considerations to the field of sustainable finance. Overall, this article develops a thorough theoretical understanding of the kind of governance that the sustainable finance policies of the EU provide and discusses the potential and limitations of this approach compared to alternative forms of governance.

Epistemic infrastructure and reflexive law

The epistemic infrastructure of markets

The concept of the epistemic infrastructure of markets stems from Herzog (Reference Herzog2020, Reference Herzog2024). She argues that economic markets can only function well if they are embedded in a suitable epistemic infrastructure that collects and transmits information between market participants. Referring to the classic discussion of the epistemic function of the price mechanism by Friedrich Hayek (Reference Hayek1945), Herzog acknowledges that the price mechanism of markets can process certain kinds of decentralised information. Hayek argues that the knowledge necessary to decide on the ideal allocation of resources is not available in a ‘concentrated or integrated form’ (Hayek, Reference Hayek1945: 519); a central planner cannot have sufficient knowledge about the constantly changing preferences of all persons and the exact availability of means of production in different places and at different times. Markets are, according to Hayek, better able to solve this epistemic task. Prices set by the market convey information on the relative scarcity of commodities.Footnote 2 If, for instance, a new opportunity for the use of a particular resource arises, a rising price informs some producers that they should substitute this resource in their activities or even reduce their production (Hayek, Reference Hayek1945: 526).

This is not the whole story, though. Herzog emphasises that information is exchanged not only through the price mechanism (Herzog, Reference Herzog2020: 270). Obviously, market participants directly communicate with each other, mechanisms of reputation are important, and market participants often spend a lot of resources on the gathering and processing of additional information (e.g., when they engage in market research). In addition, consumer organisations provide certain information and commercial data providers collect and sell information. Public institutions also take measures to ensure that relevant information is collected and transmitted between market participants. Regulations ensure that certain information is disclosed. For instance, firms are legally obliged to publish financial reports and provide information on the ingredients of food products on the packaging.

On financial markets, institutions and practices that collect, check, and transmit information are especially important (though often not well-functioning).Footnote 3 These include, for instance, credit rating agencies, auditors, financial analysts, and credit bureaus. In addition, complex mandatory or voluntary reporting practices of different kinds aim at ensuring the availability of information on financial markets.

I use the term ‘epistemic infrastructure of markets’ to refer to all these practices and institutions that collect and transmit information between market participants. As Hayek makes clear, the price mechanism itself also performs an epistemic function. However, I reserve the term ‘epistemic infrastructure of markets’ for all institutions and practices that ‘surround’ or ‘embed’ the exchange of goods or service for money and fulfil an epistemic task.

A lack or bad design of this infrastructure can be highly problematic. Herzog (Reference Herzog2020) argues that a well-functioning epistemic infrastructure is necessary to enable morally responsible agency. Morally responsible agents need to have ‘an understanding of the wider context and consequences’ (Herzog, Reference Herzog2020: 274) of what they do. Particularly in global markets that are not in the same way institutionally embedded as domestic markets, participants often lack morally responsible agency. For instance, for consumers, it is very difficult to gather information on issues such as the working conditions in the production processes of the goods that they purchase. In the global context, they can so far hardly rely on institutions to take over these epistemic tasks (Herzog, Reference Herzog2020: 276–7).

Economists have also for long described shortcomings that arise when the epistemic infrastructure is lacking or malfunctioning and market participants lack important information. The concept of ‘asymmetric information’, for instance, belongs since the 1970s to the standard repertoire of economists in diagnosing market failures (e.g. Akerlof, Reference Akerlof1970; Spence, Reference Spence1978; Stiglitz and Weiss, Reference Stiglitz and Weiss1981). Asymmetric information exists when market participants differ with respect to their knowledge relevant to an economic transaction; for instance, if the seller of a good has more information about its quality than the buyer. This can lead to market failures such as adverse selection when suppliers of high-quality goods leave the market because customers will not pay a higher price for high quality goods because they cannot easily distinguish them from lower quality goods. In this case, prices do not adequately reflect a preference of consumers for high quality goods; the price mechanism does not successfully solve the epistemic task that Hayek assigns to it. If markets are embedded in an epistemic infrastructure that collects and transmits the relevant information (in this case information on the quality of the goods at stake), this kind of market failure can be avoided.

Reflexive law

The second main concept used in this article is the concept of reflexive law. Reflexive law focuses on procedural norms to spur reflection and self-regulatory processes within a system external to the law. The concept of reflexive law was developed by Gunther Teubner (Reference Teubner1983) and has received much attention by legal scholars and political scientists since then. Besides discussing the general relevance and merits of this form of law (e.g., Maus, Reference Maus1986; Scheuerman, Reference Scheuerman2001; Ubilla, Reference Ubilla2024; Zumbansen, Reference Zumbansen2008), scholars have investigated its application in several policy areas, such as environmental regulations (Aalders and Wilthagen, Reference Aalders and Wilthagen1997; Fiorino, Reference Fiorino1999; Glasbergen, Reference Glasbergen2005; Hirsch, Reference Hirsch2010; Orts, Reference Orts1995a, Reference Orts1995b), labour law (Rogowski and Deakin, Reference Rogowski, Deakin, Rogowski, Salais and Whiteside2011; Rogowski, Reference Rogowski2013), transnational law (Calliess, Reference Calliess2002), occupational health and safety (Aalders and Wilthagen, Reference Aalders and Wilthagen1997), corporate social reporting (Buhmann, Reference Buhmann2013; Hess, Reference Hess1999; Okoye, Reference Okoye2021), factory farming (Braunig, Reference Braunig2005) and efforts to avoid slavery in supply chains (Wen, Reference Wen2016).

The reflexive law approach includes a procedural orientation: Legal requirements are limited to ensuring certain decision-making procedures, creating internal reflexive capacities, incentivising certain forms of discourse, and shaping methods of social cooperation. Teubner states that, according to the reflexive law approach, ‘focussed intervention in social processes is within the domain of law, but it [reflexive law] retreats from taking full responsibility for substantial outcomes’ (Teubner, Reference Teubner1983: 254).Footnote 4 Examples of measures that follow a reflexive law approach are regulations that require agents to provide disclosure reports on their activities or impacts in a certain area, conduct risk assessments, consult with certain other agents before decisions are taken, or undergo external reviews. None of these measures obliges the respective agents to change their behaviour in a certain way (besides conducting the described activities). Instead, the reflexive law approach assumes that agents will adapt their behaviour due to internal forces or mechanisms in the system of which they are a part (e.g., the market on which goods produced by the agent are traded) that are triggered if certain procedural measures are implemented.

Reflexive law can be contrasted with other public interventions in markets. First, governance actors can simply forbid (or require) certain activities, i.e., enact so-called ‘command-and-control regulation’. They can, for instance, outlaw wages that are below a certain minimum, require that pollution limits are not surpassed, or oblige companies to make use of certain technologies that reduce environmental externalities. Secondly, policymakers can choose market-based governance measures that aim at changing behaviour by altering prices. This can be done via the introduction of taxes, subsidies, or the creation of additional tradeable property rights. Thirdly, public entities can themselves become active as economic agents. For instance, goods or services can be provided by a government agency or a state-owned enterprise, public development banks can grant loans and make investments, and so on. The reflexive law approach refrains from such measures and builds on the conviction that the desired outcomes can be achieved through the imposition of procedural and organisational norms.

Sustainable finance policies as reflexive law

The rationale behind the idea of addressing the epistemic infrastructure of financial markets with the aim of redirecting capital flows is fairly simple: Investors should know about the sustainability impacts of their potential investment projects. Only then, can they possibly shift their capital to more sustainable activities. If financial market participants do not have access to information on sustainability impacts of investments, sustainability risks are not properly managed and investors cannot align their decisions with sustainability goals.

In recent years, efforts have been made to add new practices and institutions to the epistemic infrastructure of financial markets that collect and transmit information on the sustainability impacts of investments. Just to name a few examples, reporting on non-financial issues by financial market participants and real economy firms has strongly increased over the past two decades (Stolowy and Paugam, Reference Stolowy and Paugam2018). In addition, sustainability rating agencies, such as Sustainalytics or the Institutional Shareholder Services group of companies (ISS), gather data on the sustainability of companies and calculate ratings based on this data. In a sense, the emergence of markets for dedicated sustainable financial products, such as green bonds or sustainable equity funds, can also be seen as contributing to the transmission of information. If the providers of these products apply ambitious and credible sustainability criteria, investors that buy these products are informed about the sustainable use of the proceeds of these instruments.

However, the existing epistemic infrastructure related to sustainability information is far from working well. For instance, greenwashing is often an issue when financial market participants and other companies report on their own products and activities (Wilson, Reference Wilson2013). In addition, sustainability ratings diverge to a great extent between different rating agencies, calling their meaningfulness into question (Dorfleitne et al., Reference Dorfleitner, Halbritter and Nguyen2015). Shortcomings of these kinds reduce the credibility of the information collected and transmitted through the described mechanisms and reduce the capability of the epistemic infrastructure to make investors knowledgeable about the sustainability of their investment projects. Partly with the aim of addressing such shortcomings, governments and regulators have started to implement policy measures to alter and expand the epistemic infrastructure that collects and transmits sustainability information.

The EU sustainable finance strategy

In the EU, policy efforts of recent years to align financial markets with sustainability goals have largely focused on targeting the epistemic infrastructure (Baer et al., Reference Baer, Campiglio and Deyris2021). Although discussions on sustainable finance policies in Europe are older (and have, as Ahlström and Sjåfjell (Reference Ahlström, Sjåfjell, Cadman and Sarker2022) show, gone through different phases), this article focuses on policies implemented after the adoption of the Action Plan: Financing Sustainable Growth (European Commission, 2018). The Action plan describes three objectives of sustainable finance policies: to reorient capital flows towards sustainable investments, to manage financial risks associated with sustainability issues, and to foster transparency and long-termism. A later Strategy for Financing the Transition to a Sustainable Economy expands on the action plan (European Commission, 2021). Judged by the ambitious goals of the EU sustainable finance agenda communicated in these strategy documents and the concrete policy measures implemented, the policymaking approach of the EU in the area of sustainable finance seems to be based on the idea that limited adjustments to the ways in which sustainability information is collected and transmitted in financial markets will translate into far-reaching transformational change.

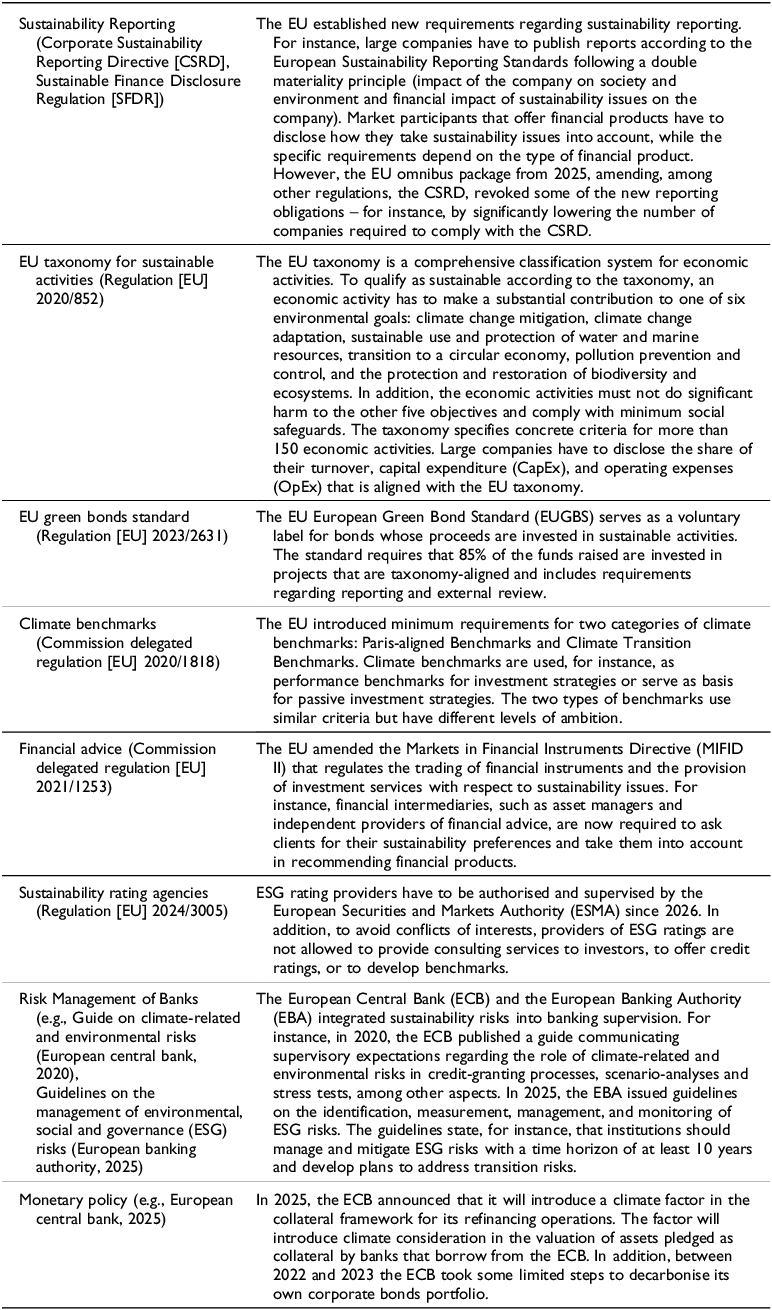

The EU chose a multistakeholder approach in designing its sustainable finance policies (Tischer and Ferrando, Reference Tischer and Ferrando2024). Over the years, the High-level Expert Group on Sustainable Finance followed by the Technical Expert Group on Sustainable Finance and the EU Platform on Sustainable Finance shaped the overall EU strategy as well as concrete policies. These groups included representatives from financial market actors, real economy firms, business associations, civil society organisations, and public entities. However, based on a network analysis, Tischer and Ferrando (Reference Tischer and Ferrando2024) argue that financial actors and ‘pro-business voices’ remained dominant in EU policymaking on sustainable finance. The strong role of financial actors might be a reason why the EU sustainable finance policies took its current form, which intervenes – as will be argued later in this article – less in the decision-making of financial market participants than potential alternative forms of governance. Some of the policy measures that were implemented (or are planned to be implemented) by EU institutions are described in Table 1.

Selection of EU sustainable finance policies of recent years.

The reflexive law approach of EU sustainable finance policies

It is easy to see that most of the EU policies listed in Table 1 address the epistemic infrastructure of financial markets. The new reporting requirements should ensure the transmission of sustainability information. The introduction of a sustainable finance taxonomy is meant to establish a ‘common language’ on financial markets on what kind of economic activities are sustainable, and thereby reduce the transaction costs associated with conveying sustainability information.Footnote 5 Likewise, the EU Green Bonds Standard has the aim to make it easier for bonds issuers to communicate to other market participants in a credible way that the proceeds of their bonds are used for green activities. Regulations regarding benchmarks and sustainability ratings also target crucial parts of the epistemic infrastructure of the financial sector.

Following de Bruin (Reference De Bruin, Sandberg and Warenski2024), the sustainable finance policies of the EU can be described as following a reflexive law approach. Not all sustainable finance policies are, strictly speaking, laws (for instance, they also take the form of guidelines, communications of supervisory expectations, etc.). Thus, I will often state in the following that certain measures are reflexive law policies or follow a reflexive law approach instead of claiming that they are reflexive laws.

To understand that the EU policies on sustainable finance follow a reflexive law approach, note, first, that these policies clearly do not take one of the alternative forms of public intervention in markets that have been described above: The EU policies do not outlaw investments in certain economic activities or even oblige investors to invest in specific activities that are considered as sustainable. Nor do they introduce taxes or subsidies to redirect investments. In addition, the described policies do not rely on public institutions to directly provide the investments that the policies aim to bring about. Instead, sustainable finance policies are usually meant to alter the structure of financial markets in a way so that dynamics within this societal subsystem lead to a redirection of capital.

A few EU sustainable finance policies directly aim at spurring reflection of financial market participants on sustainability issues. For instance, an obligation for providers of financial advice to ask clients for their sustainability preferences should stimulate reflection on the part of the clients and ensure that sustainability issues are discussed before the decision to purchase a certain financial product is taken. By asking banks to integrate climate-related and environmental risks in scenario analysis and stress testing, the EU tries to ensure that market participants actively assess sustainability issues and reflect on the role of the risks associated with these issues. Furthermore, if financial market participants have to assess whether their assets are aligned with the EU taxonomy, this can also facilitate reflection on how they can improve the sustainability impacts of their investments. For instance, Hummel and Bauernhofer (Reference Hummel and Bauernhofer2024) find that the implementation of the EU taxonomy has triggered internal discussions in companies and contributed to putting sustainability on the agenda of management. In addition, taxonomy assessments and disclosure might lead to investor engagement with the companies on sustainability issues.

Another goal of the EU taxonomy and related disclosure obligations is to increase transparency on the sustainability of investments to other market participants. While this purpose is not linked as directly to reflective processes as the policies just mentioned, it is still aligned with a reflexive law approach because the rationale behind it is to address the basis on which investment decisions by market participants are taken instead of directly interfering with these decisions. The EU taxonomy and the different kinds of non-financial reporting obligations are meant to provide investors with new information on which they can reflect and take into account in their decision-making. Similarly, regulations of sustainability rating agencies to avoid conflicts of interests should improve the reliability of the ratings on which other market participants base investment decisions.

The only EU policies listed in Table 1 that go beyond a reflexive law approach and address the epistemic infrastructure concern the monetary policy of the ECB. Efforts to decarbonise the portfolio of the ECB and reforms to the collateral framework of its refinancing operations are less focused on transmitting information or encouraging reflective processes, and more aimed at directly altering financial incentives. However, the ECB’s efforts to green its portfolio have, to date, been limited in scope (Gabor and Braun, Reference Gabor and Braun2025), and the changes to the collateral framework are expected to take effect only in the second half of 2026.

Policies that address the epistemic infrastructure of financial markets to change investment outcomes could be implemented as a basis for other governance measures. For instance, unlike in the EU, a sustainable finance taxonomy could be linked to tax reductions for taxonomy-aligned investments. However, in most cases, the EU policies addressing the epistemic infrastructure are not meant to serve as a basis for market-based governance mechanisms or command-and-control regulations, but should have an impact on capital flows in their own rights. These policies then follow a reflexive law approach: They do not directly interfere with the substantive investment decisions of market participants but address how and on what basis these decisions are made. Organisational reforms altering the informational basis of decision-making should facilitate processes within the financial sector that lead to a redirection of capital flows.

Potential advantages of the reflexive law approach in sustainable finance

Analysing sustainable finance policies through the epistemic infrastructure of financial markets and reflexive law facilitates a better understanding of their functioning, as well as their merits and shortcomings compared to alternative public interventions. Drawing on existing literature on reflexive law in different sectors, the remainder of this article discusses these merits and shortcomings. This section starts by describing the advantages in dealing with complex and dynamic situations that are often ascribed to reflexive law and considers whether sustainable finance is, in principle, a policy field where these advantages could be relevant.

Dealing with complexity

Many scholars argue that reflexive law does comparatively well in dealing with complexity (Gaines, Reference Gaines2002; Orts, Reference Orts1995a, Reference Orts1995b; Scheuerman, Reference Scheuerman2001; Wen, Reference Wen2016). If regulators merely enact organisational and procedural norms, concrete decisions on substantive issues are left to individual market participants. It is assumed that in complex circumstances these agents are best positioned to make these decisions. Along these lines, Wen (Reference Wen2016) draws from her case study on the United Kingdom Modern Slavery Act from 2015 the conclusion that the act’s reflexive law approach is to a relatively high extent able to deal with the complexities related to the transnational and often opaque nature of global supply chains that include production processes in extremely diverse circumstances.

Scholars favouring reflexive law often argue that in dealing with complexity, this governance approach does better than command-and-control regulations because regulators do not have access to the information they would need to design adequate regulations and avoid unintended consequences (remember Hayek’s argument about the difficulties of centralised institutions to process dispersed information). For instance, regulators might not be able to know where the use of a certain resource or the production of a kind of pollution can be reduced most cost-effectively. In addition, if regulation tries to track the growing complexity of economic and societal systems, this can lead to ‘juridification’, i.e., a proliferation of law (Hess, Reference Hess1999: 49–50).Footnote 6 This proliferation of law comes with disadvantages, such as the additional bureaucracy and costs that are associated with implementing the increasing number of rules and controlling compliance with them.

In addition, a growing complexity of regulations makes it more challenging to achieve a high degree of public participation in decision-making and create opportunities for democratic contestation and for holding decision-makers to account (Hess, Reference Hess1999: 50). Complexity makes it difficult for the broader public to understand and follow proposals for potential regulations and thus fosters technocratic forms of decision-making. Excessive discretion of administrators and judges in implementing and enforcing the regulations can be an issue if rules are formulated more open-ended to be applicable to many different cases and circumstances (Scheuerman, Reference Scheuerman2001: 94).

Complex situations are also challenging for the design of market-based governance measures. In these circumstances, it is often difficult to design efficient interventions that achieve the right corrections of market prices necessary to achieve a desired outcome (Orts, Reference Orts1995b: 783). For sustainability goals, it is often challenging – and includes considerable bureaucracy (Knoll, Reference Knoll2015) – to define commensurable commodities, such as tradeable pollution rights, and develop markets on which they are traded so that all relevant externalities are addressed. Take, for instance, the goal of preserving biodiversity. Economic activities affect biodiversity in many different ways so that it would be extremely difficult to create markets that lead to an internalisation of all relevant external effects. ‘To break down ecological complexity into compartmentalized tradable units’ (Gómez-Baggethun and Muradian, Reference Gómez-Baggethun and Muradian2015: 221) is in many cases an enormous challenge.

The last option of the list of potential public interventions in markets described earlier, namely to let public institutions become active agents in the economy to pursue sustainability goals, also faces challenges related to complexity. In this case, the same information deficits apply that make adequate command-and-control regulations difficult. According to critics, in contexts marked by high complexity, public institutions might simply not know where, for instance, funds are most effectively invested to further their sustainability goals. In addition, in the case of public economic activities, it is often difficult to assess how they affect private activities. However, it is crucial for the overall impact of, for instance, public investments if they ‘crowd out’ or ‘crowd in’ private investments.Footnote 7

Are these advantages of reflexive law policies found by the literature on reflexive law in other policy areas also relevant for sustainable finance? In principle, as Ahlström and Sjåfjell (Reference Ahlström, Sjåfjell, Cadman and Sarker2022) argue, high complexity is a challenge that the endeavour to redirect financial flows in line with sustainability goals clearly faces. After all, the sustainability impacts of investments are often hard to assess because they occur only in the long-term, are jointly produced together with a high number of other individual actions (and thus depend on the behaviour of others), or enfold through very indirect pathways. This is evidenced, for instance, by the challenges and controversies associated with measuring non-financial returns in impact investment (Reeder and Colantonio, Reference Reeder and Colantonio2013). Sustainable finance policies have to deal with financial markets in which highly complex financial instruments are traded that channel financial flows through complex pathways (Awrey, Reference Awrey2012). According to arguments in the literature on reflexive law, decision-makers in public institutions might, in these circumstances, find it challenging to access the information necessary to design adequate command-and-control regulations, develop well-functioning market-based governance measures, or directly decide on necessary investments.

Adapting to changing circumstances

Another advantage that is sometimes assigned to reflexive law policies, which is also partly related to epistemic issues, concerns their ability to deal with changing circumstances (Orts, Reference Orts1995b: 782; Scheuerman, Reference Scheuerman2001: 90–1). Individual market participants are taken to be more flexible in adapting their behaviour than regulators. For instance, a command-and-control regulation adopted at a certain point in time can become outdated if technology, knowledge, or societal needs change (Sinclair, Reference Sinclair1997: 542). Take a regulation that obliges firms to use a specific technology to reduce pollution. At some point, a more efficient technology might be developed that is able to meet the same goal, but firms are still obliged to use the outdated technical solution. Such regulations can also reduce incentives for firms to develop new technologies because they expect to remain obliged to use the prescribed technology (Stavins, Reference Stavins, Mäler and Vincent2003). It simply takes time to adapt regulations to such new circumstances. The need for adaptation first has to reach the agenda of the relevant regulators, new rules then have to be developed and go through the respective formal decision-making procedures before they come into force. In some circumstances, command-and-control regulations might thus be too static.

Market-based governance and direct public interventions in markets might do somewhat better in dealing with changing circumstances. If, for instance, creating pollution is associated with costs (due to environmental taxes or emission trading schemes), the choice of the most efficient technology is left to individual firms that might be able to react faster than regulators. However, market-based governance measures can also become inadequate due to changing circumstances. For instance, new scientific evidence on how certain impacts of economic activities affect environmental outcomes can create the need to adapt market-based governance schemes or create new ones. It then takes time to build up mechanisms to monitor and adequately price forms of pollution previously not paid attention to. Direct public intervention, such as public investments, could perhaps react relatively flexible to changing circumstances. However, also in this case, policymakers first need to become aware of the changes and take the decisions needed to adapt public interventions accordingly.

Again, is this potential advantage of reflexive law relevant in the area of sustainable finance? Governance measures in this area certainly face rapidly changing circumstances. For instance, market participants constantly develop new financial instruments (Awrey, Reference Awrey2012), technological innovations change production processes in the real economy, and new scientific evidence changes our knowledge about the sustainability impacts of certain economic activities. As in the case of complexity, the potential advantages of reflexive law policies in dealing with dynamic situations might thus be beneficial in the area of sustainable finance.

Shortcomings of the reflexive law approach in sustainable finance

The literature on reflexive law also describes shortcomings of this governance approach. Reflexive law confines itself to setting procedural and organisational norms. It thus leaves decision-making on substantive issues in the hand of individual private agents. The abstention of public institutions to make use of the option to set public rules on substantive matters (or take action themselves) implies leaving a lot of discretion in the hand of agents that usually have their own stake in the issue to be governed. Research on reflexive law emphasises that power asymmetries and vested interests affect the reflective processes that reflexive law policies aim to establish (Maus, Reference Maus1986; Scheuerman, Reference Scheuerman2001; Wen, Reference Wen2016). Along these lines, Wen states that ‘opponents have plausibly suggested that reflexive law in this form represents little more than handing over the crucial law-making functions to some of the most privileged interests in society’ (Wen, Reference Wen2016: 351–2).

As Braunig (Reference Braunig2005: 1532–3) finds in his study on regulations of factory farming pollution, if reflexive law policies mainly make new information accessible, their effectiveness depends on the incentives of the stakeholders to change their behaviour in response to this information. If the vested interests of relevant stakeholders are not aligned with the governance goals, reflexive law policies will fail. The worry is that the kind of steering that reflexive law policies provide is not strong enough to ensure just outcomes that reflect the interests of all affected parties. In a sense, a lower level of central steering is precisely what the reflexive law approach aims at. However, this also has downsides.

Sustainable finance policies that follow a reflexive law approach clearly intervene less in the decision-making of capital owners and financial market participants, such as banks and asset managers, than potential alternative governance approaches aimed at a redirection of capital flows. Mandatory sustainability disclosure, guidelines for the management of sustainability risks or regulations on how sustainability preferences need to be addressed in investment advice might be associated with additional bureaucratic efforts, but they do not directly change prices on financial markets or oblige anyone to refrain from investing in a certain project. In addition, capital owners and financial market participants have strong vested interests that do not necessarily align with the governance aims pursued. Taking a reflexive law approach in financial market governance thus carries the risk that these agents use their discretion in such a way that the redirection of capital flows does not take place in the way aimed for. The issue described can, first, hinder the collection and transmission of sustainability information from achieving the desired redirection of capital flows. The success of sustainable finance policies following a reflexive law approach might depend on other policies that alter the incentives of market participants.

Secondly, reflexive sustainable finance policies might not even succeed in creating a well-functioning epistemic infrastructure for sustainability information. Policies that leave financial market participants a great amount of discretion will arguably not lead to the collection and transmission of credible sustainability information. Policymakers have thus, in some cases, turned to policies that still follow a reflexive law approach but interfere to a larger extent in the decision-making of market participants. While such policies that set more concrete, detailed, and binding rules are less prone to the shortcomings of reflexive law, they also do not fully realise its alleged (epistemic) advantages. In these cases, it might thus be better to rely on conventional forms of public intervention – or at least to complement the reflexive law approach with such policies.

Lack of incentives to redirect capital flows

Let us start with the first potential failure. Even if the reflexive law approach manages to create a well-functioning epistemic infrastructure, it is anything but certain that the achieved transparency leads to the desired redirection of capital flows. If capital owners and financial market participants do not have sufficient incentives to shift to more sustainable projects, their knowledge about sustainability impacts will not lead to change. This point can be described even in the standard economics terminology of different kinds of market failures. Creating a well-functioning epistemic infrastructure solves issues related to imperfect information, such as adverse selection. But these kinds of market failures are not the only ones that are of relevance in relation to sustainability issues. Obviously, sustainability impacts usually include external effects. The environmental or social impacts of economic activities mainly affect other agents than the capital owners that finance the investments in these activities. A well-functioning epistemic infrastructure does not automatically lead to the internalisation of these external effects.Footnote 8

Procedural measures included in reflexive law policies can also aim at addressing externalities; for instance, by requiring the representation of groups affected by negative external effects in decision-making (Scheuerman, Reference Scheuerman2001: 86). However, the EU sustainable finance policies have so far not included such measures and have focused instead, as described, largely on the epistemic infrastructure of financial markets. In principle, the inclusion of representatives of organisations, such as environmental NGOs or workers’ unions, is feasible for the development of guidelines or regulations for sustainable financial products. However, it is hardly possible to ensure a representation of such groups in all investment decisions of capital owners. Ensuring that investors have incentives that are aligned with environmental and social goals is thus important for the success of sustainable finance policies.

This finding is in line with de Bruin’s (Reference De Bruin, Sandberg and Warenski2024) analysis of the reflexive law approach of the EU sustainable finance strategy. De Bruin argues, among other things, that the EU policies are unlikely to create a preference for sustainable investments among investors. He suggests that, to have a chance to change investor preferences, it is important to ‘provide different information, and [to] provide information differently’ than the EU policies demand (de Bruin, Reference De Bruin, Sandberg and Warenski2024: 164). For instance, providing information about climate-related events that make the climate catastrophe salient to investors might be more effective than the technical information the EU policies will generate. In addition, de Bruin proposes to provide information in an easily accessible way, using, for example, visual systems. Keeping in mind that the epistemic infrastructure created by the sustainable finance policies will mainly be used by highly specialised staff working at institutional investors and other financial market participants, some degree of technicality with respect to the information provided will probably be manageable for the intended addressees. Still, the way information is disclosed, made salient, and embedded with other knowledge is important.

In any case, the question remains on what grounds investors should be motivated to prefer sustainable investments. A first potential reason for investors to shift to sustainable projects might be grounded in moral considerations or societal expectations. It is certainly misleading to portray financial market actors as exclusively self-interested homines oeconomici that react only to financial incentives. Some capital owners might, for instance, prefer more sustainable investments from a moral perspective or react to a societal expectation to assume responsibility for the sustainability impacts of their investments.Footnote 9 Policies that follow a reflexive law approach can play a role in allowing investors to redirect their capital to sustainable activities due to moral reasons. As described earlier, Herzog (Reference Herzog2020) argues (with respect to markets in general) that a well-functioning epistemic infrastructure is a precondition for morally responsible agency of market participants. Creating this infrastructure might only allow investors to take moral responsibility for their investments.

To some extent, reflective processes, as they are triggered, for instance, by questions concerning sustainability preferences that providers of financial advice have to ask their clients in the EU, might also make moral issues and societal expectations more salient. However, the role of these policies in creating such incentives – and not only in being able to act on these incentives in case they exist – still appears to be rather limited. In general, empirical research raises doubts about the willingness of institutional investors, with their influential role in the financial markets, to change their investment decisions based on moral considerations (Christophers, Reference Christophers2019; Jansson and Biel, Reference Jansson and Biel2011).

Another motivation to redirect capital in response to sustainability information arises if sustainability risks are also considered to be financial risks. Economic activities with negative sustainability impacts can be associated with reputational risks for the respective company that can have financial ramifications (e.g., due to consumer boycotts). More importantly, sustainability risks can become financial risks due to policy changes. Tighter regulations of the real economy or higher carbon prices endanger the economic viability of unsustainable economic activities in the future (Semieniuk et al., Reference Semieniuk, Campiglio, Mercure, Volz and Edwards2021). Expectations of investors in this respect can be a motivation to prefer sustainable investments. Again, a well-functioning epistemic infrastructure will be necessary to allow market participants to manage these risks properly (e.g. by shifting to more sustainable investments) but it does not create these risks.

In addition, financial market policies aiming at sustainability goals are not necessarily restricted to altering the epistemic infrastructure and taking a reflexive law approach. In principle, financial market policies can also be used to put pressure on market participants to shift to sustainable investments. For instance, governments can implement credit guidance policies, such as targets for the share of credit going to green (or dirty) projects as introduced in Bangladesh (Kedward et al., Reference Kedward, Gabor and Ryan-Collins2024), use tax policy to make non-sustainable investments less profitable, or offer interest subsidised credits to companies investing in sustainable projects (Edenhofer et al., Reference Edenhofer, Klein, Lessmann and Wilkens2022).Footnote 10 Regulators can also ask market participants to develop transition plans that lay out how they will align their activities with sustainability goals (and ensure that they stick to these plans) (Dikau et al., Reference Dikau, Robins, Smoleńska, van ’t Klooster and Volz2022). In addition, financial market participants could be forced to change their managers’ remuneration schemes in such a way that managers are incentivised to take to the long-term perspective necessary to properly manage sustainability risks (Ameli et al., Reference Ameli, Drummond, Bisaro, Grubb and Chenet2020: 581).

These examples should illustrate that policies directed at the real economy or the financial sector (or, to some extent, also a change in prevailing moral norms and society’s expectation of investors) can create incentives for financial market participants to react appropriately to the knowledge about sustainability impacts that a well-functioning epistemic infrastructure would convey. However, in themselves sustainable finance policies that follow a reflexive law approach and are directed at the epistemic infrastructure hardly create such incentives. The success of this type of sustainable finance policy is thus dependent on other policies and societal changes.

This conclusion is in line with some existing literature contribution on sustainable finance. For instance, Ameli et al. (Reference Ameli, Drummond, Bisaro, Grubb and Chenet2020), based on a survey of institutional investors, find that transparency is not enough; for instance, because incentives for sustainable investments are lacking. Christophers (Reference Christophers2017) argues that currently it is not credible that non-sustainable investments are riskier. The experiences with reflexive law described in the (empirical) literature on this approach in other policy areas, thus provides additional plausibility to a point that has been raised in previous research on sustainable finance.

This is not to imply that sustainable finance policies that address the epistemic infrastructure of financial markets cannot have any impact on financial flows without additional policies that alter incentives. While the quantitative literature on the impact of the EU sustainable finance policies is still in its infancy, some studies find, for instance, a positive effect of the EU Sustainable Finance Disclosure Regulation (SFDR) on net inflows in funds reported as sustainable (Becker et al., Reference Becker, Martin and Walter2022) and a stock price premium for EU taxonomy-aligned assets (Bassen et al., Reference Bassen, Kordsachia, Lopatta and Tan2025). However, pointing in a somewhat different direction, Lucarelli et al. (Reference Lucarelli, Mazzoli, Rancan and Severini2023) find that the EU taxonomy does not per se increase the investment of firms belonging to taxonomy-eligible sectors. In any case, it is highly questionable that sustainable finance policies that address the epistemic infrastructure and take a reflexive law approach alone can achieve a redirection of capital flows at the enormous scale required.

More detailed and binding policies can lose their epistemic advantages

The tendency of reflexive law policies to leave agents with vested interests considerable discretion in decision-making might even impede these policies from achieving their immediate goal of creating a well-functioning epistemic infrastructure. Too much discretion for individual financial market participants can lead to higher transaction costs in the gathering and processing of information (Steuer and Tröger, Reference Steuer and Tröger2022). If, for instance, reflexive law policies only provide vague norms on what information has to be provided and in what form, market participants will use different definitions and criteria of sustainability and different formats of reporting. Vague and ambiguous disclosure regulations reduce the comparability of data and make it harder for other market participants to use the information in the desired way (Cardoni et al., Reference Cardoni, Kiseleva and Terzani2019). Sustainable finance policies sometimes also take the form of non-binding guidelines, which are not necessarily implemented by financial market participants.

Vague or non-binding rules make window dressing and greenwashing easier. If governance frameworks do not effectively prevent such practices, market participants might be tempted to use methods in calculating sustainability risks that downplay the risks of their investment portfolios or refer to less ambitious or even meaningless criteria in the design of sustainable financial products. Along these lines, Abouarab et al. (Reference Abouarab, Mishra and Wolfe2025) find evidence for greenwashing practices in environmental funds. These deceptive practices undermine the goal of redirecting capital flows because they make it more difficult for other market participants to distinguish between investment opportunities that are sustainable and those that are misleadingly advertised as such. The negative consequences of greenwashing on financial markets are confirmed by empirical research. For instance, greenwashing risks have been found to affect green bond pricing and thus increase the cost of capital of financial market actors that raise funds through green bonds (Baldi and Pandimiglio, Reference Baldi and Pandimiglio2022; Xu et al., Reference Xu, Lu and Tong2022).

Commercial pressures and conflicts of interests can reduce the chance that external agents (where they are involved) impede deceptive practices (Boiral et al., Reference Boiral, Heras-Saizarbitoria and Brotherton2019; Boiral et al., Reference Boiral, Heras-Saizarbitoria, Brotherton and Bernard2019). Providers of external assurance of sustainability disclosure documents, for instance, usually assess the sustainability information provided by companies from whom they get the payment for this service and often also provide consultancy services in the same sector or even for the same client, which can lead to conflicts of interest. These examples show that the discretion that sustainable finance policies that follow a reflexive law approach leave to financial market participants can in various ways be used to further the vested interests of these agents, which can impede a well-functioning epistemic infrastructure.

Not all sustainable finance policies that address the epistemic infrastructure of financial markets are equally prone to the risks associated with the large degree of autonomy that reflexive law leaves to private agents. The standards set by reflexive law policies can be more or less detailed and can interfere more or less with the decision-making of the agents whose behaviour they are supposed to govern. This does not mean that there is a spectrum between reflexive law policies and conventional approaches to public intervention in markets. Reflexive law policies that are more detailed and binding still focus on setting procedural and organisational norms and do not directly interfere with the substance of the decisions that private agents can take.

An example of a sustainable finance policy that sets comparatively concrete, detailed, and binding rules is the EU taxonomy. To determine whether an economic activity is aligned with the taxonomy, one has to assess whether it makes a substantial contribution to one of the environmental goals included, does no significant harm to the others, and meets social minimum safeguards. The taxonomy specifies for a high number of economic activities concrete screening criteria that need to be applied in the assessment of taxonomy-alignment.Footnote 11 An obligation to disclose on such a taxonomy constrains the discretion of private financial markets participants much more than, for instance, vague requirements to consider sustainability impacts in company reports.

It is plausible that more detailed and binding policies, such as the EU taxonomy, are more likely to be able to create a well-functioning epistemic infrastructure and prevent greenwashing. The more detailed and precise disclosure rules are, and the more thoroughly the accuracy of information provided is verified, the more comparable the data generated will be and the more difficult it will be for market participants to portray their activities or products as sustainable if they are in fact harming sustainability goals. In addition, organisational norms that are often part of reflexive law policies can be used to reduce conflicts of interests – as in the case of a planned EU regulation of sustainability rating agencies that prohibits these agencies to offer also consultancy services.

However, while more concrete, detailed, and binding reflexive law policies avoid some of the disadvantages often associated with the reflexive law approach, they also lose some of the advantages that are commonly ascribed to this approach. Let us consider again the example of the EU taxonomy. The taxonomy specifies for a high number of economic activities in a very detailed manner under what conditions they count as sustainable. Due to the degree of public intervention that such a taxonomy constitutes, Hans-Werner Sinn describes the EU taxonomy (and the EU green deal in general) as new ‘green dirigisme’ that is built on a ‘naive faith in the wisdom and honesty of central planners’ (Sinn, Reference Sinn2020; for a similar views, see also, Kooths, Reference Kooths2022). As investors are not obliged to invest in taxonomy-aligned projects and can, even if they wanted to do so, still invest in many different sectors and projects, these claims are greatly exaggerated. It is remarkable, though, that reflexive law policies, whose emergence was originally (at least partly) motivated by alleged epistemic advantages compared to conventional forms of more centralised public governance (Scheuerman, Reference Scheuerman2001: 83–4), are – in the field of sustainable finance – now ascribed a proximity to central planning.Footnote 12

As described, reflexive law policies are often seen as superior in complex situations because, for instance, regulators are not trusted to have the capabilities and knowledge necessary to make rules that are effective and efficient in such circumstances. But why should regulators then be able to develop an extremely detailed and comprehensive sustainable finance taxonomy that includes meaningful criteria of an adequate level of ambition? Such reflexive law policies apparently lose their epistemic advantages compared to other forms of public intervention. Similarly, if command-and-control regulations are not considered flexible enough to adapt to changing circumstances, why should sustainable finance taxonomies be more flexible?

In addition, the risk of having overly technocratic procedures with limited opportunities for democratic participation described above for decision-making on command-and-control regulations in complex circumstances applies also to more concrete and detailed reflexive law policies. Policies such as the EU taxonomy with its high number of rules and thresholds might be considered a form of juridification. To collect the necessary data, conduct taxonomy assessments, produce disclosure reports and get these reports verified is additional bureaucracy.

And indeed, the criteria for sustainable activities that the EU taxonomy specifies have in some cases been described as inadequate and the bureaucratic burden associated with taxonomy assessments is one of the main points of criticism of private actors. While such criticisms should be approached with caution due to the vested interests involved, it is worth noting that, for instance, several large German real economy enterprises and financial market participants argue in a report by the business network econsense that the criteria included in the EU taxonomy often do not refer to the most relevant sustainability issues associated with an economic activity or do not have an appropriate level of ambition (Arnold et al., 2023). The turn of sustainable finance policies to more concrete, detailed, and binding rules – which, to be clear, is necessary to make these policies effective in creating a well-functioning epistemic infrastructure – thus calls into question the advantages of the reflexive law approach compared to conventional forms of public intervention.

In this light, one might then ask why, for instance, direct public investments should not be given a stronger role (Golka et al., Reference Golka, Murau and Thie2024). If public institutions must define in a very detailed manner in sustainable finance taxonomies which economic activities private entities should invest in, why cannot they make these investments themselves? Sustainable finance policies give public institutions a considerable role in decision-making on the allocation of investments. However, unlike traditional Keynesian approaches, the EU sustainable finance approach does not assign governments the role of making these investments, but the investments should rather be made by private agents and mediated through financial markets. If reflexive law policies that are sufficiently detailed and binding to create a well-functioning epistemic infrastructure lose the alleged epistemic advantages of reflexive law, the merits of this approach are called into question.

Conclusion

This article analyses the governance approach of the EU sustainable finance policies in terms of the concepts of epistemic infrastructure and reflexive law. In contrast to command-and-control regulations, market-based governance mechanisms, and direct public investments, the EU sustainable finance policies mostly confine themselves to setting procedural and organisational norms. These norms aim at improving the epistemic infrastructure of financial markets – that is, the practices and institutions that collect and transmit information on financial markets.

While this article focuses on the EU, sustainable finance policies that address the epistemic infrastructure of financial markets and take a reflexive law approach have been popular in many jurisdictions. For instance, sustainability reporting regulations and sustainable finance taxonomies have seen a remarkable global diffusion (Cabrera et al., Reference Cabrera, Youngeun Shin and Hinojosa2022; Wen and Deltas, Reference Wen and Deltas2022: 103). However, sustainable finance policies vary substantially across jurisdictions. Policy makers in some countries are apparently more open than policymakers in the EU to introduce measures, such as subsidies for green credits and credit ceilings or quotas, that go beyond altering the epistemic infrastructure (Baer et al., Reference Baer, Campiglio and Deyris2021). While the findings of this article regarding the reflexive characteristics of EU sustainable finance policies are thus also relevant for many policies implemented in other jurisdictions, they might not apply to the whole policy package pursued.

Reflexive law policies that address the epistemic infrastructure of financial markets will only be successful if investors have incentives to shift investments in reaction to the additional information they gain. The success of sustainable finance policies is thus dependent on other measures that create these incentives. In this respect, the findings of the article are in line with existing literature that argues that creating transparency on the sustainability impacts of investment is insufficient (Ameli et al., Reference Ameli, Drummond, Bisaro, Grubb and Chenet2020; Christophers, Reference Christophers2017; Kedward et al., Reference Kedward, Gabor and Ryan-Collins2024).

In addition, the article makes the original argument that there is an unfavourable trade-off between the level of detail and binding nature of policies and their capacity to harness the benefits of reflexive law. To achieve a well-functioning epistemic infrastructure, sustainable finance policies need to be sufficiently concrete, detailed, and binding. Otherwise, a lack of data comparability and deceptive practices like greenwashing will hamper the functioning of this infrastructure. However, the more detailed and binding type of sustainable finance policies loses to some extent the alleged (epistemic) advantages of reflexive law policies. For instance, if policy makers are not trusted to have the capacities and information to design well-functioning command-and-control regulations, why should they be able to develop extremely complex sustainable finance taxonomies? Furthermore, the amount of bureaucratic effort associated with such sustainable finance policies will hardly be less than would be associated with alternative governance approaches. If the advantages of the reflexive law approach cannot be fully realised in the area of sustainable finance, this might speak in favour of giving a greater role to other approaches, such as public investments or command-and-control regulations.

However, the fact that the sustainable finance policies pursued by the EU so far have limitations, and that their success depends on other policies, does not justify abandoning them, as some have called for during the current backlash against sustainability issues in the US and the EU. First, as mentioned before, a well-functioning epistemic infrastructure can be a prerequisite for policies that do not follow a reflexive law approach. For instance, to implement credit targets for green projects, a common definition of ‘green’ is necessary and procedures need to be in place that ensure that projects that are classified as such indeed meet this definition. Similarly, if public development banks want to make their portfolios more sustainable, they also have to rely on an epistemic infrastructure to get access to the relevant information.

Secondly, a well-functioning epistemic infrastructure in financial markets that collects and transmits sustainability information is important to reduce systemic risks in the financial sector. It is one of the stated objectives of the EU sustainable finance strategy to achieve a better management of sustainability-related financial risks. In addition, sustainable finance can serve the function of pulling the impact of future policies forward into the present because, if investors see credible steps in the direction of, for instance, high carbon prices, these future changes will affect their investment decisions today.

Sustainable finance policies that take a reflexive law approach and address the epistemic infrastructure of financial markets are thus – despite their disadvantages and limitations – an important component of the comprehensive and far-reaching policy mix that is needed to transform economies. However, the idea implicit in the policymaking approach of the EU and other agents in sustainable finance, that only small changes in the epistemic infrastructure of financial markets are necessary to achieve far-reaching transformational change in the real economy, is highly unrealistic.

Acknowledgements

I am very grateful to Eike Düvel and Christoph Sommer, as well as the reviewers and editors of Finance and Society for highly valuable comments on earlier versions of this article.

Funding statement

This research was financially supported by the German Federal Ministry for Economic Cooperation and Development (BMZ).

Open access

Open access