Key messages

Chapter 3.6 addresses how payment mechanisms can foster value for money and quality in long-term care (LTC). As populations continue to age with multimorbidity and the supply of informal care declines, expenditures in LTC are expected to increase significantly. However, better value for money can be achieved in LTC. Resource allocation mechanisms for LTC and payments to providers are distinct from those for health care for a number of reasons. Key learning includes that:

LTC is particularly prone to poor quality or inadequate care, under provision, overmedicalization and to delivery in suboptimal settings.

The challenges for LTC reflect its differences from health care markets, including that:

○ In health care the focus is on improving health whereas, once an individual needs LTC, that need for care is permanent and the emphasis shifts to maintaining quality of life;

○ LTC is often provided by low-paid or informal (often unpaid) caregivers rather than highly-trained professionals;

○ LTC markets are generally fragmented, with a multitude of funding sources and payers involved;

○ Collecting data on LTC quality, defining indicators and setting targets are difficult and make value-based payments particularly challenging.

Payments for formal LTC provision should be adjusted based on risk and inevitable cost variation between patients, and then combined with other payment types that incentivize additional aspects, including quality of care and cost containment.

Informal caregivers may be compensated either with cash or nonmonetary benefits. Although these do not normally cover the full costs of providing care, they acknowledge carers’ contributions and to some extent address issues such as working hours lost.

Introduction

LTC is required by patients who are dependent on others on a daily basis because they are limited in the activities they can undertake for themselves. Since dependency on and demand for LTC are mainly associated with age and its concomitant comorbidities, the growing numbers of people living longer ensure that the demand for LTC will continue to increase. In 2018, about 25% of individuals aged more than 65 years in Organisation for Economic Co-operation and Development (OECD) countries had at least one limitation in instrumental activities of daily living (IADL), i.e. those activities that enable a person to live independently, such as shopping, laundry, cooking, the ability not to put oneself at risk by getting lost, and turning off electric appliances. Another 17% were limited in at least one of the activities of daily living (ADL), such as eating, washing and going to the toilet. An average of 11% of the OECD population aged more than 65 years received LTC in 2019, of whom 68% received LTC in the community, at home,Footnote 1 even though institutional care represented about 50% of LTC expenditures (OECD, 2021) (see Chapter 2.5).

Community care is provided by low skilled caregivers (meaning untrained or with lower level qualifications), predominantly informally by family members – most of them women. In formal LTC the gender of the caregiver often depends on that of the beneficiary. Since most beneficiaries are women, so too are their formal caregivers. Countries vary in scope of formal LTC, but it is estimated that just 10% to 30% of LTC caregivers in OECD countries are formal, i.e. paid workers (Colombo et al., Reference Colombo2011). Changes in family composition – for example, as a result of lower fertility rates – are projected to reduce the availability of informal caregivers (Brimblecombe et al., Reference Brimblecombe2018; Gragnolati et al., Reference Gragnolati and Gragnolati2011). Formal caregivers often work part time, are low-paid, low skilled (with lower level qualifications) and have a high turnover (see Chapter 2.5 for more on the differences between formal and informal LTC workers). Formal LTC is typically seen as a rather unattractive profession due to factors such as low pay or difficult working conditions, and supply has been constantly decreasing. Therefore, in many high-income countries (HICs), the LTC workforce relies particularly on immigrants. Even when wage increases are implemented in an attempt to retain the formal LTC workforce, results are modest (OECD, 2020b).

The limited supply of both formal and informal care, along with the growing demand for LTC, results in increases in total expenditures on LTC (Cravo Oliveira Hashiguchi & Llena-Nozal, Reference Cravo Oliveira Hashiguchi and Llena-Nozal2020). Per capita expenditures are projected to rise even further (Bakx, Reference Bakx2015). LTC financial pressures on families and the state require LTC systems to improve their efficiency by mitigating market failures. Payment mechanisms are one of the tools available to achieve this (Charlesworth, Or & Spencelayh, Reference Charlesworth, Or, Spencelayh, Cylus, Papanicolas and Smith2016), and this chapter presents our analysis of how best to deploy them.

First, we outline the conceptual framework for our analysis on the flow of LTC funds across the agencies. We then step outside it to argue caution: payment mechanisms cannot always be used in the same way in LTC markets as in those for health care, and we highlight the ways in which the LTC providers, markets and failures are different. Next, returning to our framework, we look first at the pooling and allocation of funds for LTC, and then at the payment methods used to purchase LTC services and the different incentives the various methods create. Finally, we draw conclusions and make suggestions for policy.

Our framework: conceptualizing LTC and financial flows

In this section we set out the terms and concepts on which our analysis relies and the framework within which we conduct it (Fig. 3.6.1). We define the services which make up LTC (personal and social, in kind or in cash), the settings in which the care takes place (community/at home, or institutional) and the workers who provide the care (formal or informal, skilled or unskilled).

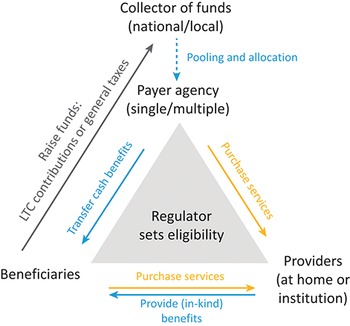

Framework to analyse financial flows in LTC and payments for providers

LTC: long-term care.

Figure 3.6.1 Long description

At the centre is a triangle that reads: Regulator sets eligibility. At the top is Payer agency (single or multiple). This entity will be the Collector of funds (national or local) through Pooling and allocation. The Payer agency Transfers cash benefits to Beneficiaries, and Purchase services from Providers (at home or institution). Beneficiaries purchase services from Providers, who then provide (in-kind) benefits to the Beneficiaries. Beneficiaries also Raise funds: L T C contributions or general taxes, which go to the Collector of funds.

The arrows shown in Fig. 3.6.1 represent the flow of funds which is central to our analysis. Within the framework, public LTC systems collect funds either nationally or locally (grey arrow “Raise funds: LTC contributions or general taxes”; see also Chapter 2.5). In systems with multiple payer agencies, the collected funds may be pooled and allocated to the payer agencies (e.g. local governments, health plans, ministries or national insurance systems; see the vertical blue dotted arrow “Pooling and allocation”). In systems with a single payer, funds are not allocated, therefore the arrow is dotted. Ideally, funds are allocated based on predicted risks or costs of the beneficiaries under responsibility of the payers, through a risk-adjustment/allocation formula. Payer agencies subsequently purchase LTC services on behalf of their beneficiaries by paying LTC providers (yellow arrow on the right hand side “Purchase services”). Alternatively, agencies can also “pay” beneficiaries directly with cash benefits (blue arrow “Transfer cash benefits”), giving them the option to use this money as they wish; for example, to pay for formal home care. Private funding exists in all LTC systems, and users often pay for LTC either entirely through out-of-pocket payments or partially, via user charges (yellow arrow at the bottom of the triangle). Voluntary LTC insurance plays a modest role in funding LTC in most countries due to many market failures (Brown & Finkelstein, Reference Brown and Finkelstein2007), and thus we do not analyse this source of funding in this chapter.

LTC: its services

LTC comprises a range of services aimed at slowing down and managing the decline in functional capacity among beneficiaries with a high degree of long-term dependency (Colombo et al., Reference Colombo2011; OECD, 2018). LTC services are provided to dependent people, such as older adults (aged more than 65 years) or people with physical or mental disabilities suffering from chronic conditions with functional or cognitive limitations over an extended period.Footnote 2 LTC services cover various forms of care. In this chapter, we include: (i) personal care and help with ADL, such as eating, bathing and toileting; and (ii) social care, which deals with assistance services that enable a person to live independently and help them with IADL, such as shopping, laundry, cooking, not putting oneself at risk (e.g. getting lost), or forgetting to turn off an electric device (Gori, Fernandez & Wittenberg, Reference Gori, Fernandez and Wittenberg2016; OECD, 2018). We include cash benefits to buy the aforementioned services (i.e. monetary benefits for people needing ADL and/or IADL), as these payments are taken as a proxy for a paid transaction. However, we exclude medical or nursing LTC, such as wound dressing, administering medication, health counselling, palliative care, pain relief and medical diagnosis with relation to a long-term condition, as this type of service is usually funded by health systems.

LTC: its settings and caregivers

The severity of beneficiaries’ dependency determines not only the type and number of hours and services, but also the setting where LTC is provided.

Community care

LTC is predominantly provided at home – referred to as community or home care in this chapter – by low skilled caregivers, whether paid workers (formal care) or family members (informal care). While the number of care hours are determined by the level of dependency (Colombo et al., Reference Colombo2011).

Institutional care

If LTC beneficiaries’ functional capacity continues to deteriorate, they may be treated in institutions with permanent nursing staff and rehabilitation-allied health professionals, such as LTC nursing homes, geriatric wards in care homes, or separate geriatric institutions (Cafagna et al., Reference Cafagna2019; OECD, 2018). Our analysis takes account of two types of LTC institutions: day care centres and nursing/care homes.

Day care centres

In day care centres, beneficiaries receive several hours of care on a daily basis, particularly preventive care. The centres include nursing and rehabilitation services such as physiotherapy, occupational therapy and mental health support, provided by skilled and unskilled caregivers. These formal caregivers are part of community care although working in an institution (the day care centre), as beneficiaries live in their own homes.

Nursing/care homes

Recipients of care in nursing/care homes are those who require LTC due to physical or mental disability/dementia, but are not in need of complex medical care. Caregivers include skilled and unskilled caregivers (such as nurses and allied health professionals). Patients admitted to nursing homes for a short period following an acute-care hospitalization to recover before being able to return to their homes are excluded from this analysis. We also exclude geriatric/LTC wards in hospitals, because the care provided in these wards is medical and the costs are typically captured in health expenditure data. Sheltered housing is also absent in our analysis, as this type of institution is designed for independent residents. Residents of sheltered housing who receive help with ADL are considered community-based care beneficiaries and are mentioned under “community care”.

Such, then, are the conceptual underpinnings and context for our analysis of the use of payment mechanisms in LTC markets, but first we need to see why caution is needed, if thinking simply to replicate the way they function in health care markets.

How LTC markets differ from health care markets

In health care markets, policy-makers use payment mechanisms as a tool at their disposal to influence providers’ behaviour and decision-making through the economic incentives created. The ultimate objective of payment mechanisms is to compensate providers fairly for services rendered and promote efficiency: to achieve more with a given number of resources without undermining quality of care; or improve quality of care while controlling expenditures (Cylus, Papanicolas & Smith, Reference Cylus, Papanicolas and Smith2016a; Reference Cylus, Papanicolas and Smith2016b). Payment mechanisms can accomplish this by incentivizing the provision of the adequate number and types of services based on need, i.e. avoiding unnecessary treatment or selection of patients (Frank, Glazer & McGuire, Reference Frank, Glazer and McGuire2000; Geissler et al., Reference Geissler and Busse2011). Likewise, payment mechanisms could potentially be used in LTC markets to balance economic incentives related to provision of LTC in a way that promotes desired objectives such as equity in access and high-quality care. However, the payment mechanisms required for LTC are not necessarily the same as those for health care, given some crucial differences between the two markets in terms of the type of care needed and the workers providing it; levels of market fragmentation; questions concerning the quality of care; moral hazard and excess demands. Here, we outline these differences and, briefly, some of the payment mechanisms which relate to them. We go into more detail about the various mechanisms in the Payment methods and the incentives they create section.

LTC versus health care: type of care

While in health care the aim is to cure or improve a patient’s condition, in LTC it is about improving quality of life, where conditions are either longstanding or permanent (Bakx, Reference Bakx2015). There is also the question of the duration of an “episode of care” and the subsequent distributions of costs. Health costs are usually unpredicted and are very high for very few people, and the demand for care is usually not known in advance. For LTC, once an individual becomes disabled, costs are usually permanent and likely to increase gradually, though the duration of care varies. While only a small fraction of the population is responsible for most expenditures in health markets, funds in LTC are dispersed over a broader percentage of those aged more than 65 years (Berk & Monheit, Reference Berk and Monheit2001; Mitchell, Reference 512Mitchell2019; Zuvekas & Cohen, Reference Zuvekas and Cohen2007). In LTC it can be challenging to predict longer-term expenditures because it is difficult to foresee: (i) the probability of need (Costa-Font, Courbage & Swartz, Reference Costa-Font, Courbage and Swartz2015); (ii) the duration of care; and (iii) the future costs of the LTC services (Barr, Reference Barr2010). For LTC it is challenging to define a clear episode of care that can be costed and priced in advance. Thus, prospective, activity-based payments are difficult to apply, and diagnosis-related group (DRG) payments are rare in LTC (Cots et al., Reference Cots and Busse2011) (see Chapter 3.2 for more on DRGs).

LTC versus health care: type of provider

While health care is provided by highly skilled professionals, most LTC is provided by low-paid, low skilled (low or untrained) formal caregivers or informal (i.e. unpaid) caregivers (see Chapter 2.5). Informal caregivers typically face high opportunity costs in terms of time spent providing care and income lost due to reduced participation in the formal labour market, as well as a loss of personal time. To compensate informal caregivers, some countries offer incentives, such as tax exemptions, work leave days or other allowances. These have important impacts on caregivers’ well-being, income, willingness to provide LTC and the interplay between formal and informal care. However, the incentives given do not compensate for the full cost of care, and there is no formal contractual relation between provider/informal caregiver and the beneficiary. Implicit contracts are mainly based on altruism or exchange motivation that might be influenced by the level and availability of supply of formal care (Costa-Font, Jiménez-Martín & Vilaplana-Prieto, Reference 509Costa-Font, Jiménez-Martín and Vilaplana-Prieto2022). Controlling for or incentivizing quality of informal care remains a challenge (OECD, 2020b).

LTC versus health care: level of fragmentation

Compared to health care markets, LTC markets are highly fragmented, with various sources of funds coexisting, and many payer agencies responsible for the different settings and types of care (see Box 3.6.1). Inadequate (re)allocation of funds may create incentives for cost shifting by LTC payers, resulting in attempts to shift unattractive (i.e. labour-intensive or high-risk) beneficiaries and costs to other care settings or payers. Shifting beneficiaries to less optimal care settings is exacerbated when different payers are responsible for different types of care settings. In the Netherlands, for example, regional care offices pay for institutional and intensive home care (ADL), while community IADL care is paid for by local government. Since local government funds are not earmarked for LTC, those with greater budgetary pressures tend not to invest in preventive, less intensive care and instead have an incentive to shift beneficiaries to more intensive care settings paid for by the regional care offices (Alders & Schut, Reference Alders and Schut2021). Beneficiaries may not only forgo IADL care, which can result in increased dependency levels, but they might end up receiving unsuitable (more intensive) care. Shifting beneficiaries to more intensive care settings may thus increase expenditures without added benefit. The undertreatment of patients, and the accompanying increase in their levels of dependency, in order to move them to other care settings and payers, has also been reported in Italy, Spain (Arlotti & Aguilar-Hendrickson, Reference Arlotti2018) and Portugal (Lopes, Mateus & Hernández-Quevedo, Reference Lopes and Mateus2018).

Two payment mechanisms used to mitigate this type of cost shifting and to promote continuity of care are bundled payments and pay for performance (P4P) (see Chapter 3.1). In health care markets, their effects have been modest (Eckhardt et al., Reference Eckhardt and Busse2019). The experience with these payments for LTC is less extensive, and outcomes are even less pronounced. The ability to reduce excess demand or total expenditures in LTC is lower than in health care, when each care setting is funded by a different payer (Kattenberg & Bakx, Reference Kattenberg and Bakx2021). To mitigate cost shifting related to LTC’s fragmentation of payers, it would be more effective to combine policy tools such as merging budgets, integrating providers or integrating LTC within health payers, rather than rely on payments as a single solution (McClellan et al., Reference McClellan2017). Experiences from England and Sweden show that pooling budgets for health care and LTC for older adults reduced duplication and fragmentation of care, improved coordination of care and collaboration between the sectors. However, no clear evidence of an improvement of quality of care was found (Hultberg et al., Reference Hultberg2005). In addition, in the short term, there was no evidence of reduced costs. In the Pooling and allocation of funds section, we describe in more detail countries’ LTC payer agencies, and how pooled funds are redistributed among payers to improve equity in financing.

Due to historical development of LTC systems, countries often have multiple LTC programmes, correspondent to the care setting; for example, institutional versus community care, or type of benefit (in kind versus cash). The different settings or types of care may have different methods of collecting funds, different budgets, different payer agencies, different pooling and redistribution systems, and sometimes also provide care for different types of beneficiaries. For example, Austria has different systems for cash and in-kind benefits. For cash benefits, the central government is the single payer, while for in-kind benefits the local governments are the multiple payers. Funds for cash benefits are transferred directly from the payer agency (the central government) to the beneficiaries, while funds for in-kind benefits are pooled and redistributed to the payer agencies through an allocation formula, and subsequently provided to the beneficiaries (Schmidt, Waitzberg & Blümel, Reference Schmidt, Waitzberg and Blümel2021). Similarly, Czechia and Italy have different LTC systems for cash and in-kind benefits. Croatia, France, Poland and the Netherlands have different LTC systems for community and institutional care. The Netherlands also has different systems for community care based on type of care (one for ADL services, and another one for IADL) (Waitzberg et al., Reference Waitzberg2020b).

LTC versus health care: quality of care

Concerns about how to incentivize high-quality care is core to the design of payments for LTC providers (Barber et al., Reference Barber2021), while those paying for health care are balancing a greater range of payment objectives (see chapters 3.1 and 3.2). In the context of LTC, poor quality care by formal (paid) providers may exist in the form of neglect, overmedicalization or provision of services in the wrong setting; for example, not providing enough hours of care at home or treating a non-severely disabled person in a nursing home (National Academies of Sciences, Engineering, and Medicine, 2022). In addition to P4P and bundled payments, already mentioned, pay for coordination, pay for quality (P4Q) and shared-savings models have also been implemented to promote quality of care with mixed results, and without evidence for positive effects in the long run (Wieczorek et al., Reference Wieczorek2022). One of the main challenges of applying value-based payments is the difficulty in defining, measuring and collecting data on quality in LTC. It is also clear that payments and their impacts are context specific, and financial incentives should be developed and tailored to each local setting (Struckmann et al., Reference Struckmann2017).

Overmedicalization is more common in nursing homes than in home care, and is a further instance of service distortion, as institutionalized beneficiaries of LTC consume more or inappropriate medication, particularly opioids and psychiatric drugs, compared to those non-institutionalized (Fog et al., Reference 510Fog2017; García-Gollarte et al., 2014; Jensen-Dahm et al., Reference Jensen-Dahm2015). Keeping beneficiaries at home might reduce the phenomenon of overmedicalization, as it is less prevalent in this setting. One way to ensure more beneficiaries are cared for at home may be to set higher or more accessible benefits for home care than for institutional care.

LTC versus health care: moral hazard and excess demand

In health economics, moral hazard is a phenomenon where, in theory, patients consume more services or technologies because they are insured and do not see real prices (see Chapter 2.4) (Stone, Reference Stone2011; van de Ven & Ellis, Reference van de Ven, Ellis, Newhouse and Cuyler2000); but in LTC this is different since beneficiaries are not typically insured and much of their care is unremunerated. Yet, moral hazard can still occur in LTC when publicly paid-for beneficiaries create an excess demand for: (i) LTC at an earlier stage of disability; (ii) more hours of care than needed; or (iii) more costly services, such as nursing homes (without real need), or replacing informal care with formal care too soon, thus potentially increasing public expenditures (Bakx et al., Reference Bakx2015a; Konetzka, Reference Konetzka2006).

Countries typically reduce the risk of this market failure by imposing cost-sharing or limiting eligibility for benefits, but this raises risk of creating barriers to accessing basic LTC (Bakx et al., Reference Bakx2015a). A better strategy to mitigate excess demand is setting clear eligibility criteria at the national level, based on need (Bakx, Douven & Schut, Reference Bakx, Douven and Schut2021; Waitzberg et al., Reference Waitzberg2020b). For example, the Netherlands publicly funds both home care and nursing home care in similar scope. Beneficiaries are allocated to the setting (home or nursing home) and intensity of care (number of hours) with clear eligibility criteria based on level of need. There is little room for choice of care setting, and thus for preferring institutional care over home care (Bakx et al., Reference Bakx, Douven and Schut2020). In Spain too, needs tests based on severity of IADL and ADL limitation allocate beneficiaries into one of four tiers of care, leaving little room for excess demand (Costa-Font, Jiménez-Martín & Vilaplana-Prieto, Reference 509Costa-Font, Jiménez-Martín and Vilaplana-Prieto2022). Eligibility should be frequently reassessed with needs tests, to allocate patients to the proper care setting. Box 3.6.2 contains a summary of LTC market failures and policy options.

1. Difficulty in defining and costing a clear “episode of care”: once an individual becomes disabled, costs are permanent and likely to increase gradually, though the duration of care varies. DRG payments are infrequent.

2. Most care is provided by informal (unpaid) workers, who face high opportunity costs. Rather than formal contracts, there are implicit contracts based on altruism, which can pose difficulties in controlling or incentivizing quality of care.

3. LTC markets are highly fragmented, with multiple sources of funds coexisting and many payer agencies each responsible for the different settings and types of care. Risk selection by LTC payers can occur when they face incentives to shift unattractive (i.e. labour-intensive or high-risk) beneficiaries and costs to other care settings and payers. Beneficiaries may receive unsuitable care. By bundling sources of funds, payers and budgets may mitigate this inefficiency. In addition, funds should be pooled at the central level, and distributed among payers according to needs-based allocation formulae.

4. Quality of care and service distortion are key concerns. Over- and underprovision of care may exist in the form of neglect, overmedicalization or provision of services in the wrong setting. For formal (paid) providers, P4P payments may promote quality, yet evidence on their effectiveness remains limited and inconclusive.

5. Moral hazard (or excess demand) can occur when demand rises for LTC in an earlier disability stage, more hours of care than needed, or more costly services, such as nursing home care without real need. Cost-sharing is a suboptimal option to mitigate excess demand, but a better alternative is setting need-based eligibility criteria, frequently reassessed.

Pooling and allocation of LTC funds

Returning now to the framework set out in Fig. 3.6.1, in this section we look at the actions and processes represented by the horizontal arrow at the top of the triangle. First, we describe the “who” of pooling and allocation – the collectors and the payer agencies, and then move on to “how” – the process of and criteria for allocating LTC funds.

Collectors and payer agencies

Payer agencies receive public LTC funds from national or local collectors of funds and commission or purchase LTC services from providers on behalf of beneficiaries (Busse, Schreyögg & Stargadt, Reference Busse, Schreyögg and Stargardt2017). Alternatively, payer agencies provide cash benefits to beneficiaries (see Fig. 3.6.1). In countries with multiple payers, payer agencies can be either local governments or health/LTC insurance plans, while countries with a single payer task the central government itself or another agency (such as a national insurance institute) as the payer agency. As such, in single-payer systems, the agency that collects funds, usually the central government, is also the payer agency since it purchases services from providers and/or transfers cash benefits to beneficiaries directly. Such agencies thus have an important role in purchasing LTC services and ensuring their supply for those in need, according to eligibility, in an equal and efficient way (Thomson, Foubister & Mossialos, Reference Thomson, Foubister and Mossialos2009). Frequently, countries have different payers for the different LTC settings, i.e. a payer responsible for institutional care, and another payer for community care (as described in Box 3.6.1).

Collectors – mostly single, sometime multiple

In many countries, LTC funds are collected by the central government, or a combination of the central government with subnational (regional or local) governments. When funds are collected by multiple agencies, such as regional or local governments, they are usually pooled at the central level, and redistributed to the payer agencies. Canada and Germany are exceptions in the sense that most of the funds are collected in a decentralized manner and are not pooled and redistributed. In Germany, the LTC plans associated with the specific sickness funds collect contributions from their members, yet funds are pooled and redistributed ex post according to the de facto expenses of each sickness fund. In Canada, each province or territory has its own LTC system, and roughly 75% of the funds are collected by the provinces and territories, which are also the payer agencies. The other 25% comes from federal transfers to the provinces and territories to fund their health care systems. These funds are not earmarked and are not pooled or redistributed across provinces and territories (Waitzberg et al., Reference Waitzberg2020b).

How are allocation decisions made?

Similar to mechanisms for allocating pooled funds to health care payers, allocation mechanisms for LTC should be based on predicted need of LTC, through a risk-adjusted capitation formula to ensure equity in financing (van de Ven & Ellis, Reference van de Ven, Ellis, Newhouse and Cuyler2000). Yet, contrary to health care, in LTC, multiple payer agencies are each responsible for different care settings, and may receive funds from different sources, and through different allocation mechanisms. LTC funds can be allocated to multiple payer agencies based on government decisions, automatic updates of past budgets or past use, or the predicted needs of the population they serve calculated via a risk/needs-based allocation formula. The more the distribution of funds is done based on objective and transparent criteria that reflect LTC needs, the higher the equity of funding. However, it is important to note that distribution of funds according to a needs-based formula alone does not ensure equity of distribution to a certain population if each region or payer agency commissions a different set of services for populations with the same need, or does so according to different eligibility criteria. Therefore, eligibility criteria should be set at the national level (Waitzberg et.al, Reference Waitzberg2020b).

In systems with single-payer agencies, funds do not need to be pooled and allocated. This is the case in Israel, where the National Insurance Institute is a single collector of funds and is a single payer for home-based LTC public provision (Asiskovitch, Reference Asiskovitch2013).

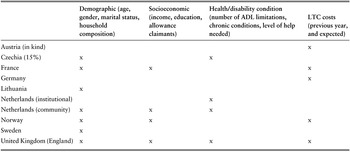

In a study that analysed 25 LTC systems in 17 countries, only seven systems had a single payer, with the central government also functioning as the payer agency (Austria, Czechia and Italy for cash benefits; Croatia and Cyprus for institutional and community care; and Israel, as mentioned in the previous paragraph). Out of the remaining 18 systems, eight distributed funds according to past budgets, government decisions or a general needs formula for public services (Waitzberg et al., Reference Waitzberg2020b). The other 10 countries did so based on a specific risk/needs-based formula for LTC, including Austria (for in-kind benefits), Czechia (for 15% of its budget), England, France, Germany, Lithuania, the Netherlands (for institutional care and community intensive ADL care), Norway, Portugal and Sweden (Table 3.6.1). Norway and Sweden applied demographic risk adjusters such as marital status to consider the existence of alternative informal care. They also used information about spoken language and residence in sparsely populated areas to reflect special caregiver needs. A few countries considered further risk adjusters such as disability, dependency level or chronic diseases (England, the Netherlands) and/or previous years’ expenditures (Austria, France, Norway). France further considered socioeconomic risk adjusters such as the number of allowance claimants and income of older people in the area overseen by the respective local authority. In England up to 2020, needs-based allocation formulae accounted for differences in wages across areas and to recognize differences in costs driven by factors outside the control of payers (local authorities) and providers.

Table 3.6.1 Long description

The table has 4 main columns: Demographic (age, gender, marital status, household composition), Socioeconomic (income, education, allowance claimants), Health or disability condition (number of A D L limitations, chronic conditions, level of help needed), and L T C costs (previous year, and expected). A cross is marked against the countries under the columns where applicable. It reads as follows. Austria (in kind): L T C costs. Czechia (15 percent): Demographic; Health or disability condition. France: Demographic; Socioeconomic. Germany: L T C costs. Lithuania: Demographic. Netherlands (institutional): Health or disability condition. Netherlands (community): Demographic; Socioeconomic; Health or disability condition. Norway: Demographic; Socioeconomic; L T C costs. Sweden: Demographic. United Kingdom (England): Demographic; Socioeconomic; Health or disability condition; L T C costs.

ADL: activities of daily living; LTC: long-term care.

Compared to allocation formulae for health care, those used for LTC are simpler (Bryndová, Hroboň & Tulejová, Reference Bryndová, Hroboň and Tulejová2019; Cylus et al., Reference Cylus2018; van de Ven et al., Reference van de Ven2007). Maybe, due to the nature of LTC markets, where age and other demographic characteristics are strong predictors of need, these adjusters are good enough to allocate funds in an equitable manner. Future studies could test this hypothesis. LTC funds could also be adjusted retrospectively to account for unpredicted expenditures. That is even more important for LTC than for health care, because LTC is a social service and, as already discussed, can be challenging to insure.

With the funds now allocated to the payer agencies, we turn to the downward yellow arrow on the right hand side of the triangle in Fig. 3.6.1: the purchase of services from the providers of LTC – in particular, the payment methods used and their associated incentives.

Payment methods and the incentives they create

As already shown, different payment mechanisms can incentivize the provision of LTC in different ways. Broadly speaking, payments that vary according to activity and that are retrospective, fine and narrow, such as fee for service (FFS), create incentives to increase productivity (i.e. the number of services or patients) and reduce the costs per unit of care. Prospective payments that are coarse, broad and fixed, such as budgets, salaries and capitation, can also create incentives to reduce the cost per unit (Ellis, Martins & Miller, Reference Ellis, Martins, Miller and Quah2017; Ellis & McGuire, Reference Ellis and McGuire1996; Jegers et al., Reference Jegers2002; Newhouse, Reference Newhouse1996; OECD, 2016; Quinn, Reference Quinn2015). Per diem and activity-based payments such as DRGs may create different incentives depending on the context. The challenge for policy-makers is to balance trade-offs between incentives to increase productivity and control expenditures and manage the different risks of unintended consequences that these incentives pose (e.g. overprovision of care, risk selection of beneficiaries, underprovision of care, provision of unsuitable care) (Chaix-Couturier et al., Reference Chaix-Couturier2000; Geruso & Mcguire, Reference Geruso and Mcguire2014; van Barneveld et al., Reference van Barneveld2001). Selection may occur if LTC providers prefer less labour-intensive beneficiaries and attempt to shift unattractive beneficiaries to other providers or other care settings. As in health care markets, prospective payments that incentivize cost containment (such as budgets, salaries, capitations and sometimes per diem) may aggravate this inefficiency. Cost containment may also undermine the supply of LTC beds in institutions or supply of formal workers.

One strategy to achieve this balance in economic incentives is to apply risk-sharing mechanisms that combine types of payments to distribute the risks of unpredictable costs between payers and providers in different ways (Newhouse, Reference Newhouse1996; Quentin et al., Reference Quentin2018). This is done by combining payments with different characteristics, also called “add-on payments”. For example, in the health care market, providers are paid with a blend of prospective and retrospective payments, such as budgets or capitations combined with FFS, or salaries combined with FFS or P4P (Brammli-Greenberg, Glazer & Waitzberg, Reference Brammli-Greenberg, Glazer and Waitzberg2019; Quentin et al., Reference Quentin2018). Another strategy employed in health markets to balance incentives is to include other mechanisms of risk offset, such as the addition of risk adjusters into capitation formulae or including case mix in payment mechanisms (van de Ven & Ellis, Reference van de Ven, Ellis, Newhouse and Cuyler2000). For example, DRG-based payments adjust the tariff of episodes of care by accounting for case mix, comorbidity and severity of case (Street et al., Reference Street and Busse2011).

In LTC, adjusting payments based on risk is particularly necessary (and common) in countries where prices are set unilaterally or negotiated collectively, as providers do not set their own prices based on their own costs. Risk-adjusted prices avoid underpricing and mitigate incentives for providers to skimp or reduce quality of care (Barber et al., Reference Barber2021). Prices are commonly adjusted based on geographical location, the degree of dependency of beneficiaries and the type and setting of services. These adjustments recognize the legitimate and unavoidable cost differences among providers. For example, in Australia, the Netherlands and the USA, geographical price adjustments are made for facilities in rural areas, while Japan uses increased tariffs in the metropolitan Tokyo area to account for higher wages and higher costs of living. Adjustments for specific conditions that require more intense labour are done for beneficiaries with dementia (Australia) or Huntington’s disease (Netherlands). Finally, some adjustments are done to incentivize provision of care to specific populations, such as for indigenous communities in Australia (Barber et al., Reference Barber2021).

In what follows below we describe the most common methods to pay LTC providers and what is known about the economic incentives the different methods create. We consider institutional care separately from community care because of the differences in type and duration of care, caregivers and cost.

Payments to institutional care (nursing or care homes)

In nursing homes, beneficiaries may receive some specialized services, such as pain and psychiatric medications, rehabilitation and other allied health services (physiotherapy, speech and occupational therapy, diet and pharmacy counselling), and receive accommodation services for each overnight stay. Like hospitals (see chapter 3.2, for more on paying for hospitals), nursing homes have fixed costs such as infrastructure and personnel and, to a lesser extent, variable costs, such as consumables and payments to independent professionals. Variable costs in nursing homes, however, are proportionally small compared to hospitals, making it easier to work out a daily LTC tariff (per diem).

Payment method 1: per diem

Most care homes are paid by day of stay (per diem), complemented by FFS schemes (Table 3.6.2), with some countries setting global budgets (Barber et al., Reference Barber2021). Such payments are often negotiated prospectively or based on a prefixed share of high-need users (Colombo et al., Reference Colombo2011). Examples of public LTC systems that pay care homes on a per diem basis are France (Le Bihan, Reference Le Bihan2018), Greece and Estonia (European Commission, 2019), and Sweden and Spain (Barber et al., Reference Barber2021). Day care institutions are also commonly paid per diem (Box 3.6.3).

| Type of payment | Nursing/care homes |

|---|---|

| Fee for service | Australia, Bulgaria, China, Czechia, Germany, Japan, Lithuania |

| Per diem | Australia, Estonia, Germany, Greece, Netherlands, Korea, Portugal, Spain, Sweden |

| Case mix-adjusted per diem | Canada, Italy, Switzerland, USA (Medicare) |

| Flat capitation | Argentina, Uruguay |

| Risk-adjusted capitation | France, Chile |

| Budgets | Czechia, Netherlands |

| Pay for performance | Germany |

Although day care is considered to be community care, the framework to analyse payments to and incentives for day care facilities is similar to that used for nursing homes, because unskilled care is provided along with some skilled care – mainly by allied health professionals. Prices for such services are often freely set by providers. Day care is also paid predominantly via the per diem system, in many countries adjusted to the severity of cases; for example, in France and Spain (Barber et al., Reference Barber2021). In Italy, per diem payments are adjusted by diagnosis, and are higher for Alzheimer centres (Hohnerlein, Reference Hohnerlein, Becker and Reinhard2018).

The USA’s experience with Medicaid’s per diem rates showed that the system incentivized nursing homes to contain costs by decreasing levels of staffing and preferring less labour-intensive beneficiaries. Adjusting per diem rates to case mix reduced these perverse incentives both in the USA and Canada (Norton, Reference Norton, Pigott and Woodland2016; Wilkinson et al., Reference Wilkinson2019). Since 2019, Medicaid sorts LTC beneficiaries in nursing homes into a patient-driven payment model based on the type of services they need: physical therapy, occupational therapy, speech–language pathology, non-therapy ancillary and nursing. Each resident is classified into one group of services, and per diem rates are adjusted accordingly (Barber, Lorenzoni & Ong, Reference Barber and Ong2019). Early evidence shows that this patient-driven payment model may have resulted in a reduction in therapy staff levels and services (National Academies of Sciences, Engineering, and Medicine, 2022). Switzerland also has LTC needs-adjusted per diem payment structures for nursing homes (Bischofberger & Landolt, Reference Bischofberger, Landolt, Becker and Reinhard2018).

Per diem rates can also be adjusted based on the facility’s features or costs (up to a ceiling). However, this blurs the economic incentives of cost containment as rates can be adjusted for increased costs. For example, Portugal has four types of nursing homes to account for different care needs, and each type is paid with a different per diem tariff (Lopes, Mateus & Hernández-Quevedo, Reference Lopes and Mateus2018).

Alternatively, per diem payments can be combined with payments that create incentives to increase productivity (FFS) or quality (P4P/P4Q). Germany has chosen to balance the economic incentives of payments to nursing homes by combining per diem payments with FFS if additional services are provided, such as allied health care, and P4P for rehabilitation services (Blümel et al., Reference Blümel2020). These add-ons may promote prevention of deterioration of patients’ functioning. These add-on retrospective payments need to be accompanied by a proof of the service provided, to avoid fraud.

As in health markets, flat per diem payments create incentives for LTC providers to contain costs, which can result in underprovision of care, neglect or the selection of lower-need beneficiaries. To mitigate these perverse incentives and promote proper and high-quality care, countries commonly adjust per diem rates to account for the variable costs of beneficiaries. For example, per diem rates are adjusted by the risks of beneficiaries in the USA and Canada (Colombo et al., Reference Colombo2011) or, as in Portugal, according to the case mix of the institution, measured by the levels set by the eligibility criteria to qualify for public funding (Barber, Lorenzoni & Ong, Reference Barber and Ong2019). Adjusting per diem rates for case mix mitigates the incentives for care providers to select beneficiaries, without significantly negating incentives for cost containment. This, though, comes at the risk of reducing incentives to prevent health deterioration: the more severe the case, the higher the payment (Wunderlich & Kohler, Reference Wunderlich, Kohler, Wunderlich and Kohler2001).

Payment method 2: FFS

FFS payments create incentives to increase productivity, which creates a risk of overprovision. This type of payment is therefore usually capped and combined with other payment methods. For example, Czechia pays nursing homes primarily via budgets to cover the operational costs, combined with FFS for certain services; the FFS component is capped to mitigate incentives for overprovision of care (Koldinská & Štefko, Reference Koldinská, Štefko, Becker and Reinhard2018). Australia, Germany and Japan combine their per diem schemes with FFS to incentivize nursing homes to provide appropriate care (Barber, Lorenzoni & Ong, Reference Barber and Ong2019). Denmark’s main payment method for institutional care settings is FFS (WHO Regional Office for Europe, 2019), which may partially explain why Denmark spent almost twice the European Union average on LTC in 2016. Lithuania and Bulgaria pay FFS for additional medical services in nursing homes (Barber et al., Reference Barber2021; OECD, 2020a).

Payment method 3: capitation

Capitation bundles the payment for all services projected for each beneficiary during a period, usually one year. However, this payment is not very frequently applied, as it is challenging to cost and price an episode or a period of care. In Argentina and Uruguay, nursing homes are paid based on the number of beneficiaries they serve during a certain year (Cafagna et al., Reference Cafagna2019). As with per diem payments, capitation creates incentives to contain costs; for example, by improving preventive care or quality of care, but also by skimping on care or selecting low-cost beneficiaries. It is therefore usually adjusted for the beneficiary characteristics that influence variation of costs. For example, Chile adjusts capitation rates according to beneficiaries’ level of dependence, their age, medical status and socioeconomic status (Matus-Lopez & Cid Pedraza, Reference Matus-Lopez and Cid Pedraza2015). In the USA, Medicare nursing homes that participated in the Evercare project and started receiving capitation-based payments (instead of FFS) invested in primary care to avoid hospitalizations, which reduced (unnecessary) hospitalizations (Konetzka, Reference Konetzka2006).

Capitation payments can be used to promote integrated LTC (see Chapter 3.5 for more on integrated care). The Program for All-Inclusive Care for the Elderly (PACE), and the Institutional Special Needs Plan (I-SNP), are examples from the USA. In the PACE programme, day care was paid by capitation to provide all social and health services in one single space during the day so the patient could keep living in their home (Konetzka, Reference Konetzka2006). In the I-SNP programme, nursing homes were paid by capitation to provide onsite integrated care (McGarry & Grabowski, Reference Mcgarry and Grabowski2019). In both cases the integration of payments supported integrated care and reduced hospitalizations. This kind of incentive can be used only in a structure that enables the integration of social and medical LTC and primary and institutional care (see Chapter 3.5).

Payment method 4: P4P

Since most LTC is provided by low-paid, low skilled caregivers and some beneficiaries lack the cognitive capacity to complain, it is crucial to supervise and promote quality of care. Failures in LTC markets can result in low-quality or improper care, so maintaining quality is a key concern. Payments such as P4P can incentivize providers to improve quality, but it is not the only tool available to achieve this; Box 3.6.4 lists some of the others, both financial and nonfinancial.

Apart from payment mechanisms designed to promote quality of care, other financial incentives can be implemented:

Quality-related subsidies

In Austria, LTC providers must meet certain quality thresholds and adhere to quality management schemes to be eligible for public funding.

In England, quality-related subsidies are given to providers that invest in and increase their nursing homes’ workforce.

Quality-related public procurement

Australia and England give greater weight to predefined quality criteria (Malley, Trukeschitz & Trigg, Reference Malley, Trukeschitz, Trigg, Gori, Fernandez and Wittenberg2015).

In addition, nonfinancial tools may also promote quality of LTC such as publicly publishing information about prices and quality.

Regulation is justified in any market with failures or distortions that are not naturally resolved and especially in markets that have social importance (Selznick, Reference Selznick1985). In LTC, regulation plays a major role in promoting quality of care, and yet there is still room for improvement (Mor, Miller & Clark, Reference Mor, Miller and Clark2010). Ideally, payment mechanisms should be used as tools to enforce quality-promoting regulation (Ullmann, Reference Ullmann1987).

P4P has been widely implemented in health markets, but to a lesser extent in LTC (Li & Norton, Reference Li and Norton2019). Its use in LTC markets is different, for two main reasons. First, “performance” is defined differently, and quality measures frequently used for health are not suitable for LTC. For example, mortality rates are unsuitable to assess quality of LTC because mortality rates are high among all providers, even high-quality nursing homes and the objective of LTC is not good health, but rather managing well-being. Second, perceived quality measured by satisfaction of beneficiaries may also be unsuitable for LTC settings because some beneficiaries may not be responsive to quality of care, particularly those with cognitive impairment such as dementia (Norton, Reference Norton, Pigott and Woodland2016; 2018).

However, if P4P payments are effective, provision of higher quality of care potentially reduces the costs and burden on both the LTC and health care systems by reducing hospital (re)admissions and improving health outcomes. This is the reason why P4P is being increasingly implemented in nursing homes, despite the difficulty in measuring “performance” in LTC.

In 2010, about 14 states in the USA had P4P programmes for LTC through government-funded Medicaid. Programmes differed in how to measure and reward “quality”. Some used traditional measures, such as customer satisfaction with care provided, rates of staffing and regulatory deficiencies, while others used clinical outcomes, such as number of urinary infections or pressure ulcers.Footnote 3 The rates of bonuses for performance were modest and varied between 2% and 6% of the per diem rate (Dyer et al., Reference Dyer2020; Konetzka, Reference Konetzka2006). Germany applies P4P payment schemes for institutional LTC whenever rehabilitation interventions can lower the level of needed care (Blümel et al., Reference Blümel2020). Japan pays an add-on payment for nursing homes that exceed the minimum standards of staffing, a measure of quality of LTC (Malley, Trukeschitz & Trigg, Reference Malley, Trukeschitz, Trigg, Gori, Fernandez and Wittenberg2015). Korean nursing homes can receive 1–2% additional P4P bonuses if they score highly in five domains of quality of care, namely management of institutions, environment and safety, guarantee of rights of beneficiaries, process and outcome. Evaluation scores are disseminated through an official LTC insurance website (Barber et al., Reference Barber2021).

Evaluations of P4P schemes in Iowa and Minnesota showed improvements in resident satisfaction with care provided, employee retention rate and nursing hours to beneficiaries. However, these very same P4P schemes resulted in the selection of beneficiaries, as they created incentives to admit beneficiaries that increased the probability of performing well (Colombo et al., Reference Colombo2011). In addition, P4P schemes have raised concerns that institutions with fewer resources have less chance of scoring high in performance. This potentially leads to a vicious circle where worse-funded institutions receive fewer payments for performance and have even less opportunities to improve performance or quality (Konetzka, Reference Konetzka2006). Other recent evaluation studies from the USA found that P4P schemes had little effect on the quality of LTC and suggest that there is room for improvement in designing these payments (Grabowski et al., Reference Grabowski2017; Li & Norton, Reference Li and Norton2019).

Given the above, policy-makers should be cautious in their enthusiasm for P4P payments. There is little reliable evidence, much of which is inconclusive, on whether these types of payments improve the quality of care. P4P payments are often technically and politically difficult to implement, and their cost–effectiveness remains unclear (Eckhardt et.al, Reference Eckhardt and Busse2019). To improve quality of care in practice, P4P payments should be carefully designed and combined with other tools (see Box 3.6.4).

Payment method 5: budgets

Budgets may be combined with other activity-based payments to balance economic incentives. In LTC, budgets are often negotiated prospectively or based on a prefixed share of high-need users. This poses a financial risk for providers, as they may face budget overruns, since public budgets are rarely adjusted later to reflect the changing disability status of care beneficiaries in institutions (Colombo et al., Reference Colombo2011). Budgets are not commonly used to pay for nursing homes, but some countries combine budgets with other activity-based payments to balance the economic incentives. In Czechia, as mentioned above, nursing homes’ budgets cover the operational costs and fees for service for allied health services, which are capped (Koldinská & Štefko, Reference Koldinská, Štefko, Becker and Reinhard2018). The Netherlands combines a per diem system with overall budgets for residential care (Barber et al., Reference Barber2021).

Community care

The key cost in community care is the labour of its formal caregivers. As in institutional care, most are low-skilled (see Chapter 2.5). In many countries, they are paid based on the number of hours they work. Elsewhere, caregivers are paid a global monthly wage or a fraction, corresponding to the worked hours. Usually, salaries are accompanied by quality norms and constant measurements. Current wages for personal home care in many countries are the minimum wage per hour and sometimes even lower, primarily due to unpaid time (i.e. unpaid travel time and “on-call” hours) (OECD, 2020b; Cravo Oliveira Hashiguchi & Llena-Nozal, Reference Cravo Oliveira Hashiguchi and Llena-Nozal2020). Since the publicly financed hours are often not enough to cover the needs of the LTC beneficiary, the caregiver might receive payments from two payers: one being the public payer, and the other being the beneficiary or their family as private funding directly paid to the caregiver to ensure the beneficiary receives the number of hours of care they need.

The caregiver’s characteristics and the way a home care beneficiary receives the payment (in kind or in cash) can impact the level of expenditure, regardless of whether the care is formal or informal. In Germany, for example, LTC beneficiaries are free to choose between cash or in-kind benefits for home care. In-kind benefits are more than double the amount of cash benefits for the same care level assessed. Cash benefits are mostly chosen when the caregiver is an informal one, usually a relative, while in-kind benefits are the preferred choice for those contracting a formal caregiver (OECD, 2020b).

Informal caregivers can be rewarded by receiving allowances (cash benefits) or non-monetary benefits (extra care leave or paid leave from their regular work to care for relatives, tax benefits, respite care services and more, to incentivize informal caregiving). Both methods increase the willingness of informal carers to provide LTC and may promote home care instead of nursing home care (Brimblecombe et.al, Reference Brimblecombe2018). Notably, in countries where the employer is not reimbursed for the paid sick leave or paid leave that an employee uses to help care for a relative, the costs of such legislation shift to the private/commercial sector. In some countries, such as Germany, LTC beneficiaries receiving cash benefits can use this money to pay their informal caregivers (Blümel et al., Reference Blümel2020). The monetary and non-monetary benefits usually do not cover the full costs of care, such as foregone working hours, and are rather simply an acknowledgement that providing care involves costs (OECD, 2020b). For example, in Spain, caregiving allowances are unconditional (paid directly to the caregiver’s bank account) but are lower than the minimum wage (Costa-Font, Jiménez-Martín & Vilaplana-Prieto, Reference 509Costa-Font, Jiménez-Martín and Vilaplana-Prieto2022). High benefits may disincentivize carers to participate in the formal labour market, particularly for low-skilled workers and especially if they are means tested (Colombo et al., Reference Colombo2011). In Spain, caregiving allowances incentivized informal care, while the effects of public funding of home care on informal care was mixed, with no clear pattern of substitution or complementarity of informal and formal home care (Costa-Font, Jiménez-Martín & Vilaplana-Prieto, Reference 509Costa-Font, Jiménez-Martín and Vilaplana-Prieto2022).

Policy relevance and conclusions

Compared to health care, LTC has unique characteristics when it comes to the type of care provided (by low/untrained caregivers, in formal and informal care settings, for an unknown duration) and the beneficiaries it serves (older people and others with impaired abilities’ whose health situation is not expected to improve). Therefore, funding and payments for LTC should be regarded as social care rather than health care. Public and private expenditures in LTC are likely to keep increasing given population ageing, declining supply of informal (unpaid) care, and the introduction of new care technologies, but better value for money can be achieved. Public funds should be allocated efficiently to payer agencies, providers and beneficiaries. Payment methods are tools that can potentially be used to change provider behaviour to provide quality LTC according to need (not too much and not too little), in the most cost-effective setting. Payment types for LTC providers are largely the same as those for health care providers, and the incentives that each payment type generates are similar. The same two guiding principles to balance economic incentives apply: payments can be adjusted based on risk or on inevitable cost variations and then combined with other types of add-on payments to incentivize additional aspects such as quality and cost containment.

However, there are important differences between the health care and LTC markets.

First, the duration of LTC is unknown, which makes case-based payments such as DRGs difficult to price. Second, selection of less labour-intensive beneficiaries can occur when payments are not adjusted to variation of risks or costs. Negative selection by payer agencies can manifest as shifting unattractive (i.e. labour-intensive or high-risk) beneficiaries and costs to less optimal care settings. Improper costing of payment fees, or prospective payments such as budgets, capitations or per diem payments can create incentives to service distortion such as underprovision of care, which usually means fewer hours of care, but also poor quality, neglect and understaffing. In extreme cases, improper costing may result in closure of nursing homes if they are not financially sustainable. Nursing homes are paid primarily per diem, which incentivizes cost control, but also service distortion. To balance economic incentives, per diem tariffs are either adjusted for severity of dependency, high costs, geographical region, or beneficiary characteristics; or combined with other types of payment such as FFS, budgets and P4P. Capitations are used to pay for day centres and nursing homes and can be used to promote integrated care. Capitations, too, are adjusted to account for variable costs and reduce incentives for selection or service distortion.

Home care is mostly provided by informal (unpaid) caregivers, who have no formal contracts, and provide quality of care dependent on their altruism, free time and opportunity costs. Formal caregivers are typically paid prospectively, by the hour or via a monthly salary, as there are few specific services that can be paid for with a specific fee. Informal caregivers can go unpaid, be paid from the cash benefits received by the care beneficiary, or receive non-monetary allowances, such as additional paid leave to provide care from the state or their regular employer, and tax exemptions. Neither the cash benefits nor the allowances fully cover the costs of care or loss of alternative income, which represent an increasing burden on informal caregivers.

Third, since LTC beneficiaries are not always able to complain, and many of the market failures may undermine quality of care, assessing and promoting quality of care is crucial for all care settings. However, quality- or performance-related payments in LTC are not yet widespread and the existing experience shows inconclusive results, with no clear evidence of benefit in the long run. Multiple coexisting policies may promote quality of care, if applied in a coordinated manner: (i) regulation that sets standards of care, promotes transparency and publicly publishes information on quality indicators; (ii) financial mechanisms such as payments to balance economic incentives and subsidies to enforce regulation; and (iii) reducing the fragmentation of LTC payer agencies and providers.

Fourth, moral hazard problems are less common in LTC than in health care due to rigorous eligibility criteria and assessment of need for services. Moral hazard is reduced with clear and objective eligibility criteria set at the national level, and detached from payers. Eligibility assessment should be done on a regular basis to account for changes in level of disability. These are better tools than cost-sharing to mitigate moral hazard, as they do not exacerbate financial access barriers. In addition, overprovision of LTC does not necessarily mean more hours of care and can result in overmedicalization.

Fifth, due to the fragmentation of LTC markets by type of care, payers may face incentives to negatively select unattractive beneficiaries, by shifting them to other care settings (and payers). Earmarked budgets or integration of payers might mitigate these perverse incentives. Equity in funding payer agencies may also reduce/end this market distortion. Equity in funding can be improved if funds are allocated to payers according to the needs of the populations they serve; this can be achieved by means of allocation formulae with clear and objective risk adjusters.

Since health care and LTC are interconnected, the effects of payments to providers in each area should be better explored. Investments in health care can prevent or delay the need of LTC. High-quality LTC and rehabilitation can save the costs of unnecessary hospitalizations. However, the systems are often fragmented, which may result in inefficiencies, and these interplays should be better understood – in particular, the incentives of payers and providers to shift beneficiaries to other settings by underproviding preventive care, or by upcoding severity of dependency. From the literature we have reviewed, it is not yet clear whether providers of LTC are more or less sensitive than health providers to changes in economic incentives created by payments. This could also be explored in future research.

Finally, payments are an important tool that influence provider behaviour, but are not the only ones. Policy-makers should bear in mind that health care and LTC providers are not motivated solely by remuneration. Other considerations often outbalance or prevail over the economic ones, such as the needs of beneficiaries, empathy or altruism, particularly among informal caregivers, who are usually relatives or friends of the person they are caring for (Berenson & Rice, Reference Berenson and Rice2015; Busse & Mays, Reference Busse, Mays, Nolte and McKee2008; Waitzberg et al., Reference Waitzberg2020a). It is key to receive the full value of LTC payments, and there is still a need to scrutinize the effects of payment mechanisms on LTC market failures. Health economics provides a starting point to define frameworks to analyse the particularities of LTC.Footnote 4

Open access

Open access

{kind=link}