Man hat behauptet die Welt werde durch Zahlen regiert; das aber weiß ich, daß die Zahlen uns belehren, ob sie gut oder schlecht regiert werde (J.W. von Goethe)Footnote 1

It has been said that the world is ruled by pay; but this I know that from figures we learn whether it is well or ill ruled.

1. Introduction

The question of fair profits has been asked ever since modern finance has emerged. During the Middle Ages, it related to the question of usury and the critical distinction between business profit-sharing and exploitative financial gains. With modern economies and the advent of classical economic theories in the 19th century, usury was claimed to be a virtuous sin which eventually (and supposedly) profits both sinners and society. More recently, this position was reframed and reshaped through shareholder value and shareholder primacy, which uphold the allegiance of business and society to financial investors active on unfettered transnational financial markets. The ‘North-Atlantic’ financial crisis of 2007–08 exposed this alleged ‘end of history for corporate law’, reopening an evergreen debate on finance and society.Footnote 2

In this context, my contribution provides a theoretical analysis of the notion of business profits, addressing the overarching accounting instruments that the law – comprising public and private arrangements, legal rules and social norms – puts in place to define and control for those corporate profits. The question of fair profits is inseparable from how profits are represented through accounting norms, and it cannot be properly addressed without looking at the underlying accounting system. My analysis is organised in two parts.

The first part addresses two ideal types of financial accounting design, contrasting: (i) an accounting system that purports to measure shareholder wealth through a fair value accounting model; (ii) another accounting system that purports to determine satisfying corporate profits through a historical cost accounting model.

The second part discusses implications for corporate fairness and sustainability according to this dualistic approach which contrasts maximising (shareholder) value and satisfying profit-sharing, the former being framed by an unsustainable multiplicative process, with the latter by a sustainable additive one. These implications concern the representation of corporate profit as much as the question of what constitutes responsible corporate conduct.

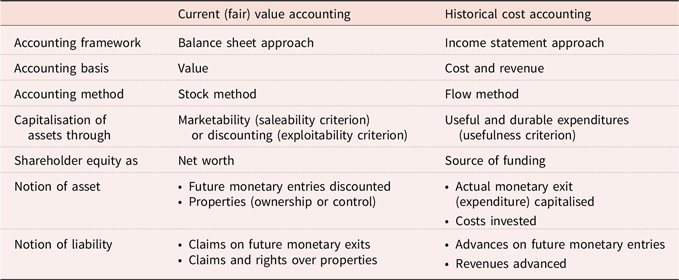

This analysis develops a constructive critique of the fair value accounting model while extending the historical cost model to cover social, environmental and governance considerations. As a matter of fact, both models co-exist in accounting theory and history and have been relied upon to keep corporate affairs accountable; recently, fair value accounting gained momentum between the 1980s and the 2000s. Concerning corporate profits, fair value accounting belongs to current value accounting models which are based on a balance sheet approach. Accordingly, corporate profits and losses are accounted for through a direct connection between measuring assets (pointing to accrued future profits) on the left side and measuring liabilities (pointing to accrued future losses) on the right side of the balance sheet. Corporate profits are assessed as the difference between these two current values (net equity is consequently understood as net worth). From this static accounting perspective (which is static because its measurements are established at an arbitrary point of time), the income statement lost its featuring contribution and can be diluted into the balance sheet. Quite the contrary, historical cost accounting is based upon an income statement approach. Accordingly, accounting must acknowledge that the business process occurs through time and hazard, involving an unfolding occurrence of overlapping operations and events; therefore, future values cannot be reliably forecasted today and may never realise. Therefore, the income statement is prioritised by recognising accrued revenues and incurred expenses over the current period; corporate profits and losses are determined through the difference between these two economic flows. At the same time, the left side of the balance sheet disentangles short-term assets that are likely to be realised (inventories and commercial financial papers) from longer-term assets that represent investments in corporate resources with future use and lifespan; the right side disentangles short-term liabilities that are likely to be due soon (commercial debt obligations) from long-term liabilities and equities which represent provisions and future obligations to stakeholders including creditors and shareholders.

This theoretical analysis aims to shed (some) light on the functional definition of corporate profit and its implications for corporate management and redistributive justice. It further highlights limits and shortcomings of resource valuation and net profit determination as suitable instruments to address matters of corporate sustainability and corporate social responsibility.

2. Accounting for corporate profit: enterprise, money and time

The Merriam-Webster dictionary defines profit as ‘the compensation accruing to entrepreneurs for the assumption of risk in business enterprise as distinguished from wages or rent’. But anything goes with profiting. The same dictionary stigmatises profiteers as those ‘who make[] what is considered an unreasonable profit especially on the sale of essential goods during times of emergency’, swindlers who ‘obtain (take) money or property (from) by fraud or deceit’, ‘dishonest person[s] who use[] clever means to cheat others out of something of value’.

This understanding still resonates with, and retains elements of, the 19th-century mindset, that is, at the epoch when modern economy and modern economic thinking emerged. At that time, notions of profit related to entrepreneurs and entrepreneurial ventures. Corporate and family patrimonies did often mingle together and so did enterprise capital and personal ownership.

When functional and institutional separation between management, control and ownership emerged between the end of nineteenth and early 20th century,Footnote 3 the understanding of profit shifted from individuals to business firms, raising the question of corporate profit.Footnote 4 Corporate profit accrues from investing into enterprise capital, and constitutes a surplus generated beyond financial or real maintenance of that capital over time.Footnote 5 Since those investments are financial or assessed in money terms, corporate profit relates to money. Since enterprise activities take time and organisation to generate that surplus, corporate profit relates to socioeconomic processes of economy and the flow of time.

From their emergence, accounting systems have assisted and facilitated business ventures. Modern corporate ventures are no exception. Accounting has been expected and required to provide a ‘true and fair view’ on corporate affairs.Footnote 6 A true and fair notion of corporate profit refers to, and depends on, an accounting system which enables corporate profit to be ascertained.Footnote 7 An accounting system defines, classifies and structures financial and non-financial flows and stocks which constitute enterprise capital and income. This system is then essential to define the net income that remains after capital has been maintained.Footnote 8 The link between the accounting system and the business firm shows the importance of the legal and institutional framework regulating corporate affairs for the benefit of economy and society.Footnote 9

From this institutional economic perspective, accounting systems are institutional arrangements which enable representation of and control over corporate affairs. They comprise a variety of dimensions: technological, organisational, institutional and ideational. The following analysis focuses on the last two dimensions. Accounting design – that is, accounting models which provide conceptual frameworks for accounting systems – is an integral part of the institutional structure that frames and shapes ongoing corporate affairs. Indeed, accounting is an institution of economy and society.

When the corporate ‘revolution’ (in Adolph A Berle’s words)Footnote 10 occurred between the last three decades of the nineteenth and the first decade of the 20th century, debates emerged around the world on the most appropriate way to account for business enterprises and the business profit.Footnote 11 With the Wall Street crash of 1929 and the historical rupture caused by the Great Depression, the so-called historical cost accounting model eventually prevailed that combined historical cost accounting basis, the flow method and the entity theory of accounting. It was preferred to an alternative current value accounting model that combined current value accounting basis, the stock method and the proprietary theory of accounting. However, through the last three decades of the 20th century and the North-Atlantic financial crisis of 2007–08, an influential shareholder value ideology prompted an ‘accounting revolution’, renewing and transforming a current value accounting model into the so-called fair value accounting model.Footnote 12

A. A tale of two business models featuring two distinctive accounting models

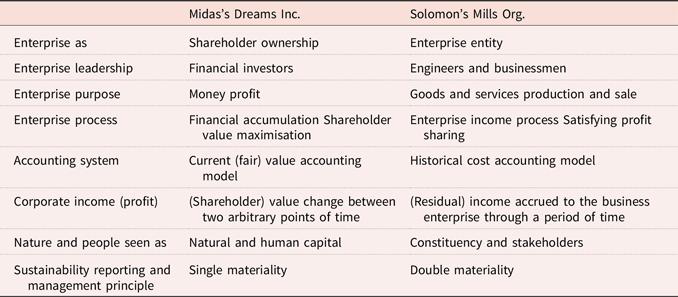

For the sake of simplicity, our analysis draws upon this dualistic approach that opposes the historical cost accounting model to the fair value accounting model, which features within a broader contrast between alternative business models. Each model is formed by combining responses to sets of binary options. Before entering into a more technical discussion (Table 2), let us tell a tale of two enterprises featuring each of these two business models and their related accounting logics (Table 1). On the one hand, Midas’s Dreams Inc. accounted for at fair value; on the other hand, Solomon’s Mills Org. accounted for at historical cost.

A dualistic approach contrasting two distinctive business models and related accounting logics

A dualistic approach contrasting two distinctive accounting models

Midas’s Dreams Inc. is a financial investment vehicle established by a posse of legal advisors and financial investors providing equity funding to their financial venture. The enterprise’s purpose is to maximise financial return over invested funds. As an organisation, Midas is pervaded by money profit motive. Since ‘Cash is King’ and ‘Time is Money’, the so-called ‘time value of money’ is dictated by benchmarking financial returns by reference to alternative financial investment opportunities. A financial logic of accumulation at compound return (the multiplicative process) drives the determination of corporate profit, on the basis of current value accounting.Footnote 13 Midas’s organisation understands the resources of the enterprise through a money lens. Everything has a financial value expressed in money terms and that value depends on potential exploitation and tradability. Even nature and employees are resources assessed in money terms, hence the terms ‘natural capital’ and ‘human capital’. Midas’s touch dreams of transforming everything into gold.Footnote 14

Solomon’s Mills Org. is an enterprise entity established by an alliance of engineers and businessmen purporting to provide goods and services to customers. The enterprise’s purpose is then to ensure this provision over time and circumstances. Solomon’s organisation is driven by other people’s utility motive, since customers are expected to pay for merchandise useful to them, comparing Solomon’s merchandise with that offered by other producers. A satisfying logic of income at simple return (additive process) drives the determination of corporate profit, on the basis of historical cost accounting.Footnote 15 Solomon’s organisation understands enterprise resources as a means of production and sale, disentangling financial and extra-financial resources. Nature and people are not deemed to be capital and do not need to be assessed in money terms, although the enterprise entity does often pay for costs and disburse for expenditures related to both.Footnote 16 Solomon’s business judgement savvies and prizes above all being fair and responsible in doing business inside and outside the going concern.Footnote 17

The notions of corporate profit that feature in the two business models are structurally different.Footnote 18 At Midas’s Dreams Inc., profit is understood as a change in the value of shareholder wealth between two arbitrary points of time. It does not necessarily depend on business results. If an asset revaluation implies an asset value change, that change is included in corporate profit; if a liability revaluation implies a liability value change, that change is also included.Footnote 19 Quite the contrary, at Solomon’s Mills Org., profit is understood as net income accruing to the enterprise entity through a period of time. It depends on business results, which match revenues accrued from customers to expenses incurred to produce and sell merchandise to them. Assets and liabilities are not re-evaluated through time, and their value changes are not included in corporate profit unless those accounting elements are either liquidated through a business transaction or permanently impaired.

B. Two alternative accounting models for corporate profits

These two distinctive notions of corporate profit cannot be defined and enacted without the two distinctive accounting models which subsume here the two main families of accounting systems, namely those based on value and those based on cost (Table 2). In order to account for corporate profits, accounting systems organise a structured representation of ongoing enterprise activity through time and circumstances. This representation (implying warranty) involves a semiotic system of recognition, classification and determination which does not depend on the real ‘objects’ to be accounted for. Quite the contrary, the system establishes, construes and enacts accounting elements which are symbols of those ‘objects’. Although accounting systems may be and have been denoted in quantities, corporate accounting does deploy money as an accounting unit which is a symbol of reality.Footnote 20

This symbolic dimension of accounting being virtual and artificial, socio-economic actors may imagine infinite variants of the accounting system, as long as they are ready to afford the far-reaching consequences of its unfolding implementation. Accounting systems are instrumental to a corporate purpose and serve a corporate organisation that shall function (and may be dysfunctional) in view of the pursuit of that purpose. Those systems therefore contribute to manage and govern the socio-economic organisation that is the business firm through time and circumstances.

Under the current value accounting model, the accounting masterpiece is the balance sheet. Objects to be accounted for are eligible to become accounting elements as long as they can be recognised as an ‘asset’ or a ‘liability’ on the balance sheet, which provides for an inventory of corporate objects on hold. Accordingly, accounting elements are deemed to be stocks accounted for at their current value, which may depend either on the marketability of the underlying object through a potential market sale transfer (saleability criterion), or any future financial returns to its holder embedded into that object (exploitability criterion).Footnote 21 Accordingly, assets denote values of future monetary entries (from sale or exploitation), while liabilities denote values of outstanding claims on future monetary exits, both discounted at current values. Profits and losses result from change in those values between the two points of time at which the inventory is updated. Shareholder equity results from the netting between all these values, embedding an implicit compound return process (multiplicative) at discount rate(s) of reference.

Under the historical cost accounting model, the accounting masterpiece is the income statement. Objects to be accounted for are eligible as long as they can be recognised as past, present or future expenses and revenues to the business firm. Realised revenues and incurred expenses are accounted for through the income statement of the period of reference. Recognition of assets and liabilities depends on this income generation process which is unfolding through time. Under a cost basis of accounting, cost-based assetisation occurs as capitalisation of expenditures which were incurred to acquire ‘objects’ that are expected to remain useful and in use beyond the current period (invested costs),Footnote 22 while outstanding liabilities involve advances on future revenues from customers (revenues advanced). Incomes to the business firm are generated by the difference between revenues and expenses, pointing to an additive process that remunerates shareholder equity as well as other stakeholder contributions to production and sales. Shareholder equity operates here as one among several sources of funding and is not expected to receive all the enterprise income which is accrued. Entity equity may be and has been disentangled from shareholder equity in order to account for retained earnings and other provisions established to maintain and sustain the ongoing enterprise process.Footnote 23

From a fair value accounting perspective, all the elements on the balance sheet are made homogeneous by money valuation. Positive values are assets, negative values are liabilities, and some elements may even shift between the two or combine them. For an accounting element to be recognised, it is then sufficient to embed those values (or some grouping of them) into a legally manipulable object (unbundled property rights), or a value difference between two outstanding legal-financial positions. The legal paperwork provides all the reality that this accounting token requires to be enacted. This stock accounting focus implies a value-based understanding of corporate profit, driving the business purpose toward shareholder net worth expressed in current money terms at one arbitrary moment in time. Enterprise risk-taking is represented here through financial risk assessment by compound discounting of the future.Footnote 24

This value-based approach does not require realisation of values through actual transactions, although those values might prove illusory through time and hazard, if not realised. At the beginning of the 20th century, prudent static accounting theorists – such as Fabio Besta and James Cummings Bonbright – amended the balance sheet approach by referring to historically realised values as the best benchmark to determine corporate profits (and other accounting elements). Nevertheless, dynamic accounting theorists – such as Gino Zappa and Ananias Charles Littleton – went further through a flow accounting focus. Accordingly, the enterprise activity flows through time and circumstances; this flowing – rather than any corporate properties (or unbundled property rights) held – generates income to the enterprise by matching revenues from customers and wages to employees, among other flows. Enterprise risk-taking is represented here by acknowledging that the future is unfolded and hazardous; the accounting system is then designed to track the unfolded and uncertain enterprise entity process over time and circumstances. As AC Littleton noted:Footnote 25

[One accounting belief is] that income cannot arise directly from new investments or borrowings, or by action of owners in creating an item in their accounts called ‘goodwill’, or by owner action in re-pricing assets already possessed. The reason for this view […] is that no service has been rendered by this enterprise in connection with these purely financial actions.

Two illustrative examples may further clarify the difference between (and the consequences of) the two accounting perspectives: accounting for business combinationsFootnote 26 and for pension schemes.Footnote 27

From a value-based accounting perspective, a business combination between two accounting entities is a financial market transaction between a buying acquiring entity and a selling third party who is willing to transfer a sold entity against a consideration. Consequently, the acquiring entity does re-evaluate at current values all the accounting elements of the acquired entity, adds other internally generated value elements which were not previously recognised, and capitalises the residual difference (if positive) between the consideration paid and the re-evaluated net assets as goodwill. The latter element does account for and depend on future cash proceeds which are only presumed at the time of recognition.Footnote 28 Under this accounting representation, the expenditures spent to achieve the business combination are not deducted from current revenues to account for corporate profits. And the equity reserve generated by goodwill capitalisation may be made immediately distributable to shareholders.

From a cost-based accounting perspective, a business combination is the coming together of two accounting entities which were previously autonomous from each another. Consequently, the combined entity aggregates all the accounting elements of both entities class by class, without recognising any goodwill, without net assets revaluation and without recognition of internally generated values.Footnote 29 Incurred disbursements to perform the combination are either expensed immediately, or capitalised as invested costs over a relatively short period of time. Accordingly, future benefits from a business combination may be eventually realised through revenues in future periods, but they cannot be accounted for today.

Concerning the accounting for pension schemes, from a value-based accounting perspective, pension benefits result from individual employees’ pension funds accumulated and invested through time. They do not fundamentally differ from financial investment funds that may generate (or not) some future uncertain proceeds to their holder. Being assimilated to a financial investment, pension schemes are then assessed at net current values; outstanding cumulated funds may be embedded in financial entitlements which may be transferable and even liquidated before retirement time. The employing entity may account for employee pension benefits either as a contribution to an independent pension fund (which assumes the pension payment responsibility), or as a change of value in the underlying pension scheme.

From a cost-based accounting perspective, corporate pension schemes prolong the employer’s commitment to pay wages beyond employment time, with a view to support retired employees through their old age. Ongoing pension payments are expensed during the period, while future payments may be provisioned by employer(s)/employee(s) cost-sharing schemes accounted for on a future cost basis.

In a nutshell, value-based assetisation transforms business firms into commodities that can be traded at financial market values (commodification),Footnote 30 and pension schemes into financial investment vehicles. On the contrary, a cost basis of accounting considers business firms as going concerns and pension schemes as intergenerational corporate solidarity arrangements.

Value-based assetisation and current (fair) value accounting have become prominent during the last decades of the 20th century and the first decade of the 21st century, involving dramatic consequences for both corporate and financial market affairs. Beyond goodwill from acquisitions and pension scheme reforms, securitisation enabled financial marketability of financial (or financialised) ‘assets’ that used to stay on the creditor balance sheet, under the creditor responsibility. More recently, tokenisation promises to push this financialisation even further, by enabling monetisation of those ‘assets’ through digital platforms.Footnote 31 The next section shall explore some implications of this trend for corporate fairness and sustainability.

3. Implications for corporate fairness and sustainability

As a matter of fact, accounting systems are complex and evolving artefacts in which both ideal types and both models coexist, namely fair value and historical accounting models. But it is quite undeniable that a fair value accounting model was promoted and enacted by US and international accounting standards-setters (respectively, the Financial Accounting Standards Board – FASB and the International Accounting Standards Board – IASB) since the 1970s.Footnote 32 These reforms brought current value measurements into corporate accounting systems, making the latter more dependent on benchmark market pricing for assets and liabilities. Although general purpose financial reporting was not designed to show the value of a reporting entity, its aim has nevertheless been to provide information to help existing and potential financial investors, lenders and other creditors to estimate that value.Footnote 33 They will do so by focusing on the amount, timing and uncertainty of (the prospects for) future net cash inflows to an entity and management’s stewardship of the entity’s economic resources.Footnote 34

Accordingly, the reporting entity and its accounting system do respond to and prioritise the information needs of financial investors, when estimating the value of the corporate entity. Management is expected to take on the stewardship of resources committed by investors to that entity, as Middle Ages stewards took care of a large household on behalf of its owners. And ‘a profit is earned only if the financial (or money) amount of the net assets at the end of the period exceeds the financial (or money) amount of net assets at the beginning of the period, after excluding any distributions to, and contributions from, owners during the period’.Footnote 35

From this shareholder ownership perspective, the enterprise entity works to enrich financial investors and maximise shareholder wealth. All the surplus remaining after having maintained that wealth belongs to them and is accounted for as corporate profit.Footnote 36

Fair values of assets and liabilities (accounting elements) are supposed to be the accounting measurements which fit best with this shareholder value-oriented approach. ‘Fair value is the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date’,Footnote 37 reflecting ‘the perspective of market participants – participants in a market to which the entity has access’.Footnote 38 Consequently, accounting representation drifts away from playing a structuring role for the enterprise as an economic institution and organisation, towards being a provider of information about the enterprise as a financial investment from a financial market viewpoint.

To be sure, fair value benchmarking to external markets does not imply actual arm’s length transactions with independent third parties.

In some cases, fair value can be determined directly by observing prices in an active market. In other cases, it is determined indirectly using measurement techniques, for example, cash-flow-based measurement techniques […], reflecting all the following factors: (a) estimates of future cash flows; (b) possible variations in the estimated amount or timing of future cash flows for the asset or liability being measured, caused by the uncertainty inherent in the cash flows; (c) the time value of money; (d) the price for bearing the uncertainty inherent in the cash flows (a risk premium or risk discount). The price for bearing that uncertainty depends on the extent of that uncertainty. It also reflects the fact that investors would generally pay less for an asset (and generally require more for taking on a liability) that has uncertain cash flows than for an asset (or liability) whose cash flows are certain; (e) other factors, for example, liquidity, if market participants would take those factors into account in the circumstances.Footnote 39

A. How does fair value accounting affect true and fair and sustainable profits?

There is no doubt that the fair value accounting model brings a financial market perspective on the enterprise entity and its resources. Corporate profit is clearly defined as the residual return of owner equity capital, as if shareholders own both the enterprise and its resources.Footnote 40 And the enterprise process is dictated by time value of money featuring compound discounting embedded in financial appraisal techniques.Footnote 41

This accounting system certainly talks the language of financial market participants, but how does it sound when matters of corporate accountability and responsibility are concerned? Does it contribute to eventually making the enterprise entity a fair and sustainable going concern over time and circumstances? How does it affect the accounting for true, fair and sustainable profits?

Generally speaking, at initial recognition, an asset expected to generate positive benefits gets a higher fair value amount, while a liability may get a lower fair value amount (due to credit risk assessment), in comparison with the respective nominal amounts which would be accounted for according to historical cost accounting basis.Footnote 42 Recognition of net profit – if assessed as the difference between asset and liability values – is then moved backward to the present time. An overall misunderstanding occurs with this appraisal-based accounting basis, since an enterprise venture is not generally supposed to hold accounting elements (economic resources) in view to benchmark them on markets of reference over time.Footnote 43 As a matter of fact, an evolving enterprise process commits and transforms resources to produce and sell goods and services, incurring liabilities which are expected to be repaid when they become due, and committing equities which are supposed to be maintained through time. Among those equities, some originate in transactions with shareholder equity investors, others occur due to unfinished and unfolding enterprise cycles (enterprise entity equity). Consequently, enterprise income is generated and possibly distributed or retained only if and as long as this enterprise process goes on.Footnote 44

From this enterprise process viewpoint, accounting for enterprise assets and liabilities at discounted present values involves anticipating future positive flows and postponing future negative flows, both unrealised at the time of reporting. A prudential paradox is triggered here since the more enterprise credit risk degrades, the more negative flows embedded in present values are lowered (reducing liability values). And an entrepreneurial paradox is triggered as well, since the more invested assets are risk-taking, the more positive flows embedded in present values are lowered, in comparison with historical cost accounting basis.

Concerning profit determination, the net value appraised by balancing present values of assets and liabilities does not match with net cash funds available for payments when they become due. This mismatch occurs since an implicit reinvestment hypothesis is embedded into the discounting logic.Footnote 45 This mismatch implies that payments based upon those values are not necessarily covered, affording the hazard of financial distress triggered by being unable to pay. Moreover, when net profit is computed at initial discounted present values at injection and through discount unwinding over time, capital gain and net profit recognitions and possibly distributions will be moved backward to the present, while future changes in discount rates of reference will affect profit and capital measurements. Consequently, unrealised paper profits may be recognised and distributed, and balance sheet elements inflated or deflated hazardously over time and circumstances. Last but not least, compound return embedded into compound discounting (multiplicative process) provides a materially higher return even at a lower discount rate when compared with simple return (additive process) embedded in a cost basis of accounting.Footnote 46

Furthermore, fair value makes accounting numbers dependent on sophisticated actuarial techniques which rely on forecasts and forecasting models, opening the door to structuring opportunities and manipulation of accounting representation. Value-based assetisation and related commodification, securitisation and tokenisation pave the ways to cheating by ‘false tokens’, implying the use of cleverly engineered or deceitfully contrived accounting elements in the view to assist misrepresented, if not false and fraudulent, business transactions.

In sum, the accounting structure of the enterprise entity is not neutral to corporate income determination and distribution. Fair value and discounting introduce financial market logic into accounting for corporate profit; this logic proves to be at odds with prudential and entrepreneurial needs by anticipating unrealised profits and postponing unrealised losses: on the one hand, it enables fictitious dividends distribution, on the other hand it threatens the very corporate capacity to generate future earnings on which the expected financial value is based upon. Therefore, fair value does undermine the fairness of corporate profit, meaning its basic legitimacy for business and society. As a whole, what is a corporate venture remunerated for? True, fair and sustainable profits accrue as far as products and services are delivered to customers, wages are paid to employees, and debts are repaid to creditors through time and circumstances. Those profits do not occur – truly, fairly and sustainably – if corporate output is not delivered, if revenue from customers is not payable, or when excess distributions are detrimental to employee and creditor protection. And this line of reasoning may be consistently extended to environmental protection and corporate social responsibility as well.

B. Fair value accounting and financialisation

Educating the ‘ideal businessman’ in 1675, Jacques SavaryFootnote 47 alerted against the desire ‘to make oneself rich in dreams, by imagining that one can own an asset which cannot yet be used’.Footnote 48 But this and other past lessons were forgotten between the 1980s and 2000s, a time dominated by the ‘popular confusion’ (in Joseph Alois Schumpeter’s words)Footnote 49 between money and wealth. In the corporate world, executive managers and asset managers (financial market investors and traders) were convinced that getting more money would mean becoming richer. In the financial world, non-bank financial institutionsFootnote 50 went ahead seeking to make more money while pushing for legal rules and social norms enabling this quest – to the point of disrupting the financial and economic system as a whole in 2007. Figure 2 provides evidence of this increasing money-making by non-bank financial institutions.Footnote 51 Such an epochal ethos of financialisation resonates with the last three decades of the 19th and the first decade of the 20th century stigmatised by AA BerleFootnote 52 as a ‘plutocratic age’ in which ‘all judgments in America were ultimately made by wealth’.

Through the financialising escalation up to the 2007 systemic rupture, the reforms introducing fair value accounting standards, driven by international accounting convergence,Footnote 54 were consistent with enacting unfettered transnational financial markets. Meanwhile local corporate regulations concerned with distributions to shareholders were relaxed, thus enabling distributions of mark-to-market unrealised capital gains on financial instruments held by corporations.Footnote 55 The share of financial earnings in total corporate profits increased substantially.Footnote 56 Under fair value accounting, the rise (and fall) of securities market prices impact directly both the balance sheet and the income statement of trading portfolios. Holding entities are then enabled to both accrue unrealised (paper) profits on their holdings, and inflate balance sheet asset values of held portfolios. Thank to this accounting dream of wealth, even if only a relatively small share of securities change hands, all the securities are re-evaluated accordingly; and, in case of mark-to-model (levels 2 and 3 fair values), market transactions may not have occurred at all; or they may occur among related parties and within the same financial holding conglomerates.

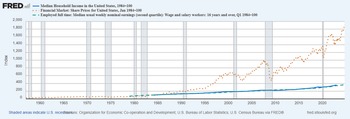

Consistently with this epochal ethos, the North-Atlantic financial crisis of 2007–08 was promptly called a ‘liquidity’ crisis, and mass injection of fresh money by governments and central banks was the response to that systemic crisis.Footnote 57 In this way, public institutions rescued and validated the private money-making machine put in place since the 1980s.Footnote 58 However, even though the interbank credit crash recalls liquidity crises of the past, careful attention to empirical evidence on price levels for cars, houses, and other assets, including financial assets (Figure 3), as well as empirical evidence of monetary aggregates (Figure 1), go against a lack of liquidity as the proper explanation of the systemic rupture. Quite the contrary, some facts argue for excess liquidity that drove financial speculative waves, including overwhelming inflation of financial securities and real estate prices,Footnote 59 along with an excess of liquidity generated by securitisation (that is, tokenisation and commodification) of sophisticated financial instruments that displaced some financial investments in the realm of money, giving them an apparent monetary dimension (Figure 2).Footnote 60

US money aggregates since 1959 (USD Billions): M1; M2 (narrow definition by Ihrig et al 2021); M2 (standard definition including money market funds); M3.Footnote 53

US money multipliers upon central bank reserves of depository institutions since 1981: ratios of M2 (narrow definition by Ihrig et al 2021), M2 (standard definition) and M3 over those reserves.Footnote 61

In the dramatic aftermath of the 2007–08 crash, the Bank for International SettlementsFootnote 62 warned that ‘financial booms sprinkle the fairy dust of illusory riches’. Money flows revolving into financial market speculative bubbling affords the hazard to redistribute purchasing power across economy and society without generating anything but self-serving financial wealth accumulation for the happy few (Figure 3),Footnote 63 triggering yet further financial bubbling and ever-increasing wealth inequality.Footnote 64

Comparison of US indexes (1984 → 100) for: Financial market share prices (2023.01.01 → 1542.4); Median household yearly income (2023.01.01 → 359.5); and Median usual weekly nominal wage and salary worker earnings (2023.01.01 → 341.1).Footnote 65

4. Fair value accounting and the issue of corporate sustainability

So far, fair value has proved to be unfair and irresponsible when corporate profit determination and distribution are concerned. It further raises overwhelming issues of corporate sustainability.

Concerning financial sustainability, fair value and discounting imply a financial accumulation logic in which money investments are supposed to return cash proceeds at compound rates over time. This implies a multiplicative process which is both unrealistic and unsustainable since it triggers ever-increasing wealth inequality.Footnote 66 According to Kenneth E Boulding,Footnote 67 ‘continuous growth at a constant rate, however, is rare in nature and even in society. Indeed, it may be stated that within the realm of common human experience all growth must run into eventually declining rates of growth’.

Concerning extra-financial sustainability comprising social and environmental concerns, a fair value approach is reductionist and adopts a misleading understanding of money as measure of value.Footnote 68 Accordingly, these corporate responsibilities should be accounted for as far as they involve money risks to financial investors, that is, as long as they provoke some material and likely damage to investor vested interests into the enterprise. But, as long as their present value is immaterial for investors, or future contingent liabilities are not borne by them, those ‘risks’ may be tolerated and even ignored. Damage to nature and people is seen here as a financial investment risk to be managed, and the impact of such damage has to be assessed in money terms under such a ‘single materiality’ accounting principle.Footnote 69

Consequently, addressing social and environmental concerns through an ‘integrated reporting’ still based on the fair value accounting model may merely enhance greenwashing and further financialised exploitation of natural resources, prolonging rather than reorienting the shareholder value drift.Footnote 70 Money is not, cannot and should not be a measure of value.Footnote 71 This concept reduces nature and people to homologues of financial capital; it further reduces human action to its monetary dimension, making money almighty. But protection of the natural environment and general interest concerns are matters of choice, not monetary valuation. Their governance and regulation imply two ordered decisions: the purpose and the cost. Therefore, other social and legal standards – non-monetary and qualitative – may be developed and implemented to enact responsible and sustainable business conduct for stakeholders, nature and society as a whole.

For instance, let us imagine assessing social and environmental impact on employee health and soil by death-threatening, highly polluting chemicals by money value measurement. Through an understanding of employees and nature as human and natural capital, it would be possible and even suitable to take business decisions by netting the values of foreseeable dead employees, destroyed heartland and implied liabilities (if any) with the potential financial benefits involved by those chemicals use; and the former values may be far lower in emerging and poorly regulated countries. And when those risks materialise, informed shareholders may sell their securities before the news spreads, while controlling parties may declare insolvency to avoid paying for the damage.

However, the crucial point about sustainability and sustainable business conduct is to govern and regulate corporate affairs with a view to achieving social welfare and environmental protection. This includes social and environmental damage prevention, not management. A fair and sustainable corporate strategy may pursue this protection as a purpose, not as a financial risk appraisal. Accordingly, social and environmental detrimental impact may be properly addressed and preferably avoided; preventative and restorative measures may be put in place; and financial provisioning for those impacts and implied corporate commitments may be prioritised over other financial outflows, including distributions to shareholders.Footnote 72 According to a ‘double materiality’ accounting principle, these corporate impacts may be reported through a joint set of quantitative and qualitative indicators, and narrative disclosures.

5. Concluding remarks

Drawing upon KE Boulding’s remark, finance and accounting may be denoted as ‘uncongenial twins’. From this dualistic perspective, historical cost accounting may be interpreted and enacted as a convenient instrument to protect the corporate capacity to generate future earnings on which the expected financial value is based. However, in order to fulfil this control function, accounting applies an additive process (simple return), while financial valuation imposes a multiplicative process (compound return) over invested financial capital.Footnote 73 Rather than drawing upon quite a misleading notion of ‘de-growth’,Footnote 74 the notion of a ‘circular economy’ may be extended beyond the recycling of physical resources and developed into an understanding of the ongoing corporate economic process which is continued and evolving through time.

This divergence between accounting and finance has path-breaking implications. On the one hand, it enables disentangling corporate profit – as determined through accounting – from money interest and ownership rent, paving the way for a theory of the business firm based upon its accounting structure.Footnote 75 On the other hand, it enables indicators of financial performance consistent with this divergence.Footnote 76

As multiplicative processes featured by financial wealth accumulation may lead to unsustainable patterns and irresponsible corporate conduct, the theory and practice of a fair and sustainable business firm may look to this divergence as a fundamental building block. An enterprise entity theory of accounting may disentangle entity income from shareholder profit, as well as disentangling entity equity and shareholder equity, which is remunerated satisfyingly on the basis of actual shareholder equity funds provided by shareholders to the enterprise in the past.Footnote 77

By disentangling corporate income from shareholder value, and the business firm from shareholding financial investors, the concept of enterprise entity understands and organises corporate income generation and reserve provisioning as pragmatic instruments to maintain the enterprise as a going concern, rather than assessing corporate income as residual earnings destined to shareholder distributions by design. This approach does not only facilitate fair, responsible and sustainable corporate management, but prompts a rethinking of both theory and practice of corporate income representation and its role in corporate management, governance and regulation, with a view to make fair, responsible and sustainable business conduct accountable to stakeholders and society.

Open access

Open access