Introduction

What kinds of institutions satisfy credit needs? Traditionally, credit needs were satisfied by banks, a type of regulated and federally insured financial institution whose numbers grew from the postwar era until the end of the 1980s. However, a sea change began in that decade, when a shift toward shareholder value in the management ethos refocused firm practices on short-term profits, causing the expansion of the financial services sector and even the financialization of nonfinance sectors of the economy [Davis Reference Davis2018; Fligstein and Dauter Reference Fligstein and Dauter2007; Fligstein and Goldstein Reference Fligstein and Goldstein2022; Tomaskovic-Devey, Lin and Meyers Reference Tomaskovic-Devey, Lin and Meyers2015].

Within this scope, regulations surrounding the financial sector loosened, giving rise to to alternative financial institutions (AFIs) that competed with banks. In a crowded ecosystem, banks increasingly wound down or consolidated, while AFIs continued to grow [Fligstein Reference Fligstein2021]. At the end of the financial crisis, there were over 13,000 AFIs in the United States alone, double the number of commercial banks nationwide [FDIC 2009]. Today, AFI loans are rapidly becoming one of the most significant sources of credit. Data from the Federal Deposit Insurance Corporation [FDIC 2023] shows that 7% of all households still use nonbank financial services provided by AFIs and close to 5% use rent-to-own services as well as payday, pawnshop, tax-refund-anticipation, and auto-title loans. Moreover, 14.1% of households are “underbanked”: in other words, although these households have a bank account, they still rely on money orders, nonbank transactions, and nonbank credit [FDIC 2023].

Although the loans offered by AFIs are valuable for satisfying the credit needs of their consumers, they are regarded as problematic. AFI loans are usually classified as predatory because of their high interest rates and their restrictive lending terms, which far exceed traditional bank loan parameters [Faber Reference Faber2018]. Much empirical research has also demonstrated the deleterious consequences of AFI loans for borrowers. Borrowers are burdened with financial obligations that drain their income and financial assets, and in some cases, may force them into dependence on further debt to finance existing debt and interest payments [Cardaci Reference Cardaci2018; Killewald, Pfeffer and Schachner Reference Killewald, Pfeffer and Schachner2017; Wherry, Seefeldt and Alvarez Reference Wherry, Seefeldt and Alvarez2019].

Predatory lenders most often target low- and lower-middle-income individuals, who seek out loan-offering AFIs rather than traditional banks for their borrowing needs because their low income and limited wealth make them credit risks to lenders [Simpson and Buckland Reference Simpson and Buckland2016; Small et al. Reference Small Mario, Akhavan, Torres and Wang2021]. Ultimately, borrowers are stripped of their ability to build wealth, pursue higher education, afford health and medical services, and maintain an adequate standard of living across generations [Dwyer Reference Dwyer2018; Faber Reference Faber2018; Wherry Reference Wherry, Wherry and Woodward2019].

However, lenders have been the subject of legislative tightening in recent years, in particular in the period from 2021 to 2023. In the United States, a flurry of state bills sought to end the deceptive practices that had been enabled by the “true-lender” rule implemented by the Office of the Comptroller of the Currency (OCC) under the Trump administration in October 2020. The entity classified as a true lender is the entity subject to oversight rules about interest and fees. True lenders are additionally obliged to investigate the financial backgrounds of prospective consumers and ensure that their financial circumstances qualify them to make debt repayments. The Trump-era true-lender rule gave legitimacy to predatory lenders’ evasive practices by allowing the bank, rather than the predatory lender using the bank, to be registered as the true lender.

Though the legislation was reversed by the House and Senate under the Biden administration in July 2021, state-level efforts have continued to legislate against the rise of predatory lenders that it had enabled. In November 2023, for instance, the Florida Senate proposed the bill Florida SB146, which sought to expand the Florida Consumer Finance Act to restrict loan conditions pervasive in predatory lending [Berman Reference Berman2024]. Sections in Florida SB146 clamped down on lenders who attempted to persuade consumers to obtain loans with higher interest rates than the rate stipulated in the bill. Anti-evasion provisions for identifying the true lender were also put in force, mirroring those of Minnesota. Four other states (Illinois, Maine, Hawaii, and New Mexico) followed suit, pursuing similar expansions of consumer finance provisions to curb true-lender evasions, targeting predatory lenders as a growing category of AFIs.

This article addresses a fundamental research question: how do predatory lenders adjust their credit risk management strategies to retain their predatory practices and profitability, especially in response to recent regulatory tightening? Addressing this gap, this article investigates the most prominent publicly listed predatory lenders and their credit risk management strategies. I focus on the core predatory lending practices of collateralization, regulatory evasion, and relational risk laundering and examine how they exhibit regional differences in the aftermath of the subprime crisis. Though their evolving credit risk management strategies are nominally meant to confine credit risks, predatory lenders design them in response to regulatory tightening to bolster and stabilize revenues, while inadvertently exacerbating the risk posed to borrowers.

Theorizing Regulatory Capitalism and Predatory Lenders

This article draws on the theory of regulatory capitalism to understand the political economy of predatory lending and its temporal trajectory across regions. Seminally described by David Levi-Faur [Reference Levi-Faur2005], regulatory capitalism theory posits a shift in governance from the state-led provision of services that had characterized the mid-20th century to a new era, beginning in the 1980s, that emphasized governance through market regulation by means of a novel interplay between states and markets, particularly in sectors like finance. Regulatory capitalism advances a Foucauldian concept of governmentality when understanding state–market relations, showing that states shape market conduct through indirect means like credit scoring, but embedded in a broader sphere of regulatory action meant to reproduce a social order that defends “economic profitability and political utility” of the private sector [Jessop Reference Jessop2007: 39].

Regulatory capitalism builds on and extends a prototypical conceptualization of the state in a capitalist society as a market-fixing entity, rooted in neoclassical economics. In this conceptualization, markets function best when the state does less, valorizing a disengaged state that only intervenes to fix illegal behaviors among agents, but without shaping their conduct [Swyngedouw Reference Swyngedouw2005]. The core of regulatory capitalism theory is the argument that in advanced capitalism, privatization advances not only through lack of state activity, but also through increased regulation itself. In regulatory capitalism, state–market relations are characterized by decentralized enforcement.

As Sarah Quinn [Reference Quinn2019] meticulously details in American Bonds, the US state uses credit to design markets and back private risk to achieve political and economic goals. The US mortgage market is illustrative: rather than acting as a direct lender, the state’s primary role has been to create and back the fundamental infrastructure for private lending through federal mortgage insurance (via the Federal Housing Administration) and the creation of Government-Sponsored Enterprises (GSEs) like Fannie Mae and Freddie Mac, which purchase conventional loans, provide guarantees, and create liquid secondary markets. Quinn’s [Reference Quinn2019: 4] historical analysis reveals that this model of using public credit guarantees to stimulate private market activity transforms the state into a market overseer that “socialize[s] risks of loans while letting private firms keep the profits from repayments” [Ibid.: 13]. As the state underwrote the market expansion of quasi-governmental mortgage dealers like the GSEs and credit-rating agencies through credit guarantees, these entities were empowered with the tools of governance itself, tasked with enforcing market standards within a government-designed framework [Quinn Reference Quinn2019: 84, 163]. By offering the private sector an outsourced role in policy design and standard-setting through industry groups, the state absolved itself of these responsibilities [Braithwaite Reference Braithwaite2008; Shamir Reference Shamir2008]. For instance, the Financial Accounting Standards Board (FASB) establishes accounting rules, but it remains industry-funded by collecting fees from publicly listed companies. Moreover, when Moody’s and S&P rate securities, they effectively enforce capital requirements, demonstrating how regulatory power becomes distributed to private institutions.

This framework proves particularly useful for understanding predatory lending. Fragmented regulatory oversight creates the potential for regulatory arbitrage, where businesses exploit gaps between jurisdictions, such as in payday lending when companies partner with banks in lenient states to circumvent regulations [Ramirez Reference Ramirez2020]. These gaps enable firms to liaise with a range of economic agents in an attempt to achieve formal compliance while violating regulatory intent to pursue risky, profit-maximizing behaviors.

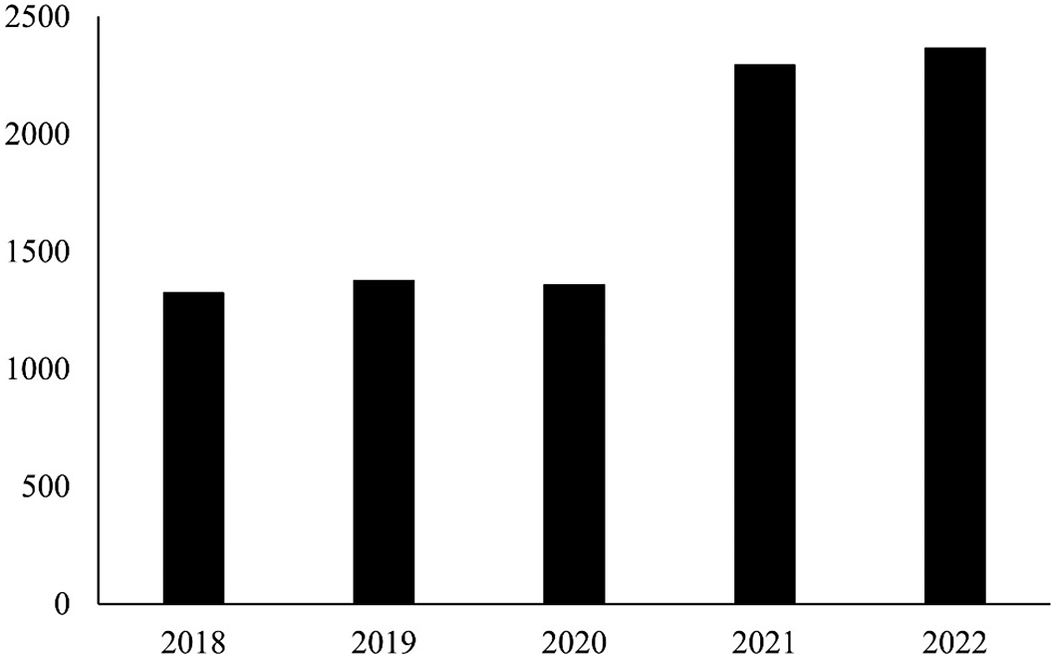

Thus, despite increased legislative tightening by lawmakers, predatory lending continues to flourish. Figure 1 presents the trajectory of the average number of branches across lenders in the sample, from which we observe a steady increase from 1,324 branches in 2018 to 1,359 branches in 2020. Following the unprecedented macroeconomic challenges that the pandemic posed to low-income workers, AFI loans grew in demand as much-needed sources of credit, resulting in an explosion of new branches, numbering almost 2,300 by 2022.

Average number of branches across lenders in the sample

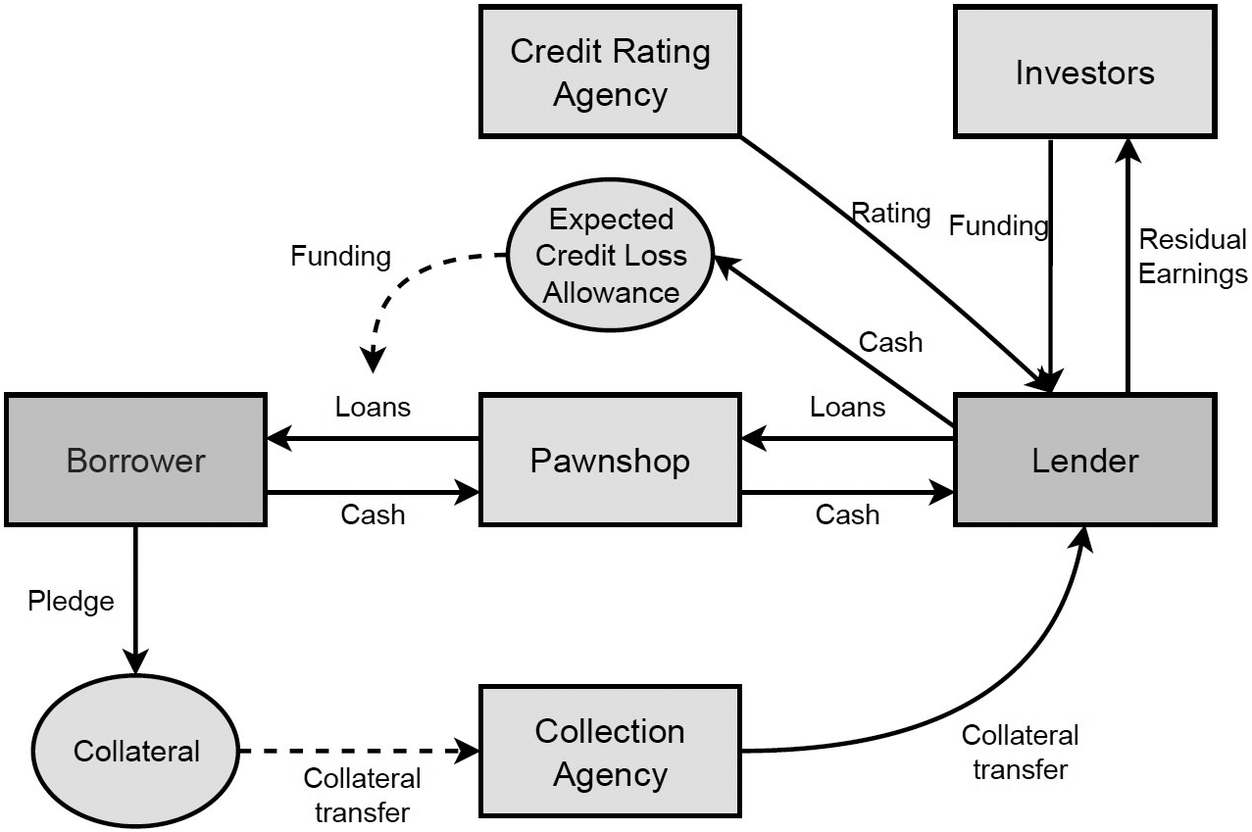

AFIs cooperate and interact with (a) third-party enforcement agencies, (b) credit ratings agencies, (c) investors, and (d) borrowers to facilitate a range of credit risk management strategies that operate across geographical boundaries (Figure 2).

The ecology of the predatory lending business

Loans are not dyadically restricted between a borrower and a lending firm. Lending firms are connected to a wide-reaching network of “storefront” pawnshops (and brokers) on the frontlines, through which they sell to prospective borrowers at arm’s length. Through these pawnshops, lenders facilitate an exchange of loan issuance (to consumers) and cash remittance (loan repayments from consumers).

Lenders face unique pressures of their own. They remain beholden to investors to shore up profits and generate shareholder returns. As equity holders, investors are entitled to residual earnings generated by lending firms (earnings after all debt obligations and expenses are paid), through which they make returns on their capital investment. Conversely, investors are important stakeholders for lending firms as they offer additional capital to satisfy the firms’ funding needs. Investors thus wield significant control over firms by having the right to appoint and replace boards of directors and managerial leadership should they feel dissatisfied with firm performance, such as when residual earnings are deemed lackluster.

Lenders also depend on credit agencies to assess their operating results and financial stability. All lenders, for instance, refer to Fitch Ratings’ credit ratings of their own firm to determine the size of their expected credit losses (ECLs). ECLs consist of the funds that lenders set aside in cash or cash equivalents (e.g., by purchasing short-term treasuries) to cover the losses they expect to book for the coming year, based on estimations of the number of counterparties who will default and the value of their loans. Firms refer not only to Fitch, but also to a multitude of large and global credit agencies, including Moody’s and S&P Global. Although the agencies themselves may differ marginally in their ratings, these three credit agencies control close to 100% of credit ratings in the financial markets [Financial Conduct Authority 2023]. Firms thus tend to be isomorphic and turn to these credit rating agencies as sources of legitimacy [DiMaggio and Powell Reference DiMaggio and Powell1983].

As a result, ECLs may fluctuate from year to year, depending on the credit rating that a lender receives from Fitch and the value of loans forecast to default in the following year (not the actual value of losses incurred). However, since GAAP accounting rules classify ECLs as an expense to be deducted from revenue, lenders are incentivized not only to grow revenue, but to shrink their ECLs to bolster profitability and improve residual earnings for investors.

Collateralization. Collateralization is when lenders mandate borrowers to pledge assets as a condition of receiving a loan. The collateral remains under the legal possession of the borrower, and reverts to them should loans be repaid on schedule. When borrowers delay or fail to make repayments, lenders move to claim the forfeited collateral through third-party collection agencies and repossession companies.

The purpose of collateral is twofold: (1) to reduce the risk of debt to lenders by enabling them to seize assets to satisfy outstanding debt obligations in the event of a default, facilitating enforcement against borrowers; and (2) to protect lenders from other creditors, should borrowers face severe credit events such as bankruptcy. Mirroring how networks of social relations penetrate irregularly and in differing degrees in different sectors [Ferrary and Granovetter Reference Ferrary, Granovetter, Bathelt, Cohendet, Henn and Simon2017], lenders possess a wide range of connections to networks of pawnbrokers scattered across business segments. This variety of penetration into different businesses allows lenders to cross-sell collateral into retail and other segments, while diversifying the types of collateral they can accept.

Regulatory evasion. Laws are rarely implemented in a clear fashion by officials [Suchman Reference Suchman, Lury and Wakeford2013], giving rise to creative interplay between regulators and the firms being regulated [Aldrich, Birkhead, and Ruef Reference Aldrich, Birkhead, Ruef, Sorensen and Thornton2025]. While this interplay can be cooperative [Aldrich, Ruef and Lippmann [(1999) Reference Aldrich, Ruef and Lippmann2020: 178], predatory lenders take advantage of the ambiguity by avoiding oversight and reducing the financial impact of legislative amendments that scrutinize the security of AFI loans.

Lenders activate connections with a host of intermediary agents (“storefront” banks, pawnshops, and third-party collection agents) to manage consumer acquisition, sales, and collateral requisition processes. Relational economic sociology stresses the importance of agents in facilitating financial purchases [Bandelj Reference Bandelj2020]. Employing intermediary agents not only expedites the sales process but also improves the legitimacy of lending firms in the eyes of regulators [Besbris and Korver-Glenn Reference Besbris and Korver-Glenn2023]. Moreover, these agents are not only scattered across business segments, but across legislative jurisdictions.

This diversity of connections additionally allows lenders to modify loan terms to accommodate legislative amendments in any one jurisdiction. The relations that lenders possess enable them to avoid increasing regulatory oversight in two ways: firstly, by diverting revenue focus to less legislated geographies. New units within an organizational field, dispersed across geographies, help channel information, capital, and even collateral to lending firms [Bastos and Silva Reference Bastos and Silva2012].

Simultaneously, lenders rely on their connections to avoid regulatory oversight by a second method: verticalizing their products through a suite of new fees and products that shift their revenue sources away from overreliance on interest rates. According to Hawley, vertical differentiation naturally occurs when “supplementary similarities” [Reference Hawley1986: 30] are achieved through symbiosis (when different units have complementary differences) and commensalism (when different units build upon similarities). In similar fashion, lending firms build “supplementary similarities” across their financial products by creating new suites of financial fees and products to sell to the same consumers. Akin to Fligstein and Roehrkasse’s [Reference Fligstein and Roehrkasse2016] observation that vertical integration may exacerbate fraudulent acts by concealing victims from complex value chains, vertical integration may also conceal firm practices from regulatory oversight.

Risk laundering. Similar to how money laundering is the process of concealing the origins of money, risk laundering refers to processes by which lenders conceal their firm-level credit risks while maintaining revenue stability. Lenders seek out investors to purchase newly issued bonds and nonperforming loans. These strategies are nominally intended to improve credit risks, but continue to overleverage firms and incentivize them to pursue predatory loan terms to bolster profitability.

Risk laundering shows similarities with the fluid conception of valuation put forward in decades of economic sociological research. This body of work has suggested that valuation is an intersubjective process of meaning-production, as much as it is an objective process decided by market consensus [Bandelj Reference Bandelj2020; Zuckerman Reference Zuckerman2012]. Recent empirical research has documented value fluidity in the US real estate market, where agents leverage the authority vested in their expertise to persuade racialized consumers to purchase houses [Besbris, et al. Reference Besbris, Kuk, Owens and Schachter2022; Besbris and Korver-Glenn Reference Besbris and Korver-Glenn2023].

To launder risk, lending firms leverage connections with investors to manufacture impressions of profitability and balance-sheet stability and thus improve their market valuations—through which firms can stay afloat and investors profit. The recursive flow of investor capital is reminiscent of the cyclical character of monetary valuation and institutional practices [Fourcade Reference Fourcade2011], but rather than focusing on cultural beliefs, my analysis foregrounds the predatory risk in loans and firm-level risks (financial instability) that risk laundering exacerbates.

The Subprime Crisis and Changes in Predatory Lending Practices

The subprime crisis of 2007–2010 was an inflection point in lending within the financial services sector, but one that largely transformed the system from one of financial exclusion to one of predatory inclusion. In the years leading up to 2007, lending was characterized by deregulation, and expanded into layers of securitization, which became the most popular and profitable practice in the financial sector. During this period, the GSEs Fannie Mae and Freddie Mac operated in an environment of significantly loosened regulatory constraints. This erosion of standards was primarily fueled by a sustained, bipartisan political effort to expand homeownership, which translated into congressionally mandated affordable housing goals set by the Department of Housing and Urban Development (HUD). These quotas, which rose dramatically throughout the late 1990s and early 2000s, pressured the GSEs to purchase an ever-increasing volume of mortgages made to low- and moderate-income borrowers. To meet these targets, Fannie and Freddie progressively weakened their own underwriting standards, acquiring vast numbers of riskier loans featuring lower down payments, weaker credit scores, and poor documentation, ultimately venturing deeply into the subprime mortgage markets. This risk-taking was abetted by the failures of their regulator, the Office of Federal Housing Enterprise Oversight (OFHEO), which was underfunded and stifled by GSE-driven lobbying that blocked legislative attempts to impose stronger oversight and higher capital requirements [Frame, Gerardi and Willen Reference Frame, Gerardi and Willen2015].

Core to private-label securitization was collateralization, which relied on bank and even nonbank lenders to issue subprime and Alt-A mortgages (undocumented loans) to sell to investment banks, which would pool them into private-label mortgage-backed securities (MBSs).

These MBSs were then divided into tranches, rated by credit rating agencies, and sold to investors for speculation. The instrument that these tranches were packaged into depended on their credit rating. Lower-rated MBS tranches were repackaged by banks into the notorious collateralized debt obligations (CDOs) and synthetic CDOs, which paid higher interest rates to investors to accommodate the risk of default. These CDOs made risky loans appear safer through diversification, but actually encapsulated new forms of risk by betting on mortgage performance through credit default swaps and not actual loans, amplifying systemic risk. Underwriting was subsequently weakened when collateral pools were polluted with a deluge of loans to poor-credit borrowers, eager to purchase mortgages, and inflated appraisals and undocumented loans by nonbank lenders, eager to sell mortgages and to secure profit, regardless of creditworthiness or systemic risk.

However, these measures proved too conservative still, as their real risks were revealed to significantly outstrip their actual credit rating when they collapsed. Many of these CDOs were constituted by subprime mortgages, issued to borrowers who purchased properties without sufficient creditworthiness, leading to a wave of mortgage defaults and the collapse of subprime mortgage lenders (e.g., New Century, Ameriquest, Countrywide) or their absorption by banks. This contagion that spread from the financial sector rippled across the globe to destabilize labor markets and credit markets worldwide.

In spite of the damage, however, regulatory capitalism theory conceptualizes the crisis not as the failure of deregulation, but as the inevitable outcome of a configuration of state–market relations premised on deregulation itself. Contrary to popular narratives about deregulation, state oversight of financial markets increasingly relied on complex rules, but these were outsourced to private actors. Credit rating agencies became de facto regulators, empowered to assess risk despite their financial dependence on the very institutions they were rating [Parker and Nielsen Reference Parker and Nielsen2009]. Banks developed sophisticated internal risk models that regulators relied upon, creating a system of “self-regulation” that partially absolved states of the responsibility for regulating adverse outcomes [Braithwaite Reference Braithwaite2008: 11].

Financial innovation consistently outpaced regulatory capacity, with complex instruments like CDOs and credit default swaps evolving faster than any government agency could monitor or control. Regulatory fragmentation meant no single entity oversaw the entire mortgage securitization chain, allowing risks to accumulate in spaces between jurisdictions and agencies [Ibid.]. Most importantly, the system created incentives whereby short-term profits consistently trumped long-term stability [Fligstein Reference Fligstein2021], with loan originators paid for volume rather than quality, and investment banks incentivized to package and sell loans rather than hold them.

After the crisis, the regulatory landscape appeared to change for lending practices. The Dodd–Frank Act was introduced in 2010, and at the same time the Consumer Financial Protection Bureau was established to police abusive lending practices, enforce transparency, and contain predatory terms. More specifically, the Dodd–Frank Act increased the liability of the credit rating agencies for issuing inaccurate ratings by “lowering the pleading standards for private legal action against them under Rule 10b-5 of the Securities and Exchange Act of 1934… [and] also makes it easier for the SEC to impose sanctions on CRAs and to bring claims against CRAs for material misstatements and fraud” [Dimitrov, Palia, and Tang Reference Dimitrov, Palia and Tang2015: 2].

These reforms led to the Ability-to-Repay rule in 2014, which introduced verification requirements for lenders against borrowers’ income, assets, and debt-to-income ratios in order to curb speculative lending, as well as a ban on the use of steering incentives by mortgage brokers to push borrowers into taking on costlier loans for higher commissions [Shatz and Angelo Reference Shatz and Angelo2014].

Through this lens, Dodd–Frank represents both a significant expansion of financial regulation and a demonstration of regulatory capitalism’s inherent limitations. However, new regulations like the Dodd–Frank Act created complex new oversight structures while maintaining the fundamental decentralized approach. For instance, the creation of the Consumer Financial Protection Bureau (CFPB) exemplified regulatory capitalism’s approach to specialized oversight, establishing a new agency focused specifically on consumer protections while maintaining the broader fragmented regulatory landscape.

For this reason, the Dodd–Frank Act and similar legislative attempts by regulatory capitalism to regulate lending inadvertently created new opportunities for regulatory avoidance. While the legislation successfully eliminated some of the most egregious predatory practices in mortgage lending, it drove financial innovation toward less-regulated products like payday loans and rent-to-own agreements. This phenomenon illustrates that comprehensive regulation often stimulates financial innovation designed to circumvent it, including regulatory capture, whereby regulators move to financial firms and vice versa, thereby softening enforcement over time.

Thus, predatory lending did not disappear after the financial crisis, but simply evolved into new forms of financial products and channels. Continued regulatory fragmentation allows predatory lenders to continue operating through jurisdictional arbitrage, shifting operations to less-regulated spaces within the financial system. Markets adapted to new rules while preserving their fundamental profit-seeking behaviors. To illustrate, the Dodd–Frank Act and similar legislation focused on (1) banks, (2) mortgages, and (3) securitization of mortgages into complex financial securities, like derivatives. The specific instruments that caused the collapse, CDOs, were replaced with simpler financial structures, such as collateralized mortgage obligations (CMOs). Moreover, the tightening of lending standards in traditional banks has pushed borrowers toward alternative high-risk lenders and allowed nonbank lenders to evade state interest-rate caps.

Varieties of Regulatory Capitalism and Forms of Lending

The theory of regulatory capitalism focuses on the linkages between regulators and industry to understand how core structures of profit maximization in the lending business thrive, despite surface-level adjustments in financial legislation. I build on this to explain the forms that predatory lending assumes in different regions, culminating in varieties of regional capitalism.

I draw inspiration from the varieties-of-capitalism perspective, one of the most prominent theoretical paradigms in explaining differences in economic performance across societies [Allen, Reference Allen2004; Hall and Gingerich, Reference Hall and Gingerich2009; Hall and Thelen, Reference Hall and Thelen2008; Mariotti and Marzano, Reference Mariotti and Marzano2019]. In this perspective, firms are the focal unit of analysis, given their centrality to economic production. Firms act as units with core competencies that depend on the relationships that connect them with producers, employees, and competitors in a market as well as institutional policies built into the political economy.

The interplay between actors and institutions within a political economic ecosystem is perhaps best described as “a terrain peopled with entrepreneurial actors seeking to advance their interests as they construe them, constrained by existing rules and institutions but also looking for ways to make institutions work for them” [Hall and Thelen Reference Hall and Thelen2008: 10]. Institutions are therefore not only the result of interactions among market actors, but also targets of action as well as resources to enable it.

I similarly theorize that varieties of regional capitalism exist. Each form of predatory lending is grounded in regional path dependence shaped by institutional histories. I theorize three regional varieties and discuss their implications for the regional variations in each predatory lending practice (collateralization, regulatory evasion, and risk laundering) due to differing regulatory environments, market structures, and borrower demographics.

North America—The United States and Canada constitute liberal market economies, wherein firms coordinate relationships with one another using formal contracts in a competitive environment. Every firm must craft its own identity, interfirm relationships, and market concerns. Businesses use informational signals to assess other businesses and determine the type of relationship to establish with each in order to reduce uncertainty and clear the path for expansion [Podolny Reference Podolny2001; White Reference White2008]. Here, firms use neoclassical economics’ marginal labor and capital calculations to modify their willingness to buy and sell items in relation to other firms, which determines market pricing [Hall and Soskice Reference Hall and Soskice2001: 27]. Together, these connections make up a market.

Liberal market economies have a financial structure that is far more focused on the stock market compared to the other forms of economy examined here. The United States is a prime example. With the exception of monitoring possible illegal conduct, more market sectors are being privatized with minimal government involvement. Businesses are constantly under pressure to increase their margins and bottom lines for short-term profit since they are obligated to investors to create returns. Coordinated interactions between lenders, borrowers (consumers), and states in this economy are shaped by this pressure. Caught between delegating autonomy to the states and provinces (subfederal levels) to design and implement social policies of their own, the United States and Canada have fragmented financial regulation between state and federal rules [Pierson Reference Pierson1995], resulting in loopholes like the “true-lender” doctrine. The Garn–St. Germain Act in 1982, for instance, sought to deregulate savings and loans by allowing them to expand beyond traditional home mortgages into riskier commercial and consumer lending, and permitted adjustable-rate mortgages (ARMs). Although the Dodd–Frank Act curtailed some of these liberties, the Garn–St. Germain Act itself was never repealed, and ARMs and interstate banking provisions are still allowable and have even expanded under other laws. These deregulatory changes helped lenders manage interest-rate risks, but laid the foundation for nonbank lending to flourish [Cornett and Tehranian Reference Cornett and Tehranian1990]. The path dependence of predatory lending that resulted from this deregulation thus derives from such fragmentation, which ultimately created an upsurge in firms exploiting jurisdictional arbitrage, such as firms partnering with Utah banks to evade interest caps.

Asia-Pacific—Asian countries are characterized by a different developmental history compared to North American and European nations. Loans in the region were early forms of microcredit with a longer history than European and North American counterparts, such as the hui in China, the chit funds in India, the arisan in Indonesia, and the paluwagan in the Philippines [Seibel Reference Seibel Hans2005]. Since most Asia-Pacific economies were rural for centuries longer than other regions, microcredit-style loans have historically been dominant in financing investment and household needs, typically revolving around small loans and the pledge of personal properties, including jewelry and gold, as collateral [Goenka and Henley Reference Goenka and Henley2013].

In the absence of strong formal institutions that have existed for hundreds of years, Asian development has been defined by weak formal institutions, as a result of colonial legacies that subordinated domestic affairs to foreign governance, an aftereffect that lingered even in the wake of decolonization in the 20th century [Acemoglu, Johnson, and Robinson Reference Acemoglu, Johnson and Robinson2001]. During the British era, for instance, the fast-growing commercial economy of the Malay states was left unsatisfied by British credit facilities, ultimately relying on loans from the Chettiar (a Tamil-speaking business caste) for investments in mining and forestry [Suppiah Reference Suppiah2014]. To compensate for weak early formal institutions, then, financial development relied instead on informal institutions, namely, local trust networks. Concomitant with communalistic-leaning cultures that emphasize membership in the social unit as the basis of trust [Bell et al. Reference Bell, Brown, Jayasuriya and Jones1995], lending and other financial transactions have often been facilitated by informal alliances and friendships between individuals, even for institutions like banks and firms [Stubbs Reference Stubbs1995].

What sets the region apart from Western counterparts is the reliance of development and financing on localized networks; this has resulted in a lag in consumer protections, whereby states regulate financial markets but leave the jurisdiction over consumer protections to firms. Ahmed and Ibrahim [Reference Ahmed and Ibrahim2018] observe, for instance, the incompleteness of laws in Malaysia. Since consumer protection laws are drawn from international Western standards, local rules missed core competencies that are taken for granted in Western countries, but missing in the Asia-Pacific, such as “knowing your customer, internal mechanisms to resolve complaints, and financial literacy and awareness issues” [Ibid.: 171]. As a result of this deregulation, firm lending is localized in dyadic relations between consumers and firms, trusting the latter to negotiate agreeable conditions on their own terms. This, however, gives rise to new forms of predatory lending, such as collateralization based on personal items, rather than traditional assets.

Moreover, debt itself is culturally associated with stigma in the Asia-Pacific [Nadeem et al. Reference Nadeem, Nagwa, Rosha, Delong and Rendak2020]. Individuals who bear debt are assumed to lack moral fiber, leading to loss of “face” or social status [Stickley Shirama and Sumiyoshi Reference Stickley, Shirama and Sumiyoshi2023], and ultimately social exclusion from communities and families. Just as important, this stigma perpetuates a lack of regulation surrounding loans by AFIs, especially since it disincentivizes borrowers from filing formal complaints about their debt or publicizing details about it, leading them to accept exploitative loan and collection conditions.

Europe— European economies are defined by coordinated market economies that rely on nonmarket actors, including the government. Informal agreements and confidential information-sharing are essential to the coordination of these interactions. As a result, rather than relying solely on pricing mechanisms and marginal calculations, business behaviors are dictated by interfirm ties that facilitate collaboration. Compared to liberal market economies, coordinated market economies experience less pressure for immediate financial gain. Businesses can provide employees with greater job stability, which encourages them to acquire firm-specific talents rather than transferable abilities in general. Governments actively collaborate with businesses to construct a system of vocational training that advances the development of firm-specific skills, reflecting the role of nonmarket institutions in coordinated market economies [Lee and Shin Reference Lee and Shin2021].

European economies’ financial systems are bank-based, emphasizing relationships between banks and firms. This synergy reduces the pressure on firms from the financial sector to produce short-term profits that characterizes liberal market economies such as those of North America. Unlike liberal market economies, the relationship between banks and firms in coordinated market economies is not just based on contracts, but extends beyond them, reflecting a financial and cultural obligation for counterparties to keep in close contact [Lehmann and Neuberger Reference Lehmann and Neuberger2001; Petersen and Rajan Reference Petersen and Rajan1994].

This arrangement creates firm advantages, such as access to more bank loans at cheaper rates, but also assigns priority to creditor rights over debtor protections [Hall and Soskice Reference Hall and Soskice2001]. As a result, regulatory gaps exist because as cross-border lending is poorly harmonized. Indeed, this market is culturally characterized by high institutional trust, which results in high trust in formal credit ratings that enable bond-based risk laundering [Zucker Reference Zucker1986].

Data and Methods

This article focuses on large, publicly listed AFIs that offer predatory lending. Publicly listed firms are among the most influential firms with the greatest reach in their operations. A flurry of acquisition activity after the financial crisis further consolidated the lending business into fewer firms (Fligstein and Roehrkasse, Reference Fligstein and Roehrkasse2016]. Being publicly listed offers a unique advantage in the lending business: publicly exchanged firms are subject to Securities and Exchange Commission (SEC) rules to disclose their operations in annual and interim reports to the general public. By providing visibility into their operations, lending firms gain much-needed credibility in the eyes of scrutinizing investors, regulators, credit ratings agencies, and even consumers.

I constructed this study’s dataset based on the Product Involvement database from Sustainalytics on Product Involvement. Sustainalytics is a research firm that investigates categories of environmental, social, and governance (ESG) concerns and assigns related ESG scores to companies located in major exchanges. The Product Involvement database is a private database of publicly listed firms (N = 11,590) that identifies the nature and extent of a given company’s involvement in a battery of products that are characterized as controversial.

I filtered Sustainalytics’ Product Involvement database for companies whose revenues depend in part or in whole on involvement with controversial practices of predatory lending. Predatory lending is defined as abusive practices that may disadvantage customers and that are engaged in in order to generate profits for the lender. These practices are abusive, though not necessarily illegal, thus coming to engender possible misconduct in marketing and customer suitability. Illustrative examples include discriminatory lending practices, setting predatory rates of interest on loans to debtors, and misleading debtors, customers, or investors through poor or illegal disclosure and foreclosure practices.

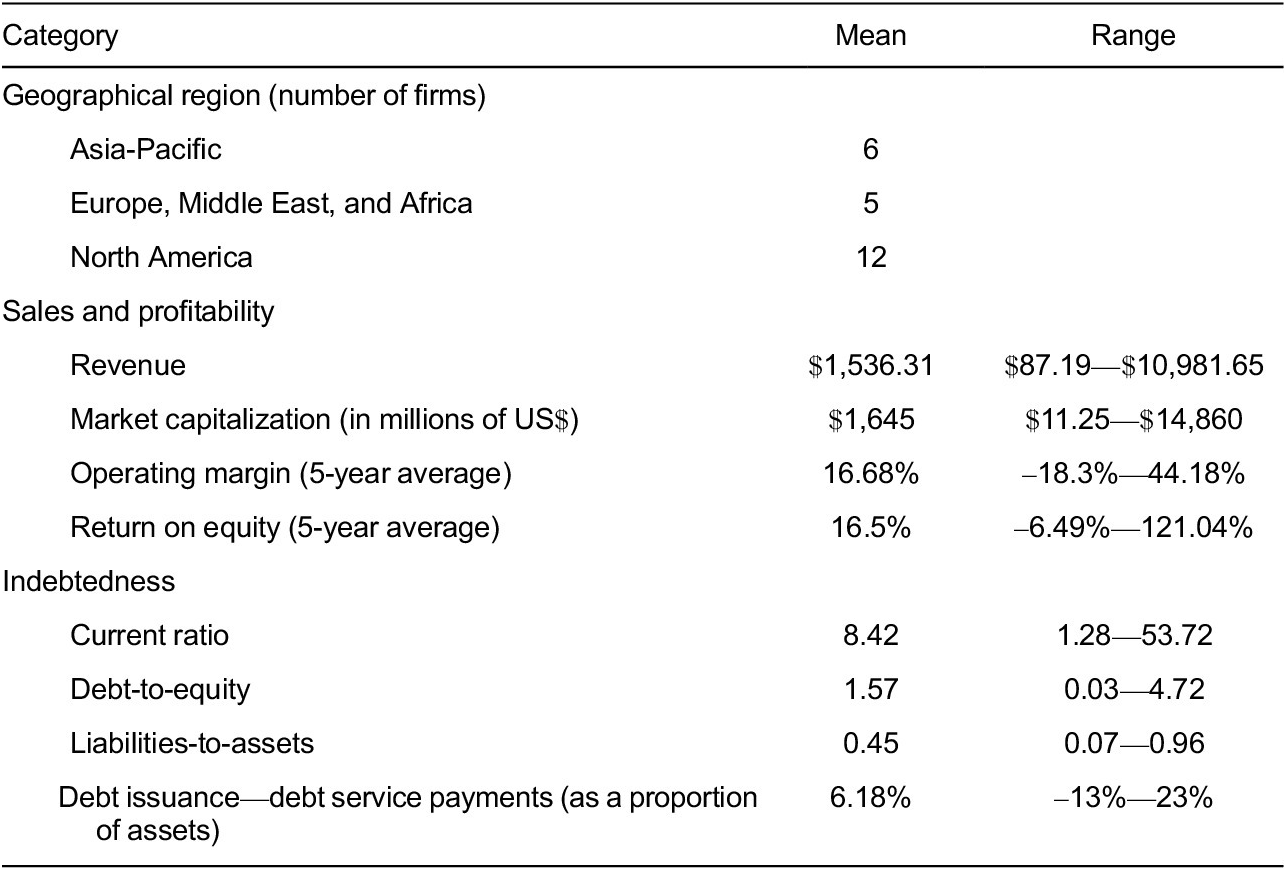

After filtering the entire Product Involvement database, I recorded 18 publicly listed financial services firms whose operating revenues were identified as deriving from some degree of predatory lending. Though these firms are not representative of all AFIs, they capture the most prominent, highest-valued, and visible AFIs. Firms from the sample are geographically diverse, headquartered across North America, Europe, Middle East, Africa, and the Asia-Pacific, but their connections often stretch across geographies to breach other regions, establishing the conditions for important relational mechanisms for credit risk management (Table 1).

Descriptive statistics of the sample

I collected metadata from Sustainalytics about the nature of each firm’s involvement in predatory lending. I separately procured sample personal loan agreement forms and annual reports from the firms (and parent company, where applicable) from 2018 to 2023, from which I distilled details about their financial circumstances and accounting practices, as well as the structure, scale, and sustainability of their lending operations over time. This produced a corpus of 19,358 pages.

I conducted content analysis of the corpus by applying the principles of abductive analysis from conceptual coding to fine-grained coding. This analysis, as Timmermans and Tavory [Reference Timmermans and Tavory2012] note, begins where induction leaves off by seeking a theory instead of facts and offering a “situational fit between observed facts and rules” [Ibid.: 171]. I examined annual reports for descriptions of firm practices of credit risk management and loan structures. I also contextualized these practices in terms of the interplay between regulatory developments and firm-level pressures for profit maximization by identifying shareholder obligations and preferences, changes in firm-level financial stability (including their profitability), their marketing strategies to reach consumers, and ECL allowances (loan loss provisions). Firms that did not change their practices were permitted to do so by native regulatory frameworks, but those that did change offered a vantage point for examining corporate adaptations to new regulations. This network of codes informed the theorizations developed here about the ecology of predatory lending.

North American Predatory Lending: Liberal Market Economies and Regulatory Fragmentation

Predatory lending remains a highly lucrative activity. Firm-level operating margins average 17.96%, but with an even higher segmented operating margin of 20.27% for the (predatory) lending segment alone. As the most profitable segment of the firm, predatory lending is the most monitored segment. Lending firms use in-house assessment teams and internally developed scoring systems based on inputs from available credit data to assess prospective borrowers’ credit quality and define credit limits.

To both guard against credit risks and improve profitability, lenders increasingly collateralize loans, mandating borrowers to pledge assets as a loan condition, which lenders seize upon default. However, regional differences exist in the use of collateralization based on their histories of regulatory capitalism. In North America, a deregulatory form of regulatory capitalism in liberal market economies enables predatory lenders to rely on high-value personal property as collateral, such as vehicles and electronics. Furthermore, loans are structured to incentivize forfeiture, because high interest rates discourage repayment. This is possible due to the long history of deregulation and fragmentation in the United States. Under past federal policies, the OCC allowed nonbank lenders to evade state interest-rate caps by partnering with national banks. This fueled the rise of “rent-a-bank” schemes, in which predatory lenders partner with small banks to exploit federal banking charters, allowing them to charge exorbitant interest rates (such as above 100% APR) even in states with strict usury laws.

To illustrate, FirstCash Holdings, a large US-based lender valued at $5 billion, operates under a similar model. With pawnshops located in the United States and Latin America, FirstCash Holdings’ revenue comes from small pawn loans secured by personal property. Collateralization using personal property enables FirstCash Holdings to present borrowers with the option of repaying their loans with high interest or forfeiting their property. Analyses of its annual reports reveal that high interest rates are used as an incentive to encourage borrowers to forfeit their property instead of repaying their loans with interest. Indeed, just 30% of FirstCash Holdings’ $3 billion in total company revenue comes from loan interest, while the remaining 70% comes from property forfeitures. FirstCash Holdings profits by repackaging and reselling the forfeited property to other retail consumers through a chain of 300 retail locations in the United States and 700 in Mexico and Guatemala.

EZCorp represents an even more extreme case. As a US-based pawnbroking and financial services company valued at $450 million, EZCorp’s bad debt expenses totaled $300 million in 2022, but the forfeiture of pledged collateral recovered the majority of these losses ($275 million). More significantly, the forfeited collateral it seized from borrowers was recorded as inventory at the lower of the principal balance of the pawn loan or the net realizable value of the collateral. This accounting reclassification permitted EZCorp to forego reserving any ECL allowance altogether and bypass possible charge-off expenses on the principal portion of forfeited loans. Despite the financial risks of having no reserves to cover prospective losses, EZCorp ultimately bolstered the image of its profitability by conserving the funds that would otherwise have been devoted to an ECL allowance, usually recorded as an expense, and recording them as assets.

North American lenders have recently been embedded in a tightening regulatory environment, from 2021 to 2023. The Biden administration revived the CFPB with more funding and rescinded a Trump-era rule from 2020 that had exempted payday lenders from verifying borrowers’ ability to repay. The Biden administration also rescinded the Trump “true-lender” rules, seeking instead to designate the true lender as the entity (such as a marketplace lender or nonbank partner) that is involved in funding, servicing, or facilitating the loan, rather than the one listed in the agreement and which originates the loan (such as a bank).

In July 2023, the Minnesota Senate enacted the Commerce Omnibus Finance Bill, which expanded provisions for consumer loans and financial institutions. The bill proposed an APR cap of 50% on the cost of credit for short-term loans, including all interest and fees charged to borrowers. The bill additionally implemented anti-evasion requirements that stipulate the true lender of loans as the AFIs (recognizing they could be nonbanks), rather than the “storefront” banks they used to facilitate the loans. This placed the obligation of investigating consumers’ financial circumstances onto predatory lenders themselves.

However, firms have devised new strategies of regulatory evasion to deepen access to consumers and gain flexibility in loan terms. Given the fragmentation between federal and state-level laws in North American regulatory capitalism, pawn lending remains regulated on a state-by-state basis, which creates important variations that can be exploited by enterprising firms. Ultimately, despite regulatory clampdowns on loan terms and excessive fees, enforcement remains inconsistent, creating the opportunity for arbitrage between states. Strict pawnshop and lending regulations in states such as Colorado contrast with others, like Texas, that allow very high interest rates and fees. For instance, FirstCash and EZCorp also strategically expanded into Texas, capitalizing on its permissive usury laws, which allow up to 200% APR, to offer high-interest loans in restricted states. World Acceptance Corp, a US-based lender worth over $700 million and with over 1,000 branches in 16 states, also bypasses usury laws by charging noninterest fees (e.g., origination and prepayment fees), making loans costlier despite nominal rate caps.

Consistent with the regulatory fragmentation of the United States, the banking sector is also highly fragmented at both state and local levels, with nearly 4,500 banks nationwide that offer products and services and take deposits from consumers. As research by the Federal Reserve reveals [Aubuchon and Wheelock Reference Aubuchon and Wheelock2010], this fragmentation leads to vulnerability to local economic shocks and regulatory difficulties with oversight. As the North American variant of regulatory capitalism rooted in a liberal market economy would predict, firm–bank relations are premised on contractual coordination for the pursuit of profits [Hall and Soskice Reference Hall and Soskice2001]. Banks willingly partner with lenders to facilitate transactions and enable them to bypass usury laws, even at the expense of consumers, in pursuit of short-term profit maximization. Given the focus of this financial system on the stock market, many state and local banks are publicly listed themselves, creating pressures to generate excess profits for shareholders [Fligstein Reference Fligstein2021]. Thus, firms still exploit true-lender loopholes by partnering with banks across states to avoid state APR caps. This fits within a long regulatory history of firms exploiting interstate differences in regulation for tax avoidance, such as the practice of incorporating in Delaware, where corporate taxes are lowest [Dyreng, Lindsey and Thornock Reference Dyreng, Lindsey and Thornock2013].

This partnership with banks also allows firms to improvise other means of regulatory evasion by verticalizing their products. To this end, lenders like Regional Management, a US-based lender valued at $220 million, and World Acceptance Corp introduced new suites of products to sell to consumers, thereby extracting greater income from each loan without over-relying on interest rates. Regional Management verticalized their product offerings to capitalize on the pledge of collateral itself and additionally offer collateral protection insurance through pawnshops. World Acceptance Corp similarly responded by selling new vertical product offerings to borrowers, including credit life insurance across 13 states and nonfiling insurance in five states.

Unlike regular life insurance, credit life insurance provides payment specifically for the borrower’s loan obligation in the event of their death. Nonfiling insurance covers the value of the loan and protects the lender in the event of borrower default, but the premium is charged to the borrower. Unlike FirstCash Holdings, which relies on seizing collateral and “perfecting” its loans by having legal documentation to facilitate forfeitures, World Acceptance Corp does not perfect its security interest. Instead, it relies on nonfiling insurance to recover its loans in the event of default. Nonfiling insurance permits the firm to avoid regulatory oversight once more by removing the need to file legal forms (e.g., a UCC-1) to regulators for recovery; in the case of World Acceptance Corp, this allowed it to recoup $12 million in insurance claims to directly offset credit losses for the year.

While these insurance products are enticing to those low-income borrowers most at risk of defaulting on their loans, they subject borrowers to a suite of additional fees. World Acceptance Corp regularly charges origination fees, account maintenance fees, and monthly account handling fees to all borrowers. As a result, even though record numbers of borrowers defaulted in 2023, the firm’s aggregate APR on loans averaged a high 45.8%, and revenues still rose over 5% (to over $600 million) compared to one year prior. Disincentivizing on-time repayments enables firms to profit more by charging overdraft fees and seizing collateral.

However, just as predatory lenders used banks to evade “true-lender” status, they rely on third-party collection agencies to distance themselves from the point of sale. Indeed, as part of a liberal market economy whose financial system is based on the stock market, lenders are connected to investors within the private lending space who enable them to launder their risk.

Using “storefront”-type proxies grants lenders flexibility in the strategies eventually used to seize collateral, while preserving their reputation and legitimacy before regulators. To illustrate, Regional Management Corp primarily uses Credit Bureau Collection Services, a major collector for subprime lenders, frequently mentioned in complaints [Federal Trade Commission 2010]; Encore Capital Group (Midland Credit Management), one of the largest debt buyers; PRA Group (Portfolio Recovery Associates), a major debt buyer that acquires Regional Management’s delinquent accounts; and unnamed local agencies. Similarly, World Acceptance Corp uses Caine and Weiner, a well-known collector used by subprime lenders; Allied Interstate (now Encore-owned), which frequently handles its charged-off loans; Northland Group, which specializes in consumer debt collections including its accounts; and Security Credit Services, another agency linked to past complaints. These collectors purchase the debt from the Regional Management and World Acceptance Corp, then sell the debt to junk debt buyers like PRA Group, who either collect it themselves or assign collection to other collectors.

Another key aspect of risk laundering in this liberal market economy is the concealment of firm-level risks by offloading bad debt to investors or reclassifying assets. In North America, the history of deregulation and prioritization of private markets gives rise to the sale of nonperforming loans (NPLs) to investors. Regional Management offers an illustrative example. In response to a challenging macroeconomic environment from 2022 to 2023, the lender tightened its customer segments by eliminating higher-risk consumer loans. These loans were owed disproportionately by low-income individuals who had experienced changes in their financial ability to repay. The $27.1 million worth of loans that became nonperforming under IFRS9 guidelines were sold in 2022, before they were written off in 2023 and classified as future income.

Investors who purchase these NPLs profit in various ways, such as by foreclosing to obtain the underlying collateral. The lending firm, meanwhile, benefits from the loan sale by laundering the risk. When loans are sold, lending firms can reclassify the value of the loan. While it may be recorded as a loss in the current year, it becomes reclassified as an addition to income in the next, which also releases the expected credit loss (ECL) provisioned for the sold loans to further bolster income. Even though no additional revenues are collected, lenders can launder their risk to improve the image of their profitability, as was the case with Regional Management. This profitability is additionally transferred to investors through residual earnings, reflected in higher short-term stock prices and higher return on equity.

Asia-Pacific Predatory Lending: Weak Formal Institutions and Localized Trust

In the Asia-Pacific, lenders enjoy superior financial flexibility under relatively lax consumer protection regulations concerning the terms of collateralization they can impose on loan deals. Collateral-based lending is also historically entrenched [Suppiah Reference Suppiah2014], making it easier to enforce forfeitures. The localized nature of trust, embedded in dyadic relations between firms and consumers with less oversight from formal institutions, also gives rise to new forms of personal collateral. For instance, predatory lenders more commonly accept jewelry and small valuables as collateral than their counterparts in North America [Seibel Reference Seibel Hans2005]. These expanded forms of collateral are not only lucrative, but easily repackaged for sale through a network of vendors across different business segments, such as the retail and trading business.

Aspial Lifestyle, a pawnbroker based in Singapore worth $127 million, offers an illustrative case. In 2022, Aspial Lifestyle generated over $300 million in revenue, an increase of 40% from $220 million in 2021. Of that, a considerable portion—$51 million—consisted of interest income from pawnbroking services, compared to $46 million in 2021. To facilitate its successful cross-selling of collateral, Aspial purchased Maxi-Cash and a 65% stake in Maxion Holdings in 2022—both of them major pawnbroking chain stores in Malaysia— marking its regional expansion via acquisitions. Mergers and acquisitions are subject to less scrutiny by regulators in the Asia-Pacific than in North America. Due to its developmental history of attracting foreign direct investment (FDI) in the postwar period [Acemoglu, Johnson, and Robinson Reference Acemoglu, Johnson and Robinson2001], the region has encouraged mergers and acquisitions as a means of restructuring and FDI generation, rather than scrutinizing them on anti-competitive grounds as in the United States. After the Asian financial crisis, for instance, cross-border mergers and acquisitions were welcomed as a means of generating capital market inflow [Modi and Negishi Reference Modi and Negishi2000].

Singapore, arguably one of the most developed nations in the Asia-Pacific and a model of policy diffusion for the rest of the region, is illustrative. Even there, the Monetary Authority of Singapore focuses more on banks than consumer lenders [Fuda Reference Fuda2025], allowing Aspial to benefit from Singapore’s light-touch financial regulation and expand into looser markets still, where pawnbroking remains less regulated than banking. These weak consumer protection laws in the Asia-Pacific region enable predatory lenders to profit from special APR rules and collateralization conditions.

By headquartering in Singapore and expanding into Malaysia, moreover, Aspial (and Maxi-Cash and Maxion Holdings) capitalized on the lack of strict APR caps on pawn loans or personal loans in the two countries, where APRs of over 100% on pawn loans remain legal. In other countries like Indonesia and Australia, some regional caps exist, but enforcement remains weak. This has led to aggressive collateral seizures, whereby pawnbrokers like Maxi-Cash quickly auction forfeited items (sometimes below market value), with little oversight.

The loan amounts offered to consumers are decided by the value of the collateral pledged, but the value of the loans is always smaller than that of the collateral, unlike in North America. Collateralization thus makes even the riskiest borrowers profitable to lend to — namely, those who are socioeconomically disadvantaged. There are few jurisdictions with cooling-off periods, so unlike Europe, which has a 14-day right of withdrawal, borrowers in the Asia-Pacific cannot cancel loans without penalties. Repayment capacity is also unregulated in the Asia-Pacific, unlike under US CFPB rules.

With collateralization, credit risks become important sources of cash flow: collateral does not affect credit risk, but expected cash flows increase when they include cash flows from the sale of held collateral. Aspial went further, creating a new tranche of non-interest-bearing loans worth $19 million. Collateralization not only insured against credit risk (default) from loans, but transformed it into an opportunity for revenue growth when the firm mandated that the collateral be worth more than the loan itself. Individuals and small businesses who received loans from Aspial, for instance, were charged interest on loans secured by debentures over property and valuable goods (such as jewelry). In fact, Aspial not only declined to increase interest rates in 2022, but even cut them from 6 to 3%, which separates it from its American counterparts, who average 45% interest rates. Although its subsidiaries charge much higher rates at over 100% by structuring loans with high “administrative fees” or rollover charges to bypass nominal rate limits, Aspial’s own corporate strategy of lowering and even abolishing interest rates on loans are important counterpoints to North American characterizations of predatory lenders.

When borrowers enter bankruptcy, are forced into financial reorganization (e.g., by unemployment), or delay their payments, their loans are deemed impaired. Loan impairment does not, however, mean they will immediately be written off. At Aspial, defaulted loans are recovered by claiming the pledged collateral, repackaging it, and selling it to its jewelry and branded merchandise businesses. Thus, bad debt expenses at Aspial totaled $4 million, all of which was recovered through the forfeiture of collateral. Due to the region’s weak formal institutions [including juridical institutions; Dressel Reference Dressel2014] and cultural stigma surrounding debt, borrowers struggle to sue lenders effectively, even for illegal repossession. With few consumer protections, lenders also have no legal barrier to prevent them from profiting from financially desperate borrowers who lack legal recourse. These patterns of exploitation are recursive: by tapping into personal items like jewelry, lenders strategically seize forms of collateral that are hard to trace, further strangling any attempt at legal recourse.

Like North American regulatory capitalism, Asia-Pacific regulatory capitalism is characterized by a degree of regulatory fragmentation, where uneven regulation and monitoring across proximal nations creates opportunities for predatory lenders to pursue regulatory evasion by arbitraging looser markets. However, there is even less cohesion in the Asia-Pacific than in North America, since no centralized credit bureaus exist; this enables predatory lenders to target countries with fewer protections, circumvent requirements to check the creditworthiness of borrowers, and even loan stack by issuing multiple loans to the same borrower.

This regulatory evasion also manifests in other unique ways in the region, such as the practice of shifting to less-regulated loan products. To illustrate, similar to the tightening of “true-lender” protections in the United States, the Australian Treasury issued an amendment for the National Consumer Credit Protection Regulations in a new policy framework for financial sector reforms on May 11, 2023. The amendment improved consumer protections for small amount credit contracts (SACCs) through two mechanisms.

First, the amendment required licensees (lenders) to verify the financial circumstances of consumers, including their income statements, their social security status, and a novel item called available income that refers to income less amounts withheld by tax-related administration (Section 28HB). Second, the amendment (Section 28LCA) mandated that consumer repayments of their SACCs or any fees related to their SACCs be equal to or less than 10% of available income during their repayment period.

These amended ordinances might have been expected to devastate the lending business. By restricting consumer repayments to lenders, legislation was effectively placing a price cap on the revenues that lenders could generate. It would not matter, for instance, whether lenders charged high or low interest rates, if legislation prohibited them from claiming any more than a fixed proportion of any given consumer’s income.

But lenders did not, in fact, suffer. On the contrary, predatory lenders evaded these regulations not only to retain, but to increase profitability and launder risk. ash Converters, a prominent lender headquartered in Australia and worth over $100 million, offers an illustrative example. Cash Converters offers SACCs transacted either in store or online, worth up to $2,000 with a short-term maturity of one year. In response to the Australian financial sector reforms, Cash Converters executed two corporate strategies using connections with a network of collaborative firms.

Firstly, Cash Converters initiated a “strategic product transition away” (italics added) from the small loan product segment. The firm aggressively offered consumers an alternative product in the form of medium amount credit contracts (MACCs) and lines of credit (LOCs). These loans, though unsecured, are worth more: up to $5,000 for a maximum of 2 years under MACCs and $10,000 for a maximum of three years under LOCs. By transitioning consumers from short-term contracts to medium-term contracts, Cash Converters effectively shifted its sources of revenue toward a less-regulated tranche of loans with which it could exercise greater pricing flexibility.

Indeed, when Australian regulators moved to cap payday loan APRs, Cash Converters rebranded products as “medium-term instalment loans” although they still carried effective APRs of over 100% due to hidden fees, such as “account maintenance fees.” As part of this transition, the firm also managed to cross-sell new varieties of loans, including vehicle financing.

This transition was made possible by the company’s franchise model, which enabled it to pass risk to local operators. Through a subsidiary, Cash Converters maintained connections with over 100 pawnbrokers and dealers distributed nationwide. Situated as they were—on the frontlines, in direct contact with consumers—these pawnbrokers were key to marketing Cash Converters’ MACC products and negotiating their terms. The transition from short- to medium-term products bore fruit: both the firm’s medium loan and vehicle financing loan books grew by over 30% year-on-year in 2022 to over $100 million and $60 million, respectively.

Secondly, Cash Converters leveraged its international franchises to adjust its loan repayment practices. Under a franchise model, it holds operations in 13 countries across Europe, the Middle East, and the Asia-Pacific. In response to the Australian legislative price cap, Cash Converters turned its attention to regions outside Australia with less regulatory activity in financial reforms, such as Spain. There, Cash Converters expanded its commercial loans segment to external parties, requiring interest to be paid in a lump sum at the maturity date.

The deferred loan repayment model increased the appeal of the firm’s loans to a broader clientele through pawnbrokers and dealers, which allowed it to capitalize on inflationary pressures from 2022 to 2023. Annual inflation averaged 8% in 2022 and 4.1% in 2023. During this period, Cash Converters’ commercial loans expanded through its network of institutional brokers and helped increase its gross loan book to over $270 million, achieving a growth rate of around 25% year-over-year in 2022 and ultimately stabilizing revenues to offset the financial reforms in its home market of Australia.

European Predatory Lending: Coordinated Market Economies and Institutional Trust

Coordinated market economies in Europe are characterized by stringent regulations and strong institutions, which shape the strategies that predatory lenders in the region pursue. Before 2015, Helsinki-based Ferratum, with major operations in Germany, primarily offered unsecured payday loans with APRs exceeding 100% and no collateral, relying on aggressive collections to profit. However, in January 2015, the Financial Conduct Authority (FCA) implemented a price cap on high-cost short-term credit (payday loans), which limited the amount that lenders can charge to a maximum of 0.8% per day (including interest and fees) of the amount borrowed. Around the same time, in 2014, the Mortgage Credit Directive and the EU Consumer Credit Directive (CCD) were introduced to implement national interest-rate caps, mandate strict affordability/creditworthiness checks to ensure consumers’ ability to repay, and mandate cool-off periods for loans.

An important difference from North American and Asia-Pacific varieties of predatory lending here is that there is less room for regulatory arbitrage between different jurisdictions, given the increasingly unitary state of regulation in Europe. In Europe, post-2008 financial crisis reforms, some of them influenced by the Dodd–Frank Act in the United States, have increased scrutiny on loan origination practices, making it harder for predatory lenders to offload risky loans. Regulations like assignee liability provisions, which hold secondary market purchasers accountable for predatory practices with regard to the original loan, also discourage legitimate buyers from purchasing such loans. There remains some regulatory arbitrage, as illustrated by the UK-based firm International Personal Finance, which markets high-fee loans in Eastern Europe (e.g., Poland) where regulations are weaker, and Ferratum, which operates in Lithuania under lighter rules whereby cross-border lending is poorly harmonized.

However, these loopholes are tightening as the EU moves toward uniformly applying a single rulebook on lending across EU member states, with the European Banking Authority (EBA) overseeing convergence. These rules are enshrined in the Capital Requirements Regulation (CRR) and Capital Requirements Directive (CRD4), which advance the CCD and implement Basel III standards, with recent updates in the 2024 Banking Package introducing stricter technical standards for capital adequacy, liquidity (e.g., Net Stable Funding Ratio), and risk management. Although the Basel III is a universal framework, the EU is unique in its implementation of the CCD on an EU-wide harmonization basis, which binds all 27 member states to uniform consumer protection standards.

Thus, even though lenders like Ferratum have adapted partly by relying on mixed collateral including property, they have largely sought to evade these regulations by pivoting to insurance products (e.g., credit life insurance), which are less subject to strict repossession laws. International Personal Finance offers SACCs and MACCs to consumers as well as collateral protection insurance through pawnshops. The firm goes further by using firm representatives to visit the homes of low-income borrowers to market these insurance products, where they also sell mobile wallet and hybrid loans (a combination of in-person and digital loan services) to those who do not qualify for digital loan offerings from traditional banks.

Consistent with coordinated market economies, high institutional trust in the region assigns greater value to credit ratings and greater authority to credit ratings agencies themselves [Zucker Reference Zucker1986]. While this has the benefit of facilitating transactions, it raises credit risk issues reminiscent of the subprime crisis, when credit ratings agencies assigned AAA-grade ratings to subprime mortgages that were packaged into CDOs, which later imploded when mortgage defaults spread through the financial system. As regulatory capitalism theory would assert, these risks are an artifact of a major contradiction in capitalist systems, even more so in coordinated market economies: credit ratings agencies are delegated regulatory powers and act as de facto regulators, empowered to assess risk despite being financially dependent on the very institutions they are rating [Parker and Nielsen Reference Parker and Nielsen2009].

Predatory lending in Europe illustrates how these risks are institutionalized in high-trust market economies, when governments outsource regulation to private firms, but the high-trust nature of these markets insulates them from scrutiny. As Carruthers [Reference Carruthers2013] argues, institutional trust when reified tends to mask the conflicts of interest and hidden agendas of credit ratings agencies. In the years leading up to the subprime crisis, credit ratings agencies rated CDOs AAA to place them in the same category as AAA corporate bonds, in order to “domesticate” them and generate public interest in purchasing CDOs structured by the investment bank clients of these very same credit ratings agencies.

As such, lenders pursue a new form of regulatory evasion, namely, issuing bonds to finesse credit ratings. Credit ratings determine the default risk of loans, and by extension, the amount of ECL that lenders must reserve. ECLs are typically calculated using input parameters that include exposure at default (EAD), probability of default (PD), and losses in the event of default (LGD), the product of which equals the ECL a firm should reserve. Assessments by credit ratings agencies have an effect on ECL calculations, for when the credit rating of the borrower falls, the PD rises, and the ECL that a firm must reserve rises accordingly.

IFRS9 guidelines stipulate a three-stage model for assessing credit risks, and by extension, the ECL allowance that lenders need to reserve. Stage 1 indicates no deterioration in credit risk; here, lenders are obliged to make ECL provisions equal to the expected loss on the contract during the next one-year period only. Stage 2 is when loans are deemed “impaired” and is associated with a higher PD (and ECL). Finally, Stage 3 is when contracts are deemed “nonperforming” and PD (and ECL) is highest. For contracts in Stage 2 or 3, ECLs rise exponentially from Stage 1, as they must cover the expected loan losses during their entire lifetime, rather than just the next year.

Predatory lenders are thus faced with a conundrum. On the one hand, high-credit-risk borrowers (and their loans) offer the highest yield in interest rates, and these customers are the most likely to purchase vertically differentiated products. On the other, the riskiest loans (closest to being “nonperforming”) pose a firm-level risk to the balance sheet as they require increasingly high ECLs that transform funds from assets into liabilities and worsen profitability. How do predatory lenders circumvent the risks inherent in loans to high-risk defaulters? To resolve this problem, lenders consistently launder the firm-level risk posed by their borrowers’ financial instability.

The firm-level risk that lenders face was compounded by a vulnerability to macroeconomic distress in 2022 and 2023. High inflation in the United States, Europe, and the Asia-Pacific—reaching levels of 8% or upward—prompted central banks to raise interest rates from close to 0% to over 5%. The combination of inflation and high interest rates increased prices while lowering real incomes and jeopardizing employment. Financial precarity among borrowers consequently increased their credit risk and raised the likelihood that their loans would shift into impairment (Stage 2) or nonperforming (Stage 3) status, as was observed with World Acceptance Corp, which saw a record net charge-off rate of 23.7% across its loans.

This precarity and contagion of credit risk held true across lenders in the sample. At the Germany-based firm Ferratum Capital, for instance, impairment losses rose from just €900 in 2021 to over €100,000 in 2022. During the same period, the firm owed close to €40 million to its parent company Multitude SE, whose Fitch credit rating stood on the brink of a downgrade. Macroeconomic uncertainty caused by COVID-19 had already led Fitch to downgrade Multitude SE’s credit rating from BB- to B+ and its outlook from “stable” to “negative” in 2020. Another downgrade would have constituted a significant increase in credit risk (SICR) trigger, which would have resulted in a substantially higher PD, and by extension, a larger ECL that would detract from Ferratum’s earnings. To avert this outcome, both Ferratum Capital and Multitude SE turned to their investors for a lifeline by issuing bonds and effectively laundering their risk.

Bond issuance is a strategy to raise capital by issuing notes (debt) for purchase. In early 2022, Ferratum Capital placed €40 million in senior unsecured bonds to investors, followed by Multitude SE, which separately issued €50 million later in the year. The fresh inflow of funds enabled the firms to escape temporarily alleviate firm-level credit risks, prompting Fitch to rerate Multitude SE’s credit rating to BB- and its outlook to “stable.” Ferratum’s bond issuances appealed to institutional investors seeking high-yield debt, legitimized by credit ratings agencies, but which obfuscated the underlying risks.

Indeed, diverting investor capital through new bonds to service existing bonds does not alleviate the problem: instead, it obscures the financial weaknesses of both firms. As a result, Ferratum was driven to buy back and retire the bonds, even when doing so resulted in a purchase price of over 100% of their face value, a costly use of capital.

Conclusion

This article illustrates important regional varieties of regulatory capitalism in the predatory lending industry. Although predatory lenders commonly use collateralization, regulatory evasion, and risk laundering as core profit-making strategies, closer inspection reveals the different forms they assume by region, shaped by their developmental histories and varieties of capitalism.

In North America, a region characterized by liberal market economies, collateralization prioritizes scalable resale markets through pawnshop chains. Meanwhile, regulatory evasion tends to rely on legal arbitrage across states and jurisdictions in a fragmented regulatory environment. The preeminence of investors and short-term profitability for stock improvements also leads to risk laundering in the form of secondary market sales, such as when NPLs are offloaded to investors and other collectors. Through relations with investors, firms recycle bonds and nonperforming loans in exchange for fresh capital to alleviate the immediate demands of current debt repayment, even at the cost of inflating future debt.

In the Asia-Pacific, where microloans are historically entrenched, collateralization emphasizes cross-sector synergy in the microscale personal items, such as gold and personal jewelry, that are sold as retail inventory and are difficult to trace. Given that formal institutions are weak and central credit bureaus are scarce, consumer protections lag behind those of counterpart regions, enabling regulatory evasion in the form of product substitution—such as firms swapping out MACCs for SACCs or pivoting to insurance products—and risk laundering by shifting operations across the region.

In Europe, characterized by coordinated market economies with strong consumer protections in the CCD that are uniformly applied in the region, firms have largely pivoted away from collateralization as a profit-making strategy and toward bundling their collateral with insurance as a means of evading regulatory frictions. High institutional trust in these economies, rooted in a legacy of strong bank–firm relations, becomes a double-edged sword by legitimizing bond-based risk laundering.